catalyzing clean infrastructure investment veronique bishop world bank workshop on risk management...

TRANSCRIPT

Catalyzing Clean Infrastructure Investment

Veronique BishopWorld Bank

Workshop on Risk Management Tools in Carbon Finance

November 19-20, 2003

Outline

• Investment constraints

• How carbon finance can help

• Risk sharing

• Combining CF with other instruments

• Workshop objectives & organization

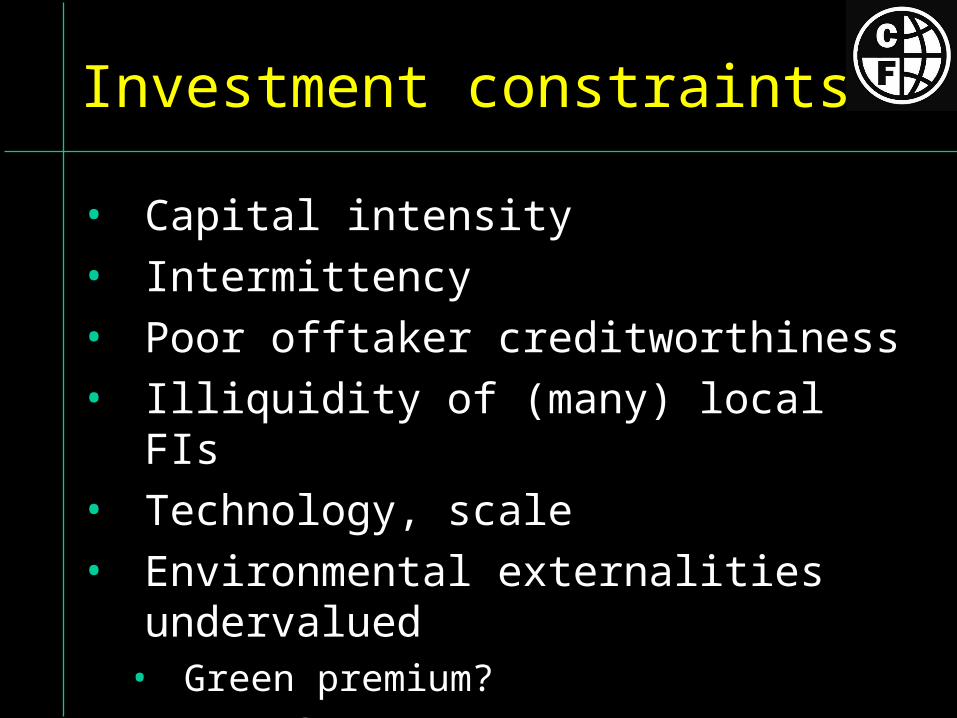

Investment constraints

• Capital intensity

• Intermittency

• Poor offtaker creditworthiness

• Illiquidity of (many) local FIs

• Technology, scale

• Environmental externalities undervalued• Green premium? • Kyoto?

Capital intensity

• [Chart showing discounted cost per kWh for range of generation sources]

