chemicals - ibef additives knowledge chemicals agrochemicals ... the indian chemicals industry is...

TRANSCRIPT

CHEMICALSNovember 2010

2

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

3

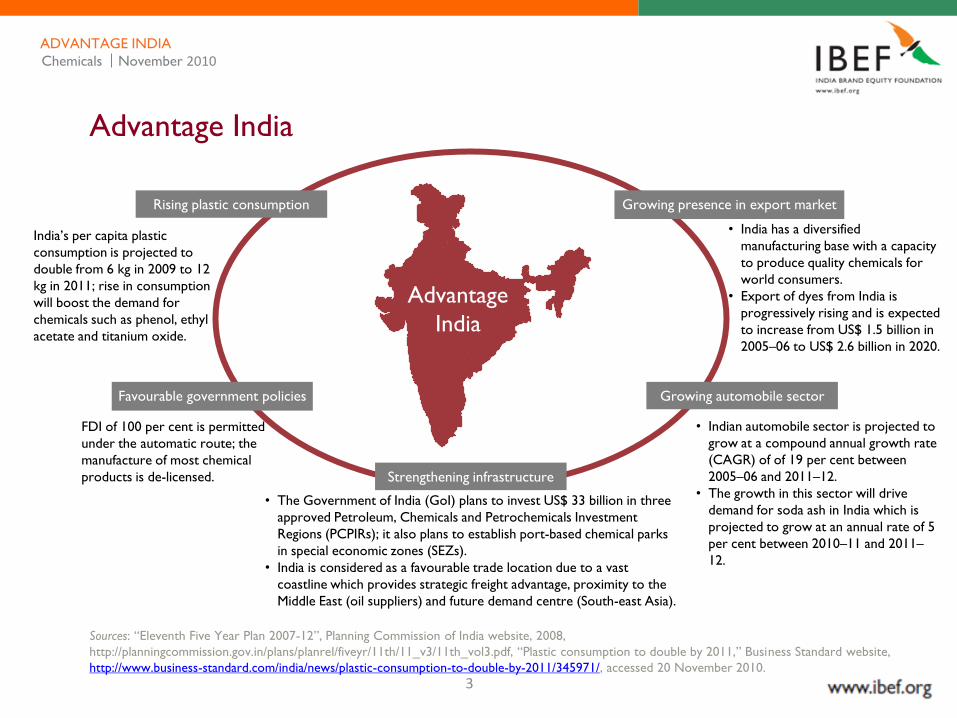

India’s per capita plastic

consumption is projected to

double from 6 kg in 2009 to 12

kg in 2011; rise in consumption

will boost the demand for

chemicals such as phenol, ethyl

acetate and titanium oxide.

• Indian automobile sector is projected to

grow at a compound annual growth rate

(CAGR) of of 19 per cent between

2005–06 and 2011–12.

• The growth in this sector will drive

demand for soda ash in India which is

projected to grow at an annual rate of 5

per cent between 2010–11 and 2011–

12.

FDI of 100 per cent is permitted

under the automatic route; the

manufacture of most chemical

products is de-licensed.

• The Government of India (GoI) plans to invest US$ 33 billion in three

approved Petroleum, Chemicals and Petrochemicals Investment

Regions (PCPIRs); it also plans to establish port-based chemical parks

in special economic zones (SEZs).

• India is considered as a favourable trade location due to a vast

coastline which provides strategic freight advantage, proximity to the

Middle East (oil suppliers) and future demand centre (South-east Asia).

Advantage

India

• India has a diversified

manufacturing base with a capacity

to produce quality chemicals for

world consumers.

• Export of dyes from India is

progressively rising and is expected

to increase from US$ 1.5 billion in

2005–06 to US$ 2.6 billion in 2020.

Growing presence in export market

Strengthening infrastructure

Growing automobile sectorFavourable government policies

Rising plastic consumption

Advantage India

Chemicals November 2010ADVANTAGE INDIA

Sources: ―Eleventh Five Year Plan 2007-12‖, Planning Commission of India website, 2008,

http://planningcommission.gov.in/plans/planrel/fiveyr/11th/11_v3/11th_vol3.pdf, ―Plastic consumption to double by 2011,‖ Business Standard website,

http://www.business-standard.com/india/news/plastic-consumption-to-double-by-2011/345971/, accessed 20 November 2010.

