company overview - rns submit on march 2013, and the company's periodic reports subsequently...

TRANSCRIPT

Company OverviewFebruary 2014

DISCLAIMERThis presentation includes statements data, forecasts, goals and Company plans that are "forward‐looking statements“, as defined in the Securities Law ‐ 1968, whose occurrence is not certain and which are not solely in the Company's control. These forward‐looking statements are included, inter alia, in discussions of strategy, objectives, goals, plans, events, future intentions or other information relating to future events or issues whose occurrence is not certain.

By their nature, forward‐looking statements involve risk and uncertainty. Whether the forward looking information occurs or not is affected, inter alia, by risk factors characteristic to the Company's operations and developments in the general environment and external factors which impact the Frutarom Group and its area of activities.

This forward looking information could include facts and data based on the Company's subjective assessment, including with regards to the current status of the Company and its business, the current situation in the industry in which the Frutarom Group operates, macro‐financial facts and information, all as are known to the Company on the date on which this presentation was prepared, some of which were given to the Company by external sources, the content of which was not independently examined by the Company, and therefore the Company is not responsible for their verity.

This presentation must be read together with the Company's periodic and immediate reports, and was not meant to replace the need for study of reports the Company has published, including, inter alia, the Company's periodic report for 2012, published on March 2013, and the Company's periodic reports subsequently published. These reports could include, inter alia, updates to the information regarding the Company's activities or of the forward looking statements appearing in this presentation.

Subject to the requirements of applicable law, the Company does not intend to update any industry information or forward‐looking statements appearing in this presentation, and is not required to publish any additional presentations for its shareholders in future.

It is to be emphasized that the financial estimations included in this presentation are based on figures which were not audited or reviewed by an auditor and therefore the actual results may differ from these financial estimations.

Frutarom’s Foundations

Founded in 1933, Frutarom combined the cultivation of aromatic plantsand flowers with the extraction and distillation of flavors, fineingredients and essential oils.

Frutarom ‐ A Leading Fast Growing Global Flavor and Fine Ingredient House

4

Global company Broad product portfolio Public companyFinancial success

since 2000

•Sales in 145 countries

•15,500 customers • A Top 10 flavor house

•31,000 products•4,000 raw materials

• Innovative pipeline

•Listed on London & TLV Stock Exchanges

•From $13M to approx. $1.2B market cap

•9.6x growth in sales (CAGR 19.1%)**

•11.1x growth in EBITDA***

•13x growth in net profit***

* 2000‐2012* based on Dec 2013 including the acquisitions made in 2013 as if consolidated from 1 January 2013** 2000‐2013 (based on Dec 2013 including the acquisitions made in 2013 as if consolidated from 1 January 2013)*** 2000‐2012

1081 108

197287

425518

618

784

0100200300400500600700800900

Renenue, $M*

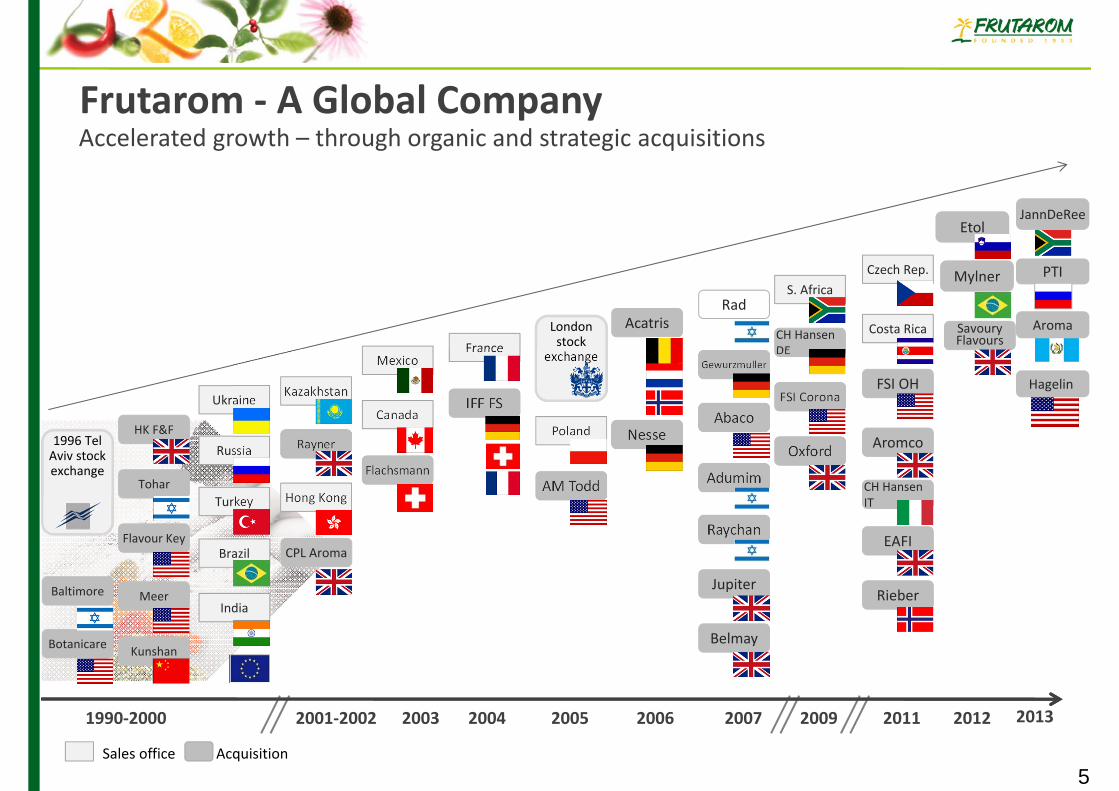

Frutarom ‐ A Global Company

5

Accelerated growth – through organic and strategic acquisitions

Sales office Acquisition

2006 2007 2009 20121990‐2000 2003 2004 20112001‐2002 2005 2013

1996 Tel Aviv stock exchange

IFF FS

Gewurzmuller

Adumim

Raychan

Rieber

EAFI

SavouryFlavours

Oxford

Belmay

Jupiter

FSI Corona

Nesse

CH Hansen DE

CH Hansen IT

Etol

Mylner

Aromco

FSI OH

Acatris

Flachsmann

Abaco

Tohar

Meer

RaynerHK F&F

CPL Aroma Flavour Key

Baltimore

Botanicare Kunshan

AM Todd

Rad London stock

exchange

Russia

Canada

Turkey

France Mexico

Ukraine

Poland

Kazakhstan

Hong Kong

Costa Rica

Czech Rep.S. Africa

India

Brazil

JannDeRee

PTI

Aroma

Hagelin

Sales & Marketing – 79 Offices

Production – 34 SitesR&D – 41 Labs

Frutarom ‐ A Global CompanyWe provide our customers with global and local support

Belgium

Brazil

China

Denmark

France

Germany

India

Indonesia

Israel

Italy

Kazakhstan

Mexico

NetherlandsNorway

Poland

Serbia

Singapore

Slovakia

Slovenia

South Africa

Turkey

UkraineUK SouthUK North

Corona, CA New JerseyCincinnati, OH Switzerland

Moscow Saint Petersburg

Perm Saratov

Hong Kong

Costa Rica

Georgia

Guatemala

NovosibirskBelarus

Moldova

7

Frutarom ‐ A Profitable Growth Story(Sales, EBITDA, Net Profit, USD M)

