consultation on private company taxation - kpmg | us · consultation on private company taxation...

TRANSCRIPT

KPMG Submission to Canada’s Department of Finance

Consultation on Private Company Taxation

KPMG LLP October 2, 2017

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 1

Table of Contents

1 Executive Summary 2

2 Introduction 4

3 Income Sprinkling Using Private Corporations 5 3.1 Tax on Split Income (TOSI) Proposals 6 3.2 Lifetime Capital Gains Exemption (LCGE) Proposals 13 3.3 Income Sprinkling Recommendations 13

4 Holding a Passive Investment Portfolio Inside a Private Corporation 15

4.1 Tax Policy for Passive Income based on Equivalent Comparables 16 4.2 Issues with Apportionment and Elective Methods 19 4.3 Considerations for Corporations Mostly Engaged in Passive

Investments 22 4.4 Scope of the New Tax Regime With Respect to Capital Gains 22 4.5 Key Transitional Issues 23 4.6 Applying the New Rules to Private Corporations Other Than CCPCs 25

5 Converting a Private Corporation's Regular Income into Capital Gains 26

5.1 Surplus Stripping Anti-Avoidance Rule in Section 84.1 27 5.2 New Surplus Stripping Anti-Avoidance Rule in Section 246.1 30

6 Conclusion 36

7 Appendix A — Integration Under the Proposed Regime 37

8 Appendix B — Investing in Passive Assets 39

9 Appendix C — Intergenerational Transfers in Different Jurisdictions 41

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 2

1 Executive Summary In the view of KPMG Canada LLP (KPMG), Finance’s proposed rules concerning the taxation of private companies represent a major shift in tax policy for private corporations. Because these proposed rules have caused significant concerns for taxpayers and their private corporations, we urge the government to delay implementing these proposals. This will allow for a more comprehensive review of tax fairness and, at the same time, ensure that any new rules are not unduly complex.

KPMG recommends that Finance reconsider its proposed legislation for income sprinkling, lifetime capital gains exemption (LCGE) and converting a private corporation’s regular income into capital gains to fix the technical and interpretive issues identified herein. Also, KPMG believes taxpayers should be given additional time to comply with the proposed legislation and that appropriate transitional rules should be implemented. In addition, KPMG recommends that Finance reconsider the taxation of investments held in private corporations as part of a comprehensive review of the owner-manager tax system. KPMG’s view is that, on the whole, these rules are complex and will be difficult for some private company owners to comply with.

However, if the government decides to proceed with these proposals, we strongly encourage Finance to consider the following:

Sprinkling income using private corporations — Finance should not differentiate between individuals aged 18-24 and individuals 25 and

older when determining “reasonableness” for labor and capital contributions (see section 3.1.1)

— Finance and the CRA should provide guidance on the scope of the proposed rules, including how the “reasonableness” test will be interpreted and applied (see sections 3.1.1 and 3.1.7)

— Finance should consider introducing safe harbours in applying certain aspects of the TOSI rules (see sections 3.1.1, 3.1.4., 3.1.5 and 3.1.7)

— Finance should amend the proposed rules so that minors are able to access the LCGE using the same criteria deemed appropriate for individuals over 18 (see section 3.2.1)

— Finance should delay the effective date of the proposed rules (see section 3.3).

Holding a passive investment portfolio inside a private corporation — Finance should review the taxation of investments held in private corporations as part of a

comprehensive review of the owner-manager tax system and compare the complete compensation packages that an employee earns on an after-tax basis against the after-tax funds available from earning passive income in a private corporation, as well as consider the different ways a private corporation deploys after-tax earnings in its active business (see section 4.1.1)

— KPMG believes that neither the apportionment method nor the elective method will fully achieve the government’s intentions if implemented. However, if implemented, Finance should allow taxpayers to choose between the apportionment/elective and passive income election methods, and allow for future transitions between them to accommodate changes in their situation (see section 4.2)

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 3

— Finance should provide adequate time for transition to any new system, allow corporations to maintain existing corporate balances and grandfather existing passive assets under the current integration system (see section 4.5).

Converting a private corporation's regular income into capital gains — Finance should grandfather existing pipeline strategies to avoid double tax (see section

5.1.1) — Finance should exempt certain intergenerational/sibling transfers from section 84.1 to

facilitate the transfer of an operating business between family members (see section 5.1.3) — Finance should limit the application of proposed section 84.1 where the non-arm’s-length

adjusted cost base is created as a consequence of death (see section 5.1.4) — Finance should simplify the process to increase the cost base of underlying corporate

assets to the extent of the gain recognized on death on the deemed disposition of the shares of the corporation (see section 5.1.5)

— Finance should draft a more targeted provision to provide more certainty on the scope of proposed section 246.1 (see sections 5.2.1 and 5.2.2)

— Finance should specifically exclude certain transactions from the application of proposed section 246.1 (see section 5.2.1).

— Finance should grandfather existing CDA balances created before July 18, 2017 (see section 5.2.3)

— Finance should ensure proposed section 246.1 does not apply to transactions that were entered into before July 18, 2017 (see section 5.2.3).

