copyright oxford university press 2009 chapter 11 depreciation

TRANSCRIPT

Copyright Oxford University Press 2009

Chapter 11Depreciation

Copyright Oxford University Press 2009

• Basic Aspects of Depreciation• Historical Depreciation Methods• Modified Accelerated Cost Recovery

System (MACRS)• Depreciation and Asset Disposal• Unit-of-Production Depreciation• Depletion• Spreadsheets and Depreciation

Chapter Outline

Copyright Oxford University Press 2009

• Understand the concepts of depreciation, deterioration, and obsolescence

• Use historical and MACRS to calculate annual depreciation charge and book value over the asset’s life

• Account for capital gains/losses, ordinary losses, and depreciation recapture due to the disposal of a depreciated asset

• Use unit-of-production and depletion depreciation methods in economic analysis

• Use spreadsheets to calculate depreciation

Learning Objectives

Copyright Oxford University Press 2009

• Decline in market value of an asset due to deterioration or obsolescence

• Decline in value of an asset to its owner• Systematic allocation of an asset’s cost over its

useful or depreciable life (accountant’s definition)

Basic Aspects of Depreciation

Copyright Oxford University Press 2009

Expenses:• Part of regular business operations• “Consumed” over short period of time• Sometimes recurring• Do not lose value gradually over time• Subtracted from business revenues as they

occur• Reduce income taxes as they can be written off

when they occur• Examples: labor, utilities, materials, insurance,…

Depreciation and Expenses

Copyright Oxford University Press 2009

Depreciation:• Business costs due to capital assets are not fully

written off when they occur• Capital assets lose value gradually over time • Capital cost must be written off or depreciated

over its depreciable life or recovery period• Reduce the taxable income, and thus reduce

income taxes as they were written off• It is a non-cash cost• Examples: building, plants, machines,…

Depreciation and Expenses

Copyright Oxford University Press 2009

A property is depreciable If:• The property must be used for business purposes

to produce income.• The property must have a useful life that can be

determined, and the useful life must be longer than one year.

• The property must be an asset that decays, gets used up, wears out, becomes obsolete, or loses value to the owner from natural causes.

Only the owner of property may claim depreciation expenses

Basic Requirements for Depreciation

Copyright Oxford University Press 2009

Tangible property: can be seen, touched, and felt.• Real property: land, buildings, and things growing on,

built upon, constructed on, or attached to the land• Personal property: equipment, furnishings, vehicles,

office machinery, and anything that is tangible excluding real property

Intangible property: has value but cannot be directly seen or touched, examples include patents, copyrights, and trademarks, trade names, and franchises.

Types of Property

Copyright Oxford University Press 2009

• Almost all tangible property can be depreciated except land, factory inventory, containers considered as inventory, and leased property.

• Tangible property used in both business and personal activities can be depreciated, but only in proportion to the use for business purposes.

• Intangible property can generally be depreciated.

Property and Depreciation

Copyright Oxford University Press 2009

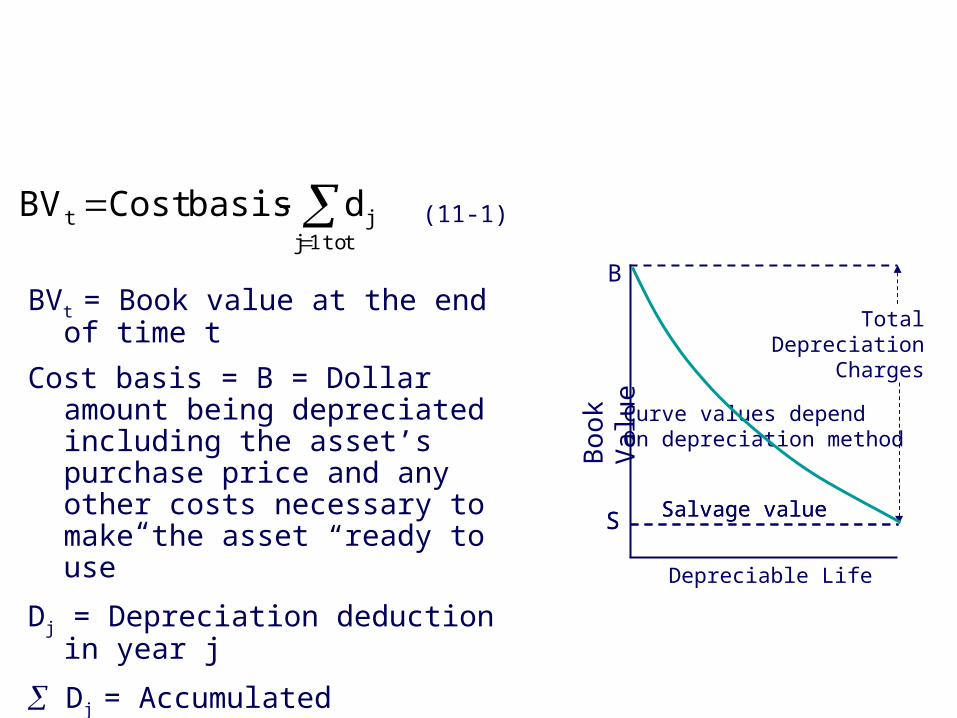

Depreciation Calculation Fundamentals

t to 1j

jt d-basis CostBV (11-1)

BVt = Book value at the end of time t

Cost basis = B = Dollar amount being depreciated including the asset’s purchase price and any other costs necessary to make the asset “ready to use”

Dj = Depreciation deduction in year j

Dj = Accumulated depreciation charges from time 1 to j

Bo

ok V

alu

e

B

Depreciable Life

Curve values dependOn depreciation method

TotalDepreciation

Charges

S Salvage valueS Salvage value

Copyright Oxford University Press 2009

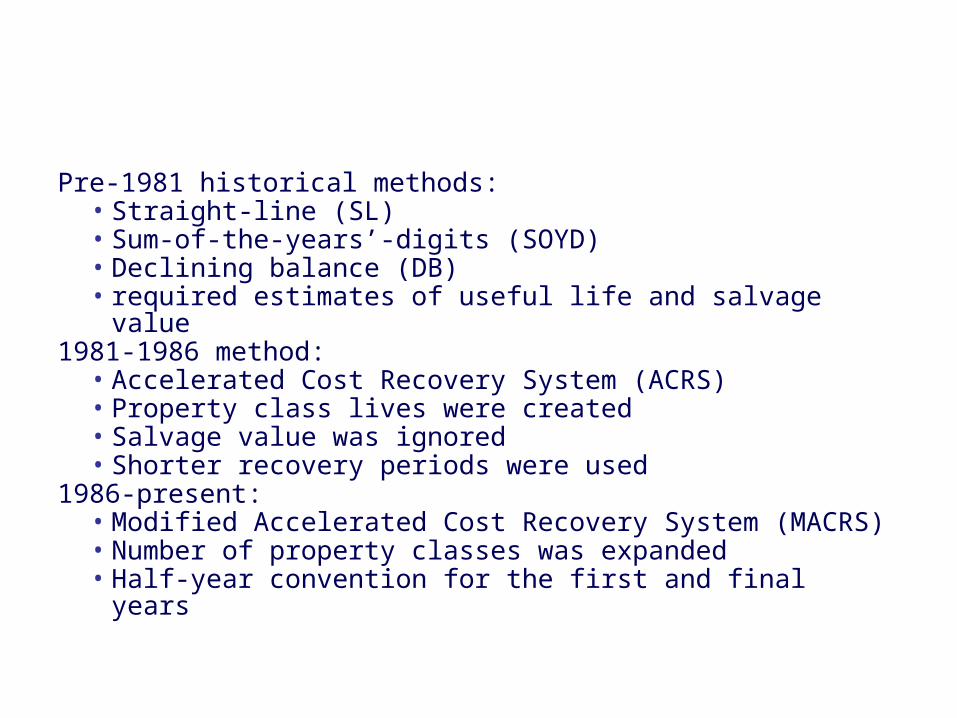

Pre-1981 historical methods:• Straight-line (SL)• Sum-of-the-years’-digits (SOYD)• Declining balance (DB)• required estimates of useful life and salvage value

1981-1986 method: • Accelerated Cost Recovery System (ACRS)• Property class lives were created• Salvage value was ignored• Shorter recovery periods were used

1986-present: • Modified Accelerated Cost Recovery System (MACRS)• Number of property classes was expanded • Half-year convention for the first and final years

