bunge - introduction to ag freight iaom – manila 2012 – andrew

TRANSCRIPT

Bunge - Introduction to Ag Freight

IAOM – Manila 2012 – Andrew Benjamin

Introduction to Ocean Freight

Bunge Propaganda

Demand

Supply (Oversupply)

Calculating Freight / Modes of “Chartering”

Outlook / Risks

2 Bunge Port Facilities

Bunge Ocean Freight Product Line

Headquarter for Bunge Global Freight is Geneva

We also have freight offices in Singapore, Shanghai, Miami and Sao Paolo

FPL manages ALL Dry Ocean Freight flows for the Bunge Group

Bunge has also an active Vegetable Oil and Container Freight presence

Bunge ships about 35 Million Tonnes per annum grains and oilseeds

Bunge ships about 2.5 Million Tonnes per annum of vegetable Oils

Bunge ships about 40,000 TEU Containers per annum

In addition to our own traded cargoes, we transport another 30 Million tonnes per annum of 3rd party cargoes

(Mainly Coal, Iron Ore and fertilizers)

Headcount of 59 persons today (of which 42 in Gva)

On any given day we are operating a fleet in excess of 170 vessels (10 Capes, 90 Panamaxes, 70 Handies)

Bunge presence in Dry Bulk Freight Market

Singapore

7 People

Shanghai

2 Research

Geneva 42 people

Chartering, Risk Mgmt, Research

Operation, Finance & Legal

Miami

3 People

Brazil

5 People

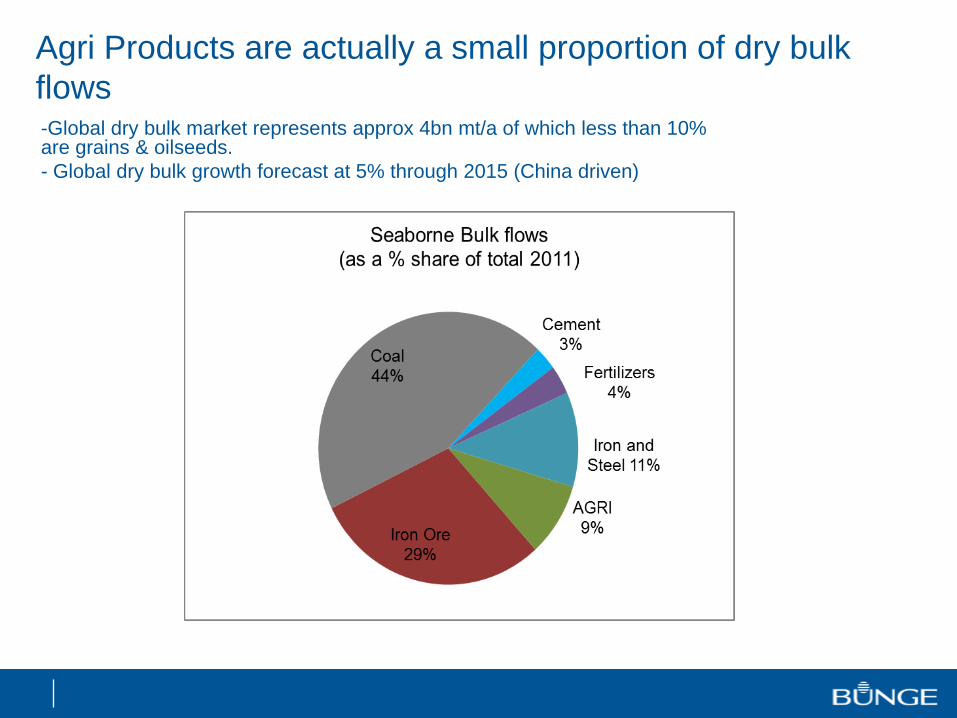

Agri Products are actually a small proportion of dry bulk

flows-Global dry bulk market represents approx 4bn mt/a of which less than 10% are grains & oilseeds.

- Global dry bulk growth forecast at 5% through 2015 (China driven)

