comparative political economy of airport infrastructure in the european union- evolution of...

TRANSCRIPT

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 1/20

- 0 -

Working Paper 2007-6

David GillenCentre for Transportation Studies

Sauder School of BusinessUniversity of British Columbia

Vancouver, BCEmail: [email protected]

Hans-Martin Niemeier University of Applied Sciences Bremen

Bremen, Germany

* We are indebted to Christiane Müller-Rostin, Vanessa Kamp and Haibin Huang for excellent research assistance aswell as to students in Transport Economics, Bremen University of Applied Science who assisted with data collection.We also thank David Starkie and Peter Forsyth for useful comments on earlier drafts as well as participants at the

workshop on Comparative Political Economy and Infrastructure Performance: The Case of Airports, MadridSeptember 2006 for comments. In addition we are grateful for constructive and helpful comments from twoanonymous referees. The research was partially funded by the research project GAP (German Airport Performance)supported by the Federal Ministry of Education and Research, Germany and by the Centre for TransportationStudies, Sauder School of Business, University of British Columbia.

Copyright © 2007 by Centre for Transportation Studies

Comparative Political Economy of Airport Infrastructure in the EuropeanUnion: Evolution of Privatization, Regulation and Slot Reform *

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 2/20

1

1. Introduction

Changes to the aviation sector in the EU over the last two decades have been far reaching and haveincluded, among other things, deregulation of the airline service sector, the formation of the EUcommon market, a [recent] signing of an EU-US Open Skies agreement, a gradual move to airport

privatization and a continuing evolution of airport regulation and slot allocation reform. The goal of thispaper is to examine the EU experience with the changes to economic regulatory policy and capacityallocation through slots and their impact on airport operations and economic efficiency. It is difficult toassess changes to airport regulation without also examining privatization initiatives and how they havevaried across European states. We therefore include a brief description and assessment of privatizationplans across member states.1

The shift to more market oriented policies in the ownership and management of airport infrastructurehas reflected a position that airports can improve their cost efficiency and level of service to passengersand airlines under privatization. With the Green Paper on fair and efficient pricing (EC, 1995) theEuropean Commission views airports as part of the general infrastructure that should be priced

according to social marginal costs principles (Frerich, 2004 a, b and 2006). Member states such as for e.g. the UK or Germany have also adopted these principles in their policy papers (Nash, 20002 ).Therefore a key objective for airport policy is that it should promote efficient provision of airportservices. Secondly, there has been a shift to considering regulation or semi-regulatory processes as analternative means of governance for the airport system. There has, for example, been substantialdebate in academic circles of the merits of types of regulation – price cap versus cost based regulationwith single versus dual till systems – and whether there needs to be regulation at all. 3 This view hasbeen taken up by airports that depict themselves as an industry facing significant competitivepressures. Airlines, on the other hand, having substantially cut their costs and fares in the last fiveyears criticize airports for not having achieved similar cuts. They see airports as natural monopolieswhich are not regulated effectively by an independent regulator.

The paper is organized in the following way. We begin with an overview of the EU airport industry andthe changes in traffic over time. We also provide a discussion of legislation which affects airports. Wetake note of the number of airports in member states and their features. Following this is a brief discussion of airport privatization as this leads naturally into the topic of airport regulation. Our purposeis to simply point out what has been happening in the EU and discuss those factors which havehindered greater privatization in the EU. This leads to an examination of the evolution of airportregulation and the distribution of differing types of regulation across member states. In this section thedifferences in single versus dual till price regulation are assessed. The second major topic of the paper is examined next; the evolution of slot allocation is examined and the methods of allocation assessed.In the summary section we take up the question of social marginal cost pricing and how and to what

1 There have been numerous other reforms that have occurred, such as deregulating ground handling andsubstantive changes in airline market structure. These have been driven by a number of factors includingimportantly a policy direction by the EU on introducing policies which focus on improving economic efficiency andcompetition. While these issues are interesting and important they are not discussed in this paper. The EU has28 member states each with their own aviation sector. Despite EU dominance in aviation policy, member statesstill have significant influence over infrastructure policy.2 We interpret the EU policy as an effort ot increase economic welfare by first and second best marginal costpricing. For a more critical view see Rothengatter.(2003)3

The most recent experiences have been to consider the role of ancillary revenue in complement with aviationrevenue in providing an incentive structure to not exercise any monopoly power with respect to on aviationrevenue.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 3/20

2

extent the current governance structures of the airport industry should be reformed to increaseeconomic welfare.

2. The EU Airport Industry

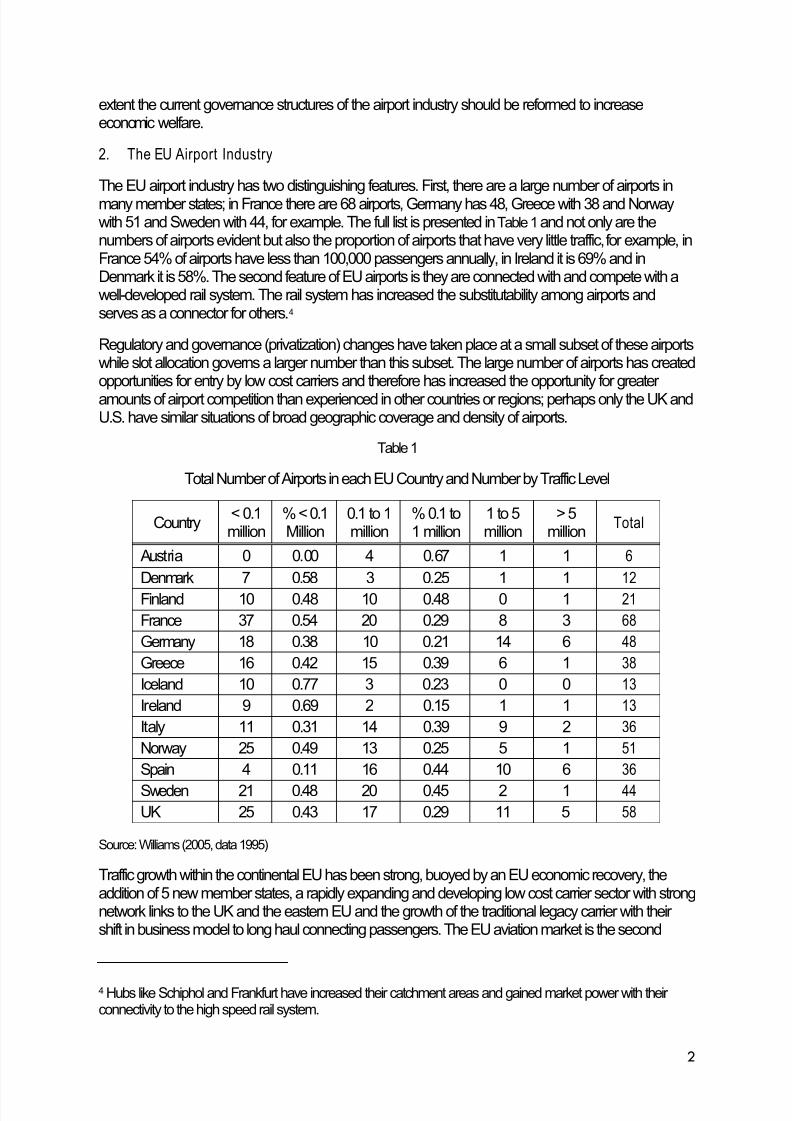

The EU airport industry has two distinguishing features. First, there are a large number of airports inmany member states; in France there are 68 airports, Germany has 48, Greece with 38 and Norwaywith 51 and Sweden with 44, for example. The full list is presented in Table 1 and not only are thenumbers of airports evident but also the proportion of airports that have very little traffic, for example, inFrance 54% of airports have less than 100,000 passengers annually, in Ireland it is 69% and inDenmark it is 58%. The second feature of EU airports is they are connected with and compete with awell-developed rail system. The rail system has increased the substitutability among airports andserves as a connector for others.4

Regulatory and governance (privatization) changes have taken place at a small subset of these airportswhile slot allocation governs a larger number than this subset. The large number of airports has createdopportunities for entry by low cost carriers and therefore has increased the opportunity for greater amounts of airport competition than experienced in other countries or regions; perhaps only the UK andU.S. have similar situations of broad geographic coverage and density of airports.

