chinese banks’ transformation for ipo success - ibm · chinese banks’ transformation for ipo...

TRANSCRIPT

IBM Business Consulting Services

ibm.com/bcs

An IBM Institute for Business Value executive brief

Chinese banks’ transformation for IPO success

IBM Business Consulting Services, through the IBM Institute for Business Value, develops

fact-based strategic insights for senior business executives around critical industry-specific

and cross-industry issues. This executive brief is based on an in-depth study by the Institute’s

research team. It is part of an ongoing commitment by IBM Business Consulting Services to

provide analysis and viewpoints that help companies realize business value. You may contact

the authors or send an e-mail to [email protected] for more information.

Chinese banks’ transformation for IPO success IBM Business Consulting Services1

IntroductionChina’s banking industry, one of the most visible symbols of the country’s explosive growth, stands at a crossroads. The four largest banks, all state-owned, are in the midst of unprecedented transformation in preparation for government-encouraged initial public offerings (IPOs). After years of dominating the Chinese banking landscape, these state-owned commercial banks (SOCBs) now face the impending rivalry of global banking competitors, as the economy opens to foreign players. Only those Chinese banks that fundamentally transform their businesses and success-fully transition to public ownership will be able to translate their domestic leadership positions into competitive status on the global stage.

Transforming a business of any size, let alone a geographically dispersed industry titan in a country with a developing banking infrastructure, is no easy task. However, while it will not be easy, the transformation represents a significant opportunity for the SOCBs to focus on becoming a bank for the 21st century, while avoiding some of the evolutionary difficulties global banks have faced during their development. Successful firms will be those which adopt a disciplined approach, one that incorporates careful planning and a steadfast attention to detail. Based on experience with numerous clients around the world, IBM, through its Institute for Business Value and its Business Consulting Services, has outlined a set of practical, achievable best practices.

Reform through public ownershipA fundamental transformation is taking place throughout the Chinese economy, driven by its desire to integrate more fully with the rest of the world. Over the past 20 years, China’s gross domestic product (GDP) has grown at an annual rate of 9.4 percent, and the country’s banking sector has been an active participant in this heady expansion, growing at a 13 percent annual rate between 1997 and 2002.1 China’s bank assets comprise roughly 76 percent of the country’s total financial system assets – compared to the United States, where bank assets represent only 26 percent of total financial assets.2

Contents

1 Introduction

1 Reform through public ownership

4 Listing internationally in an uncertain environment

5 IPO transformation process

6 Pre-IPO

11 IPO

12 Post-IPO

16 Assessing the current state

17 About the authors

17 About IBM Business Consulting Services

18 References

Chinese banks’ transformation for IPO success IBM Business Consulting Services2

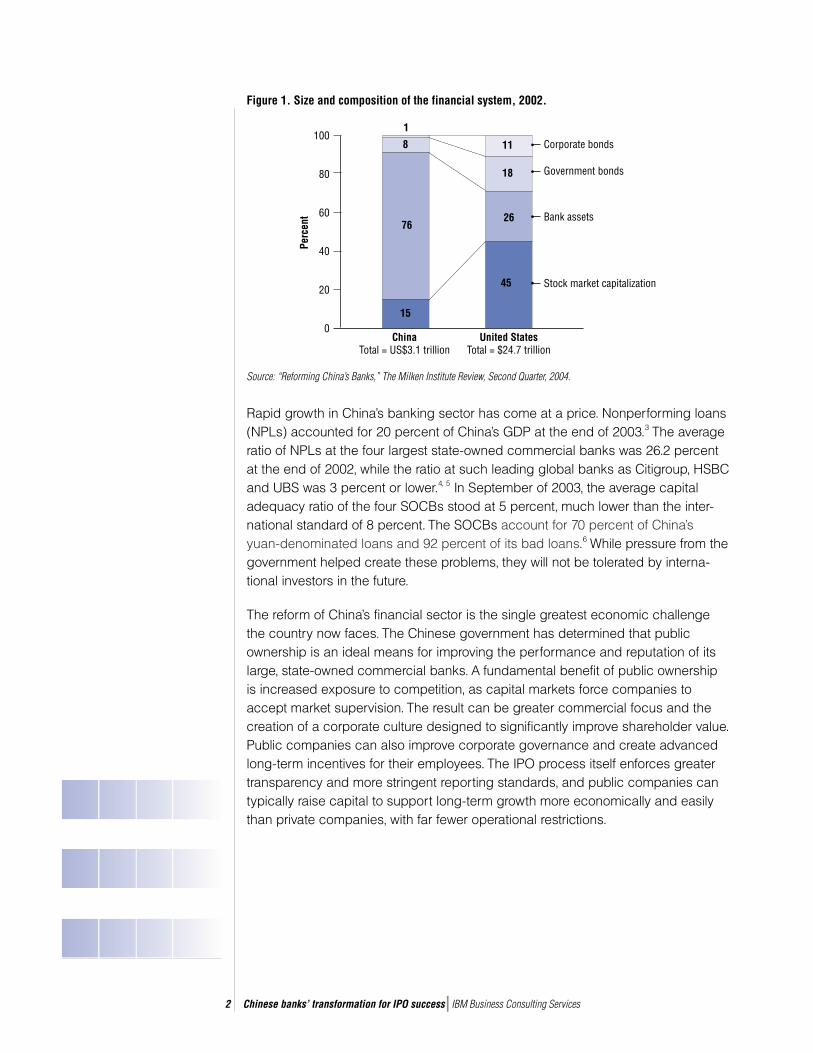

Figure 1. Size and composition of the financial system, 2002.

Rapid growth in China’s banking sector has come at a price. Nonperforming loans (NPLs) accounted for 20 percent of China’s GDP at the end of 2003.3 The average ratio of NPLs at the four largest state-owned commercial banks was 26.2 percent at the end of 2002, while the ratio at such leading global banks as Citigroup, HSBC and UBS was 3 percent or lower.4, 5 In September of 2003, the average capital adequacy ratio of the four SOCBs stood at 5 percent, much lower than the inter-national standard of 8 percent. The SOCBs account for 70 percent of China’s yuan-denominated loans and 92 percent of its bad loans.6 While pressure from the government helped create these problems, they will not be tolerated by interna-tional investors in the future.

