by ca girish kulkarni

DESCRIPTION

Imp and New Requirements with regards Tax and other Audit Report. BY CA GIRISH KULKARNI. - PowerPoint PPT PresentationTRANSCRIPT

Imp and New Requirements with regardsTax and other Audit Report

BY CA GIRISH KULKARNI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

2

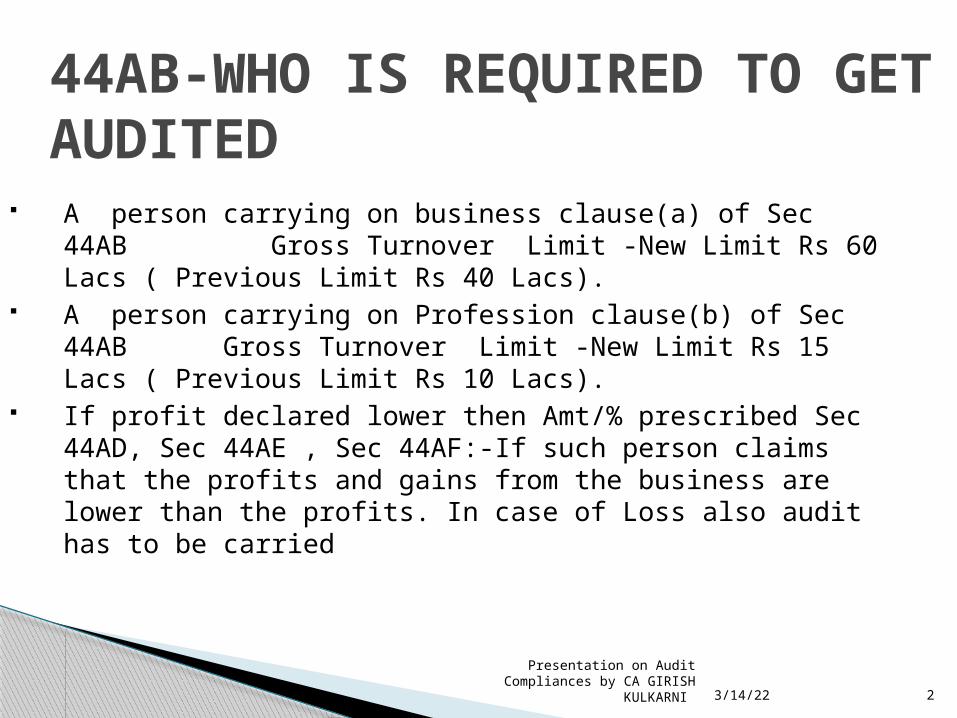

A person carrying on business clause(a) of Sec 44AB Gross Turnover Limit -New Limit Rs 60 Lacs ( Previous Limit Rs 40 Lacs).

A person carrying on Profession clause(b) of Sec 44AB Gross Turnover Limit -New Limit Rs 15 Lacs ( Previous Limit Rs 10 Lacs).

If profit declared lower then Amt/% prescribed Sec 44AD, Sec 44AE , Sec 44AF:-If such person claims that the profits and gains from the business are lower than the profits. In case of Loss also audit has to be carried

44AB-WHO IS REQUIRED TO GET AUDITED

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

3

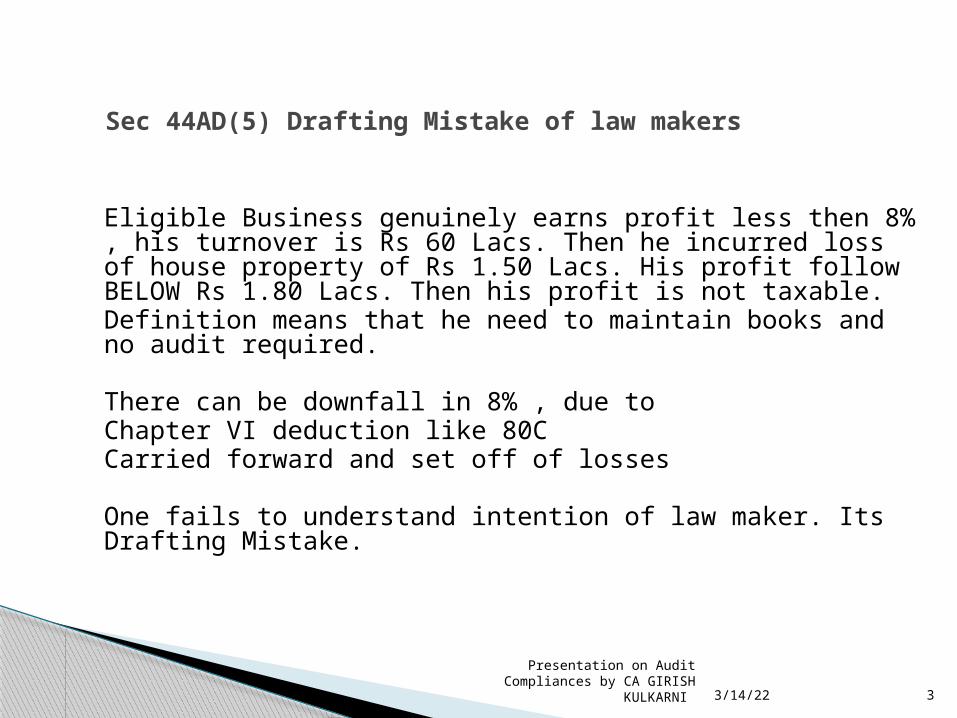

Eligible Business genuinely earns profit less then 8% , his turnover is Rs 60 Lacs. Then he incurred loss of house property of Rs 1.50 Lacs. His profit follow BELOW Rs 1.80 Lacs. Then his profit is not taxable.Definition means that he need to maintain books and no audit required.

There can be downfall in 8% , due to Chapter VI deduction like 80CCarried forward and set off of losses

One fails to understand intention of law maker. Its Drafting Mistake.

Sec 44AD(5) Drafting Mistake of law makers

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

4

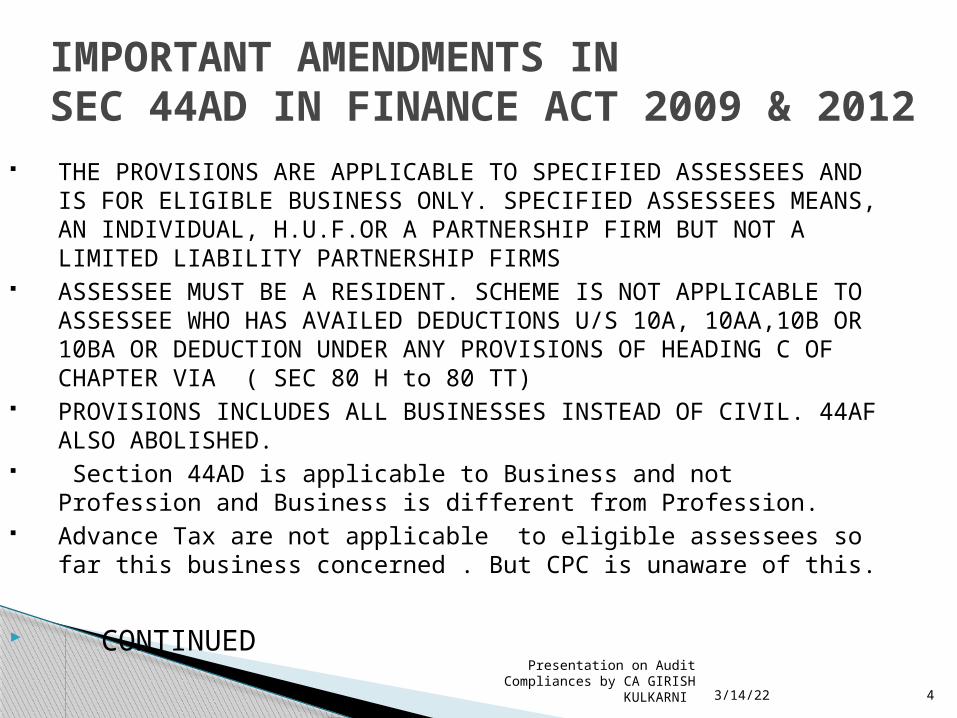

IMPORTANT AMENDMENTS IN SEC 44AD IN FINANCE ACT 2009 & 2012

THE PROVISIONS ARE APPLICABLE TO SPECIFIED ASSESSEES AND IS FOR ELIGIBLE BUSINESS ONLY. SPECIFIED ASSESSEES MEANS, AN INDIVIDUAL, H.U.F.OR A PARTNERSHIP FIRM BUT NOT A LIMITED LIABILITY PARTNERSHIP FIRMS

ASSESSEE MUST BE A RESIDENT. SCHEME IS NOT APPLICABLE TO ASSESSEE WHO HAS AVAILED DEDUCTIONS U/S 10A, 10AA,10B OR 10BA OR DEDUCTION UNDER ANY PROVISIONS OF HEADING C OF CHAPTER VIA ( SEC 80 H to 80 TT)

PROVISIONS INCLUDES ALL BUSINESSES INSTEAD OF CIVIL. 44AF ALSO ABOLISHED.

Section 44AD is applicable to Business and not Profession and Business is different from Profession.

Advance Tax are not applicable to eligible assessees so far this business concerned . But CPC is unaware of this.

CONTINUED

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

5

IMPORTANT AMENDMENTS IN SEC 44AD IN FINANCE ACT 2009 & 2012

Some activities have been held to be business:- Advertising agent, Clearing, forwarding and shipping agents–CIT v/s. Jeevanlal Lallubhai & Co. [1994] 206 ITR 548 (Bom)., Couriers, Insurance agent, Nursing home,Stock and share broking and dealing in shares and securities – CIT v/s. Lallubhai Nagardas & Sons [1993] 204 ITR 93 (Bom).,Travel agent.

44AD (6) The provisions of this section, notwithstanding anything contained in the

foregoing provisions, shall not apply (WEF 1-4-2011,AY 2011-12)???????????? (i) a person carrying on profession as referred

to in sub-section (1) of section 44AA; (ii) a person earning income in the nature of commission

or brokerage; or (iii) a person carrying on any agency business

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

6

Tax auditor BY AUDITOR i.e. Accounts of previous year be to audited by an

accountant (Defined u/s 288) ,before the specified date i.e. 30 Sept. If Return/E-Return is not submitted and Audit is completed, Then Assessee is required to submit Audit Report physically as per Sec 44AB. Part Time Practicing CA can not sign tax audit.(Para 9.3 of ICAI Guidance Note). As per council decision(12-12-2008), any Internal Auditor can not be Tax Auditor.

Signature on Auditors’ report: Tax Audit Report should be signed by the CA in Practice mentioning the name of firm, name of the member signing, Member ship No. and Registration Number of the firm (Applicable from 01.04.2010) as allotted to them by the Institute of CAs of India.

The Income Tax Dept and ICAI is investigating cases 1. Audit exceeding 45 limits 2. Audit by Fake CAs 3. Audit signed in

name of non practicing members 4. Audit signed in name of dead persons.

New process of viewing number of Audit signed by CAs likely to start with support of NSDL likely to start after 30 Sept 2012.

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

7

When Books of Accounts need not be maintain, then whether But it is necessary to submit Balance Sheet or Capital Account

Opening Balance Sheet Become Crucial if not prepared

Method of Accounting:- Still Mandate as per Sec 145.

Two Views No Books, But Sec 145 applies Sec 145 is out of Presumptive Taxation

MAINTAINANCE OF BOOKS OF ACCOUNT IN CASE OF CASES COVERED U/S 44AD OR 44AE

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

8

1) Sales Tax, excise duty, Cess, and other Levy.2) Sales of unusable empties and Packages.3) Service Charges charged for delivery

As per Guidance note, the excise duty needs to be provided where goods are manufactured and kept in warehouse/factory

What are the receipts which forms Part of Turnover?

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

9

The onus of proof is on the assessee. It is his duty to prove the turnover. If the assessee is maintaining the books of accounts, then it will be easy for him to prove the same, but if he is not maintaining the books of accounts, then it will be very difficult for him to prove, because there is no specific provision for the same.

What documents you should provide to the AO to prove the turnover?

copies of invoices issued during the PY copies of cash memo copies of Purchase bill Bank statement Inventory details, if any maintained Average G.P rate applicable to Particular business Returns filed under sales tax/vat/excise/service Tax laws.

Who bears the onus of proof to prove the turnover?

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

10

The assessee is a firm and engaged in business of financing and follows cash system of accounting. It gave a loan to a company on interest. The borrower while crediting the interest deducted TDS and issued TDS certificate. The assessee claimed the credit of TDS without offering the corresponding income to tax . The AO disallowed the claim of the assessee .The CIT (A) allowed the appeal of the assessee.

ITO Business Ward –II (4) v. M/s Shri Anupallavi Finance & Investments (2011-TIOL-78-ITAT-MAD)

Sec 199 –Does the method of accounting impact the year of TDS credit ?

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

11

When Books of Accounts need not be maintain, then whether But it is necessary to submit Balance Sheet or Capital Account

Opening Balance Sheet Become Crucial if not prepared

Method of Accounting:- Still Mandate as per Sec 145.

Two Views No Books, But Sec 145 applies Sec 145 is out of Presumptive Taxation

MAINTAINANCE OF BOOKS OF ACCOUNT IN CASE OF CASES COVERED U/S 44AD OR 44AE

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

12

If Income is exempt u/s 10 :- No Tax Audit requiredFavoured by ITAT Mumbai (in 2002): ACIT Vs India Magnum Fund 81 ITD 295 NOT FAVOURED BY ICAI GUIDANCE NOTE PARA 6.1 STATES 44AB OR OTHER SECTION OF INCOME TAX ACT DOES NOT

EXEMPT FROM TAX AUDIT IF TOTAL INCOME IS NOT TAXABLE. BUT AGRICULRIST EXEMPTED FROM TAX AUDIT.

