ceat investor presentation nov'14

TRANSCRIPT

Investor Presentation

November 2014

Disclaimer

2

The information in this presentation has been prepared by CEAT Limited (the “Company”) and has not been independently verified. No representation or

warranty expressed or implied is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of such information or

opinions contained herein. The information presented or contained in these slides is current as of the date hereof and is subject to change without notice, and its

accuracy is not guaranteed. Neither the Company, nor any of its advisers or representatives, nor any of their respective affiliates makes any undertaking to

update any such information subsequent to the date hereof. This presentation should not be construed as legal, tax, investment or other advice. No

consideration has been given to the particular objectives, financial situation or particular needs of any recipient. Neither the Company nor any of its advisors or

representatives, nor any of their respective affiliates shall have any liability whatsoever (in negligence or otherwise) for any loss arising from the use of this

presentation or its contents or otherwise arising in connection with this presentation. By assessing this presentation, you are agreeing to be bound by the trailing

restrictions.

This presentation is intended for financial institutions and professional investors only and is not intended for distribution or reproduction to, or use by, retail

investors. This presentation is also not intended for distribution or reproduction to, or use by, any person or entity in any jurisdiction or country where such

distribution or use would be contrary to law or regulation.

The information in this presentation is given in confidence, and reproduction of this presentation, in whole or in part, or disclosure of any of its contents, without

prior consent of the Company, is prohibited. This presentation should be distributed and read in its entirety. This presentation remains the property of the

Company and on request must be returned and any copies destroyed.

This presentation is for information and convenient reference and does not constitute or form part of, and should not be construed as, any offer for sale or

subscription of, or solicitation of any offer to buy or subscribe for, any securities of the Company nor should it, or any part of it, form the basis of, or be relied on

in connection with, any contract or commitment whatsoever. This presentation does not constitute an offer of securities for sale in any jurisdiction, including

the United States, and any securities described in this announcement may not be offered or sold in the United States absent registration under the US Securities

Act of 1933, as amended or an exemption from such registration.

Please refer to the financial statements of the Company that have been filed with the stock exchanges and is available on the Company’s website. This

presentation is not intended to be fully inclusive and may not contain all of the information that you may consider material. This presentation contains historical

information of the Company that should not be regarded as an indication of future performance or results.

Certain statements in these slides may be considered forward-looking. These statements are based on management’s current expectations and are subject to

uncertainty and changes in circumstances. Actual results may differ materially from those included in these statements due to a variety of factors.

By accepting any copy of this presentation, you agree to be bound by the foregoing limitations.

Table of Contents

3

Indian Tyre Industry: Outlook 1

CEAT: An Overview2

Indian Tyre Industry: Robust Fundamentals

4

Domestic Tyre Industry: An Overview

235

293

355 367 382

FY'10 FY'11 FY'12 FY'13 FY'14

OEM

32%

Replacement

68%

MHCV

49%

LCV

7%

Cars &

UVs

18%

Tractors

11%

2/3

Wheelers

12%

Others

3%

Break up by End Use1 Break up by Customer1

Competitive LandscapeMarket Share2

MRF Ltd.

27%

Apollo Tyres

Ltd.

19%

JK Tyre & Inds.

Ltd.

13%

CEAT

12%

Others

29%

• The domestic tyre industry has grown at a CAGR of

12.9% driven by robust growth in the Indian

automobile industry

• Commercial vehicles (M&HCV and LCV) account

for > 50% of the domestic market

• Top 4 players account for ~ 70% market share

Turnover (Rs Bn)

Source CRISIL

1. Based on total tonnage of 15,92,000 in FY’14

2. Market share of FY’14 as per CRISIL based on turnover

OEM Production across Key Segments

OEM Demand is likely to rebound on Economic Revival

5

OEM

560

523

504

FY'12 FY'13 FY'14

9-11%

FY'15P

(000’ Tonnes) Growth

Replacement

978

1,0551,088

FY'12 FY'13 FY'14

5-7%

FY'15P

(000’ Tonnes) Growth

385281

222

FY'12 FY'13 FY'14

(‘000s)

