chapter 7 - welcome to homepage of planning...

TRANSCRIPT

663

CHAPTER 7.1

INDUSTRY

7.1.1 In order to achieve a doubling of per capitaincome over the next decade, the Tenth Plan targetsa gross domestic product (GDP) growth rate of 8per cent per annum. The corresponding growthtarget for the industrial sector is 10 per cent. Thisrepresents a major step-up in view of the less than7 per cent growth during the last decade. A taskthat would have been quite daunting even undernormal conditions, becomes much more challengingdue to structural deformities and changes that arelikely to occur in the internal and externalenvironment.

comparative advantage based on the narrow staticinterpretation of relative factor endowments ofnations. Access, on a global basis, to moderntechnology, capital resources and markets is now amore critical determinant of internationalcompetitiveness.

7.1.4 Comparative advantage is today theaggregate sum total of technical, entrepreneurialand managerial capabilities of the constituent firmsof a country. Improvements in transport andtechnology make it possible to split businessprocesses and locate sub processes in differentcountries depending on the inherent cost advantagewhich they can derive from the investment climateand policy environment. Be that as it may, no countrycan isolate itself completely from the forces beingunleashed by a rapidly globalising community ofnations. A dynamic policy environment should not,however, be perceived as a looming threat since italso offers immense opportunities to capture muchmore affluent markets outside the country. It hasbeen estimated that developing countries couldrealise over $700 billion in the form of exportearnings if industrialised countries end theprotection of labour-intensive products. Potentialexport earnings of developing countries in textiles,clothing and other labour-intensive products aloneare estimated to exceed $500 billion if advancedindustrial countries open up their markets(UNCTAD, 2002).

The Emerging External Environment

• WTO • Regional Trading Blocs· Free Trade · NAFTA· Tariffs · EU· QRs · SAARC· FDI • Preferences for green

• Market access products and processes· Standards · Environment· Accreditation · Health· Certification · Safety

7.1.2 A highly competitive environment is rapidlyemerging, driven by rising economic and socialaspirations on the one hand and external conditionspredominantly World Trade Organisation (WTO)related market forces on the other. Other importantfactors emphasising the need for continuousimprovements in productivity and efficiency in theallocation of resources are: consumer demand forenhanced value in terms of cost and quality;consumer tastes and preferences shiftingperceptibly in favour of environment-friendlyproducts; and regulatory pressures for sustainableindustrial processes and practices based on lifecycle analysis of the impact on the environment.

7.1.3 Global integration of markets is alsochallenging the conventional concept of

Box 7.1.1Fortune 500 companies have started

sourcing initiatives in India

• ABB • GM• FORD • HP• SHARP • FIAT• CUMMINS • EMERSON ELECTRIC• GE • TOYOTA

• KODAK

TENTH FIVE YEAR PLAN 2002-07

664

7.1.5 India's inherent strength and comparativeadvantage lie in the presence of entrepreneurialacumen of the highest quality, an establishedscientific and industrial base, cheap, skilled English-speaking workforce and a large domestic market.The relocation, by large transnational companies,of their manufacturing base to India and sourcingof products from here by other Fortune 500companies is evidence of the bright future of Indianindustry.

7.1.6 Unless India is proactive in responding tothe imperatives of the changing environment, thereis a very serious danger that it would be left farbehind in today's race for the 'survival of the fittest'.In short, Indian industry has to discard its inward-looking approach and become outward-orientedand learn to operate in an unprotected,internationally competitive environment. Our dreamcan be translated into reality only if we see apparentthreats as genuine opportunities and exploit theirpotential. Industry and the Government have to workcollectively and in tandem to this end. The TenthPlan requires making a bold departure from the past.

OBJECTIVES OF INDUSTRY SECTOR

7.1.7 The contribution of industry to GDP is animportant indicator of a nation's progress in theprocess of structural transformation from a ruralagricultural society to a more urban industrialisedone. Further, an increase in per capita income isassociated with a rise in the share of industry alongwith a fall in the share of agriculture in nationalincome. In the early stages of industrialisation, whenper capita income is very low, the primary sectoroccupies a dominant position in the economicstructure. As capital and skills accumulate, bothproductivity and per capita income rise. Industry, inits broad sense of secondary sector, is followed oraccompanied by the services sector displacing therelative contribution of the primary sector.

7.1.8 It is significant to note that consumption ofmanufactured consumer goods is recognised asone of the most widely accepted measures ofstandard of living and of quality of life. Manufacturingindustry provides the driving force for stimulatingrapid economic growth. The growth rate of themanufacturing industry normally surpasses that ofthe agriculture and the service sectors. It is for thisreason that industry is considered the backbone ofan economy. It is in recognition of this specialimportance that raising industry's share in GDP isbeing ranked as the foremost objective for thissector in the Tenth Plan. The comparative cross-country position given in Table 7.1.3 amply justifiesthis objective. India's share in world industrial outputand exports is not commensurate with its size andpotential. Unless the pace of industrial growth isaccelerated, India is likely to be left behind by thelarger community of nations. It is perhaps pertinentto add that traditionally, the political stature of acountry has been commensurate with the size andstructure of its industry.

Box 7.1.2Manufacturing is moving to India

(multinational companies which have set upbase in India)

• TOYOTA • GM• MAKINO • HYUNDAI• FORD • KODAK

7.1.9 Participation in world trade is essential forIndia as it can yield multiple advantages. Risingexports can augment the availability of much-needed imports while also bridging the trade deficit.As a spin off, the concomitant requirements ofproductivity and quality of exportable manufacturedgoods would also raise our own standard of livingthrough the improved availability of diverse highquality products. Globally, trade is emerging as apowerful engine of economic growth and

Table 7.1.3Industry’s share(%) in GDP

Country Value added GNI/capas % of GDP ($) in 2000

Industry Services

India 27 46 460

China 49 34 840Malaysia 40 48 3380Indonesia 47 36 570Philippines 30 53 1040

Thailand 40 49 2010World Development Report 2002

GNI ( Gross National income) = GDP+ Net receipt ofprimary income from foreign sources

INDUSTRY

665

development. Manufactured products are generallytraded goods. Their demand also shows price andincome elasticity as a result of which the exportindustry, unlike agriculture, does not face majormarket constraints. Raising India's share in theworld exports of manufactured products is,therefore, the second important objective for theindustry sector in the Tenth Plan.

7.1.10 Free markets and competition are not apanacea for all the ills of the developing countries.Complex issues such as the elimination of regionalimbalances in industrial development, which hasdefied all solution in earlier Plans, need innovativealternatives, particularly in the absence of directintervention measures such as industrial licensingthrough which location of industry was sought tobe influenced earlier. The increasing gap betweendeveloped industrialised States and others couldhave serious implications for the country. This isparticularly true for the northeastern States, whichhave continued to lag behind the rest of the countryon account of their poor connectivity, inadequatelocal infrastructure and small size of their markets.Bringing about a balanced industrial developmentin the country is, therefore, proposed to be the thirdobjective for the sector.

7.1.11 Employment in India is skewed in favour ofthe agriculture sector which accounts for about 60per cent of total employment. As a consequence, thereis widespread unemployment and under-employmentespecially for skilled workers both in urban and ruralareas. Demographic projections suggest that about60 per cent of the population would soon be in the15-59 year age group, leading to a substantial increasein the workforce. Unless jobs are created in the moreproductive manufacturing sector, the unemploymentsituation could become quite alarming. Hence, thefourth objective for the industry sector in the TenthPlan is to create jobs for skilled workers throughindustrial growth.

STRATEGY FOR INDUSTRY SECTOR IN THETENTH PLAN

7.1.12 The Tenth Plan envisages acomprehensive and coherent strategy for attainingthese objectives. Deepening and widening ofeconomic reforms to create a positive investment

climate conducive to a dominant private sector role,including setting up state-of-the-art infrastructure,capacity building in industry in order to make itinternationally competitive, a level playing field witheffective and transparent rules of fair play,augmentation of financial resources and efficiency-enhancing policy instruments are the importantingredients of such a strategy. These have to beviewed in a holistic manner as they areinterdependent.

Creating a Positive Investment Climate

7.1.13 The industrial development strategy isbeing re-oriented towards enabling our vibrantprivate sector to reach its full entrepreneurialpotential, to contribute towards production,employment and income generation. Unless theeconomic environment is conducive to high levelsof private sector participation, there can be littleprogress in accelerating industrial development andgrowth. An inward-looking policy environment in thepast promoted import substitution with artificial propssuch as high tariff protection, quota restrictions,entry barriers etc. In order to ensure that thetransition from a closed to an outward-lookingeconomy is smooth and non-disruptive, well-conceived government interventions to dismantleexisting barriers to industrial growth andaccelerating new initiatives to create an enablingenvironment at par with the rest of the world areneeded.

7.1.14 Private initiative depends on a variety ofmarket-related factors and overarching macroeconomic policies. A conducive investment climaterequires a considerable widening and deepeningof economic reforms cutting across the Centre andStates and local bodies, including panchayati rajinstitutions (PRIs). These reforms must be aimedat ending rigidities in labour policies, reforming realestate laws, the security, transferability andenforceability of property rights, bankruptcy andforeclosure laws and easing restrictions on the inter-State movement of goods imposed by the EssentialCommodities Act, 1955, octroi checkposts and otherlocal levies/regulations. The agenda also coverspositive conditions required for a competitive marketeconomy like the establishment of an efficient world-class physical, financial and social infrastructure,

TENTH FIVE YEAR PLAN 2002-07

666

providing a level playing field and rules of fair playwhich require bold initiatives including removal ofartificial compartmentalisation of different sub-sectors. The Government also needs to addressthe issue of restrictions on market access, dumpingand predatory practices on the part of other players,especially the developed nations.