4

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

5

The Indian chemicals industry is

the twelfth-largest industry in the

world and the third largest in Asia

in terms of volume.

The industry contributes 3 per

cent to the national GDP.

The Indian chemicals industry is

currently valued at around US$ 35

billion.

The industry accounted for 9.3 per

cent of total exports in 2008–09.

Industry exports grew at a CAGR

of 18 per cent between 2003–04

and 2008–09.

Sources: Department of Chemicals & Petrochemicals annual report 2009-10; ―SIA newsletter, April 2010‖, Department of Industrial Policy &

Promotion website, Ministry of Commerce & Industry, http://siadipp.nic.in/publicat/newslttr/apr2010/index.htm, accessed 20 September 2010

The Indian chemicals industry has evolved from being a basic producer of chemicals to an innovative

industry.

Chemicals November 2010MARKET OVERVIEW

Overview of the Indian chemicals industry

Market overview

6

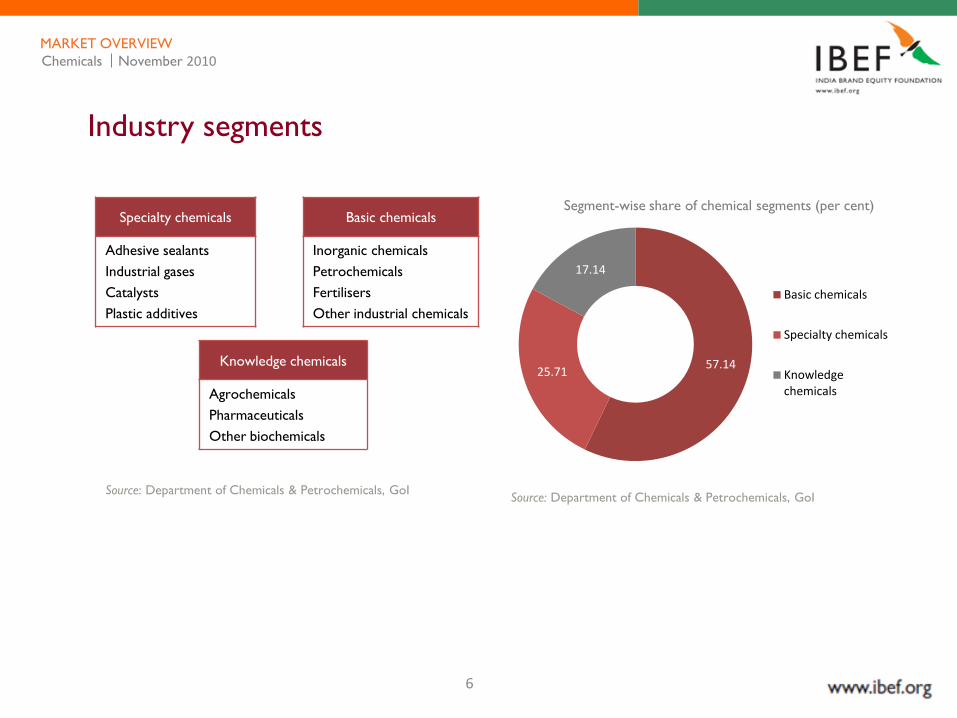

Industry segments

Source: Department of Chemicals & Petrochemicals, GoISource: Department of Chemicals & Petrochemicals, GoI

Chemicals November 2010

Basic chemicals

Inorganic chemicals

Petrochemicals

Fertilisers

Other industrial chemicals

Specialty chemicals

Adhesive sealants

Industrial gases

Catalysts

Plastic additives

Knowledge chemicals

Agrochemicals

Pharmaceuticals

Other biochemicals

Segment-wise share of chemical segments (per cent)