KPMG also participated in the Joint Committee of Taxation of The Canadian Bar Association and the Chartered Professional Accountants of Canada submission on these proposals.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 4

2 Introduction KPMG is pleased to provide Canada’s Department of Finance (Finance) with a written submission on its proposed changes to the taxation of private corporations. KPMG compliments Finance for launching a consultation process to gather feedback on its paper, “Tax Planning Using Private Corporations” (Consultation Paper), released July 18, 2017.

KPMG welcomes the opportunity to contribute to the public debate on this important matter. KPMG strongly agrees with Finance that it is in Canada’s best interest to ensure that any changes the government considers will maintain the benefits of a competitive tax regime, because these benefits are used to help corporations grow, create jobs, and innovate.

This submission addresses the three issues that Finance identifies in its Consultation Paper:

— Sprinkling income using private corporations — In which taxpayers may reduce income taxes by causing income that would otherwise be realized by a high-income individual facing a higher personal income tax rate to instead be realized (e.g., via dividends or capital gains) by family members who are subject to lower personal tax rates or who may not be taxable at all.

— Holding a passive investment portfolio inside a private corporation — Owners of private corporations may use this planning, which may help them realize financial advantages compared to other investors, because lower corporate income tax rates facilitate the accumulation of earnings in a private corporation that can be invested in a passive portfolio.

— Converting a private corporation's regular income into capital gains — In which taxpayers may reduce income taxes by taking advantage of the lower tax rates on capital gains. Income is normally paid out of a private corporation in the form of salary or dividends to the shareholders, who are taxed at the recipient's personal income tax rate (subject to a tax credit for dividends reflecting the corporate tax presumed to have been paid). In contrast, only 50% of capital gains are included in income, resulting in a significantly lower tax rate on income that is converted from dividends to capital gains.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 5

3 Income Sprinkling Using Private Corporations The government is seeking input on proposed rules to distinguish income sprinkling from the acceptable payment of “reasonable compensation” for family members. According to the Consultation Paper, it is Finance’s belief that income sprinkling provides unintended and unfair benefits to higher-income individuals, principally through the use of private corporations. To address this concern, Finance has released detailed legislative proposals and Explanatory Notes to address income sprinkling, including proposed rules to:

— Extend the tax on split income (TOSI)

— Constrain the multiplication of LCGE claims.

KPMG submits that Finance’s proposals to address its concerns on income sprinkling should be based on fundamental principles of efficiency, fairness and simplicity for taxpayers. In our review of the draft legislation, we are concerned that some of these objectives are not being met.

According to Finance, these proposed rules are intended to help determine whether compensation provided to family members is reasonable, based on their contribution of value and financial resources to the private corporation. However, KPMG’s view is that Finance’s legislative proposals, as drafted, appear to affect more taxpayers than possibly intended.

Finance’s detailed legislative proposals are extremely complex and difficult to interpret, and require taxpayers to perform a subjective analysis to determine whether they will be subject to the TOSI changes or able to claim the LCGE. In administering these rules, the CRA will also have to undertake a subjective analysis when assessing or auditing a taxpayer. Because the analysis will be subjective, it will likely result in the rules being applied inconsistently to taxpayers across the country, which does not meet the objective of providing tax fairness. Inevitably, these subjective issues will often have to be resolved by the tax courts, resulting in further costs to small business owners and Canadians. Based on KPMG’s analysis, we believe Finance should consider safe harbour rules to address some of the concerns regarding the interpretation of the proposed rules and provide further guidance on the interpretation of “reasonable”.

In considering Finance’s proposals, we have identified the following issues with the proposed TOSI rules:

— Uncertain interpretation and scope of the TOSI “reasonableness test” related to:

o Restrictions on labour and capital contributions for individuals aged 18-24 and individuals aged 25 and older

o Financial assistance

o Passive income

o The time period under consideration

o Amounts paid or that became payable

o Supporting documentation

o Ensuring consistent CRA assessments/audits

— Whether the TOSI rules may apply to family members in situation where the related person (i.e., the business owner) is not in the top marginal income tax bracket

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 6

We have identified the following issues with the proposed LCGE rules:

— Minors ineligible for the LCGE

— LCGE and the “unreasonable” portion of a capital gain

Note that this submission does not include all the possible consequences arising from the proposed legislation to address income sprinkling.

KPMG submits that the timeframe given to private corporations to comply with the rules, which are generally effective January 1, 2018, is too brief. Allowing at least an additional year for taxpayers to assess the impact of these significant changes and arrange their affairs would be helpful.

3.1 Tax on Split Income (TOSI) Proposals The new definition “split portion” in proposed paragraph 120.4(1)(b) introduces a subjective “reasonableness” test to determine if amounts are to be included in the “split income” of a “specified individual” (both terms defined in subsection 120.4(1)), if the specified individual is over 17 years of age. New subsection 120.4(1.1) contains interpretive rules for purposes of applying the TOSI rules.

Finance notes that the new reasonableness test is intended to ensure amounts that an adult specified individual receives from a business where a family member is a principal (e.g., a “connected individual” in the case of income derived from a corporation) are included in the adult specified individual’s split income “to the extent that the amounts are not commensurate with what would be expected in arrangements involving parties dealing at arm’s length”. Further, the proposed rules stipulate that “an amount would not be considered reasonable in the context of the business to the extent that it exceeds what an arm’s-length party would have agreed to pay to the adult specified individual”, with consideration of the following factors:

— Labour contributions

— Capital contributions

— Risks assumed in support of the business

— Previous remuneration or amounts received.

