comstar uts 1q2010 corporate presentation final-0

TRANSCRIPT

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 1/30

Comstar‐UTSCor orate resentation. 1 2010 results.

Integration Expansion Traditional segment

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 2/30

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 3/30

p.4

Strategy p.14

.

Appendixes p. 24

Integration Expansion Traditional segment 3

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 4/30

Comstar at a Glance

Part of MTS Group (62%)

Revenue2009 – US$ 1,484.8 mln, OIBDA margin2009 – 39.9 %

evenue1Q2010 – . , marg n1Q2010 – .

Over 7.8 million households passed, of which 6.2 million are active subscribers

The leading national broadband provider: ~ 1.4 m n residential broadband subs +

over 2.1 mln residential pay‐TV subs

e ea ng xe ‐ ne te ecommun cat ons prov er or corporates – over . m n act ve nes

>90% of revenues & opex, >80% of capex and 99% of total debt are RUR‐denominated

> 1 mln m of real estate in Moscow

Owner of 25% + 1 share in state‐owned Svyazinvest national fixed line incumbent

Integration Expansion Traditional segment 4

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 5/30

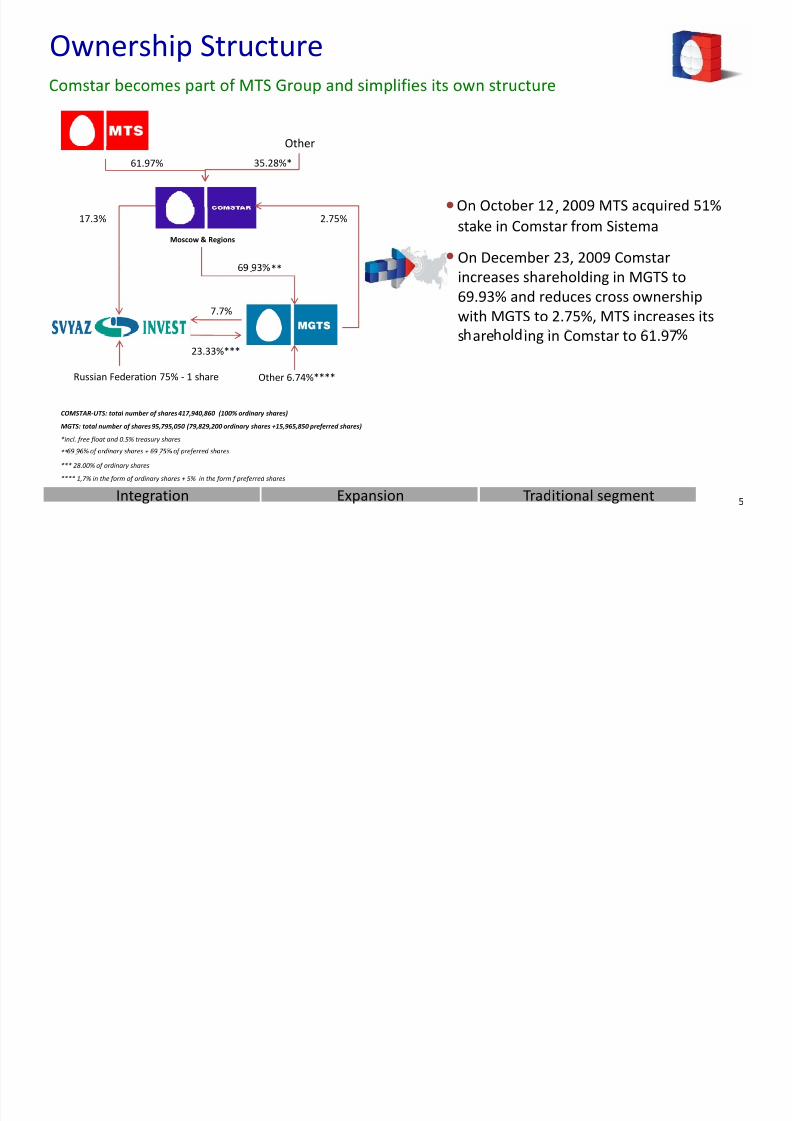

Ownership Structure

Other

•

61.97% 35.28%*

,

stake in Comstar from Sistema

• On December 23, 2009 Comstar

Moscow & Regions

2.75%

**

17.3%

increases

shareholding

in

MGTS

to

69.93% and reduces cross ownership

with MGTS to 2.75%, MTS increases its

.

