by rajeev shah cmib ukcmib, uk mortality.pdf · by rajeev shah cmib ukcmib, uk. structure • the...

TRANSCRIPT

Cohort MortalityBy Rajeev Shah

CMIB UKCMIB, UK

StructureStructure

• The Continuous Mortality I i i B (CMIB)Investigation Bureau (CMIB)

• Two way mortality tablesTwo way mortality tables

• Cohort Effects

The CMIBThe CMIB

• Role• Features

Wh ffi t ib t d t• Why offices contribute data

NB “Office” = “company”ff p y

Role of the CMIBRole of the CMIB• Research – Mortality, IP and CI.y,

– Methodologies– GraduationGraduation– Models

D t ll ti• Data collection• Analysis & reporting

– Industry experience– Contributing officesg

• Standard Tables• Projecting future experience• Projecting future experience

Features of the CMIBFeatures of the CMIB

• Governed by the actuarial professionC ti i ti ti• Continuous investigations

• Independentp• Confidentiality is paramount

d d d li / /• Produce standard mortality/IP/CI tables

• Actuarial profession provides expertise

Why offices contribute data (1)Why offices contribute data (1)• Helps the market price and reserveHelps the market price and reserve

rationally– Provides confidence to regulators and consumers

h k i• Acts as a check on own assumptions– Comparison with industry experience and trendsComparison with industry experience and trends

– Small areas of experience e.g. Cause of Claim

• Benchmarking of underwriting/claims controlcontrol

Why offices contribute data (2)Why offices contribute data (2)

B fit f h d id• Benefit from new research and ideas– CMIB provides interface for exchange of ideas between

academia and the commercial world

Li it d d ti ithi ffi• Limited resources and expertise within offices

• Confidence in the CMIB and the actuarialConfidence in the CMIB and the actuarial profession

• Benevolent?t d t di d h– e.g. promote understanding and research

Standard mortality tablesStandard mortality tables

Period Assured Lives Annuitants Pensioners1924-29 (males)( )1947-48

1949 52 (males)1949-52 (males)1967-70 (males)

1975-78 (females)1979-82

1991-94

Comparison of the mortality of male assured livesComparison of the mortality of male assured livesComparison of the mortality of male assured livesComparison of the mortality of male assured lives400

300

350

250

300

f 196

7-70

150

200

cent

age

o

1924-291949-52

100

150

Perc

1967-70

1991 941979-82

0

501991-941979-82

17 22 27 32 37 42 47 52 57 62 67 72 77 82 87 92 97

Age

Two way mortality tables

Two way mortality tablesTwo way mortality tables

• Standard tables• Show mortality rates by age and

calendar yearcalendar year• Allow for projected mortality

improvements

T t bl f th b t blTwo way table for qx – the base table

Age 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 20056061 C 1992C 199261626364

C=1992C=1992

65 66 67 68 69 70 71 72 72 73 74 75 7676 77

T t bl f f bi th 1935Two way table for qx- year of birth 1935

Age 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 200560616162636465 66 67 68 69 70 71 72

B=1935B=193572 73 74 75 7676 77

T t bl f f 2000Two way table for qx – year of use 2000

Age 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 200560 61 61 62 63 64 U=2000U=200065 66 67 68 69 70 71 72 72 73 74 75 7676 77

Cohort Effects

The problemThe problem

I h l li j i• Is the latest mortality projection (the “92” Series) still appropriate?(the 92 Series) still appropriate?

•If not, how should it change?

Pensioners 100A/E using the “92” Series projected mortality rates:Males

110110

100

tio

90

A/E

Rat

80 AmountsLi

100

701992 1993 1994 1995 1996 1997 1998 1999 2000

Lives

1992 1993 1994 1995 1996 1997 1998 1999 2000

Pensioners 100A/E using the “92” Series projected mortality g p j yrates: Males, lives, by age

66 - 70105

110

71 - 75

76 - 8095

100

atio

81 - 85

86 - 9085

90

95

0 A

/E R

a

91 - 9580

85

100

70

75

1992 1993 1994 1995 1996 1997 1998 1999

Cohort dataCohort data

• Assured lives 1947 to 1999A 10 t 100+• Age range 10 to 100+

• … 2-way table of qxy q• Pre 1974 data had to be entered manually

Ul i d i l• Ultimate durations only• Relatively homogeneousy g• Other data sets not as complete

