chapter17 managing domestic risk

TRANSCRIPT

CONTEMPORARY FINANCIAL MANAGEMENT

Chapter 17:

Managing Domestic Risk

INTRODUCTION This chapter examines the characteristics and valuation of

options and option-related financing

It explores the concepts necessary to evaluate the impact that decisions to issue or purchase these type of securities have on shareholder wealth

2

DERIVATIVE SECURITIES

As the name implies, all derivative securities derive their price from some underlying asset

Derivative securities provide a mechanism whereby companies can: Lay-off risk they don’t want Assume additional risk, with the expectation of earning a

return

3

BASIC TYPES OF DERIVATIVES

Options

Futures and forwards

Swaps

4

TYPES OF OPTION-LIKE SECURITIES

Calls and puts

Convertible fixed-income securities

Warrants

Bond refunding

Rights offering

5

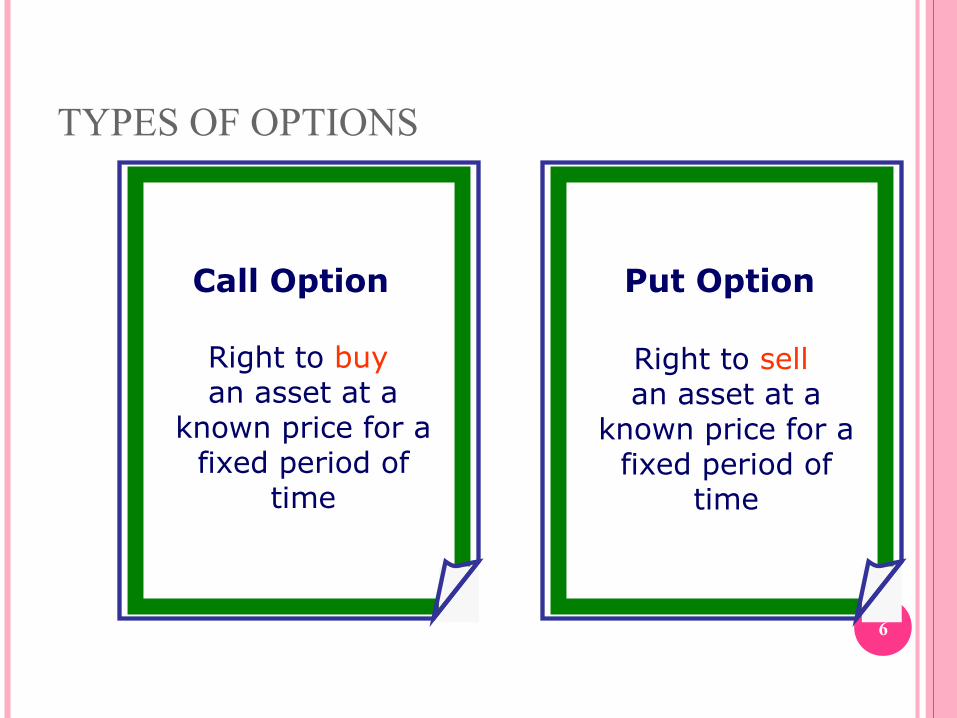

TYPES OF OPTIONS

6

Call Option

Right to buy an asset at a

known price for a fixed period of

time

Put Option

Right to sell an asset at a

known price for a fixed period of

time

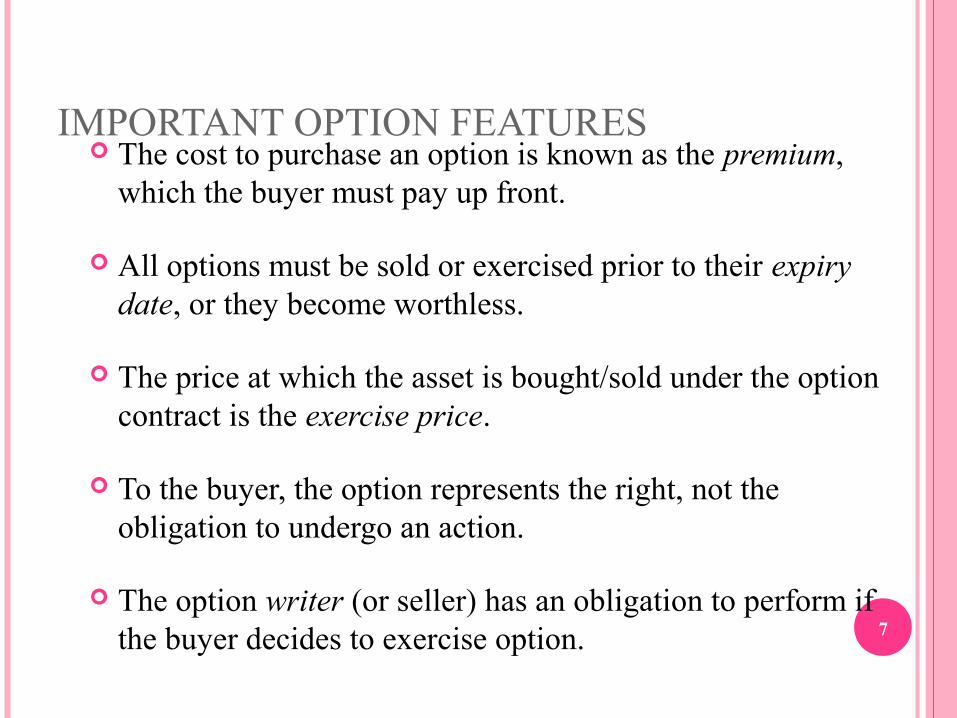

IMPORTANT OPTION FEATURES The cost to purchase an option is known as the premium,

which the buyer must pay up front.

All options must be sold or exercised prior to their expiry date, or they become worthless.

The price at which the asset is bought/sold under the option contract is the exercise price.

To the buyer, the option represents the right, not the obligation to undergo an action.

The option writer (or seller) has an obligation to perform if the buyer decides to exercise option. 7