Depreciation Methods

Copyright Oxford University Press 2009

Historical Depreciation Methods

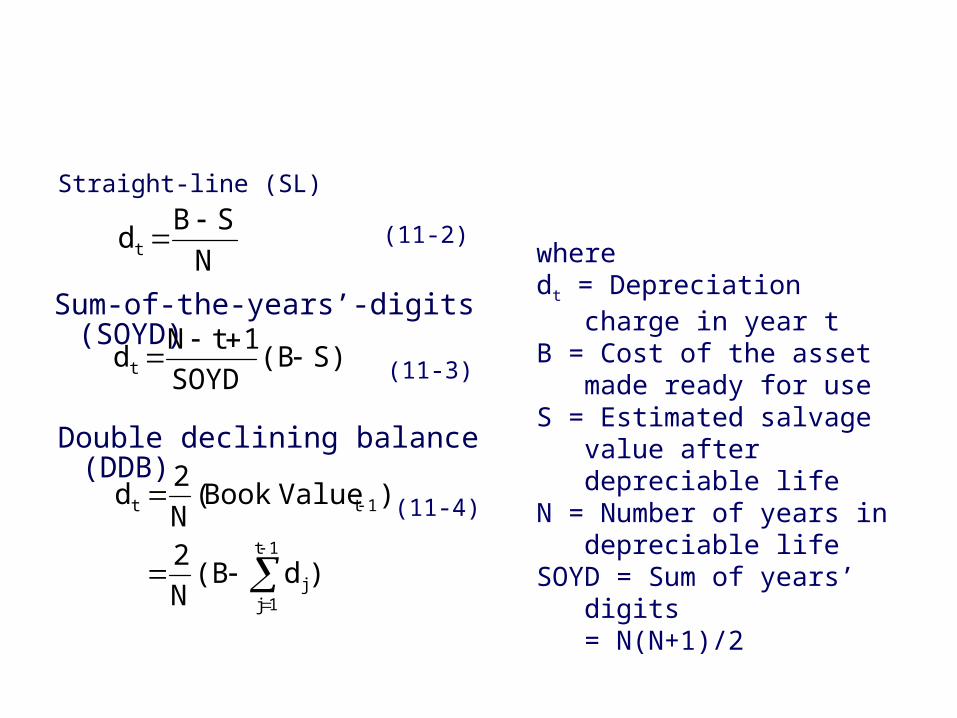

Straight-line (SL)

N

SBdt

Sum-of-the-years’-digits (SOYD)

Double declining balance (DDB)

(11-2)

S)(BSOYD

1tNdt

(11-3)

)d(BN

2

)ValueBook(N

2d

1t

1jj

1tt

(11-4)

wheredt = Depreciation charge in

year tB = Cost of the asset made

ready for useS = Estimated salvage value

after depreciable lifeN = Number of years in

depreciable lifeSOYD = Sum of years’ digits

= N(N+1)/2

Copyright Oxford University Press 2009

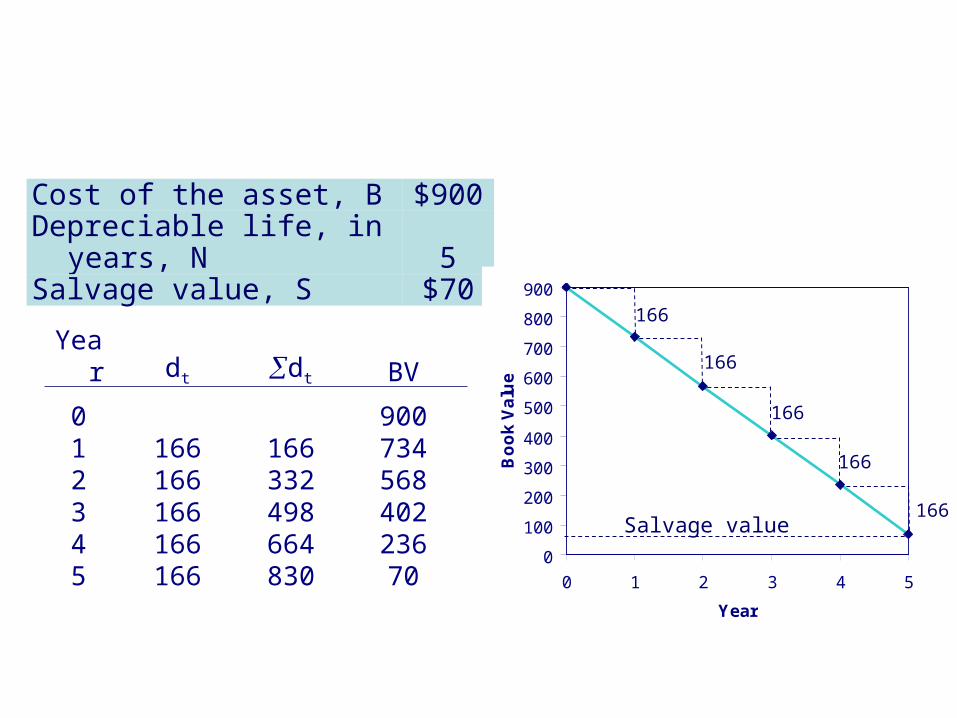

Example 11-2 SL Depreciation

Cost of the asset, B $900Depreciable life, in years, N 5Salvage value, S $70

0

100

200

300

400

500

600

700

800

900

0 1 2 3 4 5

Year

Bo

ok

Va

lue

166

166

166

166

166Salvage value

Year dt dt BV

0 9001 166 166 7342 166 332 5683 166 498 4024 166 664 2365 166 830 70

Copyright Oxford University Press 2009

Example 11-3 SOYD Depreciation

Cost of the asset, B $900Depreciable life, in years, N 5Salvage value, S $70

Year dt dt BV

0 $900.001 $276.67 $276.67 623.332 221.33 498.00 402.003 166.00 664.00 236.004 110.67 774.67 125.335 55.33 830.00 70.00

0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

0 1 2 3 4 5

Year

Bo

ok

Va

lue

277

221

166

111

55Salvage value

Copyright Oxford University Press 2009

Example 11-4 DDB Depreciation

Cost of the asset, B $900Depreciable life, in years, N 5Salvage value, S $70

Year dt dt BV

0 900.001 360.00 360.00 540.002 216.00 576.00 324.003 129.60 705.60 194.404 77.76 783.36 116.645 46.66 830.02 69.98 0.00

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

0 1 2 3 4 5

Year

Bo

ok

Va

lue

360

216

130

7847Salvage value

Copyright Oxford University Press 2009

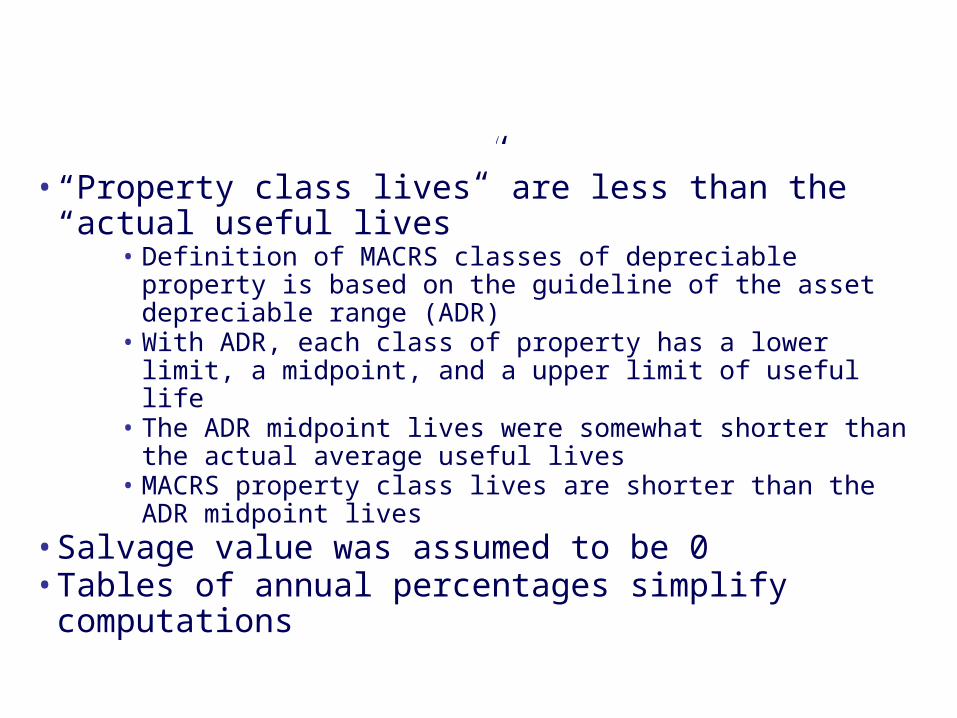

• “Property class lives” are less than the “actual useful lives”

• Definition of MACRS classes of depreciable property is based on the guideline of the asset depreciable range (ADR)

• With ADR, each class of property has a lower limit, a midpoint, and a upper limit of useful life

• The ADR midpoint lives were somewhat shorter than the actual average useful lives

• MACRS property class lives are shorter than the ADR midpoint lives

• Salvage value was assumed to be 0• Tables of annual percentages simplify computations

Advantages of Modified Accelerated Cost Recovery System

Copyright Oxford University Press 2009

• General Depreciation System (GDS)• Based on declining balance with switch to straight-line

depreciation• Alternative Depreciation System (ADS)

• ADS provides a longer recovery period and uses straight-line depreciation

• ADS must be used for • Tangible property used primarily outside the United States• Property that is tax exempt or financed by tax-exempt bonds• Farming property placed in service when uniform capitalization

rules are not applied• ADS may be elected for an asset, it is not possible to

switch back to the GDS.

