challenges in the evaluation of unconventional reserves ... · cesar guzzetti gaffney, cline &...

TRANSCRIPT

© 2013 GAFFNEY CLINE & ASSOCIATES. ALL RIGHTS RESERVED. TERMS AND CONDITIONS OF USE: BY ACCEPTING THIS DOCUMENT, THE RECIPIENT AGREES THAT THE DOCUMENT TOGETHER WITH ALL INFORMATION

INCLUDED THEREIN IS THE CONFIDENTIAL AND PROPRIETARY PROPERTY OF GAFFNEY CLINE & ASS0CIATES VALUABLE TRADE SECRETS AND/OR PROPRIETARY INFORMATION OF GAFFNEY CLINE & ASSOCIATES

(COLLECTIVELY "INFORMATION"). GAFFNEY CLINE & ASSOCIATES RETAINS ALL RIGHTS UNDER COPYRIGHT LAWS AND TRADE SECRET LAWS OF THE UNITED STATES OF AMERICA AND OTHER COUNTRIES. THE RECIPIENT

FURTHER AGREES THAT THE DOCUMENT MAY NOT BE DISTRIBUTED, TRANSMITTED, COPIED OR REPRODUCED IN WHOLE OR IN PART BY ANY MEANS, ELECTRONIC, MECHANICAL, OR OTHERWISE, WITHOUT THE EXPRESS

PRIOR WRITTEN CONSENT OF GAFFNEY CLINE & ASSOCIATES, AND MAY NOT BE USED DIRECTLY OR INDIRECTLY IN ANY WAY DETRIMENTAL TO GAFFNEY CLINES & ASSOCIATES’ INTEREST.

Thoughts from US Shale Experience

Cesar Guzzetti Gaffney, Cline & Associates

Challenges in the evaluation of unconventional

reserves – shale gas and tight oil

I was on Vacation !!!!!!!!

2 © 2013 Gaffney Cline & Associates. All Rights Reserved

Last week, in Lagoa Azul,

Angra dos Reis.

Outline

• Fundamentals

• Unconventional Resources - Shale

• Key economic drivers to call unconventional resources,

“Reserves”

• Call for caution

• Conclusions

3 © 2013 Gaffney Cline & Associates. All Rights Reserved

Fundamentals

• Reserves are estimated (not calculated or measured)

• Reserves are predicted future production (sales) volumes

• Reserves estimates depend on

– The data available

– The field development plans

– Oil and Gas prices

– Professional expertise and judgment (multi-disciplinary)

• Reserves are sub-set of “Resources”, the generic term for

all petroleum volumes

4 © 2013 Gaffney Cline & Associates. All Rights Reserved

Reserves/Resources Reporting Systems

• Petroleum Resources Management System (SPE PRMS,

2007)

– Supplemental by Application Guidance (2011)

– Endorsed by SPE/WPC/AAPG/SPEE/SEG

– Becoming de facto standard but no regulatory authority

• SEC rules (US)

– Proved Reserves definitions (1978)

– Revised regulations (2009)

• Other stock exchange/government systems

– TSX, Russia, Norway, China, India, Nigeria…

Application to unconventional resources driven by

North American practice 5 © 2013 Gaffney Cline & Associates. All Rights Reserved

PRMS Framework

6 © 2013 Gaffney Cline & Associates. All Rights Reserved

Commerciality

• Firm intention to proceed…

• …in a reasonable time frame

• Development project meeting economic criteria

• Market

• Facilities (export route, access to technology)

• Permissions (legal, contractual, environmental)

Commerciality requires reasonable expectation

that all of the above will be forthcoming

7 © 2013 Gaffney Cline & Associates. All Rights Reserved

Reservoir (volumes, productivity)

SPE-PRMS Definitions and Comments

• Unconventional resources… are pervasive throughout a

large area and …are not significantly affected by

hydrodynamic influences

• “… typically a need for increased sampling density to

define… in-place volumes and variations in reservoir

quality…”

• “successful pilots or operating projects in the subject

reservoir or successful projects in analogous reservoirs

may be required to establish a distribution of recovery

efficiencies…”

• “require specialized extraction technology, and…

significant processing prior to sale”.

8 © 2013 Gaffney Cline & Associates. All Rights Reserved

Discovery and Commerciality

• Same definitional principles and guidelines apply

as for conventional reservoirs

• Discovery is less an issue that commerciality

– Existence of the “reservoir” may not be in doubt

– Demonstrating commercial production rates is the key

issue

• Pilot projects are generally needed unless good

analogue is available

– Horizontal multi-fracked wells in shale

– Dewatering in CBM

– Need for infrastructure to avoid flaring

9 © 2013 Gaffney Cline & Associates. All Rights Reserved

Types of Unconventional Resources

• Extra-Heavy Oil/Bitumen

• Tight Gas Formations

• Coalbed Methane

• Shale Gas

• Oil Shale

• Gas Hydrates

10 © 2013 Gaffney Cline & Associates. All Rights Reserved

optional

Shale Gas Characteristics

• Shale gas is produced from organic-rich mudrocks, which serve as a

source, trap, and reservoir for the gas

• Shales have very low matrix permeability (micro- to nano-Darcy),

requiring either natural fractures and/or hydraulic-fracture stimulation

to produce the gas at economic rates

11 © 2012 Gaffney, Cline & Associates. All Rights Reserved.