How carbon finance can help

• Increased cash flow boosts returns

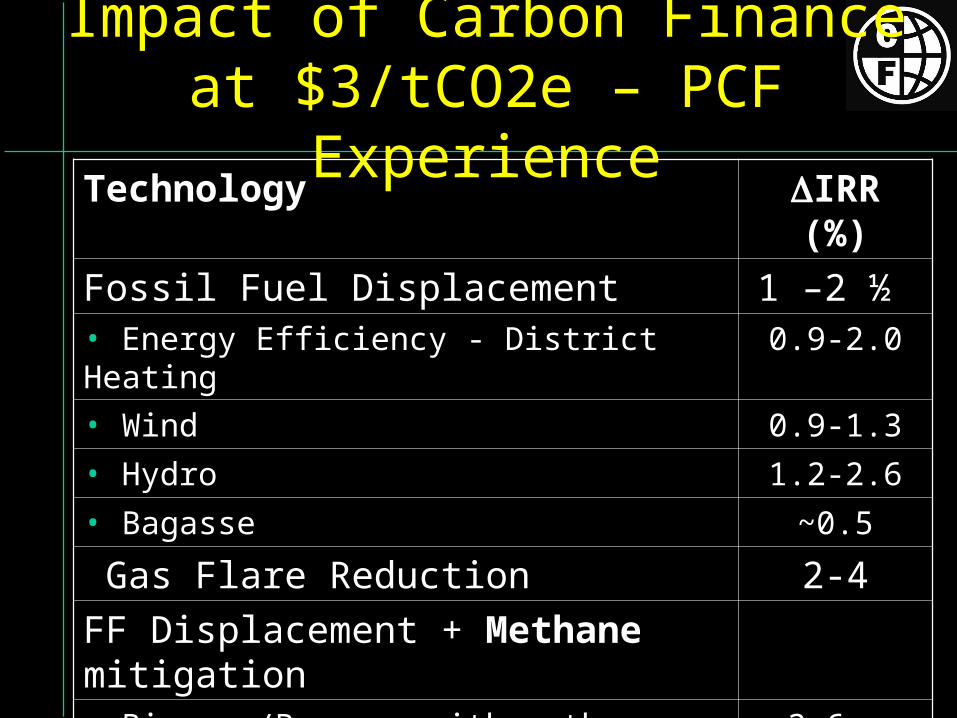

Impact of Carbon Finance at $3/tCO2e – PCF Experience

Technology IRR (%)

Fossil Fuel Displacement 1 –2 ½ • Energy Efficiency - District Heating 0.9-2.0

• Wind 0.9-1.3

• Hydro 1.2-2.6

• Bagasse ~0.5

Gas Flare Reduction 2-4

FF Displacement + Methane mitigation• Biomass/Bagasse with methane kick 3.6 - >5.0

• Municipal Solid Waste with methane kick >5.0

Annual Data Uganda Costa Rica Chile

off-grid grid grid

ERs (000 t) 49 61 79-138*

Net Gen.(GWh) 30 75 160

CO2 ERs/GWh 1664 807 494-860

ER (USc/kWh) 0.50 0.24

* Gas vs.

0.15-0.26

coal BL

Grid- vs. Off-grid Hydro ($3/tCO2e)

