bvk ivdc 20-10-2009

TRANSCRIPT

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 1/25

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 2/25

N am e of Presentation | S pea ker | D ate | Pa ge 2

Talking about US Housingbubble since 2004

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 3/25

- -H ou sing b ub ble | Ivan Va n de C loot | 2 0 1 0 2 00 9 | Pag e3

Exuberant expectations

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 4/25

- -H ou sing b ub ble | Ivan Va n de C loot | 2 0 1 0 2 00 9 | Pag e4

Markets are not efficient

=bubbles exist

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 5/25

5

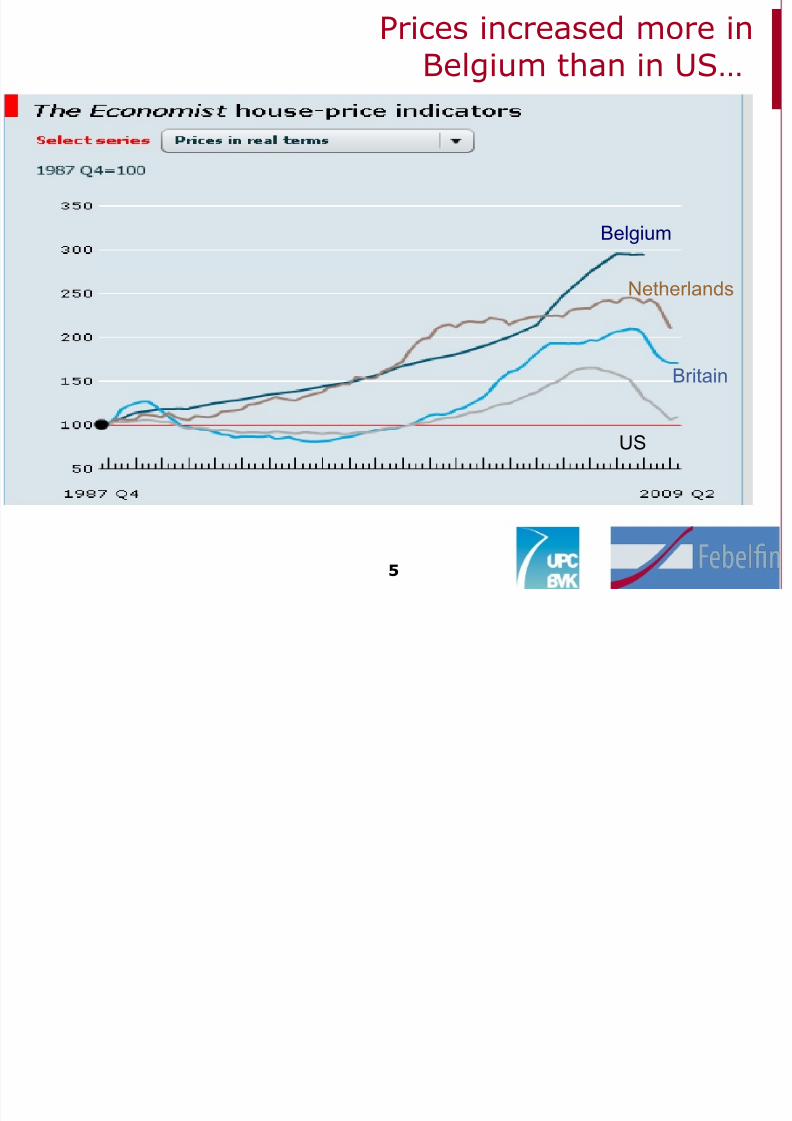

Prices increased more inBelgium than in US…

Belgium

Netherlands

US

Britain

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 6/25

6

…much more in fact.

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 7/257

House price-income ratioexploded in Belgium

Belgium

Netherlands

Britain

US

Japan

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 8/258

Macro-econometric research: eg. IMF, ING

Asset-pricing approach: eg. OESO

Eventstudies: Helbling (BIS)- House price bubbles-a tale based on housing price booms and busts

Vector Autoregressive Models (VAR): eg. 1)

Christopher Otrok Marco E. Terrones: House Prices,

Interest Rates and Macroeconomic Fluctuations:International Evidence 2) World Economic Outlook

•

•

•

Fundamentals?

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 9/25

- -Housing bubble | Ivan Van de Cloot | 20 10 2009 | Page9

Strong collateral?

