change amidst uncertainty: how banks are adapting to the emerging regulatory landscape

TRANSCRIPT

Change amidst uncertainty: how banks are adapting to the emerging regulatory landscapeThoughts

Written by the Economist Intelligence Unit

2

Written by the Economist Intelligence Unit

3

The second, related observation is that some bank

leaders may not fully understand the exposure created

by inadequate governance of trading operations within

the new environment. Laws in the United States and

the UK now impose stronger fiduciary and oversight

requirements on a firm’s board members and executives,

requirements that extend to maintaining robust

compliance around all trading operations and banking.

Whether or not their front-office moves are part

of broader corporate strategy, firms can become

exposed to significant fiduciary and reputation risks by

executing new business strategies without adequate

controls, communications strategies and change

management in place. On the up-side, reorganizing

quickly and purposefully, and creating compliance

programs that meet the test of global regulators, can

position banks to increase market share and margin,

both in existing and emerging markets.

We hope the findings of this report help you chart

a course to new opportunities, leveraging solid

governance. Please let me know if you would like to

discuss the results or have any questions.

Capco is pleased to present this

report, which explores how capital

markets firms are dealing with

the dramatic changes that are

underway in the financial services

industry. Based on research

conducted by the Economist

Intelligence Unit in March 2011,

the report provides insight into seven critical questions

regarding banks’ readiness for regulatory reform, which

were the subject of a recent Capco white paper.*

Among the many insights the survey provides, two

are especially noteworthy, and potentially reasons

for caution.

First, it is clear that the traders are driving change.

Trading operations are taking the lead in implementing

business models and processes to operate in the

newly regulated environment. In some cases, they

are quickly executing on geographic strategies, in

jurisdictions where regulations may be more favorable.

In doing so, trading operations appear to be outpacing

their back-office and compliance functions by a

wide margin. In fact, more than half of the trading

operations surveyed could be conducting business

in an environment without the necessary obligations

support – capabilities that simply may not exist in the

local back office yet, or that regulators may not have

even fully defined.

Change amidst uncertainty: how banks are adapting to the emerging regulatory landscape

Sean Culbert

Partner and Co-lead of Finance, Risk and Compliance

* For further discussion of these questions please see the Capco Thoughts white paper, Regulatory Reform: 7 Critical Questions for Financial Services Firms, available on capco.com.

4

About this report

Change amidst uncertainty: how banks are adapting

to the emerging regulatory landscape is a Capco

report, written by the Economist Intelligence Unit.

It examines how, in light of continuing regulatory

uncertainty, financial institutions are reshaping their

capital markets businesses to operate effectively in

the new environment, and focuses particularly on the

likely effect of regulation on overall structure as well

as front, middle and back office operations.

The research is based on three components:

• A survey of 60 senior executives at financial

institutions, half operating in the UK and half in

the US. All firms had annual global revenues of

more than US$5bn and all respondents work in

operations, risk, trading or regulation.

• Interviews with a range of industry participants

and experts, as well as a follow-up qualitative

questioning of survey respondents. Because of

the sensitivity of the topic, interviewees spoke off-

the-record.

• Desk research, including a review of financial

institutions’ regulatory filings.

The author of the report is Geraldine Lambe and the

editor is Monica Woodley.

5

Executive summary

As the scale and intensity of the financial crisis

became clear, industry participants knew that a tough

regulatory response would follow. Those expectations

have now been met. While the final rules remain

uncertain in many areas, a raft of regulatory change is

in process.

The regulations create new capital requirements,

address liquidity and counterparty risk, and push trading

of more products onto exchange and into central

clearing. They put in place new consumer protections

and seek to reduce systemic risk in order to avoid the

need for future government intervention. The cumulative

effect is forcing the financial industry to fundamentally

reassess business models and operating practices.

This assessment is driving significant change in

financial institutions. Banks are already exiting some

businesses and are likely to shrink or exit others as

new capital rules make them less profitable. The

location of new or expanding businesses will be

rethought as firms assess the relative impact of each

jurisdiction’s regulatory constraints. New systems and

processes are being put in place to meet demanding

data capture, data management and stress testing

requirements. Communications with clients and

counterparties are being revamped, and new

reporting lines put in place. Connectivity will have

to be developed and new processes established to

connect to a swathe of new entities that will spring up

in the clearing and settlement space.

In this changing environment, the Economist

Intelligence Unit conducted research, on behalf

of Capco, to find out where banks are in terms of

preparation for new regulations and what impact

these are having on operations. This research

is based on a survey of senior executives at 60

banks, half based in the US and half in the UK,

working in operations, risk, trading or regulation.

The survey results have been supplemented with

in-depth interviews with industry participants and

experts. Because of the sensitivity around this topic,

interviewees preferred to speak off-the-record.

Key findings from the research include:

Banks see more opportunities than threats in

the new regulatory environment. Almost a third of

respondents believe that new regulations will provide

opportunities to take market share as other banks

retrench or rethink their business models. Almost

two-thirds see regulatory change as an opportunity

to transform their business at a systems and process

level. Some see this as a way to gain competitive

edge. However, they are unsure whether the greater

transparency required by regulation will have a

positive or negative impact on competitiveness.

While preparations are well underway, the impact

of regulations on bank structures is unclear.

More than half of respondents say they are at

implementation stage. The US is further behind than

the UK, however, as the industry waits for many

elements of the Dodd-Frank Act to be translated into

regulations. Almost three-quarters have identified

where changes to systems need to be made in order

to handle the new, higher levels of data required. A

similar number say they have a strategy in place to

communicate the impact of regulatory changes to

clients and counterparties.

However, the industry remains uncertain about

how to adapt business entities and operations to

new regulations. More than half of respondents are

keen to retain existing organizational structures and

operating models. However, in 13 out of the 17 areas

of operation covered by the survey, the majority of

respondents do not know if their firms will relocate or

outsource business functions, or create a shared utility.

Boards and senior management believe they

have a good understanding of regulatory impact.

The crisis has been a wake-up call for board

members and senior management. With regulators

and policy-makers taking an increasingly tough line,

boards and executive management will be more

accountable for a firm’s decisions. According to

the majority of respondents, they have risen to this

challenge and have a good understanding of the

implications increased data transparency will have at

their own businesses as well as across the industry.

Once changes to data infrastructure are adopted,

respondents are confident that management will be

able to prove they have better control over information,

as required by regulators.

6

Introduction

In its 10-K regulatory filing to the Securities and

Exchange Commission (SEC) for the fiscal year ending

in March 2011, Goldman Sachs revealed the impact

that US regulations have already had on the bank’s

operations. “In light of the Dodd-Frank Act, during

2010, we liquidated substantially all of the positions

that had been held within Principal Strategies in our

former Equities operating segment, as this was a

proprietary trading business. In addition, during the

first quarter of 2011, we commenced the liquidation of

the positions that had been held by the global macro

proprietary trading desk in our former Fixed Income,

Currency and Commodities operating segment.”

