check21 update thursday, november 17, 2005. update startup statistics state of solutions customer...

TRANSCRIPT

Check21 UpdateCheck21 UpdateThursday, November 17, 2005Thursday, November 17, 2005

UpdateUpdate

Startup Statistics State of solutions Customer experiences

Today Experience good/bad/lessons learned

Future Shifting Payments and the Silo Meltdown

Startup Statistics State of solutions Customer experiences

Today Experience good/bad/lessons learned

Future Shifting Payments and the Silo Meltdown

Image Capture

Image Archive Largely Mature: Most all Banks have some solution in place in these areas.

Mature to moderately mature at Industry leaders. Less mature at followers. Re-engineering still to be done in many banks.

Pilot solutions, no major commitments, paper still follows.

Startup – State of Payments

Startup – State of Payments

Electronic Check Presentment (ECP)

Process Re-engineering (Day 2 and Services)Process Re-engineering (Day 2 and Services)

Image Product IntroductionImage Product Introduction

POP Transaction ElectronificationPOP Transaction Electronification

Generally lower volume, data only, with paper to follow.

StartupStartup

Statisticsa few brave “early

adopters”Pilots, low volumeFocus on Forward-

Presentment

Statisticsa few brave “early

adopters”Pilots, low volumeFocus on Forward-

Presentment

StartupStartup

Expectations (from BAI Survey 2004) “Two-thirds of the respondents believed

that one of the highest payoffs from Check 21 would come from faster funds collection”

“More than half believed that reductions in transportation costs would be another big payoff”

“More than half the respondents expected more efficient processing also would be among the highest payoffs”

All expected new product offerings to result

Expectations (from BAI Survey 2004) “Two-thirds of the respondents believed

that one of the highest payoffs from Check 21 would come from faster funds collection”

“More than half believed that reductions in transportation costs would be another big payoff”

“More than half the respondents expected more efficient processing also would be among the highest payoffs”

All expected new product offerings to result

StartupStartup

Solution OfferingsTactical solutions most often selected

Financial Institutions hesitant to make major investment

Initial reliance on existing, proven technology

ECPLegacy Item Processing

Immature definition forced early adopters to look for solutions that address a gamut of possibilities

Solution OfferingsTactical solutions most often selected

Financial Institutions hesitant to make major investment

Initial reliance on existing, proven technology

ECPLegacy Item Processing

Immature definition forced early adopters to look for solutions that address a gamut of possibilities

StartupStartup

What did we miss? Rollout not as progressive as anticipated Legal worries Regulations too vague to deal with image Surprise – in most cases, paper was moving

as well as image Current infrastructure not conducive to

exchange, but very controlled New infrastructure built for image, but

implementation of controls falling behind Many have stepped into solutions without a

complete view of requirements

What did we miss? Rollout not as progressive as anticipated Legal worries Regulations too vague to deal with image Surprise – in most cases, paper was moving

as well as image Current infrastructure not conducive to

exchange, but very controlled New infrastructure built for image, but

implementation of controls falling behind Many have stepped into solutions without a

complete view of requirements

StartupStartup

Networks – which one do I use? SVPCo Viewpointe Endpoint Exchange Federal Reserve Direct Send

Once I choose, how do I settle? What kind of images do I use?

What happens when something goes wrong?

Networks – which one do I use? SVPCo Viewpointe Endpoint Exchange Federal Reserve Direct Send

Once I choose, how do I settle? What kind of images do I use?

What happens when something goes wrong?

Customer ExperiencesCustomer Experiences

Exchange Low volume, account level Highlighted back office and Day 2 deficiencies

Forward Presentment IRDs Successful, particularly west to east

Settlement Difficult at first, matured through use of NCHA

Exceptions Image Quality, not the nightmare expected Returns, remain manual

Exchange Low volume, account level Highlighted back office and Day 2 deficiencies

Forward Presentment IRDs Successful, particularly west to east

Settlement Difficult at first, matured through use of NCHA

Exceptions Image Quality, not the nightmare expected Returns, remain manual

State of TodayState of Today“A year after the Check Clearing for the 21st Century Act took effect, and supposedly triggered a race to use image exchange networks, many bankers are still at the starting blocks.” American Banker

“A year after the Check Clearing for the 21st Century Act took effect, and supposedly triggered a race to use image exchange networks, many bankers are still at the starting blocks.” American Banker

Image Capture

Image Archive Largely Mature: Most all Banks have some solution in place in these areas.