Table 1

Total Number of Airports in each EU Country and Number by Traffic Level

Country< 0.1million

% < 0.1Million

0.1 to 1million

% 0.1 to1 million

1 to 5million

> 5million

Total

Austria 0 0.00 4 0.67 1 1 6

Denmark 7 0.58 3 0.25 1 1 12

Finland 10 0.48 10 0.48 0 1 21

France 37 0.54 20 0.29 8 3 68

Germany 18 0.38 10 0.21 14 6 48

Greece 16 0.42 15 0.39 6 1 38

Iceland 10 0.77 3 0.23 0 0 13

Ireland 9 0.69 2 0.15 1 1 13

Italy 11 0.31 14 0.39 9 2 36

Norway 25 0.49 13 0.25 5 1 51

Spain 4 0.11 16 0.44 10 6 36

Sweden 21 0.48 20 0.45 2 1 44

UK 25 0.43 17 0.29 11 5 58

Source: Williams (2005, data 1995)

Traffic growth within the continental EU has been strong, buoyed by an EU economic recovery, theaddition of 5 new member states, a rapidly expanding and developing low cost carrier sector with strongnetwork links to the UK and the eastern EU and the growth of the traditional legacy carrier with their shift in business model to long haul connecting passengers. The EU aviation market is the second

4 Hubs like Schiphol and Frankfurt have increased their catchment areas and gained market power with their connectivity to the high speed rail system.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 4/20

3

largest, after the US, common market in the world and growth within and between the EU and other parts of the world have been well beyond forecasts. In 2004, the total number of passengerstransported by air in the EU rose by 8.8%, to 650 million; 24% were carried on national (domestic)flights, 42% on intra-EU flights and 34% on extra-EU flights.5. This considerable traffic growth hasresulted in strains on some airports, most notably the mega-hubs which are reaching capacity limits. In

turn this has led to delays, ‘grey’ markets for slots and pressure to expand capacity, e.g. in Frankfurt. 6

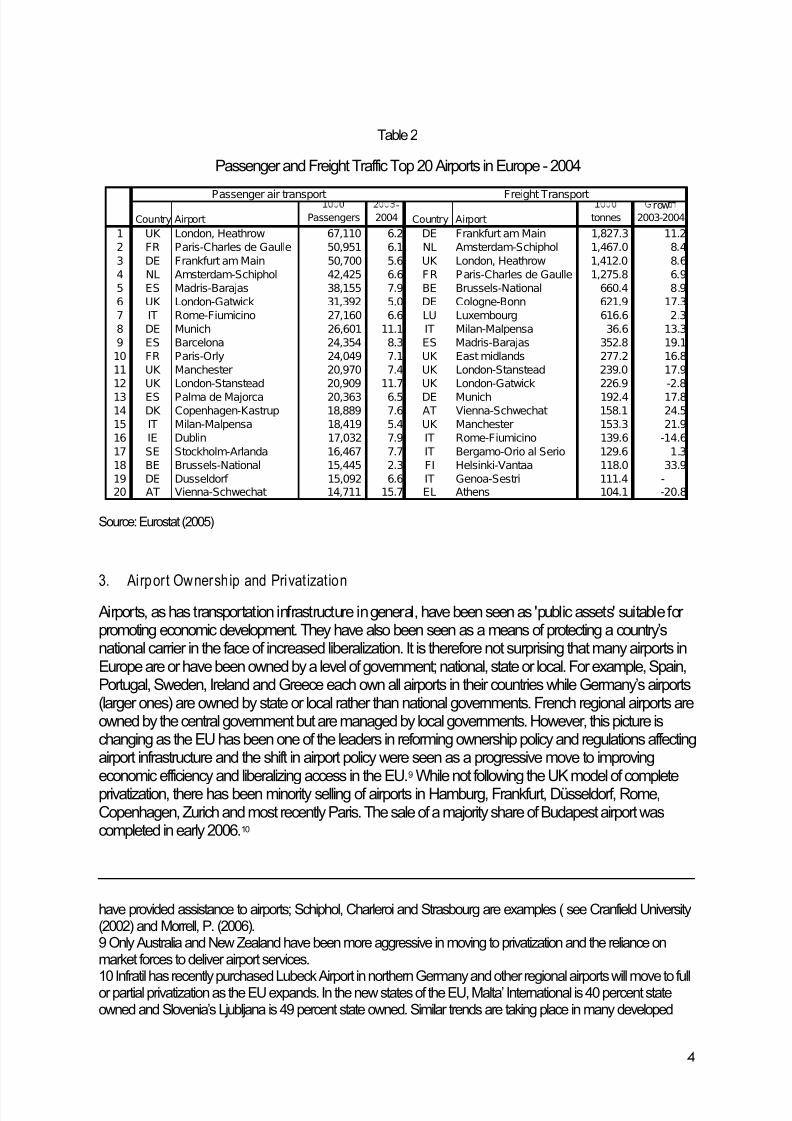

While there are essentially five large hubs in the EU (LHR, FRA, CDG, AMS, MAD, MUN) there are anumber of regional airports varying in size from 27 million passengers at Barcelona to 10 million atHamburg, 10 million at Prague and 7 million at Budapest (all 2004 data). Like the US there are multipleairport groups but unlike the US a group can sometimes include an entire country’s airports, e.g. AENA,a division of the Spanish government, owns and operates all airports in Spain, Finnish Airports group(CAA) owns and operates 25 airports in Finland, LFV (Swedish state enterprise) owns and runs 19airports in Sweden. Airport groups include Aeroports de Paris, Airports de Roma, and the ANA group,which manages all major airports in Portugal.

InTable 2passenger and freight transport numbers, are listed for 20 of Europe’s top airports includingthe growth in traffic from 2003 to 2004.7 It is clear from this table that the growth in passenger traffic hasbeen remarkable and has been spread across Europe and not concentrated at a few airports. Freighttraffic growth has been less evenly distributed reflecting the relative growth in freight carried byintegrators; the significant growth at Cologne-Bonn reflects the developments of UPS at that airport, for example.

Each country in the EU has jurisdiction over airports and can set rules and regulations. However, if anairport wishes to participate in the European Common Aviation area (ECAA) it must adhere to EU law inthe field of aviation. The “Guide to Community Legislation in the Field of Aviation” provides a detailedlist of all legislation, which applies to aviation (European Commission (2006). Such legislation covers

eight areas: economic policy, air traffic management, safety, security, environmental matters, socialmatters, passenger protection, and external relations. The ‘Guide’ makes the point that such legislationis mandatory for member countries, that there is no possibility of filing differences and perhaps mostinterestingly, that economic aspects were of particular importance in developing the policy. The EU air transport policy is a policy for the ‘whole of the transport sector’ meaning all air carriers, airports and air traffic control services.

Article 87 of the Treaty has particular application to airports, as well as carriers. Article 14 and Annex IIIof the ECAA agreement set out the conditions of state aid, specifically such aid was not allowed todistort or threaten to distort competition by favouring agents, undertakings or products. The form of aidmay be grants, interest relief, tax relief, state guarantees and preferential access to state provision of goods and services or purchasing. It could also include restructuring aid and exclusive rightsconcessions. Aid is allowed to be provided under some conditions, such as a regional developmentprogram, but such aid must be available to all parties.8

5. Source: Eurostat (2005)6. The treatment of secondary slot trading in the UK and the EU are quite different and discussed later in thischapter.7 UK airports are included for a more complete comparison.

8 The EU has made a distinction between capital and operating subsidies but they have not balanced thisdistinction across modes or between service and infrastructure. In aviation subsidies can take a number of forms;in Spain (Aena Spanish Airports) loss-making airports are assisted by profitable airports. State governments

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 5/20

4

Table 2

Passenger and Freight Traffic Top 20 Airports in Europe - 2004

Country Airport

Passengers

-

2004 Country Airport

tonnes

row

2003-2004

1 UK London, Heathrow 67,110 6.2 DE Frankfurt am Main 1,827.3 11.2

2 FR Paris-Charles de Gaulle 50,951 6.1 NL Amsterdam-Schiphol 1,467.0 8.4

3 DE Frankfurt am Main 50,700 5.6 UK London, Heathrow 1,412.0 8.6

4 NL Amsterdam-Schiphol 42,425 6.6 FR Paris-Charles de Gaulle 1,275.8 6.9

5 ES Madris-Barajas 38,155 7.9 BE Brussels-National 660.4 8.9

6 UK London-Gatwick 31,392 5.0 DE Cologne-Bonn 621.9 17.3

7 IT Rome-Fiumicino 27,160 6.6 LU Luxembourg 616.6 2.3

8 DE Munich 26,601 11.1 IT Milan-Malpensa 36.6 13.3

9 ES Barcelona 24,354 8.3 ES Madris-Barajas 352.8 19.1

10 FR Paris-Orly 24,049 7.1 UK East midlands 277.2 16.8

11 UK Manchester 20,970 7.4 UK London-Stanstead 239.0 17.9

12 UK London-Stanstead 20,909 11.7 UK London-Gatwick 226.9 -2.8

13 ES Palma de Majorca 20,363 6.5 DE Munich 192.4 17.814 DK Copenhagen-Kastrup 18,889 7.6 AT Vienna-Schwechat 158.1 24.5

15 IT Milan-Malpensa 18,419 5.4 UK Manchester 153.3 21.9

16 IE Dublin 17,032 7.9 IT Rome-Fiumicino 139.6 -14.6

17 SE Stockholm-Arlanda 16,467 7.7 IT Bergamo-Orio al Serio 129.6 1.3

18 BE Brussels-National 15,445 2.3 FI Helsinki-Vantaa 118.0 33.9

19 DE Dusseldorf 15,092 6.6 IT Genoa-Sestri 111.4 -20 AT Vienna-Schwechat 14,711 15.7 EL Athens 104.1 -20.8

Passenger air transport Freight Transport

Source: Eurostat (2005)

3. Airport Ownership and Privat ization

Airports, as has transportation infrastructure in general, have been seen as 'public assets' suitable for promoting economic development. They have also been seen as a means of protecting a country’snational carrier in the face of increased liberalization. It is therefore not surprising that many airports inEurope are or have been owned by a level of government; national, state or local. For example, Spain,Portugal, Sweden, Ireland and Greece each own all airports in their countries while Germany’s airports(larger ones) are owned by state or local rather than national governments. French regional airports areowned by the central government but are managed by local governments. However, this picture ischanging as the EU has been one of the leaders in reforming ownership policy and regulations affectingairport infrastructure and the shift in airport policy were seen as a progressive move to improvingeconomic efficiency and liberalizing access in the EU.9 While not following the UK model of completeprivatization, there has been minority selling of airports in Hamburg, Frankfurt, Düsseldorf, Rome,Copenhagen, Zurich and most recently Paris. The sale of a majority share of Budapest airport wascompleted in early 2006.10

have provided assistance to airports; Schiphol, Charleroi and Strasbourg are examples ( see Cranfield University(2002) and Morrell, P. (2006).9 Only Australia and New Zealand have been more aggressive in moving to privatization and the reliance onmarket forces to deliver airport services.

