change accountants & advisors pty ltd | head office: level ... singapore 2014/soa... ·...

TRANSCRIPT

25 August 2014 Mr John & Mrs Mary Smith 1 Brisbane Street Brisbane QLD 4000 Hello John and Mary, We are pleased to enclose your Statement of Advice. This document contains all the information you need to take control of your money and achieve your financial goals. Your Statement of Advice is your personal financial plan

Our advice and recommendations to you, and the reasons for them, are outlined in your Statement of Advice. Your Statement of Advice is personal to you. It is based on your current financial situation and the goals you want to achieve. Making it clear

It’s important that you understand, and are comfortable with, the information in your Statement of Advice. Where financial strategies contain technical concepts, we have included a Fact File to give you more information. If you do come across any information that is not clear when reading your Statement of Advice, please note it down and come back to us with any questions. A secure financial future

Having a financial plan puts you on the path to a secure financial future, but it takes discipline and commitment to see the plan through and monitor your progress. We look forward to helping you implement your plan and building a relationship were we can continue to work together to achieve your financial goals. Helping you

If you would like to discuss any aspect of your financial plan presented in this Statement of Advice, please don’t hesitate to contact us on 07 3226 9999. Yours sincerely

Timothy Munro

Authorised Representative - Count Financial Limited

Director - Change Accountants & Advisors Pty Ltd

Change Accountants & Advisors Pty Ltd | Head Office: Level 13, 40 Creek Street, Brisbane QLD 4000 | Postal: GPO Box 225, Brisbane QLD 4001 ABN 84 150 669 042 | Telephone + 61 7 3226 9999 | Facsimile +61 7 3226 9900 | twitter: @change_brisbane | www.changeaccountants.com.au

Statement of Advice (SoA)

Prepared for

Mr John & Mrs Mary Smith

25 August 2014

Authorised Representative of:

Count Financial Limited (Count) ABN: 19 001 974 625 AFS Licensee: 227232 Level 19, 1 Alfred Street Sydney NSW 2000 P: 1800 026 868 E: [email protected] W: www.count.com.au

Prepared by:

Timothy Munro Change Accountants & Advisors Pty Ltd

ASIC ID 232061

Level 13, 40 Creek Street Brisbane QLD 4001

P: 07 3226 9999 E: [email protected]

W: www.changeaccountants.com.au

Table of Contents

Your Personal and Financial Details 1

Your Goals and Needs 3

Your Tolerance to Investment Risk 4

Your Personal Insurance Needs 5

What This Advice Covers 6

Summary of Advice 7

Recommended Strategy 8

Recommended Products 17

Financial Outcomes of Recommended Strategy 22

Products to be Replaced 24

The Cost of This Advice 27

Important Documents 29

Further Explanation of This Advice 30

How to Implement This Advice 31

Agreement to Proceed 32

Electronic Instructions Authority 34

Total Financial Care Agreement 35

Statement of Advice for John & Mary Smith Page 1 of 37

Your Personal and Financial Details This section contains key information about your current circumstances and forms an important part of our advice to you.

Please review this section carefully and let us know if any important information is missing or shown incorrectly. Where we have requested information from you that has not been provided, we have noted this below. If the information you have provided is incomplete or inaccurate, you will need to consider if this advice is appropriate for your circumstances and objectives before you act on it.

Personal Details

Details John Mary

Age 34 30

Date of Birth 01/01/1980 01/01/1983

Marital Status Married Married

Occupation Software Developer Full-time Mother

Retirement Age 65 65

Smoker No No

Dependant Details

Name Date of Birth Dependant Until Age

Sam 01/09/2013 18

Income Details

Details Owner Amount

Salary (including Super) John $215,000

Other Income John $23,920

CBA Protected Shares – Dividends John $17,400

Total

$256,320

Expense Details

Details Owner Amount

Annual Living Expenses (including loan repayment) Joint $78,000

CBA Protected Share Portfolio – Interest John $39,450

Total $117,450

Lifestyle & Investment Asset Details

Type Owner Amount

Family Home Joint $635,000

Statement of Advice for John & Mary Smith Page 2 of 37

Investment Property Joint $410,000

Subaru Joint $8,000

Mazda Joint $4,000

Home Contents Joint $30,000

CBA Protected Share Portfolio John $500,000

Total $1,587,000

Liability Details

Type Owner Term Repayment Frequency Amount

Home Mortgage (BOQ at 4.85%) Joint Not disclosed $4,000 Monthly $581,000

Investment Property Mortgage (BOQ at 4.85%) Joint Not disclosed $1,200 Monthly $200,000

Car Loan Joint Not disclosed $800 Monthly $6,500

CBA Protected Loan John 2 Years $3,167 Monthly $500,000

Total $1,287,500

Superannuation Details

Product Account Owner Account Balance

Russell Investments Super Fund John $161,055

Commonwealth Bank Group Super Mary $38,000

Total $199,055

Life Insurance Details

Policy. Owner Life Insured Type Benefit Premium (p.a.)

Russell Investments Super Fund The Trustee John Life & TPD $535,000 $374.40

MLC Life John John Trauma $153,727 $620.76

MLC Life John John Income Protection $4,682/mth $1,504.44

MLC Life John John Income Protection $3,796/mth $1,219.80

Total $3,719.40

Estate Planning Details

Details John Mary

Will in Place No No

Testamentary Trust No No

Power of Attorney No No

Enduring Guardian No No

Statement of Advice for John & Mary Smith Page 3 of 37

Your Goals and Needs This section describes the reasons that you came to me for financial advice and highlights what you want to achieve.

Understanding your goals and needs is an essential part of developing a personalised financial strategy that is right for you. The goals you want to achieve, as well as additional needs that we identified from your personal and financial details, have been summarised below. The recommendations made in this Statement of Advice have been designed to meet both your goals and needs.

Your Stated Goals are:

Superannuation options including consolidating your existing super funds and making more use of your Super

monies:

- Owning a Self-Managed Super Fund (SMSF)

- Consolidating your Superannuation Funds

- Investing your Super monies into Growth assets to build for future retirement

Reviewing your current insurances compared to your insurance needs to ensure that you are covered adequately

and in the most effective way.

- You would like to ensure that you and your family are financially protected in the event of serious illness, disability or death.

- To ensure your income is protected in the event that you are unable to work due to temporary illness or

disability.

Establish Wills and Powers of Attorney for each of you.

Statement of Advice for John & Mary Smith Page 4 of 37

Your Tolerance to Investment Risk This section describes the level of investment risk that you are comfortable with and shows how we will invest your money accordingly.

During our meetings we have discussed your thoughts and feelings on investing, along with fundamental investment concepts such as risk, return, volatility and diversification. This included your level of comfort with various investment risks, as well as the returns and volatility that are associated with different investments. You also completed a risk profile questionnaire to provide us with more specific details about your attitude to the risks involved in investing. The purpose of these discussions and completion of the risk profile questionnaire was to identify your risk profile. Your risk profile is simply a description of how much risk you are comfortable with in order to achieve your goals and it is used to guide decisions around how your money is invested.

For further details on the nature of each risk profile, including the potential return expectations, please refer to the ‘Further explanation of this advice’ section and the attached fact files.

Your Results The results from the risk profile questionnaire you have completed show that you both have a ‘High Growth’ risk profile. We have discussed what this means for you, including:

The types of investments that are appropriate for this risk profile.

The risks associated with the various investments that fall within this risk profile.

Your tolerance to market fluctuations. Your main focus is maximising investment returns; risk is not a consideration. You have a high tolerance to any short-term investment market fluctuations, and are comfortable with the notion that over the long-term the best way to maximise returns is through growth assets. As such you would feel comfortable with a more aggressive portfolio structure (eg exposure to Australian and International shares).

Important Details about Your Risk Profile The details below show how your money should be invested under your risk profile. However following discussions, you have

specifically stated your interest in long term growth investments therefore as a result your investment option will not be aligned

to your benchmark asset allocation.

Benchmark Asset Allocation: High Growth

Investment term 7 Years

Benchmark: net return objective CPI plus 4%

Asset Balance: growth / income 100% / Nil

Probability of a negative return* 18.10%

Statement of Advice for John & Mary Smith Page 5 of 37

Your Personal Insurance Needs This section describes your personal insurance requirements and how we calculated the amount of insurance that you need.

Personal risk insurance gives you the peace of mind that you and your dependants are financially supported in the event of serious illness, disability or death.

Your Insurance Requirements The amount of insurance cover recommended is based on your personal and financial details. To calculate your insurance requirements we have taken into account:

Your income, expenses, assets and liabilities.

Your personal insurance goals.

