business development for consulting groundwater professionals · 6/5/2017 ngwa white paper business...

TRANSCRIPT

6/5/2017

NG

WA

WH

ITE

PAPE

R

Business Development for Consulting Groundwater ProfessionalsBy: Joan B. Berkowitz, Ph.D., and Christopher S. Frangione

All successful consulting groundwater professionals engage in business development. It usually means bringing in business, but it can also mean staying billable. In most cases it means a combination of both. Bringing in business requires selling services to prospective clients. Staying billable requires developing and maintaining good relations with those who do bring in the business. Most professional groundwater consulting firms follow a seller-doer model, requiring a balancing of bringing in business and doing billable work. Obviously, no one can be billable unless someone is bringing in business. Bringing in business has always been essential to the survival of any groundwater consulting firm, but doing so has become more difficult in the current recessionary environment. The focus of this paper is on the new skills required for a new economy. It is based on the results of an e-mail survey of more than 190 consulting groundwater professionals, telephone interviews with members of six groundwater consulting firms, a review of relevant literature, and our experience as management consultants working with design engineering firms that provide groundwater consulting services.

2

SURVEY RESULTS

Methodology Farkas Berkowitz & Company designed the online survey used to collect the data. National Ground Water Association sent it to 1,700 consulting groundwater professionals in April 2010. Of the 193 respondents, 34 percent are scientific or technical staff, 34 percent are project managers, 22 percent are presidents or CEOs, and 9 percent are vice presidents. Over half of the respondents have been involved with groundwater issues for more than 20 years, and less than one percent is relatively new to groundwater, having worked in the field for fewer than two years. These results raise the question of whether too few young people are being attracted to hydrogeology. The question is particularly important because 10 respondents identified finding and retaining qualified personnel as one of their major challenges for 2010.