The reform of China’s financial sector is the single greatest economic challenge the country now faces. The Chinese government has determined that public ownership is an ideal means for improving the performance and reputation of its large, state-owned commercial banks. A fundamental benefit of public ownership is increased exposure to competition, as capital markets force companies to accept market supervision. The result can be greater commercial focus and the creation of a corporate culture designed to significantly improve shareholder value. Public companies can also improve corporate governance and create advanced long-term incentives for their employees. The IPO process itself enforces greater transparency and more stringent reporting standards, and public companies can typically raise capital to support long-term growth more economically and easily than private companies, with far fewer operational restrictions.

Source: “Reforming China’s Banks,” The Milken Institute Review, Second Quarter, 2004.

ChinaTotal = US$3.1 trillion

United StatesTotal = $24.7 trillion

100

80

60

40

20

0

Perc

ent

45

26

18

11

15

76

8

1

Corporate bonds

Government bonds

Bank assets

Stock market capitalization

Chinese banks’ transformation for IPO success IBM Business Consulting Services3

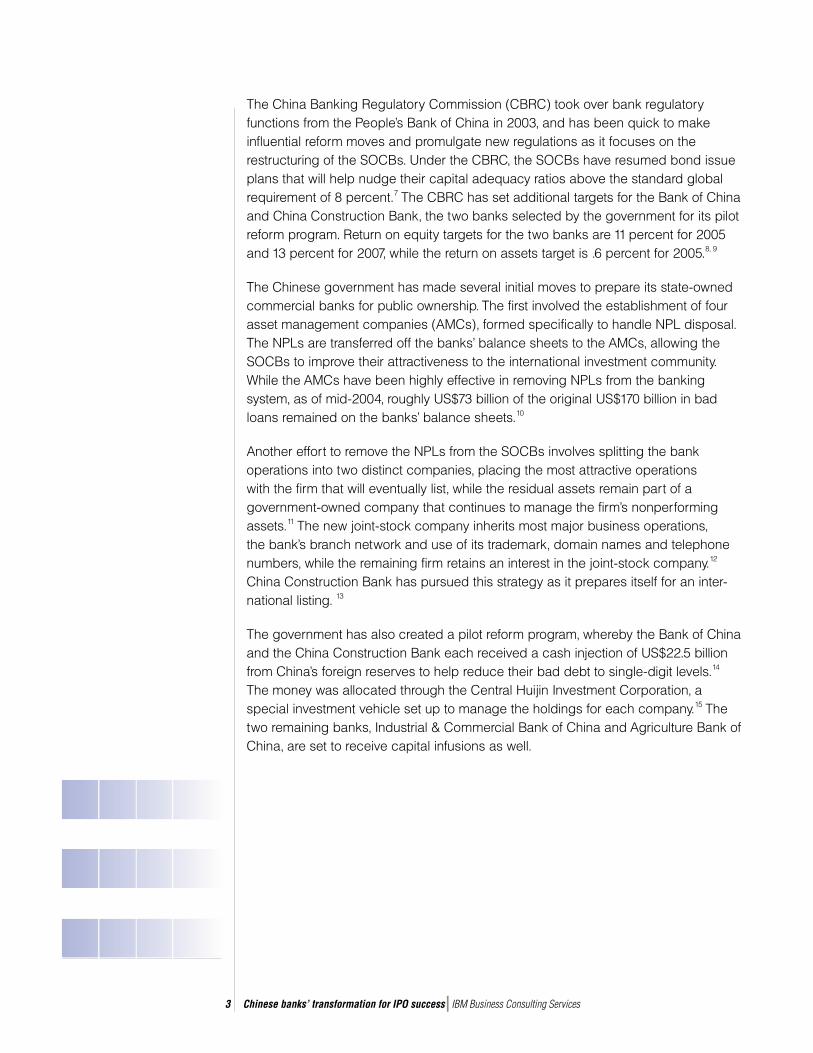

The China Banking Regulatory Commission (CBRC) took over bank regulatory functions from the People’s Bank of China in 2003, and has been quick to make influential reform moves and promulgate new regulations as it focuses on the restructuring of the SOCBs. Under the CBRC, the SOCBs have resumed bond issue plans that will help nudge their capital adequacy ratios above the standard global requirement of 8 percent.7 The CBRC has set additional targets for the Bank of China and China Construction Bank, the two banks selected by the government for its pilot reform program. Return on equity targets for the two banks are 11 percent for 2005 and 13 percent for 2007, while the return on assets target is .6 percent for 2005.8, 9

The Chinese government has made several initial moves to prepare its state-owned commercial banks for public ownership. The first involved the establishment of four asset management companies (AMCs), formed specifically to handle NPL disposal. The NPLs are transferred off the banks’ balance sheets to the AMCs, allowing the SOCBs to improve their attractiveness to the international investment community. While the AMCs have been highly effective in removing NPLs from the banking system, as of mid-2004, roughly US$73 billion of the original US$170 billion in bad loans remained on the banks’ balance sheets.10

Another effort to remove the NPLs from the SOCBs involves splitting the bank operations into two distinct companies, placing the most attractive operations with the firm that will eventually list, while the residual assets remain part of a government-owned company that continues to manage the firm’s nonperforming assets.11 The new joint-stock company inherits most major business operations, the bank’s branch network and use of its trademark, domain names and telephone numbers, while the remaining firm retains an interest in the joint-stock company.12 China Construction Bank has pursued this strategy as it prepares itself for an inter-national listing. 13

The government has also created a pilot reform program, whereby the Bank of China and the China Construction Bank each received a cash injection of US$22.5 billion from China’s foreign reserves to help reduce their bad debt to single-digit levels.14 The money was allocated through the Central Huijin Investment Corporation, a special investment vehicle set up to manage the holdings for each company.15 The two remaining banks, Industrial & Commercial Bank of China and Agriculture Bank of China, are set to receive capital infusions as well.

