bujagali ii – economic and financial evaluation...

TRANSCRIPT

Bujagali II – Economic and Financial Evaluation Study

Final Report

Main Text

February 2007

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 2 February 2007 26/02/2007-20224

LIST OF ABBREVIATIONS USED IN THE REPORT......................................................................5 EXECUTIVE SUMMARY .......................................................................................................................8 1 INTRODUCTION..........................................................................................................................18

1.1 BACKGROUND .........................................................................................................................18 1.2 OBJECTIVES AND SCOPE OF WORK .........................................................................................19

2 ELECTRICITY DEMAND FORECAST ...................................................................................20 2.1 INTRODUCTION........................................................................................................................20 2.2 PRESENT AND PAST DEMAND .................................................................................................20 2.3 METHODOLOGY AND ASSUMPTIONS.......................................................................................27 2.4 PROJECTIONS FOR UGANDAN ECONOMY ................................................................................27

2.4.1 General ..............................................................................................................................27 2.4.2 Overview of the Ugandan Economy..................................................................................27 2.4.3 Projections.........................................................................................................................28

2.5 ASSUMPTIONS FOR RESIDENTIAL SECTOR..............................................................................28 2.6 ASSUMPTIONS FOR COMMERCIAL AND INDUSTRIAL SECTORS...............................................31 2.7 REVENUE COLLECTION ...........................................................................................................31 2.8 TARIFF ASSUMPTIONS.............................................................................................................32 2.9 ASSUMPTIONS ON REDUCTION OF SYSTEM LOSSES................................................................33 2.10 ELECTRICITY EXPORTS ...........................................................................................................35 2.11 LOAD FORECAST RESULTS AND SENSITIVITY SCENARIOS .....................................................36

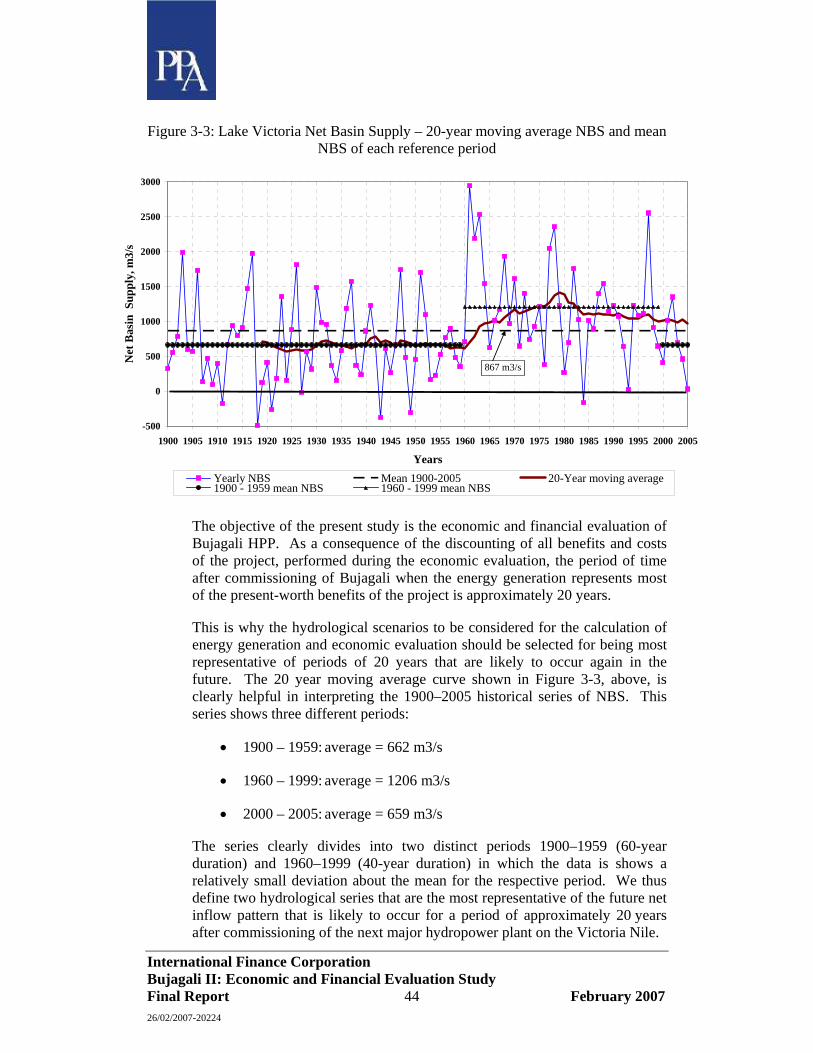

3 HYDROLOGY AND ENERGY GENERATION OF HYDRO POWER PLANTS..............41 3.1 INTRODUCTION........................................................................................................................41 3.2 LAKE VICTORIA NET BASIN SUPPLY ......................................................................................41 3.3 DEPARTURE FROM THE AGREED CURVE AND THE RECENT FALL IN THE LEVEL OF LAKE VICTORIA ...............................................................................................................................................46 3.4 LAKE OPERATION MODELLING AND ENERGY GENERATION EVALUATION ...........................47

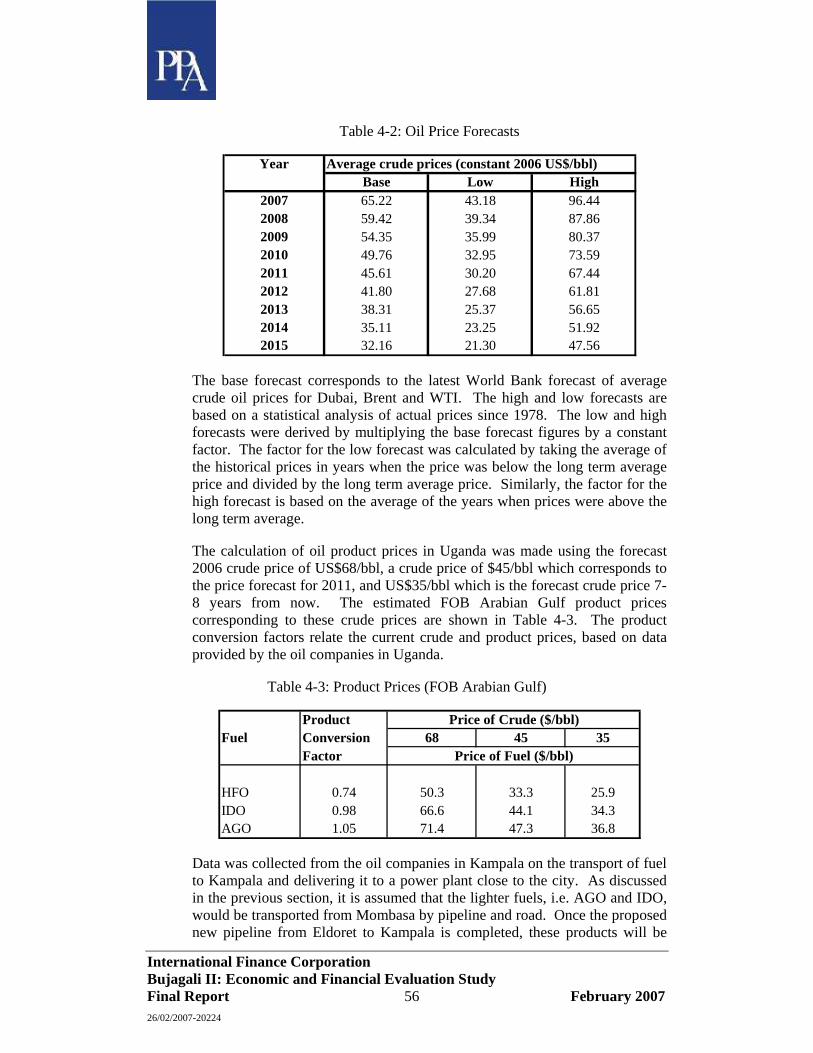

4 INTERIM SUPPLY ARRANGEMENTS (2006-2010)..............................................................52 4.1 EXISTING SHORT TERM THERMAL PLANT..............................................................................52 4.2 ADDITIONAL EMERGENCY THERMAL PLANT .........................................................................52 4.3 BIOMASS PROJECTS.................................................................................................................52 4.4 SMALL HYDRO PROJECTS .......................................................................................................53 4.5 FUEL SUPPLY ISSUES...............................................................................................................54 4.6 FUEL TYPES AND COSTS .........................................................................................................55 4.7 INTERIM GENERATING PLANT.................................................................................................58 4.8 ELECTRICITY IMPORTS............................................................................................................59 4.9 PLANT EXISTING IN 2011 ........................................................................................................59

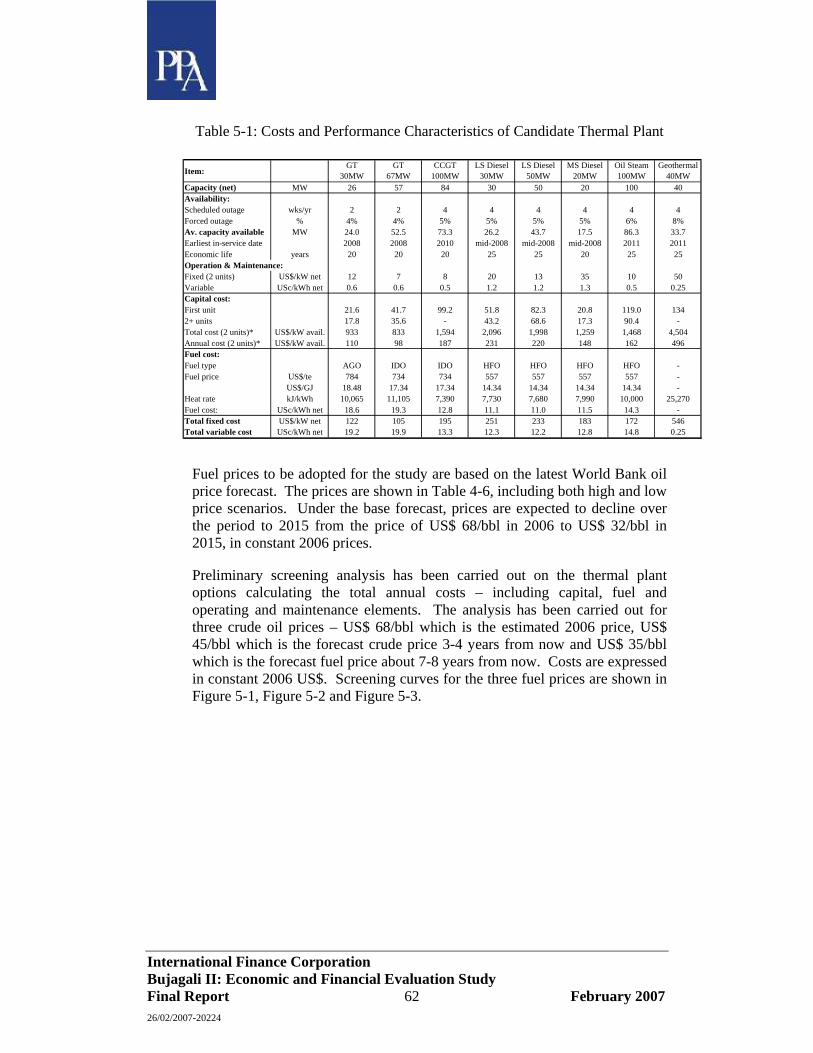

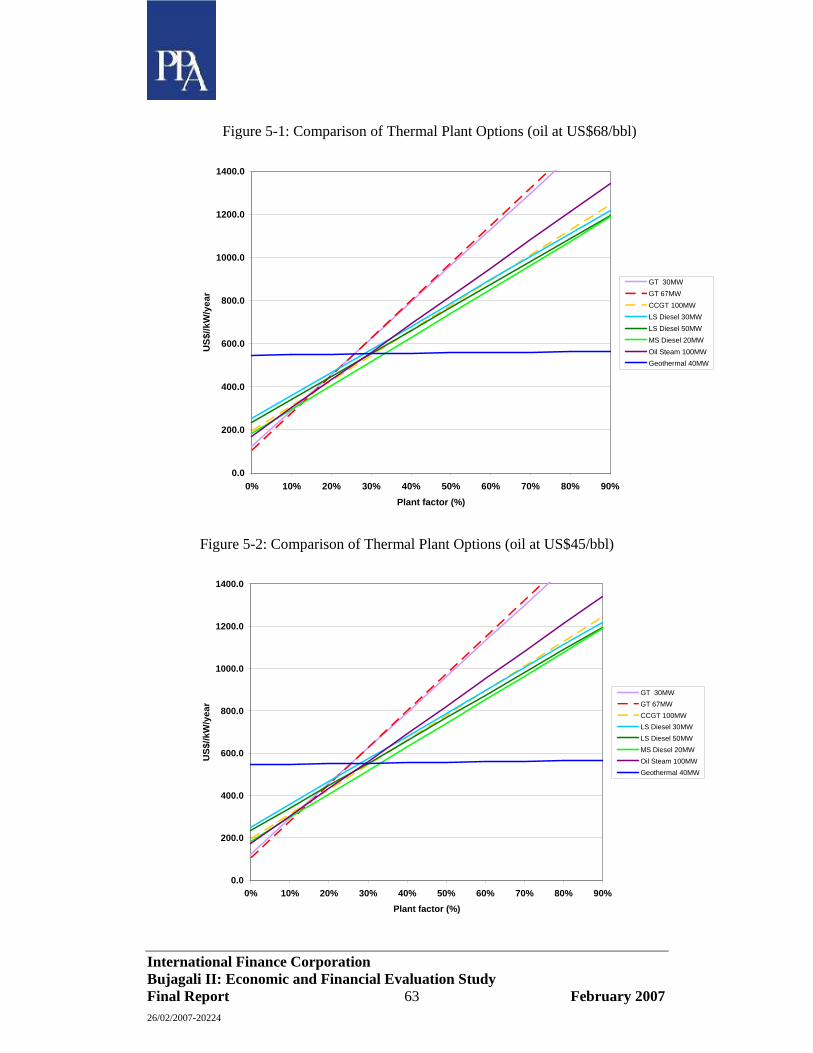

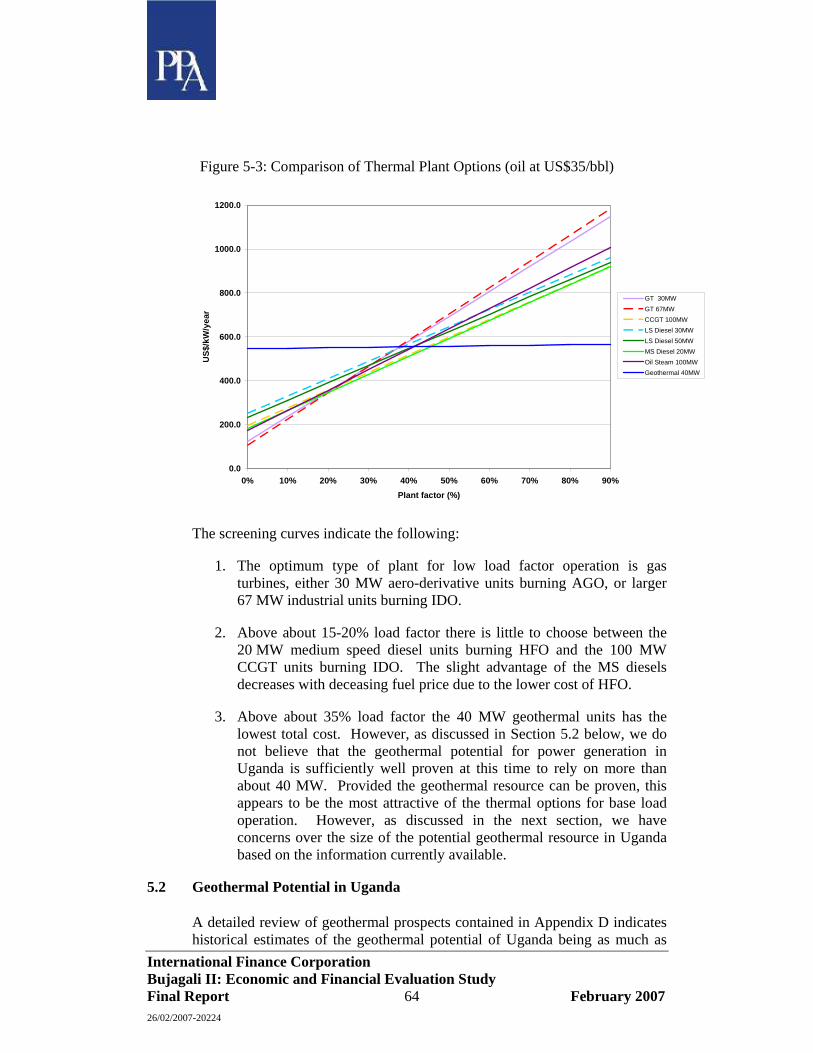

5 CANDIDATE PLANT (2011-2020) .............................................................................................61 5.1 CONVENTIONAL THERMAL PLANT..........................................................................................61 5.2 GEOTHERMAL POTENTIAL IN UGANDA...................................................................................64 5.3 EXISTING HYDRO ....................................................................................................................66 5.4 BUJAGALI HPP........................................................................................................................68

