cohen grassroots research, inc. -...

TRANSCRIPT

Cohen Grassroots Research, Inc. Excellence – Quality

www.cohengrassroots.com Telephone: 415.454.6985

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be

reproduced.

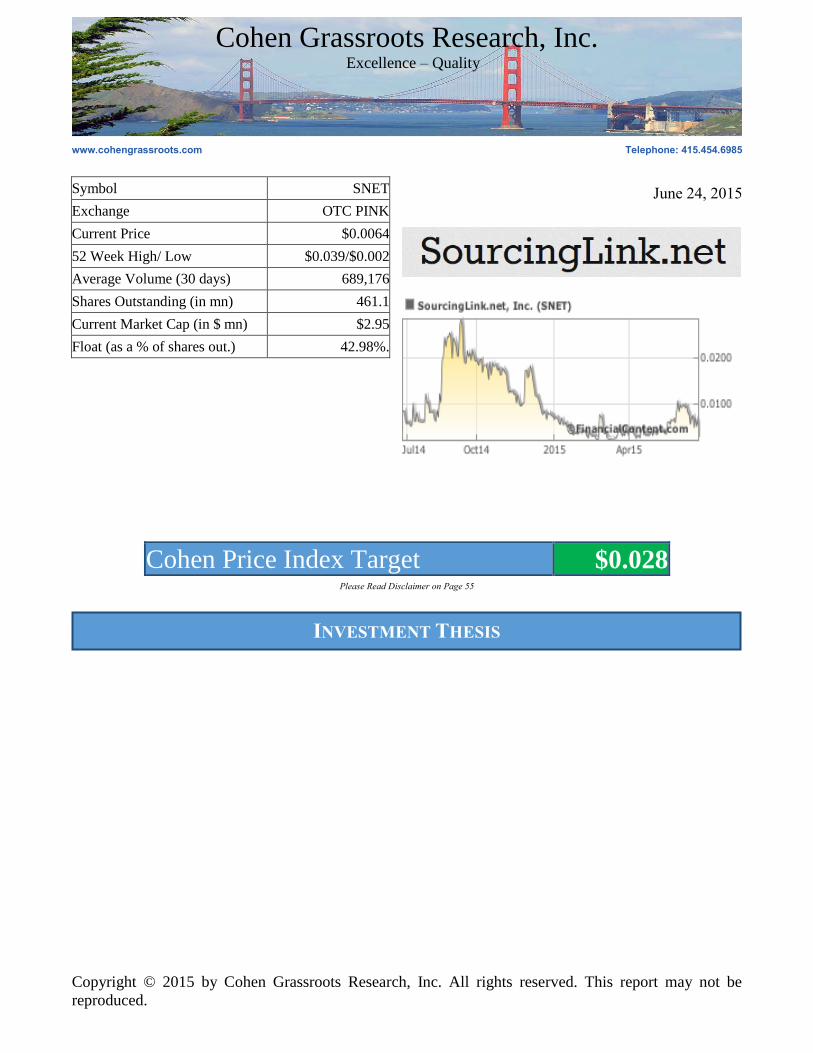

June 24, 2015

Cohen Price Index Target $0.028

Please Read Disclaimer on Page 55

Symbol SNET

Exchange OTC PINK

Current Price $0.0064

52 Week High/ Low $0.039/$0.002

Average Volume (30 days) 689,176

Shares Outstanding (in mn) 461.1

Current Market Cap (in $ mn) $2.95

Float (as a % of shares out.) 42.98%.

INVESTMENT THESIS

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 2 of 26

SourcingLink.Net, Inc. (OTC Pink: SNET) is a US based company pursuing the exploration and development of Rare

Earth Elements (REE) mining claims in the Eldor Rare Earth Property Claims in Quebec, Canada. The Company owns 34

claims covering an area of 3,951 acres adjacent to the Ashram Rare Earth Project. The economic valuation of the Ashram

project is $2.32 billion. Radioactivity readings for the Eldor Project are higher than the reading for the Ashram project.

Trenching, sampling and core drilling for further analysis are slated to begin in summer. The results will help ascertain the

quality of the mineral resource under the Eldor Claims.

The global demand for REE has been majorly fulfilled by the Chinese companies. However, their extraction process and

export restrictions have led to new sources supplying the market. The export restrictions have since been lifted, but the value

of REEs has decreased due to the excess of supply. We expect the demand to pick up based on the varied applications of

REEs. Unlike precious metals, whose applications are finite, REEs have been used in innovative ways in some sectors such

as medical science, technology, and defense.

Management has yet to decide on either of the two viable alternatives to generate returns for investors. It can either partner

with a mining firm to conduct extraction operations to sell the REEs in the market, or it can sell its ownership to a major

mining company. In addition to benefits received by virtue of being an exploration company, SNET will benefit by being a

part of the ‘Plan Nord’ – a regional Quebec government initiative to socially, environmentally and economically develop the

region.

As an economically viable mineral deposit has not yet been discovered, it is difficult to value companies like SNET which

are at a nascent stage of exploration. One method to estimate the instrinsic values of such companies is based on the amount

that can be justified to spend on explorate for a viable depsit. Based on our discussions with management, the total

exploration investment at the Eldor Claim would be a multi-million project ith $2-$3 million of funds required in the short

term and close to $15 million in the medium term. Provided the Company raises these funds, the SNET common stock is

valued at $0.028 per share, 330.4% higher than the current stock price of $0.0064 per share.

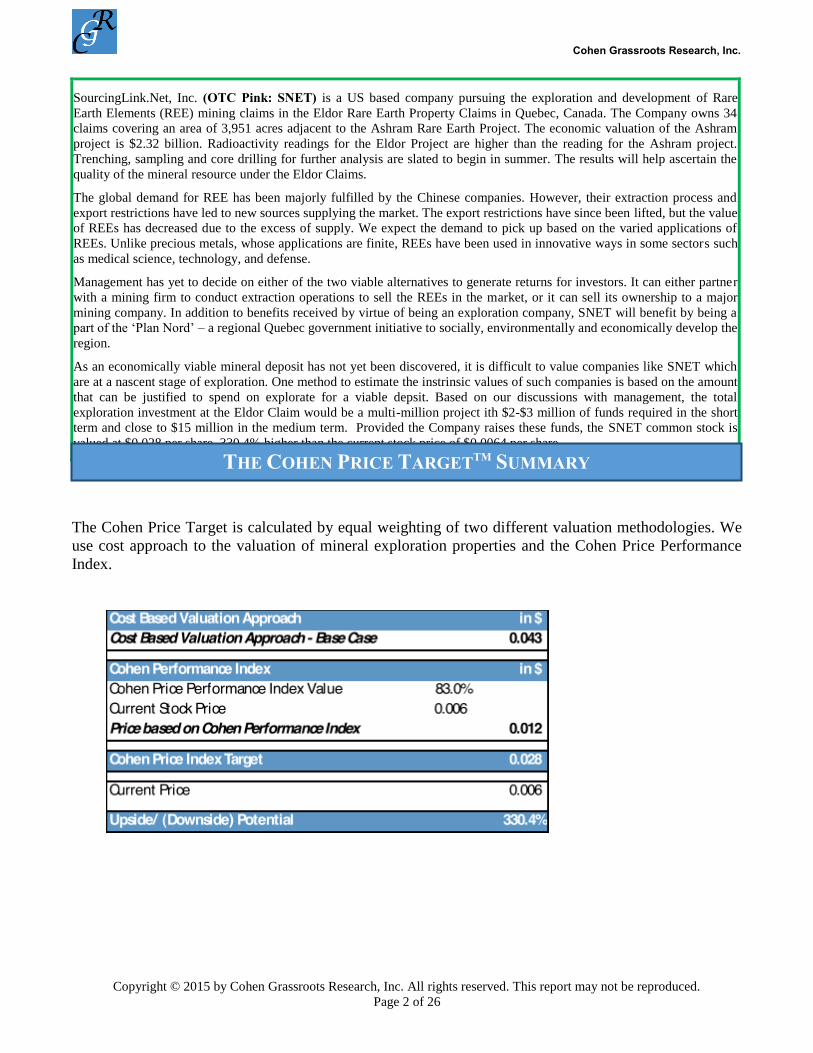

The Cohen Price Target is calculated by equal weighting of two different valuation methodologies. We

use cost approach to the valuation of mineral exploration properties and the Cohen Price Performance

Index.

THE COHEN PRICE TARGETTM

SUMMARY

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 3 of 26

SourcingLink.Net, Inc. (OTC Pink: SNET) is a mining exploration and development company incorporated in

Nevada, US. The Company is the 100% owner of the Eldor Rare Earth Property Claims in northern Quebec, Canada.

The Company’s current focus is the exploration of the rare metals and rare earth metals at the Eldor claims. These

REEs are the primary inputs in a significant number of sectors such as technology, sustainable energy, medical

science, electronics, and defense.

The Eldor claims span 3951 acres and covers 34 claims that are not up for renewal until at least November 2015. The

claims are located in one of the most favorable mining jurisdictions in the world. The Company will also be a

recipient of the benefits from the ‘Plan Nord’ to socially, environmentally and economically develop the region.

Analysis of data from samples collected by the local government has proved productive. The Company employed a

consulting geologist to conduct exploratory research. The results of the claims near the Ashram project were

positive.

The Ashram claims owned by Commerce Resources has received a valuation of $2.32 billion. The Deposit has a

measured and indicated resource of 29.3 million tons at 1.90% TREO and an inferred resource of 219.8 million tons

at 1.88% TREO. The deposits also boast a good balance between light, middle and heavy rare earth elements.

Initial radiation readings for the Eldor claims have been stronger compared to the reading at Ashram deposits. The

Company will be conducting trenching and sampling in the summer of 2015 and will be doing core drilling to get a

clear picture of the mineral resources located underneath the ground.

Management has reviewed the Strategic and Critical Materials 2015 Report on Stockpile Requirements prepared by

the US Under Secretary of Defense for Acquisition, Technology, and Logistics. The report lists the materials for

stockpiling and special attention. Some materials in the list will eventually be produced from Eldor claims giving the

Company a ready, captive market.

Risks: While China is currently the major supplier fulfilling 90% of the demand, their extraction methodology has is

in question. Countries such as Chile are developing eco-friendly ways to extract REE and are likely to provide

competition to the Company. Commerce Resources Corp. is further along in its development plan and is likely to

provide stiff competition to the Company. To continue further exploration and testing and subsequently capture a

share of the REE market, the Company will require access to sufficient capital.

The Rare Earth Elements industry is expected to experience a consistent growth of 13% CAGR for the next three

years. The industry was worth $3.93 billion in 2013 and is expected to reach $8.19 billion in 2018. The US imported

an estimated $210 million worth of REE compared to $256 million in 2013. These numbers are expected to go higher

on the back of strong demand for REE.

Financial Forecasts and Valuation

The Cost Based Valuation Method is based on the premise that the real value of an exploration property is the cost

associated with determining the potential for the existence and discovery of an economic mineral deposit in the

property.