7.7%

s are o ing in Comstar to 61.9723.33%***

Other 6.74%****Russian Federation 75% ‐ 1 share

COMSTAR‐UTS: total number of shares 417,940,860 (100% ordinary shares)

MGTS: total number of shares 95,795,050 (79,829,200 ordinary shares +15,965,850 preferred shares)

*incl. free float and 0.5% treasury shares

** . .

*** 28.00% of ordinary shares

**** 1,7% in the form of ordinary shares + 5% in the form f preferred shares

Integration Expansion Traditional segment 5

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 6/30

Operational Structure

57% of Group revenues STATE HOLDING

Alternative segmentin Moscow

Alternative segmentin regions and CIS

26% of Group revenues 18% of Group revenues

Traditional segmentin Moscow (MGTS)

70 o Group OIBDA

>4.9 mln installed lines:

Comstar owns 25%+1 share

•7ILECs + Rostelecom +

17 o Group OIBDA

>658 th. installed lines

13 o Group OIBDA

>4.1 mln households

•3.6 mln residential

lines, (incl.276 th.

voice+BB users)

+ Central Telegraph

+ 23% in MGTS

•Owner of the “last mile”

•583 th. residential

accounts (incl. 583 th.

premium BB

•2.6 mln residential subs:

• 2.0 mln pay‐TV users

• . corpora e

lines(70 th. accounts)

>90% of lines are ADSL

in the regions

•>35 million installed

lines covering 90% of

,

MGTS infrastructure)•27 th. corporate

accounts

•

426

th.

BB

users•58 th. corporate

accounts

~80% of BB users can get

20 Mb/sec

uss a•>6 000 km fiber

backbone

digital

>11 000 km fiber

Integration Expansion Traditional segment 6

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 7/30

1Q2010 results

Q1 2010 Q1 2009 Growth Q4 2009 Growth 12m 2009

Revenues 12,167 11,343 7% 12,133 0% 46,925

(RUR Million)

OIBDA 5,337 4,291 24% 4,847 10% 18,719Margin (%) 43.9% 37.8% 40.0% 39.9%

Operating Income 3,881 2,798 39% 3,175 22% 12,740 . . . .

Net income/(loss) attributable to Comstar

UTS' shareholders

1,794 494 263% (8,821) - (6,518)

Cash Capex 495 2,024 (76%) 800 (38%) 3,889% of Revenues 4.1% 17.8% 6.6% 8.3%

Free CF 3,925 1,436 173% 3,472 13% 10,849

● 7% year on year revenue growth in RUR

• Growing DLD/ILD and fixed‐to‐mobile traffic, increase in MGTS BB subscriber base

• Ongoing up‐selling of regional pay‐TV subscribers to broadband Internet services

• Increase in RUR prices

● 24% year on year OIBDA growth in RUR

● 263% year on year Net Income attributable to Comstar‐UTS’ shareholders growth in RUR

● 173% year on year Free Cash Flow growth in RUR

Integration Expansion Traditional segment 7

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 8/30

High profitability and revenue growth

Breakdown of revenues, 1Q2010 Breakdown of OIBDA, 1Q2010

13%

17%Comstar‐UTS

Traditional

Alternative in the re ions57 %

26 %

Alternative in Moscow

*

18%

28,2%32,3%

Q1

,

8%

37,8%

48,2%

18,9%28,2%

Q1

2009211 258

91 110120160

200240

10%

mln

43,9%

,2010

04080

Q1 2009 Q1 2010*Revenue in US$ millions, growth in rubles

*Revenue in US$ millions, growth in rublesIntegration Expansion Traditional segment 8

Stable traditional MGTS business provides sustainable cash flows and high profitability, regionsdrive revenue growth

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 9/30

Liquidity

• Operating cash flow RUR 4.4 bln (US$ 148 mln)

1Q 2010 Debt structure as of March 31, 2010

Debt by currency US$ million

• Cash, cash equivalents & short‐term investments RUR 16.0 bln

(US$ 545 mln)

• Cash CAPEX RUR 0.5 bln (US$ 17 mln)

Russian Ruble 973

Euro 5

US Dollar 3

Total debt * 981

• Free cash flow RUR 3.9 bln (US$ 132 mln)

• Total debt RUR 28.8 bln (US$ 981 mln)

• Total RUR debt/OIBDA 1.3

US$,

mln

In the currency of debt,

mln

• Net debt RUR 12.8 bln (US$ 436 mln)

• RUR Net debt/OIBDA of 0.6

er an cre t ne ac ty ,

MTS 1,815 RUR 62Vendor financing 436 RUR 15

Others various 19

*

* RUR/$ = 29.3638 as at March 31, 2010

e repaymen s sc e u e , m n

21 947

1753 353

3 31715 102

6 720

2Q2010 3Q2010 4Q2010 2011 2012 2013 >

2013

Integration Expansion Traditional segment 9

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 10/30

Outlook for 2010*

14821648

14852000

,

Mid

single

digit %

mln $ 6%1%

1120

0

500

100032,7%

42,4% 41,8% 39,9% 40%

35%

30%

40%

2006 2007 2008 2009 2010

*Revenue in US$ millions, organic growth in rubles

2006 2007 2008 2009 2010

as , m n

27.4% 23.3% 21.5% 8.1% 20% 10-12% % of Revenues

1 120 1 482 1 648 1 485 1 485 Revenues mln $

Regions152

170156 Others

127 132

68

Moscow

16 26

80

3

1117 50

29

78

eg ons

Development of Broadband DN (incl.

