community potential for shared solar development in india

TRANSCRIPT

The Pennsylvania State University

The Graduate School

Department of Energy & Mineral Engineering

COMMUNITY POTENTIAL FOR SHARED SOLAR DEVELOPMENT IN INDIA

A Thesis in

Energy & Mineral Engineering

by

Balaji Raman

Submitted in Partial Fulfillment

of the Requirements

for the Degree of

Master of Science

May 2016

ii

The thesis of Balaji Raman was reviewed and approved* by the following:

Jeffrey R. S. Brownson

Associate Professor of Energy & Mineral Engineering

Solar Option Lead: iMPS Renewable Energy & Sustainability Systems

Thesis Advisor

Andrew N. Kleit

Professor of Energy & Environmental Economics

Chiara Lo Prete

Assistant Professor of Energy Economics

Luis F. Ayala H.

Professor of Petroleum & Natural Gas Engineering

Associate Department Head for Graduate Education

*Signatures are on file in the Graduate School

iii

ABSTRACT

Community shared solar can offer feasible solutions for both rural electrification problems and

integrated development in emerging economies like India. In order to study the suitability of

communities to successfully host and manage a shared solar farm, the socioeconomic

characteristics of locations have been assessed in terms of the community’s (i) organizational

capabilities, (ii) financial capabilities and (iii) solar resource. India Human Development Survey

dataset was used to extract information the characteristics of different communities related to

organizational abilities. Data on financial access in rural areas was used to assess the suitability of

communities to host and manage a community based solar farm. The average annual solar resource

in India shows the technical feasibility of hosting a solar farm across different locations in India.

This study outlines the importance of the three aforementioned capabilities in successfully

managing a community shared solar resource and presents the abilities of different locations across

India in this regard.

iv

TABLE OF CONTENTS

List of Figures ................................................................................................................................. v

List of Tables ........................................................................................................................ …….vi

Acknowledgements .................................................................................................................. …..vii

Chapter 1 Introduction ........................................................................................................ 1

Chapter 2 Rural Electrification & Community Driven Development ................................ 3

Rural Electrification & Importance of Energy Access in India .......................... 3

The Role of the Community: Importance of Collective Action, Social Capital in

Rural Development ......................................................................................................... 4

Chapter 3 The Idea of Community Solar ............................................................................ 8

Incentives of Community Ownership ................................................................. 8

Concept of Community Solar .............................................................................. 8

Models of Community Solar ............................................................................... 9

Successful Community Sourced Solar Projects ................................................ 12

Chapter 4 Overview of Research Approach ..................................................................... 16

Chapter 5 Organizational Abilities in a Community ........................................................ 19

Importance of Community Based Organizations .............................................. 19

Data on Community Based Organizations ........................................................ 20

What Do The Organizations Represent? ........................................................... 22

Factor Analysis to Obtain Information on Community Organizational

Capabilities .................................................................................................................... 24

Chapter 6 Financial Abilities of a Community ................................................................. 26

Microfinance as an Instrument for Enhancing Rural Financial Services .......... 27

How Can Microfinance Impact Rural Development? ....................................... 33

Examples of Successful Projects Which Have Used Microfinance to Support

Solar Power Deployment .............................................................................................. 35

Cataloguing Financial Capabilities ................................................................... 38

Chapter 7 Solar Resource in India .................................................................................... 41

v

Solar Resource Terminologies .......................................................................... 41

Solar Resource across India .............................................................................. 41

Assessing the Solar Resource in the Indian Peninsula ...................................... 43

Chapter 8 Results ……………………………………………………………………...45

The Underlying Ability of the Community to Organize ................................... 45

Penetration of Microfinance in India ................................................................ 49

Solar Resource Aspect in Community Solar Assessment ................................. 54

Chapter 9 Discussion ........................................................................................................ 56

Chapter 10 Conclusions .................................................................................................... 60

References ......................................................................................................................... 62

Appendix ........................................................................................................................... 66

Exploratory Factor Analysis ............................................................................. 66

Mathematical Model ......................................................................................... 69

Factor Loading Estimation ................................................................................ 73

Factor Scores ..................................................................................................... 78

Political Map of India with the States ............................................................... 82

vi

LIST OF FIGURES

Figure 7-1 Annual average global horizontal irradiance data for India, represented for

solar conditions from 2002-2011[76] ............................................................................... 43

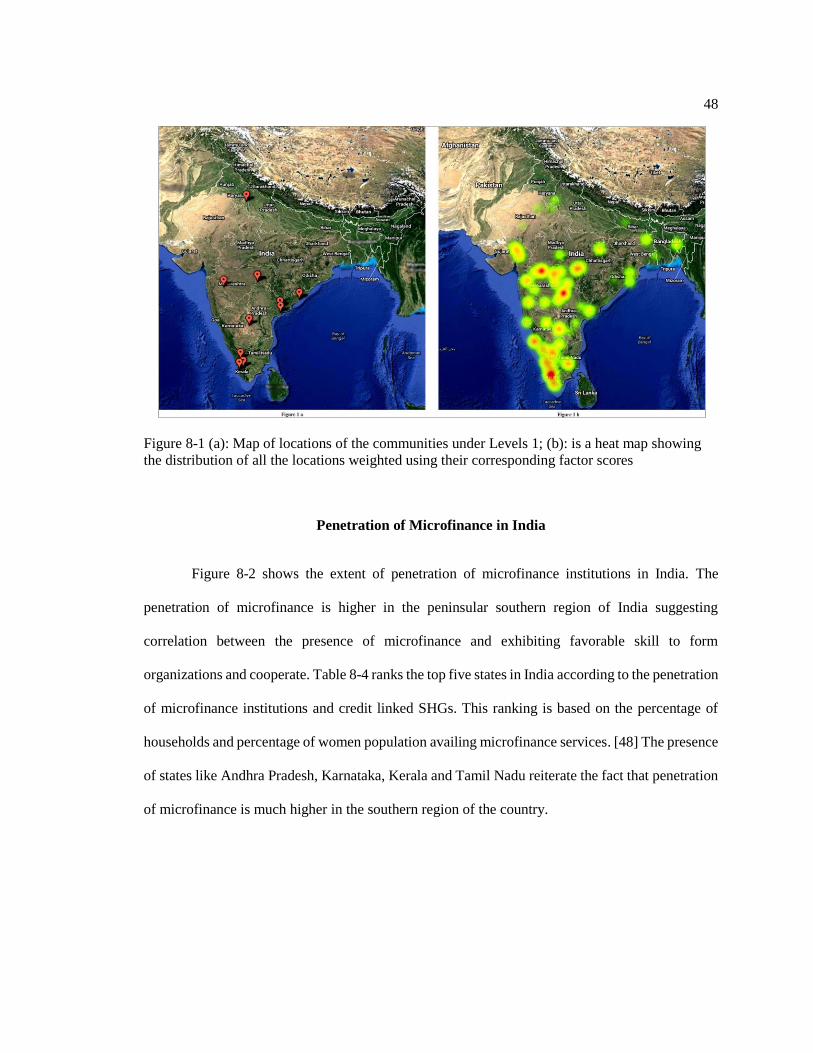

Figure 8-1 (a): Map of locations of the communities under Levels 1; (b): is a heat map

showing the distribution of all the locations weighted using their corresponding

factor scores ..................................................................................................................... 49