Major Dry Bulk Flows

6

Black = Coal

Orange = Iron Ore

Green = Grain

Atlantic

Pacific

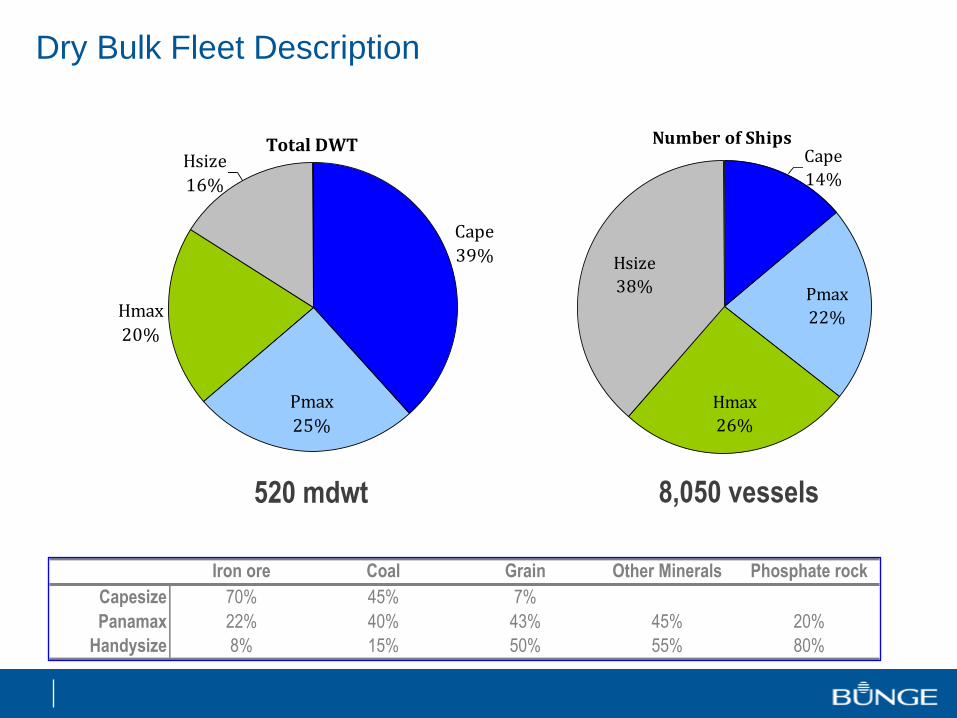

Dry Bulk Fleet Description

Total DWT

Cape

39%

Hmax

20%

Hsize

16%

Pmax

25%

Number of Ships

Hsize

38% Pmax

22%

Hmax

26%

Cape

14%

Iron ore Coal Grain Other Minerals Phosphate rock

Capesize 70% 45% 7%

Panamax 22% 40% 43% 45% 20%

Handysize 8% 15% 50% 55% 80%

520 mdwt 8,050 vessels

Fleet Development (Too many new ships!)

Dry Bulk Freight markets face real pressure due to tonnage over-supply –how did we become so desperate to buy ships ??

0

50000

100000

150000

200000

250000

31/01

/06

30/04

/06

31/07

/06

31/10

/06

31/01

/07

30/04

/07

31/07

/07

31/10

/07

31/01

/08

30/04

/08

31/07

/08

31/10

/08

31/01

/09

30/04

/09

31/07

/09

31/10

/09

31/01

/10

30/04

/10

31/07

/10

31/10

/10

31/01

/11

30/04

/11

31/07

/11

31/10

/11

Cape

pmx

The global fleet make up is shifting to bigger ship sizes

Fleet age profile: Increasingly modern & larger fleet

Handysize sector getting older (scrapping??)

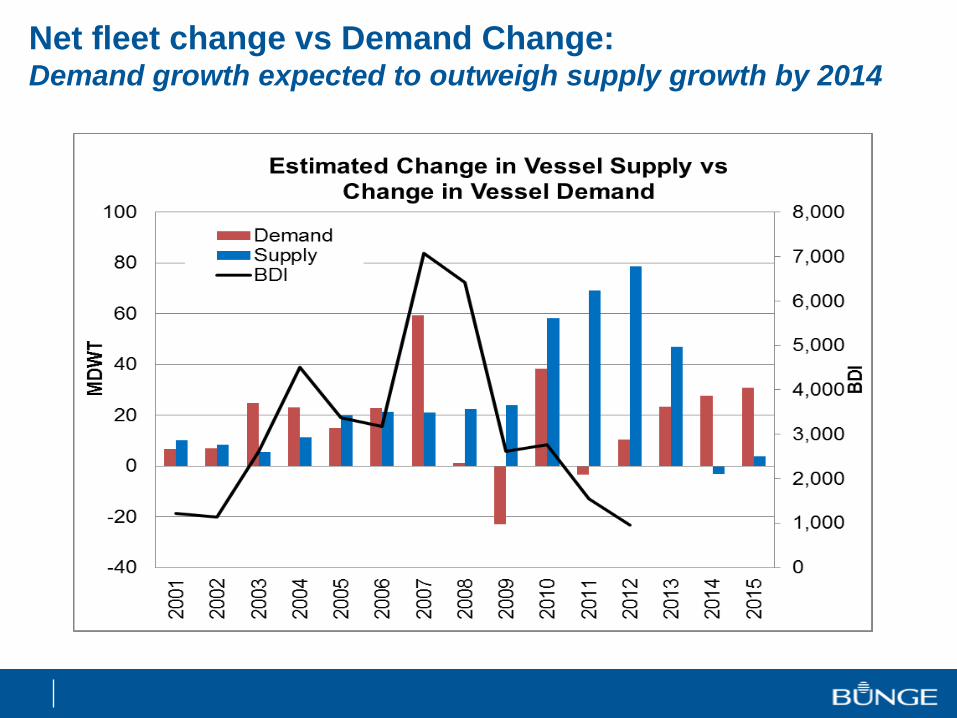

Net fleet change vs Demand Change: Demand growth expected to outweigh supply growth by 2014