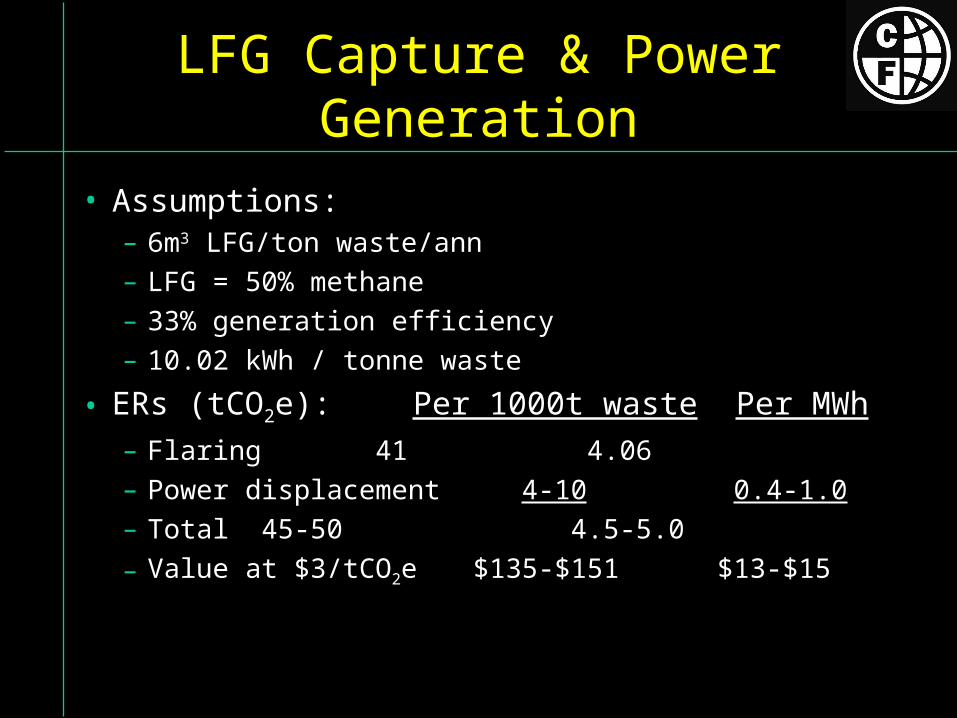

LFG Capture & Power Generation

• Assumptions: – 6m3 LFG/ton waste/ann

– LFG = 50% methane

– 33% generation efficiency

– 10.02 kWh / tonne waste

• ERs (tCO2e): Per 1000t waste Per MWh– Flaring 41 4.06

– Power displacement 4-10 0.4-1.0

– Total 45-50 4.5-5.0

– Value at $3/tCO2e $135-$151 $13-$15

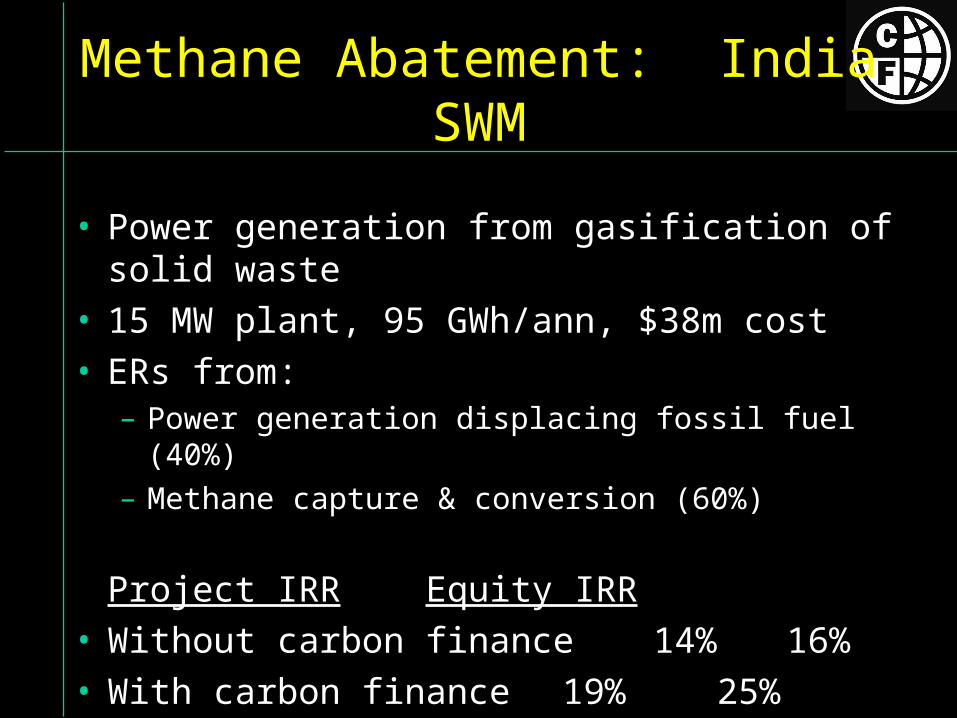

• Power generation from gasification of solid waste• 15 MW plant, 95 GWh/ann, $38m cost• ERs from:

– Power generation displacing fossil fuel (40%)

– Methane capture & conversion (60%)

Project IRR Equity IRR• Without carbon finance 14% 16%• With carbon finance 19% 25%

Methane Abatement: India SWM

Impact of Carbon Finance

0

5 0 0

1 2 3 4 5 6 7 8 9 10 11 12 13 14

Impact of Carbon Finance

0

5 0 0

1 2 3 4 5 6 7 8 9 10 11 12 13 14

• Increased cash flow boosts IRRs

• High quality cash flow reduces risk

Impact of Carbon Finance

• Increased cash flow boosts IRRs

• High quality cash flow reduces risk– OECD - sourced– $- or €- denominated– Investment grade payorEliminate currency convertibility or transfer risk

Impact of Carbon Finance

• Increased cash flow boosts IRRs

• High quality cash flow reduces risk– OECD - sourced – $- or €- denominated– Investment grade payorEliminate currency convertibility or transfer risk

