built for change - chainlinkresearch.com for change... · built for change—competitiveness for...

TRANSCRIPT

Built for Change

Competitiveness for Today’s Manufacturers Means Agility

Authored By: Ann Grackin

October, 2007

Copyright ChainLink Research 2007

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

About ChainLink Research ChainLink Research is dedicated to helping executives improve business performance and competitiveness. ChainLink was founded on the premise that supply chains are market driven and that the management of the links between companies has become the key determinant of market performance. ChainLink’s fresh approach to research, actionable analysis and high-impact decision-making workshops helps our clients enter new markets, expand share and achieve peak performance in their markets. ChainLink Research bridges the gulf between operational managers and the CEOs. Leading executives have recognized ChainLink as the foremost supply chain thought leader and action catalyst for the 21st century.

About Ramco Ramco Systems is a global provider of software products and consulting services for fast, flexible deploy-ment and change on demand for business applications. Companies can implement business processes more quickly and easily – so when their business changes, their systems change too. Because of its ser-vice-based, process-driven architecture approach, Ramco returns the highest quality software with the low-est total cost of ownership. Ramco Systems has offices in nine countries and over 300 customers in 1,000 locations worldwide across multiple verticals including banking, insurance, discrete and process manufactur-ing, aviation, transportation and logistics, healthcare, e-governance, retail, and more. The company is pub-licly held. For more on Ramco, visit www.ramco.com.

For more information, contact ChainLink Research

Harvard Square Center, 124 Mount Auburn St., Suite 200 N., Cambridge, MA 02138 Tel: (617) 762-4040 ext 484 Email: [email protected]

Website: www.clresearch.com

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Table of Contents

Executive Summary .............................................................................................1

Change is the Challenge....................................................................................1

Section One: Need for Change On Demand......................................................3

The Accelerating Pace of Change .....................................................................3 Managing the Critical Areas..........................................................................5

Section Two: Today’s IT—An Agile Framework................................................6

Today’s System Portfolio ...................................................................................7

Section Three: Achieving Change On Demand.................................................9 Service Oriented Architecture ............................................................................9 Different Approaches to Service Oriented Architecture..............................11

Conclusions........................................................................................................14 References ..........................................................................................................15

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

[This page intentionally left blank]

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 1

Executive Summary Globalization has created rich new market opportunities, but also a formidable set of chal-lenges for manufacturers:

• Huge structural change to industries—the enterprise and the value chain—changing the role of partnerships and adding fierce competition from developing economies.

• Complexity and risk in international trade. With global scandals a weekly occurrence, visibility into the extended supply chain and financial markets is now a primary recurring concern of C-level executives.

• Compliance demands from customers, channel partners and Retailers — each de-mands a unique combination of product, package, logistics, handling, and information integration.

CHANGE IS THE CHALLENGE With huge structural challenges confronting us, agility becomes a prime characteristic that an enterprise needs to acquire. But agil-ity, change, etc. are terms that are ephem-eral—hard to nail down. And most firms have been blind-sided and are only waking up to the unintended consequences of out-sourcing—lack of business continuity, in-creased sourcing costs, lack of control on quality from outsourced contract manufactur-ers, and now the added risk of illicit trade and the subsequent erosion of brand and shareholder value that follows.

Many articles, papers and pundits have talked about the ever-accelerating rate of change in business, the need for change management, or sadly, the story of “changed too late.” But they have not provided a context—and agile framework—that is tangible for executives to be able to act upon to address these concerns. So, the positive goal of learning to embrace change escapes them. We all know that companies must master Change on demand in or-der to stay in the game, so how to do it is the real question.

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 2

In this report we will focus on how we get there with process and technology agility1. These hold great promise for innovation, differentiation of service, adaptability and stream-lining of operation. There often is skepticism about technology as a source of agility, largely be-cause traditional application architectures created systems that are expensive and difficult to change.

In this report we will address these concerns by:

First, looking at the business goals and challenges today for mid-sized enterprises2. What is “C” level management indicating as their most pressing concerns? What critical areas need to be focused on to respond to business dynamics and upside, as well as to reduce risk and disruption, to improve performance?

From there we will delve into the major elements within an agile business and technology framework, and how business needs and the technology to support these changes have evolved over the last few years.

And finally, we will address how to leverage technology to support change, not stymie it. What technology approaches are available today to build change capabilities into the proc-ess and culture of the company?

Who Should Read This Paper

The audience for this paper includes:

CEOs CIOs Manufacturing Executives Supply Chain Professionals Discussions on technology in this report are written for a business audience. The imperative for executives to under-stand the role and evolution of technol-ogy is a prime issue in the enterprise.

CEO Strategic Concerns: Large Cap Business structure/model Strategic Partnerships Visibility of Operations Managing Innovation Shareholder Value

CEO Strategic Concerns: Midsize Profitable Growth- Agility/Ability to re-

spond to Market/Customer/Product opportunities

Channel/Customer Acquisition Technology Management Cost of Cash Price/Cost Management

1. Acknowledging that human change management is absolutely critical to success 2. Under $2 billion

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 3

Section One: Need for Change On Demand THE ACCELERATING PACE OF CHANGE The next ten to twenty years will be consumed with understanding, addressing and adapting to the wave of changes that we have unleashed from outsourcing and from virtual business models that have been pursued in the business community. We are now beginning to experience the unintended consequences of global trade, as well as extreme outsourcing. These changes have unleashed huge structural changes—new part-nerships, and new competitors that play the game dif-ferently. Many newer firms are not weighed down by legacy investments and are free to reinvent the game. Hard to compete against that! We are also seeing the unintended consequences of poor architecting of the global processes such as financial and supply chain. Most firms have been blind-sided by making assump-tions about the nature of the work and the scope of agreements. And critically, enterprise technology decisions based on the old models have locked in the enterprise, making it hard to respond to these critical events and imperative changes. These trends and the need for change will only intensify over time.

