chapter 4 time value of money 1: analyzing single cash flows copyright © 2011 by the mcgraw-hill...

TRANSCRIPT

Chapter 4

Time Value of Money 1: Analyzing Single Cash Flows

Copyright © 2011 by The McGraw-Hill Companies, Inc. All rights reserved.McGraw-Hill/Irwin

2

Chapter 4 Learning GoalsLG1: Create a cash flow time line

LG2: Compute the future value of money

LG3: Use the power of compounding to increase wealth

LG4: Calculate the present value of a payment made in the future

LG5: Move cash flows from one year to another

LG6: Apply the Rule of 72

LG7: Compute the rate of return

LG8: Calculate the number of years needed to grow an investment to a specific amount of money

3

Introduction

• The ability to work problems using the principles of the Time Value of Money will be one of them most important skills you will learn – Financial managers– Any kind of manager in businesses of all

sizes– Personal life

4

• The basic idea behind the time value of money is that $1 today is worth more than $1 promised next year

• Factors to consider:– Size of the cash flows– Time between the cash flows– Rate of return

• Opportunity cost• Interest rate• Required rate of return• Discount rate

5

Organizing Cash Flows• A helpful tool for analysis of cash flows

is the time line, which shows the magnitude of cash flows at different points in time– Cash we receive is called an inflow and is

represented by a positive number– Cash that leaves us is called an outflow

and is represented by a negative numberCash flow

-100

105

5%

Period 0 1 2

6

Single-period Future Value

• You invest $100 today in an account earning 5% per year. Compute the future value in one year.

Value in one year = Today’s cash flow + Interest earned

= $100 + ($100 x 0.05)

= $100 x (1 + 0.05)

= $105

In general: FV = PV x (1 + i)N

7

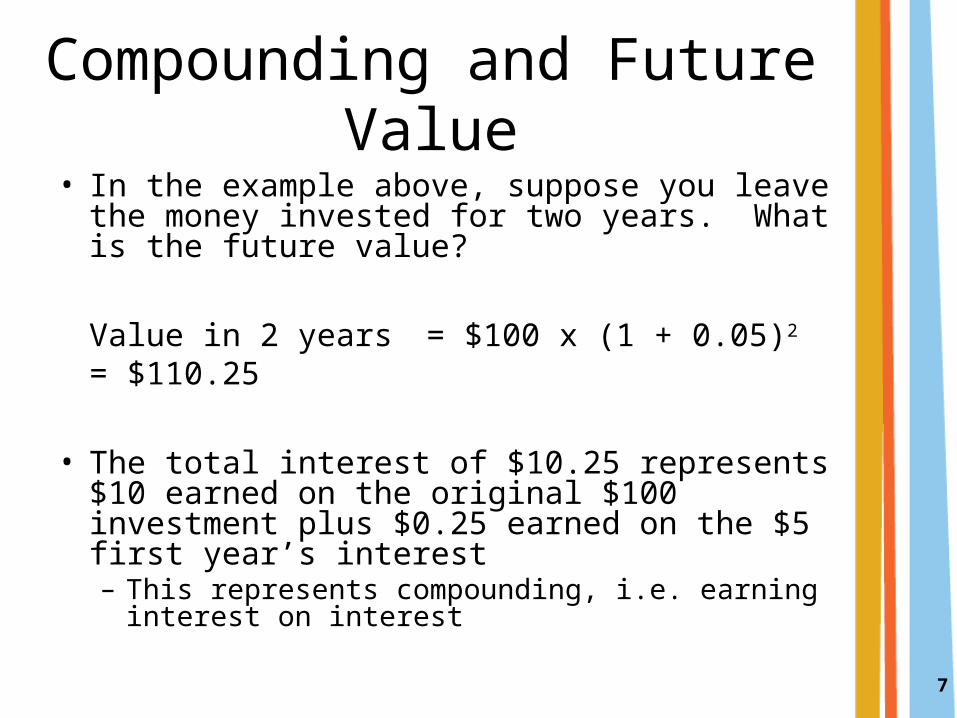

Compounding and Future Value

• In the example above, suppose you leave the money invested for two years. What is the future value?