US regulations are shaping European institutions’

strategy too. Deutsche Bank announced in March that

it would deregister its US subsidiary so that it would no

longer be a bank holding company. Deutsche hopes

that by changing the status of Taunus Corp – a part of

which is highly leveraged and under new rules would

need recapitalizing – it will take Taunus out of the

scope of the Dodd-Frank Act and avoid having to raise

billions of dollars in new capital.

Compliance is diverting management, IT and legal

resources from day-to-day operations as IT races to

keep pace with front office transformations. Some

firms have recruited additional expertise in specific

areas. The impact assessment itself is a major

task. The Dodd-Frank Act, for example, is long and

complex at 2,307 pages, 16 titles and 540 sections. It

is expected that regulators will create 243 new rules,

conduct 67 studies and issue 22 periodic reports.

Hundreds of new rules will require consultation

with the industry before they can be implemented.

One bank’s response to the Markets in Financial

Instruments Directive (MiFID) consultation alone takes

up 66 pages. The bank says its legal and compliance

department has doubled in size in the last two years.

So, while much of Dodd-Frank, the Financial Services

Act 2010 and other regulations still need to be

defined, it is clear that banks’ strategy and front

office operations are already moving forward, while

governance and compliance are lagging.

7

Assessment, understanding and implementation

The sales and trading functions of financial services

firms seem to have moved quickly to determine which

regulations are relevant to their businesses, consider

what the regulatory impact will be and even to move

forward with implementing changes based on their

impact assessments. More than half of respondents

to the survey say they are at the implementation

stage. Looking at responses by geography, the UK

is slightly ahead of the US, with 58% compared with

53%, respectively, already implementing changes.

Industry participants say that this is explained by

the fact that there is more still to be defined in US

regulation than there is in Europe, meaning that firms

in Europe have a head start. UK firms are also more

likely than those in the US to align the implementation

of their country’s main regulatory reforms with those

of Basel III and IFRS. (See Figures 1 and 2.)

The UK operations of a European bank are

already advanced in several areas, including those

surrounding internal transfer pricing models. These

are central to complying with the UK’s liquidity

buffers, which were implemented in June 2010, as

well as Basel III’s liquidity coverage ratios. The bank’s

CEO says the bank’s decentralized business model

has given it a head start in such areas.

“We introduced transfer pricing for liquidity risk to all

our branches in June 2009,” he says. “Each branch

has to match-fund itself. The reason we have been

able to move so quickly is because we operate a

devolved model, where each branch is responsible for

setting the appropriate prices for its own market. For

this kind of decentralized pricing model to work, it’s

critical for branches to be charged the correct internal

cost for liquidity, so we already had the processes in

place to enable us to implement this regulation.”

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

32%30%

58%53%

10%

17%

Figure 1. Q1, geographic split. At what stage is your company in preparing for changes required by regulatory reform?

We have identified the regulatory changes relevant to our business

We have assessed how regulatorychanges will impact our business

We have begun implementing changes to our business based on our impact assessments

U.K.U.S.

Figure 1. At what stage is your company in preparing for changes required by regulatory reform?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

68%

50%

23%27%

97%

80%

Figure 2. Q2, geographic split. Have you or do you plan to align the implementation of your country’s main regulatory reform with that

of any of the following regulations? Select all that apply.

IFRS Basel III FACTA

U.K.U.S.

Figure 2. Have you or do you plan to align the implementation of your country’s main regulatory reform with that of any of the following regulations? Select all that apply.

8

Trading is running out in front

According to the survey, by function, trading is way

out in front in terms of preparation, with almost

three-quarters (73%) saying they are already at

implementation stage. Interestingly, the regulatory

function, which may be expected to be most

advanced, is the least prepared. Only 20% say they

are at implementation, although a significant 60%

have completed the impact assessment. (See Figure 3.)

On reflection, it is unsurprising that the trading space

is the most advanced in terms of preparation; they

are already positioning for the higher capital charges

for various products contained in Basel III and for the

proprietary trading ban in the Volker Rule.

“If you look at the changes to the trading book

treatments, they are so substantial that people have

had to think through urgently what is the shape of

the business going forward, because the current

business won’t be profitable,” says the head of

prudential advisory at a consulting firm. “And those

trading book requirements hit much earlier [than

some other changes], so in the trading area it has

become critical to move quickly. The treatment of

counterparty risks in trading books and of bank-to-

bank exposures has gone up three to four times in

total, and the treatment of securitization books has

gone up enormously, so people have already taken

action, moving things out of trading books and into

banking books.”

There are concerns, however, that implementation

may be piecemeal. While many firms have created

working groups or task forces, these are typically

organized at a national level, and therefore do not

address change at a global, enterprise-wide level.

In addition, some have suggested that the amount

of new regulations flooding into the market may lead

banks to focus on the trees but lose sight of the

forest – a criticism which has been leveled at banks,

regulators, ratings agencies and politicians, and

held at least partly to blame for the financial crisis. If

regulators are aware of this danger, the feeling that

the sense of urgency for change is already dissipating

means that they want to press on while there is still a

chance of getting new regulations passed.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

27%

19% 20%

46%

73%67%

20%

46%

0%

14%

60%

8%

TradingRegulation

RiskOperations

Figure 3. Q1, job function splitAt what stage is your company in preparing for

changes required by regulatory reform?

We have identified the regulatory changes relevant to our business

We have assessed how regulatorychanges will impact our business

We have begun implementing changes to our business based on our impact assessments

Figure 3. At what stage is your company in preparing for changes required by regulatory reform?

9

A financial services partner at a consulting firm agrees

that the amount of new regulation is clearly an issue.

“The message from our research is that the sheer

volume of change is proving very challenging for

firms. And it gets more difficult as you move down

from global statements of principal into regional

rule-making, and then further down into national

interpretation. We don’t see many institutions that

have an overarching view of the impact on their firm.

They may well be doing things on a local or regional

level – but they do not have a consolidated view of the

overarching impact.” Given the new uniform fiduciary

standard obligations for advisers and broker dealers,

that could prove problematic for US executives.

Threat or opportunity?

If banks see the challenges posed by regulation, they

also see the opportunity. This is particularly true in

the UK, where almost a third (32%) of respondents

strongly agree that the new regulatory environment

is an opportunity to gain market share. Bankers in

the US, however, are less optimistic, with only 20%

clearly positive about the potential for opportunity.

(See Figure 4.)

At first sight, this looks to be accounted for by the

banning of proprietary trading and constraints on

principal investment – two of the most profitable

areas of investment banking in recent years – that

have been imposed on US banks by way of the

Volker rule. But looking into the survey results by

function reveals that 82% of traders agreed with the

potential to gain market share, and none of them

disagreed. It is the operations and risk functions

which see more danger than promise in the new

regulatory environment. (See Figure 5.)