Insurance Needs Calculations

John Mary

Mortgage Repayments

(Family home, Investment Property & Car loan) $787,500 $787,500

Replacement of Income (p.a.) $215,000 Nil

Number of years for replacement income to last (total) 21 years (till age 65) 23 years (till age 65)

Return expected from investment (post tax) 5.00% 5.00%

Assumed inflation rate 3.00% 3.00%

Dependents

Annual income required to maintain education / lifestyle costs Sam (Age 1) - $15,000 p.a.(17 years for income to last)

Expenses upon death funeral, legal etc $25,000 $25,000

Expenses upon TPD, legal & home refurbishment etc $25,000 $25,000

Housekeeper/Nanny/Childcare (not covered above) $25,000 $25,000

Expenses upon Trauma, medical / hospital costs etc $50,000 $50,000

Total ideal level of Life cover $6,000,000 $1,000,000

Total ideal level of Total & Permanent Disability cover $2,325,000 $1,000,000

Total ideal level of Trauma cover $800,000 $542,000

Total level of Income Protection cover $171,984 N/A

Statement of Advice for John & Mary Smith Page 6 of 37

What This Advice Covers This section describes what is included in our advice, and any limitations of our advice. It also outlines areas of advice that we have agreed with you are not to be included and explains why.

Advice Addressed

Superannuation planning

Wealth Protection

Estate Planning

General and Health Insurance We are not authorised or qualified to provide advice regarding general insurance products or health insurance products. These products play an important part in your overall financial plan and we recommend that you seek advice in these areas to ensure that:

Your assets (for example, your home, contents and motor vehicle) are protected from loss or damage.

You and your family are provided with the required level of health care and hospital cover.

Tax issues Please note that I am not a Registered Tax (Financial) Adviser. We therefore recommend that you seek further advice from your tax specialist about the tax consequences of the recommendations outlined in this Statement of Advice (SoA).

Product Recommendations from the Approved Product List The range of financial products we provide advice on are listed in the Count Financial Limited approved product list. These products are subject to a rigorous due diligence process by the Count Research Committee and are actively monitored on a daily basis thereafter.

Important Information In Relation To Limited Advice If you have sought advice on a specific subject you need to be aware that my advice will be limited to that subject and your circumstances relevant to that subject only. Before acting on the limited advice you need to consider how appropriate it is for you by taking your ‘overall’ objectives, financial situation and needs into account. If now or at any time in the future you decide that you would like advice on the areas that have not been addressed in this SoA, please contact our office.

Statement of Advice for John & Mary Smith Page 7 of 37

Summary of Advice This section summarises our discussion of the recommendations that have been made to meet your needs and goals.

We have offered you a full advice service, however, you have elected to restrict our advice to:

Superannuation Planning

Establish a Self-Managed Super Fund (SMSF) and consolidate both your existing superannuation funds into the SMSF. Open a Macquarie Cash Management Account as the cash hub for the SMSF.

Invest part of your super rollover monies and borrow additional funds into a share portfolio through Macquarie Equity Lever with a pre-selected portfolio.

Direct both your Super Guarantee Contributions (SGC) into the SMSF.

Wealth Protection

Implement both your Life Insurances via your SMSF, the premium will be paid by your SMSF.

Implement Mary’s Total & Permanent Disability Insurances inside your SMSF, the premium will be paid by your SMSF.

Implement John’s Total & Permanent Disability Insurances outside your SMSF, the premium will be paid by you.

Implement both your Trauma and John’s Income Protection insurances outside your SMSF, the premium will be paid by you. These strategies will maximise your tax deductions and create efficient personal cashflow.

Estate Planning

Establish a Will and Power of Attorney for each of you to ensure that your Estate is distributed in the manner you wish.

Statement of Advice for John & Mary Smith Page 8 of 37

Recommended Strategy This section provides details of the strategies that we have recommended and explains how they meet your objectives.

Goal(s) this strategy meets Owning a Self-Managed Super Fund

Establish a Self-Managed Superannuation Fund (SMSF)

We recommend that you:

Establish a Self-Managed Superannuation Fund (SMSF) with a Corporate Trustee.

Consolidate your existing superannuation funds into your SMSF.

Establish a Macquarie Cash Management Account as the cash hub of your SMSF.

Direct your Super Guarantee Contributions and/or salary sacrifice contributions to your SMSF.

Implement an Investment Strategy appropriate to your risk profile for your SMSF.

How this strategy meets your objectives

SMSFs are sometimes referred to as ‘do it yourself’ superannuation funds. SMSFs provide a greater degree of control and flexibility than a public offer superannuation fund, making them suitable for sophisticated investment and retirement strategies.

The main difference between SMSFs and other types of superannuation funds is that a SMSF member also acts as a Trustee (or Director of a Corporate Trustee) and must prepare and implement an Investment Strategy for their fund and manage the benefit payments.

With a Self-Managed Super Fund (SMSF):

You have a greater degree of control and flexibility over your superannuation.

You have the ability to invest in assets not traditionally available within the superannuation environment, such as direct property or alternative assets.

You are able to borrow to invest under a Limited Recourse Loan Arrangement.

You can obtain a more comprehensive insurance policy in the SMSF to protect you against an insured event. Please see our recommendation on insurance for more information.

You have the scope to purchase business commercial property and lease it back to your business – should either of you at some point in the future decide to commence a suitable business.

You can implement tailored Estate planning strategies within your SMSF. It is important to consult a legal professional in relation to Estate planning matters.

To ensure your retirement savings grow over time it is important to:

Make sure your employer contributes to your SMSF.

Have an appropriate Investment Strategy for your SMSF to ensure your funds are invested in accordance with the SMSF’s risk profile.

Having a Corporate Trustee is useful in situations where a single member wants full control over how the fund is managed, where the SMSF members may change, where a member has a high risk of personal litigation, or where the SMSF would like to borrow to invest.

Risks & disadvantages Each Trustee is fully responsible for the decisions and operation of the Fund - this includes overall legislative compliance.

Failure to comply with regulatory and administrative requirements can result in fines, tax penalties and even criminal charges for the Trustees.

For Funds with a lower level of assets, costs may be relatively high as a percentage of the Fund's assets, when compared to other Superannuation Funds

It is essential that you wait until you have been accepted for insurance within the SMSF before relinquishing your existing insurance benefits held in your existing product. Once your insurance application is accepted, rollover the outstanding balance into the SMSF.

Statement of Advice for John & Mary Smith Page 9 of 37

Goal(s) this strategy meets Consolidating your Superannuation Funds

Consolidate your Superannuation Funds

We recommend that you rollover the total balance of your existing superannuation funds into your Self-Managed Super Fund as detailed in the product recommendations section.

Apply for Life cover with your Self-Managed Super Fund being the policy owner. Details of our insurance recommendations can be found in the Wealth Protection section.

How this strategy meets your objectives

By consolidating your superannuation funds and contributions into your SMSF:

You will be able to invest according to your superannuation goals and preferences.

Your super will be easier to track.

You won't be doubling up on account keeping fees.

The SMSF fees are generally a fixed cost and you may find cost efficiencies by having a higher balance in your SMSF.

Please see the Replacement of Product section and for a complete analysis of the current and recommended superannuation funds.

To implement my recommendation:

The process to fully establish your SMSF will take approximately 3-6 weeks. At the end of the process you will receive the Funds’ TFN and/or ABN. You can then apply to rollover your existing superannuation into the SMSF cash hub.

You can then lodge a “Choice of Fund” form with your employer nominating your SMSF to receive your superannuation contributions.

Risks & disadvantages There is no guarantee that the SMSF will outperform your existing funds.

Any fees and costs associated with rolling over your super will reduce your super balance.

There is no guarantee that rolling over your superannuation will provide a better outcome.

If you are maintaining insurance cover in a large APRA regulated fund, the potential loss of insurance benefits as a result of switching from the large fund to a SMSF is an important consideration.

If you are taking out replacement insurance cover through the SMSF it is essential that you wait until you have been accepted for new insurance cover before relinquishing your existing insurance benefits. Once your insurance application is accepted, we recommend that you rollover the outstanding balance into the SMSF.

Time out of the market during the transaction phase may result in the potential loss of returns on your investments during this time period.

Possible loss of tax/franking credits from your current superannuation plans.

For further information regarding this recommendation refer to the following attachments:

Superannuation

Self-Managed Super Funds

SMSFs and Limited Recourse Borrowing Arrangements

Structuring assets in SMSF's

Market volatility

Risk and return

Statement of Advice for John & Mary Smith Page 10 of 37

Goal(s) this strategy meets Investing your Super monies into Growth assets to build for future retirement

Invest with Macquarie Equity Lever

We recommend that you:

Invest $150,000 of your super rollover monies and borrow an additional $150,000 into a share portfolio through Macquarie Equity Lever.

Select the Growth Plus pre-selected portfolio. This share portfolio consists of 6 stocks selected by Macquarie Equity Research.