Chinese banks’ transformation for IPO success IBM Business Consulting Services4

Both the creation of the AMCs and the cash infusions to the SOCBs illustrate the Chinese government’s efforts to make the banks more attractive to the international investment community. The government is also seeking foreign investors – in the form of global financial services firms – to take significant ownership stakes in the banks. In doing so, these firms lend their brand name, banking expertise, transfor-mation capabilities – and thus their credibility – to the Chinese SOCBs. Both the Bank of China and China Construction Bank are currently in talks with large global players regarding strategic investments, but among the top five Chinese banks, only Bank of Communications, China’s fifth largest bank, has signed a deal. In August of 2004, HSBC signed a deal to acquire 19.9 percent of the Bank of Communications.16 Other global players are deepening their relationships with the Chinese banks by investing in the firms responsible for disposing of NPLs from the big four. Citigroup, for example, recently announced it would buy a 16.4 percent stake in Silver Grant International Industries, which has strong connections with China Construction Bank and is involved in disposing of its NPLs.17

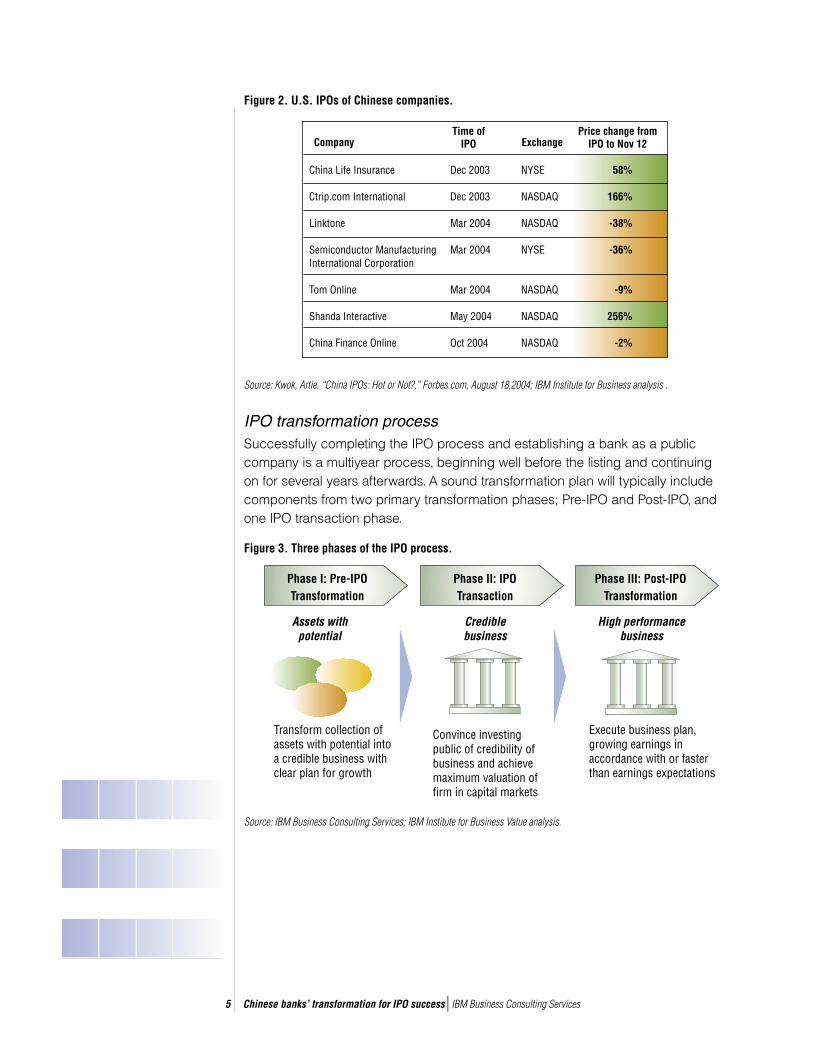

Listing internationally in an uncertain environmentExplosive growth in the Chinese economy, coupled with the government’s commitment to open up its economy in a measured way, has piqued the interest of businesses and investors around the globe.Not surprisingly, the market for listing Chinese companies on international exchanges has grown significantly in the last few years, as evidenced by China Life’s US$3 billion IPO in 2003.18

However, listing on an international exchange is not a guarantee of success. Performance of international offerings has been mixed over the past year, with the market softening during the summer of 2004. Four of the five Chinese companies that listed on U.S. exchanges in 2004 were trading below their offering price as of mid-November, and several Chinese firms have postponed their listings on the Hong Kong exchange.19, 20

Chinese banks’ transformation for IPO success IBM Business Consulting Services5

Figure 2. U.S. IPOs of Chinese companies.

