by elizabeth hund november 7, 2005 international opportunities

TRANSCRIPT

By Elizabeth Hund

November 7, 2005

International Opportunities

Rabobank International 2

Coöperatieve Centrale Raiffeisen-Boerenleenbank

Rabobank International 3

Rabobank

2005 ● Only AAA rated non-government bank

● 100 + years of agricultural/community banking experience

● 57,000 employees in 35 countries

Rabobank International 4

Rabobank International Network

Toronto Toronto

New YorkNew York

ChicagoChicago

AtlantaAtlanta

DallasDallas

San FranciscoSan Francisco

Washington Washington D.C.D.C.

Toronto Toronto

New YorkNew York

ChicagoChicago

AtlantaAtlanta

DallasDallas

San FranciscoSan Francisco

Washington Washington D.C.D.C.

Mexico CityMexico City

Curaçao Curaçao

São PauloSão Paulo

Santiago Santiago

Buenos AiresBuenos Aires

Mexico CityMexico City

Curaçao Curaçao

São PauloSão Paulo

Santiago Santiago

Buenos AiresBuenos Aires

LondonLondon

DublinDublin

AntwerpAntwerp

Frankfurt Frankfurt

ParisParis

MadridMadrid

MilanMilan

LondonLondon

DublinDublin

AntwerpAntwerp

Frankfurt Frankfurt

ParisParis

MadridMadrid

MilanMilan

Singapore Singapore

MumbaiMumbai

New DelhiNew Delhi

JakartaJakarta

BangkokBangkok

TaipeiTaipei

Hong Kong Hong Kong

BeijingBeijing

ShanghaiShanghai

TokyoTokyo

Singapore Singapore

MumbaiMumbai

New DelhiNew Delhi

JakartaJakarta

BangkokBangkok

TaipeiTaipei

Hong Kong Hong Kong

BeijingBeijing

ShanghaiShanghai

TokyoTokyo

SydneySydney

MelbourneMelbourne

BrisbaneBrisbane

PerthPerth

SydneySydney

MelbourneMelbourne

BrisbaneBrisbane

PerthPerth

Warsaw Warsaw

PoznanPoznan

MoscowMoscow

IstanbulIstanbul

Warsaw Warsaw

PoznanPoznan

MoscowMoscow

IstanbulIstanbul

AucklandAucklandAucklandAuckland

Rabobank International 5

The global FAR team has 74 members in 12 different countries

Utrecht (Global HQ)

Mumbai

Sydney

Mexico City

São Paulo

New YorkBeijing

Shanghai

Bangkok

Hong Kong

Tokyo

Singapore

New Delhi

Jakarta

Rabobank International 6

Rabobank Locations in the United States

Corporate BankRabobank NARabo AgriFinanceRabo AgServices

Rabobank International 7

Rabobank International

“The financial link in the global food chain”®

Rabobank International 8

Contents

Section 1:

Section 2:

Section 3:

Consumer Progression

Production Trends

International Opportunities

Section I

Consumer Progression

Setting the stage

Rabobank International 10

Key Drivers Behind Global Food Demand– Income and Total Population

AUSTRALIA

CANADA

JAPAN

US

CHINA

INDIA

EUROPE-25

EAST ASIA

MIDDLE EAST& NORTH AFRICA

SUBSAHARANAFRICA

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

-0.2% 0.2% 0.6% 1.0% 1.4% 1.8% 2.2% 2.6%

Population growth 2002 (annual %)

GD

P g

row

th 2

002

(an

nu

al %

)

SOUTHASIA

0%

Rabobank International 11

Asia is Key to Future Consumer Demand

China and India

• most populated countries

• highest annual GDP growth

Source: Rabobank analysis based on UN data

1.50.7

1.2

5.6

8.3

2.6

0

1

2

3

4

5

6

7

8

9

India China World

Per

cen

tag

e (%

)

Population GDP

Low income levels of those countries show enormous markets that are emerging.

Rabobank International 12

ChinaEconomic Superpower?

Source: United Nations, Rabobank

GDP Growth by Country/Bloc

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

US

Bln

s D

olla

rs (

1990

Pri

ces)

EU-25 United States China Japan India Asia-7

EU-25

USA

Japan China

India

Asia-7

Rabobank International 13

DemographicsWe are getting older!

Higher interest in functional foods

Require different serving sizes & packaging

In the western hemisphere, health becomes progressively more important.

