by elias mossialos anna dixon josep figueras joe kutzin · taxation types of taxation: • direct...

TRANSCRIPT

The

Euro

pean

Obs

erva

tory

on

Hea

lth C

are

Syst

ems

is a

par

tner

ship

bet

wee

n th

e W

orld

Hea

lth O

rgan

izat

ion

Regi

onal

Offi

ce fo

r Eur

ope,

the

Gov

ernm

ent o

f Gre

ece,

the

Gov

ernm

ent

of N

orw

ay, t

he G

over

nmen

t of

Spa

in, t

he E

urop

ean

Inve

stm

ent

Bank

, the

Ope

n So

ciet

yIn

stitu

te, t

he W

orld

Ban

k, th

e Lo

ndon

Sch

ool o

f Eco

nom

ics

and

Polit

ical

Sci

ence

, and

the

Lond

on S

choo

l of H

ygie

ne &

Tro

pica

l Med

icin

e.

This

pol

icy

brie

f is

inte

nded

for p

olic

y-m

aker

s an

d th

ose

wor

king

on

fund

ing

optio

ns fo

r hea

lth c

are

syst

ems.

The

Euro

pea

n O

bse

rvat

ory

on H

ealt

h Ca

re S

yste

ms

WH

O R

egio

nal O

ffice

for E

urop

eSc

herf

igsv

ej 8

, DK-

2100

Cop

enha

gen

ØD

enm

ark

Tel.:

+45

39 1

7 13

63

Fax:

+45

39 1

7 18

18

E-m

ail:

obse

rvat

ory@

who

.dk

ww

w.o

bse

rvat

ory.

dk

European

Observatoryon Health Care Systems

Policy brief

Funding health care:options for Europe

No. 4 · 2002

by

Elias Mossialos

Anna Dixon

Josep Figueras

Joe Kutzin

Introduction

Health care systems face ever changing andoften competing demands for resources. Fora health care system to be sustainable it mustbe able to pay for investment in buildingsand equipment, training and remunerationof personnel and for drugs and other con-sumables. How these financial resources aregenerated and managed – the process of col-lecting revenue and pooling funds – raisesimportant issues for policy-makers andplanners. This policy brief aims to sum-marise these issues from an internationalperspective and consider how funding sys-tems can be designed in order to achievepolicy objectives. It looks first at the differ-ent sources of revenue and then at theimpact of different systems of funding onspecific objectives related to social policy,politics and economics. Finally, it considersimplementation issues and some of thewider dimensions that policy-makers needto consider.

What are the different sources of revenue?

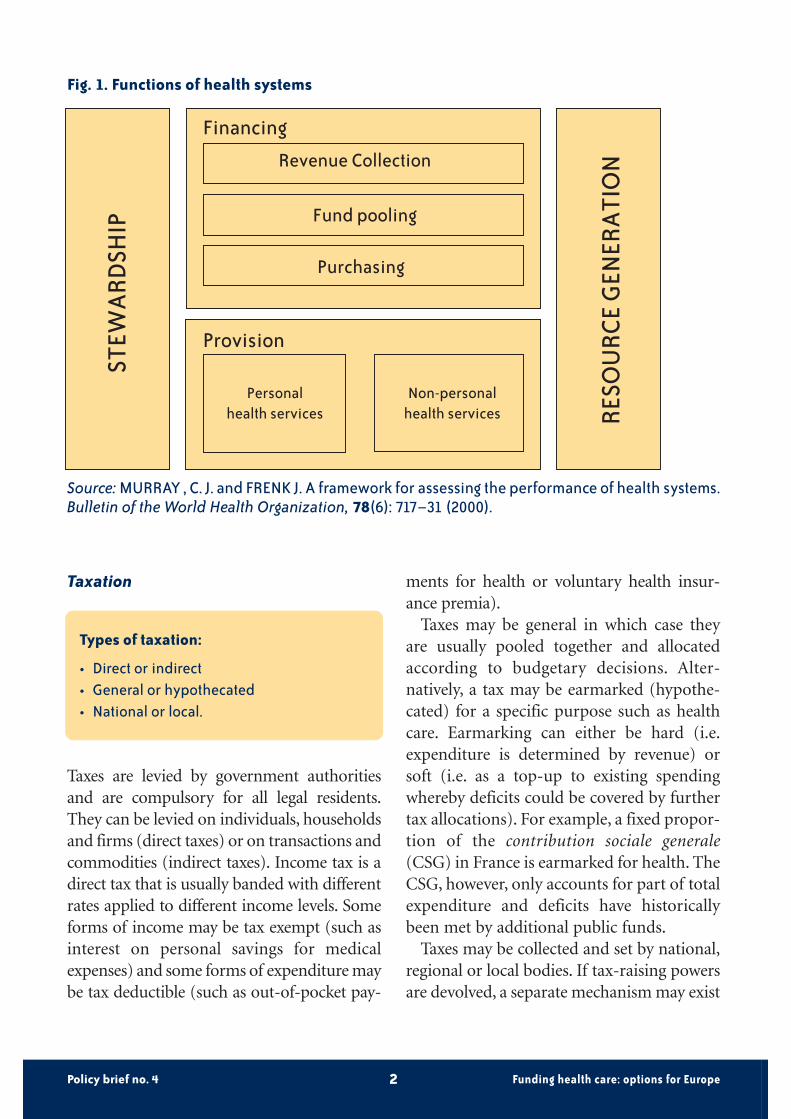

Confusion often arises in debates abouthealth care systems because the systems arecrudely defined as either social health insur-ance systems or tax-financed systems. Thisclassification conflates the method of rev-enue collection with historical patterns ofpurchasing and provision of health care. Ifwe understand revenue collection, pooling,purchasing and provision as distinct func-tions (see Fig. 1) it should be possible toanalyse each of their impacts separately. Thisbrief mainly focuses on revenue collection(and to a lesser extent the associated riskpooling arrangements).