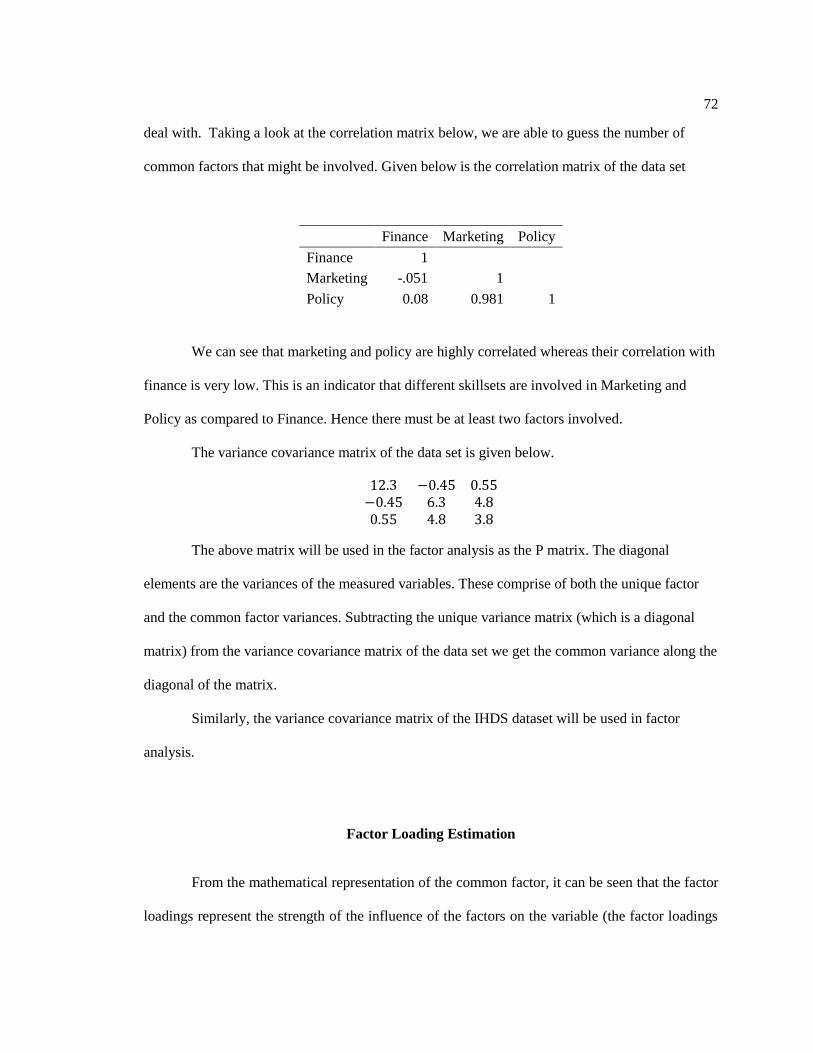

Figure 8-2 Penetration of Microfinance in India [78] .............................................................. 50

Figure 8-3 Number of credit linked SHGs in Andhra Pradesh, Maharashtra, Kerala and

Haryana (2012) ................................................................................................................ 53

Figure 8-4 Histogram showing the number of Level 1, 2 and 3 locations in the range of

GHI values ....................................................................................................................... 54

Figure 9-1 Annual average global horizontal irradiance data for India, represented for

solar conditions from 2002-2011 [76] .............................................................................. 59

vii

LIST OF TABLES

Table 3-1 Comparison of Community Solar Models by NREL .............................................. 10

Table 5-1 List of organizations considered in dataset (subset of the IHDS data) .................... 22

Table 6-1 List of Microfinance Institutions and Indicators ..................................................... 39

Table 8-1 Factor Loadings for observed variables (organizations) on Factor 1 ...................... 46

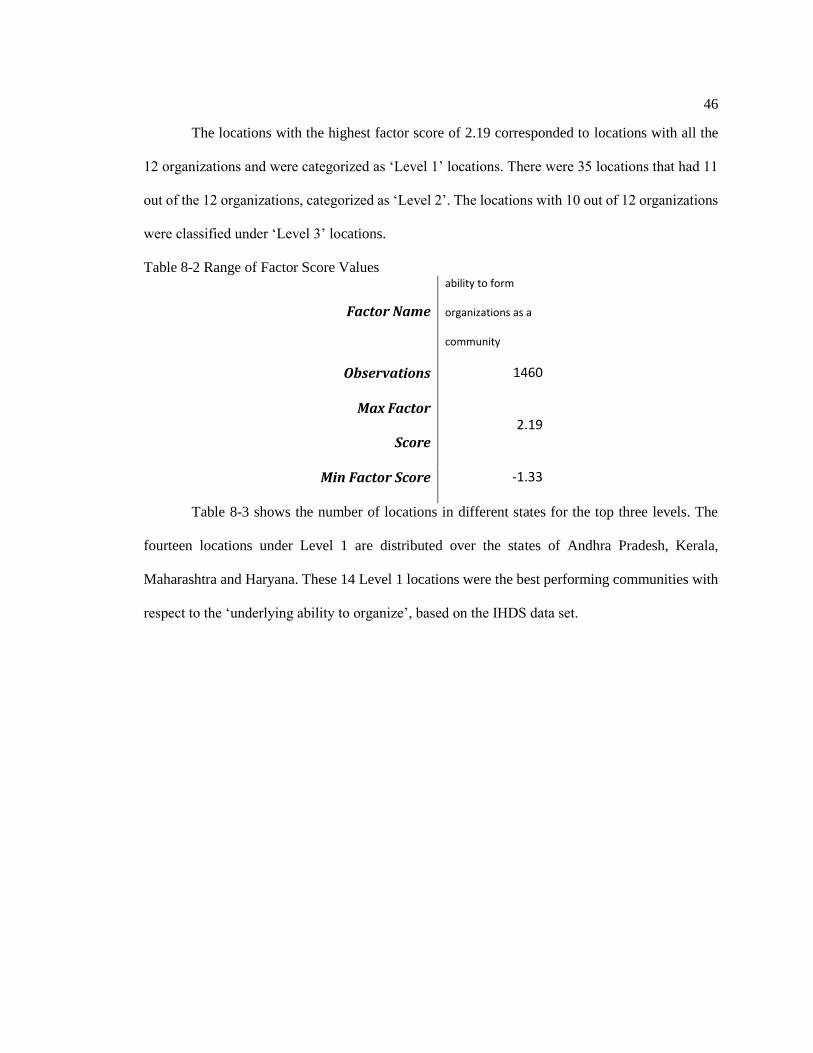

Table 8-2 Range of Factor Score Values ................................................................................. 47

Table 8-3 Number of locations (state wise) under each Level................................................. 48

Table 8-4 Top 5 States in India based on Penetration of Microfinance Institutions and

Credit-Linked SHGs ........................................................................................................ 51

Table 8-5 Ranking of states in terms of percentage growth in deposit accounts ..................... 51

Table 8-6 Primary Agricultural credit societies-ranking based on working capital

available (2011) ................................................................................................................ 52

Table 8-7 Ranking of States based on number of commercial banks functioning in rural

areas (2009) ...................................................................................................................... 53

viii

ACKNOWLEDGEMENTS

I would like to express my sincere gratitude to Dr. Jeffrey Brownson and Dr. Andrew Kleit for

their support during my time as a Masters’ student. Their guidance was invaluable in putting

together this study and also in writing this thesis. I would like to thank Dr. Chiara Lo Prete for

agreeing to be a part of my defense committee and for her inputs during the defense. Last but not

the least, I would like to thank my family and friends for their love and support throughout my

life.

1

Chapter 1 Introduction

Access to energy is regarded as one of the key factors in social and economic development. In the

context of developing economies like India, access to modern energy services like electricity is an

integral aspect of development. Integrated rural development takes a bottom up approach begins

at the base of the pyramid, which in this case are the villages. Community driven development

has been promoted by World Bank and United Nations as an important aspect of rural

development. The development process becomes a part of the community and their livelihood

ensuring their active involvement in the projects.