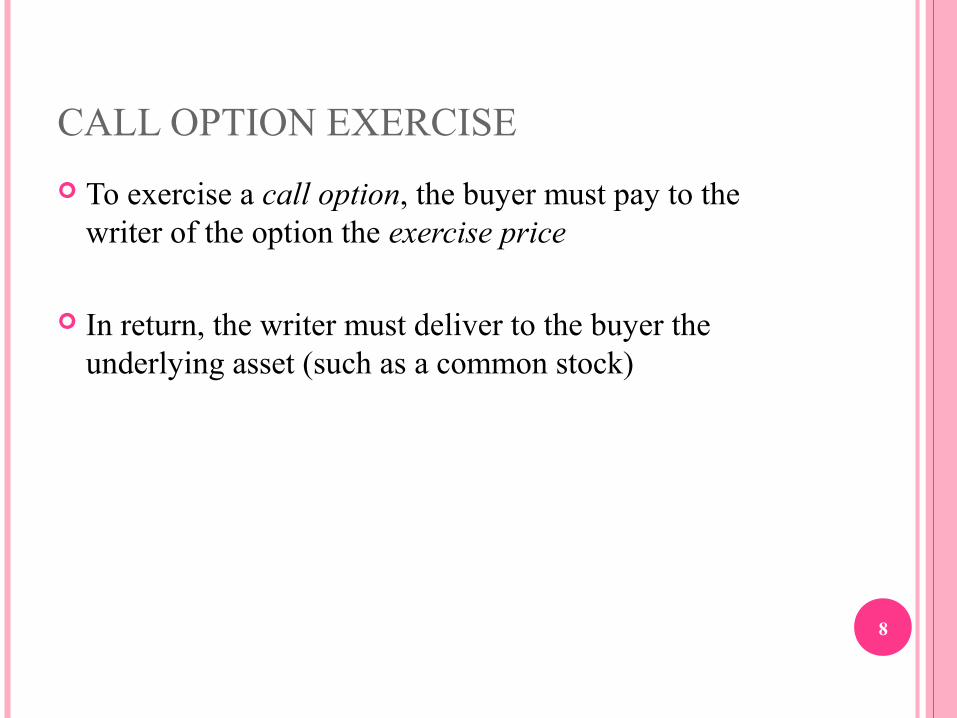

CALL OPTION EXERCISE

To exercise a call option, the buyer must pay to the writer of the option the exercise price

In return, the writer must deliver to the buyer the underlying asset (such as a common stock)

8

PUT OPTION EXERCISE

To exercise a put option, the buyer must deliver to the writer the underlying asset (such as a common stock)

In return, the writer must pay to the buyer the exercise price

9

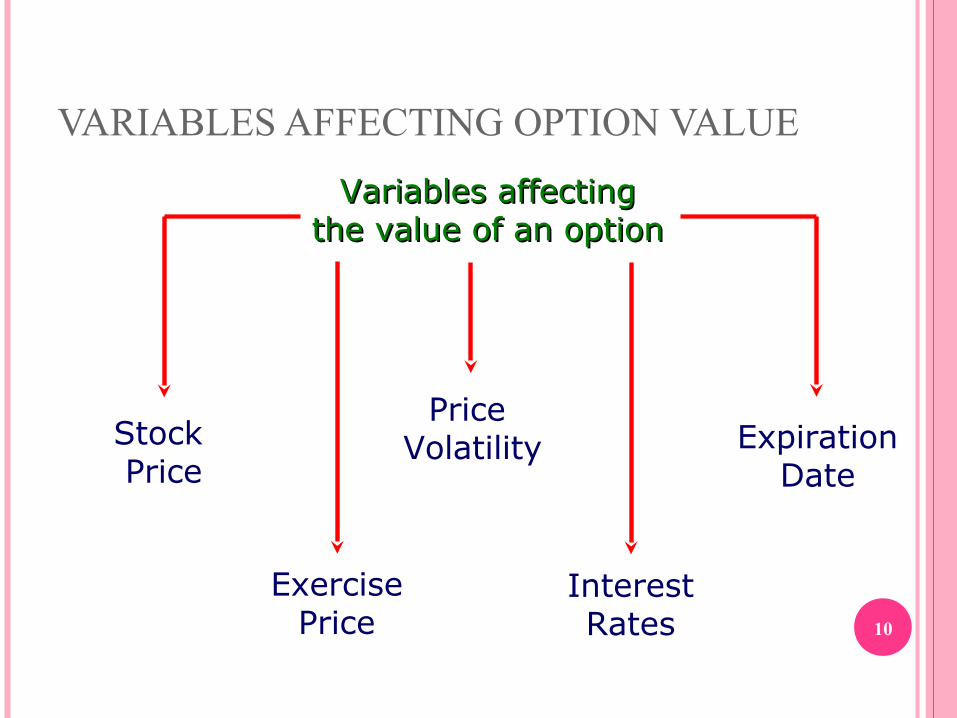

VARIABLES AFFECTING OPTION VALUE

10

Variables affectingVariables affectingthe value of an optionthe value of an option

Stock Price

ExpirationDate

Price Volatility

InterestRates

ExercisePrice

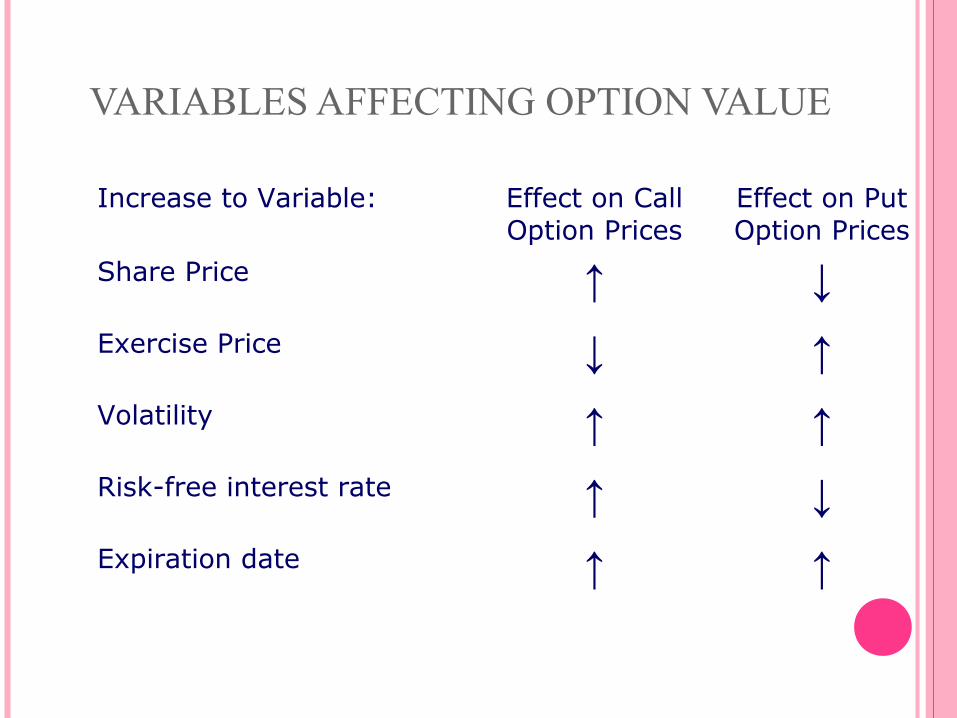

VARIABLES AFFECTING OPTION VALUE

Increase to Variable: Effect on Call Option Prices

Effect on Put Option Prices

Share Price ↑ ↓Exercise Price ↓ ↑Volatility ↑ ↑Risk-free interest rate ↑ ↓Expiration date ↑ ↑