The best way to determine this cost is to identify the past exploration expenditures in adjoining developed properties

or exisitng mining claims, which can be related to the propoerty under considerations. However, in case of SNET, it

is difficult to find the relevant data related to Ashram claims owned by Commerce Resources and hence we have

relied on management estimates and our assumptions.

Assuming the total cost associated with the exploration program to be $15 million for the Cost Based Valuation

Method, and using the Cohen Price Performance Index (average of these methods) SNET common stock is valued

at $0.028 per share, 160.9% higher than the current stock price of $0.0064 per share.

EXECUTIVE SUMMARY

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 4 of 26

SourcingLink.Net (OTC PINK: SNET) is an exploration and development company incorporated in Nevada,

USA. The Company has a strong focus on developing the REE (rare earth elements) and rare metals. SNET

acquired the Eldor claims in Northern Quebec, Canada. The Company is the full owner of 34 mining claims in the

Eldor property.

The Company conducted exploration tests on the claims in Eldor in the fall of 2014. The results from the

exploration expedition are very positive and confirmed the existence of REE. Initial results suggest significant

values have been found for the following REEs - Cerium, Lanthanum, Neodymium, Praseodymium, Samarium,

and Yttrium.

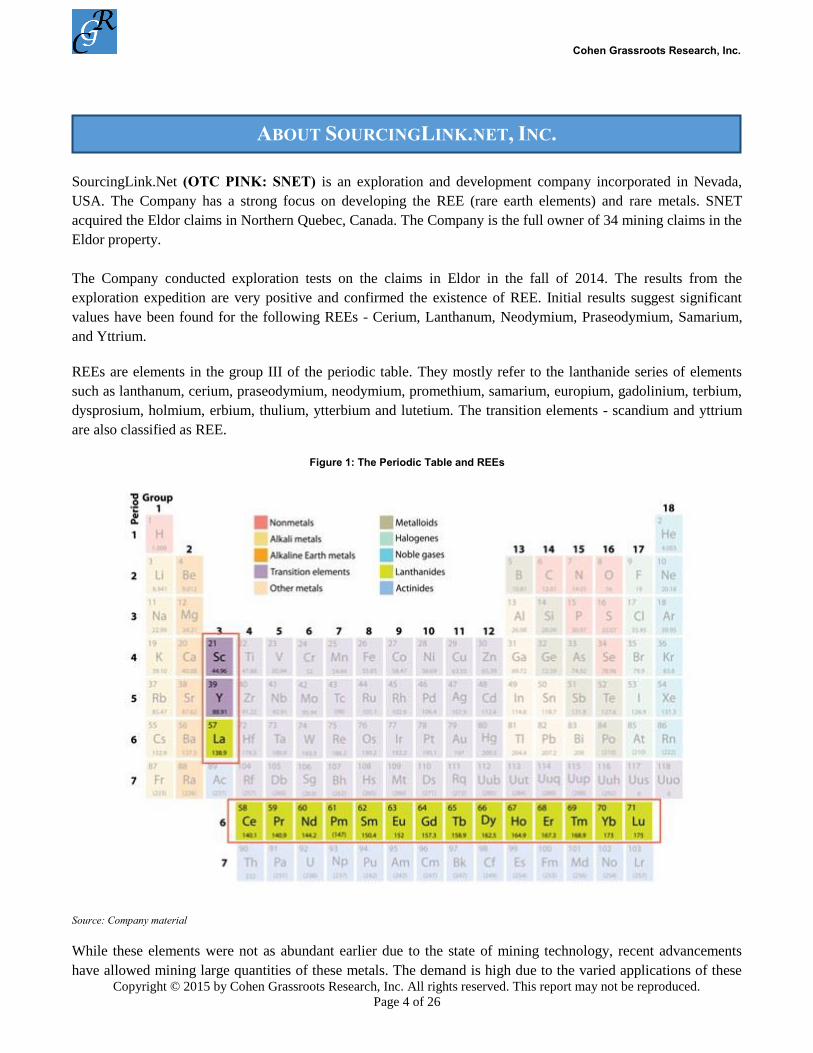

REEs are elements in the group III of the periodic table. They mostly refer to the lanthanide series of elements

such as lanthanum, cerium, praseodymium, neodymium, promethium, samarium, europium, gadolinium, terbium,

dysprosium, holmium, erbium, thulium, ytterbium and lutetium. The transition elements - scandium and yttrium

are also classified as REE.

Figure 1: The Periodic Table and REEs

Source: Company material

While these elements were not as abundant earlier due to the state of mining technology, recent advancements

have allowed mining large quantities of these metals. The demand is high due to the varied applications of these

ABOUT SOURCINGLINK.NET, INC.

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 5 of 26

materials in some industries. Due to the use of these metals, various industries such as electronics, green

technologies, medical technologies, telecommunication and defense, the Japanese rightly call them – ‘the seeds of

technology.' These materials have become virtually irreplaceable due to their unique elemental properties.

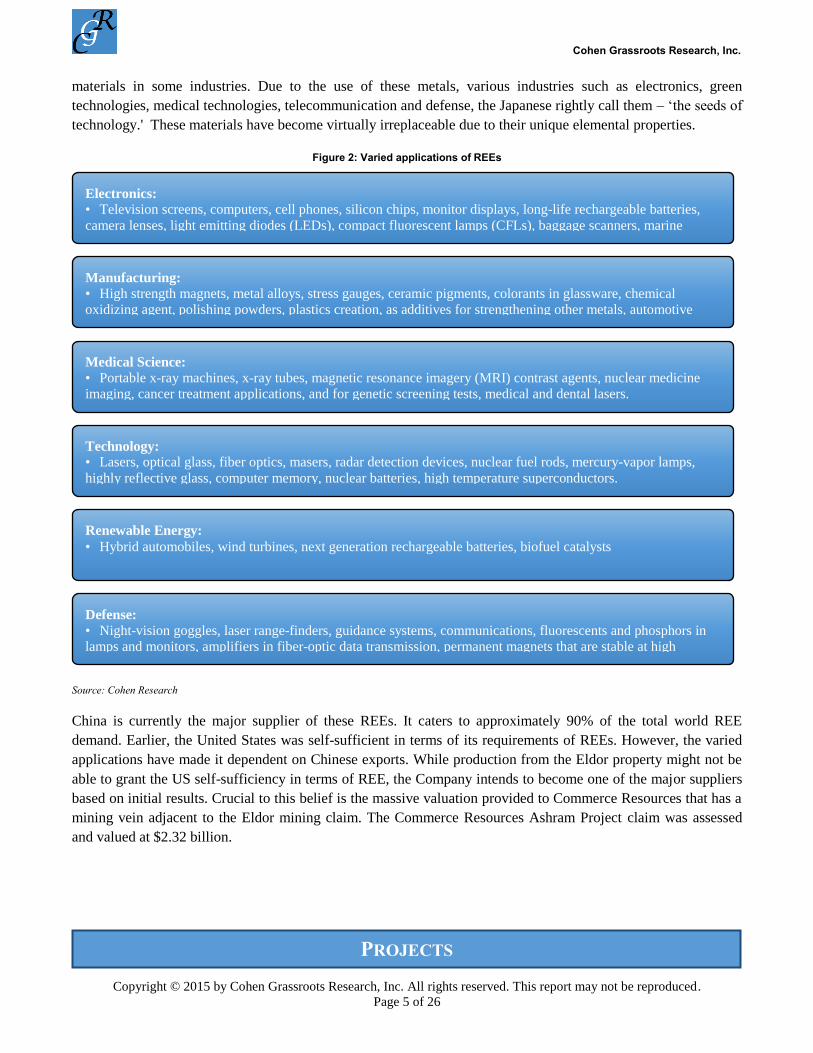

Figure 2: Varied applications of REEs

Source: Cohen Research

China is currently the major supplier of these REEs. It caters to approximately 90% of the total world REE

demand. Earlier, the United States was self-sufficient in terms of its requirements of REEs. However, the varied

applications have made it dependent on Chinese exports. While production from the Eldor property might not be

able to grant the US self-sufficiency in terms of REE, the Company intends to become one of the major suppliers

based on initial results. Crucial to this belief is the massive valuation provided to Commerce Resources that has a

mining vein adjacent to the Eldor mining claim. The Commerce Resources Ashram Project claim was assessed

and valued at $2.32 billion.

PROJECTS

Electronics: • Television screens, computers, cell phones, silicon chips, monitor displays, long-life rechargeable batteries,

camera lenses, light emitting diodes (LEDs), compact fluorescent lamps (CFLs), baggage scanners, marine

propulsion systems.

Manufacturing: • High strength magnets, metal alloys, stress gauges, ceramic pigments, colorants in glassware, chemical

oxidizing agent, polishing powders, plastics creation, as additives for strengthening other metals, automotive

catalytic converters.

Medical Science: • Portable x-ray machines, x-ray tubes, magnetic resonance imagery (MRI) contrast agents, nuclear medicine

imaging, cancer treatment applications, and for genetic screening tests, medical and dental lasers.

Technology: • Lasers, optical glass, fiber optics, masers, radar detection devices, nuclear fuel rods, mercury-vapor lamps,

highly reflective glass, computer memory, nuclear batteries, high temperature superconductors.

Renewable Energy:

• Hybrid automobiles, wind turbines, next generation rechargeable batteries, biofuel catalysts

Defense: • Night-vision goggles, laser range-finders, guidance systems, communications, fluorescents and phosphors in

lamps and monitors, amplifiers in fiber-optic data transmission, permanent magnets that are stable at high

temperatures, precision-guided weapons, "white noise" production in stealth technology