Population aged 60+ years in selected regions 2000 - 2015

0

5

10

15

20

25

30

World Europe US and Canada Asia Latin America Africa

Per

cen

tag

e

2000 2010 2015

Source: Rabobank analysis based on UN data

%

Rabobank International 14

Industry Consolidation

Turnover of top-10 retailers

0

100

200

300

400

500

600

1998 2001

Tot

al s

ales

in U

SD b

illio

n

Turnover of top-10 food service

0

25

50

75

100

125

150

1998 2001

Tot

al s

ales

in U

SD b

illi

on

USD 473bn

USD 604bn

USD 106bn

USD 130bn

Rabobank International 15

Top Ten 2001 Ranked by total sales (in USD billion)Retailers

1. Wal-Mart Stores

218 2. Carrefour (France)

62 3. Ahold (Dutch)

60 4. Kroger

50 5. Metro AG(Germany)

44 6. Albertson’s

38 7. Safeway (US)

34 8. Leclerc* (France)

34 9. Auchan * (France)

3310. Intermarché*(France) 31*2000Total above

USD 605

Food Service 1. McDonald’s

41 2. Tricon

22 3. Compass (England)

13 4. Burger King

11 5. Sodexho Alliance(Fr.) 11 6. Wendy’s

8 7. Aramark

8 8. Accor (France)

7 9. Six Contintents (UK)

610. Whitbread (UK)

4

Total above

USD 131

GlobalizationMajor players have become huge global companies

Section II

Production Trends

Rabobank International 17

South America is poised to take over North America

as the world’s largest beef producing regionSource: FAO

05

101520253035

N.AM

ERICA

C.AM

&CARIBBEAN

S.AM

ERICA

W.E

UROPE

E.EUROPE

AFRIC

A

S.ASIA

&CHINA

S.E.A

SIA

OCEANIA

Pro

du

cti

on

(%

)

1970 1990 2003

World Beef Production

Rabobank International 18

China accounts for almost half of world pork production

Source: FAO

World Pork Production

0

10

20

30

40

50

Pro

duct

ion

(%)

1970 1990 2003

Rabobank International 19Source: FAO

World Poultry Production

05

10152025303540

Pro

du

ctio

n (%

)

1970 1990 2003

Poultry production has shifted from North America & Europe to South America &

Asia

Rabobank International 20

World Dairy Production

Source : CFCE / FAO/Rabobank

05

101520253035

N.AM

ERICA

C.AM

&CARIBBEAN

S.AM

ERICA

W.E

UROPE

E.EUROPE

AFRIC

A

S.ASIA

&CHINA

S.E.A

SIA

OCEANIA

Pro

du

cti

on

(%

)

1984 2001 2005

Developing regions are becoming more important for dairy production

Rabobank International 21

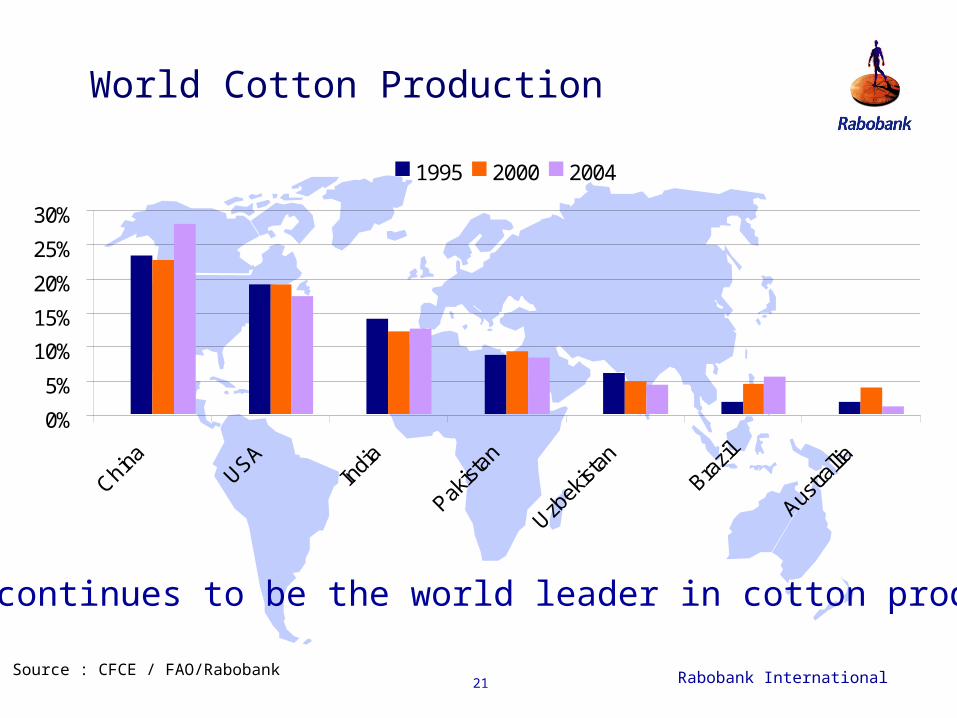

World Cotton Production

Source : CFCE / FAO/Rabobank

0%

5%

10%

15%

20%

25%

30%

China

USAIn

dia

Pakist

an

Uzbek

istan

Brazil

Austra

llia

1995 2000 2004

China continues to be the world leader in cotton production

Rabobank International 22

Consolidation of U.S. Farmers

Consolidation has been driven by:

1. Cost

2. Product sales advantages

3. Regulatory and policy considerations

U.S. Farm numbers and Gross income 1978-2002

1900

2000

2100

2200

2300

2400

2500

2600

1978 1982 1987 1992 1997 2002

Nu

mb

er

of

farm

s '0

00

0

50

100

150

200

250

300

Gro

ss

fa

rm in

co

me

$ b

illio

n

Farm numbers Gross farm income

Rabobank analysis based on US Census data

Rabobank International 23

Farmers are Moving!