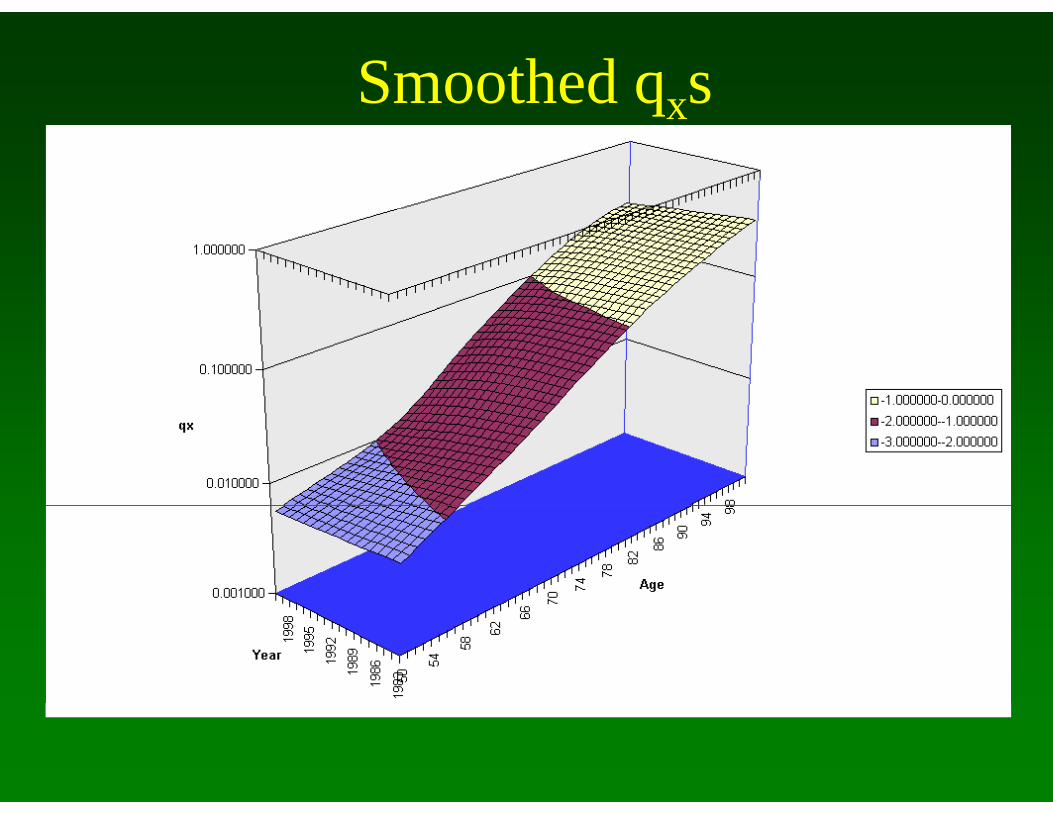

SmoothingSmoothing

• Lots of attempts, but finallyt di i l li• … two dimensional splines

• Imposes no “shape” on the datap p• Smooth in two directions

f f i d• Lots of features in data• but difficult to see patterns in qxs… but difficult to see patterns in qxs