7.1.15 Tariff imposed by the industrialised countriesare substantially loaded against manufacturedimports from developing countries, making it moredifficult for them to undertake downstream processingactivities. The use of non-tariff measures, includinganti-dumping cases, social safeguards, technicalstandards and subsidies, have restrictedopportunities for developing countries. A re-balancingof the trading system to the mutual benefit of allcountries would require, among other things,improved access to developed markets and transferof technology to developing countries formodernisation leading to enhanced productivity andinternational competitiveness.

Capacity Building

7.1.16 While the inward-looking policyenvironment did play an important role in buildingup the country's diverse scientific, technological andindustrial base, it has outlived its utility. Largesections of our industry are characterised by plantsof sub-optimal sizes using outdated technologies.As a result, the productivity of capital and labour inIndian industry is comparatively low. Modernisationand technological upgradation is the foremostrequirement for competitiveness. The Tenth Plan

plans to give an impetus to the induction of cleanproduction technologies, processes and practices.

7.1.17 Raw materials and low technologyproducts dominate India's export basket today,accounting for over 80 per cent of the totalmanufactured exports. Against this, the worldaverage ranged between 43 per cent and 35 percent during 1985 to 1996. India’s high technologyexports have performed rather poorly and theirshare has risen by only 1.4 points compared to 7.6points for the world as a whole during the 1986 to1996 period. The ratio of high technology productsto total manufactured exports in the case of India isonly one-fifth of that of China and one-tenth of SouthKorea and Taiwan. Modernisation and technologicalupgradation would, therefore, lead to value additionand diversity, lending resilience to our exports.

World Class Infrastructure

7.1.18 The state of the country's infrastructure isfar from adequate. Public sector monopoly in theownership, control and management ofinfrastructure needs to give way to private financingof infrastructure projects to leverage the privatesector's resources and productive efficiency for thebenefit of all stakeholders - the service user, theservice provider and the Government. This has beendemonstrated with success all over the world.Although efforts are being made to augment qualityand coverage of all infrastructure, the policyframework to promote private initiative is not yetfully in place. However, the magnitude of the taskis too huge for the public sector to handle on its

INDUSTRY

667

own. Without public-private partnership in this field,the desired rapid industrial growth would bejeopardised. Some States, notably Maharashtra andAndhra Pradesh, have adopted innovative modelsfor providing state-of-the-art infrastructure. Not onlydo recent investor surveys accord higher ranks tothe investment climate in these states, but the flowof investment, including foreign direct investment(FDI), is greater. While there is no one model thatsuits all situations, the swiftness with which otherStates, especially the industrially-backward statesincluding those in the northeast, come up withsimilar initiatives will determine the pace of industrialgrowth. The Tenth Plan defines the policy paradigmfor infrastructure development in terms of modelsthat encourage efficiency and leverage resourcegeneration.

Augmenting the Resource Base

7.1.19 A considerably higher measure ofinvestible resources is required in order to achievethe industrial growth rate target of 10 per cent perannum. The augmentation of the resource baserequires action on several fronts. To begin with, thebleeding of the resource base in the form ofunproductive public sector undertakings (PSUs)needs to be checked. The closure of such PSUsneeds to be expedited. A number of roadblocks tothis process need to be removed.

7.1.20 Simultaneously, vast resources need to bereleased from areas of low productivity in the publicsector. This requires disinvestment of PSUs so thatour resources are released and transferred to moreefficient management. Taking into account the slowpace of disinvestment, the issue of managementof the public sector in the transition period assumesimportance.

7.1.21 The subsidy burden also needs to bedrastically reduced. The fertiliser sector and thepublic distribution system (PDS) together accountfor over Rs. 20,000 crore of subsidies. Powerfulvested interests in favour of their perpetuation needto be tackled. Bold steps are required in order tobring about an efficient pricing policy.

7.1.22 In order to mobilise additional resources,it is necessary to evolve a healthy Indian capital and

financial market in order to tap the vast savingspotential of the Indian household sector and transferit to industry through efficient financialintermediaries. Restoration of investor confidenceis an absolute necessity for augmenting theresource base. The recent financial sector scandalspoint to the need for utmost caution on the part ofthe regulatory institutions which have been set up.Corporate governance cannot be improved unlesscredible and transparent rules of behaviour areevolved and enforced by industry associations.

7.1.23 Serious attention must also be given to theissue of foreign investment (both portfolioinvestments and FDI). According to some estimates,a quadrupling of FDI is required in order to achievea 10 per cent industrial growth rate. FDI is not onlyan additional source of funds but the technology itbrings in and the market access it provides havevast implications for productivity and quality.

Efficiency Enhancing Initiatives

7.1.24 Efficiency enhancing policies call forallowing a free play of market forces during theTenth Plan. Unless genuine strategic concernsrequire otherwise, all internationally traded goodswould be priced on international parity. Prices ofnon-traded goods would reflect their true resourcecosts. Pricing based on the long-run marginal costof production should be a dominating feature insectors such as infrastructure services, power,municipal services etc. Market-based instrumentsand indirect policies would completely substitute directintervention and the command-and-control approach.

7.1.25 As progress from a regulated economy toa fully competitive economy would be necessarilyslow and time-consuming, market imperfectionswould require a greater role for the State as awatchdog and regulator at least in some importantsectors such as drugs and pharmaceuticals.

REVIEW OF THE NINTH PLAN

Major Initiatives

7.1.26 During the Ninth Plan, the major structuralchanges and modifications in sectoral policies were:delicensing of coal, lignite and petroleum (other than

TENTH FIVE YEAR PLAN 2002-07

668

crude oil), amendment of Mines and Minerals(Regulation and Development) Act, 1957, specialpackage for revival of export growth, repeal of theUrban Land (Ceiling and Regulation) Act, 1976,allowing buy-back of shares and liberalisation oftechnology imports.

7.1.27 Foreign equity up to 100 per cent wasallowed under automatic route for majorinfrastructure sectors and the time frame forconsideration of FDI proposals has been reducedfrom six weeks to 30 days. A Foreign InvestmentImplementation Authority has been set up in theDepartment of Industrial Policy and Promotion toprovide a single-point interface between foreigninvestors and the Government. Prior approval ofthe Government is not required for increase inthe amount of foreign equity within the approvedpercentage of foreign equity in cases in whichthe original project cost was up to Rs. 600 crore.The Government has taken steps for simplifyingforeign investment procedures, allowed foreigninvestment in new activities such as Global MobilePersonal Communication Systems besidessimplifying procedures for downstreaminvestment to foreign-owned Indian holdingcompanies. FDI up to 26 per cent under theautomatic route has been allowed in theinsurance sector subject to a licence from theInsurance Regulatory and Development Authority.Progressive liberalisation in the provisions relatingto investment are : foreign institutional investors(FIIs) can invest in a company under the portfolioup to 24 per cent of the paid-up capital of thecompany; and up to 100 per cent FDI is allowedin non-banking financial companies (NBFCs) ona case-to-case basis with the condition that aminimum of 25 per cent of their holding isdivested in the domestic market.

7.1.28 The Government's approach to PSUshad a three-fold objective: revival of potentiallyviable enterprises; closing down of those thatcannot be revived; and reducing its equity in non-strategic PSUs to 26 per cent or below. Interestsof workers will be fully protected through attractiveVRS and other measures. This programme hasalready achieved some initial successes. TheGovernment is also proposing to set up a National

Company Law Tribunal (NCLT) for sickcompanies. At present the process ofrehabilitation/winding up of PSUs is done throughthe mechanism of BIFR.

7.1.29 The Department of Heavy Industry hasundertaken restructuring of PSUs in line with theGovernment policy for reform of the public sector.Cases of 20 PSUs have been referred to theMinistry of Disinvestment for disinvestment/formation of joint ventures. Out of 49 PSUs underthe Department of Heavy Industry, 26 have beenreferred to the BIFR. Revival plans for 12 havebeen sanctioned by BIFR and are underimplementation. The BIFR has favoured windingup in the case of another seven, while the casesof the remaining seven are still being consideredby the BIFR.

7.1.30 Manpower rationalisation has beenadopted extensively to shed surplus manpower.Around 3,69,277 employees have opted for VRSsince introduction of this scheme in October, 1988to November, 2001, the benefits of the VRS forwhich the Government has provided financialsupport of about Rs. 1,100 crore over the lastnine years. The statutory dues of the employees,which have been pending for long, have also beencleared along with VRS benefits under theseparation scheme. The Government has alsoprovided additional support of about Rs. 500 crorefor VSS for around 10,000 employees.

7.1.31 Considering the market sentiments andrecent developments in the United States and othercountries relating to employees stock options etc.,it was decided to liberalise certain provisions of theCompanies Act, 1956. The Companies(Amendment) Ordinance, 2001 was promulgatedin October 2001 and has been replaced withCompanies (Amendment) Act, 2001.