Value in 2 years = $100 x (1 + 0.05)2 = $110.25

• The total interest of $10.25 represents $10 earned on the original $100 investment plus $0.25 earned on the $5 first year’s interest– This represents compounding, i.e. earning

interest on interest

8

Financial Calculator Solution

INPUT 2 5 -100 0N I/YR PV PMT FV

OUTPUT 110.25

9

• Suppose we leave the deposit for five years?

• FV = $100 x (1.05)5 = $127.63

• Financial calculator solution:

INPUT 5 5 -100 0N I/YR PV PMT FV

OUTPUT 127.63

10

The Power of Compounding

• Compound interest is an extremely powerful tool for building wealth.

• Albert Einstein is supposed to have said: “the most powerful force in the universe is compound interest”

• Let’s illustrate the power of compounding over long periods of time. Using the above example, what is the future value of the $100 if it is invested for 20 years at 5% interest.

11

• Financial calculator solution:

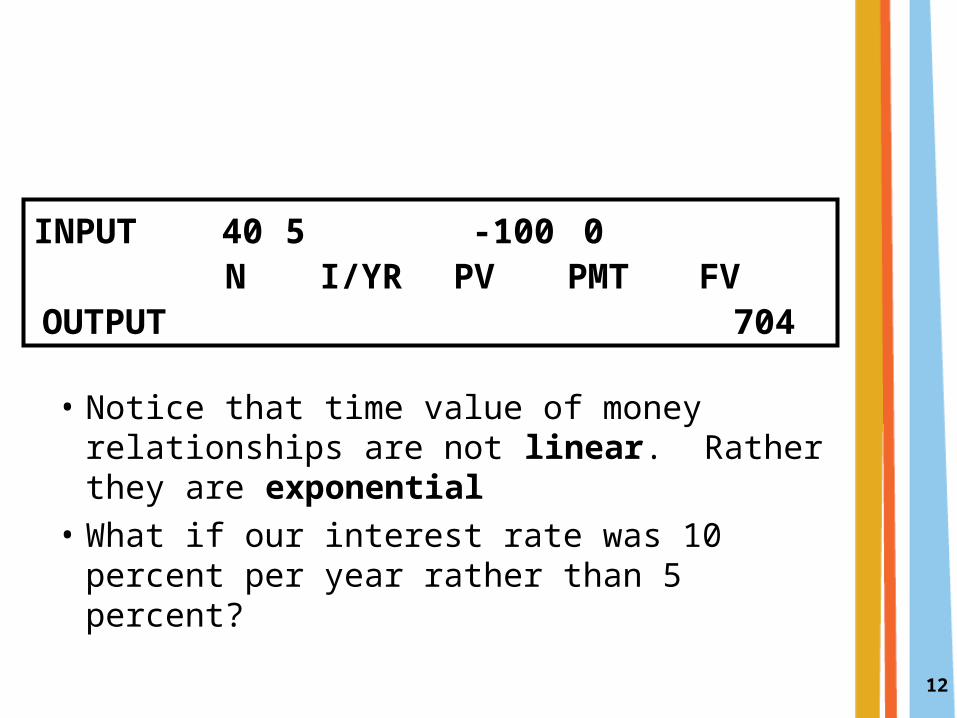

• Now let’s double the amount of time invested to 40 years. Will the future value be double as well?

INPUT 20 5 -100 0N I/YR PV PMT FV

OUTPUT 265.33

12

• Notice that time value of money relationships are not linear. Rather they are exponential

• What if our interest rate was 10 percent per year rather than 5 percent?

INPUT 40 5 -100 0N I/YR PV PMT FV

OUTPUT 704

13

• Does doubling the interest rate double the future value?

• Far from it! Because interest grows exponentially, even a small change in the interest rate causes the future value to change dramatically

INPUT 40 10 -100 0N I/YR PV PMT FV

OUTPUT 4,525.93

14

Present Value

• Watching money grow into the future (compounding) makes intuitive sense. Why would anyone care about finding the present value of a future cash flow, which uses the opposite process, called discounting?

• It may surprise you to learn that much of finance involves the application of present value. Finance is about valuing things, and that often means finding the present value of future cash flows.

15

Present Value

• Example: If I want to end up with $100 in an account at the end of one year at 5% per year, I would need to deposit how much?

$100 = PV x (1 + 5%)

$100 = PV (1.05)

PV= $95.24

16

In general: PV = FV /(1 + i)N

• This process is called discounting.