However, it will not be easy for banks to pick a

winning model – or to make it successful in a

crowded market. “The question is, what is the shape

of the business that will be profitable? And I think

the answer to that is unknown,” says the head of

prudential advisory at a consulting firm. “Moreover,

if multiple banks change their business in the same

way, how many banks can be profitable with the

same type of business? How many banks can be

major flow players, for example?”

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

32%

20%

36%

30%

7%

17%

0%

10%

26%23%

Figure 4. Q3a, Do you agree or disagree with the following statements? We are looking at the new regulatory

environment as an opportunity to gain market share

1 2 3 4 5Strongly agree Strongly disagree

U.K.U.S.

Figure 4. Do you agree or disagree with the following statements? We are looking at the new regulatory environment as an opportunity to gain market share.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

21%

33%

18%

40%

17%

10%

64%

40% 42%

33%

18%20%

8%

24%

13%

0%0% 0%0%0%

TradingRegulation

RiskOperations

Figure 5. Q3a, functional splitDo you agree or disagree with the following statements?

We are looking at the new regulatory environment as an opportunity to gain market share

1 2 3 4 5Strongly agree Strongly disagree

Figure 5. Do you agree or disagree with the following statements? We are looking at the new regulatory environment as an opportunity to gain market share.

10

There is also a worry that the changes in Basel III

are so big, if any provision unwittingly creates an

unlevel playing field it could proffer huge advantages

to certain players. Unequal treatment in just a single

area of Basel III could have far-reaching effects.

“For example, there has been a worry that the

treatment of deferred tax assets (DTAs) might be more

beneficial for US banks than for European banks and,

depending on how it’s implemented, that would have a

number of consequences. Firstly, it would immediately

make their capital levels higher and their costs lower.

Secondly, it would make it easier for an American

bank to buy a bank in difficulty than for a European

bank; banks in difficulty have hitherto been bought on

the basis of the benefits of the DTAs, because some

of that tax can be clawed back. Seemingly small

inequalities could have large ripple effects.”

New regulations as an opportunity for transformation

Part of the optimism surrounding the chance to

win market share or gain some form of competitive

advantage is tied to the potential of new regulations

to have a transformative effect on the business. This

has clearly been picked up by survey respondents,

with more than half (57%) agreeing with this proposal

and the UK, again, markedly more optimistic than the

US. (See Figure 6.)

However, more than half (54%) of respondents were

keen to maintain their current operation models and

structures. But this is not as counterintuitive as it may

seem, as it relates to where bankers see the greatest

opportunity for transformation – and this is in systems

and processes rather than at the organizational level.

“Banks have grown as groups of discrete business

silos, with each silo capturing data, interrogating

data and leveraging that data,” says the head of

IT at a large European bank operating in London.

“The industry may have gone a long way towards

achieving overall efficiency, but we have never

achieved information efficiency. New regulations –

while onerous and costly – offer us an opportunity

to take a fresh look at how we manage these and

other processes, and to retool operations in a way

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

26%23%

29%

17%

7%

20%

0%

13%

39%

27%

Figure 6. Q3b, geographic splitDo you agree or disagree with the following statements?

Scale of 1 to 5. We are looking at the new regulatory environment as an opportunity to transform our business model/structure

1 2 3 4 5Strongly agree Strongly disagree

U.K.U.S.

Figure 6. Do you agree or disagree with the following statements? Scale of 1 to 5.

We are looking at the new regulatory environment as an opportunity to transform our business model/structure.

11

that benefits the group, rather than how it suits the

individual business. If we can break down silos, there

are clearly opportunities to generate competitive

advantage from that.

“There is an element of ‘pre-crisis’, and ‘post-crisis’

thinking here, with new regulations as the catalyst

for change,” he adds. “Historically, the cost-benefit

of streamlining systems and processes relative to

the cost of doing nothing meant it was not worth the

hassle or the tax cost. Going forward, that cost-

benefit may change. Living Wills or other resolution

mechanisms, for example, will force banks to think

through a more streamlined structure, and this is

helpful in the new Basel III world.”

Will transparency help or hurt bank competitiveness?

A common motif of the emerging regulatory

environment is the aim of shedding new light on every

area of banks and financial markets. For example,

Dodd-Frank aims for greater transparency into risk

exposure across the financial system, and several

key components of the law require financial services

institutions to collect and report on risk exposure

in their business. The Financial Stability Oversight

Council, in its role as systemic risk monitor, will

collect risk data from various sources including

federal and state financial regulatory agencies and

the newly created Office of Financial Research (OFR);

among other things, the OFR will be responsible for

collecting data from financial services companies.

Similarly, the UK’s Financial Services Act and Basel

III both impose a high degree of transparency on key

metrics, including bank capital, liquidity, collateral and

counterparty risk, requiring such data to be reported

to bank boards and regulators. The European Market

Infrastructure Regulation, meanwhile, will try to bring

transparency to the over-the-counter markets and

impose data reporting requirements for transactions

to new trade repositories. A central plank of the

review into the Markets in Financial Instruments

Directive, currently underway, is to increase

transparency in post-trade reporting.

12

Banks are uncertain about the effect of these

transparency requirements on their competitiveness,

although some have expressed concern that

sensitive data about capital, liquidity and exposures

could easily leak out into the marketplace. Although

some of the regulations specifically aim to increase

transparency in the trading arena, the trading function

is the least concerned about the impact. (See Figure 7.)

From data deficit to information advantage?

All new regulations mandate significant additional

data and reporting requirements. These present

collection, integration and management challenges

for banks’ information architecture.

Basel III, for example, aims to eliminate the kind of

regulatory arbitrage where a bank moves assets from

the banking book into the trading book in order to get

better capital treatment. It therefore requires banks to

consolidate positions from all of their trading desks

and to make their trading book compatible with their

banking book. This requires data to be both accurate

and clean, and will be a challenge for any US banks

which have not been applying Basel rules up to now.

To meet the UK’s liquidity rules, banks will be required

to identify, measure, monitor and stress test liquidity

risk in a much more detailed way, and to process and

deliver the data to the Financial Services Authority

(FSA) on a regular basis.

Basel III also requires a unified view of counterparties

and counterparty credit risk, and the capacity to

measure and process the data. In addition, the move

to centralized collateral management, as well as the

introduction of the net stable funding ratio and the

liquidity coverage ratio, will require new data models.