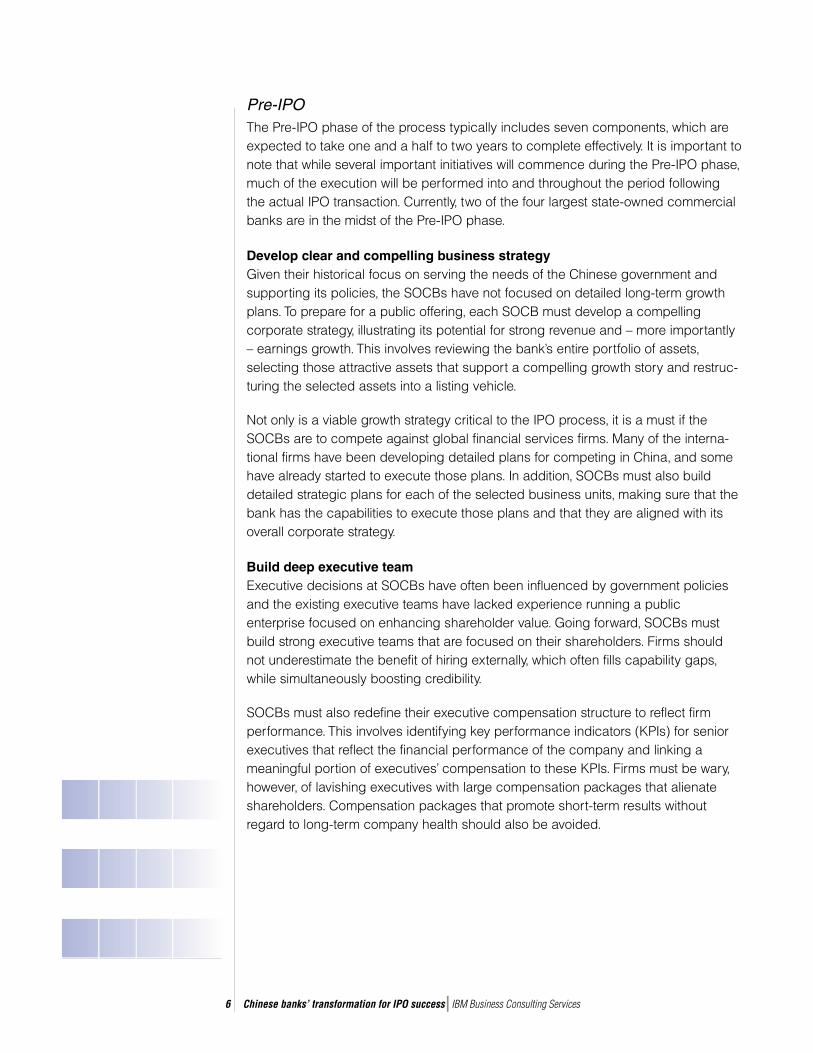

IPO transformation processSuccessfully completing the IPO process and establishing a bank as a public company is a multiyear process, beginning well before the listing and continuing on for several years afterwards. A sound transformation plan will typically include components from two primary transformation phases; Pre-IPO and Post-IPO, and one IPO transaction phase.

Figure 3. Three phases of the IPO process.

Source: Kwok, Artie. “China IPOs: Hot or Not?,” Forbes.com, August 18,2004; IBM Institute for Business analysis .

China Life Insurance

Ctrip.com International

Linktone

Semiconductor Manufacturing International Corporation

Tom Online

Shanda Interactive

China Finance Online

CompanyTime of

IPO ExchangePrice change from

IPO to Nov 12

Dec 2003

Dec 2003

Mar 2004

Mar 2004

Mar 2004

May 2004

Oct 2004

NYSE

NASDAQ

NASDAQ

NYSE

NASDAQ

NASDAQ

NASDAQ

58%

166%

-38%

-36%

-9%

256%

-2%

Phase I: Pre-IPOTransformation

Phase II: IPOTransaction

Phase III: Post-IPOTransformation

Assets with potential

Credible business

High performance business

Convince investing public of credibility of business and achieve maximum valuation of firm in capital markets

Execute business plan, growing earnings in accordance with or faster than earnings expectations

Transform collection of assets with potential into a credible business with clear plan for growth

Source: IBM Business Consulting Services; IBM Institute for Business Value analysis.

Chinese banks’ transformation for IPO success IBM Business Consulting Services6

Pre-IPOThe Pre-IPO phase of the process typically includes seven components, which are expected to take one and a half to two years to complete effectively. It is important to note that while several important initiatives will commence during the Pre-IPO phase, much of the execution will be performed into and throughout the period following the actual IPO transaction. Currently, two of the four largest state-owned commercial banks are in the midst of the Pre-IPO phase.

Develop clear and compelling business strategyGiven their historical focus on serving the needs of the Chinese government and supporting its policies, the SOCBs have not focused on detailed long-term growth plans. To prepare for a public offering, each SOCB must develop a compelling corporate strategy, illustrating its potential for strong revenue and – more importantly – earnings growth. This involves reviewing the bank’s entire portfolio of assets, selecting those attractive assets that support a compelling growth story and restruc-turing the selected assets into a listing vehicle.

Not only is a viable growth strategy critical to the IPO process, it is a must if the SOCBs are to compete against global financial services firms. Many of the interna-tional firms have been developing detailed plans for competing in China, and some have already started to execute those plans. In addition, SOCBs must also build detailed strategic plans for each of the selected business units, making sure that the bank has the capabilities to execute those plans and that they are aligned with its overall corporate strategy.

Build deep executive teamExecutive decisions at SOCBs have often been influenced by government policies and the existing executive teams have lacked experience running a public enterprise focused on enhancing shareholder value. Going forward, SOCBs must build strong executive teams that are focused on their shareholders. Firms should not underestimate the benefit of hiring externally, which often fills capability gaps, while simultaneously boosting credibility.

SOCBs must also redefine their executive compensation structure to reflect firm performance. This involves identifying key performance indicators (KPIs) for senior executives that reflect the financial performance of the company and linking a meaningful portion of executives’ compensation to these KPIs. Firms must be wary, however, of lavishing executives with large compensation packages that alienate shareholders. Compensation packages that promote short-term results without regard to long-term company health should also be avoided.

Chinese banks’ transformation for IPO success IBM Business Consulting Services7

Develop performance-based cultureThe single greatest challenge facing state-owned Chinese banks will likely be the transition to a competitive, effectively functioning, performance-based culture. The difficult task of preparing hundreds of thousands of employees for this transition begins with the design of performance-based compensation plans and effective training plans. Moving beyond these initiatives, firms must also focus on the more intangible aspects of encouraging employees to embrace the philosophy of a public company.

Historically, employee value proposition at SOCBs has not been geared toward rewarding high performance. Compensation is often based on tenure, and conse-quently, motivation tends to be low. Creating a direct link between performance and compensation will be critical as the SOCBs begin to compete with global players that have already instituted similar plans. Banks can link employee compensation to performance by using operational metrics related to an employee’s position and performance, or using nonmonetary rewards, such as training and certification, in addition to, or in place of, monetary rewards.

While these human resources initiatives must begin prior to the IPO transaction, the transformation to a performance-based culture is a lengthy process and will undoubtedly continue into the Post-IPO period. Instead of culminating after a certain number of years, these cultural changes will simply become part of the banks’ status quo of doing business. SOCBs have the opportunity to facilitate this cultural transition by leveraging the lessons learned by global banks and thereby avoiding serious mistakes.