M&

HC

V 6%

H1 FY'15 (YOY)¹

Growth rates

Improved Economic Growth and Consumer Sentiment will drive sales across categories (M&HCV, PC + UV

and 2/3 Wheeler)

PC

+ U

V 3,146

3,231

3,066

FY'12 FY'13 FY'14

(‘000s) Growth rates

3%

H1 FY'15 (YOY)¹

2/3

Wh

ee

ler

15,42815,744

16,879

FY'12 FY'13 FY'14

(‘000s) Growth rates

18%

H1 FY'15 (YOY)¹

Source CRISIL

1. Growth in H1 FY’15 is over H1 FY’14

Radialisation Trend

6

Radialisation in M&HCV and LCV Segment to gain momentum on back of improved road infrastructure , launch of multi-

axle vehicles and stricter regulation

Source: ATMA

M&HCV & Passenger Cars(%)

3%4%

6%

10%

12%

18%

22%

25%

95% 95%

97% 97%

98% 98% 98% 98%

80%

84%

88%

92%

96%

100%

0%

5%

10%

15%

20%

25%

30%

35%

FY'07 FY'08 FY'09 FY'10 FY'11 FY'12 FY'13 FY'14

M&HVC (LHS) Passenger Cars (RHS)

Raw Material Price Trend

7

3.0

1.7

184.6

123.3

100

120

140

160

180

200

1.5

2.0

2.5

3.0

3.5

Sep-12 Dec-12 Mar-13 Jun-13 Sep-13 Dec-13 Mar-14 Jun-14 Sep-14

International ($ per Kg) (LHS) Domestic (Rs per Kg) (RHS)

Rubber Prices have fallen due to weak global demand amidst an increase in supply

102.1

82.680.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

1-Sep-12 23-Dec-12 15-Apr-13 6-Aug-13 27-Nov-13 20-Mar-14 11-Jul-14 4-Nov-14

Natural Rubber

Brent Crude Oil (US$/bbl)

