ceat: us launch strategy

TRANSCRIPT

Submitted by:

Team Tri-Us IIM Ranchi

Varun Jaiswal || Sayan Kar || Snehal Vasant Madne

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

Situational Analysis Strategic Direction Launch Strategy Financials

Strategic

Objectives

To understand the market

dynamics in terms of USA

economy demand drivers,

raw material costs and

competitive scenario

To proactively search for best

suppliers, understand buying

behavior, target the appropriate

market segment

To formulate detailed

entry strategy for 3 years

and lay down concrete

marketing plan

To understand and support

distribution & marketing

expenditures and create

financial roadmap for 3 years

Analysis • Rise in demand

• Fall in raw materials cost

• Lower labor costs in India

and reduced import

duties in India

• Robust equipment sales in

farming industry

• Small & large OTR segment

constitute maximum sales

• Actively seeking ecological

product

• Tie up with top 15

clients,

• Leverage on the

relationship with

Mahindra

• Differentiate with

dedicated Service

Program

• Projected year wise

market share & revenue

break up to be achieved

• BKT, with closest business

model has good revenue

growth

• CEAT has added

advantage of lower

capital intensity

Insights • Manufacturing Set Up in

India

• Enter value segment

• Focus on Farm, then

construction & mining

• Focus on the credit norm

payment period

• Green Marketing

• Enter Replacement Market

through clients & establish

OEM relationship

• One OEM in each

secto , utilize it s service center

• Exclusive dealer in

each state, 24*7

emergency service

Estimated marketing budget

is $1.6 Million for year 2016.

Year wise OTR revenue break

up is forecasted by projecting

year wise break up of market

share.

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

• Falling Natural Rubber

Prices globally

• Growth in replacement

segment coupled with

product mix

• Structural Shift

technology: cross ply to

radial tires

• Better trade relations,

after cheap Chinese tire

industry increased tariffs

Growth Drivers

• US Market GDP growth is poised to stabilize as per industry standards

• Revenue is expected to increase at an annualized rate of 3.5% per year to $ 3.0 billion USD

• Industry growth around 6.4% with OEM segment, while Replacement targeted to grow at 9% CAGR

• The tire industry is highly sensitive to fluctuations in raw materials prices

• Raw materials constitute 75% of the operational costs, 70% of the sales turnover

• Manufacturing Setup – India, since low cost labor and natural rubber input material availability

• As per forecasts, margins will expand on account of decline in rubber prices. (INR prices by 5-7%)

Takeaway: OEM demand expected to remain under pressure in short term whereas replacement demand

would continue to remain the growth engine in near term for US market.

31%

25% 16%

13%

8%

7%

Raw Material

Natural Rubber Synthetic Rubber

Fillers Chemicals

Steelcord Textile

Source: Michelin

Units

- Steady or up

Raw Material Costs

- Lower

Price Control

= Improved Margins

Net Result

Positive

Takeaway: Firestone and BKT have less number of products in their portfolio and still have

a very high M.S. This shows a focused strategy helps in this industry. Rather than going for

a wide variety of products CEAT should seek to build expertise in few application areas.

18%

34%

18%

14%

6%

5%

0

10

20

30

40

50

60

70

-5% 0% 5% 10% 15% 20% 25% 30% 35% 40%

Ag

ri.

- P

rod

uct

Mix

Market Share by Value

Strategic Groups

BKT

Firestone

Goodyear

Titan

Michelin

Alliance

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

Source: MTD Facts Issue 2015

• Titan has extensive focus on the farm equipment tires offering

• Goodyear focuses on safety & fuel efficiency

• Alliance provides customized solutions, heat & cut resistant thread compounds

• Firestone has a strong distribution presence in the US, via the Bridgestone network

• BKT has a large product mix for the farm equipment sector, and a strong M.S by value

18%

34%

18%

14%

6% 5%

6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

US Market - Farm

US Market - Farm

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

- The $3 billion U.S. OTR tire market

breaks down as follows:

• 69%, or $2.07 billion, for small

OTR (rim diameters of less than 25

inches)

• 15%, or $450 million, for large

OTR (rim diameters of 26 to 49

inches)

