chanakya volume i issue ix

TRANSCRIPT

8/14/2019 Chanakya Volume I Issue IX

http://slidepdf.com/reader/full/chanakya-volume-i-issue-ix 1/4

ChanakyaIs Colombo Port humbled by Indian Ports! Sri Lankan shippers are feeling the pressure of India's booming export-

import trade with some of the major shipping lines deciding to give

priority to Indian ports over Colombo.

Maersk, UASC, K-line and Norasia, one the leading shipping lines in theworld, have diverted some of their services to Nhava Sheva in Mumbai.

Some have withdrawn their European services to and from Colombo.

Hanjin-K Line-UASC combine used to operate two services to Europe

from Colombo, but recently pulled out one. Norasia-Zim Line pulled

out its weekly European service. This action of these leading shipping

lines have created a shortage of 650 TEUs (twenty-foot equivalent

units) a week for the Colombo-Europe sector.

Why did they orphan Colombo Port? The answer is obvious, India is

booming. Look beneath we find interesting facts. The direct services

from India obviate the need for Indian cargo to be transshipped through

the Colombo port to Europe or the US thus saving around $100 a TEU

for the shippers. India is now a cargo-rich base as industry is booming.

Consider this; the shipping lines will consider diverting the ships based

on the volume. For example, Maersk Line recently introduced a route

change and also introduced a new service out of Chennai. Its European

vessel has now been dedicated to the UK trade mainly giving preference

to garments to the UK. This is despite expenses incurred due to delays

at Indian ports.

The infrastructure in the Colombo Port is also one the concerns, which

has not seen a major investment for the past 15 years. The worst hits

are Sri Lanka's exporters of garments, tea and coir. However, the

Colombo port is not ready to give up its ‘numero uno’ position in the

region and is investing heavily. The strategic advantage of Colombo is its

geographical location, but can it withstand the onslaught of the volume

advantage that Indian ports provide. Remains to be seen!

This Issue

Is Colombo Port Humbled by Indian

Ports ‐ 1

Indian Real Estate Boom: Shifting

Geographies 2

Construction Boom: Are we Ready 3

Economic Indicators 4

Team Chanakya 4

DATE: 1ST December 2007

VOLUME NO: I

ISSUE NO: IX

8/14/2019 Chanakya Volume I Issue IX

http://slidepdf.com/reader/full/chanakya-volume-i-issue-ix 2/4

When Far

and its joi

11-acre pr

$54.5 milli

idiocy by l

same joint

nearby pr

Property

biggest citi

country, agrows at f

more inve

India is on

primary d

trading up.

sector will

by 2015. T

corridors

bubble havrisk weigh

and mortg

as a result

most India

questions

which has

estate sto

an end.

The run-u

Stanley, M

bucks in t

IndiaGeogr

allon Capital

t-venture par

operty in cen

on an acre, th

ocal develope

venture offer

perty, it was

rices in India

es. As the tec

more Indiansster than 8%

tors, many of

e of the last fe

mand for real

. Merrill Lynch

grow from $

his optimism i

of power. Co

e led the Resage on real es

age rates have

. That's still w

ns were used

about whethe

driven land pr

ks up as muc

p in prices has

errill Lynch et

e Indian mark

Realaphies

anagement, a

ner, Indiabulls

ral Mumbai in

e purchase wa

s. A few mon

ed $95.5 millio

he second-lo

are rising fast,

h boom sprea

buy homes, aa year, real es

them from ab

w countries w

estate rather

forecasts tha

12 billion in 20

s not bought

cerns about a

rve Bank of Intate loans ext

gone from 7.

ll below the 1

to, but it's en

the speculati

ices up by 30

as 2,000%, m

attracted the

c., to name fe

et. Foreign co

state B

U.S. hedge fu

, snapped up

March 2005 f

s called an act

hs later, when

n an acre for

est bid.

and not just in

s across the

nd as the ecoate is attracti

road.