Source CRISIL

Source Bloomberg

Table of Contents

8

Indian Tyre Industry: Outlook 1

CEAT: An Overview2

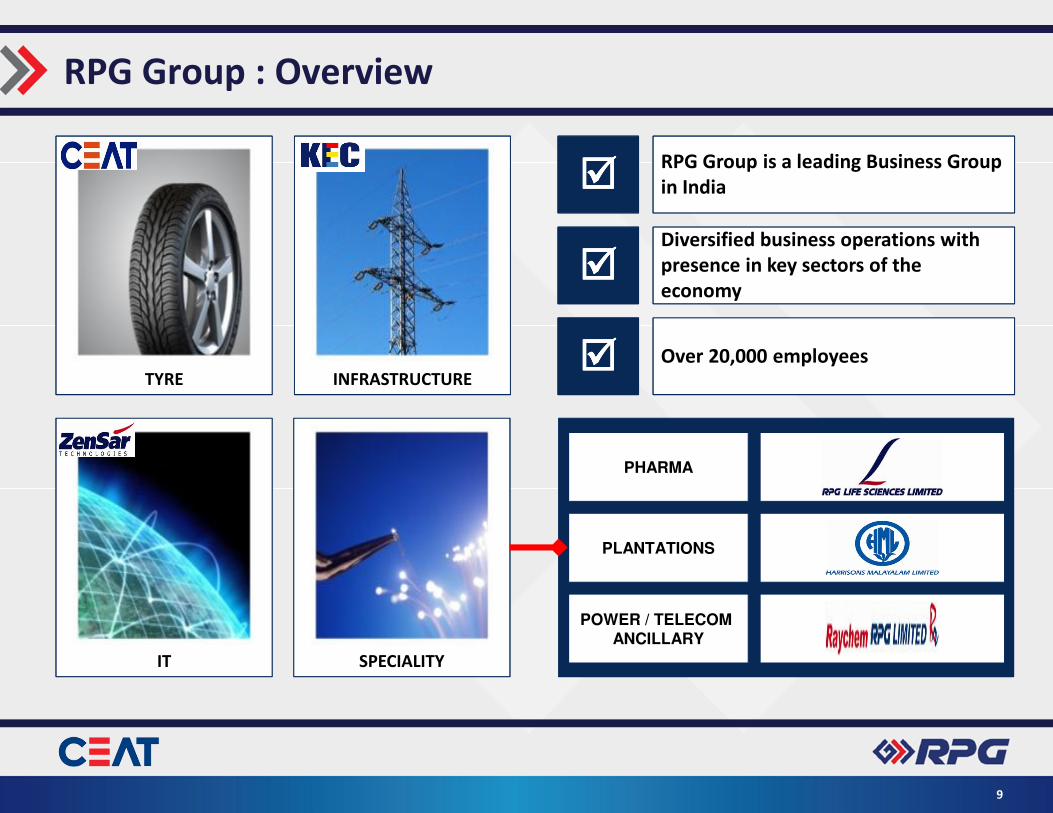

RPG Group : Overview

9

TYRE INFRASTRUCTURE

IT SPECIALITY

PHARMA

PLANTATIONS

POWER / TELECOM

ANCILLARY

����RPG Group is a leading Business Group

in India

����Diversified business operations with Diversified business operations with

presence in key sectors of the

economy

���� Over 20,000 employees

CEAT : Overview

10

CEAT Distribution Reach

India

Sri Lanka

88 countries where

CEAT Products were sold

in FY’14

• Leading Tyre Company in India with

over 50 yrs of presence

• 4th Largest Company in India with

Market Share of ~ 12%1

• Manufacturing Facilities in Bhandup,

Nashik and Halol

• Pan India Distribution Network

comprising of 3,500+ Dealers and 300+

CEAT Franchisees (CEAT Shoppe + CEAT

Hubs)

• Presence through 50% interest in a JV

with Kelani Tyres Ltd

• Strong presence in the Sri Lankan tyre

market

• Sri Lanka JV companies operates from

two manufacturing facilities in Sri Lanka

Note

1. Market share of FY’14 as per CRISIL based on turnover

3 Pronged Growth Strategy…

11

Effective Implementation of Business Strategy resulting in Improved Profitability

• Strong Brand Recall

• Barriers to Entry

• Proven Model in Sri Lanka

• Replicate in Bangladesh

• Competitive Advantage

• CEAT Global Brand

Passenger

segment1

Emerging

markets

Exports

Focus on

Profitable

Growth

Brand

Building

Channel

Expansion

R&D

Capability

Note

1. Consists of Two Wheeler, Passenger Cars and Utility Vehicles sub segments

…resulting in Favourable change in Business Mix

12

Gross Sales1 by Customer

Gradual shift towards profitable segments and radial tyres

Gross Sales1 by End Use Gross Sales1 by Tyre Type

Replacement

64%

OEM 16%

Exports 20%

FY’12

Replacement

61%

OEM 21%

Exports 18%

FY’14

Bias 87%

Radial 13%

FY’12

FY’14

Bias 81%

Radial 19%

Truck & Bus

53%

2/3 Wheeler

12%

LCV 10%

Cars & Uvs 6%

Farm &

Speciality 15%Last Mile 4%

FY’12

FY’14

Truck & Bus

46%

Two Wheeler²

17%

LCV 8%

Cars & Uvs 9%

Farm &

Speciality 14% Last Mile 5%

Note

1. Gross Sales represents Standalone Gross Sale of Products (Including excise Duty before discount)

Passenger Segment1: Overview and Strategy

13

• Achieved higher than industry growth in both the 2 Wheeler as well as PC + UV categories

• Partner of choice for many 2 Wheeler OEMs

• Increased share of business with leading passenger car OEMs mainly due to ability to produce low rolling resistant passenger car radial tyres