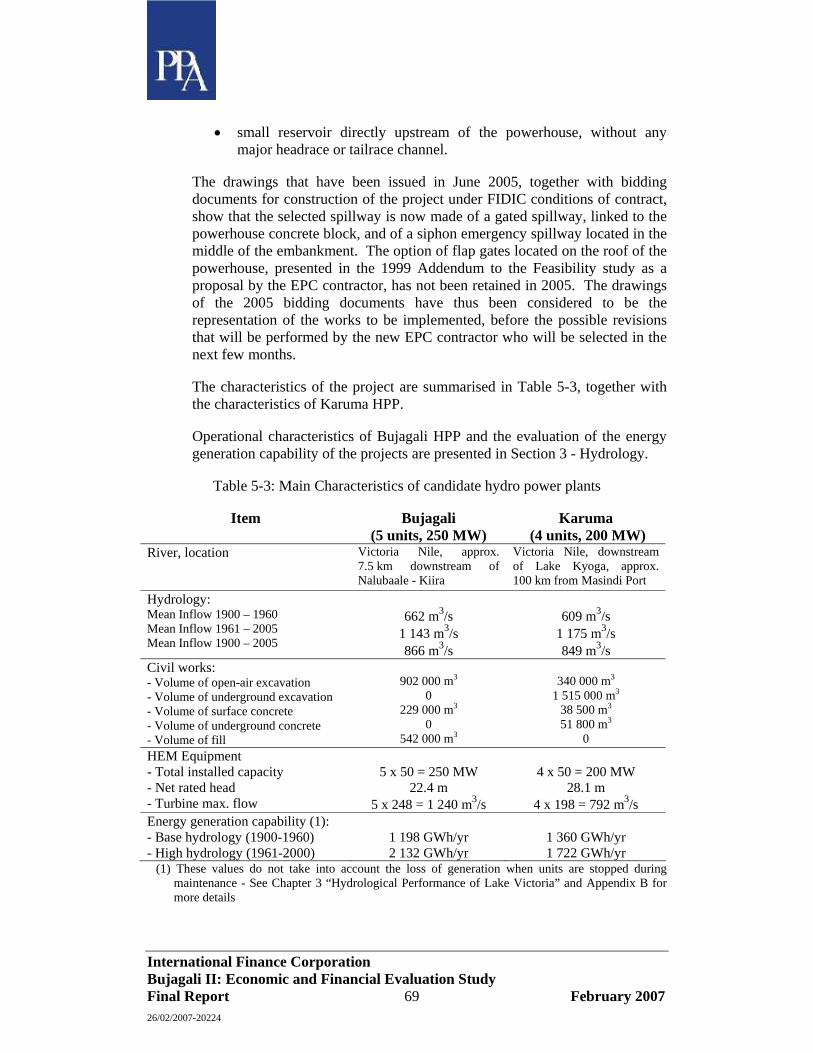

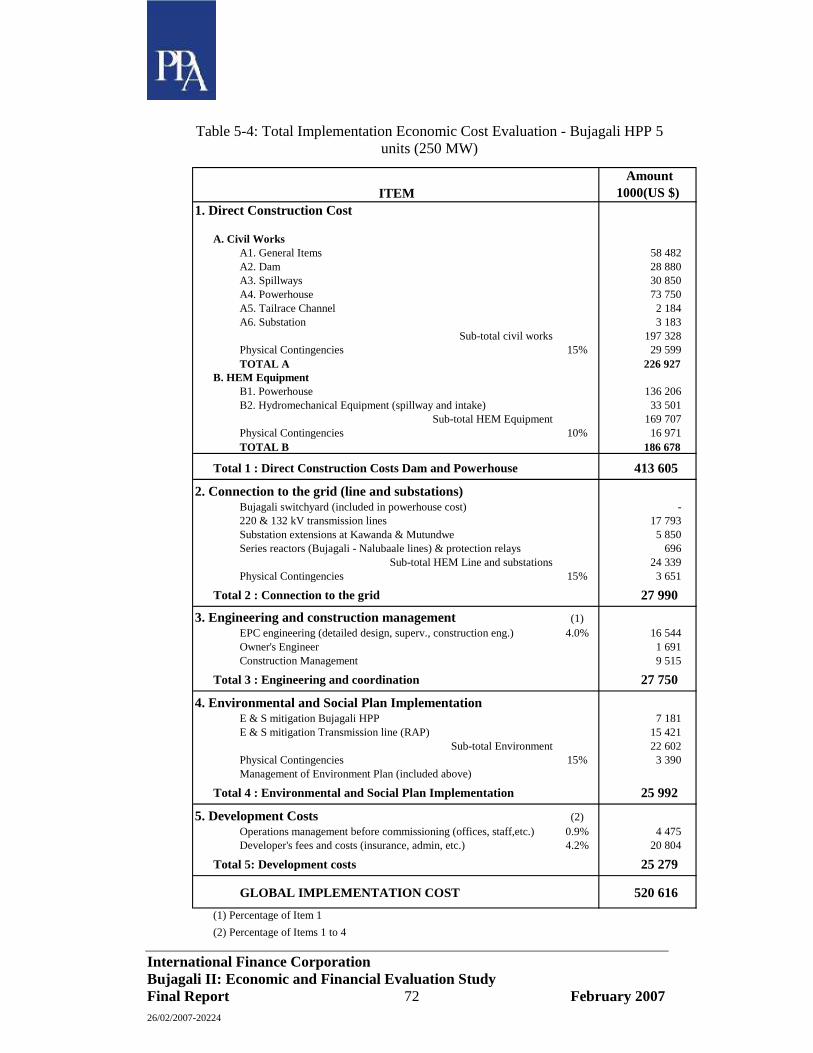

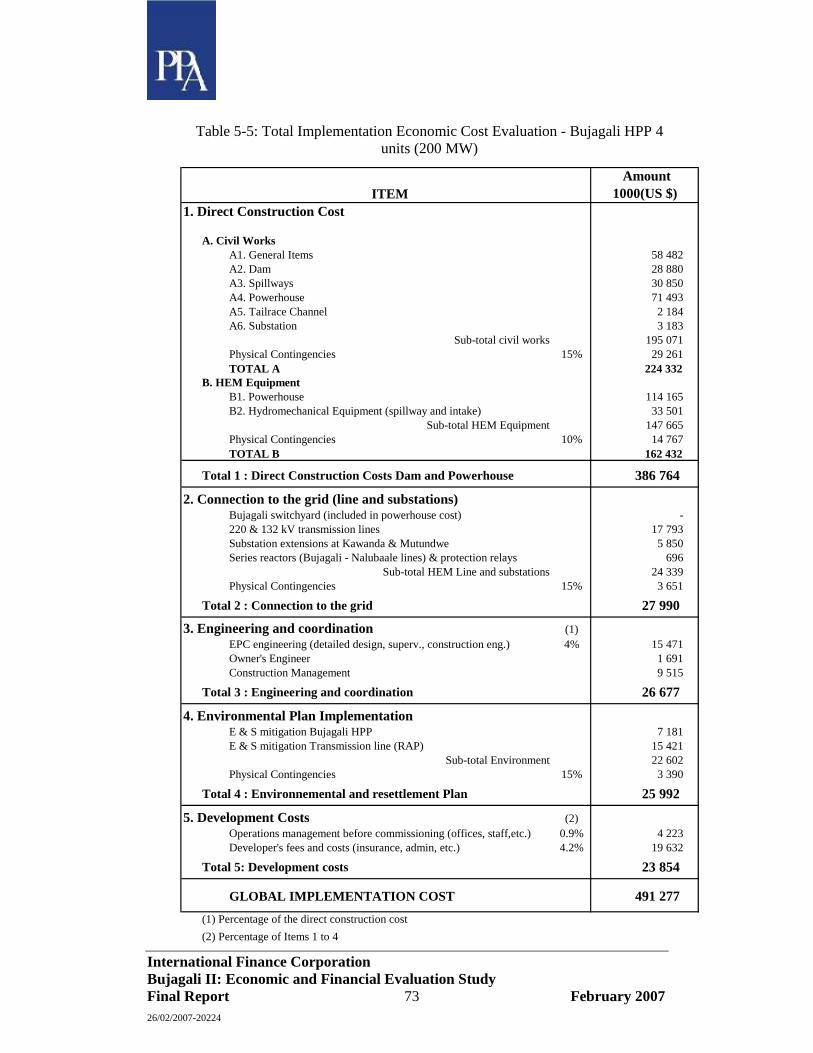

5.4.1 Characteristics of the project............................................................................................68 5.4.2 Construction Costs ............................................................................................................70 5.4.3 Other costs and resulting total cost of implementation....................................................71 5.4.4 Range of capital costs variations for risk analysis...........................................................74

5.5 KARUMA HPP .........................................................................................................................75 5.5.1 Characteristics of the project............................................................................................75 5.5.2 Construction costs .............................................................................................................76

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 3 February 2007 26/02/2007-20224

5.5.3 Other costs and resulting total cost of implementation....................................................77 5.6 OTHER CANDIDATE HYDRO....................................................................................................79

5.6.1 Other major hydro power projects....................................................................................79 5.6.2 Small and Medium Scale Hydro........................................................................................79

6 ENVIRONMENTAL AND SOCIAL COSTS ............................................................................81 6.1 INTRODUCTION........................................................................................................................81 6.2 ENVIRONMENTAL COSTS AND BENEFITS OF BUJAGALI..........................................................81

6.2.1 Dam and Power Station ....................................................................................................81 6.2.2 Transmission Line .............................................................................................................82 6.2.3 Environmental Benefits .....................................................................................................83

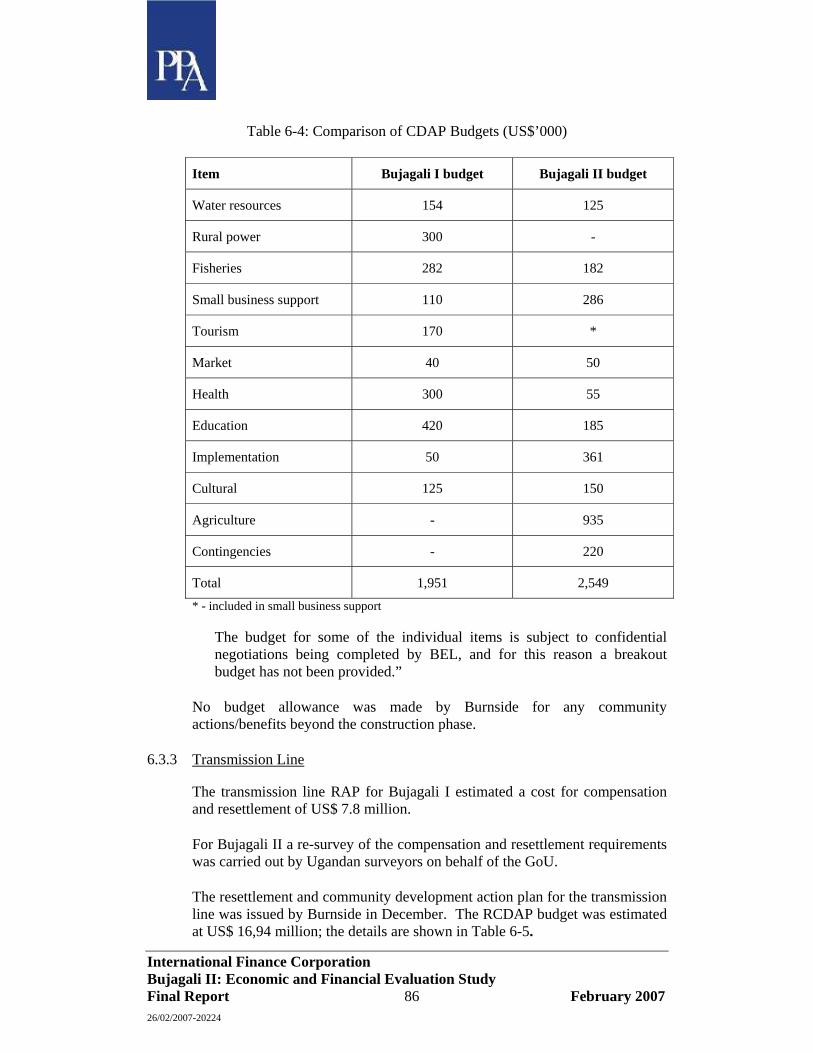

6.3 SOCIAL COSTS AND BENEFITS OF BUJAGALI ..........................................................................84 6.3.1 Compensation and Resettlement of Dam and Power House............................................84 6.3.2 Community Development Action Plan – CDAP ...............................................................85 6.3.3 Transmission Line .............................................................................................................86 6.3.4 Social costs by year ...........................................................................................................87

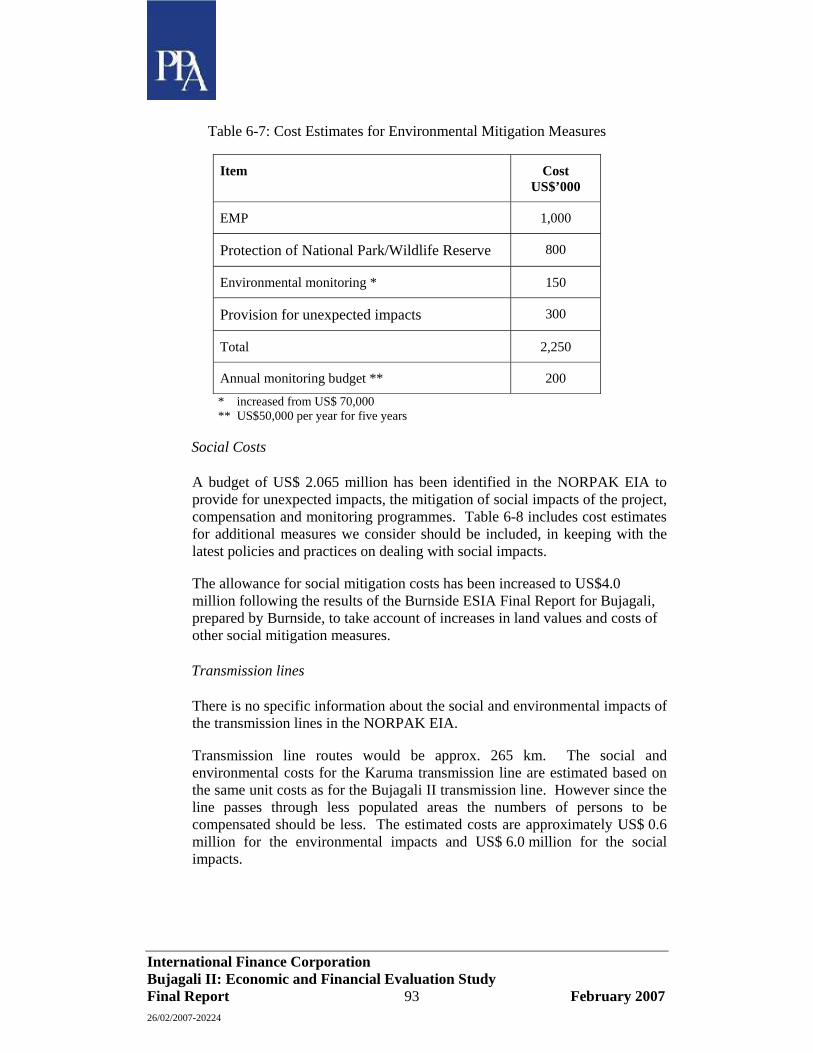

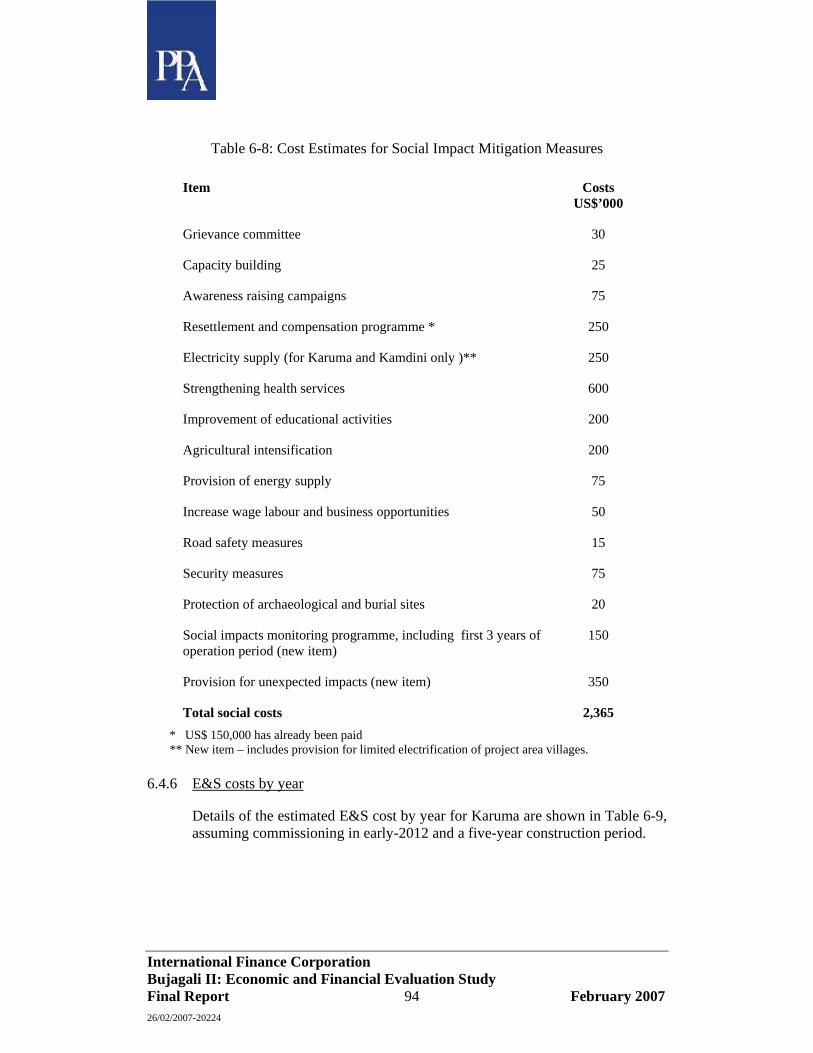

6.4 ENVIRONMENTAL COSTS AND BENEFITS OF KARUMA ...........................................................88 6.4.1 Introduction .......................................................................................................................88 6.4.2 Environmental Impacts......................................................................................................89 6.4.3 Social Impacts....................................................................................................................89 6.4.4 Mitigation and Compensation Measures ..........................................................................91 6.4.5 Environmental and Social Costs .......................................................................................92 6.4.6 E&S costs by year..............................................................................................................94 6.4.7 Environmental Benefits .....................................................................................................95

7 LEAST COST EXPANSION PLAN............................................................................................97 7.1 OBJECTIVES.............................................................................................................................97 7.2 PLANNING CRITERIA, METHODOLOGY AND BASIC DATA ......................................................97

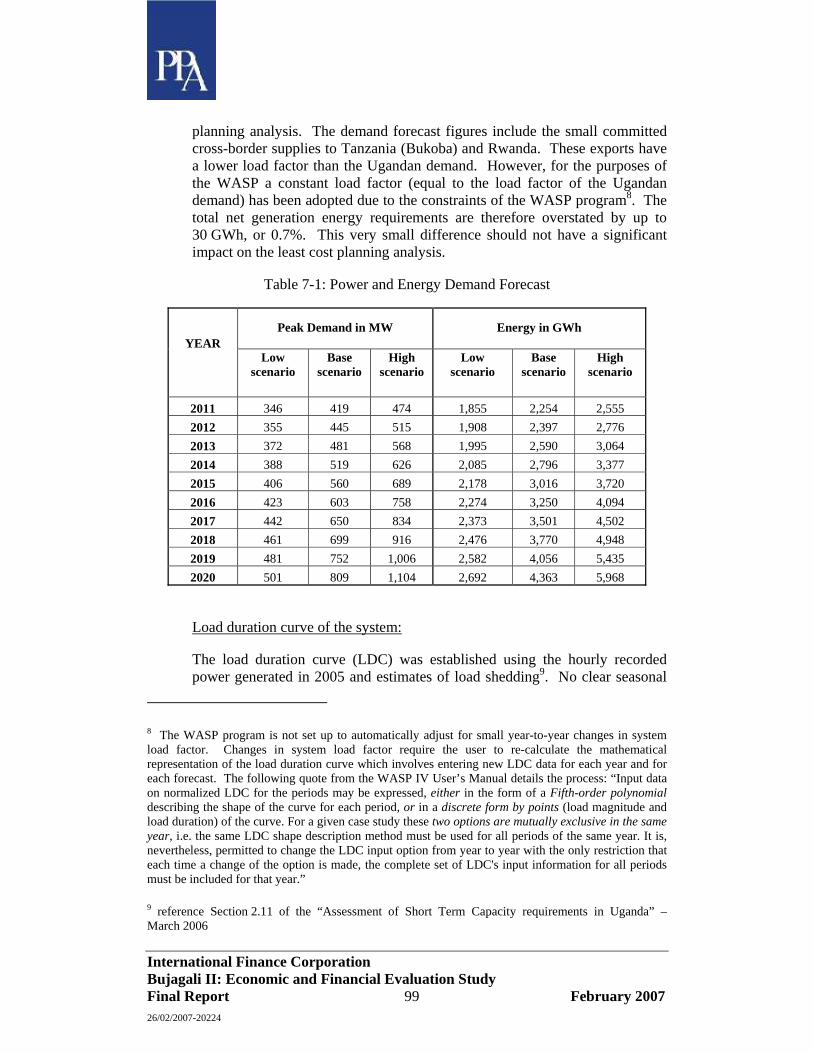

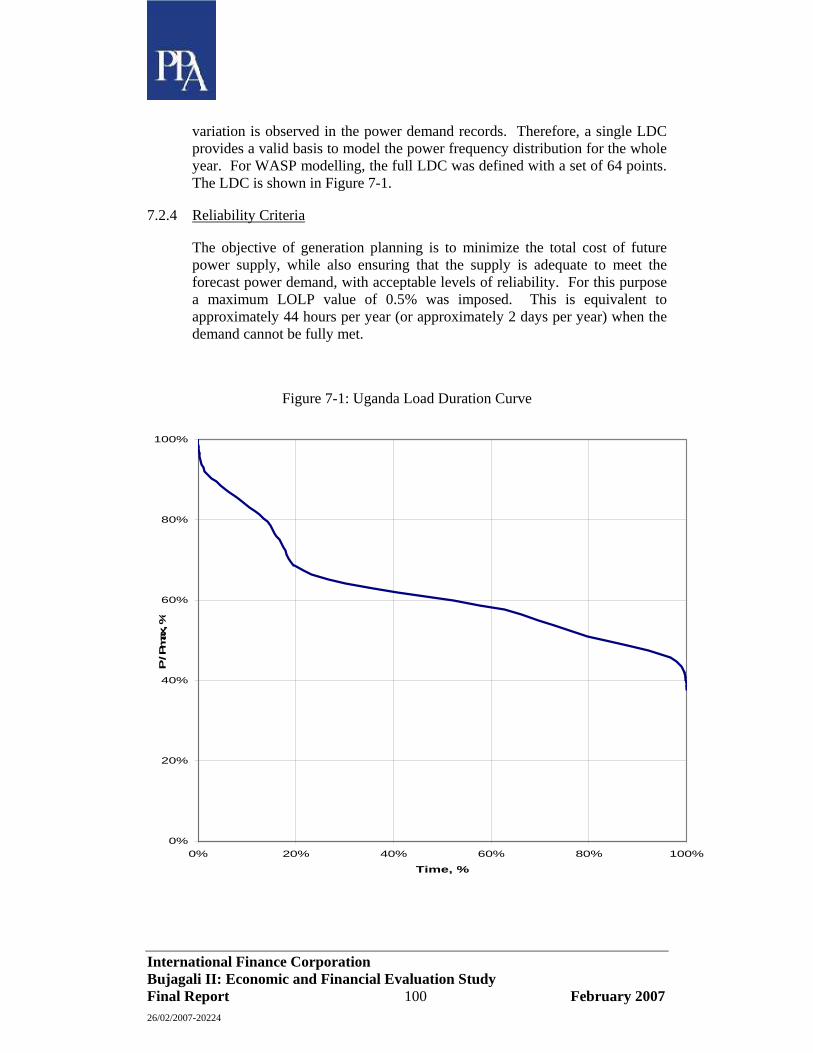

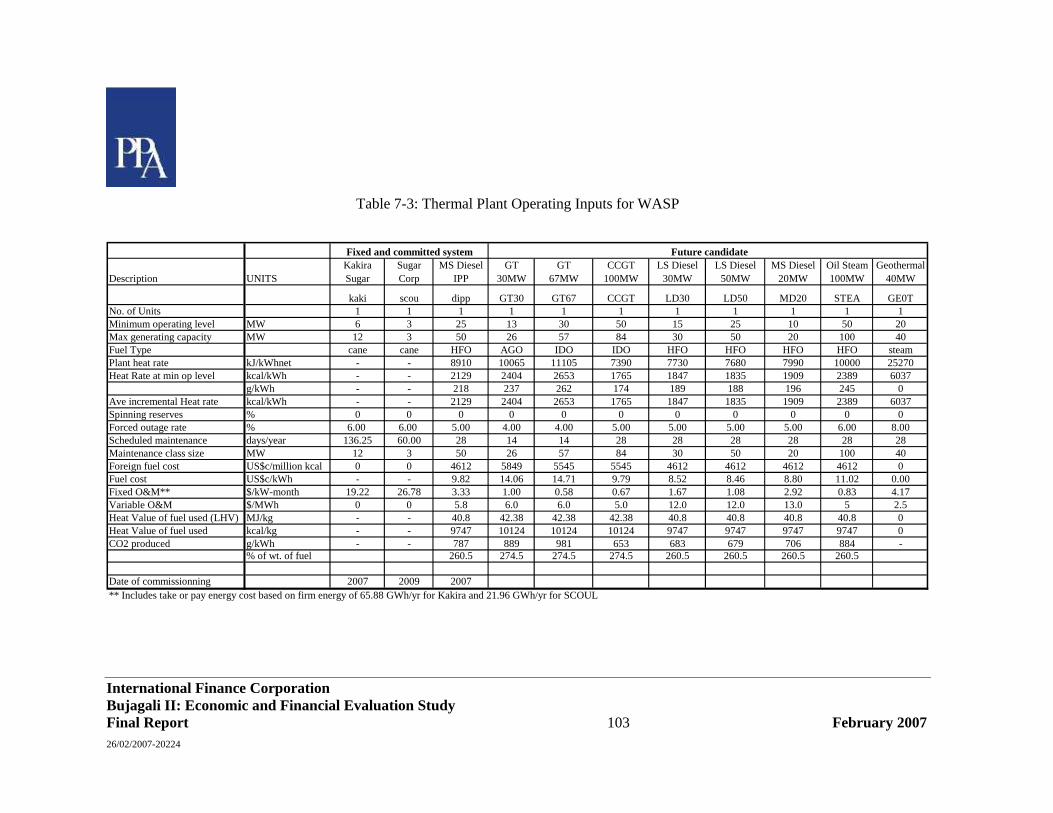

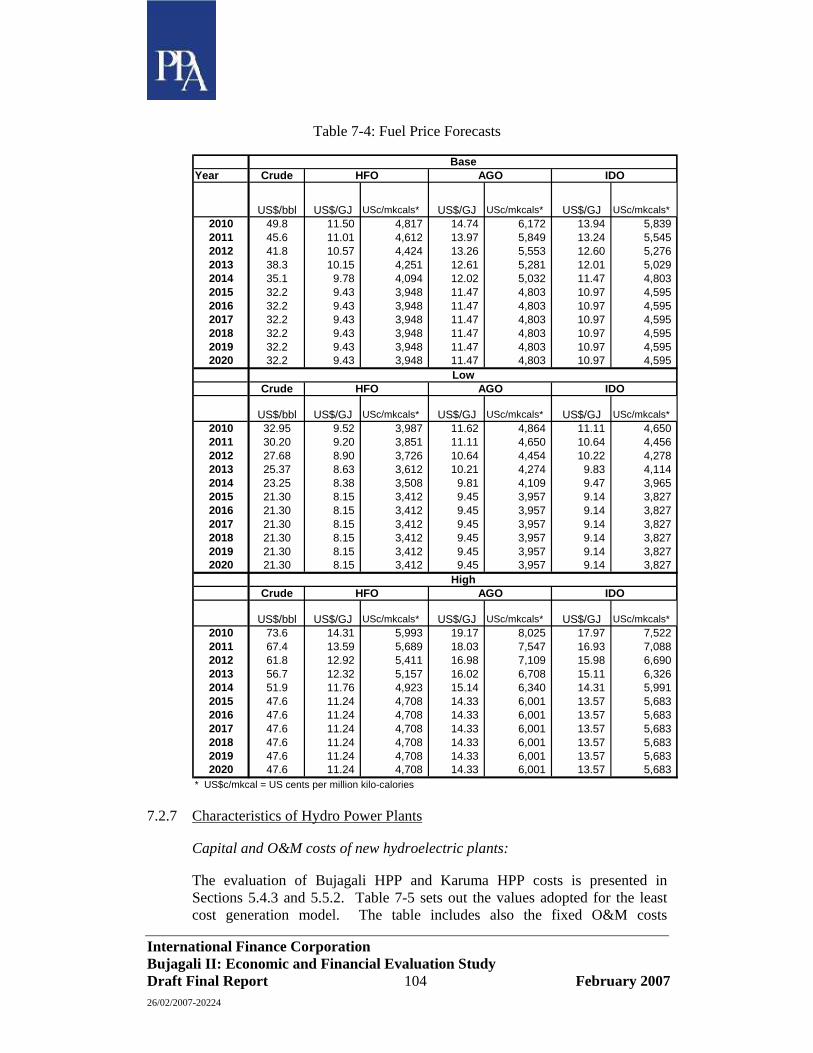

7.2.1 Computer tool and methodology.......................................................................................97 7.2.2 Planning Period.................................................................................................................98 7.2.3 Demand forecast................................................................................................................98 7.2.4 Reliability Criteria...........................................................................................................100 7.2.5 Economic Criteria ...........................................................................................................101 7.2.6 Characteristics of Thermal Plants ..................................................................................101 7.2.7 Characteristics of Hydro Power Plants..........................................................................104