11

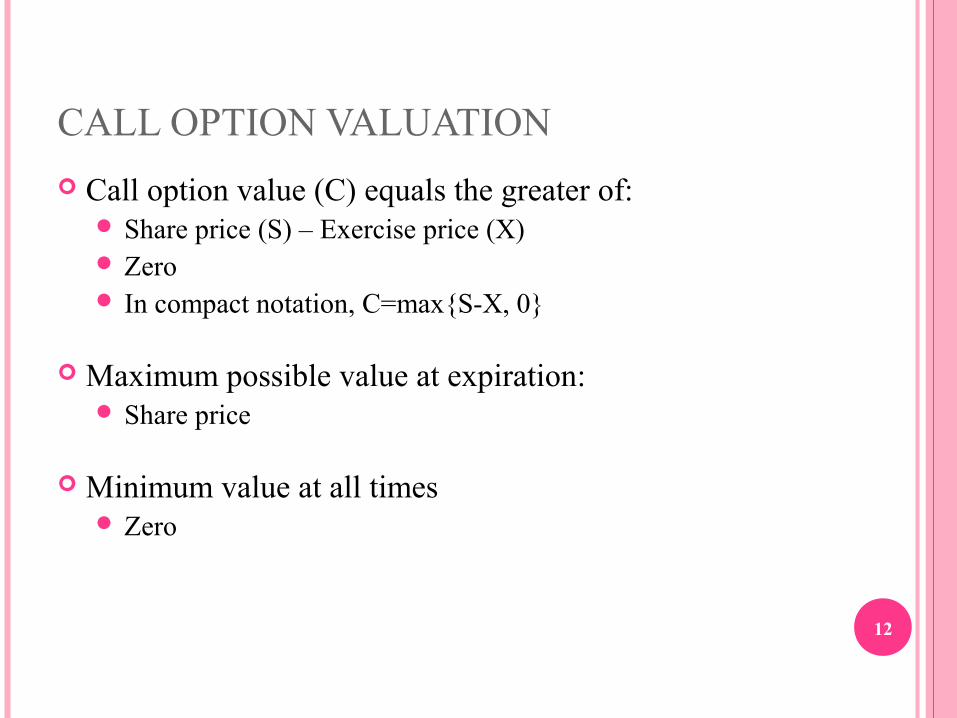

CALL OPTION VALUATION

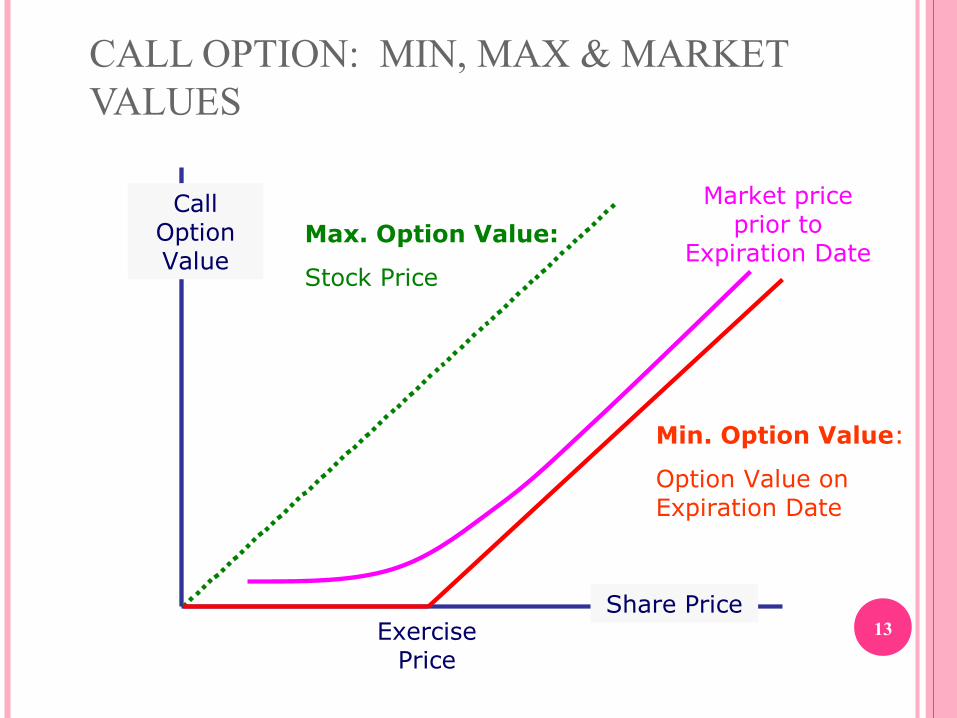

Call option value (C) equals the greater of: Share price (S) – Exercise price (X) Zero In compact notation, C=max{S-X, 0}

Maximum possible value at expiration: Share price

Minimum value at all times Zero

12

CALL OPTION: MIN, MAX & MARKET VALUES

13

Max. Option Value:

Stock Price

Min. Option Value:

Option Value on Expiration Date

Market price prior to

Expiration Date

Exercise Price

Share Price

Call Option Value

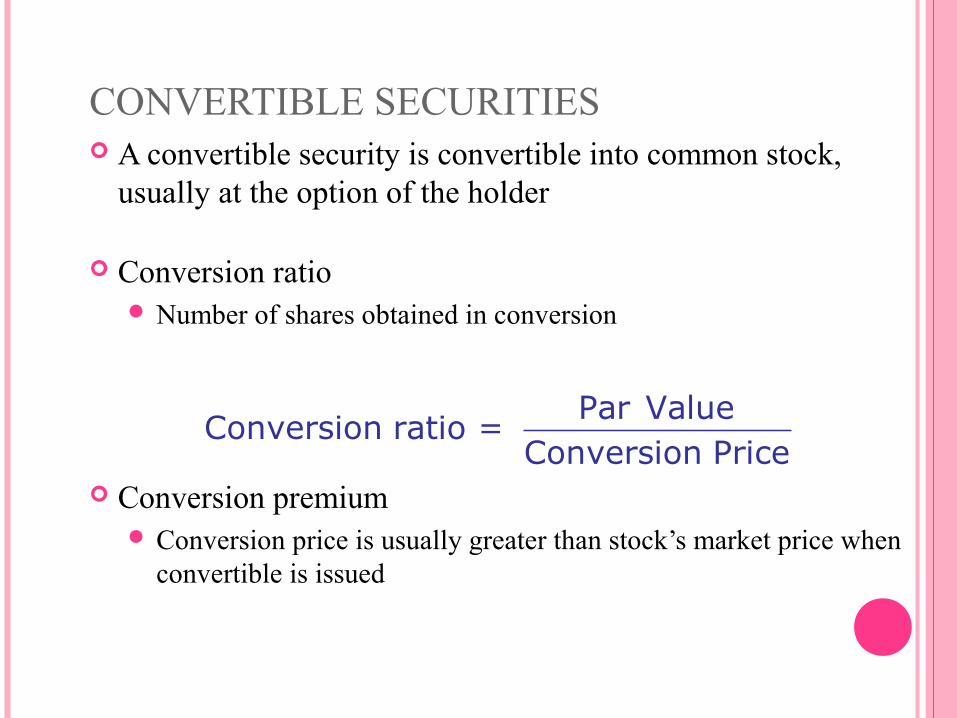

CONVERTIBLE SECURITIES A convertible security is convertible into common stock,

usually at the option of the holder

Conversion ratio Number of shares obtained in conversion

Conversion premium Conversion price is usually greater than stock’s market price when