7.1.32 The Export Promotion Industrial Park(EPIP), is a centrally sponsored scheme forproviding financial assistance to State Governmentsfor setting up and maintaining industrial parks withappropriate infrastructure for housing industrial unitswith export commitment. An expenditure of Rs. 250crore was approved by the Cabinet for setting up25 EPIPs in 25 States. The Central Government's

INDUSTRY

669

grant for EPIP would be 75 per cent of the capitalexpenditure, up to a limit of Rs. 10 crore in eachcase. So far the Government has approved 20proposals for setting up EPIPs in Punjab, Haryana,Himachal Pradesh, Rajasthan, Karnataka, Kerala,Maharashtra, Tamil Nadu, Andhra Pradesh, UttarPradesh, Gujarat, Bihar, Jammu and Kashmir,Assam, Madhya Pradesh, West Bengal, Orissa,Meghalaya, Manipur and Nagaland. Nine EPIPshave been completed so far, and other parks are invarious stages of implementation. Proposals fromthe other States are awaited.

7.1.33 The Critical Infrastructure Balance Scheme(CIBS) scheme envisages investment in areas ofcritical deficiency in the interest of export promotion.The balancing investment may inter-alia relate toinfrastructure in export intensive areas includingexport processing zones (EPZs), seaports andairports, improvement of feeder roads and effluenttreatment units etc. Since its inception, 44 projectshave been sanctioned in 16 States. Specific projectsassisted include construction of common facilitiesin the apparel export park at Gundapochampally,power supply to software unit in Export PromotionIndustrial Park at Bhubaneshwar, infrastructuredevelopment at Saharanpur, computerisation inEPZs at Kochi, Vishakhapatnam, Mumbai, Chennai,Falta, Kandla and Noida.

7.1.34 SEZs were set up with a view to enablinghassle-free manufacturing and trading activities forthe purpose of exports. The units in these zoneswill not be subjected to any pre-determined value-addition or export obligation. They shall be treatedas being outside the customs territory of the country.Sale in the domestic tariff area by the units in thesezones can only be done after payment of full Customsduty. A private sector SEZ covering an area of about3,500 hectares has been sanctioned at Pipavav inGujarat. Another private sector SEZ has beensanctioned at Tuticorin in Tamil Nadu. Besides, theexisting EPZs in Mumbai, Vizag, Kandla and Kochiare also being converted into SEZs.

7.1.35 For involving State Governments in theexport effort, a new scheme - Assistance to Statesfor Infrastructure Development for Export and AlliedActivities (ASIDE) - has been evolved for grantingassistance to the States for development of export-

related infrastructure on the basis of their exportperformance. The difference in the proposedscheme and the existing infrastructure-orientedschemes (e.g. CIBS, EPIP, EPZ, ExportDevelopment Fund-North East Region (EDF-NER)is that these schemes do not involve StateGovernments in decision-making. The proposedscheme is area-specific and not product-specific.States would use the money for complementaryexport-related infrastructure, such as roadsconnecting the production centres with ports,research and development (R&D) in State-specificproducts, development of cold chains for agroexports, development of minor ports, creation of newexport promotion industrial parks, human resourcedevelopment and developing marketinginfrastructure.

7.1.36 Many export incentives are not compliantwith the WTO framework and are being phasedout. Thus the instruments which were availableto neutralise the negative impacts of varioushandicaps in the form of higher capital costs,higher tariffs, transactions costs and unrebatedduties will no longer be available. Aggressiveefforts and systematic export marketingschemes like the Market Access Initiative (MAI),Agri Economic Zone (AEZs), SEZs have,therefore, been worked out. The MAI has beendevised to put in place an instrument which isnot only WTO compatible but would also mitigatethe negative effects of various handicaps facedby the exporters vis-à-vis their counterparts in thecompeting countries. The strategy would aim atachieving a double-digit growth rate in our exports(in dollar terms) on a sustained basis.

7.1.37 In October 2001, the Governmentincreased the duty drawback rate for 300 productgroups covering the textiles, leather and engineeringgoods sectors and removed the Duty EntitlementPass Book (DEPB) value cap on 4,000 items, whichwill also benefit the chemicals and plastic goods'industries. The step was undertaken as a one-timemeasure for promoting exports and the policy willbe reviewed. A Directorate General of Anti-Dumpingand Allied Duties was constituted in 1998 toinvestigate complaints of dumping and recommendthe amount of anti-dumping duties. A Task Force

TENTH FIVE YEAR PLAN 2002-07

670

was set up to prepare a common nomenclature at8-digit level for trade data on Customs and Excise.The collection, compilation, and dissemination oftrade statistics is now taking place with reduced timelag. Electronic filing and on-line processing of licenseapplications, on-line payment of duty drawback, andabolition of special import license (SIL), removal ofquantitative restrictions etc. have been effected.

7.1.38 Besides, the continuation of Growth Centreand Transport Subsidy scheme, a major policyinitiative by the Department of Industrial Policy andPromotion was the Northeast Industrial Policy(NEIP). A new industrial policy was announced forthe development of industrial infrastructure in thenortheastern region. The Transport SubsidyScheme was extended for a period of another sevenyears, up to 31 March 2007.

7.1.39 In the textile sector, several long-termand short-term measures were taken to minimisethe adverse effects of the external conditions onexports. These included concessions under thequota policy to reduce transaction costs forexports, resolving of the issue of DEPB rates forblended textiles and wool tops, revision in Duty-drawback rates, etc. Two new Plan schemes forpromoting textile exports were also formulated –Apparel Parks for exports for giving a thrust tosetting up of apparel units of internationalstandards and Textile Centre InfrastructureDevelopment Scheme for providing financialassistance for infrastructural facil i t ies atestablished textile growth centres.

7.1.40 The Technology Upgradation Fund Scheme(TUFS) was introduced to modernise the textilesector. All the sub-sectors of the textiles likespinning, weaving, knitting, processing, garmentmaking, cotton ginning and pressing and jute sectorare covered under the scheme. The TechnologyMission on Cotton (TMC) was established toimprove the productivity and quality of cotton so asto increase the income of farmers and makingquality cotton available to the textiles industry atcompetitive prices. The ginning and pressing units,which operate with obsolete technology, poor qualityof cotton and increased wastage are proposed tobe modernised either by capital subsidy under TMC

Scheme or by 5 per cent interest subsidy under theTUFS. The implementation of the National TextilesPolicy (NTxP), 2000 was also announced during thePlan period. It recommended, among other things,duty relief, concessions and special measure forprogrammes aimed at accelerating modernisationand growth of textile industries. It lays specialemphasis on modernisation of the weaving sectorby launching a programme for the induction of50,000 shuttle-less looms and 250,000 semi-automatic and automatic looms in the decentralisedpowerloom sector.

7.1.41 The Competition Bill, 2001 seeks to ensurefair competition in India by prohibiting trade practiceswhich cause appreciable adverse effect oncompetition in markets within India and, for thispurpose, provides for the establishment of a quasi-judicial body to be called the CompetitionCommission of India which shall also undertakecompetition advocacy for creating awareness andimparting training on competition issues.

REVIEW OF NINTH PLAN POLICY REFORMS

7.1.42 While formulating the Ninth Plan, severalareas were identified for urgent Government actionto realise a target of 8.2 per cent annual growthrate of industry. These were: disinvestment; closureof non-viable sick PSUs; removal of regionalimbalances in industrial development; review andrevamping of the BIFR mechanism; policy andprocedural reforms in the States; feedstock andpricing policy for fertilisers; review of the sugarpolicy, pharmaceutical pricing policy and small-scaleindustry (SSI) reservation (particularly for criticalexport-oriented industries such as toys, garmentsand leather goods) and review and modifications offood laws; and policy and fiscal measures fordeveloping the packaging industry for increasingexport of processed foods.

Foreign Direct Investment

7.1.43 Liberalised trade and an open door foreigninvestment policy ensure efficient allocation ofresources. India is an eminently attractivedestination for FDI in view of the stability of itsdemocratic polity, rule of law, steadily growingeconomy, low inflation rate, sizeable domestic

INDUSTRY

671

market, reservoir of skilled English speakingmanpower, well-developed social and economicinfrastructure, diversified industrial base and evolvedfinancial/capital market. According to the GlobalCompetitiveness Report, (World Economic Forum)India's current competitiveness ranking has movedup 6 notches from 42nd position in 1999 to 36thposition in 2001. The Report highlights licensing oftechnology, availability of suppliers the mediancorporate tax rates, export promotion and quality ofbusiness environment as some of India's positivefeatures. The share of emerging markets in inwardFDI has declined from 28 per cent in 1998 to thepresent 26.5 per cent, even though global FDI levelshave increased by 25 per cent in 1999 to reach $ 1trillion in 2000. India's share in total FDI flow todevelopment countries has been reported by the UNto be 1 per cent. While China gets FDI of roughly $40 billion a year, the flow to India remains $ 2 billion.FDI is driven more by economic environmentcomprising cost conditions, wage levels andindustrial capability, market size and infrastructureof export processing zones, than by directincentives or performance obligations.

7.1.44 Although a number of steps have beentaken to ensure a liberal FDI policy, there is scopefor substantial improvement in terms of bringing FDIunder the automatic route and expediting approvals.

