chapter 3: multicollinearity and model...

TRANSCRIPT

1. Multicollinearity2. Model Selection

CHAPTER 3: Multicollinearity and ModelSelection

Prof. Alan Wan

1 / 89

1. Multicollinearity2. Model Selection

Table of contents

1. Multicollinearity1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

2. Model Selection2.1 Model Selection Techniques2.2 Mallows’ Cp

2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

2 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I There is another serious consequence of adding too manyvariables to a model besides depleting the model’s d.o.f. If amodel has many variables, it is likely that some of thevariables will be strongly correlated.

I It is not desirable for strong relationships to exist among theexplanatory variables. This problem, known asmulticollinearity, can drastically alter the results from onemodel to another, making them harder to interpret.

3 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I There is another serious consequence of adding too manyvariables to a model besides depleting the model’s d.o.f. If amodel has many variables, it is likely that some of thevariables will be strongly correlated.

I It is not desirable for strong relationships to exist among theexplanatory variables. This problem, known asmulticollinearity, can drastically alter the results from onemodel to another, making them harder to interpret.

3 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I How serious the problem is depends on the degree ofmulticollinearity. Low correlations among the explanatoryvariables generally do not result in serious deterioration of thequality of O.L.S. results, but high correlations may result inhighly unstable estimates.

I The most extreme form of multicollinearity is perfectmulticollinearity. It refers to the situation where anexplanatory variable can be expressed as an exact linearcombination of some of the others. Under perfectmulticollinearity, O.L.S. fails to produce estimates of thecoefficients ((X ′X )−1 becomes non-invertible due to lineardependency in the columns of X ). A classic example ofperfect multicollinearity is the ”dummy variable trap”.

4 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I How serious the problem is depends on the degree ofmulticollinearity. Low correlations among the explanatoryvariables generally do not result in serious deterioration of thequality of O.L.S. results, but high correlations may result inhighly unstable estimates.

I The most extreme form of multicollinearity is perfectmulticollinearity. It refers to the situation where anexplanatory variable can be expressed as an exact linearcombination of some of the others. Under perfectmulticollinearity, O.L.S. fails to produce estimates of thecoefficients ((X ′X )−1 becomes non-invertible due to lineardependency in the columns of X ). A classic example ofperfect multicollinearity is the ”dummy variable trap”.

4 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Dummy Variable Trap

I A dummy variable takes on two values, either 0 and 1, toindicate whether a sample observation does or does notbelong in a certain category. For example, a dummy variablecould be used to indicate when an individual was employed byconstructing the variable as

Di = 1 if the individual i is employed

= 0 if the individual i is unemployed

I One can also define the dummy variable in the opposite way,i.e.,

D ′i = 1 if the individual i is unemployed

= 0 if the individual i is employed

5 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Dummy Variable Trap

I A dummy variable takes on two values, either 0 and 1, toindicate whether a sample observation does or does notbelong in a certain category. For example, a dummy variablecould be used to indicate when an individual was employed byconstructing the variable as

Di = 1 if the individual i is employed

= 0 if the individual i is unemployed

I One can also define the dummy variable in the opposite way,i.e.,

D ′i = 1 if the individual i is unemployed

= 0 if the individual i is employed

5 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Dummy Variable Trap

I Obviously, one cannot use Di and D ′i simultaneously in thesame regression because Di + D ′i = 1. The vector containingthis sum is perfectly correlated with the intercept term (also avector of ones).

I For the same reason, in seasonal analysis, we use m − 1,instead of m, dummy variables to represent the m seasons.The default season is inherently defined within the m − 1dummy variables (zero value of all m − 1 dummy variablesindicate the default season).

6 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Dummy Variable Trap

I Obviously, one cannot use Di and D ′i simultaneously in thesame regression because Di + D ′i = 1. The vector containingthis sum is perfectly correlated with the intercept term (also avector of ones).

I For the same reason, in seasonal analysis, we use m − 1,instead of m, dummy variables to represent the m seasons.The default season is inherently defined within the m − 1dummy variables (zero value of all m − 1 dummy variablesindicate the default season).

6 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I (Imperfect) multicollinearity is also known as near collinearity:the explanatory variables are linearly correlated but they donot obey an exact linear relationship.

I Consider the following three models that explain therelationship between HOUSING (number of housing starts (inthousands) in the U.S., and POP (U.S. population inmillions), GDP (U.S. Gross Domestic Product in billions ofdollars) and INTRATE (new home mortgage interest rate)between 1963 and 1985:

1)HOUSINGi = β1 + β2POPi + β3INTRATEi + εi

2)HOUSINGi = β1 + β4GDPi + β3INTRATEi + εi

3)HOUSINGi = β1 + β2POPi + β3INTRATEi + β4GDPi + εi

7 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I (Imperfect) multicollinearity is also known as near collinearity:the explanatory variables are linearly correlated but they donot obey an exact linear relationship.

I Consider the following three models that explain therelationship between HOUSING (number of housing starts (inthousands) in the U.S., and POP (U.S. population inmillions), GDP (U.S. Gross Domestic Product in billions ofdollars) and INTRATE (new home mortgage interest rate)between 1963 and 1985:

1)HOUSINGi = β1 + β2POPi + β3INTRATEi + εi

2)HOUSINGi = β1 + β4GDPi + β3INTRATEi + εi

3)HOUSINGi = β1 + β2POPi + β3INTRATEi + β4GDPi + εi

7 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Results for the first model:

The REG Procedure Model: MODEL1 Dependent Variable: housing Number of Observations Read 23 Number of Observations Used 23 Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 2 1125359 562679 7.50 0.0037 Error 20 1500642 75032 Corrected Total 22 2626001 Root MSE 273.91987 R-Square 0.4285 Dependent Mean 1601.07826 Adj R-Sq 0.3714 Coeff Var 17.10846 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 -3813.21672 1588.88417 -2.40 0.0263 pop 1 33.82138 9.37464 3.61 0.0018 intrate 1 -198.41880 51.29444 -3.87 0.0010

8 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Results for the second model:

The REG Procedure Model: MODEL1 Dependent Variable: housing Number of Observations Read 23 Number of Observations Used 23

Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 2 1134747 567374 7.61 0.0035 Error 20 1491254 74563 Corrected Total 22 2626001 Root MSE 273.06168 R-Square 0.4321 Dependent Mean 1601.07826 Adj R-Sq 0.3753 Coeff Var 17.05486 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 687.92418 382.69637 1.80 0.0874 gdp 1 0.90543 0.24899 3.64 0.0016 intrate 1 -169.67320 43.83996 -3.87 0.0010

9 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Results from Models 1) and 2) both make sense - estimates ofthe coefficients are of the expected signs: β2 > 0, β3 < 0 andβ4 > 0 and the coefficients are all highly significant.

I Consider the third model that combines regressors of the firstand second models:

The REG Procedure Model: MODEL1 Dependent Variable: housing Number of Observations Read 23 Number of Observations Used 23

Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 3 1147699 382566 4.92 0.0108 Error 19 1478302 77805 Corrected Total 22 2626001 Root MSE 278.93613 R-Square 0.4371 Dependent Mean 1601.07826 Adj R-Sq 0.3482 Coeff Var 17.42177 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 -1317.45317 4930.68042 -0.27 0.7922 pop 1 4.91398 36.55401 0.41 0.6878 gdp 1 0.52186 0.97391 0.54 0.5983 intrate 1 -184.77902 58.10610 -3.18 0.0049

10 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Results from Models 1) and 2) both make sense - estimates ofthe coefficients are of the expected signs: β2 > 0, β3 < 0 andβ4 > 0 and the coefficients are all highly significant.

