canned tuna in the middle east: a market in turmoil?infofish.org/v2/images/ptf2017/slide/day 2am - 6...

TRANSCRIPT

Canned Tuna in the Middle East: A market in turmoil? September 2017

Arnab Sengupta

Phoenix Commodities

Is Middle East an interesting market for canned tuna?

Parameters processors should take into account while entering ME

What should be done to gain more market share

This document aims to answer the following:

Key Questions

1

2

3

Table of Contents

Market Entry Opportunities

Communication Review

Tuna Market Overview

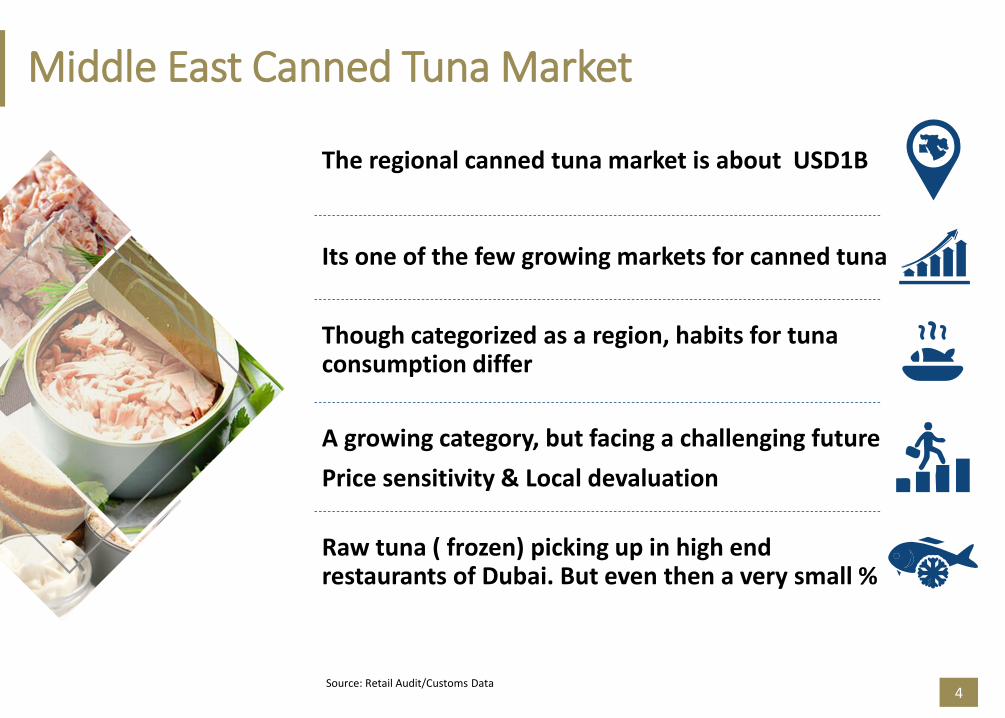

The regional canned tuna market is about USD1B

Its one of the few growing markets for canned tuna

A growing category, but facing a challenging future

Price sensitivity & Local devaluation

Raw tuna ( frozen) picking up in high end restaurants of Dubai. But even then a very small %