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 6 of 26

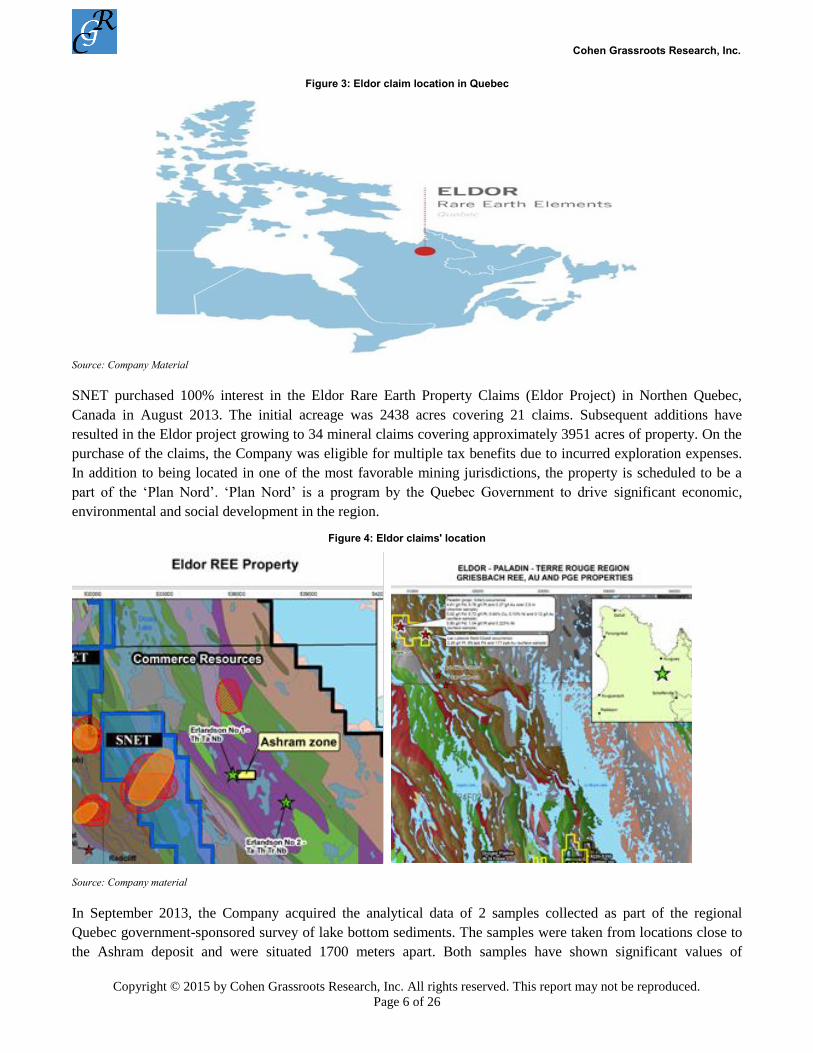

Figure 3: Eldor claim location in Quebec

Source: Company Material

SNET purchased 100% interest in the Eldor Rare Earth Property Claims (Eldor Project) in Northen Quebec,

Canada in August 2013. The initial acreage was 2438 acres covering 21 claims. Subsequent additions have

resulted in the Eldor project growing to 34 mineral claims covering approximately 3951 acres of property. On the

purchase of the claims, the Company was eligible for multiple tax benefits due to incurred exploration expenses.

In addition to being located in one of the most favorable mining jurisdictions, the property is scheduled to be a

part of the ‘Plan Nord’. ‘Plan Nord’ is a program by the Quebec Government to drive significant economic,

environmental and social development in the region.

Figure 4: Eldor claims' location

Source: Company material

In September 2013, the Company acquired the analytical data of 2 samples collected as part of the regional

Quebec government-sponsored survey of lake bottom sediments. The samples were taken from locations close to

the Ashram deposit and were situated 1700 meters apart. Both samples have shown significant values of

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 7 of 26

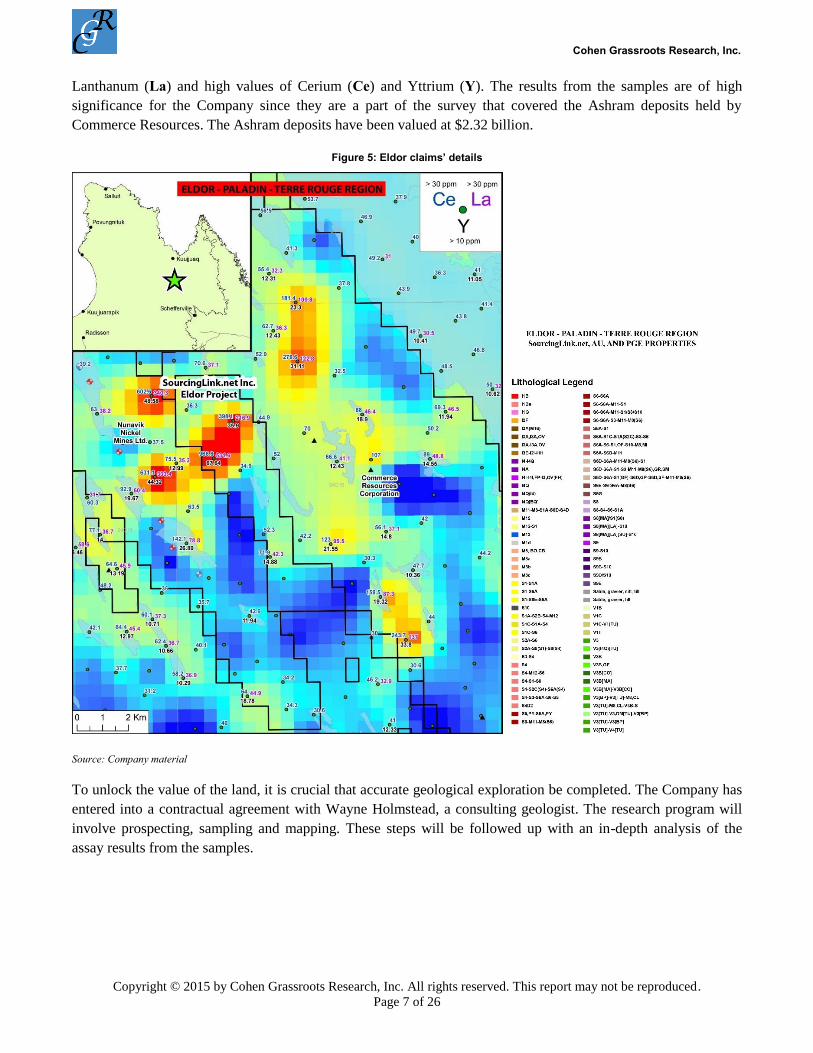

Lanthanum (La) and high values of Cerium (Ce) and Yttrium (Y). The results from the samples are of high

significance for the Company since they are a part of the survey that covered the Ashram deposits held by

Commerce Resources. The Ashram deposits have been valued at $2.32 billion.

Figure 5: Eldor claims’ details

Source: Company material

To unlock the value of the land, it is crucial that accurate geological exploration be completed. The Company has

entered into a contractual agreement with Wayne Holmstead, a consulting geologist. The research program will

involve prospecting, sampling and mapping. These steps will be followed up with an in-depth analysis of the

assay results from the samples.

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 8 of 26

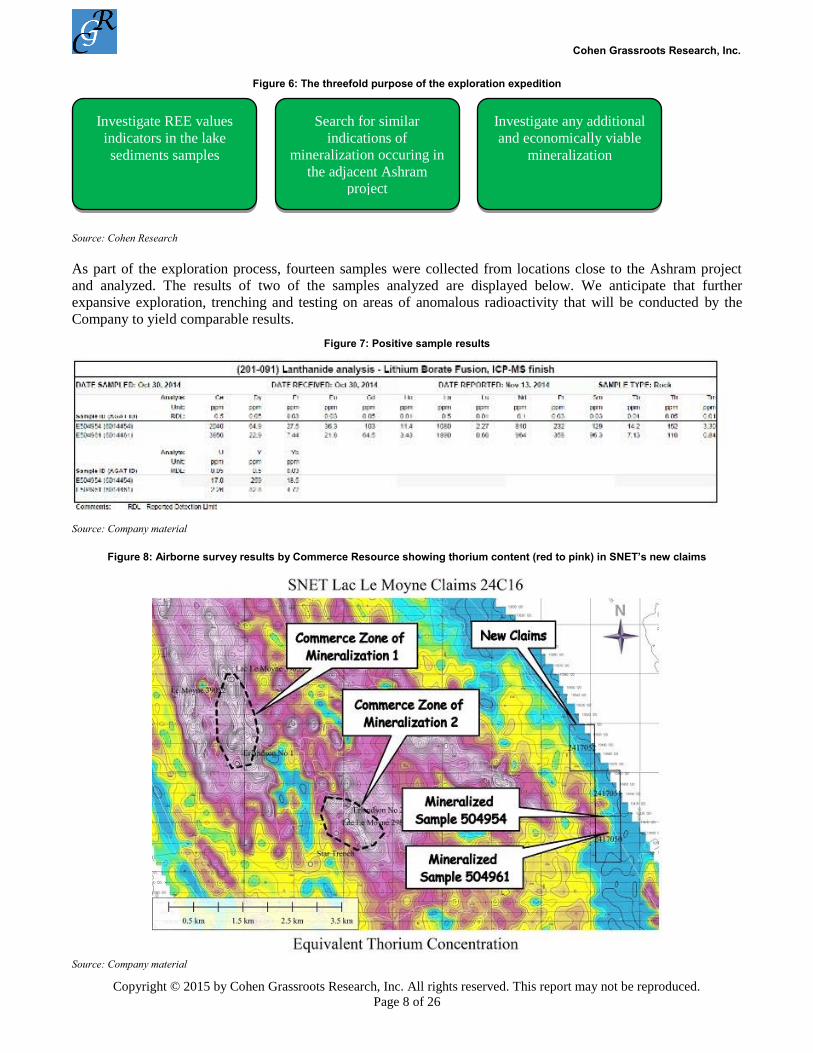

Figure 6: The threefold purpose of the exploration expedition

Source: Cohen Research

As part of the exploration process, fourteen samples were collected from locations close to the Ashram project

and analyzed. The results of two of the samples analyzed are displayed below. We anticipate that further

expansive exploration, trenching and testing on areas of anomalous radioactivity that will be conducted by the

Company to yield comparable results.

Figure 7: Positive sample results

Source: Company material

Figure 8: Airborne survey results by Commerce Resource showing thorium content (red to pink) in SNET’s new claims

Source: Company material

Investigate REE values

indicators in the lake

sediments samples

Search for similar

indications of

mineralization occuring in

the adjacent Ashram

project

Investigate any additional

and economically viable

mineralization

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 9 of 26

Based on the data available, we believe the Eldor claims have explosive potential. Manazement believes its stake

to the 34 claims has no claims up for renewal until November 2015. The claims are renewed with the Province of

Quebec’s Ministry of Natural Resources and Fauna. Five of its claims are valid through June 16, 2017. The

increased validity will allow the Company to plan further exploration shortly.

The results from the Ashram Project testing by Commerce Resource in 2015 and its adjacency to the Eldor claims

are the driving factors for the Company’s interest in the Eldor project. Below are the highlights and visuals

concerning the Ashram Project1:

Highlights

Study results show a strongly positive cash flow from a 4,000 tonne per day open-pit operation at Ashram

with a 25-year mine life, a pre-tax and pre-finance Net Present Value (NPV) at a 10% discount rate of

$2.32 billion, a pre-tax/pre-finance Internal Rate of Return (IRR) of 44% and a pre-tax/pre-finance

payback period of 2.25 years.

SGS's economic evaluation was based on the March 6, 2012 resource estimate which used a base case

geologic cut-off grade of 1.25% TREO and provided 29.3 million tonnes (Mt) of measured and indicated

resource, as well as 219.8 Mt of inferred resource averaging 1.88% TREO.

The rare earth elements at Ashram occur in simple and well-understood mineralogy, being primarily in

the mineral monazite and to a lesser extent in bastnaesite and xenotime. These minerals dominate the

currently known commercial extraction processes for rare earths.