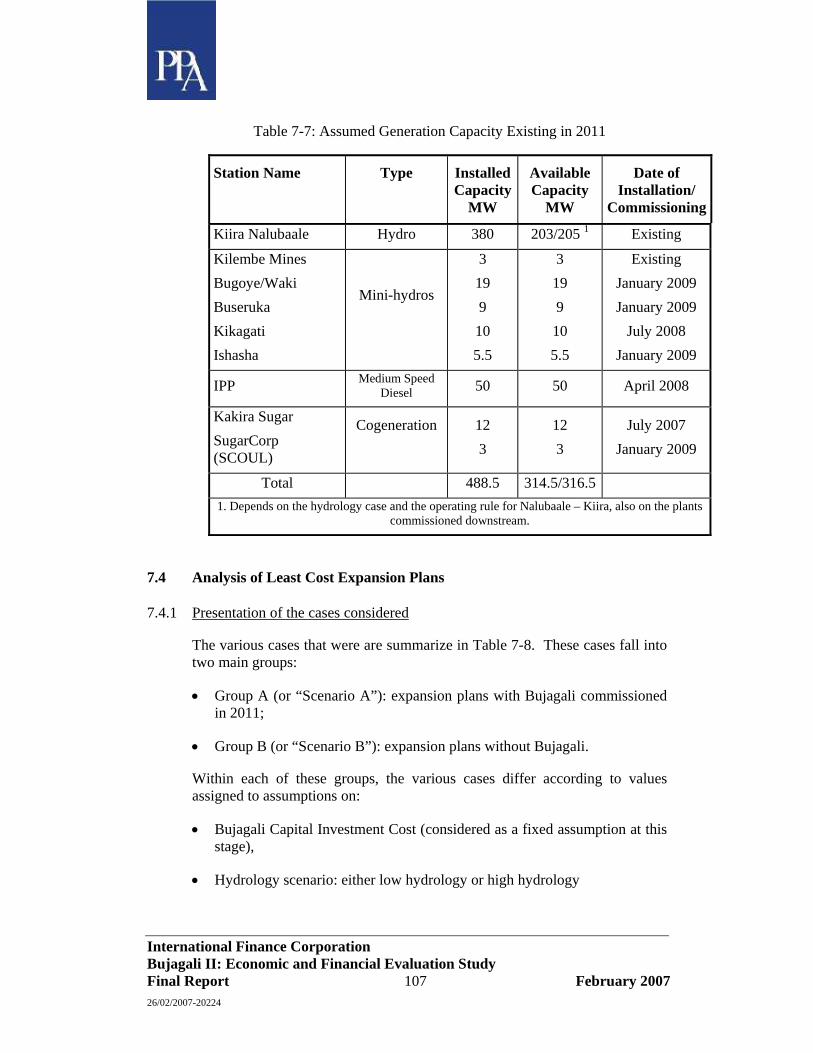

7.3 POWER GENERATION SITUATION IN 2011 ............................................................................106 7.4 ANALYSIS OF LEAST COST EXPANSION PLANS ....................................................................107

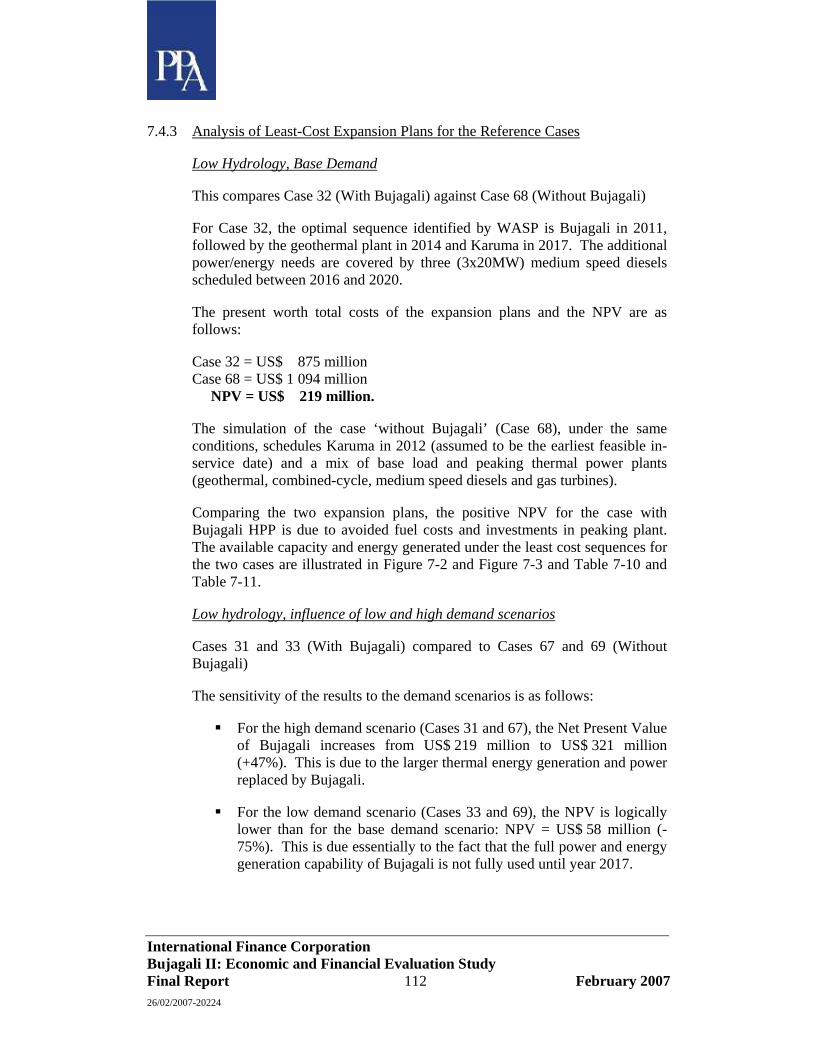

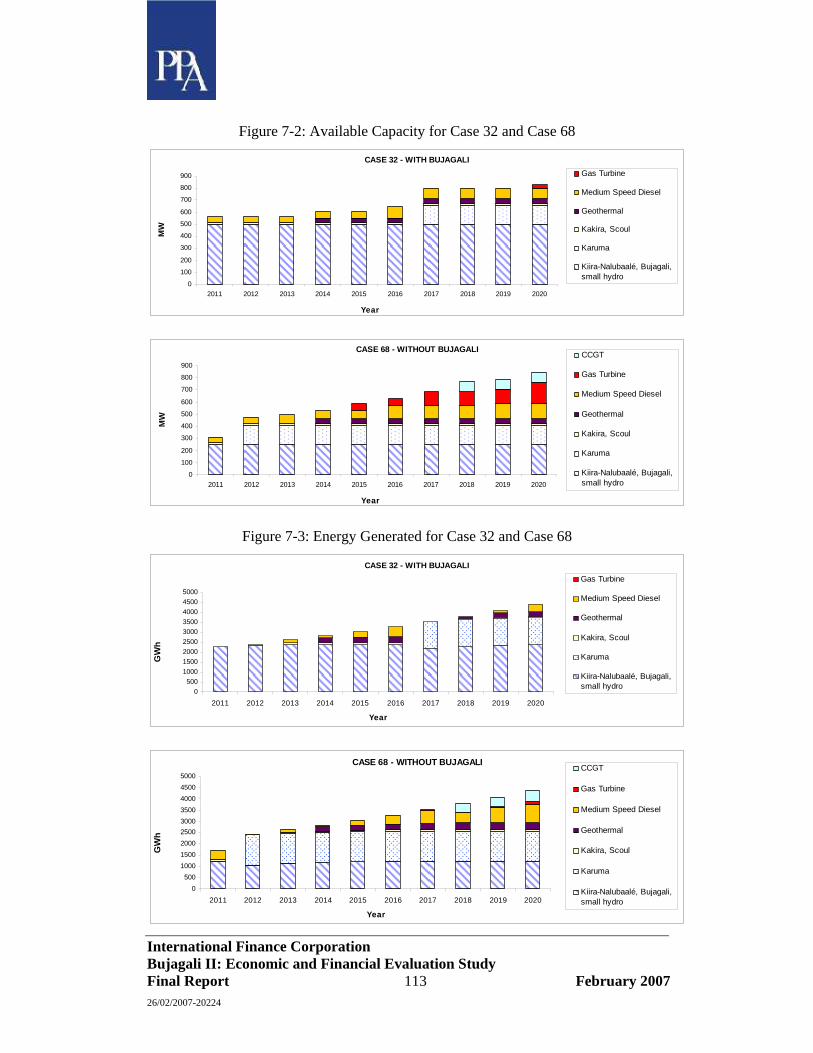

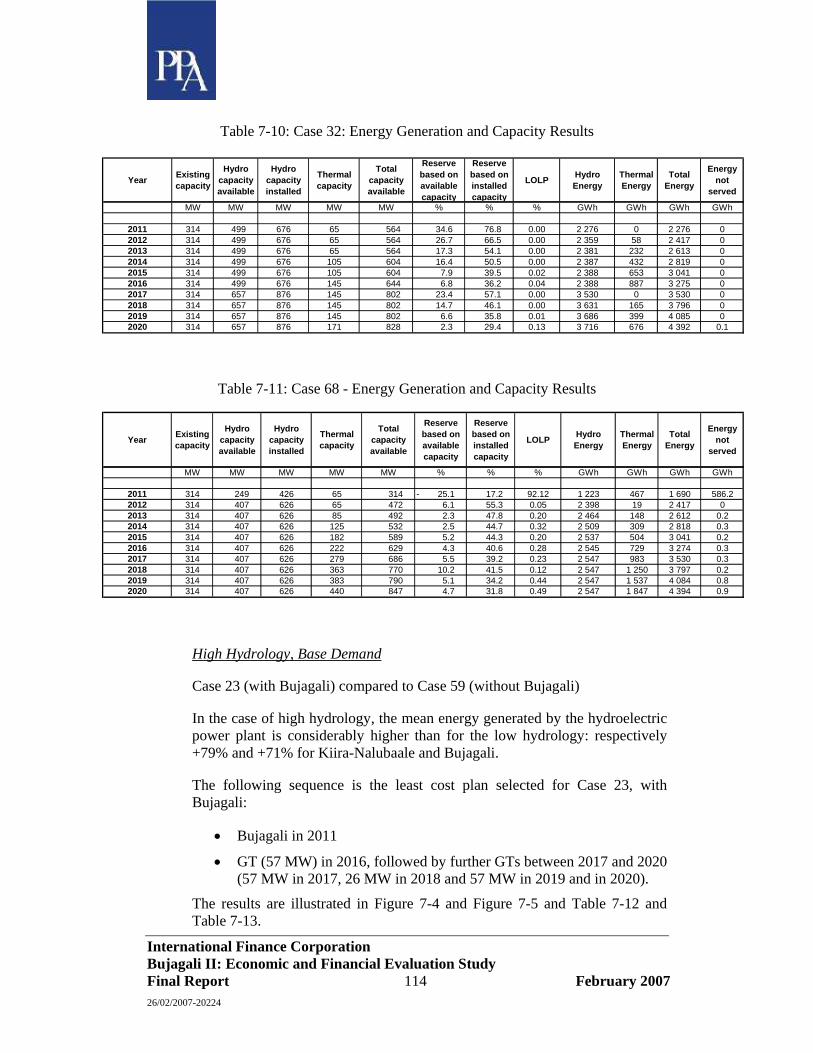

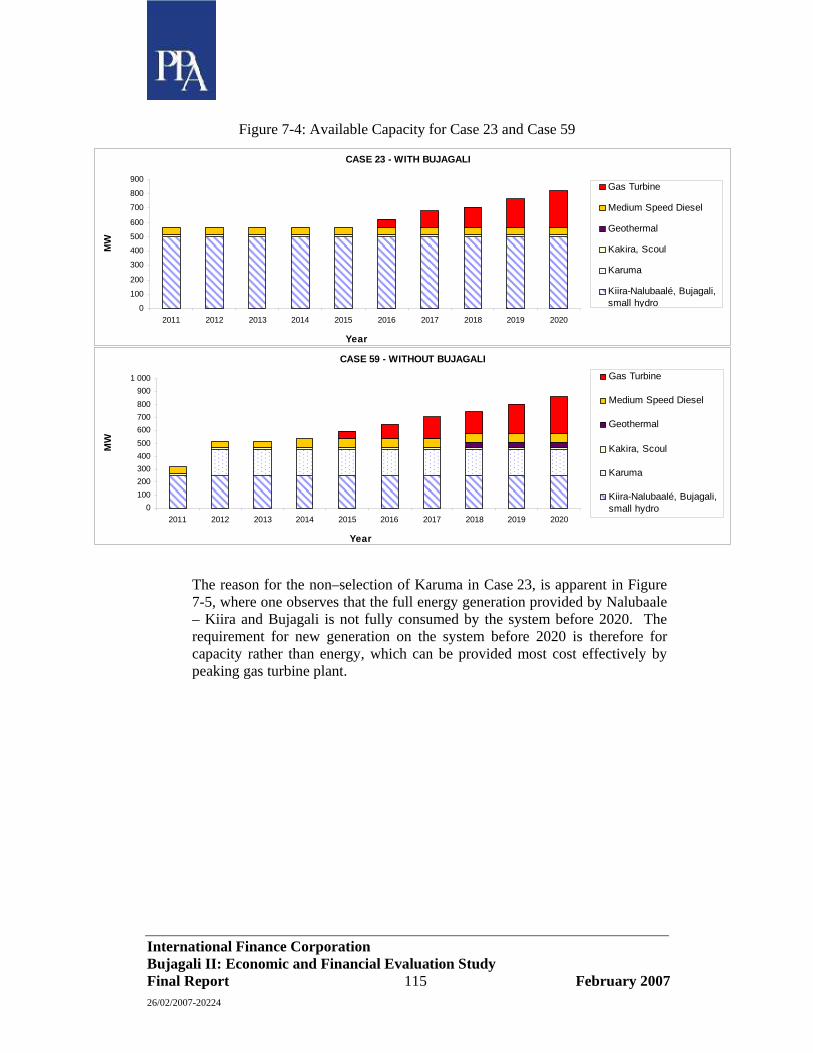

7.4.1 Presentation of the cases considered ..............................................................................107 7.4.2 Main Results and Conclusions of the Analysis ...............................................................108 7.4.3 Analysis of Least-Cost Expansion Plans for the Reference Cases.................................112 7.4.4 Analysis of Least-Cost Expansion Plans for sensitivity cases........................................117

7.5 RISK ANALYSIS .....................................................................................................................120 8 ECONOMIC RATE OF RETURN............................................................................................125

8.1 METHODOLOGY ....................................................................................................................125 8.2 ASSUMPTIONS .......................................................................................................................125

8.2.1 Baseline Assumptions for Incremental Costs and Demand............................................125 8.2.2 System Expansion Costs ..................................................................................................126 8.2.3 Reduction in Greenhouse Gas Emissions .......................................................................126 8.2.4 Incremental Demand .......................................................................................................127 8.2.5 Residual Displaced Thermal Energy ..............................................................................128 8.2.6 Unserved Energy Cost.....................................................................................................128

8.3 BENEFIT ASSUMPTIONS.........................................................................................................129 8.3.1 Household Willingness-to-Pay........................................................................................129 8.3.2 Industrial and Commercial Willingness-to-Pay .............................................................129 8.3.3 Export Willingness-to-Pay ..............................................................................................129

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 4 February 2007 26/02/2007-20224

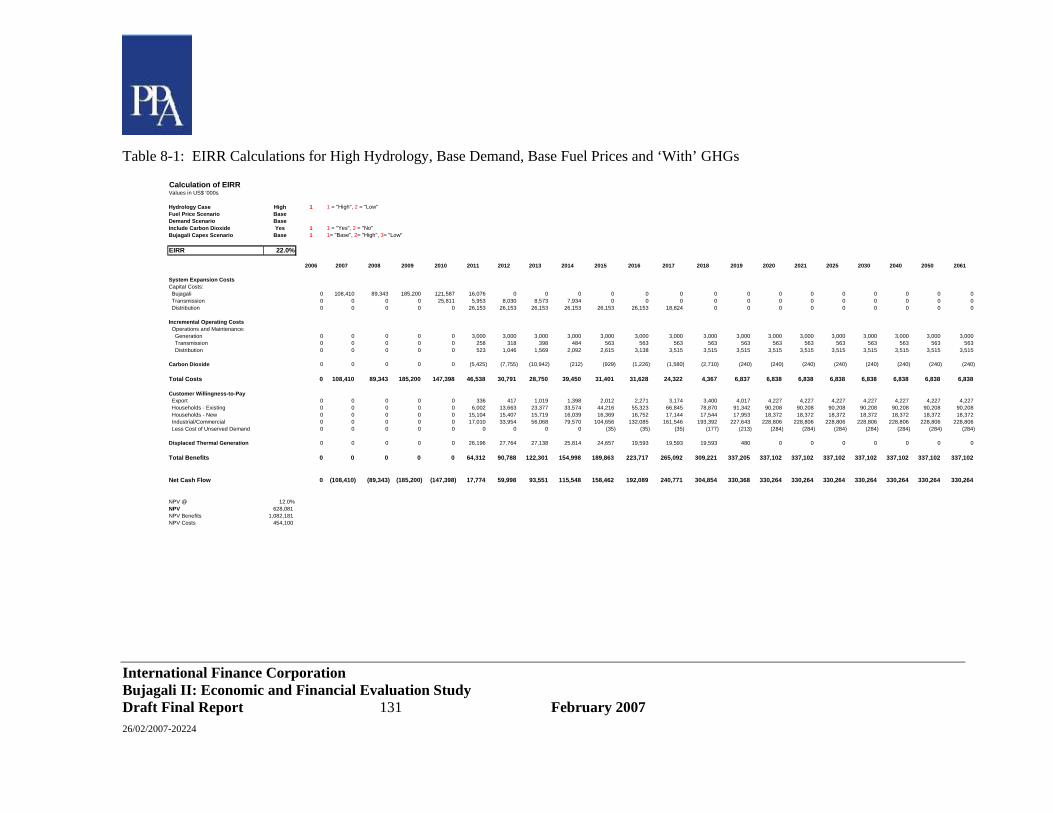

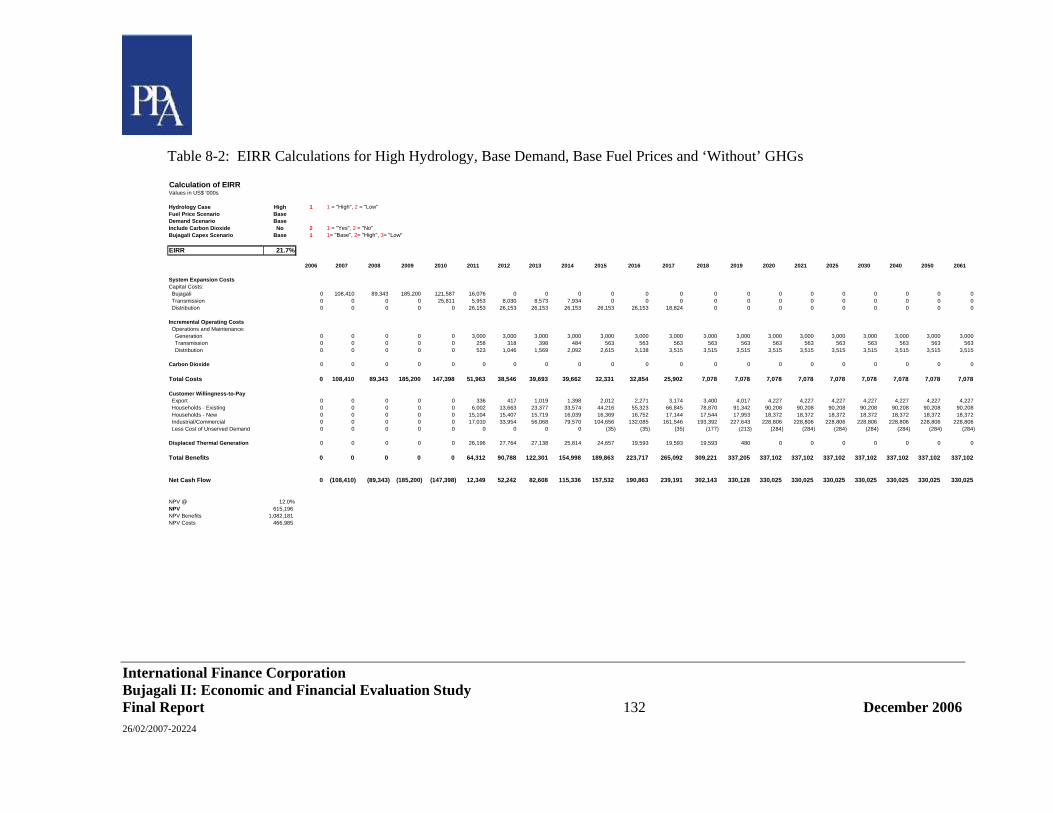

8.4 EXPECTED EIRR ...................................................................................................................130 8.4.1 General ............................................................................................................................130 8.4.2 High Hydrology ...............................................................................................................130 8.4.3 Low Hydrology ................................................................................................................130