Modified Accelerated Cost Recovery System (MACRS)

Copyright Oxford University Press 2009

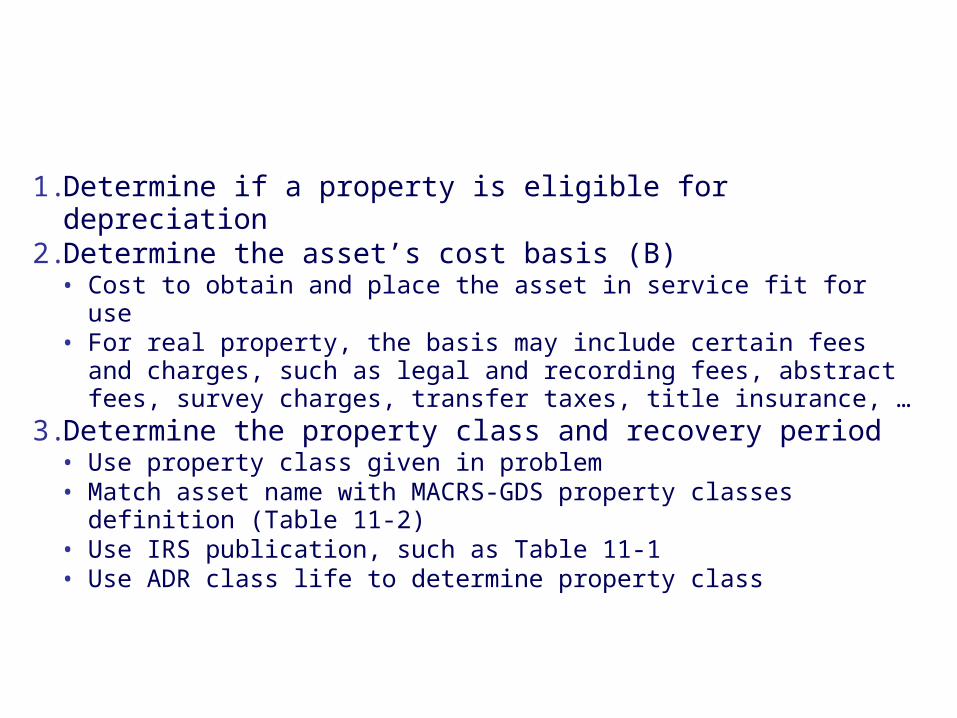

1. Determine if a property is eligible for depreciation2. Determine the asset’s cost basis (B)

• Cost to obtain and place the asset in service fit for use• For real property, the basis may include certain fees and

charges, such as legal and recording fees, abstract fees, survey charges, transfer taxes, title insurance, …

3. Determine the property class and recovery period• Use property class given in problem• Match asset name with MACRS-GDS property classes

definition (Table 11-2)• Use IRS publication, such as Table 11-1• Use ADR class life to determine property class

Procedures in Applying MACRS-GDS Depreciation

Copyright Oxford University Press 2009

Applying MACRS-GDS Depreciation

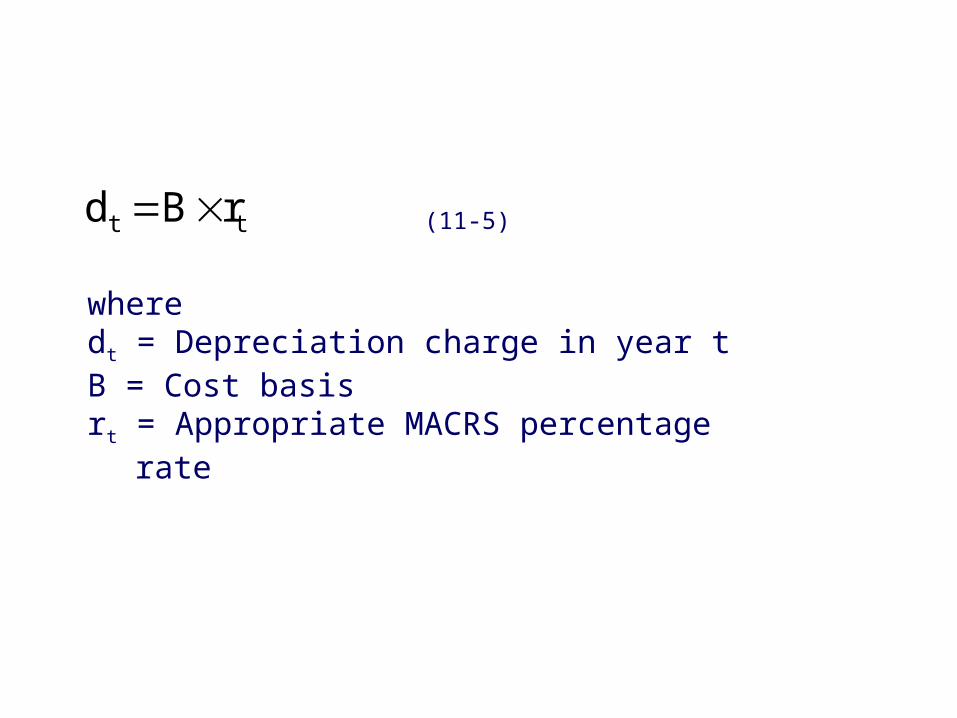

tt rBd (11-5)

wheredt = Depreciation charge in year tB = Cost basisrt = Appropriate MACRS percentage rate

Copyright Oxford University Press 2009

Table 11-1 Example Class Lives and MACRS Property Classes

IRS Asset Class

Asset DescriptionClass Life

(years)ADR

MACRS Property Class (years)

GDS ADS

00.11 Office furniture, fixtures, and equipment 10 7 1000.12 Information Systems: computer/peripheral 6 5 600.22 Automobiles, taxis 3 5 500.241 Light general-purpose trucks 4 5 500.25 Railroad cars and locomotives 15 7 1500.40 Industrial steam and electric distribution 22 15 2201.11 Cotton gin assets 12 7 1201.21 Cattle, breeding or dairy 7 5 713.00 Offshore drilling assets 7.5 5 7.513.30 Petroleum refining assets 16 10 1615.00 Construction assets 6 5 6

Copyright Oxford University Press 2009

Table 11-1 Example Class Lives and MACRS Property Classes

IRS Asset Class

Asset DescriptionClass Life

(years)ADR

MACRS Property Class (years)

GDS ADS

21.10 Manufacture of grain and grain mill products 17 10 1722.2 Manufacture of yarn, thread, and woven fabric 11 7 1124.10 Cutting of timber 6 5 632.20 Manufacture of cement 20 15 2037.11 Manufacture of motor vehicles 12 7 1248.11 Telephone Communications assets and buildings 24 15 2448.2 Radio and television broadcasting equipment 6 5 649.12 Electric utility nuclear production plant 20 15 2049.13 Electric utility steam production plant 28 20 2849.23 Natural gas production plant 14 7 1450.00 Municipal wastewater treatment plant 24 15 2480.00 Theme and amusement park assets 12.5 7 12.5

Copyright Oxford University Press 2009

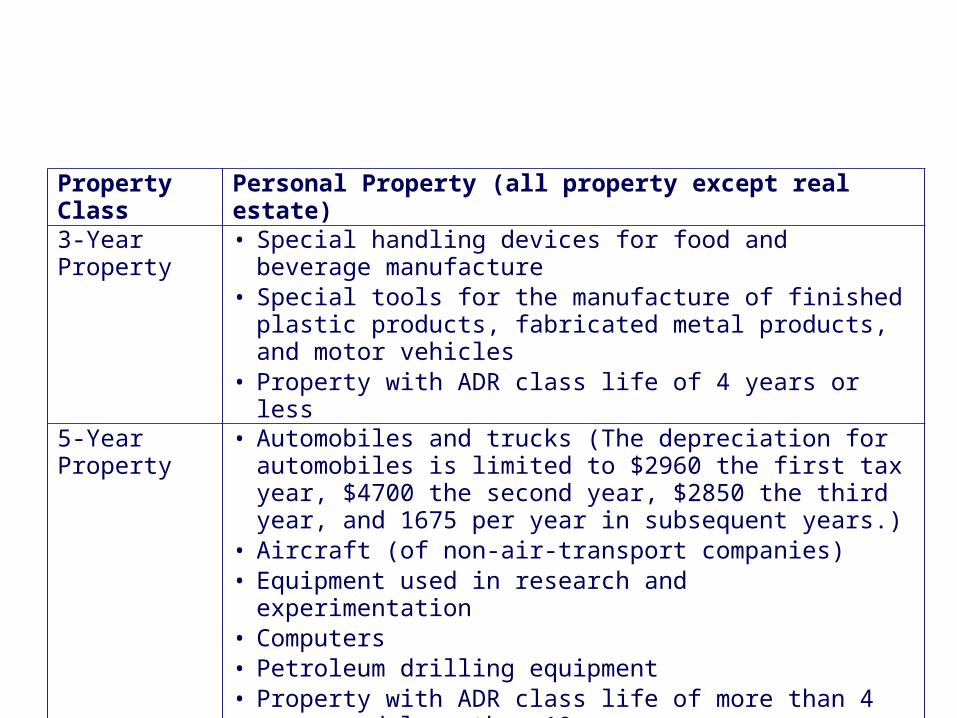

Table 11-2 MACRS GDS Property Classes

Property Class Personal Property (all property except real estate)3-Year Property • Special handling devices for food and beverage manufacture

• Special tools for the manufacture of finished plastic products, fabricated metal products, and motor vehicles

• Property with ADR class life of 4 years or less5-Year Property • Automobiles and trucks (The depreciation for automobiles is limited to

$2960 the first tax year, $4700 the second year, $2850 the third year, and 1675 per year in subsequent years.)