There are basically four main methods ofrevenue collection: taxation, social insur-ance contributions, voluntary insurancepremia and out-of-pocket payments or usercharges. Taking each of these in turn, wedefine the terms and highlight their mainfeatures and the variations possible.

Policy brief no. 4 Funding health care: options for Europe1

Policy brief no. 4

Funding health care: options for Europe1

1 All the issues contained in this briefing are explored in more detail in MOSSIALOS, E., DIXON A., FIGUERAS J.and KUTZIN J., EDS.Funding health care: options for Europe. European Observatory on Health Care Systems Series. Buckingham, the UK: OpenUniversity Press, 2002. Where appropriate we make cross-references to information in this book.

Taxation

Types of taxation:

• Direct or indirect• General or hypothecated• National or local.

Taxes are levied by government authoritiesand are compulsory for all legal residents.They can be levied on individuals, householdsand firms (direct taxes) or on transactions andcommodities (indirect taxes). Income tax is adirect tax that is usually banded with differentrates applied to different income levels. Someforms of income may be tax exempt (such asinterest on personal savings for medicalexpenses) and some forms of expenditure maybe tax deductible (such as out-of-pocket pay-

ments for health or voluntary health insur-ance premia).

Taxes may be general in which case theyare usually pooled together and allocatedaccording to budgetary decisions. Alter-natively, a tax may be earmarked (hypothe-cated) for a specific purpose such as healthcare. Earmarking can either be hard (i.e.expenditure is determined by revenue) orsoft (i.e. as a top-up to existing spendingwhereby deficits could be covered by furthertax allocations). For example, a fixed propor-tion of the contribution sociale generale(CSG) in France is earmarked for health. TheCSG, however, only accounts for part of totalexpenditure and deficits have historicallybeen met by additional public funds.

Taxes may be collected and set by national,regional or local bodies. If tax-raising powersare devolved, a separate mechanism may exist

Policy brief no. 4 Funding health care: options for Europe2

Fig. 1. Functions of health systems

Financing

Revenue Collection

Fund pooling

Purchasing

Provision

Personalhealth services

Non-personalhealth services

STEW

ARD

SHIP

RESO

URC

E G

ENER

ATI

ON

Source: MURRAY , C. J. and FRENK J. A framework for assessing the performance of health systems.Bulletin of the World Health Organization, 78(6): 717–31 (2000).

for redistributing resources between locali-ties. Where revenue collection is devolved, theresponsibilities for purchasing and provisionare also usually devolved. Local taxes accountfor a significant proportion of health expen-diture in Bulgaria, Denmark, Finland, Italy(since 2000), Norway and Sweden.

Social health insurance2

Basic features of social health insurance:

• Income related contribution with variableor uniform rates;

• Mandatory for all or most of the population;• Proportion of contribution paid by employ-

er, employee or other agent;• Single or multiple funds;• Assigned membership or choice of insurer;• Upper and lower income thresholds for

contributions.

Social health insurance contributions arelegally mandatory for all or part of the popu-lation, they are not related to risk and they arekept separate from other legally mandatedtaxes or contributions. They are usually leviedby a designated (statutory) third-party payerwith some independence from governmentauthorities. Contributions are usually leviedas a proportion of income. In theory, contri-butions could be levied at different rates ac-cording to income, but in practice they arenot. There may be a uniform rate (e.g. theNetherlands) or contribution rates may varybetween insurance funds (e.g. Germany). InAustria contribution rates vary by type ofemployment. Contribution rates may be set

by the government (e.g. France and theNetherlands), an association of insurancefunds (e.g. Luxembourg) or individual funds(e.g. Germany). There may be upper andlower income thresholds above and belowwhich contributions are not levied (e.g.Austria, Germany and Luxembourg). Em-ployers and employees usually share the con-tributions; however, the proportion each paysvaries widely between countries.

Social health insurance contributions maybe collected by individual funds (as in Germa-ny), an association of funds (as in Luxem-bourg), a central fund (as in the Netherlands)or local branches (as in France). There may bea single national fund for all eligible persons ormultiple funds. Membership may be assignedeither according to occupation and/or region(as in Austria) or the population may have afree choice of fund (as in Belgium, CzechRepublic, Germany and the Netherlands).Where funds compete there is usually a mech-anism to ensure risk pooling between funds,either through the central allocation of fund-ing (as in the Netherlands) or reallocationbetween funds (as in Germany).

Eligibility is usually based on contributionstatus. However, where health care coverage isa universal right (as in France and many east-ern European countries), eligibility may bebased on residency and/or citizenship. Non-working dependents may be covered eitherthrough the working spouse or parents’insurance. Contributions may be made onbehalf of non-working members by the state(through tax transfers) or from other sources,e.g. pension funds and unemployment funds.