I Consider the third model that combines regressors of the firstand second models:

The REG Procedure Model: MODEL1 Dependent Variable: housing Number of Observations Read 23 Number of Observations Used 23

Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 3 1147699 382566 4.92 0.0108 Error 19 1478302 77805 Corrected Total 22 2626001 Root MSE 278.93613 R-Square 0.4371 Dependent Mean 1601.07826 Adj R-Sq 0.3482 Coeff Var 17.42177 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 -1317.45317 4930.68042 -0.27 0.7922 pop 1 4.91398 36.55401 0.41 0.6878 gdp 1 0.52186 0.97391 0.54 0.5983 intrate 1 -184.77902 58.10610 -3.18 0.0049

10 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I In the third model, POP and GDP change to becominginsignificant although they are both significant when enteringseparately in the first and second models. This is because thethree explanatory variables are strongly correlated. Thepairwise sample correlations of the three variables are asfollows: rGDP,POP = 0.99, rGDP,INTRATE = 0.88 andrPOP,INTRATE = 0.91.

11 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

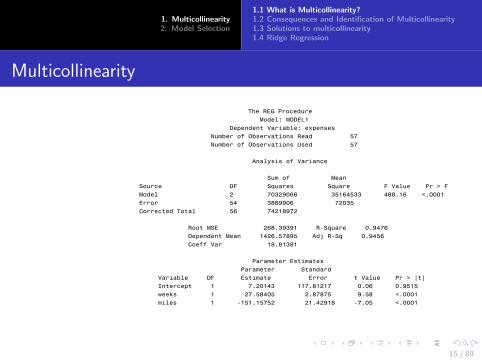

I Consider another example that relates EXPENSES, cumulativeexpenditure on the maintenance of an automobile, to MILES,the cumulative mileage in thousand of miles, and WEEKS, theautomobile’s age in weeks since first purchase, for 57automobiles. The following three models are considered:

1)EXPENSESi = β1 + β2WEEKSi + εi

2)EXPENSESi = β1 + β3MILESi + εi

3)EXPENSESi = β1 + β2WEEKSi + β3MILESi + εi

I A priori, we expect β2 > 0 and β3 > 0; a car that is drivenmore should have a greater maintenance expense; similarly,the older the car the greater the cost of maintaining it.

12 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Consider another example that relates EXPENSES, cumulativeexpenditure on the maintenance of an automobile, to MILES,the cumulative mileage in thousand of miles, and WEEKS, theautomobile’s age in weeks since first purchase, for 57automobiles. The following three models are considered:

1)EXPENSESi = β1 + β2WEEKSi + εi

2)EXPENSESi = β1 + β3MILESi + εi

3)EXPENSESi = β1 + β2WEEKSi + β3MILESi + εi

I A priori, we expect β2 > 0 and β3 > 0; a car that is drivenmore should have a greater maintenance expense; similarly,the older the car the greater the cost of maintaining it.

12 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Consider results for the three models:

The REG Procedure Model: MODEL1 Dependent Variable: expenses Number of Observations Read 57 Number of Observations Used 57 Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 1 66744854 66744854 491.16 <.0001 Error 55 7474117 135893 Corrected Total 56 74218972 Root MSE 368.63674 R-Square 0.8993 Dependent Mean 1426.57895 Adj R-Sq 0.8975 Coeff Var 25.84061 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 -626.35977 104.71371 -5.98 <.0001 weeks 1 7.34942 0.33162 22.16 <.0001

13 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

The REG Procedure Model: MODEL1 Dependent Variable: expenses Number of Observations Read 57 Number of Observations Used 57 Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 1 63715228 63715228 333.63 <.0001 Error 55 10503743 190977 Corrected Total 56 74218972 Root MSE 437.00933 R-Square 0.8585 Dependent Mean 1426.57895 Adj R-Sq 0.8559 Coeff Var 30.63338 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 -796.19928 134.75770 -5.91 <.0001 miles 1 53.45246 2.92642 18.27 <.0001

14 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

The REG Procedure Model: MODEL1 Dependent Variable: expenses Number of Observations Read 57 Number of Observations Used 57 Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 2 70329066 35164533 488.16 <.0001 Error 54 3889906 72035 Corrected Total 56 74218972 Root MSE 268.39391 R-Square 0.9476 Dependent Mean 1426.57895 Adj R-Sq 0.9456 Coeff Var 18.81381 Parameter Estimates Parameter Standard Variable DF Estimate Error t Value Pr > |t| Intercept 1 7.20143 117.81217 0.06 0.9515 weeks 1 27.58405 2.87875 9.58 <.0001 miles 1 -151.15752 21.42918 -7.05 <.0001

15 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I It is interesting to note that even though the coefficientestimate for MILES is positive in the second model, it isnegative in the third model. Thus there is a reversal in sign.

I The magnitude of the coefficient estimate for WEEKS alsochanges substantially.

I The t-statistics for MILES and WEEKS are also much lower inthe third model even though both variables are still significant.

I The problem is again due to the high correlation betweenWEEKS and MILES.

16 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I It is interesting to note that even though the coefficientestimate for MILES is positive in the second model, it isnegative in the third model. Thus there is a reversal in sign.

I The magnitude of the coefficient estimate for WEEKS alsochanges substantially.

I The t-statistics for MILES and WEEKS are also much lower inthe third model even though both variables are still significant.

I The problem is again due to the high correlation betweenWEEKS and MILES.

16 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I It is interesting to note that even though the coefficientestimate for MILES is positive in the second model, it isnegative in the third model. Thus there is a reversal in sign.

I The magnitude of the coefficient estimate for WEEKS alsochanges substantially.

I The t-statistics for MILES and WEEKS are also much lower inthe third model even though both variables are still significant.

I The problem is again due to the high correlation betweenWEEKS and MILES.

16 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I It is interesting to note that even though the coefficientestimate for MILES is positive in the second model, it isnegative in the third model. Thus there is a reversal in sign.

I The magnitude of the coefficient estimate for WEEKS alsochanges substantially.

I The t-statistics for MILES and WEEKS are also much lower inthe third model even though both variables are still significant.

I The problem is again due to the high correlation betweenWEEKS and MILES.

16 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I To explain, consider the model

Yi = β1 + β2X2i + β3X3i + εi

It can be shown that

var(b2) = σ2∑ni=1(X2i−X2)2(1−r223)

and

var(b3) = σ2∑ni=1(X3t−X3)2(1−r223)

,

where r23 is the sample correlation between X2i and X3i .

17 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I The effects of increasing r23 on var(b3):

r23 var(b3)

0 σ2∑ni=1

(X3i−X3)2 = V

0.5 1.33×V0.7 1.96×V0.8 2.78×V0.9 5.26×V0.95 10.26×V0.97 16.92×V0.99 50.25×V0.995 100×V0.999 500×V

I The sign reversal and decrease in t values (in absolute terms)are caused by the inflated variances of the estimators.

18 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Common consequences of multicollinearity:

I The standard errors associated with coefficient estimates aredisproportionately large, leading to wide confidence intervalsand insignificant t statistics even when the associated variablesare important in explaining the variations in Y

I High R2 and consequently F can convincingly rejectH0 : β2 = β3 = · · · = βk = 0, but few significant t values.

I O.L.S. estimates are unstable and very sensitive to a smallchange in the data because of the high standard errors.

I Multicollinearity is very much a norm in regression analysisinvolving non-experimental data. It can never be eliminated.The question is not about the existence or non-existence ofmulticollinearity, but how serious the problem is.