Though categorized as a region, habits for tuna consumption differ

4Source: Retail Audit/Customs Data

Middle East Canned Tuna Market

Middle East Tuna Market: Overview

5

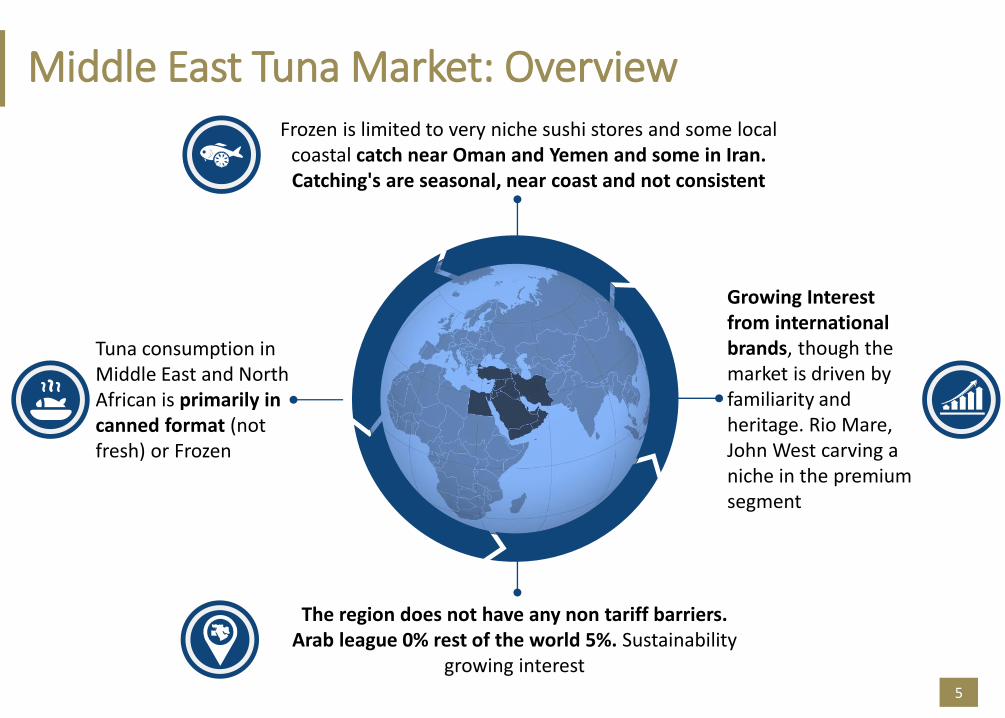

Frozen is limited to very niche sushi stores and some local coastal catch near Oman and Yemen and some in Iran. Catching's are seasonal, near coast and not consistent

Tuna consumption in Middle East and North African is primarily in canned format (not fresh) or Frozen

The region does not have any non tariff barriers. Arab league 0% rest of the world 5%. Sustainability

growing interest

Growing Interest from international brands, though the market is driven by familiarity and heritage. Rio Mare, John West carving a niche in the premium segment

Market Sizes – Canned Tuna

6

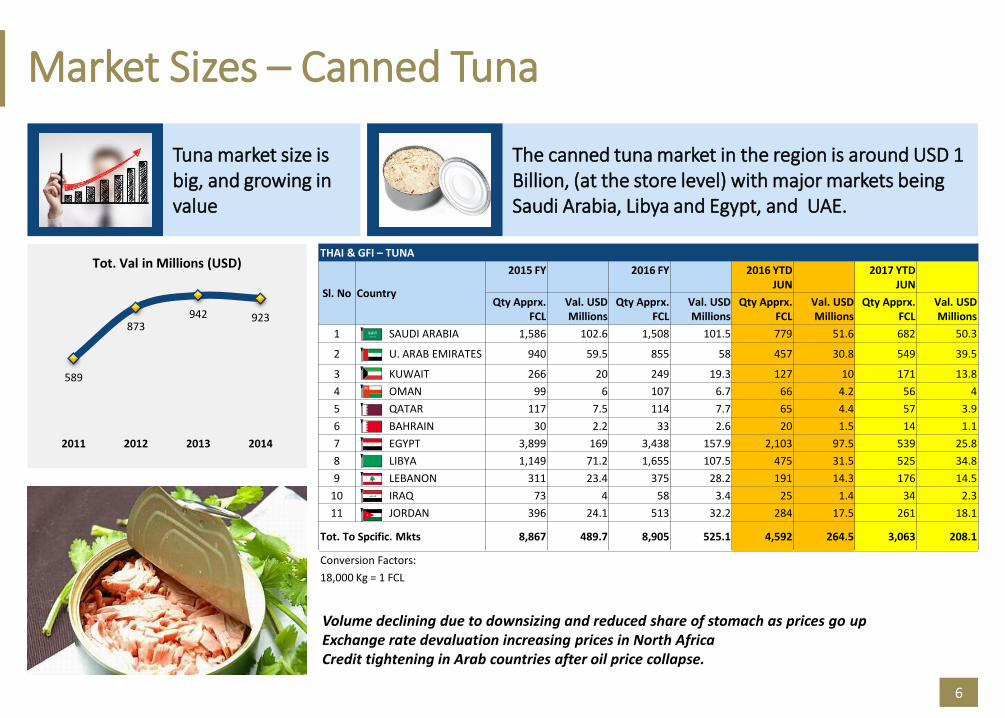

Tuna market size is big, and growing in value

The canned tuna market in the region is around USD 1 Billion, (at the store level) with major markets being Saudi Arabia, Libya and Egypt, and UAE.

589

873942 923

2011 2012 2013 2014

Tot. Val in Millions (USD)THAI & GFI – TUNA

Sl. No Country

2015 FY 2016 FY 2016 YTD JUN

2017 YTD JUN

Qty Apprx. FCL

Val. USD Millions

Qty Apprx. FCL

Val. USDMillions

Qty Apprx. FCL

Val. USDMillions

Qty Apprx. FCL

Val. USDMillions

1 SAUDI ARABIA 1,586 102.6 1,508 101.5 779 51.6 682 50.3

2 U. ARAB EMIRATES 940 59.5 855 58 457 30.8 549 39.5

3 KUWAIT 266 20 249 19.3 127 10 171 13.8

4 OMAN 99 6 107 6.7 66 4.2 56 4

5 QATAR 117 7.5 114 7.7 65 4.4 57 3.9

6 BAHRAIN 30 2.2 33 2.6 20 1.5 14 1.1

7 EGYPT 3,899 169 3,438 157.9 2,103 97.5 539 25.8

8 LIBYA 1,149 71.2 1,655 107.5 475 31.5 525 34.8

9 LEBANON 311 23.4 375 28.2 191 14.3 176 14.5

10 IRAQ 73 4 58 3.4 25 1.4 34 2.3

11 JORDAN 396 24.1 513 32.2 284 17.5 261 18.1

Tot. To Spcific. Mkts 8,867 489.7 8,905 525.1 4,592 264.5 3,063 208.1

Conversion Factors:

18,000 Kg = 1 FCL

Volume declining due to downsizing and reduced share of stomach as prices go upExchange rate devaluation increasing prices in North AfricaCredit tightening in Arab countries after oil price collapse.