Produce clear IT strategy to support overall business strategyAs part of their transformation, China’s banks must take steps to align their information technology (IT) and business strategies while remaining mindful of the developing the state of China’s technical infrastructure. For the most part, the IT infra-structures of the state-owned commercial banks were built at a time when the banks were simpler, less complicated organizations. The banks have historically had fairly rigorous, formal organizational structures, with very clear lines between the business and IT portions of the enterprise. However, the current transformations within the banks make it increasingly important – in some cases vital – to see greater collabo-ration between these two groups.

Chinese banks’ transformation for IPO success IBM Business Consulting Services8

Over the past several years, leading global banks have made significant strides in increasing the alignment of their IT and business organizations and are increas-ingly finding themselves using IT as a tool to enable superior business results. As Chinese banks move toward a more sophisticated, competitive structure, they must focus on shifting spending away from infrastructure maintenance and toward application development. Globally, the percentage of IT spend devoted to maintenance in financial services is projected to decline 6.3 percent between 2004 and 2008.21 A flexible new IT architecture must then be designed to support future growth as customers become more demanding and competition continues to increase.

Strengthen corporate governanceGood corporate governance is key to China’s banking reforms, and taking steps to improve corporate governance practices among Chinese banks prior to their IPOs is critical. Globally, investors have indicated a willingness to pay a premium for a well-governed company. However, the history of corporate governance in China is quite short, with the concept first introduced to China’s economic reform in 1993 and officially recognized a major goal in 1999, when the government began to encourage the establishment of modern enterprise systems in the SOCBs.22

Going public will not automatically improve the performance of banks; it is sound corporate governance that will attract foreign investors and facilitate the banks’ IPOs. Chinese banks will need to restructure current corporate governance systems and procedures to reflect leading practices, especially around audit, risk and compen-sation committees, three areas of focus in today’s environment.23 Given the sheer size of the SOCBs, technological advances will also be critical to strengthening internal controls throughout the banks, and further preventing the formation of bad loans. The banks will then need to reform personnel policies, transform the culture of their organizations to reflect these policies, and update and redefine the role of the board of directors.24 For example, banks might develop boards that actively oversee management, help set corporate strategy, monitor risk management and help develop succession plans.

“In my view, listed companies

as a whole, still boast the best

corporate governance in China –

experience has proven that share-

holding reform is a major way to

boost corporate governance”

– Zhou Xiaochuan, Governor of the

People’s Bank of China 25

Chinese banks’ transformation for IPO success IBM Business Consulting Services9

Improve transparencyIn order to improve transparency, China’s banks need to focus on three areas within the financial management function:

• Financial operations and infrastructure

• Profitability measurement and reporting

• Planning and forecasting.

Firms should assess all three of these areas, identify existing gaps and design solutions to fix critical problems, while retaining the flexibility to increase functionality in the future as leading practices are adopted.

Revamping the financial operations and infrastructure to provide robust, timely and consistent financial information across the company is crucial for creating sound controls, meeting regulatory requirements and successfully growing the business. Transformation in this area will be significant as firms redesign their organizations, processes and technology infrastructures, taking advantage of opportunities for consolidation, shared services – and in some cases – outsourcing.

Enabling profitability measurement and reporting will also become increasingly important as state-owned banks focus on the bottom line. Building the capabilities to analyze the business by division, product, and customer segment will enable firms to compete more effectively, with global players already leveraging this information to optimize their capital allocation.

Finally, improving the firms’ ability to accurately forecast the financial performance of the company, both short and long term, will be critical as firms manage expectations in the capital markets and try to sustain a high valuation. To enhance their capabil-ities in this area, firms should focus on implementing continuous and integrated budgeting and planning, rolling forecasts and activity-based budgeting. It is important to note that while several of the banks have hired accountants to perform the enormous, manual task of creating a one-time financial statement for their IPOs, this does not constitute the attainment of financial transparency. Transformation within the financial management function is necessary for firms to provide ongoing transparency to regulators and investors and to effectively serve clients.

Chinese banks’ transformation for IPO success IBM Business Consulting Services10

Develop sound risk management and internal controlsChinese banks need to develop consistent, enterprisewide, risk management systems, and create an effective system of internal controls to help ensure compliance with risk management policies and procedures. Risk frameworks for credit, market and operational risk need to be constructed in line with upcoming regulations, including Basel II. Risk frameworks can be further enabled through the:

• Hiring of experienced risk professionals

• Establishment of a risk-aware culture throughout the organization

• Creation of necessary systems to support this risk infrastructure.

The immediate focus for China’s financial sector is credit risk, with market and operational risk becoming increasingly important as the transformation progresses. There is currently little credit risk infrastructure in China; the People’s Bank of China is considering the creation of such a system, but it has yet to be developed. However, individual firms have started exploring ways to develop their own solutions. ICBC has just signed a deal with American Express, where – in addition to rolling out the company’s credit card – the bank will receive training and technology from American Express to improve its credit-risk assessment systems. And Bank of China has just been approved to open its own bank card center, which will allow it to better coordinate the revolving credit mechanism that is at the heart of the credit card system. 26

Bank of China - On the path to public ownership

When discussing the transformation of Bank of China and China Construction Bank – two of the “big

four” banks slated for an international listing in 2005 – Vice-Premier Huang Ju referred to “a war that must be won.”27 The scope of the transformation necessary at the Bank of China is daunting due to its sheer size, US$6.5B in profits during the first 10 months of 2004 and over 11,600 branches.28, 29 However, the Bank, in the middle of a multiyear transformation, is winning the war on several fronts, making significant strides in the critical areas of corporate governance, risk management and culture. Although much work remains, a quick review of the progress to date shows just how far Bank of China has come in the last 18 months.