1996 Tel Aviv stock exchange

IFF FS

Gewurzmuller

Adumim

Raychan

Rieber

EAFI

SavouryFlavours

Oxford

Balmey

Jupiter

FSI Corona

Nesse

CH Hansen DE

CH Hansen IT

Etol

Mylner

Aromco

FSI OH

Acatris

Flachsmann

Abaco

Tohar

Meer

RaynerHK F&F

CPL Aroma Flavour key

Baltimore

Botanicare Kunshan

AM Todd

Rad London stock

exchange

Russia

Canada

Turkey

France Mexico

Ukraine

Poland

Kazakhstan

Hong Kong

Costa Rica

Czech Rep.S. Africa

India

Brazil

JannDeRee

PTI

AROMA

Heglin

Net Profit2000-2012

X13

EBITDA Profit2000-2012

X11.1

Sales2000-2013

X9.6108

8110

197287

425518

618784*

* Dec 2013 including the acquisitions made in FY13 as if consolidated from 1 January 2013

4 6

18

30 33

42

52

914

32

49

66

80

100

1990 2000 2002 2004 2006 2009 2011 2012 2013Proforma

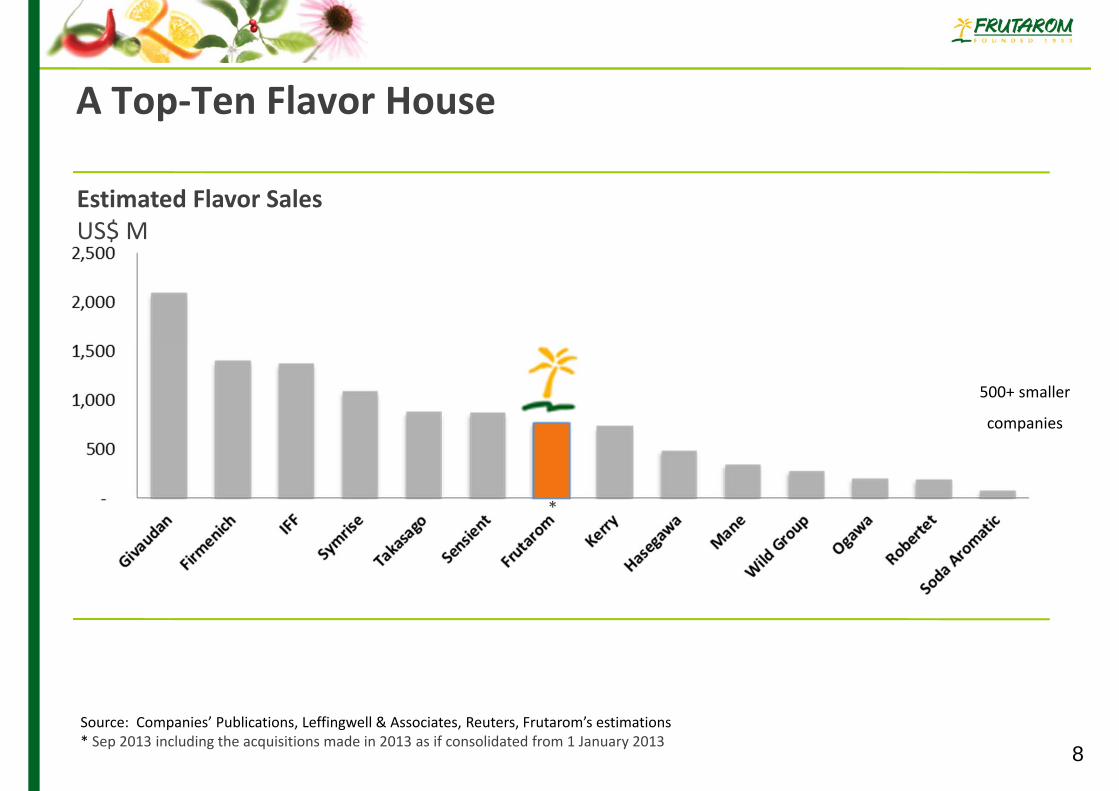

Estimated Flavor Sales US$ M

A Top‐Ten Flavor House

Source: Companies’ Publications, Leffingwell & Associates, Reuters, Frutarom’s estimations * Sep 2013 including the acquisitions made in 2013 as if consolidated from 1 January 2013

8

500+ smaller

companies

*

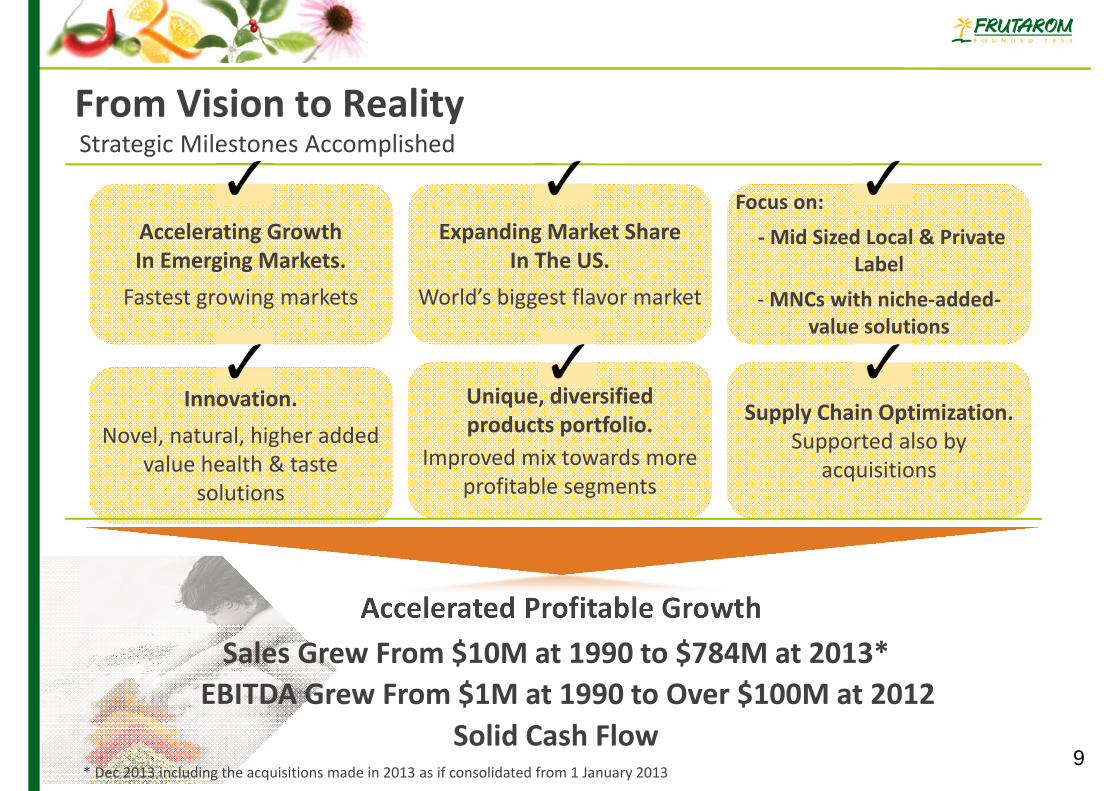

From Vision to RealityStrategic Milestones Accomplished

Sales Grew From $10M at 1990 to $784M at 2013*

Accelerating GrowthIn Emerging Markets.Fastest growing markets

Unique, diversified products portfolio.

Improved mix towards more profitable segments

Expanding Market Share In The US.