convertible is issued

Par ValueConversion ratio =

Conversion Price

14

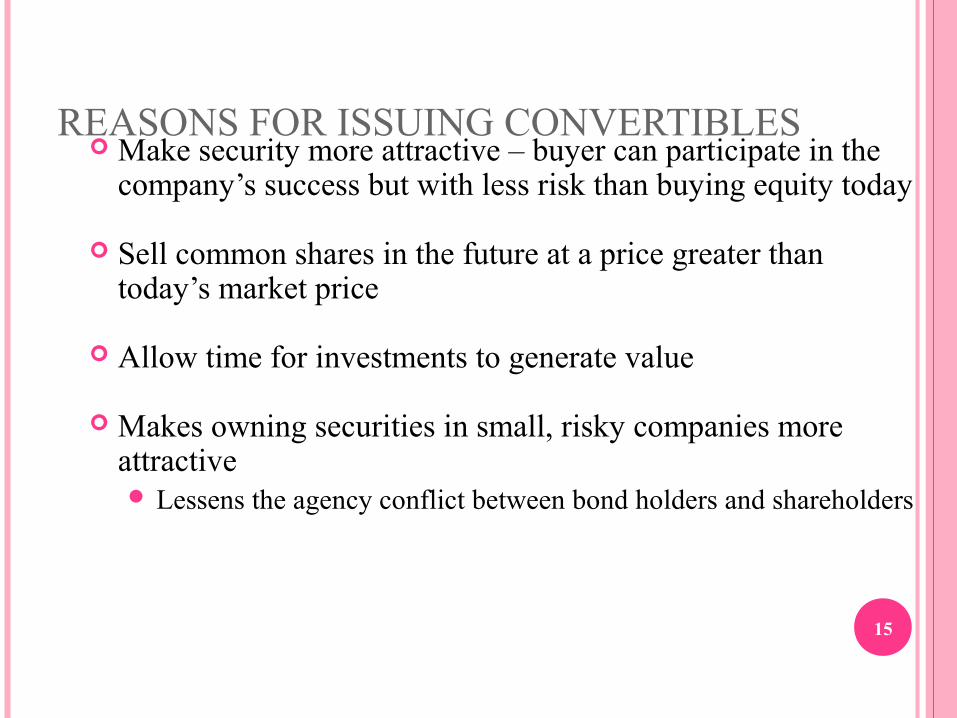

REASONS FOR ISSUING CONVERTIBLES Make security more attractive – buyer can participate in the

company’s success but with less risk than buying equity today

Sell common shares in the future at a price greater than today’s market price

Allow time for investments to generate value

Makes owning securities in small, risky companies more attractive Lessens the agency conflict between bond holders and shareholders

15

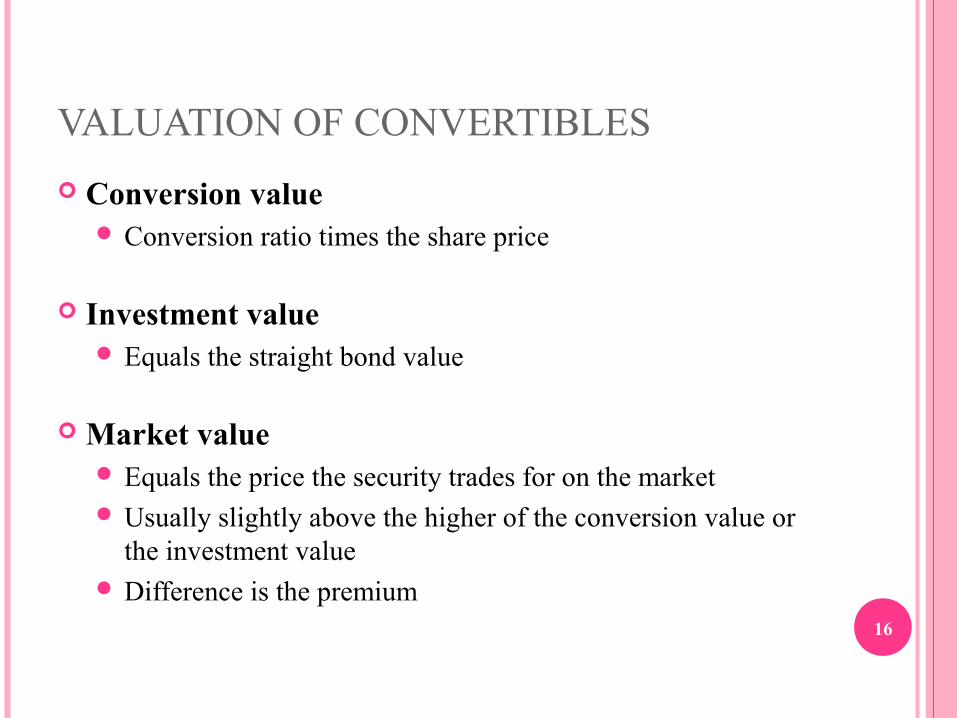

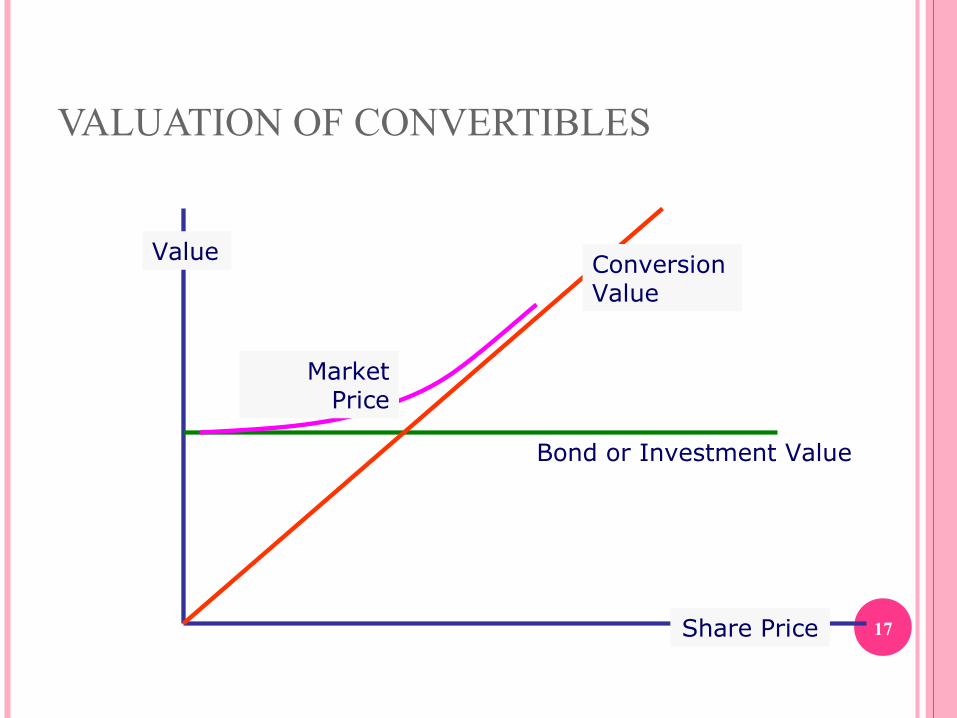

VALUATION OF CONVERTIBLES

Conversion value Conversion ratio times the share price

Investment value Equals the straight bond value

Market value Equals the price the security trades for on the market Usually slightly above the higher of the conversion value or