Some of the population who are notmandatory members of social health insur-

Policy brief no. 4 Funding health care: options for Europe3

2 See Table 3.1 in the book Funding health care: options for Europe, for a summary of the main features of social health insurancein western Europe and Table 4.3 for key features of social health insurance in eastern Europe available on www.observatory.dkunder “studies”.

ance may be voluntary members, i.e. have theright to opt-in (as in Germany). Those noteligible for membership of social health insurance may be covered through alternative

mechanisms such as a parallel tax finance sys-tem of health care or social assistance orthrough the compulsory or voluntary pur-chase of voluntary health insurance.

Policy brief no. 4 Funding health care: options for Europe4

B o x 1

Social health insurance funding ineastern Europe

The macroeconomic context in a number ofcountries in eastern Europe has meant thatthe ability to generate a significant propor-tion of health care expenditure from social health insurance contributions has been lim-ited.

In addition, factors such as the size of theinformal economy and the size of the agricul-tural labour force have made compliance dif-ficult. Finally, the high levels of unemploy-ment mean that the proportion of the popu-lation in formal employment is low, thus cre-ating a very narrow revenue base from whichto draw contributions.

Due to the historical legacy of the commu-nist era, many of the countries had anenshrined constitutional right to health carefor all. This meant that from the outset entitle-ments to health care benefits were universaland unrelated to contribution status. This con-trasts with the gradual expansion of socialhealth insurance in western Europe during thetwentieth century to different population

groups as economic development progressed.Thus, in eastern Europe there were reducedincentives to contribute whilst at the sametime large expenditures for the funds.

In higher income countries (namelyCroatia, the Czech Republic, Estonia,Hungary, Slovakia and Slovenia) social insur-ance appears to have been an effective wayof mobilizing resources for the health sector.Lower income countries in the region such asAlbania, Romania and Kazakhstan, with lessinstitutional capacity and little formalemployment, found that payroll taxes werenot a viable alternative to general taxation.Furthermore, the lack of strong strategic pur-chasing meant administrative efficiency,expenditure control and quality did not nec-essarily improve. Moving from general taxesto social insurance or increased out-of-pock-et payments reduced the equity of healthcare financing. Finally, the delegation ofresponsibility for revenue collection toquasi-state agencies or independent insur-ance funds has created significant challengesfor the state in terms of regulation and stew-ardship of the health care system.

Voluntary health insurance3

Types of voluntary health insurance:

• Substitutive, supplementary or comple-mentary;

• For-profit or non-profit insurers;• Individually purchased or employer

purchased;• Risk rated, community rated or group rated.

Voluntary health insurance is health insur-ance that is taken up and paid for at the dis-cretion of individuals or employers on behalfof individuals. It can be offered by public andquasi-public bodies or by for-profit or not-for-profit private organizations (Mossialosand Thomson 2002). In most EuropeanUnion (EU) countries voluntary healthinsurance premia account for less than 10%of total expenditure on health, except inFrance (12.2%) and the Netherlands(17.7%). In fact, in Belgium, Denmark, Fin-land, Greece, Italy, Luxembourg, Portugal,Spain, Sweden and the United Kingdom itaccounts for well under 5% of total expendi-ture. In the countries of central and easternEurope, voluntary health insurance has asmall market share. However, the role of vol-untary health insurance is important in pol-icy terms, particularly its relationship withsocial insurance and how it is regulated.

Private health insurance may be an indi-vidual’s sole form of insurance cover (substi-tutive); it may provide full or partial coveragefor services that are excluded or not fully

covered by the statutory health system (com-plementary) or it may increase subscriberchoice of provider and improve (speed of)access (supplementary). In Germany, peopleearning over € 3375 monthly have the choiceof remaining in the social insurance schemeor opting out. Of those who have this choice,less than one in four choose to opt out of thestatutory scheme.

Premia are usually risk rated based on anassessment of the risk of an individual, allemployees of a firm (group rated) or all res-idents of a defined geographical area (com-munity rated). Risk equalization betweeninsurers may be utilised to prevent insurersfrom selecting only those with low risk(known as cream skimming).

Tax relief (i.e. an expenditure allowed to bededucted from gross income before tax ischarged) or a tax credit (deduction from anindividual’s or household’s tax liability) maybe used to encourage the purchase of volun-tary health insurance. Tax expenditure subsi-dies, however, result in a net tax revenue lossand should be considered as expenditure.

Other options for regulating private insur-ers include: open enrolment (i.e. require-ment that insurers underwrite all applicantsfor insurance); lifetime cover (i.e. require-ment that insurers underwrite policies forlife, rather than annual renewals); or stan-dard benefits (i.e. requirement that mini-mum benefits be included in all insurancepolicies). EU legislation prevents MemberStates from regulating prices and benefits ofvoluntary health insurance, except substitu-tive health insurance4.

Policy brief no. 4 Funding health care: options for Europe5

3 Voluntary health insurance is also sometimes referred to as private health insurance or private medical insurance. As someinsurance policies are offered by public bodies the term voluntary health insurance is preferred.

4 Pre-accession countries also need to consider the implications of this when reforming or introducing the regulation of volun-tary health insurance.

Out-of-pocket payments

Out-of-pocket payments:

• Formal or informal payments;• Co-payment, co-insurance, deductible;• Exemption schemes;• Differential rates in some countries;• Annual out-of-pocket limit.

In most countries patients are required tomake a contribution to the cost of health care.The rationale behind user charges is twofold:to reduce unnecessary or excessive use of serv-ices and to raise additional revenue. The for-mer relies on health care being price elastic(that is that by increasing the price of servicespeople will stop using them); the latter relieson health care being price inelastic (that isdespite increasing the price, people will carryon using health services). However, due toprovider moral hazard (excessive supply ofhealth care services: see Box 2) user chargestend to result in a higher intensity of serviceuse for each patient treated. Furthermore,user charges tend to deter use of both neces-sary and unnecessary services.