• 10%, or $300 million, for giant

OTR (rim diameters of 50 to 63

inches)

• 5%, or $180 million, for repair

materials (products used for the

repair of OTR tires)

Source: IBIS US Market Statistics Source: Tire Industry Association

Consructi

on

43% Mining

24%

Exports

23%

Agricultu

re

6%

Others

4%

OTR tire U.S - Revenue

Consruction Mining Exports

Agriculture Others

• Agriculture production is concentrated on a small number of large, specialized farms in rural areas where 15% of the U.S. population lives

• Tractor Sales in U.S Market is consistently better than the 5 Yr Average (2010-2014) figures

• Equipment sales in other relevant industries is not so robust

Source: Association of Equipment Manufacturers (September, 2015)

Target:

- Value Segment (Many Indian Players in Low End Segment)

- Product: Small & Large OTR Segment [84% of the OTR market]

- Industry Focus: Construction, Mining & Agriculture

Positioning: Providing quality value products, timely service and reliable collaborators

Takeaway:

Differentiating in the areas possible can help CEAT develop awareness in the US Market, and pave the way for a strong market capture.

Dealers will have better deals for replacement markets in the Value Segment, same which can be passed in the market.

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

PR

OD

UC

T

• Variety: Focused

• Quality: Strong R&D and testing labs

• Design: OE Collaborations

• Services: Business Solutions for clients

• Warranties: As per industry norms

• Returns: 3 month cycle

PR

ICE

• Follow a Value Optimized Pricing Strategy

• Margins: Smart Pricing via an extensive PSM Study

• Credit: 2.5 months, 15 days more than the industry average since engaging with Low Risk Clients

• Working Capital Cycle: 3 months

PLA

CE

• Locations: CEAT to have strategic Distribution Centers setup across the country

• Coverage:

• - Direct Dealer n/w at high demand points

• - Indirect: Capitalize on building up relationship with OEMs

• Inventory Days at

DC: 90 days

PR

OM

OT

ION

• Advertising: Develop a strong Brand Salience via engagements

• PR: Engage with trade journals and trade shows to highlight the Eco- Friendly and other differentiators vis-à-vis the industry

• Buzz: Service Centers Visibility & frequent ATLs

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

• U.S.A shopper is mostly credit driven, proven historically

• A phenomenal 33.3% of the tire buyers do not specify the tire brand, scope for penetration exists

• Farm Equipment industry is growing in the USA, and the consumer willingness to spend will increase

• The main focus area identified are:

- The equipment depth & load resistance [Efficiency]

- Average distance of travel on the work-site [Durability]

Takeaway: Focus on the credit norm payment period, rather than competing on price in the replacement market for consumers.

• Job-Site Visit by the

Nearest Dealer has to

be implemented

religiously to ensure

the customer business

requirements &

processes are better

understood, the tire

maintenance is smooth

& investments are

value worthy for the

customer.

• Due to quality Value

Added Services (VAS)

the price can be

marginally hiked, and

value price segment

pricing can be justified.

Source: World Tire Report

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

• Replacement Market (73%) is a major revenue earner in the tire industry

vis-à-vis the OEM (28%) market

• Focus on obtaining tie-ups with: M&M, John Deere

• CEAT India has strong business relationships with Mahindra. It should be

extended to USA for farm equipment tires, since Mahindra is the largest

tractor manufacturer.

• Promote the eco-friendly aspect of fuel consumption

• Make the CEAT tires available in the Service Centers of Mahindra, via a

Service Bundled Offer (discounted retreading rates) during repairs &

replacement of the OE tires.

• Mahindra dealer network would be a helpful source for the procurement

of Specialty Farm Equipment tires. This would help capture the Agriculture

Industry tire requirements faster.

• Supplier as an OEM to: Komatsu, Escorts International Tractors, and

Caterpillar has to be developed in the next phase

• This is needed to break into the lucrative Mining & Construction Industry

• Pitch for Dealers:

- Increased Fill Rate

- Better Warranty/Adjustment Policy & Technical Support

Incremental Planning - Timeline

Time

Go

al

Where we are now?