10 Infratil has recently purchased Lubeck Airport in northern Germany and other regional airports will move to fullor partial privatization as the EU expands. In the new states of the EU, Malta’ International is 40 percent stateowned and Slovenia’s Ljubljana is 49 percent state owned. Similar trends are taking place in many developed

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 6/20

5

Governments have had several motives for privatization, including a desire to stimulate more efficientperformance from their airports. Airports which remain publicly owned are often corporatized, meaningthat they are expected to behave more like private corporations. Privatization can be expected to alter the incentives faced by the airport’s owners. Thus privatization combined with strong incentiveregulation, can be expected to give the owners an incentive to keep costs low and achieve productive

efficiency.

However, privatization is an opportunity for governments to convert fixed assets into cash. While mosteconomists see no particular merit in this, some governments see the additional cash as desirable. Thismotive might explain why governments shelter private airports in many cases from competition11 andeffective regulation, an issue discussed below. Privatization does not necessarily involve higher airportcharges since if the airport remains in government ownership, the government can choose to increasecharges when and if it so desires. If fact, privatization limits the government’s ability to raise morerevenue from its airports, since it involves giving up control over their pricing. Governments will oftenincrease rates and charges just before privatizing their airports- this is their last opportunity to do so.While privatization does not necessarily mean higher airport prices, the co-incidence of the two can

lead many to associate privatization with higher prices.

Airport privatization gained momentum in the 90s with the first wave of privatization of Vienna (share of 27 %) in 1992, Copenhagen (25%) in 1994, Athens (45%) in 1996, Dusseldorf (50%), Rome (45.5%)and Naples (65%) in 1997, Skavsta Stockholm (90 %), Florence (39%), Turin (41 %), Hamburg (36%)and Zurich (50%) in 2000 and finally Fraport (29%) in 2001. The crisis of aviation from 2001 onwardsmore or less broke this wave and only recently has the process seems to start off again with the partialprivatization of Brussels, Budapest, Bratislava, Lübeck, Malta and Paris in 2006.

Very often full privatization is restricted as the former public owners want to secure certain politicalinterests to be guarantied by a golden share or a wide ownership clause. Currently at most airports the

private owner has only a minority stake either in form of a stake of up to 49 % signalling private publicpartnership in roughly equal terms or in form of a minority of less that 25 %. Only the airports of Bratislava, Brussels, Copenhagen, Malta, Vienna (50 % plus 10% employee foundation) are privatelyowned by a majority share. No major airport in Continental Europe has been fully privatized without anyownership restrictions. Only for Ireland, Netherlands and Malta are there strong expectations thatairports will be partially or completely privatized.

Parallel to the privatization process public European airports have changed their governance structureas well. The federal government of Austria for instance has not only sold its 50% stake in Viennaairport but also the 50% stake in regional international airports such as Graz, Innsbruck, Linz to regionaland local administrations (Schneider, 2004, 150). Other countries like the Slovak Republic have donethe same.

In the public sphere, where airports have yet to be privatized, we observe different owners at thevarious levels of the state from the level of the municipality, to the region and up to the central

and developing countries around the world,11 Privatisation has not lead to more airport competition as the examples of BAA and ADP sold under commonownership and the takeovers of Frankfurt with Hahn and the failed takeover of Vienna with Bratislava show. Theprivatization of Bratislava was stopped due to a change in government by the anti monopoly office of the SlovakRepublic in September 2006. Before the takeover was permitted under some conditions by the Austrian catell

office. In early 2006 Erste Bank commented that profits from Bratislava/Kosice will be low but “it is still better topay a high price and receive low contributions thant let a strong competitor grow next door” (2006, p. 1). ErsteBank estimated that the purchasing price of € 525.7mn includes a premium of € 359mn.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 7/20

6

government. At the lowest level, the city government is typically the owner of the airport. In federalstates such as Austria and Germany the regional state also has a share in the airport. In other countriesairports are owned by the central government either fully, or partially. While there seems to be lesschange within the ownership of public airports the owners have adopted new organizational structuresover the past three decades.

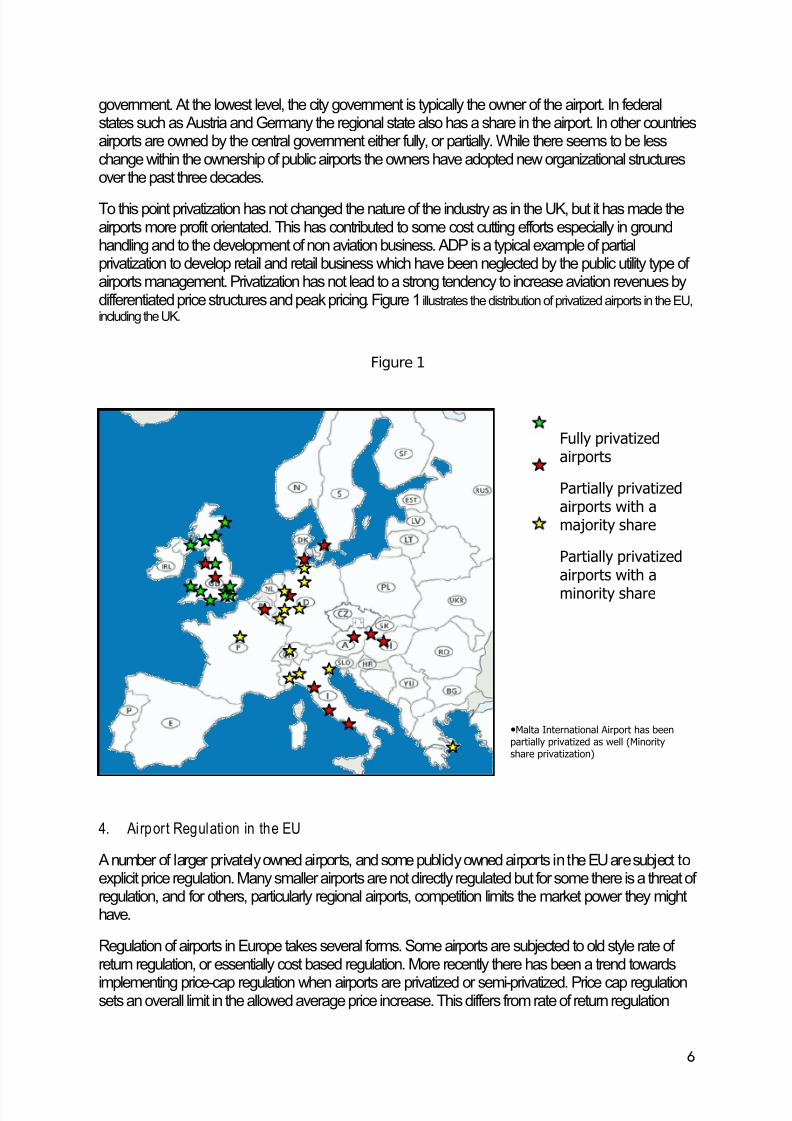

To this point privatization has not changed the nature of the industry as in the UK, but it has made theairports more profit orientated. This has contributed to some cost cutting efforts especially in groundhandling and to the development of non aviation business. ADP is a typical example of partialprivatization to develop retail and retail business which have been neglected by the public utility type of airports management. Privatization has not lead to a strong tendency to increase aviation revenues bydifferentiated price structures and peak pricing. Figure 1 illustrates the distribution of privatized airports in the EU,

including the UK.

4. Airport Regulation in the EU

A number of larger privately owned airports, and some publicly owned airports in the EU are subject toexplicit price regulation. Many smaller airports are not directly regulated but for some there is a threat of regulation, and for others, particularly regional airports, competition limits the market power they mighthave.

Regulation of airports in Europe takes several forms. Some airports are subjected to old style rate of return regulation, or essentially cost based regulation. More recently there has been a trend towards

implementing price-cap regulation when airports are privatized or semi-privatized. Price cap regulationsets an overall limit in the allowed average price increase. This differs from rate of return regulation

Figure 1

Fully privatizedairports

Partially privatizedairports with amajority share

Partially privatizedairports with a

minority share

•Malta International Airport has been

partially privatized as well (Minority

share privatization)

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 8/20

7

which seeks to regulate individual prices.12 Price caps can be regarded as a form of incentiveregulation, though the strength of the incentives varies. The price cap can be under a single or dual tillregime; under a single till all revenues are considered when setting the price cap while in a dual till onlyrevenues derivative from aviation operations (landing, passenger and parking charges) are considered.Some price capped airports are subject to regular cost based resets, and this form of regulation can be

seen as a combination of cost based and incentive regulation (or hybrid regulation).