To fulfill many of the requirements, banks need to

collect more detailed information from the trading

partners and their clients. Respondents to the

survey highlighted several areas where they needed

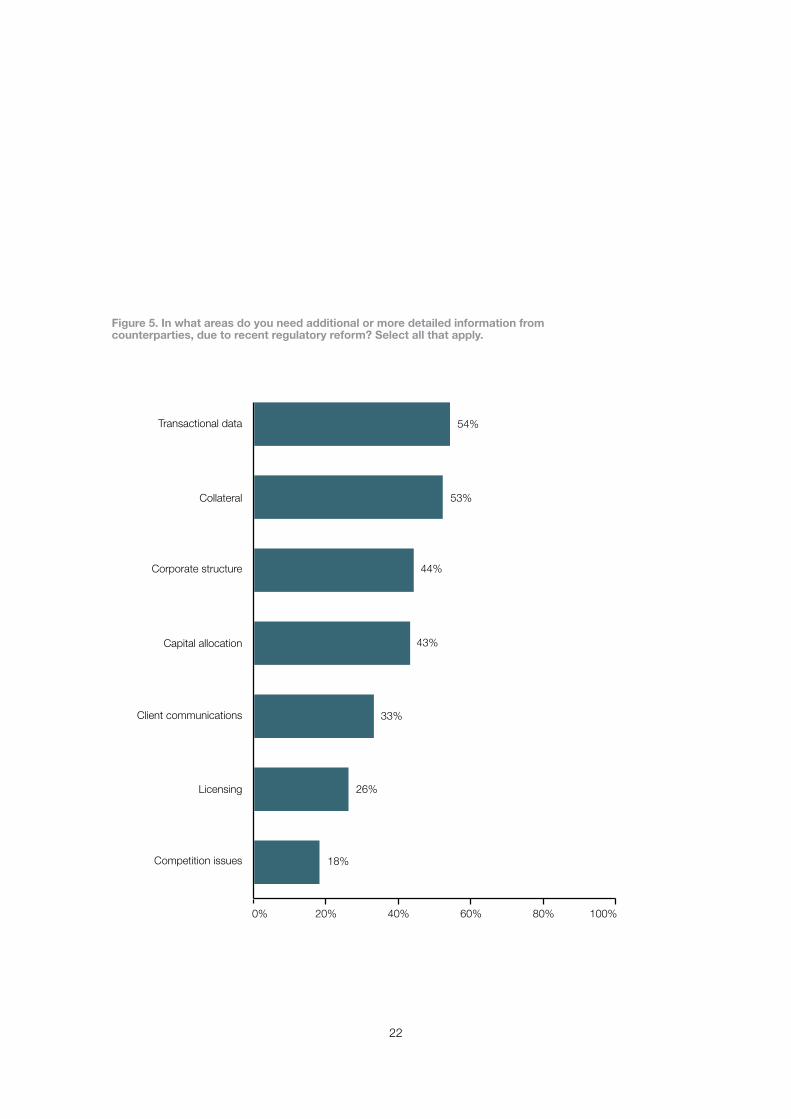

additional data from counterparties, led by collateral

and transaction data. By function, there were some

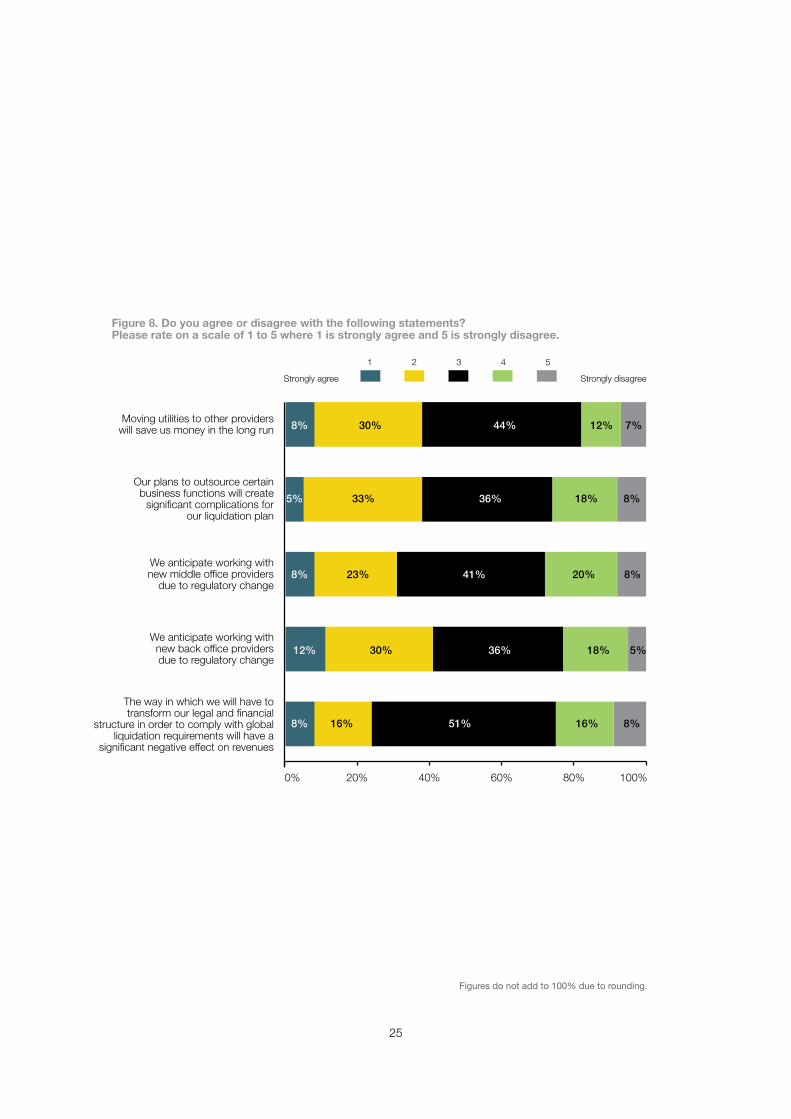

noticeable spikes in data requirements. (See Figures 8

and 9 on page 13.)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

8%10%

0%

20%

25%24%

27%

0%

38%

24%

18%

40%

25%

38%

4%

46%

20%

5%9%

20%

TradingRegulation

RiskOperations

Figure 7. Q10d, functional splitDo you agree or disagree with the following statements?

Rate 1 to 5. We are concerned that the increased transparency required by new regulations will be a threat to our competitiveness

1 2 3 4 5Strongly agree Strongly disagree

Figure 7. Do you agree or disagree with the following statements? Rate 1 to 5.

We are concerned that the increased transparency required by new regulations will be a threat to our competitiveness.

13

For some banks, data projects are about creating

value as well as compliance. “We identified information

architecture as the lynchpin in meeting new regulations

early on, so we are quite a long way down the road in

terms of where we need to be in order to change our

information systems,” says the head of IT at a large

US bank. “Because we also identified that this is an

area where we could create value for the business, we

prioritized this over some other IT projects.”

There is a high cost associated with meeting new

requirements, however. “There is a huge impact on

data systems across multiple product and business

lines,” says the head of compliance at a large

European bank operating in London. “Estimates

suggest that it will cost large banks around $100m

each to put the systems and processes in place to

comply with Basel III. We will have to find ways of

calculating the newly introduced net stable funding

ratio and the liquidity coverage ratio, and have the

capability to stress test our calculations and report

to our board and to regulators. Because the Basel

Senior Supervisors Group favors a standardized

centralized risk data set – the so-called single source

of truth – on the IT side, this means banks will have

to integrate data sources and adopt new data

modeling techniques.”