Mature to moderately mature at Industry leaders. Less mature at followers. Re-engineering still to be done in many banks.

Pilot or scaling solution at leaders. Followers are in evaluation or pre-commit position.

Today – State of PaymentsToday – State of Payments

Electronic Check Presentment (ECP)

Process Re-engineering (Day 2 and Services)Process Re-engineering (Day 2 and Services)

Image Product IntroductionImage Product Introduction

POP Transaction ElectronificationPOP Transaction Electronification

Generally lower volume, data only, with paper to follow.

Image ExchangeImage Exchange

Everybody wants to “send”

Everybody wants to “send”

Partners required

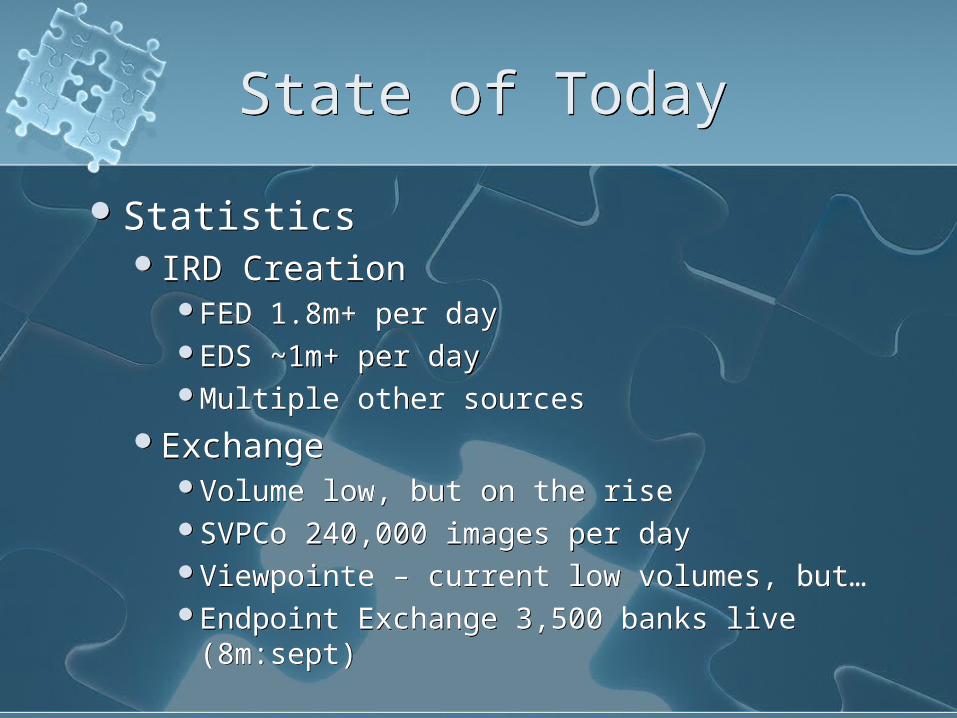

State of TodayState of Today

StatisticsIRD Creation

FED 1.8m+ per dayEDS ~1m+ per dayMultiple other sources

ExchangeVolume low, but on the riseSVPCo 240,000 images per dayViewpointe – current low volumes, but…Endpoint Exchange 3,500 banks live

(8m:sept)

StatisticsIRD Creation

FED 1.8m+ per dayEDS ~1m+ per dayMultiple other sources

ExchangeVolume low, but on the riseSVPCo 240,000 images per dayViewpointe – current low volumes, but…Endpoint Exchange 3,500 banks live

(8m:sept)

State of Today – Federal Reserve

State of Today – Federal Reserve

Product usage: FedForward: 200 ICL customers; 200 paper-

to-image customers FedReturn : 3 customers depositing

FedReturn image cash letter FedReceipt : 4 customers receiving image

cash letters as presentment Projections:

100,000 new items per day per month through year end 2006

20% of Check 21 presentments will be via FedReceipt or FedReceipt Plus by year end 2006 (currently .01%)

Product usage: FedForward: 200 ICL customers; 200 paper-

to-image customers FedReturn : 3 customers depositing

FedReturn image cash letter FedReceipt : 4 customers receiving image

cash letters as presentment Projections:

100,000 new items per day per month through year end 2006

20% of Check 21 presentments will be via FedReceipt or FedReceipt Plus by year end 2006 (currently .01%)