These factors are contained in the definition of “split portion” in subparagraph 120.4(1)(b)(iii).

3.1.1 Reasonableness test — Restrictions on labour and capital contributions The proposed legislation differentiates labour and capital contributions based on an individual’s age. For individuals aged 18-24, clause 120.4(1.1)(e)(iii)(A) states:

The individual is to be considered to have performed functions in respect of a “source business” (defined in the definition of “split portion” in clause 120.4(1)(b)(ii)(B)) only to the extent the individual is actively engaged on a regular, continuous and substantial basis in the activities of the source business.

A “reasonable” return for these individuals’ capital contributions is considered to be a prescribed rate (currently 1%) of the fair market value of the assets contributed in support of the source business, under clause 120.4(1.1)(e)(iii)(B).

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 7

In contrast, an individual who is 25 or older over must be “engaged in the activities of the business” in determining whether he or she meets the labour contribution factor in the reasonableness test, under the split portion definition in proposed subparagraph 120.4(1)(b)(iii). For these individuals, the “assets contributed” and “risks assumed” by the individual in support of the source business will also be factors in determining whether an amount received by the individual will be considered to exceed a reasonable amount in the definition of “split portion” under proposed clauses 120.4(1)(b)(iii)(B) and (C), respectively, and hence subject to TOSI.

KPMG recommendations

From a tax policy perspective, we question why a distinction was made based on an individual’s age. If a reasonableness test is considered appropriate for individuals aged 25 and over, the same should be true for individuals 18-24. Further, because many individuals 18-24 are not in post-secondary studies and may have already entered the workforce, the test that applies to them should not be different from those in the 25 and over age group.

To illustrate some of the issues with the reasonableness test for both age brackets (i.e., individuals 18-24 and individuals aged 25 and over), we include two examples below that highlight some of the related interpretive issues.

Issues for labour and capital contributions by individuals 18-24

The proposed rules require that taxpayers include, in TOSI, amounts that are not commensurate with what would be expected in arrangements involving arm’s-length parties. Further, what is considered to be “reasonable” depends on an individual’s age. An individual who is 18-24 years of age must be “actively engaged on a regular, continuous and substantial basis”, otherwise they are not considered to have made labour contributions to the business. However, it is not clear what this phrase means, including whether this test refers to engagement that is equivalent to, or less than, full-time employment. A safe harbour rule may be helpful for taxpayers to make this determination.

The proposed rules allow an individual who is 18-24 years old to receive a 1% return on their investment in a business in which, among other things, a related person is involved. However, this proposed rule may not be fair or reasonable in practice. Consider, for example, a young entrepreneur, who is also a student, and develops a successful and profitable computer application by investing thousands of hours during her or his free time after school, and has a related person (e.g., a parent) invest start-up money in the business. Finance should consider whether this entrepreneur should only be allowed a 1% return, with the amount in excess of 1% being considered TOSI and thus taxed at the top marginal tax rate.

The following hypothetical situation illustrates some of the uncertainty regarding the intended scope of the proposed rules.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 8

Example 1

— Sister1 and Sister2, both university students between 18-24 years old, start a university tutorial business

— As with many small businesses owned by young people with no salary/wages or collateral to obtain a bank loan, Sister1 and Sister2 turn to their family for financial assistance

— Mother loans funds to Sister1 and Sister2 so they can incorporate Opco, pay rent for premises, purchase training materials, and cover other start-up costs

— Opco eventually becomes profitable, paying salary and dividends to Sister1 and Sister2, who use some of their earnings to repay Mother’s loan.

Under the proposed rules, Sister1 and Sister2 will be deemed not to have made capital contributions to their business under clause 120.4(1.1)(e)(ii)(B), because Mother, a related individual, lent them funds (see section 3.1.2 for our recommendation regarding this clause). It is unclear whether some or all of the salary or dividends received by Sister1 and Sister2 will be caught by the TOSI rules. In this case, we recommend that Mother should be able to make a loan that is comparable to an arm’s-length loan without having the sisters’ capital contributions discounted.

Under the proposed rules, a determination will need to be made regarding how “actively engaged” the sisters are to arrive at their labour contributions. Where the sisters hire tutors to teach students, it is unclear whether the sisters would be considered “actively engaged” in the business.

This hypothetical example is representative of the situation that many start-up businesses will face. Under the proposals, these businesses will face uncertainty and complexity with the proposed tax rules. Also, it appears these businesses will have to create additional documentation to track the source of funds, creating a further administrative burden.

Issues for labour and capital contributions by individuals 25 and older

For an individual who is 25 and older, it is not clear what Finance means by “engaged in the activities of the business”. Some clarification is needed to specify the threshold between an individual who is engaged compared to an individual who is not engaged.

For these individuals, another factor in determining whether an amount received is reasonable is the risks assumed related to the source business. It is unclear what would constitute an assumed risk and it is not certain how this risk can be translated into a quantified amount to determine if it is “reasonable”.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 9

The following hypothetical situation further illustrates the uncertainty regarding the intended scope of the proposed rules.