A majority of the rural households in India use bio-mass based fuels for cooking and

lighting. Apart from being inefficient, these pose various health and environmental hazards.

Providing access to energy has been included in the United Nation's Millennium Development

Goals. Electricity can substitute the fuels used for lighting while providing cleaner and reliable

lighting. Although, the Government of India has targeted rural electrification through multiple

schemes, the central grid does not cover the entire country. There is also the issue of providing

round the clock reliable power to villages. Distributed generation using renewable technology is a

viable option for providing reliable access to electricity. Micro and mini grids also offer

flexibility in terms of regulating and managing the power according to intermittency issues in the

renewable technology.

Community based solar projects can serve as rural electrification projects while actively

involving the community in development and management of the resource. Solar photovoltaic

technology has been shown to be a viable option for rural electrification in India. India also has a

history of collective action in forest and watershed management. However, community managed

solar projects are few and far between. A successful community solar project requires more than

2

good solar resource. It demands for a conducive environment where the community can cooperate

to work towards maximizing everyone’s benefit rather than the individual. The community must

have the capacity to regulate the use of the resource, ensure that the rules are followed and also

manage the finances of the resource system. Lack of knowledge about technology and education

in the rural areas discourages many developers to invest in such projects. However, it has been

shown that communities are more than capable of managing their own resources.

Often times, the suitability of the location to successfully host a community based project

is ignored. The assessment studies fail focus on the ability of the local population to engage in

collective action for management of the resource. While the capacity building process is targeted

towards bridging the technology gap, the importance of community characteristics and

capabilities are ignored. This study selected three underlying characteristics for community based

solar projects in villages across India, namely i) a community’s organizational capabilities, ii) a

community’s financial capabilities and iii) the local solar resource. By justifying the importance

of the abovementioned characteristics in developing community solar, the potential of

communities in India have been explored. The goal is to use the underlying characteristics as

yardsticks to assess the potential of different communities across India. This assessment will be

made based on data obtained for the three different underlying characteristics. The potential will

be a clear indicator of the suitability of the location to successfully host a community based

energy project. In this study, community is defined as a group of people living in geographic

proximity, as in the case of a village. Although this study looks at the potential for community

solar projects, no assumptions are made on the type of the solar technology that can be

implemented. Solar power in this case is purely treated as a resource which can be used as the

community sees fit.

3

Chapter 2 Rural Electrification & Community Driven Development

Rural Electrification & Importance of Energy Access in India

As of the year 2005, 412 million people in India did not have access to electricity. 92% of this

population was in rural India. [1] Rural electrification has been one of the top priorities for the

Indian and it has constantly rolled out numerous schemes and policies in this regard. Though

electricity is not the primary source of energy used in rural household activities in India, it is a

viable substitute for traditional lighting fuels. According to the Government of India, a village is

considered electrified, if 10% of the households in the village have electricity access and

electricity is provided to all the public spaces such as schools, health centers, community centers,

etc. [2] The Central Electricity Authority reports that only 9 out of the 29 states in India have

achieved 100% village electrification and 12 out the remaining 20 states have achieved between

90-99% village electrification. [3] Major reasons for a number of villages being unelectrified is

their remote location and the high cost of extending the grid to such locations. Hence, the

Government of India has started promoting distributed generation projects to provide access to

electricity in remote areas.

A number of the ‘electrified’ villages in India do not have 24 hour access to electricity or

have reliable power supply. Not one state in India can boast of 100% household electrification in

India. [3] Although, global level studies have not been able to unearth a causal relationship

between energy consumption and economic growth[4], there are community level studies that

have shown the positive impact of access to energy on rural development. [5] The Global Energy

Network Institute has shown that electricity consumption per capita has strong positive

correlations with social development indices like human development index, maternal mortality

4

rates, infant mortality rates, etc. [6] Studies have also shown that village level microgrids have

contributed to rural development in developing countries like Kenya. [7] These studies establish

the importance of access to electricity in improving the quality of life.

Due to the inability of the central grid to reach every part of the country, many avenues

open up for using renewable power as for rural electrification. Renewable power can be set up

independent of the grid and can be used as a distributed source targeting the needs of the local

community. Renewable power can not only be used to supply electricity to un-electrified villages,

but can also be considered as an option for providing supplemental power to villages that cannot

rely on the grid for reliable power supply round the clock. Studies have shown solar power to be a

viable option for decentralized power generation in India. Most of India has an annual global

solar radiation greater than 1900 kWh/m2/year. In comparison, Germany, which is one of the top

countries employing solar power successfully, the annual solar radiation ranges from 800

kWh/m2/year to 1200 kWh/m2/year. [8-16] The National Electricity Policy of India emphasizes

deployment of renewable power in locations where it is suitable and economical. [17] Renewable

energy is a viable option for distributed generation. Solar photovoltaics have been adapted

globally as well as in India for rural electrification. Electricity from solar photovoltaics can be

from a micro-grid, individual solar home systems, solar lanterns, etc. Photovoltaics have minimal

operational costs and can be set up in different ways according to the needs of the society. Solar

power is a feasible solution for distributed power generation in rural areas in India.

The Role of the Community: Importance of Collective Action, Social Capital in Rural

Development

Marshall[18] defined collective action as the action taken by a group in pursuit of

members’ perceived shared interests. This action can be taken by a group of people or an

5

organization acting on their behalf. Social capital is the structure of relationship between

individuals in a community that encourages productive activities. [19] In this context, social capital

indicates the strength of trust in the society. Social capital covers several aspects of community

strength like networks, group memberships, civic and public participation. Social capital can also

be interpreted as a common resource that enables access to social, economic and natural resources

for the entire community. [20] Social capital reduces the transaction costs of interacting with

members of the community and hence facilitates cooperative action. [21] Social capital is also

related to aspects of organizations like networks, rules and trust that facilitate collective action and

cooperation. [22] It is hypothesized that a community with high social capital will have a better

ability to manage a resource collectively. [23] The capacity of a community to cooperate is an

underlying ability of the community to create formal or informal frameworks to achieve collective

action. [24] The underlying ability can also be interpreted as a form of social capital, but of the

community and not an individual. The presence of community based organizations in the

community indicate high social capital among the community members and hence, higher

inclination to engage in collective action.

Examples in literature prove effectiveness of community driven development and focus on

community involvement in developmental projects across the world. Review of literature on

successful community sourced projects across the world point call attention to the following as

factors leading to success. Participatory governance, which entails the involvement of locals in the

decision making process has been shown to be a primary reason for success of many community

level projects. A study to assess the importance of institutions in a rural community, survey of

agricultural households in Kenya showed that using Producer Marketing Groups that are farmer

run organizations, the farmers in rural Kenya were able to overcome market imperfections and

facilitate access to new technology. In this case, the key factor in success was found to be

mobilizing the farmers and collective decision making. [25] Apart from involving the locals in

6

decision making, friendly policies from the government also boost the chances of success of

community development projects. In India, forest management has been carried out for decades

collectively by the community with assistance from the forest department. A study by the Center

for International Forestry Research showed that, for successful management of forest resources the

involvement of people, especially women and NGO organizations is necessary along with friendly

government policies backing the locals. A study in West Bengal showed that, involving women in

forest resources management led to more prudent use of resources and better prevention of

misappropriation of resources. This was attributed to the fact that more women were directly

involved in using the forest resources and contributing to household income compared to men .[26]