Smoothed qxsqx

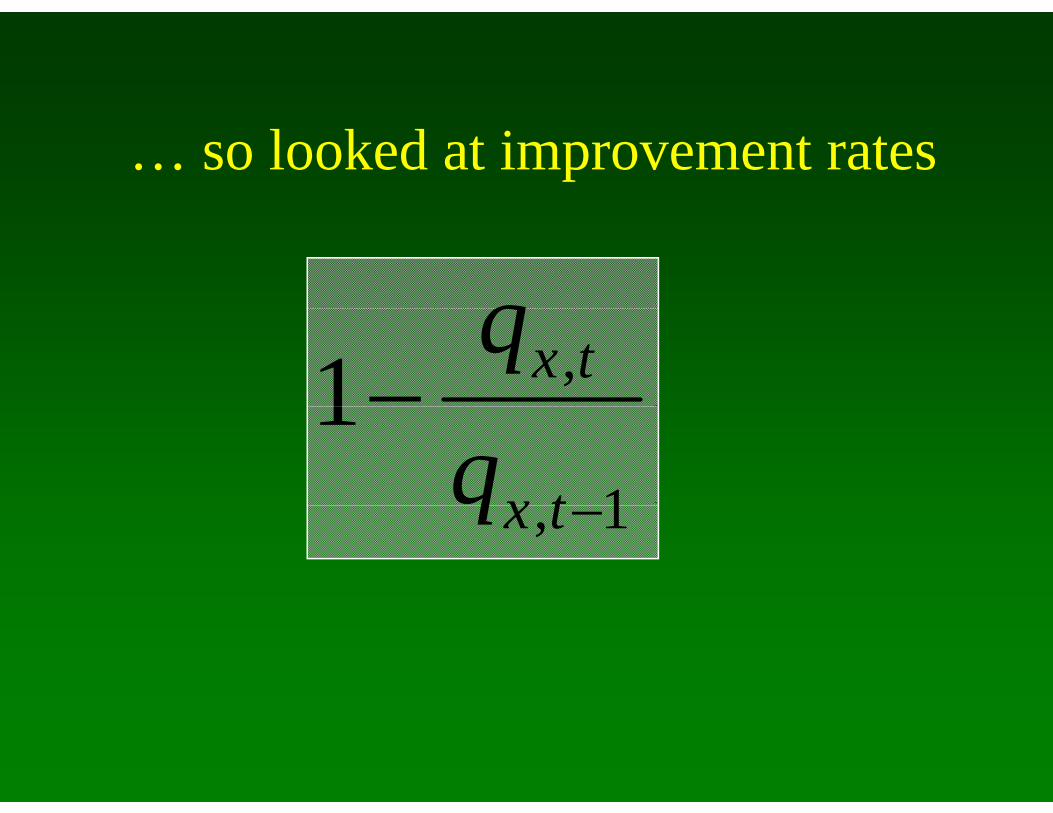

… so looked at improvement rates

q ,1 txq

1

1txq 1, txq

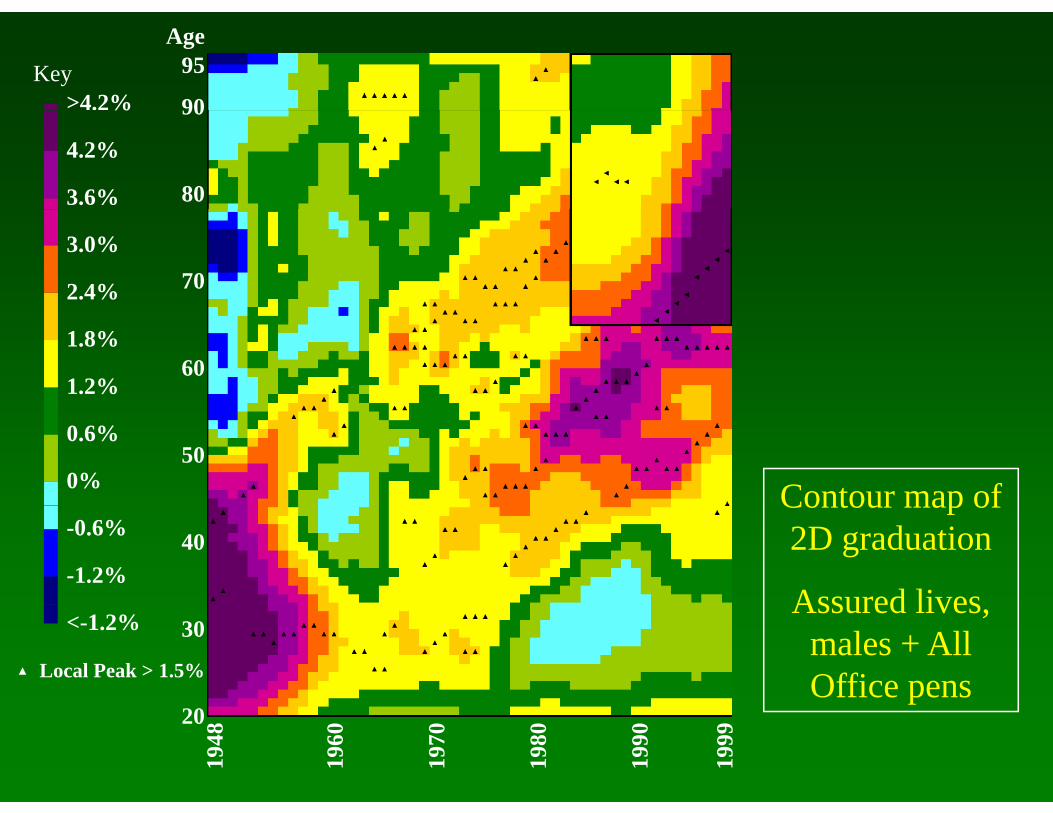

Improvement factorsp

95

90

AgeKey

>4.2%

80

90%

4.2%

3.6%

703.0%

2.4%

601.8%

1.2%

500.6%

0% Contour map of40-0.6%

-1.2%

Contour map of 2D graduation

Assured lives30

Local Peak > 1.5%

<-1.2%Assured lives,

males, all durations

20

1948

1960

1970

1980

1990

1999

Key>4.2%

95

90

Age

%

4.2%

3.6% 80

90

3.0%

2.4% 70

1.8%

1.2%60

0.6%

0%50 GAD Contour

map-0.6%

-1.2%40

map

Male Population<-1.2% 30Population, England &

Wales20

1948

1960

1970

1980

1990

1999

Wa es

Pensioner cohort dataPensioner cohort data

• 1983 – 1999 • Males, Females, Lives & Amounts• Data issues• Data issues• All Offices & Loyal Officesy• Males – improving more quickly than

A d LiAssured Lives

All Office Pensioners 100A/E using the “92” Series projected with Assured lives actual mortality improvements - Males

110110

100

tio

90

A/E

Rat

80 AmountsLi

100

A

701992 1993 1994 1995 1996 1997 1998 1999

Lives

1992 1993 1994 1995 1996 1997 1998 1999

95

90

AgeKey

>4.2%

80

90%

4.2%

3.6%

703.0%

2.4%

601.8%

1.2%

500.6%

0% Contour map of40-0.6%

-1.2%

Contour map of 2D graduation

Assured lives30

Local Peak > 1.5%

<-1.2%Assured lives,

males + All Office pens

20

1948

1960

1970

1980

1990

1999

p

95

90

AgeKey

>4.2%

80

90%

4.2%

3.6%

703.0%

2.4%

601.8%

1.2%

500.6%

0% Contour map of40-0.6%

-1.2%

Contour map of 2D graduation

Assured lives30

Local Peak > 1.5%

<-1.2%Assured lives, males + Loyal

Office pens20

1948

1960

1970

1980

1990

1999

p

All Office crude data to 1992 then “92” Series projectionAll Office crude data to 1992, then 92 Series projection