Strengthening corporate governance. In early 2003, Bank of China’s board included 63 members.30 Not only was the board unwieldy, it also lacked the independence and international expertise that international investors look for on corporate boards.31 During the past 18 months, the Bank of China has trimmed the number to a manageable 12 members.32 Now, instead of a group of retired general managers, the board consists of only four executives, with six government officials and two international directors filling the remaining seats.33 The bank intends to further strengthen the board by appointing

Chinese banks’ transformation for IPO success IBM Business Consulting Services11

Peter Cooke, formerly of the Bank of England.34 Additional international expertise is being sought, with former U.S. Federal Reserve Chief Paul Volcker and Nobel laureate Joseph Stiglitz as potential targets.35 While only time will tell how effective this new board will be, Bank of China has sent a clear message to investors that it is serious about corporate governance.

Developing a performance-based culture. Prior to the current transformation, Bank of China, like the other three large state-owned banks, retained excess capacity, lacked focus on the bottom line, and often failed to link employee compensation to performance. Today, the bank is taking steps to tackle these shortcomings and develop a performance-based culture. Before the restructuring, many positions lacked something as basic as a job description. Going forward, job descriptions are being created and eventually all 230,000 employees aside from the top 10 executive managers will have to reapply for their jobs.36 After years of rewarding employees based on seniority, key performance indicators are being developed to link compensation directly to employee performance. Previous attempts to develop this link proved unsuccessful when compensation was linked to top-line growth, primarily in assets, and employees were rewarded without regard to risk and the bottom line.37 New compensation plans are focusing on the bottom line. “Profit has become the sole goal” according to Zhu Min, head of restructuring and listing at Bank of China.38

Developing sound risk management and internal controls. During the rapid expansion of the Chinese economy over the past several years, banks, feeling pressure from government officials, paid only limited attention to risk and capital adequacy. Fitch analyst David Marshall estimates that local governments illegally underwrote US$100 billion in loans.39 Only recently have the banks begun to seriously address this issue. Bank of China has set up committees to review credit risk and has transferred the loan approval process from localities where high rates of bad debt originated to a centralized location.40 By the end of 2004, Bank of China will have “tried and penalized” 50,000 staff for fraud.41 Progress is being made, but a significant amount of work remains. Loan growth has slowed, but banks still lack the adequate risk management systems and internal controls to compete with global firms.

IPOThe second phase of the IPO process, the transaction phase, involves convincing the investing public of the business’ credibility, and achieving the optimum initial valuation of the firm in the capital markets. This phase typically takes about six months.

During the IPO phase, a critical focus of the Chinese banks will be partnering with, and providing support to, intermediaries, most importantly a lead IPO manager. Each SOCB will need to select a lead manager for its IPO with experience in both China and international markets. In addition, the banks will need to identify and choose an internationally credible accounting firm for audit and projections, and an experienced and credible law firm. It is essential that the bank work closely and openly with all intermediaries to provide the necessary information for due diligence work. These partnerships are crucial to securing approval from domestic and inter-national regulators.

Chinese banks’ transformation for IPO success IBM Business Consulting Services12

Chinese banks must also extend resources toward the development and delivery of a strong message to investors. SOCBs will need to collaborate with their lead manager to develop a credible investing theme and verify that the executive team includes effective communicators in the appropriate positions. The banks must also work with the lead manager to deliver a strong road show and support their listing with effective communications around the IPO. In addition to their external messaging, firms should develop an internal communication strategy as part of their change management program to keep employees informed and involved in the process and to avoid any potential legal or regulatory complications.

Post-IPOThe Post-IPO phase revolves around executing the business plan to increase revenue and earnings in line with, or faster than expectations. For transformations this large and complex, the third phase could take approximately three to five years, at which time the business activities involved will simply become part of the bank’s “way of doing business.” After the IPO, firms must stay focused on completing their transformation. Capital markets will continue to reward firms that improve their operations and deliver on their revenue and earnings targets while penalizing those that do not. The Post-IPO phase involves six primary areas of focus.

Deliver on revenue & earnings targetsCentral to the Chinese banks’ success following their IPOs will be their ability to follow through and deliver on the revenue and earnings targets developed prior to listing. This will require the banks to implement both their overall corporate plan and their strategic business unit plans. The SOCBs must create dedicated teams in all strategic business units to:

• Implement strategies developed pre-IPO

• Build effective business models

• Cascade KPIs and balanced scorecards to business lines to monitor and verify performance

• Develop performance incentives throughout organizational levels.

Progress achieved during the transformation must be maintained and even pushed forward if the SOCBs are going to compete against the global banking leaders.

Chinese banks’ transformation for IPO success IBM Business Consulting Services13

Lead the way in product innovation and developmentDelivering on long-term financial targets necessitates a commitment to product innovation and development. SOCBs must build strong product development teams to facilitate the launch of, or further penetration of the innovative and differentiated products that Chinese consumers want. Credit cards and wealth management represent two critical areas of focus for SOCBs. International banks entering China possess deep expertise in both of these areas. Losing the most attractive customers to the international banks is not something the SOCBs can afford. On the commercial side, the rapidly growing area of trade finance should be a strong area of focus.

In order to strengthen their product development capabilities, firms should fill gaps in current teams with demonstrated experts who can effectively assess potential demand and differentiation factors for new and existing products, and develop business models for new product development and launch. This can be further enhanced by aligning the compensation of product development teams with performance. Banks must also leverage – either through external hires or research – the knowledge developed by leading players in other markets, in order to jumpstart their own efforts in the credit card and wealth management space. Moving beyond the product development staff, banks need to promote a strong culture of innovation throughout the organization. Capital One is a prime example of a company committed to fostering innovation in its workforce. The firm’s U.K. operations have instituted a number of initiatives, starting in the recruiting process, where specific types of interviews are designed to identify the creative abilities of candidates and are sustained in daily operations where peer awards are given for innovative thinking.42

Build trusted brandFollowing their IPOs, each state-owned bank will need to shed the image of a monolithic government institution, and begin to build their brand with both customers and investors. Currently, SOCBs enjoy strong name recognition but trail interna-tional banks in the area of customer service. Lack of competition in the industry has led to an absence of focus on customer service at SOCBs, as evidenced by long lines for tellers. At the same time, international firms offer much quicker access through multiple channels. Significant investment and focus on customer service will be required to build a reputation as a leading financial services provider. SOCBs have an opportunity to avoid some of the mistakes, such as lack of both channel integration and a single customer view that have slowed the progress of global banks in the last decade.