Involving the local community members in the day to day activities of the project also increase the

chances of success. This type of involvement is different from participatory governance in the

manner that the locals are actively involved in the daily operations. Being a direct beneficiary of

the project success, the community members have an incentive to work towards achieving the

project goals. The success of rural development projects have been shown to depend on the

involvement of locals and community based organizations in both the planning and the operational

aspect of the project.[27] Nepal is a prime example of where successful community based

management of natural resources led to a bylaw being passed for promotion of community based

organizations for rural electrification.[28] The examples from both India and Nepal show the

importance of local governance, involving the community in the project activities and the need for

backing from the government in success of community sourced projects. Re-iterating on the

importance of local involvement throughout the project, Wijayaratna points out that a bottom up

approach is required for integrated rural development. [29] A bottom up approach starts with

involving the members of the targeted community in every stage of the process. This aligns with

Ostrom’s principles of collective action, which calls for the involvement of the locals in

management of the resource. [30] Studies of watershed management projects have shown that

7

participation of the people is a significant indicator of success of the overall project [31] and social

capital has been shown as a significant determinant of participation and project effectiveness.[32]

8

Chapter 3 The Idea of Community Solar

Community renewable energy projects are renewable energy project which involve select

members of the community or the entire community in various stages of the project. The

members of the community are stakeholders in the project. The scope of community renewable

energy projects is very broad in terms of the level of involvement of the community members and

the various stages of the project at which they are involved. Community shared solar answers

rural electrification issues and also promotes community driven development.

Incentives of Community Ownership

The benefits of a community owned/managed energy project vary according to the stakes

of the community and its members in the project itself [33]. Some of the incentives are listed

below.

● Reliable power supply and steady electricity prices

● Local income and employment creation

● Local control in managing the project to suit the specific need of the community

● A channel of financial investment

Concept of Community Solar

‘Community Shared Solar’ is a solar electric power system that provides electricity or

financial benefits to multiple community members. Community scale renewable energy projects

hedge against increasing fuel costs, reduce carbon emissions and create jobs in the community.

9

[34] A community solar plant, also called a community solar garden, is defined as a solar array

with subscribers who share the benefits of the solar plant. It is a solar project with multiple

individual owners living in geographic proximity of the project and sharing the costs and benefits

of the project. [35] Community based solar, being a decentralized energy source; offers a solution

for rural electrification problems. The involvement of the community in the project ties in with

the bottom up approach targeting integrated development. It has been suggested that community

shared solar improves quality of life by bringing together residents on issues of sustainability of

development. Community solar projects also make the local community economically

competitive. [36] Community solar ties in both collective action and renewable energy. By

involving the local community, a community solar project takes the bottom up approach in rural

development. Based on how the project is structured, a community solar project can provide

electricity to the community and/or serve as an income generating entity in the community.

Models of Community Solar

The National Renewable Energy Lab [34] classifies community solar models into three

main categories. Table 3-1below distinguishes the salient features of each model.

10

Table 3-1 Comparison of Community Solar Models by NREL

Utility

Special Purpose Entity

(SPE) Non Profit

Owner Third Party or Utility Members of the special

purpose entity

Non-Profit

Organization

Financed By Utilities through

grants of subscriptions

Member investments

and incentives.

Sometimes it could be

state promoted grants

Member donations

and contributions

Host Utility or Third Party Third Party not for profit

organization as host

Subscriber

Subscribers/Customers

of the utility (Rate

Payers

Community investors Donors/members

Intent of the

subscriber

Offset (Save) personal

electricity use

Return on investment (

in some cases it can be

to offset personal

electricity use)

Philanthropy or tax

benefits from

charitable donations

Long Term

Strategy

The utility aims to

offer its customers a

solar power option,

thereby meeting

renewable portfolio

standards

The SPE either sells

system to the host after

a certain period or

retains the system to

make money off the

generated electricity

Retain the system for

electricity production

Utility Sponsored Model

In this model, the project is owned and/or by a utility but the project is open to ratepayer

subscription. The utility funds the project either by itself or using grants or by having a

subscription fee. The customers of the utility then buy into the solar plants buy paying the

subscription fee and the benefits and the incentives are added to their electric bills. The biggest

advantage to the community, the members of which are the customers of the utility in this model

is the pre-existing legal, financial and managerial infrastructure of the utility which can be used in

implementing the project. In a utility sponsored model, the ratepayers are the subscribers and

11

hence indirect users. The electricity generated from the solar plant, does not reach them directly,

but is a part of the utility’s portfolio. The solar plant in this case is a dedicated solar power plant

in a suitable location and not individual rooftop systems.

Special Purpose Entity Model

This model is useful if the members of the community want to take advantage of the tax

incentives and other benefits themselves. In this case the members of the community structure the

project as a business. The community forms a for-profit organization to take advantage of the

benefits of generating solar power. The members of the community are ‘tax-motivated investors’

who wish to avail the tax benefits of generating solar power. The community organization my

hence deal with the legal and financial procedures in setting up and running a business. In this

model, the solar plant is a revenue generating entity. The benefit to the investors is the return on

investment.

Non-Profit Model

In this model, a non-profit organization engages a community in developing a community

shared solar project. The benefits of the solar project can be shared between the non-profit and

the community or the community just acts a donor and finances the project as a gesture of

goodwill. Recently, many non-profits have teamed up with third party for-profit entities that own

and install the system for tax benefits and the non-profit organization uses the power generated

from the project. Non-profit organizations are not eligible for tax benefits themselves, but they

can take advantage of many grants and other sources of funding available for non-profits. The

12

advantage for community members in this model is that they can deduct their contribution to the

project as a donation if the non-profit manages to obtain a status as a charitable organization.

Successful Community Sourced Solar Projects

University Park Community Solar LLC, University Park, Maryland

The University Park (UP) Community Solar LLC[37] is a 36 member limited liability

company of residents of University Park, Maryland formed to establish and maintain a solar

power generation system for the community. A centralized generation unit is set up on the rooftop

of the Church of the Brethren, which acts as the host site for the solar system. The solar panels

were installed on the roof of the church with the help of outside experts, Standard Solar Inc., who

are also responsible for the maintenance of the panels. The cost of the panels was covered by the

proceeds of the membership purchase in the LLC. This is the initial investment for the members

of the community. By becoming an LLC, they found it easier to raise capital, incentivizing

contributors with a possible return on their investment. Their "for-profit" status also allowed

them to collect a 30% cash grant (rebate) on their total cost, $133,550. They targeted smaller

investments, looking for approximately thirty-five people to contribute at $2000, with the average

investment being $4000. They plan to offer investors a return on their investment in the following

ways,

Selling electricity to the church (13% below retail rate of utility company)

Federal and state support (30% cash grant from federal government as well as $10,400

demonstration grant from Maryland Energy Administration) and

By selling solar renewable energy credits (SRECs).

13

Through these avenues, they plans to be able to pay off investors in 6-7 years, with a 7-

8% return on investment over the twenty year life of the project. The Church of the Brethren also

has the option to purchase the system before the 20 year lease is up1. This model is an example of

a ‘Special Purpose Entity’ formed by the community members to take advantage of the legislation

the state of Maryland.

Sunderbans- Sagar Island- West Bengal, India [8, 13, 38]

Sagar Island is located in the Sunderban delta on the banks of river Ganga on the eastern

coast of India. It is one of the hundreds of islands which make up the Sunderbans. The terrain in

the Sunderban delta is primarily mangrove swamps. Due to the challenging terrain and the fact

that there a number of these small islands, it is economically not feasible to extend the grid to

these islands. The state electricity board currently serves around 650 customers on the islands by

means of diesel powered generators which provide power for 4 hours a day. In 1996 the West

Bengal Renewable Energy Development Agency (WBREDA) set up solar power plants on the

islands to serve as a distributed power generation source. Seeing the success of solar power in the

locations, the program was promoted and not there are 10 solar power plants in the islands

powering 1600 households for up to 6 hours a day.