FTTX)

MGTS network upgrade and development

2006 2007 2008 2009 2010 After the end of

digitalization

Integration Expansion Traditional segment 10

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 11/30

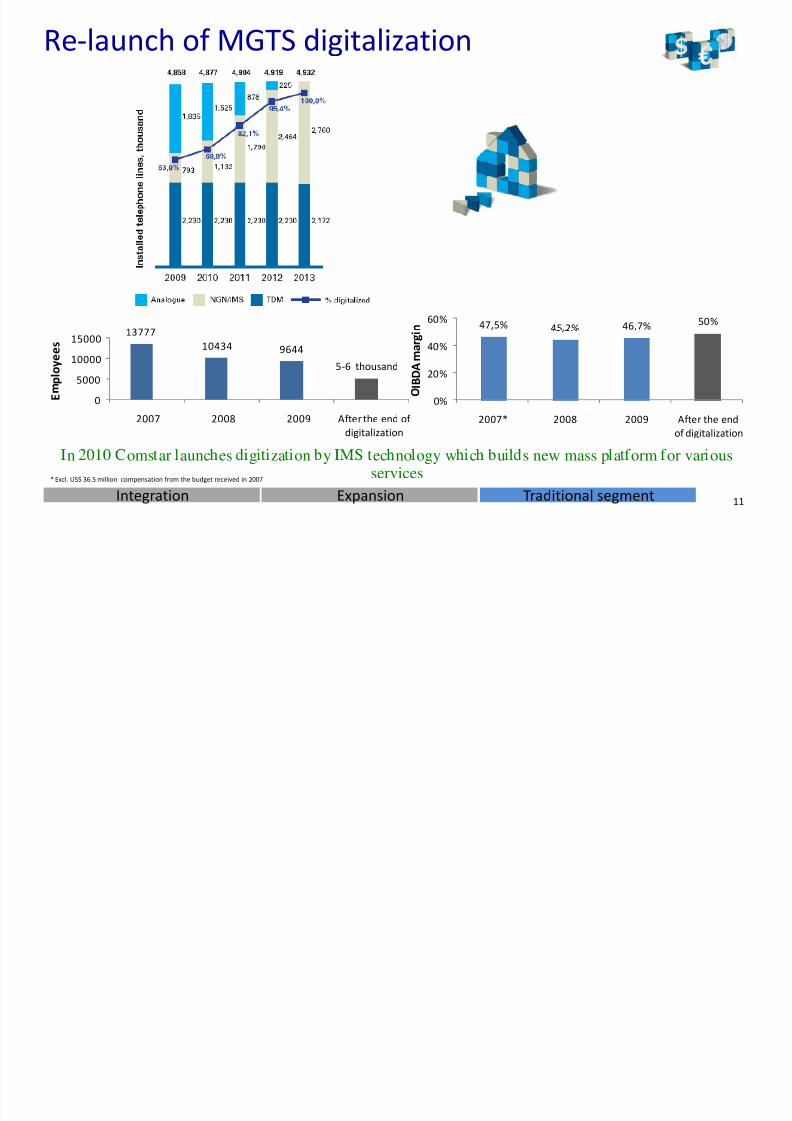

Re‐launch of MGTS digitalization

47,5% 45 2% 46,7% 50%60% n

10434 9644

5‐6 thousand

5000

10000

15000

p

l o y e e s

20%

40%

I B

D A m a r g i

0

2007 2008 2009 After the end of

digitalization

E 0%

2007* 2008 2009 After the end

of digitalization

Integration Expansion Traditional segment 11

n oms ar aunc es g za on y ec no ogy w c u s new mass p a orm or var ous

services* Excl. US$ 36.5 million compensation from the budget received in 2007

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 12/30

MGTS real estate potential

Location of the real estate

• 2 1st zone ; 1% 2nd zone ;

.