• Financial engineering helps access capital markets

Impact of Carbon Finance

Host Country

LendersSponsor/ Project

CF

ERPA

Financing Agr.’s

Engagements re:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

Ltr. of Approval

ERs

Basic Deal Structure

ER payment

Debt service

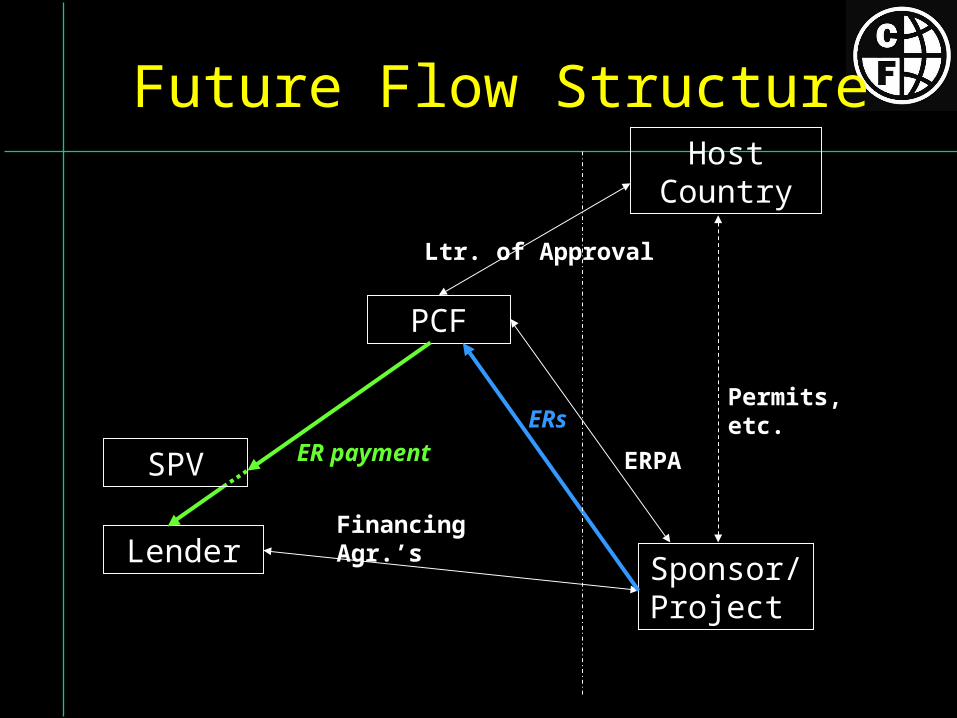

Host Country

Lender Sponsor/ Project

PCF

ERPA

Financing Agr.’s

Ltr. of Approval

ER paymentSPV

ERsPermits, etc.

Future Flow Structure

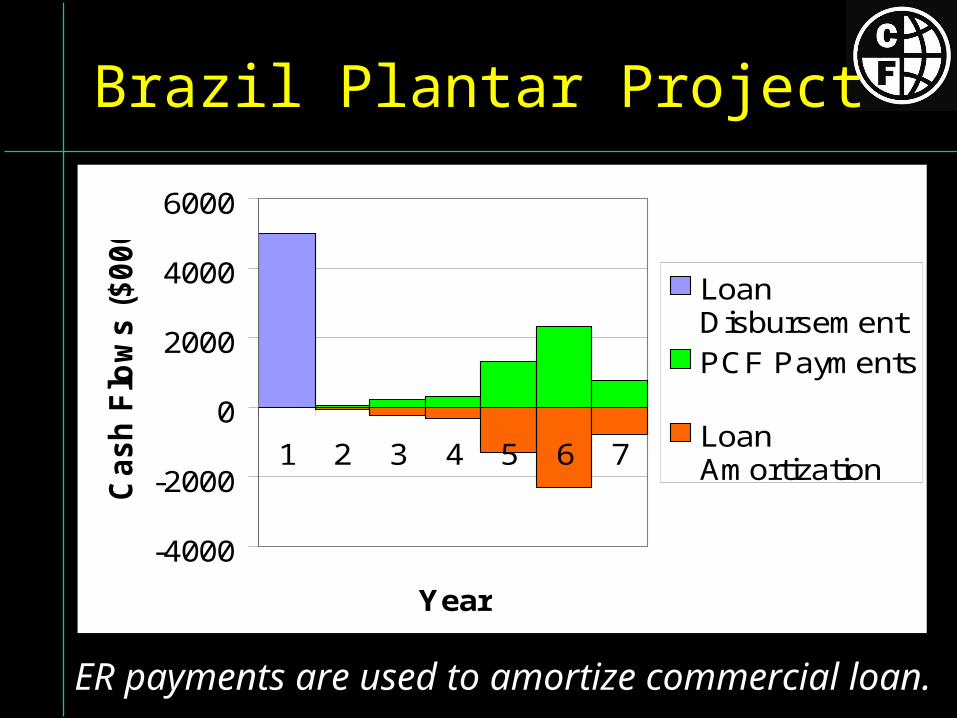

Brazil Plantar Project

-4000

-2000

0

2000

4000

6000

1 2 3 4 5 6 7

Year

Cash

Flo

ws (

$000)

LoanDisbursementPCF Payments

LoanAmortization

ER payments are used to amortize commercial loan.