World’s biggest flavor market

Supply Chain Optimization. Supported also by

acquisitions

Innovation.Novel, natural, higher added

value health & taste solutions

Focus on:‐Mid Sized Local & Private

Label ‐MNCs with niche‐added‐

value solutions

Accelerated Profitable Growth

Solid Cash Flow * Dec 2013 including the acquisitions made in 2013 as if consolidated from 1 January 2013

EBITDA Grew From $1M at 1990 to Over $100M at 2012

9

Accelerated Growth and Market Share in Emerging Markets

Asia

Central & South America Africa

Central and Eastern Europe

• Acquired Etol in Slovenia and PTI in Russia• One of the only global players with major

production sites in Russia• Market leadership in Central and East Europe• Cross selling and optimization opportunities

• Fast growing operation in South Africa, reinforced by JannDeRee Acquisition

• Enhance R&D and sales force in fast growing markets (Kenya, Nigeria and others)

• Building State of the Art manufacturing facility

• Expanded R&D and sales force in China, Indonesia, Philippines, Thailand, Vietnam, Sri Lanka

• Setting up flavor operation in India• Building a state‐of‐the‐art plant in China with

both savory and sweet flavors capabilities• Evaluating strategic acquisition opportunities

• Acquired Mylner in Brazil and Aroma in Guatemala

• Set up an independent operation in Costa Rica and Mexico

• Evaluating strategic acquisition opportunities

10

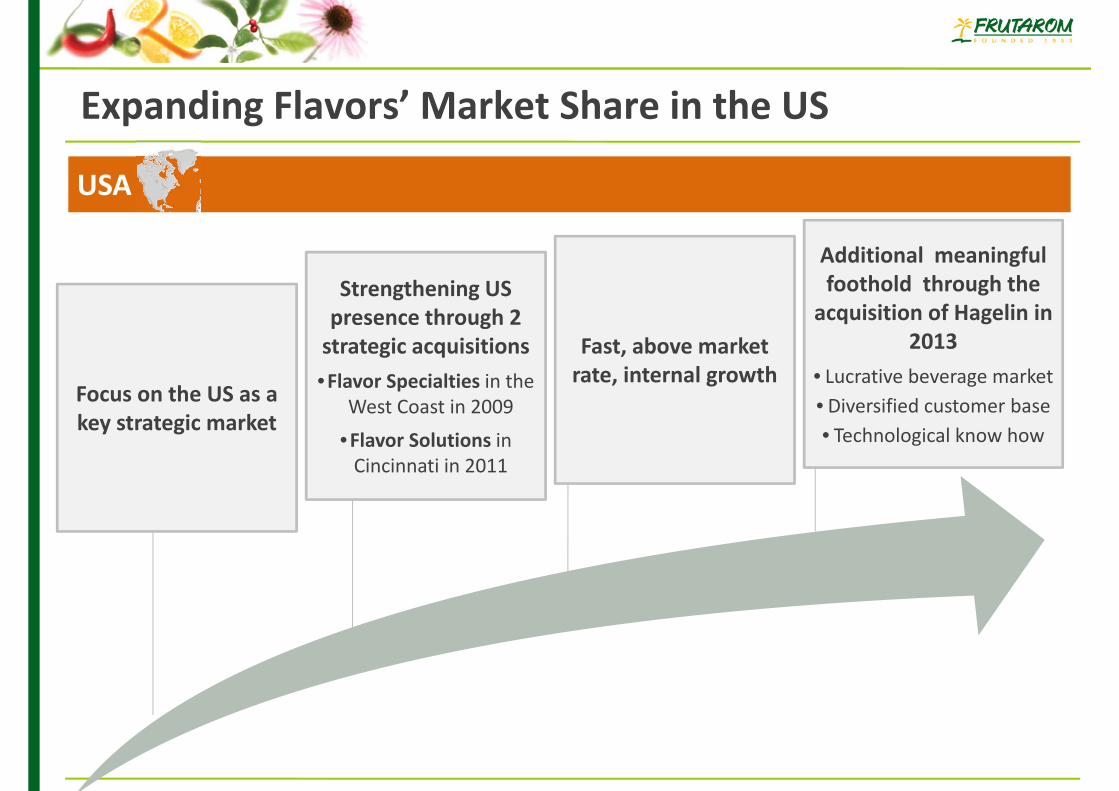

Expanding Flavors’ Market Share in the US

USA

Focus on the US as a key strategic market

Fast, above market rate, internal growth

Additional meaningful foothold through the acquisition of Hagelin in

2013• Lucrative beverage market• Diversified customer base • Technological know how

Strengthening US presence through 2 strategic acquisitions •Flavor Specialties in the

West Coast in 2009

•Flavor Solutions in Cincinnati in 2011

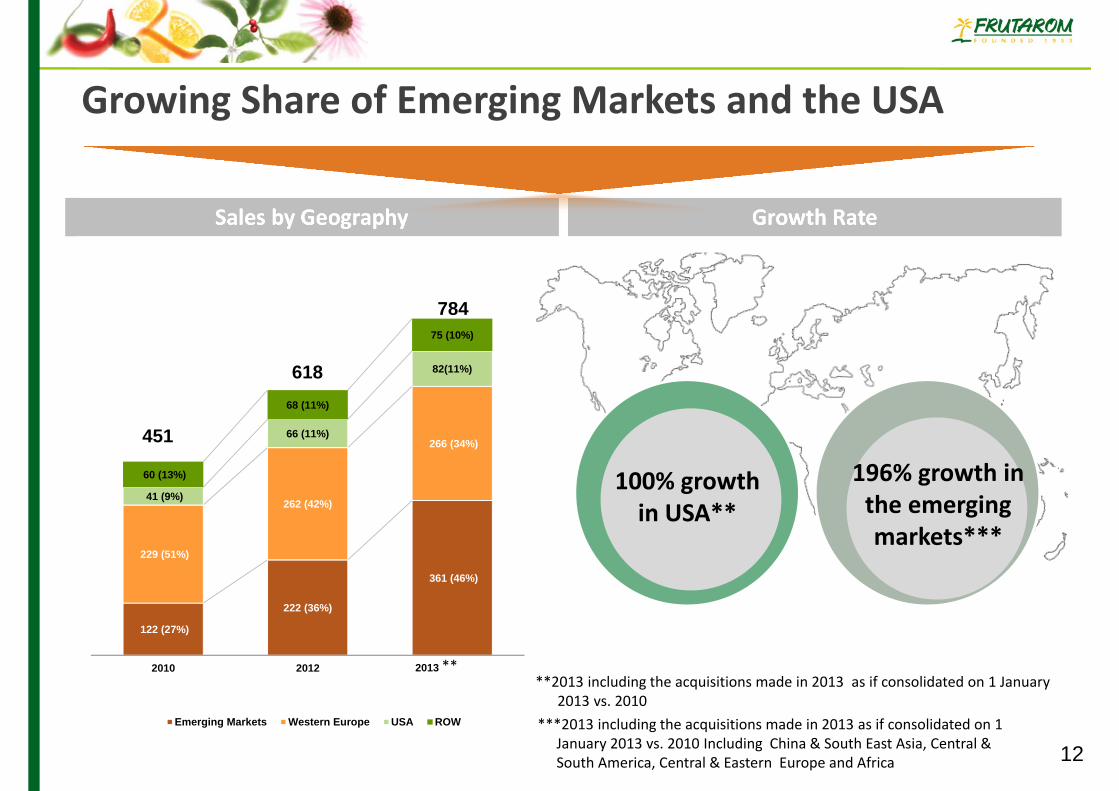

122 (27%)

222 (36%)

361 (46%)

229 (51%)

262 (42%)

266 (34%)

41 (9%)

66 (11%)

82(11%)

60 (13%)

68 (11%)