• Aircraft (of non-air-transport companies)• Equipment used in research and experimentation• Computers• Petroleum drilling equipment• Property with ADR class life of more than 4 years and less than 10 years

7-Year Property • All other property not assigned to another class• Office furniture, fixtures, and equipment• Property with ADR class life of 10 years or more and less than 16 years

Copyright Oxford University Press 2009

Table 11-2 MACRS GDS Property Classes

Property Class Personal Property (all property except real estate)10-Year Property • Assets used in petroleum refining and certain food products

• Vessels and water transportation equipment • Property with ADR class life of 16 years or more and less than 20 years

15-Year Property • Telephone distribution plants • Municipal sewage treatment plants • Property with ADR class life of 20 years or more and less than 25 years

20-Year Property • Municipal sewers • Property with ADR class life of 25 years or more

Property Class Real Property (real estate)27.5 Year Residential rental property (does not include hotels and motels)

39 Years Nonresidential real property

Copyright Oxford University Press 2009

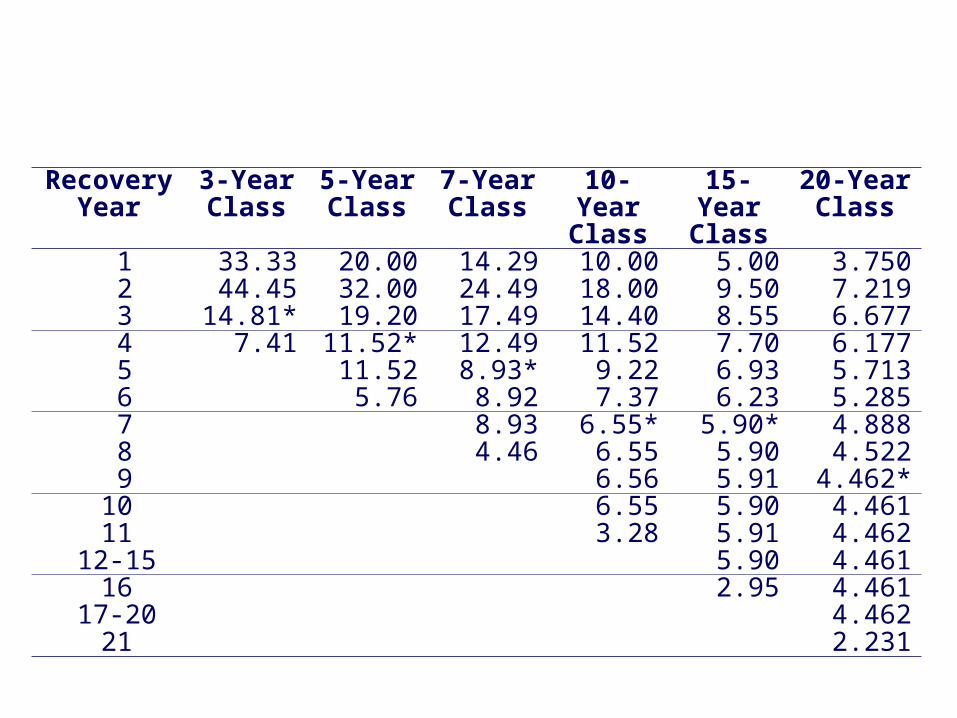

Table 11-3 MACRS GDS Percentage Rate

Recovery Year

3-YearClass

5-YearClass

7-YearClass

10-Year Class

15-Year Class

20-Year Class

1 33.33 20.00 14.29 10.00 5.00 3.750 2 44.45 32.00 24.49 18.00 9.50 7.219 3 14.81* 19.20 17.49 14.40 8.55 6.677 4 7.41 11.52* 12.49 11.52 7.70 6.177 5 11.52 8.93* 9.22 6.93 5.713 6 5.76 8.92 7.37 6.23 5.285 7 8.93 6.55* 5.90* 4.888 8 4.46 6.55 5.90 4.522 9 6.56 5.91 4.462* 10 6.55 5.90 4.461 11 3.28 5.91 4.462