MARKET OVERVIEW

57.1425.71

17.14

Basic chemicals

Specialty chemicals

Knowledge chemicals

7

Chemicals and petrochemicals — segmentation

Chemicals November 2010

Major chemicals

• Alkali chemicals

• Inorganic chemicals

• Organic chemicals

• Pesticides

• Dyes and dyestuffs

Major petrochemicals

• Synthetic fibres

• Polymers

• Synthetic rubber

• Synthetic detergent intermediates

• Performance plastics

• Fibre intermediates

• Olefins

• Aromatics

MARKET OVERVIEW

Source: Department of Chemicals & Petrochemicals , GoI

8

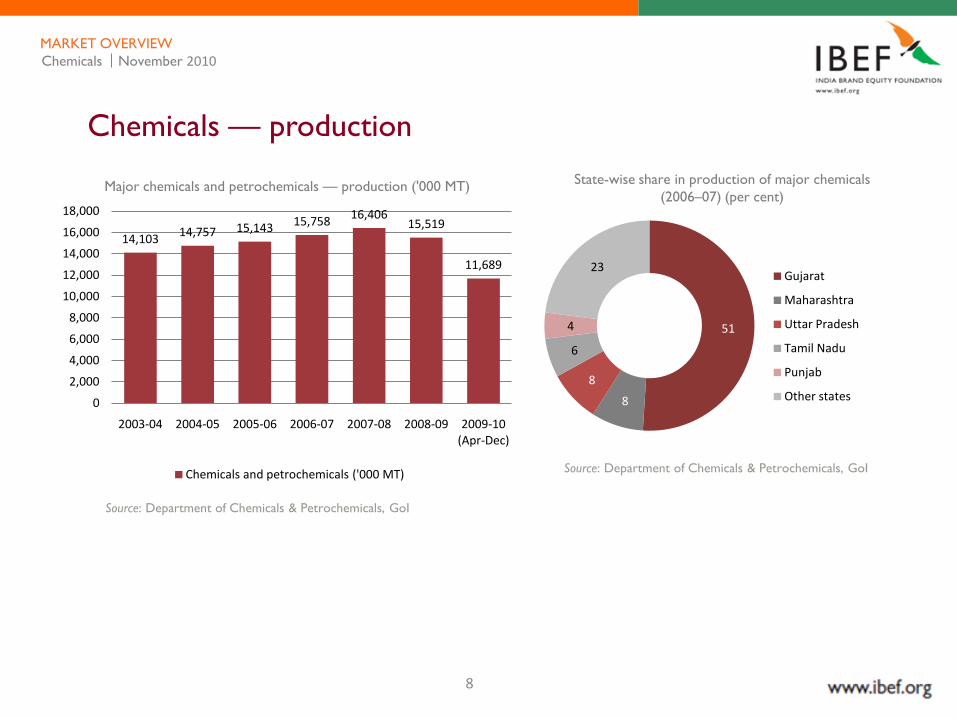

14,10314,757 15,143 15,758

16,40615,519

11,689

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10 (Apr-Dec)

Major chemicals and petrochemicals — production ('000 MT)

Chemicals and petrochemicals ('000 MT)

Source: Department of Chemicals & Petrochemicals, GoI

State-wise share in production of major chemicals

(2006–07) (per cent)

Source: Department of Chemicals & Petrochemicals, GoI

Chemicals — production

Chemicals November 2010MARKET OVERVIEW

51

8

8

6

4

23Gujarat

Maharashtra

Uttar Pradesh

Tamil Nadu

Punjab

Other states

9

Share of chemicals sector in India’s exports

2009–2010 (per cent)

Source: Department of Commerce, GoI, Annual Report, 2009–2010

341431

507612 657

780

331429

546643

731

989

0

200

400

600

800

1,000

1,200

2003-04 2004-05 2005-06 2006-07 2007-08 2008-09

Exports Imports

Exports and imports in the chemicals and

petrochemicals sectors (INR billion)

Source: Department of Chemicals & Petrochemicals, GoI

• The chemicals and related products sector contributed 13.8 per cent to national exports in 2009–2010.

• The chemicals and petrochemicals segments grew at a CAGR of 17.97 per cent from 2003–04 till 2008–09.

• The majority of chemicals exported were dyes, dyestuffs and alkali chemicals.

