city of missoula, montana audit exit conference year ended june 30, 2013 presented february 26, 2014

TRANSCRIPT

CITY OF MISSOULA, MONTANA

Audit Exit ConferenceYear Ended June 30, 2013Presented February 26, 2014

Presentation Outline

• Acknowledgements• Scope of Audit• Summary of Audit Results• Financial Statement Highlights• Internal Controls and Compliance• Audit Committee Communications• Component Units• Looking Forward

Audit Scope

• U.S. Generally Accepted Auditing Standards• Government Auditing Standards• Single Audit Act/OMB Circular A-133• All City Funds• Component Units – Missoula Parking Commission– Missoula Redevelopment Agency– Business Improvement District

New Standards

• GASB 61 – amends the definition of component units

• GASB 62 – clarifies the applicability of certain FASB and AICPA pronouncements for business-type activities

• GASB 63 – amends definition of certain assets and liabilities, provides guidance for the reporting of deferred inflows and outflows and redefines the residual measure as net position

Summary of Audit Results

• Clean (unmodified) opinion on financial statements

• No internal control findings over financial reporting

• No findings related to major federal programs

Financial Statement Highlights

• Government-wide net position• Governmental funds fund balances• Revenues • Expenses• Mill Levies• Taxable Values• Debt Margin

Net Position (000)

2009 2010 2011 2012 2013 -

50,000

100,000

150,000

200,000

250,000

300,000

Governmental Business-type

Net Position by category(000)

2009 2010 2011 2012 2013 -

50,000

100,000

150,000

200,000

250,000

300,000

Net Invest in Capital Assets Restricted Unrestricted

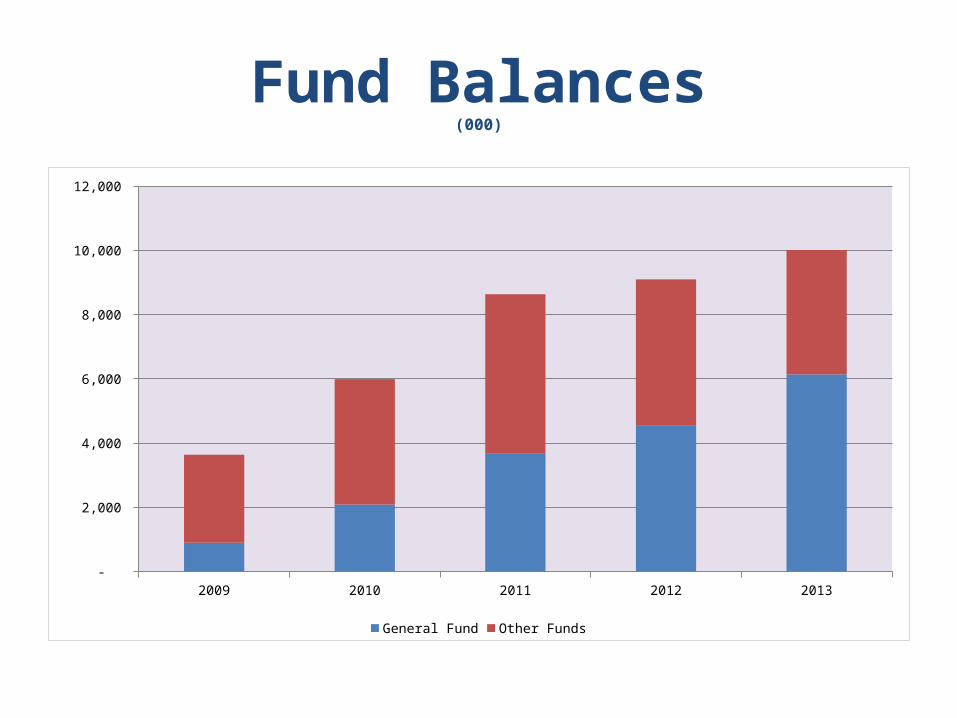

Fund Balances(000)

2009 2010 2011 2012 2013 -

2,000

4,000

6,000

8,000

10,000

12,000

General Fund Other Funds

Fund Balance Classifications under GASB 54

GASB 54 CLASSIFICATIONS

2013 2012 2011

Nonspendable $ 1,259,186 $ 1,244,344 $ 1,160,272

Restricted 6,947,461 7,515,122 8,077,142

Committed 2,892,425 2,048,128 1,374,228

Assigned 1,757,237 1,284,045 1,203,481

Unassigned (2,841,994) (2,990,903) (3,178,969)

Total $ 10,014,315 $ 9,100,736 $ 8,636,154

Fund Revenues (000)

2009 2010 2011 2012 2013 -

10,000

20,000

30,000

40,000

50,000

60,000

70,000

General All other

Fund Expenditures(000)