12-15 5.90 4.461 16 2.95 4.461

17-20 4.462 21 2.231

Copyright Oxford University Press 2009

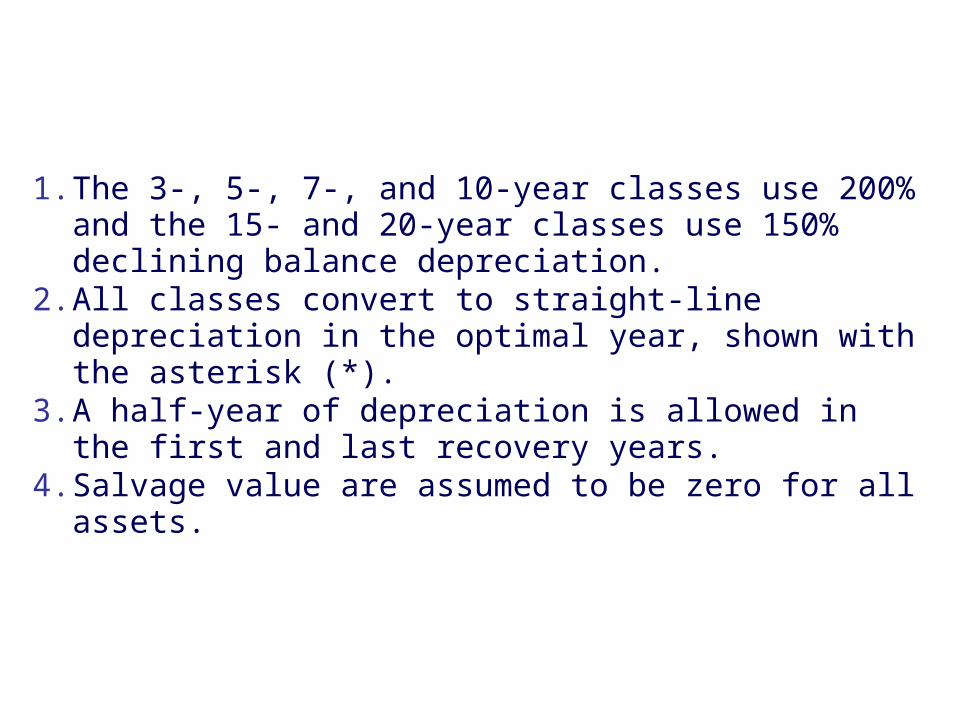

1. The 3-, 5-, 7-, and 10-year classes use 200% and the 15- and 20-year classes use 150% declining balance depreciation.

2. All classes convert to straight-line depreciation in the optimal year, shown with the asterisk (*).

3. A half-year of depreciation is allowed in the first and last recovery years.

4. Salvage value are assumed to be zero for all assets.

Calculation of MACRS GDS Percentages

Copyright Oxford University Press 2009

Table 11-4 MACRS GDS Percentage Rate

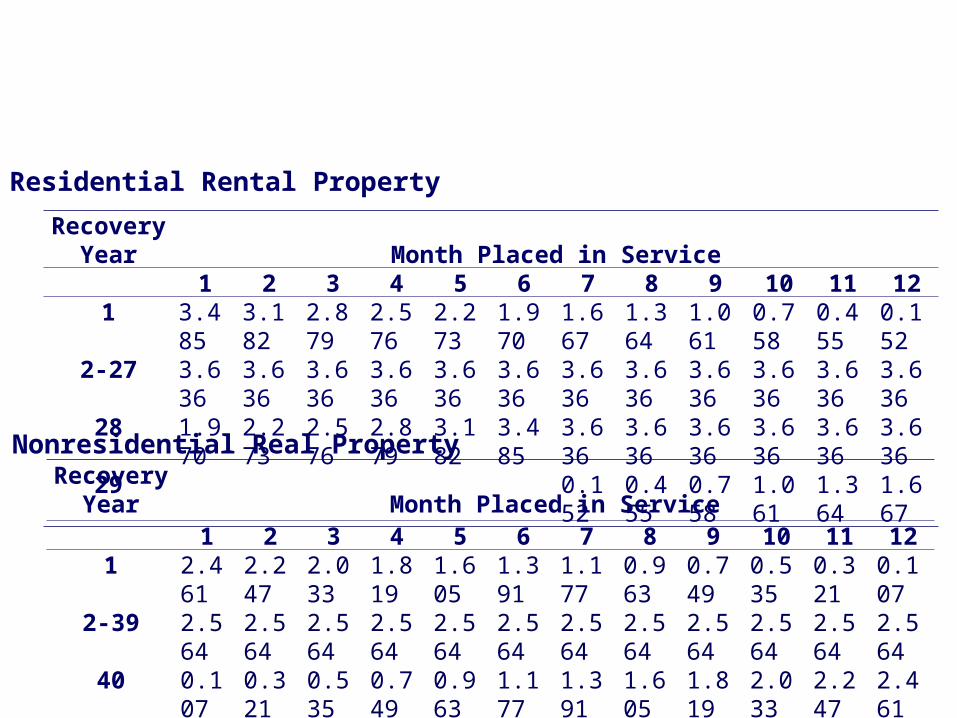

Residential Rental Property

RecoveryYear Month Placed in Service

1 2 3 4 5 6 7 8 9 10 11 121 3.485 3.182 2.879 2.576 2.273 1.970 1.667 1.364 1.061 0.758 0.455 0.152

2-27 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.636 3.63628 1.970 2.273 2.576 2.879 3.182 3.485 3.636 3.636 3.636 3.636 3.636 3.63629 0.152 0.455 0.758 1.061 1.364 1.667

RecoveryYear Month Placed in Service

1 2 3 4 5 6 7 8 9 10 11 121 2.461 2.247 2.033 1.819 1.605 1.391 1.177 0.963 0.749 0.535 0.321 0.107

2-39 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.564 2.56440 0.107 0.321 0.535 0.749 0.963 1.177 1.391 1.605 1.819 2.033 2.247 2.461

Nonresidential Real Property

Copyright Oxford University Press 2009

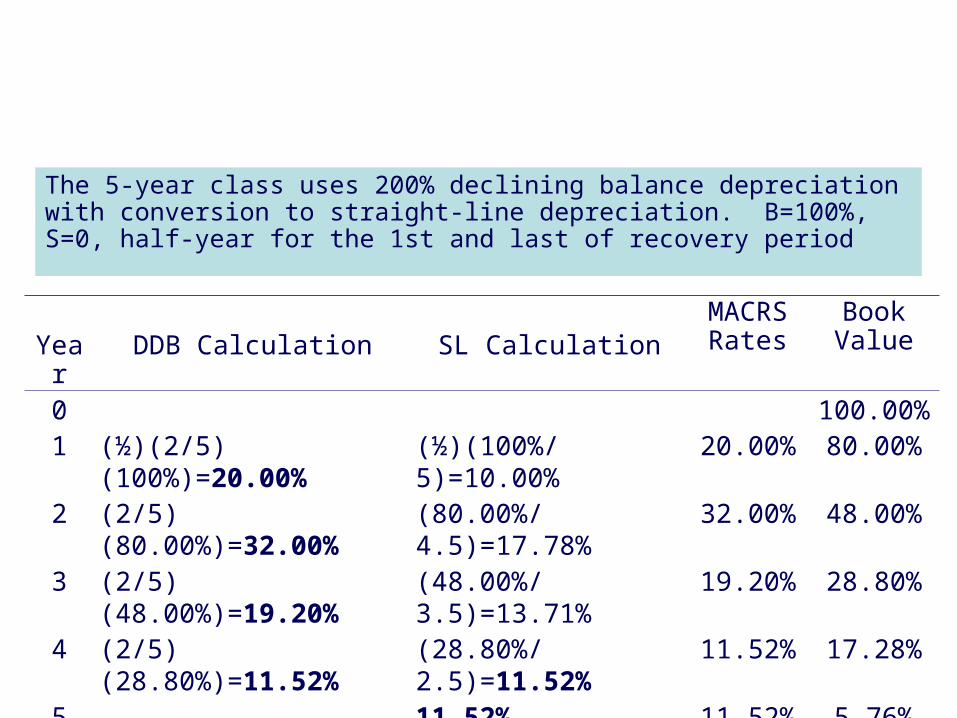

Example 11-5 Calculation of MACRS GDS Percentages

The 5-year class uses 200% declining balance depreciation with conversion to straight-line depreciation. B=100%, S=0, half-year for the 1st and last of recovery period

Year DDB Calculation SL CalculationMACRS Rates

Book Value

0 100.00%1 (½)(2/5)

(100%)=20.00%(½)(100%/5)=10.00%

20.00% 80.00%

2 (2/5)(80.00%)=32.00%

(80.00%/4.5)=17.78%

32.00% 48.00%

3 (2/5)(48.00%)=19.20%

(48.00%/3.5)=13.71%

19.20% 28.80%

4 (2/5)(28.80%)=11.52%

(28.80%/2.5)=11.52%

11.52% 17.28%

5 11.52% 11.52% 5.76%6 (½)11.52%=5.76% 5.76% 0.00%

Copyright Oxford University Press 2009

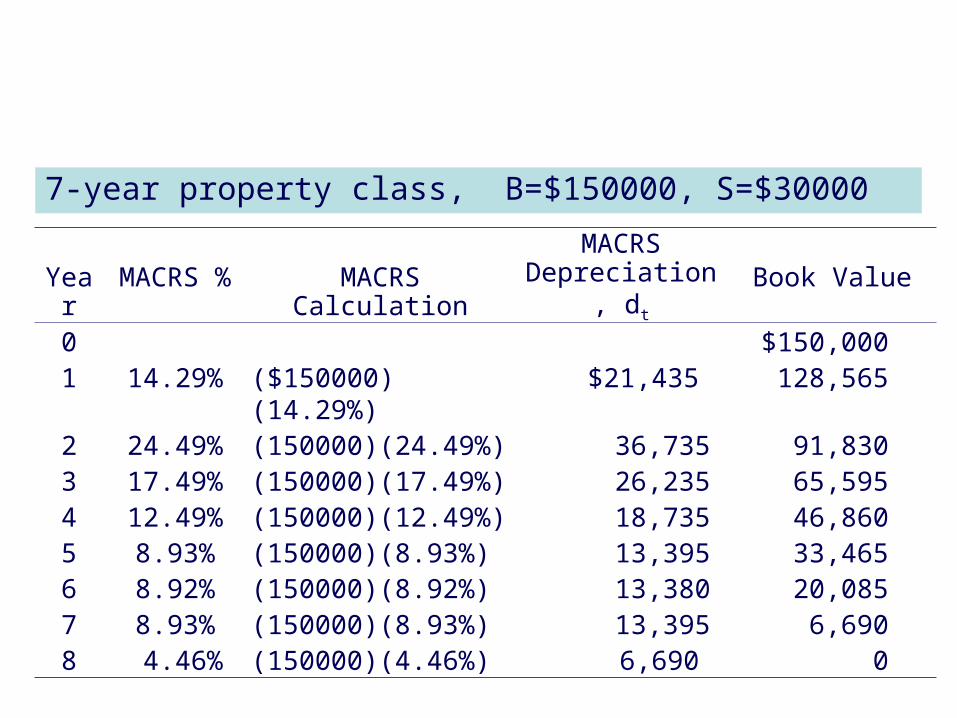

Example 11-6 Calculation of MACRS GDS Depreciation

7-year property class, B=$150000, S=$30000

Year MACRS % MACRS CalculationMACRS

Depreciation, dt Book Value0 $150,0001 14.29% ($150000)(14.29%) $21,435 128,5652 24.49% (150000)(24.49%) 36,735 91,8303 17.49% (150000)(17.49%) 26,235 65,5954 12.49% (150000)(12.49%) 18,735 46,8605 8.93% (150000)(8.93%) 13,395 33,4656 8.92% (150000)(8.92%) 13,380 20,0857 8.93% (150000)(8.93%) 13,395 6,6908 4.46% (150000)(4.46%) 6,690 0

