c o m p a n ie s : fo rm a tio n a n d o p e ra tio n s

TRANSCRIPT

1

Chapter 16

Companies: formation and operations

PowerPoint presentation by Anne AbrahamUniversity of Wollongong

©2009 John Wiley & Sons Australia, Ltd

2

TYPES OF COMPANIES

• Limited companies– Proprietary companies– Public companies– Companies limited by guarantee

• Unlimited companies• No-liability companies• Special companies

– Investment– Banking– Life insurance

3

ADVANTAGES AND DISADVANTAGES OF THE CORPORATE ENTITY

• Advantages– Limited liability– Broad source of capital– Continuity of existence– Ready transferability of shares– Use of professional management– Potential income tax savings

2

What issues do you consider when advising a client on the most appropriate structure for

their business?

4

5

ADVANTAGES AND DISADVANTAGES OF THE CORPORATE ENTITY

continued

• Disadvantages– Greater governmental regulation– Separation of ownership and management

Under what circumstances would you advise a client to consider changing their business

structure?

6

3

7

FORMING A COMPANY

• Replaceable rules and constitution• Certificate of registration• The prospectus• Formation costs and share issue costs

8

ADMINISTERING A COMPANY

ShareholdersShareholders

Board of DirectorsBoard of Directors

Managing DirectorManaging Director

SecretarySecretary TreasurerTreasurerChief

FinancialOfficer

ChiefFinancialOfficer

General ManagerInfo Sys

General ManagerInfo Sys

General ManagerProd’n

General ManagerProd’n

9

ADMINISTERING A COMPANY continued

• Duties of the board of directors include– Protecting rights of shareholders– Setting officers’ salaries– Recommending and declaring dividends– Authorising long-term borrowing,

additional share issues and major capital projects

– Reviewing the system of internal control

4

10

EQUITY IN A COMPANY

• The equity of a typical company split into 3 major categories:– Share capital

• Fully or partly paid shares• Ordinary or preference shares

– Retained earnings• Accumulated losses

– Other reserves

11

ACCOUNTING FOR SHARE ISSUES

• Types of shares– Ordinary shares– Preference shares

• Payment for shares– Payable in full on application– Deposit payable on application and the

remainder on allotment– Part payment on application, part on

allotment, and remainder in one or more instalments or calls

12

Private share placements

• Money may be raised privately by prospective shareholders contributing funds to the company

Jul 1 Cash at Bank $100 000Share Capital $100 000

(Cash contributed to the company by its shareholders)

5

13

Public share issue, payable in full on application

• Shares issued via a prospectusExample

Brazil Ltd– Received applications for 100 000 shares– Issue price of $10 per share

Sep 30 Cash Trust $1 000 000Application $1 000 000

(Receipt of cash of $10 per shareon 100 000 shares)

14

Public share issue, payable in full on application continued

• Refund of excess application monies

Oct 30 Application XXXCash Trust XXX

(Refund of excess application moneyto unsuccessful applicants)

15

Public share issue, payable in full on application continued

• Allotment of shares

Oct 1 Application 1 000 000Share Capital 1 000 000

(Funds contributed for 100 000shares paid in full)

Oct 1 Cash at Bank 1 000 000Cash Trust 1 000 000

(Transfer of application moneyinto a general cash account)

6

16

Public share issue, payable by instalments

ExampleBrazil Ltd– Issues 100 000 shares on 15 September – Payable: $4 on application

$3 on 15 October$3 on 1 December

Sep 30 Cash Trust $400 000Application $400 000

(Receipt of cash of $4 per shareon 100 000 shares)

17

Public share issue, payable by instalments continued

• Allotment of shares

Oct 1 Application 400 000Share Capital 400 000

(Application fee of $4 on 100 000 shares )

Oct 1 Cash at Bank 400 000Cash Trust 400 000

(Transfer of application moneyinto a general cash account)

18

Public share issue, payable by instalments continued

• Amount due on allotment

• Receipt of allotment monies

Oct 15 Cash at Bank 300 000Allotment 300 000

(Cash received on allotment )

