chapter 4c depreciation

TRANSCRIPT

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 1/19

If you want to make your dreams come true,

the first thing you have to do is wake up

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 2/19

Depreciation

Chapter 4

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 3/19

Depreciation is an expense

Is an expense of the business and to be

charged to the profit and loss account to

reduce net profit

Depreciation = cost of buying - amount

received on disposal

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 4/19

Causes of Depreciation

Physical deterioration--

wear andtear; erosion, rust, rot and decay

Economic factors – obsolescence;inadequacy

The time factor –

lease, patent, theterm amortization is used instead ofdepreciation

Depletion – the wasting away of anasset as it is used up (due to the extractionof raw materials), e.g. natural resourcessuch as mines, quarries and oil wells

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 5/19

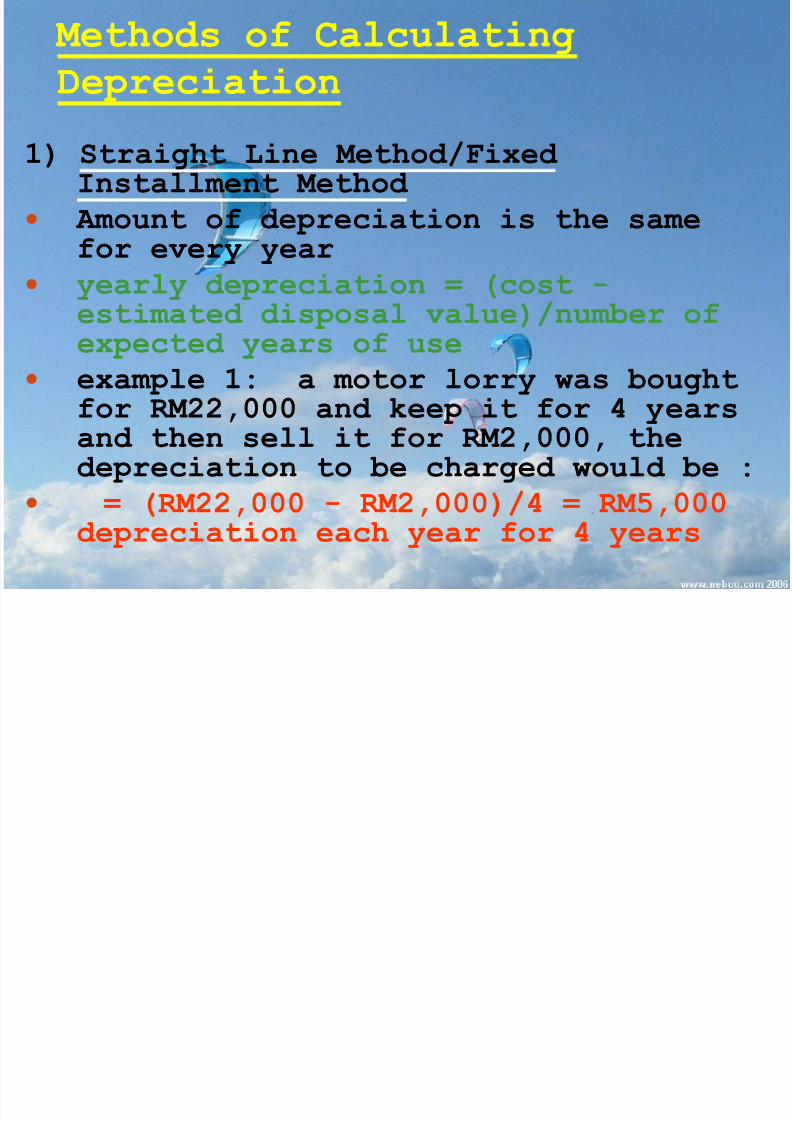

Methods of Calculating

Depreciation

1) Straight Line Method/Fixed Installment Method

Amount of depreciation is the samefor every year

yearly depreciation = (cost -estimated disposal value)/number ofexpected years of use

example 1: a motor lorry was bought

for RM22,000 and keep it for 4 yearsand then sell it for RM2,000, thedepreciation to be charged would be :