The single till principle was recommended by ICAO and has been widely used in Europe, but this longtradition is slowly breaking down. The price cap for Hamburg Airport was the first to be set on a dual tillin 2000 on the argument that regulation should be confined to the monopolistic bottleneck andincentives for developing the non-aviation business should not be stifled (Niemeier, 2002). In 2001Malta airport followed with dual till price cap and most recently Budapest airport has adopted a dual tillprice cap for the period 2006 - 2011. Brussels Airport being regulated on a rate of return basis withsome yardstick elements has defined a stepwise move from the single to the dual till over the next 20years. The regulatory framework for ADP sets some mixed incentives to develop non aviation business.One might think that the French government may have an interest to develop this business as this

increases the value of the airport. However, the chosen regulatory framework is a single till with avaguely defined option to take part of real estate and retail income out of the till in the next regulationperiod from 2011 to 2015.13 The differences are mainly due to different degrees of non-aviationbusiness left out of the till.

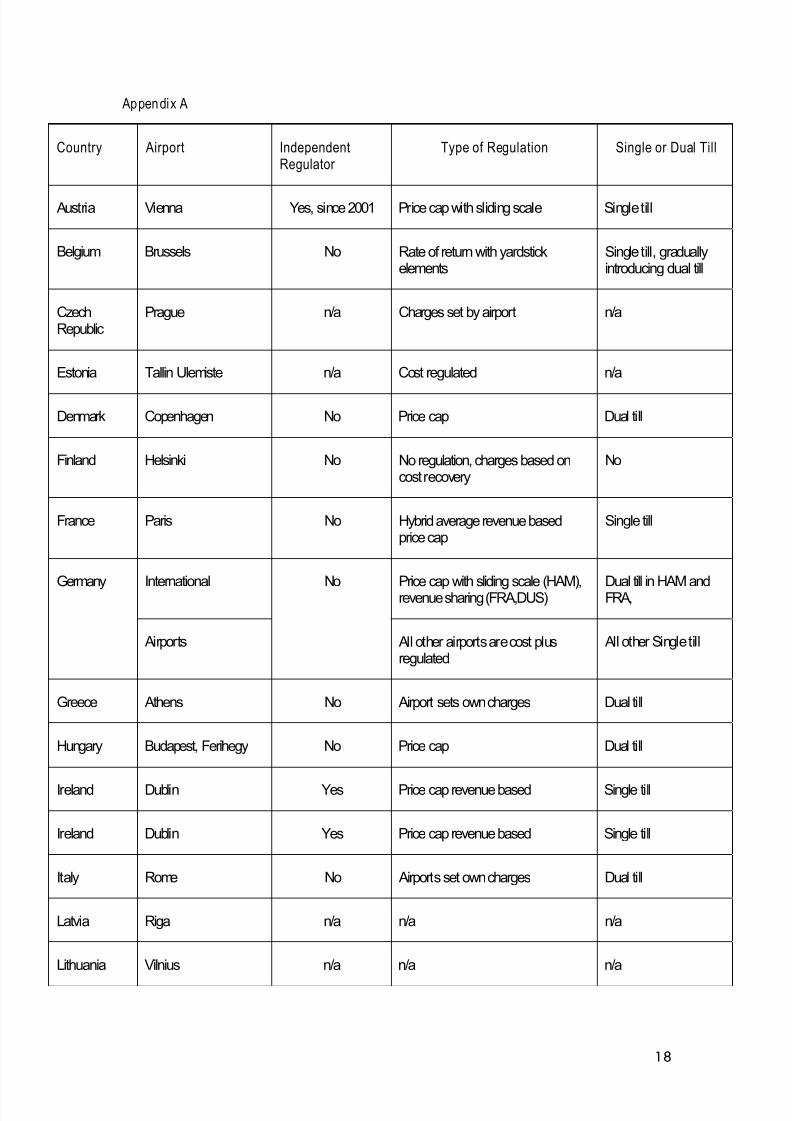

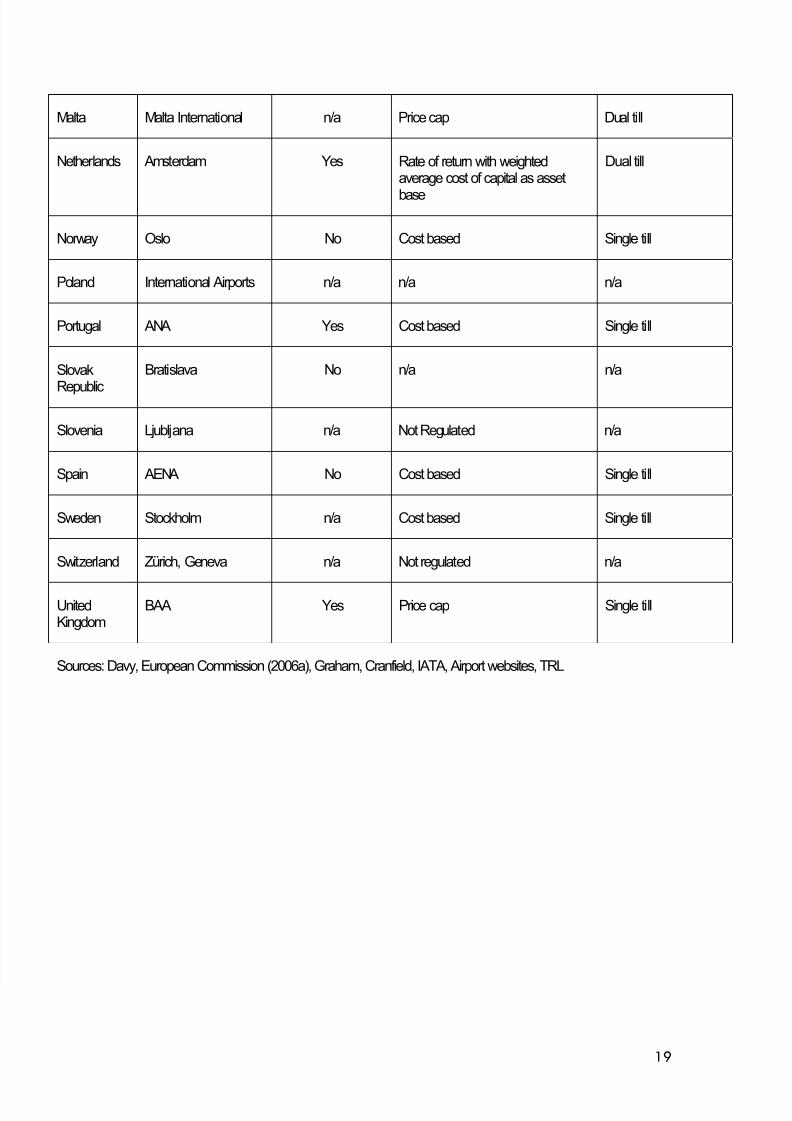

In Europe airport charges have traditionally been regulated on a rate of return or cost plus basis. Wedifferentiate between cost based regulation, pure price caps, hybrid price caps and revenue sharingagreements; a detailed table is contained in Appendix A.

To begin a number of airport authorities regulate airport charges according to principles of costrelatedness. The charges should create just enough revenues to cover total costs including the

depreciation of capital and a normal rate of return on capital. The structure of charges should also becost related, namely each charge should reflect its costs. In Europe many of the public airport systemslike Greece, Poland and Finland set their charges in this way. Charges are supposed to be setaccording to ICAO principles of cost relatedness. CAA’s and Departments of Transport which operateand manage airports directly follow this principle. In the case of formally privatized airports such asmost German airports the regulator approves charges only if they are cost related.

The problems with cost based regulation are twofold. Firstly, the lack of incentives to minimize overallcosts generally leads to an inefficient choice of inputs and secondly, cost based regulation leads to aninefficient price structure (Sherman, 1989). Under cost based regulation the airport has no incentive tominimize costs because if costs go up the airport suffers to loss since industry prices can be increased.Secondly, an airport with peak traffic has no incentive to price efficiently and adopt peak pricing, but“rather to lower the price of capital intensive peak demand in order to justify more capital assets, andcharge a monopoly price at off-peak times to realize a profit that greater capital will justify” (Sherman,1989). The incentives at cost based regulated airports lead to average cost pricing with noconsideration for peak and congestion pricing. Weight related charges are kept even if demandoutstrips capacity at peak times or over the entire day; among the six busiest European airportsDüsseldorf, Frankfurt, Madrid and Paris Orly have weight related charges (Forsyth and Niemeier,2003).