Most change dynamics naturally come from either the customer/channel side, or supply markets. As we look at “C level” concerns, the dynamics, plus several other critical areas, emerge that require management attention.

Supplier Visibility and Total Cost Sourcing —Not just visibility into product creation, but all the elements contributing to total cost—going beyond material costs to a model of cost to market, including total transportation, risk management and compliance. Added to that fi-nancial model of these sourcing costs today is further visibility into challenges such as sup-ply chain of authentication, Fair Trade, carbon foot prints, etc., exacerbated by the scandals in the market place.

Integrated Channel Management & Visibility—Loss of control in the channel is a huge threat to continued market existence, as well as competitiveness. Poor visibility stymies product innovation and customer delight. Compliance requirements, as well, are ever-increasing, usually adding to cost of goods sold, and increasing lead times (see side bar). Our research shows that the operational cost of compliance, without the cost of deductions, for most sup-

The most common challenges and issues for Manufacturers today are: Globalization—Longer, riskier supply chains, increased competition from Asia and other regions Changing Channel Dynamics—Loss of con-trol in the channel leading to price erosion Increased Compliance Requirements—both from customers as well as government regu-latory agencies Wall Street Pressures—Asset reduction, ROA, ROIC, have driven manufacturers back to Lean as a strategy to address cost man-agement Trading Partner Integration and Visibility—Extreme outsourcing of the supply chain has amplified the need to integrate with and have transparent processes with trading partners (suppliers, customers, and service providers) Technology and Innovation Management—Methods to increase product differentiation, provide new services, provide information management and analytics to manage the processes and enterprise

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 4

pliers to retailers is in the range of ½% to 2% of revenue3. Add to the above the cost of de-ductions and penalties, which for many suppliers is greater than 5% of revenue! In indus-trial contracts, late fees can mean thousands and (sometime millions) of dollars a day in fines. So, al-though being compliant has added expense, it can be offset by increased sales—preferred supplier—and ironically a profitability advantage over those who can’t comply.

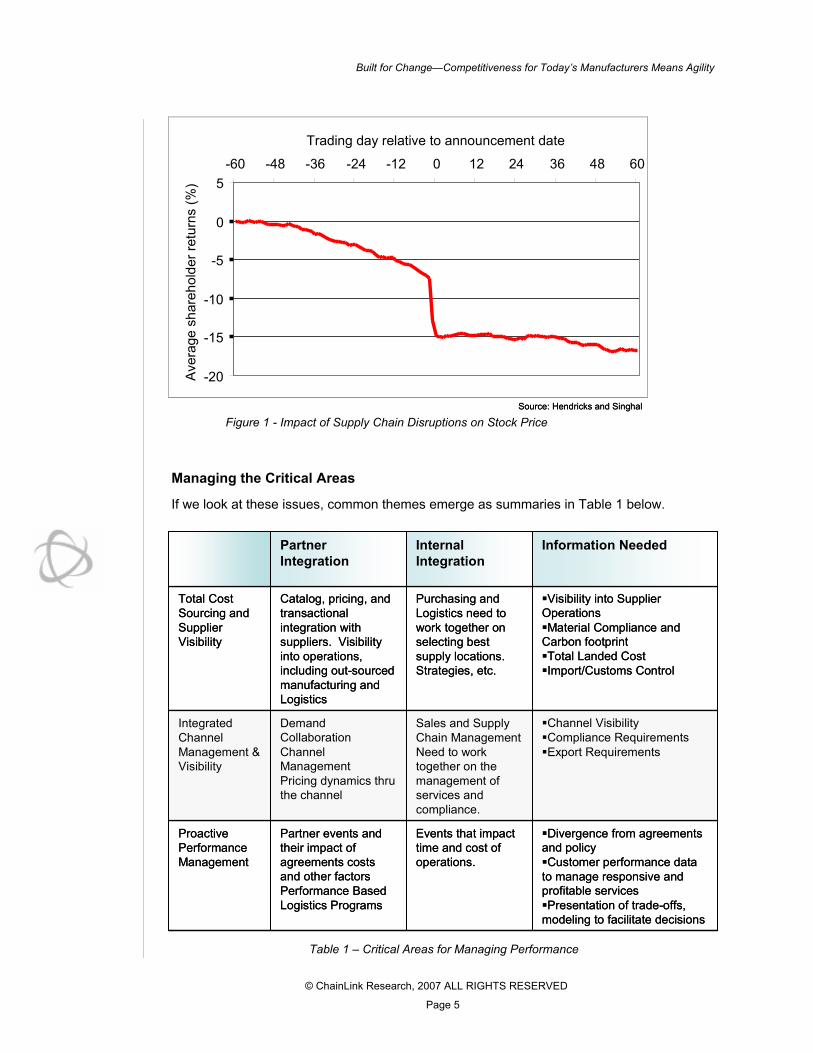

Proactive Performance Management—Poor manage-ment of the supply chain has impact right to the boardroom. The impact is not only profit, but share-holder value. The ability to proactively see and correct problems before the fact to improve performance, then, is desired. The linkage between supply chain disruptions and shareholder value was clearly shown in a study by Hendricks and Singhal4. They reported the impact to stock prices of almost 1,000 companies after a supply chain glitch was announced. The Stock price decline on average was an astounding 25%5.

Lack of visibility has costs6, as you can see in figure 1 (next page). The requirement for Performance Visibil-ity has strong quantifiable benefits—not a soft benefit, as some state.

Technology Management—Agile, adaptive and high visibility frameworks to address the above needs.