• 5000 m2 – average size of the building

• –

r zone ;

10%

5th zone

;

• > 50% will be freed up after the end of

digitalization

•∼ US$ 1000 – current selling price/1m2 (office

space class B/C) 4th zone ;

64%

•∼ US$ 430 – current rental rate/1m2

1st zone ‐ Boulevard Ring

2nd zone

‐Garden

Ring

Road

3rd zone ‐ Third Ring Road

4th zone ‐ Moscow Ring Road

5th zone ‐ outside Moscow Ring Road

Integration Expansion Traditional segment 12

After the end of digitalization significant real estate potential will be unlocked

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 13/30

Overview p.4

p.14

Broadband p.18

Appendixes p.24

Integration Expansion Traditional segment 13

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 14/30

Strategy: “5 Angles of Attack” (2008)

Penetration into the mass market in Moscow

Increasin ARPU in the remium se ment

3K: Comstar → Client → Quality

BB development in the regions

Restructuring of regional operations

2 legal entities : Comstar & MGTS

STRUCTUREBROADBAND MGTSREGIONS SVYAZINVEST

Integration of Stream‐ Ca italizin on

Enhancing existing

operations via

strate ic M&As

ost opt m zat on

increase in efficiency

Regulated tariff increases

Svyazinvest stake

Integration Expansion Traditional segment 14

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 15/30

Priorities in crisis (2009)

2009 resultsActions

towards maximizing cash flows and integration of the assets

• Maximizing cash flows

• Optimization of capital investments

• Service the debt

Ensure financial

stabilit

1• RUR 10.8 bln free cash flow

• Cash CAPEX of 8.1% of revenues

• Timel a ment of interest

• Reduction of debt level

2

• Restructuring of terms of Sberbank

loan repayment

Refocus from

expansion

to optimization

• eep an eve op e ex s ng su scr er

base• 3K programme of quality enhancement

‐ ‐

with no promo• 9% y‐o‐y residential BB RUR

ARPU rowth in Moscow‐

VAS

• Ac uisition of re ional o erators

3

• Increase in ownership in MGTS to 70%

from 56%

restructuring

• Restructuring of ownership in Svyazinvest• ecrease n cross‐owners p w t

to 3% from 14%

• Restructuring of ownership in Svyazinvest

‐ ,

financials

Integration Expansion Traditional segment 15

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 16/30

Priorities for 2010

Integration with MTS in orderto extract synergies

Aggressive expansion on the Russian market, revenue growth

of cable‐TV and BB assets

2) Green‐field

3) Leadership in corporate segment

1) Re‐branding in alternative

segment

2) Cross‐sales

(excl. SVI)

4) Aggressive development on the

long‐distance market

mass‐market

4) Optimization of expenses

through intercompany

business‐models to create growth potential

outsourcing

5) Streamlining of business‐

processes

Managing traditional segment (MGTS+SVI)

to ensure stable free cash flow generation1) Increase in ownership in MGTS/completion of SVI ownership restructuring

2) Completion of digitalization/IT optimization

3) Strengthen leadership position on the mass‐market broadband

4) Optimization and stabilization of revenues from infrastructure

Integration Expansion Traditional segment 16

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 17/30

Overview p.4

.

p.16p.18

Appendixes p.24

Integration Expansion Traditional segment 17

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 18/30

Growth in subscriber base is driven by the mass‐market segment (MGTS),

Residential BB market In Moscow

94%100%

ARPU development is driven by the premium segment (Comstar)

Moscow Residential Fixed‐line BB Market, 3Q2009 Broadband penetration, %

83%

74%74%73%71%66%66%

62%61%60%59%57%55%55%52%51%49%45%43%42%

39%38%36%35%

50%

60%

70%

80%

90%

Comstar;

32%Net

by

Net

;

9%

Qwerty; 7%Others; 8%

European

average 55%

31%

23%

0%

10%

20%

30%

Vimpelcom;

Moscow 3Q2009

Direct

Info

OECD Communications Outlook 2008Total

market:

2.6

mn

subsDirect Info

Penetration of BB among MGTS subscriber base, %Comstar residential subscriber base, ‘000

Akado; 23%

BB

+voice

24%Saturation of the market

Active increase in subs

Launch of IPTV

Increasing

speeds

Launch of

140 262 360 651 784 847 860Voice

76%

mass‐market

offering

*

2004 2005 2006 2007 2008 2009 1 2010* incl.

583

thousand

premium

segment

subs

and

276

thousand

mass

‐market

segment

subs

Integration Expansion Traditional segment 18

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 19/30

Rationalization of BB model in Moscow

Mass‐market segmentPremium segment

Current

Fixed voice is the main service in the bundleMobile voice is the main service in the bundle

• Fixed voice+BB from MGTS + VAS from Comstar and

MTS (DLD/ILD, IPTV, Wi‐Fi, WiMAX, 3G, mobile voice

etc)