Chemicals — exports and imports

Chemicals November 2010MARKET OVERVIEW

19.8

13.813.8

17.8Engineering goods

Petroleum products

Chemicals and related products

Gems and jewellery

INR

bill

ion

Year

10

Key trends

Industry trends

• The Indian chemicals industry is highly fragmented and is currently going through a major restructuring

and consolidation phase.

• At present, most of the domestic capacity of chemicals caters to a strong domestic market. However, this

with the GoI initiating PCPIRs and SEZs, the export capacity is also expected to increase significantly.

• With investments in R&D growing, the industry is registering significant growth in the knowledge

chemicals sector.

• The industry is focusing on increasing innovations to produce environment-friendly technology and

products.

Investment trends

• Since 1991, the Indian chemicals sector has been consistently ranked third among all sectors in India, in

terms of the amount of investment.

• Between August 1991 and August 2010, investment intentions worth US$ 112.14 billion (INR 5,382.7

billion) have been received in the chemicals sector. This accounts for 7.17 per cent of total investment

intentions in the country.

Source: ―SIA Statistics-September 2010,‖ Department of Industrial Policy & Promotion website,

http://siadipp.nic.in/publicat/stats/sep2010/index.htm, accessed 10 November 2010.

Chemicals November 2010MARKET OVERVIEW

11

High domestic demand potential

• The per capita consumption of chemical products in India is about one-tenth of the world average.

• Consumption grew at a CAGR of 3.9 per cent between 2003–04 and 2008–09.

• Favourable factors such as strong economic growth have ensured that the domestic demand potential for chemicals

is rising.

Key growth drivers

Focus on R&D

India has a strong base for innovation in its network of 200 national laboratories and 1,300 R&D units, which can be

leveraged for the shift towards an innovation-based industry.

Outsourcing

An increasing number of multinational companies (MNCs) are viewing India as a base for manufacturing and supplying

to their global markets.

Consolidation

The Indian chemicals industry is moving towards greater consolidation in order to achieve economies of scale.

Sources: Department of Chemicals & Petrochemicals; Department of Chemicals & Petrochemicals annual report 2009-10

Chemicals November 2010MARKET OVERVIEW

12

Key players — Indian*

Sources: Relevant company websites and annual reports; Prowess

•This list is indicative ; # 2008–09 figures

CompanySales in 2009–2010

US$ million (INR million)Products

Tata Chemicals Limited (TCL) 2,122.0 (101,856)Soda ash, salt, marine chemicals, caustic soda,

cement and bulk chemicals

United Phosphorus Limited (UPL) 1,184.0 (56,832) Agrochemicals

Nirma Ltd 1,071.0 (51,408)Alkyl benzene, alfa olefin sulphonate, sulfuric acid,

soda ash, pure salt

Gujarat Heavy Chemicals Ltd (GHCL) 320.5 (15,384) Soda ash

Gujarat Alkalies and Chemicals Ltd (GACL 292.0 (14,016) Caustic soda

Solaris Chemtech Industries Ltd 52.1 (2,500)# Bromine and bromine chemicals

Chemicals November 2010MARKET OVERVIEW

13

Key players — International*

Sources: Relevant company websites and annual reports

* This list is indicative

CompanySales in 2009

US$ billionProducts

BASF 69.1 Chemicals, plastics, performance and nutrition products

The Dow Chemicals 46.6 Specialty chemicals, agrochemicals and plastics

Bayer 43.4 Agrochemicals, pharmaceuticals, polymers, technology services

E. I. du Pont de Nemours and Company 27.3 Specialty and fine chemicals

INEOS 25.1 PVC films and specialty resins

Evonik Industries 19.3 Specialty chemicals

AkzoNobel 18.9 Coatings, decorative paints and specialty chemicals

Lanxess 7.3 Plastics, rubber, specialty chemicals and intermediates

Wacker Chemie 5.7 Silicone, polymer, specialty and fine chemicals

Chemicals November 2010MARKET OVERVIEW

14

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

15

Industry infrastructure

Jamnagar,

Thane, Pune , Chiplun

Ahmedabad

Hyderabad

Vadodara

Cochin

Haldia

Bengaluru

NCR

Chennai

Bharuch, Hazira, Vapi

Baddi

DerabassiPanipat

Nagda

Visakhapatnam,

Kakinada

Cuddalore, Puducherry

Mangalore

Industry clusters

Sources: ―SEZ India‖ SEZ India Invest website, http://www.sezindiainvest.com/index.htm, accessed 20 November 2010.