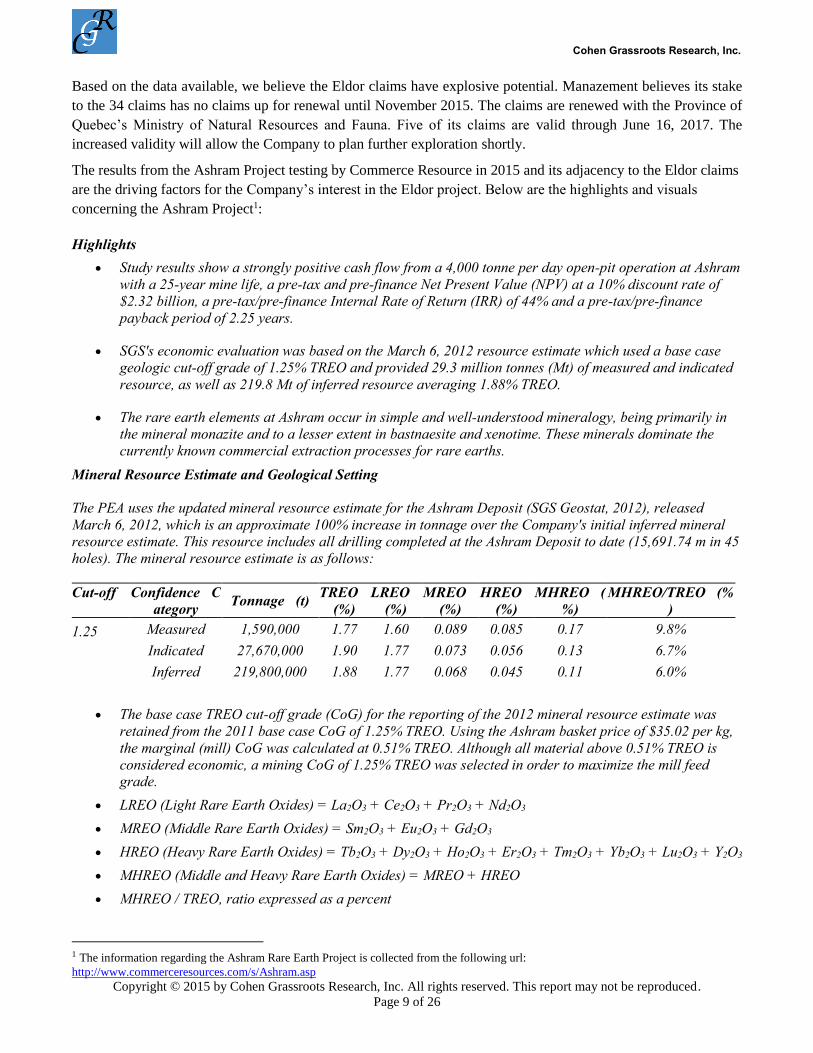

Mineral Resource Estimate and Geological Setting

The PEA uses the updated mineral resource estimate for the Ashram Deposit (SGS Geostat, 2012), released

March 6, 2012, which is an approximate 100% increase in tonnage over the Company's initial inferred mineral

resource estimate. This resource includes all drilling completed at the Ashram Deposit to date (15,691.74 m in 45

holes). The mineral resource estimate is as follows:

Cut-off Confidence C

ategory Tonnage (t)

TREO

(%)

LREO

(%)

MREO

(%)

HREO

(%)

MHREO (

%)

MHREO/TREO (%

)

1.25 Measured 1,590,000 1.77 1.60 0.089 0.085 0.17 9.8%

Indicated 27,670,000 1.90 1.77 0.073 0.056 0.13 6.7%

Inferred 219,800,000 1.88 1.77 0.068 0.045 0.11 6.0%

The base case TREO cut-off grade (CoG) for the reporting of the 2012 mineral resource estimate was

retained from the 2011 base case CoG of 1.25% TREO. Using the Ashram basket price of $35.02 per kg,

the marginal (mill) CoG was calculated at 0.51% TREO. Although all material above 0.51% TREO is

considered economic, a mining CoG of 1.25% TREO was selected in order to maximize the mill feed grade.

LREO (Light Rare Earth Oxides) = La2O3 + Ce2O3 + Pr2O3 + Nd2O3

MREO (Middle Rare Earth Oxides) = Sm2O3 + Eu2O3 + Gd2O3

HREO (Heavy Rare Earth Oxides) = Tb2O3 + Dy2O3 + Ho2O3 + Er2O3 + Tm2O3 + Yb2O3 + Lu2O3 + Y2O3

MHREO (Middle and Heavy Rare Earth Oxides) = MREO + HREO

MHREO / TREO, ratio expressed as a percent

1 The information regarding the Ashram Rare Earth Project is collected from the following url:

http://www.commerceresources.com/s/Ashram.asp

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 10 of 26

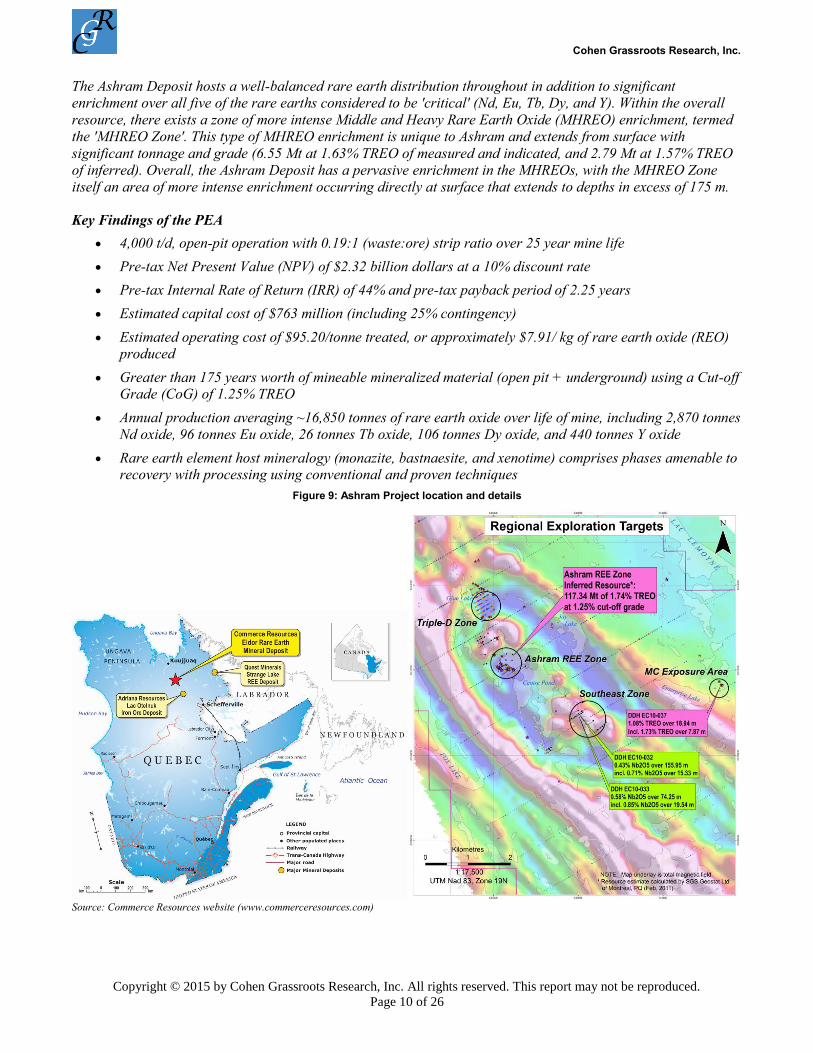

The Ashram Deposit hosts a well-balanced rare earth distribution throughout in addition to significant

enrichment over all five of the rare earths considered to be 'critical' (Nd, Eu, Tb, Dy, and Y). Within the overall

resource, there exists a zone of more intense Middle and Heavy Rare Earth Oxide (MHREO) enrichment, termed

the 'MHREO Zone'. This type of MHREO enrichment is unique to Ashram and extends from surface with

significant tonnage and grade (6.55 Mt at 1.63% TREO of measured and indicated, and 2.79 Mt at 1.57% TREO

of inferred). Overall, the Ashram Deposit has a pervasive enrichment in the MHREOs, with the MHREO Zone

itself an area of more intense enrichment occurring directly at surface that extends to depths in excess of 175 m.

Key Findings of the PEA

4,000 t/d, open-pit operation with 0.19:1 (waste:ore) strip ratio over 25 year mine life

Pre-tax Net Present Value (NPV) of $2.32 billion dollars at a 10% discount rate

Pre-tax Internal Rate of Return (IRR) of 44% and pre-tax payback period of 2.25 years

Estimated capital cost of $763 million (including 25% contingency)

Estimated operating cost of $95.20/tonne treated, or approximately $7.91/ kg of rare earth oxide (REO) produced

Greater than 175 years worth of mineable mineralized material (open pit + underground) using a Cut-off Grade (CoG) of 1.25% TREO

Annual production averaging ~16,850 tonnes of rare earth oxide over life of mine, including 2,870 tonnes

Nd oxide, 96 tonnes Eu oxide, 26 tonnes Tb oxide, 106 tonnes Dy oxide, and 440 tonnes Y oxide

Rare earth element host mineralogy (monazite, bastnaesite, and xenotime) comprises phases amenable to recovery with processing using conventional and proven techniques

Figure 9: Ashram Project location and details

Source: Commerce Resources website (www.commerceresources.com)

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 11 of 26

Figure 13: SNET Value Proposition

Source: Cohen Research

According to Transparency Market Research, the worldwide demand for Rare Earth Elements was worth $3.93

billion in 2013. The expected CAGR growth till 2018 is expected to be 13%, and the market value is expected to

be worth $8.19 billion. REEs are used in most of the today’s technology products. The use of REE will only

continue to grow as more and more applications are discovered. According to the USGS Mineral Commodity

Summaries, US imported am estimated $210 million worth of REE, a clear decrease from the $256 million in