Some out-of-pocket payments cover partof the cost of services otherwise covered bypublic or private insurance. Some are forservices that are fully excluded from publicand private insurance. Others are for servic-es which are in theory covered but for whichaccess is difficult due to long waiting times orthe poor distribution of facilities. In thesecircumstances patients may choose to pur-chase services directly in the private sector.Finally, in some countries patients are askedto make additional payments in the publicsector for services that should be fully cov-ered, called informal payments, envelopepayments or under-the-table payments.

Formal user chargesThe levels of user charges and the services towhich they are applied vary considerablybetween countries. Charges may be levied as aflat-rate payment for each service (co-pay-ment), a percentage of the total cost of theservice (co-insurance) or a fixed amount upto which the patient is liable after which theinsurer covers the remaining cost (deduc-tible). An annual out-of-pocket limit may bedefined up to which the patient is liable for allcosts and after which the insurer covers anyfurther expenditure in that year. In order toensure equal access to needed medical care,exemption schemes are common. Exemptionsfrom user charges may be means tested (e.g.income related); based on disease categories(e.g. diabetes or other chronic illnesses); forparticular products (e.g. contraceptives) orpopulation sub-groups (e.g. pensioners or theunemployed). User charges may also be set atvariable rates for different services in order to“steer” patients to more cost-effective services,e.g. to use the gatekeeping primary care doc-tor, or generic drugs.

Informal paymentsInformal payments take a number of formsand may exist for a number of reasons. Theyrange from the ex post gift in-kind to the exante cash payment. These payments or giftsmay be part of the culture, may be due to thelack of a cash economy or a lack of financesto pay health care workers and providedrugs and basic equipment to treat patientsor simply due to weak governance. At theirworst they may be a form of corruption,undermine official payment systems andreduce access to health services.

Data on the extent of informal payments ina selection of eastern European countriessuggest they are widespread in both ambula-tory and hospital care. Experience from low

Policy brief no. 4 Funding health care: options for Europe6

and middle income countries outside Europesuggests that formalizing payments andestablishing systems of pre-payment (orinsurance) is extremely difficult and requiresgovernment and technical capacity, andrecognition of external constraints. Informalpayments do exist in western Europe; howev-er, these are currently under-researched.

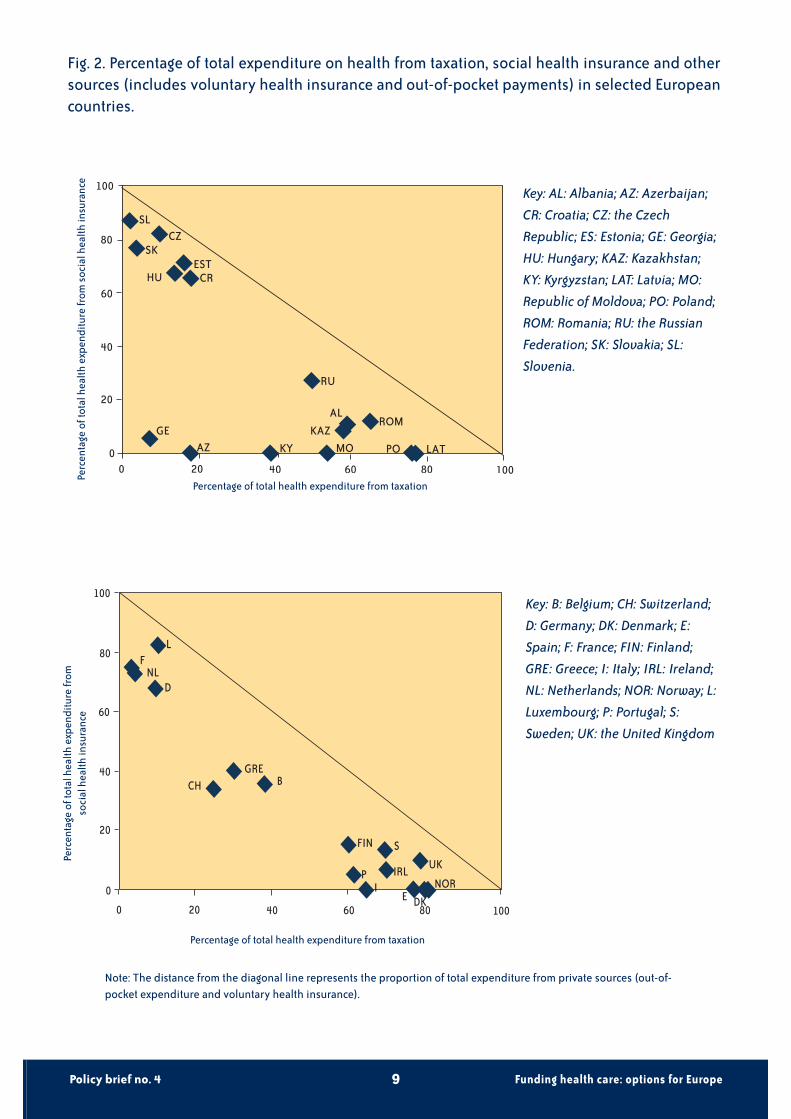

The health care funding mix in Europe

Each country in the European Region has aunique mix of sources of health care revenues.Fig. 2 shows data on the current compositionof health care revenues in a number of coun-tries in eastern and western Europe at the end

Policy brief no. 4 Funding health care: options for Europe7

B o x 2

User charges in western Europe

User charges have been advocated in west-ern Europe as a source of additional revenuewhen citizens are not prepared to fundhealth services through increased taxation orcontributions. It is also argued that in theabsence of user charges, where patients havethird-party insurance (public or private),there will be excessive demand for the cov-ered health services, thereby contributing toescalating expenditure. This is generallyreferred to as the problem of moral hazard.