Chemicals November 2010INDUSTRY INFRASTRUCTURE

16

Industry infrastructure — SEZs

Jubilant Chemicals SEZ

LocationVilayat, Bharuch (Gujarat )

(20 km from Dahej)

Area 160 hectares

Developer Jubilant Infrastructure Ltd

Contact

Details

I-A, Sector 16-A,

Industrial Area, Noida – 201301, Uttar

Pradesh, India

Tel: 91 120 2580309

Fax: 91 120 2580310

Website: www.jubl.com

Sources: Department of Commerce 2008–09 annual report, GoI,; ―List of SEZ in India‖ SEZ India Invest website,

http://www.sezindiainvest.com/State_wise.htm , accessed 20 November 2010.

SEZ

Vilayat, Bharuch

Jubilant Chemicals SEZ is the major exclusive chemicals SEZ located in Bharuch, Gujarat, apart from the five major PCPIR regions in India.

Chemicals November 2010INDUSTRY INFRASTRUCTURE

17

• A PCPIR is a specifically delineated investment region with an area of around 250 sq km.

• The region has planned infrastructure to establish manufacturing facilities for domestic and export-led production in petroleum, chemicals and petrochemicals.

• It is designed to house production units, public utilities, logistics infrastructure, environmental-protection mechanisms, residential areas and administrative services.

• PCPIR includes SEZs, industrial parks, free trade and warehousing zones (FTWZs), export-oriented units (EOUs) or growth centres.

• PCPIRs are linked through external physical infrastructure such as rail, road (the National Highways), ports, airports and telecommunications.

Petroleum, Chemicals and Petrochemicals Investment Regions

(PCPIR) … (1/2)

Source: Department of Chemicals & Petrochemicals annual report 2009-10

Chemicals November 2010INDUSTRY INFRASTRUCTURE

Vizag and East

Godavari

Vagra- Bharuch

Haldia

Cuddalore & Nagapattinam

18

Petroleum, Chemicals and Petrochemicals Investment Regions

(PCPIR) … (2/2)

Source: ―Presentations‖, Petroleum, Chemicals and Petrochemicals Investment Region Policy website, http://www.indiachem.in/pcpir.htm, accessed