the investment value Difference is the premium

16

VALUATION OF CONVERTIBLES

17Share Price

Value Conversion Value

Bond or Investment Value

Market Price

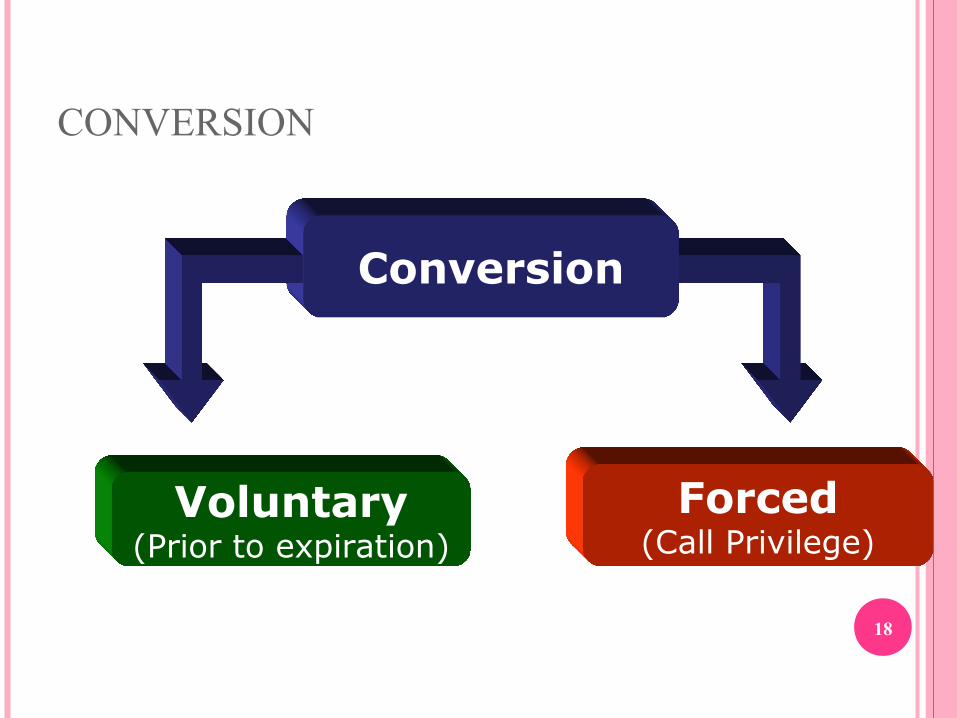

CONVERSION

18

Conversion

Voluntary(Prior to expiration)

Forced(Call Privilege)

WARRANTS Allows the holder to purchase additional common shares for

some period of time at a fixed exercise price

Usually issued as a sweetener attached to other securities

Exercise price Price at which common stock may be purchased Usually 10% to 35% above the market price when the warrants

are issued

19

WARRANTS Expiration date

Date when the option to purchase ends 5–10 years

Usually trade separately from the underlying security

Provide leverage to investors (similar to a long-dated call option)

Market value of warrant Usually exceeds the difference between the stock price and

exercise price (its intrinsic value) The difference is called the time value premium

20

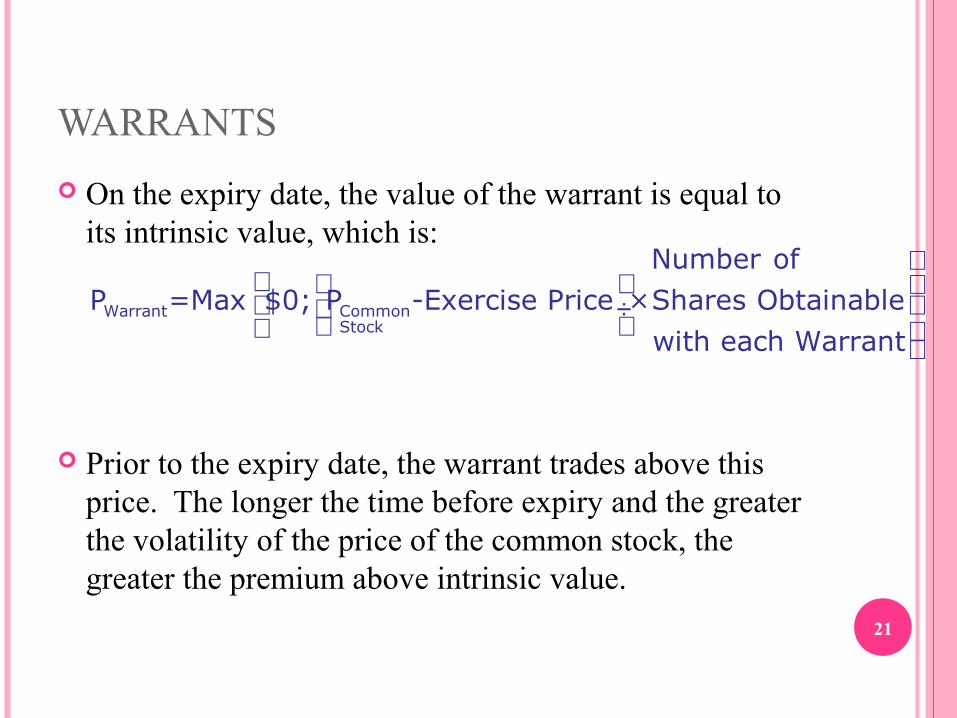

WARRANTS

On the expiry date, the value of the warrant is equal to its intrinsic value, which is:

Prior to the expiry date, the warrant trades above this price. The longer the time before expiry and the greater the volatility of the price of the common stock, the greater the premium above intrinsic value.