Compliance Just Won’t Go Away… With over 15,000 global regulations, the issues get larger over time… Customer Compliance:

• Charge backs, Deductions, Fines and Fees, Returns

• On Time Delivery Windows • Documentation / EDI • Routing Guides and Carrier Restric-tions

• Packing Sequence, Stacking limits • Packaging, Floor-ready Merchan-dise

• Bar-coding, RFID, Labeling • More and more…

Global Trade Management:

• Security, C-TPAT and Increase in DHS requirements

• Harmonization codes, Duties and tariffs

• Denied parties screening, embar-goed countries, etc.

• Other Customs requirements

Purchase Agreements:

• Restocking fees • Safety Stock levels • Returns • Rigid contract and lead times

Regulatory Compliance Financial Regulations

3. Cooperation and Competition in the Retailer-Supplier Relationships ChainLink Research report www.chainlinkresearch.com/research/detail.cfm?guid=D407B01A-8004-6D99-1CAA-F1904484959E 4. Supply Chain Glitches and Shareholder Value Destruction Hendricks and Singhal report www.touchbriefings.com/pdf/976/02.pdf 5. An Empirical Analysis of the Effect of Supply Chain Disruptions on Long-run Stock Price Performance and Equity Risk of the Firm Hendricks and Singhal report Nov 2003 (e-mail:[email protected]) 6. Track and Trace - Indispensable Enabler for Global Trade ChainLink Research article www.chainlinkresearch.com/research/detail.cfm?guid=1DD32C85-3048-785E-317F-377CC0BBB0D1

The Ramco-powered Hub enables us to manage the distribution

channel so effectively because it provides visibility into all points in

the chain, from production to retailer, and it connects us with the sys-

tems used by our distributors. When a bottleneck begins to form, we

know it right away and can act immediately to fix it. When a distribu-

tor or retailer begins to experience a shortage, we can anticipate it

and solve it before it becomes a problem.”

“Compliance requirements are so specific to each client that we have to have a sepa-rate outbound management process—from packaging, to carriers, to EDI transaction—for each one.” Supply Chain Manager of digital electronic firm

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 5

Managing the Critical Areas

If we look at these issues, common themes emerge as summaries in Table 1 below.

Figure 1 - Impact of Supply Chain Disruptions on Stock Price

Table 1 – Critical Areas for Managing Performance

Divergence from agreements and policyCustomer performance data

to manage responsive and profitable servicesPresentation of trade-offs,

modeling to facilitate decisions

Events that impact time and cost of operations.

Partner events and their impact of agreements costs and other factorsPerformance Based Logistics Programs

Proactive Performance Management

Channel VisibilityCompliance RequirementsExport Requirements

Sales and Supply Chain Management Need to work together on the management of services and compliance.

Demand CollaborationChannel ManagementPricing dynamics thru the channel

Integrated Channel Management & Visibility

Visibility into Supplier OperationsMaterial Compliance and

Carbon footprintTotal Landed Cost Import/Customs Control

Purchasing and Logistics need to work together on selecting best supply locations. Strategies, etc.

Catalog, pricing, and transactional integration with suppliers. Visibility into operations, including out-sourced manufacturing and Logistics

Total Cost Sourcing and Supplier Visibility

Information NeededInternal Integration

Partner Integration

Divergence from agreements and policyCustomer performance data

to manage responsive and profitable servicesPresentation of trade-offs,

modeling to facilitate decisions

Events that impact time and cost of operations.

Partner events and their impact of agreements costs and other factorsPerformance Based Logistics Programs

Proactive Performance Management

Channel VisibilityCompliance RequirementsExport Requirements

Sales and Supply Chain Management Need to work together on the management of services and compliance.

Demand CollaborationChannel ManagementPricing dynamics thru the channel

Integrated Channel Management & Visibility

Visibility into Supplier OperationsMaterial Compliance and

Carbon footprintTotal Landed Cost Import/Customs Control

Purchasing and Logistics need to work together on selecting best supply locations. Strategies, etc.

Catalog, pricing, and transactional integration with suppliers. Visibility into operations, including out-sourced manufacturing and Logistics

Total Cost Sourcing and Supplier Visibility

Information NeededInternal Integration

Partner Integration

T-values associated with these abnormal returns are in the range of –-10 to –15 (all highly significant)

Source: Hendricks and Singhal

-20

-15

-10

-5

0

5-60 -48 -36 -24 -12 0 12 24 36 48 60

Trading day relative to announcement date

Ave

rage

sha

reho

lder

retu

rns

(%)

T-values associated with these abnormal returns are in the range of –-10 to –15 (all highly significant)

Source: Hendricks and Singhal

-20

-15

-10

-5

0

5-60 -48 -36 -24 -12 0 12 24 36 48 60

Trading day relative to announcement date

Ave

rage

sha

reho

lder

retu

rns

(%)