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

48%

42%

36%33%

17%20%

60%

43%

64%

54%

62%

46%

100%

33%

10%9%

0%

21%

62%

55%

40% 42%

33%

20%18%

42%

60%

36%

Figure 16. Q6, “don’t know list”Due to regulatory change, which business functions do you anticipate

having to relocate or outsource, partly or completely?

Col

late

ral

Lice

nsin

g

Cor

pora

te

stru

ctur

e

Tran

sact

iona

l da

ta

Com

petit

ion

issue

s

Cap

ital

allo

catio

n

TradingRegulation

RiskOperations

Clie

nt

com

mun

icat

ions

Figure 9. In what areas do you need additional or more detailed information from counterparties, due to recent regulatory reform?

Figure 8. In what areas do you need additional or more detailed information from counterparties, due to recent regulatory reform?

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

53%54%

26%

18%

33%

43%44%

Figure 8. Q5, overallIn what areas do you need additional or more detailed

information from counterparties, due to recent regulatory reform?

Tran

sact

iona

lda

taC

olla

tera

lC

orpo

rate

stru

ctur

e

Cap

ital

allo

catio

n

Clie

nt

com

mun

icat

ions

Lice

nsin

gC

ompe

titio

niss

ues

14

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

38%36%

2%

8%

16%

Figure 10. Q10a, overallDo you agree or disagree with the following statements?

Scale 1-5. We have a company-wide strategy for identifying the systems that will require modification/upgrade to handle the

new, higher levels required by new regulation.

1 2 3 4 5Strongly agree Strongly disagree

Figure 10. Do you agree or disagree with the following statements? Scale 1-5.

We have a company-wide strategy for identifying the systems that will require modification/upgrade to handle the new, higher levels required by new regulation.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

38%33%

46%

20%25%

52%

46%

0%

25%20%

5%

60%

8%10%

4%9%

0%0% 0%0%

TradingRegulation

RiskOperations

Figure 7. Q10d, functional splitDo you agree or disagree with the following statements?

Rate 1 to 5. We are concerned that the increased transparency required by new regulations will be a threat to our competitiveness

1 2 3 4 5Strongly agree Strongly disagree

Figure 11. Do you agree or disagree with the following statements? Scale 1-5.

We have a company-wide strategy for identifying the systems that will require modification/upgrade to handle the new, higher levels required by new regulation.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

44%

28%

2%

10%

16%

Figure 12. Q10b, overallDo you agree or disagree with the following statements? Scale 1-5.

We have a company-wide strategy for identifying the systems that will require modification/upgrade to handle the new, higher levels required by new regulation

1 2 3 4 5Strongly agree Strongly disagree

Figure 12. Do you agree or disagree with the following statements? Scale 1-5.

We have already identified the systems that will require modification/upgrade to handle the new, higher levels of data required by new regulation.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

25%

36%33%

54%

38%36%

0%4%

40%

19%18%

60%

13% 10%

4%9%

0%0% 0%0%

TradingRegulation

RiskOperations

Figure 13. Q10b, functionalDo you agree or disagree with the following statements?

Scale 1 to 5. We have already identified the systems that will require modification/upgrade to handle the new,

higher levels of data required by new regulation

1 2 3 4 5Strongly agree Strongly disagree

Figure 13. Do you agree or disagree with the following statements? Scale 1 to 5.

We have already identified the systems that will require modification/upgrade to handle the new, higher levels of data required by new regulation.

15

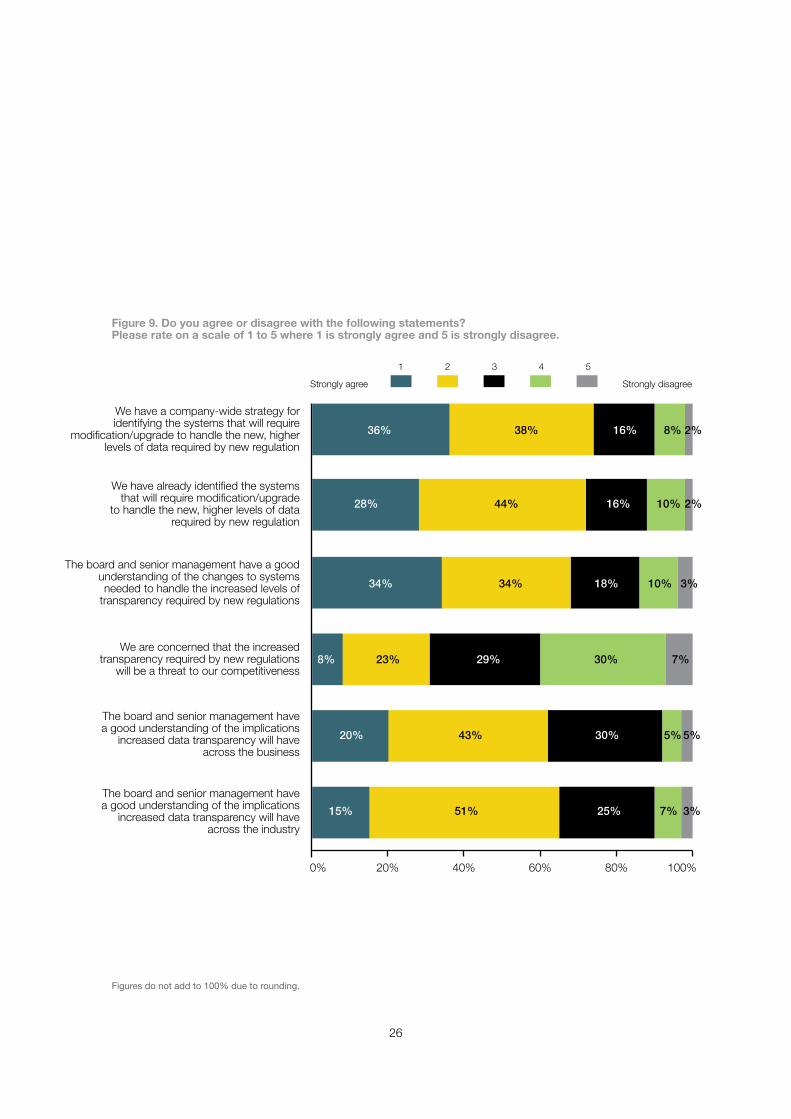

Banks are acutely aware of new data requirements

The survey revealed that almost three-quarters of

banks have a strategy in place in order to identify

where changes to systems need to be made, or

have already identified the systems which will need

modification. Three of the four business functions

surveyed are well advanced in terms of preparation,

led by operations, with only the regulatory function

lagging. (See Figures 10 through 13 on page 14.)

Banks have a strategy for communicating the impact

of regulatory changes to clients and counterparties.

About three-quarters (74%) agree or strongly agree

that they have a strategy to communicate changes to

clients and counterparties.

Most banks are confident that once they have adopted

planned changes to their data infrastructure, their

management will be able to prove they have better

control of information, as required by regulators.