19 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Multicollinearity

I Common consequences of multicollinearity:

I The standard errors associated with coefficient estimates aredisproportionately large, leading to wide confidence intervalsand insignificant t statistics even when the associated variablesare important in explaining the variations in Y

I High R2 and consequently F can convincingly rejectH0 : β2 = β3 = · · · = βk = 0, but few significant t values.

I O.L.S. estimates are unstable and very sensitive to a smallchange in the data because of the high standard errors.

I Multicollinearity is very much a norm in regression analysisinvolving non-experimental data. It can never be eliminated.The question is not about the existence or non-existence ofmulticollinearity, but how serious the problem is.

19 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

How to identify multicollinearity?

I High R2 (and significant F value) but low values of tstatistics. This method is not always effective becausemulticollinearity can result in some, but not all, of the t valuesbeing small. The question of whether the variable is genuinelyunimportant or it just appears so due to multicollinearitycannot be answered.

I Coefficient estimates are sensitive to small changes in modelspecification.

20 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

How to identify multicollinearity?

I High R2 (and significant F value) but low values of tstatistics. This method is not always effective becausemulticollinearity can result in some, but not all, of the t valuesbeing small. The question of whether the variable is genuinelyunimportant or it just appears so due to multicollinearitycannot be answered.

I Coefficient estimates are sensitive to small changes in modelspecification.

20 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

How to identify multicollinearity (continued)?

I High pairwise correlations between the explanatory variables,but the converse need not be true. In other words,multicollinearity can still be a problem even though thecorrelation between two variables is not high. It is possible forthree or more variables to be strongly correlated with lowpairwise correlations, for example, X1 may be highly correlatedwith a2X2 + a3X3 even though the pairwise correlationsbetween X1 and each of X2 and X3 may be small.

21 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

How to identify multicollinearity (continued)?

I One rule of thumb that has been suggested as an indication ofserious multicollinearity is when any of the pairwisecorrelations among the X variables is larger than the largest ofthe correlations between Y and the X variables. But thisapproach still suffers from the same limitation concerningmore complex relationships among the X variables.

22 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

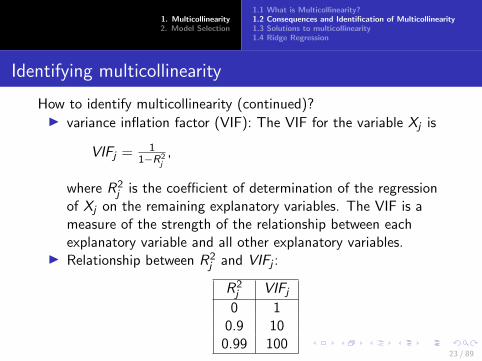

How to identify multicollinearity (continued)?I variance inflation factor (VIF): The VIF for the variable Xj is

VIFj = 11−R2

j,

where R2j is the coefficient of determination of the regression

of Xj on the remaining explanatory variables. The VIF is ameasure of the strength of the relationship between eachexplanatory variable and all other explanatory variables.

I Relationship between R2j and VIFj :

R2j VIFj

0 10.9 10

0.99 100

23 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

How to identify multicollinearity (continued)?I variance inflation factor (VIF): The VIF for the variable Xj is

VIFj = 11−R2

j,

where R2j is the coefficient of determination of the regression

of Xj on the remaining explanatory variables. The VIF is ameasure of the strength of the relationship between eachexplanatory variable and all other explanatory variables.

I Relationship between R2j and VIFj :

R2j VIFj

0 10.9 10

0.99 10023 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

I Rule of thumb for using VIF:- An individual VIFj larger than 10 indicates thatmulticollinearity may be seriously influencing the least squaresestimates of regression coefficients.- If the average of the VIFj ’s of the model exceeds 5 thenmuilticollinearity is considered to be serious.- If the VIF are less than 1/(1− R2) then multicollinearity isnot strong enough to affect the coefficient estimates. In thiscase, the independent variables are more strongly related tothe Y variable than they are to each other.

24 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Identifying multicollinearity

I For the HOUSING example,

The REG Procedure Model: MODEL1 Dependent Variable: housing Number of Observations Read 23 Number of Observations Used 23

Analysis of Variance

Sum of Mean Source DF Squares Square F Value Pr > F Model 3 1147699 382566 4.92 0.0108 Error 19 1478302 77805 Corrected Total 22 2626001 Root MSE 278.93613 R-Square 0.4371 Dependent Mean 1601.07826 Adj R-Sq 0.3482 Coeff Var 17.42177 Parameter Estimates Parameter Standard Variance Variable DF Estimate Error t Value Pr > |t| Inflation Intercept 1 -1317.45317 4930.68042 -0.27 0.7922 0 pop 1 14.91398 36.55401 0.41 0.6878 87.97808 gdp 1 0.52186 0.97391 0.54 0.5983 64.66953 intrate 1 -184.77902 58.10610 -3.18 0.0049 7.42535 25 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Solutions to multicollinearity

Solutions to multicollinearity:

I Benign neglect: If an analyst is less interested in interpretingindividual coefficients but more interested in forecasting thenmulticollinearity may not a serious concern. Even with highcorrelations among independent variables, if the regressioncoefficients are significant and have meaningful signs andmagnitudes, one need not be too concerned withmulticollinearity.

26 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Solutions to multicollinearity

I Eliminating Variables: Remove the variable with strongcorrelation with the rest would generally improve thesignificance of other variables. There is a danger, however, inremoving too many variables from the model because thatwould lead to bias in the estimates. Another drawback of thisapproach is that no information is obtained on the omittedvariable.

27 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Solutions to multicollinearity

I Respecify the model: For example, in the housing regression,we can include the variables as per capita rather thanincluding population as an explanatory variable, leading to

HOUSINGi/POPi = β1 + β2GDPi/POPi + β3INTRATEi + εi The REG Procedure

Model: MODEL1 Dependent Variable: phousing Number of Observations Read 23 Number of Observations Used 23 Analysis of Variance Sum of Mean Source DF Squares Square F Value Pr > F Model 2 26.33472 13.16736 7.66 0.0034 Error 20 34.38472 1.71924 Corrected Total 22 60.71944 Root MSE 1.31120 R-Square 0.4337 Dependent Mean 7.50743 Adj R-Sq 0.3771 Coeff Var 17.46531 Parameter Estimates Parameter Standard Variance Variable DF Estimate Error t Value Pr > |t| Inflation Intercept 1 2.07920 3.34724 0.62 0.5415 0 pgdp 1 0.93567 0.36701 2.55 0.0191 3.45825 intrate 1 -0.69832 0.18640 -3.75 0.0013 3.45825

28 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Solutions to multicollinearity

I Increase the sample size if additional information is available.

I Use alternative estimation techniques such as Ridge regressionand principal component analysis. We will touch on Ridgeregression but principal component analysis is beyond thescope of this course.

29 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Solutions to multicollinearity

I Increase the sample size if additional information is available.

I Use alternative estimation techniques such as Ridge regressionand principal component analysis. We will touch on Ridgeregression but principal component analysis is beyond thescope of this course.

29 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

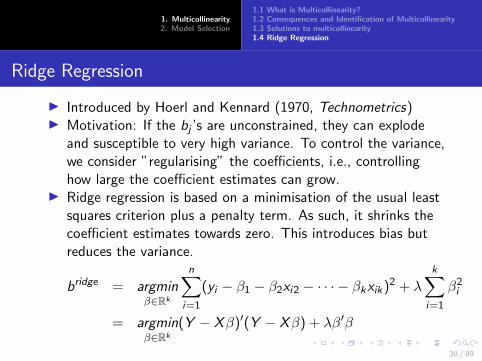

I Introduced by Hoerl and Kennard (1970, Technometrics)I Motivation: If the bj ’s are unconstrained, they can explode

and susceptible to very high variance. To control the variance,we consider ”regularising” the coefficients, i.e., controllinghow large the coefficient estimates can grow.