75 (10%)

2010 2012 2013 Proforma

Emerging Markets Western Europe USA ROW

12

196% growth in the emerging markets***

31% growth in the BRIC countries*

100% growth in USA**

451

618

784

Growth Rate

Growing Share of Emerging Markets and the USA

Sales by Geography

***2013 including the acquisitions made in 2013 as if consolidated on 1 January 2013 vs. 2010 Including China & South East Asia, Central & South America, Central & Eastern Europe and Africa

**2013 including the acquisitions made in 2013 as if consolidated on 1 January 2013 vs. 2010

**

Above‐Industry Organic Growth

Frutarom’s Strategy

Proven Acquisition Track Record

Margin Expansion

13

Reaching revenues of $1 billion

Continue successful strategy of combining rapid profitable organic growth with strategic acquisitions

Achieving 20% EBITDA in our core business, given the current product mix

Fine Ingredients~19% of sales

Taste Solutions~72% of sales

• Unique, high quality creation of sweet and savory flavors for food and beverage products

• Expertise in local and global tastes• Operational flexibility and local global supply chain

• Value‐added functional savory solutions for the food industry (snacks, meat, fish, organic, and culinary segments)

• Comprehensive sweet and savory food systems

• Unique technologies for fruit, spice, vegetable, meat and fish preparations

• Specialty botanical extracts, distillates, essential oils and aroma chemicals

• Innovative, science‐based health ingredients for phyto‐pharmaceuticals, nutraceuticals, dietary supplements, functional foods, cosmetics, and personal care

• Supporting the growing demand forhealth, wellness and beauty

14Trade & Marketing, ~9% of salesStrengthening Frutarom’s partnership and offering to customers

Growing the Core Business

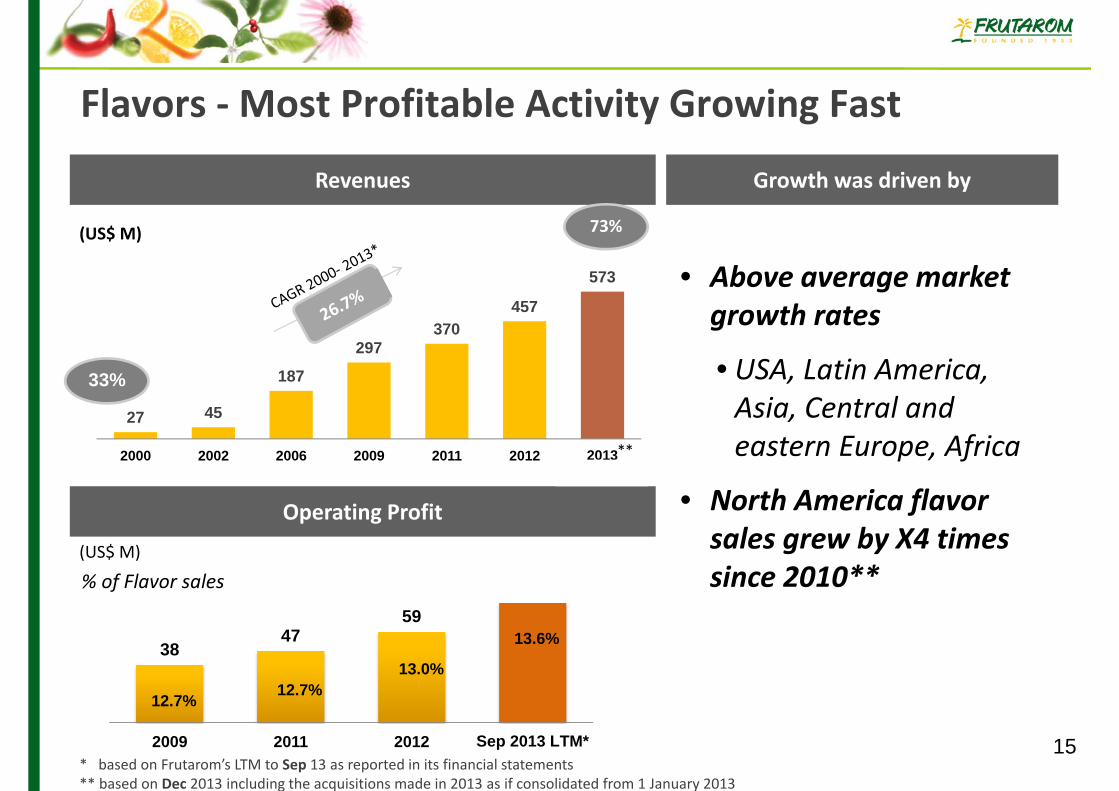

3847

59

2009 2011 2012 Sep 2013 LTM*

Flavors ‐Most Profitable Activity Growing Fast

15

Revenues

(US$ M)

• Above average market growth rates

• USA, Latin America, Asia, Central and eastern Europe, Africa

• North America flavor sales grew by X4 times since 2010**

33%

Operating Profit

Growth was driven by

(US$ M)

14.7%

73%

% of Flavor sales

12.7% 12.7%13.0%

* based on Frutarom’s LTM to Sep 13 as reported in its financial statements** based on Dec 2013 including the acquisitions made in 2013 as if consolidated from 1 January 2013

13.6%

27 45

187

297370

457

573

2000 2002 2006 2009 2011 2012 2013Proforma

**

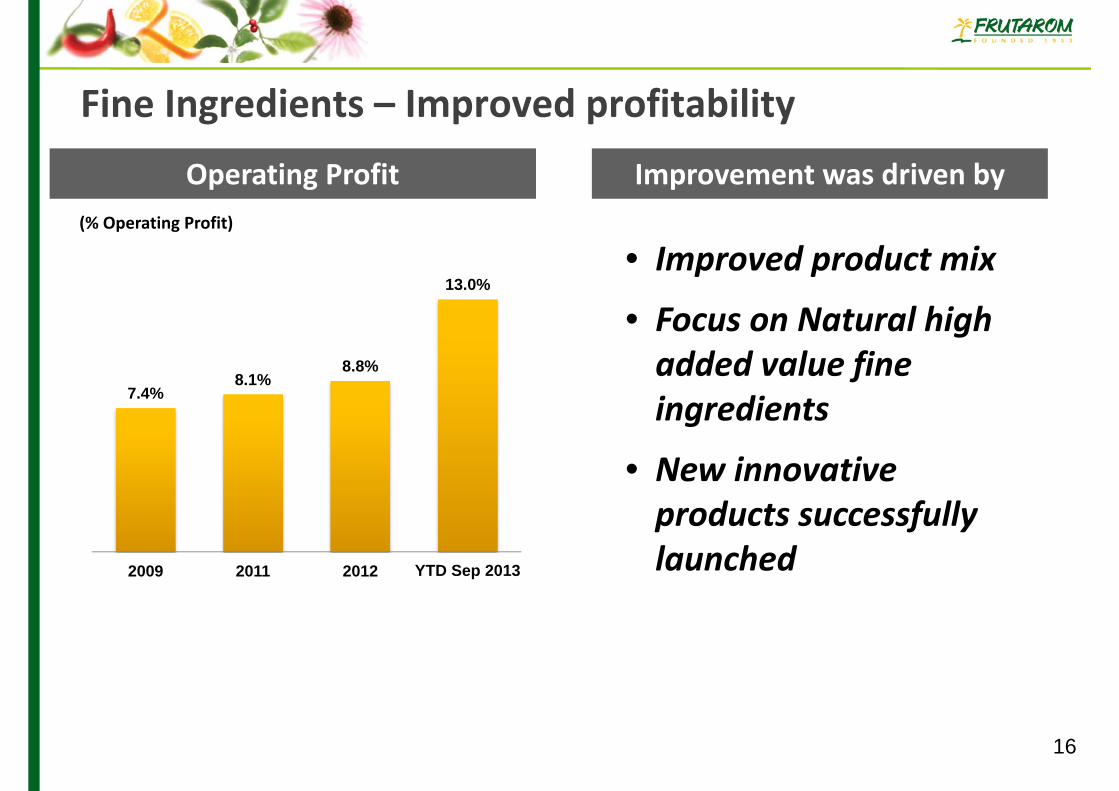

Fine Ingredients – Improved profitability

16

Operating Profit

• Improved product mix

• Focus on Natural high added value fine ingredients

• New innovative products successfully launched

Improvement was driven by(% Operating Profit)