here there is

than individua

the Indian re

05 to $90 billi

y all in the

n asset-price

dia to raise thended by bank

% to about 1

5% rates that

ugh to raise

n of the past

to 100% and

ay be coming

likes of Morga

, to pour gre

mpanies have

om: Shi

po

GE

inv

IT

Fun

Re

Re

rais

mu

Bri

W

Indi

op

But

the

maj

run

billi

co

pla

exp

Th

ma

ma

as

So

sev

sec

Bo

d,

n

r

of

the

a

the

omyg

ls

lty

on

es,

.5%

two,

real

o

n

n

lso

fting

red money in

Commercial

sted $63 milli

arks, and Cal

d have invest

lty fund.

l estate funds

ed more than

ch as $4 billio

ain's Knight F

rburg Pincus,

ia, says it is sp

ortunities in t

it isn’t going

nature of the

ority of devel

organizations

on of investm

panies are av

ers, who wou

ectations of t

second majo

gins that thes

kets were up

f now.

to find a way

eral funds are

ond-tier devel

om is In Tie

o funds that i

inance Real Es

on in an $800

ers and the

d $100 millio

set up to inve

$6.7 billion. A

are being pla

ank, and othe

the largest pri

ending nearly

his area.

o be a cake w

Indian real est

pment is bein

. In country th

ent in real est

ailable and all

ld not have th

e funds.

r concern is th

e funds came

ards of 35%

o circumvent

focusing on se

opers. The N

II Markets!

vest in Indian

tate, for exa

million fund t

regon Public

each in the I

t only in India

nd new funds

nned by J.P. M

r foreign inves

ate-equity inv

third of its ti

alk. The one i

ate business it

g done by sm

at need aroun

te, only 15 lis

thers are sm

e ability to sca

e falling margi

o expect fro

hich is langui

and still sail ab

cond-tier tow

ext Wave of

developers.

ple, has

at is building

etirement

&FS India

have already

worth as

organ,

tors.

estor in

e studying

pediment is

self. A

ll and family

d US$100

ed

ll regional

le-up to the

ns. The

Indian

shing at 20%

ove waters,

ns and

Real Estate

8/14/2019 Chanakya Volume I Issue IX

http://slidepdf.com/reader/full/chanakya-volume-i-issue-ix 3/4

Indi

US$

year

wou

of t

whi

Con

earn

$35

Lars

engi

sale

billi

Andwith

Just

out

exc

tod

wor

mor

The

aro

of $

Indi

will

to b

suc

sect

mo

For

exis

thei

Indi

Don

Indu

ord

glob

Hol

ent

's planned inf

475 billion. T

on infrastruc

ld be spendin

is can be see

h have also r

sider just a fe

ed 72% more

9.43 million. Y

en & Toubro,

neering and c

rose 47% in

n, and yet its

Patel Engineesales of $405

to highlight th

of highways b

eds the total

y. Even if all t

k on building

e work to off

turnover of al

nd $15 billion

95 billion is sl

, which requi

need several b

e able to exec

companies, c

or to build ou

e.

ign firms mig

ting capabilitie

r mark in Indi

has benefite

gfang Electric

stries and Co

rs for turbine

al constructio

ings and Italia

red India.

astructure ou

e country cur

ure, compare

close to US$

in the order

ached a multi

examples: P

income for th

et, its order b

one of Asia's l

nstruction co

he quarter en

order backlog

ring, which ex.58 million, ha

e enormity of

the NHAI ov

turnover of all

e companies

irports and p

r then firms c

ll construction

. This year it

ted to be spe

es a capability

illion-dollar, p

ute such proj

alling into que

t infrastructur

t view the hu

s and those re

. Indeed, the i

a bevy of ov

Corporation i

struction Co

s used to gen

n companies, s

n-Thai Develo

tlay over the

rently spends

d to China's $

95 billion a ye

books of infra

year high.

unj Lloyd, an E

e quarter end

acklog rose to

argest vertical

mpanies, anno

ded Septembe

rose to a rec

pects to closean order bo

the opportuni

er the course

construction

did only road

wer plants as

an take.