How this strategy meets your objectives

Macquarie Equity Lever enables you to borrow to invest in selected ASX-listed securities through instalment receipts. Borrowing to invest (or gearing) enables you to boost your investment earning power by increasing the amount of money you have available to invest.

With the Macquarie Equity Lever:

You benefit from any growth and income potential of the selected share portfolio.

You invest a greater amount of total money than you would be able to on your own. This means you can increase your wealth at an accelerated rate.

Interest is capitalised and dividends from the underlying securities are used to reduce the outstanding balance.

You can choose to borrow up to 50% of your share portfolio.

There is no credit assessment upon application.

Your SMSF can choose to receive full legal ownership of the underlying securities once you have made the completion payment.

The Macquarie Equity Lever has a Limited Recourse feature. This simply means that if the final proceeds of the sale of your underlying securities are insufficient to pay the completion payment for all of your instalment receipts, Macquarie cannot seek further payment from you.

You can acquire additional instalment receipts at any time to take advantage of opportunities as they arise.

No withdrawal fees or termination fees apply for early closure of instalment receipts or an early completion payment.

It is an eligible investment for Self-Managed Super Funds (SMSFs) giving you the opportunity to borrow to invest using your SMSF.

You can see the impact of this recommendation on your cashflow in the Summary of Financial Outcomes section of this document.

Risks & disadvantages The Macquarie Equity Lever product has similarities to a margin lending facility in that the investment product is subject to margin calls called ‘instalment acceleration events’. If an instalment acceleration event occurs, you must reduce your current facility Leverage to Valuation Ratio (LVR) to 5% below the maximum facility LVR.

Should you trigger the ‘instalment acceleration event’, you may be forced to sell during a declining market.

Whilst the investors hold the beneficial ownership to the instalment receipt, investors are not entitled to voting rights.

Your investment returns may not offer you above inflation returns.

If your instalment receipt has a fixed interest rate, you may be charged break costs as a consequence of a number of circumstances, including paying your outstanding instalment balance in whole or in part prior to the completion date or as a result of your request for an early closure of your instalment receipts.

Issuance and Advisor brokerage fees apply.

In the same way that gearing has the ability to magnify returns it can also magnify the losses.

You may need to apply for adequate wealth protection cover to protect your income, in the event you cannot return back to work. Insurance premiums may place a strain on your cash flow.

Rising interest rates may dilute the total earnings of this investment product.

Direct shares carry the administration burden of keeping track of paperwork for each stock.

Your direct share portfolio heavily relies on the performance of the Australian stock market. There will be times when the Australian stock market underperforms compared to other asset classes.

In some very minor cases, the listed company may be suspended from the ASX and you may not be able to access these funds until the suspension is removed.

Statement of Advice for John & Mary Smith Page 11 of 37

Goal(s) this strategy meets You would like to protect your family / Estate in the event of disability or death

Implement Life and TPD Insurance

We recommend that each of you apply for the below insurance covers and cancel your insurance policies within your existing super funds:

Implement Life insurance via your SMSF with a benefit amount of $6,000,000 for John and $1,000,000 for Mary.

Implement Total & Permanent Disability (TPD) insurance inside your SMSF with a benefit amount of $1,000,000 Mary. Select ‘Any’ occupation definition because you are currently not working and this is the only available option.

Implement Total & Permanent Disability (TPD) insurance outside of super with a benefit amount of $2,325,000 for John. Select ‘Own’ occupation definition because it is more certain and definitive when it comes to claim-time.

Select a Stepped premium structure as it will be more affordable at the start of the policy however the cost will increase in line with your age.

Select the Premium Waiver option as it waives the premiums payable on your

Life & TPD covers if you are significantly disabled and unable to work for 6 or

more consecutive months.

Through our needs analysis we have modelled the likely financial consequences to you and your family in the unlikely event you were to die prematurely, or were unable to work ever again due to a serious injury or illness which causes total and permanent disability.

Our needs analysis demonstrates that the financial consequences to your family would be very severe.

For this reason, it is our recommendation that increasing your Life and TPD cover to the recommended amount is a prudent risk management strategy. This will ensure that you and your family are protected against the financial consequences of:

Your premature death or diagnosis of a terminal illness; and,

A serious injury or illness which causes Total and Permanent Disability (TPD) and prevents you from working again.

How this strategy meets your objectives

As part of the insurance premiums are paid from your superannuation fund, your disposable income is less affected. It is also tax-effective, as the premiums are tax-deductible to the Trustee of the superannuation fund.

Where the beneficiary is a ‘dependent’, there is no additional tax payable on any life benefit received; do note however that there may be tax payable once the proceeds are invested outside the superannuation environment in their own name (e.g. income tax). ‘Dependent’ in this instance means a spouse, child, financial dependent, or a person who is an interdependent relationship with you.

In the event a TPD benefit is paid, you may choose to receive part, or all, as an income stream, in which case you may be entitled to a 15% tax offset on any taxable component received.

Life and TPD policies can vary in their terms and conditions. Please refer to the product recommendations section for an overview of the features we have recommended.

Risks & disadvantages The recommended TPD amount assumes that you will implement the recommended Income Protection cover, otherwise a much higher amount of TPD cover is required.

You may be subject to premium loadings and/or exclusions.

You may be required to undertake a number of medical assessments and procedures to have your claim approved.

There is a possibility that a claim may not be successful.

For further information regarding this recommendation refer to the following attachments:

Holding insurance through your SMSF

Statement of Advice for John & Mary Smith Page 12 of 37

Goal(s) this strategy meets You would like to ensure that you and your family are financially protected in the event that you suffer from serious illness

Apply for Trauma Insurance We recommend that you apply for the below insurance covers and cancel your existing Trauma insurance:

Implement Trauma insurance with a benefit amount of $800,000 for John.

Implement Trauma insurance with a benefit amount of $542,000 for Mary.

Select the Reinstatement option because if the full Trauma cover lump sum is

paid out you will be offered the opportunity to reinstate your Trauma insurance

12 months after the claim is paid.

Select a Stepped premium structure because it will be more affordable at the

start of the policy however the cost will increase in line with your age.

Select the Premium Waiver option as it waives the premiums payable on your

Trauma covers if you are significantly disabled and unable to work for 6 or more

consecutive months.

The insurance policy should be held in your own names and paid for through your disposable income.

Trauma policies can vary in their terms and conditions. Please refer to the product recommendations section for an overview of the features we have recommended.

How this strategy meets your objectives

Our needs analysis demonstrates that if you or your family experienced a serious health condition that resulted in unexpected medical expenses and affected your ability to work for up to 2 years, the financial consequences to your family would be severe.

Implementing the recommended level of Trauma insurance would allow you to address immediate medical expenses, maintain existing living expenses, and focus on the task of rehabilitation and recovery.

Health conditions that are often classified as trauma events include cancer, heart attack, and stroke among others. A full listing of the conditions that you would be insured against in the recommended policy can be found in the Product Disclosure Statement (PDS).

Key benefits of this strategy include:

You receive a lump sum benefit when you suffer a condition specified in your policy regardless of your ability to return to work.

The lump sum benefit can be used for any purpose you choose, such as paying for medical treatment/s or reducing debts.

Owning and paying for the policy in your own name means that you retain control of the policy and no tax will be payable upon payment of the benefit.

Risks & disadvantages The recommended Trauma amount assumes that you have, or will take out, Income Protection cover. If you do not have any Income Protection cover a much higher amount of Trauma cover is required.

Premiums are to be paid from your disposable income which reduces your overall cash flow.

Some less severe conditions attract a partial payment only.

For further information regarding this recommendation refer to the following attachments:

Protecting you and your family

Statement of Advice for John & Mary Smith Page 13 of 37

Goal(s) this strategy meets To ensure your income is protected in the event that you are unable to work due to temporary illness or disability.

Apply for Income Protection Insurance

We recommend that you implement Income Protection insurance covers and cancel your existing cover:

With a benefit of $14,332 per month (based on John’s annual income of $215,000 including SGC).

Cover at an Agreed Value - This type of policy provides more certainty regarding Income Protection benefits as your salary is assessed at time the policy commences.

Select a benefit with a Waiting Period of 30 days and a Benefit Period ‘to Age 65’ so you can receive benefits up to your presumed retirement age.

Select the SuperSaver option that allows you to cover regular superannuation contributions.

Select a Stepped premium structure because it will be more affordable at the start of the policy however the cost will increase in line with your age.

Held in your own name and paid for through your disposable income.

Income Protection policies can vary in their terms and conditions. Please refer to the product recommendations section for a more detailed explanation of the features we have recommended.

How this strategy meets your objectives

Our needs analysis demonstrates that if your income were interrupted due to a protracted illness or injury, the financial consequences to you and your family would be severe.