24 November 2010

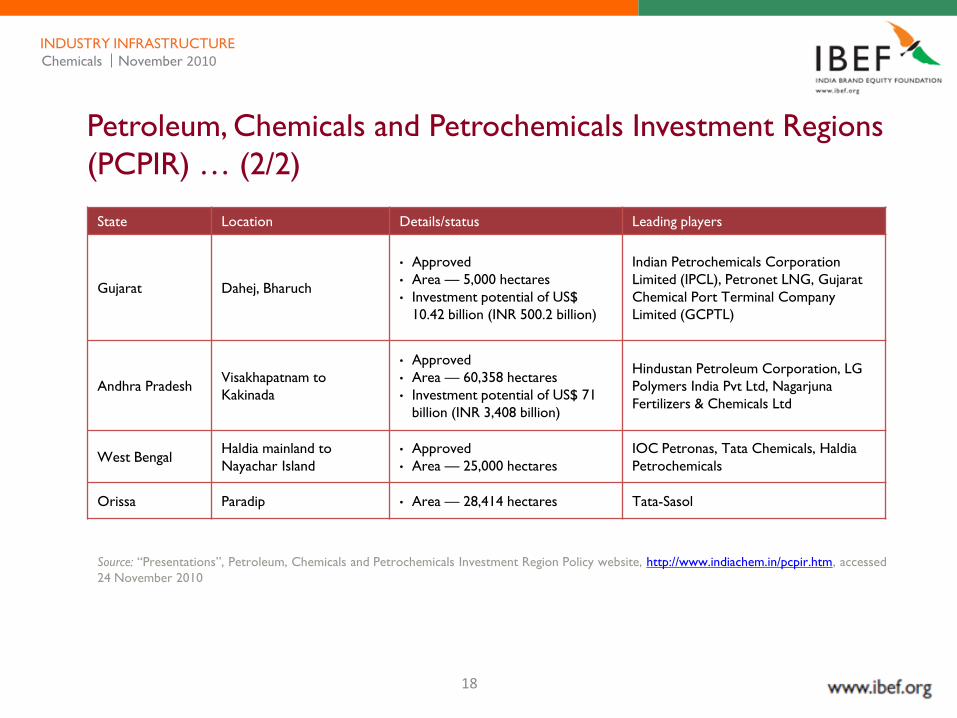

State Location Details/status Leading players

Gujarat Dahej, Bharuch

• Approved

• Area — 5,000 hectares

• Investment potential of US$

10.42 billion (INR 500.2 billion)

Indian Petrochemicals Corporation

Limited (IPCL), Petronet LNG, Gujarat

Chemical Port Terminal Company

Limited (GCPTL)

Andhra PradeshVisakhapatnam to

Kakinada

• Approved

• Area — 60,358 hectares

• Investment potential of US$ 71

billion (INR 3,408 billion)

Hindustan Petroleum Corporation, LG

Polymers India Pvt Ltd, Nagarjuna

Fertilizers & Chemicals Ltd

West BengalHaldia mainland to

Nayachar Island

• Approved

• Area — 25,000 hectares

IOC Petronas, Tata Chemicals, Haldia

Petrochemicals

Orissa Paradip • Area — 28,414 hectares Tata-Sasol

Chemicals November 2010INDUSTRY INFRASTRUCTURE

19

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

20

Investments

Announcement

dateAcquirer Target

Deal value (US$

million)

November 2010 Songwon Industrial Co, Ltd High Polymer Labs Limited 20

September 2010 BASF India Ltd BASF Construction Chemicals (India) Pvt Ltd 33

September 2010 Jairam Phosphates-Facilities Khaitan Chem & Fertilizers Ltd -

July 2010Agri and Performance Polymer business of

Jubilant Organosy LtdJubilant Organosys Ltd (Shareholders) -

July 2010 Huntsman Corp Laffans Petrochemicals Limited -

June 2010 Atul Ltd Polygrip Rubber Production Pvt Ltd 2.2

May 2010 Godrej Sara Lee Ltd Godrej Consumer Products Ltd 233.6

March 2010 The Valspar (Singapore) Corporation Pte Ltd DIC Coatings India Ltd 9

Indian deals

*Excluding fertilisers

Sources: Chemicals NewViews, July–September 2010, ―M&A Transactions,‖ ThomsonOne Banker, accessed 24 November 2010

Mergers and acquisitions

• The chemicals sector* attracted cumulative foreign direct investment (FDI) of US$ 362 million in 2009–2010.

• Between August 1991 and September 2009, approvals for more than 900 foreign technology transfers (FTT) have been granted in the chemicals sector, accounting for 11.20 per cent of the total approvals.

Chemicals November 2010INVESTMENTS

21

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

22

Policy and regulatory framework

Licensing policy

• Licensing requirements have been removed, except for hazardous chemicals and a few special drugs.

• Entrepreneurs are allowed to set up chemicals industries following the Industrial Entrepreneurs’ Memorandum (IEM) route.

• Under the automatic route, 100 per cent FDI is allowed for all chemicals except hazardous ones.

Customs duty

• The peak rate of customs duty on most chemicals is 7.5 per cent.

Source: Department of Chemicals & Petrochemicals annual report

2009-10

Excise duty

• Excise duty of 16 per cent is applied on almost all chemicals.

PCPIR policy

• The PCPIR Policy has been introduced to boost the development of chemicals and petrochemicals investment regions.

Others

• Plans are underway to set up port-based chemicals parks in SEZs to encourage clustering, provide infrastructure and enable tax concessions.

• Downstream SEZs have been planned to use the output of chemicals parks.