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 6

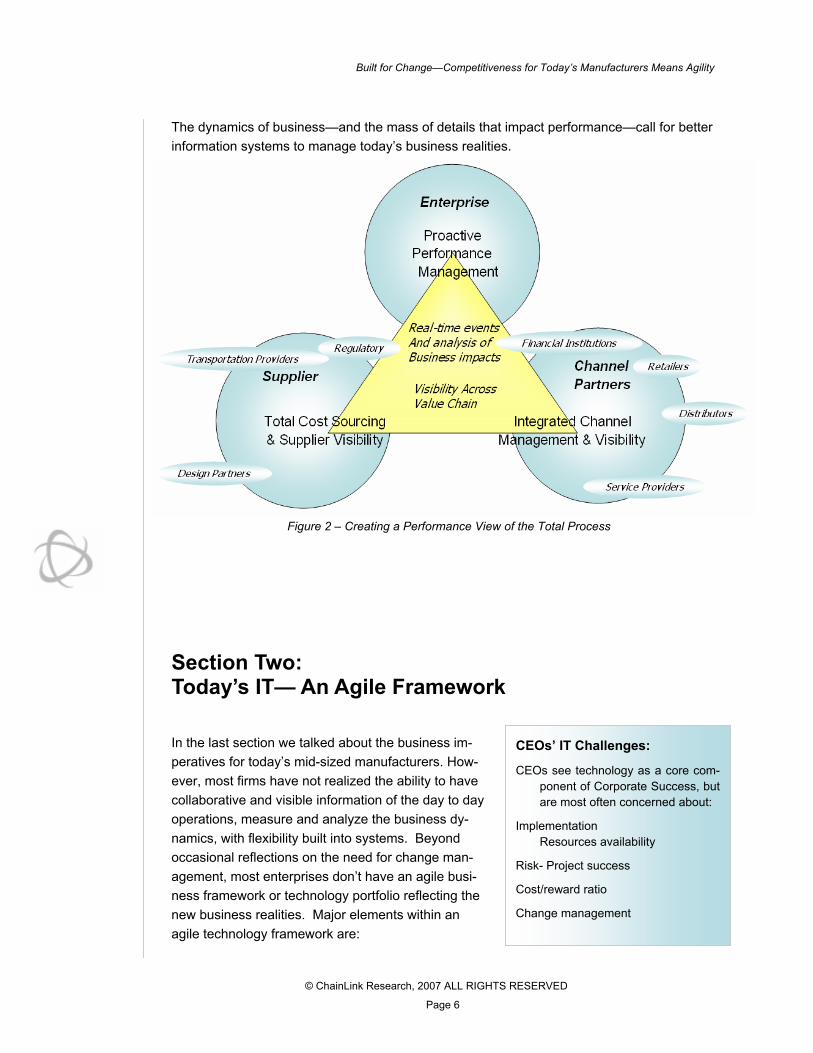

The dynamics of business—and the mass of details that impact performance—call for better information systems to manage today’s business realities.

Section Two: Today’s IT— An Agile Framework

In the last section we talked about the business im-peratives for today’s mid-sized manufacturers. How-ever, most firms have not realized the ability to have collaborative and visible information of the day to day operations, measure and analyze the business dy-namics, with flexibility built into systems. Beyond occasional reflections on the need for change man-agement, most enterprises don’t have an agile busi-ness framework or technology portfolio reflecting the new business realities. Major elements within an agile technology framework are:

Figure 2 – Creating a Performance View of the Total Process

CEOs’ IT Challenges:

CEOs see technology as a core com-ponent of Corporate Success, but are most often concerned about:

Implementation Resources availability

Risk- Project success

Cost/reward ratio

Change management

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 7

• Rapid Connectivity—visibility and connectivity, not just throughout the enterprise, but architected for rapidly on-boarding trading partners, with shared data and processes.

• Nimble Platform—ability to quickly deploy and (more importantly) easily modify and update business process to keep pace with ever changing requirements.

• Proactive Performance Management—real-time business performance methods to manage the impacts of business dynamics.

So what are those systems that can be part of this agile technology framework today?

TODAY’S SYSTEM PORTFOLIO Technology has evolved as business models / business requirements have evolved (figure 3, next page). Many manufacturers look to ERP as a way to address the above business challenges. ERP evolved during the era of the vertical business model. Through mergers and acquisitions and through the need to see internal operations, ERP provides that cohe-sive view. But ERP alone will not get you there. Enterprise software is good for the transac-tions, the counting of things, but does not provide orchestration and visibility between trad-ing partners. ERP is designed for four walls business—not for today’s outsourced world.

Since the 90s, we then moved into new business models that have leveraged newer tech-nologies. E-commerce is useful in that it provides access to a global view of ‘who’s in busi-ness globally’ and a way to conduct transaction management. But e-commerce systems are still based on a traditional view of an enterprise. Virtual business models have challenged these systems—to share work and information across business process.

As we move into a highly federated business world, firms are focusing more on leveraging the partnership process-mastery—rather than a transaction-based relationship of goods pur-chasing. This creates the need for real-time visibility of the process—with workflow and pre-dictive based systems being the core.

Predictive based systems can, therefore, support views into workflow and events, helping to alert users of deviation from the agreed to the policy. They also give management a new way of driving performance management—moving from a traditional business intelligence system which is reporting based—to real-time dashboards, to see in motion as events un-fold and the impact they are having. Real-time feeds into these platforms can be supported with scan data, auto/id, voice, video, as well as traditional data from transactions systems that percolate up.

Change on demand means…. “We work closely with our customers and partners and when we see an opportunity—a new process or idea—that can be used from one partner to another, across the business, we like to include that in the other parts of the business. For example, our “VOS” (Vendor On Site Inventory Manage-ment Program); through this our partners can also submit ideas, and if they can add value in the Supply Chain, we want to im-plement them quickly. We can go to our partner, Ramco, and get this done easily, and be able to externalize that function to our partners. “

MJB Wood Group, Inc.

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 8

These elements all become part of the IT portfolio of the enterprise. We are still left, though, with core change management issues. Although we need the ERP-like functions—we need to rapidly change or modify the business capabilities—and also share these func-tions with our partners for consistency in management.

Traditional ERP vendors did not foresee (when they architected an enterprise cohesion ap-proach) the radical pace of changes that would be thrust upon business due to the Internet, global-ization, and the pressures of Wall Street (to re-duce the asset structure of the firm), as well as significant acceleration and changes in how we design, manufacture, and bring goods to market.