With Income Protection cover, up to 75% of your income is replaced if you are unable to work due to illness or injury. So you don't have to worry about covering your existing expenses and can focus on the task of rehabilitation and recovery.

You would begin receiving the monthly benefit if you were unable to return to work beyond the end of the waiting period. Your benefit would continue to be paid until one of the following events happen:

You return to work

The benefit period ends

The policy end-date is reached.

Commencement of the waiting period typically begins on the day your condition is diagnosed by a Doctor. For this reason it is crucial that you visit a medical Doctor immediately if you experience an illness or injury that affects your work capacity. Please

contact our office in the first instance should there be a potential claim. Our job is to assist you in this process.

Key benefits of this strategy include:

Up to 75% of your income is replaced if you are unable to work due to illness or injury.

Where you have a disability that partially affects your work capacity, you may be eligible to a partial disability benefit.

Owning and paying for the policy in your own name means that you retain control of the policy.

The premiums are generally deductible for tax purposes to the policy owner. Please speak to your Accountant should you require more information.

Risks & disadvantages The premiums are paid from your post-tax income which reduces your overall disposable income.

The monthly benefit received in the event of a claim is generally considered as assessable income for tax purposes. The Insurer will pay you the full monthly benefit and it is your responsibility to set aside the amount which is payable to the Australian Taxation Office. Please speak to your Accountant should you require more information.

For further information regarding this recommendation refer to the following attachment:

Protecting you and your family

Statement of Advice for John & Mary Smith Page 14 of 37

Goal(s) this strategy meets Establish a Will and Power of Attorney to ensure that your Estate is distributed in the manner you wish.

Establish a Will and POA We recommend that you establish a Will and Power of Attorney for each of you with a legal professional.

How this strategy meets your objectives

Having a current and valid Will is the only way of ensuring that your wealth is transferred to the people you would like it to go to once you pass away. Without a Will, your assets will be distributed according to a government formula that may not provide the best result for your family and loved ones.

Key benefits of having a Will:

You can decide now how you would like your assets and possessions to be distributed.

You have peace of mind that your wishes will be carried out once you pass away

You can appoint a guardian for any children under 18 years of age.

You can provide your family with certainty with regards to the distribution of your Estate.

An Enduring Power of Attorney is a legal document that allows a person to act on your behalf if you are unable to take care of your financial matters. An Enduring Power of Attorney is useful to have for times when you cannot manage your financial affairs yourself, such as:

When you are absent for an extended period, such as travelling overseas.

When you have a prolonged illness that prevents you from looking after your day-to-day finances.

In the event of your mental incapacity.

An Enduring Power of Attorney gives you peace of mind that your financial interests will be looked after by someone you have chosen and who you trust.

Risks & disadvantages You should seek independent legal advice to ensure all your Estate planning needs are in order. This is a complex area and I am not a legal practitioner.

Failure to obtain independent legal advice may result in your Estate planning not being structured in an appropriate manner.

The person you grant an Enduring Power of Attorney to may act dishonestly or improperly and you may be placed at a disadvantage as a result of your attorney's actions.

If you cancel or alter your Power of Attorney you will have the responsibility of informing all organisations you deal with otherwise they can continue to operate under the previous arrangement.

The power that is bestowed may be limited to financial matters depending on the state you reside in.

For further information regarding this recommendation refer to the following attachments:

Estate Planning

Statement of Advice for John & Mary Smith Page 15 of 37

Review Service We are committed to providing you with regular reviews and an ongoing service of professional advice and support. We have provided you with our Total Financial Care offer and Agreement (attached) that details the benefits of our ongoing service, including regular reviews. Below is a summary of our recommended review package:

What’s Included Growth

Unlimited Phone / Email Support Moderate

(Next Day)

Portfolio Snapshots Quarterly

Transaction per annum (e.g. Fund-Switches, Rebalances, Withdrawals) 3

Online access to your portfolio via client portal

Active monitoring of your investment portfolio’s research status

Will Review Service

Home Loan Review Service

Annual Financial Plan Review

Quarterly Education Newsletter

Quarterly Wealth Webinars

Half-Yearly Financial Plan Review

Share-Trading: Same Day Execution

Interim review in the event your circumstances change

Half Yearly Seminars

Share Trading: Priority / Instant Execution

Exclusive Economist & Fund Manager Invitation-only Presentations

$275 / month Including GST

(Paid by your SMSF)

Cost of Ongoing Service

To ensure you keep on track with your financial position including your insurances and new superannuation fund, we would like to conduct an annual review and therefore recommend you implement our Growth Package which comes at the cost of $275 (incl. GST) per month. In your particular instance rather than charging this amount to you each individually, we have elected to waive part of the fee and cover you both under the one ongoing service subscription. Should you require any additional services outside of any agreement between you and your Advisor, an amount of up to $650 (incl. GST) per hour may be applied. Count may retain a portion of fees and commissions received from the providers of the underlying products. Where this applies all fees and commissions will be disclosed in your Statement of Advice. Acceptance of the Total Financial Care service does not waive your right to retain absolute discretion over decisions affecting your financial plan. Strategic advice and financial product implementation will only occur with your signed authorisation. However, should you not accept the review service, once the recommendations contained in this financial plan have been implemented, our service to you will be deemed completed. Either party may request an amendment or cancellation of this review agreement at any time. We look forward to providing you with services that meet all your future financial planning needs. Should you require any further advice please do not hesitate to contact any of our staff on 07 3226 9999. As part of our Review service, we will address the following matters during our next Review Meeting:

Financial Position How your personal situation has changed

Goals & Objectives How you are tracking towards meeting your goals / Addressing any new goals or objectives you have identified

Financial Position Income and expenses position / Review of your Assets and Liabilities and Investments under Advice

Wealth Protection If your debt levels have changed / Changes to your employment or income levels / Changes in marital status or dependents

Estate Planning How current your Will and Power of Attorney arrangements are / Whether you have a disaster plan in place that your family can rely upon

Your Portfolio Your portfolio performance, asset allocation and other points relevant to your portfolio

Statement of Advice for John & Mary Smith Page 16 of 37

Alternative Strategies Considered Below are the alternative strategies that we considered before making a final recommendation to you. From the possible strategies that we considered, we have selected the recommended strategy because it is more appropriate your financial situation, needs and goals.

Retaining your current superannuation monies ‘as-is’, however this won’t allow you to invest into shares as you

have specifically mentioned your intention/wish to do.

Self-Funding your potential insurance needs, however this was discounted due to your cashflow being insufficient

at least in the short-term to adequately fund the needs of your family and dependents in the event of sudden

death/injury/accident/disablement.

From the available strategies that we considered, we have selected the recommended strategy because it is appropriate for

your objectives, financial situation and needs and seeks to achieve the goals detailed in the Meeting Your Goals and

Objectives.

Statement of Advice for John & Mary Smith Page 17 of 37

Recommended Products This section provides you with detail about the products that we have recommended to meet your needs.

Superannuation Product Recommendations Outlined below are our superannuation investment recommendations. We believe that the recommended portfolio along with our strategy recommendations will assist you to achieve your goals and needs. Please see the investment summaries attached for a description of the individual investments that we have recommended. Investment summaries have been provided within the attachments accompanying this Statement of Advice.

Existing Investments

Russell Investments Super Allocation Current Adjustment Proposed

Australian Shares 20% $32,870 -$32,870 $0.00

Russell Conservative 20% $30,093 -$30,093 $0.00

Russell Growth 50% $81,687 -$81,687 $0.00

Socially Responsible Australian Shares 10% $16,405 -$16,405 $0.00

Total 100% $161,055 -$161,055 $0.00

Commonwealth Bank Group Super Allocation Current Adjustment Proposed

Mix 70 100% $38,000 -$38,000 $0.00

Total 100% $38,000 -$38,000 $0.00

Proposed Investments

Self-Managed Super Fund Allocation Current Adjustment Proposed

Macquarie Cash Management Account 100% $0.00 $ 49,055 $ 49,055

Total Cash 100% $0.00 $ 49,055 $ 49,055

Macquarie Equity Lever*

BHP Billiton (BHP) 17.50% $0.00 $ 50,565 $ 50,565

CSL Ltd (CSL) 20.00% $0.00 $ 57,788 $ 57,788

Oil Search (OSH) 17.50% $0.00 $ 50,565 $ 50,565

Ramsay Health Care (RHC) 20.00% $0.00 $ 57,788 $ 57,788

Sonic Healthcare (SHL) 15.00% $0.00 $ 43,341 $ 43,341

Wesfarmers (WES) 10.00% $0.00 $ 28,894 $ 28,894

Total Macquarie Equity Lever 100.00% $0.00 $ 288,940 $ 288,940

Total SMSF 100.00% $0.00 $ 337,995 $ 337,995

* The Macquarie Equity Lever portfolio value is end result of all the investment costs being deducted

Macquarie Equity Lever Facility Details - Growth Plus

Investment Term 5 years

Interest Election

Interest Rate 7.55%

Marginal Tax Rate 15%

LVR % 50%

Total Portfolio Value $288,940

Variable in arrears

BHP17.50%

CSL20.00%

OSH17.50%

RHC20.00%

SHL15.00%

WES10.00%

ASSET EXPOSURE

Statement of Advice for John & Mary Smith Page 18 of 37

The investment amounts above are subject to change due to market fluctuation in prices. Therefore, the final balance should be invested in proportion to the percentages as shown in the portfolio projection sheets attached to this Statement of Advice.