The Sagar Rural Energy Development Cooperative was established to oversee the

operations of the rural electrification project. The cooperative consists of local officials who work

with the WBREDA, which has maintained an advisory role. The cooperative is responsible for

collecting the tariffs and passing them on to the WBREDA and is also responsible for dealing

with non-payment and deciding on sanctions. We see that the projects based on community

1 "Solar Gardens | Community Power!." 2010. 29 May. 2014 <http://www.solargardens.org/>

14

centric, village specific schemes. Once a plant is commissioned in a village, a village level Local

Management Committee is formed and this body oversees the daily operations of the plant. The

implementation of renewable energy in the Sunderban delta has been hailed as success story and

the project also received the Ashden Award in 2003 for promoting local clean energy solutions.

Research on the impacts of installing distributed power generation to electrify villages has shown

a significant improvement in the socio economic conditions of the people.

Community Solar Power Plant-Jhansi, Uttar Pradesh, India [39]

Another example of a successful community managed power plant is a community

managed solar power plant set up in the Jhansi district of Uttar Pradesh in India. Scatec Solar, a

Norwegian company partnered with Development Alternatives, an NGO in India to setup two

community solar power plants in Rampura and Gopalpura villages in the district. The projects

were entirely funded by Scatec Solar and Development Alternatives played a role in facilitating

the project by training the villages in management practices and the technology. A Village

Energy Committee (VEC) was formed and the VEC was trained in the operation and maintenance

of the plant. The VEC oversees the daily plant operations. A local bank was used to manage the

finances of the VEC and the bank also acted as an institution to develop trust and increase social

capital in the village community.

The plant was designed to suit the needs of the local population and the land for the solar

power plant was obtained with the help of the village Panchayat. The NGO took the responsibility

of training the villagers by offering them various workshops and creating an awareness about

renewable technology. The villages were urged to attend all meetings between the project

developers, local government and district agencies. A Build-Operate-Transfer model was

15

implemented where the community members ultimately own the project. There has been a

marked improvement in the quality of life in the village since the power plants went into effect.

The above examples help illustrate the fact community based renewable energy is a

viable option to serve the energy needs at a community level. Considering the case of rural India,

where there is no reliable power supply from the grid, solar power is a viable option to provide

electricity access to villages. Community participation in such projects will ensure the long term

success and sustainability of such projects.

The Colorado Community Solar Act is one of the first instances where the state

government has taken initiative in promoting community owned solar power. Following

Colorado’s footsteps, Minnesota is also putting together legislation for promoting community

solar. Community based projects involve empowering the community to manage their resources

and contribute to their development [40]. Community shared solar takes a bottom up approach

towards rural electrification by making the community members active beneficiaries. The bottom

up approach aligns with community driven development, which is integral to development in

emerging economies.

16

Chapter 4 Overview of Research Approach

There are many complexities in setting up a community energy. In the context of developing

economies like India, developing a rural community managed energy project also calls for

educating the people about the technology [33]. This study selected three underlying characteristics

for community based solar projects in villages across India, namely i) a community’s organizational

capabilities, ii) a community’s financial capabilities and iii) the local solar resource. We

hypothesize that a community with an existing social framework has a better chance of engaging

in collective action. Hence, this community will be better suited to host a community shared solar

farm. Community-based organizations offer a good framework to implement collective action.

Strong community network and high social capital have a positive impact on developmental

projects and quality of life in rural areas. [31, 32, 41] Community participation not only helps in

the initial stages of the project, but also ensures the long term sustainability of the project. NGOs

involved in rural electrification projects spend a lot of resources on capacity building in the

communities. Apart from educating the community on the renewable energy technology, the

community must also be trained to engage in collective action and managing the resource as a

community. As Ostrom mentions, no two communities are similar and there is no standard template

that can be followed in common property resource management. [30] The underlying

organizational ability of a community can be used as a yardstick to assess the community’s

suitability for collective action. It is the characteristics of the community that enable the locals to

become active stakeholders in the project, the essence of community shared solar. This study

intends to include a piece of information characteristic to the community as a part of initial studies

17

for developing such projects. This study aims to extract the information about the underlying

characteristic from the existing societal frameworks. The assessment will be purely based on the

existing strengths and weaknesses of the community.

The financial abilities of the community here refer to both resource management as well as

access to financial services. Financial capabilities are important to the success of a shared solar

project. [42] Microfinance has been shown to improve access to financial services in rural areas.

[43-48] Penetration of microfinance can serve as a proxy for the financial capabilities of rural

communities. Solar projects are capital intensive and familiarity with financial services and

schemes will assist the locals in managing the project.

The third aspect, the solar resource is an important criterion for the technical success of

the system. Usually considered the limiting criterion, in India where the average solar irradiation

is around 1200 kWh/m2 to 2300 kWh/m2 [14], the solar resource is more than sufficient for a

successful distributed solar power plant. The solar resource is consistent across a large part of India

thereby marginalizing solar resource aspect of the distributed solar project.

The following chapters will outline the methods used to extract information about the

underlying characteristics that contribute to a successful community shared solar plant. Information

regarding (i) community based organizations, (ii) a community’s access to financial services and

(iii) the local solar resource will be pieced together to present a well-rounded picture representing

the potential or suitability of multiple locations across India to host community shared solar farms.

The assessment of community characteristics and financial capabilities will be important in

designing a project structure suitable to the local needs. The different characteristics justify the role

of socioeconomic characteristics in a successful community solar project and support a

multidimensional approach to developing community shared solar projects. Identifying the

strengths and weaknesses of a given location will not only help determine the suitability to host a

18

community based energy project but also help the developers prepare to overcome the deficiencies

whenever possible.

19

Chapter 5 Organizational Abilities in a Community

The importance of community involvement in rural electrification process has been emphasized

in literature but has never been a criterion in the feasibility studies of projects. Community

participation not only helps in the initial stages of the project, but also ensures the long term

sustainability of the project. It is the characteristic of the community that enables the locals to

evolve from being just a beneficiary to being active stakeholders in the project. One of the

essential requirements of successful collective action is that the rules and penalties must be

decided locally by the appropriators of the resource. [30] The ideal community should be capable

of putting aside differences and taking decisions with the common goal in mind or in other words,

to cooperate with each other. The capacity of the community to cooperate is the inherent

capability to form social networks, both formal and informal, to achieve the goals of collective

action. [24]

Importance of Community Based Organizations

A multiple stakeholder approach is very useful in initiating collective action for

protection and provision of public goods [22] and local organizations offer a platform for this

type of approach. Hussain et. al. showed the positive impact of community based organization on

socio economic development in rural Pakistan. [41] Viable community groups have been shown

to be important drivers in development. Community based organizations also help streamline

common interest provide effective outreach of the project benefits. Narayan also illustrates the

benefits of nurturing existing organizations to improve capacity and engage in collective action

20

rather than forming new organizations. [49] Isham, Narayan et. al.[31] suggest approaches to

examine ways cooperative action can overcome individualistic inefficiencies like free riding.

We propose to use a characteristic of the community that enables the members to

organize themselves as a yardstick to assess the community’s suitability for collective action.

Although not the only metric, institutions and organizations indicate the presence of good social

network and capacity to cooperate. The examples in literature support the hypothesis that a

community with an existing social framework i.e. organizations and networks has a better chance

of engaging in collective action. The organizations are the result of the underlying characteristic.

This study uses statistical techniques to extract information about the underlying characteristics

which will then be used as an indicator of the potential to host and manage a community shared

project.