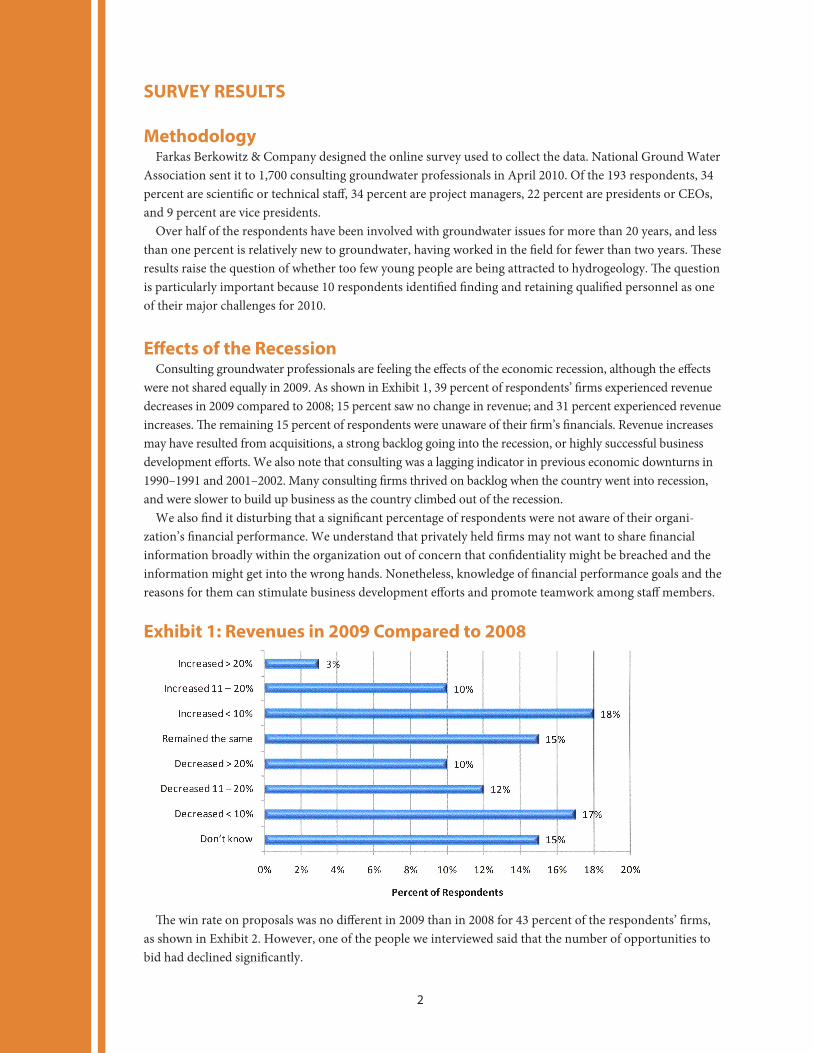

Effects of the Recession Consulting groundwater professionals are feeling the effects of the economic recession, although the effects were not shared equally in 2009. As shown in Exhibit 1, 39 percent of respondents’ firms experienced revenue decreases in 2009 compared to 2008; 15 percent saw no change in revenue; and 31 percent experienced revenue increases. The remaining 15 percent of respondents were unaware of their firm’s financials. Revenue increases may have resulted from acquisitions, a strong backlog going into the recession, or highly successful business development efforts. We also note that consulting was a lagging indicator in previous economic downturns in 1990–1991 and 2001–2002. Many consulting firms thrived on backlog when the country went into recession, and were slower to build up business as the country climbed out of the recession. We also find it disturbing that a significant percentage of respondents were not aware of their organi-zation’s financial performance. We understand that privately held firms may not want to share financial information broadly within the organization out of concern that confidentiality might be breached and the information might get into the wrong hands. Nonetheless, knowledge of financial performance goals and the reasons for them can stimulate business development efforts and promote teamwork among staff members.

Exhibit 1: Revenues in 2009 Compared to 2008

The win rate on proposals was no different in 2009 than in 2008 for 43 percent of the respondents’ firms, as shown in Exhibit 2. However, one of the people we interviewed said that the number of opportunities to bid had declined significantly.

3

Exhibit 2: Win-Rate on Proposals in 2009 Compared to 2008

In response to the recession, 62 percent of respondents’ firms took special measures to maintain or improve profitability. As shown in Exhibit 3, cost-cutting measures were adopted by the largest percentage of firms. These measures included laying off staff, cutting the costs of training, reducing fringe benefits, and reducing the costs associated with information technology. Twenty-four percent of respondents chose the “other” category. Their measures also focused mainly on cost cutting, including salary cuts, putting some staff on furlough, unpaid holidays, failing to replace staff who left voluntarily, and general overhead reductions. One respondent who works for a state-funded agency faced a budget reduction of 10 percent. A smaller percent-age of firms adopted more strategic measures including improving the effectiveness of marketing and sales, discontinuing unprofitable client relationships, and closing marginal offices, measures that probably should have been taken even in the boom times. .

Exhibit 3: Special Measures Taken in Response to the Recession

Approach to Sales and Marketing The seller-doer model prevails in over half of the respondents’ firms, and only 15 percent of the firms have a dedicated sales and marketing staff, as shown in Exhibit 4. When asked who should have primary re-sponsibility for selling business, respondents opted for assigning a much larger role to a dedicated sales and marketing staff, and a somewhat smaller role for individual technical staff members, as shown in Exhibit 5. Four respondents in the “other” category identified themselves as sole proprietors, obviously responsible for

4

marketing and sales. An additional four respondents are in organizations that do not sell services: two work for state agencies supported from the general fund, and one is an in-house environmental specialist in an organization that only buys services. Respondents choosing the “other” category pointed out that “Everyone, directly or indirectly, ‘sells’ the company.” Those respondents also distinguished between selling additional services to existing clients and selling to new prospects. The former requires not only “performing in a way that promotes us to the client in the best manner,” but also being alert to additional services the client might need and remembering to ask for the sale. Client surveys, conducted in person or by phone, preferably by someone not directly connected with the assignment, can also be an excellent source of market intelligence. One of the old saws of marketing is “I don’t care how much you know until I know how much you care.”