companies in

ay rise to $2

t on construc

of 5 times th

ure-play const

cts, but it has

tion the abilit

e in a public-p

e gap betwee

quired as an o

nfrastructure s

rseas compan

n China and D

pany in Kore

rate power.

uch as Austra

pment Public

ext five years

around $21 bi

150 billion and

r. The effect

tructure build

PC company,

d June 2007,

$3,859.32 mil

ly integrated

unced that gr

r 2007 to $1.

rd $10.14 bill

the current yk of $1.37 bill

ty the planned

of the next 10

companies in I

rojects and le

ide, NHAI still

India last year

billion. But a

tion every ye

sector's size.

ruction comp

only a couple

of the privat

ivate partners

the sector's

pportunity to

pending boo

ies, such as

oosan Heavy

a, who are filli

number of le

lia's Leighton

Company, hav

is

llion a

now

f all

ers,

t

lion.

ss

1

ion.

arion.

roll-

years

ndia

ft all

has

was

total

r in

India

nies

of

e

hip

make

in

ng

ading

e also

Const

Th

fo

In

Of en

Th

lik

As

int

co

m

su

rebr

als

Inv

La

pr

pr

Inf

th

Sp

de

its

Th

m

an

se

Th

fo

eq

W

uction

ere is a defini

eign compani

ia.

India’s largestgineering equi

ese foreign co

ely to set-up s

companies ta

ensity of their

mpanies to rel

rkets. So far,

portive of thi

l estate develaking IPO ear

o managed to

estment Mark

ely, as real es

ssure, many c

miums they c

rastructure bu

stock marke

ecial Economi

veloper to go

investor’s for

e Indian oppo

rkets are rec

d all this are

tor.

is will call for

m of SEZs. A

uipment SEZ

e are placed

Boom:

e requiremen

s to put their

imports by vament comma

mpanies flocki

hop in India.

ke on larger si

operations in

y on private e

he Indian capi

s, with DLF Lt

opers -- raisinlier this year.

raise funds on

et for investin

ate stocks ha

ompanies hav

an hope to re

ilders, howev

is still recepti

Zone becom

public in Octo

une triple on

rtunity is posit

ptive, the Indi

aking a great

more industri

construction

ill make a lot

right at the

re we r

of space for

manufacturin

lue, next tonds a lot of w

ng the Indian

e projects, th

reases, forcin

quity or the p

tal markets ha

d. -- one of In

capital in a rMany realty c

London's Alt

g in projects i

e come unde

begun to rea

eive when th

r, have discov

ive, with Mund

ing the first SE

ber this year

he day of listi

ive, the Indian

an Governme

ase for a boo

l space creati

nd infrastruct

of sense in thi

middle of th

ady?

hese

base in

il, Heavyightage.

arket are

e capital

g many

blic

ve been

ia's largest

cord-mpanies

rnative

India.

increasing

ssess the

y go public.

ered that

ra Port &

Z

nd has seen

ng.

capital

t is inviting,

m in this

n in the

ure

s condition.