Risk sharing in WB CF deals

• Project risk: assumed primarily by Seller• Kyoto & Baseline risk: primarily by CF

– Delivery = VERs (not CER/ERU)– JI VERs backed by AAUs– Early crediting– Switch to first track if eligible

• Market risk: assumed entirely by CF• Country risk: shared

– Letter of Approval (ERPA)– Host Country Agreement (JI)

Combining CF with other instruments

• Guarantees

• Subsidy funds

Host Country

LendersSponsor

PCF

ERPA

Financing Agr.’s

Engagements re:• Regulation (e.g. tariffs)• Kyoto Protocol compliance

Ltr. of Approval

ER payment

Project

Future Flow + Guarantee

SPV

ERs

Guaran-tor Counter-guarantee

Guarantee Agr.

Uganda

Lenders

Energy Fund

PCF

ERPA

Financing Agr.’s, Loan

Host Country Agr.

ER payment

Project

Uganda Hydro: Energy Fund

SPV

ERs

IDA

Credit Agr.

Concession, Subsidy

$

$

$

Conclusions

• Carbon finance can:Improve returns, esp. non-CO2 GHGsProvide a bankable revenue stream (like PPA)Reduce subsidy required for renewables

• ERPA minimizes lenders’ “Kyoto” exposure

• How can we increase lending:Improve ERPA?Combine with risk instruments?

Workshop objectives

• Break down risks faced by clean tech projects

• Examine risk instruments

• Consider how to tailor risk instruments to CDM/JI projects

• Agree to move forward

Workshop programme

• Overview

• Case studies

• Risk instruments– Plenary – Breakout groups– Rapportage

• Next steps

Thank you!

www.carbonfinance.org

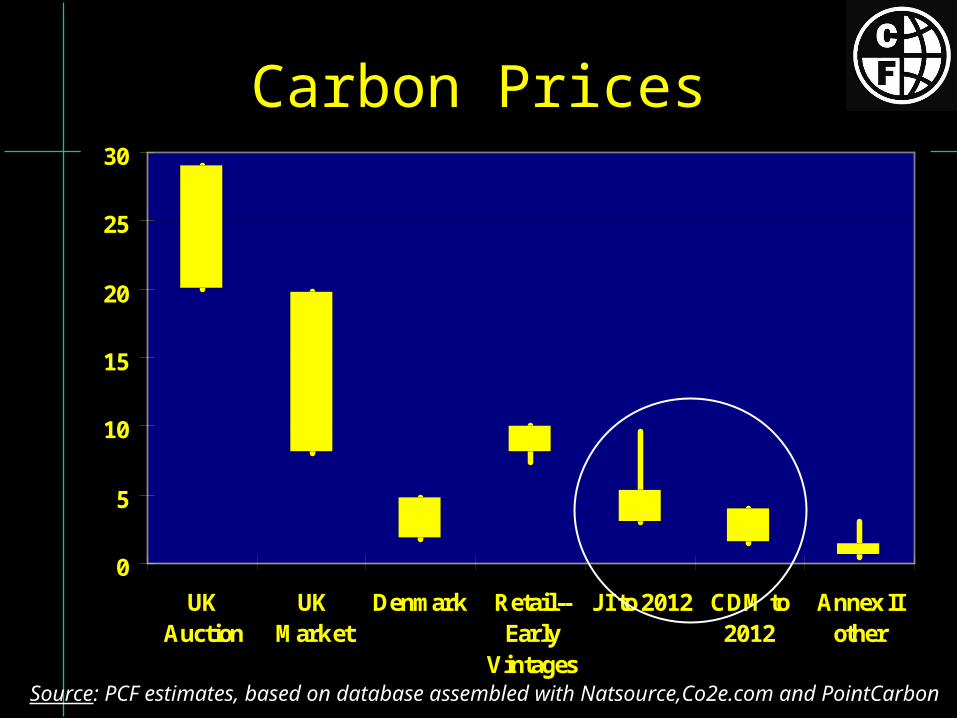

Carbon Prices

0

5

10

15

20

25

30

UKAuction

UKMarket

Denmark Retail--Early

Vintages

JI to 2012 CDM to2012

Annex IIother

Source: PCF estimates, based on database assembled with Natsource,Co2e.com and PointCarbon