VOLUNTARY CONTRIBUTION TO POLITICAL PARTIES ARE NOT PROFESSIONAL RECEIPTS AND NOT LIABLE FOR AUDIT. BOARD INSTRUCTION DT 19-10-2000

Continued

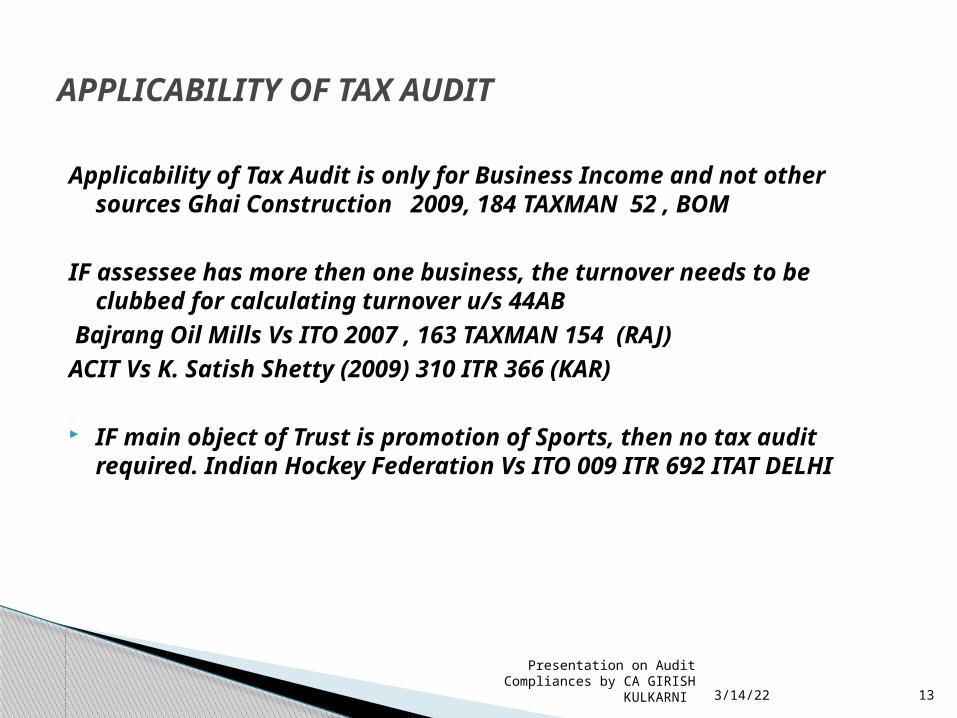

APPLICABILITY OF TAX AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

13

Applicability of Tax Audit is only for Business Income and not other sources Ghai Construction 2009, 184 TAXMAN 52 , BOM

IF assessee has more then one business, the turnover needs to be clubbed for calculating turnover u/s 44AB

Bajrang Oil Mills Vs ITO 2007 , 163 TAXMAN 154 (RAJ)ACIT Vs K. Satish Shetty (2009) 310 ITR 366 (KAR)

IF main object of Trust is promotion of Sports, then no tax audit required. Indian Hockey Federation Vs ITO 009 ITR 692 ITAT DELHI

APPLICABILITY OF TAX AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

14

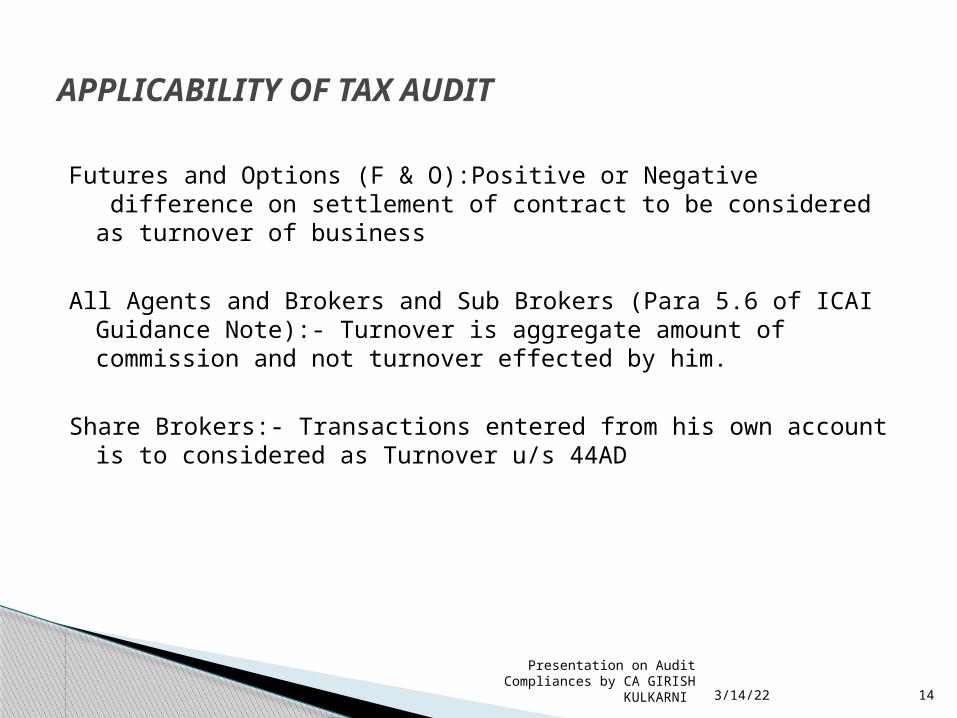

Futures and Options (F & O):Positive or Negative difference on settlement of contract to be considered as turnover of business

All Agents and Brokers and Sub Brokers (Para 5.6 of ICAI Guidance Note):- Turnover is aggregate amount of commission and not turnover effected by him.

Share Brokers:- Transactions entered from his own account is to considered as Turnover u/s 44AD

APPLICABILITY OF TAX AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

15

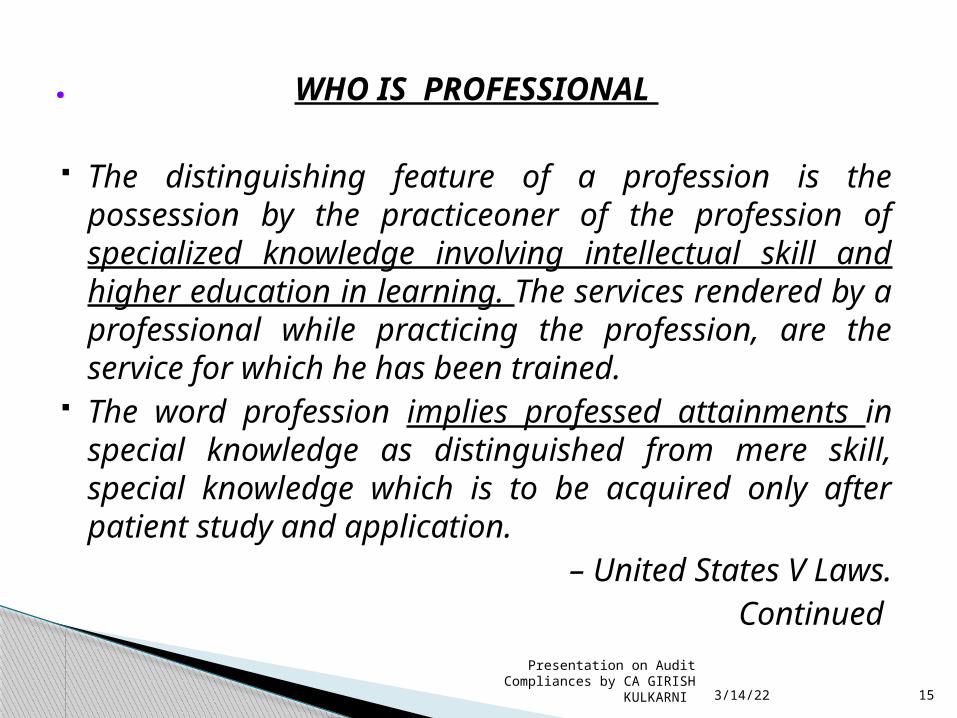

. WHO IS PROFESSIONAL

The distinguishing feature of a profession is the possession by the practiceoner of the profession of specialized knowledge involving intellectual skill and higher education in learning. The services rendered by a professional while practicing the profession, are the service for which he has been trained.

The word profession implies professed attainments in special knowledge as distinguished from mere skill, special knowledge which is to be acquired only after patient study and application.

– United States V Laws. Continued

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

16

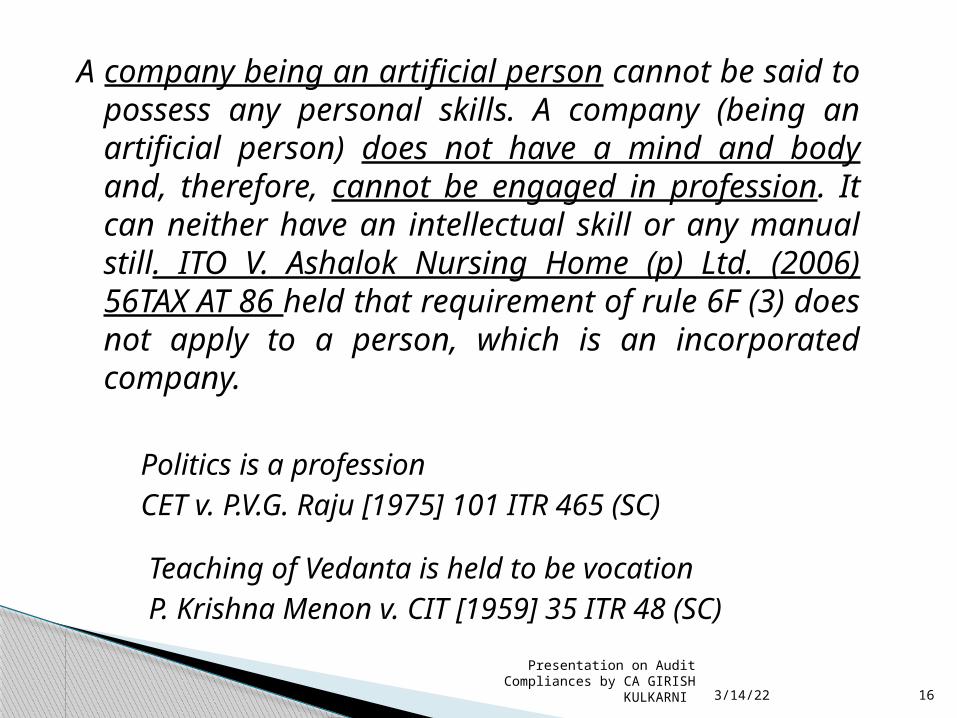

A company being an artificial person cannot be said to possess any personal skills. A company (being an artificial person) does not have a mind and body and, therefore, cannot be engaged in profession. It can neither have an intellectual skill or any manual still. ITO V. Ashalok Nursing Home (p) Ltd. (2006) 56TAX AT 86 held that requirement of rule 6F (3) does not apply to a person, which is an incorporated company.

Politics is a professionCET v. P.V.G. Raju [1975] 101 ITR 465 (SC)

Teaching of Vedanta is held to be vocationP. Krishna Menon v. CIT [1959] 35 ITR 48 (SC)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

17

The word Claim signifies the right of assessee, and it is not an obligation of the assessee.

The following judicial decisions support this view :

Samta construction Co V. Pawan Kumar sharma (2000)244 ITR 845 (MP)CIT V. ARVIND MIILS LTD(1992) 193 ITR 255 AC, (SC)BANGLORE VELLIAPA TEXTILES LIMITED AND ANOTHER (2003) ITR 560

(SC)

Claim Vs Obligation

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

18

CHECK PARTNERSHIP DEED CLAUSE ON REMUNERATION.

NEEDS TO FILE CERTIFIED COPY WITH INCOME TAX OFFICE U/S 184(4) OF INCOME TAX ACT.

ELSE LOSE CLAIM.

PARTNERHIP DEED :- Make Changes & Submittion

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

19

CIT Vs Surinder Pal Anand(2010) 192 Taxman 264 ( P & H)Assessee was not under obligation to explain Individual Entry of cash deposit in the bank unless such entry has nexus with gross receipts.

CIT Vs Amarshiv Construction P Ltd(2004) 88 ITD 381 (Ahd)Retention money detected from bills of the assessee contractor for satisfactory completion of work, has to be treated as income in the year in which bills are raised.

ACIT Vs Balaji Constructions (2000) 110 TTJ 719 (Ahd.) Legislature has recognized 92% of contract as expenditure. The assessee can not be asked to explain the entries of expenditure.

Shivani Builders V Income Tax officer(2007) 110 TTJ 719 (Ahd)

During Survey , suppressed contract receipts found. It can not be ignored.

Continue

FEW IMPORANT CASES –MAY HELP U FOR AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

20

CIT V Bhavan Va Path Nirmal(Bohra) & C.(2002)[110 TTJ 719 (Ahd.) :

Profit assessed on estimated income.Sales tax refund in current year. Sales Tax refund can not be deemed to be income by invoking Sec 41(1).

Mohd Aslam Vs ITO (ITA No 2028 of1996 decided on 13-9-2004, Jodhpur ITAT)

44AE estimated assessee’s income from truck plying. Sale of scrap Continue

FEW IMPORANT CASES –MAY HELP U FOR AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

21

Merilyne Shipping and Trasports at Vishakhapatam Highcourt (2012): s.40(a)(ia) apply only to expenditure remaining payable. whether the provisions of sec.40(a)(ia) would apply to all payments made during the course of the year or it would apply only to the expenditure which remain payable as at the end of relevant year was considered by the Visakhapatnam Special Bench in the case of Merilyn Shipping & Transports, referred (Supra) and the Special bench, by majority view, has held that the provisions of section 40(a)(ia) of the Act would apply only to the expenditure which is payable as on 31st March of every year and cannot be invoked to disallow the amounts which have already been paid during the previous year without deducting tax at source.

Decision will depend on your case and judgement of assessing officer.

Continue

FEW IMP CASES –MAY HELP U

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

22

1. Penalty does not depend on return income. JCIT, Surat vs Saheli Leasing & Industries Ltd [2010] 191 TAXMAN 165 (SC) held that even if return is NIl and after addition , there is no tax payable , the penalty u/s 271(1)( c) lies . does not depend on the issue whether the return pertains to income or loss . Even if there is loss return and no tax was levied after dis allowance, penalty u/s 271(1)( c) sustains.

2.Penalty cannot be imposed just for making incorrect claim :Supreme Court judgment in CIT vs Reliance Petroproducts Pvt Ltd [2010] 322 ITR 158 is path breaking judgment specially the tendency of the income tax officers to initiate penalty proceeding for any claim by assessee which is not as per law. In this judgment, the Supreme Court also defined what is the meaning of “furnishing incorrect particulars of income” Continue

Few Imp Cases :4 Supreme Court Principles on 271 (1)( c)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

23

3.Mens Rea Not Necessary For Imposing Penalty u/s 271(1)( c) :-Apex Court in case of Union of India vs Dharmendra Textile [2008] 166 TAXMAN 65 (SC ) held that the penalty u/s 271(1)( c) is a civil liability and it is not necessary for revenue authorities to prove that the assessee has deliberately did the error or intention of the assessee was to evade tax. This judgment also questioned earlier order of Supreme Court in Dilip N. Shroff v. Jt. CIT [2007] 161 Taxman 218 and held “.

4. A.O must prove that There was concealment of income or The return of income furnished by assessee or documents

submitted by assessee during scrutiny proceeding is based on incorrect fact , falsity and untruth.