Example 2

— Mr. A, Mr. B and Ms. C are siblings and all are over 25 years old

— Mr. A, Mr. B and Ms. C each own one third of the shares of a manufacturing company (Opco) and receive dividends from those shares

— Mr. A, Mr. B and Ms. C received their shares for a nominal amount following an estate freeze involving their mother and father (Parents) several years ago

— Parents were former owners of Opco, but are no longer shareholders because their shares were redeemed several years ago

— None of Mr. A, Mr. B and Ms. C are active in the operations of the business.

— Opco’s operations are run by a third party arm’s-length (not related) management team.

Under the proposed legislation, the issue arises as to whether the dividends that Mr. A, Mr. B and Ms. C receive are “reasonable”.

Mr. A, Mr. B and Ms. C are specified individuals because, among other things, Opco was carried on in a prior year by a related individual; it does not matter that Parents are no longer involved in the business. The term “in the year or a previous year” in the definition of “specified individual” in subsection 120.4(1) may make this provision extremely broad, as it could require a taxpayer to trace the source of funds back to the inception of a business to see if these funds were generated from the same business which was operated by the related person in the past.

It appears that, since Mr. A, Mr. B and Ms. C are not involved in Opco’s activities, their labour contributions would likely be considered to be negligible. Further, their capital contributions would likely be considered to be a nominal amount, since their shares were acquired for a nominal amount following the freeze. The only other factor left to determine reasonableness in this situation is whether the siblings are considered to have assumed risks associated with the operation of Opco. The proposed legislation is unclear in this regard and thus, as taxpayers, Mr. A, Mr. B and Ms. C would have difficulty in complying with the legislation if enacted as drafted. KPMG questions whether the proposed rules were intended to be so broad as to capture this fact pattern.

In this situation involving a previous estate freeze, KPMG submits that Mr. A, Mr. B and Ms. C should be considered to have made the equivalent contributions previously made by their parents. A rule

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 10

should be introduced that is similar to the rule in clause 120.4(1.1)(e)(ii)(C) that, among other things, deems an individual to have made the same labour and asset contributions, and assumed the same risks in support of the business, as their deceased parent when the individual inherits property from the deceased parent. Essentially, Mr. A, Mr. B and Ms. C should be considered to have stepped into their parents’ shoes, so that they are not negatively affected by the TOSI rules.

3.1.2 Reasonableness test — Financial assistance The proposed legislation contains “specific anti-avoidance rules that apply to exclude certain labour and capital contributions from the reasonableness test” (as stated by Finance in its Explanatory Notes for clauses 120.4(1.1)(e)(ii)(A) and (B)).

An individual is deemed not to have contributed assets to a business where the assets are derived from an amount included in the individual’s split income, or the assets were acquired in connection with a person related to the individual becoming obligated to ensure repayment of a loan or other indebtedness incurred by the individual (e.g., a guarantee) or providing any other financial assistance to the individual (see clause 120.4(1.1)(e)(ii)(B)). See Example 1 above for an illustration of how this clause could negatively affect a small business owner.

KPMG recommendations

Small business owners are often unable to secure financing from an arm’s-length party. KPMG submits that the small business owner should not be penalized because they obtained a loan from a related person. If an interest rate is charged on a loan based on a prescribed interest rate, we submit that the TOSI rules should not apply.

3.1.3 Reasonableness test — Passive income As mentioned above, the proposed legislation contains specific anti-avoidance rules that apply to exclude certain labour and capital contributions from the reasonableness test.

An individual is deemed not have performed labour functions where the source business’ principal purpose is to derive income form property or where 50% or more of all income of the person (or partnership) for the year is from property or taxable capital gains from property, under proposed clause 120.4(1.1)(e)(ii)(A). As a result, it appears that passive income will be caught by the TOSI proposals.

KPMG recommendations

Since the Income Tax Act (R.S.C., 1985, c. 1 (5th Supp.)) already contains measures to prevent certain income splitting with income derived from passive investments, including in the attribution rules, and because Finance is consulting on tax regimes that could apply to passive income (see section 4), we recommend that Finance should not target passive income in its TOSI proposals.

3.1.4 Reasonableness test — Time period under consideration A “specified individual”, as defined in subsection 120.4(1) includes, among other things, an adult who has income from a business that is carried on “in the year or a previous year” by a related individual

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 11

or by a corporation of which the related individual was a specified shareholder or a “connected individual” (as defined in subsection 120.4(1)).

KPMG recommendations

It is not clear how far back in time a taxpayer (such as the taxpayers in Example 2 above) may need to look at to determine if a related person carried on a business. KPMG submits that Finance should consider introducing a safe harbour rule that specifies, for instance, the number of years that taxpayers would be required to consider when making this determination.

3.1.5 Reasonableness test — Amounts paid or that became payable In determining whether a specified individual is considered to have received an amount in excess of a “reasonable” amount, another factor that must be considered is, in general terms, having to take into account the total of all amounts that were paid or that became payable by any person for the benefit of the individual in respect of the business, under the definition of “split portion” in clause 120.4(1)(b)(iii)(D).

