chapter 16 auditing operations and completing the audit mcgraw-hill/irwincopyright © 2014 by the...

TRANSCRIPT

Chapter 16

Auditing Operations and Completing the Audit

McGraw-Hill/Irwin Copyright © 2014 by The McGraw-Hill Companies, Inc. All rights reserved.

Auditing OperationsAuditing Operations

Corporate earnings are considered as an extremely important indicator of health and well-being of corporations

Measurement of income is generally regarded as the single most important function of accounting

16-2

Objectives for audit of revenue and Objectives for audit of revenue and expensesexpenses

1. Use the understanding of the client and its environment to consider inherent risks, including fraud risks, related to revenues and expenses.

2. Consider internal control over revenues and expenses.

3. Assess the risks of material misstatement of revenues and expenses and design further audit procedures that:

a. Establish the occurrence of recorded revenue and expense transactions.

b. Determine the completeness of recorded revenue and expense transactions.

c. Establish the accuracy of revenue and expense transactions.

d. Verify the cutoff of revenue and expense transactions.

e. Determine that the presentation and disclosure of revenue and expense accounts are appropriate, including the proper classification of amounts and the proper presentation of earnings-per-share data.

16-3

Audit of Statement of Cash FlowsAudit of Statement of Cash Flows

Amounts are audited in conjunction with the audit of balance sheet and income statement accounts

Presentation and disclosure important audit objective is important Operating Investing Financing

16-4

Audit Procedures Completed Audit Procedures Completed Near the End of Field WorkNear the End of Field Work

Search for unrecorded liabilities Review the minutes of meetings Perform final analytical procedures Perform procedures to identify loss

contingencies Perform the review for subsequent

events Obtain the representation letter

16-5

Loss ContingenciesLoss Contingencies

Loss contingencies should be reflected in the financial statement amounts when:

It is probable that a loss had been sustained before the balance sheet date

The amount of the loss can be reasonably estimated

Loss contingencies should be disclosed in the notes to the financial statements when it is at least reasonably possible that a loss has been sustained

Loss contingencies need not be disclosed when the possibility of loss is remote

16-6

LitigationLitigation

Most common loss contingency – pending or threatened litigation Letter of inquiry to client’s legal counsel

• Evidence of pending and threatened litigation• Unasserted claims - need to be disclosed if

probable and reasonably possible SAS 12

• Auditors should obtain from management a list describing and evaluating threatened or pending litigation

16-7

Other ContingenciesOther Contingencies

Income tax disputes Accommodation endorsements and other

guarantees of indebtedness Accounts receivable sold or assigned with

recourse Environmental issues Commitments General risk contingencies

16-8

Audit Procedures for Loss ContingenciesAudit Procedures for Loss Contingencies

1. Review the minutes of directors’ meetings to the date of completion of fieldwork.

2. Send letter of inquiry to client’s lawyer

3. Send confirmation letters to financial institutions to request information on contingent liabilities of the company.

4. Review correspondence with financial institutions for evidence of accommodation endorsements, guarantees of indebtedness, or sales or assignments of accounts receivable.

5. Review reports and correspondence from regulatory agencies to identify potential assessments or fines.

6. Obtain a representation letter from the client indicating that all liabilities known to officers are recorded or disclosed.

16-9

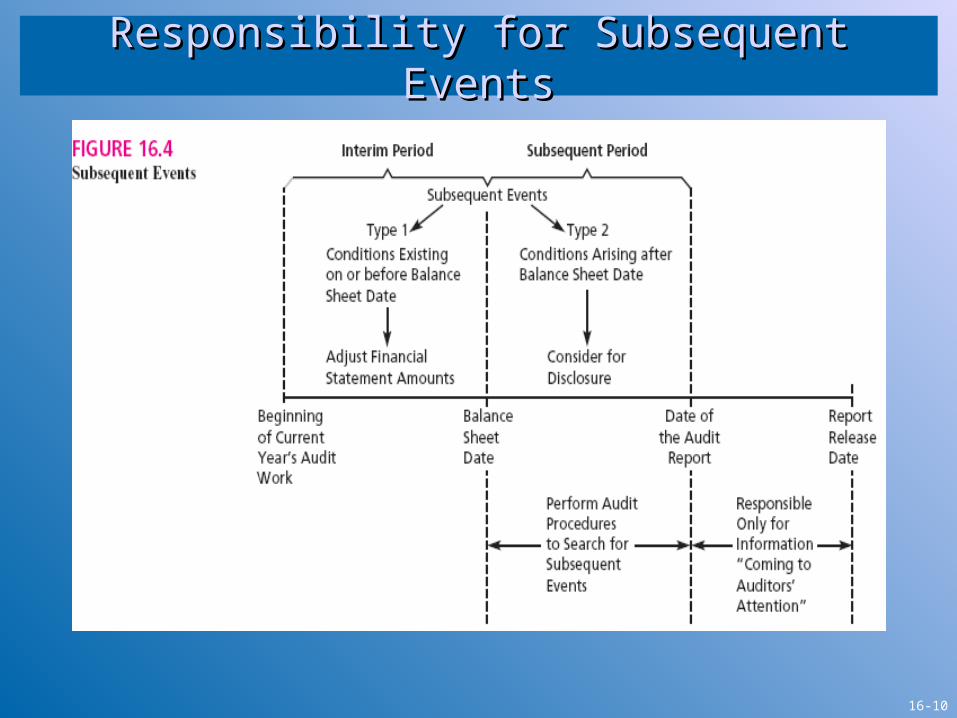

Responsibility for Subsequent EventsResponsibility for Subsequent Events

16-10

Procedures to Identify Subsequent EventsProcedures to Identify Subsequent Events

Review latest available financial statements and minutes of the board and selected committees