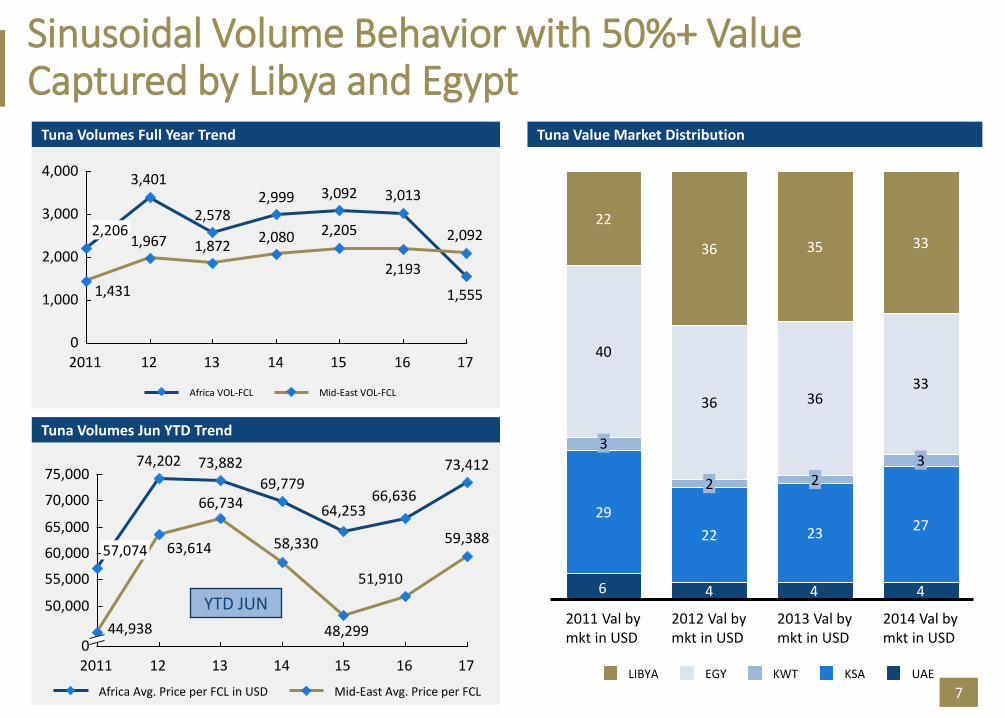

Tuna Volumes Jun YTD Trend

Sinusoidal Volume Behavior with 50%+ Value Captured by Libya and Egypt

7

Tuna Volumes Full Year Trend Tuna Value Market Distribution

4 4

29

22 23 27

40

36 3633

22

36 35 33

46

32

2013 Val by mkt in USD

3

2014 Val by mkt in USD

2

2012 Val by mkt in USD

2011 Val by mkt in USD

KSAEGY UAEKWTLIBYA

3,0133,0922,9992,578

3,401

1,555

2,0922,2052,0801,8721,967

2,193

1,431

2,000

4,000

3,000

0

1,000

16132011 1714

2,206

1512

Africa VOL-FCL Mid-East VOL-FCL

75,000

55,000

50,000

65,000

70,000

60,000

0

66,636

17

73,412

51,910

15

58,330

69,779

64,25366,734

73,882

63,614

2011

57,074

44,938

16

48,299

14

74,202

12 13

59,388

Mid-East Avg. Price per FCLAfrica Avg. Price per FCL in USD

YTD JUN

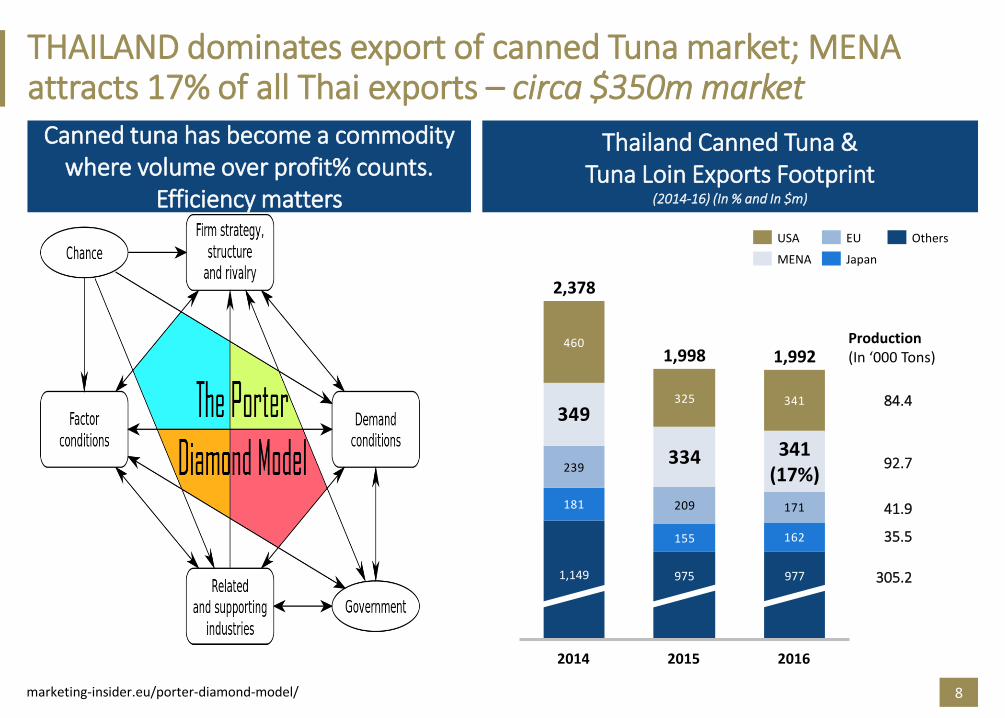