• Mobile voice + ADSL BB+VAS from MTS• One bill from MTS

• Mostly pre‐paid

• Post paid• Direct marketing via MGTS bills• MGTS will start selling 3Mb/sec+•

‐

Integration Expansion Traditional segment 19

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 20/30

Scale of regional development

## 2-3 regional BB Player (excl. Svyazinvest)

Vimpelcom5%

Multiregion

3%

Other

14%

Санкт‐Петербург

Svyazinvest

62%R‐Telecom

11%

oms ar‐

5%

Source: Direct-Info, AC&M Consulting, J’son &

Partners, companies’ data

Comstar‐UTS

21%

#1 Player on the regional Pay-TV market

R‐Telecom

10%

Multiregion

Other

57%

8%

Svyazinvest

4%20 Integration Expansion Traditional segment

Excl. satellite TV

20

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 21/30

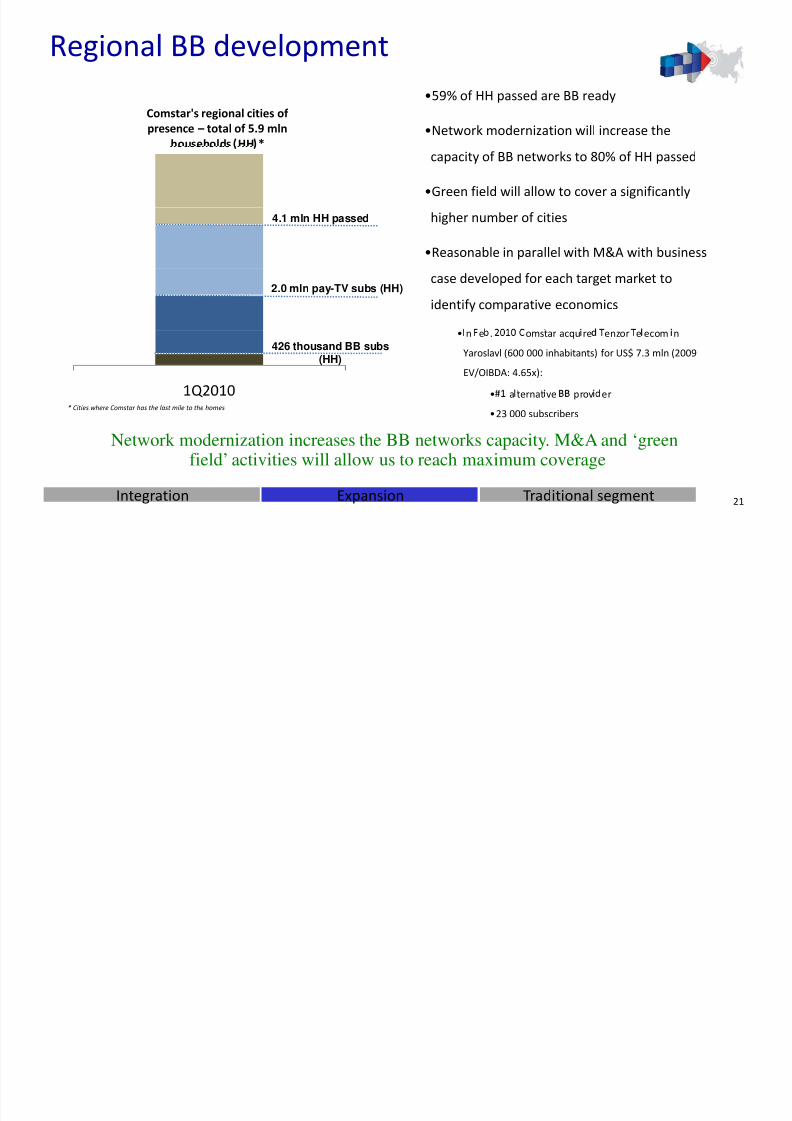

Regional BB development

Comstar's regional cities of

presence – total of 5.9 mln

households HH *

•59% of HH passed are BB ready

•Network modernization will increase the

capacity of BB networks to 80% of HH passed

•Green field will allow to cover a significantly

higher number of cities

•Reasonable in parallel with M&A with business

4.1 mln HH passed

case developed for each target market to

identify comparative economics2.0 mln pay-TV subs (HH)

• n e . omstar acqu re enzor e ecom n

Yaroslavl (600 000 inhabitants) for US$ 7.3 mln (2009

EV/OIBDA: 4.65x):

426 thousand BB subs(HH)

Network modernization increases the BB networks capacity. M&A and ‘green

• a ternat ve prov er

•23 000 subscribers* Cities where Comstar has the last mile to the homes

field’ activities will allow us to reach maximum coverage

Integration Expansion Traditional segment 21

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 22/30

Investment Case

National fixed‐line provider with operations in 83 cities of Russia with combined population of >48 mln people

Low exposure to forex risks – all business in RUR

Unique combination of Regulated and non‐regulated business

High profitable incumbent business and growing altnet business

‐ ‐

telecommunication space

Balanced mix of customer types (residential, corporates, operators)

After MTS/SSA deal:

Sell SI stake/Increase the stake in MGTS

+ Branding

+ Backbone

+ Bundling

Integration Expansion Traditional segment 22

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 23/30

Contacts

For additional information please visit

. ‐ .