2009 2010 2011 2012 2013 -

10,000

20,000

30,000

40,000

50,000

60,000

70,000

General All other

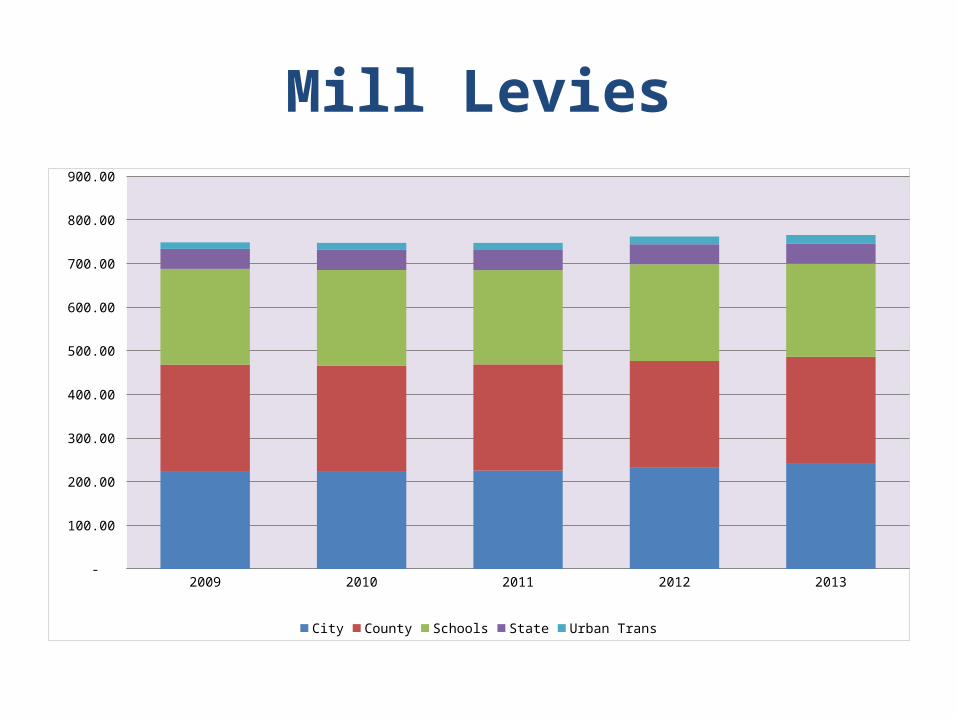

Mill Levies

2009 2010 2011 2012 2013 -

100.00

200.00

300.00

400.00

500.00

600.00

700.00

800.00

900.00

City County Schools State Urban Trans

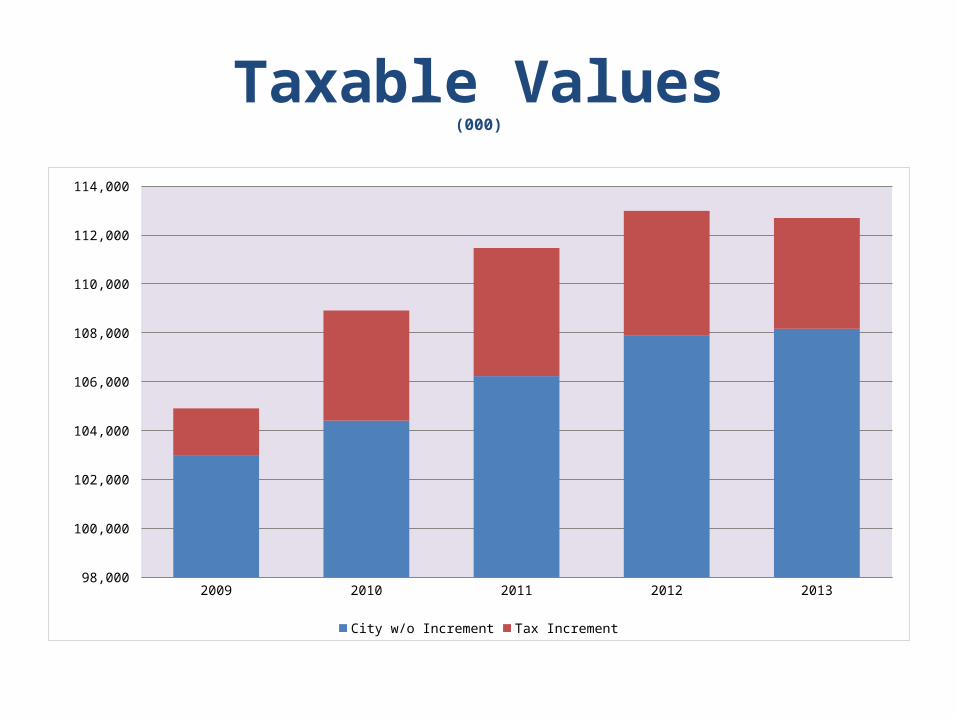

Taxable Values(000)

2009 2010 2011 2012 2013 98,000

100,000

102,000

104,000

106,000

108,000

110,000

112,000

114,000

City w/o Increment Tax Increment

Debt Margin(000)

2009 2010 2011 2012 2013 70,000

75,000

80,000

85,000

90,000

95,000

Governance Communications

• Auditor Responsibilities• Planned Scope and Timing• Accounting Policies• Significant Audit Findings• Difficulties in Performing the Audit• Corrected and Uncorrected Misstatements• Other Information in the CAFR• Disagreements with Management• Management Representations• Consultations with Other Accountants

Component Units

• Missoula Redevelopment Agency– Clean opinion on financial statements– No findings related to internal control over

financial reporting, no compliance findings

• Missoula Parking Commission– Clean opinion on financial statements– No findings related to internal control over

financial reporting, no compliance findings

Component Units

• Business Improvement District– Included in CAFR as a discretely-presented

component unit–No separate report issued– Two internal control findings

Looking Forward

• The Missoula economy is slowly recovering • ARRA funds were still present on extended

grants in 2013

• OMB proposal related to Single Audit– May affect scope of testing

Looking Forward

• Single Audit proposed changes:– Increase in threshold to $750,000– One “super” circular to merge all current circulars– Reduction in number of compliance requirements

QUESTIONS?