THAILAND dominates export of canned Tuna market; MENA attracts 17% of all Thai exports – circa $350m market

8

Thailand Canned Tuna & Tuna Loin Exports Footprint

(2014-16) (In % and In $m)

181

155 162

239

209 171

460

325 341

334

349

2016

1,992

341(17%)

977

2015

2,378

1,998

1,149

2014

975

EUUSA Others

JapanMENA

Production(In ‘000 Tons)

84.4

92.7

41.9

35.5

305.2

Canned tuna has become a commodity where volume over profit% counts.

Efficiency matters

marketing-insider.eu/porter-diamond-model/

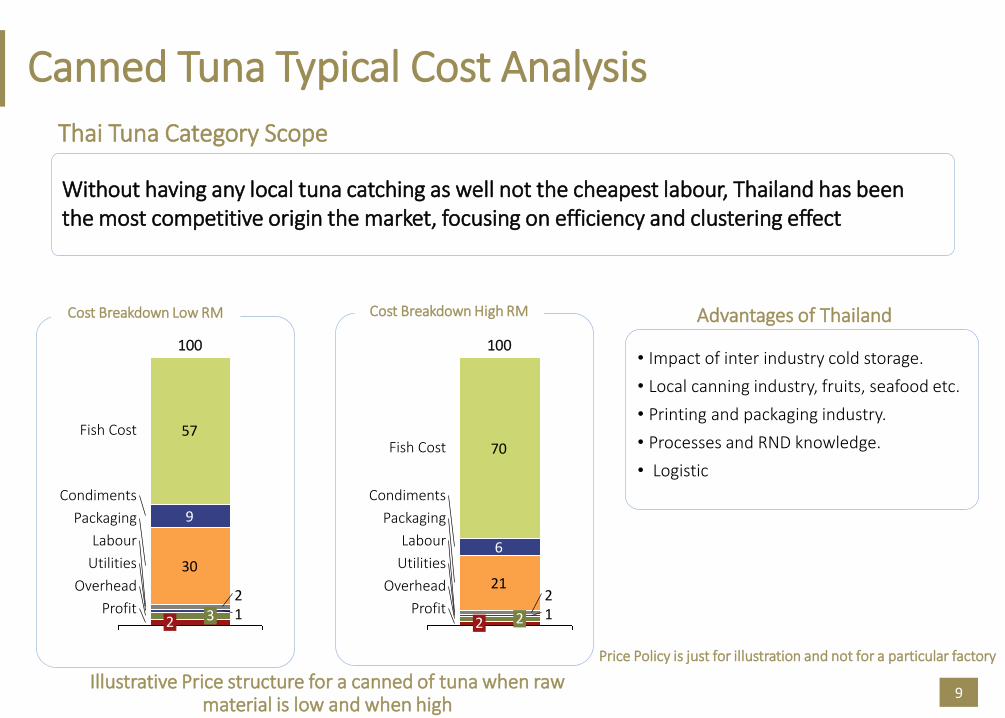

Canned Tuna Typical Cost Analysis

9

Thai Tuna Category Scope

Cost Breakdown High RM

12

21

6

70Fish Cost

Utilities

Condiments

Profit

Overhead

Packaging

Labour

100

2 2

Advantages of Thailand

• Impact of inter industry cold storage.

• Local canning industry, fruits, seafood etc.

• Printing and packaging industry.

• Processes and RND knowledge.