2013. The table for concerning the import and export of Rare Earths is pasted below:

INDUSTRY OVERVIEW

SNET's Value Proposition

High

valuation

expected on

Eldor claims

based on

similar

valuation for

Ashram

Project

Large

number of

uses of REE

and many

potential

applications

still

unexplored

Additional

benefits as

part of 'Plan

Nord' set up

by Quebec

regional

government

Captive

defence

industry

market after

review of the

Strategic and

Critical

Materials

2015 Report

on Stockpile

Requirement

s

VALUE PROPOSITION

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 12 of 26

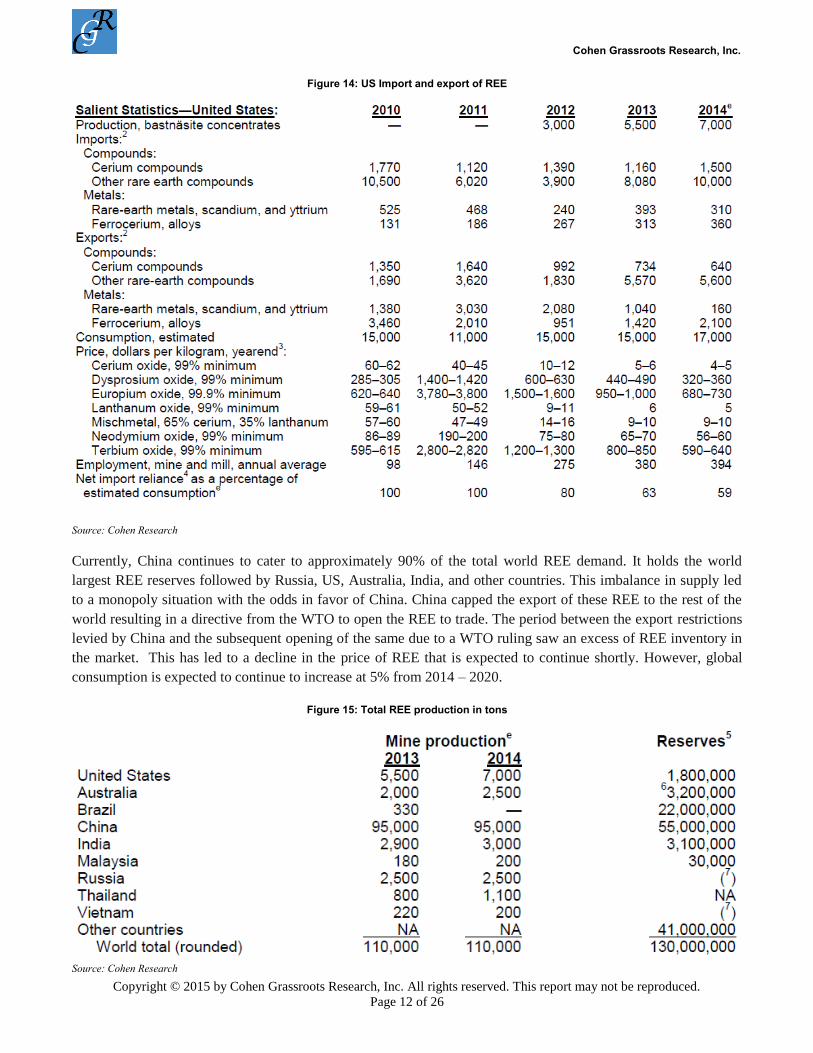

Figure 14: US Import and export of REE

Source: Cohen Research

Currently, China continues to cater to approximately 90% of the total world REE demand. It holds the world

largest REE reserves followed by Russia, US, Australia, India, and other countries. This imbalance in supply led

to a monopoly situation with the odds in favor of China. China capped the export of these REE to the rest of the

world resulting in a directive from the WTO to open the REE to trade. The period between the export restrictions

levied by China and the subsequent opening of the same due to a WTO ruling saw an excess of REE inventory in

the market. This has led to a decline in the price of REE that is expected to continue shortly. However, global

consumption is expected to continue to increase at 5% from 2014 – 2020.

Figure 15: Total REE production in tons

Source: Cohen Research

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 13 of 26

We believe these low prices will allow existing companies to capitalize on the resources. The growing

applications of REE will result in increased demand and subsequently higher prices for the firms that can shortly

enter into production. A Mining.com article tries to quantify the growth REE businesses are expected to see with

REEs being crucial to the manufacturing sector worth $2 trillion to $4.8 billion.

Risks factors:

Substantial capital requirement: SNET requires access to substantial capital to continue its exploration and

infrastructural development activities. Without the expected capital, the Company might not be able to capitalize

on the slowdown in the REE market and miss out on a tremendous opportunity to generate massive returns.

Competition: The Company does not have to compete against anyone for the mining claims in the near future.

The adjacent Ashram Project has similar reading and has been valued at $2.32 billion and will be competing for

the same market share. However, countries such as Chile are looking at eco-friendly alternatives to produce

REEs and might take away the future market share of SNET.

SourceLinking.Net (OTC Pink: SNET) is an exploration stage company focused on the development of the

Eldor Rare Earth Project in Northern Quebec, Canada. The Eldor Project consists of 34 claims over an area of

3951 acres. Initial tests from the samples collected by the regional government and exploration expeditions

conducted by the Company has returned very favorable results for producing economically viable REEs.

The Company’s management realizes that the greatest increase in value for the Company will happen when the

raw land at Eldor is converted into a claim with confirmed mineral resources. They have added a few claims

adjoining to their existing ones and extended their ownership of the claims until November 2015. This period will

allow them to conduct further exploration and verify their results. Once the results of its explorations and

expeditions are confirmed, management will decide on whether to enter into operations or to sell off its whole or

part of ownership to a major mining firm.

The market for REEs is expected to grow. Some new firms will want to enter the market since China is slowly

losing market share. With additional uses for REEs being discovered more and more frequently, SNET is well

poised to benefit from being a new entrant intending to makes its entry into the REE market.

We believe the Company’s strong management, strategic partnerships, robust projected revenue streams and

growth potential of the REE markets makes the stock a potentially valuable investment proposition.

SourceLinking.Net may provide a potential short term and long term investment opportunity for risk-averse

investors.

CONCLUSION

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 14 of 26

RS/Grass Roots Distribution Research

The SNET team understands the complexity involved in generating exceptional returns from the Eldor mining

claims. We believe their experience and expertise will help to drive the Company forward.

Anne M Carioti GG,

CEO and Director

Anne is the Chief Executive Officer of SourcingLink.net and a member of its Board of Directors. Extensive

experience in upper management and company development has spanned over two decades. She is highly

involved with daily operations.

Prior to becoming CEO, Carioti held a senior management position within a successful precious metals and

mineral business. Carioti began her career at Birks-Mayor, Canada as a metal and mineral analyst after earning

her graduate degree from Gemological Institute of America.

Chuck Wagner,

President

Mr. Wagner is the President of SourcingLink.net, with over 15 years of formidable experience in the financial

services industry. Outside of Wagner’s role in the financial services industry, Mr. Wagner has spent the last few

years establishing relationships in the basic materials industry, along with the mining and oil and gas industries.

Mr. Wagner is an instrumental part of the team at SourcingLink.net.

He graduated from the University of Colorado and currently resides in San Francisco, CA.

Mani Pirouzbakht GG,

COO and Director

Mani was appointed as the Chief Operating Officer of SourcingLink.net and a member of the Board of Directors.

Mr. Pirouzbakht’s previous experience includes performing feasibility studies for mineral deposits, conducted

research on exploring specific avenues leading to introduction of new fields in active mines. Mr. Pirouzbakht

assisted in interpreting geochemical data and provided estimation maps of ore deposits by geochemical and

geostatistical approaches, proved geological maps by GIS, prepared technical reports for Aalikav Zagros

Consulting Engineers Co. Pirouzbakht has a Master of Science degree, Mining Engineering (Exploration),

Bachelor of Science, Mining Engineering (Exploration)

Tina Chan,

Director

Tina was appointed as a member of the Board of Directors. Her experience includes project coordinator handling

10-20 projects simultaneously with consistent positive feedback for GM Casting House, Inc, Chicago, IL. Ms.

Chan holds a Bachelors Degree from AI of Chicago.

Wayne Holmstead,

MANAGEMENT BIOS

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 15 of 26

Consulting Geologist

Mr. Wayne Holmstead, Bachelor of Science, University of Toronto, Earth Science is an accomplished geologist

with over 30 years experience, having previously worked with many Canadian (TSX) listed mining exploration

companies including Windy Mountain Exploration and Western Troy Capital Resources. Mr.Holmstead has a

significant amount of experience working with exploration mining projects in northern Quebec.

SourcingLink.net Inc. Comments on Department of Defense 2015 Stockpile Requirements Report

SAN DIEGO, CA--(Marketwired - Jun 8, 2015) - SourcingLink.net Inc. (OTC PINK: SNET) has reviewed the

Strategic and Critical Materials 2015 Report on Stockpile Requirements prepared by the US Under Secretary of

Defense for Acquisition, Technology and Logistics. Within the Report, the Department of Defense recommends

certain materials for stockpiling and special attention. SNET believes that its Eldor property has a number of the

materials that are recommended for Stockpiling.

Chuck Wagner, President of SourcingLink.net commented: "This Report is just further validation of what we at

our Company already believe that it is important for us to continue work on our property and prepare for mining

materials that are commercially viable, necessary and as we also read in the DoD report, strategic for our

country."

The Company is preparing itself for the upcoming mining season and will keep its shareholders posted on

developments and implementation of the business plan.

About The Eldor Project:

SourcingLink.net, Inc. signed an agreement to acquire 100% interest in the Eldor Rare Earth Property Claims

(The Eldor Project) located in Northern Quebec, Canada (one of the most favorable mining jurisdictions in the

world). The Eldor Project consists of 34 mineral claims covering approximately 3951 acres and is located in

Northern Quebec which is considered one of the most favorable mining jurisdictions in the world.

About SourcingLink.net, Inc.:

SourcingLink.net is a U.S. based publicly traded exploration and development company. Their focus in on rare

metals and rare earth elements which are among the primary input materials for the 21st Century technology.

Forward-looking Statements

This release contains "forward-looking statements" within the meaning of the Private Securities Litigation Reform

Act of 1995. Forward-looking statements, which contain words such as "expect," "believe" or "plan," by their

nature address matters that are, to different degrees, uncertain. These uncertainties may cause actual future events

to be materially different than those expressed in our forward-looking statements. We do not undertake to update

our forward-looking statements.

Contact:

LATEST PRESS RELEASE

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 16 of 26

SourcingLink.net

12526 High Bluff Drive, Ste 300

San Diego, CA 92130

Phone 858-792-3620

Website: www.sourcinglink.org

Email: Email Contact

Copyright © 2015 Marketwired. All Rights Reserved

The above news release has been provided by the above company via the OTC Disclosure and News Service.

Issuers of news releases and not OTC Markets Group Inc. are solely responsible for the accuracy of such news

releases.

SNET Discovers Rare Earth Mineralization on the Eldor Property

SAN DIEGO, CA- (Marketwired May 12, 2015) SourcingLink.net, Inc is full of pride to announce that

anomalous / precious earth mineralization has been discovered on newly acquired claims by SNET. This

undiscovered resource in Northern Quebec “Lac Le Moyne” property, is just adjacent to the goliath property of

Commerce Resources (valued @ 2.32 billion). SNET’s property had similar radiation readings then Commerce

Resources.. Within this property we have discovered new claims that were staked to cover a thorium equivalent

radiometric anomaly (see map below).

North American Rare Earth Suppliers — Vital for Future Global Needs

SAN DIEGO, CA–(Marketwired – Feb 27, 2015) – SourcingLink.net, Inc. (PINKSHEETS:SNET) — “We

believe the rare earth metal (REM) industry is poised for a turnaround. Initially, we went into the area because of

the recorded radiation readings by the Canadian Government. Our first exploration resulted in more findings than

we had expected. We are excited for these early results,” said Chuck Wagner, president of SourcingLink.net

SourcingLink.net, Inc. President, Chuck Wagner Exclusive Interview on StockTradersTalk.com

SAN DIEGO, CA–(Marketwired – Feb 5, 2015) – SourcingLink.net, Inc. (OTC PINK: SNET) a Rare Earth

mining and exploration company will be a featured guest in an exclusive interview today at 9am EST.An archived

recorded version can be found on the homepage of Stock Traders Talk at http://www.stocktraderstalk.com/,

following the interview.