Few Imp Cases :4 Supreme Court Principles on 271 (1)( c)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

24

The Employers normally make deductions from salaries of the employees towards their contribution for welfare funds like PF, ESI etc. These deducted amounts in the first instance treated as income of the employer assessee u/s 2(24)(x) and if it is paid before the due date to the credit of employees A/c of the welfare fund, it is allowed as deduction u/s 36(1)(va). Therefore if the payment has not been made before the due date, the deduction will not be allowed and it will result into an addition to the income of the assessee.

CIT vs. AIMIL Limited (Delhi High Court), CIT vs. Dharmendra Sharma 297 ITR 320, CIT vs. Sabari Enterprises 298 ITR

141(Karnataka)

Clause 16 on Employers contribution Section 36(1)(va)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

25

Clause 17(L) –Amount inadmissible under section 14A

Expenditure incurred in relation to income which does not form part of the total income is not allowed as a deduction

Primary responsibility of the assessee to furnish details

Rule 8D [inserted vide Notification no. 208/2006 dated 24 March 2008] provides method for AO to determine the amount of expenditure in relation to income not included in total income

Whether Rule 8D is mandatory for assessees?

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

26

Sub Clause (L) on Sec 14A Disallowance of expenditure incurred

in relation to Exempted income.

It is in my opinion toughest responsibility has been cast on the Tax Auditor to determine the amount of inadmissible deduction of expenditure incurred in relation to an income which does not form part of total income. Recently the Hon’able Bombay High Court has delivered the Judgment in case of Godrej & Boyce vs DCIT ITA No; 626 of 2010 on 12.08.2010 whereby it has decided following issues:-

(1) The argument that dividend on shares is not tax free in view of payment of dividend distribution tax is not acceptable as the said tax is being paid by the company and not the shareholder.

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

27

Section 14A and rule 8D

In view of the above facts if separate account books are maintained in respect sources generating exempted income, so as to show and account for amount of expenditure incurred for earning the exempted income, then to my opinion the severity of provisions of section 14A and rule 8D could be reduced.

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

28

Clause 17(l) –Amount inadmissible under section 14A

ICAI –280thCouncil meeting 7 –9 August 2008 –considered the appropriate guidance to members on clause 17(l):

Rule 8D applicable when AO not satisfied with claim of assessee. This is during assessment, i. e., after tax audit is completed. Hence, tax auditor to verify inadmissible expenditure as determined by the assessee

Rule 8D does not mandate that assessee should compute inadmissible amount under that rule

Tax auditor to examine details and verify with reference to established principles of allocation of expenditure

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

29

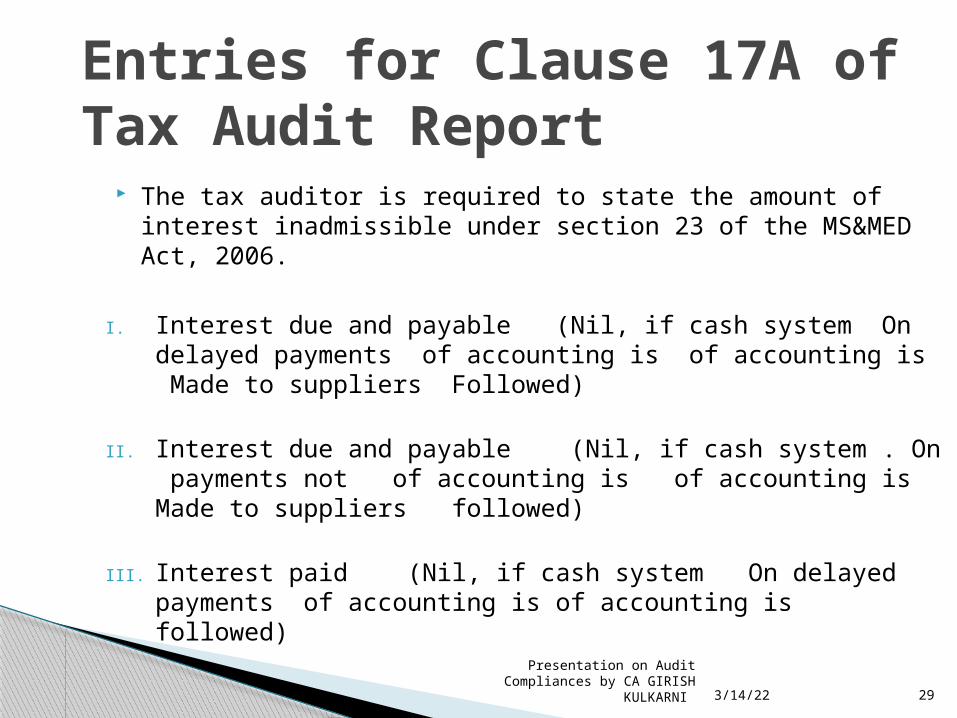

Entries for Clause 17A of Tax Audit Report

The tax auditor is required to state the amount of interest inadmissible under section 23 of the MS&MED Act, 2006.

I. Interest due and payable (Nil, if cash system On delayed payments of accounting is of accounting is Made to suppliers Followed)

II. Interest due and payable (Nil, if cash system . On payments not of accounting is of accounting is Made to suppliers followed)

III. Interest paid (Nil, if cash system On delayed payments of accounting is of accounting is followed)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

30

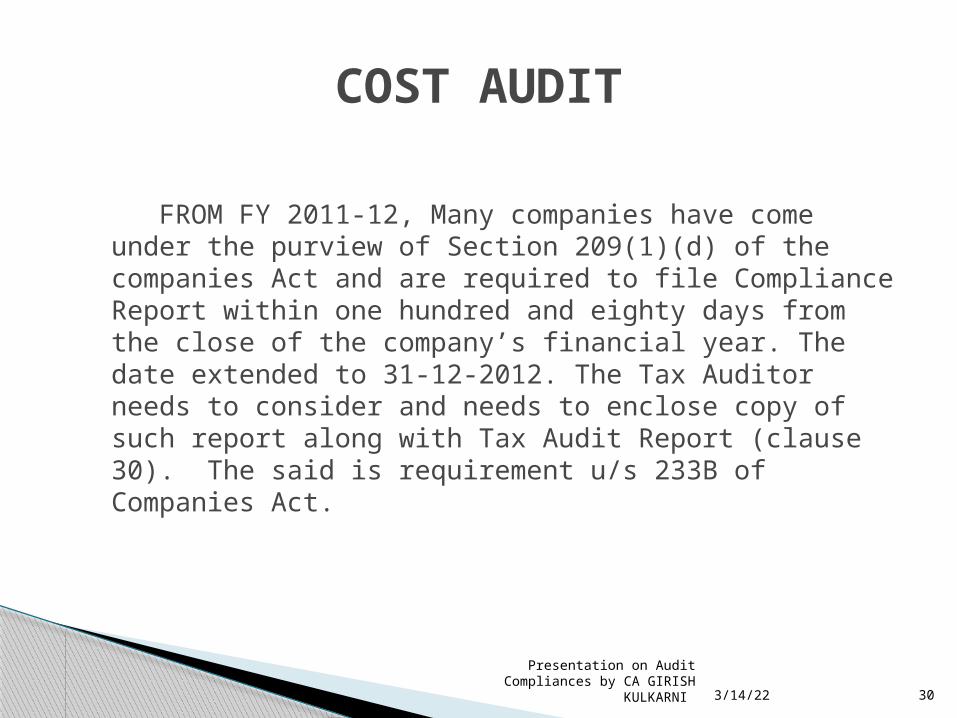

FROM FY 2011-12, Many companies have come under the purview of Section 209(1)(d) of the companies Act and are required to file Compliance Report within one hundred and eighty days from the close of the company’s financial year. The date extended to 31-12-2012. The Tax Auditor needs to consider and needs to enclose copy of such report along with Tax Audit Report (clause 30). The said is requirement u/s 233B of Companies Act.

COST AUDIT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

31

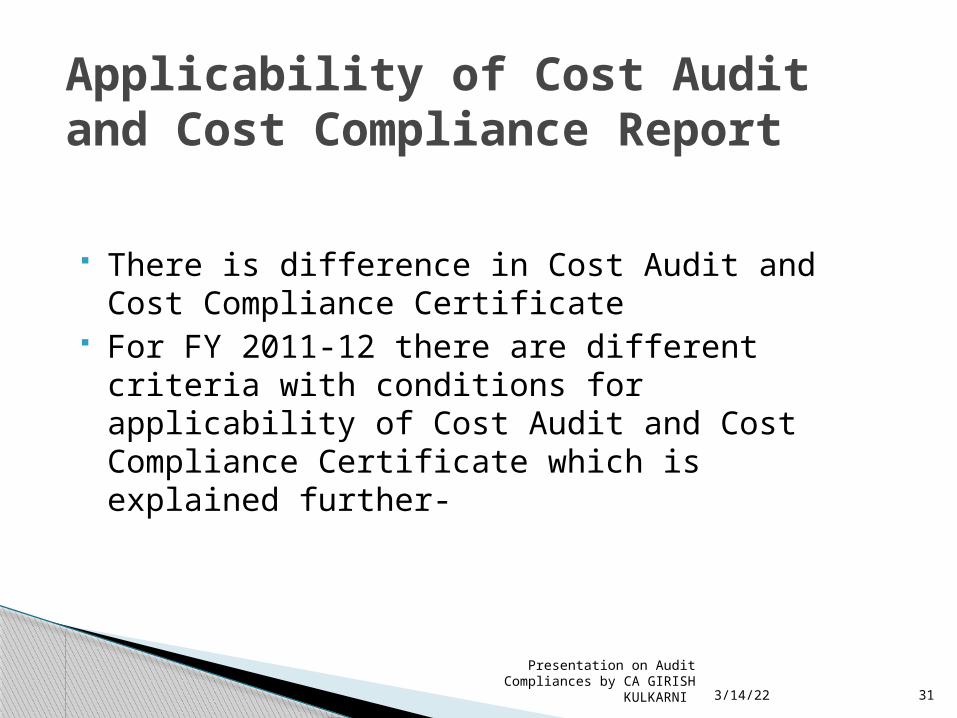

There is difference in Cost Audit and Cost Compliance Certificate

For FY 2011-12 there are different criteria with conditions for applicability of Cost Audit and Cost Compliance Certificate which is explained further-

Applicability of Cost Audit and Cost Compliance Report

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

32

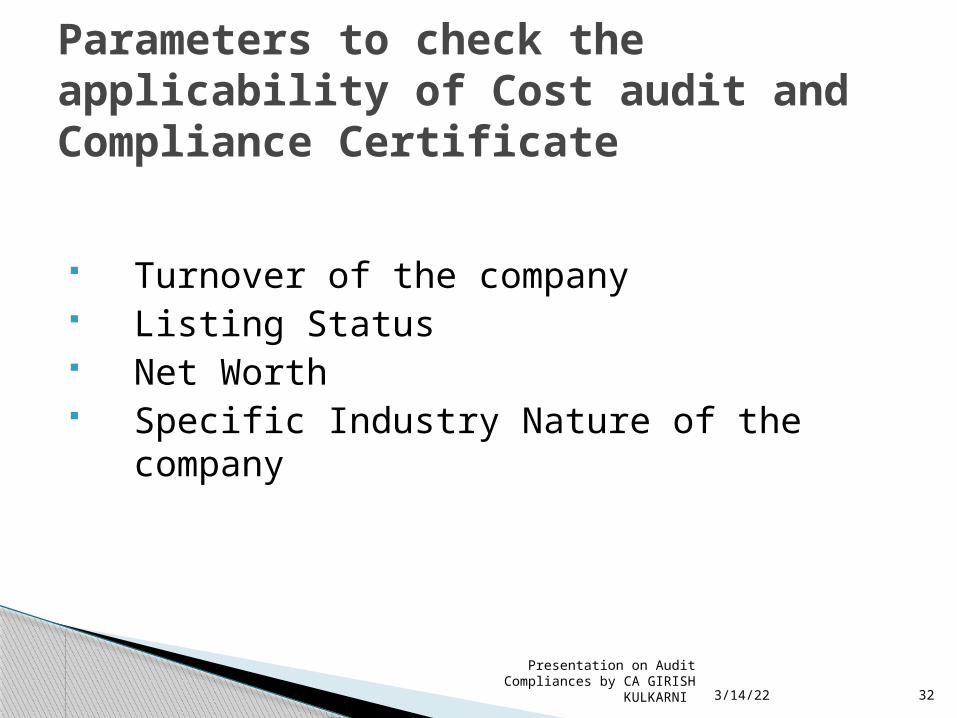

Turnover of the company Listing Status Net Worth Specific Industry Nature of the company

Parameters to check the applicability of Cost audit and Compliance Certificate

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

33

`33

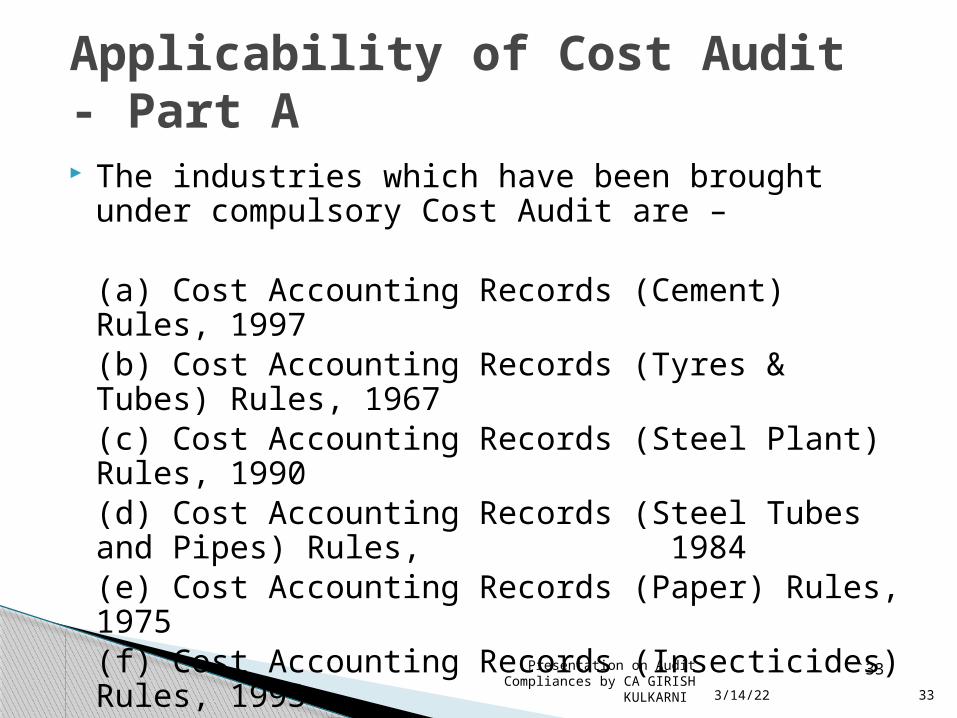

The industries which have been brought under compulsory Cost Audit are –

(a) Cost Accounting Records (Cement) Rules, 1997(b) Cost Accounting Records (Tyres & Tubes) Rules, 1967(c) Cost Accounting Records (Steel Plant) Rules, 1990(d) Cost Accounting Records (Steel Tubes and Pipes) Rules, 1984(e) Cost Accounting Records (Paper) Rules, 1975(f) Cost Accounting Records (Insecticides) Rules, 1993