Chinese banks’ transformation for IPO success IBM Business Consulting Services14

Beyond the traditional customer, SOCBs that move to public ownership will have a new constituency that must be won: investors. Firms must not overlook the importance of brand in the area of investor relations. Timely and accurate communi-cation with the investment world will be critical for firms looking to limit volatility and sustain high valuations.

Improve operational efficiencyInvestors will look to the newly public banks for clear evidence of improved operational efficiency following the IPO. The existing decentralized operations of the enormous branch networks in the SOCBs will be unsustainable in the face of foreign competition. Banks will need to continue to take processes out of the individual branches and centralize them, leveraging their economies of scale. To do this, they will design new operational architectures, and then define the operational require-ments and workflow. They must also implement finance, reporting, management control, and human resource systems, which integrate existing financial data marts with the processes to produce financial reports.

Moving beyond systems and processes, SOCBs must focus on the cultural aspects of their organization. Due to the sheer size of their organizations, a strong change management office will be critical as firms seek to implement plans developed in the pre-IPO stage. Firms must verify that they have the systems in place to collect and monitor the selected KPIs so that they can follow through on the initiatives to compensate employees based on performance.

Strengthen risk management & internal controlsFollowing the IPO, Chinese banks will need to demonstrate to investors that they have taken concrete steps to strengthen their organizations’ risk management and internal controls. SOCBs face a difficult dilemma; they must exhibit attractive growth rates without taking undue risk. Investors will not tolerate the enormous credit losses of years past. In order to accomplish this, the banks will have to follow through on pre-IPO plans to implement leading risk management systems. Once a risk management system has been implemented and integrated with the business’ workflows and processes, the banks should develop incentive plans to foster adoption and use throughout the organization.

Build competitive IT infrastructureFinally, it is critical for Chinese SOCBs to follow their IPOs by building a competitive IT infrastructure, with viable operational, analytical, and technical capabilities. This transformation of existing IT infrastructures will involve the construction of a new architecture, based on the competitive master plan developed by the bank pre-IPO. Successful firms will create a flexible and resilient architecture that will allow the firm to respond to customer demands and evolving industry dynamics.

Chinese banks’ transformation for IPO success IBM Business Consulting Services15

Bank of China Hong Kong – Lessons of a listed bank Bank of China Hong Kong’s (BOCHK) listing on an international exchange in Hong Kong serves as the prime example of a state-owned bank that has gone through the entire IPO process. Born through the integration of 10 sister banks over a two-year period, BOCHK listed on the Hong Kong exchange in July of 2002.43 Debuting in a down market, the stock closed down 3 percent the first day and traded between HK$7.50 and HK$ 9.00 for over a year before beginning its climb to the mid-teens, where it is trading as of this writing.44 A brief examination of BOCHK’s pre-IPO and post-IPO planning and execution provides valuable lessons for the mainland’s “big four.”

Bank of China Hong Kong’s strong commitment to corporate governance prior to the IPO makes it stand out as a model for banks entering the process. BOCHK took several steps to dramatically improve the independence and effectiveness of the board. The Bank appointed four independent directors, including three with significant international experience in the industry. In addition, the Bank set up risk management, remuneration and audit committees at the board level that received direct reports from functional department heads. Taking these steps earned BOCHK high marks from analysts.

BOCHK also dedicated significant resources to improving risk management, a primary concern for analysts. The bank ended 2001 with a nonperforming loan ratio of 11 percent, more than twice the ratio of the average Hong Kong Bank.45 By the Bank’s own admission, its risk management processes lacked rigor. For example, BOCHK has indicated that it “relied excessively on the governmental relationships or guarantees, failing to pay sufficient attention to the repayment ability of the borrower of guarantor.”46 Recognizing this shortcoming, the Bank hired an internationally respected consultancy to redesign the risk management function, from the risk policies to the infrastructure and rating models. Improved risk management, write-offs and collections allowed the bank to reduce its nonperforming loan ratio to 4.1 percent by the end of June 2004.47

BOCHK’s strong focus on governance and risk management was partially offset by the difficulties it faced as it tried to move beyond basic transparency requirements and transition to a performance-based culture. Prior to the IPO, Bank of China Hong Kong satisfied the minimal requirements for listing, but did not complete the improvements necessary to avoid significant manual reconciliation and provide management information for responsive decision-making. Fragmented and out-of-date data systems continued to hamper the firm’s business capabilities even after the company listed shares on the exchange. Despite a carefully constructed change management plan, the bank was not able to execute the transition to a performance-based culture. Two years after the public offering, the bank was still compensating employees based on tenure, rather than on their qualifications or performance. However, in July of 2004, the bank said management was “redefining human capital management” policies and a

bank source confirmed that compensation would be linked to qualifications and performance.48

Bank of China Hong Kong’s difficulties in the areas of risk management, transparency and culture change led to skepticism by international investors and perhaps a less than optimal market valuation for the firm. The “big four” banks must learn from BOCHK’s experience and ensure that none of the critical objectives of the pre- or post-IPO stages are ignored.

Chinese banks’ transformation for IPO success IBM Business Consulting Services16

Assessing the current stateLarge-scale transformation is one of, if not the most, complex and challenging initiatives a firm can undertake. As you assess the progress of your firm’s transfor-mation initiatives and long-term plans for success, consider the following questions:

• Does your firm’s transformation plan address all seven critical areas of pre-IPO preparation? Does your plan contain the details necessary to implement such a complex plan?

• How well-equipped is your firm to execute your transformation plan? Do your employees possess the necessary skill sets?

• Have you identified the areas that will require external expertise? Is there a plan in place to select the most appropriate partners?

• Has your firm adequately planned for post-IPO execution? Will your firm be able to deliver the growth and earnings that the capital markets are expecting?

To learn more about transforming your business and planning for long-term success as a public company, please e-mail Ian Ball at [email protected] or visit us at http://www-900.ibm.com/cn/services/bcs/index.shtml.