Access to labor

Environmental regulations

Water availability– Shift in focus of crops

Market access and non tariff barriers

Rabobank International 24

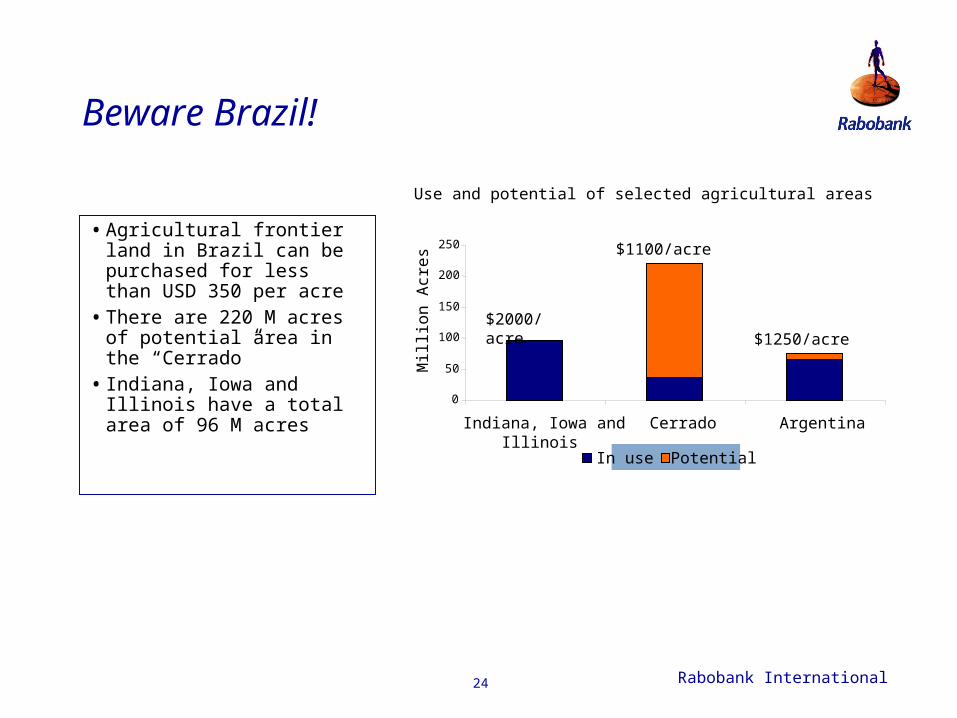

Beware Brazil!

•Agricultural frontier land in Brazil can be purchased for less than USD 350 per acre

•There are 220 M acres of potential area in the “Cerrado”

• Indiana, Iowa and Illinois have a total area of 96 M acres

Use and potential of selected agricultural areas

0

50

100

150

200

250

Indiana, Iowa andIllinois

Cerrado ArgentinaM

illio

n A

cre

s

In use Potential

$2000/acre

$1100/acre

$1250/acre

Section IIIInternational Opportunities

Rabobank International 26

Top 5 Exporters

1.United States 15.50%

2.Netherlands 10.60%

3.France 8.60%

4.Germany 7.40%

5.Canada 7.30%

% World Market Share in 2002

Rabobank International 27

Top 5 Growth Exporters

1. United States

2. Netherlands

3. France4. Germany5. Canada6. Belgium7. Spain8. Brazil9. Italy10.China

• The next 5 exporters are gaining

• U.S. is still the largest exporter but is consistently losing market share:

1990 = 18.2% of the world exports2002 = 15.5% of the world exports

• Australia and Argentina have been growing rapidly.

Top 10 Exporters (2002)

Rabobank International 28

ExportsWhat are they exporting?

Source: Rabobank analysis based on UN data

Top 6 Exports(USD 193.8 Billion)

Cereals, 15%

Meat, 21%

Beverages, 20%

Fruits & Nuts 14%

Fish & fish products

16%

Dairy, Eggs 14%

Rabobank International 29

U.S. Export Trends

Rabobank International 30

Don’t Forget Exchange Rates

Exchange rate index for selected currencies, 2000 - April 2005

70

80

90

100

110

120

130

140

Jan-00

Apr-00

Jul-00

Oct-00

Jan-01

Apr-01

Jul-01

Oct-01

Jan-02

Apr-02

Jul-02

Oct-02

Jan-03

Apr-03

Jul-03

Oct-03

Jan-04

Apr-04

Jul-04

Oct-04

Jan-05

Apr-05

Ind

ex

CAD EUR GBP AUD YEN

Rabobank International 31

Tools of the Trade

Political risk

Rule of law

Local financing

Rabobank International 32

Joint VenturesIf you can’t beat ‘em, join ‘em

Difficult but not impossible Loads of opportunities Key success factors are:

– Partner selection

– Careful structuring of the deal

– Cost control

– Attracting and retaining local talen

– Branding

Rabobank International 33

Summary

Consumer Progression– Income– Demographics– Trends

Production Trends– Consolidation– Globalization– New Major Players

Expansion of international trade