EIA

Fractured Horizontal Well Schematic

12 © 2011 Gaffney, Cline & Associates. All Rights Reserved.

Source: ESG Solutions

And this is What it Really Looks Like … 52,000 HP in the Woodford Shale

13 © 2012 Gaffney, Cline & Associates. All Rights Reserved.

$0.0

0

$1.3

2

$1.4

0 $

2.2

3

$2.8

6

$2.8

9

$3.1

5

$3.1

7

$3.3

0

$3.4

5

$3.6

6

$3.7

5

$3.7

7

$3.8

8

$4.0

3

$4.3

7

$4.6

9

$4.9

3

$5.4

9

$5.7

3

$6.1

9

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$/M

MB

tu

NYMEX BEP @ 10% After Tax ROR

Breakeven gas price for major U.S. shale gas plays

14 © 2013 Gaffney Cline & Associates. All Rights Reserved Source: Credit Suisse Dec 2012

How Do We Establish Commerciality?

Key Value Drivers

Technical (Subsurface)

Resource Assessment & Quantification

Understanding the missing information: Lack of Analogues & Historic Data

Decline Rates Across Wells

Initial Production Rates/Type Curves

Total No of Wells Required

EUR Per Well

Liquid Gas Ratio

Commercial

Understanding Costs

Pipeline, Infrastructure, Facilities, Water supply & handling

External Barriers

Applicable Fiscal regime

Project Break-even

(Price, Well count, IP rate)

Time to Market

Single Well vs. Pad Economics

© 2013 Gaffney Cline & Associates. All Rights Reserved 15

Key Elements for the sustainable development

of hydrocarbon resources

16 © 2013 Gaffney Cline & Associates. All Rights Reserved

Hypothetical Development under a 25-year -

Schematic

17 © 2013 Gaffney Cline & Associates. All Rights Reserved

0

200

400

600

800

1,000

0

50

100

150

200

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

US

$ M

M

Ga

s P

rod

ucti

on

Bcf

Contract Year

Conventional Production and Costs Opex MM$ 2,061

Capex MM$ 3,092

Production Bcf 2,061

0

200

400

600

800

1,000

0

50

100

150

200

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

US

$ M

M

Ga

s P

rod

ucti

on

Bcf

Contract Year

Unconventional Production and Costs Opex MM$ 1,031

Capex MM$ 9,276

Production Bcf 2,061

Much slower production build up and

extended capex spend

Checks

• EUR estimates with time

– SEC requirement for “reasonably certain EUR to increase or

remain constant”

– Any analysis that fails this test does not comply

• Use of Dmin?

– Any value accepted by SEC?

• 5% for shales?

• 7-8% for tight gas?

• Ultimately 2-3% may apply??

18 © 2011 Gaffney, Cline & Associates. All Rights Reserved.

The Unconventional Challenges

• How to predict performance for unconventional reservoirs,

especially shale gas wells

• How and when to assign reserves

Type Well

Most critical assumption is often over-simplified

Not all shale formations are the

same!

• Does not involve natural constraints

• Difficult to explain well design effects

• Optimization is based on “trial and error”

• Large investments for “know-how”

• Geo-mechanical effects are ignored

• Long term predictions are questionable

Assimilation of historical data and building of

“type curves” has drawbacks:

The Problem

• Shale reservoir performance prediction is more complex than more traditional formations

• Conventional theory does not work

• Limited history can lead to forecasting errors

• Type curves are widely used and, potentially, abused

• The choice of which type curve to use depends on a number of factors including area, permeability-thickness, lateral length, and completion effectiveness

• What other options are there?

Inconvenient Facts

• Flow may be transient for many years

• Initial best-fit “b” will almost always be greater than unity

• It will decline with time, but this cannot (yet) be predicted

• Some use a terminal decline (or Dmin) to try to prevent

over-estimation of EUR

– Does this work?

– What should the value be?