Refer CAB Order [F. No. 52/26/CAB-2010], dated 2-5-2011

Applicability of Cost Audit - Part A

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

34

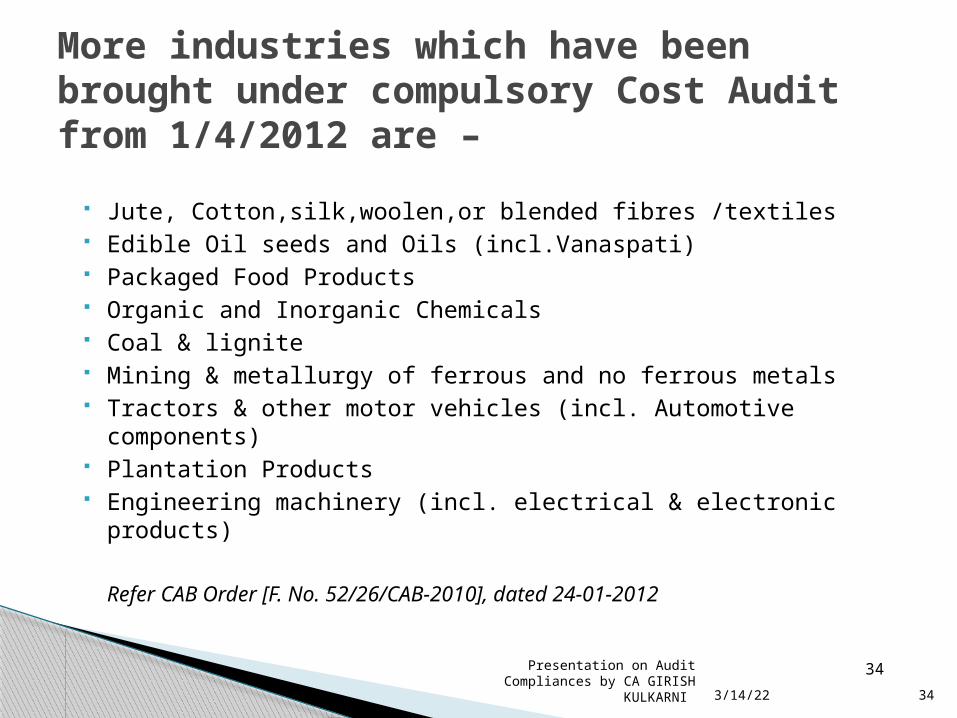

Jute, Cotton,silk,woolen,or blended fibres /textiles Edible Oil seeds and Oils (incl.Vanaspati) Packaged Food Products Organic and Inorganic Chemicals Coal & lignite Mining & metallurgy of ferrous and no ferrous metals Tractors & other motor vehicles (incl. Automotive components) Plantation Products Engineering machinery (incl. electrical & electronic products)

Refer CAB Order [F. No. 52/26/CAB-2010], dated 24-01-2012

More industries which have been brought under compulsory Cost Audit from 1/4/2012 are –

34

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

35

35

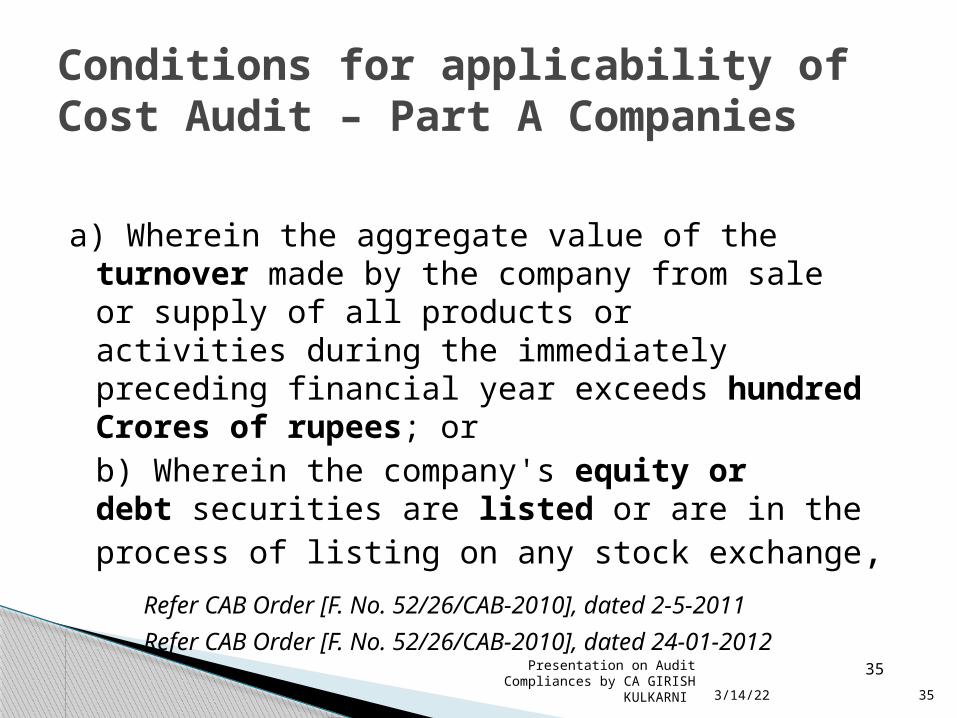

a) Wherein the aggregate value of the turnover made by the company from sale or supply of all products or activities during the immediately preceding financial year exceeds hundred Crores of rupees; orb) Wherein the company's equity or debt securities are listed or are in the process of listing on any stock exchange,

Refer CAB Order [F. No. 52/26/CAB-2010], dated 2-5-2011

Refer CAB Order [F. No. 52/26/CAB-2010], dated 24-01-2012

Conditions for applicability of Cost Audit – Part A Companies

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

36

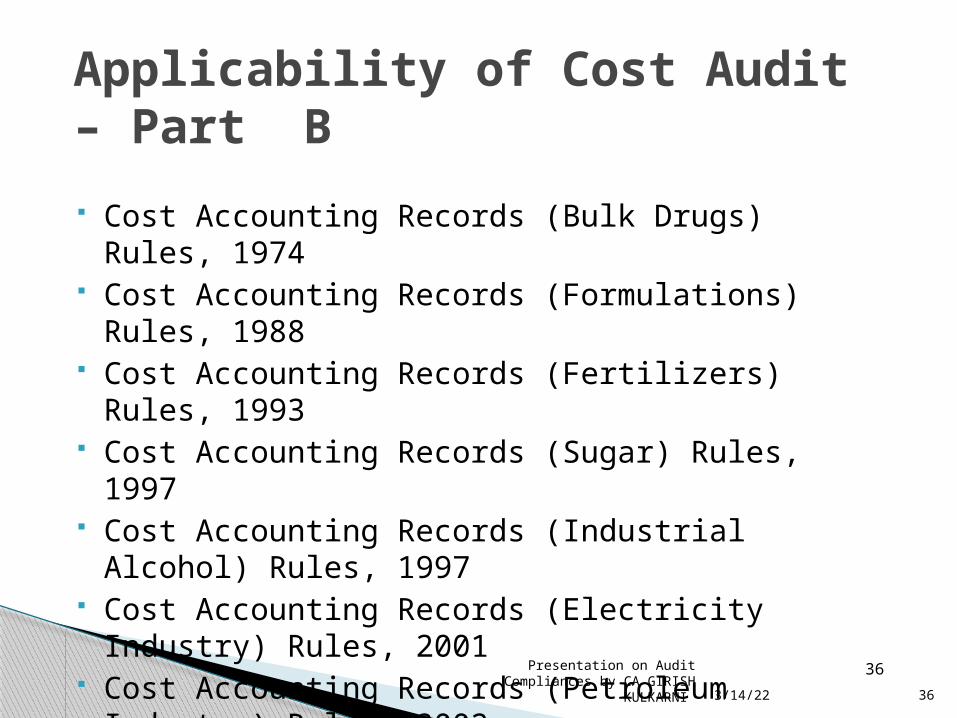

Cost Accounting Records (Bulk Drugs) Rules, 1974 Cost Accounting Records (Formulations) Rules, 1988 Cost Accounting Records (Fertilizers) Rules, 1993 Cost Accounting Records (Sugar) Rules, 1997 Cost Accounting Records (Industrial Alcohol) Rules, 1997 Cost Accounting Records (Electricity Industry) Rules, 2001 Cost Accounting Records (Petroleum Industry) Rules, 2002 Cost Accounting Records (Telecommunications) Rules, 2002

Refer CAB Order [F. No. 52/26/CAB-2010], dated 2-5-2011

Applicability of Cost Audit – Part B

36

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

37

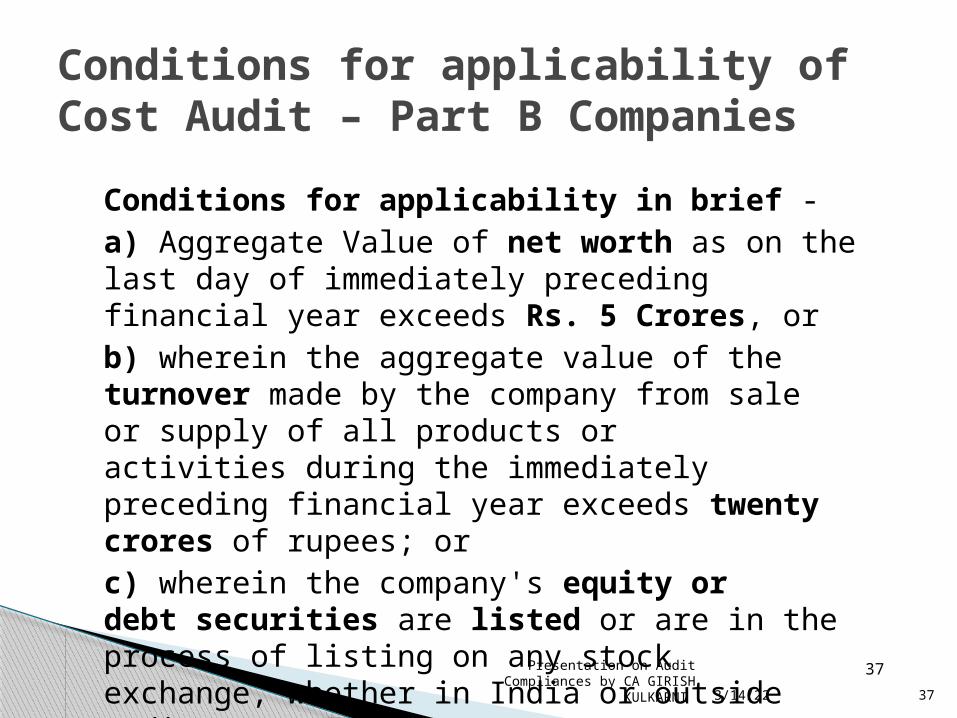

Conditions for applicability in brief - a) Aggregate Value of net worth as on the last day of immediately preceding financial year exceeds Rs. 5 Crores, orb) wherein the aggregate value of the turnover made by the company from sale or supply of all products or activities during the immediately preceding financial year exceeds twenty crores of rupees; orc) wherein the company's equity or debt securities are listed or are in the process of listing on any stock exchange, whether in India or outside India

Refer CAB Order [F. No. 52/26/CAB-2010], dated 2-5-2011

Conditions for applicability of Cost Audit – Part B Companies

37

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

38

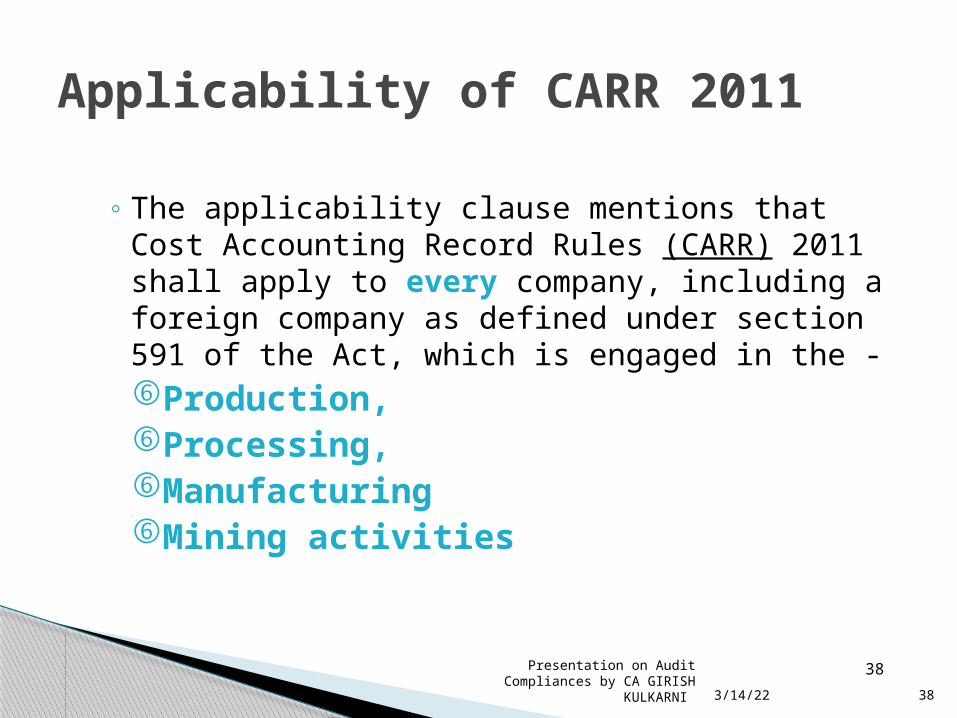

◦ The applicability clause mentions that Cost Accounting Record Rules (CARR) 2011 shall apply to every company, including a foreign company as defined under section 591 of the Act, which is engaged in the -oProduction, oProcessing, oManufacturingoMining activities