Disinvestment of Central Public Enterprises

7.1.45 In 1998-99, the Government decided tobring down its shareholding in PSUs to 26 per cent(thus facilitating ownership changes, as wasrecommended by the Disinvestment Commission)in a majority of cases. The Government classifiedthe PSUs as strategic and non-strategic anddecided to retain majority holding in strategic PSUs.It was also decided that the interests of the workerswould be protected in all cases.

7.1.46 During the Ninth Plan, there had beensteady progress in the disinvestment of non-corePSUs. However, this has been linked with anassurance of job security for the employees orproviding opportunities for retraining andredeployment. The Disinvestment Commission setup in 1996 had earlier examined each of 58 PSUsreferred to it and advised the Government on the

extent of disinvestment feasible as well as the modeof disinvestment and the steps to be initiated. TheDisinvestment Commission had maderecommendations under five broad categories.These were: (a) strategic sale involving change inownership/management in 29 PSUs and trade saleof eight; (b) offer of sale of shares involving nochange in ownership/management in five PSUs; (c)deferment of disinvestments in eight PSUs and nodisinvestments in one; (d) closure/sale of assets infour PSUs; and (e) employee buy-out/strategic salein two. After the reconstitution of DisinvestmentCommission in July 2001, it has been decided thatall ̀ non-strategic' PSUs, including subsidiaries (butexcluding Indian Oil Corporation (IOC), Oil andNatural Gas Commission (ONGC) and GasAuthority of India Ltd or GAIL) will be referred tothe Commission for independent advice.

7.1.47 Since 2000-01, the Government pursuedthe policy of reducing its stake to below 26 per centin some non-strategic PSUs. There was increasingemphasis on strategic sales of and the entireproceeds from disinvestment/privatisation wasintended to be deployed in social sector,restructuring of PSUs and retirement of public debt.The salient features of the disinvestment policy in2000-01 are: to restructure and revive potentiallyviable PSUs; to close down those which cannot berevived; bringing down Government equity in allnon-strategic PSUs to 26 per cent or below, ifnecessary; to fully protect the interests of workers;to put in place mechanisms to raise resources fromthe market against the security of PSU assets forproviding an adequate safety net to workers andemployees; to establish a systematic policyapproach to disinvestment and privatisation and togive a fresh impetus to this programme by settingup a new Department of Disinvestment.

7.1.48 Accordingly the Government hasdecided to disinvest a substantial part of its equityin enterprises such as Indian Airlines, Air India,India Tourism Development Corporation (ITDC),Indian Petrochemicals Ltd. (IPCL), VideshSanchar Nigam Ltd. (VSNL), CMC, BharatAluminium Company Ltd (BALCO), HindustanZinc Ltd and Maruti Udyog Ltd. Where necessary,strategic partners would be selected through atransparent process.

TENTH FIVE YEAR PLAN 2002-07

672

7.1.49 The successfully privatised/disinvestedPSUs are: Lagan Jute Machinery CompanyLimited (LJMC), Modern Food Industries Limited(MFIL), BALCO, ; CMC, Hindustan TeleprintersLtd. (HTL); IBP Ltd., VSNL, nine hotels of ITDC,three hotels of the Hotel Corporation of India(HCI), Paradeep Phosphates Limited, Jessop andCo. Ltd. (subject to BIFR approval) and HindustanZinc Ltd.

7.1.50 Forty-seven PSUs (including a fewsubsidiaries) have been taken up for thedisinvestment between 1990-91 and 2001-02. Theproceeds realised amount to Rs. 26,738 croreagainst the target of Rs. 66,000 crore.

7.1.51 Out of these 47, strategic sales weredone in the case of only 12 companies. The totalface value of equity sold so far through strategicsale is Rs. 744.34 crore and the realisation ofthe order of Rs. 7,165 crore. The yearly benefitthat accrues to the public from these salesexceeds Rs. 824 crore. Considering the totalequity in Central PSUs or CPSUs (held by theCentral Government and the holding companies)as on 31 March 2000 is of the order of Rs. 78,484crore, equity sold through strategic sale so far isless than 1 per cent. If Rs. 7,165 crore could berealised by just selling 1 per cent of the total equity,the potential realisation by selling the total equityin all non-strategic CPSUs can be estimated atseveral lakh crores of rupees.

7.1.52 The emphasis on strategic sale, from1999-2000 onwards has started yielding excellentresults. The Price/Earning ratios obtained between1991 - and 1999, from sale of shares of highlyprofitable CPSUs ranged between 4.4 and 6.0whereas the P/E ratios obtained through strategicsales have been much higher, reaching up to 63 incase of the IBP disinvestment.

Closure of Non-revivable Sick PublicEnterprises

7.1.53 At present the process of rehabilitation/winding up of an PSEs is through the mechanism ofBIFR under SICA. BIFR examines various possibilitiesand approves revival plan for the sick PSUs orrecommend closure. The Companies (Amendment)

Bill, 2001, which will seek the establishment of theNCLT to address of sickness and bankruptcy hasbeen introduced in Parliament. The abolition of SICAbill was introduced in Lok Sabha in August, 2001. Asthese Bills get enacted the process of industrialrestructuring should become easier and faster.

Removal of Regional Imbalances in IndustrialDevelopment

7.1.54 The Growth Centres Scheme and TransportSubsidy Scheme were initiated as Centrally sponsoredschemes to promote industrialisation of backwardareas and promote industries in hilly, remote andinaccessible regions. The funding pattern of GrowthCentres envisaged an equity contribution of Rs. 10crore by the Centre, Rs. 5 crore by the concernedState, Rs. 4 crore (including Rs. 2 crore as equity)from financial institutions, Rs. 1 crore from nationalisedbanks and Rs. 10 crore as market borrowings. Thisadds up to Rs. 30 crore per Growth Centre. Of the 71identified Growth Centres, 68 have been approvedand of these 38 are functional and plot allotment hascommenced in 56. Two Growth Centres have beensanctioned for the Jammu and Kashmir and three inthe newly created States of Uttaranchal, Jharkhandand Chattisgarh. The respective State Governmentshave been asked to expedite progress on theremaining 16 Growth Centres. The non-performingGrowth Centres are in Orissa, Bihar, Andhra Pradeshand Pondicherry.

7.1.55 The implementation of the scheme hasbeen rather unsatisfactory. Too many GrowthCentres have been taken up at the same time,resulting in thin spread of resources. Besides, ithas not been possible to mobilise marketborrowings as envisaged in the original scheme.More importantly, industrially advanced Stateshave been able to mobilise financial andmanagerial resources and make good progress,whereas there has been not much progress inindustrially backward States/most backwardregions. Thus, instead of reducing regionalimbalances in industrial development, thescheme has only aggravated them.

7.1.56 Further, because of funds constraints,State Governments did not release funds to theimplementing agencies. After some mid-course

INDUSTRY

673

corrections, there has been an improvement in theimplementation of the scheme during the past twoyears. In order to overcome the difficulties faced inthe implementation of the scheme, it is proposed tomodify the Growth Centres Scheme by bringingchanges and allowing split location up to a maximumof three locations for hilly States and two for theother States. There is a proposal to transfer thescheme to the States along with funds.

The number of functional Growth Centres, duringthe last two years has increased from 26 to 38 andthe amount of Central assistance has increasedfrom Rs. 291 crore to Rs. 371 crore. The contributionof the State Government and their implementingagencies increased from Rs. 405 crore to Rs. 689crore in the same period. The number of industrialunits has also increased from 656 to 833, attractingcapital investment of Rs. 8,531 crore and creatingdirect employment for 28,233 persons, as on 31March 2002.

7.1.57 The Transport Subsidy Scheme wasintroduced in July 1971 to promote industries in hilly,remote and inaccessible areas of Jammu andKashmir, Himachal Pradesh, Sikkim, Andaman andNicobar Islands and Lakshadweep, the Darjeelingdistrict of West Bengal, eight hill districts of UttarPradesh and the northeastern States. Under thescheme, subsidy at rates ranging from 50 per centto 90 per cent on the transport cost incurred onmovement of raw materials and finished goods from/to designated rail heads/ports is provided to allindustrial units except plantations, refineries andpower generation units. The scheme works onreimbursement basis i.e. subsidy to eligible units isfirst disbursed by the States/ Union territoriesconcerned and the disbursement is claimed fromthe Centre.

7.1.58 The scheme has been extended up to 31March 2007 for the northeastern States and Sikkim.It was valid up to 31 March 2000 for other States. Aproposal to transfer the Transport Subsidy Schemeto States along with funds is under consideration ofthe Government.

7.1.59 Total disbursal under the scheme from 1April 1976 to 31 March 2002 is Rs. 706.77 crore.The major beneficiaries have been Himachal

Pradesh (Rs. 209 crore), Assam (Rs. 200.34 croreup to 31 March 2001), Jammu and Kashmir (Rs.29.34 crore) and the hill districts of Uttar Pradesh(Rs. 15.83 crore) besides the northeastern regionincluding Assam which received Rs. 403.36 crore.