Data on Community Based Organizations

The India Human Development Survey (IHDS) is used as the source of information about

community based organizations in various locations. The survey was organized by the University

of Maryland in coordination with National Council of Applied & Economic Research, New

Delhi, India. [50] The IHDS is a nationally representative survey covering 41,554 households in

1503 villages and 971 urban neighborhoods across India. The section on village-level data was

used, with the questions oriented towards socioeconomic conditions, infrastructure and presence

of organizations/institutions in the village. As a part of the bigger survey, IHDS enquired into the

presence of 12 different community-based organizations in each village. The responses to these

12 questions were down-selected as the dataset for analysis. The responses were recorded as a 1

for a ‘yes’, 0 for a ‘no’ and -1 for a ‘don’t know’. All the locations with at least one ‘-1’ value in

21

the list of responses were removed from the data set. This reduced the number of villages in the

list to 1460 from the initial 1503 sampled.

Table 5-1 displays the organizations considered in this study. This list covers a range of

formal and informal organizations in a typical village. Institutions are varied in their functions as

well as the background of the members. Depending on the type of organization, membership is

either voluntary or by virtue of profession or religion. Informal institutions thrive based on the

characteristics of individuals and their willingness to participate. The formal institutions available

vary greatly depending on location and hence an individual’s affiliation to such institutions also

depends on their location. [51]

22

Table 5-1 List of organizations considered in dataset (subset of the IHDS data)

Name of the Organization Function/Purpose

Agriculture & Milk

cooperatives

Formal and larger trade groups that sell

their products under one banner

Caste associations Represent caste members in issues of

importance

Community Centers Convention centers for local events

Credit or Savings groups Credit facilities and household

improvement services

Mahila Mandals

Federations that help women participate in

rural activities and work towards women

empowerment

Non-Governmental

Organizations (NGOs)

Voluntary organizations working on

developmental projects in rural areas.

Usually based out of cities

Panchayat

Local self-governance institutions at the

village level recognized by the Govt. of

India

Pani Panchayats Formal bodies which deal with water

(pani) related issues

Religious and social

groups Organize religious festivals and events

self-help groups (SHG)

Groups of 10-20 women who pool their

savings, which will be used to provide

credit to members when needed

Trade Unions Professional groups formed by local

businessmen

Youth clubs Associations that involve the youth of the

community in various activities

What Do The Organizations Represent?

‘Mahila Mandals’ are federations that help women participate in rural activities and work

towards women empowerment in the village. These can be formal as well as informal. A typical

self-help group (SHG) consists of 10-20 women from socio economic background who pool their

savings, which will be used to provide credit to members when needed. Youth clubs and

associations are formed to involve the youth of the community in development and community

activities. Credit or Savings groups provide credit facilities and household improvement services.

23

Trade unions and cooperatives are business related organizations that help in promoting local

businesses and income generating activities. In cooperatives, the members pool their resources in

order to earn greater economic benefits. Religious and caste associations are involved in

celebrating religious festival and representing the caste members in issues of importance. Non-

Governmental Organizations (NGOs) are typically based in urban locations and consists of

people who wish to contribute to rural development[52]. A Panchayat is a local self-governance

institution at the village level in India.

This list of institutions and organizations considered covers a range of formal and

informal organizations in a typical village. The institutions are varied in their functions as well as

the background of the members. People gain membership in religious and caste institutions

because they were born in a particular religion or caste whereas membership in professional

groups like trade associations and credit groups is by virtue of their profession. Women join self-

help groups voluntarily to help their livelihood. Agricultural and milk cooperatives indicate the

presence of business oriented people in the community. Credit and savings groups show that the

members of the community place their trust in the group with regards to their savings and have

access to credit in time of need. Panchayats indicate the presence of a formal institution to resolve

local issues and take care of local administration. The formal institutions available vary greatly

depending on location and hence an individual’s affiliation to such institutions also depends on

their location[51]. Informal networks thrive based on the characteristics of the individuals and

their willingness to participate. This set of institutions and organizations can present a

comprehensive picture of the formal and informal networks in the community and hence translate

to their ability to cooperate. This will provide us with a good basis to understand some

characteristic abilities favoring the success of community based project.

24

Shortcomings of the IHDS Dataset

Though the India Human Development Survey is as comprehensive as one can hope, it

must be noted that the purpose of the survey was not to determine locations for community based

resource management. The questions are not tailored towards the capacity or the inclination of the

people to form organizations for resource management. However, it is the best available data set

in this regard. For this study, we are using a particular section of the village level survey. Also,

the IHDS dataset does not have any information on how active an organization is in the village.

An inactive institution does not serve any good. On the contrary it might be detrimental to

development. With the limited resources and information available we decided to proceed with

the study using the IHDS data set.

The ideal way to select the location will be conduct a field survey of potential locations

where the respondents are asked questions very specific to the project to gauge their capabilities

in managing a resource and resolving conflicts. The ability to form organizations can be used as

an initial screening criterion for selecting locations. Hence, even though the available survey is

not directly focusing on community based actions, it is related to successful implementation of

collective action projects (by providing information on organizations and institutions) and the use

of the data in the study is justified.

Factor Analysis to Obtain Information on Community Organizational Capabilities

The correlations between survey responses in the survey were used to identify the

underlying characteristic in the community that favored the formation of organizations and

institutions. Underlying characteristics like ability to cooperate and factors influencing

willingness to participate are unobservable. The results of such characteristics, however, are

25

observable outcomes like community-based organizations. Studies have used statistical

techniques like exploratory factor analysis to extract common factors which are used as indicators

of unobservable underlying characteristics of community. [24, 53, 54] Exploratory factor analysis

was used to extract common factors based on a linear model involving the correlations in the

variables. The theory and mathematics behind factor analysis is presented, with an example in the

Appendix section. The common factor represents the unobservable characteristic that influences

the formation and functioning of such institutions. The coefficients of the common factors are the

factor loadings that represent the strength of the influence of the common factors on the observed

outcomes. The factor score is a numerical estimate of the unobservable common factor. In this

context, factor scores were used to compare the ability of the community to form organizations

across different villages. The factor scores aided in processing 12 pieces of information (the 12

types of institutions considered) using one numerical value. Factor analysis of the data and

calculation of factor scores was carried out using STATA. To geographically visualize the

distribution of the better performing locations, the Google Fusion Tables plotting tool was used to

plot the locations based on their factor scores.

26

Chapter 6 Financial Abilities of a Community

In many studies on common property resource management and community based projects best

practices suggest that community must be more than just the targeted beneficiary. The community

must be involved as a stakeholder in the project. Not only will this give the members a sense of

ownership of the project but also ensures that they will work towards the success of the project.

One of the many ways to make someone a stakeholder is to make them invest capital in the project.

Like most renewable technology, solar photovoltaic are capital intensive. There is high initial cost

and financial success depends on regular payments for the electricity generated.

There are quite a few ways to finance a community solar project. The capital to set up the

project can come from various avenues

● Grants from non-profit organizations

● Grants from a corporate entity as a part of their Corporate Social Responsibility project

● Investment by a company

● Investment by entrepreneurs

● Loans from banks and financial institutions

Considering most of the intended beneficiaries i.e. the targeted community, depend on

agriculture for their livelihood or earn irregular wages, access to credit is not easy. [55] Not many

financial institutions will be willing to loan money to this section of the society due to lack of

information about their creditworthiness. The Rural Finance Access Survey, 2003 conducted

jointly by the World Bank and the National Council of Applied Economic Research, India showed

that rural banks serve primarily the needs of the rural rich. The rural poor on the other hand, face

difficulties in accessing financial services. Even with economies of scale playing a role in

community based projects, many rural households might not be able to make an initial investment

27

in a solar project without any assistance. Apart from the initial investment, renewable energy

projects also require the resource appropriators to make pay their tariffs (depending on the tariff

structure) regularly. An issue, which regularly comes up is the inability of the community members

to pay regularly for the energy. [42] This causes the projected financial model of the project to

break down and disrupts the entire structure. Hence it is very important to look at the financial

capabilities of the community before deciding to proceed with the project.