• Logistic

Price Policy is just for illustration and not for a particular factory

Cost Breakdown Low RM

12

30

9

57Fish Cost

Utilities

Condiments

Profit

Overhead

Packaging

Labour

100

2 3

Illustrative Price structure for a canned of tuna when raw material is low and when high

Without having any local tuna catching as well not the cheapest labour, Thailand has been the most competitive origin the market, focusing on efficiency and clustering effect

10

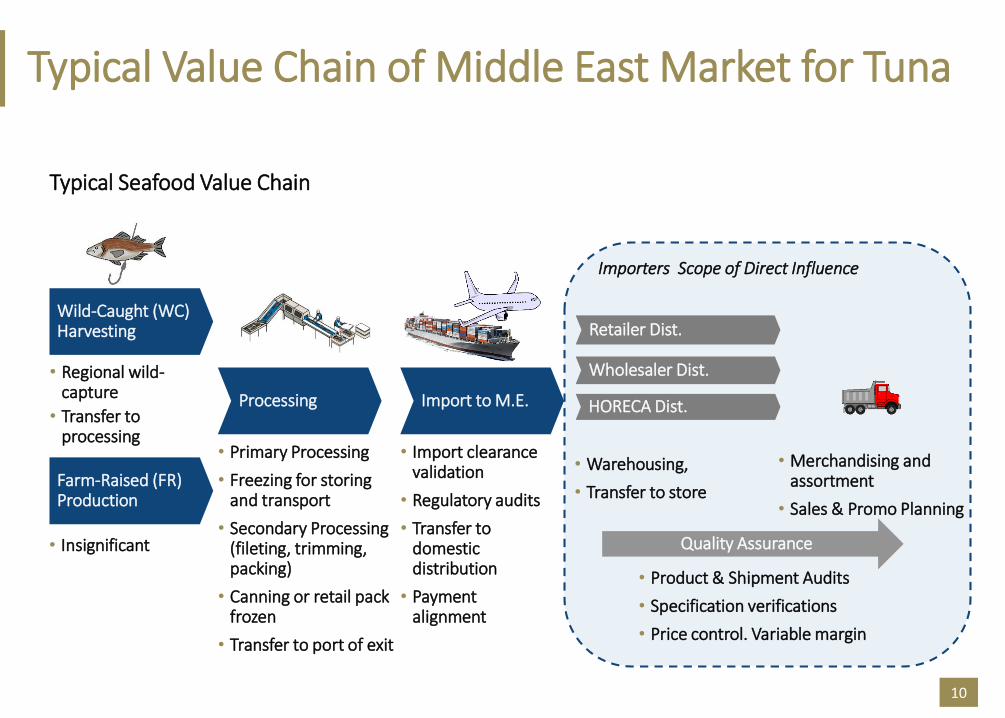

Typical Value Chain of Middle East Market for Tuna

Typical Seafood Value Chain

Wild-Caught (WC) Harvesting

Processing

Farm-Raised (FR) Production

Import to M.E.

Retailer Dist.

• Primary Processing

• Freezing for storing and transport

• Secondary Processing (fileting, trimming, packing)

• Canning or retail pack frozen

• Transfer to port of exit

• Import clearance validation

• Regulatory audits

• Transfer to domestic distribution

• Payment alignment

• Merchandising and assortment

• Sales & Promo Planning

• Warehousing,

• Transfer to store

• Regional wild-capture

• Transfer to processing

• Insignificant

Importers Scope of Direct Influence

Wholesaler Dist.

HORECA Dist.

Quality Assurance

• Product & Shipment Audits

• Specification verifications

• Price control. Variable margin

Within MENA, KSA & Egypt Captures 55-60% of Canned Tuna Market

11

ALL Canned Tuna Exports Footprint(2014-16) (In % and In $m)

510

17%

35%

15%

490

21%

5%

12%

5%

2%4%

2014

31%

24%

7%4%

494

10%

32%

26%

5%

15%

3%

4%

4%

24%

22%

3%

2013

11%

5%

588

2011

330

5%

1%

4%

2012

21%

20%

8%5%

31%

37%

1%

2015

11%

2%

Qatar

Egypt

Kuwait

Oman

KSA

UAE

Iraq

Libya

Jordan

Lebanon

Bahrain

KSA – Market Overview

12

Market Size+11% on volume +16% on value

Total Market (KSA) MAT'15 MAT'14 Diff-15/14

Sales Volume 1000KGS 25046.9 22878.7 9%

Sales Value SR 100000 8932.7 7727.1 16%

Solid: Biggest segment (68.4%), yet declining (-2.6ppts).

Chunks: Fastest growing (+1.1ppts), reaching 11%.

Flakes: Grew (+0.4%) to reach 11.9%.