Applicability of CARR 2011

38

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

39

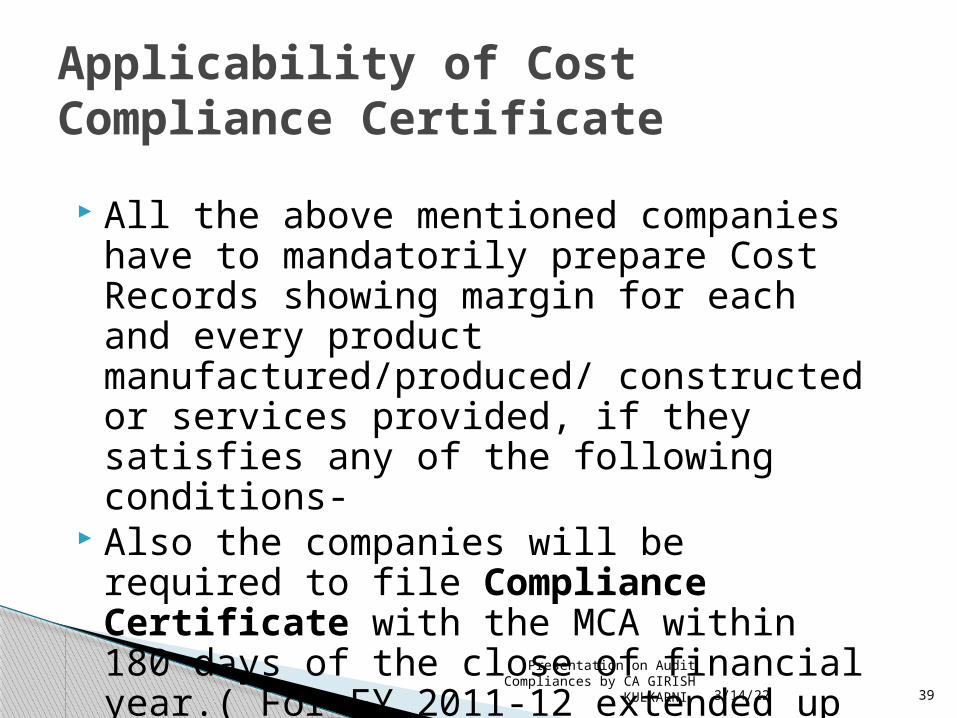

All the above mentioned companies have to mandatorily prepare Cost Records showing margin for each and every product manufactured/produced/ constructed or services provided, if they satisfies any of the following conditions-

Also the companies will be required to file Compliance Certificate with the MCA within 180 days of the close of financial year.( For FY 2011-12 extended up to 31-12-2012)

Applicability of Cost Compliance Certificate

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

40

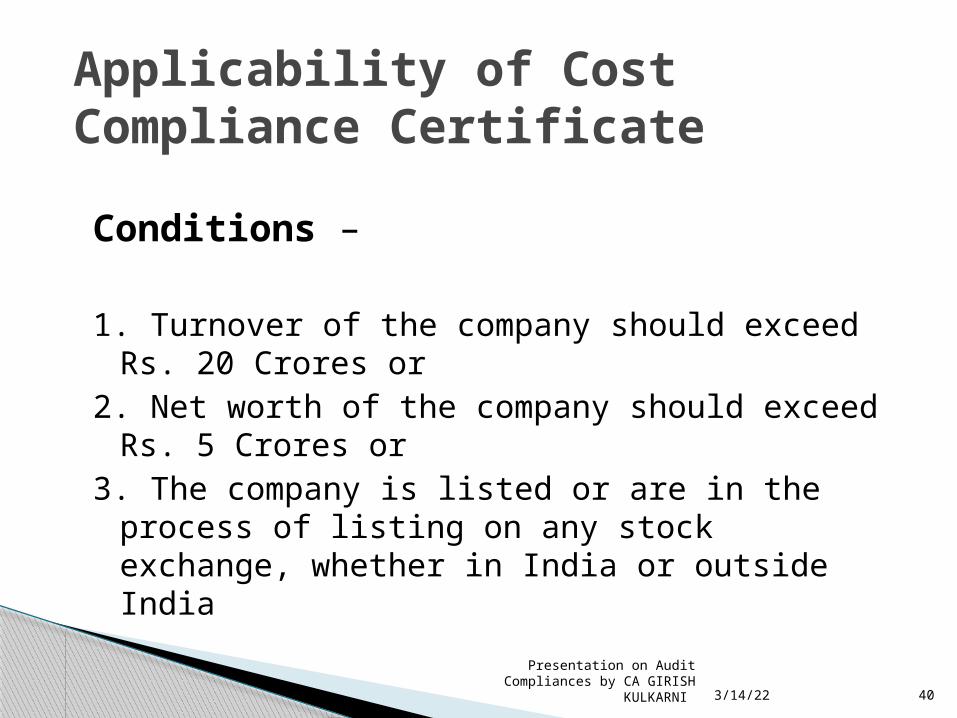

Conditions –

1. Turnover of the company should exceed Rs. 20 Crores or2. Net worth of the company should exceed Rs. 5 Crores or3. The company is listed or are in the process of listing on any

stock exchange, whether in India or outside India

Applicability of Cost Compliance Certificate

Presentation on Audit Compliances by CA GIRISH KULKARNI

41Apr 19, 202341

Basic requirements to be fulfilled while preparing Cost records

Now as all the old notifications with regard to cost records have been abolished, the companies are required to maintain the cost records in any formats provided the records are capable of filling in the information in formats as are required under Cost Audit Report Rules.

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

42

I. E-Filing of application (Form 23C) on MCA website. Filing to be done within 90 days from the commencement of each financial year i.e. by 29th of June

The following two documents needs to be filed along with form 23Ca. Certified copy of the Board Resolution proposing appointment of the cost auditor; andb. Copy of the certificate obtained from the cost auditor regarding compliance of section 224 (1-B) of the Companies Act, 1956.

ii. Now there is no need for the Central Government to accord approval for appointment of Cost Accountant, the appointment will be deemed to be approved unless any objection is received from Central Government within 30 days of filing the application

iii. The company has to issue formal letter of appointment after expiry of thirty days.

iv. The Cost Auditor has to file Form 23D with MCA within thirty days of receipt of formal letter of appointment

Procedure with regard to Appointment of Cost Auditor

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

43

Auditors Role

Auditor having consolidated all the findings, auditors should invest adequate time in reviewing these findings and should assess the impact of significant audit findings on opinion.

Having assessed the impact, if matter affects opinion, auditors should consider issuing report as per guidance i.e. qualified, disclaimer, and adverse.

If it does not affect opinion, auditor should assess whether

matter requires emphasis.

Auditor needs to change his role totally after Implementation of changed IFRS likely to heat by 1-4-2013 and Implementation of SA 700

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

44

Form an opinion on the Financial Statements(FS) based on an evaluation of the conclusions drawn from the audit evidence obtained

Express clearly the above opinion through a written report that also describes the basis for the opinion

Objectives of the Auditor

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

45

General Purpose FS includes Balance Sheet, Statement of Profit andLoss, Cash Flow Statement (where applicable) and statements andexplanatory notes which form part thereof, issued for the use ofvarious stakeholders, Government and their agencies and the Public

General purpose framework -A financial reporting framework designed to meet the common financial information needs of a wide range of users. The financial reporting framework may be a fair presentation framework or a compliance framework

Unmodified opinion – The opinion expressed by the auditor when theauditor concludes that the FS are prepared, in all material respects, inaccordance with the applicable financial reporting framework

Key Role in respect of Audit Report

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

46

Issues:

Notes to Accounts – What to include?

Accounting Policies considering Standards

Disclosure under various Accounting Standards

Changes in Accounting Policies, financial impact

Unusual Items / transactions, Prior period items

Management Representation Letter

Standards on Auditing

Changes in Reporting Format due to recent and upcoming changes in taxation and other laws

NOTES TO ACCOUNTS

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

47

1983 -APC (AUDITING PRACTICE COMMITTEE) WAS CONSTITUTED

1985-APC ISSUED FIRST STANDARD 2002-APC NAME CHANGED TO AUDITING AND

ASSURANCE STANDARD BOARD(AASB) AASB ISSUED 43 STANDARDS (AAS)

EVOLUTION OF AUDITING STANDARDS

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

48

Background worldwide and identify areas in which Standards on Quality Control, Engagement Standards and Statements on Auditing need to be developed.

Review existing Standards and Statements on Auditing to Assess their relevance in the changed conditions and to undertake their revision, if necessary. Formulate Engagement Standards, Standards on Quality Control and Statements on Auditing

OBJECTIVES OF AASB :

Review existing & Emerging auditing practices

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

49

ICAI has issued “Preface to the Standards on Quality Control, Auditing, Review, Other Assurance and Related Services”, which sets out the authority of the “Standards on Auditing (SAs)”.

All SAs interlinked - not to be implemented in isolation, but as a cohesive set of guidelines

Number given to SAs is similar to the numbering system followed for ISAs and at times the standards are also nearly similar.

Objective – help Auditor to reduce the risk of material misstatements to an acceptably low level

ICAI ON SAs

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

50

CORRESPONDING NEW NUMBERS FOR EACH AAS NUMBER.

THE PRINCIPLES AND PROCEDURES LAID DOWN IN THE RECLASSIFIED STANDARDS ARE IMPORTANT

RECLASSIFIED STANDARDS ON AUDITING SA , SAE , SRE , SRS

RECLASSIFICATION OF AAS IN TO SA, SAE, SRE AND SRS

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

51

SA-200-Basic Principles, Objective and Scope of Audit of Financial Statements

SA-210- Agreeing the Terms of Audit Engagements SA-230- Audit Documentation SA-240- Revised- Auditor’s Responsibilities Relating to Fraud SA-250- Revised- Auditor’s Responsibilities Relating to Laws and

Regulations SA-260- Revised- Communication with Those Charged with Governance SA-315- NEW STANDARD-VERY IMP.-Identifying and Assessing Risks of

Material Misstatements SA-320- Materiality in Planning and Performing an Audit SA-330- NEW STANDARD-VERY IMP-Auditor’s Responses to Assessed Risks SA-510- Initial Audit Engagements- Opening Balances SA-540- Auditing Accounting Estimates SA-550- Related Parties Continued on Next Page

RECLASSIFIED STANDARDS ON AUDITING(SA, SRE, SAE, SRS)

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

52

SA-560- Subsequent EventsSA-570- Going ConcernSA-580- Written RepresentationsSA-610- Using the Work of Internal AuditorsSA-620- Using the Work of an Auditor’s Expert SA-700- (AAS-28) – Auditor’s Report on Financial Statements SA-720- Auditor’s Responsibility in Relation to Other Information in Documents

SRS-4410- (AAS-31)- Engagements to compile Financial informationSRS-4400-(AAS-32)- Engagements to perform agreed upon proceduresSRE-2400-(AAS-33)- Engagements to Review financial statements

SAE-3400-(AAS-35)-Examination of prospective financial information

SQC-1- Standards on Quality Control Note: AAS-6, AAS-20, AAS-29 have been withdrawn due to issue of SA-315 and SA-

330

RECLASSIFIED STANDARDS ON AUDITINGContinued from last page

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

53

CHARTERED ACCOUNTANTS NEEDS TO FOLLOW SAs

04/19/2023CA GIRISH KULKARNI 54

Is compliance with all SAs required?

Basic obligation, comply with all SAs relevant to the audit.

Conditional requirements need not be applied if conditions do not exist

Not all SAs may be relevant SA 402, if SME does not use a service organization

SA 501, if SME does not have any inventory SA 600, if SME audit is not a group audit SA 610, if SME has no internal audit function

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

55

The report is signed by the auditor in his personal name. Where the firm is appointed as the auditor, the report is signed in the personal name of the auditor and

in the name of the audit firm. As per council decision on 13-1-2010 , The partner/proprietor signing the audit report also needs to

mention the membership number assigned by the Institute of Chartered Accountants of India. They also include the

registration number of the firm, wherever applicable, as allotted by ICAI, in the audit reports signed by them .”

The financial statements have been prepared by management of the entity in accordance with the financial reporting provisions established by a regulator (i.e., a special purpose framework) to meet the requirements of that regulator. Management does not have a choice of financial reporting frameworks.

The applicable financial reporting framework is a fair presentation framework.

The terms of the audit engagement reflect the description of management’s responsibility for the financial statements in SA 210 (Revised).

Distribution or use of the auditor’s report is not restricted.

SIGNIFICANT CHANGES RELATED TO SA

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

56

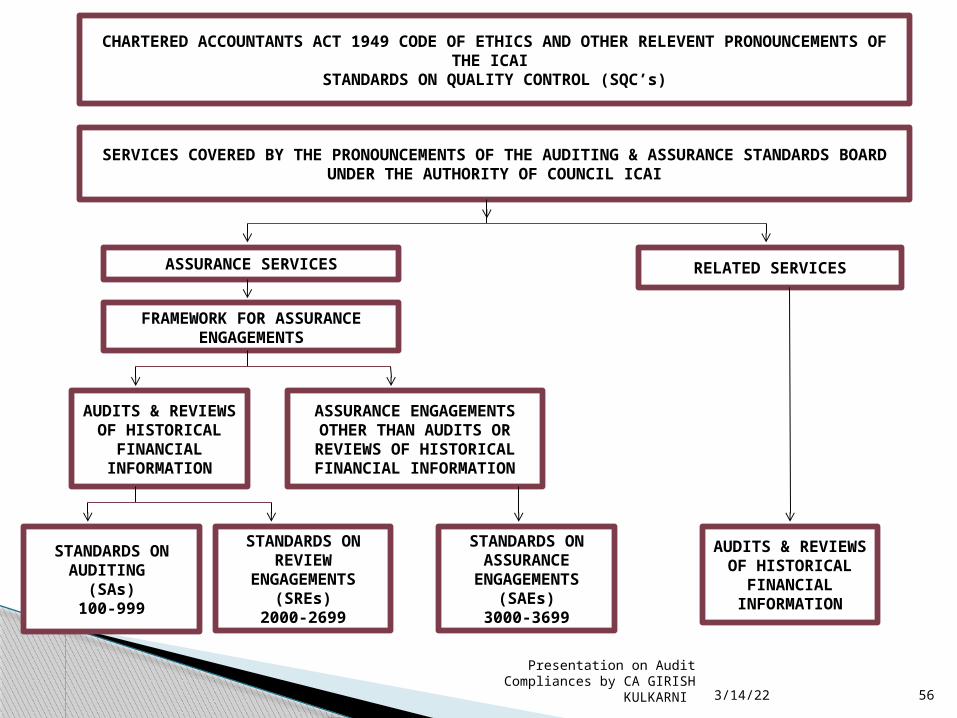

CHARTERED ACCOUNTANTS ACT 1949 CODE OF ETHICS AND OTHER RELEVENT PRONOUNCEMENTS OF THE ICAI

STANDARDS ON QUALITY CONTROL (SQC’s)