Exhibit 4: Responsibility for Business Development Currently

Exhibit 5: Desired Responsibility for Business Development

There are basically two aspects to business development—identifying prospective clients and closing the sale. In our experience, a dedicated marketing staff can be effective in identifying and qualifying new pros-pects, but with very few exceptions, the seller-doer is critical to closing the sale. The exceptions tend to be competitive procurements that are awarded to the low bidder. In most cases, clients give greater weight to the

5

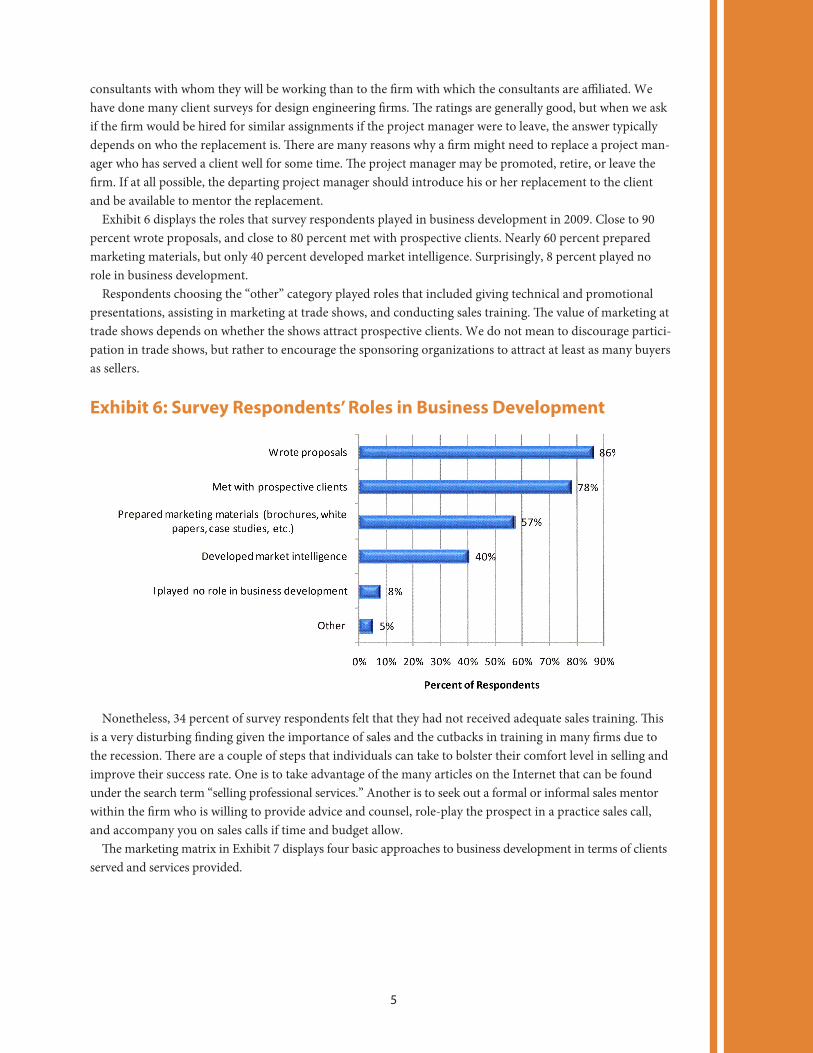

consultants with whom they will be working than to the firm with which the consultants are affiliated. We have done many client surveys for design engineering firms. The ratings are generally good, but when we ask if the firm would be hired for similar assignments if the project manager were to leave, the answer typically depends on who the replacement is. There are many reasons why a firm might need to replace a project man-ager who has served a client well for some time. The project manager may be promoted, retire, or leave the firm. If at all possible, the departing project manager should introduce his or her replacement to the client and be available to mentor the replacement. Exhibit 6 displays the roles that survey respondents played in business development in 2009. Close to 90 percent wrote proposals, and close to 80 percent met with prospective clients. Nearly 60 percent prepared marketing materials, but