However, UK banks are much more confident than

their US counterparts. (See Figure 14 and 15.)

The shape of things to come

Some banks have already taken steps to refine the

shape of their organizations to minimize the impact

of regulations. In February, for example, the UK’s

Barclays disclosed that in November 2010 it had

deregistered its US bank-holding company. The bank

said this was to better align the business with the

appropriate capital regimes; in doing so, the bank

avoided having to inject as much as $12bn to make

up a capital shortfall in the US.

As a result of the change, Barclays folded a credit-

card operation into a new US entity that is a direct

subsidiary of the British parent company. The

credit-card bank is regulated by the Federal Deposit

Insurance Corporation and needs no additional

injection of capital. Before the move, Barclays

Capital, the group’s investment bank, was held within

Barclays Group US Inc., which was subject to federal

capital requirements. It will now be subject to SEC

regulation instead.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

36%

30%

7%8%

20%

Figure 14.Q3d, overallDo you agree or disagree with the following statements? Please rate on a scale of 1 to 5. Once we have adopted changes to our data infrastructure, management will be able to

prove they have better control of information, as required by regulators

1 2 3 4 5Strongly agree Strongly disagree

Figure 14. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5.

Once we have adopted changes to our data infrastructure, management will be able to prove they have better control of information, as required by regulators.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

39%

20%

10%

30%

3%

13%

3%

10%

45%

27%

Figure 15. Q3d, geographicDo you agree or disagree with the following statements?

Please rate on a scale of 1 to 5. Once we have adopted changes to our data infrastructure, management will be able to prove they have better

control of information, as required by regulators

1 2 3 4 5Strongly agree Strongly disagree

U.K.U.S.

Figure 15. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5.

Once we have adopted changes to our data infrastructure, management will be able to prove they have better control of information, as required by regulators.

16

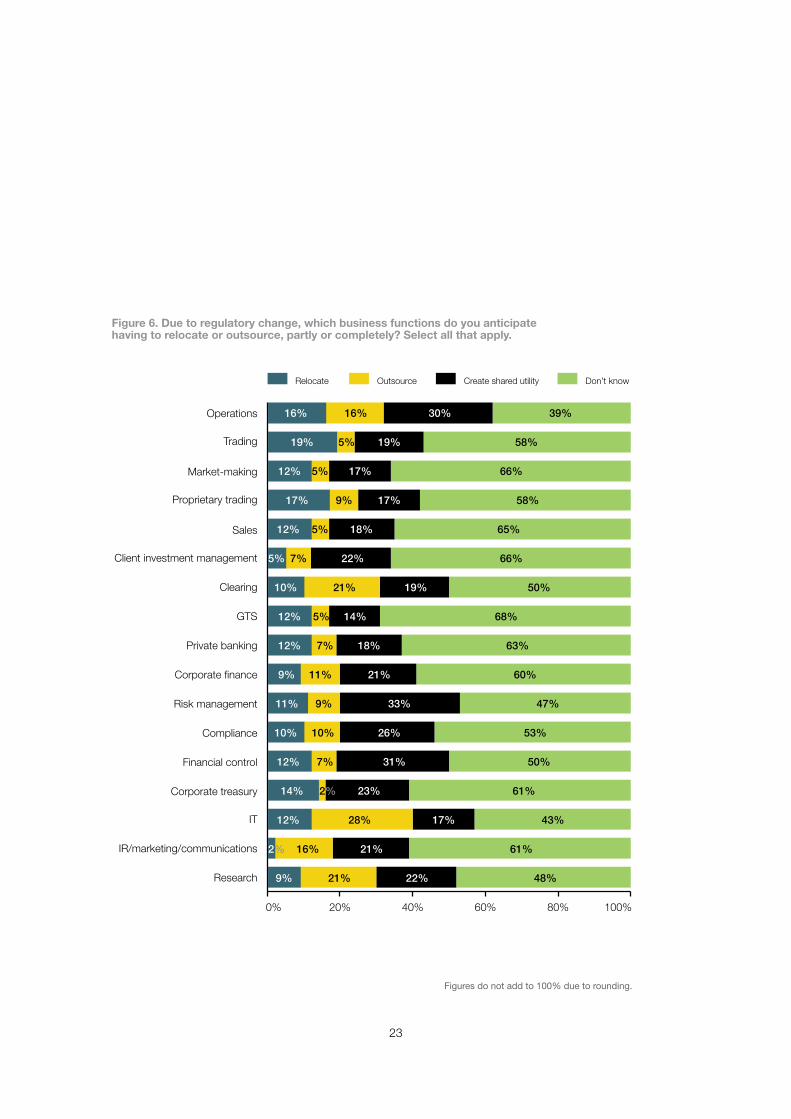

While the restructuring of Barclays and other banks

suggest that senior management is swiftly taking steps

to reshape business entities, survey respondents across

most areas of business were undecided about whether

new regulations would lead firms to relocate or outsource

any business functions, or create a shared utility. In 13

of the 17 areas of operation, the majority of respondents

said they did not know what the impact of regulation

would be on organizational structure. (See Figure 16.)

However, over a third (36%) of UK and almost half

(47%) of US respondents agreed or strongly agreed

that they anticipate working with new back office

providers due to regulatory change, compared to about

a quarter of UK and over a third of US respondents who

anticipate working with a new middle office provider.

There are four areas (operations, risk management,

financial control and IT) where new strategies are

clearly being contemplated. In operations, more than

a quarter (26%) of US respondents and a third of

UK respondents said they anticipated the creation

of shared utilities. Operations professionals were

even more enthusiastic, with almost 48% suggesting

this was a possible route. Similarly, the creation of

a shared utility was seen as a likely choice for risk

management, with a third of all respondents and 43%

of risk professionals suggesting this option.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

60%61%61%63%65%66%66%68%

50% 50% 48% 47%43%

39%

53%58%58%

Figure 16. Q6, “don’t know list”Due to regulatory change, which business functions do you anticipate

having to relocate or outsource, partly or completely?

GTS

Mar

ket-m

akin

gC

lient

inve

stm

ent

man

agem

ent

Sale

sPr

ivate

ban

king

Cor

pora

te tr

easu

ryIR

/mar

ketin

g/

com

mun

icat

ions

Cor

pora

te

finan

cePr

oprie

tary

trad

ing

Trad

ing

Com

plia

nce

Cle

arin

gFi

nanc

ial c

ontro

lRe

sear

chRi

sk m

anag

emen

t

ITO

pera

tions

Figure 16. Due to regulatory change, which business functions do you anticipate having to relocate or outsource, partly or completely?

17

By function, traders see the greatest potential for

regulations to shape operations strategy: 40% of

traders thought new regulations would lead to trading

operations being relocated; 30% thought that market-

making and prop trading will be relocated; 40%

thought that a shared utility may be created for client

investment management; and a third thought that IT

may be outsourced.