Farm Equipment

Tires, Mahindra

Dealership

Priority Areas

Develop a deeper dealer

network in the country

2017

2016

2018

Increase the OEM market

share

Total Span: 3 years (2016-2018)

All Activities to be undertaken simultaneously with the focus on P1, P2 & P3 respectively

P1 P2

P3

• Target the top 15 clients in the Farming Equipment, Construction & Mining Industry value-wise

• Reach out with customized credit norms, and service delivery mechanisms – for replacement tires

Reduced import duties for manufacture of tires in India, since majorly exported to US for OTR

3PL firm would help to bring down cost

This would help to cushion the extended credit and better margins for dealers

• Pitch For Clients:

- 24-Hour Emergency Roadside Service – Dealer Proximity

- Tire Maintenance Program (includes the Job-Site Service visits)

Marketing Focus

ATL Activities:

- Extensive targeted Advertisements, focus on the industry connect

- CEAT brand history leverage

- Establish endorsements of opinion leaders to drive sales in replacement market

• BTL Activities:

- Participate in Industrial Shows, Auto Expos to build

familiarity

- Ensure participation in ConExpo – Con/Agg,

Agritechnica Trade Shows in the US

- Focus on showing how the selected industrial tires are

a right fit for their business

TTL • TTL Activities:

- Provide further details on website about the Eco

Friendly Product & the Improved Credit Norms

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

U.S.A Map

Mahindra Dealer Presence

Legend:

Bridgestone OTR Distribution

Centre

Source: MahindraUSA.com, Bridgestone

Proposed CEAT – OTR

Distribution Centers

United States – Agri.

o/p $395,068,677,000

Rank Commodity Cash Receipts Percent

1 California $44,738,132,000 11.30%

2 Iowa $31,985,370,000 8.10%

3 Nebraska $24,465,882,000 6.20%

4 Texas $22,726,067,000 5.80%

5 Minnesota $20,580,696,000 5.20%

6 Illinois $19,649,939,000 5.00%

7 Kansas $16,223,254,000 4.10%

8 Wisconsin $12,110,055,000 3.10%

9 Indiana $12,052,964,000 3.10%

10 North Carolina $11,706,602,000 3.00%

Iowa

California

Pennsylvania

Texas

Georgia

• In accordance with the Central Place Theory, the Distribution Centers are decided by mapping farm

equipment requirement by industry, Mahindra farm tractor dealer presence & OTR DCs by competitors

• There should be an extensive n/w of on-ground dealers to enable timely delivery

• Keeping the investment setup in mind, the OTR DC number has been tried to be kept minimal till a necessary

M.S. is captured

• Have an Exclusive Dealer in each State. Logistics Partner is different zone.

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

Hero Logistics Lp

(Texas)

TLD Logistics Services, Inc

(Tennessee)

Neovia

(Wyoming)

CEAT Mahindra Adventure Contest

A

I

D

A

Co su e s Co ce

Concerted Consumer Action

Green Marketing, Optimized

Fuel Economy

• TNS survey found that 26% were

actively seeking environmental

products

• Washington Post poll in 2014 found

that 96% respondents were willing to

personally improve the situation by

buying green products

• Rising percentage of US adults who

believe global warming will pose a

serious threat

Cause 1: Friction between tire and the

road, causes extra fuel to burn along with

Green House Gas emission

Approach 1: Reduce rolling resistance of

tires (5 % less friction) Fuel economy

boosted by 4-8% that is 40-300 ltr over

lifetime of a tire

Approach 2: Renewably sourced raw

materials to replace current oil-based

ingredients of tires and non petroleum

versions of special additives boost (fillers)

Approach 3: Modified silica to replace some

of the carbon black reinforcement in

standard tires, lessens the frictional heat that

the rubber compound creates as it flexes,

stretches and recovers with each turn

Approach 4: Natural rubber that grips

better than unmodified versions, along

with vegetable-derived processing oil,

and cellulose-based (rayon) casing

fibers

Recycling: recycle more of the estimated 300

million used tires Freezes the rubber with

liquid nitrogen before grinding it into

pulverized rubber feedstock that could go

into tires

Tire And Rubber Recycling & it’s i pact o the e viro e t

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

Takeaway: Taking cue from the buying behavior of US consumers focus should be on innovative and smart credit norms to stand out from

competition. Credit Norms: 75 days for Dealers.