• Notice that this isn’t a new equation. It is really the same as the future value equation we saw before (just rearranged to solve for PV instead of FV)

17

Present Value

• Suppose we discount the deposit for two years?

PV = $100 / (1.05)2 = $90.70

• Suppose we discount for five years?

PV = $100 / (1.05)5 = $78.35

18

Financial Calculator Solution

INPUT 2 5 0 100N I/YR PV PMT FV

OUTPUT -90.70

19

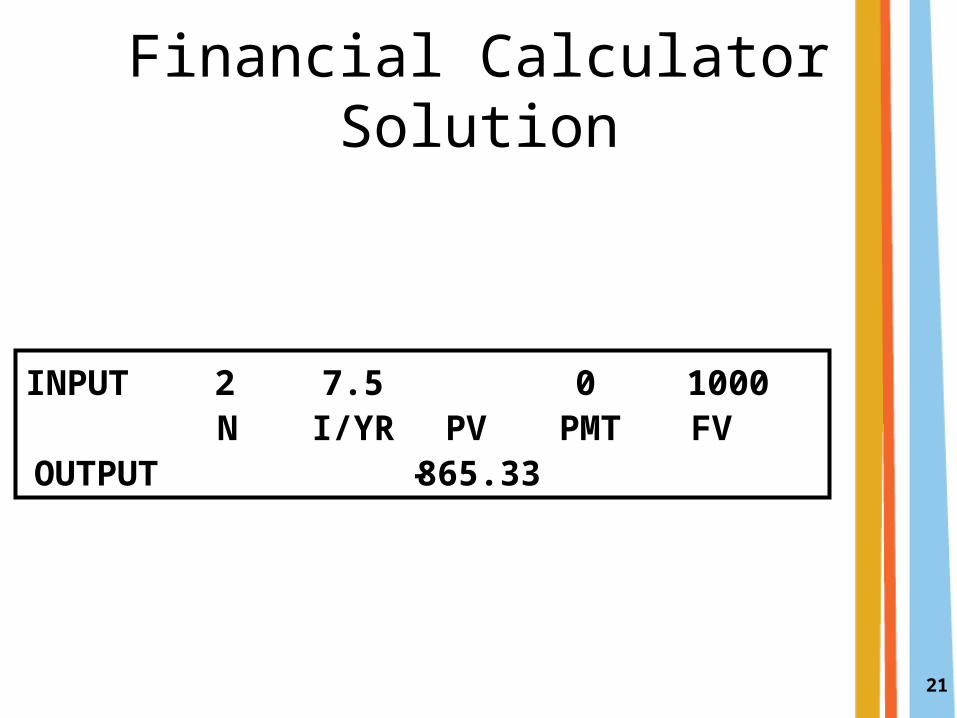

Example 4-3

• N = 2 years

• i = 7.5%

• FV = $1000 (value at the end of 2 years)

20

Example 4-3 (cont’d)

• PV = $1000 = $865.33

(1.075)2

21

Financial Calculator Solution

INPUT 2 7.5 0 1000N I/YR PV PMT FV

OUTPUT -865.33

22

Discounting with Multiple Rates

• Rather than using an exponent, we have to discount using the individual discount rates

• Example: the interest rates over the next three years are 7%, 8%, and 8.5%. What is the present value of $2,500 to be received at the end of the third year?

PV = $2,500 / [(1.07)(1.08)(1.085)]

= $1993.90

23

Using Present Value and Future Value

• Businesses often need to move cash flows around in time. That is no problem – we can use FV and PV to do that.

• Example: We expect to receive a cash flow of $200 at the end of 3 years. What is the value of the cash flow if we move it to year 2 using a discount rate of 6%?– We must discount the CF for one year.

PV2 = FV3 / (1 + i)1

= $200 / (1.06)= $188.68

24

• Now, what if we want to move the CF to year 5?