12 Price cap regulation is defined more thoroughly in a subsequent section.13 Morgan Stanley (2006) values the ADP in different scenarios between € 38.1 and € 127.1 per share.-

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 9/20

8

Price cap regulation involves setting an allowed average price increase plus or minus a value ‘X’ where‘X’ is generally some measure of expected productivity growth. The allowed average price increase iscommonly set according to a widely available price index such as the consumer price index (CPI). Thisis referred to the RPI-X formula where RPI is the of price increase’ and ‘X’ is the limiting offset. Thevalue of X is determined by the regulator based on a range of criteria including, for example, whether

the industry is high or low productivity, the performance of the firm in the previous regulated period andwhether the regulator wishes to incentivize the firm to reduce costs.

Unlike cost based regulation price caps do not regulate profits, but set incentives for cost reduction. Thegains from cost reduction can be kept by the regulated airport within the regulation period and mightthen be passed on to the users via lower charges in the next period. Quality might be monitored or regulated since the airport might try to achieve cost reductions by lowering quality. A criticism of pricecap regulation is its short run focus and lack of incentive to invest.

Pure and hybrid price caps differ in the way in which the X in the price cap formula is set; a pure pricecap sets X without reference to the costs of the airport regulated but may set it with reference to a

broad airport benchmarked cost while hybrid price caps set the X with reference to a regulated costbase.14 Hybrid price caps provide fewer incentives for cost reductions. For European airports none of the regulators have developed a pure price capping system. The price caps at ADP, Copenhagen andDublin are based on costs. Most important price cap regulation does not regulate the charging structureaccording to arbitrary cost allocations based on historic costs.

Revenue sharing agreements in the European airport industry often relate the level of charges to thepassenger growth over a certain period. These so called sliding scales can be combined with price capregulation as in the case of Hamburg (Immelmann, 2004) and Vienna. At two German airports Frankfurtand Düsseldorf the revenue sharing agreements are the result of Memorandum of Understandingbetween the airports and its users legalized as a public contract between the airport and regulator

(Klenk, 2004). In case of disagreement the charges would be fixed according to cost based regulations.The core of these contracts is a revenue sharing agreement. The average charge per passenger will bedetermined by the future passenger growth rate. At Frankfurt airport, for example, both parties agreedthat with a projected growth rate of 4% average charges could be raised by 2%cent.15 In the case of ahigher growth rate airlines participate with a 33% share in additional revenues. With lower growth ratesthe airport cannot fully compensate revenue losses through higher charges. Only 33% of the loss canbe compensated. The agreement results in a sliding scale of airport charges that is related topassenger growth.

Such agreements have the important advantage that they break with the tradition of low powered costplus regulation. Within the contract period, the airport may behave as though it is subject to a price cap,

though not of the CPI-X form. Furthermore, at first sight they offer some stability if demand fluctuates. Ademand shock leads to higher charges so that the airport can cover average costs as to avoidbankruptcy, which would undermine the political stability of regulation as well. However, there aredisadvantages. Firstly, in the cases of Frankfurt and Düsseldorf the incentives for cost reduction and for traffic increase are rather mild as the level of charges is stabilized at a high level. It could be that for example Fraport prefers the contract to the cost plus regulation because the rate of return on theaeronautical assets is higher than the normal rate of return accepted by the cost related regulation.

14 Hybrid price cap regulation is superior to cost based regulation because it is forward looking while cost plusregulation relies on historic costs.15 Note that these are nominal prices as the agreement is not related to the price level.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 10/20

9

Secondly, a flat linear sliding scale guarantees the airport nearly the same revenues irrespective of output. This reduces the incentives to differentiate charges and increase output. Thirdly, it usuallycreates an inefficient price structure; fast rising demand leads to lower charges and lower demand tohigher charges.

One key issue surrounding price setting at airports is the independency and transparency as to theinstitution and basis of how rates and charges are set; there is an independent regulator established inonly the Netherlands. Interestingly very often countries are privatizing their airports without avoidingconflicts of interest. In Austria Vienna airport was privatized in three steps in 1992, 1995 and 2001. Upto the last step the central government held a major share and regulated the airport charges. Germanairports are regulated by the federal states that have a minority or majority share in the partial privatizedairports of Frankfurt, Hahn, Hamburg and Hannover (for further discussions see Niemeier, 2002).

A fair, accessible and open process requires as a minimum a consultation process. In the past 15 yearsmore and more European states have implemented a consultation on airport charges and it hasbecome standard practice today. Still there is room for improvement as in most consultation processes

the airports do not provide the necessary information to make a decision on airport charges transparentor plausible to the airlines. The standards of UK regulation which are open even to the general publicare hardly met in continental Europe with the exception of Brussels airport in which the regulator demands a consensus among the airport and its main users. This lack of transparency is clearlyindicated by the recent decision of Lufthansa to acquire a 9.1 % share in their main hub Frankfurt, sothat Lufthansa can obtain a seat on the board of directors in order to be better informed and, by therecent price cap regulation of Aeroports de Paris in which “the value of the regulated asset base andthe percentage return on capital are not disclosed by ADP or the French government (Morgan Stanley,2006, p. 4).16

5. Capacity Constraints and Slot Allocation

Excess demand for airport facilities is evident in the EU as elsewhere. Increasing the capacity of airports is difficult, partly because it is expensive, and partly because such expansion often encountersenvironmental challenges. As a consequence, there are many airports which face excess demand,some for part of the day, and several, like Frankfurt, for all of the day. In the EU capacity at airports isrationed by means of a slot system.

A slot is most commonly known as a landing or take-off right at designated airports during a specifiedperiod of time; the definition of and regulations governing slots is discussed below. The IATA(International Aviation Transport Association) scheduling process is a well recognized means of allocating slots and managing demand at slot coordinated airports around the world including the EU;approximately 213 and all international airlines take part in the scheduling meetings which are held

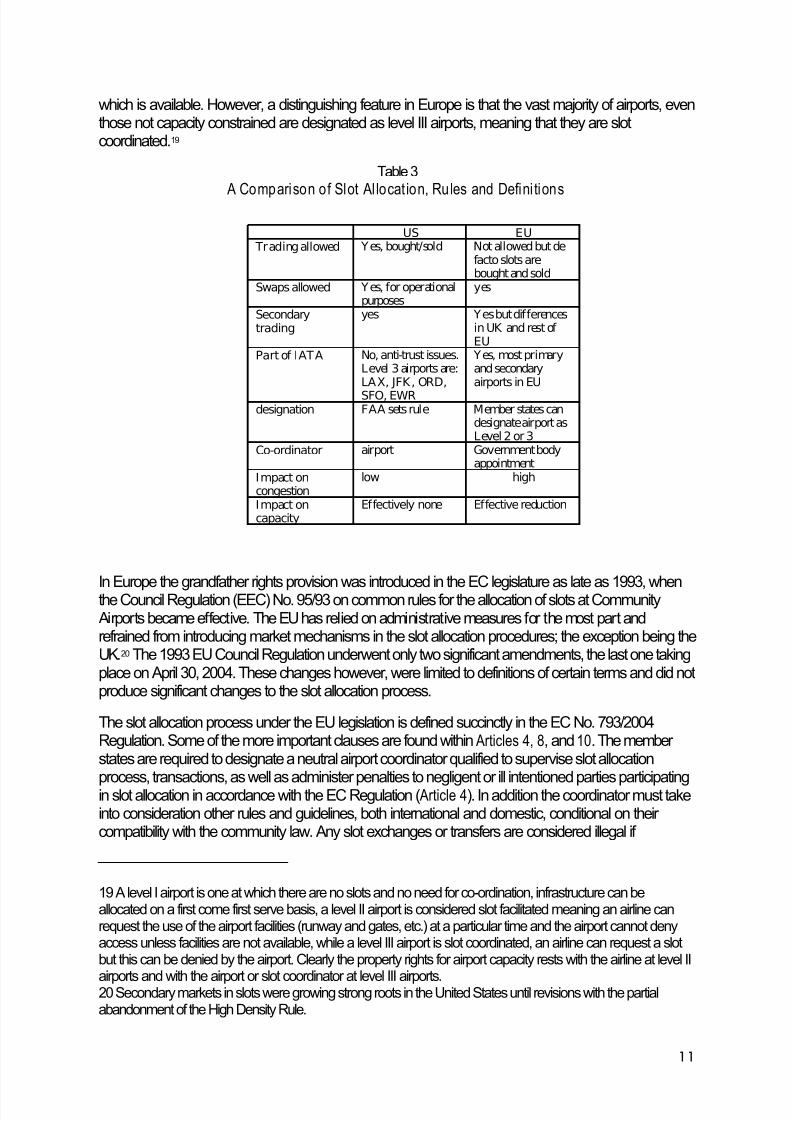

twice per year before the winter and summer schedule is announced. Each slot coordinated airport,defined below, has a slot coordinator (termed ASC – airport slot coordinator) whose appointment variesfrom jurisdiction to jurisdiction (see Table 3 for differences between US, Canada and EU).