Federal Reserve IRD Volume

40,000

165,000

720,000

1,047,000

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

Nov. 2004 Feb. 2005 Jun. 2005 Aug. 2005

Federal Reserve IRD Average Value

$17,500 $17,576

$11,389

$9,360

$0

$2,000

$4,000

$6,000

$8,000

$10,000$12,000

$14,000

$16,000

$18,000

$20,000

Nov. 2004 Feb. 2005 Jun. 2005 Aug. 2005

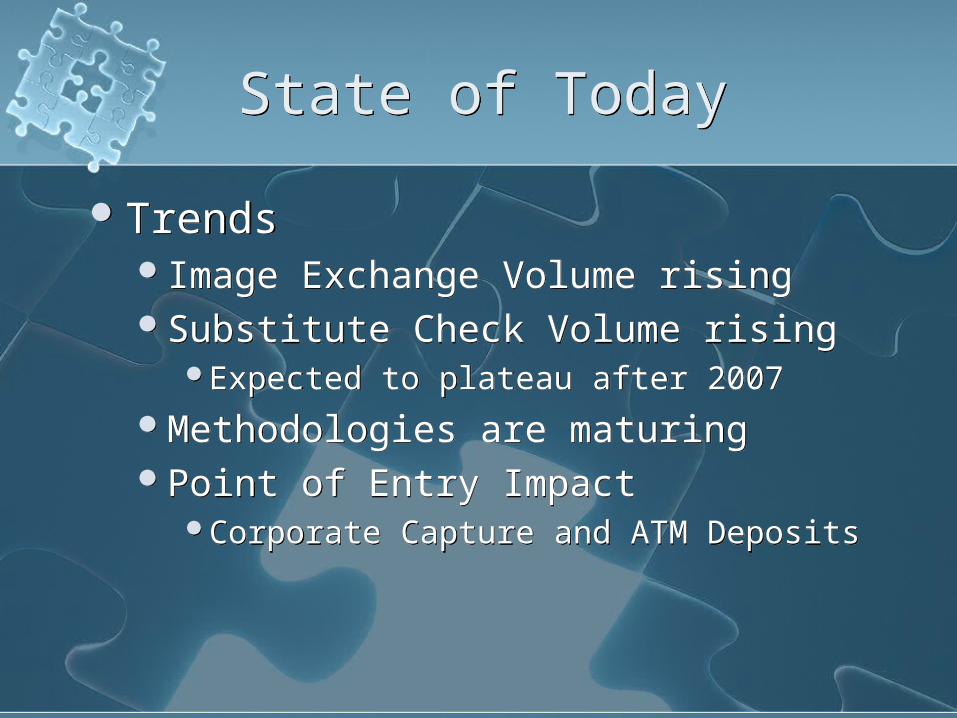

State of TodayState of Today

TrendsImage Exchange Volume risingSubstitute Check Volume rising

Expected to plateau after 2007Methodologies are maturingPoint of Entry Impact

Corporate Capture and ATM Deposits

TrendsImage Exchange Volume risingSubstitute Check Volume rising

Expected to plateau after 2007Methodologies are maturingPoint of Entry Impact

Corporate Capture and ATM Deposits

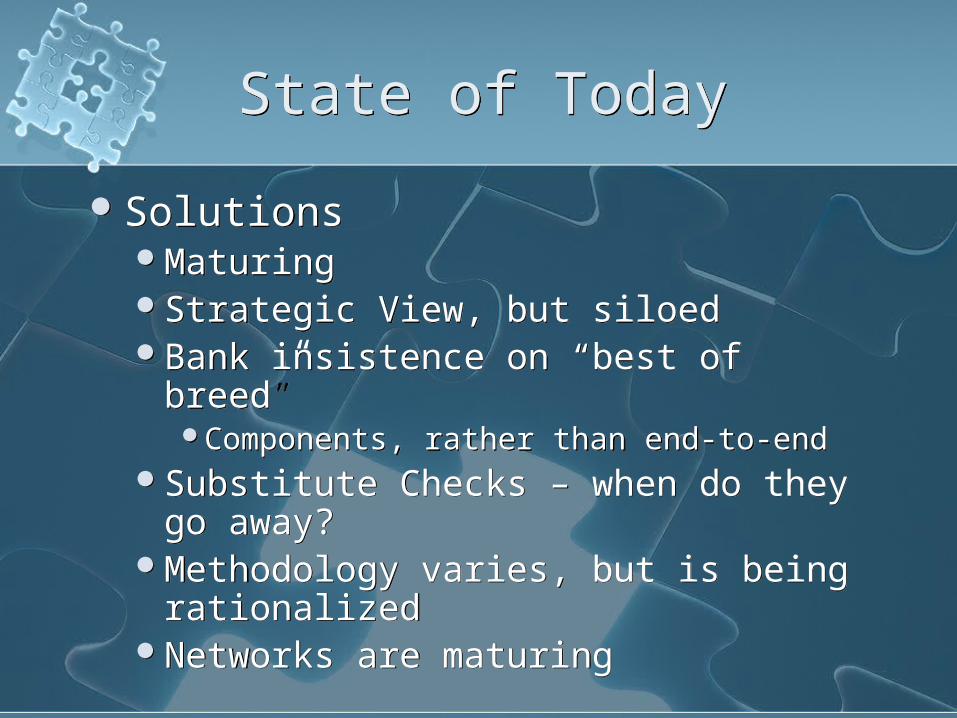

State of TodayState of Today

SolutionsMaturingStrategic View, but siloedBank insistence on “best of breed”

Components, rather than end-to-endSubstitute Checks – when do they go

away?Methodology varies, but is being

rationalizedNetworks are maturing

SolutionsMaturingStrategic View, but siloedBank insistence on “best of breed”

Components, rather than end-to-endSubstitute Checks – when do they go

away?Methodology varies, but is being

rationalizedNetworks are maturing

State of TodayState of Today

Expected this… What happened? Mass adoption of exchange Use of substitute check as transition

instrument only Business case development around

exchange of images Image Formats Standards Image Security Features Fraud expected to be among the highest

risks of Check 21 Belief that Check 21 would increase

exposure to fraud

Expected this… What happened? Mass adoption of exchange Use of substitute check as transition

instrument only Business case development around

exchange of images Image Formats Standards Image Security Features Fraud expected to be among the highest

risks of Check 21 Belief that Check 21 would increase

exposure to fraud

State of TodayState of Today

Didn’t expect that… Substitute Checks

Multiple sends Duplicates Fraud (intentional and inadvertent) Business case windfall (especially east-west) Develop a life of their own

Slow adaptation of Exchange Lack of partners Low volumes leading to poor business