Evidence on cost-sharing schemes in theEU suggests that they can be complex andexpensive to implement and administer.Therefore, they may have a limited role as amethod of generating additional revenue.This is likely to be especially true if efforts aremade to preserve equity and social solidaritythrough exemptions from payment for vul-nerable groups.

Cost-sharing has been shown throughempirical studies to deter both appropriateand inappropriate utilization. Finally, usercharges disproportionately affect lower-income groups as observed through changesin their utilization of services. In addition,studies show a similar impact on vulnerable

groups, such as the elderly and people withchronic diseases, independently of theirincome. This suggests that cost-sharing as ameans of reducing demand or raising rev-enue may not be as cost-effective as alterna-tive policy instruments.

Cost-sharing policies also have significantpolitical implications. In the United Kingdom,for example, the National Health Service wasfounded in 1948 on the principle of servicesbeing free at the point of use. Early decisions tointroduce user charges for spectacles in the1950s caused considerable political turmoiland ministerial resignations. Subsequent pro-posals to increase charges have generally metwidespread resistance. Increases in usercharges in the 1990s in Germany became thesource of intense political debate particularlyduring the federal election campaign of 1998and may have contributed to the defeat of theConservative-Liberal coalition. In Sweden, usercharges are levied across the board irrespec-tive of incomes. In order to protect individuals,particularly those with chronic diseases, fromunacceptably high expenditure there is a maxi-mum annual out-of-pocket limit. After this ceil-ing is reached no further charges are imposed.The lack of exemptions has raised equity con-cerns and political debate continues aboutreforming the system of charges.

of the 1990s.5 There are four western Euro-pean countries where health care expenditureis predominantly funded from social or com-pulsory insurance contributions:

• France• Germany• Luxembourg• Netherlands.

Belgium and Switzerland, which are usuallyclassified as having social health insurancesystems, and Greece whose system is nor-mally classified as tax funded, rely on a mixof social health insurance contributions andtaxation. The nine countries which rely pre-dominantly on taxation are:

• Denmark• Finland• Ireland• Italy• Norway• Portugal• Spain• Sweden • United Kingdom.

However, Fig. 2 does not reflect fully the taxtransfers which exist within social healthinsurance systems. In western Europe, onlyGreece, Italy, Portugal and Switzerland have30% or more of total expenditure on healthfrom private sources (mostly out-of-pocketpayments).

In eastern Europe, there are seven coun-tries which fund health care predominantlyfrom taxation:

• Albania• Kazakhstan• Latvia• Moldova• Poland

• Romania • Russian Federation.

There are six countries which rely predomi-nantly on social insurance contributions:

• Czech Republic• Croatia• Estonia• Hungary• Slovakia • Slovenia.

In Armenia, Azerbaijan, Georgia and Tajiki-stan forms of pre-payment have almost to-tally collapsed and health care is predomi-nantly funded by out-of-pocket payments.In Moldova and Kyrgyzstan out-of-pocketpayments account for more than 40% oftotal expenditure on health.

Weighing up the options

The challenge for policy-makers then is toensure that the mix of revenue sourcesenables sufficient funds to be generatedwhilst at the same time meeting a number ofpolicy objectives. Here, we briefly answer anumber of questions in relation to the objec-tives of equity and efficiency. Clearly, theoverall impact of health care funding willdepend on how it is designed and how thedifferent sources are combined . For example,a system funded predominantly from pro-gressive taxes might still have problems withaccess if user charges are applied withoutexemption to a wide range of services.

1. Is the funding system progressive?Whether a funding system is progressive ornot depends to what extent people on differ-

Policy brief no. 4 Funding health care: options for Europe8

5 These data are likely to have changed. For example, since 1998 Poland has implemented a 7.5% social health insurance contribution.

Policy brief no. 4 Funding health care: options for Europe9

Fig. 2. Percentage of total expenditure on health from taxation, social health insurance and othersources (includes voluntary health insurance and out-of-pocket payments) in selected Europeancountries.

Key: AL: Albania; AZ: Azerbaijan;

CR: Croatia; CZ: the Czech

Republic; ES: Estonia; GE: Georgia;

HU: Hungary; KAZ: Kazakhstan;

KY: Kyrgyzstan; LAT: Latvia; MO:

Republic of Moldova; PO: Poland;

ROM: Romania; RU: the Russian

Federation; SK: Slovakia; SL:

Slovenia.