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 10/2510

Macroeconometric

research

nInteresting to look at “average reactions”

n= Bell Curve economics: won’t be able to detectbubbles

nEven this conservative research: overvaluation of Belgian real estate

IMF (2006): 17%

ING (2009): 16% probable, 44% if in line with previous

correction

n

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 11/2511

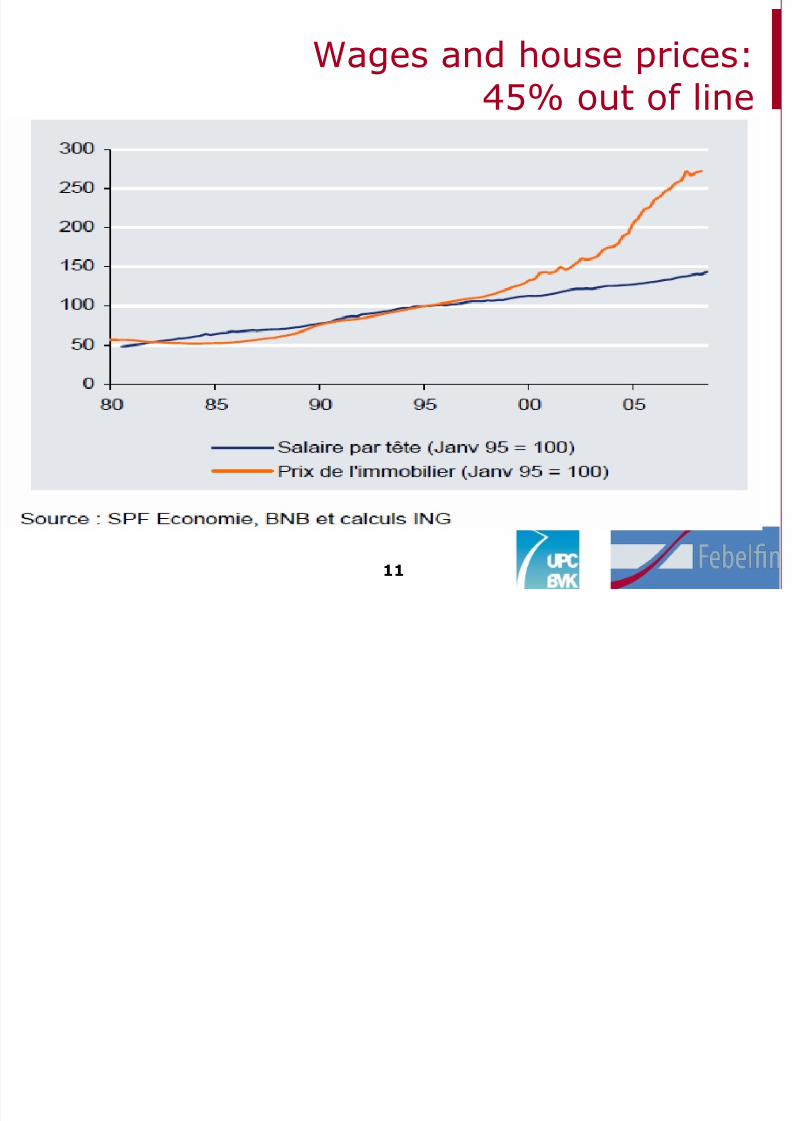

Wages and house prices:

45% out of line

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 12/2512

IMF: Macroeconometric

study

-10

-5

0

5

10

15

20

25

30

35

I r e l a

n d

N e

t h e r l a n

d s

U K

A u s

t r a

l i a

F r a n

c e

N o r w

a y

D e n m a

r k

B e

l g i u

m

S p a

i n

S w e d e n

I t a l y

J a p

a n

U S A

F i n l a

n d

G e r m a

n y

C a n a

d a

A u s

t r i a

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 13/25

13

Upward shock in realinterest rates

9

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 14/25

14

Overvaluation measures sensitive

to choice of “equilibrium”