• Aim to further strengthen position by building brand loyalty through

• Product innovations and differentiated customer services

• Innovative marketing campaigns

• Optimum mix of in-house vs outsourced production

Gross Sales2 (Rs mn) Market Share3

6,088

10,652

FY'12 FY'14

2 Wheelers Passenger Car & Utility Vehicle

(PC + UV)

3,224

5,557

FY'12 FY'14

Notes1. Consists of Two Wheeler, Passenger Cars and Utility Vehicles sub segments2. Gross Sales represents Standalone Gross Sale of Products (Including excise Duty before discount)3. Market share data in FY’12 and H1 FY’14 is based on production (No of tyres) of CEAT and industry production as per ATMA for respective period

2 Wheelers Passenger Car & Utility Vehicle

(PC + UV)

5%

8%

FY'12 H1 FY'14

8%

14%

FY'12 H1 FY'14

Emerging Markets: Overview and Strategy

14

• Presence through CEAT Kelani Ltd : a 50% JV with Kelani Tyres Ltd

• CEAT Kelani Ltd has a strong presence in the truck, light truck, three-wheeler, two-wheeler and other radial tyre segments in Sri Lanka

• Sri Lanka JV companies operate from two manufacturing facilities in Sri Lanka with total capacity2 of 61 tonnes per day

• Manufacturing within Sri Lanka enables avoidance of import duty on tyres thereby enabling CEAT Kelani Ltd to competitively price

products

• Plans to replicate the Sri Lankan success in Bangladesh (through a 70:30 JV with AK Khan & Company Ltd) with the aim to cater to local

and eastern part of Indian market

• Setting up a manufacturing plant with an initial capacity of 65 tonnes per day that is likely to be operational by end CY’15

• Commencement of seed marketing campaign to prepare for product launch

• Imports from Bangladesh to India enjoy zero basic customs duty

Sri

La

nk

aB

an

gla

de

sh

Revenue

(SL Rs mn)

EBITDA1 (SL Rs mn) &

EBITDA Margin (%)

PAT

(SL Rs mn)

EBITDA

Margin 12.2% 20.1%

Net Worth

(SL Rs mn)

4,357

4,889

FY'12 FY'14

532

983

FY'12 FY'14

316

687

FY'12 FY'14

1,071

1,924

FY'12 FY'14

Notes

1. EBITDA = Profit before taxation + Depreciation and Amortization Exps + Finance Costs

2. Capacity refers to achievable capacity

Investment in Brand Building

Key Catalysts of Growth

15

“Monsoon Smart”“Monsoon Smart”