Key: B: Belgium; CH: Switzerland;

D: Germany; DK: Denmark; E:

Spain; F: France; FIN: Finland;

GRE: Greece; I: Italy; IRL: Ireland;

NL: Netherlands; NOR: Norway; L:

Luxembourg; P: Portugal; S:

Sweden; UK: the United Kingdom

EST

ROM

RU

KYAZGE

HU

CZSL

SK

KAZAL

PO LATMO

CR

80

80

60

40

20

00 20 40 60 100

100

LF

NLD

CHGRE

B

FIN S

UKP IRL

NORDK

I

800 20 40 60 100

0

20

40

60

80

100

E

Perc

enta

ge o

f tot

al h

ealth

exp

endi

ture

from

soc

ial h

ealth

insu

ranc

e

Percentage of total health expenditure from taxation

Perc

enta

ge o

f tot

al h

ealth

exp

endi

ture

from

so

cial

hea

lth in

sura

nce

Percentage of total health expenditure from taxation

Note: The distance from the diagonal line represents the proportion of total expenditure from private sources (out-of-pocket expenditure and voluntary health insurance).

ent incomes pay different amounts. If afflu-ent people pay proportionately more oftheir income than the poor the system isprogressive. If everyone pays the same pro-portion regardless of income the system isproportional. And where affluent people payproportionately less than the poor the sys-tem is regressive.

Overall taxation is progressive; however, itdepends on the mix of indirect and direct taxesand the number of tax bands. Indirect taxes arenormally regressive because those on lowincomes spend a greater proportion of theirincome on consumption. Social health insur-ance is usually proportional. Upper incomeceilings, above which income is exempt fromcontributions, result in social health insurancebeing mildly regressive. If an opt-out existsbased on income (as in Germany and theNetherlands), it will result in overall financingbeing more regressive. Voluntary health insur-ance with individual risk rated premia is high-ly regressive. Group premia are less regressiveand proportional within the firm. Communityrated premia are proportional within the com-munity. User charges are highly regressive:means tested exemptions (e.g. for those on lowincomes) may reduce regressivity.

2. Is the funding system horizontally equitable?This concept of equity concerns whetherpeople on the same income pay the sameamount for health care. Together with thefirst objective discussed above it gives ameasure of how equitable the financing ofhealth care is. Under each type of revenuecollection method there might be a numberof reasons why horizontal equity is reduced:• under taxation if there is variation in local

tax rates or differential tax treatment ofincome and expenditure;

• under social health insurance if there aredifferent contribution rates between funds;

• under voluntary health insurance if indi-vidual premia vary according to risk (i.e.family history); group premia vary betweenfirms (large and small employers); commu-nity rated premia vary between high-riskand low-risk communities; or

• under user charges if there are non-meanstested exemptions e.g. for pregnant women,pensioners or those suffering from chronicdiseases.

3. Does the funding system result in redistribution?The two previous questions have mostly beenconcerned with the question “who pays andwhat share do they pay?” It is also importantto think about “who receives and what bene-fits do they get?” Redistribution is concernedwith the overall distribution of both the costsand the benefits of the health care systembetween income groups. The health care sys-tem is of course only one amongst severaltools available to policy-makers to achievegreater redistribution. For this reason it is dif-ficult (and might not be desirable) to isolatethe redistributive effect of health care fromthat of overall public policy. In addition,because health care benefits are usually pro-vided in-kind, their incidence is harder tomeasure than for cash benefits. However, it isworth weighing up equity on the financingside with the equity of access to benefits. Forexample, if additional revenue could be gener-ated through a less progressive system of col-lection but public spending disproportionate-ly benefited low-income people, the net effectmight be better for low-income people than asituation in which collection is more progres-sive but less is collected and public spendingdoes not benefit people with low incomes tothe same degree.

Policy brief no. 4 Funding health care: options for Europe10

4. How does the funding system affect coverage and access to health care?Equity of access may be analysed accordingto who is covered (this will depend on theeligibility criteria associated with a particu-lar system of funding) and what is covered(this will depend on the definition of bene-fits). Access to services in this contextdepends primarily on whether access isdependent on the patient’s ability to pay ornot (in other words whether access is free atthe point of use).

Coverage under taxation is usually basedon citizenship and/or residence and is there-fore universal. Coverage under social healthinsurance is based mostly but not exclusivelyon contributory status and is therefore par-tial. However, in Europe, due to the continualextension of coverage, social health insuranceis attaining near universal coverage. Somesmall groups continue to lack cover. In somecountries eligibility is related to residence/-citizenship although health care continues tobe funded from social health insurance con-tributions. Under these circumstance compli-ance is more difficult. Some of those not eli-gible for social health insurance may find itdifficult to obtain coverage privately due totheir age or risk (in the Netherlands sub-sidised private insurance policies are guaran-teed to ensure these people cover).

Voluntary health insurance cover by itsnature usually only covers a proportion ofthe population. Normally insurers have theright to refuse and therefore may excludehigh-risk subscribers (known as risk-selec-tion or cream skimming). Before it wasmade compulsory in Switzerland over 90%of the population had cover. Also in France,before the Universal Health Coverage(CMU) Act 2000, 86% of the populationwere covered by complementary insuranceto cover co-payments.

Under both taxation and social healthinsurance access to health care services existsregardless of the ability to pay. In practice,there may be non-financial barriers to access(such as waiting lists or distance to travel).Depending on how public insurance is com-bined with private insurance and user chargesit may create inequities in access. Under bothvoluntary health insurance and user charges,access depends on the patient’s ability to pay.User charges impose strong financial barriersto access care, which disproportionately affectthe low income, elderly and chronically ill,unless adequate exemption schemes are inplace. In addition, they appear to create sig-nificant political opposition, as they are high-ly visible, as described in Box 2.

5. How does the funding system affect cost containment?The ability to control expenditure has beenshown to depend on at least three factors: a(hard) budget for health care, monopsonypower (a market situation in which there isa single buyer for all sellers) and providerpayment methods.