14.7%

7.4%8.1%

8.8%

13.0%

2009 2011 2012 YTD Sep 2013

We share the…

Passion for Taste & Health

Flavors Fine Ingredients

We develop tailored solutions combining excellent taste with health and functionality all under one roof

17

Growing Mid‐Sized Food & Beverage MarketOver 65% of Market Controlled by Mid‐Sized and Local Companies

18

• New mid‐sized/local companies emerging

• Private label• Developing markets

• Service expectations

• Fragmented market

Large (>US$ 10B),

15%

US$3-10B10%

US$1-3B7%

Small & Local (< US$1B)

68%

2012 Total

Market Size$4,600bn

(% of Market Share) The global food market

*Source: Feb, 2012 Datamonitor, Euromonitor and Frutarom’s estimations

F&F Market Fragmented But Consolidating

*Source: Leffingwell & Associates, company’s estimations

(% of Market Share)

Market Share by size2011 F&F Sales*

19

Large (>US$ 1B),

6 Companies65%Mid Size

(US$100-1B)7 companies

17%

Small & Local (< US$100M)

+500 companies

19%

2012 Total

Market Size$23bn

• Large number of small niche companies with limited service capability and regional focus only

• Few mid‐sized players with both regional strength and global platform

• Large F&F players with full service platform, focused ontop multinational customers

Large(>US$ 1B)

6 Companies 64%

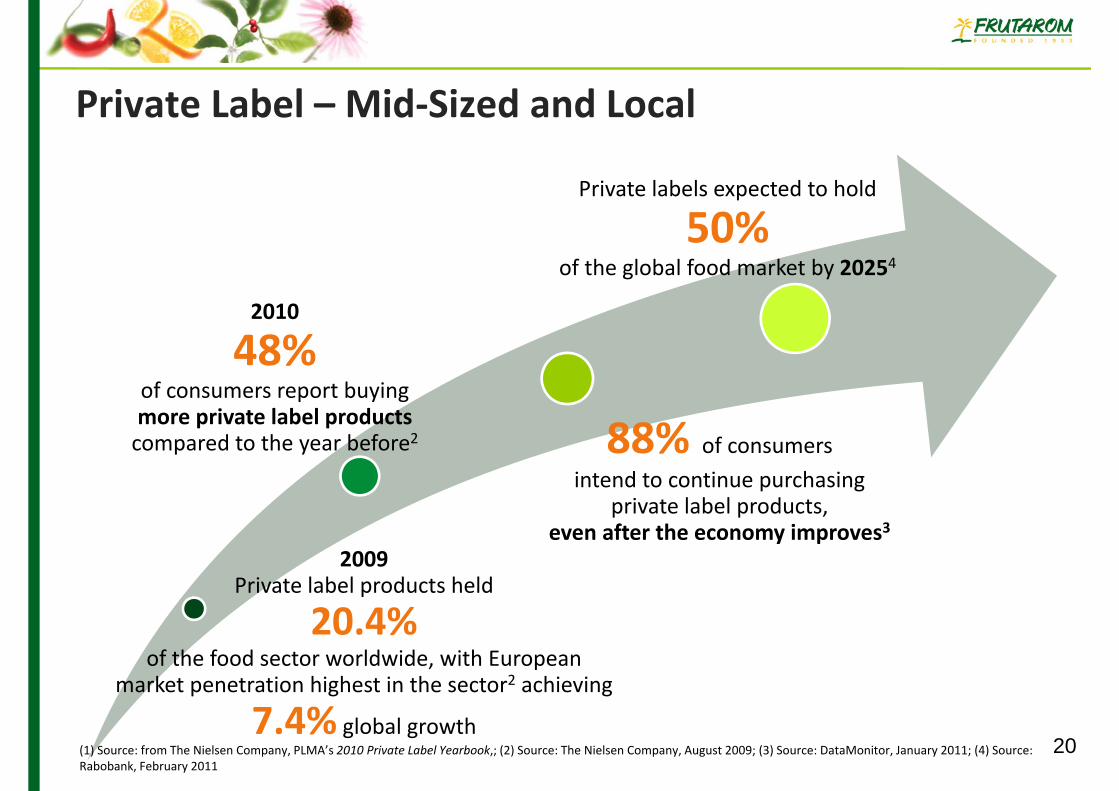

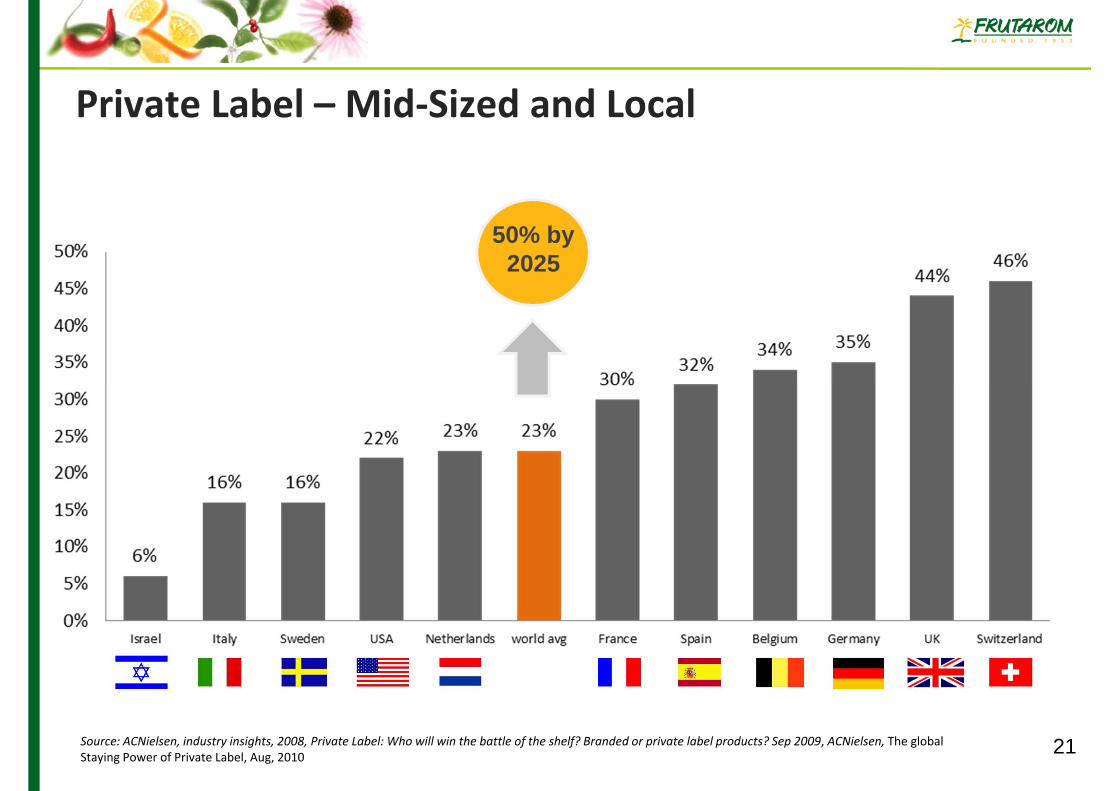

Private Label – Mid‐Sized and Local

2009 Private label products held

20.4% of the food sector worldwide, with European

market penetration highest in the sector2 achieving

7.4% global growth

2010

48%of consumers report buying more private label products compared to the year before2 88% of consumers

intend to continue purchasing private label products,

even after the economy improves3

Private labels expected to hold

50%of the global food market by 20254

20(1) Source: from The Nielsen Company, PLMA’s 2010 Private Label Yearbook,; (2) Source: The Nielsen Company, August 2009; (3) Source: DataMonitor, January 2011; (4) Source: Rabobank, February 2011