cases What downstream changes are required

when the paper not available?

Didn’t expect that… Substitute Checks

Multiple sends Duplicates Fraud (intentional and inadvertent) Business case windfall (especially east-west) Develop a life of their own

Slow adaptation of Exchange Lack of partners Low volumes leading to poor business

cases What downstream changes are required

when the paper not available?

FutureFuture

Image Capture

Image Archive

Process Re-engineering (Day 2 and Services)Process Re-engineering (Day 2 and Services)

Image Product IntroductionImage Product Introduction

POP Transaction ElectronificationPOP Transaction Electronification

Image ExchangeImage Exchange

Payments ConvergencePayments Convergence

Shared CommodityShared Commodity

Largely Mature: Most all Banks have some solution in place in these areas.

Mature to moderately mature at Industry leaders. Less mature at followers. Re-engineering still to be done in many banks.

Pilot or scaling solution at leaders. Followers are in evaluation or pre-commit position.

Early days at majority of banks.Exploration or planning in process.

“reconstructing the check world”

Future – One Step at a Time

Future – One Step at a Time

SILO“something that is kept separate or

compartmentalized”

SILO“something that is kept separate or

compartmentalized”

CheckProcessing

Credit/DebitCard

Lockbox

ACH

CorporateDeposits

RetailBranch

Point of Sale

FutureFuture

OfferingsWill address multiple forms of

paymentWill integrate traditional Day 2

functions in-line, near real timeFraud DetectionExceptions identification

Vendor co-existence matures

OfferingsWill address multiple forms of

paymentWill integrate traditional Day 2

functions in-line, near real timeFraud DetectionExceptions identification

Vendor co-existence matures

FutureFuture

Convergence – The Silo MeltdownPaper vs Electronic vs ACH vs …Fraud DetectionPayments Tracking

Across silos“Batch of One” view

Convergence – The Silo MeltdownPaper vs Electronic vs ACH vs …Fraud DetectionPayments Tracking

Across silos“Batch of One” view

SummarySummary

Volume Trends to ContinuePayments view shiftingSilos Merging

Volume Trends to ContinuePayments view shiftingSilos Merging

Thank YouThank Youwww.carreker.comwww.carreker.com