or contact Masha Eliseeva

Head of Investor Relations

E‐mail: ir@comstar‐uts.ru

Integration Expansion Traditional segment 23

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 24/30

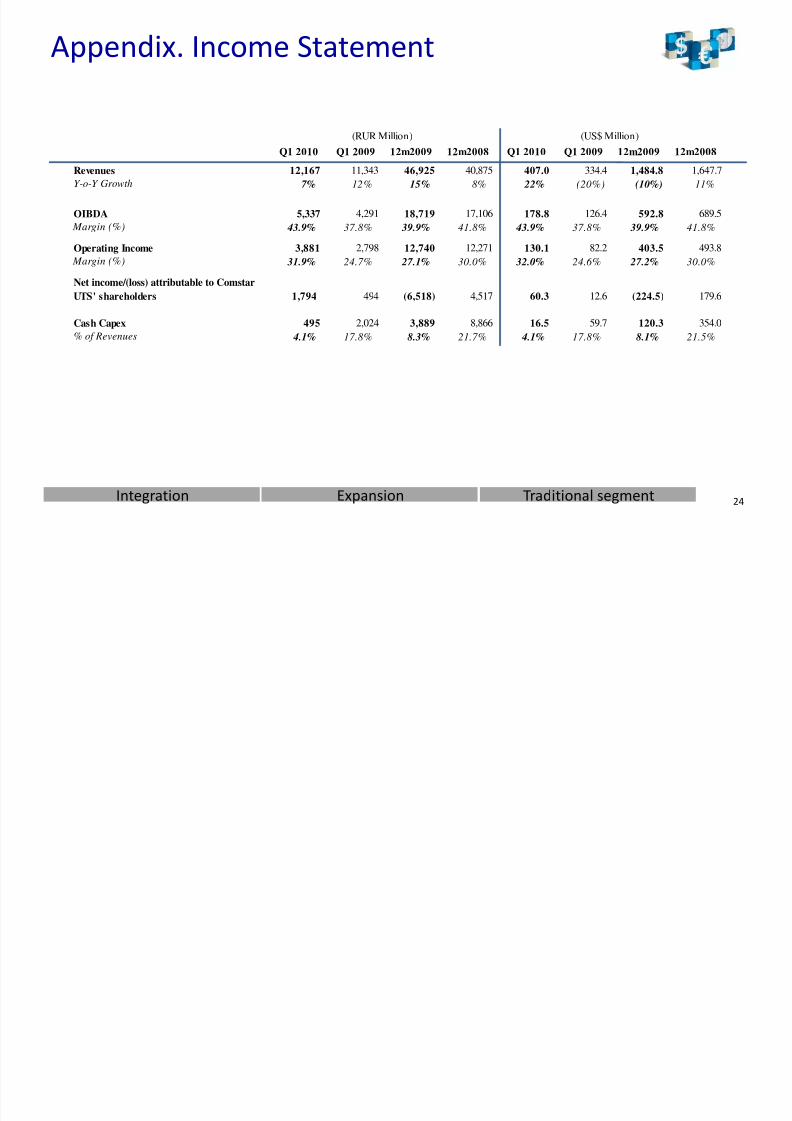

Appendix. Income Statement

(RUR Million) (US$ Million)

Q1 2010 Q1 2009 12m2009 12m2008 Q1 2010 Q1 2009 12m2009 12m2008

Revenues 12,167 11,343 46,925 40,875 407.0 334.4 1,484.8 1,647.7

Y-o-Y Growth 7% 12% 15% 8% 22% (20%) (10%) 11%

OIBDA 5,337 4,291 18,719 17,106 178.8 126.4 592.8 689.5

Margin (%) 43.9% 37.8% 39.9% 41.8% 43.9% 37.8% 39.9% 41.8%

Operating Income 3,881 2,798 12,740 12,271 130.1 82.2 403.5 493.8

Margin (%) 31.9% 24.7% 27.1% 30.0% 32.0% 24.6% 27.2% 30.0%

Net income/(loss) attributable to Comstar

UTS' shareholders 1,794 494 (6,518) 4,517 60.3 12.6 (224.5) 179.6

Cash Capex 495 2,024 3,889 8,866 16.5 59.7 120.3 354.0

% of Revenues 4.1% 17.8% 8.3% 21.7% 4.1% 17.8% 8.1% 21.5%

Integration Expansion Traditional segment 24

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 25/30

Appendix. Resilience to FX movements

Revenue breakdown Operating expenses breakdown

10%

10%

RUR >

90%

RUR >

90%

Total debt breakdown CAPEX breakdown

Other

1%

other

20%

RUR >

RUR >

80%

99%

Integration Expansion Traditional segment 25

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 26/30

Appendix. Segmental Breakdown

Q1 2010 Q1 2009 12m2009 12m2008 Q1 2010 Q1 2009 12m2009 12m2008

Revenue

Traditional se ment in Moscow MGTS

(RUR Million) (US$ Million)

, , . , .