This issue is critically important in today’s outsourced world, where companies are mixing and matching elements of the business processes, as they outsource processes like assem-bly, distribution, logistics, service and support, or even IT. We need an enterprise architec-ture that reflects the new business model—agile, flexible and able to support diverse proc-ess requirements in each situation.

Since that business model is likely to change, we need systems that are an enabler to that change—not the impediment. This is the central theme for IT over the next ten years—how to deal with ever accelerating change. And how to orchestrate the rich context of proc-esses—dynamically—across the ecosystem of trading partners.

ServiceOriented

Frameworks

1980s 1990s 1998 2000 2004 2007

POLICYPOLICY: Do It All Price Compliance

PROCESSPROCESS: Push Pull Lean

PERFORMANCEPERFORMANCE: Cost Accounting/ROI Optimization/ROA Risk Management

Technology Portfolio Evolution

BUSINESS DRIVER: Enterprise Cohesion WW Presence Responsiveness

BUSINESS Model Vertical Virtual Federated

PredictiveNetworks

ECommerceframework

Enterpriseframework

Data WH,Spread Sheets

OLAPDepartmentcomputing

Enablers:Enablers:

PARTNERSHIPSPARTNERSHIPS: Transactions Structural Process

ServiceOriented

Frameworks

1980s 1990s 1998 2000 2004 2007

POLICYPOLICY: Do It All Price Compliance

PROCESSPROCESS: Push Pull Lean

PERFORMANCEPERFORMANCE: Cost Accounting/ROI Optimization/ROA Risk Management

Technology Portfolio Evolution

BUSINESS DRIVER: Enterprise Cohesion WW Presence Responsiveness

BUSINESS Model Vertical Virtual Federated

PredictiveNetworks

ECommerceframework

Enterpriseframework

Data WH,Spread Sheets

OLAPDepartmentcomputing

Enablers:Enablers:

PARTNERSHIPSPARTNERSHIPS: Transactions Structural Process

Figure 3 - Technology and Business Co-Evolution

“The nature of our business is (with the time between contact reward and an initial customized delivery) often in a matter of weeks. Being able to con-figure and deploy new processes to meet the demands of new customers is of paramount importance.” Preferred Meals

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 9

Section Three: Achieving Change On Demand Although keeping pace with innovation is a CEO issue, doing it on limited budget is a CIO’s issue. Investments have to achieve results. If built for change is the goal, we have to do it with less risk.

Of late, traditional ERP companies have pushed their ‘template’ approaches to implementation.

We need to address better approaches to technology and its adoption if we want the rich capabilities and the change management required.

SERVICE ORIENTED ARCHITECTURE Many firms are exploring Service Oriented Architecture frameworks as a way to address the acquisition and adoption of new technology. No doubt there are many technical definitions of SOA, but business value is our focus here.

Fundamentally, SOA addresses several key factors:

• Reuse—it makes sense to leverage what you have. Modules are in a library which can be used by developers. Years of thought have gone into the processes, reports, etc. You save development dollars with this as well as staff time to benefit.

• Data Management—creating and managing com-mon repositories of data so that everyone can ac-cess these, and use them in their programs. This is so critical in a compliance driven world.

What is SOA? Service Oriented Architecture is an ar-chitectural approach to systems devel-opment that relies on modularity and reuse as the fundamental design princi-ple. Developers avoid writing new code if they can access existing modules/ services. With these services they as-semble applications. Another principle of SOA is that the application should run on any platform. This is called independence. SOA achieves code, data and workflow inde-pendence “independent services” that can be accessed without knowledge of the underlying platform. The services are also independent in that each one can be modified and evolved without impacting other parts of the system, provided that the service interface remains intact. This allows companies to more easily evolve their systems, selectively customizing with-out requiring major rework or painful upgrades. Developers can access and assemble like a ‘prime contractor,’ procuring the services of carpenters, plumbers and electricians to build a house. Thus the term ‘service oriented’. MDM is the management of data that is both technical (creating a sharable re-pository) as well as policy—with com-mon standards around data classifica-tion, structure and semantics. The “MDM” is set up to allow data to be shared by several disparate IT systems. So, for example, if your ERP system and your Warehouse Management sys-tem both need customer data, that data can be developed once, stored in a sharable library, and then be available for these systems to use. What SOA is not Although you hear terms like Software as a Service or Web services, these are not SOA. Software as a Service (SaaS), also known as On-Demand, is a busi-ness and delivery model for technology firms to deliver applications to custom-ers over the web, usually in a Pay-as-you-go financial model.

“we have all but abandoned the goal of differentiation because of IT—which is a mistake in a world of increased competition.”

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 10

• Portable/sharable—a standards-based un-derpinning is used. This allows you to move from enterprise, to web, to trading partner, sharing your services. This eases the path to trading partner connectivity.

• Model-Driven architectures allow for a true and current representation of the business model—this includes work flow within and beyond the enterprise, and the ‘remodeling’ or reflowing of processes, on demand. This pulls all the elements or services together in a harmonious way that addresses that criti-cal issue. What is the process and data that I need to support this business instance?

When we look at these technical elements, what emerges is an agile and flexible capability to model and respond to systems’ requirements, allowing process change and easier con-nectivity between systems with greater speed. With dynamic modeling techniques, you model a business process and directly create a set of business services (software) that make up the actual application. This obviously reduces development and implementation time resulting in an overall reduction in the Total Cost of Ownership of technology.

For Service Oriented Architecture to work, there has to be a rich library of services to access. Other-wise, it is like going to the public library—a great concept to share all those books, save money from buying them yourself, and having them when you want (or at least finding a great substitute)—yet there are no books there! Fortunately, SOA adop-tion is growing, due to its benefits. Our research7 has shown that more firms are adopting SOA and are ‘exposing’ service to their trading partners. (figure 4, next page)

Using the SOA approach, MJB was able to model a business process from end to end and then develop the software so that the process flows logically and seamlessly to all parties engaged in this process.