= (RM22,000 - RM2,000)/4 = RM5,000depreciation each year for 4 years

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 6/19

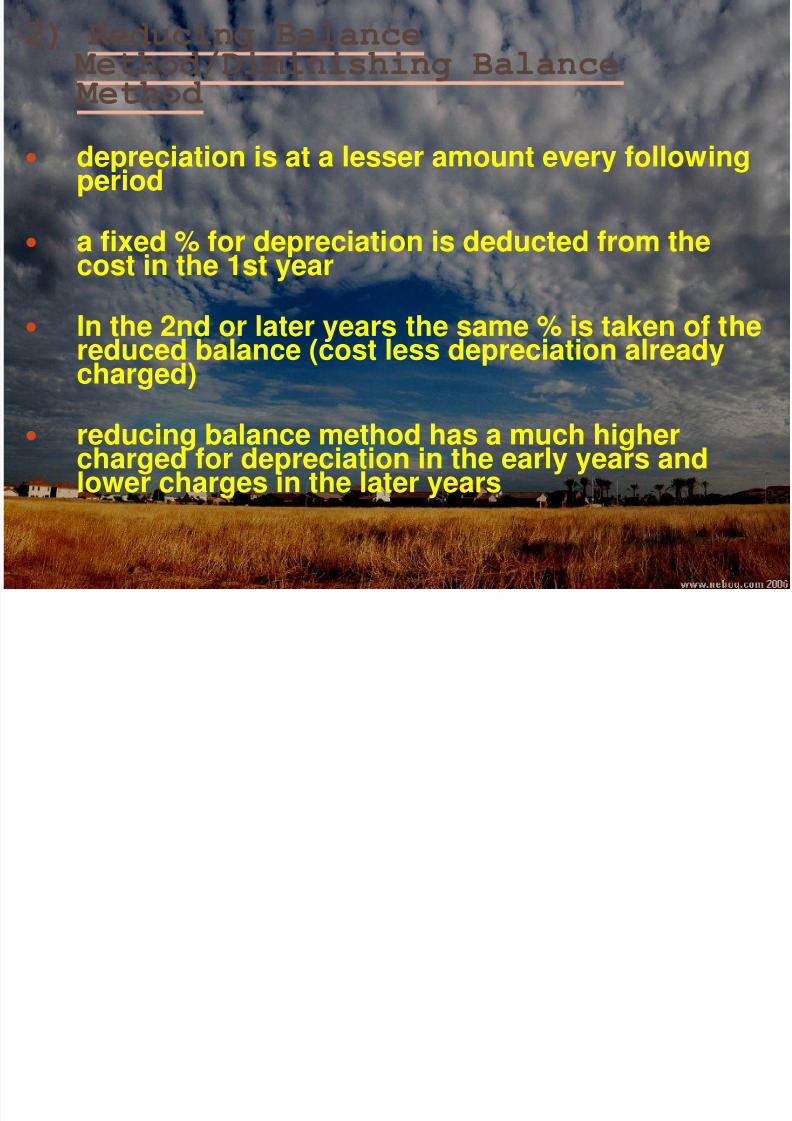

2) Reducing Balance Method/Diminishing Balance Method

depreciation is at a lesser amount every followingperiod

a fixed % for depreciation is deducted from the

cost in the 1st year

In the 2nd or later years the same % is taken of thereduced balance (cost less depreciation alreadycharged)

reducing balance method has a much highercharged for depreciation in the early years andlower charges in the later years

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 7/19

Example 2 A machine is bought for RM10,000 and

depreciation is to be charged at 20%,the calculations for the first three

years would be as follows:

Cost RM10,000

1st year: depreciation (20% of RM10,000) RM 2,000

RM 8,000

2nd year: depreciation (20% of RM8,000) RM 1,600

RM 6,400

3rd year: depreciation (20% of RM6,400) RM 1,280

Cost not yet apportioned, end of year 3 RM 5,120

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 8/19

3) Sum of the Years’ Digits provides for higher depreciation to be

charged early in thelife of an asset withlower depreciation inlater year

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 9/19

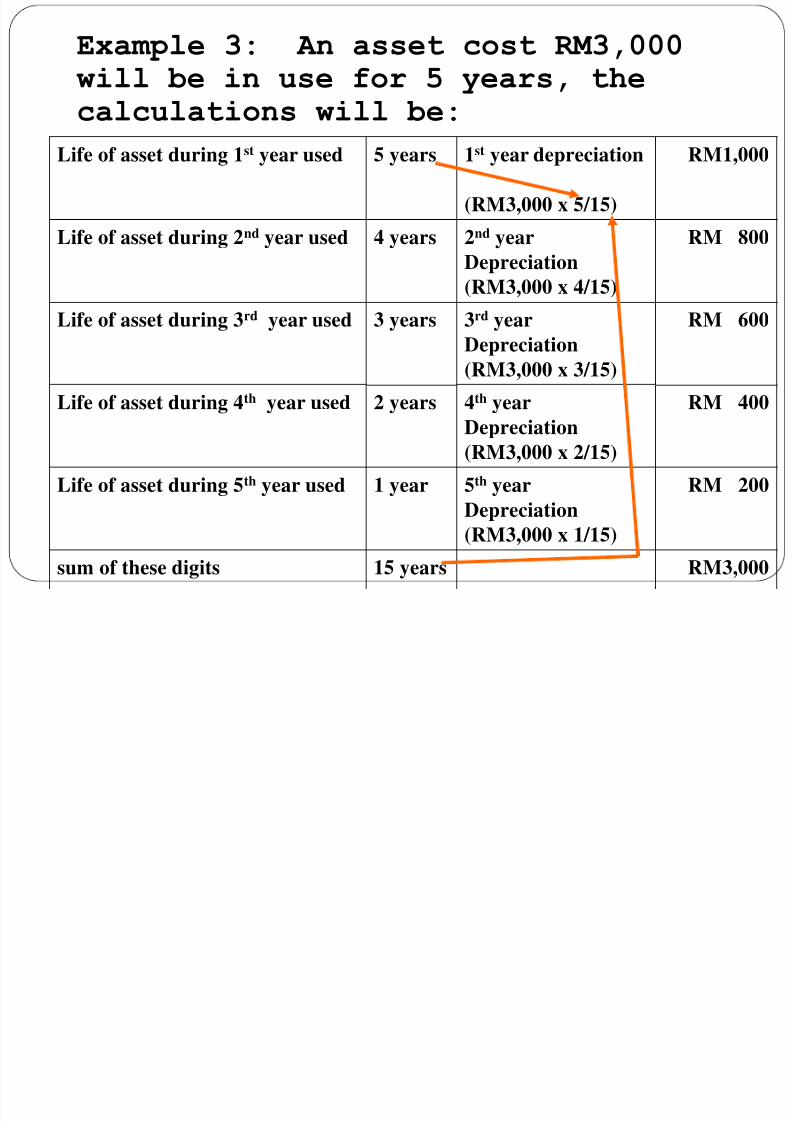

Example 3: An asset cost RM3,000 will be in use for 5 years, thecalculations will be:

Life of asset during 1st year used 5 years 1st year depreciation

(RM3,000 x 5/15)

RM1,000

Life of asset during 2nd year used 4 years 2nd year

Depreciation

(RM3,000 x 4/15)

RM 800

Life of asset during 3rd year used 3 years 3rd year

Depreciation

(RM3,000 x 3/15)

RM 600

Life of asset during 4th year used 2 years 4th year

Depreciation

(RM3,000 x 2/15)

RM 400

Life of asset during 5th year used 1 year 5th year

Depreciation

(RM3,000 x 1/15)