Due to the budgeting process associatedwith taxation, there is a fixed budget forhealth care. This facilitates global cost con-trol but may result in sub-optimal levels ofspending. Under social health insurance,expenditure is generally determined by rev-enue and any overspend is met throughincreased contribution rates in subsequentyears or through tax subsidies. This does notallow for overall controls on expenditure.Other ways of regulating expendituregrowth have been attempted: in France theparliament now sets a global budget (target)for health care spending. Under voluntaryhealth insurance, premia levels are deter-mined by individual insurers and will bedriven by expenditure (claims) and a desire

Policy brief no. 4 Funding health care: options for Europe11

to generate a surplus (or profit). Whereinsurers are free to determine their ownrates there is little incentive to controlexpenditure through efficiency gains.

Traditionally, taxation has been associatedwith centralized purchasing and monopsonypower. Decentralization has created smallerpurchasing organizations which may haveweaker purchasing power vis-à-vis provi-ders. Social health insurance with a singlefund creates a strong purchasing function.Where multiple funds exist purchasingpower might be more diffuse. However, ifcorporate bargaining takes place this mayenhance purchaser power.

Social health insurance used to be associ-ated with per diem and fee for service.However, this has begun to change with theintroduction of budgets, capitated pay-ments and diagnosis related groups(DRGs). Taxation has historically beenassociated with budgets, salaries and capita-tion whereas voluntary health insurance ismore usually associated with retrospectivereimbursement, direct billing and fee forservice.

6. How does the funding system affect the wider economy?Another aspect of efficiency to consider isthe impact of the method of funding healthcare on the wider economy. Healthy workersare essential to a productive economy: if aparticular system of funding cannot deliversufficient funds to provide quality healthcare this might adversely affect the economy.The health care industry itself may createjobs and wealth. However, the most com-monly debated concern is the financial bur-den of health care funding on employers.

Social health insurance contributions arelevied on earned income and paid byemployers and employees. Thus they direct-

ly contribute to increased labour costs. It hasbeen argued that high labour costs deterinward investment by multinational compa-nies and may increase unemployment.

Another concern is job mobility, seen as thekey to a successful economy. Where healthcare cover is dependent on employment theremay be interference with job mobility. Mostvoluntary health insurance is purchased onbehalf of the employee by the employer(either as a fringe benefit or premia deductedfrom wages). This may result in a reductionin job mobility, particularly where suchinsurance is substitutive (i.e. a person’s onlyinsurance cover). Conversely, taxation andsocial health insurance, where cover is neitherregionally or occupationally determined, donot provide any disincentives to move jobs.

7. How does the funding system affect allocative and technical efficiency?Allocative efficiency is essentially concernedwith maximizing health given constrainedresources. An assessment of allocative effi-ciency might consider the allocationsbetween health and other areas of publicspending: allocations within the health sec-tor to different sectors or cost-effective ver-sus non-cost-effective treatments. Technicalefficiency is concerned with maximisingoutputs for a set of given resources (inputs)or minimising resources (inputs) for a givenlevel of output. Any links between revenuecollection and allocative and technical effi-ciency are difficult to establish throughempirical evidence. Indeed, to the extentthat these are more a function of purchasingthan revenue collection, the links may notexist at all. However, certain methods of col-lection may have indirect implications forallocative and technical efficiency resultingfrom their associated market structure ofpooling and purchasing.

Policy brief no. 4 Funding health care: options for Europe12

Macro allocations to health care are nor-mally determined politically under a systemof general taxation, but may be pre-deter-mined if there is a strictly hypothecatedhealth tax. Trade-offs are usually possiblebetween health care and other areas of pub-lic spending but may also be open to politicalmanipulation and thus result in sub-optimalallocation. Social health insurance contribu-tions are in effect, earmarked so allocationsto health care are determined by revenue.Allocations are therefore more susceptible tofluctuations in the economic cycle due to thereliance on wage-related contributions. Involuntary health insurance markets, healthcare allocations are largely determined bywillingness to pay. Where tax subsidies areprovided it may result in over-insurance bypart of the population. Within the healthsector, allocations of public money are usual-ly subject to planning and priority setting byeither government or insurance funds, orboth, and may use cost-effectiveness infor-mation to inform these decisions.

There is no clear evidence that fundingmethods determine the level of technicalefficiency with which health care services areproduced. However, administrative andtransaction costs may be associated with revenue collection. Central taxation and cen-trally collected social health insurance con-tributions benefit from economies of scalewhich are not fully exploited by local taxa-tion or when individual funds collect contri-butions. Transaction costs tend to be higherunder private health insurance due to con-siderable administrative costs related tobilling, contracting, utilization review andmarketing. Risk rating involves extensiveadministration to assess risk, set premiums,design complex benefit packages and reviewand pay or refuse claims. Social health insur-ance which reimburses patients, rather than

contracting with providers directly, is likelyto face significant administrative costs asso-ciated with billing.

Implementation issues

So far, we have looked at the different fund-ing options and to what extent they enablepolicy-makers to meet certain objectives.How feasible they are, however, will dependon the context. There is no single blueprintthat will be appropriate to all countries.

A funding policy, even when based on evi-dence and experience, has a greater chanceof achieving its objectives if the context inwhich it is to be implemented has beenassessed. A number of factors can be identi-fied (see Fig. 3) which may affect the poten-tial size of the revenue pool:

• political structures• economic activity• demographic profile• environmental factors• external pressures• social values.