only 40 percent developed market intelligence. Surprisingly, 8 percent played no role in business development. Respondents choosing the “other” category played roles that included giving technical and promotional presentations, assisting in marketing at trade shows, and conducting sales training. The value of marketing at trade shows depends on whether the shows attract prospective clients. We do not mean to discourage partici-pation in trade shows, but rather to encourage the sponsoring organizations to attract at least as many buyers as sellers.

Exhibit 6: Survey Respondents’ Roles in Business Development

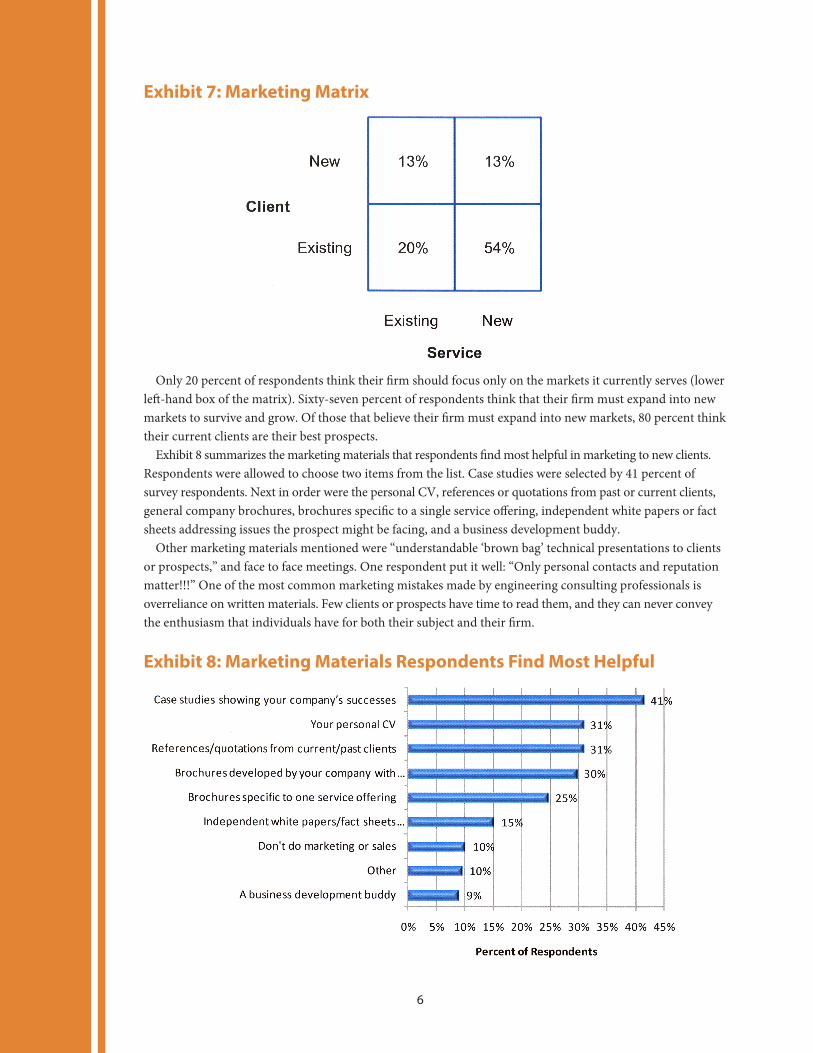

Nonetheless, 34 percent of survey respondents felt that they had not received adequate sales training. This is a very disturbing finding given the importance of sales and the cutbacks in training in many firms due to the recession. There are a couple of steps that individuals can take to bolster their comfort level in selling and improve their success rate. One is to take advantage of the many articles on the Internet that can be found under the search term “selling professional services.” Another is to seek out a formal or informal sales mentor within the firm who is willing to provide advice and counsel, role-play the prospect in a practice sales call, and accompany you on sales calls if time and budget allow. The marketing matrix in Exhibit 7 displays four basic approaches to business development in terms of clients served and services provided.