I Ridge regression is based on a minimisation of the usual leastsquares criterion plus a penalty term. As such, it shrinks thecoefficient estimates towards zero. This introduces bias butreduces the variance.

bridge = argminβ∈Rk

n∑i=1

(yi − β1 − β2xi2 − · · · − βkxik)2 + λk∑

i=1

β2i

= argminβ∈Rk

(Y − Xβ)′(Y − Xβ) + λβ′β

30 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I Introduced by Hoerl and Kennard (1970, Technometrics)I Motivation: If the bj ’s are unconstrained, they can explode

and susceptible to very high variance. To control the variance,we consider ”regularising” the coefficients, i.e., controllinghow large the coefficient estimates can grow.

I Ridge regression is based on a minimisation of the usual leastsquares criterion plus a penalty term. As such, it shrinks thecoefficient estimates towards zero. This introduces bias butreduces the variance.

bridge = argminβ∈Rk

n∑i=1

(yi − β1 − β2xi2 − · · · − βkxik)2 + λk∑

i=1

β2i

= argminβ∈Rk

(Y − Xβ)′(Y − Xβ) + λβ′β

30 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I This results in the solution

bridge = (X ′X + λI )−1X ′Y

I This is, in general, a biased estimator of β but more efficientthan b:

E (bridge) = (X ′X + λI )−1X ′Xβ

Cov(bridge) = (X ′X + λI )−1X ′X (X ′X + λI )−1

I This bias is zero if λ = 0 but Cov(b)− Cov(bridge) is apositive definite matrix for λ > 0. Over some range of λ,bridge has smaller mean square error (MSE) than b.

31 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I This results in the solution

bridge = (X ′X + λI )−1X ′Y

I This is, in general, a biased estimator of β but more efficientthan b:

E (bridge) = (X ′X + λI )−1X ′Xβ

Cov(bridge) = (X ′X + λI )−1X ′X (X ′X + λI )−1

I This bias is zero if λ = 0 but Cov(b)− Cov(bridge) is apositive definite matrix for λ > 0. Over some range of λ,bridge has smaller mean square error (MSE) than b.

31 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

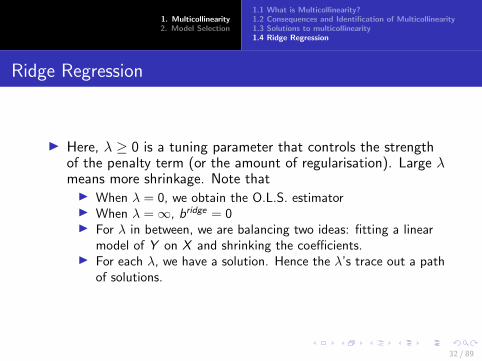

Ridge Regression

I Here, λ ≥ 0 is a tuning parameter that controls the strengthof the penalty term (or the amount of regularisation). Large λmeans more shrinkage. Note thatI When λ = 0, we obtain the O.L.S. estimatorI When λ =∞, bridge = 0I For λ in between, we are balancing two ideas: fitting a linear

model of Y on X and shrinking the coefficients.I For each λ, we have a solution. Hence the λ’s trace out a path

of solutions.

32 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I We need to ”tune” the value of λ.I In their original paper, Hoerl and Kennard (1970) introduced

”ridge traces”:

I Plot the ridge estimates against λ.I Choose λ for which the coefficient estimates are not rapidly

changing and have sensible signs.I No objective basis; heavily criticised by others.

I Hoerl and Kennard (1970) also suggested estimating λ usingthe O.L.S. coefficient and variance estimates. This leads to afeasible generalised ridge regression estimator.

I However, if λ is estimated this introduces a new stochasticelement into the estimator. Consequently, the MSE of bridge isnot necessarily smaller than that of the O.L.S. estimator andresulting tests based on t and F distributions are not valid(and may therefore be misleading).

33 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I We need to ”tune” the value of λ.I In their original paper, Hoerl and Kennard (1970) introduced

”ridge traces”:I Plot the ridge estimates against λ.I Choose λ for which the coefficient estimates are not rapidly

changing and have sensible signs.

I No objective basis; heavily criticised by others.I Hoerl and Kennard (1970) also suggested estimating λ using

the O.L.S. coefficient and variance estimates. This leads to afeasible generalised ridge regression estimator.

I However, if λ is estimated this introduces a new stochasticelement into the estimator. Consequently, the MSE of bridge isnot necessarily smaller than that of the O.L.S. estimator andresulting tests based on t and F distributions are not valid(and may therefore be misleading).

33 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I We need to ”tune” the value of λ.I In their original paper, Hoerl and Kennard (1970) introduced

”ridge traces”:I Plot the ridge estimates against λ.I Choose λ for which the coefficient estimates are not rapidly

changing and have sensible signs.I No objective basis; heavily criticised by others.

I Hoerl and Kennard (1970) also suggested estimating λ usingthe O.L.S. coefficient and variance estimates. This leads to afeasible generalised ridge regression estimator.

I However, if λ is estimated this introduces a new stochasticelement into the estimator. Consequently, the MSE of bridge isnot necessarily smaller than that of the O.L.S. estimator andresulting tests based on t and F distributions are not valid(and may therefore be misleading).

33 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I We need to ”tune” the value of λ.I In their original paper, Hoerl and Kennard (1970) introduced

”ridge traces”:I Plot the ridge estimates against λ.I Choose λ for which the coefficient estimates are not rapidly

changing and have sensible signs.I No objective basis; heavily criticised by others.

I Hoerl and Kennard (1970) also suggested estimating λ usingthe O.L.S. coefficient and variance estimates. This leads to afeasible generalised ridge regression estimator.

I However, if λ is estimated this introduces a new stochasticelement into the estimator. Consequently, the MSE of bridge isnot necessarily smaller than that of the O.L.S. estimator andresulting tests based on t and F distributions are not valid(and may therefore be misleading).

33 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I We need to ”tune” the value of λ.I In their original paper, Hoerl and Kennard (1970) introduced

”ridge traces”:I Plot the ridge estimates against λ.I Choose λ for which the coefficient estimates are not rapidly

changing and have sensible signs.I No objective basis; heavily criticised by others.

I Hoerl and Kennard (1970) also suggested estimating λ usingthe O.L.S. coefficient and variance estimates. This leads to afeasible generalised ridge regression estimator.

I However, if λ is estimated this introduces a new stochasticelement into the estimator. Consequently, the MSE of bridge isnot necessarily smaller than that of the O.L.S. estimator andresulting tests based on t and F distributions are not valid(and may therefore be misleading).