This flow includes internal MJB employ-ees, external partners like vendors, logistics and third party service providers using EDI. We have also enabled many proc-esses using workflow that have enabled process efficiency.

SOA allow us to take components of one part of the business model and use them in other areas.

MJB Wood Group, Inc.

7. Single Version of the Truth ChainLink Research report: www.chainlinkresearch.com/research/detail.cfm?guid=F6F06550-A81A-4F05-EF17-F501BAD84E68

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 11

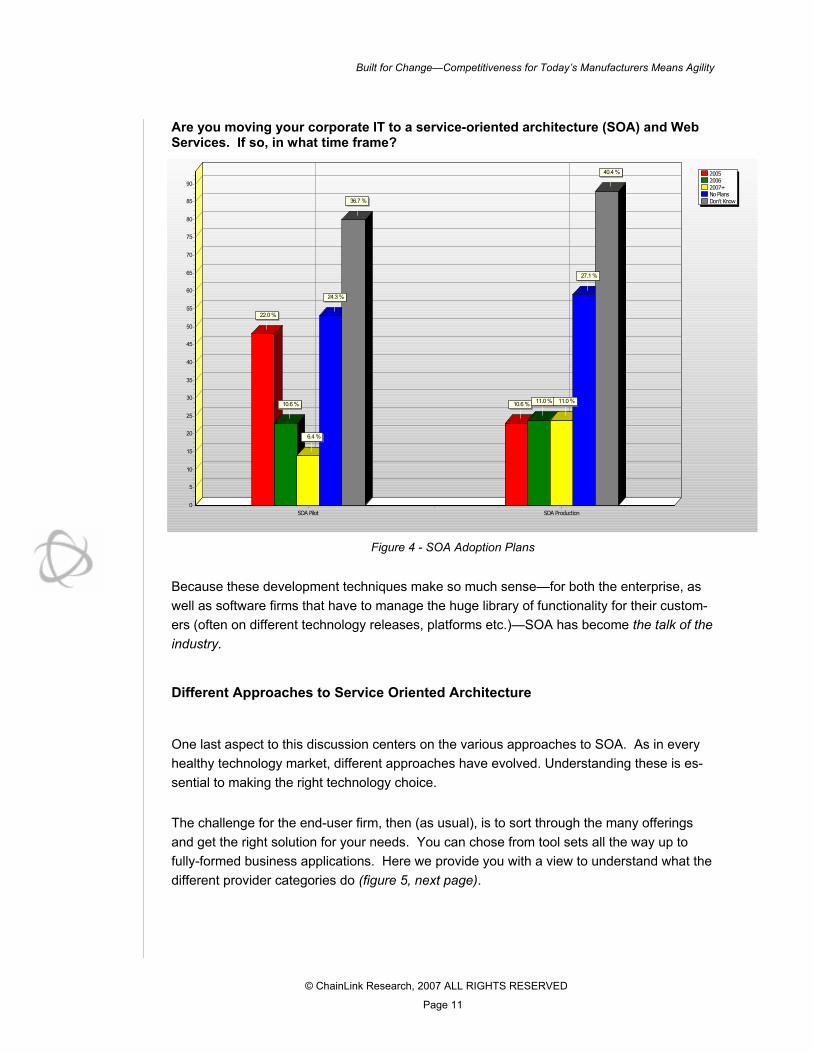

Are you moving your corporate IT to a service-oriented architecture (SOA) and Web Services. If so, in what time frame?

Because these development techniques make so much sense—for both the enterprise, as well as software firms that have to manage the huge library of functionality for their custom-ers (often on different technology releases, platforms etc.)—SOA has become the talk of the industry.

Different Approaches to Service Oriented Architecture

One last aspect to this discussion centers on the various approaches to SOA. As in every healthy technology market, different approaches have evolved. Understanding these is es-sential to making the right technology choice.