Smart Credit Norms- A Differentiator

Will not reduce price but play on credit

This will help protect CEAT from low-price image while attracting consumers

Loyal customers to gradually get

increased credit facilities

and hence better credit

terms

Provide improved

credit norms for bundled

offerings (Replacement + Retreading)

Provide extra credit features

to small consumers

referring CEAT tyres to others

Precautions

• Adequate checking of credit ratings of

consumers to minimize default

• Focus on service and product bundling as

a customer becomes more regular

• Being flexible enough to extend

favorable credit norms to even

organizations if they so need

• Keep an adequate balance between

credit and cash payments to stay on track

with liquidity

• Mai tai the uality p oduct i age of CEAT of all times and not trivializing it by

allowing too much credit to all

consumers

• Proper evaluation criteria to list

consumers in different bands eligible for

different levels of credit facilities

• Change the credit pattern as per demand

seasonality quarterly

- It is up to deale s discretion depending on

the competitiveness to

extend credit in the

market or not.

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

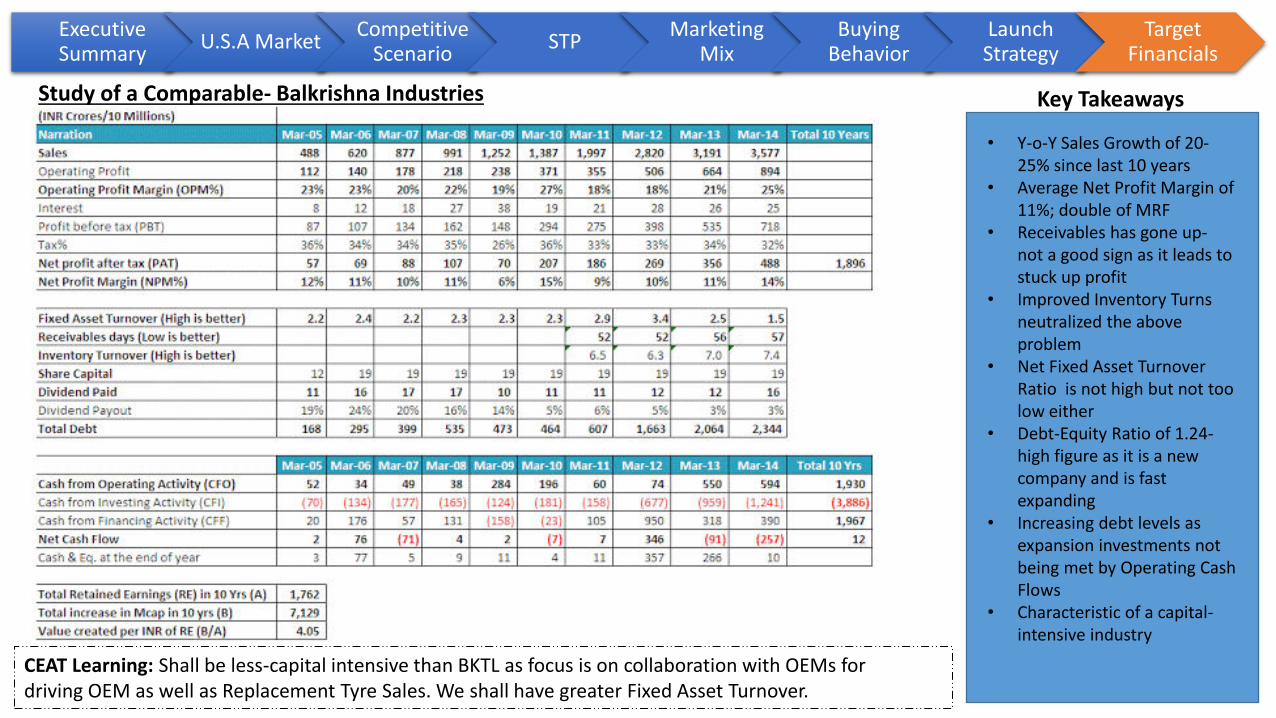

Study of a Comparable- Balkrishna Industries Key Takeaways

• Y-o-Y Sales Growth of 20-

25% since last 10 years

• Average Net Profit Margin of

11%; double of MRF

• Receivables has gone up-

not a good sign as it leads to

stuck up profit

• Improved Inventory Turns

neutralized the above

problem

• Net Fixed Asset Turnover

Ratio is not high but not too

low either

• Debt-Equity Ratio of 1.24-

high figure as it is a new

company and is fast

expanding

• Increasing debt levels as

expansion investments not

being met by Operating Cash

Flows

• Characteristic of a capital-

intensive industry

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

CEAT Learning: Shall be less-capital intensive than BKTL as focus is on collaboration with OEMs for

driving OEM as well as Replacement Tyre Sales. We shall have greater Fixed Asset Turnover.

Source: Industry Reports

• The revenue source of 2015 US OTR

market has been used, flat line growth

assumed

• Target goal is assumed to capture 5%

M.S in overall OTR market, in US

• In order to capture the M.S heavy

focus has been given to tap into the

growing market in the farm machinery

sector

• The data points have been considered

over a period of 3 years (2016-2018)

• With a aggressive penetration

approach 2% M.S in the 1st year would

be driven by the Farm Machinery OE

& replacement markets

• Growth estimates has been done

taking in account the maturity of the

US market

Assumptions (by value) (in Million USD)

OTR 2015 Market Revenue in US 3000

Goal (in 3 years) 5% Market Share 150

Projected Break-up

2016 2% M.S 60.0

2017 3% M.S 90.0

2018 5% M.S 150.0

OTR Revenue Breakup by Industry

Construction 43% 1290

Mining 24% 720

Exports 23% 690

Agriculture 6% 180

Others 4% 120

Forecasted Revenue Breakup (2018)