16 While it might be very complicated to completely avoid the risk of capture many of the European regulatorysystems which do not separate the functions of ownership and regulation and lack transparency and fairnessseem to be perfect for regulatory capture. It gives the management of the airport the rare opportunity to influencethrough the owner the regulator in various ways which in turn lessens incentives for efficiency and might createrents for management and employees.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 11/20

10

The allocation and trading of slots follows the following process:

z Each airline submits its desired schedule to the ASCs about six months before the start of theseason, and the ASCs then allocate slots according procedures

z The ASCs’ decisions are formally announced at the start of the relevant international conferenceand this is also when airlines first see the planned schedules of their competitors.

z Trading starts, with airlines who did not receive their desired slots seeking to improve their allocations and also ensuring that they have consistent sets of departure and arrival times.

z ASCs provide information showing slot mismatches and who ‘owns’ various slots (brokerage role)z Airlines may trade slots at the same or different airports alter the type of aircraft flown and the

destination (origin) of the flight, subject to the approval of the ASCs.z All trades must be authorized by the relevant ASC to ensure that there is sufficient terminal

capacity and parking space to accommodate any changes.z Trading can be complex, involving many parties in simultaneous swaps of slots.z Any slots not used are placed in a slot pool and the ASC allocates these slots under set rules,

many governing new entrant airlines.

Slots can be obtained from the ASC from the slot pool and through grandfather rights. Slots can be alsobe ‘swapped’ between two or more carriers. This is fairly commonplace among many carriers for scheduling and logistic reasons. Slots can be ‘leased’ which is more attractive than selling as the holder retains control. They are also useful for short-term agreements with early termination clauses. Slots canbe sold but there are relatively few outright sales. There are a number of reasons for this; first, airlinesdo not hold the property rights to slots only the right to use them and therefore slots are treated asquasi-permanent assets with a sizable amount of risk of loss attached. Second, incumbent slot holdersengage in strategic behaviour based on the potential network opportunity costs and knowledge of whom current and potential competitors are. This creates an incentive for hoarding and babysitting.Third, the value of slots is higher as a package than individually—incumbents if selling will want the full

package value of each slot, but potential buyers may not be willing to pay full package value for a singleslot. Slots can also be reallocated due to bankruptcy proceedings, as part of a route transfer betweencarriers, to redeploy slots within an alliance group and to baby-sit surplus slots for current owner.17

Slot allocation using grandfather rights to capacity, mean incumbent airlines which have serviced amarket are given first rights to access airport capacity and generally these rights are provided at nocost.18 Also, generally, slot allocation is reserved for airports at which demand for capacity exceeds that

17 Air carriers operating in the EU depend on two provisions in their choice to service new routes at congestedairports, namely acquisitions of slots from transfers and/or slot pools. After the primary allocation of slots, airlinesare allowed to transfer slots between themselves but only under the supervision of a slot coordinator and under the provisions outlined in Article 8a of the 793/04. Airlines also have access to the slots retrieved by slotcoordinators and placed in the slot pool. The rules governing access to the landing and take-off rights placed inthe slot pool are outlined in Article 8 of the 793/2004. However, some scholars who? have argued these slots donot possess a high commercial value. As a result, in the UK a compensatory grey market has developedwhereby monetary slot transactions are disguised as slot swaps. This situation lead to the EC to conduct aninvestigation into commercial slot allocation mechanisms at EU airports. Other studies that critically assess thecurrent administrative slot allocation policy and potential benefits of market mechanisms include DotEcon 2001,Nera 2004, Task Force 2005, Madas & Zografos 2005.18 Available slot capacity is established twice a year before the allocation of slots at the IATA schedulingconferences. This capacity is declared on the basis of a collaborative decision mechanism, where all parties

concerned examine all factors, technical, operational and environmental, that affect the throughput performanceof airport infrastructure. Once the process of establishing and allocating slots is completed the coordinator isresponsible for monitoring and enforcement.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 12/20

11

which is available. However, a distinguishing feature in Europe is that the vast majority of airports, eventhose not capacity constrained are designated as level III airports, meaning that they are slotcoordinated.19

Table 3

A Comparison of Slot Al locat ion, Rules and Defini tions

US EU Trading allowed Yes, bought/sold Not allowed but de

facto slots arebought and sold

Swaps allowed Yes, for operationalpurposes

yes

Secondarytrading

yes Yes but differencesin UK and rest of EU

Part of IATA No, anti-trust issues.Level 3 airports are:LAX, JFK, ORD,

SFO, EWR

Yes, most primaryand secondaryairports in EU

designation FAA sets rule Member states candesignate airport asLevel 2 or 3

Co-ordinator airport Government bodyappointment

Impact oncongestion

low high

Impact oncapacity

Effectively none Effective reduction

In Europe the grandfather rights provision was introduced in the EC legislature as late as 1993, whenthe Council Regulation (EEC) No. 95/93 on common rules for the allocation of slots at Community Airports became effective. The EU has relied on administrative measures for the most part andrefrained from introducing market mechanisms in the slot allocation procedures; the exception being theUK.20 The 1993 EU Council Regulation underwent only two significant amendments, the last one takingplace on April 30, 2004. These changes however, were limited to definitions of certain terms and did notproduce significant changes to the slot allocation process.

The slot allocation process under the EU legislation is defined succinctly in the EC No. 793/2004Regulation. Some of the more important clauses are found within Articles 4, 8, and10. The member states are required to designate a neutral airport coordinator qualified to supervise slot allocationprocess, transactions, as well as administer penalties to negligent or ill intentioned parties participatingin slot allocation in accordance with the EC Regulation ( Article 4). In addition the coordinator must takeinto consideration other rules and guidelines, both international and domestic, conditional on their compatibility with the community law. Any slot exchanges or transfers are considered illegal if

19 A level I airport is one at which there are no slots and no need for co-ordination, infrastructure can beallocated on a first come first serve basis, a level II airport is considered slot facilitated meaning an airline canrequest the use of the airport facilities (runway and gates, etc.) at a particular time and the airport cannot denyaccess unless facilities are not available, while a level III airport is slot coordinated, an airline can request a slotbut this can be denied by the airport. Clearly the property rights for airport capacity rests with the airline at level II

airports and with the airport or slot coordinator at level III airports.20 Secondary markets in slots were growing strong roots in the United States until revisions with the partialabandonment of the High Density Rule.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 13/20

12

completed prior to the approval of the slot coordinator ( Article 8). Further, in order to ensure competitionis maintained, the service provided by new entrants is protected under Articles 8 and10. For example,section 3c of Article 8a dictates “slots allocated to a new entrant as defined in Article 2(b) may not beexchanged as provided for in paragraph 1(c) of this Article for a period of two equivalent schedulingperiods, except in order to improve the slot timings for these services in relation to the timings initially

requested.”21 Likewise, Article 10 of the EC document ensures new entrants are able to gain access toan airport by allowing the first half of the slot pool slots to service these requests and only subsequentlyare the remaining slots distributed to incumbent airlines.

Two of the major discrepancies in the EC Regulations between 1993 and 2004 pertain to theinterpretation of the words slot and new entrant. In Europe, the word slot means “the entitlement established under this Regulation, of an air carrier to use the full range of airport infrastructurenecessary to operate an air service at a coordinated airport on a specific data and time for the purposeof landing and take-off as allocated by a coordinator in accordance with this Regulation”. 22 23 Another radical change in content relates to the word ‘new entrant’. The 793/2004 regulation expanded thedefinition to include the number of slots held by the air carrier as a percentage of the total number of

slots available on the day in question as a determining factor of whether the party should be labeled asa new entrant. Fundamental differences in the slot allocation process between the EU and US arecontained inTable 3.

The acquisition of slots through monetary exchanges is restricted in Europe where the movementtowards market-based mechanisms for the allocation of scarce airport resources has demonstrated agreater dependency on administrative instruments. This reliance on administrative rules in mainland EUcould be partly attributed to the economic integration of the European Union (EU) – having a simplecommon allocation mechanism - and also to the fear of airline competition being compromised shouldentry at an airport be left unregulated. As a result the European Commission (EC) exercises thegrandfather rule24 for the initial allocation of slots or otherwise known as the primary market. In the EU

slot trading is allowed in secondary markets but not slot sales; the UK has had an active slot tradingmarket since 2001.25However, in Europe, the secondary slot market is restricted to slot swaps only.Nevertheless, a recent staff working document developed by the European Commission in 2004exemplifies serious deliberations of market forces outcomes by the regulatory authorities.26

There are two recurrent themes amongst scholars and regulators with respect to the grandfather rulecriterion (See DotEcon 2001, Nera 2004, Task Force 2005, Madas & Zografos 2005. The first atteststhat the grandfather rights ordinance stifles competition and nurtures inefficiency in the airline industry. Although incumbent airlines, upon failure to fulfill the requirements of the 80/20 rule, are subsequentlyobligated to relinquish the relevant landing and take-off rights to the slot coordinator in order to beplaced in the slot pool, some argue air carriers have an incentive to strategically utilize these slots even

if it would be unprofitable to do so; this practice, is known as ‘slot hoarding’..

Naturally, this translates

21 Ibid.22 Regulation (EC) No. 793/2004 of the European Parliament23 Note that in contrast to the FAA definition which refers only to runway use, the EU definition does not limit aslot to mean a period of time set aside for the use of the runway space but it also considers the infrastructureneeded to complete an arrival or a take-off at an airport and the exchange of passengers.24 If a slot is used 80% of the time in the previous season by an air carrier the party is entitled to the same slot inthe following season.