33 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

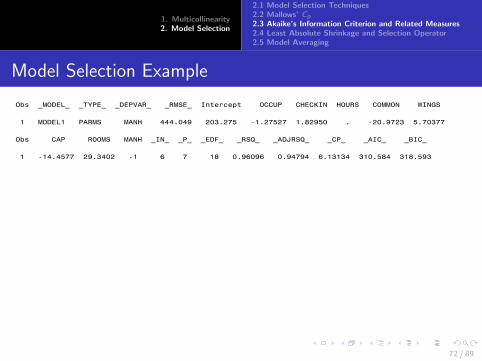

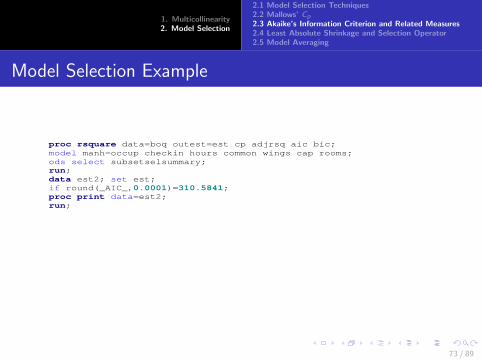

I Example 3.1 The following example comes from a study ofmanpower needs for operating a U.S. Navy Bachelor OfficersQuarters (BOQ). The observations are recorded for 24establishments. The response variable represents the monthlyman-hours (MANH) required to operate each establishment,and the independent variables are:

OCCUP = average daily occupancy

CHECKIN = monthly average number of check-ins

HOURS = weekly hours of service desk operation

COMMON = square feet of common use area

WINGS = number of building wings

CAP = operational berthing capacity

ROOMS = number of rooms 34 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I Results obtained using SAS:SAS Output

SAS Output_htm#IDX10.htm[10/31/2016 1:52:19 PM]

The SAS System

The REG ProcedureModel: MODEL1

Dependent Variable: MANH

Number of Observations Read 24

Number of Observations Used 24

Analysis of Variance

Source DFSum of

SquaresMean

Square F Value Pr > F

Model 7 87497673 12499668 154.32 <.0001

Error 16 1295987 80999

Corrected Total 23 88793659

Root MSE 284.60353 R-Square 0.9854

Dependent Mean 2050.00708 Adj R-Sq 0.9790

Coeff Var 13.88305

Parameter Estimates

Variable DFParameter

EstimateStandard

Error t Value Pr > |t|VarianceInflation

Intercept 1 171.47336 148.86168 1.15 0.2663 0

OCCUP 1 21.04562 4.28905 4.91 0.0002 43.63222

CHECKIN 1 1.42632 0.33071 4.31 0.0005 4.54154

HOURS 1 -0.08927 1.16353 -0.08 0.9398 1.36076

COMMON 1 7.65033 8.43835 0.91 0.3781 4.06083

WINGS 1 -5.30231 9.45276 -0.56 0.5826 3.79996

CAP 1 -4.07475 3.30195 -1.23 0.2350 56.60333

ROOMS 1 0.33191 6.81399 0.05 0.9618 178.7015935 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I The O.L.S. results clearly indicate serious multicollinearity.I R2 = 0.985 is rather high. Since 1/(1− R2) = 68.5, any

variables associated with VIF values exceeding 68.5 are moreclosely related to other explanatory variables than they are tothe dependent variable.

I ROOMS has a VIF that exceeds 68.5, and it is notstatistically significant.

I OCCUP has a VIF that exceeds 10 and a t − stat with a verysmall p−value. One may conclude that multicollinearity existsthat decreases the reliability of estimates.

I CAP has a large VIF and is not significant; this variable mighthave been useful had it not been associated withmulticollinearity.

36 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I The O.L.S. results clearly indicate serious multicollinearity.I R2 = 0.985 is rather high. Since 1/(1− R2) = 68.5, any

variables associated with VIF values exceeding 68.5 are moreclosely related to other explanatory variables than they are tothe dependent variable.

I ROOMS has a VIF that exceeds 68.5, and it is notstatistically significant.

I OCCUP has a VIF that exceeds 10 and a t − stat with a verysmall p−value. One may conclude that multicollinearity existsthat decreases the reliability of estimates.

I CAP has a large VIF and is not significant; this variable mighthave been useful had it not been associated withmulticollinearity.

36 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I The O.L.S. results clearly indicate serious multicollinearity.I R2 = 0.985 is rather high. Since 1/(1− R2) = 68.5, any

variables associated with VIF values exceeding 68.5 are moreclosely related to other explanatory variables than they are tothe dependent variable.

I ROOMS has a VIF that exceeds 68.5, and it is notstatistically significant.

I OCCUP has a VIF that exceeds 10 and a t − stat with a verysmall p−value. One may conclude that multicollinearity existsthat decreases the reliability of estimates.

I CAP has a large VIF and is not significant; this variable mighthave been useful had it not been associated withmulticollinearity.

36 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I The O.L.S. results clearly indicate serious multicollinearity.I R2 = 0.985 is rather high. Since 1/(1− R2) = 68.5, any

variables associated with VIF values exceeding 68.5 are moreclosely related to other explanatory variables than they are tothe dependent variable.

I ROOMS has a VIF that exceeds 68.5, and it is notstatistically significant.

I OCCUP has a VIF that exceeds 10 and a t − stat with a verysmall p−value. One may conclude that multicollinearity existsthat decreases the reliability of estimates.

I CAP has a large VIF and is not significant; this variable mighthave been useful had it not been associated withmulticollinearity.

36 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I The ridge plot is given as follows:The SAS SystemThe SAS System

Coeffici

ent Es

timate

-10

-5

0

5

10

15

20

25

Ridge k

0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0

Plot OCCUP CHECKIN HOURS COMMONWINGS CAP ROOMS 37 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I VIFs of estimates at varying values of λ:SAS Output

SAS Output_htm#IDX10.htm[10/31/2016 3:17:25 PM]

The SAS System

Obs _RIDGE_ OCCUP CHECKIN HOURS COMMON WINGS CAP ROOMS

3 0.00 43.6322 4.54154 1.36076 4.06083 3.79996 56.6033 178.702

6 0.05 3.3779 2.60290 1.16762 1.58426 2.08551 2.8171 1.332

9 0.10 1.5606 1.75533 1.02578 1.27207 1.50400 1.4726 0.539

12 0.15 0.9261 1.28481 0.90939 1.05990 1.17392 0.9523 0.334

15 0.20 0.6270 0.99168 0.81228 0.90266 0.95480 0.6826 0.241

18 0.25 0.4605 0.79480 0.73028 0.78112 0.79775 0.5210 0.189

21 0.30 0.3574 0.65519 0.66033 0.68448 0.67975 0.4152 0.155

24 0.35 0.2886 0.55203 0.60014 0.60600 0.58811 0.3414 0.131

27 0.40 0.2402 0.47330 0.54796 0.54116 0.51516 0.2877 0.114

30 0.45 0.2045 0.41163 0.50240 0.48684 0.45592 0.2470 0.101

33 0.50 0.1774 0.36226 0.46239 0.44078 0.40703 0.2154 0.091

36 0.55 0.1562 0.32203 0.42705 0.40134 0.36612 0.1903 0.083

39 0.60 0.1393 0.28873 0.39567 0.36726 0.33149 0.1700 0.076

42 0.65 0.1255 0.26081 0.36769 0.33757 0.30187 0.1532 0.070

45 0.70 0.1141 0.23713 0.34262 0.31153 0.27632 0.1391 0.066

48 0.75 0.1045 0.21683 0.32007 0.28855 0.25410 0.1273 0.062

51 0.80 0.0963 0.19929 0.29972 0.26815 0.23463 0.1171 0.058

54 0.85 0.0893 0.18400 0.28128 0.24995 0.21748 0.1084 0.055

57 0.90 0.0832 0.17058 0.26452 0.23363 0.20227 0.1007 0.052

60 0.95 0.0779 0.15873 0.24924 0.21895 0.18871 0.0941 0.050 38 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I Coefficient estimates at varying values of λ:SAS Output