Construction 34% 51.0

Mining 28% 42.0

Agriculture 35% 52.5

Others 3% 4.5

Net Value 100% 150.0

Industry Size

Construction Machinery US Market (in million USD) 40000

Farm Equipment Market - Global CAGR forcasted growth - 9.2%

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

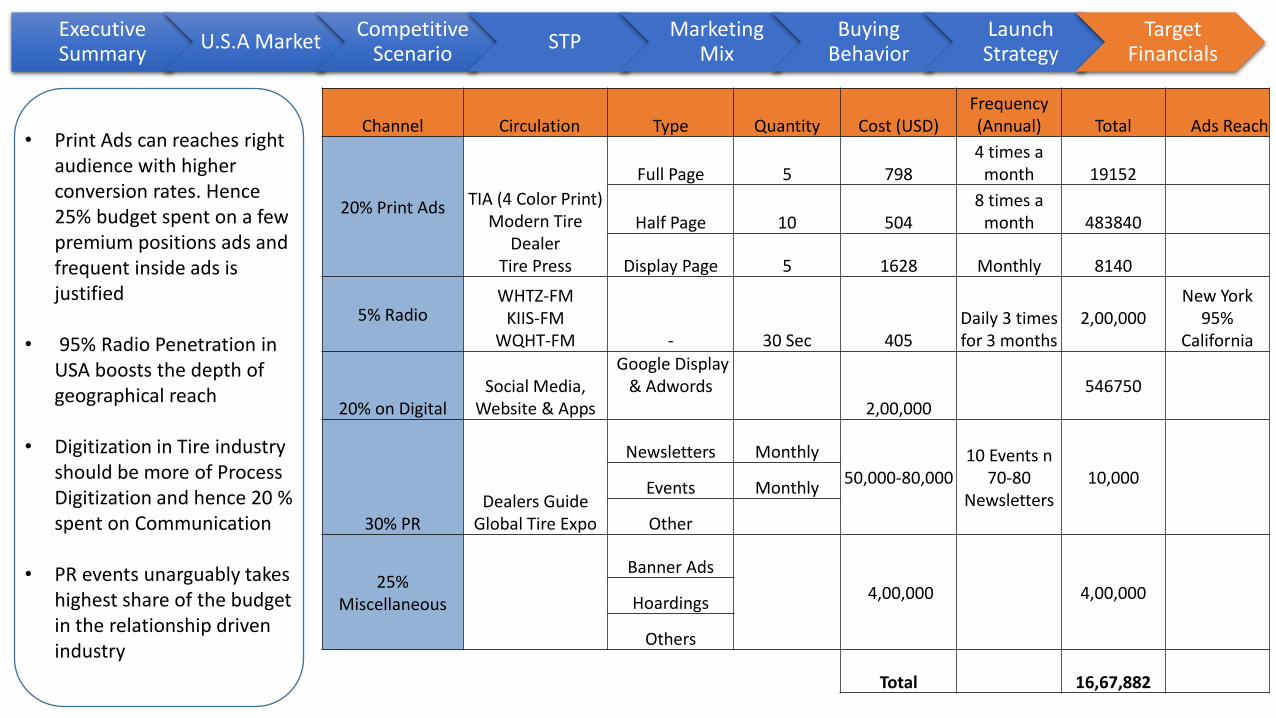

Channel Circulation Type Quantity Cost (USD)

Frequency

(Annual) Total Ads Reach

20% Print Ads TIA (4 Color Print)

Modern Tire

Dealer

Tire Press

Full Page 5 798

4 times a

month 19152

Half Page 10 504

8 times a

month 483840

Display Page 5 1628 Monthly 8140

5% Radio WHTZ-FM

KIIS-FM

WQHT-FM - 30 Sec 405

Daily 3 times

for 3 months

2,00,000

New York

95%

California

20% on Digital

Social Media,

Website & Apps

Google Display

& Adwords

2,00,000

546750

30% PR

Dealers Guide

Global Tire Expo

Newsletters Monthly

50,000-80,000

10 Events n

70-80

Newsletters

10,000 Events Monthly

Other

25%

Miscellaneous

Banner Ads

4,00,000 4,00,000 Hoardings

Others

Total 16,67,882

• Print Ads can reaches right

audience with higher

conversion rates. Hence

25% budget spent on a few

premium positions ads and

frequent inside ads is

justified

• 95% Radio Penetration in

USA boosts the depth of

geographical reach

• Digitization in Tire industry

should be more of Process

Digitization and hence 20 %

spent on Communication

• PR events unarguably takes

highest share of the budget

in the relationship driven

industry

Executive Summary

U.S.A Market Competitive