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

23

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

24

Opportunities … (1/5)

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

Water treatment

chemicals

Alkali chemicals

Sources: ‖Working group on Indian chemical industry,‖ Planning Commission website,

http://www.planningcommission.gov.in/aboutus/committee/wrkgrp11/wg11_chemical.pdf, accessed November 19, 2010; ―On-Farm Land and

Water Management,‖ Central Soil Salinity Research Institute website, http://www.cssri.org/onfarm.pdf, accessed 15 November 2010.

• Alkali chemicals constitute the largest segment in the Indian inorganic chemicals sector and presents

high growth potential in domestic market.

• Net imports in the alkali chemicals sector grew at a CAGR of 24.3 per cent between 2003–04 and

2008–09.

• Increasing usage of recycled water and stringent government legislations will create demand for

water treatment chemicals such as chlorine.

• The utilisation of water treatment chemicals such as chlorine in India presents a significant

opportunity for chemical companies to tap their potential market demand in India.

25

Research &

Development

Eco-friendly

technology and

products

Logistics services

Opportunities … (2/5)

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

Sources: ‖Working group on Indian chemical industry,‖ Planning Commission website,

http://www.planningcommission.gov.in/aboutus/committee/wrkgrp11/wg11_chemical.pdf, accessed November 19, 2010

• The chemical industry in India is witnessing increased focus towards research and development,

which in turn provides opportunities for growth of R&D hubs and industry specific institutes.

• The government is also providing support to industry specific research institutes to promote

research. The Central government has planned to lend US$ 3.12 million (INR 149.8 million) in 2009–

2010 to Central Institute of Plastic Engineering & Technology (CIPET) to promote R&D efforts.

• There is a rising awareness in the industry about developing eco-friendly technology to reduce the

wastes generated and to develop similar products. Investing in R&D to develop such technology/

products is a potential growth area for the chemicals industry.

• Logistics services addressing the specific needs of the chemicals industry can serve as one of the

significant support infrastructure to promote the development of the industry.

• This can be leveraged by setting up logistic parks and transport hubs to support exports to other

parts of the world.

26

Dyestuff

Opportunities … (3/5)

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

Specialty chemicals

Sources: ‖Working group on Indian chemical industry,‖ Planning Commission website,

http://www.planningcommission.gov.in/aboutus/committee/wrkgrp11/wg11_chemical.pdf, accessed November 19, 2010; ―Specialty Chemicals

Market in India to Reach $40 Billion in Next Three Years,‖ Chemical Week website,

http://www.chemweek.com/markets/specialty_chemicals/flavors_and_fragrances/26018.html#, accessed 20 November 2010

• Textile sector is a major consumer of dyestuffs and accounts for 70 per cent of dyestuff

consumption in India. The GoI's policy to promote export of cotton goods and promote blend of

polyester fibres with cotton/viscose domestically is expected to result in continued high demand for

disperse dyes. The market demand for dye and dye intermediates in India is expected to grow at a

CAGR of 4.7 per cent from 652,000 tonnes in 2004–05 to 900,000 tonnes in 2010–11.

• Stringent environmental laws in the western countries have resulted in discontinuance of production

of certain dyes for textiles and leather, giving an opportunity to Indian chemical companies to

manufacture such products and export to these countries.

• India has emerged as an exporter of dyes, exporting dyes to Germany, U.K., U.S., Switzerland, Spain,

Turkey, Singapore and Japan. The export of dyes is expected to increase from US$ 1.5 billion in

2005–06 to US$ 2.6 billion in 2020.

• A rebound in consumer demand (driven by economic recovery) and significant outsourcing

opportunities are expected to drive growth in the Indian specialty chemicals market.

• The Indian specialty chemicals market is expected to grow from US$ 18 billion in 2006 to US$ 40

billion by 2013.

27

Petrochemicals

Opportunities … (4/5)

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

Agrochemicals

Sources: ‖India’s Petrochemical Sector Set for Higher Growth,‖ Chem Guide website, http://chemguide.asia/news/top/2010/01/05/indias-

petrochemical.html, accessed 15 November 2010; ‖Working group on Indian chemical industry,‖ Planning Commission website,

http://www.planningcommission.gov.in/aboutus/committee/wrkgrp11/wg11_chemical.pdf, accessed November 19, 2010.