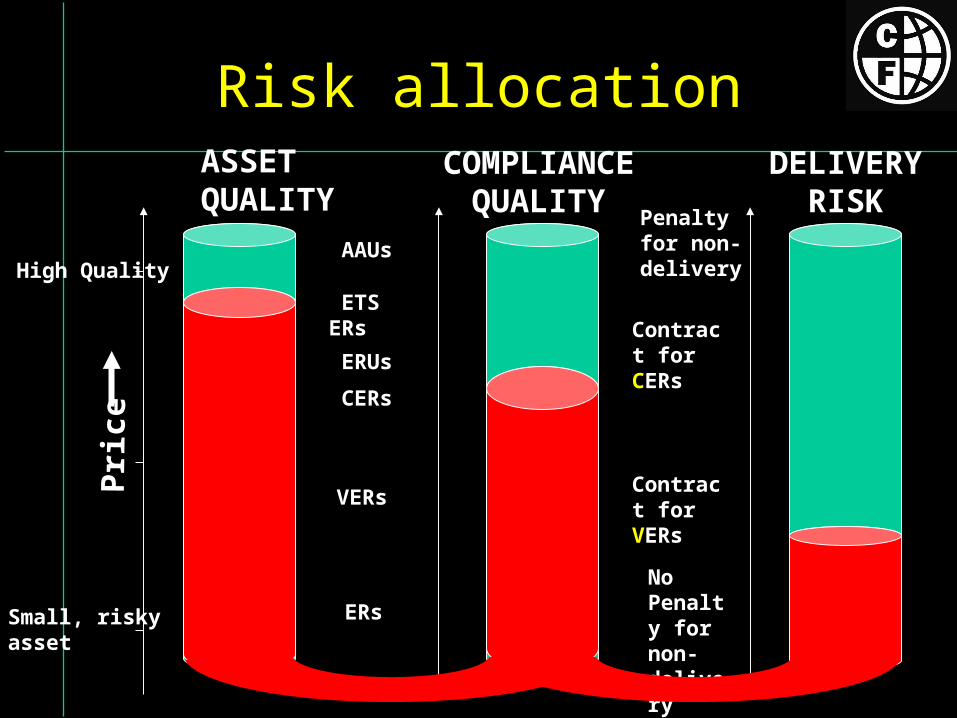

Small, risky asset

High Quality

ASSET QUALITY

CERs

VERs

COMPLIANCE QUALITY

No Penalty for non-delivery

Penalty for non-delivery

DELIVERY RISK

ERs

Risk allocation

AAUs

ERUs

Pri

ce

ETS ERsContract for CERs

Contract for VERs

What accounts for the price range?

• Supply & demand• Compliance quality• Asset quality• Allocation of risks

1. Supply and demand

• Willingness to pay:– price signals / announcements

• C/ERUPT tender signals• penalties: UK >= £20/tCO2e; Denmark max €5/tCO2e• tax benefits• expectations

– additional environmental/social benefits

• Market imperfections: – information – uncertainty esp. Russia, US– short-term supply/demand factors e.g. UK market

2. Compliance quality

• Government allowances• Eligibility: KP, ETS,“green certificates”• 2008-12 ERUs/CERs• Pre-2008 VERs

3. Asset quality

• Delivery risk: – quality of carbon asset (baseline risk)– financial viability of:

• project entity

• sponsor (recourse)

• offtaker (strength of offtake contract or market)

– construction period– contract duration

• Country risk

• Pricing as a function of:– Market conditions (current and projected)– Project, sector and country risk– Volatility of projected ERs (generally related to

baseline and resource risk)– Degree of overcollateralization– Whether KP has been ratified by host country– Upfront payments– Credit enhancement