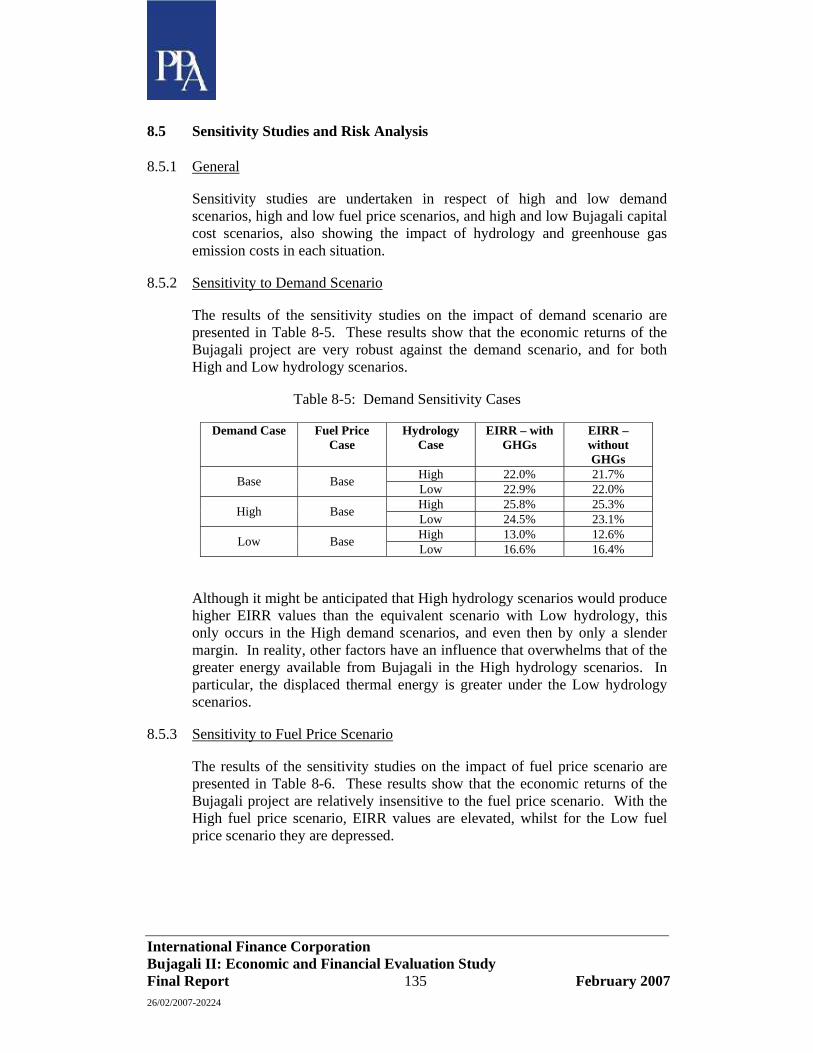

8.5 SENSITIVITY STUDIES AND RISK ANALYSIS .........................................................................135 8.5.1 General ............................................................................................................................135 8.5.2 Sensitivity to Demand Scenario ......................................................................................135 8.5.3 Sensitivity to Fuel Price Scenario ...................................................................................135 8.5.4 Sensitivity to Bujagali Capital Cost Scenario.................................................................136

8.6 RISK ANALYSIS .....................................................................................................................136 8.7 CONCLUSIONS .......................................................................................................................138

9 FINANCIAL FEASIBILITY......................................................................................................140 9.1 OBJECTIVES AND OUTPUTS ...................................................................................................140 9.2 REVIEW OF TARIFF METHODOLOGY ......................................................................................140

9.2.1 Tariff methodology for existing licensed generators......................................................141 9.2.2 Tariff methodology for other licensed generators ..........................................................141 9.2.3 Tariff methodology for planned and future generators ..................................................142 9.2.4 Tariff methodology for UETCL.......................................................................................142 9.2.5 Tariff methodology for Umeme .......................................................................................143 9.2.6 Subsidies ..........................................................................................................................145 9.2.7 Tariff stabilisation ...........................................................................................................146

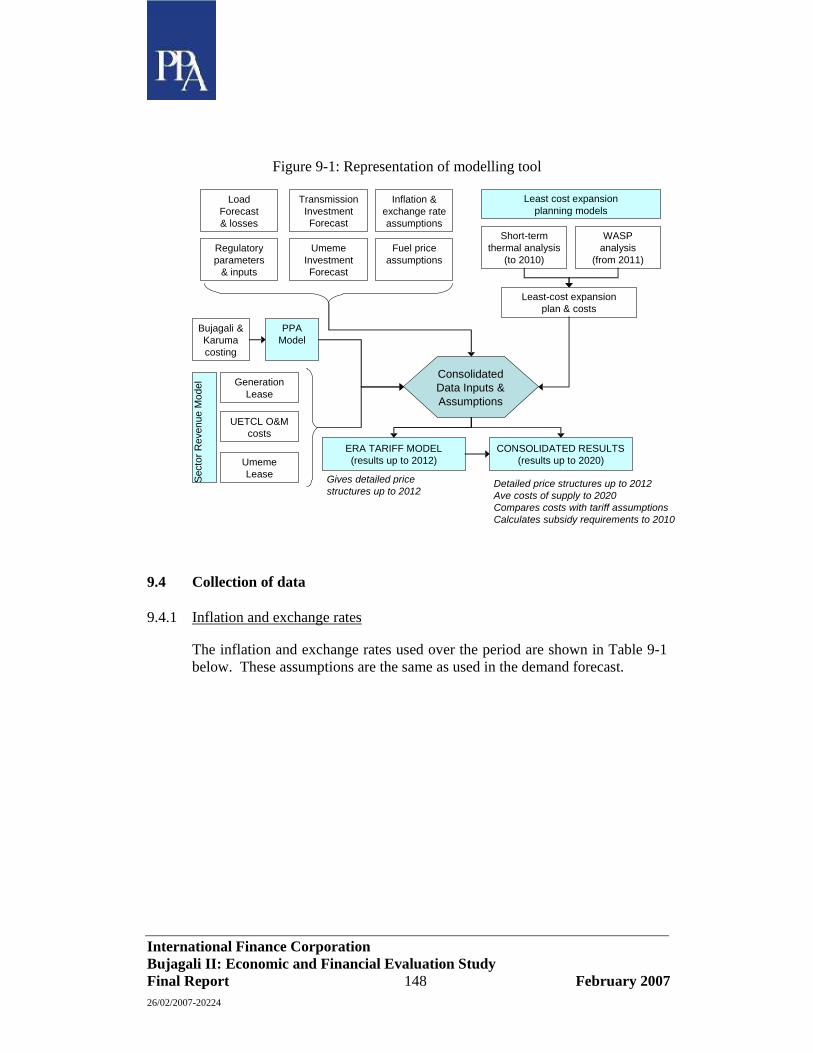

9.3 REVIEW OF TARIFF MODELS AND MODEL DEVELOPMENT .....................................................146 9.4 COLLECTION OF DATA...........................................................................................................148

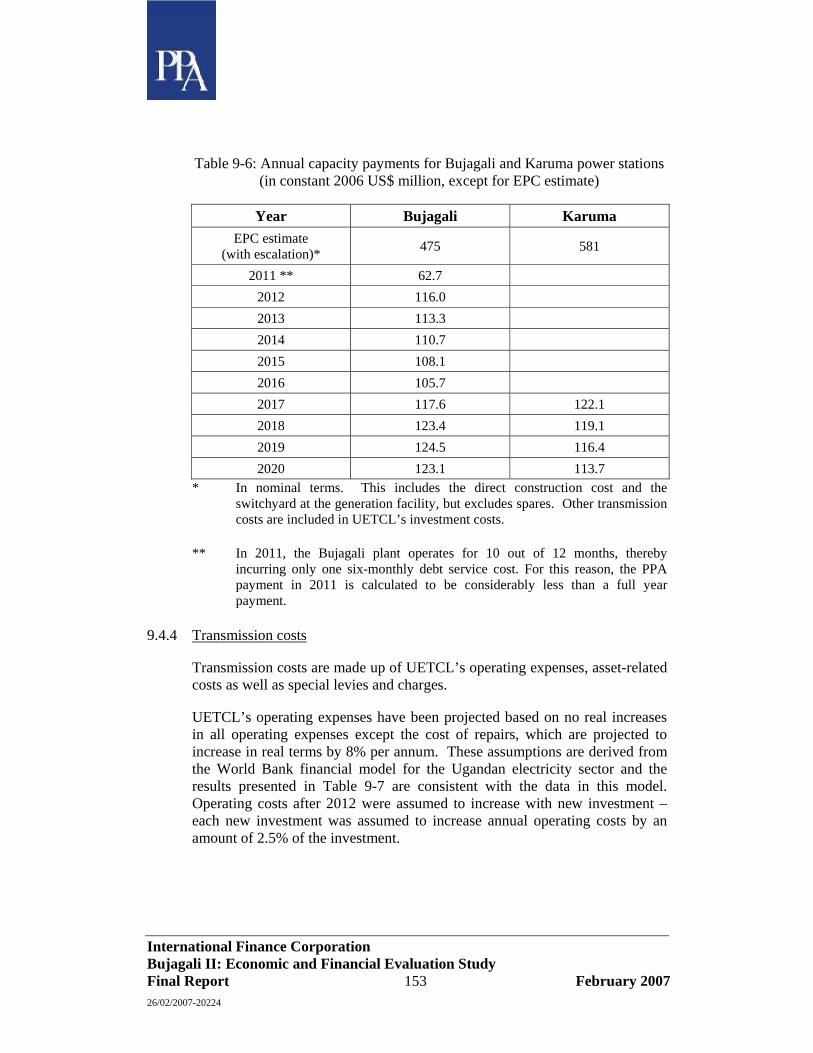

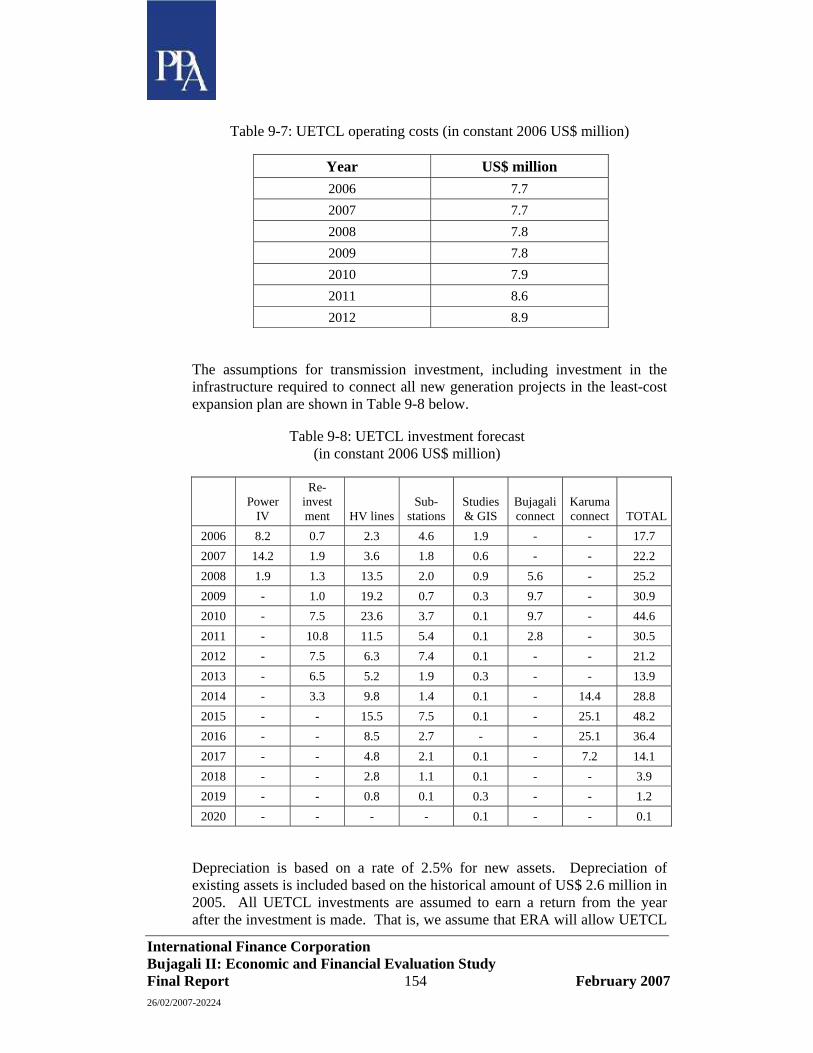

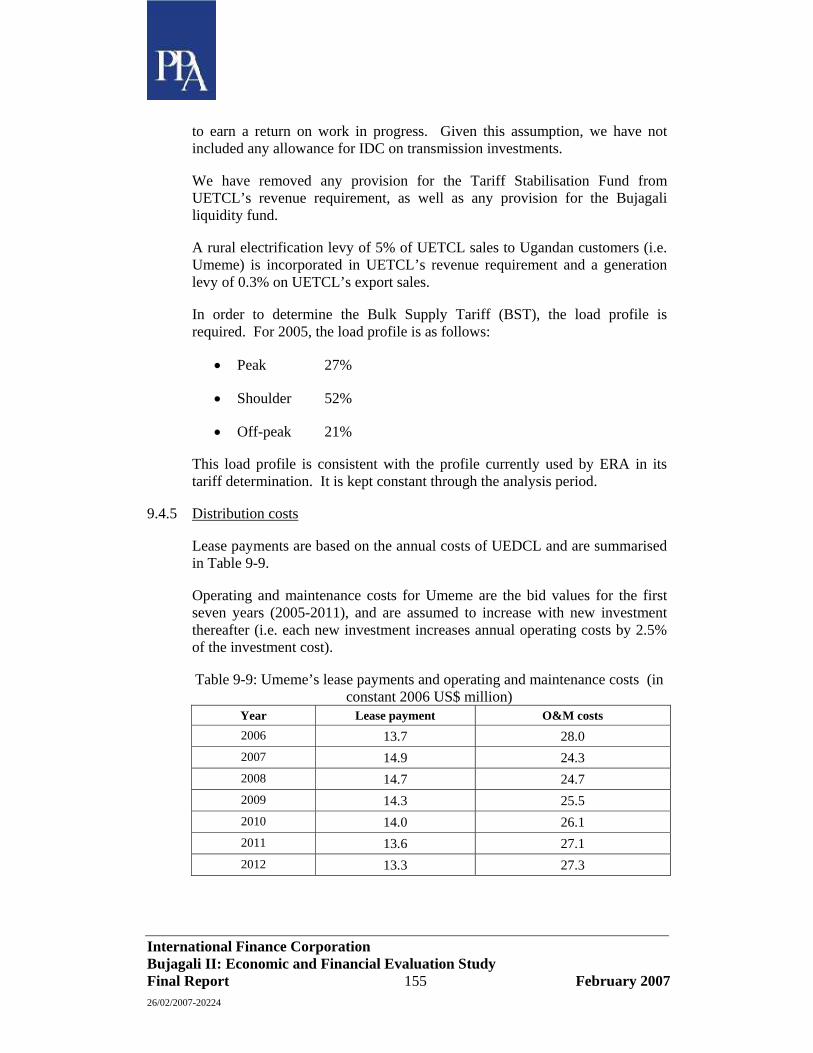

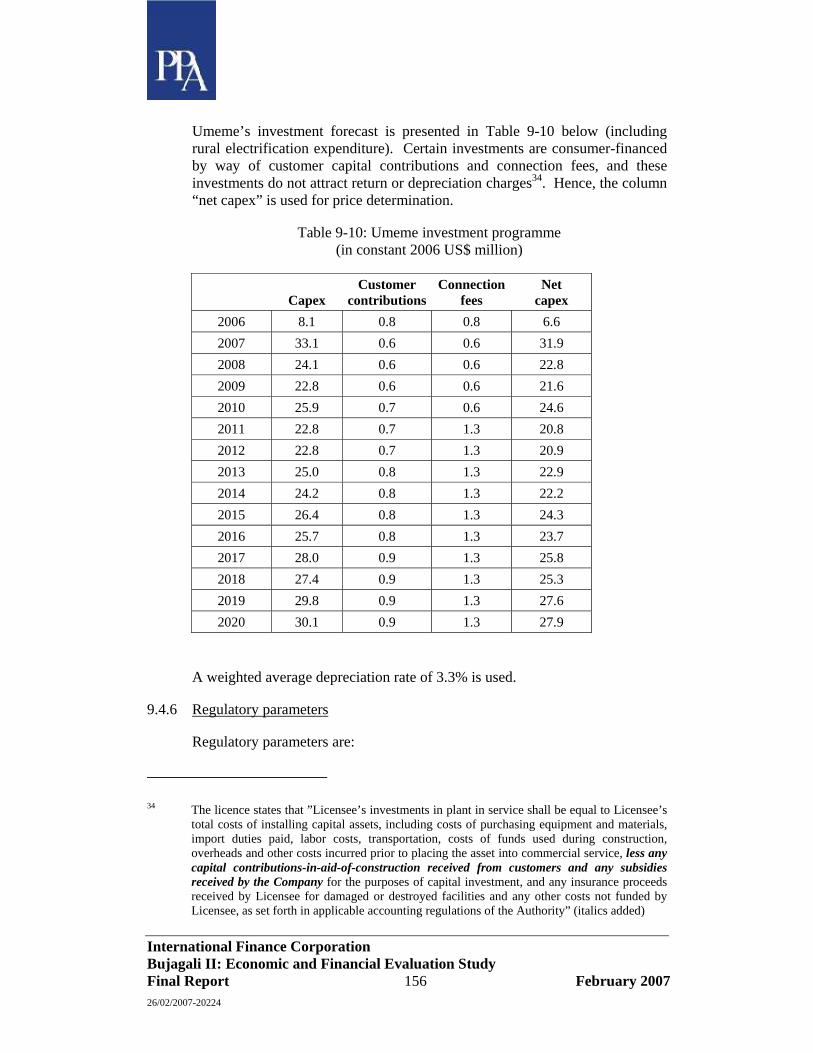

9.4.1 Inflation and exchange rates ...........................................................................................148 9.4.2 Demand forecast and losses............................................................................................149 9.4.3 Generation costs ..............................................................................................................150 9.4.4 Transmission costs...........................................................................................................153 9.4.5 Distribution costs.............................................................................................................155 9.4.6 Regulatory parameters ....................................................................................................156

9.5 RESULTS................................................................................................................................158 9.5.1 Revenue requirements in the electricity sector ...............................................................158 9.5.2 Comparing costs of supply with assumed tariffs ............................................................158 9.4.7 Impact of lower tariffs on demand forecast ....................................................................160

10 MACRO-ECONOMIC ANALYSIS ..........................................................................................162 10.1 SUMMARY .............................................................................................................................162 10.2 MACRO-ECONOMIC PARAMETERS ........................................................................................163

10.2.1 Availability of Modelling Tools..................................................................................163 10.2.2 Developments up to 2011 – the starting point ...........................................................163