Crude Projection

100Age

C udedata Projection

90

80

61

70

61

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%

1967

2040

1986

1992

2000

2010

2020

2030

1980

<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

All Office to 1992, then “92” Series projection

Crude data Projection

Graduated data

, p j

100Age data Projectiondata

90

80

61

70

1967

2040

1983

1992

2000

2010

2020

2030

1980

61

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

All Office to 83 - Loyal Office to 99 - then “92” Series

Crude d t Projection

Graduated d t

yprojection

100Age data Projectiondata

90

80

61

70

61

1967

2040

1983

1992

2000

2010

2020

2030

1980

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

Sh t h tShort cohortCrude d t Projection

Graduated d t

100Age data Projectiondata

90

80

61

70

61

1967

2040

1983

1999

2010

2020

2030

1980

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

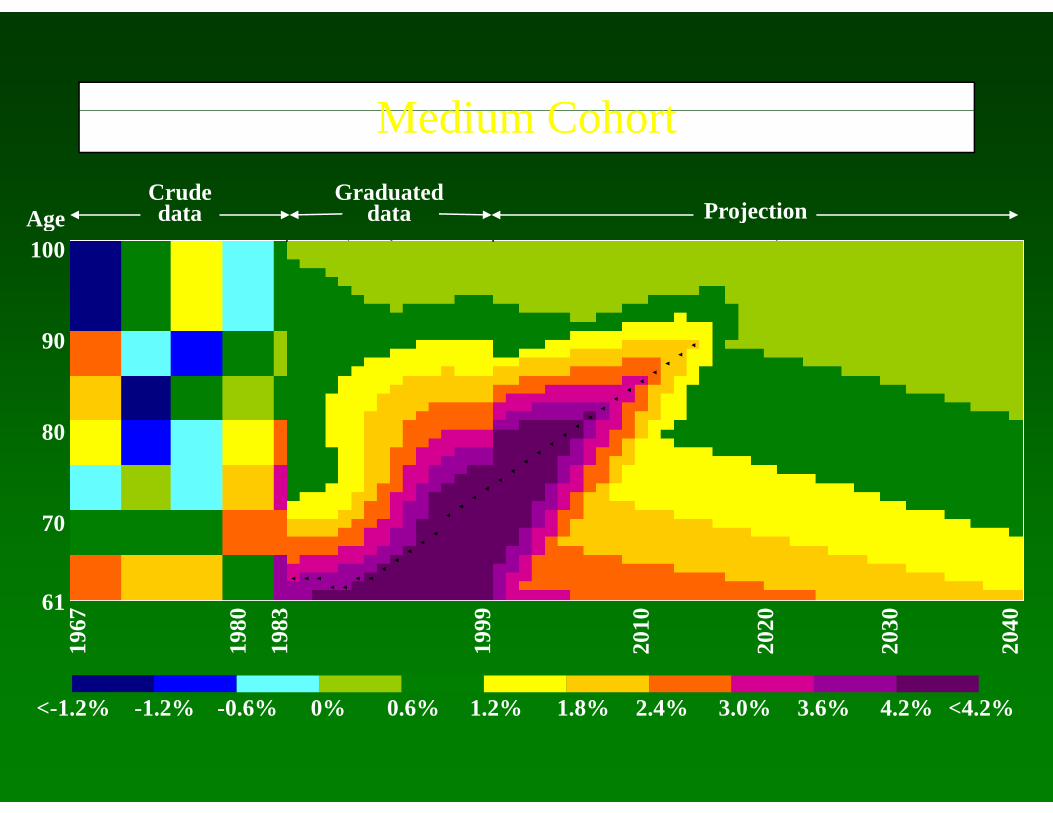

M di C h tMedium CohortCrude d t Projection

Graduated d t

100Age data Projectiondata

90

80

61

70

61

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%

1967

2040

1983

1999

2010

2020

2030

1980

<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

L C h tCrude d t Projection

Graduated d t

Long Cohort

100Age data Projectiondata

90

80

61

70

61

< 1 2% 1 2% 0 6% 0% 0 6% 1 2% 1 8% 2 4% 3 0% 3 6% 4 2% <4 2%

1967

2040

1983

1999

2010

2020

2030

1980

<-1.2% -1.2% -0.6% 0% 0.6% 1.2% 1.8% 2.4% 3.0% 3.6% 4.2% <4.2%

95

90

AgeKey

>4.2%

80

90%

4.2%

3.6%

703.0%

2.4%

601.8%

1.2%

500.6%

0% Contour map of40-0.6%

-1.2%

Contour map of 2D graduation

Assured lives30

Local Peak > 1.5%

<-1.2%Assured lives,

males + Medium Cohort

1948

1960

1970

1980

1990

1999

20

D i fi h 1992 99 d ?Does it fit the 1992-99 data?