RM 200

sum of these digits 15 years RM3,000

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 10/19

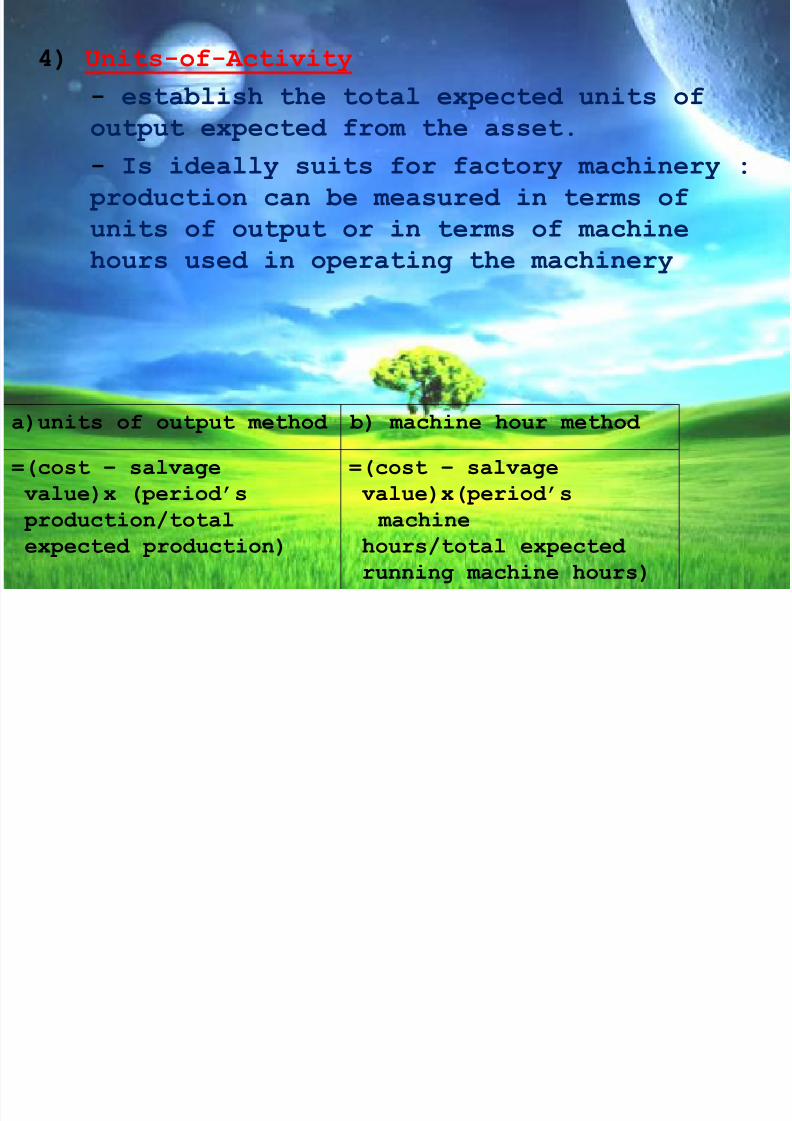

4) Units-of-Activity

- establish the total expected units of

output expected from the asset.- Is ideally suits for factory machinery :

production can be measured in terms of

units of output or in terms of machine

hours used in operating the machinery

a)units of output method b) machine hour method

=(cost – salvage

value)x (period’s

production/total

expected production)

=(cost – salvage

value)x(period’s

machine

hours/total expected running machine hours)