Total MarketVOLUME SHARE

DiffVOLUME SHARE

DiffYTD'15 YTD'14

CHUNK 11 1.1 9 1

FLAKES 11.9 0.4 9.1 0.3

SOLID 68.4 -2.6 69.2 -2.7

READY TO EAT 2.9 0.5 5.4 0.7

SLICES 5.7 0.6 7.3 0.6

Egypt – Market Overview

Market Size-8.5% on volume -5.5% on value

Total Market MAT'15 MAT'14 Diff-15/14

Sales Volume 1000KGS 61901 72590 -8.5%

Sales Value LE 100000 25770 24655 +5.5%

Flakes: Biggest segment (53.2)% declined a few points (2.3%)

Solid: Growing segment (13.7%), growing

Chunks: Fastest growing (+1.1ppts), reaching 30.8%

Egypt currency has devalued ( 8.5 to 18) pushing the

prices in the market

13

Solid: Remains to be the largest cut at 54.9% (flat vs. YA), followed by

Chunks: at 18.8% (also flat), then

Flakes: at 16.2% (+0.4ppts)

UAE – Market Overview

14

Market Size+6% (volume and value)

Total Market MAT'15 MAT'14 Percentage Growth

Sales Volume 1000 KGS 3781.9 3554.5 6%

Sales Value 1000 AED 144165 132041 6%

Total MarketVOLUME SHARE

DiffYTD'15 YTD'14

SOLID 54.9 55.0 -0.1

CHUNK 19.8 18.7 0.0

FLAKES 17.2 15.8 1.4

READY TO EAT 7.9 7.6 0.3

SLICES 1.4 2.8 -0.4

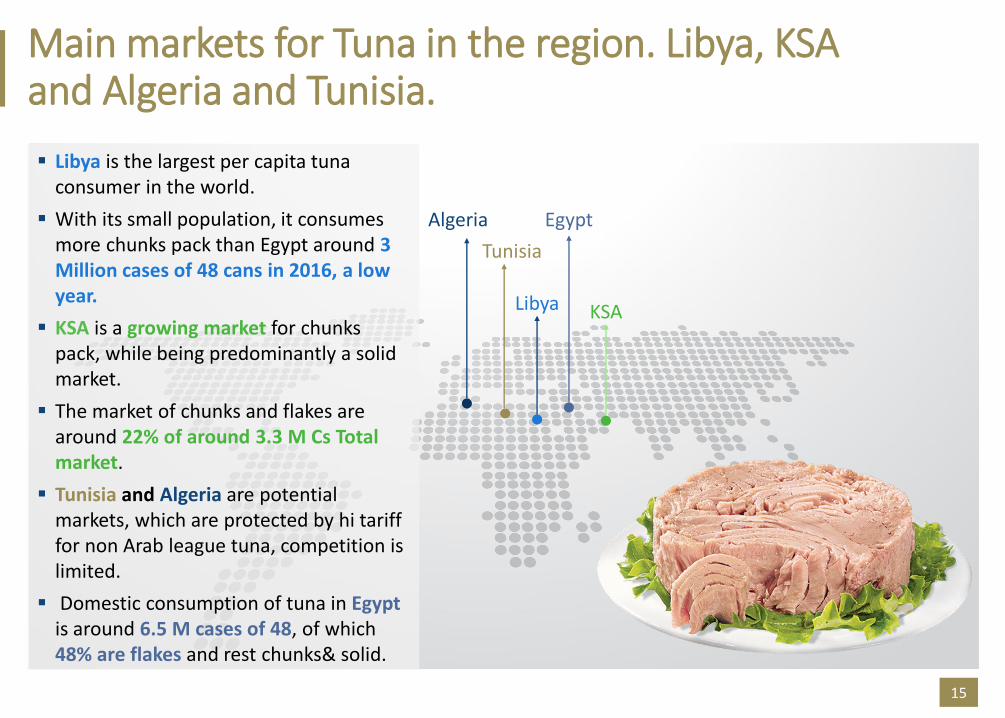

Main markets for Tuna in the region. Libya, KSA and Algeria and Tunisia.

15

Libya is the largest per capita tuna consumer in the world.

With its small population, it consumes more chunks pack than Egypt around 3 Million cases of 48 cans in 2016, a low year.

KSA is a growing market for chunks pack, while being predominantly a solid market.

The market of chunks and flakes are around 22% of around 3.3 M Cs Total market.

Tunisia and Algeria are potential markets, which are protected by hi tariff for non Arab league tuna, competition is limited.

Domestic consumption of tuna in Egyptis around 6.5 M cases of 48, of which 48% are flakes and rest chunks& solid.

Tunisia

Libya KSA

Algeria Egypt

16

Opportunities in the Middle East Market

Seafood Category Overview

Sourcing Process

• Tuna pricing is driven by commodity index hence spot purchased in favorable periods

• A mix of and spot buy are popular. Usually contacts are in 20 fcl or 2 fcl lots

ME Internal Demand

• Market demand's cheap source for protein. Tuna satisfy key criteria

• Devaluation of regional currencies in North Africa.

• Demand of tuna at the HORECA level

• Demand falling, lead by North Africa

Market Outlook

• Canned tuna market in Middle East has seen more than 15% dip this year due to currency.

• Frozen Fresh tuna demand increasing in GCC.

• Pet food market in UAE 65% of human food

Benefits Potential

Key Strategic Initiatives

~12-15 M USD

Low hanging fruits

Restaurant Items

• Focus on Horeca needs. Ready to serve sushi, pouch tuna, opportunity to consolidate

Pet Food

• Hit directly, high margin category. Allowing for efficiency gaps

Tuna

• Efficiency of production, work on ancillary business. Packaging and printing technology.