Portfolio Construction Following is an outline of how your portfolio was constructed. It explains how we selected the individual investments to construct your overall portfolio.

Share Portfolio Use the rollover monies of $150,000 and borrow an additional $150,000 to invest into a share portfolio through Macquarie Equity Level. Please refer to the attached appendix for further details, i.e. Cashflow summary, dividend yields.

Cash At this stage, we’d recommend that you retain the monies referred to above in your SMSF’s Cash Account (approximately $49,055) in Cash to cover various expenses such as insurance premiums in the SMSF.

Macquarie Equity Lever - Structure of the Investment Equity Lever is a Limited Recourse structured product that allows investors to purchase certain ASX-listed securities (called the Underlying Securities) from Macquarie in two or more instalment payments. Instalment Receipts are a permitted investment for Self-Managed Superannuation Funds (SMSFs) provided the investment complies with the fund's investment strategy and is in the best interests of its members. Each time the investor purchases an Underlying Security via Equity Lever, they are acquiring an Instalment Receipt. Individual Instalment Receipt holdings of each investor are consolidated under their Equity Lever Facility for purposes of reporting and risk management. By investing in Instalment Receipts, an investor can leverage their exposure to the performance of a particular Underlying Security by paying only a portion of the Purchase Price upfront. During the term of the investment, the investor is entitled to all capital growth as well as rights and entitlements to ordinary dividends, income distributions and franking credits (subject to eligibility and own circumstances). Ordinary dividends are generally directed to reduce the Final Instalment on the Instalment Receipts. Instalment Receipts in Equity Lever are “unlisted”, which means that they cannot be traded on the ASX or any stock exchange.

Macquarie Cash Management Account When you set-up a Self-Managed Super Fund (SMSF), you will need to open a cash account in your fund's name so that you can accept contributions and rollovers of super benefits. A Macquarie Cash Management Account is well suited for the management of SMSFs because it acts as a central source for the movement of money in and out of the multiple cash streams.

Statement of Advice for John & Mary Smith Page 19 of 37

Asset Allocation Your recommended asset allocation is based on your risk profile. For more information on your risk profile please refer to the ‘Your tolerance to investment risk’ section.

Asset allocation is a term used to describe how much of your money is invested in different asset classes. Our investment research has shown that consistent long-term returns can be enhanced through a diversified portfolio that contains a selection of asset classes.

Your Actual and Recommended Asset Allocation

The chart and table below show the asset allocation of your portfolio once my recommendations in this Statement of Advice have been implemented. It also shows how this asset allocation compares to the benchmark allocation appropriate for your risk profile.

Asset Allocation Current -

John Current -

Mary Proposed

Weight Target

Weight Target

Min Target

Max Variance from Target Weight

Alternative - Absolute Return 3.94% 17.00% 0.00% 10.50% 0.00% 20.50% -10.50%

Alternative - Real Return 0.00% 0.00% 0.00% 9.00% 4.50% 13.50% -9.00%

Australian Equities 50.29% 25.00% 89.70% 43.00% 33.00% 53.00% 46.70%

International Equities 20.00% 20.00% 0.00% 29.00% 19.00% 39.00% -29.00%

Property & Infrastructure 6.60% 12.00% 0.00% 8.50% 4.30% 12.80% -8.50%

Fixed Interest 13.88% 24.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Cash 5.04% 2.00% 10.30% 0.00% 0.00% 0.00% 10.30%

Other 0.25% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Total 100.00% 100.00% 100.00% 100.00% 0.00%

To ensure the Fund’s portfolio properly reflects the investment strategy, it is important that it is closely aligned to the Fund’s

benchmark asset allocation. Ideally, the portfolio should be allocated and remain within 10% of the member’s benchmark asset

allocation in all asset classes.

The recommended portfolio does not match the Fund’s benchmark asset allocation within a + or – 10% range in all asset

classes. However you have stated a preference in particular for Shares as an investment asset, and therefore while we have

attempted to create a well-diversified portfolio, as you can see in the graph above, the resulting underlying assets of this

portfolio will be heavily weighted towards Australian Share and Cash and subsequently underweight in all the other asset

classes. Following discussions you have stated you are comfortable and happy with this.

Statement of Advice for John & Mary Smith Page 20 of 37

Insurance Product Recommendations To determine the best product to suit your overall personal insurance needs we researched a wide range of insurance products that could provide the required cover, as detailed in the summary of insurance requirements table below. As part of this research, we also took into consideration:

Products that had the features which best suited your circumstances and needs.

Generic issues such as the insurance provider’s claims history, competitiveness of premiums, administration efficiency,

and underwriting process.

Your Existing Insurance

Cover Policy Owner Life Insured Benefit Amount Premium (p.a.)

Life & Total Permanent Disability Insurance

Trustee of the Russell Investments Super

John

$535,000 $374.40

Trauma Insurance

John

$153,727 $620.76

Income Protection Insurance $4,682/mth $1,504.44

Income Protection Insurance $3,796/mth $1,219.80

Total $3,719.40

Personal Insurance Policy Recommendations Based on our research and your requirements we recommend you implement the following personal insurance through Asteron Life and cancel your existing insurances:

Cover Policy Owner Life Insured Benefit Amount Premium (p.a.)

Life Insurance SMSF

John

$6,000,000 $2,761

Total Permanent Disability Insurance (outside Super)

John

$2,325,000 $1,196

Trauma Insurance $800,000 $1,456

Income Protection Insurance $171,894

($14,324/mth) $2,642

Total $8,056

Cover Policy Owner Life Insured Benefit Amount Premium (p.a.)

Life Insurance SMSF

Mary

$1,000,000 $390

Total Permanent Disability Insurance (inside Super)

$1,000,000 $693

Trauma Insurance Mary $542,000 $1,253

Total $2,335

* Please note policy fees and stamp duty will apply upon application

Product Features As part of this insurance strategy and product recommendation we have selected the following policy options and features to meet your specific requirements. Further detail can be found in the insurance Product Disclosure Statements (PDS) provided with this document. The Asteron Life insurance cover we are recommending contains the following options and features which, in our opinion, are relevant to your protection requirements. Should you require more information please refer to the Asteron Life Disclosure Statements (PDS). Life Cover Features

Type Description

Stepped Premium Stepped Premiums start lower than a Level Premium and increase as you age. This means the earlier years of your policy are more affordable, but as it becomes more expensive as you age, the policy may be less affordable further down the track.

Waiver of Premium Asteron will waive the premiums payable on your Life Cover while you are significantly disabled and unable to work for 6 consecutive months or more.

Statement of Advice for John & Mary Smith Page 21 of 37

Total Permanent Disability (TPD) Cover Features

Type Description

Stepped Premium Stepped Premiums start lower than a Level Premium and increase as you age. This means the earlier years of your policy are more affordable, but as it becomes more expensive as you age, the policy may be less affordable further down the track.

Waiver of Premium Asteron will waive the premiums payable on your TPD Cover while you are significantly disabled and unable to work for 6 consecutive months or more.

TPD - Own Occupation An 'Own' TPD definition assesses TPD on the basis of the Insured's inability to complete their own or usual occupation, and typically provides a stronger overall level of protection relative to other TPD definitions.

TPD - Any Occupation An ‘Any’ TPD definition allows you to move in and out of the workforce without having to change the TPD definition. At claim time, Asteron will assess you under either the home-make TPD definition or ‘Any occupation’ TPD definition depending on whether you are a home-maker or in paid employment at the time of disablement.

Trauma Cover Features

Type Description

Stepped Premium Stepped Premiums start lower than a Level Premium and increase as you age. This means the earlier years of your policy are more affordable, but as it becomes more expensive as you age, the policy may be less affordable further down the track.

Waiver of Premium Asteron will waive the premiums payable on your Trauma Cover while you are significantly disabled and unable to work for 6 consecutive months or more.

Reinstatement Option If the full Trauma cover lump sum is paid out you will be offered the opportunity to reinstate your Trauma insurance 12 months after the claim is paid.