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 11/19

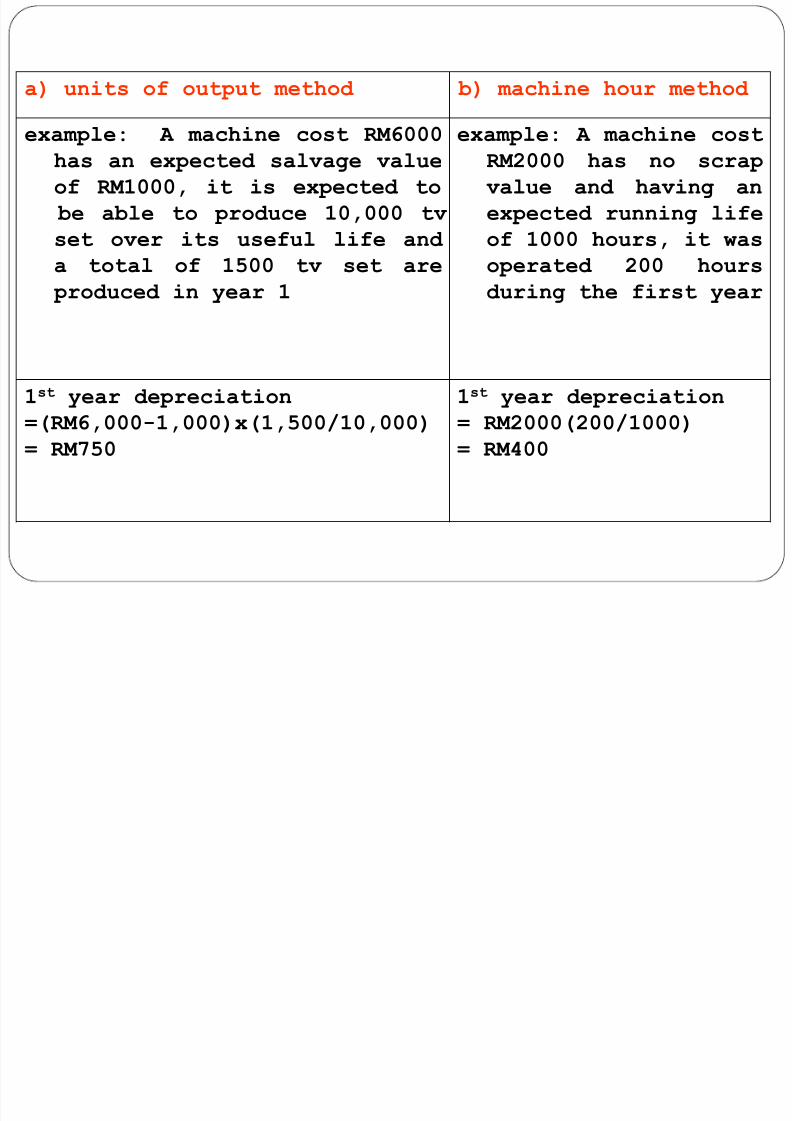

a) units of output method b) machine hour method

example: A machine cost RM6000has an expected salvage value

of RM1000, it is expected to

be able to produce 10,000 tv

set over its useful life and

a total of 1500 tv set are

produced in year 1

example: A machine costRM2000 has no scrap

value and having an

expected running life

of 1000 hours, it was

operated 200 hours

during the first year

1st year depreciation

=(RM6,000-1,000)x(1,500/10,000)= RM750

1st year depreciation

= RM2000(200/1000)= RM400

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 12/19

eprec a on rov s ons an Assets Bought or Sold

Ignore the dates during the year that the assets

were bought or sold , merely calculating a full

period’s depreciation on the assets in use at theend of the period

assets sold during the accounting period will have

had no provision for depreciation made for that

last period irrespective of how many months they

were in use i.e sold June 2006, so depreciation forJan – June can be ignored.

assets bought during the period will have a full

period of depreciation provision calculated even

though they may not have been owned throughout the

whole of the period i.e bought Nov 2006, sodepreciation charged from Jan – Dec 2006