Source: ACNielsen, industry insights, 2008, Private Label: Who will win the battle of the shelf? Branded or private label products? Sep 2009, ACNielsen, The global Staying Power of Private Label, Aug, 2010 21

50% by 2025

Private Label – Mid‐Sized and Local

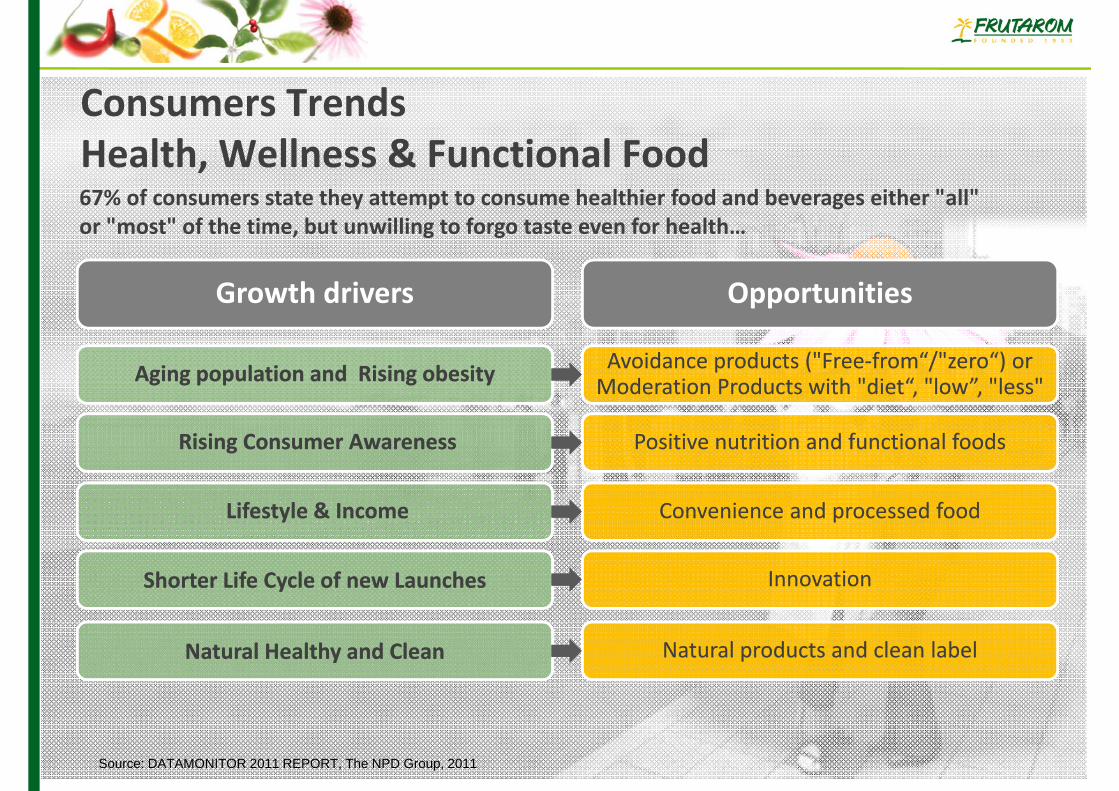

Consumers TrendsHealth, Wellness & Functional Food67% of consumers state they attempt to consume healthier food and beverages either "all" or "most" of the time, but unwilling to forgo taste even for health…

Source: DATAMONITOR 2011 REPORT, The NPD Group, 2011

Growth drivers

Aging population and Rising obesityAging population and Rising obesity

Rising Consumer Awareness Rising Consumer Awareness

Lifestyle & IncomeLifestyle & Income

Opportunities

Positive nutrition and functional foodsPositive nutrition and functional foods

Convenience and processed foodConvenience and processed food

Avoidance products ("Free‐from“/"zero“) or Moderation Products with "diet“, "low”, "less"Avoidance products ("Free‐from“/"zero“) or Moderation Products with "diet“, "low”, "less"

Shorter Life Cycle of new LaunchesShorter Life Cycle of new Launches InnovationInnovation

Natural Healthy and Clean Natural Healthy and Clean Natural products and clean labelNatural products and clean label