Income Protection Cover Features

Type Description

Stepped Premium Stepped Premiums start lower than a Level Premium and increase as you age. This means the earlier years of your policy are more affordable, but as it becomes more expensive as you age, the policy may be less affordable further down the track.

Agreed Value The monthly benefit is the agreed amount when Asteron accept your application including any increases under Automatic Increase, regardless of any subsequent rise or fall in your income.

Waiting Period – 30 days The waiting period is the period of time that must elapse before Asteron will pay a claim. Payments are made monthly in arrears after the end of the waiting period. For example, your waiting period is 30 days Asteron will make the first payment after 60 days.

Benefit Period – to age 65 The benefit period is the maximum period of time for which Asteron will pay a benefit whilst you’re disabled.

Super Saver Option You can apply to insure an additional 5% of your monthly income for superannuation contributions.

Crisis Benefit (built-in) If you suffer one of the defined medical events (listed on page 47 of the PDS). Asteron will treat you are if you are totally disabled any pay the Totally Disabled Benefit for up to 6 months without applying the waiting period. Asteron will also boost your monthly benefit by 1/3 during the specified payment period only.

Specific Injury Benefit

(built-in)

If you suffer one of a list of specified injuries, Asteron will pay the Totally Disabled Benefit for a specified payment period without applying the waiting period.

Please refer to the attached Product Disclosure Statement (PDS) for more information on the above benefits.

Important Notes This is not an offer of insurance

The above recommendation is not an offer for insurance. It is a recommendation that you apply to get insurance. The insurance companies will then review your application and come back to you with one of the following responses:

An offer to provide you with cover on standard terms

An exclusion of cover for pre-existing conditions

An offer based on an increased premium due to your personal or employment circumstances

Decline to offer you cover due to your personal or employment circumstance Important information on applying for personal insurance During the insurance application process you have a duty of disclose to the Insurer. This means that you must disclose everything you know or could reasonably be expected to know, that is relevant to the Insurer’s decision whether to accept the risk of providing you with terms of insurance. Refer to the Product Disclosure Statement for full details.

Statement of Advice for John & Mary Smith Page 22 of 37

Financial Outcomes of Recommended Strategy This section highlights the value of this advice by demonstrating the financial benefits of the recommended strategies.

Financial Outcome of the Macquarie Equity Lever The below table shows the estimated portfolio cashflow for the next 10 years, based on the reasonable assumptions made when formulating our recommendations. Please note that as dividend yields, market performance, interest rates and taxation rates are all subject to future change, any such changes may impact both this projection as well as the future outcome of the portfolio and our recommended strategy. This is why it is vital that you and your portfolios and strategies are regularly reviewed. CASHFLOW SUMMARY

Pre-Tax Cashflow Analysis 30-Jun-

15 30-Jun-

16 30-Jun-

17 30-Jun-

18 30-Jun-

19 30-Jun-

20 30-Jun-

21 30-Jun-

22 30-Jun-

23 30-Jun-

24 1-Jul-24

Distributions Received 8,136 9,549 10,387 10,843 12,080 12,857 13,588 13,588 13,588 13,588 -

Interest Paid (11,016) (11,219) (11,285) (11,338) (11,329) (11,272) (11,088) (10,893) (10,682) (10,485) (28)

Pre-Tax Benefit / (Cost) (2,880) (1,670) (898) (495) 750 1,585 2,499 2,695 2,906 3,103 (28)

Post-Tax Cashflow Analysis - Income Account

Assessable Income

Distribution Received 8,136 9,549 10,387 10,843 12,080 12,857 13,588 13,588 13,588 13,588 -

Franking Credits 2,456 2,435 2,720 2,851 3,180 3,308 3,493 3,493 3,493 3,493 -

Total Assessable Income 10,592 11,983 13,107 13,694 15,259 16,165 17,081 17,081 17,081 17,081 -

Allowable Deductions

Deductible Interest (10,112) (10,298) (10,359) (10,408) (10,399) (10,347) (10,179) (9,999) (9,806) (9,625) (26)

Total Allowable Deductions (10,112) (10,298) (10,359) (10,408) (10,399) (10,347) (10,179) (9,999) (9,806) (9,625) (26)

Taxable Gain / (Loss) 480 1,685 2,748 3,286 4,860 5,818 6,903 7,082 7,275 7,457 (26)

Tax Refund / (Payment) (72) (253) (412) (493) (729) (873) (1,035) (1,062) (1,091) (1,119) 4

Franking Credits 2,456 2,435 2,720 2,851 3,180 3,308 3,493 3,493 3,493 3,493 -

Net Tax Refund / (Payment) 2,384 2,182 2,308 2,358 2,451 2,436 2,458 2,431 2,402 2,375 4

Pre-Tax Benefit / (Cost) (2,880) (1,670) (898) (495) 750 1,585 2,499 2,695 2,906 3,103 (28)

plus: Net Tax Refund / (Payment) 2,384 2,182 2,308 2,358 2,451 2,436 2,458 2,431 2,402 2,375 4

After-Tax Benefit / (Cost) (496) 512 1,410 1,863 3,201 4,020 4,957 5,126 5,307 5,478 (24)

After-Tax Benefit / (Cost) (as % of Outstanding Instalment Balance) (0.34%) 0.35% 0.94% 1.24% 2.12% 2.68% 3.34% 3.51% 3.70% 3.90% (0.02%) Outstanding Instalment Balance 147,817 149,487 150,385 150,880 150,130 148,545 146,046 143,351 140,445 137,343 137,371

Post-Tax Cashflow Analysis - Capital Account (At Maturity)

Market Value of Securities 316,011 344,479 375,475 409,263 446,093 486,255 530,014 577,711 629,702 686,387 686,549

Cost Base (incl. Brokerage) - - - - - - - - - - 301,018

Notional Put Cost Base - - - - - - - - - - 9,078

Taxable Capital Gain / (Loss) - - - - - - - - - - 385,531

Immediate CGT Offset / (Payable) - - - - - - - - - - (38,553)

Marginal Tax Rate 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00% 15.00%

Initial Position

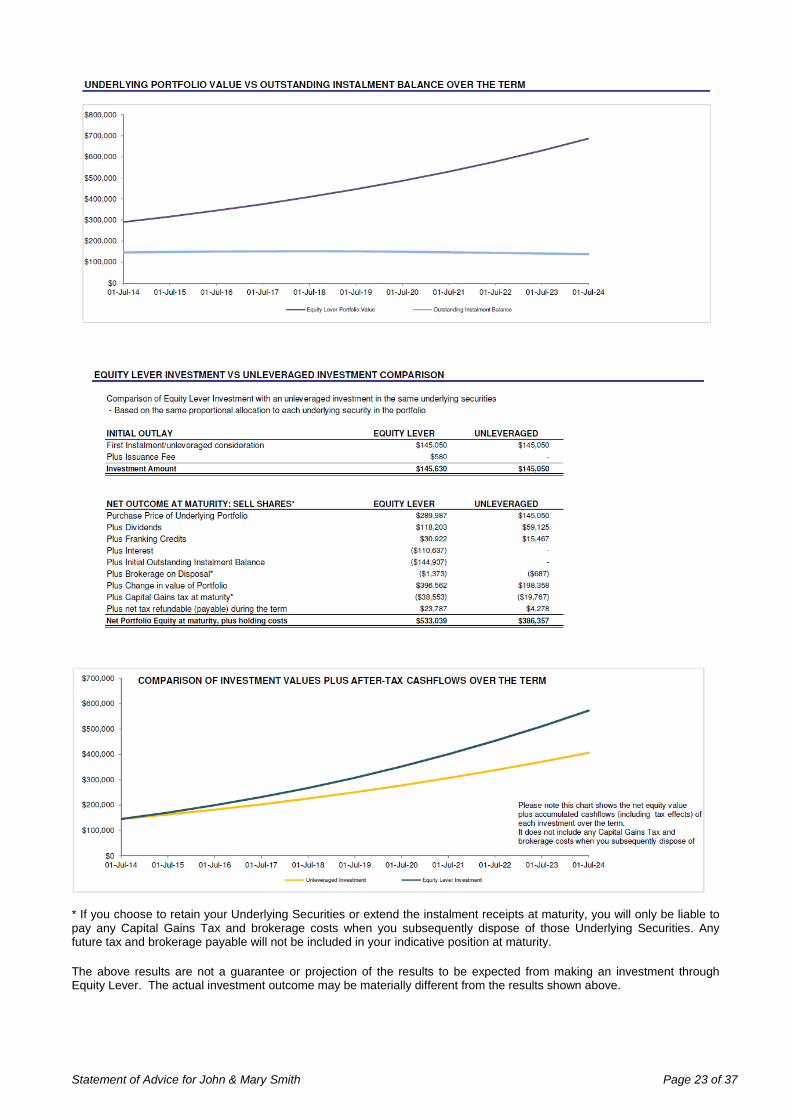

Investment Start Date 2014 Investment Term 10 Years Completion Date 2024 Interest Election Variable in arrears Interest Rate 7.55% First Instalment $145,050 Issuance Fee $580 Investment Amount $145,630 Initial Final Instalment $144,937

Net Outcome at Maturity: Sell Shares*

Value of Underlying Portfolio $686,549 Plus Brokerage on Disposal* ($1,373) Plus Outstanding Instalment Balance to be paid ($137,371) Plus Capital Gains tax at maturity * ($38,553) Plus net tax refundable (payable) during the term $23,787

Net Portfolio Equity at maturity, plus holding costs $533,039

Statement of Advice for John & Mary Smith Page 23 of 37

* If you choose to retain your Underlying Securities or extend the instalment receipts at maturity, you will only be liable to pay any Capital Gains Tax and brokerage costs when you subsequently dispose of those Underlying Securities. Any future tax and brokerage payable will not be included in your indicative position at maturity.