Copyright Oxford University Press 2009

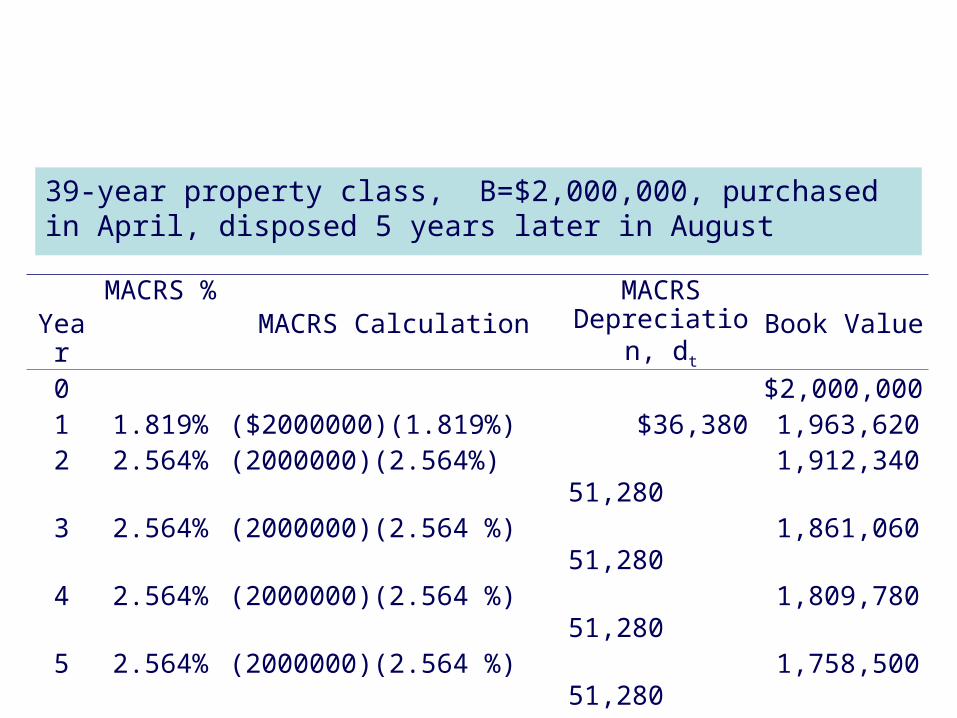

Example 11-7 Calculation of MACRS GDS Depreciation

39-year property class, B=$2,000,000, purchased in April, disposed 5 years later in August

YearMACRS

% MACRS CalculationMACRS

Depreciation, dt Book Value0 $2,000,0001 1.819% ($2000000)(1.819%) $36,380 1,963,6202 2.564% (2000000)(2.564%) 51,280 1,912,3403 2.564% (2000000)(2.564 %) 51,280 1,861,0604 2.564% (2000000)(2.564 %) 51,280 1,809,7805 2.564% (2000000)(2.564 %) 51,280 1,758,5006 2.564% (7.5/12)(2000000)(2.564 %)

32,1001,726,400

273,600

Copyright Oxford University Press 2009

Example 11-8 Comparison of Depreciation Methods

0

25000

50000

75000

100000

125000

150000

0 1 2 3 4 5 6 7 8 9 10

Year

Bo

ok

Va

lue

MACRS

SL

SOYD

DDB

Copyright Oxford University Press 2009

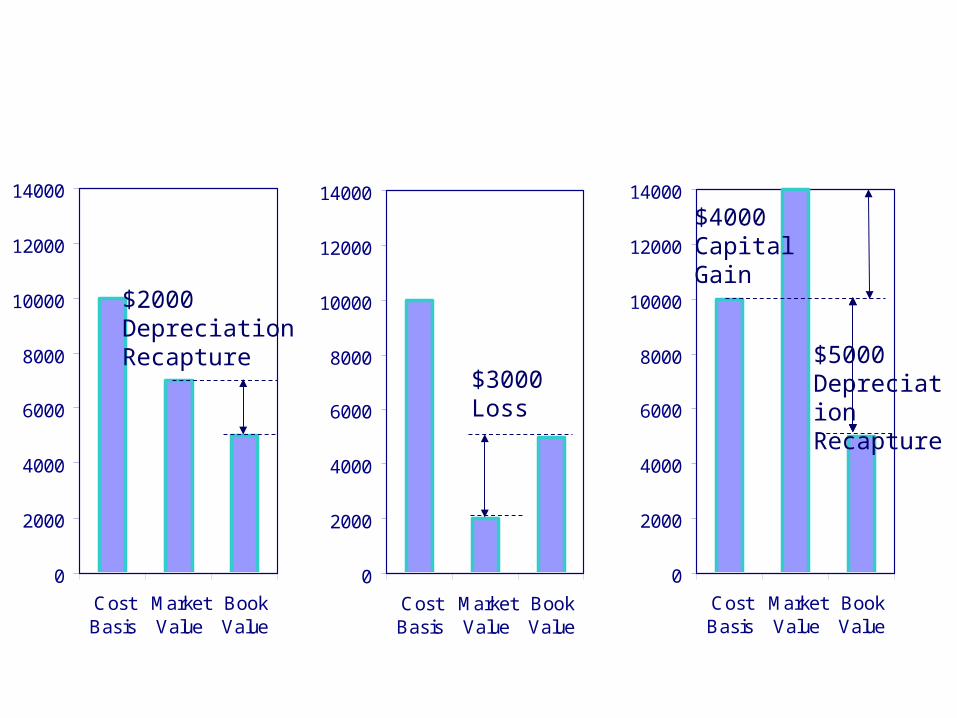

When a depreciable asset is disposed of, and the market value is different than the book value, the difference must be treated as:

• Depreciation recapture (ordinary gains): Depreciation recapture occurs when an asset is sold for more than its current book value, but less than the original cost basis.

• Losses: A loss occurs when an asset is sold for less than its current book value.

• Capital gains: Capital gain occur when an asset is sold for more than its original cost basis. Capital gains may be taxed at lower rate than ordinary gains.

Depreciation and Asset Disposal

Copyright Oxford University Press 2009

Depreciation and Asset Disposal

0

2000

4000

6000

8000

10000

12000

14000

CostBasis

MarketValue

BookValue

0

2000

4000

6000

8000

10000

12000

14000

CostBasis

MarketValue

BookValue

0

2000

4000

6000

8000

10000

12000

14000

CostBasis

MarketValue

BookValue

$2000 DepreciationRecapture

$4000 CapitalGain

$3000 Loss

$5000 DepreciationRecapture

Copyright Oxford University Press 2009

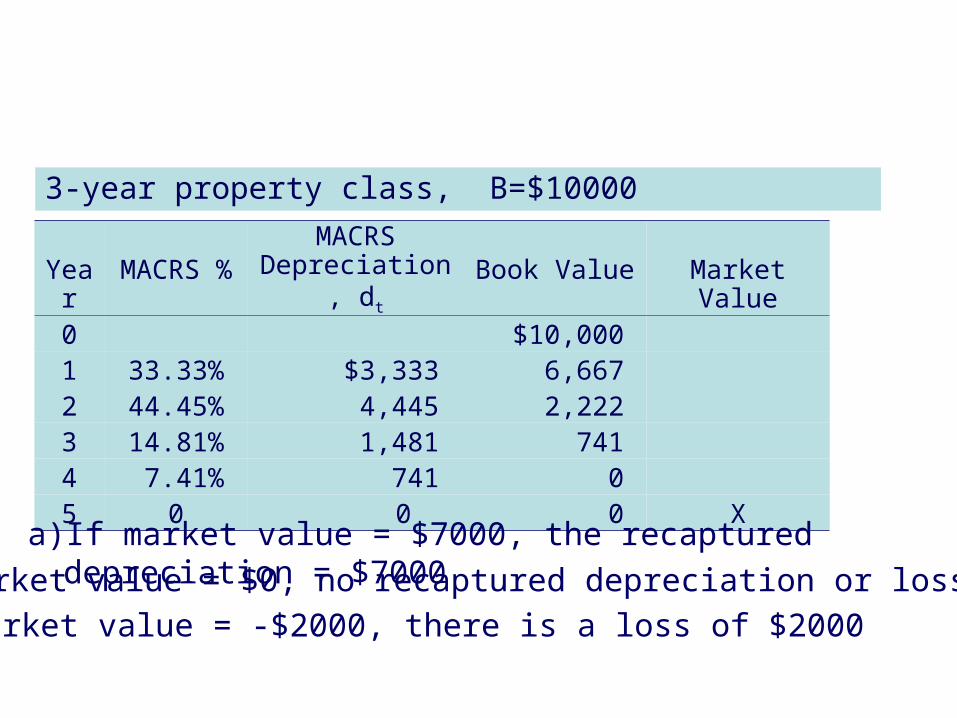

Example 11-9 Depreciation and Asset Disposal

3-year property class, B=$10000

Year MACRS %MACRS

Depreciation, dt Book Value Market Value0 $10,0001 33.33% $3,333 6,6672 44.45% 4,445 2,2223 14.81% 1,481 7414 7.41% 741 05 0 0 0 X

a) If market value = $7000, the recaptured depreciation = $7000

b) If market value = $0, no recaptured depreciation or loss

c) If market value = -$2000, there is a loss of $2000

Copyright Oxford University Press 2009

Example 11-10 Depreciation and Asset Disposal

Year MACRS %MACRS

Depreciation, dt Book Value Market Value0 $10,0001 33.33% $3,333 6,6672 44.45% 4,445 2,2223 14.81% (1/2)1,481=740.5 1,481.5 $2500