Scenario STP

Marketing Mix

Buying Behavior

Launch Strategy

Target Financials

Price Sensitivity Meter Questions:

• At what price would you begin to

think product is too expensive to

consider?

• At what price would you begin to

think product is so inexpensive

that you would question the

quality and not consider it?

• At what price would you begin to

think product is getting

expensive, but you still might

consider it?

• At what price would you think

product is a bargain – a great buy

for the money -

List of Prospective Clients

Top 15 Construction Companies (US)

• Bechtel Group Inc., San Francisco, CA

• Fluor Corporation, Irvine, CA

• Skankska Inc., Greenwich, CT

• CENTEX Construction Group, Dallas, TX

• The Turner Corp., NY

• Halliburton- Kellogg Brown & Root, Houston, TX

• Peter Kiewit Sons Inc., Omaha, NE

• Washington Group International, Inc

• J.A. Jones Inc., Charlotte, NC

• Bovis Lend Lease, NY

• Gilbane Buidling Co., Providence, RI

• The Clark Construction Group Inc., Bethesda, MD

• The Whiting-Turner Contracting Co., Baltimore, MD

• Jacobs Engineering Group, Pasadena, CA

• Foster Wheeler Corp., Clinton, NJ

Top 15 Mining Companies (US)

• Rio Tinto

• Barrick

• Freeport-McMoRan

• Goldcorp

• Norilsk Nickel

• The Mosaic Company

• Newmont Mining Corporation

• Alcoa

• AngloGold Ashanti

• Kinross Gold

• Peabody Energy

• 3M

• Dells Mining Company

• Sugarland Mining Company

• Omaha Mining Company

Source: CEAT.com

http://www.quirks.com/advertise/print/adrates.aspx