• The long-term outlook for India’s petrochemicals industry is robust.

• The demand for plastics in the country is expected to record double-digit growth by 2015, driven

by population growth and increased industrialisation. In addition, the domestic demand for

polymers will double to11 MT by 2015.

• The robust demand forecast, along with GoI’s plans to develop PCPIRs in India, holds immense

opportunities companies to invest in petrochemicals sector in India.

• The GoI is placing increased emphasis on the growth of agriculture in India. The GoI is taking

initiatives to put the agriculture sector on the growth radar and achieve 4 per cent growth in the

Eleventh Five Year Plan period (2007–2012), up from the 2.5 per cent growth achieved in 2002–

2007.

• The government initiatives, amid rising food demand in India, is likely to give immense growth

opportunities to companies dealing in agrochemical products in the country.

• In addition, growing focus on biofuels is expected to give additional opportunities to agrochemical

companies in India. India plans to include 5 per cent biofuels in transportation by 2012 and 10 per

cent by 2017.

28

Fertilisers

Opportunities … (5/5)

Chemicals November 2010POLICY AND REGULATORY FRAMEWORK

Source: Chemicals NewViews, July–September 2010

• Urea consumption in India is growing and is expected to increase at a CAGR of 3.5 per cent from

26.5 MT in 2009–2010 to 31.4 MT in 2014–15. However, the domestic supply of urea is projected

to support only 24.6 MT in 2014–15, which gives opportunities to fertiliser companies to add

capacities in India and tap growing demand.

• The rise in contract farming trend is also expected to benefit fertiliser companies in India. Under

contract farming, the fertiliser companies produce products at economical labour and land costs in

India to export to high–demand regions of the world.

29

CHEMICALS November 2010

Contents

Advantage India

Market overview

Industry infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

30

Industry associations

Indian Chemical Council

Sir Vithaldas Chambers, 16-Mumbai Samachar Marg, Mumbai – 400023

Phone: 91 22 22047649/ 22846852

Fax: 91 22 22048057

Website: www.icmaindia.com

Alkali Manufacturers Association of India

3rd Floor, Pankaj Chambers, PreetVihar Commercial Complex, Vikas Marg, New Delhi – 110092

Phone: 91 11 22432003, 22410150, 55253401

Fax: 91 11 22468249

Website: www.ama-india.org

Indian Specialty Chemical Manufacturers' Association

1156, Bole Smruti, Suryavanshi Kshatriya Sabhagriha Marg, Off. Veer Savarkar Marg, Dadar (West)

Mumbai – 400 028

Tel: 91 22 2446 5003

Website: www.iscma.in

Chemicals November 2010INDUSTRY ASSOCIATIONS

31

Note

Wherever applicable, numbers in the report have been rounded off to the nearest whole number.

Conversion rate used: US$ 1= INR 48

Chemicals November 2010NOTE

32

India Brand Equity Foundation (―IBEF‖) engaged Ernst &

Young Pvt Ltd to prepare this presentation and the same

has been prepared by Ernst & Young in consultation with

IBEF.

All rights reserved. All copyright in this presentation and

related works is solely and exclusively owned by IBEF. The

same may not be reproduced, wholly or in part in any

material form (including photocopying or storing it in any

medium by electronic means and whether or not

transiently or incidentally to some other use of this

presentation), modified or in any manner communicated

to any third party except with the written approval of

IBEF.

This presentation is for information purposes only. While

due care has been taken during the compilation of this

presentation to ensure that the information is accurate to

the best of Ernst & Young and IBEF’s knowledge and belief,

the content is not to be construed in any manner

whatsoever as a substitute for professional advice.

Ernst & Young and IBEF neither recommend nor endorse

any specific products or services that may have been

mentioned in this presentation and nor do they assume

any liability or responsibility for the outcome of decisions

taken as a result of any reliance placed on this

presentation.

Neither Ernst & Young nor IBEF shall be liable for any

direct or indirect damages that may arise due to any act

or omission on the part of the user due to any reliance

placed or guidance taken from any portion of this

presentation.

DISCLAIMER

CHEMICALS November 2010