KPMG recommendations

Under the proposed legislation, it is unclear whether factors used to determine what is considered to be a reasonable amount must be considered on an annual or, as implied in clause 120.4(b)(iii)(D), a cumulative basis. A cumulative basis would require taking into account all years that an individual is a specified individual, since clause 120.4(b)(iii)(D) refers to “the total of all amounts that, before the end of the year, were paid or that became payable”. If these factors must be considered on a cumulative basis, Finance should consider introducing a safe harbour rule that specifies the number of years that taxpayers would be required to consider.

Finance should also consider clarifying that, where the factors are determined on a cumulative basis, whether an individual who received an unusually large (“unreasonable”) dividend in the past would be precluded from receiving “reasonable” salary or dividend in the current year (assuming the rules were effective currently).

3.1.6 Reasonableness test — Supporting documentation Business owners have substantial documentation requirements under the Income Tax Act and other legislation. The Government of Canada’s “Red Tape Reduction Plan,” recognizes that “cutting red tape” is a key priority. In particular, the government states:

If Canada is to maintain its competitive edge, increase productivity and spur innovation, we must constantly strive to improve the conditions for doing business. Given the current global uncertainty, it is more important than ever that Canadian businesses, indeed all Canadians, are able to operate in a climate of predictability, transparency and accountability.

KPMG recommendations

These proposed rules appear to require more documentation requirements, which seems to run contrary to the government’s “Red Tape Reduction Plan”. Specifically, the reasonableness test

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 12

necessitates a subjective analysis, requiring an understanding of how family members are involved in the business, among other things. Presumably, under these proposals, taxpayers will need some form of documentation to support the “reasonableness” of amounts received, including substantiating a specified individual’s labour and capital contributions, risks assumed, and other amounts paid or that became payable to them. Furthermore, what is reasonable in regards to labour, capital and risks assumed will vary by industry. Entrepreneurs need to focus on their business and should not have to devote more time to produce documentation above what is currently required to support their tax filings.

3.1.7 Reasonableness test — Ensuring consistent CRA assessments/audits The underlying factors that are required to determine whether an amount is “reasonable”, as outlined in section 3.1, are not easily quantifiable. In order to comply with the proposed TOSI rules, taxpayers and the CRA will have to perform a subjective analysis to determine whether taxpayers will be subject to the proposed tax regime.

KPMG recommendations

As previously noted, the proposed rules will make the tax system more complex and subjective. As a result, it may be challenging for the CRA to ensure that the “reasonableness” analysis will be applied consistently and fairly across the country. Taxpayers will need guidance from Finance and the CRA on how these tests will be applied and, given the subjective nature of the tests, safe harbour rules would be welcome.

3.1.8 Individuals not in the top marginal income tax bracket Finance states that it is concerned that a high-income individual facing a higher personal income tax rate may use income sprinkling to have income realized (e.g., via dividends or capital gains) by family members who are subject to lower personal tax rates or who may not be taxable at all.

KPMG recommendations

Although Finance specifies in the Consultation Paper that it intends the proposed rules to apply to high-income individuals, it appears that the rules can negatively affect anyone using a private corporation to “income sprinkle” even if the individuals involved are not in the top marginal income tax bracket.

Consider the following example. Two shareholders equally hold the common shares of ABC Co; one is actively involved in the day-to-day business operations (Ms. X) and another (Mr. X) is not involved at all. Ms. X and Mr. X are adult individuals who are married to each other and have no other sources of income. If ABC Co. paid a dividend of $150,000 on the common shares, then the passive shareholder, Mr. X, would pay tax on his $75,000 dividend at the top marginal rate to the extent that he is caught under the proposed TOSI rules. Had there been no splitting of the dividend with Mr. X, Ms. X would have paid tax at a lower marginal tax rate than Mr. X on his $75,000 portion of the dividend because all of her income would be subject to tax at a level below the top marginal tax rate (in 2017 the top federal tax bracket applies to income in excess of $202,800).

Finance should clarify whether this is intended.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 13

3.2 Lifetime Capital Gains Exemption (LCGE) Proposals We commend Finance for providing transitional rules in the proposed LCGE legislation. Proposed subsection 110.6(18.1) effectively allows certain individuals and trusts to elect to trigger a capital gain on “eligible property” (essentially defined to include qualified farm or fishing property and qualified small business corporation shares, under proposed 110.6(17.1)) anytime in 2018 so that the less restrictive pre-2018 rules apply to the capital gain.

3.2.1 Minors ineligible for LCGE Under paragraph 110.6(12)(a) of the proposed legislation, any capital gain that accrues on “eligible property” (as defined in proposed subsection 110.6(17.1)) before the year in which an individual turns 18 will not be eligible for the LCGE. It is not clear why the proposal will deny the LCGE to an individual under 18 years of age, especially where that individual has made significant contributions to increase the value of the business.

KPMG recommendations

Finance should reconsider whether minors should be automatically excluded from being able to claim the LCGE. These individuals should be able to access the LCGE using the same criteria deemed appropriate for individuals over 18.

3.2.2 LCGE and the “unreasonable” portion of a capital gain The concept of “split income” (and thus the reasonableness test that accompanies that term in the TOSI proposals) affects taxpayers’ eligibility to claim the LCGE. Under the proposed rule in paragraph 110.6(12)(d), an individual who is 18 years of age or older will have his or her LCGE deduction reduced by twice the amount of the individual’s taxable capital gain for the year, from a disposition of property in the year that would be included in his or her split income (as defined in newly expanded subsection 120.4(1)). Essentially, this means that an individual 18 years or older may not claim LCGE on the “unreasonable” portion of a capital gain.