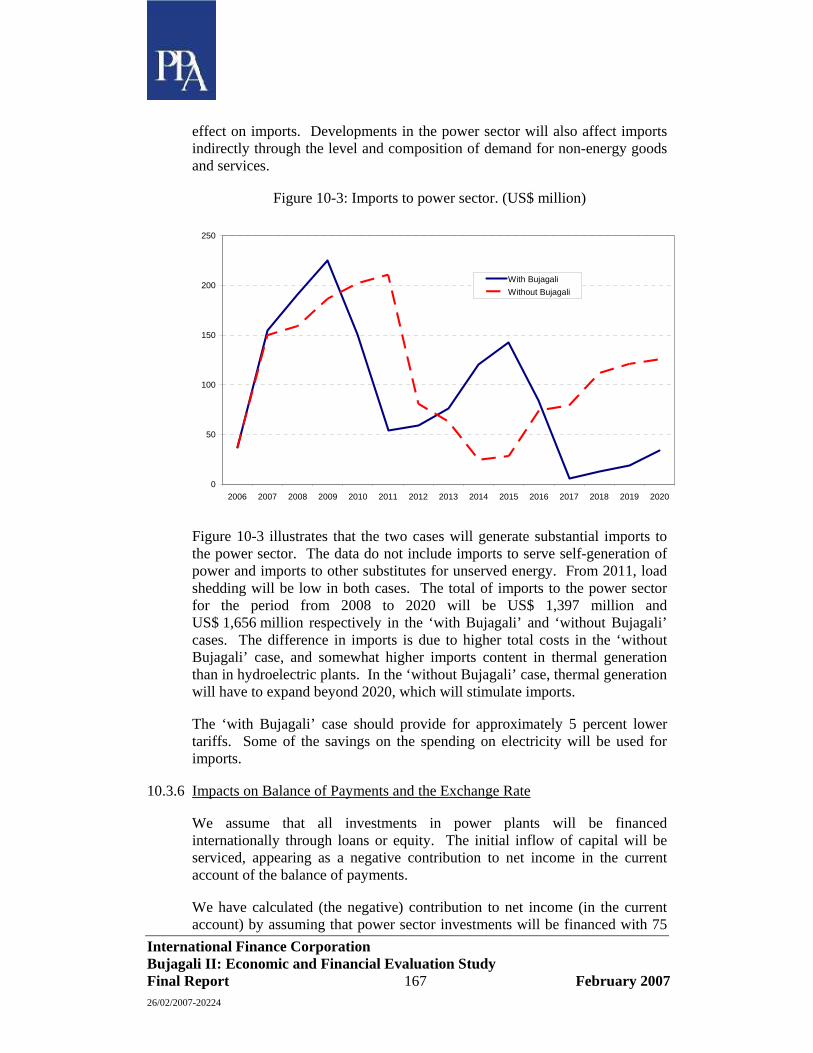

10.3 EFFECTS ON GDP COMPONENTS...........................................................................................163 10.3.1 Household consumption .............................................................................................163 10.3.2 General government consumption and investment....................................................164 10.3.3 Business investment ....................................................................................................164 10.3.4 Exports ........................................................................................................................166 10.3.5 Imports ........................................................................................................................166 10.3.6 Impacts on Balance of Payments and the Exchange Rate.........................................167

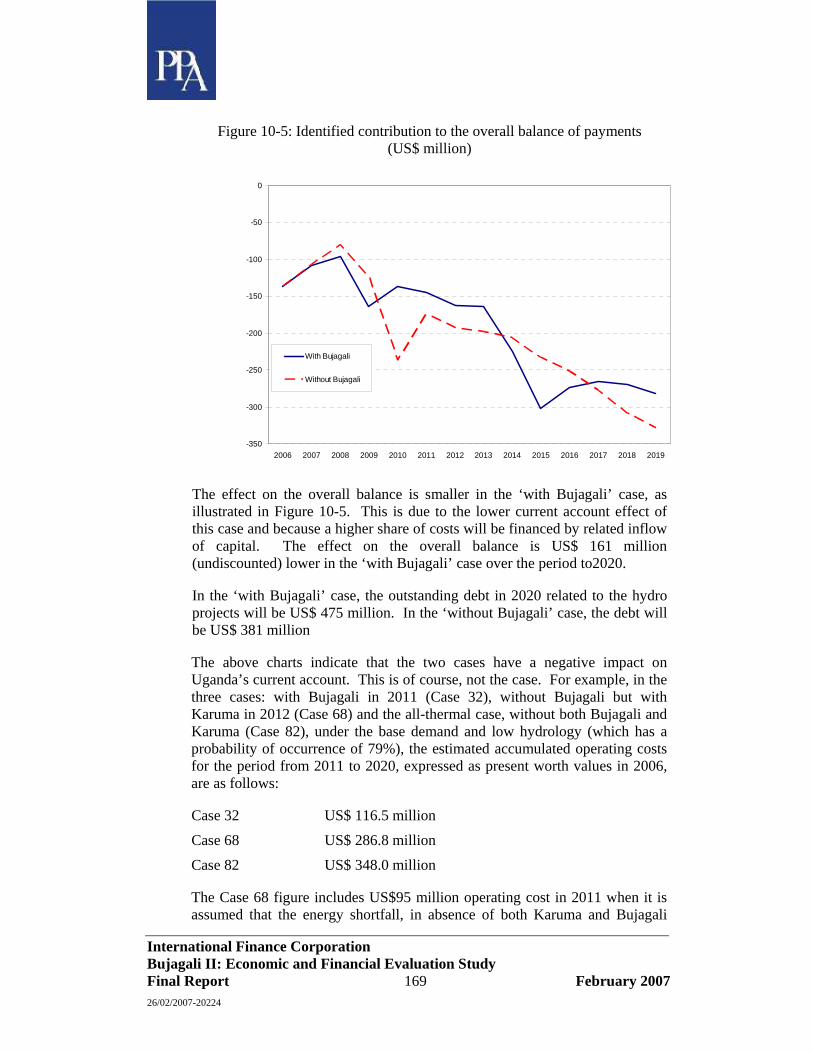

10.4 EFFECTS ON THE GOVERNMENT’S FINANCIAL POSITION ......................................................171

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 5 February 2007 26/02/2007-20224

List of Abbreviations used in the Report

ADO Automotive Diesel Oil

AGO Automotive Gas Oil

BEL Bujagali Electricity Limited

BIU Bujagali Implementation Unit

BOT Build, Operate and Transfer

BoU Bank of Uganda

C&R Compensation and Resettlement

CCGT Combined Cycle Gas Turbine

CDAP Community Development Action Plan

cSt Centi-Stokes

CUE Cost of Unserved Energy

DWD Department for Water Development

E&S Environmental and Social

EPC Engineer procurement and construct

ERA Electricity Regulatory Authority

ESIA Environmental and Social Impact Assessment

ESMAP Energy Strategy & Management Action Program

EV Evaporation

FOB Free on board

GDP Gross Domestic Product

GHG Greenhouse Gases

GoU Government of Uganda

GT Gas Turbine

HFO Heavy Fuel Oil

HPP Hydro Power Plant

HV High Voltage

IAEA International Atomic Energy Authority

IDA International Development Agency

IDC Interest during construction

IDO Industrial Diesel Oil

IMF International Monetary Fund

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 6 February 2007 26/02/2007-20224

IPP Independent Power Producer

ISO International Standards Organisation

KPLC Kenya Power & Lighting Company Limited

LDC Load Duration Curve

LOLP Loss of Load Probability

LSD Low Speed Diesel

LHV Lower heating value

Masl Metres above sea level

MoFPED Ministry of Finance Planning and Economic Development

MSD Medium Speed Diesel

MW Megawatt

NBS Net Basin Supply

NGO Non-Governmental Organisation

NPV Net Present Value

PPA Power Purchase Agreement

PW Present-worth

RAP Resettlement Action Plan

RE Rural Electrification

REA Rural Electrification Agency

RF Rainfall

RO Runoff

ROW Right of way

SCADA Supervisory Control and Data Acquisition

SCOUL Sugar Company of Uganda Limited

STD Sexually-Transmitted Disease

ToR Terms of Reference

UBOS Uganda Bureau of Statistics

UEB Uganda Electricity Board

UEDCL Uganda Electricity Distribution Company Limited

UETCL Uganda Electricity Transmission Company Limited

US$ United States Dollar

US¢ United States cents

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 7 February 2007 26/02/2007-20224

USh Uganda Shilling

WASP Wien Automatic System Planning Package

WREM Water Resources and Environmental Management

WTI West Texas Intermediate

WTP Willingness-to-Pay

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 8 February 2007 26/02/2007-20224

Executive Summary

Power Planning Associates was appointed by the IFC in January 2006 to carry out an economic and financial evaluation study of the 250 MW Bujagali II hydropower project in Uganda. The ToR for the assignment are reproduced in Appendix A. The purpose of this study is to evaluate the economic viability of the Bujagali II project taking into account economic, financial, social and environmental aspects.

An Interim Report was submitted in February 2006; the report was presented to the Government of Uganda (GoU) and other stakeholders in Kampala in March 2006. Work was then held up for a number of months whilst the World Bank carried out an independent review of the analysis of the hydrology presented in the Interim Report. The demand forecast was also reviewed and amended to include updated GDP estimates and a detailed assessment of the assumptions of future levels of technical and commercial losses. The revised forecast was presented to GoU and other stakeholders in Kampala in September 2006.

The Draft Final Report was submitted to IFC in December 2006 and presented to the government and other stakeholders in Kampala in mid-January 2007. The report was also presented to the Bujagali lenders in London at the end of January.

We now present a brief synopsis of the results and conclusions of the study following the order of the sections in the Main Text of the Report. The Main Text volume is supported by Appendices which are included in a separate volume.

Background

The economic and financial analysis of the Bujagali project in this study includes an update for the hydrology of the lake and development of potential future hydrological scenarios, both for the short and medium term. Had the Bujagali project been commissioned in 2005/06, as envisaged back in 2000, the current problems would not have arisen, or at least not to the same extent. In the intervening years there has been continuing demand growth, coupled with severe supply constraints that would have been alleviated had Bujagali come into service in 2005. The experience has demonstrated the high cost penalties of long term delays in the Bujagali project that was needed to meet the growing electricity demand of Uganda.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 9 February 2007 26/02/2007-20224

Electricity Demand Forecast for the Uganda System

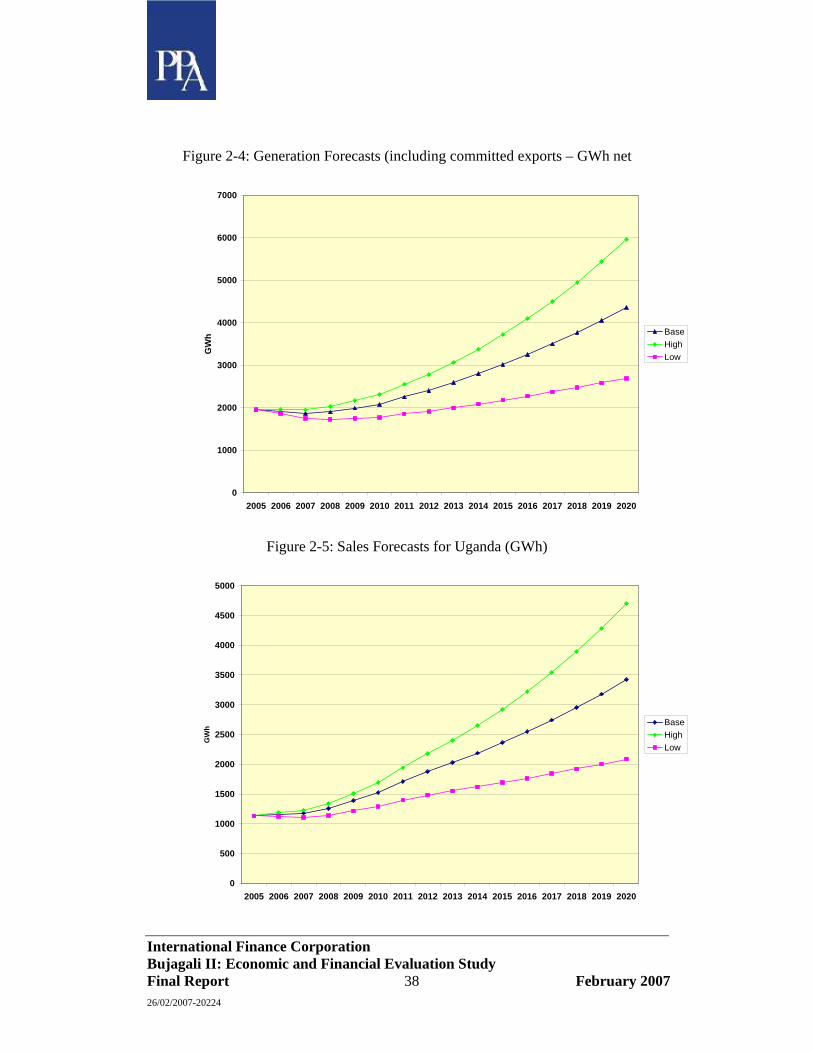

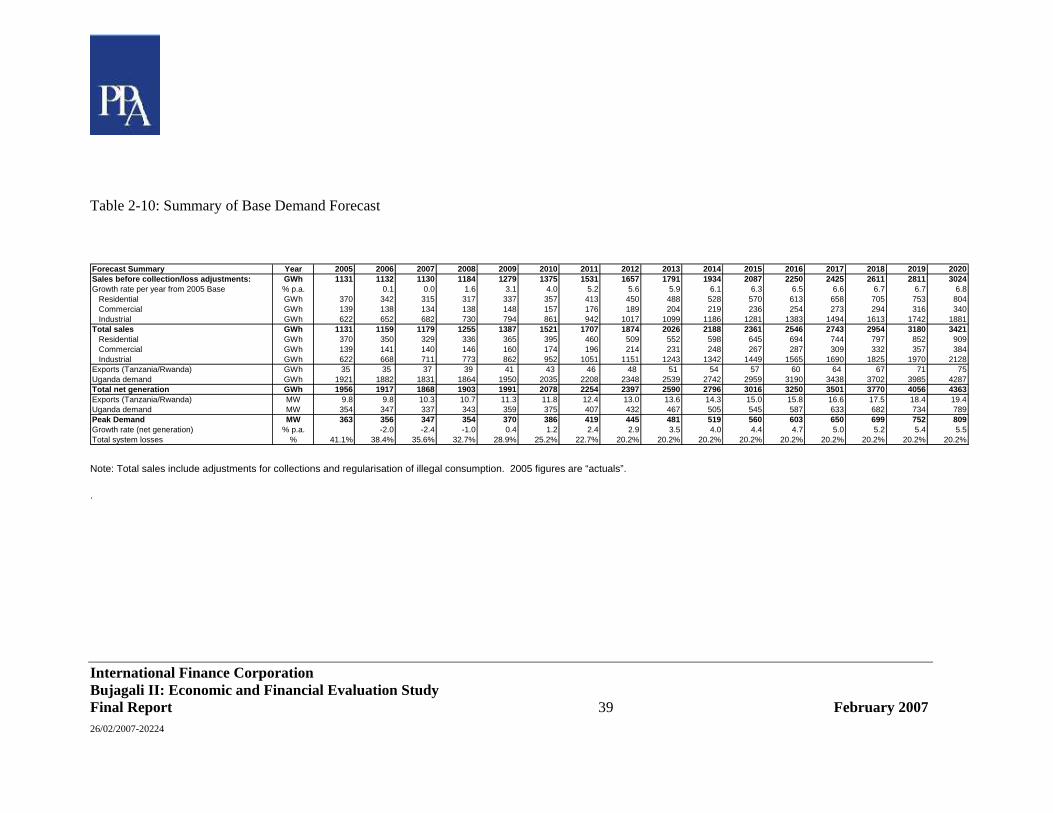

A demand forecast for the Ugandan grid has been derived using the most recent data on the economy and the electricity sub-sector1. The forecast is predicated on assumptions for the growth of the economy, connection of new consumers, and the reduction of system losses, in particular commercial losses. The base case forecast is summarised in the table below.

Year Peak Demand

(MW) Generation (GWh net)

Sales (GWh)

2005 (actual) 354 1921 1131

2010 375 2208 1521

2015 545 2959 2361

2020 789 4287 3421 Note: Figures in table above exclude exports to Tanzania and Rwanda.

High and low sensitivity forecasts have also been derived based on alternative economic growth and consumer connection assumptions. The base, high and low forecasts are predicated on forecast tariffs during the period up to 2011 when Bujagali is expected to come into service. The tariff projections are based on the financial requirements of the short-term emergency thermal power generation programme and the estimated generation availability from Nalubaale – Kiira.

The 2007 to 2011 tariff assumptions have been derived from the detailed financial analysis of an independent consultant contracted by the World Bank as part of the appraisal of the emergency thermal power project, for which GoU is seeking IDA funding. The tariff assumptions are for increases in real tariffs of 37% in 2006, 45% in 20072 and 15% in 2008. A reduction of 15% is assumed in 2011, when the commissioning of Bujagali should reduce thermal generation substantially. The demand forecast, least cost planning studies and associated financial/tariff analysis were carried out on the basis of the above tariff assumptions. The resulting cost of supply and imputed tariffs were then checked against the original tariff assumptions to ensure that the price

1 Note: data collection for the demand forecast was carried out in January 2006.

2 Tariffs were in fact increased by approximately 42% in November 2006, which was not known when the load forecast was finalized. This increase will have its full impact on 2007 demand, almost in line with the Consultant’s assumption.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 10 February 2007 26/02/2007-20224

elasticity effect which has been factored into the demand forecast remained valid. It was found that the assumed tariffs were above the cost of supply, post-2011, by approximately 1.2 US¢/kWh (7%). Even if the tariff were to drop in line with cost of supply, the positive impact on the demand forecast would be minimal.

Hydrology and Energy Outputs of Hydro Plants

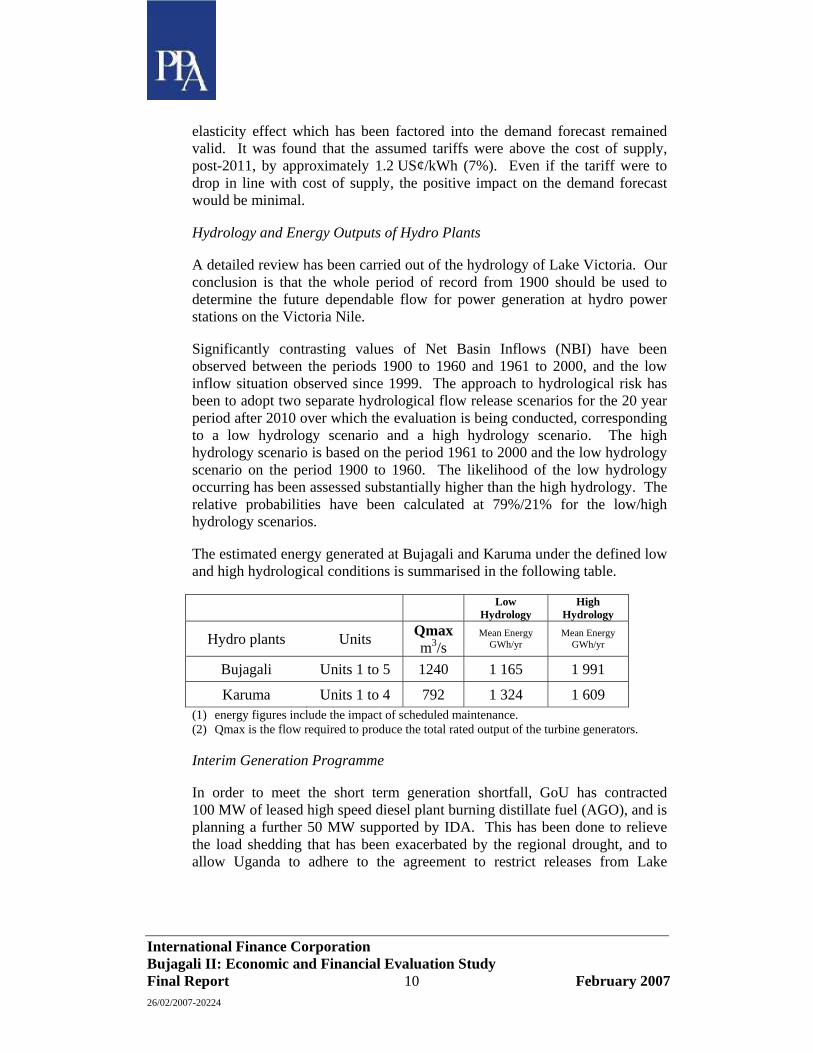

A detailed review has been carried out of the hydrology of Lake Victoria. Our conclusion is that the whole period of record from 1900 should be used to determine the future dependable flow for power generation at hydro power stations on the Victoria Nile.

Significantly contrasting values of Net Basin Inflows (NBI) have been observed between the periods 1900 to 1960 and 1961 to 2000, and the low inflow situation observed since 1999. The approach to hydrological risk has been to adopt two separate hydrological flow release scenarios for the 20 year period after 2010 over which the evaluation is being conducted, corresponding to a low hydrology scenario and a high hydrology scenario. The high hydrology scenario is based on the period 1961 to 2000 and the low hydrology scenario on the period 1900 to 1960. The likelihood of the low hydrology occurring has been assessed substantially higher than the high hydrology. The relative probabilities have been calculated at 79%/21% for the low/high hydrology scenarios.

The estimated energy generated at Bujagali and Karuma under the defined low and high hydrological conditions is summarised in the following table.

Low Hydrology

High Hydrology

Hydro plants Units Qmax m3/s

Mean Energy GWh/yr

Mean Energy GWh/yr

Bujagali Units 1 to 5 1240 1 165 1 991

Karuma Units 1 to 4 792 1 324 1 609 (1) energy figures include the impact of scheduled maintenance. (2) Qmax is the flow required to produce the total rated output of the turbine generators.

Interim Generation Programme

In order to meet the short term generation shortfall, GoU has contracted 100 MW of leased high speed diesel plant burning distillate fuel (AGO), and is planning a further 50 MW supported by IDA. This has been done to relieve the load shedding that has been exacerbated by the regional drought, and to allow Uganda to adhere to the agreement to restrict releases from Lake

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 11 February 2007 26/02/2007-20224

Victoria to the “Agreed Curve”3. A further 50 MW of medium speed diesel plants burning heavy fuel oil (HFO) is expected to be installed as an Independent Power Project (IPP). The emergency thermal plant is intended to fill the generation capacity gap until 2011 when Bujagali is expected to enter service. The thermal plant will be supplemented by several small hydro projects to be developed as IPPs. In addition, UETCL has negotiated contracts with two sugar producers for 15 MW of power produced from bagasse (sugar cane residue).

Geothermal Potential

We have made a detailed review of the geothermal potential of Uganda and conclude that the resource may be substantially lower than previously estimated. It is considered that only approximately 40 MW of geothermal power generating capacity may be developed economically on the basis of present knowledge, as discussed in detail in Appendix D.