6

Exhibit 7: Marketing Matrix

Only 20 percent of respondents think their firm should focus only on the markets it currently serves (lower left-hand box of the matrix). Sixty-seven percent of respondents think that their firm must expand into new markets to survive and grow. Of those that believe their firm must expand into new markets, 80 percent think their current clients are their best prospects. Exhibit 8 summarizes the marketing materials that respondents find most helpful in marketing to new clients. Respondents were allowed to choose two items from the list. Case studies were selected by 41 percent of survey respondents. Next in order were the personal CV, references or quotations from past or current clients, general company brochures, brochures specific to a single service offering, independent white papers or fact sheets addressing issues the prospect might be facing, and a business development buddy. Other marketing materials mentioned were “understandable ‘brown bag’ technical presentations to clients or prospects,” and face to face meetings. One respondent put it well: “Only personal contacts and reputation matter!!!” One of the most common marketing mistakes made by engineering consulting professionals is overreliance on written materials. Few clients or prospects have time to read them, and they can never convey the enthusiasm that individuals have for both their subject and their firm.

Exhibit 8: Marketing Materials Respondents Find Most Helpful

7

When asked for a wish list of marketing materials they would like their firm to provide, case studies were again rated number one by 51 percent of respondents. The major difference was a business development buddy, which 29 percent of respondents put on their wish list, but only 9 percent identified as most helpful. We can only conclude that few respondents currently have business development buddies. Based on our experience, two are more than twice as effective as one in marketing and sales calls. Some prospects alternate eye contact roughly equally between the two consultants, but some clearly relate better to one than the other. This is something to be mindful of in conducting sales calls because, as noted earlier, selling consulting services is much more person-to-person than business-to-business.

Sources of Revenue The largest area of activity, by far, for survey respondents in 2009 was remediation, as shown in Exhibit 9. There has also been little change in the mix of activity over the past five years. According to a recent industry report developed by Farkas Berkowitz & Company, the U.S. remediation consulting market sank from $5.7 billion in 2008 to $5.0 billion in 2009, a 13 percent decline. Two important growth drivers were lacking—brownfields development, and mergers and acquisitions. Nonetheless regulatory driven projects continued, and the electric utility, oil and gas, and mining markets were fairly strong. We would have expected that there would be little demand for remediation services 30 years after the passage of Superfund. However, Super-fund created increased sensitivity to the possibility for groundwater contamination. Therefore sites with the potential to contaminate groundwater are more closely monitored today than they might have been 30 years ago. In 2010 and 2011, Farkas Berkowitz & Company anticipates that growth in mergers and acquisitions will stimulate demand for remediation services as part of environmental due diligence and firms with global practices will see increased demand for remediation in China and India.

Exhibit 9: Major U.S. Markets for Groundwater Consulting Services in 2009

Only 18 percent of respondents were active in aquifer storage and recovery in 2009. The threats of drought in the West and the potential impact of climate change on water resources should generate demand for groundwater consultants, but growth has been slow. According to the telephone interviews we conducted, most of the assignments so far have been feasibility studies associated with conjunctive use. Even though groundwater is the primary drinking water source for 46 percent of the U.S. population, groundwater continues to be a stepchild to surface water. Too few prospective clients appreciate the nexus between surface water and groundwater, and the relationship between water and energy which is currently higher on the political agenda.