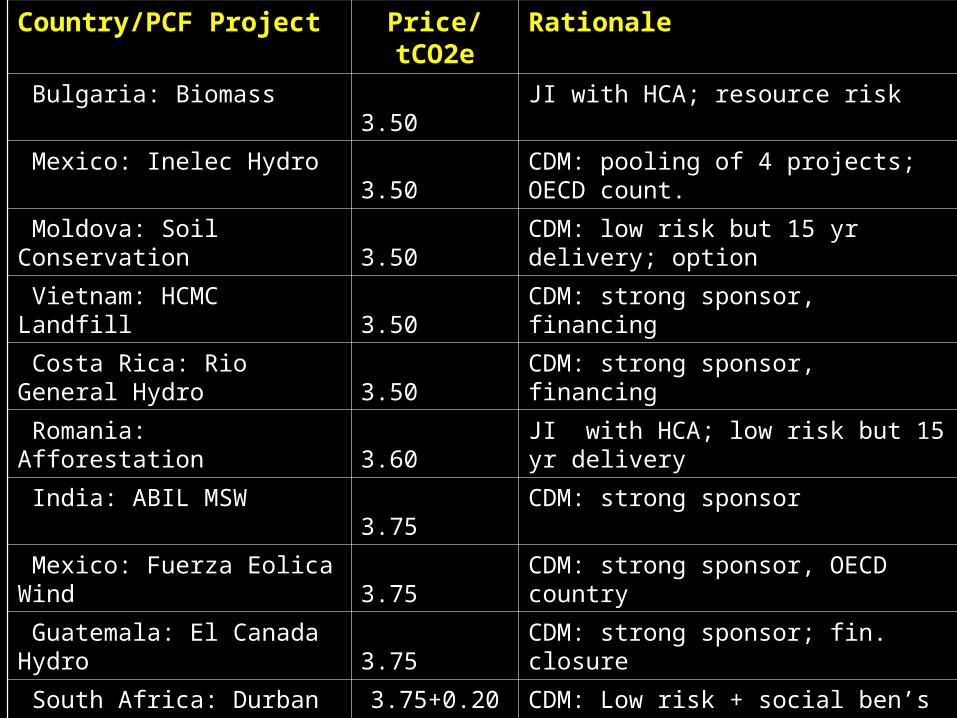

CF Carbon Prices

Country/PCF Project Price/tCO2e Rationale Volume 000tCO2e Value US$m

Bulgaria: Biomass 3.50 JI with HCA; resource risk 500 1.75

Mexico: Inelec Hydro 3.50 CDM: pooling of 4 projects; OECD count. 1,857 6.5

Moldova: Soil Conservation 3.50 CDM: low risk but 15 yr delivery; option 1,456+ opt =1,800 5.10

Vietnam: HCMC Landfill 3.50 CDM: strong sponsor, financing 2,500 8.75

Costa Rica: Rio General Hydro 3.50 CDM: strong sponsor, financing 1,800 6.30

Romania: Afforestation 3.60 JI with HCA; low risk but 15 yr delivery 777 2.80

India: ABIL MSW 3.75 CDM: strong sponsor 1,500 5.63

Mexico: Fuerza Eolica Wind 3.75 CDM: strong sponsor, OECD country 2,000 7.50

Guatemala: El Canada Hydro 3.75 CDM: strong sponsor; fin. closure 2,000 7.50

South Africa: Durban MSW 3.75+0.20 CDM: Low risk + social ben’s 3,800 15.01

Colombia: Wind 3.50+0.50 CDM + social ben’s 800 3.20

Bulgaria: District Heating 4.00 JI with HCA; ERPA with Municipality 1,000 3.50

Uganda: Small Hydro (2001) 3.00 CDM; semi-fixed payments 1,300 3.90

Brazil: Seq. & Biomass 3.50 CDM 1,514 5.30

Chile: Small Hydro –firm 3.50 CDM 1,000 3.50

Costa Rica: Renewables 3.50 CDM : umbrella; small projects 547 wind +172 hydro 1.92 +0.60