1)Year MACRS %

MACRS Depreciation, dt Book Value Market Value

0 $10,0001 33.33% $3,333 6,6672 44.45% (1/2)4,445=2,222.5 4,444.5 $2500

Market Value – Book Value = $2500 – 4444.5 = - 1944.5 (Loss)

2)

Market Value – Book Value = $2500 – 1481.5 = 1018.5 (Recaptured Depreciation)

Copyright Oxford University Press 2009

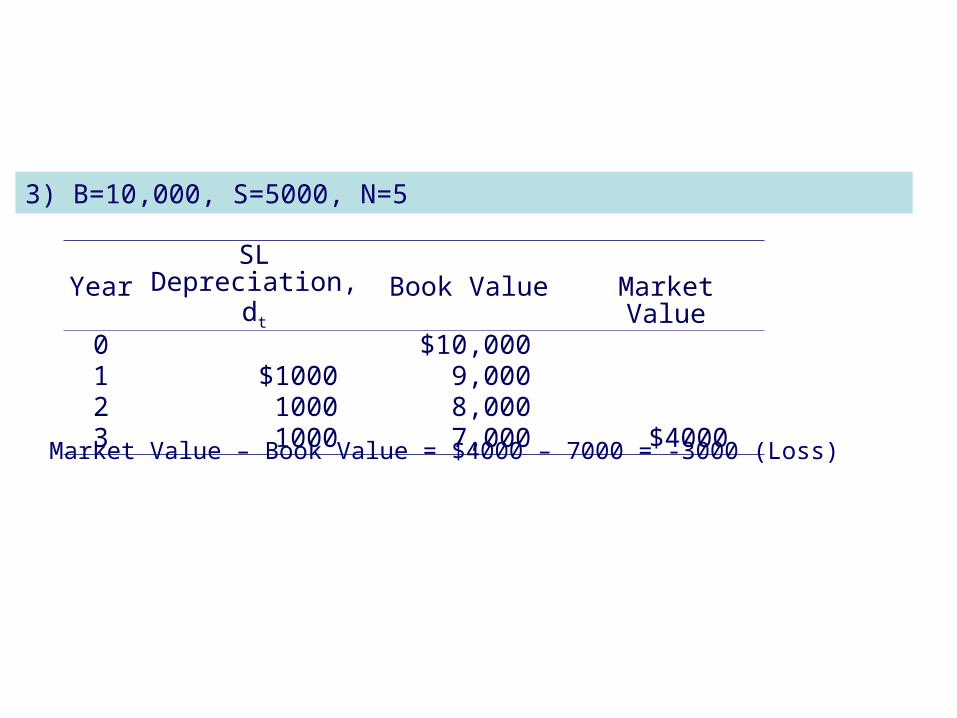

Example 11-10 Depreciation and Asset Disposal

YearSL Depreciation,

dt Book Value Market Value0 $10,0001 $1000 9,0002 1000 8,0003 1000 7,000 $4000

3) B=10,000, S=5000, N=5

Market Value – Book Value = $4000 – 7000 = -3000 (Loss)

Copyright Oxford University Press 2009

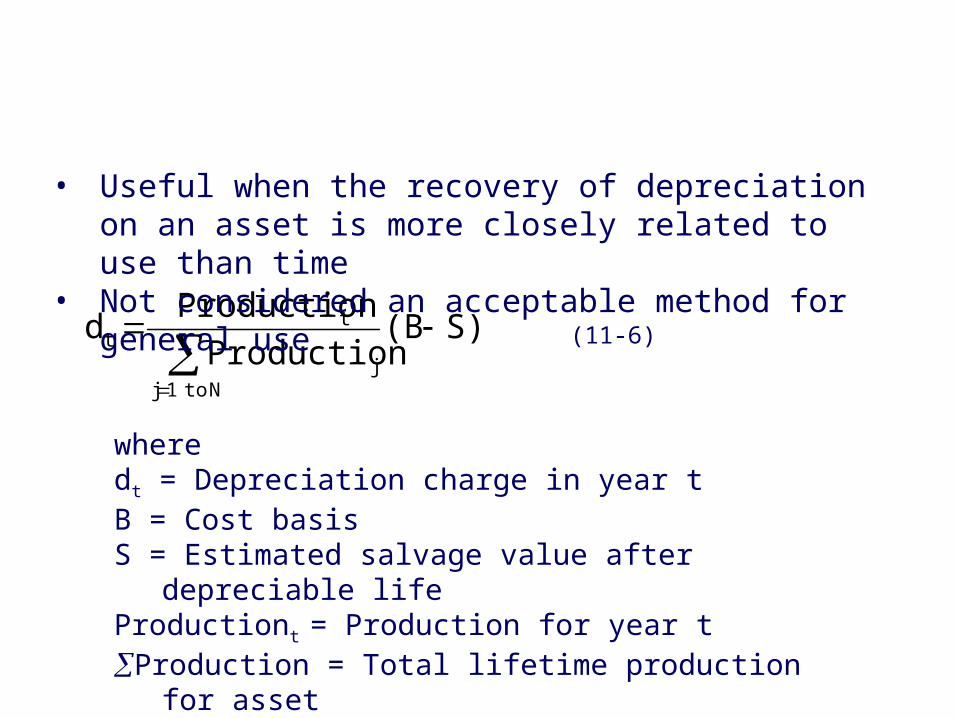

Unit-of-Production Depreciation

S)(BProduction

Productiond

N to 1jj

tt

(11-6)

wheredt = Depreciation charge in year tB = Cost basisS = Estimated salvage value after depreciable lifeProductiont = Production for year tProduction = Total lifetime production for asset

• Useful when the recovery of depreciation on an asset is more closely related to use than time

• Not considered an acceptable method for general use

Copyright Oxford University Press 2009

Example 11-11 Unit-of-Production Depreciation

5-year depreciable life, B=$900, S=$70

YearAnnual

ProductionUOP Depreciation

CalculationUOP

Depreciation, dt

Book Value

0$900

1 4,000 (4,000/40,000)(830) $83817

2 8,000 (8,000/40,000)(830) 166651

3 16,000 (16,000/40,000)(830) 332319

4 8,000 (8,000/40,000)(830) 166153

5 4,000 (4,000/40,000)(830) 8370

40,000

Copyright Oxford University Press 2009

Depletion

• Depletion is the exhaustion of natural resources as a result of their removal.

• Except for standing timber and most oil and gas wells, depletion allowance is the larger of the two methods.

• Cost Depletion:• Similar to the unit-of-production depreciation method• Permissible for standing timber and most oil and gas wells• Cost of land must be excluded from the property cost

• Percentage Depletion:• Depletion allowance is a certain percentage of the property’s

gross income during the year• Cannot exceed 50% of the property’s taxable income

computed without the depletion deduction

Copyright Oxford University Press 2009

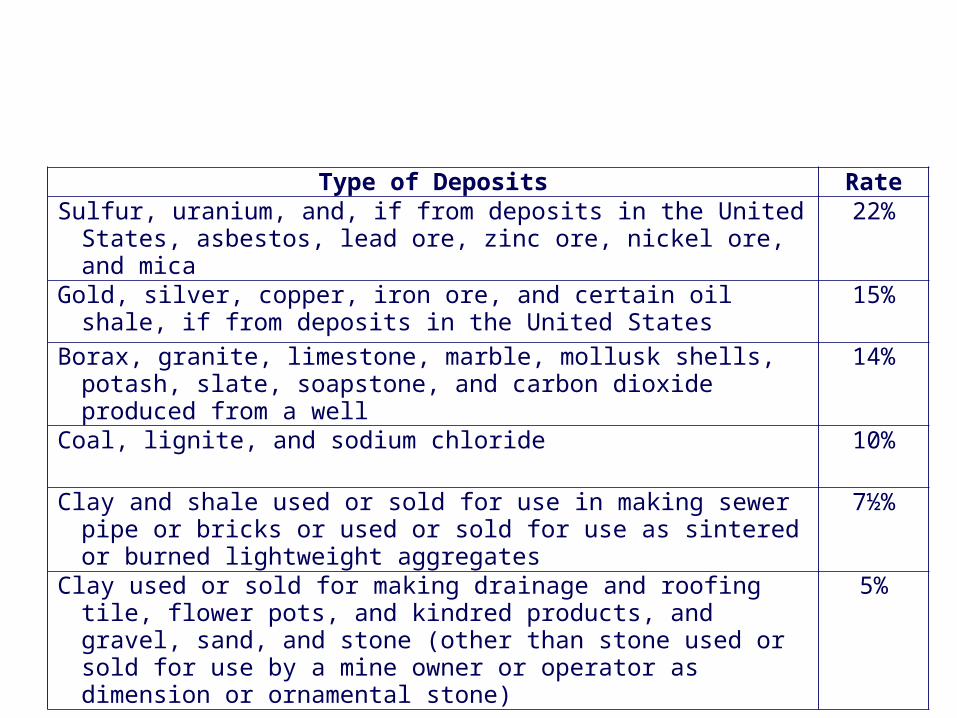

Table 11-6 Percentage Depletion Allowance

Type of Deposits RateSulfur, uranium, and, if from deposits in the United States, asbestos,

lead ore, zinc ore, nickel ore, and mica22%

Gold, silver, copper, iron ore, and certain oil shale, if from deposits in the United States