Chinese banks’ transformation for IPO success IBM Business Consulting Services17

About the authorsIan Ball is the Asia Pacific Financial Services Sector Leader for IBM Business Consulting Services. He can be reached at [email protected].

Allison Hilberg is a Senior Consultant with the IBM Business Consulting Services Strategy & Change Practice. She can be reached at [email protected].

Shanley Lee is an Associate Partner with IBM Business Consulting Services. He can be reached at [email protected].

Sally Sha is a Senior Consultant with IBM Business Consulting Services. She can be reached at [email protected].

Greg Robinson is a Senior Consultant with the IBM Institute for Business Value Financial Services Team. He can be reached at [email protected].

ContributorsDan Latimore is the Executive Director of the IBM Institute for Business Value. He can be reached at [email protected].

Sunny Banerjea is the Global Banking Leader for the IBM Institute for Business Value. He can be reached at [email protected].

About IBM Business Consulting ServicesWith consultants and professional staff in more than 160 countries globally, IBM Business Consulting Services is the world’s largest consulting services organi-zation. IBM Business Consulting Services provides clients with business process and industry expertise, a deep understanding of technology solutions that address specific industry issues, and the ability to design, build, and run those solutions in a way that delivers bottom-line business value.

Chinese banks’ transformation for IPO success IBM Business Consulting Services18

References1 “World Bank Competitiveness Report,” World Bank Group, 2003.2 Barth, James, Rob Koepp, and Zhongfei Zhou. “Reforming China’s Banks,” The

Milken Institute Review, Second Quarter 2004.3 “China’s economic slowdown could trigger new wave of bad loans – Fitch,” AFX

Asia, August 31, 2004.4 “China economy: Concerns over “systemic credit risk,” Economist Intelligence Unit

– Views Wire, December 29, 2003.5 IBM Institute for Business Value analysis.6 “CRBC to Announce Defensive Measures for China’s Financial Sector” China

Business Strategy, November 30, 2004.7 “Basel II: International Convergence of Capital Measurement and Capital

Standards: a Revised Framework,” Bank of International Settlements, June 20048 Dickie, Mure. “China sets tough targets for leading state banks,” Financial Times,

March 12, 2004.9 Chi-chu, Tschang. “China sets benchmarks for 2 big banks,” The Straits Times,

March 12 2004.10 “Non-Performing Loan Securitization in the People’s Republic of China,” Stanford

University, May 2004.11 “China Construction Bank Splits Operations Amidst Management Doubts” Dow

Jones, June 10, 2004.12 “China Construction Bank Statement Confirms Restructuring” Dow Jones, June

9, 2004.13 Ibid.14 Dingmin, Zhang. “Funds Infusion to Boost Banking Reform,” China Daily, January

7, 2004.15 “Bank of China, Construction Bank nearer listing after capital injection,” AFX

International Focus, January 6, 2004.16 “HSBC takes stake in Bank of Communications,” Business Daily Update, August

6, 2004.17 “China Finance: Citigroup to deepen involvement in disposal of NPLs,” Economist

Intelligence Unit – Views Wire, November 24, 2004.18 Kwok, Artie. “China IPOs: Hot or Not?,” Forbes.com, August 18,200419 Ibid.

Chinese banks’ transformation for IPO success IBM Business Consulting Services19

20 IBM Institute for Business Analysis.21 Garcia, Virginia. “2005 Global IT Spending Outlook: Revving Growth Engines with

‘Under-the-Hood’ Investments,” TowerGroup, December 2004.22 “Corporate Governance Key to Banks.” December 8, 2004. http:/www.China.org.cn23 Ibid.24 Ibid.25 Ibid.26 “Chinese Banks to Offer U.S. Credit Cards,” The Boston Globe, December 8, 2004.27 “Banking on foreign talent,” South China Morning Post, November 16, 2004.28 “Daily Alert- Bank of China Profits Up,” Emerging Markets Daily News, December

1, 2004.29 “Massive shake-up for Bank of China,” Business Daily Update, November 18, 2004.30 McGregor, Richard. “Chinese bank plans personnel revolution: The Bank of

China has big changes in mind for its 230,000 workers,” Financial Times, November 17, 2004.

31 Ibid.32 Ibid.33 Ibid.34 Seawright, Stephen. “Bank of China hires former Bank of England regulator,”

Sunday Business, August 29, 2004.35 “Root and branch – China’s banks,” The Economist, November 6, 2004.36 Ibid.37 Ibid.38 McGregor, Richard. “Chinese bank plans personnel revolution: The Bank of

China has big changes in mind for its 230,000 workers,” Financial Times, November 17, 2004

39 “Root and branch – China’s banks,” The Economist, November 6, 200440 Ibid.41 Ibid.

Chinese banks’ transformation for IPO success IBM Business Consulting Services20

42 Brownlee, Fergus. “How to create an innovative work force,” Financial World, February 2004.

43 McBride, Sarah. “Questioning the books: Bank of China (Hong Kong) is latest to drop Andersen – Account goes to PricewaterhouseCoopers,” The Asian Wall Street Journal, April 11, 2002.

44 IBM Institute for Business Value analysis.45 Lau, Dominic and Bei Bei She. “Update 1 – BOC HK says may take time to tighten

controls,” Reuters News, July 9, 2002.46 Ibid.47 “Fitch: Bank of China Hong Kong’s ratings assigned,” The Asian Banker,

November 15, 2004.48 Yiu, Enoch. “New BOCHK; ideology to shatter iron rice bowl,” South China

Morning Post, July 17, 2004.

© Copyright IBM Corporation 2005

IBM Global ServicesRoute 100Somers, NY 10589U.S.A.

Produced in the United States of America02/05All Rights Reserved

IBM and the IBM logo are trademarks or registered trademarks of International Business Machines Corporation in the United States, other countries, or both.

Other company, products and service namesmay be trademarks or service marks of others.

References in this publication to IBM products and services do not imply that IBM intends to make them available in all countries in which IBM operates.

G510-4005-00