7.1.60 The National Productivity Council (NPC)was asked to examine the impact of the schemeon the industrialisation process in the beneficiaryStates, including nature and pattern ofindustrialisation, size of unit, employmentgeneration and ancillarisation. The study coveredAssam, Himachal Pradesh, the hills districts of UttarPradesh, Jammu and Kashmir, Meghalaya,Mizoram, Nagaland for the 1989-90 to 1997-98period. The NPC study concluded that though therehas been industrial growth, it has been uneven. InHimachal Pradesh, the number of factories grew atan annual rate of 10.5 per cent, while Assam had amoderate growth of 1.59 per cent in number offactories, output (2.21 per cent) and employment(3.05 per cent). The employment generated bybeneficiary units in these remote, hilly andinaccessible areas is approximately for 25,600people. There has been expansion anddiversification in the units though ancillary units didnot develop significantly. There have been indirectbenefits also like infrastructure development andgeneration of income for the State Governmentsthrough other levies. The study also indicated theareas which require strengthening, in order toimprove implementation and reduce delays.

Review and Revamping of BIFR Mechanism

7.1.61 The present legal framework - the SICAunder which sick companies are referred to BIFRwas originally designed to provide sick companieswith assistance to allow them to restructure and tobe rehabilitated, thus forestalling closure and lossof employment. It has proved to be almostcompletely ineffective. It has provided unscrupulousmanagements with an extended period during whichall recovery action is stayed and the time gained inthe process is often used to siphon funds out ofsick companies making them un-revivable. Thisensures that companies that run into difficulties areinvariably driven into terminal sickness. At times,promoters may even perceive a benefit in pushinga company into sickness. Unfortunately, the Indian

TENTH FIVE YEAR PLAN 2002-07

674

financial and legal system lacks an effective systemfor enforcing recovery of debts through speedybankruptcy procedures with mechanism that wouldallow inefficient firms failing to service loans to bespeedily liquidated or taken over by a newmanagement. In order to solve the problem, theCompanies (Amendment) Bill 2001 was introducedin Parliament in August 2001 along with the Abolitionof Sick Industrial Companies (Amendment) Bill,2001.

Policy and Procedural Reforms in States

7.1.62 The process of liberalisation in theindustrial sector has advanced considerably at theCentre. Industrial licensing has been eliminated forall but six industries and the number of industriesreserved for the public sector has been reduced tothree. The remaining controls at the CentralGovernment level need to be reviewed for furtherliberalisation. Indian industry still suffers from aplethora of controls and regulations relating tomatters in the purview of State and these controlscumulatively impose a heavy burden of delay andeven harassment of entrepreneurs. A throughrevamping of these controls and procedures at theStates Government level would help create a climateconducive to Indian industry to flourish.

Feedstock and Pricing Policy for Fertilisers

7.1.63 With the introduction of Retention Pricecum Subsidy scheme (RPS), the country achievedself-sufficiency by the end of Ninth Plan to the extentof nearly 100 percent of urea and 85 percent incase of DAP. This price arrangement however hasencouraged the urea manufacturers to focus moreon claiming costs rather than controlling costs byenhancing production efficiency. The urea pricingpolicy parameter for VII and VIII pricing periods havebeen recommended by the Group of Ministers(GOM) headed by Deputy Chairman, PlanningCommission. Corresponding retention prices havebeen notified for most of the units. The ExpenditureReforms Commission (ERC) recommendation onrationalisation of fertiliser subsidy by introducinggroup based urea pricing is under examination alongwith other alternatives on a new urea pricing policy.In response to the import parity pricing of feedstock,a new pricing mechanism for hydrocarbons wasimplemented and oil companies started following

this from 9 July 2001. The NPK ratio which had gotdistorted to 10.0:2.9:1 during 1996-97 has sinceimproved to 6.9:2.9:1 in 1999-2000. It needs to bekept in mind that bio-fertilisers, micronutrients andorganic compost should remain an integral part ofbalanced fertiliser application and integrated nutrientmanagement. Use of these supplements needs tobe promoted by research, better marketing andcompetitive pricing.

Sugar Policy

7.1.64 The Government has taken a number ofimportant policy decisions as part of the reformprocess in the sugar sector. The sugar industry wassubjected to compulsory licensing at thecommencement of the Ninth Plan and wasdelicensed in September 1998. Some of thesedecisions are:

• Reduction of levy obligation of domestic sugarproducers from 40 per cent to 30 per cent witheffect from 1 April 2000, from 30 per cent to 15per cent from 1 February 2001 and from 15per cent to 10 per cent from 1 March 2002.

• Restructuring Sugar Development Fund Rules,1982 for providing loans at concessional ratesfor the rehabilitation of potentially viable sicksugar mills.

• The Government has also approved a proposalfor legislation to amend the SugarDevelopment Fund (SDF) Act,1982 for loansfor bagasse-based co-generation powerprojects, by-product utilisation and defrayingexpenditure on internal transport and freightcharges on export shipments of sugar. Thiswas being done to improve the viability of thesugar factories as also to augment the powergeneration in the country.

• Relaxation in controls on the sale of non-levy freesale sugar and substituting the monthly regulatoryrelease by quarterly regulatory release andallowing the sugar factories to sell up to 10 percent of the quarterly quota as additional quota.This has become effective from January 2002.

• Withdrawal of stockholding limits on wholesaledealers of sugar was done with effect from 7July 2000.

INDUSTRY

675

• Turnover limits on wholesale dealers wereabolished with effect from 20 August 2001.

• A notification under the Forward Contracts(Regulation) Act, 1952, allowing futures/forward trading in sugar was issued on 14 May2001.

Pharmaceutical Pricing Policy

7.1.65 The Pharmaceutical Policy, 2002, aims toensure abundant and good quality essentialpharmaceuticals at reasonable prices, strengthenindigenous capability for cost effective qualityproduction, reduce trade barriers and encourageR&D. Items appearing in the list of essential drugsissued by the Ministry of Health and Family Welfareand other items considered important on accountof their use in various health programmes, inemergency care etc. have been kept under the DrugPrice Control Order (DPCO) and will form the totalbasket from which selection of bulk drugs will bemade for price control. However, items like sera andvaccines and blood products have been excludedfrom DPCO. As per the new criteria, molecules witha turnover of less than Rs. 10 crore for the fiscalended March 2001 will not fall under DPCO, but adrug having a turnover between Rs. 10-25 croreand a single formulator having a market share ofover 90 per cent will be covered by the price controlorder. Further, a drug with a turnover of over Rs. 25crore and a single formulator and having a marketshare of over 50 per cent will be under price control.New drugs coming out of research from within thecountry would be off price control for the life of thepatent. It has been decided to permit up to 100 percent foreign equity under the automatic route so asto promote FDI. India, as a signatory to WTO, iscommitted to the introduction of a product patentregime in 2005. This will be a major change thatwill impact the Indian pharmaceutical industry. Theremay be a need for a review of the newly announcedPharmaceutical Policy 2002 to deal with thechanged scenario.

Review and Modification of Food Laws and Drugand Cosmetics Act

7.1.66 During the Ninth Plan, many provisionsof the food laws and their implementation strategyhave created hurdles in the way of growth and

development. The Prevention of FoodAdulteration Act, (1954) and Rules (1955) hasbeen a source of considerable harassment. Thestandards are unrealistic and there is moreemphasis on policing than on prevention ofadulteration. It has been recommended that thevarious food laws would need to be reviewed andsuitably modified at an early date. However, therehas been no appreciable progress in themodification of food laws. The Drugs andCosmetics Act, 1940 was reviewed so as toincorporate the provisions of World HealthOrganisation-Good Manufacturing Practices(WHO-GMP).

Policy And Fiscal Measures For ThePackaging Industry

7.1.67 The packaging industry for processedfoods, it has been observed, is yet to developand there is a wide gap between the indigenousand contemporary packaging practices of foodproducts. The cost of packaging is also very high.The Ninth Plan has recommended thatappropriate policy and fiscal measures be takento encourage scientific development of packagingindustry. However, there appears to be littleprogress towards this.

PERFORMANCE OF THE INDUSTRIAL SECTOR

7.1.68 The post-liberalisation period ischaracterised by three distinct phases ofindustrial activity. The first is the period after theannouncement of liberalisation of industrial andtrade policy in July 1991 till the start of rapidgrowth in 1993-94. The second phase recordeda high growth rate during 1993-94 to 1995-96.The third phase is one when industrial activityslowed down since 1996-97.

Growth Of Industry

7.1.69 The Ninth Plan proposed a target growthrate of 8.2 per cent (value added) for the industrysector. As against this, the actual growth rate(value added actual at factor cost) was 4.5 percent. The actual growth rates of various sub-sectors vis-à-vis targets at the start of the NinthPlan as well as revised targets after the Mid-Term

TENTH FIVE YEAR PLAN 2002-07

676

Appraisal are indicated in Table 7.1.5. The year-wise growth rates are shown in the Graph 7.1.6.

7.1.70 During the Ninth Plan period, a CompoundAnnual Growth Rate (CAGR) of 5 per cent in

industrial production was recorded compared to 7.3per cent during the Eighth Plan (Table-7.1.7). TheCAGR in manufacturing, mining and electricitygeneration during Ninth Plan were 5.3 per cent, 2.5per cent and 5.5 per cent respectively.