SAN DIEGO, CA–(Marketwired – Dec 10, 2014) – SourcingLink.net Inc. (PINKSHEETS: SNET) gives a

more definitive explanation to the shareholders regarding assay results reported in the last news release.

SourcingLink.net CEO, Anne Carioti feels, “We are well positioned with the Eldor Project to benefit from

increased Rare Earth Metal prices. Rare earth elements prices are relatively low when compared with the all time

highs.”

“Rare earth elements are increasingly important to everyday life and progress. We, the management, feel that rare

earth elements have gotten close to the bottom of the market and are poised for a rebound in 2015. Mining rare

earth elements is essential for technology.”

KEY HISTORICAL DEVELOPMENTS

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 17 of 26

SourcingLink.net stakes additional claims for the Eldor Project

SAN DIEGO, CA–(Marketwired – Dec 4, 2014) – SourcingLink.net Inc. (PINKSHEETS: SNET) We are pleased

to provide shareholders with an informational update from a recent geological exploration program conducted in

late October of 2014 at the Eldor Project. The surveying geologist recorded a radiometric survey that detected

anomalous values of rare earth elements and thorium. FOUR NEW CLAIMS WERE STAKED SOUTHEAST OF

THE CURRENT ELDOR CLAIMS and are contiguous to the Commerce Resources claim group. Several

locations were discovered with total radiometric count of 150 to 200 cps. A sub-crop mineralized with sulphides

was also noted.

SourcingLink.net conducts exploration program on the Eldor Project, Quebec, Canada

SAN DIEGO, CA–(Marketwired – Nov 24, 2014) – SourcingLink.net Inc. (PINKSHEETS: SNET) has completed

a reconnaissance exploration program on the Eldor Rare Earth Property Claims ( Eldor Project ) . The geological

exploration program included an initial examination of the property for rare earth mineralization.

The purpose of the exploration project was threefold:

1. To investigate the high Rare Earth and Rare Earth indicator values in lake sediments on the property

which were previously surveyed by the Quebec Government.

2. To look for similar Rare Earth mineralization found by Commerce Resources. Commerce Resources has

a property to the east and contiguous with the Eldor property of SNET. The neighboring property,

Ashram project, currently has a PEA with a NPV at a 10% discount rate of $2.32 billion.

3. To investigate any other mineralization on the property that may be of economic interest.

SourcingLink.net Inc. Is Pleased to Announce The Addition of a New President

SAN DIEGO, CA–(Marketwired –September 30, 2014) – SourcingLink.net Inc. (OTC Markets: SNET) is pleased

to welcome and announce the addition of Mr. Chuck Wagner to the management team as President of the

Company. Ms. Anne Carioti remains as Chairman and Chief Executive Officer.

SourcingLink.net Amendment to Renewal of Claims for Eldor Project in Northern Quebec, Canada

SourcingLink.net (PINKSHEETS: SNET) would like to amend the press release dated August 25, 2014 whereas

the Company actually renewed all of 32 of the existing claims, not 21 as originally announced, pursuant to its

original agreement (announced August 16, 2013). The Eldor Property consists of 32 mineral licenses (claims) that

cover an area totaling 3719 acres. The claims were renewed with the Province of Quebec’s Ministry of Natural

Resources and Fauna. All the mineral licenses are in good standing with the Ministry of Natural Resources and

Fauna with no further renewals required prior to November 2015. The Eldor Property borders the west boundary

of Commerce Resources’ Ashram Project which currently has a Preliminary Economic Assessment (PEA) with a

Net Present Value (NPV) at a 10% discount rate of $2.32 billion. Please see link to map of Eldor Project and

surrounding region (http://www.sourcinglink.org/projects).

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 18 of 26

SourcingLink.net signs contractual agreement with Geologist, Wayne Holmstead, to conduct an

exploration program on the Eldor Project

SAN DIEGO, CA–(Marketwired – Aug 27, 2014) – SourcingLink.net Inc. (PINKSHEETS: SNET) has signed a

contractual agreement with consulting geologist, Wayne Holmstead, to conduct an exploration program on the

Eldor Rare Earth Property Claims ( Eldor Project ) . The geological exploration program includes significant

prospecting, sampling and mapping followed by extensive analysis of rock and sediment samples collected during

the program.

SourcingLink.net Inc. Provides Market Update Including Plans for an Exploration Reconnaissance

Program on Eldor Rare Earth Property Claims

SAN DIEGO, CA–(Marketwired – Aug 20, 2014) – SourcingLink.net Inc. (PINKSHEETS:SNET) is updating

shareholders and the market pertaining to its expected plans to initiate a near term geological exploration and

reconnaissance program on Eldor Rare Earth Property Claims ( Eldor Project ) in attempts to identify specific drill

targets. The expected geological exploration program includes significant prospecting, sampling and mapping

followed by extensive analysis of assay results from samples. The Eldor Project located in Northern Quebec,

Canada adjoins the west boundary of Commerce Resources’ Ashram Project. The neighboring property, Ashram

project, currently has a Preliminary Economic Assessment (PEA) with a Net Present Value (NPV) at a 10%

discount rate of $2.32 billion, (a pre-tax/pre-finance Internal Rate of Return (IRR) of 44%).

SourcingLink.net Inc. REE Properties To Take Advantage of Growing Industry Sector

SAN DIEGO, CA–(Marketwired –August 4, 2014) – SourcingLink.net Inc. (OTC Markets:SNET) Is continuing

its work with its property and looking to expand its work in this growing sector. As the tech industry is in need of

Rare Earth Elements (“REE”) in its manufacturing, Sourcing Link is constantly looking to work in its existing

properties and potentially adding to its portfolio of existing properties. As per the recent published article in

Mining.com article on June 29, 2014 the REEs support a manufacturing sector worth between $2 trillion and $4.8

trillion. Director general of the industry and analyst for the Canadian Department of Natural Resources, Christiane

Villemure, says in its report: “Over the last 10 to 15 years, the world consumption of REEs has increased at 8% to

12% per annum, a trend that experts agree will continue, and may increase.”

The Cohen Price TargetTM2 is derived using a combination of academic and market-based valuation approaches.

The following four equal weighted (25%) components used in calculating our target price, include the assumption

of capital raised:

1. The first 25% equal weighted component: is the market multiple based valuation methodology. This

method uses the industry average Price-to-Earnings ratio to calculate the potential stock price (and/or

price to Book if an asset based Company). We take the average Price-to-Earnings multiple of a given

2 Since SNET is an exploration stage company, we have not used the Cohen Price TargetTM as explained here.

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 19 of 26

industry. This means that, on an average, stocks in this industry should currently trade at a multiple times

their 2011 expected earnings. These earnings are usually only generated by a small Company raising

cash to meet its master budget. The index, therefore, reflects capital invested in any micro/small cap

Company.

2. The second 25% equal weighted component: Cohen Capital Employed based valuation. Most start-up and

micro/small cap companies require significant capital to meet our projections. Our Cohen Price TargetTM

reflects the Company’s ability to raise additional capital. Based on our capital projection and long-term

price target from our Cohen DCFTM valuation model, we derive a Price-to-Capital Employed ratio. We

then multiply this ratio with our capital employed per share assumption to derive this target price.

3. Our third 25% equal weighted component is our use of the Cohen Price Performance IndexTM, which

calculates the average price increase of all the stocks covered by Grass Roots Research and Distribution

Inc. and Cohen Research after their release. Currently, for the period ending July 14, 2013, the Cohen

Price Performance IndexTM is up by 83.0%, meaning that we expect the stock to follow the same trend

and rise by 83.0%. To date, since May 2009, 96.2% of all of our stocks post report release have traded

above the price of our initiate coverage report within 20 days. The Index assumes that all of its

companies had capital employed in each Company.

4. Our fourth 25% equal weighted component is our Cohen Discounted Cash Flow (DCF) method of

valuation. Our Cohen DCFTM valuation includes a complex trademarked formula proprietary to our firm,

which includes an assumed long-term sustainable growth rate, cost of capital and assumed capital

invested in a given Company. Our DCF price target values a Company today, based on projections of

how much future cash will be generated from a given Company. We assume that a Company is worth all

of the cash it can make available to investors in the future. It is called 'discounted' cash flow because cash

in the future is worth less than cash today, and therefore must be discounted to today. We forecast

various line items including assuming a given amount of capital is raised, to calculate the free cash flow

we project a Company to generate during our 5 year forecasted time period. If a Company does not raise

our estimated cash requirements, it is highly unlikely to reach our forecasts and can go out of business.

After using a formula to discount free cash flow, we divide the total forecasted equity of the Company by

the shares of stock outstanding to calculate our Cohen DCFTM valuation, or theoretical price per share

target. We believe the Cohen DCFTM formula is a more accurate measurement of operating cash than the

traditional DCF used by most Wall Street research analysts. A DCF, or 5 year forecasted free cash flow

projection, cannot be calculated without forecasting the three statements (IS,BS,CF) for 5 years. We are

the only firm in the investor awareness industry that forecasts all of our companies for 5 years in three

assumed cases. We believe this in depth level of securities analysis is a must for all of our companies,

and is a foundation of the Cohen Research MethodTM.

Capital raising and cash are the life blood of any micro-cap/small Company. Our Cohen Price TargetTM includes

4 components, 25% equal weighted, that together reflect capital is raised in our client companies. Our

components are trademarked and proprietary to our firm, as is the Cohen Performance IndexTM.

Most micro/small cap companies have difficulty raising sufficient funds to reach our theoretical forecasts; hence

there is considerable risk for any investor. While we do not give investment advice, any Company that cannot

raise adequate capital to finance its business model is a highly risky investment, short term or long

THE COHEN PRICE TARGETTM

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 20 of 26

term. Investment awareness campaigns also affect our price targets. Do not rely on our price targets because they

are based on academic theory. Do your own research or consult with your investment professional.

Price Targets Price targets can be heavily influenced by investor awareness campaigns. In general, we observe the more money

spent on such campaigns, the greater the probability for short term price increases post report release. Our price

targets assume capital raising and forecast 5 year Income Statement, Balance Sheet and Cash Flow statements. In

a perfect world, these assumptions may be realized. We do not give investment advice. However, in the

practical/real world, it is very difficult for a small Company to reach our theoretical 5 year projections. We are

not aware of any research firm that forecasts the three statements (IS, BS, CF) in 3 cases for 5 years. We believe

our price targets are unique to the body of knowledge in the field of securities analysis.