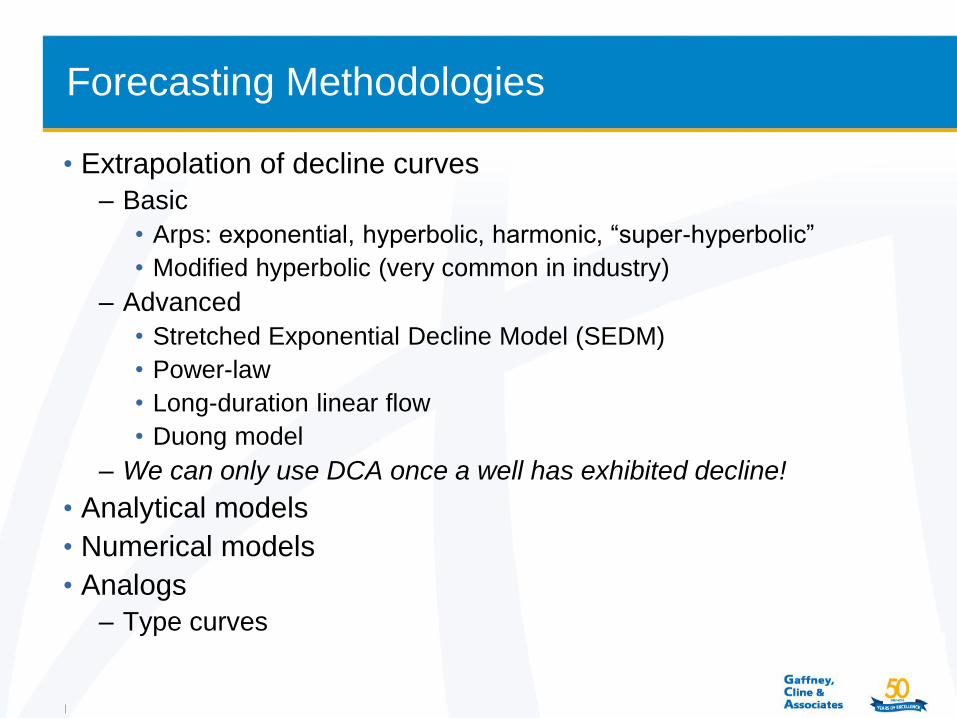

Forecasting Methodologies

• Extrapolation of decline curves

– Basic

• Arps: exponential, hyperbolic, harmonic, “super-hyperbolic”

• Modified hyperbolic (very common in industry)

– Advanced

• Stretched Exponential Decline Model (SEDM)

• Power-law

• Long-duration linear flow

• Duong model

– We can only use DCA once a well has exhibited decline!

• Analytical models

• Numerical models

• Analogs

– Type curves

Examples of Minimum Terminal Decline

EUR = 6.7

EUR = 8.6

EUR = 10

EUR = 11

EUR = 22

EUR = 7.9

Plot from Fekete Harmony Software

Advanced Decline Methods

• Stretched Exponential Decline Model (SEDM) – Empirical

• 𝑄 = 𝑄𝑖𝑒−(𝑡

𝜏)𝑛

– The EUR is limited to reasonable numbers (unlike b>1)

– Model also fits transient data

• Power Law – Empirical

• 𝑄 = 𝑄𝑖𝑒(−𝐷∞𝑡−𝐷𝑖𝑡𝑛)1

• Same as SEDM when Dinf = 0

– Model also fits transient data

• Linear Flow – Plot of q vs. 1/√(t) is a straight line with slope ½ only when s=0

– Plot of 1/q’ vs. log(t) will be straight line with slope ½ even with s/=0

• Duong Method – Empirical

– 𝑞 = 𝑞1𝑡−𝑛

–𝑞

𝐺𝑝= 𝑎𝑡−𝑚 + 𝑞∞ , 𝑞 = 𝑞1𝑡 𝑎, 𝑚 ,

– t a, m = 𝑡−𝑚𝑒𝑎

1−𝑚(𝑡1−𝑚−1)

Change in EUR with Time (Time limit: 30 yr. or Zero Rate)

1

2

3

4

5

6

7

500 1000 1500 2000 2500

EU

R (

Bcf)

Time (Days)

EUR vs Time

Exp Hyp Dmin=5% PLE Duong Dmin = 10 %

Basic Evaluation and Audit Requirements

• It is crucial that those charged with the preparation of the Reserve

and Contingent Resource estimates are fully conversant with the

relevant definitions

• Each declared volume should be supported by clear references to all

analyses and documentation that were used to derive that number

– This applies whether the audit is carried out by internal or external

advisors

– An adequate audit trail is also a requirement to ensure that the company

is in compliance with SOX reporting

• It is not the intent of an audit that the auditor undertakes a significant

amount of evaluation work, but rather that its role is limited to an

appropriate level of checking

26 © 2011 Gaffney, Cline & Associates. All Rights Reserved.

Conclusions

• Classification of unconventional Reserves and Resources

is governed by the same principles that apply to

conventional hydrocarbon accumulations

– Application of these principles is still a subject of debate

• Reserves can be booked only for projects that meet the

criteria for “commerciality”

– A pilot project is generally needed

• Estimates of GIIP and recoverable volumes per well are

still subject to significant uncertainty

– Actual field experience is still relatively limited

– Assessment tools are still under development

27 © 2013 Gaffney Cline & Associates. All Rights Reserved

Final Conclusions

• Know the definitions and guidelines

• Follow company-specific guidelines and procedures

• Use the appropriate methodologies

– And compare with more than one approach

• Be consistent across assets, and time

• Maintain a thorough audit trail

– Documentation is critical to SOX compliance

• And always exercise informed professional judgment

28 © 2011 Gaffney, Cline & Associates. All Rights Reserved.

optional