Alternative segment in Moscow (Comstar & Comstar-Direct) 3,296 3,077 13,178 12,893 110.3 90.7 417.3 519.5

Alternative segment in the regions & CIS (Comstar) 2,186 1,984 8,230 4,109 73.1 58.5 260.5 164.9

Intersegment Sales (1,031) (869) (3,811) (4,282) (34.5) (25.6) (120.9) (172.6)

ota evenue 12,167 11,343 46,925 40,875 407.0 334.4 1,484.8 1,647.7

OIBDA

Traditional segment in Moscow (MGTS) 3,716 3,180 13,680 12,726 124.4 93.8 433.0 513.9

Alternative segment in Moscow (Comstar & Comstar-Direct) 929 582 2,770 3,079 31.2 17.2 87.9 123.4

Alternative segment in the regions & CIS (Comstar) 705 560 2,323 1,400 23.6 16.3 73.4 56.4

Effect of eliminations and other consolidation adjustments (12) (31) (54) (99) (0.4) (0.9) (1.6) (4.1)

Total OIBDA 5,337 4,291 18,719 17,106 178.8 126.4 592.8 689.5

Integration Expansion Traditional segment 26

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 27/30

Q1 2010 Q1 2009 Change Q4 2009 Change

Traditional segment in Moscow (MGTS)

Appendix. Operating highlights

Residential

Number of subscribers / active lines (000s ) 3,609 3,595 0% 3,608 0%

incl. BB subscribers 276 160 73% 246 12%

ARPU (RUR) 349 309 13% 335 4%

Number of subscribers (000s) 70 96 -27% 70 1%

incl. BB subscribers 30 33 -7% 32 -4%

ARPU (excl. revenue from points of interconnect) (RUR) 6,468 4,457 45% 6,485 0%

Alternative segment in Moscow

Residential subscribers

Number of subscribers (000s) 583 666 -12% 607 -4%

incl. BB subscribers 583 635 -8% 601 -3%

ARPU (RUR) 527 367 44% 549 -4%

Corporate subscribers

Number of subscribers (000s) 27 30 -8% 27 2%

incl. BB subscribers 15 18 -18% 15 -2%

ARPU (RUR) 13,668 11,951 14% 14,737 -7%

Alternative segment in the regions & CIS

Number of subscribers (000s) 2,630 2,524 4% 2,606 1%

incl. pay-TV subscribers 1,997 1,952 2% 1,996 0%

incl. BB subscribers 426 300 42% 378 13%

ARPU (RUR) 158 152 4% 150 5%Corporate subscribers

Number of subscribers (000s) 58 52 13% 52 12%

incl. BB subscribers 28 23 20% 26 9%

ARPU (RUR) 3,299 3,532 -7% 3,579 -8%

Total number of households passed (000s) 7,756 7,173 8% 7,502 3%

Total number of broadband internet subscribers (000s) 1,359 1,169 16% 1,298 5%

Total number of pay-TV subscribers (000s) 2,122 2,090 2%

2,1240%

Integration Expansion Traditional segment 27

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 28/30

Appendix. Segmental Operating Expenses &

2007 2008 2009#Employees *

Traditional segment 13,777 10,434 9,644

Alternative segment in M oscow 2,154 2,231 2,041

Alternative segment in the regions & CIS 1,084 2,878 5,595

Average salary

Traditional segment $ 956.0 $ 1,257.5 $ 1,131.5, . , . , .