Table 7.1.5 : Value added growth rate in sub sectors of Industry in the Ninth Plan

Share of sub sectors Growth rate Revised targets Growth ratein 1999-2000(provisional) (value added) after Mid Term actual

at 1993-94 prices -target Appraisal (5 years) (value added)

Manufacturing 16.75 8.2 7.1 3.7

Electricity, Gas and Water 2.49 9.3 8.4 6.5

Mining 2.34 7.2 5.1 3.9

Construction 5.12 4.9 6.8 6.8

Table 7.1.7 : Annual growth rates of industrial production in major sectors of industry

(Base: 1993-94 = 100) (per cent)

Period Mining Manufacturing Electricity General

(Weight) (10.4) (79.4) (10.2) (100.0)

(11.5)* (77.1)* (11.4)* (100.0)*

1992-93 0.5 2.2 5.0 2.3

1993-94 3.5 6.1 7.4 6.0

1994-95 9.8 9.1 8.5 9.1

1995-96 9.7 14.1 8.1 13.0

1996-97 -1.9 7.3 4.0 6.1

1997-98 6.9 6.7 6.6 6.7

1998-99 -0.8 4.4 6.5 4.1

1999-2000 1.0 7.1 7.3 6.7

2000-01 3.7 5.3 4.0 5.0

2001-02 1.8 2.9 3.1 2.8

Compound Annual Growth Rate (CAGR) 1997-2002 2.5 5.3 5.5 5.0

Growth rates from 1994-95 onwards are based on IIP; Base : 1993-94=100 and those for earlier years are based on IIP;Base : 1980-81=100.*Relates to weights for IIP Base:1980-81=100

INDUSTRY

677

7.1.71 Table 7.1.8 shows the annual average rateof growth recorded in industry groups on use-basedclassification.

7.1.72 Industrial production, measured by theindex of industrial production (IIP), registered agrowth rate of 6.7 per cent in 1997-98. This highergrowth rate compared to previous year was onaccount of improved performance of the mining andelectricity sectors. In 1998-99, the industrial growthrate was merely 4.1 per cent because of poorperformance by the mining and manufacturingsectors. Use-based growth rate indicates thatgrowth in basic goods, intermediate goods andconsumer goods in 1998-99 declined to 1.6 per centand 6.1 per cent and 2.2 per cent respectively.Industrial production had shown a distinctimprovement (6.7 per cent growth) in 1999-2000.The improvement was particularly noticeable inmanufacturing and electricity generation.

7.1.73 The IIP registered a significantly lowergrowth rate of 5 per cent in 2000-01 compared toa growth rate of 6.7 per cent in 1999-2000. Growthrates also fell in both the manufacturing andelectricity sectors from 7.1 per cent and 7.3 percent in 1999-2000 to 5.3 per cent and 4 per centrespectively in 2000-01. However, the miningsector recorded a higher growth rate of 3.7 percent in 2000-01 compared to 1 per cent in 1999-2000. Trends in 2001-02 in overall industrialgrowth and by sectors suggest an all roundslowdown in industrial activity. A growth rate of2.9 per cent in the manufacturing sector in 2001-02 was recorded. Similarly, the electricitygeneration growth rate of 3.1 per cent was alsosignificantly lower than 4 per cent growthrecorded during the last year. The mining sectorgrowth of 1.8 per cent was also significantly lowerthan the 3.7 per cent recorded during the lastyear.

Table 7.1.8Growth Rates Of Industrial Production By Use-based Classification

(Base : 1993-94=100) (per cent)

Sectors (Weight) 1995- 1996- 1997- 1998- 1999- 2000- 2001-96 97 98 99 2000 01 02

Basic Goods 35.5 10.8 3.0 6.9 1.6 5.5 3.9 2.8

Capital Goods 9.3 5.3 11.5 5.8 12.6 6.9 1.8 -3.9

Intermediate Goods 26.5 19.4 8.1 8.0 6.1 8.8 4.7 1.6

Consumer Goods 28.7 12.8 6.2 5.5 2.2 5.7 8.0 6.0

of which (Consumer Durables) (5.4) (25.8) (4.6) (7.8) (5.6) (14.1) (14.5) 11.5

(Consumer Non-Durables) (23.3) (9.8) (6.6) (4.8) (1.2) (3.2) (5.8) 4.0

IIP (Index of Industrial Production) 100.0 13.0 6.1 6.7 4.1 6.7 5.0 2.8

Note : The indices are based on revised item wise weights.

TENTH FIVE YEAR PLAN 2002-07

678

7.1.74 Table 7.1.9 shows the annual average rateof growth recorded in industry groups at the twodigit level during the Eighth Plan and Ninth Planperiods.

7.1.75 The group-wise industrial growth rate(Table 7.1.9) indicate that five out of 17 industrygroups, accounting for 24.17 per cent share in IIP,recorded a CAGR of more than 8 per cent during1997-2002. Three groups, accounting for 19.28 percent share in IIP, recorded 6 to 8 per cent CAGRduring 1997-2002. Ten industry groups, accountingfor 35.9 per cent share in IIP, recorded less than 6per cent growth rate.

7.1.76 Basic metal and alloys, cotton textiles,wood and wood products, paper and paper productsand transport equipment experienced lower growth

rates in Ninth Plan compared to Eighth Plan period.Sectors like non-metallic mineral products, man-made fibre textile (except cotton), leather products,rubber, plastics and petroleum products, chemicaland chemical products achieved higher growth ratesin the Ninth Plan compared to Eighth Plan period.

Internal and External Factors for the Slowdown

7.1.77 The industrial slowdown is widespread,covering all broad sectors e.g. manufacturing,electricity and mining and all end use based groupssuch as capital goods, intermediate goods andconsumer goods (both durable and non-durables).The slowdown in domestic and global demandappeared to be a major factor constraining industrialgrowth. Another major reason has been the declinein investment, noticeably by private sector.

Table 7.1.9Trends in The Performance of Industrial Sub-Sectors

Annual Growth Rate (Per Cent)

Industry Industry Name Weight 1997- 1998- 1999- 2000- 2001- CAGR AverageCode in IIP 98 99 2000 01 02 1997- growth

2002 VIII Plan

20-21 Food Products 9.08 -0.40 0.70 4.20 10.12 -1.68 2.49 3

22 Beverages & Tobacco 2.38 19.40 12.90 7.60 4.32 12.18 11.17 11

23 Cotton Textiles 5.52 2.40 -7.70 6.70 2.91 -2.20 0.29 4

24 Wool, Silk & Man-made Fibre 2.26 18.50 2.80 11.90 5.81 4.40 8.53 0Textiles (Except Cotton)

25 Jute Textiles 0.59 16.90 -7.30 -0.90 0.76 -5.86 0.37 0

26 Textiles Products 2.54 8.50 -3.50 2.00 4.04 2.40 2.60 0

27 Wood & Wood Products 2.70 -2.60 -5.80 -16.20 2.86 -11.03 -6.79 4

28 Paper & Paper Products 2.65 6.90 16.00 6.30 -9.14 2.99 4.29 9

29 Leather & Fur Products 1.14 2.20 8.10 13.80 10.70 5.93 8.07 5

30 Chem. & Chem. Products 14.00 14.40 6.60 10.00 7.29 4.76 8.56 7

31 Rubber, Plastic, Petroleum 5.73 5.20 11.30 -1.10 11.81 11.08 7.55 3

32 Non-metallic Mineral Products 4.39 13.40 8.30 24.40 -1.18 1.37 8.89 6

33 Basic Metals & Alloys 7.45 2.60 -2.50 5.00 1.84 4.01 2.16 10

34 Metal Products & Parts 2.81 7.90 17.00 -1.20 15.02 -9.59 5.34 5

35-36 Machinery & equipment 9.57 5.80 1.50 17.70 7.29 1.02 6.51 6-8

37 Transport equipment 3.98 2.50 20.10 5.70 -1.96 6.83 6.40 13

38 Other Manufacturing Industries 2.56 -1.30 1.00 -16.00 11.65 8.86 0.35 1

Source : Central Statistical Organisation.Note : The indices from April 1998 onwards are based on revised weights.

INDUSTRY

679

7.1.78 The industrial deceleration was due to anumber of structural and cyclical factors such asnormal business and investment cycles, a lack ofboth domestic and external demand, continuing highreal interest rates, infrastructure bottlenecks inpower and transport, lack of reforms in land andlabour markets, inherent adjustment lags resultingfrom industrial restructuring through merger andacquisitions, and delays in establishing appropriateinstitutional and regulatory frameworks in some keysectors.

7.1.79 The difficulties caused by internalconstraints were exacerbated by the slow growthin the world economy, which contributed to asubstantial slowdown in manufactured exports.Further, the 11 September 2001 terrorist attacksand related events slowed down the recoverythrough lack of external demand and adverseimpact on air transport, communications andtourism.

Gross Capital Formation and Sanctions by AllFinancial Institutions

7.1.80 The CAGR of gross capital formation(GCF) at constant prices (1993-94 prices) duringthe first four years of the Ninth Plan was 7.92per cent compared to 7.38 per cent during 1993-97. The CAGR of GCF for the public sector atconstant prices during the first four years of theNinth Plan increased to 6.22 per cent comparedto 1.04 per cent during 1994-97. In the privatecorporate sector, the CAGR of GCF during thefirst four years of the Ninth Plan has beennegative at (-) 1.24 per cent compared toimpressive 18.91 per cent during 1993-97.

7.1.81 The fall in interest rates has been lowerthan fall in inflation in recent years. As a result, realinterest rates continue to remain high. Comparedwith a real prime lending rate of 2.4 per cent in 1994-95, it was around 7.3 per cent in 2001. The CAGRof sanctions by All Financial Institutions (AFIs)during the first four years of the Ninth Plan was21.21 per cent compared to 19.53 per cent in theEighth Plan. The CAGR of disbursement in thecorresponding periods were 14.30 per cent and21.28 per cent respectively.