Chile: Small Hydro –option 3.50+0.75 CDM 750 3.19

Latvia LFGTE (2000) 4.11+ JI : Minimum guaranteed by Host Country 388-602 2.47

World BankCarbon Finance Vehicles

BioCarbon Fund

Netherlands CDM Facility

Development + Carbon = Carbon with a human face

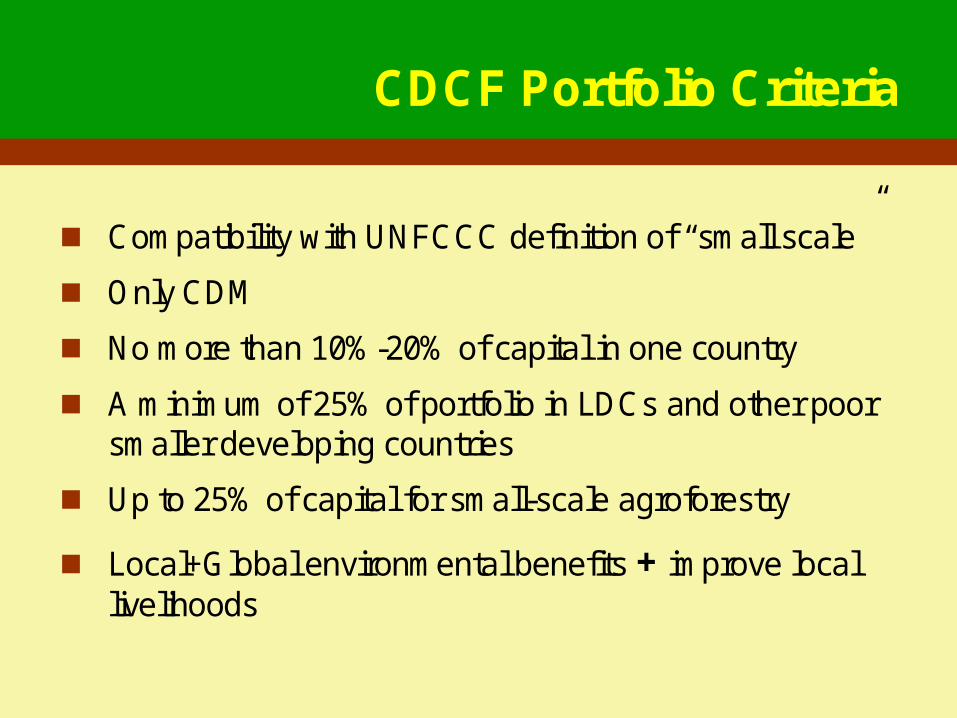

CDCF Portfolio Criteria

Compatibility with UNFCCC definition of “small scale”

Only CDM

No more than 10%-20% of capital in one country

A minimum of 25% of portfolio in LDCs and other poor smaller developing countries

Up to 25% of capital for small-scale agroforestry

Local+Global environmental benefits + improve local livelihoods

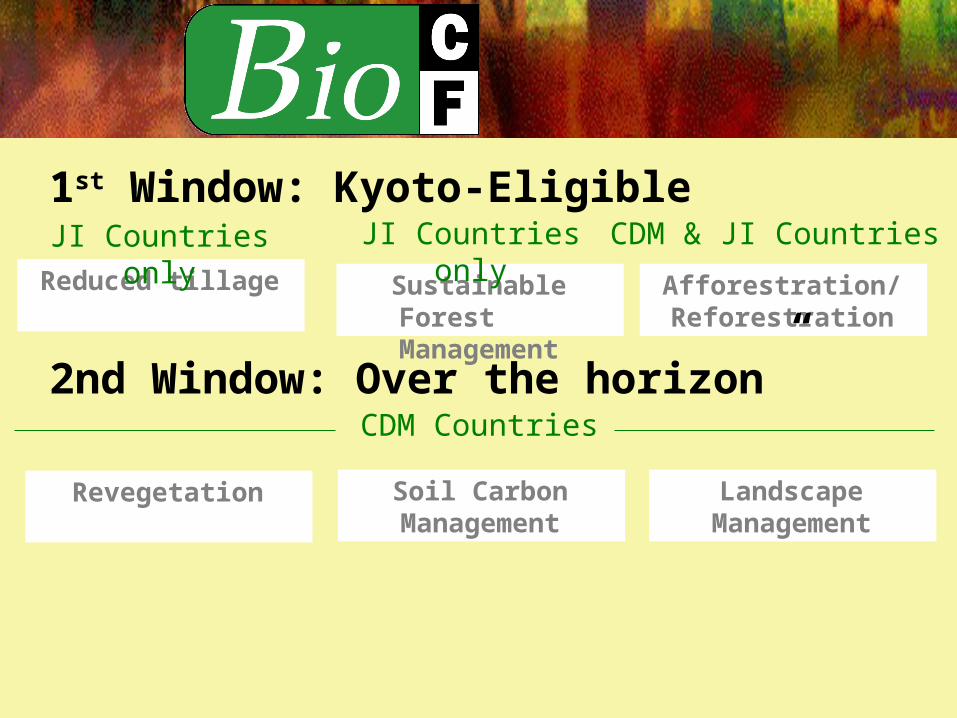

BioCarbon Fund

Harnessing the carbon market to sustain ecosystems and alleviate poverty

Reduced tillage

JI Countries only

1st Window: Kyoto-Eligible

Sustainable Forest Management

Afforestration/ Reforestration

CDM & JI CountriesJI Countries only

2nd Window: Over the horizon”

Revegetation Soil Carbon Management

Landscape Management

CDM Countries