“Be Idiot Safe”“Be Idiot Safe” SUV Tyre CampaignSUV Tyre Campaign

Other InitiativesOther Initiatives

Effie Award Winning Campaigns Branded Campaign Others

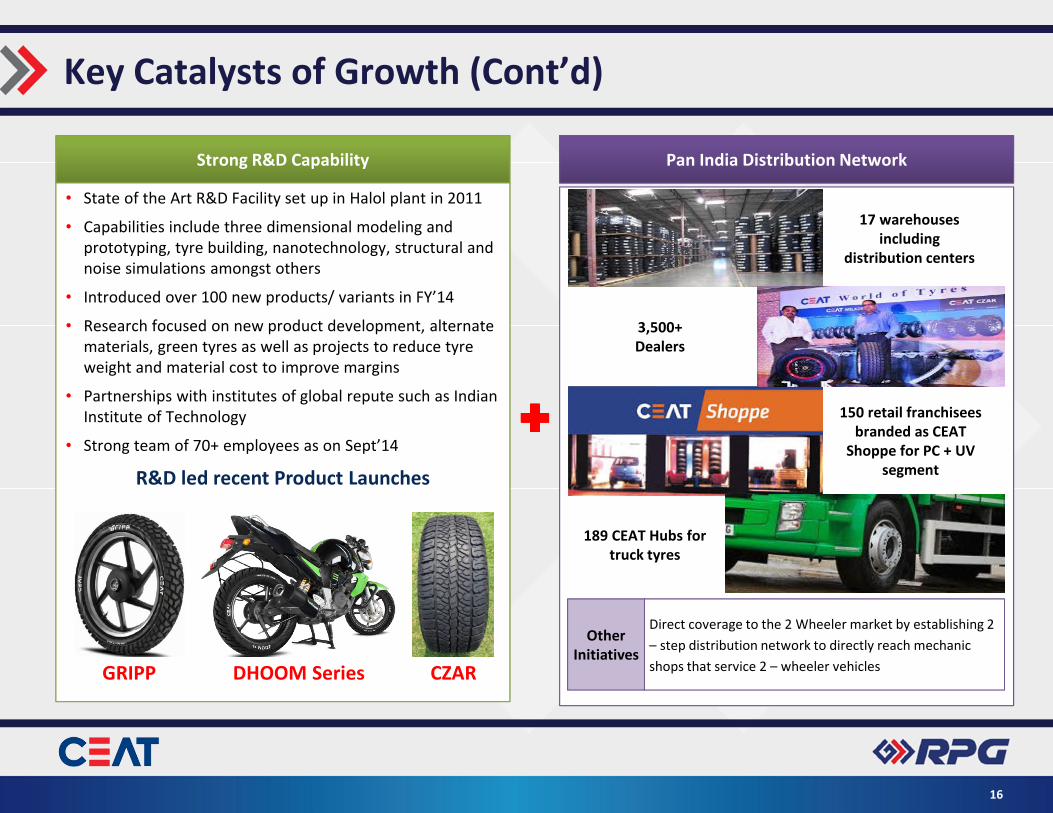

Key Catalysts of Growth (Cont’d)

16

����

Strong R&D Capability

• State of the Art R&D Facility set up in Halol plant in 2011

• Capabilities include three dimensional modeling and

prototyping, tyre building, nanotechnology, structural and

noise simulations amongst others

• Introduced over 100 new products/ variants in FY’14

• Research focused on new product development, alternate

materials, green tyres as well as projects to reduce tyre

weight and material cost to improve margins

• Partnerships with institutes of global repute such as Indian

Institute of Technology

• Strong team of 70+ employees as on Sept’14

GRIPPGRIPP DHOOM SeriesDHOOM Series CZARCZAR

R&D led recent Product Launches

Pan India Distribution Network

17 warehouses

including

distribution centers

150 retail franchisees

branded as CEAT

Shoppe for PC + UV

segment

3,500+

Dealers

Direct coverage to the 2 Wheeler market by establishing 2

– step distribution network to directly reach mechanic

shops that service 2 – wheeler vehicles

Other

Initiatives

189 CEAT Hubs for

truck tyres

Financial Overview¹

17

46,52750,522

55,540

29,003

FY'12 FY'13 FY'14 H1 FY'15

Growth 28.1% 8.6% 9.9%

2,737

4,379

6,579

3,128

FY'12 FY'13 FY'14 H1 FY'15

EBITDA

Margin 5.9% 10.9%

PAT and RoE2

(Rs mn)

182

1,202

2,712

1,340

FY'12 FY'13 FY'14 H1 FY'15

RoE 2.7% 15.3% 26.4%

Total Debt³ and Total Debt/ Net Worth(Rs mn)

11,049

8,288

10,202

7,914

FY'12 FY'13 FY'14 H1 FY'15

Total Debt/

Net Worth1.6x 1.0x 0.7x 1.1x

8.7% 11.9%

23.3%

Notes1. Numbers for FY12, FY13 and FY14 are based on the audited consolidated financial statements; numbers for H1FY15 are based

on the auditors’ review report on interim condensed consolidated financial statements2. EBITDA: Earnings before Depreciation & Amortization, Interest and Tax; RoE: Return on Equity on closing networth. For H1 FY’15

PAT has been annualized to compute RoE

3. Total Debt = LT debt + ST Debt excluding Current maturities of Long Term Debt

Net Revenue from Operations and its Growth(Rs mn)

EBITDA² and EBITDA Margin (Rs mn)

18

Y O UT H A N K