8

Fifty-eight respondents mentioned other groundwater activities in which they were involved besides those listed in Exhibit 9. The ones mentioned most frequently relate to groundwater supply, develop-ment, and management. Three activities focused on specific industries—groundwater related to mining, groundwater protection as it applies to the natural gas industry, and soil and groundwater remediation of petroleum contamination. Three respondents mentioned litigation support, expert testimony, and forensic hydrogeology. Only one mentioned involvement in climate change issues. Groundwater activities account for a significant fraction of revenue for the firms we interviewed, but none has a stand-alone groundwater section or department. Groundwater professionals support and often lead assignments in other business segments such as remediation and water resources. Sole propri-etors and a few small firms do focus exclusively on groundwater. Over 80 percent of the survey respondents reported private industry as one of their major clients, followed by municipal government authorities and water districts, other consulting, engineering or construction firms, state government agencies, law firms, and federal government agencies, as shown in Exhibit 10. Other clients mentioned include developers and banks.

Exhibit 10: Major Clients of Groundwater Consulting Firms in 2009

Major Challenges The challenge mentioned most frequently by survey respondents is overcoming the poor economy. They noted limited spending by clients while at the same time recognizing that their clients face economic chal-lenges too. Clients in the oil and gas industry were cited specifically as having taken cost-cutting measures. Many clients have been slow to pay. Respondents are also facing increased competition in the marketplace, competition from bigger companies chasing smaller jobs, and from “unqualified ‘professionals’ who low ball project costs and deliver a low ball product.” One respondent, however, was trying to convince management to accept lower profit margins to win work. One respondent identified the major challenge as “determining how to compete in a business world focused on low price after having worked in a relatively expansive specialty area.” Others stated their major challenge in more general business development terms, as follows:

• Maintain sales• Maintain existing clients• Continue to develop external client-focused relationships• Strengthen existing relationships• Develop new clients• Reach out to prospective commercial clients on our capabilities

9

• Expand services to new business sectors• Specialize and become more competitive in specific markets• Effectively market the advantage of “small/nimble” versus “enormous/ponderous.”

Several respondents would like additional training in sales and marketing techniques. One respondent who mainly does report writing would like to interact more with clients. Another respondent summed it up with “It is all about being able to bring in work.” While business development has taken on new urgency, two respondents commented on the challenge of balancing time between selling and doing—keeping up with current work while at the same time looking for new opportunities. Many respondents claimed lack of time to pursue business development, but that may be a lack of discipline to go out and visit with clients and potential clients. Not everyone is happy about the increased emphasis on business development, as indicated by the following two comments:

• “The company has now placed too much emphasis on marketing. A marketing person is now managing our Technical Services Division, not a scientist.”

• A major challenge in the respondent’s firm is “getting recognized for technical excellence apart from marketing prowess.”

FINDING THE PROSPECTS – MAKING THE SALE

Business Development The ancient Rabbi Hillel, one of the most honored scholars in Jewish history, captured the essence of business development in three questions: If I am not for myself, who will be for me? If I am for myself alone, what am I? If not now, when? The first rule of selling is a can-do attitude. When you meet with a prospect, put yourself in a frame of mind that assumes the sale is made. One way to do that is to relive in your mind a time when everything was going right for you and you felt really good about yourself. Do not play it like a movie; relive it. In reality, the best sales people in the best of times will fail to make the sale two times out of three. In difficult economic times, the win rate can be much lower, but whether you get the door slammed in your face two times out of three or nine times out of ten, you cannot lose faith in yourself. The second rule of selling is showing that you genuinely care about your prospect and his or her success. Learn as much as you can about the prospect’s organization and industry before your meeting, so that you can talk the prospect’s language. At a minimum, study the prospect’s website. Many people begin a sales call by asking, “What keeps you up at night?” or “What are your major challenges?” We often ask, “What would you like to accomplish in the next year or two?” The answer we usually get is a surprised “Me personally?” We nod. The prospect responds and then invites us to tell our story. It doesn’t always work. We remember a time when the answer was “What business is it of yours?” A colleague helped us recover. No matter how you do it, you want the prospect to do most of the talking. The third rule of selling is try it, you might like it, and if you listen and get some honest feedback, you will get better at it. The seller-doer model is the only viable alternative for a sole proprietor. Larger firms typically have dual track paths for advancement, a management track and a technical track. Those on the management track are expected to bring in business. Those on the technical track need to build a reputation within the firm for both their technical expertise and their ability to work with a team. Those on the management track sell externally; those on the technical track sell internally. In both cases, technical capability is half the sale; the other half is relationship and rapport.