SAS Output_htm#IDX10.htm[10/31/2016 3:17:25 PM]

The SAS System

Obs _RIDGE_ Intercept OCCUP CHECKIN HOURS COMMON WINGS CAP ROOMS

4 0.00 171.473 21.0456 1.42632 -0.08927 7.65033 -5.3023 -4.07475 0.33191

7 0.05 150.557 12.2806 1.53469 0.38682 0.51146 9.7589 -1.47494 2.86432

10 0.10 140.775 9.7164 1.49356 0.62657 -0.24718 14.0025 -0.16568 2.95724

13 0.15 135.946 8.3991 1.43806 0.79962 -0.05448 15.7514 0.51504 2.99289

16 0.20 134.517 7.5788 1.38536 0.93650 0.41616 16.6172 0.92646 3.00585

19 0.25 135.604 7.0087 1.33797 1.04940 0.96391 17.0913 1.19731 3.00591

22 0.30 138.627 6.5829 1.29571 1.14469 1.51548 17.3648 1.38550 2.99787

25 0.35 143.178 6.2487 1.25789 1.22625 2.04212 17.5248 1.52105 2.98452

28 0.40 148.955 5.9765 1.22380 1.29674 2.53300 17.6152 1.62115 2.96763

31 0.45 155.725 5.7485 1.19285 1.35805 2.98510 17.6603 1.69630 2.94833

34 0.50 163.307 5.5532 1.16456 1.41164 3.39890 17.6742 1.75333 2.92739

37 0.55 171.555 5.3830 1.13852 1.45864 3.77643 17.6658 1.79684 2.90537

40 0.60 180.350 5.2325 1.11444 1.49997 4.12031 17.6408 1.83003 2.88264

43 0.65 189.594 5.0978 1.09203 1.53637 4.43336 17.6033 1.85522 2.85947

46 0.70 199.208 4.9760 1.07111 1.56847 4.71830 17.5558 1.87409 2.83607

49 0.75 209.124 4.8649 1.05147 1.59677 4.97770 17.5006 1.88792 2.81258

52 0.80 219.284 4.7629 1.03299 1.62173 5.21392 17.4389 1.89769 2.78911

55 0.85 229.641 4.6686 1.01554 1.64371 5.42912 17.3722 1.90415 2.76573

58 0.90 240.155 4.5809 0.99901 1.66305 5.62523 17.3011 1.90789 2.74252

61 0.95 250.789 4.4990 0.98330 1.68002 5.80401 17.2266 1.90939 2.71951 39 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

I Picking a value of λ is quite subjective. It appears that thecoefficient estimates stabilise at around λ = 0.65. The VIF’sare also reasonably small at λ = 0.65 and the coefficientestimates have the right signs.

SAS Output

SAS Output_htm#IDX10.htm[10/31/2016 3:17:25 PM]

The SAS System

Obs _TYPE_ Intercept OCCUP CHECKIN HOURS COMMON WINGS CAP ROOMS

1 PARMS 171.473 21.0456 1.42632 -0.08927 7.65033 -5.3023 -4.07475 0.33191

2 SEB 148.862 4.2890 0.33071 1.16353 8.43835 9.4528 3.30195 6.81399

3 RIDGEVIF . 0.1255 0.26081 0.36769 0.33757 0.3019 0.15317 0.07038

4 RIDGE 189.594 5.0978 1.09203 1.53637 4.43336 17.6033 1.85522 2.85947

5 RIDGESEB 243.906 0.5262 0.18130 1.38363 5.56579 6.0951 0.39295 0.30936

40 / 89

1. Multicollinearity2. Model Selection

1.1 What is Multicollinearity?1.2 Consequences and Identification of Multicollinearity1.3 Solutions to multicollinearity1.4 Ridge Regression

Ridge Regression

DATA BOQ; INPUT id $ OCCUP CHECKIN HOURS COMMON WINGS CAP ROOMS MANH; DROP ID; CARDS; A 2 4 4 1.26 1 6 6 180.23 B 3 1.58 40 1.25 1 5 5 182.61 C 16.6 23.78 40 1 1 13 13 164.38 : : X 384.5 1473.66 168 7.36 24 540 453 8266.77 Y 95 368 168 30.26 9 292 196 1845.89 ; proc reg data=boq; model manh=occup checkin hours common wings cap rooms/vif; run; proc reg data=boq outvif outseb outest=bfout ridge=0 to 1.0 by 0.02; model manh=occup checkin hours common wings cap rooms/noprint; plot/ridgeplot nomodel nostat; run; proc print data =bfout; var _RIDGE_ occup checkin hours common wings cap rooms; where _TYPE_='RIDGEVIF'; run; proc print data=bfout; var _RIDGE_ intercept occup checkin hours common wings cap rooms; where _TYPE_='RIDGE'; run;

41 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I We consider two broad types of model selection techniques:all possible regressions and penalised regression.

I Penalised regression bears a similarity to Ridge regressionexcept that penalised regression actually allows somecoefficients to become identically zero.

I For all possible regressions, we consider the followingcommonly used criteria for choosing between models:I Adjusted R2 Criterion - select the model with the highest

adjusted R2

I Mallows’ Cp CriterionI Information Criterion

42 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I We consider two broad types of model selection techniques:all possible regressions and penalised regression.

I Penalised regression bears a similarity to Ridge regressionexcept that penalised regression actually allows somecoefficients to become identically zero.

I For all possible regressions, we consider the followingcommonly used criteria for choosing between models:I Adjusted R2 Criterion - select the model with the highest

adjusted R2

I Mallows’ Cp CriterionI Information Criterion

42 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I We consider two broad types of model selection techniques:all possible regressions and penalised regression.

I Penalised regression bears a similarity to Ridge regressionexcept that penalised regression actually allows somecoefficients to become identically zero.

I For all possible regressions, we consider the followingcommonly used criteria for choosing between models:I Adjusted R2 Criterion - select the model with the highest

adjusted R2

I Mallows’ Cp CriterionI Information Criterion

42 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I In the process we will also examine the effects of omittingimportant regressors and including irrelevant regressors.

I If important variables are omitted the effects of these variablesare not taken into account. The estimators of othercoefficients will become biased.

I If unimportant variables are included then the variances ofcoefficient estimators will become inflated. Thus, forecastsand estimates will become more variable than they would behad the irrelevant regressors been excluded.

43 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I In the process we will also examine the effects of omittingimportant regressors and including irrelevant regressors.

I If important variables are omitted the effects of these variablesare not taken into account. The estimators of othercoefficients will become biased.

I If unimportant variables are included then the variances ofcoefficient estimators will become inflated. Thus, forecastsand estimates will become more variable than they would behad the irrelevant regressors been excluded.

43 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Model Selection Techniques

I In the process we will also examine the effects of omittingimportant regressors and including irrelevant regressors.

I If important variables are omitted the effects of these variablesare not taken into account. The estimators of othercoefficients will become biased.

I If unimportant variables are included then the variances ofcoefficient estimators will become inflated. Thus, forecastsand estimates will become more variable than they would behad the irrelevant regressors been excluded.

43 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The Mallows’ Cp is one of the most commonly used criteriafor choosing between alternative regressions with differentcombinations of regressors. The Cp’s formula is given by

Cp =SSEp

MSEF− (n − 2p)

where SSEp is the sum of squared errors of the regression withp coefficients and MSEF is the MSE corresponding to the fullmodel, the model that contains all of the explanatoryvariables.