The above results are not a guarantee or projection of the results to be expected from making an investment through Equity Lever. The actual investment outcome may be materially different from the results shown above.

Statement of Advice for John & Mary Smith Page 24 of 37

Products to be Replaced This section explains the benefits, consequences and costs of our recommendation to replace your existing product(s) with new product(s).

We have recommended that you replace one or more of your existing products with new products based on our research into the advantages and disadvantages associated with the replacement. But before you replace any products, it is important that you understand the implications of cancelling. Outlined below is a comparison between your existing and recommended products to help you understand the implication of replacing any products. This includes information on:

Any charges which you may incur as a result of the product replacement.

Any benefits which you may lose (even if only temporarily) or gain if you accept my recommendation.

Information about any other significant consequences we are aware of.

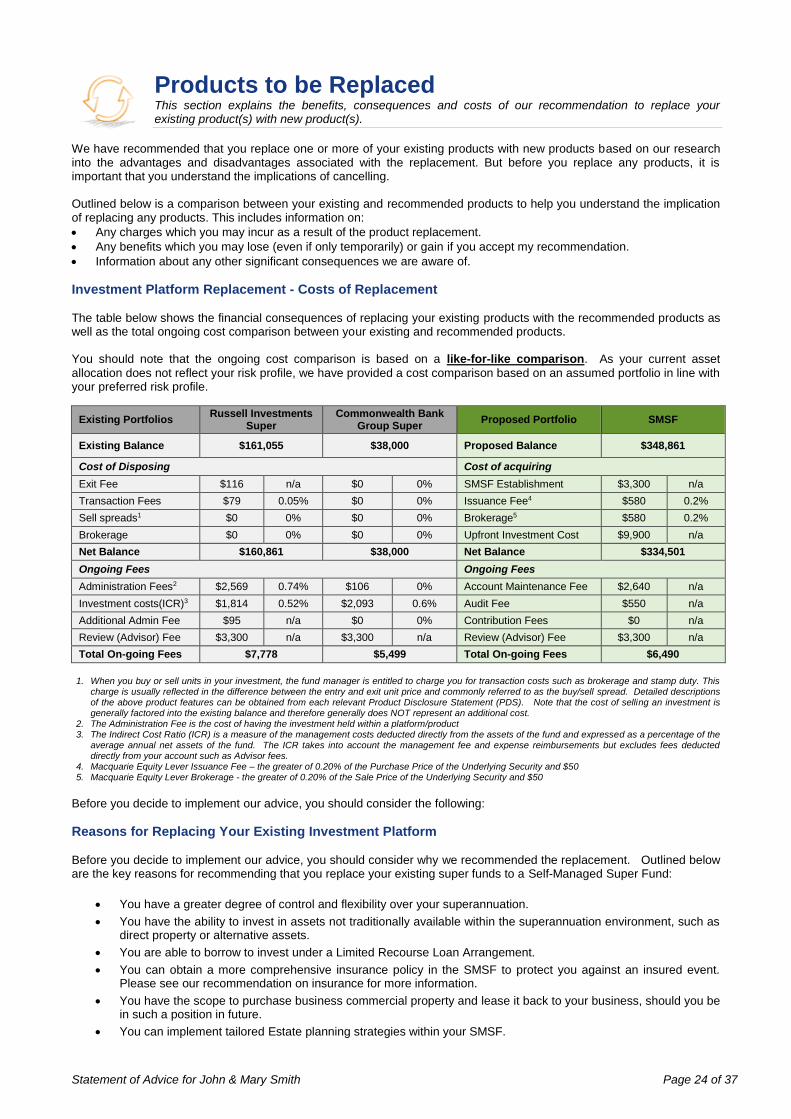

Investment Platform Replacement - Costs of Replacement The table below shows the financial consequences of replacing your existing products with the recommended products as well as the total ongoing cost comparison between your existing and recommended products. You should note that the ongoing cost comparison is based on a like-for-like comparison. As your current asset

allocation does not reflect your risk profile, we have provided a cost comparison based on an assumed portfolio in line with your preferred risk profile.

Existing Portfolios Russell Investments

Super Commonwealth Bank

Group Super Proposed Portfolio SMSF

Existing Balance $161,055 $38,000 Proposed Balance $348,861

Cost of Disposing Cost of acquiring

Exit Fee $116 n/a $0 0% SMSF Establishment $3,300 n/a

Transaction Fees $79 0.05% $0 0% Issuance Fee4 $580 0.2%

Sell spreads1 $0 0% $0 0% Brokerage5 $580 0.2%

Brokerage $0 0% $0 0% Upfront Investment Cost $9,900 n/a

Net Balance $160,861 $38,000 Net Balance $334,501

Ongoing Fees Ongoing Fees

Administration Fees2 $2,569 0.74% $106 0% Account Maintenance Fee $2,640 n/a

Investment costs(ICR)3 $1,814 0.52% $2,093 0.6% Audit Fee $550 n/a

Additional Admin Fee $95 n/a $0 0% Contribution Fees $0 n/a

Review (Advisor) Fee $3,300 n/a $3,300 n/a Review (Advisor) Fee $3,300 n/a

Total On-going Fees $7,778 $5,499 Total On-going Fees $6,490

1. When you buy or sell units in your investment, the fund manager is entitled to charge you for transaction costs such as brokerage and stamp duty. This

charge is usually reflected in the difference between the entry and exit unit price and commonly referred to as the buy/sell spread. Detailed descriptions of the above product features can be obtained from each relevant Product Disclosure Statement (PDS). Note that the cost of selling an investment is generally factored into the existing balance and therefore generally does NOT represent an additional cost.

2. The Administration Fee is the cost of having the investment held within a platform/product 3. The Indirect Cost Ratio (ICR) is a measure of the management costs deducted directly from the assets of the fund and expressed as a percentage of the

average annual net assets of the fund. The ICR takes into account the management fee and expense reimbursements but excludes fees deducted directly from your account such as Advisor fees.

4. Macquarie Equity Lever Issuance Fee – the greater of 0.20% of the Purchase Price of the Underlying Security and $50 5. Macquarie Equity Lever Brokerage - the greater of 0.20% of the Sale Price of the Underlying Security and $50

Before you decide to implement our advice, you should consider the following:

Reasons for Replacing Your Existing Investment Platform Before you decide to implement our advice, you should consider why we recommended the replacement. Outlined below are the key reasons for recommending that you replace your existing super funds to a Self-Managed Super Fund:

You have a greater degree of control and flexibility over your superannuation.

You have the ability to invest in assets not traditionally available within the superannuation environment, such as direct property or alternative assets.

You are able to borrow to invest under a Limited Recourse Loan Arrangement.

You can obtain a more comprehensive insurance policy in the SMSF to protect you against an insured event. Please see our recommendation on insurance for more information.

You have the scope to purchase business commercial property and lease it back to your business, should you be in such a position in future.

You can implement tailored Estate planning strategies within your SMSF.

Statement of Advice for John & Mary Smith Page 25 of 37

Consequences of Replacing Your Existing Investment Platform

You will lose the following benefits by transferring to the recommended product. We believe that the benefits gained outweigh the benefits lost:

The potential loss of tax benefits (i.e. franking credits) could affect the amount of tax you may be required to pay.

As a result of redeeming your existing products you may crystallise a capital loss / incur a capital gain. You should seek tax advice on your entire Capital Gains Tax position.

Time out of the market during the transaction phase may result in the potential loss of returns on your investments during this time period.

Liquidity issues may arise which may impact your ability to access this capital during that time.

There is no guarantee that the replacement product will outperform your existing investment.