Method of calculating depreciation provision

for assets bought or sold during an

accounting

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 13/19

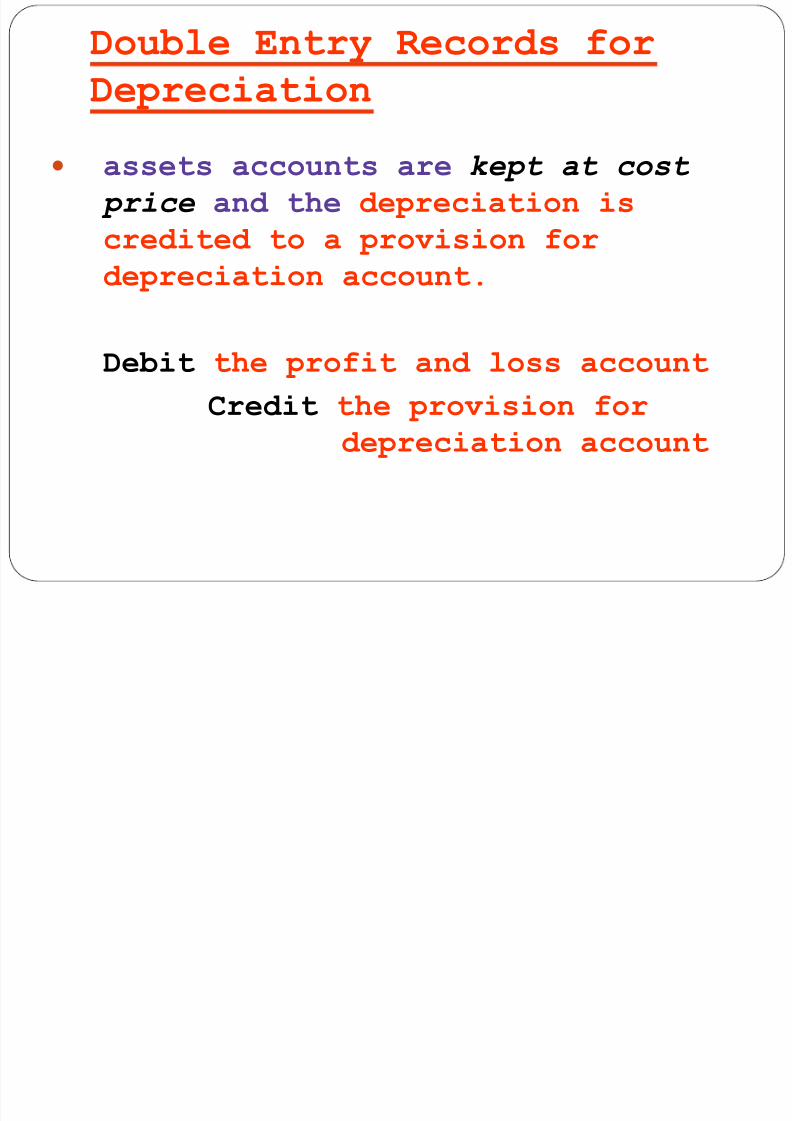

Double Entry Records for

Depreciation

assets accounts are kept at cost

price and the depreciation is

credited to a provision for

depreciation account.

Debit the profit and loss account

Credit

the provision fordepreciation account

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 14/19

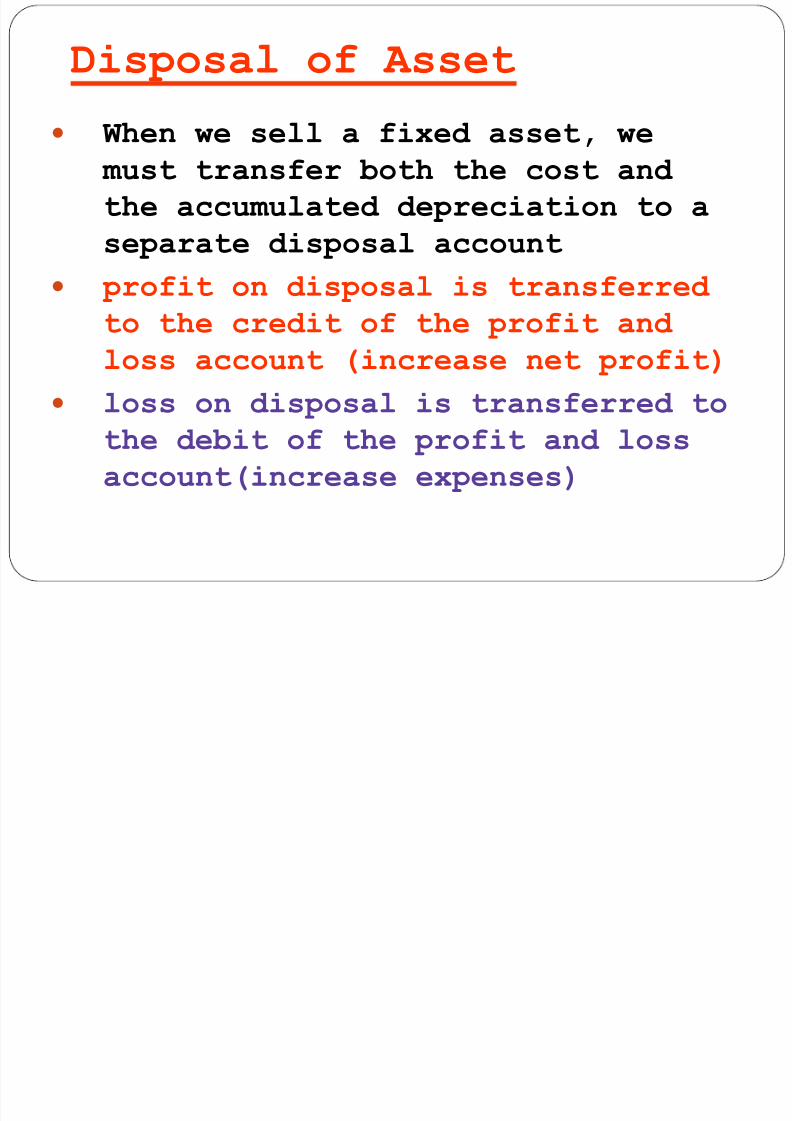

Disposal of Asset

When we sell a fixed asset, we must transfer both the cost and

the accumulated depreciation to a

separate disposal account

profit on disposal is transferred to the credit of the profit and

loss account (increase net profit)

loss on disposal is transferred tothe debit of the profit and loss

account(increase expenses)