10

For some, sales may seem undignified for a scientist or engineer, but sales is really making friends and the opportunity to apply your technical skills to help a sponsor solve a real-world problem.

Prospecting How do you identify and qualify prospects? Government procurements are typically advertised. However, once the potential opportunity is made public, it is often too late to make personal contact with the technical project sponsor. Chances for success improve if that relationship is established before the request for pro-posal (RFP) or request for quotation (RFQ) are issued. Also, many recent federal procurements have been indefinite delivery/indefinite quantity (ID/IQ) contracts for which there are multiple awards. The awardees then have the opportunity to submit competitive bids on task orders issued under the contract. Ways to identify non-government prospects mentioned in the telephone interviews we conducted include:

• Personal contacts and networks• Business networking with professional organizations• Word of mouth• Knocking on doors • Existing clients.

You build personal contacts and networks by becoming known to prospective clients. There are many ways to do that. One is to attend, and preferably to speak at, conferences and meetings that attract prospects. Another that one of the firms we interviewed found to be even more effective is to make technical presenta-tions for prospects at brown bag lunches. A third is to publish papers in journals, magazines, or other media that prospects read. Since much communication today is via the Internet, every groundwater consulting professional should make sure that his or her name and capabilities can be found readily on the Internet. Among our survey re-spondents, 42 percent did not have Internet presence or were not sure whether they did. Internet presence can help cultivate a strong personal reputation which might lead to potential customers calling you. That is obviously more desirable than knocking on doors, but those prospects need to be able to find you easily. Many professionals use a professional social networking site such as LinkedIn. Similarly, potential clients may find your firm on the Internet when they search for a consultant who might meet their needs. We have visited many websites of firms that provide groundwater consulting services. Some describe a dozen or more services, but the firm’s competitive strength may be in no more than three or four of those service areas. Case studies, as pointed out by many of the survey respondents, are particularly effective in helping prospects assess the firm. Over 80 percent of our survey respondents either agreed or strongly agreed with the statement “Our cur-rent clients are our best prospects.” One of the firms we interviewed by telephone said that in any given year, 90 to 94 percent of their business comes from returning customers. That does not happen automatically. Doing a good job is critical, but you have to put in the effort to learn what additional needs the client may have that your firm can satisfy, and to “educate” the client on the full range of your firm’s relevant technical capabilities. That is much easier to do when you already have a relationship with a client than when you are meeting with a new prospect. If at first you don’t succeed, should you try, try again? That’s a difficult question to answer. In my early days as a consultant, I went out knocking on doors with one of my firm’s most successful marketers. One of the people we called on greeted us with “When I need a consultant, I go to the best source in the United States, and for anything I have needed you have not been it.” Even my experienced mentor crawled out on his belly, figuratively speaking. A year or so later, I sat next to the prospect at a dinner. He remembered the call and asked me why I had not returned. Ultimately, he became a loyal client.

11

Most firms have an attractive marketing brochure. Handing it out at conferences or mass mailing it is not usually a good way to attract prospects. Few, if any, of the business cards visitors leave in a fishbowl at your booth at an environmental fair are likely to be good prospects. However, engaging those visitors in conversa-tion can help identify whether or not they qualify as prospective clients.