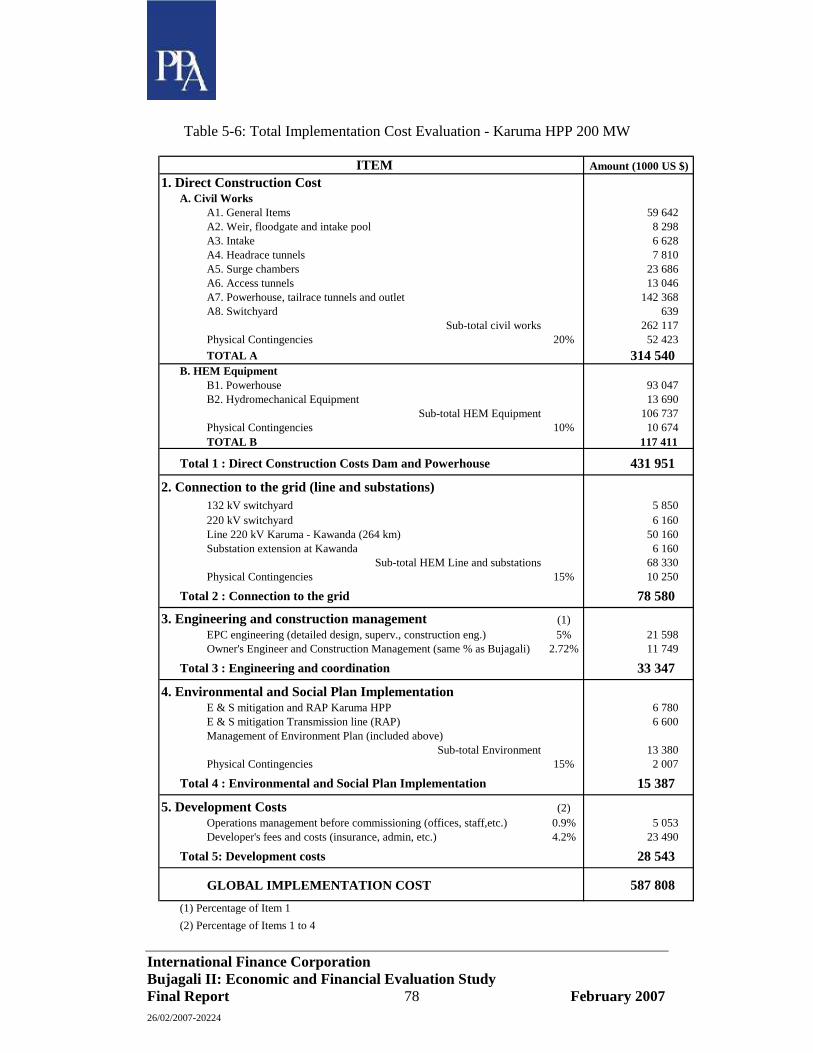

Bujagali and Karuma Cost Estimates

A detailed review and update of the cost estimates for Bujagali and Karuma has been carried out. These are considered to be the only two major hydro plant options for the medium term. These estimates take into consideration the information received from the Bujagali sponsor on the EPC contract negotiations and on development costs relating to Bujagali.

The total economic cost estimates for Bujagali and Karuma resulting from our review are as follows (in constant 2006 US$)4:

3 The “Agreed Curve” represents the allowable outflow from Lake Victoria into the Nile, corresponding to the flow that would have occurred in the absence of man-made intervention, e.g. the dam at Nalubaale-Kiira.

4 Just after this report was completed, BEL informed PPA and the Bank Group of the most recent results of on-going negotiations with the EPC contractor, indicating the addition of a $20 to $ 30 million risk premium in exchange for a comprehensive turnkey contract, plus another $ 5 to $10 million for improvements to the electro-mechanical works, bringing the total EPC cost increase into a range of $30 to $35 millions, nominal and undiscounted. At the same time, BEL and the contractor are negotiating an incentive scheme to accelerate commissioning by 3 to 4 months, which would create for Uganda a real economic cost saving on thermal plant operation estimated at $30 to $40 million (in dollars of 2006). The net impact of these proposed changes on the project’s economic viability is judged to be minimal.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 12 February 2007 26/02/2007-20224

ITEM Bujagali 5 units (US$ million)

Karuma 4 units (US$ million)

Direct construction costs: - Civil works - Equipment

227 187

315 117

Connection to the grid 28 79

Engineering and coordination 28 33

Environmental and Social Impacts 26 15

Development Costs 25 29

Total Implementation Cost (excluding Interest During Construction) 521 588

Environmental and Social Costs of Bujagali and Karuma

The Consultant undertook a field mission to Uganda in July 2006 to collect data on the E&S costs of the Bujagali and Karuma projects. Moreover, Burnside, who prepared the Bujagali Social and Environmental Assessment reports, estimated the project’s environmental and social impact cost based on substantial and detailed field investigations and compilation of new cost data. We have reviewed and commented on the Burnside figures and have used them for the economic analysis of Bujagali. We have also prepared E&S cost estimates for Karuma based on the existing ESIA, which was undertaken in 1999. The cost estimates adopted for Karuma take cognisance of the higher unit cost rates derived from the Burnside studies. The total incremental E&S expenditures for Bujagali and Karuma are shown in the cost table above.

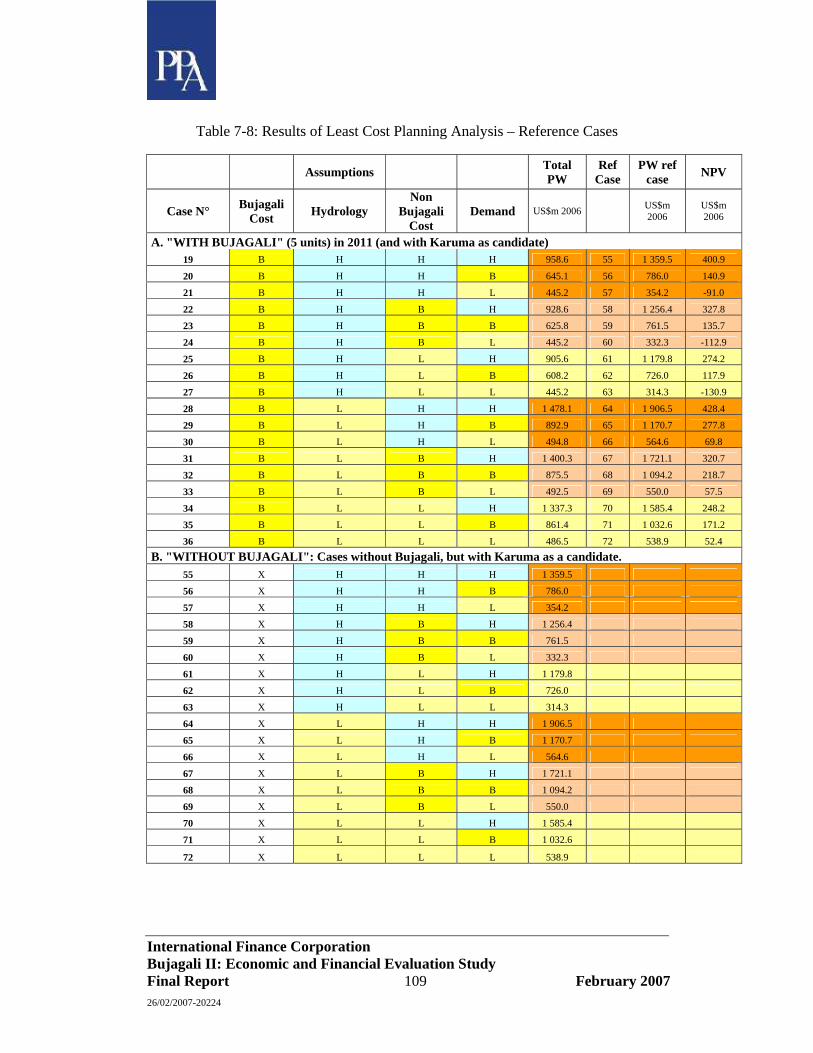

Least Cost Generation Expansion Plans

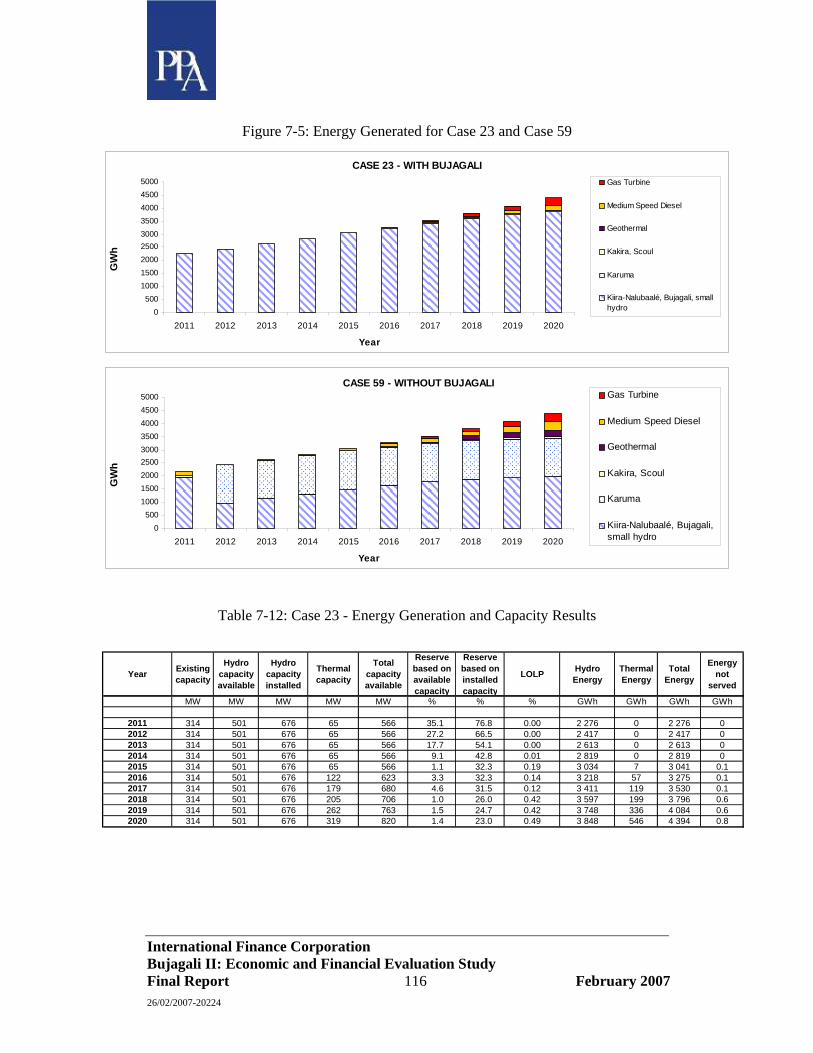

Detailed least cost generation expansion plans were developed for the Ugandan system for the period from 2010 to 2020 using the WASP IV system expansion program. The analysis was undertaken for base, high and low demand forecasts; low hydrology and high hydrology scenarios; base, low and high fuel price projections; and base, low and high Bujagali cost estimates. Alternative least cost sequences were determined for both the ‘with Bujagali’ and ‘without Bujagali’ cases. Karuma was retained as a candidate plant in both the ‘with Bujagali’ and ‘without Bujagali’ cases. A total of 72 cases were evaluated to cover the full risk analysis, and 13 further cases were considered for additional sensitivity analysis. The main results showed that Bujagali commissioned in 2011 was part of the least cost programme under all demand forecast scenarios with the low hydrology, and also for the high and base

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 13 February 2007 26/02/2007-20224

demand with high hydrology. In the high hydrology, low demand cases, the least cost expansion plan comprises only new thermal plant up to 2020, i.e. neither Bujagali nor Karuma could be justified. However, the total probability of occurrence of these cases is low, estimated at 5.5%, and the maximum probability of any one case occurring is only 1.5%.

Sensitivity studies were carried out to confirm the optimum timing of Bujagali, by delaying commissioning from 2011 to 2012 for the base demand. This leads to higher present worth (PW) costs for the low hydrology and marginally higher costs for the high hydrology. The analysis also showed that a 4-unit Bujagali design was less attractive economically than the 5-unit reference design. A further sensitivity study confirmed that Karuma commissioned before Bujagali (by forcing Karuma in 2012) leads to higher PW costs, and that the cost of Bujagali would need to increase by 49%5 to justify the commissioning of Karuma as the next plant before Bujagali.

A full risk analysis was made for the ‘with Bujagali’ and ‘without Bujagali’ cases, with the following probabilities assigned to the key variables:

Demand forecast: base/high/low - 40%/30%/30%

Hydrology: high/low - 21%/79%

Fuel Prices base/low/high – 40%/30%/30%

Bujagali Cost base/low/high - 60%/20%/20%

Assigning the probability weightings to the PW costs resulted in a total net present value (NPV) advantage of US$ 184.0 million (in 2006 US$ with discounting to 2006) in favour of the ‘with Bujagali’ cases. The NPV value is robust in respect of the assumption on hydrology. For example, if 100% probability is assigned to either the low or the high hydrology scenarios, the NPVs, representing the differences between the ‘with Bujagali’ and ‘without Bujagali’ programmes, are:

Low hydrology US$ 202 million, and

High hydrology US$ 116 million

in favour of the ‘with Bujagali’ cases.

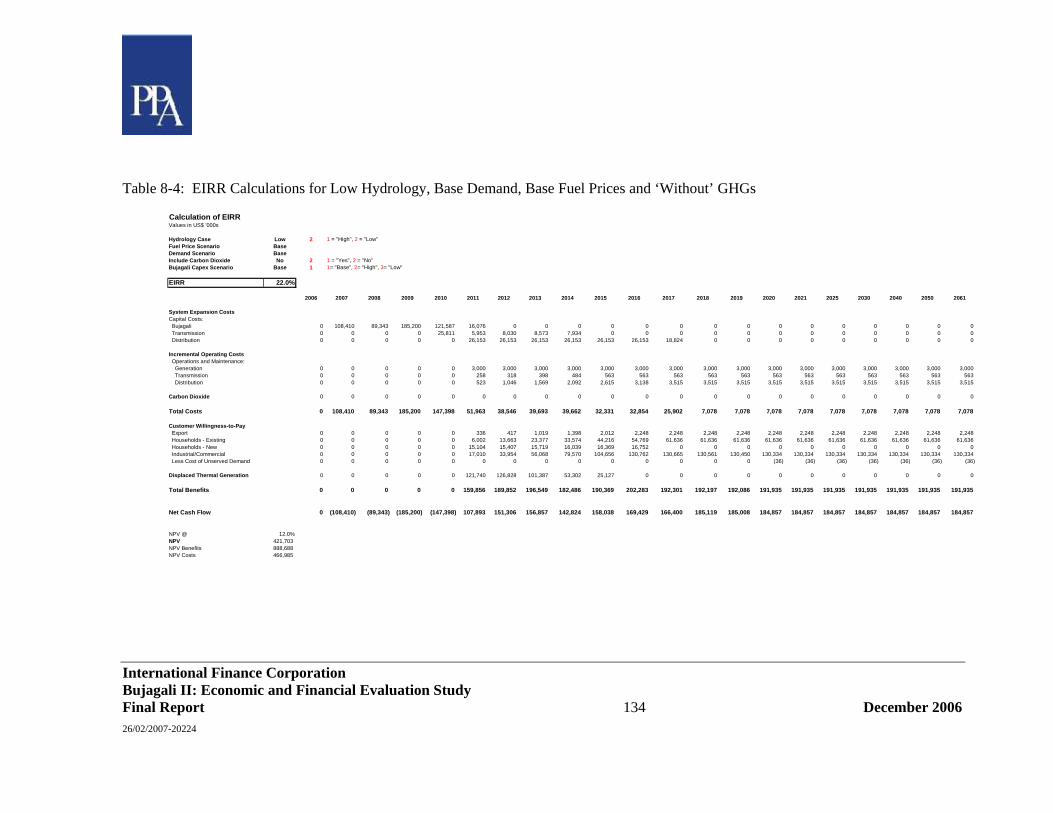

Bujagali Economic Internal Rate of Return (EIRR)

5 This result was obtained by progressively increasing the cost of Bujagali in the simulation analysis until the WASP program no longer selected Bujagali as the next major plant. In this case the least cost sequence included Karuma in 2012.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 14 February 2007 26/02/2007-20224

The EIRR for the Bujagali project was estimated by evaluating the cost and benefits of the project in terms of the capital and operating costs of Bujagali and the incremental transmission and distribution capital and operating costs associated with meeting the increment of demand supplied by the project. The benefits were measured in terms of the displacement of costly thermal power and incremental demand of the various categories of consumer, that is met by Bujagali, valued at their respective willingness to pay.

The EIRR values for the references cases obtained are summarised in the table below.

High hydrology Low Hydrology

EIRR 21.7% 22.0%

When the benefits of avoided greenhouses cases are included the EIRRs increase to 22.0% for the high hydrology and 22.9% for the low hydrology.

Sensitivity studies indicate that the project EIRR is robust against all key risk factors, including: hydrology, demand forecast, fuel prices and the capital cost of the project. The demand scenario has the greatest impact on EIRR, but in the most adverse combination of scenarios using the low demand case the resulting EIRR value of 12.5% remains comfortably greater than the 10% benchmark discount rate for World Bank Group-supported projects.

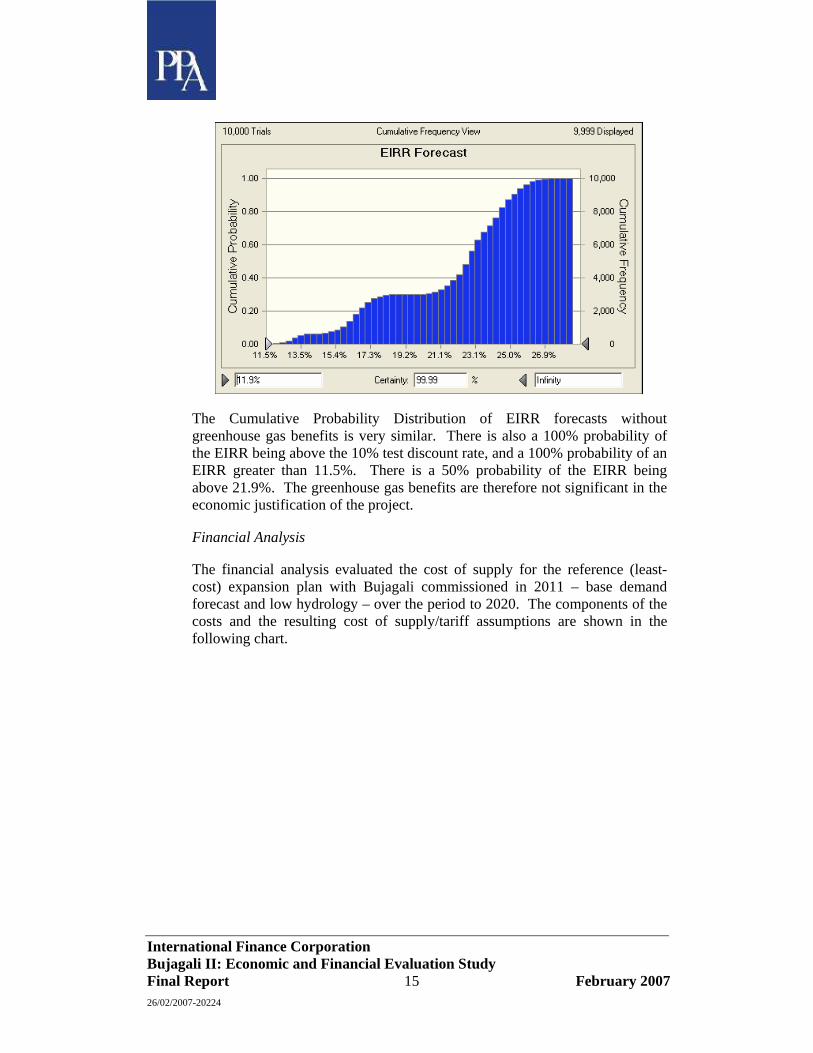

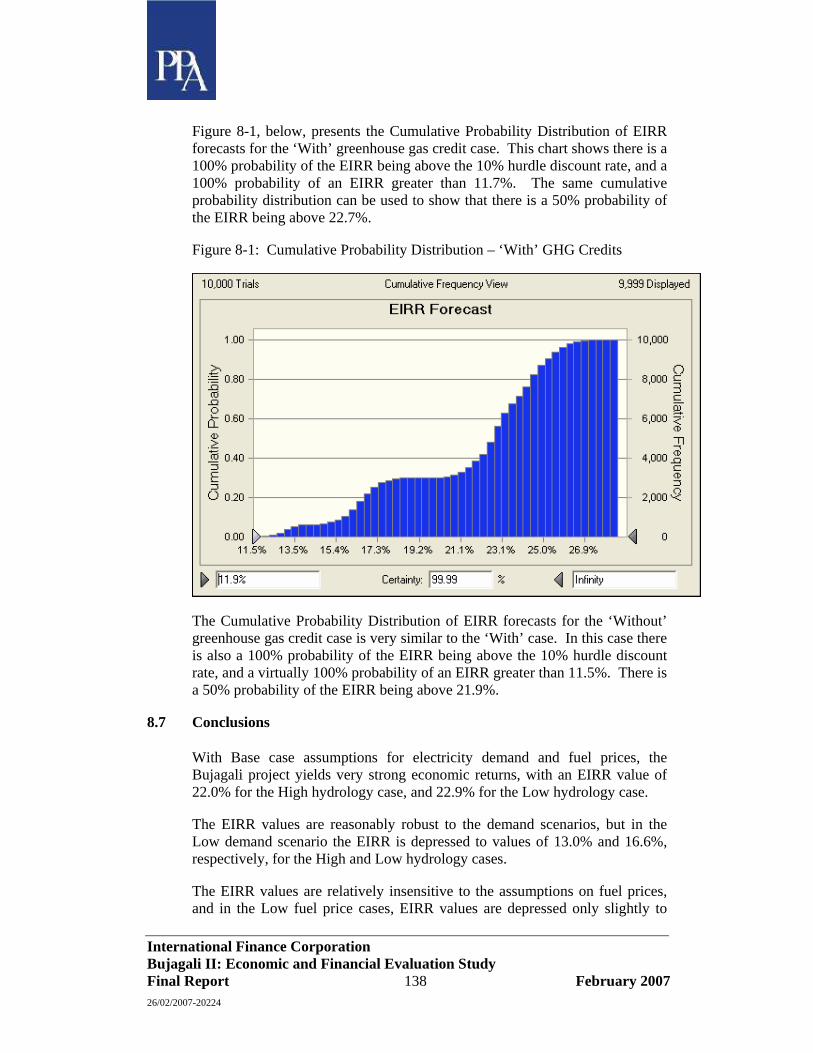

In addition to the sensitivity studies, a probabilistic risk analysis was undertaken on the EIRR value using the Crystal Ball software package with the following parameters subject to a probabilistic range of outcomes: demand forecast, crude oil price, Bujagali capital cost, T&D capital costs, willingness-to-pay of newly-connected customers, and hydrology. The following chart presents the Cumulative Probability Distribution of EIRR forecasts including the impact of greenhouse gas credits to the project. This chart shows there is a 100% probability of the EIRR being above the 10% benchmark discount rate, and a 100% probability of an EIRR greater than 11.7%. The same cumulative probability distribution can be used to show that there is a 50% probability of the EIRR being above 22.7%.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 15 February 2007 26/02/2007-20224

The Cumulative Probability Distribution of EIRR forecasts without greenhouse gas benefits is very similar. There is also a 100% probability of the EIRR being above the 10% test discount rate, and a 100% probability of an EIRR greater than 11.5%. There is a 50% probability of the EIRR being above 21.9%. The greenhouse gas benefits are therefore not significant in the economic justification of the project.