Oct 1 Allotment 300 000Share Capital 300 000

(Allotment fee of $3 payable on100 000 shares)

7

19

Public share issue, payable by instalments continued

• Amount due on call

• Receipt of call monies

Dec 1 Cash at Bank 285 000Call 285 000

(Receipt of call monies on 95 000 shares )

Nov 15 Call 300 000Share Capital 300 000

(Call of $3 payable on 100 000 shares)

20

Public share issue, payable by instalments continued

Reported on balance sheet:

Share Capital (100 000 ordinary shares called to $10) $1 000 000Less: Unpaid calls (5000 shares @ $3) 15 000Total share capital $ 985 000

21

UNDERSUBSCRIPTION AND OVERSUBSCRIPTION

• Undersubscription– Applicants for fewer shares than offered

• Oversubscription– Applicants in excess of shares– Treatment depends on constitution and

prospectus– Excess monies may be refunded or held

against future calls

8

22

Rights issue of shares

• An issue of new shares giving existing shareholders right to additional number of shares in proportion to current shareholding

• If renounceable, then 3 options:– Exercise rights and acquire more shares– Decline to exercise rights and let lapse– Sell rights on stock exchange

23

Rights issue of shares continued

• Example– Mexico Ltd– Planned to raise $4.2 million from existing

shareholders through a renounceable 1-to-6 rights issue

– Terms were 6 478 611 shares to be issue at 65c each

– Market price of company’s shares was 80c

Date Cash at Bank 4 211 097Share Capital 4 211 097

(Receipt of 65c per share on rightsissue of 6 478 611 share )

24

Bonus share issue

• An issue of shares to existing shareholders in proportion of their current shareholdings, at no cost to shareholder

• Reasons for bonus share issue– Provide ‘return’ to shareholder without

cash outlay– Capitalise reserves or retained earnings by

converting to share issue– Signal to capital market that company

expects good future profitability levels

9

25

Bonus share issue continued

• Assuming that a bonus issue of $60 000 is declared and paid out of general reserve, accounting entry is:

Date General Reserve 60 000Share Capital 60 000

(Payment of bonus share issue out ofgeneral reserve)

26

PREFERENCE SHARES

• Preferential treatment– Dividend distribution (@ fixed rate)– Distribution of assets on liquidation– Redemption

• Usually no voting rights• Debt or equity?

27

DIVIDENDS

• Distribution of cash or other assets• May be interim or final• Directors determine if dividend is payable

and fix amount, payment time and payment method

• Company must have sufficient cash or other assets to distribute to shareholders without putting undue strain on ability of company to continue to operate efficiently