Note: How we calculate our Price Targets We further explain our Cohen DCF, which is an important 25% component of The Cohen Price Target. The

Cohen Discounted Cash Flow Analysis (DCF) creates a price target and values a Company today, based on

projections of how much future cash will be generated from a Company. Our DCF analysis assumes that a

Company is worth all of the cash that it can make available to investors in the future. It is called "discounted" cash

flow because cash in the future is worth less than cash today, and therefore must be discounted to today. We

forecast various line items including assuming capital is raised, to calculate the free cash flow we expect a

Company to generate during our 5 year forecasted time period. After using a formula to discount free cash flow,

we divide the total forecasted equity of the Company by the shares of stock outstanding to calculate our Cohen

DCF (Discounted Cash Flow) valuation, or theoretical price per share target. We believe our Cohen DCF is a

more accurate method of calculating operating cash. We forecast three assumed price targets because companies

change during 5 years, Base Case, Optimistic Case, and Pessimistic Case.

Note: What is our formula used to calculate our DCF, the Cohen Price Target? Some line items include free cash flow to the firm, the weighted average cost of capital, assumption of capital

raised and capital spent, and the total enterprise value of the business less its debt, total equity value, total shares

outstanding, and our projected price per share. A DCF cannot be academically calculated without projecting the 5

year cash flow statement.

Risks of the Cohen Price Target Our Price Targets assume capital will be raised in our four components, or 100% of the Cohen Price Target. The

majority of micro-cap/small cap companies need capital to reach our 5 year sales and cash flow projections. In

the academic world, The Gordon Growth Model justifies an analyst's decision to forecast for 5 years. We

forecast the three statements for 5 years in 3 cases. However, in the practical/real world, buying a micro-cap

stock based on 5 year forecasting is highly risky.

If smaller companies are able to raise capital, our theoretical price targets in a perfect world might be justified,

providing the Company executes on its business model. If an investor believes that a given Company cannot raise

the necessary capital to reach our projections, then any investment becomes highly risky.

The investor should consider all of the possibilities of any given Company being able to raise capital and execute

over 5 years. Few micro to small cap companies are able to raise enough capital and execute over an extended

period of time, primarily due to competition, management competence, access to capital and continued execution

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 21 of 26

of their master plan, agenda and budget. Our price targets are academic theory and should not be relied upon.

Investors should do their own research and consult with their financial consultants.

Disclaimer

Cohen Grassroots Research, Inc.

Short Disclaimer

Cohen Grassroots Research, Inc. (CGR) is an Investor Relations firm hired by companies and third parties to provide Investor Awareness services. This

disclaimer is to be read and understood before using Information. When the words 'research' and 'report' are used in our reports, websites, disclaimers,

distributed Information, documents, programs and commercial products, they mean commercial advertisement. CGR distributes Information purchased and

compiled from outside sources and analysts. This report/release/advertisement is hereinafter defined as an investor relations report and is for general

Information purposes only. Do not base any investment decision or rely on Information in this investor relations report including financial projections, price

targets which are academic theory, buy/sell and trading observations and forecasted business prospects. Never invest in any stock featured, distributed,

posted, written and/or edited by CGR or a third party on web sites, emails, newsletters, or other media unless you can afford to lose your entire investment.

All Information should be validated by the issuing company. This publication is not provided to any particular individual with a view toward their

investment circumstances. CGR does not give investment advice and is not a registered Investment Advisor or a member of any association for other

research providers. Under no circumstances is this investor relations report to be used or considered as an offer to sell or a solicitation of any offer to buy

any security or other debt instruments, or any options, futures or other derivatives related to such securities herein. By accessing, viewing or using our

website, analytical documents or communications, you agree that you alone bear complete responsibility for your own investment research, due diligence

and investment decisions. The majority of these profiled companies are highly risky OTC Bulletin Board or Pink Sheet companies. CGR’s history and past

results are the combination of Cohen Independent Research Group, Inc., and Grass Roots Research and Distribution, Inc.

Release of Liability

CGR assumes no liability for any short term or long term investment decision by any investor of our profiled stocks or any third party’s use of CGR

materials. The reader of the Information hereby indemnifies CGR from any liability for any claimed direct, indirect, incidental, punitive, or consequential

damages pertaining to the disseminated Information. The reader acknowledges that CGR will not be liable to any person or entity for the quality, accuracy,

completeness, reliability, background information on personnel, or timeliness of Information in this investor relations report, or for any direct, indirect,

consequential, incidental, special or punitive damages that may arise out of the use of Information, products or services from any person or entity including

but not limited to lost profits, loss of opportunities, trading losses, and damages that may result from any incompleteness or inaccuracy in any of CGR’s

profiled companies of the disseminated Information. CGR does not undertake any responsibility or liability whatsoever for any forward looking statements

or any legal obligation whatsoever for updating the Information.

Quality and Limitations of Information

CGR analysts rely on Information considered to be reliable. This Information may come from issuing companies, SEC and other regulatory filings, and

other sources available to the analyst. CGR and its analysts are limited in validating, quantifying and researching such distributed information. This

Information may or may not be used by CGR analysts for writing their analytical documents. The Information used and statements of fact made are not

guarantees, warranties or representations as to their completeness or accuracy. Investor relations report opinions are the personal views of the outside

contracted analyst. (a) This Information may or may not be accurate or truthful. CGR and its analysts have no access to this Information beyond available

public information. (b) CGR does not independently verify or assert the truthfulness, completeness, accuracy or reliability of the Information and is not

responsible for errors and omissions. (c) Because the Information is presented on an “as is” basis, your use of the Information is at your own risk. (d) CGR

disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the

Information is accurate or reliable or free of errors. (e) Statements contained in the Information that are not historical facts are forward looking statements

that involve risks and uncertainties as indicated by words such as ‘believes’, ‘expects’, ‘estimates’, ‘may’, ‘will’, ‘should’ or ‘anticipates’ or similar

expressions. These forward looking statements may materially differ from the Issuer’s presentation of Information to CGR analysts, and actual operational

and financial results or its actual achievements, claimed or otherwise. (f) Reading our analytical documents alone (including other reasons cited herein)

should never be used as the sole basis for making an investment decision. We urge you to use the Information (if you find such Information to be useful)

only as a starting point for your further investigation and research. Consult with your investment or financial adviser, attorney or other counselor as to the

advisability of taking any actions including buying or the selling of securities. Do your own research.

Corporate and Promotional Firm’s Activities

CGR disclaims and is not a part of any ‘third party’ (defined as a corporation, shareholder, outside entity, Investor Relations, Public Relations, Promotional

Firm or Investor Awareness firm) or associated with their methods of operation, distribution, programs and use of CGR’s materials. (a) CGR may act as an

independent non-affiliated subcontracting vendor of Information materials to certain third party corporations, shareholders, investor awareness, IR and PR

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 22 of 26

firms. (b) All subcontracted CGR vended materials become assets of a paying third party client to use at their choice, and do not represent in any way

CGR’s endorsement or participation in any third party’s corporation, shareholder, IR, PR or investment awareness programs. (c) CGR is not a part of or

connected to any and all potentially illegal corporate, third party, shareholder, promotional firms, IR, PR firms, outside communications of all types,

including outside trading activities. (d) CGR has no knowledge or inside Information or participation in any illegal activities, including illegal trading, of any

of its profiled companies or third party clients. (e) CGR and its outside sources have no firsthand knowledge of any profiled company or third party,

corporation, shareholder, IR, PR and investment awareness firm’s capabilities, intent, resources, financing, operations, politics, inner workings, plans,

management competence and decisions, internal corporate and third party goals, ethical standards, or their ability to reach their corporate or third party goal.

CGR reserves the right to co-market its separate services with other third party firms.

General Information

CGR advises recipients of all such data to be validated from the issuing company including all statistical Information derived from SEC filings, from data

sources, the opinion of the analyst, or financial Information and data from the issuing company contained herein. The reader should seek professional

financial advice, verify all claims and do his/her own research and due diligence before investing in any securities mentioned. When paid in stock, Readers

are advised to review SEC periodic reports, Section 27A of the Securities Act of 1993 and Section 21E of the Securities Exchange Act of 1934 includes

statements and caution regarding expected continual growth of a profiled company and the value of its securities, Forms 10-Q, 10K, Form 8-K, insider

reports, Forms 3, 4, 5 Schedule 13D, www.sec.gov.nasd.com, www.pinksheets.com, www.sec.gov and www.finra.com. CGR is compliant with the Can

Spam Act of 2003. Investing in micro-cap and small cap securities is speculative and carries a high degree of risk. Investors can lose their entire

investment. Future prospects may not be realized. Do your own research.

The Private Securities Litigation Reform Act of 1995

The Private Securities Litigation Reform Act of 1995 provides investors a 'safe harbor' in regard to forward-looking statements. CGR cautions all investors

that such forward-looking statements in this investor relations report are not guarantees of future performance. Investors should understand that statements

regarding future prospects may not be realized. This investor relations report does not have regard to the specific investment objective, financial situation,

suitability, and the particular need of any specific person who may receive this investor relations report. Investors should note that income from such

securities, if any, may fluctuate and that each security's price or value may rise or fall substantially. Accordingly, investors may receive back less than

originally invested, or lose their entire investment. Past performance is not indicative of future performance. Please click to: www.grassrootsrd.com to read

the full text of this disclaimer.

Compensation and Trading

Because we receive compensation for CGR’s dissemination of the Information, our publicly disseminated publications should not be regarded in any manner

whatsoever as independent. CGR certifies that no part of the analysts’ compensation was, is, or will be, directly or indirectly, related to the specific

observation or views expressed by the analyst in the report. CGR services and analytical documents rendered are not related to, connected to, nor are they

contingent on a client’s stock price performance. CGR is sometimes paid for analytical documents and distribution in cash, stock, Rule 144 stock, warrants,

options or other securities in lieu of or in addition to CGR's stated compensation schedule. This compensation and ownership of securities of a client’s

common stock constitutes a conflict of interest as to our ability to remain objective in our communication regarding our profiled companies. More

information can be received from our client company’s website. The majority of our assignments are for 30 days. We may write analytical documents or

promote a given company on other occasions. DGR Advisors, LLC paid $7,500 for this commercial advertisement program. This document shall not be

copied and is copyrighted by Cohen Grassroots Research Inc. and D. Paul Cohen

Full Disclaimer:

Cohen Grassroots Research, Inc.

Cohen Grassroots Research, Inc. (CGR) is an Investor Relations firm hired by certain companies and third parties to provide Investor Awareness services to

micro-cap, small cap companies and other private and public companies. When the words ‘research’ and ‘report’ are used in our reports, websites,

distributed Information, and all commercial products, they mean commercial advertisement. Readers of our Information are hereinafter referred to as

‘Reader’ or ‘Readers’. This disclaimer is to be read and understood before using Information. By using or viewing any Information, you agree that you

have read this disclaimer in full, understand it and proceed to use or view Information in agreement that you alone bear complete responsibility for your own

investment research, investment decisions and due diligence. CGR’s history and past results are the combination of Cohen Independent Research Group,

Inc., and Grass Roots Research and Distribution, Inc.