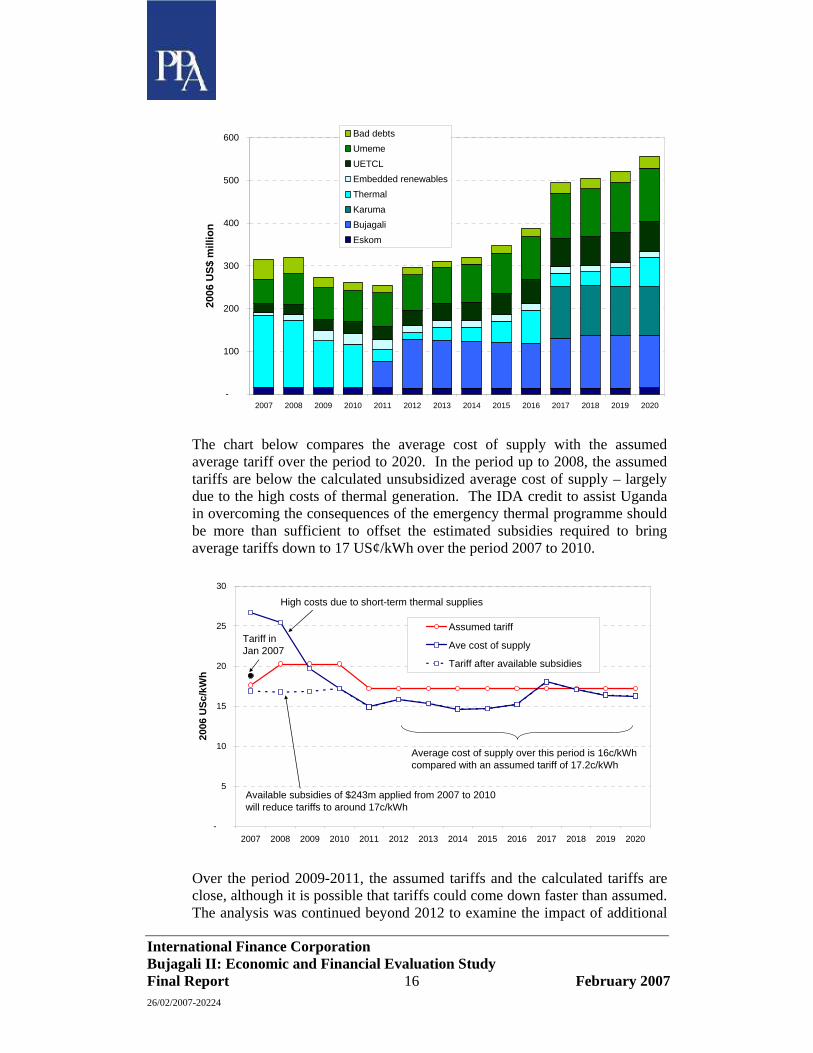

Financial Analysis

The financial analysis evaluated the cost of supply for the reference (least-cost) expansion plan with Bujagali commissioned in 2011 – base demand forecast and low hydrology – over the period to 2020. The components of the costs and the resulting cost of supply/tariff assumptions are shown in the following chart.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 16 February 2007 26/02/2007-20224

-

100

200

300

400

500

600

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2006

US$

mill

ion

Bad debtsUmemeUETCLEmbedded renewablesThermalKarumaBujagaliEskom

The chart below compares the average cost of supply with the assumed average tariff over the period to 2020. In the period up to 2008, the assumed tariffs are below the calculated unsubsidized average cost of supply – largely due to the high costs of thermal generation. The IDA credit to assist Uganda in overcoming the consequences of the emergency thermal programme should be more than sufficient to offset the estimated subsidies required to bring average tariffs down to 17 US¢/kWh over the period 2007 to 2010.

-

5

10

15

20

25

30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

2006

USc

/kW

h

Assumed tariff

Ave cost of supply

Tariff after available subsidies

Tariff in Jan 2007

Average cost of supply over this period is 16c/kWhcompared with an assumed tariff of 17.2c/kWh

High costs due to short-term thermal supplies

Available subsidies of $243m applied from 2007 to 2010 will reduce tariffs to around 17c/kWh

Over the period 2009-2011, the assumed tariffs and the calculated tariffs are close, although it is possible that tariffs could come down faster than assumed. The analysis was continued beyond 2012 to examine the impact of additional

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 17 February 2007 26/02/2007-20224

capacity requirements in the expansion plan, including the tariff impact of the Karuma plant. After 2012, the average tariff is approximately 1.2 US¢/kWh lower than the assumed constant tariff level of 17.2 US¢/kWh.

Macro-economic Impact

A macro-economic analysis was undertaken to evaluate the impact of Bujagali on the Ugandan economy. Overall, the impact of Bujagali relative to the next best option without Bujagali (which includes Karuma in 2012) is relatively small, and positive. There will be an immediate positive impact from Bujagali in 2011 resulting from the balancing of supply and demand, and therefore an end to load shedding. The main macro-economic impacts will be provided through power sector investments, which will add a maximum of 0.3 percent to GDP in 2009. In the longer term, the ‘with Bujagali’ expansion plan should afford 5 percent lower electricity tariffs than the ‘without Bujagali’ plan.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 18 February 2007 26/02/2007-20224

1 Introduction

1.1 Background

Uganda has suffered intermittent periods of shortages of electricity and this situation has exacerbated in recent times due to the critical drought in the region that has led to a significant reduction in the level of Lake Victoria and a cut-back in the output of the existing Nalubaale and Kiira hydro plants. The shortage of generating plant led to load shedding during the 1990s; this was relieved briefly in August 2000 with the commissioning of the first two 40 MW units at Kiira power station. However, over the past two years the drought has led to reduction in the available water for power generation and consequently there has been load shedding on a daily basis. By the end of 2005, the combined output of Nalubaale and Kiira had been reduced to 170 MW (out of a total installed capacity of 300 MW). A further two 40 MW units at Kiira are now in service, raising the installed capacity at Kiira/Nalubaale to 380 MW.

In early-2005, the government entered into a three-year leasing agreement for 50 MW of emergency short-term thermal plant comprising packaged high-speed diesel units burning distillate fuel. These units entered service in May 2005. The Ministry of Energy and the Electricity Regulatory Authority have been pursuing a further 150 MW of emergency thermal plant, 50 MW as an IPP or 100 MW on a leased basis. A further 50 MW of leased high speed diesel plant has been installed and entered service in October 2006. A further 50 MW of lease plant is expected to enter service in August 2007 and the 50 MW IPP medium speed diesel burning HFO in April 2008.

Following a regional conference in January 2006, Uganda agreed to reduce the flow through the power stations to the ‘agreed curve’ by June 2006. Consequently, in early-February the release from Nalubaale/Kiira was reduced to 73.44 million m3/day, equivalent to a continuous output of 135 MW. In July 2006, there was a further reduction to 64.8 million m3/day. UETCL changed the operating regime of Nalubaale/Kiira from one of constant power output to a two-block regime, thus providing additional power during the evening peak period. The economic and financial analysis of the Bujagali project in this study includes an update for the hydrology of the lake and development of potential future hydrological scenarios, both for the short and medium term. Had the Bujagali project been commissioned in 2005/06, as envisaged back in 2000, the current problems would not have arisen, or at least not to the same extent. In the intervening years there has been continuing demand growth, coupled with severe supply constraints that would have been alleviated had Bujagali come into service in 2005. The experience has demonstrated the high cost penalties of long term delays in the Bujagali project that was needed to meet the growing electricity demand of Uganda.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 19 February 2007 26/02/2007-20224

1.2 Objectives and Scope of Work

The purpose of this study is to evaluate the economic viability of the Bujagali II project, drawing on the evaluation and due diligence that was carried out during the first round of the project in the early-2000s. The Terms of Reference for the study are reproduced in Appendix A. These call for a comprehensive update of the previous due diligence work that was carried out in the first round of the Bujagali project, since much of the data is now four or five years old.

The basic tasks to be covered are:

Task A – Forecast of electricity demand

Task B – Update of the hydrology of Lake Victoria

Task C – Assessment of interim supply arrangements

Task D – Assess the optimal timing of Bujagali

Task E – Estimate incremental environmental and social costs

Task F – Calculate the economic rate of return

Task G –Assess financial feasibility

Task H – Macro-economic analysis

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 20 February 2007 26/02/2007-20224

2 Electricity Demand Forecast

2.1 Introduction

The basic information for the demand forecast task was collected during a visit to Uganda in January 2006. Thus the historical data on which the future demand projections are predicated covers the period up to and including December 2005. The initial findings of the team and a preliminary forecast were presented to the government and other stakeholders at a meeting in Kampala on 25th January 2006. The demand forecast was presented in the Interim Report submitted in February 2006 and presented at a meeting in Uganda on 16th March 2006. Following this meeting, comments were received on the forecast, including comments from the government. As a result of the comments and to take into account new or revised data that has become available, a revised demand forecast was prepared and presented to the government and lenders at a meeting in Kampala on 12th September 2006. The demand forecast presented in this section is the revised forecast presented at the September meeting. The principal changes from the initial forecast presented in the Interim Report are in the assumptions on the future levels of system losses, including commercial losses. Also, new GDP projections have been adopted, although the differences between the new projections and those used for the Interim Report forecast are small.

2.2 Present and Past Demand

Electricity demand growth in Uganda has been reasonably strong over the past ten years, in spite of supply constraints that have led to load shedding during peak periods. In each year the peak demand has been virtually equal to the total installed capacity. For a brief period following the commissioning of the first two 40 MW units at the Kiira hydro plant in 2000 and again in 2002 with the commissioning of the third unit at Kiira, UEB/UETCL was able to meet the peak demand in Uganda.

As a result, Uganda’s ability to export firm power to Kenya has been reduced. In recent years Kenya has also suffered a shortage of generating capacity and therefore has no surplus for export to Uganda.6

Details of the estimated generation and supply balances for the past five years are shown in Table 2-1.

The difference between the suppressed and unsuppressed peak demands is estimated by UETCL based on records from it’s SCADA system, whereby the

6 It is understood that UETCL has recently concluded an agreement with Kenya for the import of 10 MW of off-peak energy.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 21 February 2007 26/02/2007-20224

estimated demand on feeders that are being shed (based on recent records of similar periods when the demand on the feeder was supplied) is added back to determine the unsuppressed demand.

Table 2-1: Historical Generation and Demand

2001 2002 2003 2004 2005

Net generation (GWh) 1574.4 1700.3 1767.8 1887.7 1891.0

Sales to UEDCL/Umeme (GWh) 1358.8 1356.5 1438.4 1608.9 1746.7

Transmission losses (GWh)7 73.6 76.5 79.5 86.9 82.7

Net exports 142.0 261.8 215.5 191.9 61.6

Unserved energy (GWh) 33.8 23.4 29.7 74.1 93.9

Domestic peak demand met (MW) 236.3 264.1 274.5 269.5 253.4

Domestic peak demand (unsuppressed) (MW) 260.6 272.1 293.7 333.5 356.9 Source: UETCL and Consultant’s estimates

Thus sales to UEDCL/Umeme have grown at an average annual rate of 6.5% over the 2000 to 2005 period. The estimated peak domestic demand in Uganda has increased from 260.6 MW to 356.9 MW over the same period, a gross increase of 37%, whereas the suppressed peak demand (actually met) has fallen over the period from a maximum of 274.5 MW, recorded in 2003, to 253.4 MW in 2005.

Transmission system losses have remained essentially constant at about 4.5% of net generation on an energy basis.

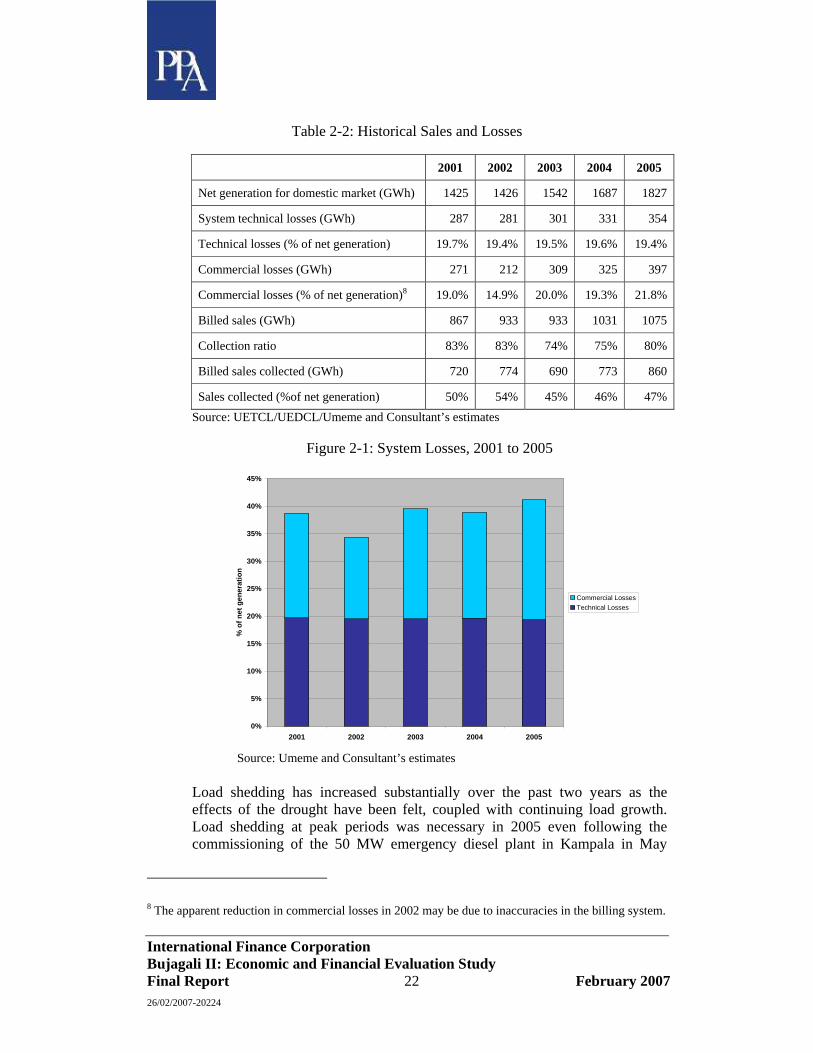

Details of the domestic electricity demand in Uganda, including the estimated breakdown from net energy generation to end-consumer sales, and system losses is shown in Table 2-2. The figures include estimates of unserved energy due to load shedding and system outages (including both planned and unplanned outages).

The data indicates that for the past five years billed sales revenue collected represents less than 50% of net generation. Technical losses are estimated to comprise about 4.5% for transmission and about 15% for distribution based on net energy generated. The resulting commercial or non-technical losses vary between 15% and almost 22% (in 2005), as shown in Figure 2-1.

7 Transmission losses for 2002 and 2003 have been adjusted to remove inconsistencies caused by metering problems.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 22 February 2007 26/02/2007-20224

Table 2-2: Historical Sales and Losses

2001 2002 2003 2004 2005

Net generation for domestic market (GWh) 1425 1426 1542 1687 1827

System technical losses (GWh) 287 281 301 331 354

Technical losses (% of net generation) 19.7% 19.4% 19.5% 19.6% 19.4%

Commercial losses (GWh) 271 212 309 325 397

Commercial losses (% of net generation)8 19.0% 14.9% 20.0% 19.3% 21.8%

Billed sales (GWh) 867 933 933 1031 1075

Collection ratio 83% 83% 74% 75% 80%

Billed sales collected (GWh) 720 774 690 773 860

Sales collected (%of net generation) 50% 54% 45% 46% 47% Source: UETCL/UEDCL/Umeme and Consultant’s estimates

Figure 2-1: System Losses, 2001 to 2005

Source: Umeme and Consultant’s estimates

Load shedding has increased substantially over the past two years as the effects of the drought have been felt, coupled with continuing load growth. Load shedding at peak periods was necessary in 2005 even following the commissioning of the 50 MW emergency diesel plant in Kampala in May

8 The apparent reduction in commercial losses in 2002 may be due to inaccuracies in the billing system.

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

2001 2002 2003 2004 2005

% o

f net

gen

erat

ion

Commercial LossesTechnical Losses

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 23 February 2007 26/02/2007-20224

2005. Load shedding has increased from 1-2% of net generation in 2001/02 to 4-5% in 2004-05, as shown in Figure 2-2.

Figure 2-2: Details of Load Shedding, 2001 to 2005

Details of sales by tariff category are shown in Table 2-3. It should be noted that this data is not corrected for load shedding. Residential sales include tariff Code 10.1, which covers residential and small, single-phase, commercial premises metered at low voltage. Commercial sales include larger commercial consumers with a three-phase supply not exceeding 100 Amp, supplied at low voltage (Code 10.2/10.3). This category includes time of use (TOU) charging. The third category covers medium scale industrial consumers supplied at low voltage, three-phase up to 500 kVA (Code 20) and large scale industrial consumers supplied at 11 kV or 33 kV with a maximum demand between 500 kVA and 10 MVA. Street lighting (Code 50) is aggregated with the industrial consumption for the purposes of the demand forecast.

0

10

20

30

40

50

60

70

80

90

100

2001 2002 2003 2004 2005

GW

h

0%

1%

2%

3%

4%

5%

6%

% o

f net

gen

erat

ion

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 24 February 2007 26/02/2007-20224

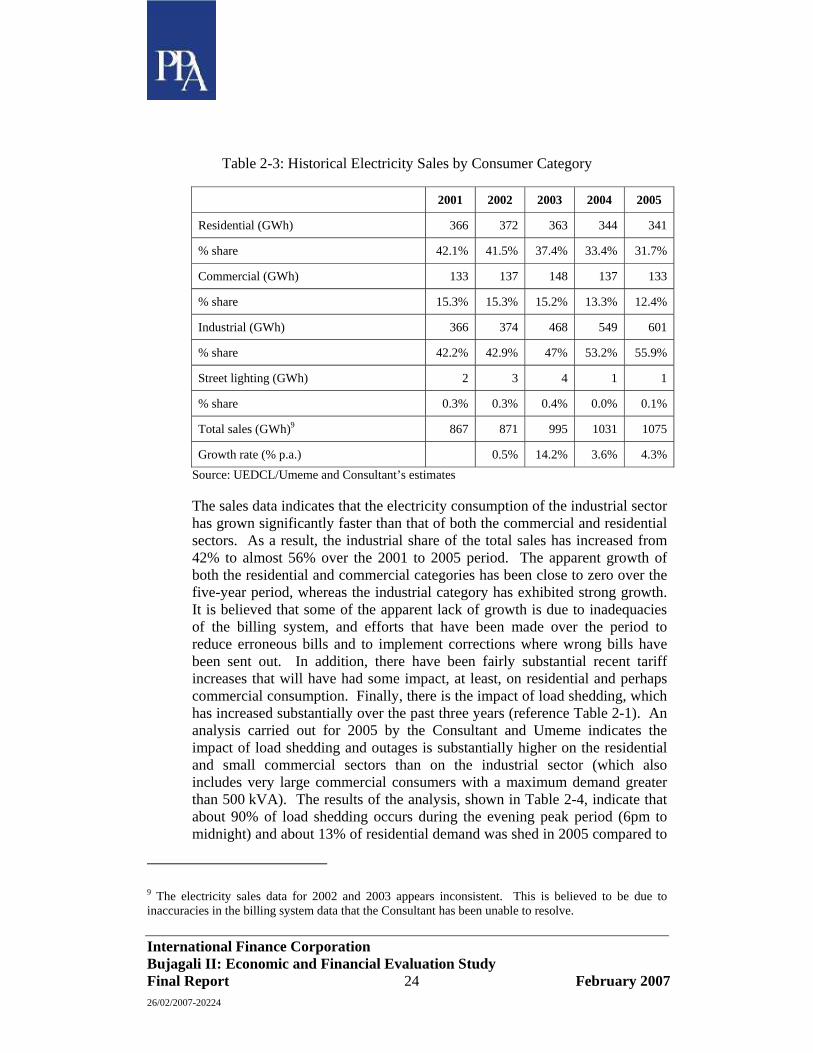

Table 2-3: Historical Electricity Sales by Consumer Category

2001 2002 2003 2004 2005

Residential (GWh) 366 372 363 344 341

% share 42.1% 41.5% 37.4% 33.4% 31.7%

Commercial (GWh) 133 137 148 137 133

% share 15.3% 15.3% 15.2% 13.3% 12.4%

Industrial (GWh) 366 374 468 549 601

% share 42.2% 42.9% 47% 53.2% 55.9%

Street lighting (GWh) 2 3 4 1 1

% share 0.3% 0.3% 0.4% 0.0% 0.1%

Total sales (GWh)9 867 871 995 1031 1075

Growth rate (% p.a.) 0.5% 14.2% 3.6% 4.3% Source: UEDCL/Umeme and Consultant’s estimates

The sales data indicates that the electricity consumption of the industrial sector has grown significantly faster than that of both the commercial and residential sectors. As a result, the industrial share of the total sales has increased from 42% to almost 56% over the 2001 to 2005 period. The apparent growth of both the residential and commercial categories has been close to zero over the five-year period, whereas the industrial category has exhibited strong growth. It is believed that some of the apparent lack of growth is due to inadequacies of the billing system, and efforts that have been made over the period to reduce erroneous bills and to implement corrections where wrong bills have been sent out. In addition, there have been fairly substantial recent tariff increases that will have had some impact, at least, on residential and perhaps commercial consumption. Finally, there is the impact of load shedding, which has increased substantially over the past three years (reference Table 2-1). An analysis carried out for 2005 by the Consultant and Umeme indicates the impact of load shedding and outages is substantially higher on the residential and small commercial sectors than on the industrial sector (which also includes very large commercial consumers with a maximum demand greater than 500 kVA). The results of the analysis, shown in Table 2-4, indicate that about 90% of load shedding occurs during the evening peak period (6pm to midnight) and about 13% of residential demand was shed in 2005 compared to

9 The electricity sales data for 2002 and 2003 appears inconsistent. This is believed to be due to inaccuracies in the billing system data that the Consultant has been unable to resolve.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 25 February 2007 26/02/2007-20224

about 5% of industrial demand. The corresponding figure for the commercial category is 6%. This substantially higher load shedding in the residential sector has obviously impacted on the level of sales in 2005. Based on this analysis the unserved energy due principally to load shedding has been added back into the end-user sales figures, after allowing for losses. The resulting sales figures that formed the starting point for the demand forecast projections are shown in Table 2-5. The resulting average annual growth rate of total sales adjusted for unserved energy is 6.2% compared to 5.5% for the unadjusted total sales. It is interesting to note that residential sales do not appear to have increased over the period. Whilst part of this may be due to inaccuracies in the UEDCL billing records, the general consensus is that residential demand has been growing steadily. The conclusion that may be drawn, therefore, is that much of the increased consumption may be ‘hidden’ by increasing commercial losses.