• Catering size opportunities

Consumer Insights

Tuna Category is Driven by Familiarity Mainly by BRAND CONSIDERATION Driving BRAND EQUITYEquity Drivers For Tuna

Sources of

Brand Equity

Industry Norms

Awareness: 30% Consideration: 10% Associations: 60%

Awareness 11%

Consideration 64%

Association 25%Based on FMCG & Retail categories

Importance of Association Factors

LIGHT & HIGH QUALITY

HEALTHY & PROVIDES VALUE

AESTHETICS MEAT QUALITIES

8% 8% 7% 2%

18Source: Winning Brands Categories

2% 2%14%

25% 27%28%

2%1% 3%14%

34%21%

27%

1% 3%17%

39%

17%24%

0%0% 0%

18%

36%23% 22%

0%0% 1%14%

42%

14%

29%

0%

Once or more a day 4 - 6 Times a week 2 - 3 Times a week Once a week Bi-Weekly Once a month Less than once amonth

W4 '14 W1 '15 W2 '15 W3 '15 W4 '15

Purchase & consumption frequency remain stable, so has the quantities purchased in each type of shopping trip WITH AN INCREASE IN QUANTITY PURCHASES IN THE TOP UP SHOPPING TRIP THIS QUARTER

19

CONSUMPTION FREQUENCYWEEKLY MEAN: 1.8 times

3% 6%

44% 41%

4%2% 4%

46% 46%

2%1% 6%

42% 49%

2%0% 2%

49% 47%

1%0% 2%

45% 51%

1%

Once or more a day 4 - 6 Times a week 2 - 3 Times a week Once a week Bi-Weekly

W4 '14 W1 '15 W2 '15 W3 '15 W4 '15

Cans of Tuna Bought Main Shopping Trip

Cans of Tuna BoughtTop Up Shopping Trip

Average 5 cans 5 cans

PURCHASE FREQUENCYWEEKLY MEAN: 1 time

Base: W3 ‘14: 201, W4 ‘14: 206, W1 ’15: 192, W2’ 15: 190, W3 ‘15:209, W4 ‘15:210Source: Q37ab, Q35ab

Consumer Perceptions on tuna

21

A protein within reach

It has a ritual and special way of

eating

Its valuable… its fish

It tastes good, and everyone eats

it in their special way

With some additions it

becomes a main meal

Perceived to be a VALUABLE variant of fish protein and meat that is affordable

It is a main and regular meal, that they happily arrange the appropriate setting for, to strengthen their bond with the product and create a pleasant eating experience.

Tuna is very versatile, and family members accustom it to their taste preferences using simple ingredients

The main trigger of purchase is the eating experience and its affordability, plus convenience and time saving

Who consumes it?

All Family members: Each one has his/her taste preferences, but everyone consumes tuna either alone, or with the family as a family dish

Who prepares it?

Usually, Mothers prepare tuna for the whole family. However, at occasions when family members eat it alone/quickly/as snack, they may prepare it for themselves.

When do they eat it?

Tuna can be eaten at lunch or dinner, or as a late snack. It can be put as a main dish during lunch/dinner, or as part of a dish (pasta, salad).

C1 and C2 class eat tuna in lunch, dinner, and late night snack.

B class consumers mainly consume Tuna for dinner (with other small dishes), and serve it at lunch only when it is an ingredient in another dish (pasta/salad).

Consumer – Consumption habits

23

Consumer – Purchase habits

24

How often?

High consumption families (C1 and C2): 3 times/week.

Lower consumption (B-class): 1-2 times/week.

How many cans opened per serving?

Depending on the occasion, the number of

cans varies. Generally, ONE can per family

member is the NORM.

When tuna is served as a main dish along with other sides/additives, 3 cans can be enough for a family of 4-5 members.