30 0%

40,0%

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 15/25

15

Belgium is not cheap if corrected for bubbles

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 16/25

- -Housing bubble | Ivan Van de Cloot | 20 10 2009 | Page16

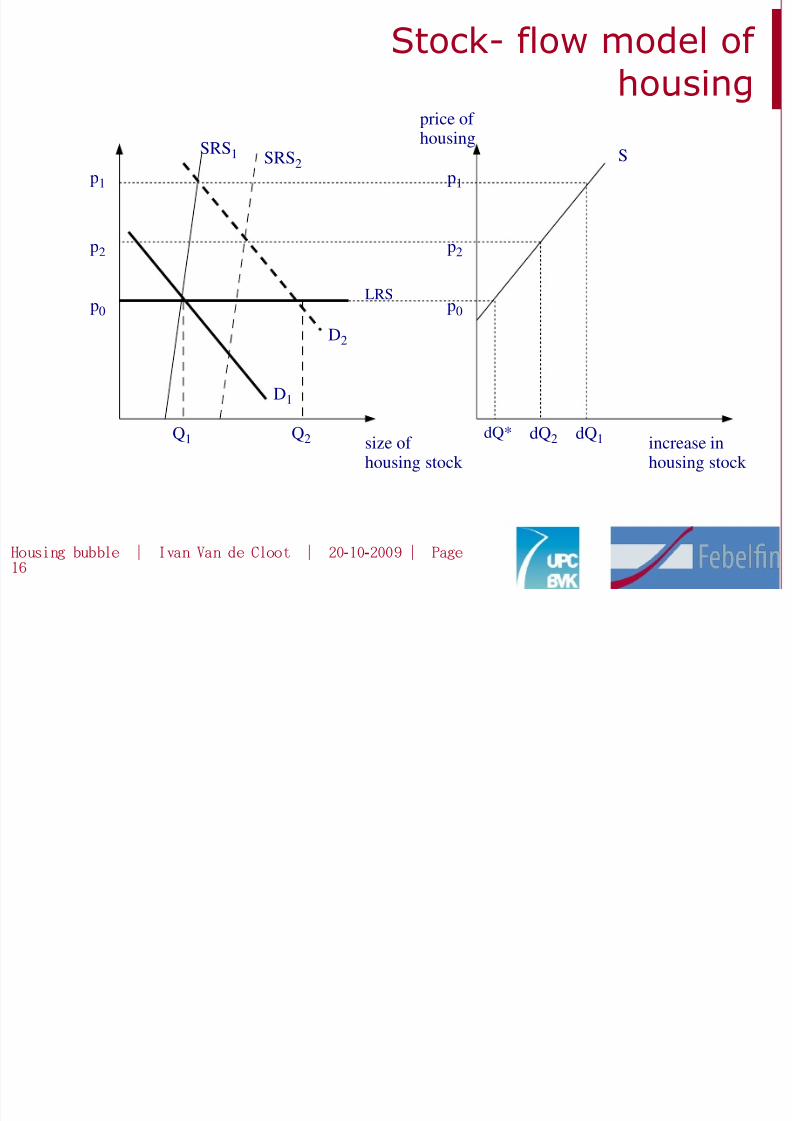

Stock- flow model of

housing

size of housing stock

increase inhousing stock

price of

housing

LRS

SRS1

D1

p0 p0

Q1 dQ*

S

D2

p1 p1

dQ1

SRS2

Q2

p2 p2

dQ2

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 17/25

17

Dynamics

t0

P

Demand shock:overshooting

t0

P

Supply shock:undershooting

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 18/25

18

Asset pricing approach:expectations matter

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 19/25

19

OECD: Asset pricingapproach

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 20/25

20

User cost of housing= P*(i+t+f-p)i=mortgage rate, t=tax, f= depreciation,

p=Expected capital gain

Equilibrium: rent=buy, E= P*(i+t+f-p) / = /(P E 1 i+t+f-p)So: as long as we come across exuberant

people, … (the market can stay irrationallonger than you can stay solvent, Keynes)

Expectations matter

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 21/25

21

... It has been argued that the striking housing

price increases in some countries in recentyears were a response to the sharp decreasesin interest rates, as central banks eased theirmonetary policy stance during the downturn...Monetary policy tightening appears to have

played a role in triggering housing price bustsafter booms, as short-term rates typicallyincreased toward the end of a boom andremained high into the first year of a bust.

•

•

•

Helbling (BIS)-Event study

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 22/25

22

Helbling (BIS)-Event study

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 23/25

23

House Prices and Monetary

Policy: A Cross-Country Study,Federal Reserve

IMF World Economic Outlook

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 24/25

24

“The dynamic factor model/FAVAR analysis

assumes that house prices are driven byfundamentals and is not designed to test forthe existence of potential bubbles.”

“In cases where house prices may have

exceeded fundamentals— which may includeAustralia, Ireland, Spain, and the UnitedKingdom-, there is a danger that higherinterest rates could trigger a much larger

downward adjustment in house prices, withconsiderably more severe consequences forreal activity.

•

•

•

IMF, World Economic Outlook,

September 2004

8/8/2019 BVK IVDC 20-10-2009

http://slidepdf.com/reader/full/bvk-ivdc-20-10-2009 25/25

- -Housing bubble | Ivan Van de Cloot | 20 10 2009 | Page25

Mortgage indebtness at

an all time high

90%

100%

Debt to disposable income