SERVICES COVERED BY THE PRONOUNCEMENTS OF THE AUDITING & ASSURANCE STANDARDS BOARD UNDER THE AUTHORITY OF COUNCIL ICAI

ASSURANCE SERVICES RELATED SERVICES

FRAMEWORK FOR ASSURANCE ENGAGEMENTS

AUDITS & REVIEWS OF HISTORICAL FINANCIAL

INFORMATION

ASSURANCE ENGAGEMENTS OTHER

THAN AUDITS OR REVIEWS OF HISTORICAL FINANCIAL INFORMATION

STANDARDS ON AUDITING

(SAs)100-999

STANDARDS ON REVIEW

ENGAGEMENTS(SREs)

2000-2699

STANDARDS ON ASSURANCE

ENGAGEMENTS(SAEs)

3000-3699

AUDITS & REVIEWS OF HISTORICAL FINANCIAL

INFORMATION

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

57

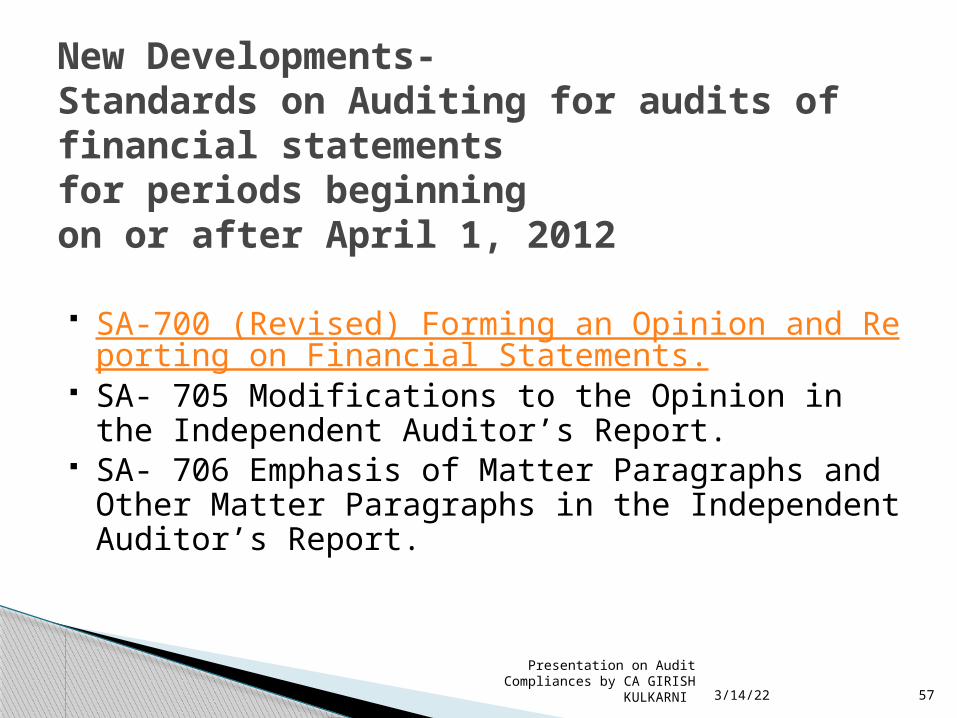

SA-700 (Revised) Forming an Opinion and Reporting on Financial Statements.

SA- 705 Modifications to the Opinion in the Independent Auditor’s Report.

SA- 706 Emphasis of Matter Paragraphs and Other Matter Paragraphs in the Independent Auditor’s Report.

New Developments-Standards on Auditing for audits of financial statements for periods beginning on or after April 1, 2012

04/19/2023CA GIRISH KULKARNI 58

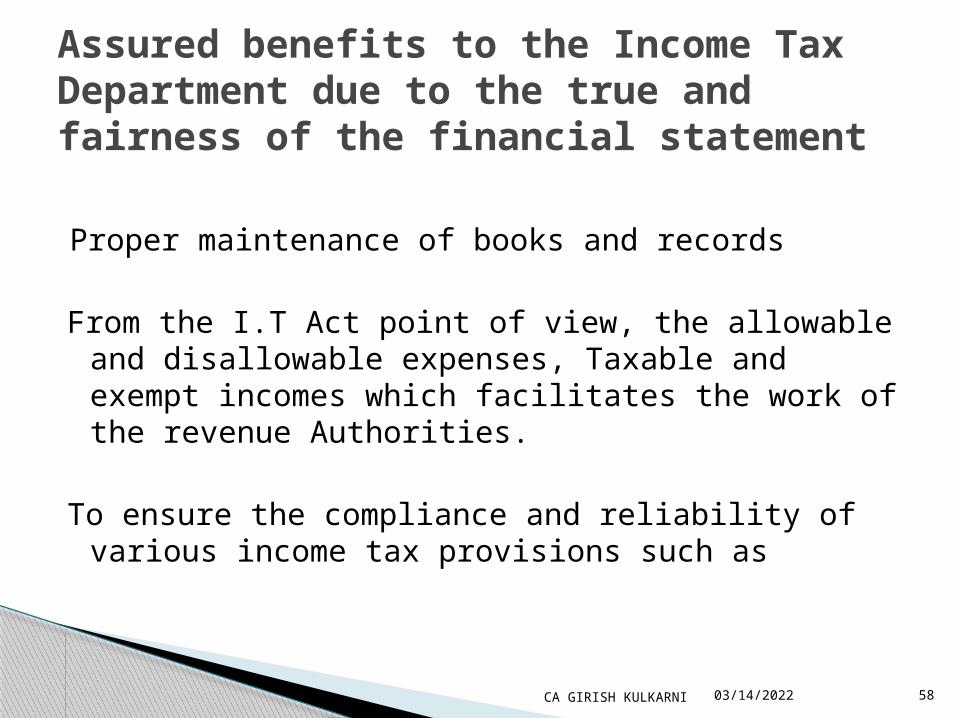

Assured benefits to the Income Tax Department due to the true and fairness of the financial statement

Proper maintenance of books and records

From the I.T Act point of view, the allowable and disallowable expenses, Taxable and exempt incomes which facilitates the work of the revenue Authorities.

To ensure the compliance and reliability of various income tax provisions such as

04/19/2023CA GIRISH KULKARNI 59

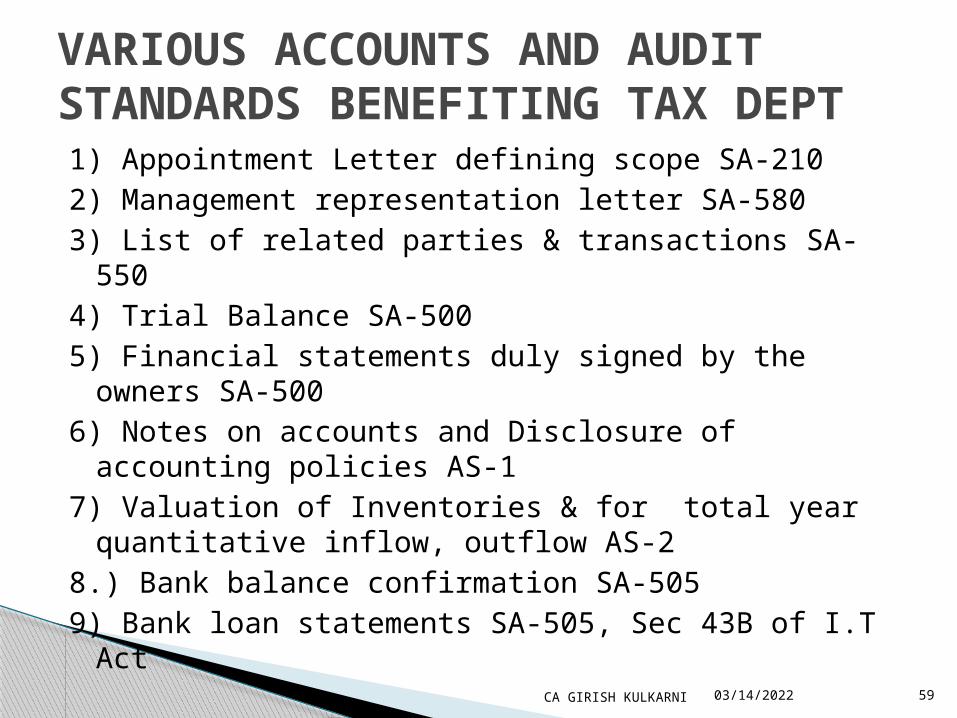

VARIOUS ACCOUNTS AND AUDIT STANDARDS BENEFITING TAX DEPT 1) Appointment Letter defining scope SA-2102) Management representation letter SA-5803) List of related parties & transactions SA-5504) Trial Balance SA-5005) Financial statements duly signed by the owners SA-

5006) Notes on accounts and Disclosure of accounting

policies AS-17) Valuation of Inventories & for total year quantitative

inflow, outflow AS-28.) Bank balance confirmation SA-5059) Bank loan statements SA-505, Sec 43B of I.T Act

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

60

10) Major sundry debtors and creditors balance confirmation SA-505

11) Analytical Ratio analysis SA-52012) Sample purchase and sales bills SA-50013) Proof of assets purchased & revenue expenditure SA-

500,Sec 36(1)(iii) & 43A of I.T Act.14) Extraordinary Items nature & disclosure SA-50015) Notes on the nature of business SA-31016) Depreciation calculation statement AS-6, Sec 32 of I.T Act17) Liabilities including contingent liabilities estimation A.S 29

with detailed working18) Statutory Compliances Relevant P.F, ESI, Bonus, VAT Act’s

provisions

VARIOUS ACCOUNTS AND AUDIT STANDARDS BENEFITING TAX DEPT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

61

The Primary responsibility of Auditor is to certify as to reliability of the books of accounts and other records are properly maintained, with the assertion that Profit & Loss Account and Balance sheet give a true and fair view of state of Affairs of the Assessee. Hence CA doing audit is responsible.

Clause (xxi) of Paragraph 4 of the Companies (Auditor’s Report) Order, 2003 further requires the auditor to specifically report “whether any fraud on or by the entity has been noticed or reported during the year; if yes, the nature and amount involved is to be indicated”

1277 VAT HAWALA DEALER FRAUDS or MATERIAL FRAUDS–SA 315 & SA 330 TO DEALT

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

62

Overall Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with Standards on Auditing states ‘In conducting an audit of financial statements, the overall objectives of the auditor are

To obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, thereby enabling the auditor to express an opinion on whether the financial statements are prepared, in all material respects, in accordance with an applicable financial reporting framework’

Para 11 of SA 200 (Revised) : :-

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

63

Para A5:- identifies Fraud to include ‘Causing an entity to pay for goods and services not received (for example, payments to fictitious vendors, kickbacks paid by vendors to the entity’s purchasing agents in return for inflating prices, payments to fictitious employees).’

Para A18:- Professional skepticism includes being alert to, for example: ♦ Audit evidence that contradicts other audit evidence obtained. ♦ Information that brings into question the reliability of documents and responses to

inquiries to be used as audit evidence. ♦ Conditions that may indicate possible fraud. ♦ Circumstances that suggest the need for audit procedures in addition to those required

by the SAs. Para A21 :- The auditor may accept records and documents as genuine unless the auditor

has reason to believe the contrary. the SAs require that the auditor investigate further and determine what modifications or additions to audit procedures are necessary to resolve the matter.

Thus, Such Frauds are already known and expected to be known to Auditors and hence he

is expected to exercise Professional Skepticism while using the information available publically relating to Suspicious Dealers on Vat Website.

Extracts from SA 240 (Revised):

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

64

Auditor may inquire with Management and also evaluate internal controls relating to purchases cycle.

Auditor may consider verifying Purchase Invoice, Delivery Challan/ Transporters Copy, Mode of Payment to such Vendor.

If Stock Register is maintained, Auditor may consider verifying whether such goods are reflected as Purchase in such Stock Register.

If Stock Register is maintained, Auditor may consider verifying the consumption of such Raw material in course of manufacturing activity or Sold/ issued to whom in course of business.

If such purchase forms part of Inventory, Then Auditor can be present at Inventory physical counting.

The Auditor may also resort to method of obtaining External Confirmations Procedures as per SA 505 (Revised).

The Auditor should also consider to obtain a Representation from Management with respect to such Purchases.

FAKE OR GENUNINE TRANSACTION –TO CONFIRM AUDITOR CAN AUDIT AS UNDER

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

65

Notification Date 28 February 2011

Effective Date 1 April 2011

Applicable to the financial statements to be prepared for the

Financial Year commencing on or after 1 April 2011

No provision in the notification for early application

New Schedule VI Revised

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

66

Schedule VI format and disclosures shall yield to Accounting standards and the requirements of the Act.

Financial statements vertical format mandatory. Clear mandate on disclosure

◦ on the face of financial statements and ◦ In the accompanying notes

Certain accounting terms defined in the schedule. The non-defined terms shall have the meaning as per the

accounting standards. Separate head for Share application money pending allotment Liabilities to be classified as Current and Non-current liabilities

◦ Creditors may be classified as Non-current liabilities in certain circumstances

Schedules to the Financial Statements to be given as notes to accounts

Conceptual Changes

Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

67

Notes to accounts shall contain information in addition to that presented in the Financial Statements and shall provide where required◦ Narrative descriptions or disaggregation of items recognized in those statements

and◦ Information about items that do not qualify for recognition in those statements.

Each item on the face of the Balance Sheet and Statement of Profit and Loss shall be cross-referenced to any related information in the notes to accounts.

In preparing the Financial Statements including the notes to accounts, a balance shall be maintained between◦ providing excessive detail that may not assist users of financial statements and◦ not providing important information as a result of too much aggregation.

Notes to accounts

Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

68

Comparatives for the immediately preceding year to be given for all items shown in Financial Statements including notes

Depending upon the turnover of the company, the figures appearing in the Financial Statements may be rounded off as below :

Turnover Rounding offLess than one hundred crore To the nearest hundreds, thousands,rupees lakhs or millions, or decimals thereof.

one hundred crore rupees or To the nearest lakhs, millions or crores,more or decimals thereof.

Rounding off is optional.