All Office Pensioners 100A/E using the “92” Series projected with Medium Cohort improvement factors - Males

110110

100

tio

90

A/E

Rat

80 AmountsLi

100

A

701992 1993 1994 1995 1996 1997 1998 1999

Lives

1992 1993 1994 1995 1996 1997 1998 1999

Loyal Office Pensioners 100A/E using the “92” Series projected with Medium Cohort improvement factors - Males

110110

100

io

90

A/E

Rat

i

80 AmountsLi

100

A

701992 1993 1994 1995 1996 1997 1998 1999

Lives

1992 1993 1994 1995 1996 1997 1998 1999

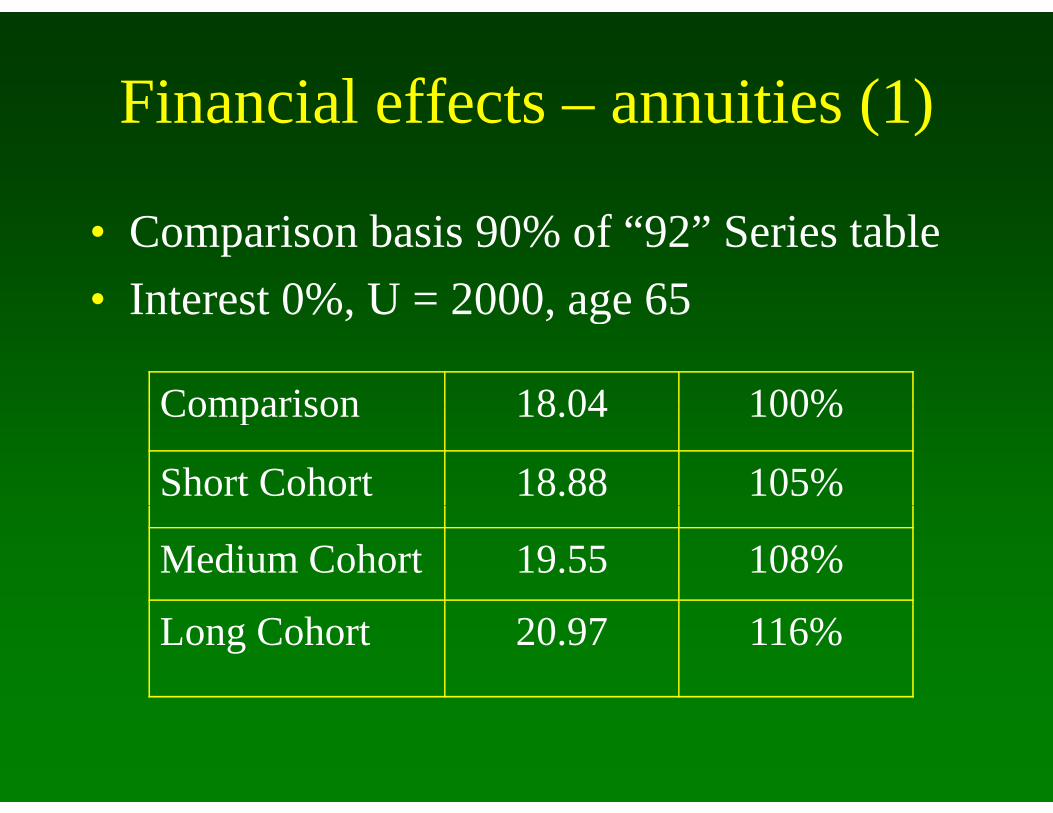

Financial effects – annuities (1)Financial effects annuities (1)

• Comparison basis 90% of “92” Series table• Interest 0% U = 2000 age 65Interest 0%, U 2000, age 65