25 Slot swaps occur in a number of countries where airports are slot constrained and are26 Commission of the European Communities, Commission Staff Working Document, Brussels, 17.9.2004http://europa.eu.int/comm/transport/air/rules/competition2/doc/2004_09_17_consultation_paper_en.pdf

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 14/20

13

into a crippling effect on the ability of new entrants to countervail the market power of incumbentairlines.27

The alternative view maintains the regularly observed slot abuses, against which better safeguards arerecommended, are not the result of anti-competitive behaviour but rather examples of “the business

environment in which airlines are required to operate” (Bauer 2005). Some of these inefficiencies whichare generally cited as airline misconduct include ‘late hand-backs’ and ‘no-shows’. Firstly, owing to theuncertainty associated with receiving the corresponding slots, it could be argued airlines are compelledto hold on to these assets, sometimes past the return deadline, while they wait for confirmation for landing rights at other airports. Secondly, no-shows could occur due to negligence and intentionalwrong-doing, but both are punishable by the slot legislation. However, these events amount to aninsignificant 0.5% of total capacity and a solution to eliminate this behaviour would not greatly improvecapacity utilization (Bauer 2005).

Presently there are several unfavourable characteristics of the EU grey market that could be correctedthrough legalization. The slots are traded mostly among the members of each alliance and as alliances

expand so does the effortlessness to maintain this cycle. The lack of a public notice for each intendedsale or purchase means many potential buyers and sellers are excluded from the trading table.Furthermore, the uncertainty that accompanies the events in the grey market, especially amongstforeign air carriers, has lead to acquisitions of the entire business of airlines. In response to the fear expressed by policy-makers over legalization of the grey market, the EU Competition Authority arguesthe extant competition law is sufficient to correct or prevent anti-competitive behaviour, such as intra-alliance transactions and slot hoarding, which would have a far greater chance of being correctlyapplied if the monetary slot transactions were not shrouded in secrecy. The consequence of relying onslot allocations based principally on grandfather rights is there are no signals to either allocate scarceairport capacity or to indicate how much and what type of investment in new capacity should beundertaken.28

6. Summary and Conclusions

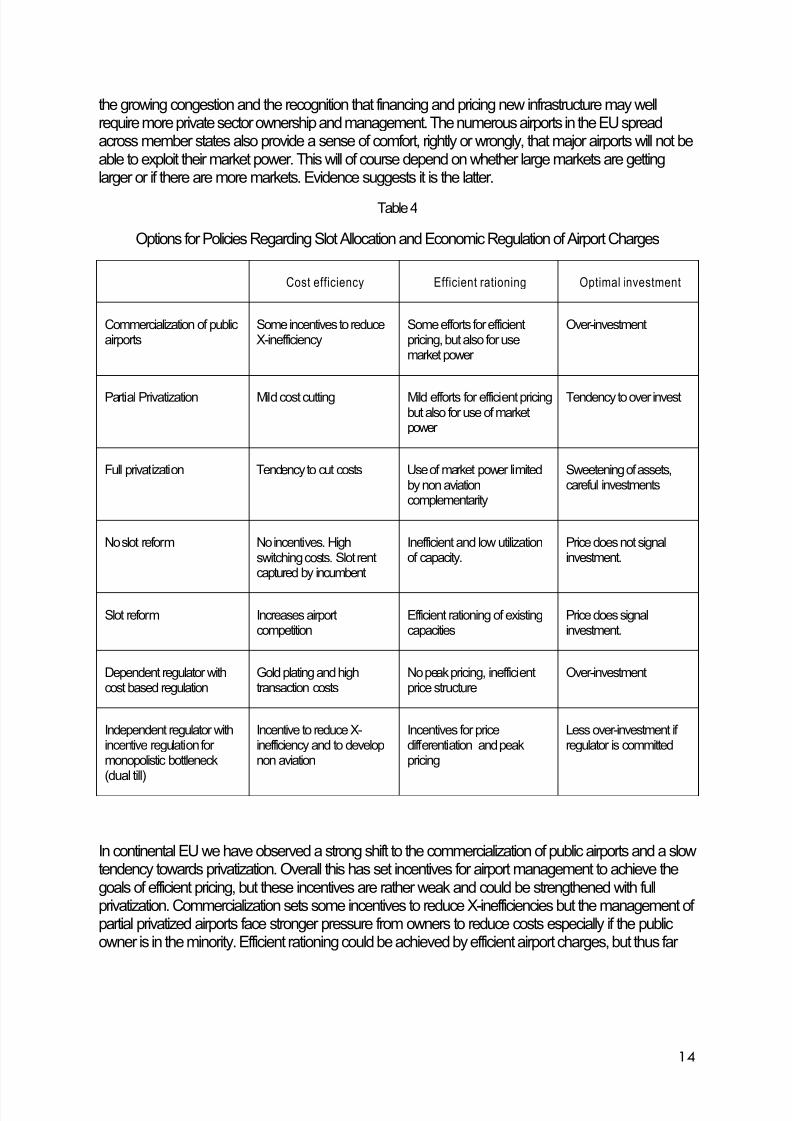

This paper has examined three key areas in airport management and policy in the EU; privatization,regulation, and slot allocation and management. It analyzes the major trends of economic andinstitutional change over the last two decades. These changes raise two fundamental policy questions.Firstly, will the goal of fair and efficient pricing be achieved given the current trends of aviationliberalization, privatization and competition? If so, the major policy reforms of European aviation wouldbe deemed to be successful. However, if the current trends do not move in the direction of achievingthe goals major policy reforms are necessary in order to increase efficiency of the system. This leads toa second question; what are the options for policies regarding slot allocation and economic regulation of airport charges? These questions are summarized in Table 4. It summarizes the trends and tendenciesof the changing governance on cost efficiency, efficient use of airport capacity, and optimal investment

The EU has been one of the leaders in moving to greater privatization coupled with regulatory changes.The underlying forces for this shift in governance lie in several areas and include an integration of aviation policy into general transport policy and the movement of transport policy to rely on competitionlaws to discipline the behaviour of firms rather than rely on government ownership. There is in addition

27 http://www.garsonline.de/downloads/slots%20Market/031107-matthews.pdf 28

The secondary markets at airports in the UK has improved efficiency of slot use but discouraging thedevelopment of such markets in mainland Europe has led to inefficient airport resource use and less effectivegrey markets.

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 15/20

14

the growing congestion and the recognition that financing and pricing new infrastructure may wellrequire more private sector ownership and management. The numerous airports in the EU spreadacross member states also provide a sense of comfort, rightly or wrongly, that major airports will not beable to exploit their market power. This will of course depend on whether large markets are gettinglarger or if there are more markets. Evidence suggests it is the latter.

Table 4

Options for Policies Regarding Slot Allocation and Economic Regulation of Airport Charges

Cost efficiency Efficient rationing Optimal investment

Commercialization of publicairports

Some incentives to reduceX-inefficiency

Some efforts for efficientpricing, but also for usemarket power

Over-investment

Partial Privatization Mild cost cutting Mild efforts for efficient pricingbut also for use of marketpower

Tendency to over invest

Full privatization Tendency to cut costs Use of market power limitedby non aviationcomplementarity

Sweetening of assets,careful investments

No slot reform No incentives. Highswitching costs. Slot rentcaptured by incumbent

Inefficient and low utilizationof capacity.

Price does not signalinvestment.

Slot reform Increases airportcompetition

Efficient rationing of existingcapacities

Price does signalinvestment.

Dependent regulator withcost based regulation

Gold plating and hightransaction costs

No peak pricing, inefficientprice structure

Over-investment

Independent regulator withincentive regulation for monopolistic bottleneck(dual till)

Incentive to reduce X-inefficiency and to developnon aviation

Incentives for pricedifferentiation and peakpricing

Less over-investment if regulator is committed

In continental EU we have observed a strong shift to the commercialization of public airports and a slowtendency towards privatization. Overall this has set incentives for airport management to achieve thegoals of efficient pricing, but these incentives are rather weak and could be strengthened with fullprivatization. Commercialization sets some incentives to reduce X-inefficiencies but the management of partial privatized airports face stronger pressure from owners to reduce costs especially if the publicowner is in the minority. Efficient rationing could be achieved by efficient airport charges, but thus far

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 16/20

15

commercialization and privatization has not resulted in peak and congestion pricing.29 Privatization alsosets strong incentives to raise charges as management objectives shift from ensuring service andaccess to maximizing shareholder returns, albeit with regulatory constraints in most cases.

In our view the key elements of policy reform in the EU are the question of economic regulation of

airports and slot reform.30

EU policy could leave regulation as it is or demand substantial changes. Weexamined dependent and independent regulators. A dependent regulator with cost based regulation wefound has led to x-inefficiency and gold-platting, inefficient price structures with no peak pricing andoverinvestment. It appears the prevailing system of European airport regulation is not only setting theincentives too low, but in the wrong direction. Airport pricing does not reflect the relative scarcity of airport and airway resources and this might distort airline competition and lessen the welfare gains of liberalization.