General Information

Do not base any investment decision on Information in this report/release/advertisement, hereinafter referred to as an investor relations report; including

financial projections, price targets, buy/sell and trading observations and forecasted business prospects. This publication is not provided to any particular

individual with a view toward their investment circumstances. CGR is hereinafter collectively referred to as CGR, “we” or “us” or “our”. The words “third

party” are collectively defined as private and public corporations, IR, PR, investor awareness firms, third party shareholders and other outside entities not

affiliated with CGR. Investor Awareness programs are designed to help companies communicate their investment characteristics. CGR does not give

investment advice and is not a registered Investment Advisor or a member of any association for other research providers. CGR distributes analytical

documents and other Information and are for general Information purposes only.

Distribution Sources

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 23 of 26

Never invest in any stock featured, distributed, posted, written and/or edited by CGR or a third party, on CGR or third party Web Sites, Emails / Newsletters,

Social Media posts or Social Media profiles or Social Media networks including Facebook Status / Posts / Updates, Twitter Tweets / Posts / Updates or any

other Social Media based source, Blog Postings, YouTube or other Video Content, Corporate Profiles, Research Reports, Analyst Reports, PowerPoint

Presentations, Corporate Videos, CEO Video Interviews, Press Releases, Banners, Google / Yahoo/ Bing or other Search Engine Advertising or Listings,

Images, and/or Web-Based Discussion Board Postings or any other Information, Electronic Content and Written Content (Collectively referred hereafter as

“Information”), unless you can afford to lose your entire investment. CGR electronically disseminates the Information on its Websites, in newsletters,

featured reports and spam compliant email communications pertaining to Profiled Companies’ (the “Issuer” or “Issuers” or “Profiled Company” or “Profiled

Companies”), the securities of which are most frequently common stock shares quoted on the Over the Counter Bulletin Board (“OTCBB”) or Pink Sheets

(the “Securities”).

Information, Electronic or Written

All Information herein is not intended to be used for investment advice. Under no circumstances is this investor relations report to be used or considered as

an offer to sell or a solicitation of any offer to buy any security or other debt instruments, or any options, futures or other derivatives related to such

securities herein. CGR electronically disseminates the Information on its websites, analytical documents, in newsletters and email communications

pertaining to issuers of securities (the "Issuer" or "Issuers" or "Profiled Company" or "Profiled Companies"). A Profiled Company's securities are most

frequently quoted on the Over the Counter Bulletin Board ("OTCBB") or the Pink Sheets. Certain Pink Sheet stocks may or may not have audited financial

statements. CGR and its data vendors do not warranty that such SEC filing data, or any third party information or distribution of CGR Information and other

compiled data is accurate. CGR advises recipients of all such data to be validated by the issuing company including all statistical Information derived from

SEC filings, from data sources or financial Information and data from the issuing company contained herein. The Information is forecasted in analytical

documents and is primarily based on publicly available Information, such as quarterly (sometimes with un-audited financial statements) and annual reports

(with audited financial statements) filed with the Securities and Exchange Commission ("SEC"), quarterly and annual audited and/or un-audited financial

reports and Information and Disclosure Statements filed with Pink Sheets, the Issuer's website and Information obtained through contracted analysts, search

engines such as Yahoo Finance, Market Watch and Business Wire. CGR does not endorse, independently verify or assert the truthfulness, validity,

accuracy, completeness, or reliability of the Information disseminated by an issuing company used in any CGR investor relations report.

Release of Liability

CGR assumes no liability for any short term or long term investment decision by any investor of our profiled stocks or any third party’s use of CGR

materials. The reader of the Information hereby indemnifies CGR from any liability for any claimed direct, indirect, incidental, punitive, or consequential

damages pertaining to the disseminated Information. The reader acknowledges that CGR will not be liable to any person or entity for the quality, accuracy,

completeness, reliability, background information on personnel, or timeliness of Information in this investor relations report, or for any direct, indirect,

consequential, incidental, special or punitive damages that may arise out of the use of Information, products or services from any person or entity including

but not limited to lost profits, loss of opportunities, trading losses, and damages that may result from any incompleteness or inaccuracy in any of CGR’s

profiled companies of the disseminated Information. CGR does not undertake any responsibility or liability whatsoever for any forward looking statements

or any legal obligation whatsoever for updating the Information.

Quality and Limitation of Information

CGR analysts rely on Information considered to be reliable. This Information may come from issuing companies, SEC and other regulatory filings, and

other sources available to the analyst. CGR and its analysts are limited in validating, quantifying and researching such distributed information. This

Information may or may not be used by CGR analysts for writing their analytical documents. The Information used and statements of fact made are not

guarantees, warranties or representations as to their completeness or accuracy. Investor relations report opinions are the personal views of the outside

contracted analyst. (a) This Information may or may not be accurate or truthful. CGR and its analysts have no access to this Information beyond available

public information. (b) CGR does not independently verify or assert the truthfulness, completeness, accuracy or reliability of the Information and is not

responsible for errors and omissions. (c) Because the Information is presented on an “as is” basis, your use of the Information is at your own risk. (d) CGR

disclaims, expressly and impliedly, all warranties of any kind, including those of merchantability and fitness for a particular purpose or whether the

Information is accurate or reliable or free of errors. (e) Statements contained in the Information that are not historical facts are forward looking statements

that involve risks and uncertainties as indicated by words such as ‘believes’, ‘expects’, ‘estimates’, ‘may’, ‘will’, ‘should’ or ‘anticipates’ or similar

expressions. These forward looking statements may materially differ from the Issuer’s presentation of Information to CGR analysts, and actual operational

and financial results or its actual achievements, claimed or otherwise. (f) Reading our analytical documents alone (including other reasons cited herein)

should never be used as the sole basis for making an investment decision. We urge you to use the Information (if you find such Information to be useful)

only as a starting point for your further investigation and research. Consult with your investment or financial adviser, attorney or other counselor as to the

advisability of taking any actions including buying or the selling of securities. Do your own research.

Corporate, Third Party and Promotional Firm’s Activities

CGR disclaims and is not a part of any corporation or third party IR, PR or investor awareness firm’s methods of operation, distribution, programs, inner

workings and use of CGR’s materials. (a) CGR may act as an independent non-affiliated subcontracting vendor of materials to certain third parties. (b) All

CGR subcontracted vended materials become assets of a paying third party client to use at their choice, and do not represent in any way CGR’s endorsement

or participation in any third party’s programs. CGR is not a part of, or responsible for any content, associated links, resources, or services associated with

any third party website or means of communication. (c) CGR is not a part of or connected to any and all potentially illegal corporate, third party outside

communications of all types, including outside trading activities. (d) CGR has no knowledge or inside Information or participation in any illegal activities,

including illegal trading, of any of its profiled companies or third party clients. (e) Such activities might include: causes of potential bankruptcy, fraud,

fraudulent and false dissemination of Information and other dissemination of Information, insider trading, corporate and third party non-disclosure, illegal

trading, trading manipulation, other legal issues and regulatory violations. (f) Certain content in our releases or website may be written, edited and published

by our clients or third parties. Our releases and website may contain the symbols of companies and/or news feeds about companies that are not being profiled

by us but refer to certain activity in the micro-cap or penny stock market that we have profiled or are currently highlighting. Readers are advised that all

reports and news feeds are issued solely for informational purposes. (g) Our profiled companies on our website may not have approved certain or any

Cohen Grassroots Research, Inc.

Copyright © 2015 by Cohen Grassroots Research, Inc. All rights reserved. This report may not be reproduced.

Page 24 of 26

statements within the website or reports. (h) This release may provide hyperlinks to third party websites or access to third party content for which we are not

responsible. (i) By accessing, viewing, or using our website, release or communications originating from this investor relations report, you agree that you

alone are entirely responsible for your investment decision(s). (j) CGR and its outside sources have no firsthand knowledge of any profiled company or third

party’s capabilities, intent, resources, financing, operations, politics, inner workings, plans, management competence and decisions, internal corporate and

third party goals, legal compliance, historical activities, ethical standards, or their ability to reach their corporate or third party goals. CGR reserves the right

to co-market its separate services with other third party firms.

Reader’s Due Diligence and Regulatory Sources

The Information should only be used, at most, and if at all, as a starting point for Readers to conduct a thorough investigation of the Profiled Company and

its securities, to consult with their financial, legal or other advisor(s) and avail themselves of filings and Information that may be accessed at www.sec.gov .

or www.picksheets.com or other electronic medium, including: (a) Reviewing SEC periodic reports (Forms 10-Q and 10-K), reports of material events

(Form 8-K), insider reports (Forms 3, 4, 5 and Schedule 13D); (b) Reviewing Information and Disclosure Statements and unaudited financial reports filed

with the Pink Sheets; (c) Obtaining and reviewing publicly available Information contained in commonly known search engines such as Google; and (e)

Investment guides at www.sec.gov and www.finra.com pertaining to the risks of investing in penny stocks. The SEC has published an investor-focused

website to help your due diligence and protect you against fraud at www.investor.gov. FINRA has published information on its website outlining how to

invest carefully at www.Finra.org/investors/index.htm.

Readers Risks

You agree that you alone, Readers of our documents and users of our website must evaluate and bear all the risks associated with the Information, including

reliance on its accuracy, completeness or usefulness. In all instances, the Reader should conduct further inquiry into the Profiled Company and its securities.

The Profiled Companies are subject to possible risks, including but not limited to: (a) The Information pertains to penny stocks that are subject to the SEC’s

penny stock rules and commonly involve a high degree of risk that may result in the loss of some or all of an investment in the Profiled Company’s

securities; (b) The Issuer’s penny stock may be thinly traded, which may lead to difficulties of selling its securities; (c) The SEC reporting issuer may be

delinquent (not current) in its periodic reporting obligations (i.e., in its quarterly and annual reports) or the Pink Sheet quoted company may be delinquent in

its Pink Sheet reporting obligations as indicated by Pink Sheets New Service’s posting a negative “sign” pertaining to the Issuer at www.pinksheets.com , as

follows: (i) “Limited Information” for companies with financial reporting problems, economic distress, or that are unwilling to file required reports with the

Pink Sheets; (ii) “Pink Sheets – No Information”, which indicates companies that are unable or unwilling to provide disclosure to the public markets, to the

SEC or the Pink Sheets; and (iii) “Caveat Emptor”, signifying “Buyer Beware” that there is a public interest concern associated with a company’s illegal

spam campaign, questionable stock promotion, known investigation of a company’s fraudulent or alleged fraudulent activities or its insiders, regulatory

suspensions or disruptive corporate actions;

Risks of Small Companies

(d) If the Issuer is a development stage company with little or no operations, the securities should be considered extremely speculative for investment

purposes; (e) Many companies that have their securities quoted on the OTCBB or Pink Sheets (as well as Exchange listed companies) have been negatively

affected by the economic downturn, the general economy and the lack of adequate financing to meet their operational goals or expansion plans; (f) Many of

the energy related and other Profiled Companies are subject to increasing environmental and other governmental regulations, which subjects them to

significant costs and possible fines and liabilities for failure to comply with applicable state and federal statutes; (g) The future success of many OTCBB and

Pink Sheet quoted Issuers is dependent upon receiving adequate financing or raising sufficient capital, which they may be unable to obtain;

Conflict of Interests Risks