For example, changes in the political econo-my of the countries of central and easternEurope both precipitated and influenced thetransition to social health insurance (see Box1). Social values of solidarity and externalpressures to contain public expenditure haveproduced conflicting responses to usercharges in western Europe (see Box 2).

Furthermore, the ability to collect suffi-cient revenue will also depend on the insti-tutional and technical capacity of govern-ment, the administration and the health caresystem. For example, where corruption andfraud are rife within the administration theability to establish a functioning tax collec-tion system will be impeded.

Policy brief no. 4 Funding health care: options for Europe13

In summary, when weighing up the optionsfor funding health care, wider societal objec-tives and the feasibility of implementationmight be as important as the equity and effi-ciency of the funding method itself.

Summary

Most health care systems in Europe arefunded from a mix of sources, including tax-ation, social health insurance contributions,voluntary health insurance premia and out-of-pocket payments. Nevertheless, taxationand social health insurance dominate asmethods of funding in nearly all Europeancountries, while voluntary health insurancestill plays a supplementary role.

The fact that most countries rely on a mixof revenue sources means that evaluating ahealth care system’s performance based onthe sources of funding is difficult. However,there are apparent advantages in terms ofequity and efficiency of systems of publicfunding (access free at the point of use,extensive risk pooling, near universal cover-age and cost control). User charges and vol-untary health insurance relate access to theability to pay, risk pooling is limited and costcontrol tends to be weaker. The key toimproving policy outcomes is to weigh upcarefully the advantages and disadvantagesof each funding method and take fullaccount of the context in which the system isintended to operate.

Policy brief no. 4 Funding health care: options for Europe14

War

RevolutionNatural disaster

IMF WTO

EMU

Corruption

EU directives and legislation

Administrative capacity Household structure

Dependency ratio

Urbanization

Ageing population

Support for welfare state

Informal payments

Rule of law

Trust in governmentStatus of professionals

Policy process

Stability of political institutions

Capital vs. earned incomeLabour market participation

Informal economy

Public deficits

CorruptionUnemployment

Unionization

Labour market structure

Economic activity

Political structures Demographic profile

Social values

Envi

ronm

enta

lfa

ctor

sExternal

pressures

Revenuepotential

Decentralization

Fig. 3. Contextual factors affecting the ability to raise revenue for health care

Policy brief no. 4 Funding health care: options for Europe15

Key references

KUTZIN, J. A descriptive framework for country-level analysis of health care financing arrangements. Health Policy

56(3): 171-203 (2001).

MOSSIALOS E. and THOMSON, S. Voluntary health insurance in the European Union, Report prepared for the

Directorate General for Employment and Social Affairs of the European Commission, Brussels: European

Commission (2002). Available at http://europa.eu.int/comm/employment_social/soc-prot/social/index_en.htm

MURRAY, C. J. and FRENK, J. A framework for assessing the performance of health systems. Bulletin of the World

Health Organization 78(6): 717-31 (2000).

The European Observatory on Health Care Systemssupports and promotes evidence-based health policy-making through comprehensive and rigorousanalysis of health care systems in Europe. It bringstogether a wide range of academics, policy-makersand practitioners to analyse trends in health carereform, utilising experience from across Europeto illuminate policy issues. More details of itsupdate service, publications, articles, conferen-ces and training can be found on the website:www.observatory.dk.

The Observatory is a partnership between theWorld Health Organization Regional Office forEurope, the Governments of Greece, Norway and Spain,the European Investment Bank, the Open Society Institute,the World Bank, the London School of Economics and PoliticalScience, and the London School of Hygiene & Tropical Medicine.

Books in the EuropeanObservatory on Health Care Systems

series, edited by Josep Figueras,

Martin McKee, Elias Mossialios and Richard Saltman,

can be ordered directly fromwww.observatory.dk.

Policy brief no. 4 Funding health care: options for Europe16

Funding health care: options for Europe is the fourth policy brief

in the European Observatory on Health Care Systems policy brief series,

available online on www.observatory.dk.

Edited by Jeffrey V. Lazarus and Viv Taylor Gee.

It draws on Funding health care: options for Europe.

Edited by Elias Mossialos, Anna Dixon, Josep Figueras and Joe Kutzin,

European Observatory on Health Care Systems series.

Buckingham, the UK: Open University Press, 2002.

Winner of the Baxter Prize 2002.

© World Health Organization 2002

Paperback ISBN 0 335 20924 6

Hardback ISBN 0 335 20925 4

The contents of the book “Funding health care: options for Europe” are as follows:

1. Funding health care: an introductionElias Mossialos and Anna Dixon

2. Financing health care: taxation and the alternativesRobert G. Evans

3. Social health insurance financingCharles Normand and Reinhard Busse

4. Health financing reforms in central and eastern Europe and the former Soviet UnionAlexander S. Preker, Melitta Jakab and Markus Schneider

5. Voluntary health insurance and medical savings accounts: theory and experienceAlan Maynard and Anna Dixon

6. Voluntary health insurance in the European UnionElias Mossialos and Sarah M. S. Thomson

7. User charges for health careRay Robinson

8. Informal health payments in central and eastern Europe and the former Soviet Union: issues, trends and policy implicationsMaureen Lewis

9. Lessons on the sustainability of health care funding from low and middle income countriesAnne Mills and Sara Bennett

10. Funding long-term care: the public and private optionsRaphael Wittenberg, Becky Sandhu and Martin Knapp

11. Strategic resource allocation and funding decisionsNigel Rice and Peter C. Smith

12. Funding health care in Europe: weighing up the optionsElias Mossialos and Anna Dixon