Inquiry about matters dealt with at meetings for which minutes are not available

Inquiry of management Obtain lawyer’s letter Obtain representations from management

16-11

Obtain Representation LetterObtain Representation Letter

Purpose is to have the client’s principal officers acknowledge that they are primarily responsible for the fairness of the financial statements

Dated as of the date of the audit report Not a substitute for application of

necessary audit procedures

16-12

MisstatementsMisstatements

Known misstatements Specific misstatements identified during the

course of the audit Likely misstatements

Due to extrapolation from audit evidence or differences in accounting estimates

Evaluation Material misstatements must be corrected

• Quantitative and qualitative factors

16-13

Review the EngagementReview the Engagement

Review of work of audit staff accomplished through review of audit working papers

Typically performed by seniors Review of working papers not completed until

near (of after) completion of fieldwork Partner and manager devote attention to

accounts with higher risk of material misstatement

Second partner review prior to issuance of audit report

16-14

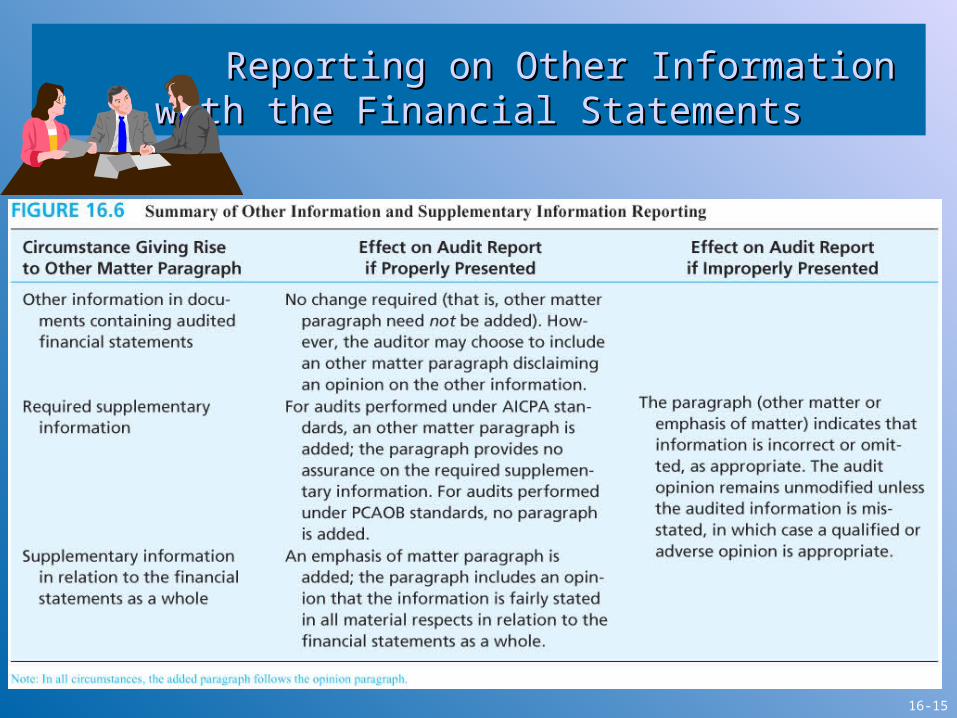

Reporting on Other Information with the Reporting on Other Information with the Financial StatementsFinancial Statements

16-15

Required Communication with Required Communication with Those Charged with GovernanceThose Charged with Governance

Auditor responsibility under generally accepted auditing standards (e.g., to form and express an opinion, and management’s responsibilities)

An overview of the planned scope and timing of the audit

Significant findings from the audit Qualitative aspects of accounting practices Audit difficulties encountered Uncorrected misstatements Disagreements with management Management consultations with other accountants Auditor independence issues Other issues.

16-16

Post-Audit ResponsibilitiesPost-Audit Responsibilities

Auditor subsequent discovery of facts existing at date of report Advise client to make appropriate disclosure

of the facts to anyone actually or likely to be relying upon the audit report and financial statements

If client refuses to make disclosure, CPA should inform each member of board and notify regulatory agencies

16-17

Subsequent Discovery of Subsequent Discovery of Omitted Audit ProceduresOmitted Audit Procedures

Discovered during peer review or other subsequent review of working papers

Assess importance of omitted procedures to their previously issued opinion If omission impairs ability to support issued

opinion and report being relied upon by third parties, attempt to perform omitted procedure or appropriate alternative procedure

16-18