Microfinance as an Instrument for Enhancing Rural Financial Services

Microfinance aims to provide financial services to the rural population in a regulated

manner like commercial banks but without the requirement for a collateral or credit history. It

involves group-based models, where several entrepreneurs come together to apply for loans and

other services as a group. [56] Microfinance works on relationship-based banking for individual

entrepreneurs and small businesses. Microfinance clients address usually self-employed low

income, no access to formal financial institution.

Evolution of Microfinance in India

The primary purpose of microfinance in India is to provide a means through which

impoverished families who are generally excluded from financial systems may access credit. [57]

The origin of microfinance lies in the various traditional and informal forms on money lending

present in communities over centuries. Community based financial transactions were based on trust

and social status. These informal money lenders-usually the richer people in the society- loaned

money without collateral based on verbal agreements and trust in the borrower. [45] All the

transactions were within the community and rules were set by the money lenders based on their

28

culture and religion. The local money lenders were able to stay in business without any outside

competition because of their knowledge of the creditworthiness of the borrowers. Since the local

money lenders were not regulated, they had the ability to design interest rate structures based on

the borrower. The nature of the transaction in itself puts the moneylender higher up in the village

hierarchy. [58] In 1904, exploitation of the farmers by moneylenders led to riots in the Deccan

region (modern day Andhra Pradesh) and this led to the then British Government passing the

Cooperative Societies Act. The intent was to regulate moneylending and promote the formation of

cooperative societies as an institution of rural finance. The members of the cooperatives pooled

their resources and helped other members out, thereby eliminating the money lender. In post-

independence India (after 1947), delivering credit and financial services to the rural farm sector

was a priority. At the time, the commercial banks, which were a part of the private sector, did not

have much of a presence in the rural areas and there were not sufficient incentives to help them

venture into farm sector. This along with the lack of information about the creditworthiness of the

rural poor and the preconceived notion about their inability to pay back or provide collateral

discouraged the commercial banks from setting up branches in rural locations. The cooperatives

were the government’s only choice to provide credit service to rural areas. [59]

The nationalization of banks in 1969 resulted in the establishment of Regional Rural Banks

and adoption of priority sector lending in order to eradicate poverty. This was one of the first steps

in involving formal commercial institutions in rural banking. Also, state led small scale programs

experimented different models to cater to the financial needs of the rural poor and this led to the

development of self-help groups and NGOs which were beginning to get involved in microfinance.

These developments over the years came with their own share of problems. The cooperatives were

dysfunctional due to poor governance and repayment issues. The regional rural bank’s financial

position deteriorated due to the restricted interest regime and poorly directed rural credit. The

Indian government had focused on expanding services and not much importance was given to how

29

and to whom the loan was sanctioned. This led to losses of more than Rs. 3000 crores by the year

1999. In 1992, the government of India proposed linking of cooperatives (SHGs) with commercial

banks. The National Bank of Agriculture and Rural Development led this initiative and published

guidelines to banks for financing SHG through the conventional banking system. In 1996, financing

SHGs was made a mainstream activity under priority sector financing for all the banks. [59]

Post 2000, the microfinance process was commercialized and saw the entry of many for-

profit agencies. This led to the formation of Non-Banking Finance Companies which were eligible

to take deposits and then would use the deposits as funds for loans. Microfinance was seen as a

social entrepreneurship instrument to gain social and financial returns. [59]

The informal traditional sources of finance (money lenders) have dominated the rural

financial sector for ages in India. Prior to the introduction of microfinance institutions (MFIs) in

India in the 1980s, the poor predominantly relied on informal commercial lenders, as formal banks

were unwilling to provide credit to those who were insolvent or could provide no collateral. These

moneylenders were easily accessible and unregulated, and were thus able to charge exorbitant

interest rates. [60] In the year 1961, 83.7% of the total dues in rural households were owed to

informal source of finance.[61] This number has dropped down to 36% in 1991. This can be

correlated to the development of formal microfinance services over this period. However, as

recently as 2002, several location specific studies showed that informal, traditional sources of

finance still dominate the financial transactions of the rural poor. Microfinance aims to provide

financial services to the rural population in a regulated manner like commercial banks but without

the requirement for a collateral or credit history. There are a few different microfinance delivery

models which have been successful over the years. Three of these models are described below.

30

Self Help Group Model

This model is unique and distinct to India. The self-help groups (SHGs) mobilize member

savings and provide need based loans to members. [47] Members make the rules and elect their

own leaders. Almost 90% of the SHGs in India consist primarily of women members as the poorest

households also rely on the income generated by the women of the house. The Federated SHG

model brings together a number of SHGs under a single governing body. The governing body has

around 15-20 elected members who interact with the NGOs and other organizations supporting the

SHGs. Federations can be linked with formal banking institutions and help serve a larger section

of the society. [62]

Grameen Model

The Grameen bank is the brainchild of Prof. Muhammad Yunus from Bangladesh. During

his travels through the villages of Bangladesh, he discovered that the rural poor suffer not from the

lack of skills, but from the lack of credit. In one of his interviews, he recollects his conversations

with the women in the village of Jogra. The women made a livelihood by selling chairs made of

bamboo. Due to the lack of finances, the women were forced to buy the raw materials and sell their

products through the same middleman. The women were also charged interest on the loan they

borrowed to buy the raw materials. At the end of the day, the women made roughly 2 cents a day.

He realized that, by eliminating the middleman, the moneylender, the women would be much better

off. This was the motivation for Prof. Yunus to work on providing the rural poor with access to

credit. After experimenting with multiple models, in 1983, with special charter from the

Bangladesh Government, he established Grameen Bank as a formal, independent financial

31

institution. [63] Grameen Bank model assumes that, rural individuals, when provided with credit,

will engage in income generating activities2.

A bank unit is set up with a field manager and bank workers. A bank typically covers 15

to 20 villages. The bank manager visits the villages to educate the local populations about the

operation and benefits of the back and identify prospective clients. Groups of five prospective

borrowers are formed. For the first 2 to 3 weeks, the members are required to make small deposits

to the bank. Only two of these five are eligible for and receive a loan. Only if the two borrowers

pay the principal and interest over a period of 50 weeks do the others become eligible. Hence, there

is group pressure on individuals to conform to bank rules. [47] Loans are provided for all purposes

at nominal interest rates. The purpose of the loan request is discussed in the group meetings and

the members monitor the use of money to ensure that the loan is repaid. Only if the initial loans are

clears, credit will be extended to other group members. A five member group is considered to be

ideal for peer monitoring. In larger groups, there is a chance of members leaving the monitoring

responsibility to others. Apart from providing credit, the system also encourages the members to

make weekly savings in the form of deposits. This will be held in a savings account for that member.

Grameen Bank also offers the opportunity to purchase an equity share through a group fund. This

offers the members a stake in the bank's operations. [63] Repayment of loans in small chunks is

one of the reasons for the high success rate of this model. [62] Grameen Bank has demonstrated

that the poor are creditworthy and has made micro-credit a global movement. Grameen Bank plays

dominant role in microcredit financial market in Bangladesh. Service charge on credit varies from

10% to 20% at flat method of collection. [64]

2 "Grameen Bank | Bank for the poor - Breaking the vicious ..." 2008. 1 Jun. 2014

<http://www.grameen-info.org/index.php?option=com_content&task=view&id=25&Itemid=169>

32

Cooperative Model

This model is based on the premise that every community has the human and financial

resources to manage their own financial institutions. The members of the cooperative institutions

are those who wish to avail its services. If there is good social capital in the community, a

sustainable cooperative can be set up to provide a variety of services. The ownership and control

of the cooperative will remain with the locals. An example of a successful cooperative organization

in India is the Sahavikasa (meaning development for everyone) or the Cooperative Development

Fund which is based on a savings first strategy. The success of the CDF in Andhra Pradesh led to

the government passing a legislation supporting the flexible functioning of cooperatives in the state.