Turning Prospects into Clients If you can get prospects talking about their concerns, their needs, or their goals, then you should discuss your services in terms of how they will address the issues the prospect has already identified as important. If the prospect is unresponsive to your initial probe, then you should be prepared with a back-up sales pitch. Within the context of professional services, the purpose of a sales pitch is to engage the prospect in a con-versation on a topic related to a service your firm provides that you think should be of interest. You might start with an initial benefit statement—a sentence introducing the topic, followed by a brief statement of your perspective on the topic. It might be of the form “We have found that many firms in your industry are con-cerned about . . . Our firm has helped them by . . . How are you dealing with that issue?” It might take two or three similar initial benefit statements to get the prospect’s attention. Once you have succeeded in developing a dialogue with the prospect on an area of mutual business interest, don’t forget to ask for the sale. A word of caution – some prospects will ask for a proposal just to get rid of you. Be aware of that possibility, and avoid it to the extent possible.

About the Authors Joan B. Berkowitz, Ph.D., is a managing director. She began her management consulting career at Arthur D. Little, where she was a vice president. She specializes in analyzing environmental and infra-structure markets in support of the firm’s strategy practice. She has a Ph.D. in physical chemistry from the University of Illinois and is a graduate of the senior executive program of the MIT Sloan School. She is an adjunct professor at the University of Maryland and a member of NGWA. She can be reached at [email protected].

Christopher S. Frangione is a managing associate. He has more than more than 12 years experience as a corporate executive and management consultant. His experience includes the promotion and development of renewable energy and clean coal technologies. Since joining the firm in early 2004, he has assisted clients by conducting customer surveys, by evaluating markets for diversification, and by advising on entry strategies. He leads the firm’s market assessment practice. Frangione holds an M.B.A. and Master of Environmental Management from Duke University and a B.A. in environmental policy from Colby College. He can be reached at [email protected].

About Farkas Berkowitz & Company Farkas Berkowitz & Company is a management consulting firm serving companies that provide design, construction, and operational services for government and industry. Established in 1983, the firm assists clients with strategy, mergers and acquisitions, and operations improvement. Inquiries should be addressed to Christopher Frangione at 202 833.7530 or [email protected] or visit their Website: www.farkasberkowitz.com.

12

This white paper was funded by the National Ground Water Association as a benefit to our members working in the groundwater consulting sector. We hope you find the results informative and will help you and your business. Thank you for your membership.

Kevin McCray, CAE Trisha Freeman Executive Director Director of Community/Membership

© 2010 by National Ground Water Association PressISBN 1-56034-034-7

Published by: NGWA Press National Ground Water Association Address 601 Dempsey Road, Westerville, Ohio 43081-8978 U.S.A. Phone (800) 551-7379 • (614) 898-7791 Fax (614) 898-7786 Email [email protected] Websites NGWA.org and WellOwner.org

The GroundwaterNGWA

Association

SM

Pres

s

The National Ground Water Association is a not-for-profit professional society and trade association for the global groundwater industry. Our members around the world include leading public and private sector groundwater scientists, engineers, water well system professionals, manufacturers, and suppliers of groundwater-related products and services. The Association’s vision is to be the leading groundwater association advocating for responsible development, management, and use of water.

Disclaimer: This White Paper is provided for information purposes only so National Ground Water Association members and others using it are encouraged, as appropriate, to conduct an independent analysis of the issues. NGWA does purport to have conducted a definitive analysis on the topic described, and assumes no duty, liability, or responsibility for the contents of this White Paper. Those relying on this White Paper are encouraged to make their own independent assessment and evaluation of options as to practices for their business and their geographic region of work.

Trademarks and copyrights mentioned within the White Paper are the ownership of their respective companies. The names of products and services presented are used only in an education fashion and to the benefit of the trademark and copyright owner, with no intention of infringing on trademarks or copyrights. No endorsement of any third-party products or services is expressed or implied by any information, material, or content referred to in the White Paper.