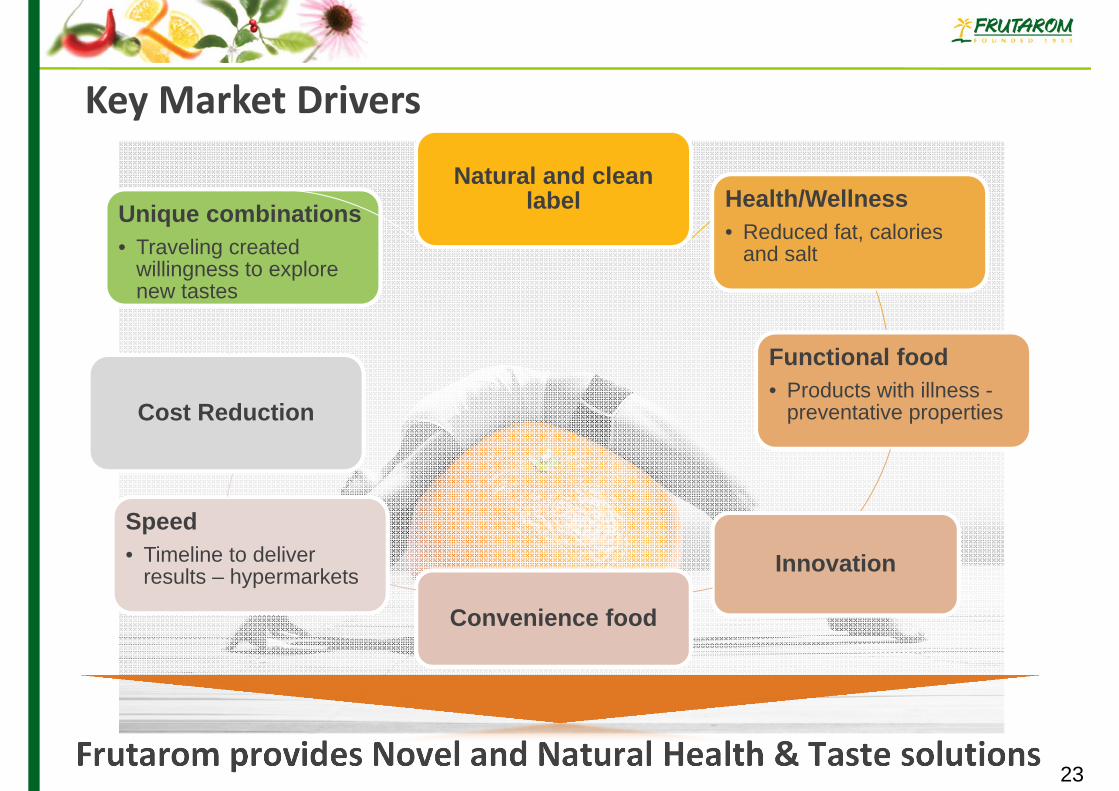

Frutarom provides Novel and Natural Health & Taste solutions

Natural and clean label Health/Wellness

• Reduced fat, calories and salt

Functional food• Products with illness -

preventative properties

Innovation

Convenience food

Speed• Timeline to deliver

results – hypermarkets

Cost Reduction

Unique combinations• Traveling created

willingness to explore new tastes

23

Key Market Drivers

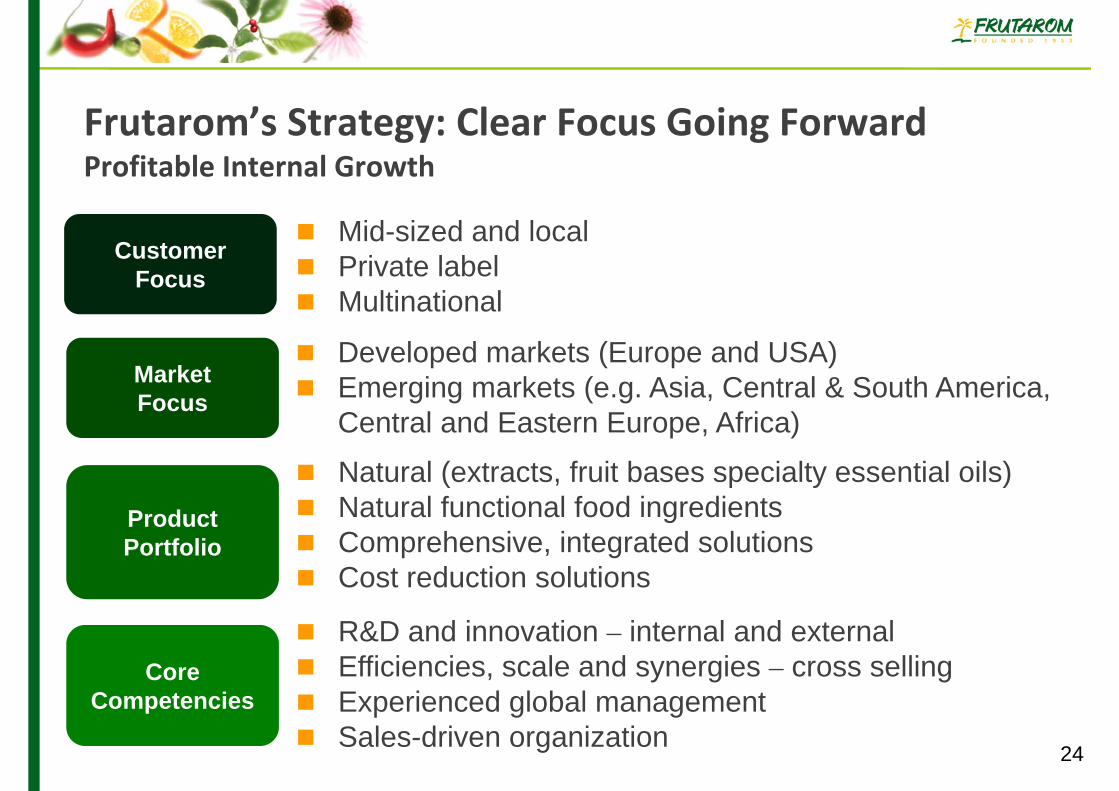

Frutarom’s Strategy: Clear Focus Going Forward Profitable Internal Growth

CustomerFocus

Mid-sized and local Private label Multinational

Market Focus

Developed markets (Europe and USA) Emerging markets (e.g. Asia, Central & South America,

Central and Eastern Europe, Africa)

Product Portfolio

Natural (extracts, fruit bases specialty essential oils) Natural functional food ingredients Comprehensive, integrated solutions Cost reduction solutions

Core Competencies

R&D and innovation – internal and external Efficiencies, scale and synergies – cross selling Experienced global management Sales-driven organization

24

36 successful acquisitions Strict acquisition criteria:

Highly valuable and experienced employees

Major synergies and cross-selling potential

Additional unique products and technology

Positive impact on EPS Focus on integration execution

Optimization of cross selling opportunities

Optimization and harmonizationof resources

Proven Acquisition Track Record

26

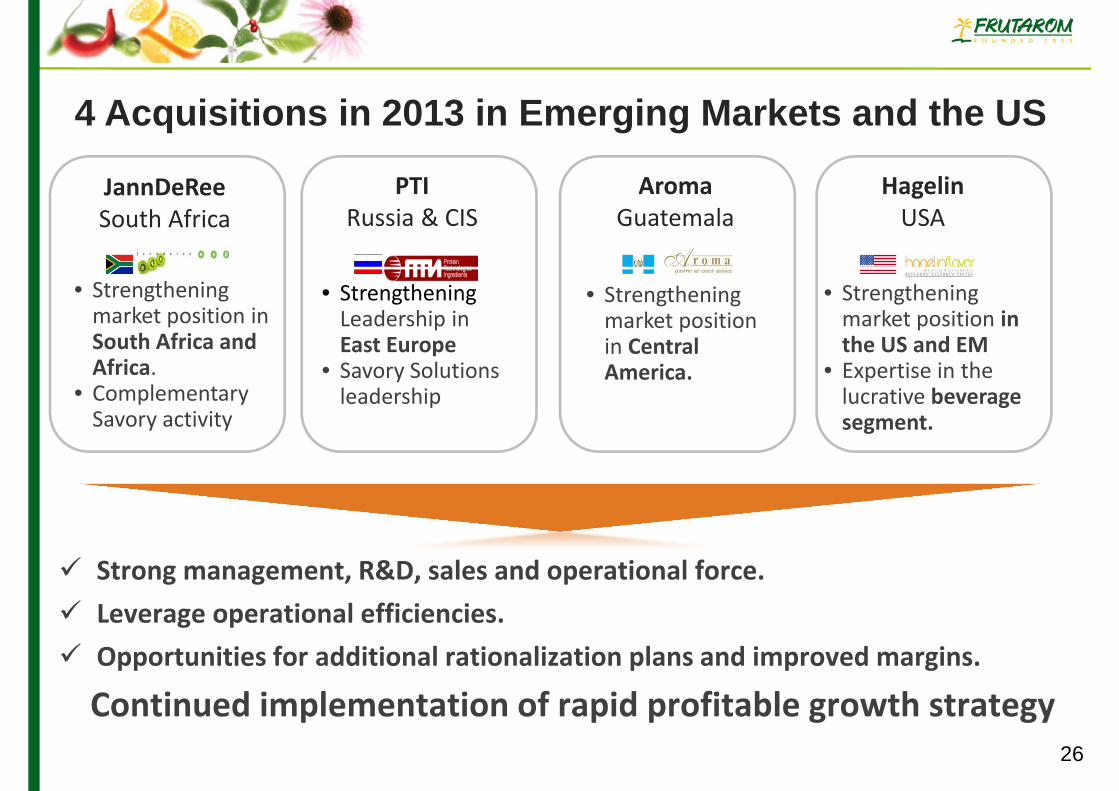

4 Acquisitions in 2013 in Emerging Markets and the US

• Strengthening market position in South Africa and Africa.