21

÷

Warrant Common

Stock

Number ofP =Max $0; P -Exercise Price ×Shares Obtainable

with each Warrant

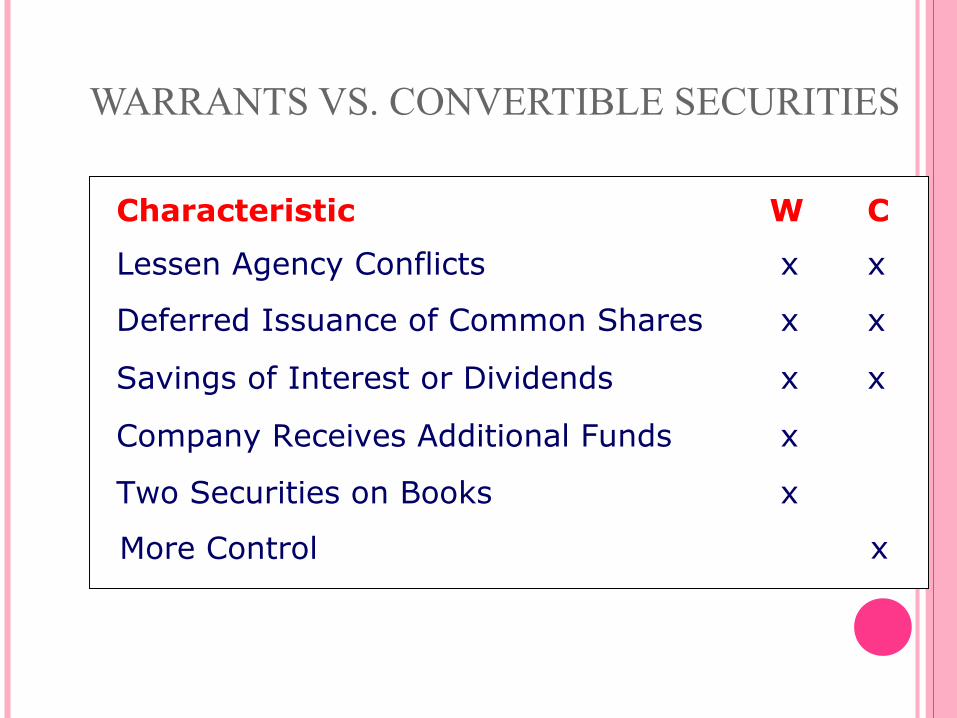

WARRANTS VS. CONVERTIBLE SECURITIES

22

Characteristic W C

Lessen Agency Conflicts x x

Deferred Issuance of Common Shares x x

Savings of Interest or Dividends x x

Company Receives Additional Funds x

Two Securities on Books x

More Control x

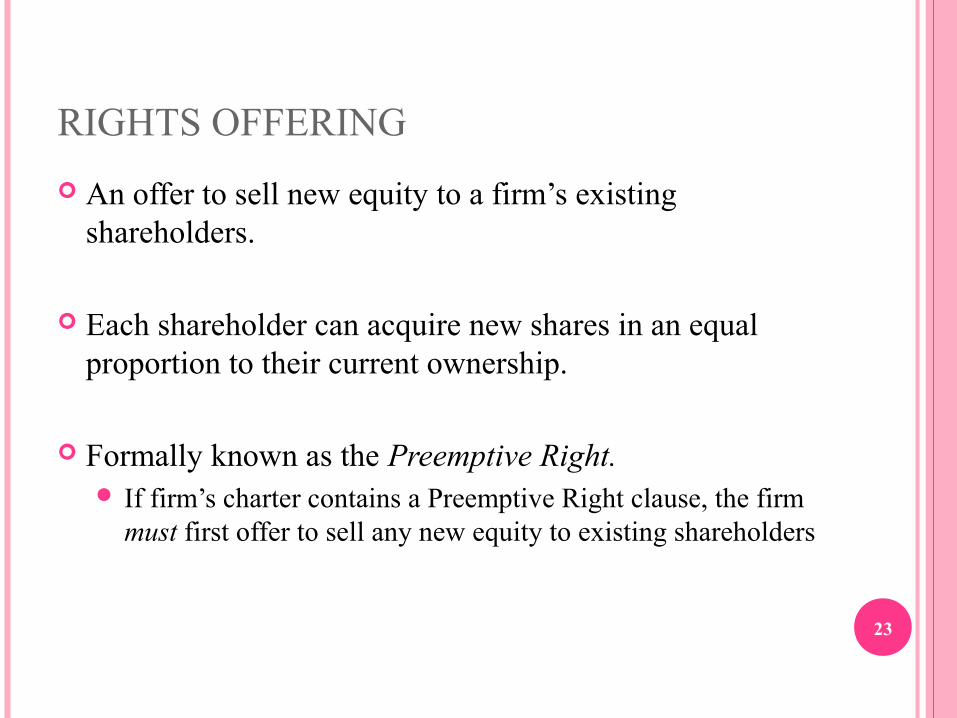

RIGHTS OFFERING

An offer to sell new equity to a firm’s existing shareholders.

Each shareholder can acquire new shares in an equal proportion to their current ownership.

Formally known as the Preemptive Right. If firm’s charter contains a Preemptive Right clause, the firm

must first offer to sell any new equity to existing shareholders

23

RIGHTS OFFERING

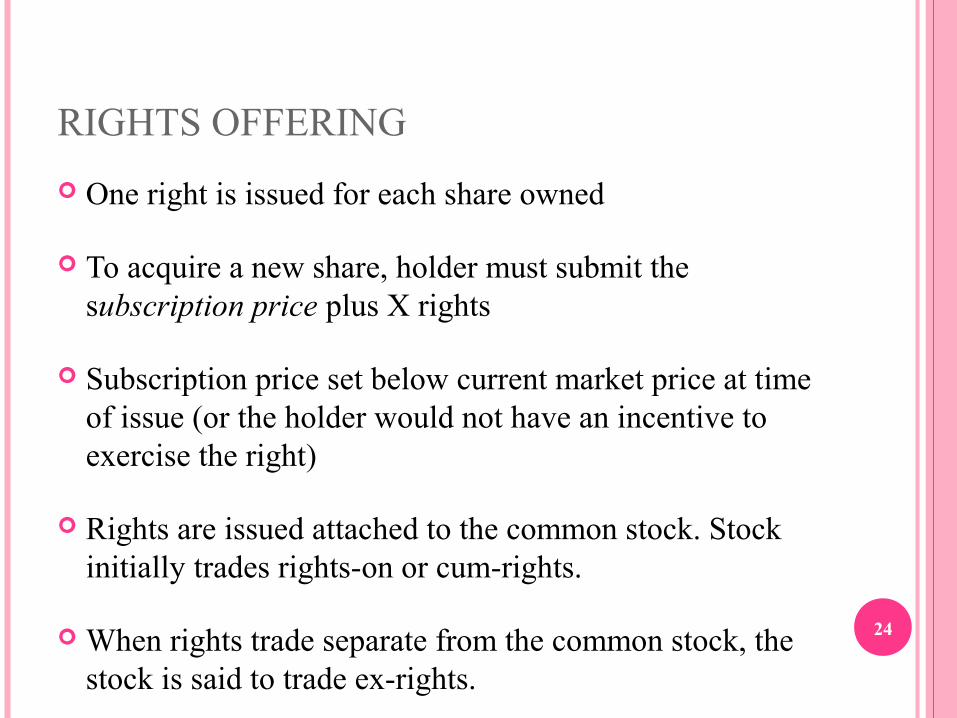

One right is issued for each share owned

To acquire a new share, holder must submit the subscription price plus X rights

Subscription price set below current market price at time of issue (or the holder would not have an incentive to exercise the right)

Rights are issued attached to the common stock. Stock initially trades rights-on or cum-rights.