KPMG recommendations Because the concept of “split income” in the TOSI proposals also applies under the LCGE proposals, the complexities we previously identified with the factors in the reasonableness test (see sections 3.1.1 to 3.1.7) apply equally to the LCGE proposals. As a result, KPMG recommends that Finance address these complexities.

3.3 Income Sprinkling Recommendations As a result of the issues and concerns we have identified, we recommend that Finance amend its legislative proposals on TOSI and those affecting taxpayer’s claims of the LCGE. Finance should consider simplifying the proposed rules and provide further guidance to achieve better consistency in interpreting “reasonableness”.

The TOSI and LCGE proposals are generally effective January 1, 2018. Given that these extremely complex and broad-based proposals adversely affect so many taxpayers, and given that these

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 14

changes were only announced on July 18, 2017, we submit that the timeframe given to comply with the rules is too brief. If Finance proceeds with these proposals, we recommend that they be effective January 1, 2019 at the earliest.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 15

4 Holding a Passive Investment Portfolio Inside a Private Corporation In its Consultation Paper, Finance asks for input on alternative methods it is proposing to tax investments inside a private corporation to neutralize what it believes is a financial advantage of investing passively through a private corporation.

Because corporate tax rates are generally lower than personal tax rates, there is an incentive to earn income in a private corporation and then retain the after-tax earnings in the corporation to earn passive income. The current tax system applies additional refundable taxes on passive income to theoretically equate the tax paid on the passive income through a corporation to what an individual in the top bracket would pay.

However, Finance concludes that there is no tax provision to align the after-tax earnings available to fund passive investments within a corporation with the after-tax amount that would be available to an individual to fund passive investments if such income was earned personally. As a result, using a corporation results in a greater amount of funds available for passive investment or savings.

To address this, Finance is proposing alternative tax regimes it believes will equate the after-tax savings available from earning passive income through a private corporation to the after-tax savings by an individual.

Finance has asked for comments on two alternative approaches to achieve this: the apportionment method and the elective method. In considering alternative methods to tax investments inside a private corporation, KPMG has prepared responses to the following questions that Finance poses in the Consultation Paper:

1. In your view, what approach would be preferable in order to improve the fairness of the tax systemwith respect to passive income?

2. If you prefer the apportionment or elective methods described in this paper, what criteria or broadconsiderations should the Government consider in selecting a method?

3. Regarding the tax treatment of corporations mostly engaged in passive investments, are thereconsiderations that you would like to bring to the Government’s attention?

4. In your view, what would be the appropriate scope of the new tax regime with respect to capitalgains? What criteria should be used by the Government in making this determination?

5. Are there key transition issues that you would like to bring to the Government’s attention?

6. Is there any reason why any aspects of the new rules should not apply to private corporationsother than Canadian-controlled private corporations (CCPCs)?

KPMG’s view is that, overall, the new proposed taxation regime will significantly increase tax for owners of private corporations that earn passive income through the corporation. In considering Finance’s proposals, KPMG submits that neither the apportionment method nor the elective method will fully achieve the government’s intentions. KPMG recommends that Finance conduct a comprehensive review of the private corporation tax system that provides an accurate comparison between an employee’s full, after-tax compensation package and a private corporation’s after-tax funds available from earning passive income. As well, this review should consider the different ways a private corporation deploys after-tax earnings in its active business. Further, KPMG believes that Finance should provide adequate time for transition to any other new system, and allow corporations

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 16

to maintain existing corporate balances and grandfather existing passive assets under the current integration system.

4.1 Tax Policy for Passive Income based on Equivalent Comparables In considering alternative methods to improve the fairness of the tax system with respect to passive income (Question 1), we submit that Finance should:

— Ensure that it is making an appropriate and complete comparison between passive income earned through a private corporation and passive income earned by a salaried employee, including the benefits each receives on an after-tax basis during times of active work and in retirement years

— Consider the effect of the new regime on existing small business corporate owners, including on the capital that they have accumulated to date and their ability to save for the future

— Consider how a private corporation deploys additional capital generated under the current system in an active business

— Consider situations where shareholders or owners may prefer to bonus out after-tax earnings to avoid the higher proposed passive income rates

— Consider whether the tax rates that apply to successful entrepreneurs still encourage businesses to set up in Canada.

Overall, we note that the proposed taxation regime will likely impose a very significant tax increase on passive income for owners of private corporations. Under Finance’s proposed systems, the effective tax rates on investment income of 73% and capital gains of 59% will negatively affect many owners of private corporations of all sizes (see Section 4.2 for the details of this calculation).

4.1.1 Passive income comparison — Private corporation owner vs. salaried employee Active income earned in a private corporation may provide the corporation with more after-tax earnings for passive investment compared to a salaried employee. However, any new tax policy should be based on a comparison that goes beyond looking at just an employee’s salary. To develop a tax policy that treats a salaried employee and private corporation owner the same in this situation, it is important to weigh the complete after-tax compensation package that an employee earns against the after-tax funds available from earning passive income in a private corporation.