15%

Borax, granite, limestone, marble, mollusk shells, potash, slate, soapstone, and carbon dioxide produced from a well

14%

Coal, lignite, and sodium chloride 10%

Clay and shale used or sold for use in making sewer pipe or bricks or used or sold for use as sintered or burned lightweight aggregates

7½%

Clay used or sold for making drainage and roofing tile, flower pots, and kindred products, and gravel, sand, and stone (other than stone used or sold for use by a mine owner or operator as dimension or ornamental stone)

5%

Copyright Oxford University Press 2009

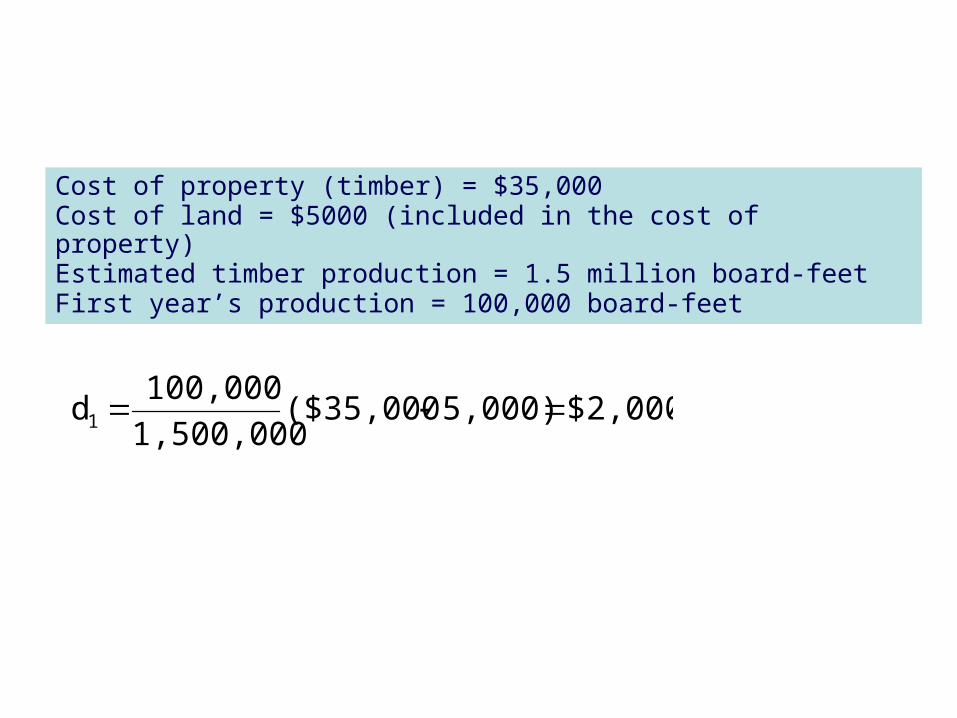

Example 11-12 Cost Depletion

Cost of property (timber) = $35,000Cost of land = $5000 (included in the cost of property)Estimated timber production = 1.5 million board-feetFirst year’s production = 100,000 board-feet

$2,0005,000)($35,0001,500,000

100,000d1

Copyright Oxford University Press 2009

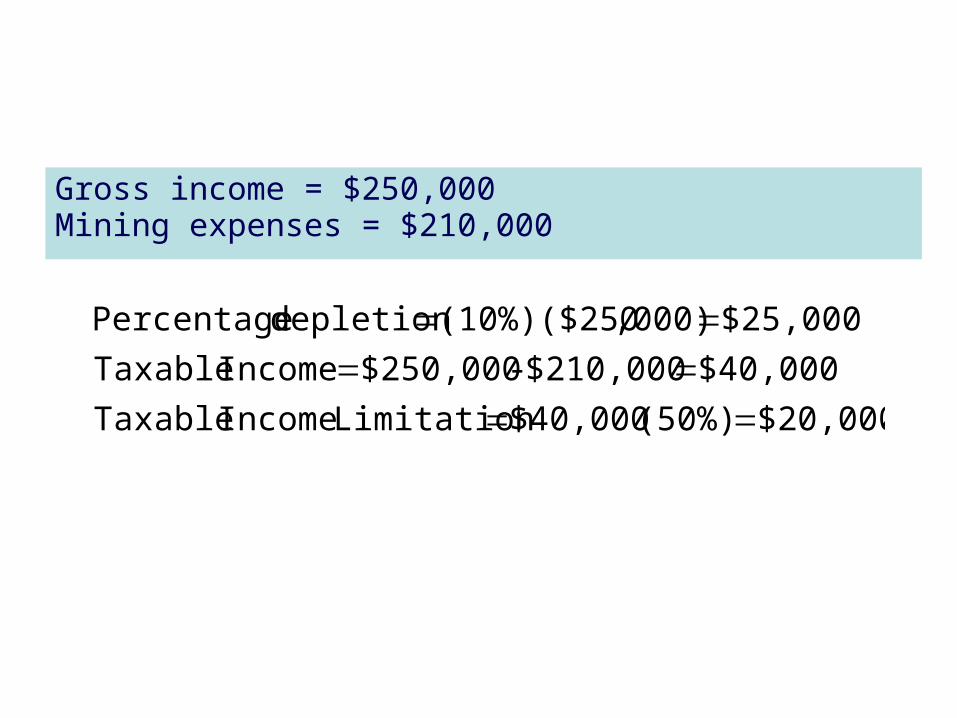

Example 11-13 Percentage Depletion

Gross income = $250,000Mining expenses = $210,000

$20,000(50%) $40,000Limitation Income Taxable

$40,000$210,000 - $250,000Income Taxable

$25,000,000)(10%)($250depletion Percentage

Copyright Oxford University Press 2009

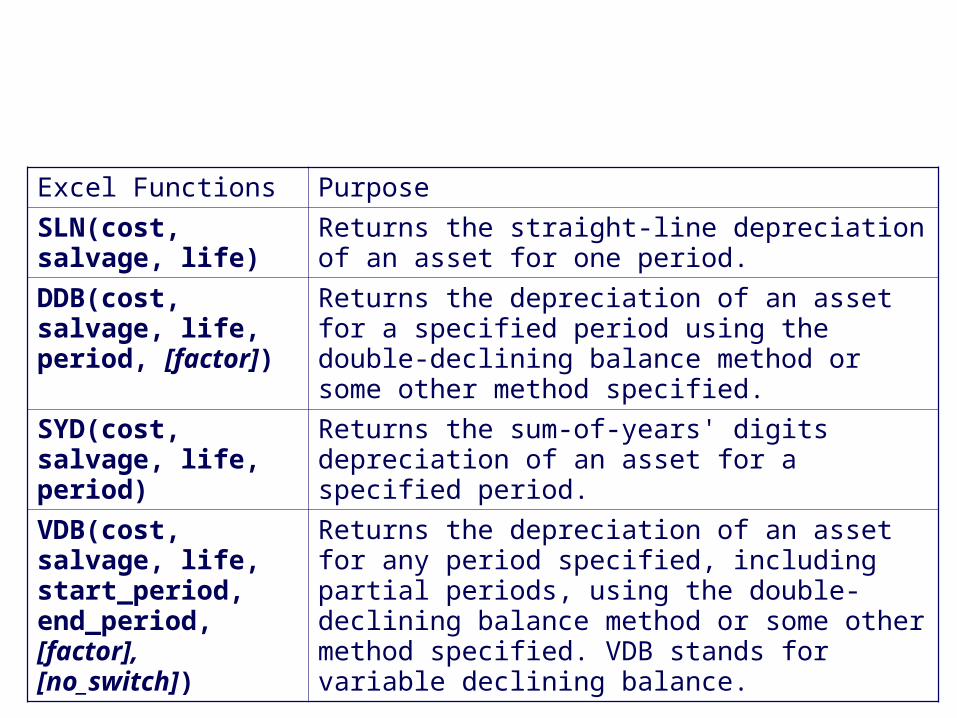

Spreadsheet and Depreciation

Excel Functions Purpose

SLN(cost, salvage, life)

Returns the straight-line depreciation of an asset for one period.

DDB(cost, salvage, life, period, [factor])

Returns the depreciation of an asset for a specified period using the double-declining balance method or some other method specified.

SYD(cost, salvage, life, period)

Returns the sum-of-years' digits depreciation of an asset for a specified period.

VDB(cost, salvage, life, start_period, end_period, [factor], [no_switch])

Returns the depreciation of an asset for any period specified, including partial periods, using the double-declining balance method or some other method specified. VDB stands for variable declining balance.