10

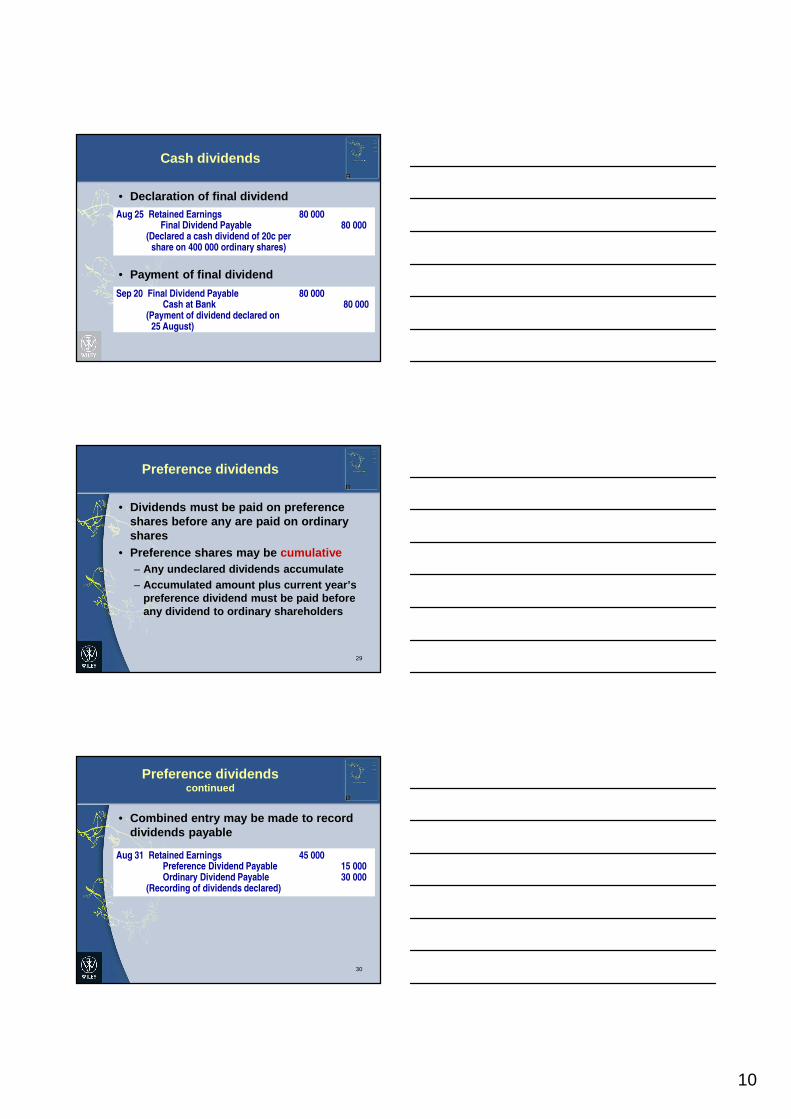

28

Cash dividends

• Declaration of final dividend

• Payment of final dividend

Sep 20 Final Dividend Payable 80 000Cash at Bank 80 000

(Payment of dividend declared on 25 August)

Aug 25 Retained Earnings 80 000Final Dividend Payable 80 000

(Declared a cash dividend of 20c pershare on 400 000 ordinary shares)

29

Preference dividends

• Dividends must be paid on preference shares before any are paid on ordinary shares

• Preference shares may be cumulative– Any undeclared dividends accumulate– Accumulated amount plus current year’s

preference dividend must be paid before any dividend to ordinary shareholders

30

Preference dividends continued

• Combined entry may be made to record dividends payable

Aug 31 Retained Earnings 45 000Preference Dividend Payable 15 000Ordinary Dividend Payable 30 000

(Recording of dividends declared)

11

31

Share dividends

• Pro rata distribution of additional shares to shareholders

• No effect on corporate assets or total equity

Jan 10 Retained Earnings 12 500Share Capital 12 500

(Distribution of 1-for-20 share dividendon 250 000 ordinary shares, at a valueof $1 each)

32

Share splits

• Share splits– Reduce the market price of shares– Make shares available to wider range of

investors

• No journal entry necessary because no change in balance in any of the equity accounts

33

Reserves

• Represent those items of equity other than capital contributed by owners

• Often created by ‘transfers’ from retained earnings

• Examples:– General reserve– Options reserve– Plant replacement reserve

12

34

Reserves

• Creation of reserve

Jun 30 Retained Earnings XXXReserve XXX

(Creation of reserve by appropriatingprofits)

35

Reserves continued

• Creation of revaluation reserve when non-current assets are revalued upwards

Jun 30 Asset XXXAccumulated Depreciation XXX

Revaluation Reserve XXX(Revaluation upwards of the carrying

amount of a non-current asset tofair value)

36

Reserves continued

• Disposal of reserves

Jun 30 Reserve XXXRetained Earnings XXX

(Transfer of reserve account back toretained profits)

13

37

INCOME TAX

• Deducted after all other expenses before arriving at final profit after tax

• Based on ‘taxable income’– Income Tax Assessment Act

• Methods for determining tax expense– Tax payable method– Tax-effect accounting method

38

PREPARING THE FINANCIAL STATEMENTS

Income statement

Statement of changes in equity

Balance sheet

Statement of cash flows

� Shows all relevant income and expenses to measure profit performance for the period

� Shows how equity accounts have changed in the period

� Shows assets, liabilities and equity on last day of period

� Shows sources and uses of cash resources during the current period

39