44 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I When the estimated regression has no bias, Cp is equal to p.When evaluating which model is best, it is recommended thatregression with small Cp values and those with values close top be considered. If Cp is substantially larger than p, thenthere is a large bias component in the model.

45 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The development of the Mallows’ Cp is based on theestimation of the trace of the MSE (also known as risk undersquared error loss) of an estimator of Xβ scaled by σ2.

I Consider the O.L.S. predictor Xb, the risk of Xb is given byR(Xb)

=E [(Xb − Xβ)′(Xb − Xβ)]

=E [(Xb − E (Xb) + E (Xb)− Xβ)′(Xb − E (Xb) + E (Xb)− Xβ)]

=E [(Xb − E (Xb))′(Xb − E (Xb))] + (E (Xb)− Xβ)′(E (Xb)− Xβ)

46 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The development of the Mallows’ Cp is based on theestimation of the trace of the MSE (also known as risk undersquared error loss) of an estimator of Xβ scaled by σ2.

I Consider the O.L.S. predictor Xb, the risk of Xb is given byR(Xb)

=E [(Xb − Xβ)′(Xb − Xβ)]

=E [(Xb − E (Xb) + E (Xb)− Xβ)′(Xb − E (Xb) + E (Xb)− Xβ)]

=E [(Xb − E (Xb))′(Xb − E (Xb))] + (E (Xb)− Xβ)′(E (Xb)− Xβ)

46 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the variances of the elements ofY = Xb, while the second term is the sum of the bias squaresof the elements of Y when E (Y ) = Xβ is the unknownquantity of interest.

I Assuming that the model is correctly specified such thatE (ε) = 0, b is unbiased and the second term vanishes to zero.

I If b is unbiased, the first term (the sum of variances) may bewritten as

E (ε′X (X ′X )−1X ′ε)

=E [tr((X ′X )−1X ′εε′X )]

=σ2k

47 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the variances of the elements ofY = Xb, while the second term is the sum of the bias squaresof the elements of Y when E (Y ) = Xβ is the unknownquantity of interest.

I Assuming that the model is correctly specified such thatE (ε) = 0, b is unbiased and the second term vanishes to zero.

I If b is unbiased, the first term (the sum of variances) may bewritten as

E (ε′X (X ′X )−1X ′ε)

=E [tr((X ′X )−1X ′εε′X )]

=σ2k

47 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the variances of the elements ofY = Xb, while the second term is the sum of the bias squaresof the elements of Y when E (Y ) = Xβ is the unknownquantity of interest.

I Assuming that the model is correctly specified such thatE (ε) = 0, b is unbiased and the second term vanishes to zero.

I If b is unbiased, the first term (the sum of variances) may bewritten as

E (ε′X (X ′X )−1X ′ε)

=E [tr((X ′X )−1X ′εε′X )]

=σ2k

47 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Now, suppose that the choice of X is uncertain and Xp isused as the regressor matrix instead. So,

Y = Xpβp + u

where u = ε+ Xeβe or u = ε− Xeβe .

I Thus, bp = (X ′pXp)−1X ′pY and

Xpbp − E (Xpbp) = Xp(βp + (X ′pXp)−1X ′pε± (X ′pXp)−1X ′pXeβe)

−Xpβp ∓ (X ′pXp)−1X ′pXeβe

= Xp(X ′pXp)−1X ′pε

I Hence

E [(Xpbp − E (Xpbp))′(Xpbp − E (Xpbp))] = σ2p

48 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Now, suppose that the choice of X is uncertain and Xp isused as the regressor matrix instead. So,

Y = Xpβp + u

where u = ε+ Xeβe or u = ε− Xeβe .I Thus, bp = (X ′pXp)−1X ′pY and

Xpbp − E (Xpbp) = Xp(βp + (X ′pXp)−1X ′pε± (X ′pXp)−1X ′pXeβe)

−Xpβp ∓ (X ′pXp)−1X ′pXeβe

= Xp(X ′pXp)−1X ′pε

I Hence

E [(Xpbp − E (Xpbp))′(Xpbp − E (Xpbp))] = σ2p

48 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Now, suppose that the choice of X is uncertain and Xp isused as the regressor matrix instead. So,

Y = Xpβp + u

where u = ε+ Xeβe or u = ε− Xeβe .I Thus, bp = (X ′pXp)−1X ′pY and

Xpbp − E (Xpbp) = Xp(βp + (X ′pXp)−1X ′pε± (X ′pXp)−1X ′pXeβe)

−Xpβp ∓ (X ′pXp)−1X ′pXeβe

= Xp(X ′pXp)−1X ′pε

I Hence

E [(Xpbp − E (Xpbp))′(Xpbp − E (Xpbp))] = σ2p48 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I So, the sum of the variances of y1, · · · , yn changes from σ2kto σ2p as the number of coefficients changes from k to p.Thus, if the model is under-fitted (i.e., p < k), the sum of thevariances actually decreases whereas if the model is over-fitted(i.e., p > k), this sum increases.

I However, when the model is misspecified, the second term inthe MSE expression related to the bias is not always zero.Note that

E (Xpbp) = Xp(X ′pXp)−1X ′pXβ,

which equals Xβ if Xpbp is unbiased.

49 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I So, the sum of the variances of y1, · · · , yn changes from σ2kto σ2p as the number of coefficients changes from k to p.Thus, if the model is under-fitted (i.e., p < k), the sum of thevariances actually decreases whereas if the model is over-fitted(i.e., p > k), this sum increases.

I However, when the model is misspecified, the second term inthe MSE expression related to the bias is not always zero.Note that

E (Xpbp) = Xp(X ′pXp)−1X ′pXβ,

which equals Xβ if Xpbp is unbiased.

49 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Obviously, when the model is under-fitted,Xp(X ′pXp)−1X ′pXβ 6= Xβ. That is, a bias is introduced to theestimator of E (Y ).

I On the other hand, when the model is over-fitted, we canwrite X = XpZ , where

Z =

[I(k×k)

0((p−k)×k)

]leading to Xp(X ′pXp)−1X ′pXβ = Xβ. That is, the estimatorremains unbiased when the model is over-fitted.

50 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Obviously, when the model is under-fitted,Xp(X ′pXp)−1X ′pXβ 6= Xβ. That is, a bias is introduced to theestimator of E (Y ).

I On the other hand, when the model is over-fitted, we canwrite X = XpZ , where

Z =

[I(k×k)

0((p−k)×k)

]leading to Xp(X ′pXp)−1X ′pXβ = Xβ. That is, the estimatorremains unbiased when the model is over-fitted.

50 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I So, when the model is under-fitted, the O.L.S. estimator ofE (Y ) is biased but has a reduced sum of variances. When themodel is over-fitted, the O.L.S. estimator of E (Y ) remainsunbiased but its sum of variances increases.

I Now, the sum of bias squares of Y is

(E (Xpbp)− Xβ)′(E (Xpbp)− Xβ)

= (Xp(X ′pXp)−1X ′pXβ − Xβ)′(Xp(X ′pXp)−1X ′pXβ − Xβ)

= β′X ′(I − Xp(X ′pXp)−1X ′p)Xβ

51 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I So, when the model is under-fitted, the O.L.S. estimator ofE (Y ) is biased but has a reduced sum of variances. When themodel is over-fitted, the O.L.S. estimator of E (Y ) remainsunbiased but its sum of variances increases.