Shared services such as regional data centers are

already common practice at many global financial

institutions, particularly at retail banks, which rely heavily

on gathering, processing and analyzing customer

information in order to tailor services. The CEO of the

EMEA consumer division of a major US bank says

shared services offer big advantages for bank and

customer. But he notes that there are already forces in

play which may put pressure on this business model.

“Customers execute business with us through

applications hosted in our data centers. One

example is the fraud analysis we do on credit cards.

Another is the risk analysis we perform under the

new requirements of various jurisdictions. Using

regional data centers is an advantage for several

reasons. The facilities are state of the art, present

a closed circuit and have no major single points of

failure within the core infrastructure. Our data centers

enhance the bank’s risk management, allowing us

to mitigate or accept risks based on a composite

impact analysis rather than through isolated and

market-specific analyses. Such centers allow us to

maintain consistent processes across regions. We

have an ‘end-to-end’ view of the data, which improves

the quality and timeliness of services provided. It

also allows us to better comply with legal/regulatory

requirements. Several jurisdictions are looking to

require local data processing, however. The intentions

are understandable, but as outlined above, would

undermine several of the same public policy goals.”

The impact of resolution regimes on structures

The push towards bank resolution regimes, or Living

Wills, will also have a material impact on strategies

in this area because the patchwork nature of many

banking groups do not lend themselves to drawing

clean lines between businesses.

Global banks are complex entities that have typically

evolved to satisfy a variety of drivers from growth,

to cost cutting, to tax benefits. Often, they do not

develop as standalone entities but share functions

with other parts of the group. Business done in

one country may be transferred somewhere else

for management. Likewise, income generated in

one location may be paid away somewhere else.

The result is sprawling global institutions, often

comprising hundreds of different entities, vehicles

and participations, which have been made more

efficient through the use of cross-agreements for the

provision of services, people and funding.

Up to now, banks have been indifferent to how these

structures looked. But in the world of Living Wills and

resolution regimes, if a crisis means a bank must ring-

fence a particular business, write it down or sell it, the

parent needs to know exactly how it interrelates with

all the other parts of the jigsaw. Regulators will want

reassurance that, if firms have transferred positions

from one jurisdiction to another, there is enough capital

and risk management capacity to contain the risks in

the transferred positions. If the business has paid away

income, regulators will ask how that affects profitability

and risk management of the entity that is paying

away. Untangling this spaghetti to create an enterprise

map will prove extremely difficult for some. And the

existence of shared services may make it more difficult.

“The detail is challenging,” says the head of prudential

advisory at a consulting firm. “Banks have to ask

themselves if a business could be broken up and sold

off, and what they would do about critical elements

that they would have to pass on to someone else?

Is it standalone or is it dependent on other parts of

the organization? If it’s not standalone, what needs

to be done to make it saleable as a standalone

operation? Could they provide the right information

to the authorities so that they can maintain critical

functions such as current accounts? All of this is

actually extremely difficult to achieve. In that sense,

shared services could become an obstacle to a viable

resolution plan. If you wanted to sell a business that is

dependent on a shared service, how standalone is it?

Can someone else buy it, or does the shared service

affect the viability of the business?”

18

Conclusion

As financial institutions operating in the US and UK

continue to ask themselves questions such as these,

attempting to determine how best to reshape their

businesses in light of new regulatory requirements, they

also await clarification from regulators on both sides

of the pond. The interim report of the Independent

Banking Commission in the UK was released mid-

April, but the final report is not out until September.

However, the recommendations of the Commission,

such as ring-fencing retail operations and improving

capital buffers, are just that – recommendations, which

must be accepted by the government and implemented

before banks have absolute clarity on the detail of new

regulation. In the US, the SEC and other regulators are

working towards a July deadline for implementation of

Dodd-Frank but already there is talk of a delay of up

to 18 months for some parts of the Act. These delays

may give gives banks more opportunity to work with

regulators to find solutions that make the financial

system safer while maintaining competitiveness –

or they may just drag out the uncertainty.

19

0% 20% 40% 60% 80% 100%

89%

59%

25%

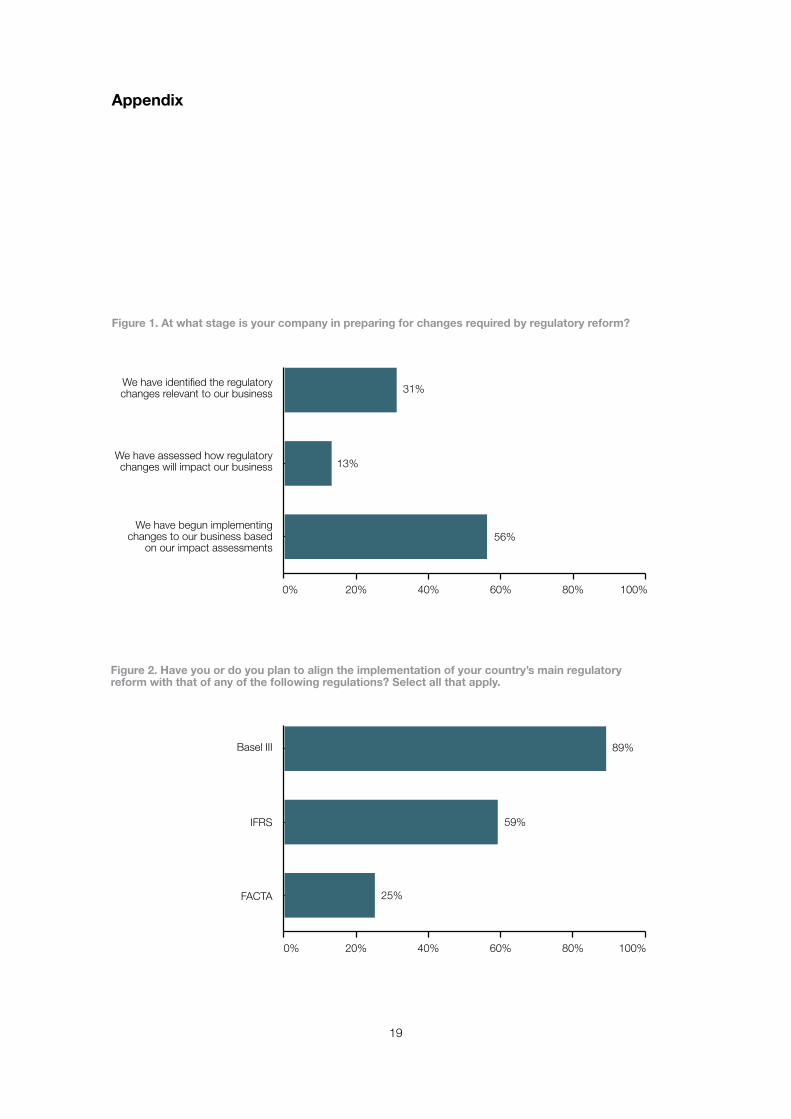

Figure Q2. Have you or do you plan to align the implementation of your country’s main regulatory reform with that of any of the following regulations? Select all that apply

Basel III

IFRS

FACTA

0% 20% 40% 60% 80% 100%

31%

13%

56%

Figure A-1. At what stage is your company in preparing for changes required by regulatory reform?