When rights trade separate from the common stock, the stock is said to trade ex-rights.

24

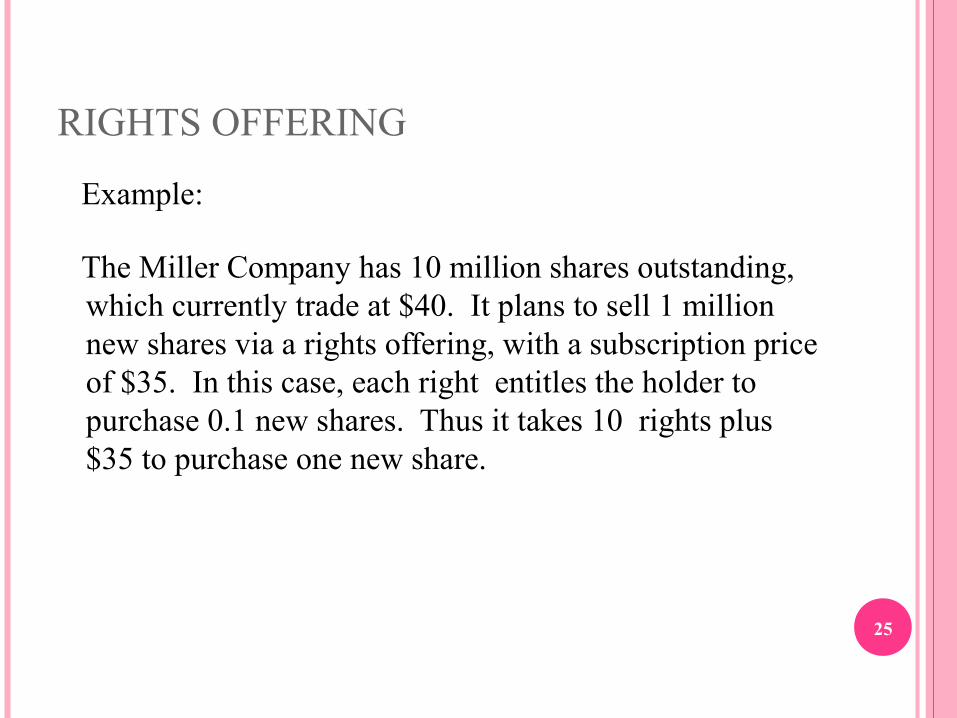

RIGHTS OFFERING

Example:

The Miller Company has 10 million shares outstanding, which currently trade at $40. It plans to sell 1 million new shares via a rights offering, with a subscription price of $35. In this case, each right entitles the holder to purchase 0.1 new shares. Thus it takes 10 rights plus $35 to purchase one new share.

25

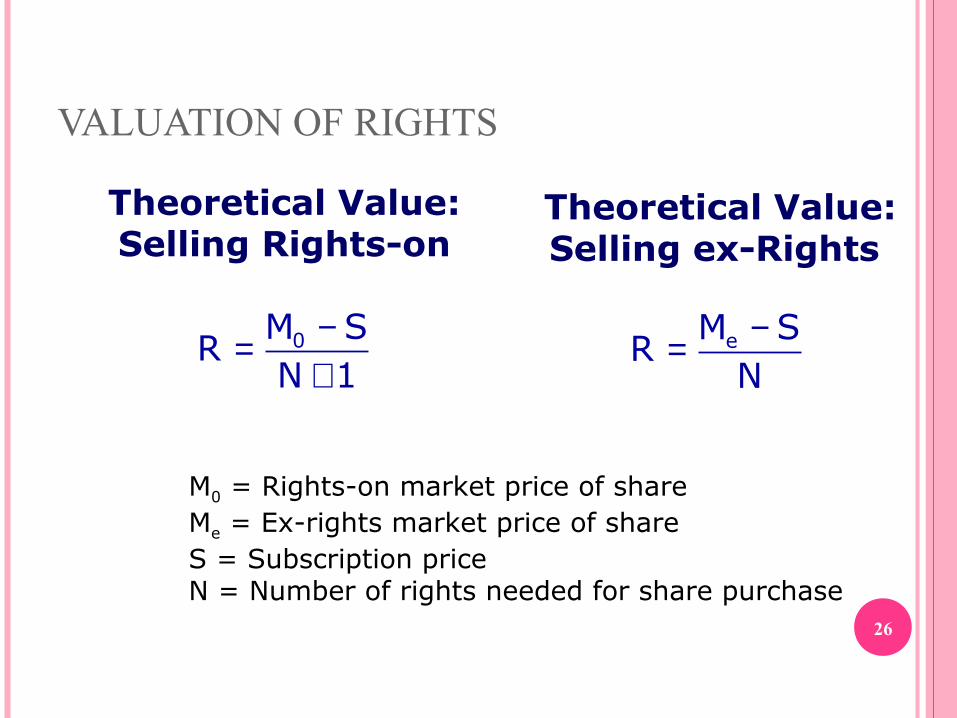

VALUATION OF RIGHTS

26

Theoretical Value:Selling Rights-on

−=+

0M SR

N 1

Theoretical Value:Selling ex-Rights

−= eM SR

N

M0 = Rights-on market price of shareMe = Ex-rights market price of shareS = Subscription priceN = Number of rights needed for share purchase

RIGHTS

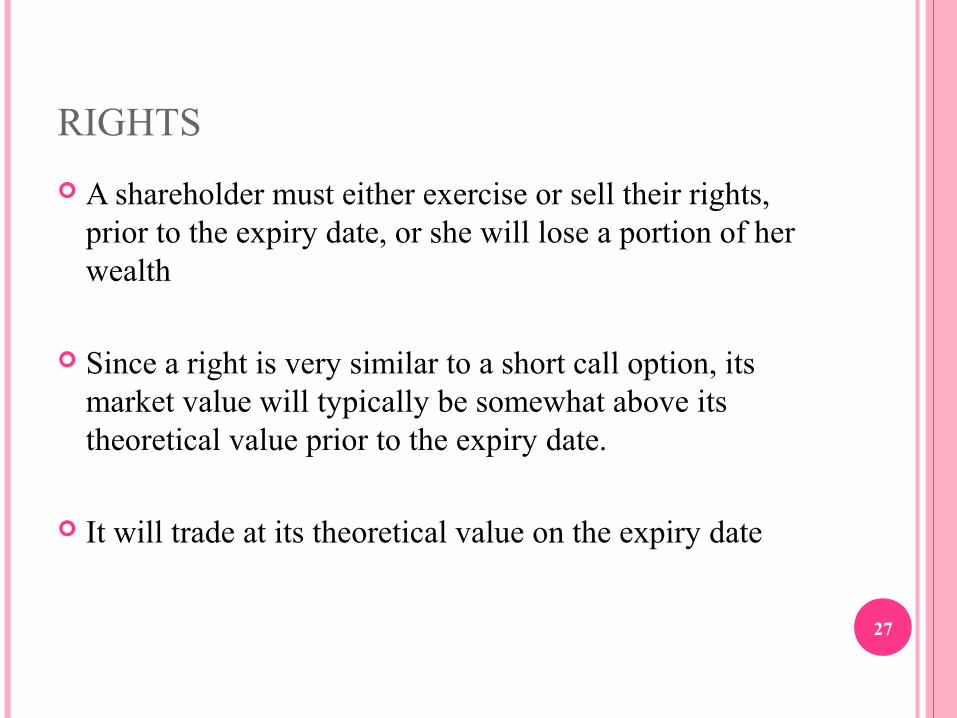

A shareholder must either exercise or sell their rights, prior to the expiry date, or she will lose a portion of her wealth

Since a right is very similar to a short call option, its market value will typically be somewhat above its theoretical value prior to the expiry date.