Comparison 18 04 100%Comparison 18.04 100%

Short Cohort 18.88 105%

Medium Cohort 19.55 108%

Long Cohort 20.97 116%

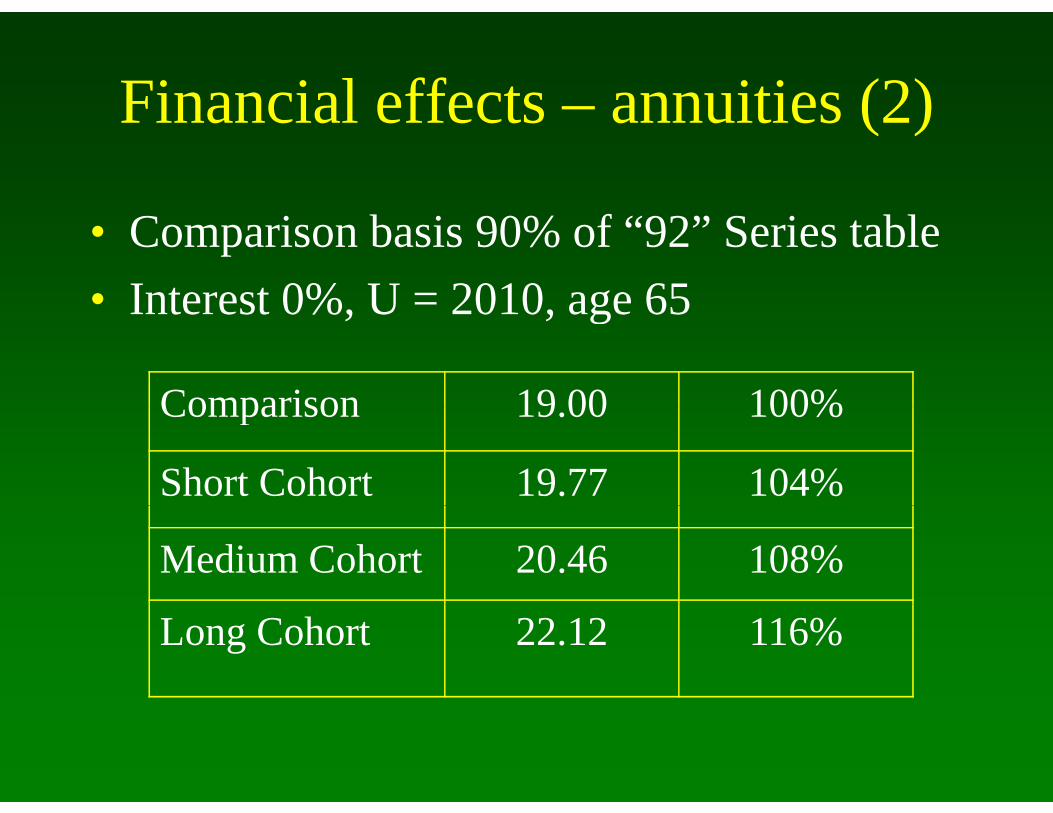

Financial effects – annuities (2)Financial effects annuities (2)

• Comparison basis 90% of “92” Series table• Interest 0% U = 2010 age 65Interest 0%, U 2010, age 65

Comparison 19 00 100%Comparison 19.00 100%

Short Cohort 19.77 104%

Medium Cohort 20.46 108%

Long Cohort 22.12 116%

Financial effects – annuities (3)Financial effects annuities (3)

• Comparison basis 90% of “92” Series table• Interest 3% U = 2000 age 65Interest 3%, U 2000, age 65

Comparison 13 08 100%Comparison 13.08 100%

Short Cohort 13.61 104%

Medium Cohort 13.94 107%

Long Cohort 14.58 112%

Financial effects – annuities (4)Financial effects annuities (4)

• Comparison basis 90% of “92” Series table• Interest 3% U = 2010 age 65Interest 3%, U 2010, age 65

Comparison 13 65 100%Comparison 13.65 100%

Short Cohort 14.14 104%

Medium Cohort 14.48 106%

Long Cohort 15.24 112%

Expectation of life for males aged 60 in 2000

a(55)M29

1999

1999 lc

a(55)M

PA(90)M

PMA8025

27

Life

1992

1999 mc

1999 sc

PMA92

PMA92mc23

25

ctat

ion

of L

1980

1992

PMA92lc

PMA92sc19

21

Expe

c

1955

1968

1970

1980

1990

2000

2010

2020

2030

17

1955

2 2 2 2

Things not yet doneThings not yet done

• Amounts v Lives• Males v Females• Males v Females• Graduate crude improvement factors• Comparison with other countries• Medical experts• Medical experts• Causes of death• Demography• Projection techniques (1 s d ?)• Projection techniques (1 s.d.?)

Where to get CMIB papers?Where to get CMIB papers?

www actuaries org ukwww.actuaries.org.uk