Investment Intentions and Foreign DirectInvestment

7.1.82 A total of 14,969 Industrial EntrepreneursMemoranda (IEM) and 911 Letter of Intents (LOI)were filed between 1997 and October 2001.Investment intentions in terms of number under IEMreduced from a cumulative level of 25,307 duringthe Eighth Plan period to 14,969 during the NinthPlan. These 14,969 IEMs correspond to investmentof Rs. 3,91,292 crore and employment generationof 26.42 lakh. The reported implementation of IEM(out of 14,969) is however, only 1,931 numbersinvolving investment of Rs. 79,905 crore indicatingimplementation of only 12.9 per cent in terms ofnumber and 20 per cent in terms of investment.The 911 LOIs proposed an investment of Rs. 15,906crore and employment of 1.84 lakh.

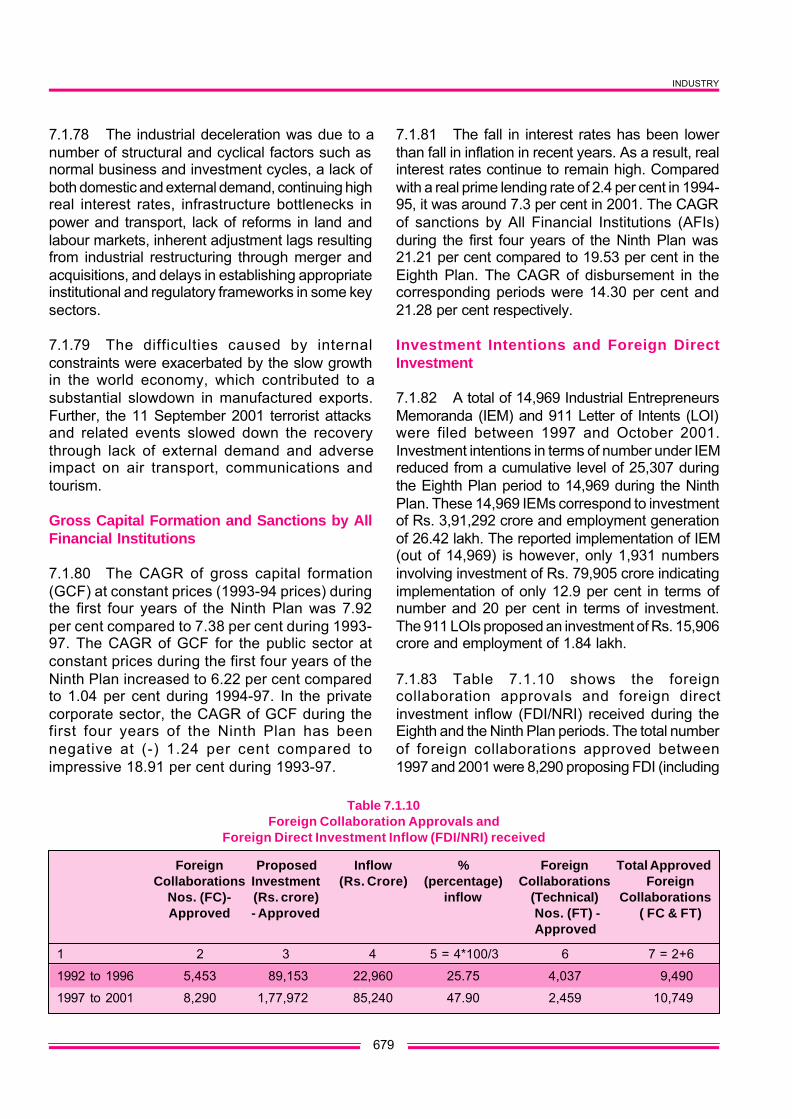

7.1.83 Table 7.1.10 shows the foreigncollaboration approvals and foreign directinvestment inflow (FDI/NRI) received during theEighth and the Ninth Plan periods. The total numberof foreign collaborations approved between1997 and 2001 were 8,290 proposing FDI (including

Table 7.1.10Foreign Collaboration Approvals and

Foreign Direct Investment Inflow (FDI/NRI) received

Foreign Proposed Inflow % Foreign Total ApprovedCollaborations Investment (Rs. Crore) (percentage) Collaborations Foreign

Nos. (FC)- (Rs. crore) inflow (Technical) CollaborationsApproved - Approved Nos. (FT) - ( FC & FT)

Approved

1 2 3 4 5 = 4*100/3 6 7 = 2+6

1992 to 1996 5,453 89,153 22,960 25.75 4,037 9,490

1997 to 2001 8,290 1,77,972 85,240 47.90 2,459 10,749

TENTH FIVE YEAR PLAN 2002-07

680

ADRs /GDRs/FCCBs) of Rs. 1,77,972 crore. Theactual inflow of FDI (including ADRs/GDRs/FCCBs)during the period was Rs. 85,240 crore as againstapproval for Rs.1,77,972 crore representing anoverall inflow of 47.9 per cent. A major change inquantum of foreign technology transfer proposals(i.e. not involving FDI) during the Ninth Plancompared to Eighth Plan is observed. Between 1997and 2001, only 2,459 technology transfer proposalswere approved compared to 4,037 numbers from1992 to 1996. This may be partly because of lackof willingness to transfer technology withoutownership control and costly technology importsmay also not be offering the benefits which wereavailable in restrictive environment.

Export

7.1.84 The CAGR of exports during the first fouryears of the Ninth Plan was 7.42 per cent comparedto 13.38 per cent during the Eighth Plan. The shareof manufactured goods in overall exports was 78per cent during the Ninth Plan vis-à-vis 75 per centduring the Eighth Plan. Engineering goodsconstitute 19 per cent within the manufacturedgoods. The growth of manufactured goods however,has been slower in the Ninth Plan compared to theEighth Plan. A medium term export strategy,unveiled in January 2002 to provide a quantum jumpto exports in the next five years, provides a mix ofmacro policies and sector-specific policies indicatingattainable goals. The CAGR of imports during firstfour years of the Ninth Plan was 6.6 per centcompared to 15.05 per cent during the Eighth Plan.The import of capital goods, which was 16.66 percent in 1997-98, declined to a level of 15.9 per cent

in 2000-01. The CAGR of capital goods importduring the first four years of the Ninth Plan periodwas (-) 3 per cent compared to 18.58 per cent duringthe Eighth Plan. A positive development during 2001-02 has been the reversal of the trend in import ofcapital goods which have increased by 6.6 per centduring April-October 2001. The share of importrelated to export items has been steady in the rangeof 15-16 per cent over the Ninth Plan period.

Employment Situation In The ManufacturingSector

7.1.85 Table 7.1.11 shows the employmentsituation in organised manufacturing in theprivate and public sectors. The organisedmanufacturing sector employs approximately 23-24 per cent of total manpower. The role of thepublic sector as a provider of employment hassharply reduced during the Ninth Plan period. Atthe same time, there was no appreciable growthin employment in the private sectormanufacturing. In terms of total numbers, theemployment has been stagnant in manufacturingsector from 1996 to 2000.

SECTORAL PROFILE OF THE TENTH PLAN

Iron and Steel Sector

7.1.86 The PSUs of the Ministry of Steel are: SteelAuthority of India Ltd. (SAIL), Rashtriya Ispat NigamLtd. (RINL), Sponge Iron India Ltd. (SIIL), HindustanSteelworks Construction Ltd. (HSCL), MECON Ltd.,Bharat Refractory Ltd. (BRL), MSTC Ltd., and FerroScrap Nigam Ltd. (FSNL).

Table 7.1.11Employment situation in Organized manufacturing

(in lakh)

Manuf. Manuf. Total Employment Employment Total % (percentage)(Private (Public Employment (in public (in private Employment Employmentsector) Sector) in manufacturing Sector) Sector) in organised in organised

Sector manufacturing

1991 44.81 18.52 63.33 190.57 76.77 267.34 23.69

1996 50.49 17.38 67.87 194.29 85.12 279.41 24.29

2000 50.85 15.31 66.16 193.14 86.46 279.60 23.66

Source : Economic Survey, 2001-02 Ministry of Finance

INDUSTRY

681

7.1.87 Some of the PSUs have had the advantageof capital restructuring in the Ninth Plan. The profitmargins of the private and public sector steel-making units were hit by the general economicslowdown resulting in depressed domestic demandand stagnant market conditions, protectionistmeasures in the developed countries, liberalisationof trade, removal of entry barriers, reduction inCustoms duty on imports of steel items etc. WhileRINL and SIIL have shown a relatively betterperformance, SAIL continues to make losses.Therefore, priority needs to be given to strategieswhich would ensure long-term as well as short-termprofitability of the PSUs. The removal of entrybarriers has attracted relatively large privateinvestment in the private sector. This could beattributed to liberalisation and policy reforms. Therewas a sudden spurt in investment during the firsthalf of the Ninth Plan. However, due to recessionduring the latter half of the 1990s, the investmentalready made as well as committed is not yieldingthe desired results.