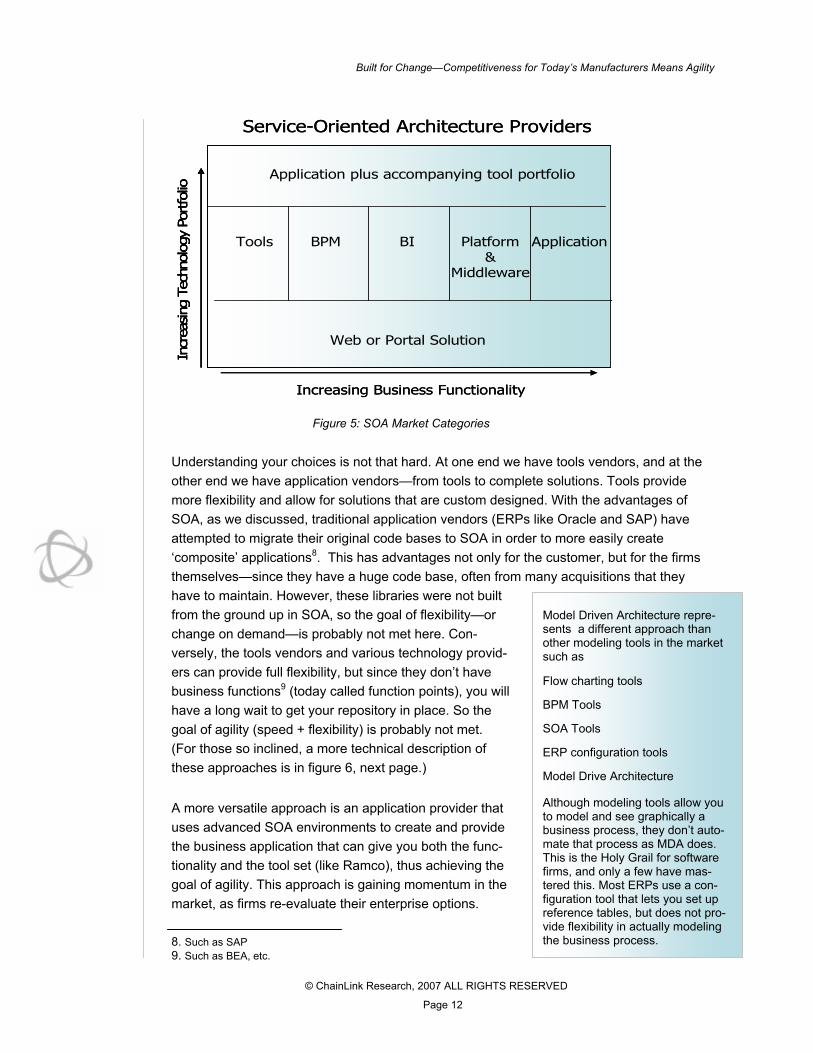

The challenge for the end-user firm, then (as usual), is to sort through the many offerings and get the right solution for your needs. You can chose from tool sets all the way up to fully-formed business applications. Here we provide you with a view to understand what the different provider categories do (figure 5, next page).

200520062007+No PlansDon't Know

( y y )

SOA Pilot SOA Production

90

85

80

75

70

65

60

55

50

45

40

35

30

25

20

15

10

5

0

22.0 %

10.6 % 10.6 % 11.0 %

6.4 %

11.0 %

24.3 %

27.1 %

36.7 %

40.4 %

Figure 4 - SOA Adoption Plans

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 12

Understanding your choices is not that hard. At one end we have tools vendors, and at the other end we have application vendors—from tools to complete solutions. Tools provide more flexibility and allow for solutions that are custom designed. With the advantages of SOA, as we discussed, traditional application vendors (ERPs like Oracle and SAP) have attempted to migrate their original code bases to SOA in order to more easily create ‘composite’ applications8. This has advantages not only for the customer, but for the firms themselves—since they have a huge code base, often from many acquisitions that they have to maintain. However, these libraries were not built from the ground up in SOA, so the goal of flexibility—or change on demand—is probably not met here. Con-versely, the tools vendors and various technology provid-ers can provide full flexibility, but since they don’t have business functions9 (today called function points), you will have a long wait to get your repository in place. So the goal of agility (speed + flexibility) is probably not met. (For those so inclined, a more technical description of these approaches is in figure 6, next page.)

A more versatile approach is an application provider that uses advanced SOA environments to create and provide the business application that can give you both the func-tionality and the tool set (like Ramco), thus achieving the goal of agility. This approach is gaining momentum in the market, as firms re-evaluate their enterprise options.

Figure 5: SOA Market Categories

Model Driven Architecture repre-sents a different approach than other modeling tools in the market such as

Flow charting tools

BPM Tools

SOA Tools

ERP configuration tools

Model Drive Architecture

Although modeling tools allow you to model and see graphically a business process, they don’t auto-mate that process as MDA does. This is the Holy Grail for software firms, and only a few have mas-tered this. Most ERPs use a con-figuration tool that lets you set up reference tables, but does not pro-vide flexibility in actually modeling the business process.

8. Such as SAP 9. Such as BEA, etc.

Increasing Business Functionality

Incr

easing

Tec

hnol

ogy

Portfo

lio

Web or Portal Solution

BPM Platform&

Middleware

Tools BI Application

Application plus accompanying tool portfolio

Service-Oriented Architecture Providers

Increasing Business Functionality

Incr

easing

Tec

hnol

ogy

Portfo

lioIn

crea

sing

Tec

hnol

ogy

Portfo

lio

Web or Portal Solution

BPM Platform&

Middleware

Tools BI Application

Application plus accompanying tool portfolio

Service-Oriented Architecture Providers

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 13

Services Bus

ERP SCM CRM PLM

Web Services

MRP

HR

Procurement

General Ledger

Composite Application

Composite Application

Composite Application

Many traditional enterprise application vendors have realized that the original architecture they built their software on does not allow for sufficient flexibility for modern businesses. In addition, many have grown through acquisition, and have a portfolio of relatively disparate applications. Therefore, for both integrating their application portfolio and to provide additional agility, they have started exposing (as web services) the functionality that they’ve already built in their applications.

Examples include SAP NetWeaver and Oracle Fusion.

Traditional Enterprise Application with Functions As Composites “Exposed” as Web Services

Services Bus

ERP SCM CRM PLM

Web Services

MRP

HR

Procurement

General Ledger

Composite Application

Composite Application

Composite Application

Many traditional enterprise application vendors have realized that the original architecture they built their software on does not allow for sufficient flexibility for modern businesses. In addition, many have grown through acquisition, and have a portfolio of relatively disparate applications. Therefore, for both integrating their application portfolio and to provide additional agility, they have started exposing (as web services) the functionality that they’ve already built in their applications.

Examples include SAP NetWeaver and Oracle Fusion.

Traditional Enterprise Application with Functions As Composites “Exposed” as Web Services

Figure 6: SOA: Three Approaches

Web Service Repository / Registry

Services Bus – Process ExecutionWeb

Services

Services Created and Maintained by

End User Organization

Process Design & Modeling

Master Data Management

Process Monitoring, Optimization

Business Intelligence / Dashboard

The second approach, of which there are many choices, is to offer an SOA Toolkit. Examples include BEA, IBM, and many smaller BPM vendors.These offer a very flexible environment and set of tools to build anything you want. The challenge is that the end user’s organization is starting from scratch, or from a library of functions to build up the full system they need.