Alternative segment in the regions & CIS $ 1,340.0 $ 1,099.3 $ 880.6

Average monthly revenue per Employee

Traditional segment $ 6,729.1 $ 9,071.4 $ 8,017.5

Alternative segment in M oscow $ 17,506.3 $ 19,404.7 $ 17,039.5

Alternative segment in the regions & CIS $ 3,601.9 $ 4,774.8 $ 3,880.3

Alternative Segment, mln US$Traditional Segment, mln US$

235

232

175

Eliminations

233185 Eliminations

156 164 162

59 61 4288

142115

132139

114

‐1‐30 ‐16

SGA

Interconnection costs

Network maintenance 94153 160

7191 87114

111 147

‐

Interconnection costs

Employee costs

SGA

Other expenses, net

2007 2008 2009

Other expenses, net

* At the end of period Integration Expansion Traditional segment 28

‐ ‐

2007 2008 2009

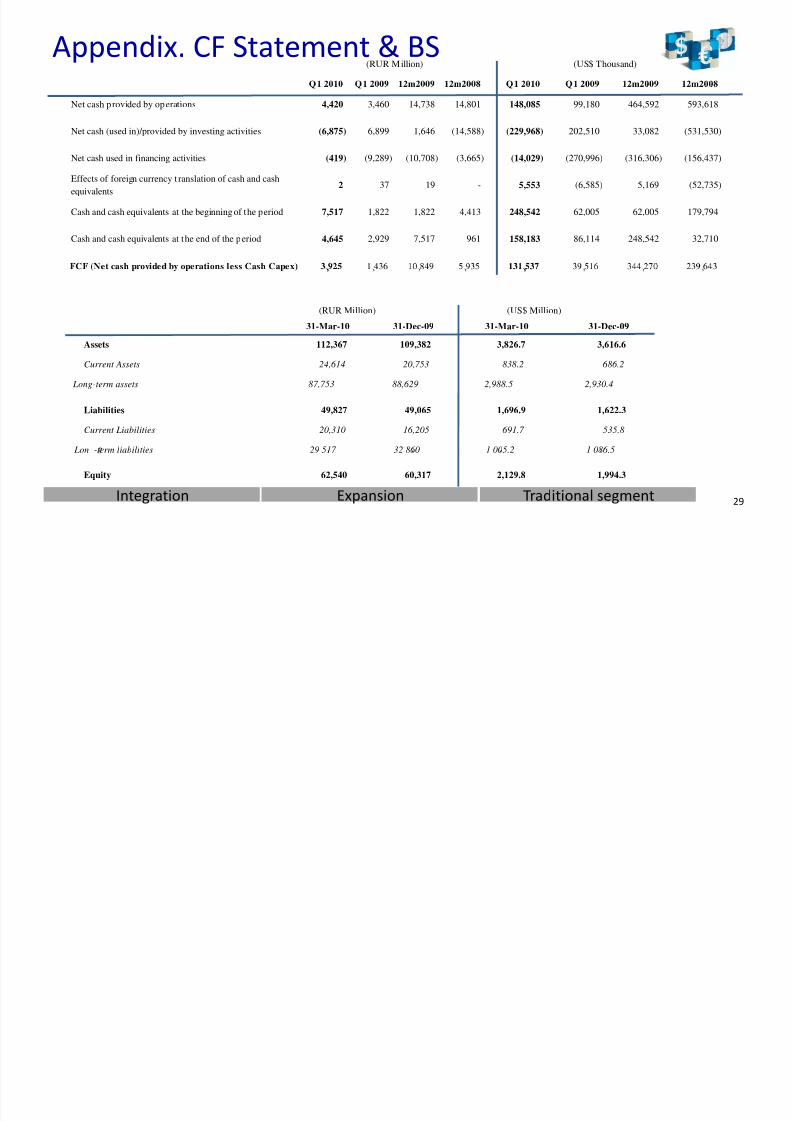

A di CF S & BS

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 29/30

(RUR Million) (US$ Thousand)Appendix. CF Statement & BS

Net cash provided by operations 4,420 3,460 14,738 14,801 148,085 99,180 464,592 593,618

Net cash (used in)/provided by investing activities (6,875) 6,899 1,646 (14,588) (229,968) 202,510 33,082 (531,530)

Net cash used in financing activities (419) (9,289) (10,708) (3,665) (14,029) (270,996) (316,306) (156,437)

Effects of foreign currency t ranslation of cash and cash

equivalents

2 37 19 - 5,553 (6,585) 5,169 (52,735)

Cash and cash equivalents at the beginning of the period 7,517 1,822 1,822 4,413 248,542 62,005 62,005 179,794

Cash and cash equivalents at the end of the period 4,645 2,929 7,517 961 158,183 86,114 248,542 32,710

31-Mar-10 31-Dec-09 31-Mar-10 31-Dec-09

(RUR Million) (US$ Million)

, , , , , , , ,

Assets 112,367 109,382 3,826.7 3,616.6

Current Assets 24,614 20,753 838.2 686.2

Long-term assets 87,753 88,629 2,988.5 2,930.4

Liabilities 49,827 49,065 1,696.9 1,622.3

Current Liabilities 20,310 16,205 691.7 535.8

Lon -term liabilities 29 517 32 860 1 005.2 1 086.5

Equity 62,540 60,317 2,129.8 1,994.3

Integration Expansion Traditional segment 29

8/3/2019 Comstar UTS 1Q2010 Corporate Presentation Final-0

http://slidepdf.com/reader/full/comstar-uts-1q2010-corporate-presentation-final-0 30/30

Appendix. Glossary

ADSL....................................... Asymmetric digital subscriber line

ADSL technology using the ITU G.992.5 standard. Allows for ................................... .

Docsis……………………............... Data Over Cable Service Interface Specifications

Ethernet.................................. Packet based transmission rotocol rimaril used in LANs

FTTB........................................ Fiber‐to‐the‐Building

‐.........................................

MMDS..................................... Microwave Multipoint Distribution System

Integration Expansion Traditional segment 30