Specifically, an employee may receive other employment benefits besides a salary, including:

— Medical benefit plans, medical leaves and employee assistance programs

— Registered pension plans and the ability to split income from such plans on retirement with a spouse

— Employment insurance

— Government-funded parental leave.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 17

In contrast, a private business owner has to self-fund these same costs and build up equivalent assets from the corporation’s after-tax earnings. As a result, Finance should compare an employee’s full, after-tax compensation package to a private corporation’s after-tax funds available from earning passive income, to ensure an accurate comparison.

Compared to employees, small business owners sometimes may not contribute as much to their RRSPs. As small-business owners establish their businesses, they often experience fluctuations in income requiring that they retain more income in the corporation until their business becomes established. Consequently, these small-business owners are unable to pay substantial salaries to themselves to generate maximum RRSP room in these early years. Instead, these owners rely on corporate savings to supplement future retirement requirements. These same business owners will not be able to split the dividend income they receive on retirement (in contrast with pension benefits from an RRSP, which can be split) with their spouse under the proposed TOSI rules. The introduction of the TOSI rules may tax “split” dividend income at the top marginal tax rate.

In comparison, an employee who has contributed to an RPP or RRSP can split the pension income with their spouse to ensure that they can access lower marginal tax rates in retirement.

Further, an RPP or an RRSP allows capital to accumulate on a tax-free basis, whereas any passive income generated in a private corporation is taxed on an annual basis as it is earned. Although a private corporation may have a larger initial amount of capital to invest in passive assets compared to an employee, the annual taxation of the investment income means that it will grow at a smaller rate than an RPP or RRSP. This should also be factored into any comparison.

KPMG recommendations

KPMG recommends that any new tax policy relating to the taxation of passive income should compare the complete compensation package that an employee earns (on an after-tax basis) against the after-tax funds available from earning passive income in a private corporation.

4.1.2 Effect on existing small-business owners’ retirement decisions Small-business owners who have based their investment and retirement decisions on the current rules may be disadvantaged under the proposed passive income rules. Specifically, they may not have any RRSP deduction room available to make up for retirement shortfalls for years where they did not contribute to an RRSP, either because they could not draw a salary from the corporation to generate “earned income” or because the current tax rules encouraged them to take dividends instead of a salary.

Further, if the proposed passive income regime is implemented, private company owners that intend to fund their retirement from the eventual sale of their business assets (e.g., goodwill, equipment, real property) may also find that, under the proposed regime, their retirement fund will be lower than anticipated. Under the proposed new regimes for passive income, capital gains realized by private corporations will no longer be subject to refundable taxes and eligible for capital dividend account (CDA) additions. Currently, the refundable tax and CDA treatment eliminate double taxation on the ultimate distribution of funds to private business owners. Any alternative tax system should ensure that private business owners are not taxed at a rate that is in excess of the rate at which an unincorporated person would be taxed (see section 4.2).

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 18

KPMG recommendations

As explained in section 4.5, it is critical that there be proper grandfathering of current investment assets in private corporations to ensure that investment and retirement decisions based on current are not disadvantaged. KPMG recommends that Finance consider addressing the issue of business owners who may not have any RRSP deduction room available by introducing a lifetime RRSP limit that is not tied to earned income.

KPMG also believes that the non-taxable portion of capital gains on the sale of business assets should continue to be added to the CDA account and generate refundable tax, even if the company does not make the passive investment company election (see section 4.4).

4.1.3 Deployment of capital generated by a private corporation’s active business KPMG believes that any tax policy changes should also take into account how a private business owner deploys the additional capital generated in his or her business under the current system. This is critical when the contemplated new regime will tax passive income at a high rate (approximating the highest personal marginal tax rate), with no refundable dividend tax on hand (RDTOH) in the future. In the Consultation Paper, Finance says that:

The proposed reforms would generally affect corporate owners who are setting aside some of their corporate profits for passive investments.

The initial benefit from the lower corporate tax rates would also be preserved when the corporate owner reinvests its passively–invested funds to expand the active business. This will help ensure that our corporate tax system continues to support economic growth and job creation.

Not all after-tax earnings of a private corporation are used to earn investment income on a long-term basis. In its early years, a start-up’s after-tax income is often used to mitigate income fluctuations as its product or service becomes established, and this income provides a cushion against ebbs in cash available to the business. As the business grows, additional capital provides an opportunity to self-finance future growth in the business. A small business does not always have access to the same sources for capital as a larger business, and might have no choice but to self-fund future investments (e.g., new equipment, larger facilities, or the start or acquisition of a new business). Obtaining bank funding often requires corporations to demonstrate they have additional funds available for unforeseen expenditures or business expansion.

While the current tax regime also taxes passive income in a private corporation at a higher rate than active income, the RDTOH system provides a refund of part of this tax to the corporation when the funds are distributed as taxable dividends. However, Finance is proposing a non-refundable permanent tax on passive income.