• Complementary Savory activity

JannDeReeSouth Africa

PTIRussia & CIS

• Strengthening Leadership in East Europe

• Savory Solutions leadership

Aroma Guatemala

• Strengthening market position in Central America.

HagelinUSA

• Strengthening market position in the US and EM

• Expertise in the lucrative beverage segment.

Strong management, R&D, sales and operational force. Leverage operational efficiencies. Opportunities for additional rationalization plans and improved margins.

Continued implementation of rapid profitable growth strategy

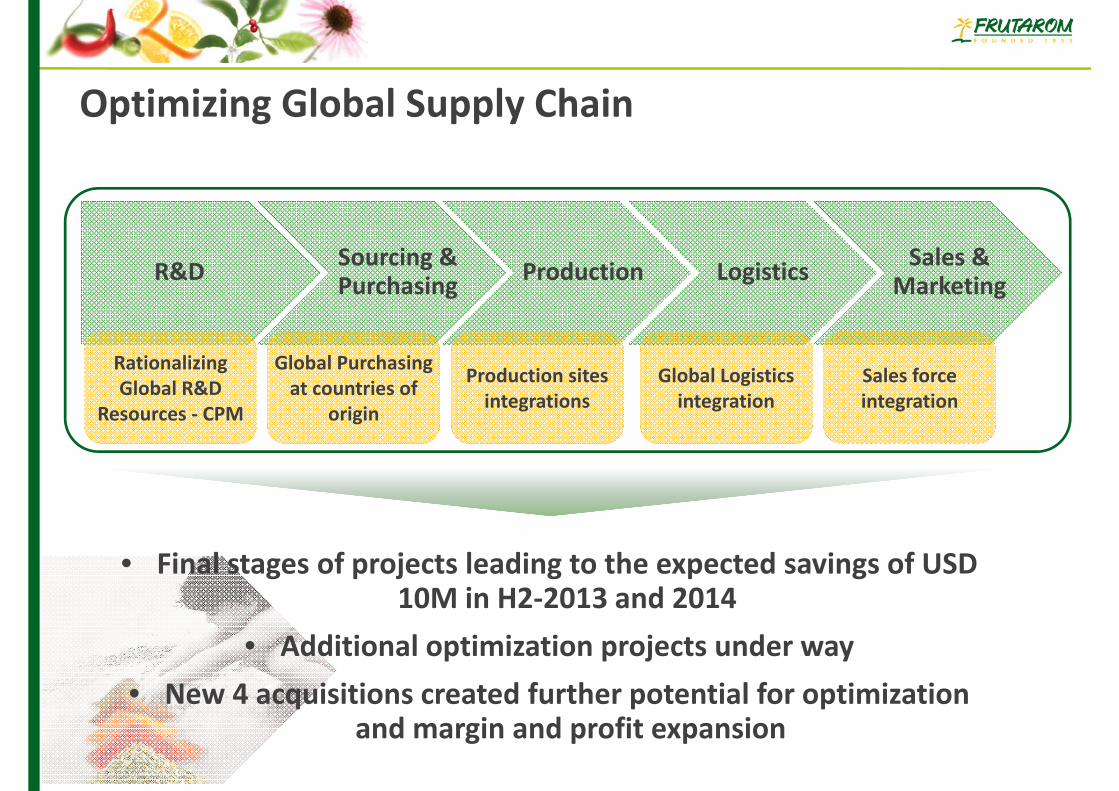

Optimizing Global Supply Chain

ProductionSourcing & Purchasing Logistics Sales &

Marketing R&D

Rationalizing Global R&D

Resources ‐ CPM

Global Purchasing at countries of

origin

Production sites integrations

Global Logistics integration

Sales force integration

• Final stages of projects leading to the expected savings of USD 10M in H2‐2013 and 2014

• Additional optimization projects under way • New 4 acquisitions created further potential for optimization

and margin and profit expansion

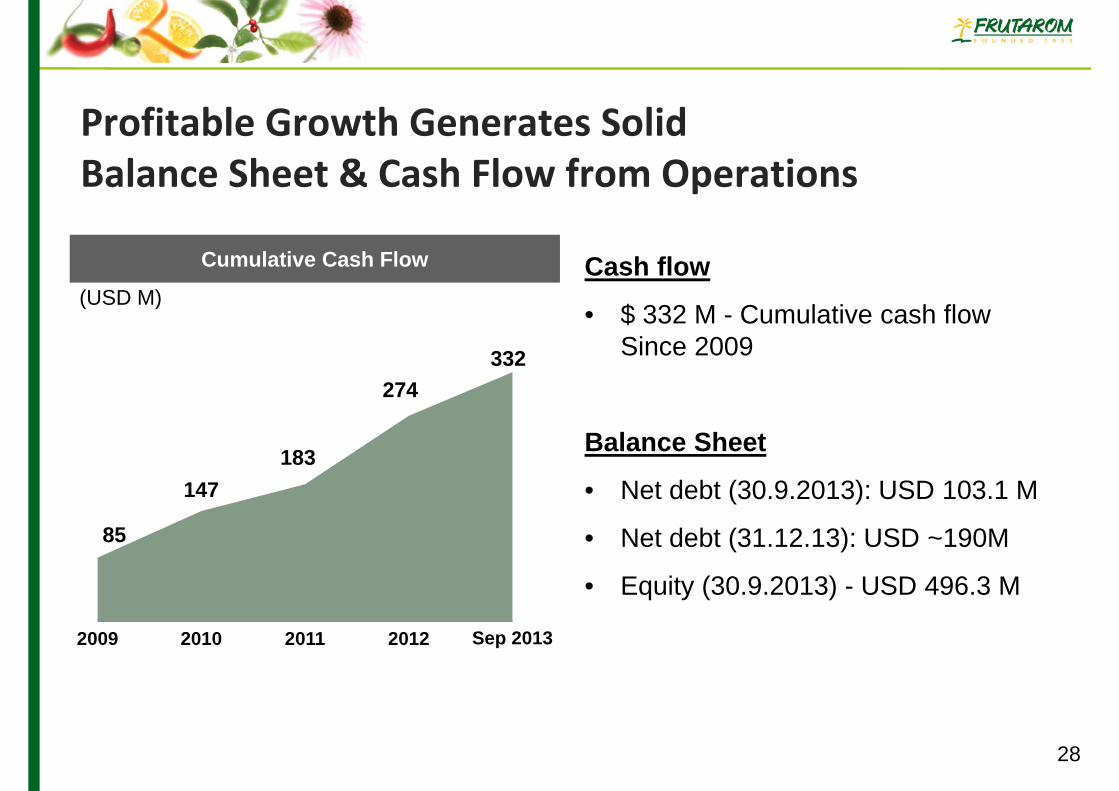

Profitable Growth Generates Solid Balance Sheet & Cash Flow from Operations

(USD M)Cash flow

• $ 332 M - Cumulative cash flow Since 2009

Balance Sheet

• Net debt (30.9.2013): USD 103.1 M

• Net debt (31.12.13): USD ~190M

• Equity (30.9.2013) - USD 496.3 M

Cumulative Cash Flow

28

85

147183

274332

2009 2010 2011 2012 Sep 2013

Positive Outlook for 2014

Profitable internal growth

Focus on innovative natural healthy product mix

Successful integration of the acquisitions

Additional projects to improve efficiency and merge activities and operations

Strengthening & leveraging global purchasing

Strong acquisitions pipeline

29

Frutarom’s Vision

30

To Be The Preferred Partner For Tasty And Healthy Success