I Now, the sum of bias squares of Y is

(E (Xpbp)− Xβ)′(E (Xpbp)− Xβ)

= (Xp(X ′pXp)−1X ′pXβ − Xβ)′(Xp(X ′pXp)−1X ′pXβ − Xβ)

= β′X ′(I − Xp(X ′pXp)−1X ′p)Xβ

51 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I To estimate the bias which is unobservable, note that

(Y − Xpbp)′(Y − Xpbp) = Y ′(I − Xp(X ′pXp)−1X ′p)Y = SSEp

is the sum of squared errors in the observation sample basedon the estimated model with p coefficients. Using Theorem1.17 of Seber (2008): A Matrix Handbook for Statisticians,E (Y ′AY ) = E (Y ′)AE (Y ) + tr(ΣA), where Σ is the Cov(Y ),we can write

E ((Y − Xpbp)′(Y − Xpbp))

= E (Y ′)(I − Xp(X ′pXp)−1X ′p)E (Y ) + tr(I − Xp(X ′pXp)−1X ′p)σ2

= β′X ′(I − Xp(X ′pXp)−1X ′p)Xβ + σ2n − σ2p

52 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the bias squares. We canestimate this sum by SSEp − σ2(n − p).

I Recall that the Mallows’ Cp is defined as R(Xpbp)/σ2. By ourderivation,

R(Xpbp)/σ2 = p +SSEp − σ2(n − p)

σ2

I σ2 is unknown but can be estimated by e ′e/(n − k), the MSEin the ANOVA table of the full model. This yields the formula:

Cp = p +SSEp

MSEF− n + p

=SSEp

MSEF− (n − 2p)

53 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the bias squares. We canestimate this sum by SSEp − σ2(n − p).

I Recall that the Mallows’ Cp is defined as R(Xpbp)/σ2. By ourderivation,

R(Xpbp)/σ2 = p +SSEp − σ2(n − p)

σ2

I σ2 is unknown but can be estimated by e ′e/(n − k), the MSEin the ANOVA table of the full model. This yields the formula:

Cp = p +SSEp

MSEF− n + p

=SSEp

MSEF− (n − 2p)

53 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I The first term is the sum of the bias squares. We canestimate this sum by SSEp − σ2(n − p).

I Recall that the Mallows’ Cp is defined as R(Xpbp)/σ2. By ourderivation,

R(Xpbp)/σ2 = p +SSEp − σ2(n − p)

σ2

I σ2 is unknown but can be estimated by e ′e/(n − k), the MSEin the ANOVA table of the full model. This yields the formula:

Cp = p +SSEp

MSEF− n + p

=SSEp

MSEF− (n − 2p)

53 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Thus, if the model is correctly specified, the bias is zero andthe (scaled) sum of variances (and hence the Cp) should equalp.

I For two models with Cp’s that are both close to theirrespective p’s, the model with the smaller Cp is preferred tothe model with the larger Cp because a large Cp probablyindicates over-fitting which results in a larger sum of variancesthan otherwise.

I When the model is grossly under-fitted, the bias term willdominate the reduced variance, leading to a value of Cp

substantially larger than p.

54 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Thus, if the model is correctly specified, the bias is zero andthe (scaled) sum of variances (and hence the Cp) should equalp.

I For two models with Cp’s that are both close to theirrespective p’s, the model with the smaller Cp is preferred tothe model with the larger Cp because a large Cp probablyindicates over-fitting which results in a larger sum of variancesthan otherwise.

I When the model is grossly under-fitted, the bias term willdominate the reduced variance, leading to a value of Cp

substantially larger than p.

54 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Mallows’ Cp

I Thus, if the model is correctly specified, the bias is zero andthe (scaled) sum of variances (and hence the Cp) should equalp.

I For two models with Cp’s that are both close to theirrespective p’s, the model with the smaller Cp is preferred tothe model with the larger Cp because a large Cp probablyindicates over-fitting which results in a larger sum of variancesthan otherwise.

I When the model is grossly under-fitted, the bias term willdominate the reduced variance, leading to a value of Cp

substantially larger than p.

54 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Information Criteria

I Information Criteria use the observed data to give a candidatemodel a certain score; this then leads to a fully ranked list ofcandidate models from worst to best.

I Virtually all Information Criteria are penalised version of theattained maximum log-likelihood of the model, aimed atbalancing between goodness of fit (high value oflog-likelihood) and complexity (complex models are penalisedmore than simple ones).

55 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Information Criteria

I Information Criteria use the observed data to give a candidatemodel a certain score; this then leads to a fully ranked list ofcandidate models from worst to best.

I Virtually all Information Criteria are penalised version of theattained maximum log-likelihood of the model, aimed atbalancing between goodness of fit (high value oflog-likelihood) and complexity (complex models are penalisedmore than simple ones).

55 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Likelihood Function and Maximum Likelihood

I Suppose that a sample of observations (y1, y2, · · · , yn) isavailable, and it is assumed that each yi is drawn from someparticular distribution which has a probability density functionp(yi |β). Assuming that the yi ’s are independent, the jointdensity of the sample is given by

p(y1|β)p(y2|β) · · · p(yn|β) =n∏

i=1

p(yi |β) = f (y |β) = L(β|y)

56 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Likelihood Function and Maximum Likelihood

I L(β|y) is the likelihood function which is a function of theparameters for a given set of observations.

I Clearly, the value of L(β|y) will be higher for some values of βthan for others, and the method of maximum likelihoodanswers the question:What value of the parameters maximises the likelihood?

I Denote this parameter value by bMLE . The joint densityf (y |β) is then maximised at bMLE , and so bMLE is theparameter value that maximises the probability of observingthe sample at hand.

57 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Likelihood Function and Maximum Likelihood

I L(β|y) is the likelihood function which is a function of theparameters for a given set of observations.

I Clearly, the value of L(β|y) will be higher for some values of βthan for others, and the method of maximum likelihoodanswers the question:What value of the parameters maximises the likelihood?

I Denote this parameter value by bMLE . The joint densityf (y |β) is then maximised at bMLE , and so bMLE is theparameter value that maximises the probability of observingthe sample at hand.

57 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Likelihood Function and Maximum Likelihood

I In practice, maximum likelihood typically does not use thelikelihood function itself, but uses the log-likelihood function

lnL(β|y) = lnf (y |β) =n∑

i=1

lnp(yi |β)

I The advantage of working with the log-likelihood is that thisis an additive rather than a multiplicative function andmaximising this function is analytically easier than maximisingthe likelihood itself. Of course the two approaches lead to thesame solution because the log-likelihood is a monotonictransformation of the likelihood.

58 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Likelihood Function and Maximum Likelihood

I In practice, maximum likelihood typically does not use thelikelihood function itself, but uses the log-likelihood function

lnL(β|y) = lnf (y |β) =n∑

i=1

lnp(yi |β)

I The advantage of working with the log-likelihood is that thisis an additive rather than a multiplicative function andmaximising this function is analytically easier than maximisingthe likelihood itself. Of course the two approaches lead to thesame solution because the log-likelihood is a monotonictransformation of the likelihood.

58 / 89

1. Multicollinearity2. Model Selection

2.1 Model Selection Techniques2.2 Mallows’ Cp2.3 Akaike’s Information Criterion and Related Measures2.4 Least Absolute Shrinkage and Selection Operator2.5 Model Averaging

Akaike’s Information Criterion

I The Akaike’s Information Criterion (AIC) is arguably the mostpopular information criteria due to its ease. For the sth

model, the AIC is defined as

AICs = −2lnf (y |bs) + 2ks

where lnf (y |bs) and ks are the (computed) log-likelihood ofand the number of coefficients in the sth model respectively.

I lnf (y |bs) is the goodness of fit term and ks is the penaltyterm.

59 / 89

1. Multicollinearity2. Model Selection