Communication Review

Communication: Tuna middle East

26

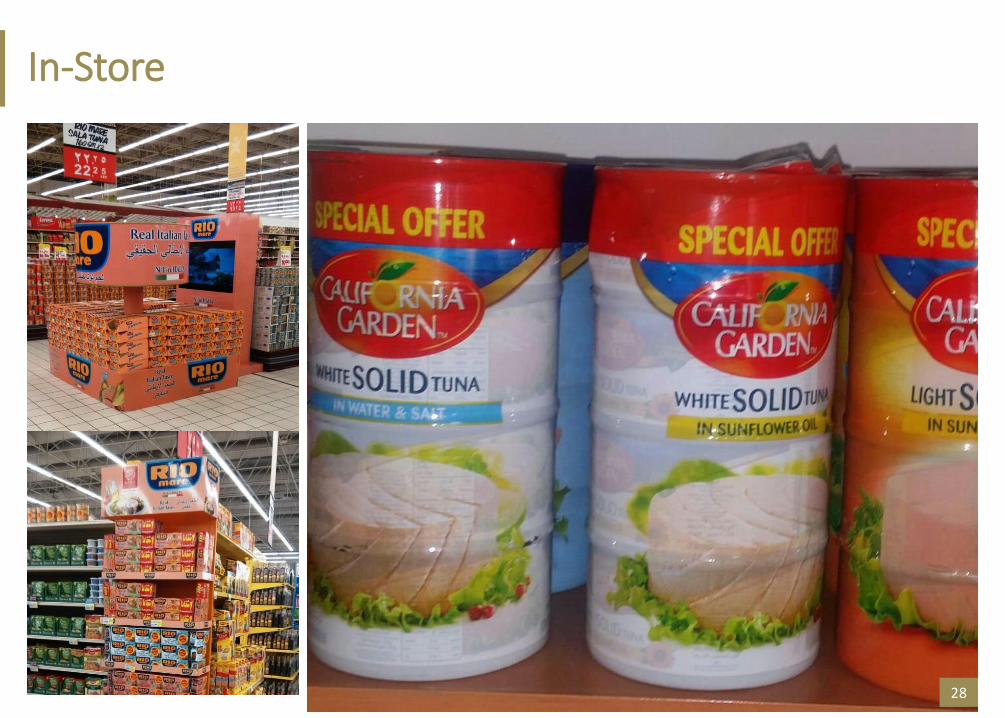

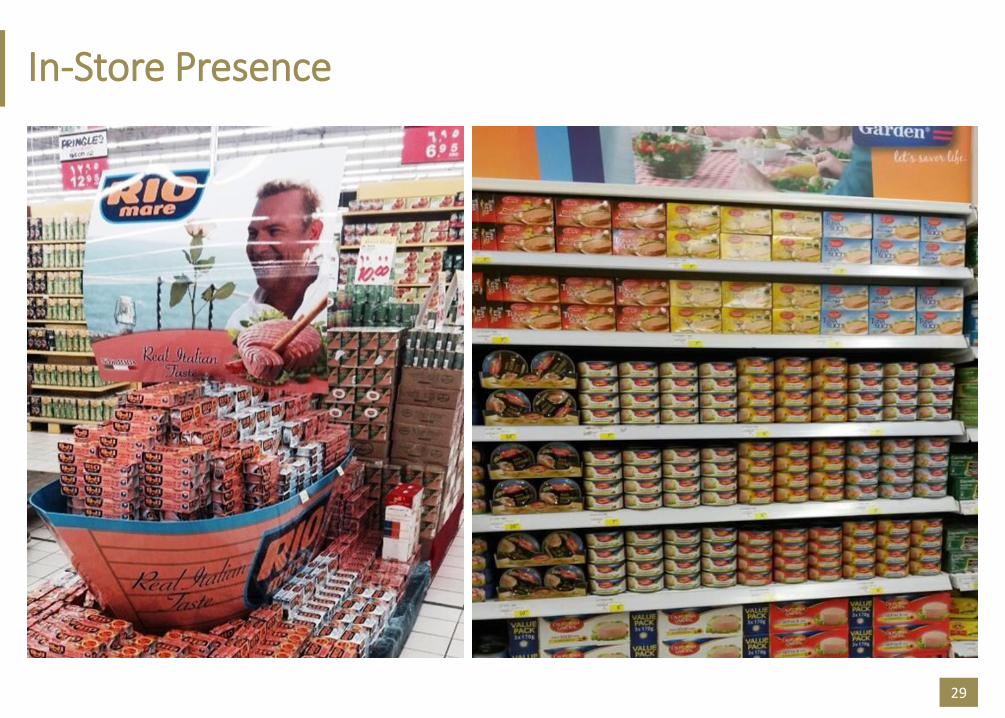

Merchandising support growing

ATL in certain premium brands,

category lead by Rio Mare

Internet based tools are gaining

popularity

Mostly promotions,

with secondary display

Activations

27

In-Store

28

In-Store Presence

29

From the Internet

Communication review

30

Going beyond display campaigns few tuna brands are building microsites on popular portals that included games/competitions as well as content sharing

and knowledge sharing about tuna

Digital

31

TV Copy – KSA

33

https://youtu.be/036k7Kgw-fg

Sunshine

https://youtu.be/s6kPaX0Jc3M

Goody

Recommendation

34Source: Ipsos Pan Arab-GCC 2012- 2013

• Middle East is big enough and easy enough to enter to make it a market of focus, for new origin for canned tuna. No preapproval needed. Basic Cordex specs followed

• All variants/ quality finds a market here

• Price competitiveness being paramount in large part of the market, current high price of tuna gives a good opportunity to beat Thailand advantage of clustering

• Regional semi-govt. groups could market, freshness of regional tuna, sustainability, at the grass route consumer level, while demonstrating the quality and texture of the product. ( eg. Australia Meat Work at retail level)

• Focus on high value & profitable pet food and frozen fish market: Focus on a niche or a single market and create success

Thank [email protected]