It will trade at its theoretical value on the expiry date

27

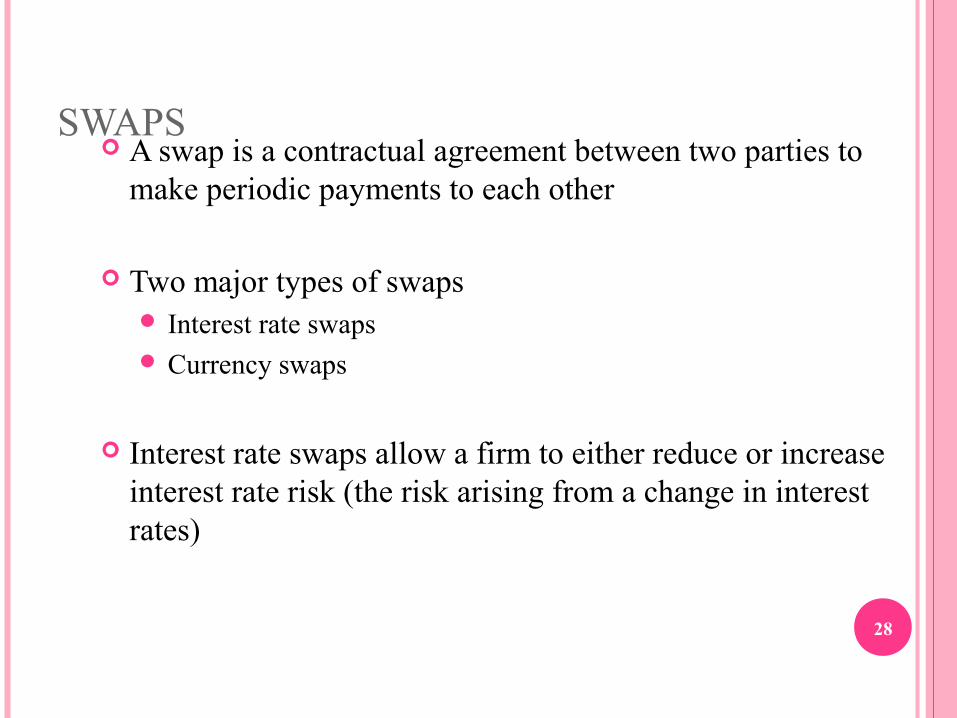

SWAPS A swap is a contractual agreement between two parties to

make periodic payments to each other

Two major types of swaps Interest rate swaps Currency swaps

Interest rate swaps allow a firm to either reduce or increase interest rate risk (the risk arising from a change in interest rates)

28

INTEREST RATE SWAPS: TYPICAL USE

Company has a fixed rate asset and a floating rate liability. It is exposed to the risk that interest rates might rise.

To reduce risk, company may enter into a swap whereby it exchanges its floating rate liability for a fixed rate liability, thereby reducing interest rate risk

29

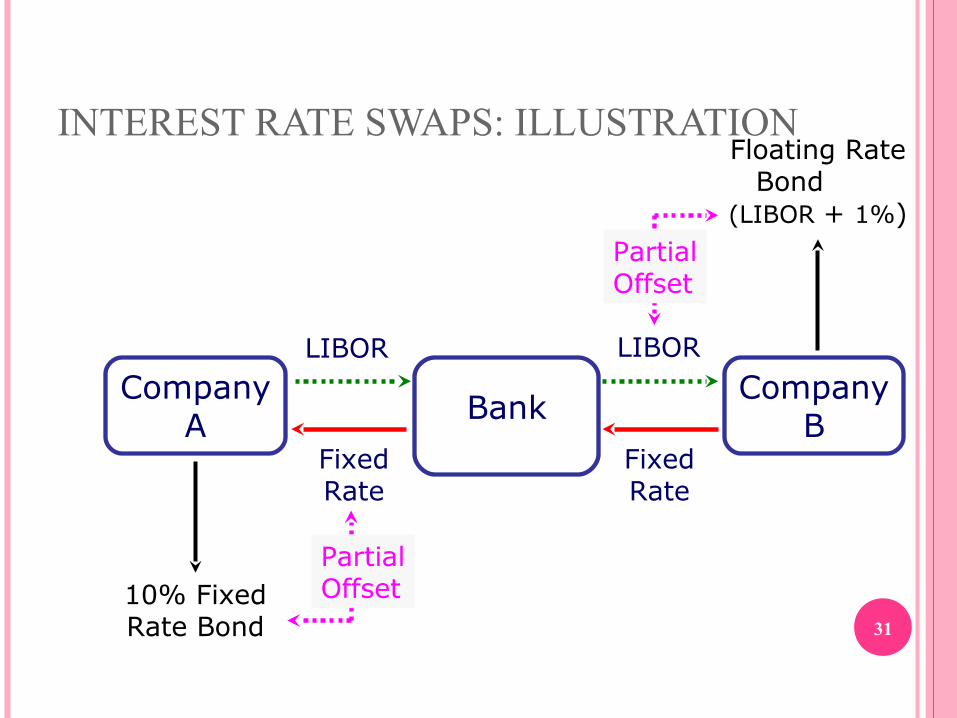

INTEREST RATE SWAPS: EXAMPLE

Company A has a fixed rate bond with a 10% coupon. It wants to swap this fixed rate liability for a floating rate liability.

Company B has a floating rate bond on which it pays LIBOR plus 1%. It wants to exchange this floating rate liability for a fixed rate liability.

A bank acts as a mediary to help Company A and Company B arrange a swap.

30

INTEREST RATE SWAPS: ILLUSTRATION

31

10% Fixed Rate Bond

Floating Rate Bond

(LIBOR + 1%)

CompanyA Bank

CompanyB

LIBOR LIBOR

FixedRate

FixedRate

PartialOffset

PartialOffset

MAJOR POINTS

The price of all derivative securities is derived from the price of some underlying asset.

Options give the holder the right but not the obligation to undertake some action.

Options exist in many forms, such as call & puts, warrants, rights and convertible securities.

Swaps allow companies to exchange cash flows to reduce (or assume) risk.

32