Investment Option Replacement We have recommended a change in your underlying investment options. In making this recommendation we have, where possible, attempted to:

Align your asset allocation with your preferred risk profile

Invest your portfolio in higher Lonsec rated funds An analysis of our recommendation is as follows:

Existing Products

Russell Investments Super Invested ($) ICR (%) ICR ($) Buy/Sell (%) Buy/Sell ($)

Australian Shares $32,870 0.59% $194 0.00% $0

Russell Conservative $30,093 0.36% $108 0.00% $0

Russell Growth $81,687 0.43% $351 0.00% $0

Socially Responsible Australian Shares $16,405 1.08% $177 0.00% $0

Total $161,055 0.52% $831 0.00% $0

Commonwealth Bank Group Super Invested ($) ICR (%) ICR ($) Buy/Sell (%) Buy/Sell ($)

Mix 70 $38,000 0.60% $228 0.00% $0

Total $38,000 0.60% $228 0.00% $0

Proposed Products

Self-Managed Super Fund Invested ($) Brokerage Issuance fees Advice Fee

Macquarie Equity Lever $288,940 $580 (0.2%)

$580 (0.2%)

$9,900

Macquarie Cash Management Account $49,055 n/a n/a n/a

Total $337,995 $580 $580 $9,900

When you buy or sell units in your investment, the fund manager is entitled to charge you for transaction costs such as

brokerage and stamp duty. This charge is usually reflected in the difference between the entry and exit unit price and

commonly referred to as the buy/sell spread. Detailed descriptions of the above product features can be obtained from

each relevant Product Disclosure Statement (PDS). Note that the cost of selling an investment is generally factored into

the existing balance and therefore generally does NOT represent an additional cost.

You should seek tax advice on your entire Capital Gains Tax position. Other considerations to be aware of include:

The potential loss of tax benefits (i.e. franking credits) could affect the amount of tax you may be required to pay.

Time out of the market during the transaction phase may result in the potential loss of returns on your

investments during this time period.

Liquidity issues may arise which may impact your ability to access this capital during that time.

The potential for increased volatility resulting from a higher exposure to growth assets.

Statement of Advice for John & Mary Smith Page 26 of 37

Insurance Product Replacement We have recommended that you replace your existing insurance covers with new policies that are more appropriate to your needs.

Product/Underwriter Russell Investment Super - Life Cover

To be replaced with Asteron Life - Life Cover

Costs of replacement The total premium for our recommended policies are higher than your current insurance policies, however it does mean that financially you are better protected overall if an insured event occurs. This is consistent with the needs analysis explained in this advice document.

Reasons for replacement Death cover through your existing fund will cease at age 70 whereas Asteron’s Death

cover continues until you turn age 99.

Your existing covers do not have Guaranteed Future Insurability available.

Benefits gained (Built in benefit)

Automatic Increase / Guarantee to Upgrade / Guaranteed Future Insurability / Grief Support Service / Funeral Advancement Benefit / Premium Freeze Option / Financial Planning Benefit / Premium and Cover Suspension Benefit / Continuation of Cover

Product/Underwriter Russell Investments Super - Total & Permanent Disability (TPD) Cover

To be replaced with Asteron Life – Total & Permanent Disability Cover

Costs of replacement The total premium for our recommended policies are higher than your current insurance policies, however it does mean that financially you are better protected overall if an insured event occurs. This is consistent with the needs analysis explained in this advice document.

Reasons for replacement

TPD covers through your existing fund will cease at age 70 whereas Asteron’s TPD cover continues until you turn age 99.

Select the ’own’ occupation definition because it is more certain and definitive when it comes to claim-time, where your existing insurance product do not have this option available.

Your existing covers do not have Guaranteed Future Insurability available.

Benefits gained (Built in benefit)

Automatic Increase / Guarantee to Upgrade / Guaranteed Future Insurability / Grief Support Service / Financial Planning Benefit / Premium and Cover Suspension Benefit / Premium Freeze Option / Continuation of Cover / Conversion Benefit

Product/Underwriter MLC Life – Trauma Insurance

To be replaced with Asteron Life – Trauma Cover

Costs of replacement The total premium for our recommended policies are higher than your current insurance policies, however it does mean that financially you are better protected overall if an insured event occurs. This is consistent with the needs analysis explained in this advice document.

Reasons for replacement

Supplementary Benefits – additional benefits included such as Conversion Benefit; Premium & Cover Suspension Benefit and Grief Support Service whereas your existing cover do not have such benefits available.

Asteron provides better cover definitions specifically with regards to Prostate Cancers and Heart Attacks as just two examples, and also have a reputation within the industry as having a better track record when it comes to Claims-time (which is when you need to be able to rely on an Insurer).

Benefits gained (Built in benefit)

Automatic Increase / Guarantee to Upgrade / Guaranteed Future Insurability / Grief Support Service / Financial Planning Benefit / Premium and Cover Suspension Benefit / Premium Freeze Option / Continuation of Cover / Conversion Benefit

Product/Underwriter MLC Life – Income Protection

To be replaced with Asteron Life – Income Protection Cover

Costs of replacement The total premium for our recommended policies are higher than your current insurance policies, however it does mean that financially you are better protected overall if an insured event occurs. This is consistent with the needs analysis explained in this advice document.

Reasons for replacement

Critical Condition Benefits – A built in benefit that covers 41 conditions plus numerous claims are allowed under this benefit whereas your existing provider do not have such option available.

Specified Injury Benefit – A built in benefit where If you suffer one of a list of specified injuries, Asteron will pay the Totally Disabled Benefit for a specified payment period without applying the waiting period, whereas your existing policy do not have such option available.

Benefits gained (Built in benefit)

Automatic Increase / Guarantee to Upgrade / Guaranteed Future Insurability / Grief Support Service / Financial Planning Benefit / Premium and Cover Suspension Benefit / Premium Freeze Option / Continuation of Cover / Conversion Benefit

If you are unsure of any of this information, please contact our office.

Statement of Advice for John & Mary Smith Page 27 of 37

The Cost of This Advice This section explains the advice fees and product fees that you will pay as well as the remuneration that member name and Count Financial Limited will receive.

All fees and commissions disclosed are inclusive of GST and are estimates (unless specified below) based on the investment amounts detailed throughout this Statement of Advice (SoA). The actual commission received may vary depending on the initial investment amounts (excluding borrowed amounts) received and the influence of market movements on the value of your investments.

Advice Preparation Fee

The Statement of Advice preparation fee usually comes at the cost of $4,950 (incl. GST). In this instance, however, we

have elected to reduce this fee to $3,300 (incl. GST) for you due to your ongoing relationship with our Firm. You will be

charged for this fee with Change Accountants & Advisors Pty Ltd receiving 85% and Count receiving the remaining 15%.

This fee can be paid from your Self-Managed Super Fund (SMSF). Should you elect to proceed with our advice, this fee

will form part of the plan preparation fees described below.

SMSF Establishment Fees

The table below shows the relevant fees associated with establishment and ongoing maintenance for your SMSF.

Description Amount ($) Who Pays

SMSF Establishment Fee $3,300

Your SMSF

Audit Fee (annually) $550

Ongoing Maintenance Fee (annually) $2,640

Investment Fees – Macquarie Equity Lever

The table below shows the initial advice fees associated with our strategy and product recommendations.

1 1 1 Fee Allocation ($)

Who Pays Description Owner Investment Fee ($)

Change Accountants & Advisors

Count Financial

Macquarie

Issuance Fee

SMSF $300,000

$580 $0 $0 $580

Your SMSF

Brokerage $580 $0 $0 $580

Upfront Investment Fee $9,900 $8,415 $1,485 $0

Total $300,000 $11,060 $8,415 $1,485 $1,160

Investment Fees Explained

Issuance Fee – the greater of 0.20% of the Purchase Price of the Underlying Security and $50.

Brokerage - the greater of 0.20% of the Sale Price of the Underlying Security and $50.

Upfront Investment Fee – an amount of $9,900 will be paid to us from your SMSF. Of this amount, Change Accountant & Advisors will receive 85% and Count will receive the remaining 15%.

Fees are also payable on transfer of an Instalment Receipt or if a direct debit in relation to your Facility is declined. Please see Section 5 of the Equity Lever Combined Product Disclosure Statement and Financial Services Guide dated 1 July 2013 for more information on the fees that apply to an investment in Equity Lever.

Statement of Advice for John & Mary Smith Page 28 of 37

Personal Insurance Commissions - Upfront The table below shows the initial advice fee for the next full year associated with our wealth protection recommendations.

Commission Allocation ($)

Who Pays

Product Name Owner Premium

(pa) Commission

(%) Commission

($)

Change

Accountants &

Advisors

Count

Financial

Life SMSF $2,761 116% $3,203 $2,723 $480 Your SMSF

TPD (Out)

John

$1,196 116% $1,387 $1,179 $208

John Trauma $1,456 116% $1,689 $1,436 $253

Income Protection $2,642 116% $3,065 $2,605 $460

Life SMSF