Sectoral ship sizes are increasing.

Upstream and downstream port development will follow

Handy (Dwt 20k -> 45k)

Limited Newbuilding program coupled with an already ageing fleet

Supramax :

52k Dwt 58k Dwt 62k Dwt 68k Dwt

Panamax :

68k Dwt 74k Dwt 82k Dwt 90-95k Dwt (Post Pnmx)

Capes :

149k Dwt 161k Dwt 172k Dwt 177-182k Dwt

220k Dwt 400k Dwt (Vale Max)

DWT (DEADWEIGHT) (mts) : Combined weight of cargo, water, bunkers and constant-weights that can be safely

carried by the vessel.

Calculating Freight ($pmt)

Total Voy. Costs / Cargo Quantity = Freight Rate

Total Voyage Costs;

Voy Duration x Daily Hire Rate (Time Charter Rate)

Port and Canal Transit Costs (CRD circa US$250k for 55kmts Wheat)

Cost of Bunkers (Fuel) in mts/day consumed (S’pore currently $680pmt IFO)

Insurance (Gulf of Aden Transit, etc..)

Misc costs (cargo separation, hold cleaning, etc..)

Cargo Quantity;

Type of Cargo, it’s stowage factor (sf)

Cubic Capacity of Vsl

Load and Disport and Canal Transit Draft Restrictions

How are freight rates determined

Voyage Duration is typically inclusive of ;

- Pre ballast to Loadport

- Days at Load and disport

- Laden passage to discharge port

- All calculated in number of days x Time Charter Rate & Daily Fuel

Cost» Fuel : 30mts IFO x $680pmt = $20,500/Day (65% of daily cost)

» Time Pacific Rounds (35% of daily cost)

» Handies : $7k/day

» Supramax : $6k/day

» Pnmx : $4k

Load/Discharge rates

• With time charter levels so low, there is minimal discounts afforded to charterers for

increased discharge rates

Type of shipping contracts

Voyage Charter

Contract between shipowner & charterer for transport of specified amount of commodity from specified loading port(s) to specified discharging port(s) on single vsl/trip.

Shipowner responsible for all the costs

Charterers pays and agreed $/ton rate and settles dem/des with owners.

Time Charter

Charterer hires vessel for specified period of time & assumes commercial control of vessel and pays the owners a $/day rate.

Shipowner responsible for operation and capital costs (maintenance, crew, insurance and finance)

Charterer responsible for all voyage costs. (Fuel, Port Costs, etc)

Contract of Affreightment, CoA

Contract between shipowner & charterer for transport of a specified amount of commodity from a specified loading port(s) to specified discharging port(s) for 2 or more cargoes.

Shipowner responsible for all costs

Charterer pays an agreed $/ton rate and settles dem/des with owners.

One charter party covers numerous cargo shipments

Bareboat charter

Charterer hires the vessel for a very long time, normally the whole economic life of the vessel.

Shipowner responsible for capital costs only

Charterer responsible for all other costs, including ship management (crewing, maintenance, etc…)

Rates are on a $/day basis

SummaryDemand

• Global drybulk trade about 4mmt / year, up by more than 50% over last 10 yrs.

• Bunge moves 60 mln tons of freight per year ~ 1.6% of global flows.

• Coal and iron ore the two most shipped dry bulk commodities.

• Steel industry & power production integral to dry bulk market.

• Grains and oilseeds relatively small volume but important swing factor in market & for sub-Cape sizes.

• Moderate growth principally driven by Asia (and China in particular).

• Global dry bulk demand expected to grow by about 5% per year through 2015.

Supply

• Over 650mdwt of carrying capacity by end-2012, more than 9,000 ships in total

• Fleet growth expected to slow as yards move to higher margin biz and robust scrapping programs in low rate market.

• Age profile of the fleet increasingly modern across the larger sizes.

• Dry bulk fleet to grow >10% in 2012 & average of 4% over the next 5 years.

COUNTER PARTY RISK !!!

Thank You

17 Bunge Port Facilities