7.1.88 The strategies relied upon during the NinthPlan included cost reduction, rightsizing ofmanpower, stabilisation of production, sale of idleassets, sale of non-core assets, identification andclosure of uneconomic units, focus on corecompetence, reduction in input-cost, ensuringmaximisation of output per unit, improvement inoperational efficiency, enhancement in productivityper man hour and achieving the optimum productmix.

7.1.89 Research and Development (R&D) in theiron and steel sector is carried out mainly by thesteel plants, national research laboratories andacademic institutions. Around Rs. 80 crore is spentannually on R&D, which is only about 0.2 per centof the total turnover of the steel Industry in thecountry as against approximately 3 per cent inadvanced countries. To encourage R&D activity inthe country, the Government has decided to spendup to Rs. 150 crore per year from the SteelDevelopment Fund (SDF) on R&D.

7.1.90 As the Indian economy is going through arecession, its adverse impact would be felt on theiron and steel sector. The growth of domesticdemand for finished steel during the Tenth Plan

could be at the modest rate of about 6.25 per cent.The apparent consumption of finished steel during2001-02 was estimated to be around 27 millionmetric tonnes (mmt). This is expected to rise to 38mmt by the terminal year of the Tenth Plan (2006-07). While imports would be confined to two milliontonnes (mt), the scope for exports depends uponthe competitiveness of Indian steel in theinternational market. The threat of dumping of steelin the domestic market could continue because offalling prices in the international market.

7.1.91 Due to general slowdown in the major steelconsuming sectors and restrictions imposed bymajor steel importing countries, there is excesscapacity in the domestic steel manufacturing sector.Therefore, no additional capacity is likely to becreated in the Tenth Plan, particularly in the hot rolledproducts.

Capital goods and Engineering Industry

7.1.92 The engineering industry comprises ofindustries manufacturing engineering goods suchas metal products, office machinery, electronicgoods etc., in addition to capital goodsmanufacturing industry. The capital goods industryas covered in the IIP comprises 53 industry sectors.The main sectors are machine-tools, industrialmachinery, electrical machinery, shipbuilding, dieselengines and commercial vehicles etc.

7.1.93 None of the industry sectors under capitalgoods attract any industrial licensing provisions and100 per cent FDI is allowed under the automaticroute.

7.1.94 During the first four years of Ninth Plan,the capital goods sector registered a CAGR of6.71 per cent. The sector grew at an impressivegrowth rate of 12.6 per cent in 1998-99. However,with the slackening of demand in different sectorsof economy, the growth rate reduced to merely1.8 per cent in 2000-01. The sector registered anegative growth rate of (-) 3.9 per cent during2001-02.

7.1.95 With the abolition of quantitativerestrictions on import of capital goods since 1991,and emphasis on modernisation in different

TENTH FIVE YEAR PLAN 2002-07

682

manufacturing sectors, the share of imported capitalgoods in gross fixed assets (GFA) increased from12.2 per cent in 1993-94 and touched a peak of 20.8per cent in 1995-96. This trend has, however,reversed since 1996-97. The share of importedcapital goods in GFA decreased to 17.6 per cent in1999-2000 within the overall manufacturing sector.The propensity to import in certain segment ofindustries like textiles, electrical machinery,automobile, auto-ancillary and leather products,however, have been very high. The share ofimported capital goods in these segment ofindustries varies in the range of 20-50 per cent.

7.1.96 The intensity of uses of importedequipment is on the lower side in chemicalsmanufacturing barring a few sectors like alkalies,plastic products and fertilisers. Indian industrialmachinery manufacturers have the capability tomanufacture a variety of unit equipments ofstringent specifications required for the chemicalindustry. Similarly, ferrous and non-ferrous metalmanufacturing industries largely depend onindigenous equipment except for some tailor-madeequipment.

7.1.97 Industry sector-wise FDI inflow (excludinginflows under non-resident Indian (NRI) directinvestment and inflows due to acquisition of sharesunder Section 5 of the Foreign ExchangeManagement Act (FEMA), 1999 indicate that inflowsto engineering sector between 1997-98 and 2000-01 has been to the tune of $ 1,607 millionrepresenting 19.02 per cent of FDI inflows. The FDIinflows in the electronics and electrical equipmentsector during first four years of the Ninth Plan hasbeen $ 1,258 million representing 14.89 per cent oftotal inflows. However, the increase in GFA in thecapital goods sector has not kept pace with themanufacturing sector.

7.1.98 The industry has undergone restructuringby phasing out certain lines of production andclosure of some unviable units. The machine toolssector has focused on certain specific areas andthere is increasing trend of segmentation in it.

7.1.99 Barring a few exceptions, PSUsmanufacturing capital goods have been facingserious competitive pressure and many of them

were referred to the BIFR. The process ofdisinvestment in many of these PSUs is underway. Bharat Heavy Electricals Ltd. (BHEL) hashowever, operated profitably despite stiffcompetition in the power equipmentmanufacturing sector. They have initiated topackage their equipments with limited financialparticipation also in line with global trends. The shareof Hindustan Machine Tools (HMT) in the machinetools sector reduced to 35 per cent in 2000-01. Thecompany is on the revival path and is in the processof being disinvested after financial restructuring in1997. The three issues concerning the capital goodsindustry are: (i) high cost structure of industrybecause of low level of production, lack ofspecialisation etc., something the industry wouldneed to address; (ii) need to encouragemodernisation and R&D to withstand competition;and (iii) unfavourable duty structure particularly zerocustoms duty on import of items for certain sectors.

Ship-building and Ship-repair Sector

7.1.100 There are 28 shipyards in the country, 19of them in the private sector. Four public sectorshipyards two under the Ministry of Shipping andtwo under the Ministry of Defence are capable ofbuilding large ocean-going vessels. The annualturnover of the shipbuilding and ship repair industryis approximately Rs. 2,000 crore and it employsaround 31,000 persons.

7.1.101 The two public sector shipyards under theMinistry of Shipping – Hindustan Shipyard Ltd.(HSL) and Cochin Shipyard Ltd. (CSL) – constitute25 per cent of the industry turnover, i.e. an annualturnover of approximately Rs. 450 crore. Theemployee strength in CSL, HSL and Hooghly Dockand Port Engineers Ltd. (HDPE) is approximately7,800. The three shipyards under the Ministry ofDefence – Mazgaon Dock Ltd. (MDL), GardenReach Shipbuilders & Engineers Ltd (GRSE) andGoa Shipyard Ltd.(GSL) – build a variety of shipsand vessels primarily for Indian Navy and CoastGuard.

7.1.102 The assessed production capacity of fourlarge PSUs constitute 95 per cent of the industryturnover. The present annual shipbuilding capacityin India is 0.15 million compensated gross tonnage

INDUSTRY

683

(CGT), vis-à-vis 20 million CGT globally. As such,the Indian shipbuilding capacity is less than one percent of the global capacity. The global shipping andshipbuilding industry have advanced considerablyin the last 10 years, while the Indian industry hasbeen stagnant. The trend is towards high capacitycontainerships, cargo ships, tankers so as toachieve competitiveness in tariff. These trends havenecessitated modernisation in ports as well asshipbuilding/repairing facilities. Despite providing acompetitive policy environment in India (i.e. statusof 100 per cent export-oriented units (EOU) to theship repair industry), the industry could not grow tothe expected levels. The main constraints seem tobe lack of infrastructural and managerial capacity.

7.1.103 The overall performance of theshipbuilding and ship repair industry during the NinthPlan has improved. As a matter of policy, emphasiswas given to ship-repair activity by the yards toimprove their financial performance. CSL has beena profit-making yard during the Ninth Plan period.The Hindustan Shipyard Ltd., however, could notimprove the performance even after financialrestructuring. The Committee of Secretaries hasrecommended the closure of the HDPE. Indianshipyards however, find it difficult to cope withcompetition from abroad, the main reasons beinglack of design-base, very high cost of productionand long delivery periods. Further, the shipbuildingindustry is cyclical in nature and, therefore, the shipbuilders usually undertake ship repair activitiesduring the downward trend in shipbuilding.

7.1.104 The main policy issues concerning theshipbuilding and ship repair sector arecontinuation of the Shipbuilding Subsidy Schemeand budgetary support for the R&D Scheme. TheShipbuilding Subsidy Scheme is meant for PSUsmanufacturing ocean-going vessels but is notdirectly linked to any specific objectives to beattained by the shipyards. The desirability ofcontinuation of this Subsidy Scheme would needto be looked into.

7.1.105 Classification societies are involved fromthe initial stage of ship design and shipbuilding asa third party certification agency. With the changingtechnological environment, increasing applicationof information technology and changes in safety

norms, it is imperative for shipyards to keep pacewith such developments to meet emergingclassification standards. The National Ship Designand Research Centre (NSDRC), Vishakapatnam,which was set up as a registered society becamefully operational in May 1993. NSDRC is presentlyinvolved in a diversified range of activities in theshipbuilding and marine industry. In the abovecontext, the society may primarily focus on theshipbuilding sector. The R&D Scheme in theshipbuilding sector may cover projects for industry-wide improvement in knowledge base,standardisation and skill development.

7.1.106 During the Tenth Plan, emphasis would begiven on productivity improvement in theshipbuilding sector and to have a more balancedapproach to the development of shipbuildingcapabilities in addition to business focus in shiprepair capabilities. There is a case for theprivatisation/disinvestment of public sectorshipyards to achieve these objectives.