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 15/19

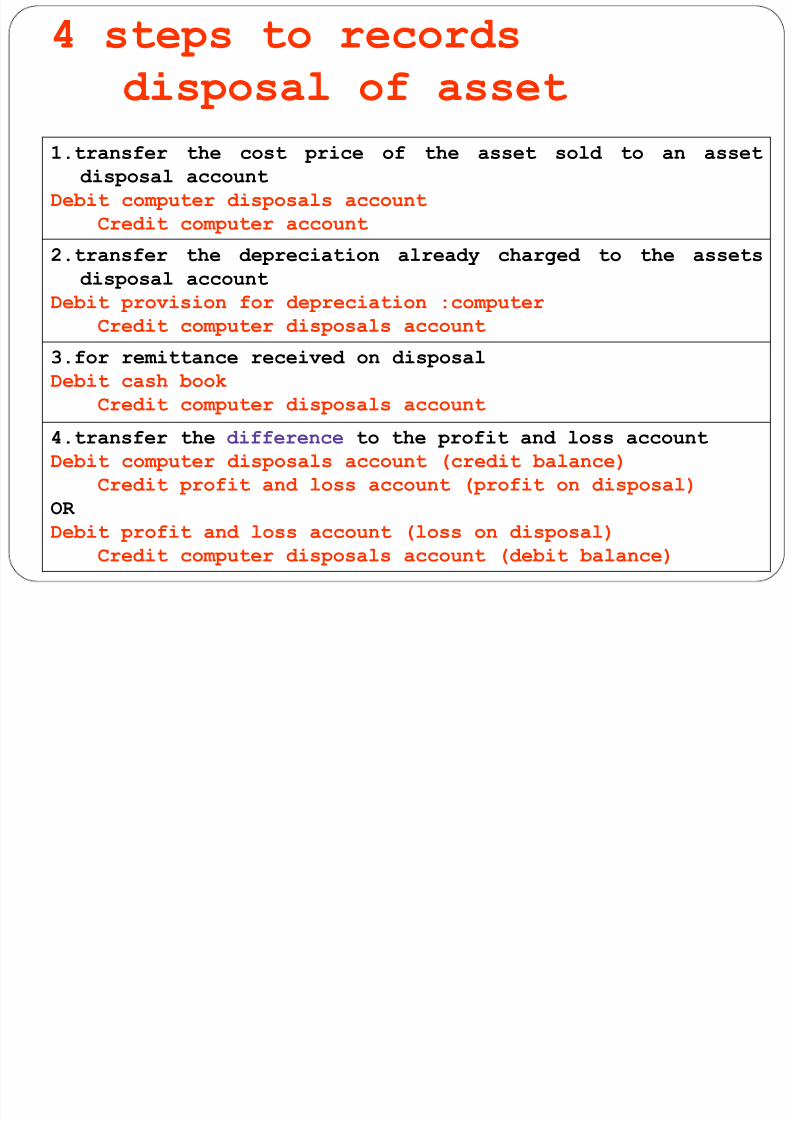

4 steps to records

disposal of asset

1.transfer the cost price of the asset sold to an asset

disposal account

Debit computer disposals account

Credit computer account

2.transfer the depreciation already charged to the assets

disposal accountDebit provision for depreciation :computer

Credit computer disposals account

3.for remittance received on disposal

Debit cash book

Credit computer disposals account

4.transfer the difference to the profit and loss account

Debit computer disposals account (credit balance)

Credit profit and loss account (profit on disposal)

OR

Debit profit and loss account (loss on disposal)

Credit computer disposals account (debit balance)