SOA Platforms and Tool Kits

Web Service Repository / Registry

Services Bus – Process ExecutionWeb

Services

Services Created and Maintained by

End User Organization

Process Design & Modeling

Master Data Management

Process Monitoring, Optimization

Business Intelligence / Dashboard

The second approach, of which there are many choices, is to offer an SOA Toolkit. Examples include BEA, IBM, and many smaller BPM vendors.These offer a very flexible environment and set of tools to build anything you want. The challenge is that the end user’s organization is starting from scratch, or from a library of functions to build up the full system they need.

SOA Platforms and Tool Kits

Process Design & Modeling

Web Service Repository / Registry

Master Data Management

Process Monitoring,

Optimization

Business Intelligence / Dashboard

Services Bus – Process ExecutionWeb

Services

Rich Library of Services Created and Maintained by Solution Provider

MRP

HR

Procurement

General Ledger Factory Planner

WMS

Call Center Management

TMS

DesignCollaboration

PDM

The third approach is an attempt to offer the best of both worlds. This is where a set of enterprise application functionality has been architected from the ground up, on top of an SOA Platform. An example is Ramco.

Done right, this third approach gives the user the full functionality desired, but with the ability to continually evolve the process configurations and functionality over time.

SOA-architected Enterprise Application & Platform

Process Design & Modeling

Web Service Repository / Registry

Master Data Management

Process Monitoring,

Optimization

Business Intelligence / Dashboard

Services Bus – Process ExecutionWeb

Services

Rich Library of Services Created and Maintained by Solution Provider

MRP

HR

Procurement

General Ledger Factory Planner

WMS

Call Center Management

TMS

DesignCollaboration

PDM

The third approach is an attempt to offer the best of both worlds. This is where a set of enterprise application functionality has been architected from the ground up, on top of an SOA Platform. An example is Ramco.

Done right, this third approach gives the user the full functionality desired, but with the ability to continually evolve the process configurations and functionality over time.

SOA-architected Enterprise Application & Platform

Three Approaches of SOA

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 14

Conclusion

Today, businesses live in a rich ecosystem of partnerships. Competition is growing and mar-kets are more complex. How a company re-sponds to these changes—with speed, yet prof-itably—makes the difference in success. Re-ducing risk and the cost to get to the outcomes desired is obviously the way forward.

Technology acquisition is still considered a risky proposition by most, yet is a most central ele-ment to business change. Reducing the confu-sion of options for mid-sized firms is key. With the number of firms seeking ERP-like capabili-ties, yet needing increased visibility across the ecosystem, going the SOA toolkit route is a very long road. Yet traditional ERP (which many of these firms have and are trying to migrate up-ward from) does not support the change man-agement goals.

Your forage through the technology market, then, should settle on application vendors that have built their solution in the SOA architec-tures, but who have business services that truly run with the other elements or services that you may already have in your library, that you have honed through the years.

The dream business is the one where you can change in an instant as business requires, ready with a quick market response, changing on demand. As each customer becomes more demanding with unique expectations, the prac-tical pursuit of this capability becomes more challenging. With the right platform, these challenges can be met.

Our value solution is what sets us apart from our competition. We made the decision about ten years ago to invest in technology that could help us deliver these solutions.

Our process was based on a specific list of critical business functions that were deal breakers if the vendor could not meet them. After evaluating the products, we felt that Ramco was the best fit. Flexibility and Rapid Changes were the driving factors.

Amy Quaid, Vice President and CIO, MJB Wood Group, Inc.

Built for Change—Competitiveness for Today’s Manufacturers Means Agility

© ChainLink Research, 2007 ALL RIGHTS RESERVED

Page 15

References Single Version of the Truth - Journey to a Unified Supply Chain, Carla Reed and Bill McBeath, 2006 www.chainlinkresearch.com/research/detail.cfm?guid=F6F06550-A81A-4F05-EF17-F501BAD84E68

Cooperation and Competition in Retailer-Supplier Relationships, Bill McBeath, 2004 www.chainlinkresearch.com/research/detail.cfm?guid=D407B01A-8004-6D99-1CAA-F1904484959E

Future Forward Logistics, Creating an Extended Global Enterprise, Carla Reed, 2004 www.chainlinkresearch.com/research/detail.cfm?guid=53271B29-D92D-06FC-20E5-F0A4420287DA

Dynamics of the Retailer - Supplier Relationship, Bill McBeath, 2003 www.chainlinkresearch.com/research/detail.cfm?guid=5312EB6C-0C7C-624F-6557-47ECD92B6A89

Supply Chain Glitches and Shareholder Value Destruction, Hendricks and Singhal, 1999, 2007 www.touchbriefings.com/pdf/976/02.pdf

Ramco’s Business Process Delivery System—Combining Process and Technology for Business Success, Joshua Greenbaum, 2007, www.ramco.com/collateral/white%20papers/whitepaper.pdf

US Middle Market Outlook The Economist Intelligence Unit, Ltd July 2007 www.cit.com/NR/rdonlyres/9CEEBD7F-44F3-4862-A094-4C2B4732E58E/0/MiddleMarketOutlookWhitepaper.pdf

Key Customer References for this study:

Preferred Meal Systems, a subsidiary of Maramont Holdings Corporation www.preferredmealsystems.com

MJB Wood Group, Inc. http://www.mjbwood.com

HERO, AG http://www.hero.ch

Columbia Helicopters http://www.colheli.com

Harvard Square Center 124 Mount Auburn Street, Suite 200 N.

Cambridge, MA 02138 Tel: (617) 762-4040

Email: [email protected]. Website: www.clresearch.com