Table 2-4: End-User Load Shedding Analysis for 2005

Item

Billed sales

Adjusted for system losses

Unsuppressed demand

GWh GWh % GWh GWhPeak consumption:Domestic/small commercial 170.3 48.5 22%Commercial 26.6 7.6 22%Industrial 99.8 28.4 18%Industrial (dedicated) supply 32.2 0

Total (peak) 328.9 84.5 20% 49.8 378.7

Non-peak consumption:Domestic/small commercial 170.3 2.5 1%Commercial 106.4 1.6 1%Industrial 361.9 5.3 1%Industrial (dedicated) supply 107.8 0

Total (non-peak) 746.4 9.39 1% 5.5 751.9

Total consumption:Domestic/small commercial 340.6 51.0 13%Commercial 133.0 9.1 6%Industrial 461.7 33.8 5%Industrial (dedicated) supply 140.0 0.0

Total (peak + non-peak) 1075.3 93.9 8% 55.3 1130.6

Load shed

Source: Umeme and Consultant’s analysis

The industrial dedicated supply covers large consumers that are supplied at HV on a ‘dedicated’ feeder that allows these consumers to remain on supply when other consumers in the area are subject to load shedding.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 26 February 2007 26/02/2007-20224

Table 2-5: Historical Electricity Sales adjusted for Load Shedding

2001 2002 2003 2004 2005

Residential (GWh) 377 380 373 369 370

Commercial (GWh) 135 138 150 142 139

Industrial (GWh) 376 392 467 566 622

Total sales (GWh)10 888 910 989 1076 1131

Growth rate (% p.a.) 2.5% 8.7% 8.8% 5.1% Source: UEDCL/Umeme and Consultant’s estimates

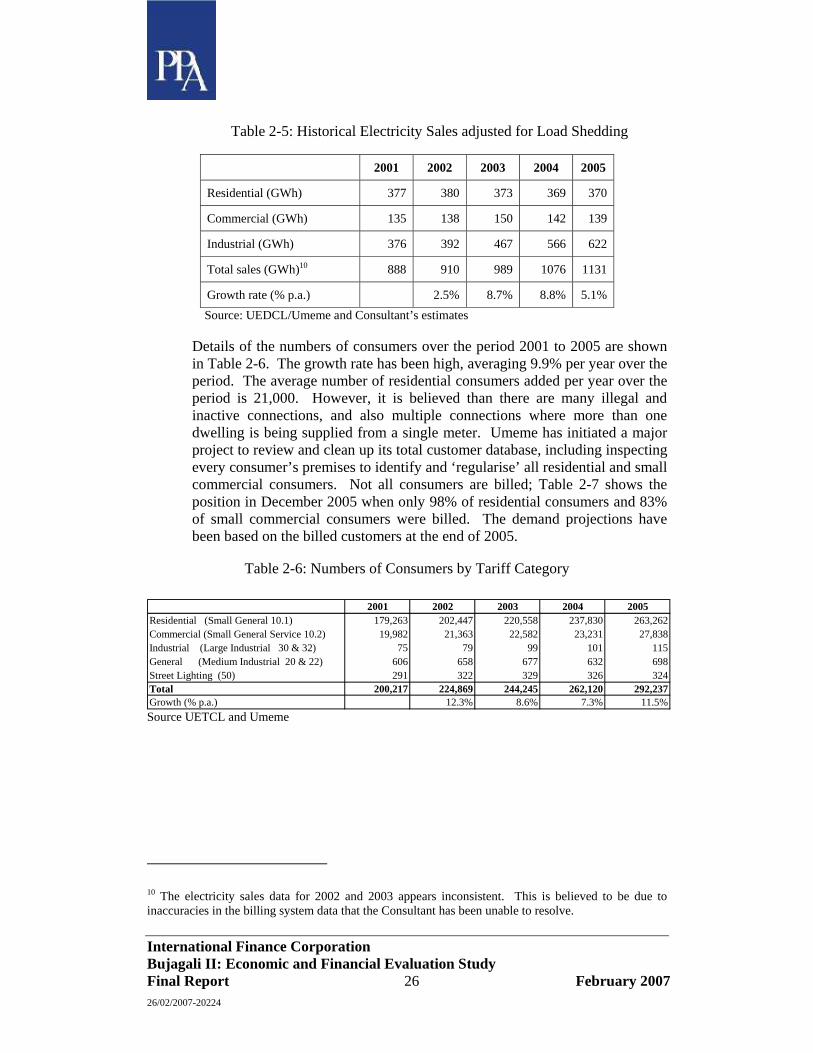

Details of the numbers of consumers over the period 2001 to 2005 are shown in Table 2-6. The growth rate has been high, averaging 9.9% per year over the period. The average number of residential consumers added per year over the period is 21,000. However, it is believed than there are many illegal and inactive connections, and also multiple connections where more than one dwelling is being supplied from a single meter. Umeme has initiated a major project to review and clean up its total customer database, including inspecting every consumer’s premises to identify and ‘regularise’ all residential and small commercial consumers. Not all consumers are billed; Table 2-7 shows the position in December 2005 when only 98% of residential consumers and 83% of small commercial consumers were billed. The demand projections have been based on the billed customers at the end of 2005.

Table 2-6: Numbers of Consumers by Tariff Category

Source UETCL and Umeme

10 The electricity sales data for 2002 and 2003 appears inconsistent. This is believed to be due to inaccuracies in the billing system data that the Consultant has been unable to resolve.

2001 2002 2003 2004 2005Residential (Small General 10.1) 179,263 202,447 220,558 237,830 263,262Commercial (Small General Service 10.2) 19,982 21,363 22,582 23,231 27,838Industrial (Large Industrial 30 & 32) 75 79 99 101 115General (Medium Industrial 20 & 22) 606 658 677 632 698Street Lighting (50) 291 322 329 326 324Total 200,217 224,869 244,245 262,120 292,237Growth (% p.a.) 12.3% 8.6% 7.3% 11.5%

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 27 February 2007 26/02/2007-20224

Table 2-7: Consumers Billed in December 2005

Source UETCL and Umeme

2.3 Methodology and Assumptions

Projections of electricity demand for the Ugandan interconnected system are required for the period up to 2020 for the analysis of the Bujagali project. The starting point for the projections is the 2005 demand, as discussed in Section 2.1. In this section, the methodology adopted for the demand forecast and the various assumptions are presented. A base case forecast, plus high and low sensitivity forecasts, are then developed based on projections for the economy, estimated new connections and assumptions on the future levels of system losses. Finally, forecasts are added covering committed exports to Tanzania and Rwanda.

The demand forecast has been built up from separate forecasts for each main consumer category based on a consistent set of economic and other assumptions, using actual data for 2005 as a starting point.

In the following sections, projections for the Ugandan economy are developed following a brief review of the recent performance of the economy.

2.4 Projections for Ugandan Economy

2.4.1 General

Projections of economic growth in Uganda are an integral component of the demand forecasting process. The Consultant’s projections are founded on short to medium term projections made by authorities on the Ugandan economy, such as MoFPED, BoU and the IMF. Since the Consultant’s projections have a considerably longer perspective than those prepared by these authorities, a view of the long-term prospects for the Ugandan economy has been taken. This view was formed on the basis of interviews with senior individuals at MoFPED, BoU and the IMF, and the review of recent reports prepared by MoFPED, BoU and the World Bank.

2.4.2 Overview of the Ugandan Economy

The Ugandan economy has enjoyed considerable stability for more than 10 years. Since the 1990/91 fiscal year, economic growth has averaged around 6.5% per year. In recent years, there has been a slight reduction in the average

Live Billed %Residential (Small General 10.1) 263,262 258,805 98%Commercial (Small General Service 10.2) 27,838 23,170 83%Industrial (Large Industrial 30 & 32) 115 115 100%General (Medium Industrial 20 & 22) 698 698 100%Street Lighting (50) 324 324 100%Total 292,237 283,112

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 28 February 2007 26/02/2007-20224

rate of growth, and the average for the past 5 years has been around 5.7%. In the most recent fiscal year (2004/05) GDP growth was 5.7%. It is, however, important to consider that population growth in Uganda is quite strong, at around 3.4%. Per capita GDP growth over the past 5 years is therefore around 2.3% per year.11

2.4.3 Projections

The GDP projections adopted for the base case demand forecast are taken from the current forecasts of the Ugandan economy agreed jointly between GoU, IMF and World Bank, adjusted for calendar years. These are summarised in Table 2-8. Projections provided by GoU cover financial year 2008/09 and we have extrapolated the projections up to 2011. It is assumed that the rates remain constant at the 2011 levels up to 2020.

It should be noted that the forecast overall GDP growth is lower than both the commercial and industrial GDP growth. This is due to the effect of the agriculture and informal sectors.

Table 2-8: Uganda GDP Projections

2006 2007 2008 2009 2010 2011-2020GDP at factor cost 5.75% 6.10% 6.45% 6.85% 6.45% 6.00%Commercial GDP growth 8.20% 7.25% 7.70% 8.35% 7.55% 7.90%Industrial GDP growth 6.15% 6.50% 6.85% 7.25% 6.85% 6.40%Source: Government of Uganda/IMF

2.5 Assumptions for Residential Sector

As discussed in Section 2.1, the growth in numbers of residential consumers has been strong, averaging almost 21,000 per year since 2001. The assumption adopted for new residential connections in the short term is 17,000 per year over the period 2006 to 2010 inclusive. This is assumed to comprise 12,000 by Umeme in urban and peri-urban areas, as per the target in their concession, plus a further 5,000 per year of grid-connected rural consumers from the RE programmes being implemented by the REA and UEDCL. Umeme is not expecting to connect more consumers than they are committed to in their concession in view of the shortages of generation and high tariffs that are likely to be experienced until Bujagali comes into service. From 2011 to 2020, it is assumed that the numbers of connections will increase following the end to generation capacity constraints, which will trigger an increase in the rate of connections, both urban and rural. Over this period it is assumed that 25,000 new residential consumers will be connected each year, including both urban and rural connections.

11 In the 12 years to 2002, the population of Uganda grew by 7.7 million, to stand at 24.4 million.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 29 February 2007 26/02/2007-20224

The forecast for the residential sector has been made in two parts: existing consumers and new connections. For existing consumers, future consumption is linked to the forecast increase in real household income that is taken at 2.3% per year over the period of the forecast. This is based on the average GDP per capita growth from recent UBOS surveys12.

For new connections, it is assumed that on average the initial consumption will be lower than for existing residential consumers. Based on figures obtained from Umeme for new consumers connected in 2005 since they took over on 1st April, the average consumption of new residential consumers is 108 kWh/month. This compares with the average for all residential consumers for 2005 of 134 kWh/month13, or approximately 20% lower. This figure of 108 kWh/month has been adopted for the demand projections for new residential consumers. After the first year, the consumption of the new residential consumers is assumed to increase in line with increases in real household income, in common with the consumers existing at the start of the forecast, i.e. end-2005. Given that new consumers are assumed to be connected at a uniform rate throughout the year, the first year’s consumption of the new consumers is taken at 50% of the estimated full-year consumption.

An income elasticity of 1.0 and a price elasticity of –0.5 have been adopted. The income elasticity is based on the performance of the residential sector in recent years taking into account the connection of new consumers, load shedding and inadequacies of the billing system. The residential demand for existing residential consumers is assumed to be sensitive to tariff increases. Data from a recent survey commissioned by ERA14, extracted by the consultant based on 735 urban, peri-urban and rural households surveyed in six districts, showed an average household income of about USh 800,000 and an average monthly expenditure on electricity of USh 43,000. This indicates an average expenditure of 5.4% of household income. However, taking median values, as opposed to average values, gives very different figures, since it removes the skewing effect of the very high income/expenditure households.

The median monthly household income is USh 302,000 and the corresponding expenditure on electricity is USh 30,000 per month, or 9.9% of the total household income. This is a high proportion of total household income to

12 Growth in real household income increased by approximately 7% in the three-year period between the 1999/2000 and 2002/03 UBOS surveys.

13 This is calculated from data provided by Umeme of billed sales and numbers of customers billed per month for the months of March to December 2005.

14 Study on Social and Economic Impact of Electricity Tariff Changes, Makerere University, Kampala, November 2004.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 30 February 2007 26/02/2007-20224

spend on electricity. These figures indicate that the demand of the majority of residential consumers is relatively highly elastic and therefore a price elasticity of –0.5 has been adopted for the demand forecast. The median figures also indicate an average consumption of about 123 kWh/month at current early-2006 tariff levels, compared with an average of 134 kWh/month based on the Umeme billing data for March to December 200515. Applying the 24% tariff increase in April 2005 to the median figure, and using price elasticity of –0.5, gives an average consumption of 138 kWh per month, which is close to the ‘actual’ figure from Umeme for 2005. It is considered justifiable therefore to adopt a price elasticity of demand for the residential sector of –0.5. It should also be noted that the residential consumer category (tariff code 10.1) also includes small shops and other small commercial premises. It has been assumed that any impact of these consumers on the above analysis will be small. This assumption is supported by the analysis of willingness to pay for electricity which indicates that, the price elasticity of demand at the marginal residential tariff (point P2Q2 on the income compensated demand curve) is -0.45 (see Appendix E.1.3).

It is useful to consider that multiple households are actually being served by the average Umeme residential connection. Statistics Norway consultants’ analysis of 2002 UBOS survey data found that 451,000 households were connected to mains electricity, whereas 2005 Umeme data indicated just 255,000 official residential connections. This suggests that there are approximately 1.8 households supplied by each residential connection. When this information is applied to the average residential customer, the proportion of household income spent on electricity is reduced to just 3.2%, which is much closer to expectations.

It is also useful to consider whether electricity will still be affordable in 2011, with the tariff trajectory that is expected. Assuming a 2.3% real annual income growth over the 6 years between 2005 and 2011 suggests that the average residential income will grow by 14.6% from US$ 3,952 to US$ 4,529 per year and, assuming an income elasticity of demand of 1.0, electricity consumption will also grow by 14.6% from 134 kWh/month to 154 kWh/month. With a 2011 tariff of 23.0 US¢/kWh, in 2006 money, the implicit expenditure on electricity increases to US$ 35.4 per month, or US$ 425 per year. This represents 9.4% of household income, on the basis of a single household per connection, or 5.2% on the basis of 1.8 households per connection. The Consultant considers that 5.2% is towards the upper end of the range of expectations for the proportion of household income expended on electricity for non-cooking purposes.

15 This is higher than the average residential consumption per consumer on which the demand forecast is based since the demand forecast uses the year-end consumer numbers whereas the Umeme average consumption data is based on average month-by-month billing data.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 31 February 2007 26/02/2007-20224

2.6 Assumptions for Commercial and Industrial Sectors

The demand projections for the commercial and industrial sectors are based on GDP projections for the services and industrial sectors presented in Section 2.4.3. The following assumptions have been adopted for demand and prices elasticities for these sectors:

Commercial: GDP elasticity 1.0 Price elasticity -0.3 Industrial: GDP elasticity 1.3 Price elasticity -0.1

These figures have been derived from an analysis of historical GDP and electricity sales for these sectors. For the commercial sector an analysis was carried out for the period 1977-2003. The average growth in electricity sales was 6.75 and the average growth in GDP was 6.8%, giving a GDP elasticity of demand for the sector of 0.99. Therefore, a value of 1.0 has been adopted. The analysis was only made for the period up to 2003 in view of suspected problems with the billing data that the Consultant was unable to resolve.

A similar analysis was made for the industrial sector. In this case, the period 1997 to 2005 was adopted and a GDP elasticity of demand of 1.38 was obtained. A value of 1.3 has been adopted for the demand projections.

The price elasticities adopted were based on more judgemental arguments. It is considered that the demand of the industrial sector is highly inelastic due to the high cost of alternative sources of generation and the high establishment costs of auto-generation. A low price elasticity of –0.1 has therefore been adopted for the demand projections. For the commercial sector it was also felt that the demand is relatively inelastic. However, it was also considered that the commercial demand would be less price elastic than the residential sector. For the commercial sector, a price elasticity of –0.3 has therefore been adopted for the demand projections.

2.7 Revenue Collection

The present collection ratio for energy billed is 80% and Umeme is committed under the concession agreement to improving the ratio to 92.5% by 2008. The demand forecast is based on achieving 90% by 2008 and 97.55 by 2011, remaining constant thereafter. A price elasticity of demand on improved revenue collections of -0.30 has been adopted, implying that there will be 0.3% reduction in demand for each perceived 1% price increase as a result of Umeme’s improved collection of billed revenue.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 32 February 2007 26/02/2007-20224

2.8 Tariff Assumptions

Electricity tariffs increased twice in 2005, in April and October by a total of 24% on average and by 37% in June 2006. ERA increased tariffs by a further 42% on average in November 200616 in view of the rising cost of the thermal generation and the planned additional short term emergency thermal plant. The capacity costs of the future short term thermal are expected to be covered by the World Bank, under IDA funding and GoU is expected to waive the fuel duty and further subsidise the fuel cost. However, at the time of writing this report, the amount of the subsidy, and therefore the amount that would have to be passed through to consumers through the tariff, is not known.

A separate short-term study has been commissioned by the World Bank17 to evaluate the short term thermal generation proposed program. Based on the findings of this study the following real increases in average end-user tariffs will be required over the period up to the commissioning of Bujagali in 2011:

2006 +37% 2007 +45% 2008 +15% 2009 0% 2010 0% 2011 -15%

The above tariffs are based on the proposed short term thermal programme, including an additional 150 MW firm of generating plant – 100 MW leased high-speed diesels and 50 MW firm of medium speed diesel plant burning heavy fuel oil (HFO)18. The tariff projections also assume that there would be continuing direct budgetary support to the sector, plus IDA support of a further US$ 175 million.

The revised demand forecast used for developing the least cost development programme for the Ugandan system has been based on the above tariff assumptions. The financial analysis based on the least cost programme will provide a forecast of the tariffs required to meet the financial requirements of the electricity sector. If the calculated tariffs are no greater than the tariffs underlying the demand forecast, the expected demand and supply conditions

16 This latest increase was not known when the Consultant finalized the demand forecast, but is close to the assumed tariff increase in 2007.

17 Assessment of Short Term Generation Requirements in Uganda, Draft Report, February 2006, Power Planning Associates

18 This is the plant that is to be developed as an IPP on a BOT basis, with ownership passing to the government after 6 years of operation.

International Finance Corporation Bujagali II: Economic and Financial Evaluation Study Final Report 33 February 2007 26/02/2007-20224

would be not far from equilibrium. However, if the tariffs calculated for the investment plan based on the original tariff assumptions end-up exceeding the latter, then the forecast and least cost plan will be revised based on the calculated tariffs. This process will be re-iterated until there is approximate coherence between prices, demand and supply.

2.9 Assumptions on Reduction of System Losses

As discussed in Section 2.1, system losses on the Ugandan system are currently very high. It is estimated that losses in 2005 were 41.1% of net generation on an energy basis, made up as follows:

Transmission losses 4.4% Distribution losses 16.0% Commercial losses 20.7%

The commercial loss percentage does not include for consumption that is billed but not paid which is allowed-for separately in the demand forecast.

Based on discussions with Umeme staff the estimated breakdown of the distribution technical losses is as follows:

11 & 33 kV distribution networks 6% LV distribution networks 10% (including a substantial contribution from unbalanced loadings on LV networks) Umeme has engaged Norconsult to investigate the present level of losses and to make proposals for loss reduction. Based on these findings and additional discussions with Umeme, the consultant estimates the following current (2006) system losses, expressed as percentages of net generation: Technical losses: Transmission 4.0% Distribution 16% Sub-total 20%

Commercial losses 19%

Total losses 39%

The Umeme capital investment programme for the period to 2010 includes a budget of US$ 56.6 million to address the above issues and it is considered that reduction of about 4% should be possible over the next seven years, to 2012. Allowing for a modest decrease in transmission losses from 4.4% to 4.0%, the estimated target technical loss level for the base demand forecast is 16%, comprising 4% transmission losses and 12% distribution losses. However, there is a strong incentive for Umeme to exceed these loss targets