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 16/19

Accruals,

prepayments

and other

adjustments

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 17/19

Other Adjustments for Final

Accounts

Adjustments are needed so that theexpenses and income shown in thefinal accounts will equal theexpenses incurred in the period and

the revenue that has accrued. the balances caused by the

adjustments will be shown on the B/Sat the end of the period

example: The rent for building isRM6000 p.a. :

a) Firm A pays RM5000 in the year;

b) Firm B pays RM6500 in the year

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 18/19

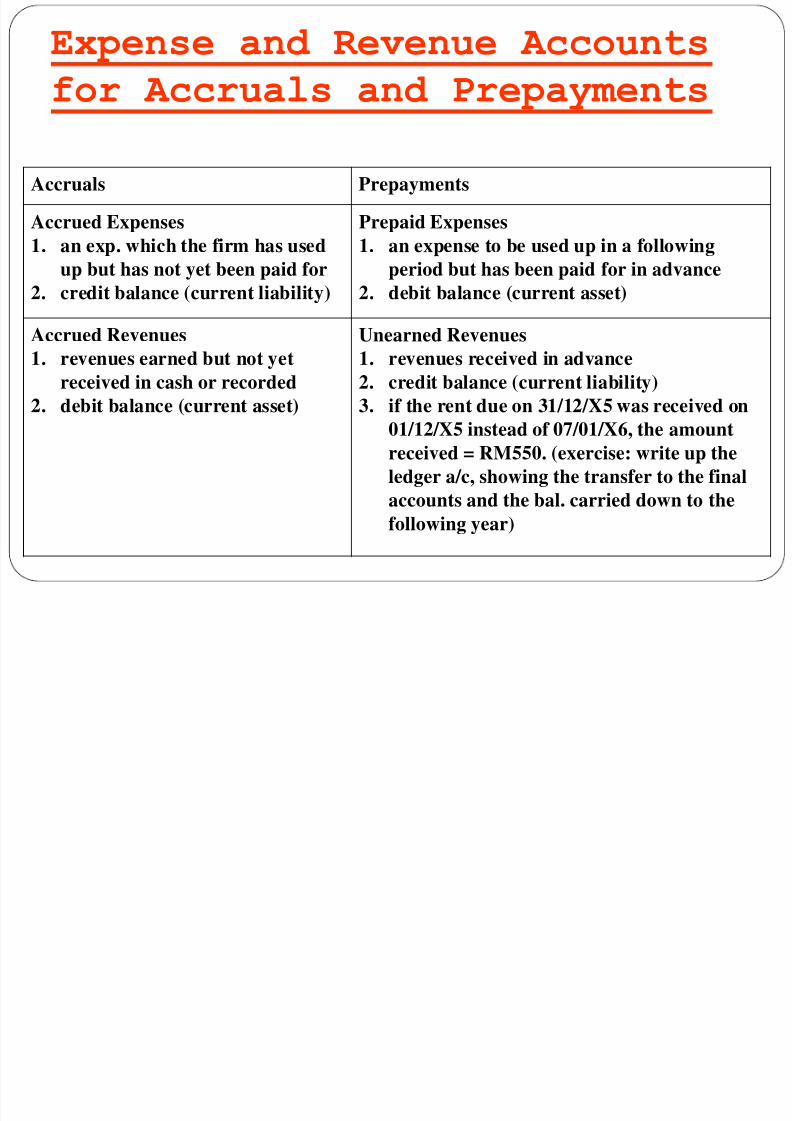

Expense and Revenue Accounts

for Accruals and Prepayments

Accruals Prepayments

Accrued Expenses

1. an exp. which the firm has used

up but has not yet been paid for2. credit balance (current liability)

Prepaid Expenses

1. an expense to be used up in a following

period but has been paid for in advance2. debit balance (current asset)

Accrued Revenues

1. revenues earned but not yet

received in cash or recorded

2. debit balance (current asset)

Unearned Revenues

1. revenues received in advance

2. credit balance (current liability)

3. if the rent due on 31/12/X5 was received on

01/12/X5 instead of 07/01/X6, the amount

received = RM550. (exercise: write up the

ledger a/c, showing the transfer to the final

accounts and the bal. carried down to the

following year)

8/2/2019 Chapter 4c Depreciation

http://slidepdf.com/reader/full/chapter-4c-depreciation 19/19

Teachers open the door. You

enter by yourself