We have identified the regulatorychanges relevant to our business

We have assessed how regulatory changes will impact our business

We have begun implementing changes to our business based

on our impact assessments

Figure 1. At what stage is your company in preparing for changes required by regulatory reform?

Figure 2. Have you or do you plan to align the implementation of your country’s main regulatory reform with that of any of the following regulations? Select all that apply.

Appendix

20

0% 20% 40% 60% 80% 100%

25% 33% 11% 5%26%

23% 13% 7%33%25%

18% 23% 5%43%11%

20% 8% 7%36%30%

15% 7% 5%43%31%

Figure Q3. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

*Figures do not add to 100% due to rounding.

We are looking at the newregulatoryenvironment

as an opportunityto gain market share

We are looking at the newregulatory environment as an

opportunity to transformour business model/structure

We aim to maintain our currentoperational model/structure as much

as possible, only making changeswhere explicitly required by new regulation

Once we have adopted changes to ourdata infrastructure, management will be

able to prove they have better controlof information, as required by regulators

We have a strategy for communicatingthe impact of regulatory changes to

our clients and counterparties

Strongly agree

1 2 3 4 5

Strongly disagree

Figure 3. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

Figures do not add to 100% due to rounding.

21

0% 20% 40% 60% 80% 100%

80%

39%

38%

23%

23%

Figure Q4. In what areas do you need additional or more detailed information from clients, due to recent regulatory reform? Select all that apply.

Risk tolerance

Areas willing to invest in/areas to avoid

Willingness to lend securities

Demographic information

Household/individualbalance sheet

Figure 4. In what areas do you need additional or more detailed information from clients, due to recent regulatory reform? Select all that apply.

22

0% 20% 40% 60% 80% 100%

44%

53%

54%

43%

33%

26%

18%

Figure Q5. In what areas do you need additional or more detailed information from clients, due to recent regulatory reform? Select all that apply.

Transactional data

Collateral

Corporate structure

Capital allocation

Client communications

Licensing

Competition issues

Figure 5. In what areas do you need additional or more detailed information from counterparties, due to recent regulatory reform? Select all that apply.

23

0% 20% 40% 60% 80% 100%

30% 39%16%16%

19% 58%5%19%

17% 66%5%12%

17% 58%9%17%

18% 65%5%12%

22% 66%7%5%

19% 50%21%10%

14% 68%5%12%

18% 63%7%12%

21% 60%11%9%

33% 47%9%11%

26% 53%10%10%

31% 50%7%12%

23% 61%2%14%

17% 43%28%12%

21% 61%16%2%

22% 48%21%9%

Figure Q6. Due to regulatory change, which business functions do you anticipate having to relocate or outsource, partly or completely? Select all that apply.

*Figures do not add to 100% due to rounding.

Operations

Trading

Market-making

Proprietary trading

Sales

Client investment management

Clearing

GTS

Private banking

Corporate finance

Risk management

Compliance

Financial control

Corporate treasury

IT

IR/marketing/communications

Research

Relocate Outsource Create shared utility Don’t know

Figure 6. Due to regulatory change, which business functions do you anticipate having to relocate or outsource, partly or completely? Select all that apply.

Figures do not add to 100% due to rounding.

24

0% 20% 40% 60% 80% 100%

33%

33%

34%

33%

31%

25%

18%

Figure Q7. What impact will relocation and/or outsourcing decisions have on attracting and retaining talent? Select all that apply.

The ability to hire qualifiedstaff is a top criterion whenselecting where to relocatespecific business funtions

We are confident that our outsourcing arrangements

will help us retain staff

We are concerned thatwe are likely to lose staff

due to outsourcing

We are concerned that we are likely to lose staff

due to relocation

We are concerned that we will have difficulty hiring qualified

staff in the areas we are considering for relocation

We are confident thatour relocation arrangements

will help us retain staff

We have a retention strategy to lock in key staff when

outsourcing, relocating or creating a shared utility

Figure 7. What impact will relocation and/or outsourcing decisions have on attracting and retaining talent? Select all that apply.

25

0% 20% 40% 60% 80% 100%

30% 44% 12% 7%8%

36% 18% 8%33%5%

41% 20% 8%23%8%

36% 18% 5%30%12%

51% 16% 8%16%8%

Figure Q8. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

Moving utilities to other providers will save us money in the long run

Our plans to outsource certain business functions will create

significant complications for our liquidation plan

We anticipate working with new middle office providers

due to regulatory change

We anticipate working with new back office providers due to regulatory change

The way in which we will have to transform our legal and financial

structure in order to comply with global liquidation requirements will have a

significant negative effect on revenues

Strongly agree

1 2 3 4 5

Strongly disagree

Figure 8. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

Figures do not add to 100% due to rounding.

26

0% 20% 40% 60% 80% 100%

44% 16% 10% 2%28%

38% 16% 8% 2%36%

18% 10% 3%34%34%

29% 30% 7%23%8%

30% 5% 5%43%20%

25% 7% 3%51%15%

Figure Q9. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

*Figures do not add to 100% due to rounding.

We have already identified the systems that will require modification/upgrade

to handle the new, higher levels of data required by new regulation

We have a company-wide strategy for identifying the systems that will require

modification/upgrade to handle the new, higher levels of data required by new regulation

The board and senior management have a good understanding of the changes to systems needed to handle the increased levels of

transparency required by new regulations

We are concerned that the increased transparency required by new regulations

will be a threat to our competitiveness

The board and senior management have a good understanding of the implications

increased data transparency will have across the business

The board and senior management have a good understanding of the implications

increased data transparency will have across the industry

Strongly agree

1 2 3 4 5

Strongly disagree

Figure 9. Do you agree or disagree with the following statements? Please rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

Figures do not add to 100% due to rounding.

About CapcoCapco, a global business and technology consultancy dedicated solely to the financial services

industry. We work in this sector only. We recognize and understand the opportunities and the

challenges our clients face. We apply focus, insight and determination to consulting, technology

and transformation. We overcome complexity. We remove obstacles. We help our clients realize

their potential for increasing success. The value we create, the insights we contribute and

the skills of our people mean we are more than consultants. We are a true participant

in the industry. Together with our clients we are forming the future of finance. We serve

our clients from offices in leading financial centers across North America and Europe.

Worldwide officesAmsterdam • Antwerp • Bangalore • Chicago • Frankfurt • Geneva • Johannesburg

London • New York • Paris • San Francisco • Toronto • Washington DC • Zürich

To learn more, contact us at +1 212 284 8600 (+44 20 7426 1500

from outside the United States or Canada), or visit our website at CAPCO.COM

© 2011 The Capital Market Company NV. All rights reserved. T1054A-01-GL/A4