[62]

Microfinance as Collective Action

The involvement of the locals in microfinance reduces the transaction cost and makes use

of local level knowledge, thereby eliminating risk. We have seen separately how social capital and

collective action can lead to better organization and management of resources, which in turn leads

to development. Microfinance and microfinance institutions offer similar avenue for development.

By organizing regular meetings and collective services microfinance institutions can increase the

social capital in the society. [65] Ostrom et al. [66] have shown that given the right framework to

communicate the members were successful in coordinating actions to improve yield, come to verbal

agreements for implementing the actions and structuring methods to deal with nonconforming

members. Microfinance institutions can provide this framework in a society. By encouraging

regular meetings, microfinance not only improves the social capital for economic transactions but

also offer a platform for the members to communicate. With such regularity creates a culture of

33

conforming to the rules and it reduces the incentive to default from the rules. [67] The Grameen

Bank model requires the group to monitor each other to ensure the appropriate use of the loan

money. The presence of such models will reduce the cost of monitoring and enforcing rules in

common property management analogous to how the presence of organizations will reduce the cost

of capacity building in the community.[58]

How Can Microfinance Impact Rural Development?

Microfinance aims to reduce the information gap in providing financial services to the rural

population. This is done by involving the community in the process so that the members can provide

the information. We saw how community participation has a positive impact on rural development

projects. Microfinance, being community based, has the potential to reach all levels of the society

and provide services to those in need. Failures in multiple rural energy projects have been linked

to lack of community participation and inequality in the society. By inequality, we mean not

involving all sections of the society, especially women of the household. Women are managers of

household energy and are the worst affected by energy shortage. When they are not involved in the

process, it makes it difficult to judge the effectiveness of the program. [68] An analysis by the

Microfinance Exchange in India showed that 90% of the borrowers from microfinance institutions

are women. Newly established microfinance institutions (established after 1995), almost all clients

are women. Even in the microfinance institutions established before 1995 about 85% of the clients

are women. Microfinance has a great reach in the society and can provide financial services to

everyone in a rural community. Microfinance institutions can finance the access to renewable

energy for small and micro enterprises and low income households through location specific

innovative financial schemes. They can raise awareness about the opportunities in investing in

renewable energy and how it can improve the livelihood for everyone in the community.

34

Imai et al. show that the presence of microfinance institutions increases the welfare in the

society and contribute to poverty reduction. [44] The intention of the borrower plays an important

role in poverty reduction outcomes. In models like the Grameen Bank model, where group lending

model is used, the intention and proper use of the loan is monitored by the group members. In

Bangladesh, the presence of microfinance institutions and access to microfinance has resulted in

an increase in household income, generate employment, reduce income disparity and increase

social welfare. [46] Experiences with Central American NGOs have shown improvement in the

economic status and quality of life of microfinance clients due to their continued participation in

personal savings program initiated by the NGOs. [43]

Microfinance & Solar Power

Solar power is a very viable option for off grid rural electrification project. However, like

any renewable energy technology, solar power is also capital intensive and has high upfront costs.

Rural population in developing countries cannot afford such high investments. Hence, there is a

need to mobilize financial resources in order to provide the access to energy. [69] In deploying

solar power systems there are multiple technical, economic, political and social challenges which

have to be overcome. [16] Among other issues like capacity building, maintenance of technology

and community impact, financial issues related to solar power have been regularly discussed in

literature. [9, 11] Traditionally solar power for the poor has always been made available through

donations from the industry or the work of development organizations. However, there has been an

increased interest in developing strategies that enable the rural poor to finance their own needs.

[70] The solar market is limited by the buying capacity of the end user. This scenario can be

changed if the end user is able to finance the purchase of the products. Microfinance due to its

outreach and penetration can play a major role in enabling the poor to finance their energy needs.

35

The local presence enables the microfinance institutions to design appropriate loans where the loan

payments match the existing energy expenditures or income flows. [71] Partnering energy

companies with microfinance institutions offers three important benefits

1. Enables access to energy services for the rural poor

2. Expands the market for energy service companies

3. Improves the operations of the microfinance institutions and expands their client base

Morris et al. suggest that as links improve between microfinance institutions and energy

companies, formal/commercial financial institutions will be more willing to provide loans for

energy services. [72]

Examples of Successful Projects Which Have Used Microfinance to Support Solar Power

Deployment

Innovative Microfinance Schemes Leads to Success in Rural Electrification Projects in

Bangladesh [64]

Bangladesh has developed an economically viable solution for providing electricity to rural

areas where the national grid is difficult or expensive to extend. The Renewable Energy

Development Agency of Bangladesh proposed the use of solar home systems in rural electrification

projects. Solar home system units are well received by small entrepreneurs for lighting and

extending their business hours. The electrification program uses innovative financial schemes to

ensure that energy access is provided to the rural poor. Microcredit programs (MCP) are

implemented by various formal financial institutions (nationalized commercial banks and

specialized banks), specialized government organizations and Non-Government Organizations

(NGOs).

36

The Rural Electrification Board offers a fee for service model where the customers pay a

flat fee for their use of the solar home systems. The systems are owned by the Rural Electrification

Board. The second model is a permanent ownership model which is more popular in remote areas

surrounded by rivers. This model is handled by the Infrastructure Development Company Limited

(IDCOL), established by the Government of Bangladesh. IDCOL offers soft loans of 10-year

maturity, with a 2-year grace period, at 6–8% per annum interest to its partner organizations, who

then loan the money out to the microcredit customers. The microcredit customer pays 20% of the

project cost as down payment and the rest is loaned out by the partner organizations. The loan

period is usually 2-3 years. The repayment is through monthly payments in most cases. The solar

home systems were able to compete with kerosene and the program was accepted by the people.

The solar home system (SHS) program in Bangladesh is considered to be one of the most successful

programs in the world.

The success of SHS program was driven by

● The strong motivation of the rural population to improve the lifestyle

● The existence of infrastructure of microfinance institutions

● Making available facile credit for SHS by Government

● The support of domestic and international institutions.

We see that participation of the people and presence of microfinance institutions which

have helped the rural poor gain access to credit has been instrumental in the success of this program.

Solar Electricity for Rural Development in Dominican Republic [73]

In 1984, Enersol Associates, a non-profit organization from United States were successful

in linking solar power and microfinance to provide electricity in village of Bella Vista in the

37

Dominican Republic. Called SO-BASEC, the Solar Based Rural Electrification Concept model

links PV power with the local institutional resource to provide electricity access to the communities.

Firstly the local were trained in operating and maintaining small scale solar energy equipment. The

locals formed an enterprise which designs and installs PV power system according to the local

need. Enersol Associates worked with NGOs to establish revolving credit programs to enable

financing for solar power system purchases. Local microcredit services do not require collateral or

credit history and it was seen that access to credit increased the percentage of households which

could afford photovoltaic systems. Three year loans were provided at reasonable interest rates to

enable the purchase of PV modules. The installation of solar power had a direct positive impact on

the quality of life in the villages. Forming the enterprise generated jobs in the community. Solar

power was used to provide electricity to schools and health centers. The power supply boosted

small scale cottage industries and other farm related activities. This is an example of a replicable

model which uses microfinance and solar power for development in rural areas.

Some Other Examples