Comparatives and Rounding off

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

69

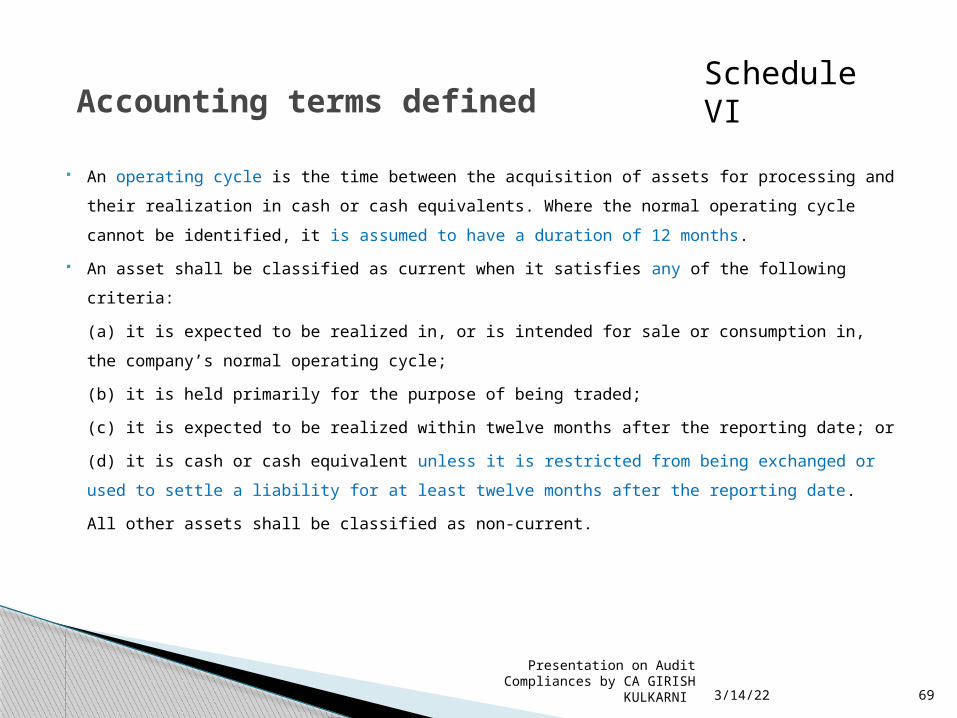

An operating cycle is the time between the acquisition of assets for processing and

their realization in cash or cash equivalents. Where the normal operating cycle

cannot be identified, it is assumed to have a duration of 12 months.

An asset shall be classified as current when it satisfies any of the following criteria:

(a) it is expected to be realized in, or is intended for sale or consumption in, the

company’s normal operating cycle;

(b) it is held primarily for the purpose of being traded;

(c) it is expected to be realized within twelve months after the reporting date; or

(d) it is cash or cash equivalent unless it is restricted from being exchanged or used

to settle a liability for at least twelve months after the reporting date.

All other assets shall be classified as non-current.

Accounting terms definedSchedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

70

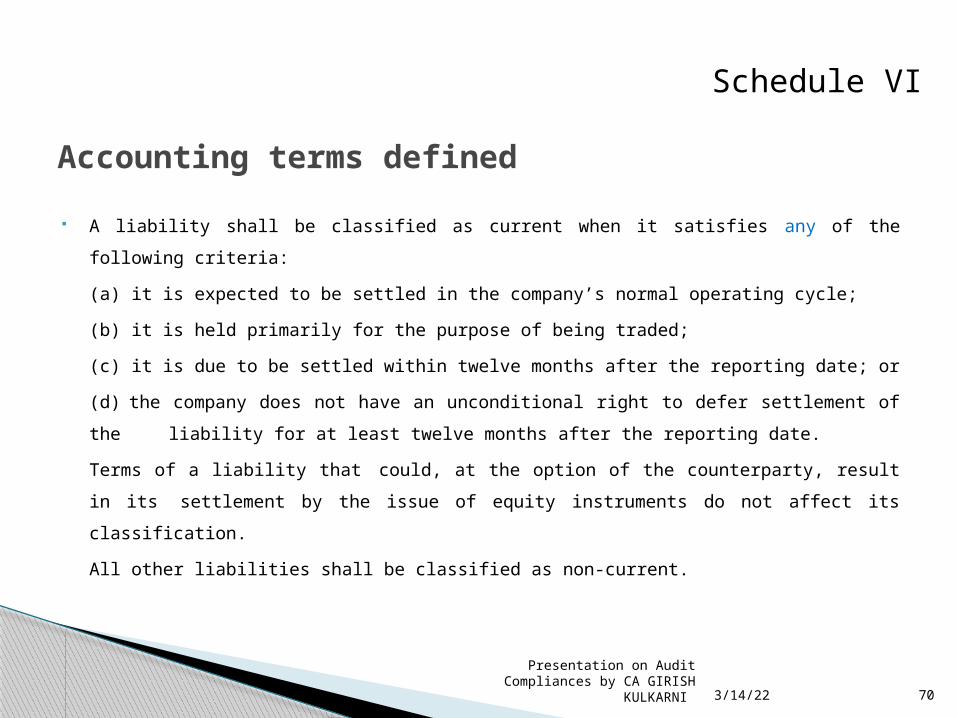

A liability shall be classified as current when it satisfies any of the following criteria:

(a) it is expected to be settled in the company’s normal operating cycle;

(b) it is held primarily for the purpose of being traded;

(c) it is due to be settled within twelve months after the reporting date; or

(d) the company does not have an unconditional right to defer settlement of

the liability for at least twelve months after the reporting date.

Terms of a liability that could, at the option of the counterparty, result

in its settlement by the issue of equity instruments do not affect its

classification.

All other liabilities shall be classified as non-current.

Accounting terms defined

Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

71

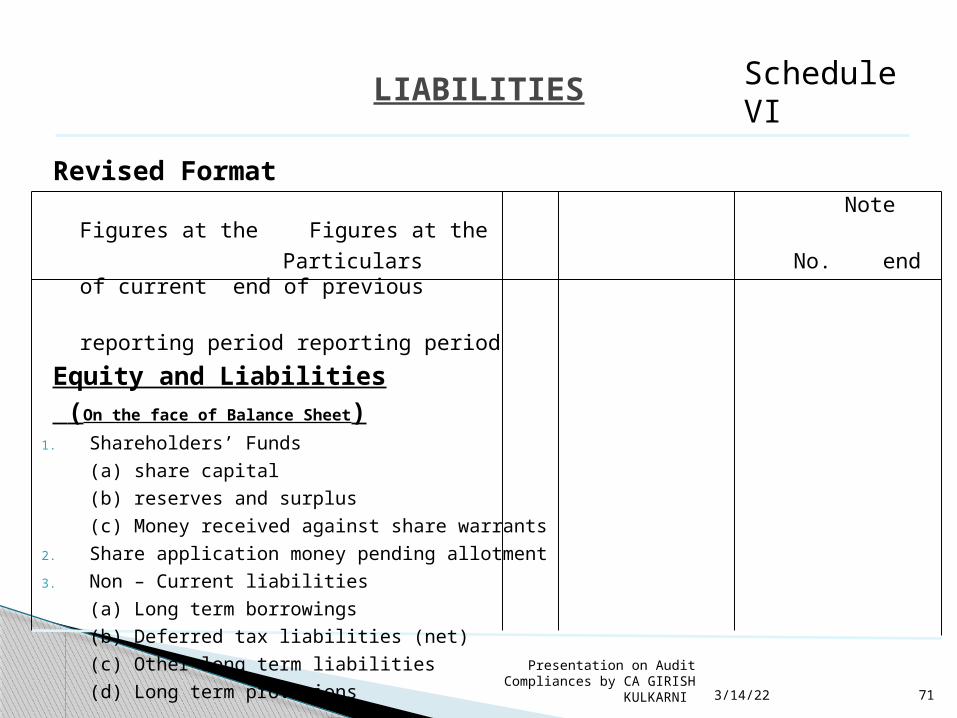

Revised Format Note Figures at the Figures at the Particulars No. end of current end of previous reporting period reporting period

Equity and Liabilities (On the face of Balance Sheet)

1. Shareholders’ Funds

(a) share capital

(b) reserves and surplus

(c) Money received against share warrants

2. Share application money pending allotment

3. Non – Current liabilities

(a) Long term borrowings

(b) Deferred tax liabilities (net)

(c) Other long term liabilities

(d) Long term provisions

LIABILITIES Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

72

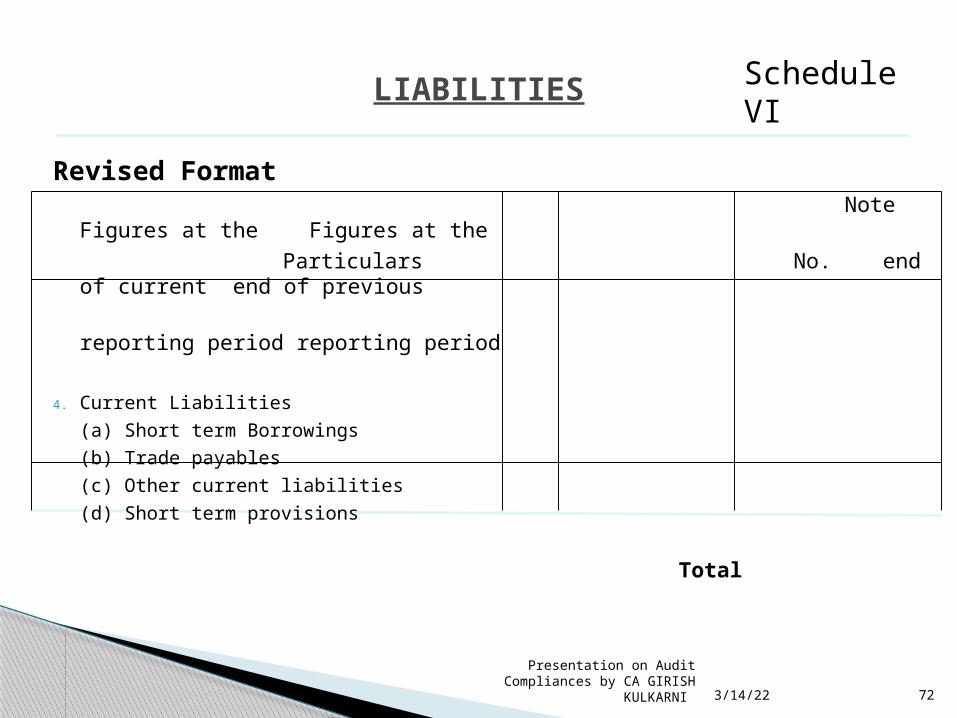

Revised Format Note Figures at the Figures at the Particulars No. end of current end of previous reporting period reporting period

4. Current Liabilities

(a) Short term Borrowings

(b) Trade payables

(c) Other current liabilities

(d) Short term provisions

Total

LIABILITIES Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

73

Revised Format Note Figures at the Figures at the Particulars No. end of current end of previous reporting period reporting period

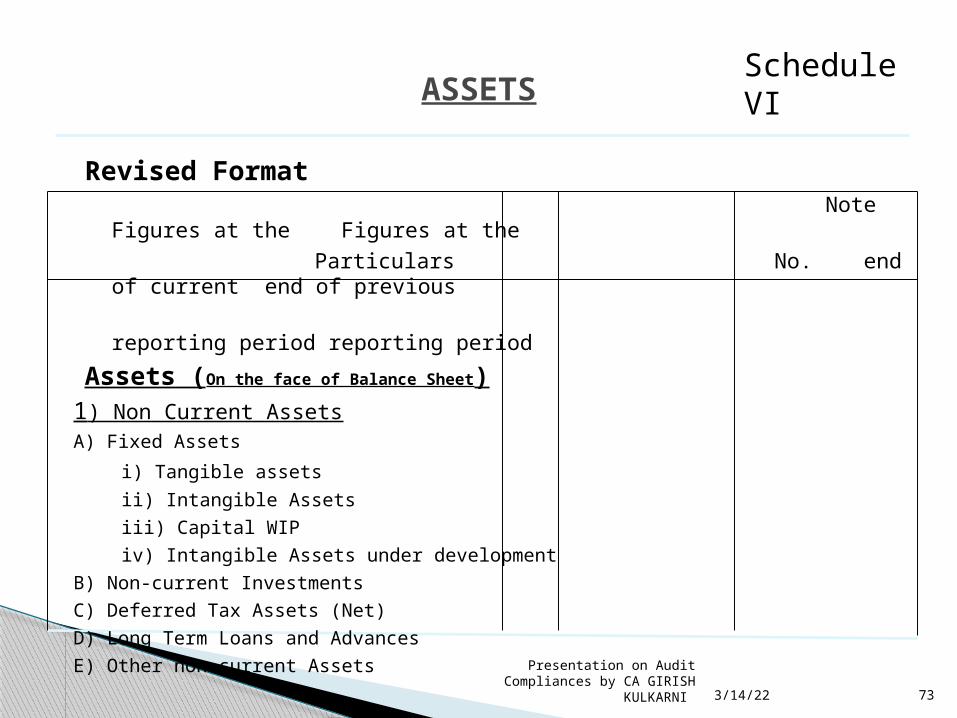

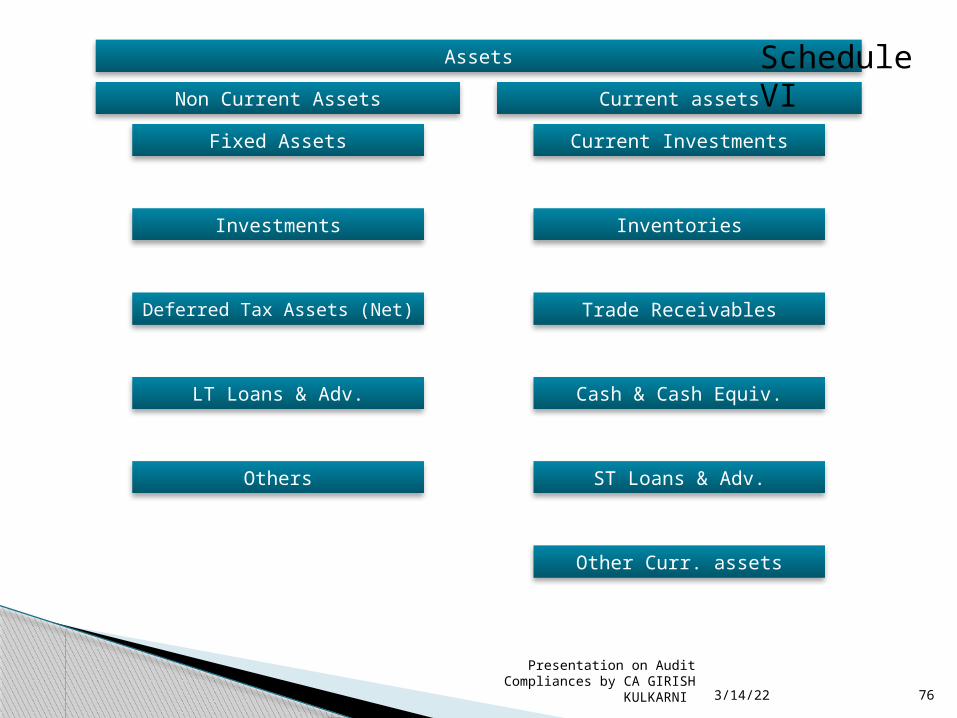

Assets (On the face of Balance Sheet)1) Non Current AssetsA) Fixed Assets

i) Tangible assets

ii) Intangible Assets

iii) Capital WIP

iv) Intangible Assets under development

B) Non-current Investments

C) Deferred Tax Assets (Net)