On the other hand, with an independent regulator with incentive based regulation and dual till, we findthere is an incentive to reduce x-inefficiency and to develop the complementary non-aviation businessrevenue. There are incentives for price differentiation to increase traffic and to manage demand through

peak pricing. Underinvestment might occur but can be prevented by a committed regulator.The current debate on reform of charges and slots is a sign of intensified conflict between airlines andairports (IATA 2005, ACI, 2006). Slot allocation will not go away even with airport expansion; there willalways be a need to have some basis of allocation. Issues of equity, efficiency and competition are allintertwined in such methods of allocation. The [continental] EU clearly favours administrative rules anddespite a growing grey market in the EU argues slot trading is not appropriate for improving the system.This approach would seem to protect incumbent, particularly current or former, national carriers. TheEU slot coordinators have stated they feel the current system is working and the issue is more one of fine tuning and adding capacity than a wholesale change in the IATA approach; the IATA processprotects status quo, entrenches incumbents, is anti-competitive, and is generally blocking effective

entry. However, the DG of the EU Competition Authority has indicated they, the Competition Authority,favours a shift toward market mechanisms. As a replacement of the grandfather rule, some measuresmight completely redefine the initial allocation of slots through the creation of an ongoing andanonymous primary market, such as slot auctions.

The move to policy and regulatory reform for airport infrastructure in the EU was driven by many forces.The move to privatization was important for airports but underlying this was a move to moreshareholder value focused owners. Regulatory indecision was stimulated by the lack of agreement onregulatory principles or even recognizing the problem associated with regulation. Governments alsosaw airports as cash cows and permitting higher charges. There was a growing awareness by airlinesand IATA that airlines were paying a good deal more than they should for airport services. There were‘glacial’ moves to reform slot trading and generally a lack of interest in making efficient use of theexisting capacity. There have been very few moves to improve decision-making over investment.

29

As in other jurisdictions, efficient pricing is opposed and challenged by airlines as monopolistic behavior.30 Of course, this is not sufficient for social marginal cost pricing as the internalization of externalities should betackled by the appropriate environmental instruments, but this is a different topic

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 17/20

- 16 -

References

ACI (2006), Understanding Airport Business, URL: http://www.aci-europe.org/

CAA (2002) Competition Commission Current Thinking on Dual Till - CAA statement onprocess Press Release, 13 August 2002, London, www.caa.co.uk.

CAA (2001) Heathrow, Gatwick, Stansted and Manchester Airports Price Caps - 2003-2008:CAA Preliminary Proposals - Consultation Paper , London, www.caa.co.uk

Commission of the European Communities, Commission Staff Working Document: Commercialslot allocation mechanisms in the context of a further revision of Council Regulation (EEC)95/93 on common rules for the allocation of slots at Community Airports, September 17, 2004

Council of the European Communities, Council Regulation (EEC) No. 95/93 on Common Rulesfor the Allocation of Slots at Community Airports, January 18, 1993 http://europa.eu.int/eur-lex/lex/LexUriServ/LexUriServ.do?uri=CELEX:31993R0095:EN:HTML

Council of the European Communities, Regulation (EC) No. 793/2004 of the EuropeanParliament and of the Council, Official Journal of the European Union :April 21, 2004http://europa.eu.int/eur-lex/pri/en/oj/dat/2004/l_138/l_13820040430en00500060.pdf

Cranfield University (2002), Study on Competition between Airports and the Application of State Rules, Study for the EU- Commission, Brussels

Davy European Transport & Leisure (2004), Late arrival: A Competition Policy for Europe`s Airports, Dublin, Davy Research Department

DotEcon, Auctioning airport slots, A Report for HM Treasury and the Department of the

Environment, Transport and the Regions, 2001

European Commission, Activities of the European Union: Summaries of Legislation,http://europa.eu.int/scadplus/leg/en/lvb/l24085.htm

European Commission (2006), Guide to Community Legislation in the Field of Aviation, ReportIssued for Director General Energy and transport, May 2006 http://europa.eu.int

European Commission, Transport Directorate (1995) Towards Fair and Efficient Pricing inTransportation, Policy Options for Internalizing The External Costs of Transport In theEuropean Union

Erste Bank (2006), Flughafen Wien, Company report, April 11 2006, www.erstebank.at

Eurostat (2005),http://epp.eurostat.ec.europa.eu/portal/page?_pageid=1090,30070682,1090_33076576&_dad=portal&_schema=PORTAL

Federal Aviation Administration, Reservation System for Unscheduled Arrivals at Chicago’sO’Hare International Airport, Vol. 70, No. 130, [July 8, 2005]

Forsyth, P and Niemeier H-M., (2003) Price Regulation and the Choice of Price Structures atBusy Airports, paper given at the Air Transport Research Society Conference, Paper for the Air Transport Research Society Conference, Toulouse, France, 2003

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 18/20

17

Graham, A. (2004), Managing airports: an international perspective, 2nd edition AmsterdamElsevier

IATA (2005), Airport Privatisation, www.iata.org

IATA, Worldwide Scheduling Guidelines, 12th Edition: December, 2005http://www.iata.org/NR/ContentConnector/CS2000/SiteInterface/sites/whatwedo/scheduling/file/fdc/WSG-12thEd.pdf

Immelmann, T. (2004), Regulation in Times of Crisis: Experiences with a public-private pricecap contract at Hamburg Airport in: Gillen, D, Forsyth, P., Knorr, A., Mayer,O. G., Niemeier, H-M. and Starkie, D. (editors), The Economic Regulation of Airports - Recent Developments in

Australasia, North America and Europe, Aldershot, Ashgate forthcoming

Klenk, M (2004), New Approaches to Airline/Airport Relations: The Charges Framework for

Frankfurt Airport, in Forsyth, P., Gillen, D., Knorr, A., Mayer, W., Niemeier, H-M. and Starkie,D., (ed.), The Economic Regulation of Airports, German Aviation Research Society Series, Aldershot, Ashgate,

Madas M., Zografos K., (2005), "Practical Implementation of Airport Demand Management:From Instruments to Strategies", 84th Transportation Research Board Annual Conference,Session on "Management and Analysis of Airport Demand and Delay", Airfield and AirspaceCapacity and Delay Committee, 10 January, Washington, U.S

Morgan Stanley, (2006), Aeroports de Paris Attractive Catlysts… But in 2010, July 31, London

Morrell, P. (2006), Airport Competition and Network Access? A European Perspective (mimeo,Cranfield University)

National Economic Research Associates, Study to Assess the Effects of Different Slot Allocation Schemes: A Final Report for the European Commission, January 2004http://europa.eu.int/comm/transport/air/rules/doc/2004_01_24_nera_slot_study.pdf

Nash, C. (2000), Transport and the Environment, in Helm, D (ed.), Environmental Policy,Oxford, OUP, p 241-259

Niemeier, H.-M. (2002) Regulation of Airports: The Case of Hamburg Airport – a View from thePerspective of Regional Policy, Journal of Air Transport Management, Vol. 8, pp. 37-48.

Rothengatter, W. (2003), How good is first best? Marginal cost and other pricing principles for

user charges in transport, Transport Policy 10, 121-130

Sherman, R. (1989) The Regulation of Monopoly, Cambridge UK, Cambridge University Press.

Transport Research Laboratory (2005), Review of Airport Charges, Wokingham

Task Force, Outcome of Study on Slot Allocation Procedures, European Civil AviationConference, December 7, 2005, DGCA/124-DP/6

Williams, G. (2005), A Comparison of Airports in the EU, Research paper, Cranfield UniversityDepartment of Air Transport

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 19/20

18

Appendix A

Country Airport IndependentRegulator

Type of Regulation Single or Dual Till

Austria Vienna Yes, since 2001 Price cap with sliding scale Single till

Belgium Brussels No Rate of return with yardstickelements

Single till, graduallyintroducing dual till

CzechRepublic

Prague n/a Charges set by airport n/a

Estonia Tallin Ulemiste n/a Cost regulated n/a

Denmark Copenhagen No Price cap Dual till

Finland Helsinki No No regulation, charges based oncost recovery

No

France Paris No Hybrid average revenue basedprice cap

Single till

International Price cap with sliding scale (HAM),revenue sharing (FRA,DUS)

Dual till in HAM andFRA,

Germany

Airports

No

All other airports are cost plusregulated

All other Single till

Greece Athens No Airport sets own charges Dual till

Hungary Budapest, Ferihegy No Price cap Dual till

Ireland Dublin Yes Price cap revenue based Single till

Ireland Dublin Yes Price cap revenue based Single till

Italy Rome No Airports set own charges Dual till

Latvia Riga n/a n/a n/a

Lithuania Vilnius n/a n/a n/a

7/28/2019 Comparative Political Economy of Airport Infrastructure in the European Union- Evolution of Privatization, Regulati…

http://slidepdf.com/reader/full/comparative-political-economy-of-airport-infrastructure-in-the-european-union- 20/20

Malta Malta International n/a Price cap Dual till

Netherlands Amsterdam Yes Rate of return with weightedaverage cost of capital as asset

base

Dual till

Norway Oslo No Cost based Single till

Poland International Airports n/a n/a n/a

Portugal ANA Yes Cost based Single till

Slovak

Republic

Bratislava No n/a n/a

Slovenia Ljubljana n/a Not Regulated n/a

Spain AENA No Cost based Single till

Sweden Stockholm n/a Cost based Single till

Switzerland Zürich, Geneva n/a Not regulated n/a

UnitedKingdom

BAA Yes Price cap Single till

Sources: Davy, European Commission (2006a), Graham, Cranfield, IATA, Airport websites, TRL