FV5 = PV3 x (1+ i)2

= $200 x (1.06)2

= $224.72

• Note: we could have also moved the $188.68 from the previous problem 3 years ahead to year 5 for the same answer

25

Computing Interest Rates

• So far we have solved for future values and present values

• If you look at your financial calculator, you will see that there are 5 variables used to solve these types of time value problems: – N, I, PV, PMT, and FV

• It turns out that we can solve for any one of the 5 variables if we know the other 4 variables– If we only know three variables there are an

infinite number of solutions

26

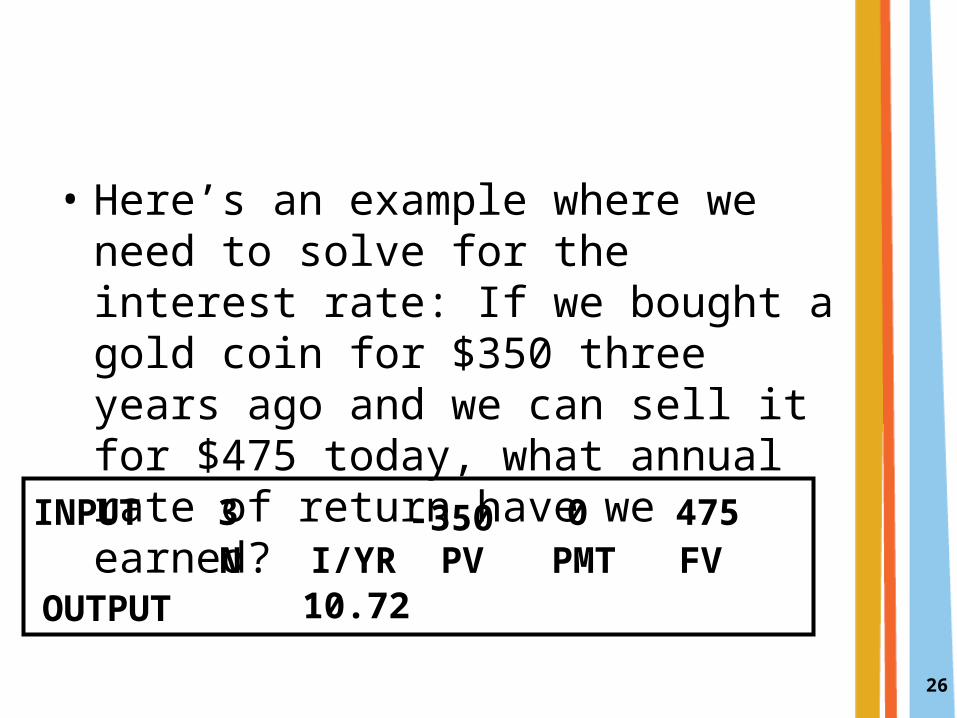

• Here’s an example where we need to solve for the interest rate: If we bought a gold coin for $350 three years ago and we can sell it for $475 today, what annual rate of return have we earned?

INPUT 3

10.72

0 475N I/YR PV PMT FV

OUTPUT

-350

27

• Note: what happens if you forget to make the present value a negative number?– You will get an “error” message on your

calculator– Either PV or FV must always be negative

28

Solving for Time

• Example 4-5: Suppose your company currently has sales of $350 million. If the company grows at 7 percent per year, how long will it take before the firm reaches $500 million in sales?

INPUT 7 -350 0 500N I/YR PV PMT FV

OUTPUT 5.27

29

Rule of 72

• We just solved a problem where we needed to know the amount of time to get from one cash flow level to another cash flow in the future at a certain growth rate.

• What if we needed to know how long it takes for the cash flow to double in size?

• We can calculate this directly using the technique we just learned.

• Alternatively, there is an approximation for this particular problem called the Rule of 72.

30

• The Rule of 72 is based on compounding and shows that the amount of time needed for an amount to double can be approximated by dividing 72 by the interest rate.

• For example, at 6% it should take 12 years for any amount to double.

• 12 years = 72/6

31

Rule of 72 (cont’d)

• How long would it take a sum to double if the growth rate was 4% per year? Use the Rule of 72?

32

Rule of 72 (cont’d)

• It would take 72/4 or 18 years.

• Using our calculator, we can solve for the amount exactly:

INPUT 4 -1 0 2N I/YR PV PMT FV

OUTPUT 17.67

33

• Notice that we don’t need to know the beginning or ending amount (we can just make our lives easy and use 1 and 2)

• The Rule of 72 is surprisingly accurate for small growth rates. As the rate gets very high the rule is pretty crummy (e.g. try 36 percent, or more dramatically 72 percent)

• The rule also works backwards: If we want to know how high our growth must be to double our sales in 10 years:– 72/10 = 7.2 years