D) Long Term Loans and Advances

E) Other non-current Assets

ASSETSSchedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

74

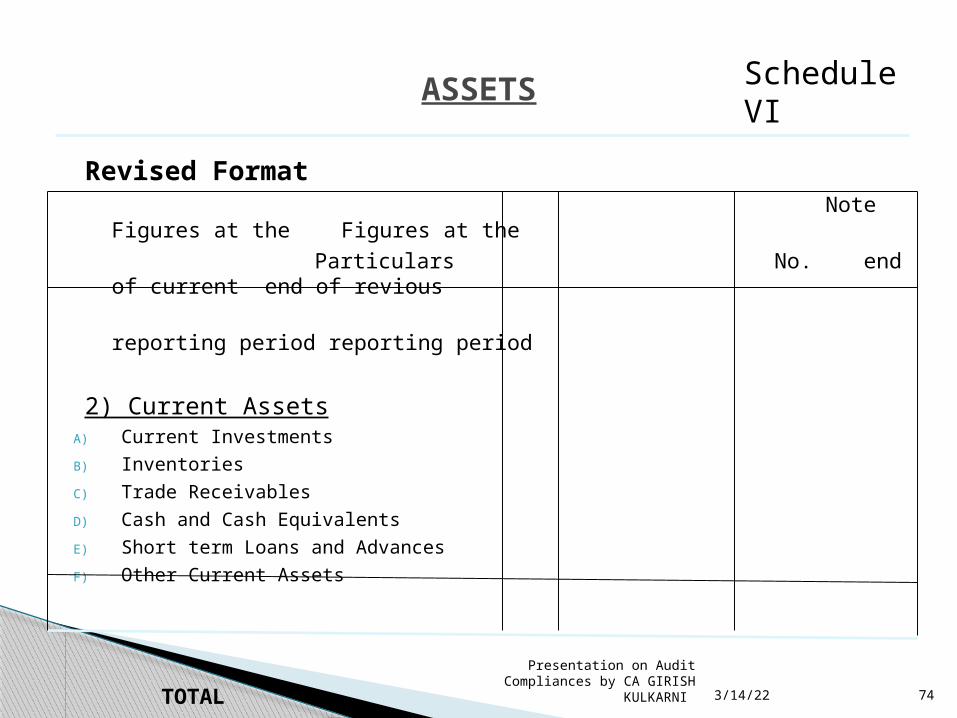

Revised Format Note Figures at the Figures at the Particulars No. end of current end of revious reporting period reporting period

2) Current AssetsA) Current Investments

B) Inventories

C) Trade Receivables

D) Cash and Cash Equivalents

E) Short term Loans and Advances

F) Other Current Assets

TOTAL

ASSETS Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

75

Equity and liabilities

Shareholders’ Funds

Share Capital

Reserves and surplus

Money received against share warrants

Share application money pending allotment

Non – current liabilities

Long term borrowings

Deferred tax liabilities (net)

Other long term liabilities

Long term provisions

Current Liabilities

Short term borrowings

Trade payables

Other current liabilities

Short-term provisions

Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

76

Assets

Non Current Assets

Fixed Assets

Investments

Deferred Tax Assets (Net)

LT Loans & Adv.

Others

Current assets

Current Investments

Inventories

Trade Receivables

Cash & Cash Equiv.

ST Loans & Adv.

Other Curr. assets

Schedule VI

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

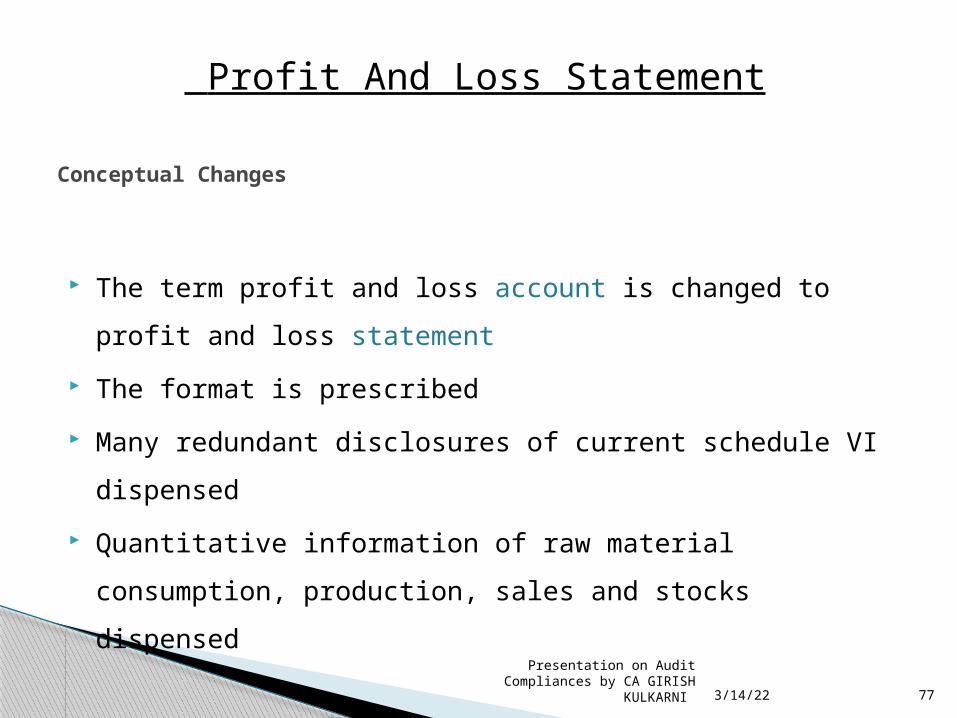

The term profit and loss account is changed to profit and

loss statement

The format is prescribed

Many redundant disclosures of current schedule VI

dispensed

Quantitative information of raw material consumption,

production, sales and stocks dispensed

Conceptual Changes

Profit And Loss Statement

77

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

Note Figures for Figures for No. Current previous reporting reporting

period period

I) Revenue From Operations II) Other incomes

Total Revenue

III) Expenses Cost of Materials Consumed Purchases of Stock in trade Changes in Inventories of finished goods,

WIP,and stock in trade Employee benefits expenses Finance Cost Depreciation and Amortization Exp Other Expenses

Total Expenses

Profit & Loss Statement

78

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

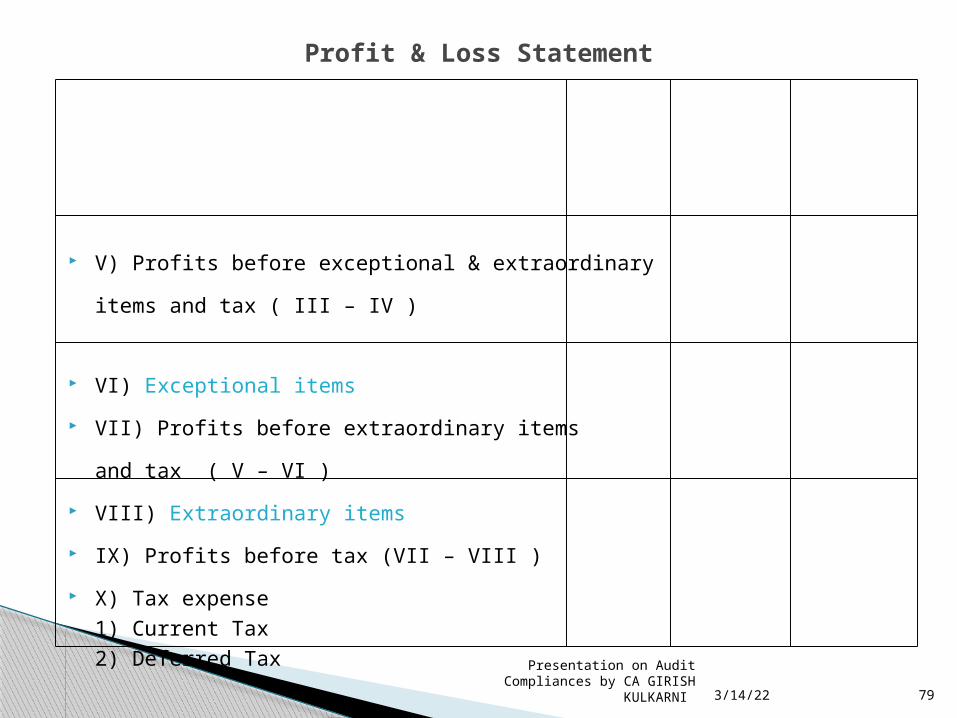

V) Profits before exceptional & extraordinary

items and tax ( III – IV )

VI) Exceptional items

VII) Profits before extraordinary items

and tax ( V – VI )

VIII) Extraordinary items

IX) Profits before tax (VII – VIII )

X) Tax expense1) Current Tax2) Deferred Tax

Profit & Loss Statement

79

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

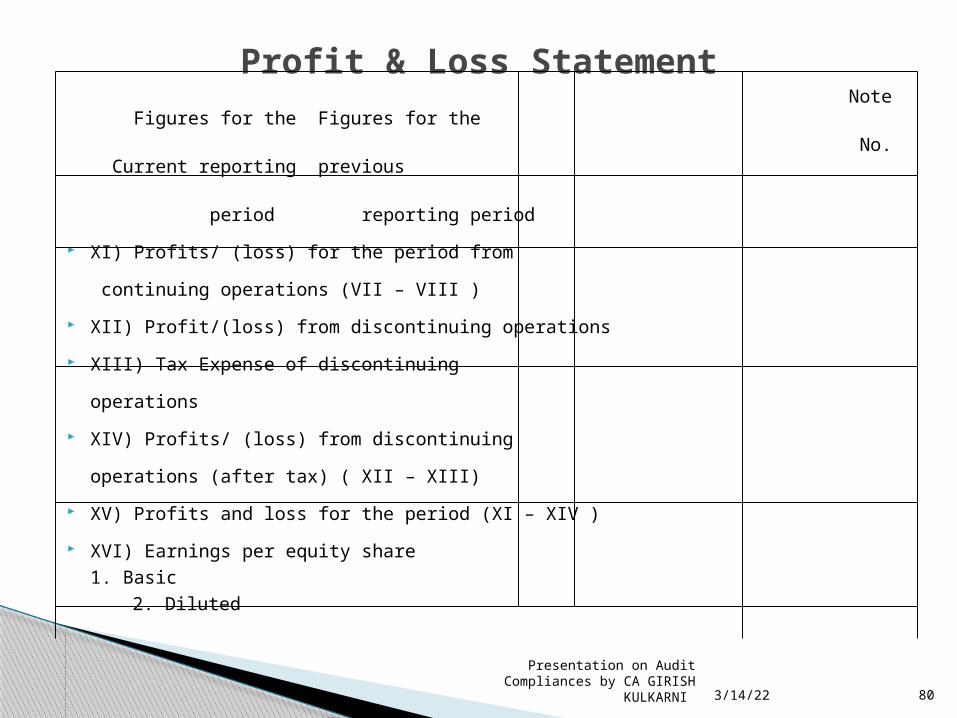

Note Figures for the Figures for the No. Current reporting previous period reporting period

XI) Profits/ (loss) for the period from

continuing operations (VII – VIII )

XII) Profit/(loss) from discontinuing operations

XIII) Tax Expense of discontinuing

operations

XIV) Profits/ (loss) from discontinuing

operations (after tax) ( XII – XIII)

XV) Profits and loss for the period (XI – XIV )

XVI) Earnings per equity share1. Basic

2. Diluted

Profit & Loss Statement

80

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

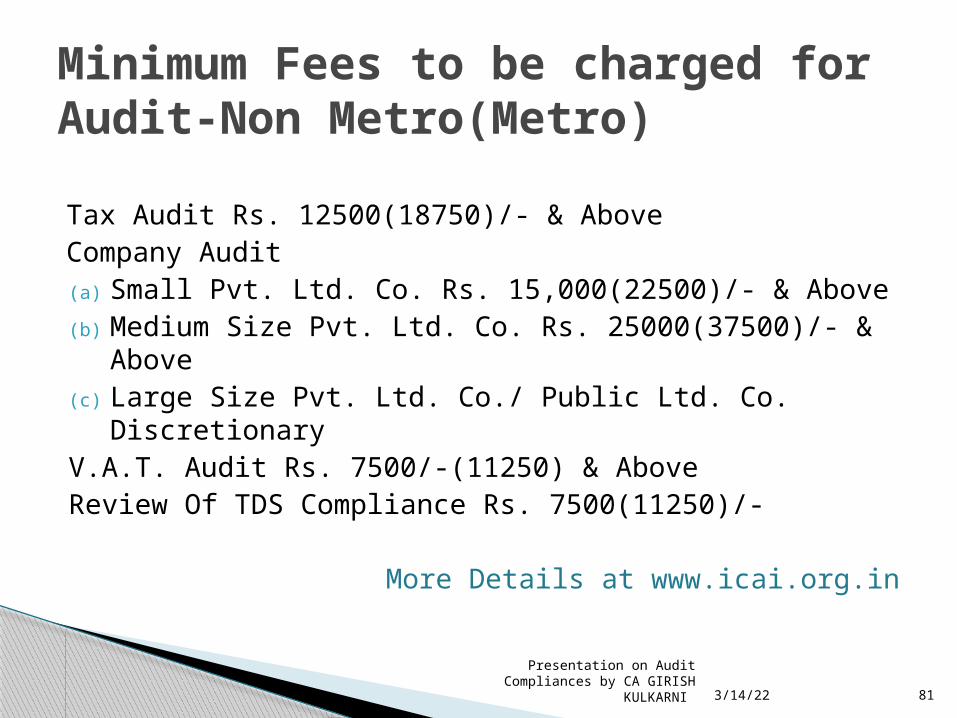

Tax Audit Rs. 12500(18750)/- & Above Company Audit (a) Small Pvt. Ltd. Co. Rs. 15,000(22500)/- & Above (b) Medium Size Pvt. Ltd. Co. Rs. 25000(37500)/- &

Above(c) Large Size Pvt. Ltd. Co./ Public Ltd. Co.

Discretionary V.A.T. Audit Rs. 7500/-(11250) & Above Review Of TDS Compliance Rs. 7500(11250)/-

More Details at www.icai.org.in

Minimum Fees to be charged for Audit-Non Metro(Metro)

81

Comments..?

Apr 19, 2023Presentation on Audit Compliances by CA GIRISH KULKARNI

T H A N K Y O U