is

8/14/2019 Chanakya Volume I Issue IX

http://slidepdf.com/reader/full/chanakya-volume-i-issue-ix 4/4

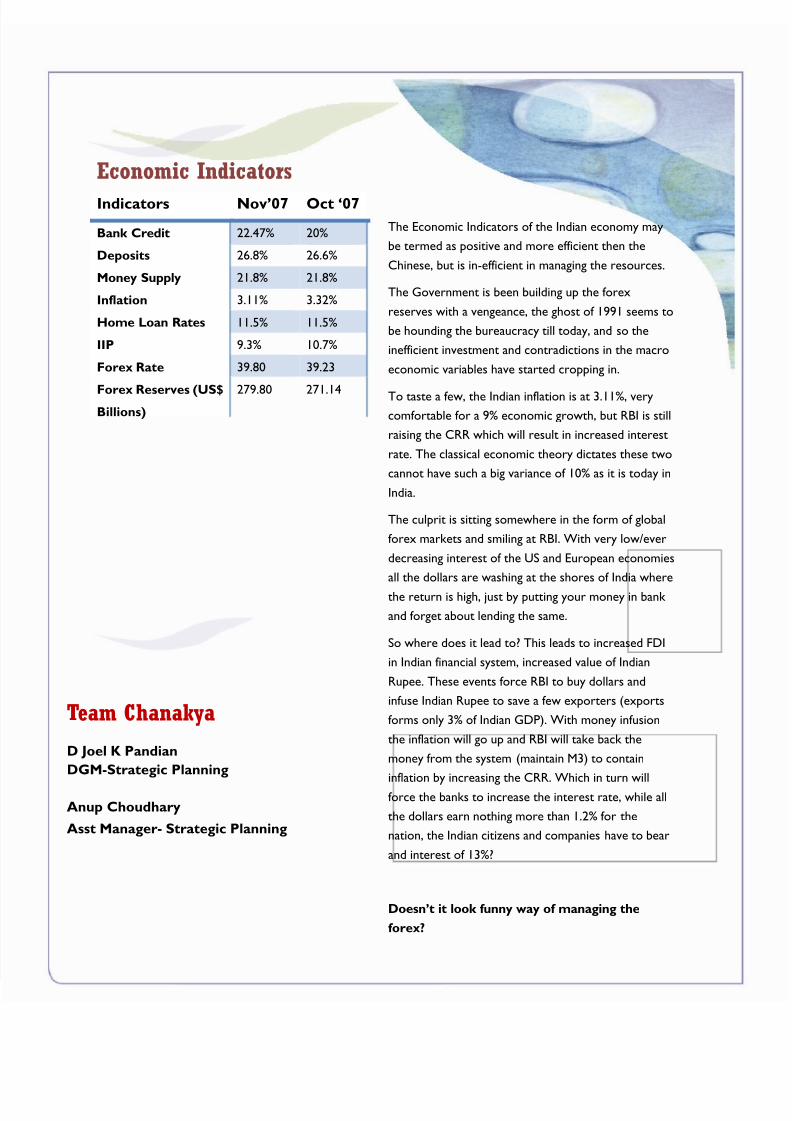

Indicators Nov’07 Oct ‘07

Bank Credit 22.47% 20%

Deposits 26.8% 26.6%

Money Supply 21.8% 21.8%

Inflation 3.11% 3.32%

Home Loan Rates 11.5% 11.5%

IIP 9.3% 10.7%

Forex Rate 39.80 39.23

Forex Reserves (US$Billions)

279.80 271.14

Economic Indicators

Team Chanakya

D Joel K Pandian

DGM-Strategic Planning

Anup Choudhary

Asst Manager- Strategic Planning

The Economic Indicators of the Indian economy may

be termed as positive and more efficient then the

Chinese, but is in-efficient in managing the resources.

The Government is been building up the forex

reserves with a vengeance, the ghost of 1991 seems to

be hounding the bureaucracy till today, and so the

inefficient investment and contradictions in the macro

economic variables have started cropping in.

To taste a few, the Indian inflation is at 3.11%, very

comfortable for a 9% economic growth, but RBI is still

raising the CRR which will result in increased interest

rate. The classical economic theory dictates these two

cannot have such a big variance of 10% as it is today in

India.

The culprit is sitting somewhere in the form of global

forex markets and smiling at RBI. With very low/ever

decreasing interest of the US and European economies

all the dollars are washing at the shores of India where

the return is high, just by putting your money in bank

and forget about lending the same.

So where does it lead to? This leads to increased FDI

in Indian financial system, increased value of Indian

Rupee. These events force RBI to buy dollars and

infuse Indian Rupee to save a few exporters (exports

forms only 3% of Indian GDP). With money infusion

the inflation will go up and RBI will take back the

money from the system (maintain M3) to contain

inflation by increasing the CRR. Which in turn will

force the banks to increase the interest rate, while all

the dollars earn nothing more than 1.2% for the

nation, the Indian citizens and companies have to bear

and interest of 13%?

Doesn’t it look funny way of managing the

forex?