KPMG recommendations

KPMG recommends that Finance provide further examples of investments that would be considered to be part of an active business, rather than passive income, where the benefits of the lower corporate tax rates would be preserved. Further, to encourage private corporations to maintain capital in their corporations to grow and innovate, KPMG suggests that Finance could consider developing a safe harbour rule, such as allowing a certain amount or percentage of investment assets to be regarded as part of the capital of the active business and not as passive investments.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 19

4.1.4 Bonusing out after-tax earnings on an annual basis Currently, the passive investment rules apply additional refundable taxes on passive income to ensure that a corporation’s tax on the passive income approximates what an individual in the top tax bracket would pay. However, once the money is distributed from the company as dividends to individual shareholders, the dividend income is taxed at the individual’s current marginal tax rate. In effect, the current regime achieves integration by ensuring that the total tax paid by the corporation and shareholder on the passive income equals the amount that the individual would have paid if such income was earned directly.

Under the proposed regime, because all of the corporate tax is non-refundable, business owners may have to “bonus out” any after-tax income to avoid punitive tax rates. These owners will also be unable to recover the taxes on the bonus if the business loses money in the following years, giving them even less money to weather a downturn in their business.

KPMG recommendations

KPMG recommends that, in considering any new tax policy relating to the taxation of passive income, Finance consider whether making all of the corporate tax non-refundable may create an incentive for business owners to simply “bonus out” all after-tax income, thus discouraging small businesses to grow and innovate because it will leave them with less cash in the company to do so.

4.1.5 Tax rates for successful entrepreneurs in Canada Although the government says it is committed to innovation, and is maintaining a low small business tax rate on active income of CCPCs, the new rules may inadvertently discourage businesses from establishing themselves in Canada. This could happen if the capital gains tax rate on the sale of a business by a private corporation in Canada is higher than in another country that provides a preferential rate on capital gains realized on the sale of a business. Setting the highest personal tax rates in Canada at more than 50% (currently 53.53% in Ontario) may also discourage new entrepreneurs from moving to, or even remaining in, Canada. Finally, the proposed restrictions on the new definition of “split income” in the TOSI proposals may limit the LCGE for individuals who are not actively involved in the business but provide seed money.

KPMG recommendations

KPMG recommends that Finance clarify that its proposed restriction on the LCGE for individuals not actively involved in the business will not apply in situations where family members provide seed money in return for shares of a new entrepreneurial corporation.

KPMG also recommends that Finance should consider Canada’s high individual personal tax rates in designing any tax regime to ensure Canada is able to retain and attract young entrepreneurs.

4.2 Issues with Apportionment and Elective Methods In considering what criteria or broad considerations Finance should use in selecting either the apportionment or elective methods (Question 2), we have outlined our understanding of these two methods and their inherent deficiencies. Finance is also proposing that corporations mostly engaged

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 20

in passive investments be eligible to make a passive investment company election, to maintain the current refundable tax regime (see section 4.3).

Apportionment method

Under the apportionment method, a CCPC would have to track three separate pools:

— Income taxed at the small business corporate tax rate

— Income taxed at the general corporate tax rate

— Amounts contributed by shareholders.

The corporation’s annual passive investment income would be apportioned based on its cumulative share of these pools, which could be distributed, respectively, to shareholders as:

— Non-eligible dividends

— Eligible dividends

— Tax-free dividends (e. g., return of capital).

The apportionment method eliminates the RDTOH mechanism. Under this method, there will be no refundable taxes. This method will involve a significant amount of complexity, as taxpayers will have to accurately track the three pools and determine what is “passive income” that is not ancillary to the business.

Having so many variables determine a tax rate could make it difficult for a private business owner to forecast their after-tax cash flow, which is information that they must provide to their lenders.

Furthermore, such a complex system will make it difficult to comply with tax reporting requirements, possibly resulting in CRA reassessments if there is a reallocation between pools.

Elective method

As an alternative to the apportionment method, Finance is suggesting the elective method, under which private corporations would be subject to a default tax treatment unless they elect otherwise. Both options under the elective method would eliminate the RDTOH mechanism. The choice between the default tax treatment and the elective treatment would determine whether passive income would be treated as eligible or non-eligible dividends when distributed to shareholders, without the need for tracking. Under the default tax treatment, passive income earned in a CCPC would be subject to non-refundable taxes (generally equivalent to the top personal income tax rate) and dividends distributed from such income would, by default, be treated as non-eligible dividends. The small business deduction would be available for active income. Alternatively, corporations could choose, under the elective method, to pay out dividends from passive income as eligible dividends, but they would not be permitted to claim the small business deduction.

Under both new proposed systems, Finance has indicated that it will continue to treat capital gains as eligible for the 50% inclusion rate, but the non-taxable portion would no longer be added to the CDA.

As is illustrated in Appendix A, by removing the RDTOH regime, the elective method will result in an effective tax rate on fully distributed investment income of 73% (in Ontario), compared to the current

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 21

56% rate. It should be noted that, because integration does not work perfectly, it already costs 2.4% more to earn passive investment income through a corporation in Ontario.

For capital gains, the effective tax rate on a fully distributed basis using the elective method by default is 59% (in Ontario) due to the removal of the RDTOH system and the loss of the CDA treatment. This can be compared to the current 28% effective tax rate for capital gains earned through a private corporation (which is already 1.2% higher than what an individual in Ontario would pay on capital gains).

We suggest that a 31% increase in the capital gains rate in this situation may motivate private business owners to ensure that they do not earn any capital gains in a corporation, which in turn may mean that they undertake less risk taking for new business ventures.

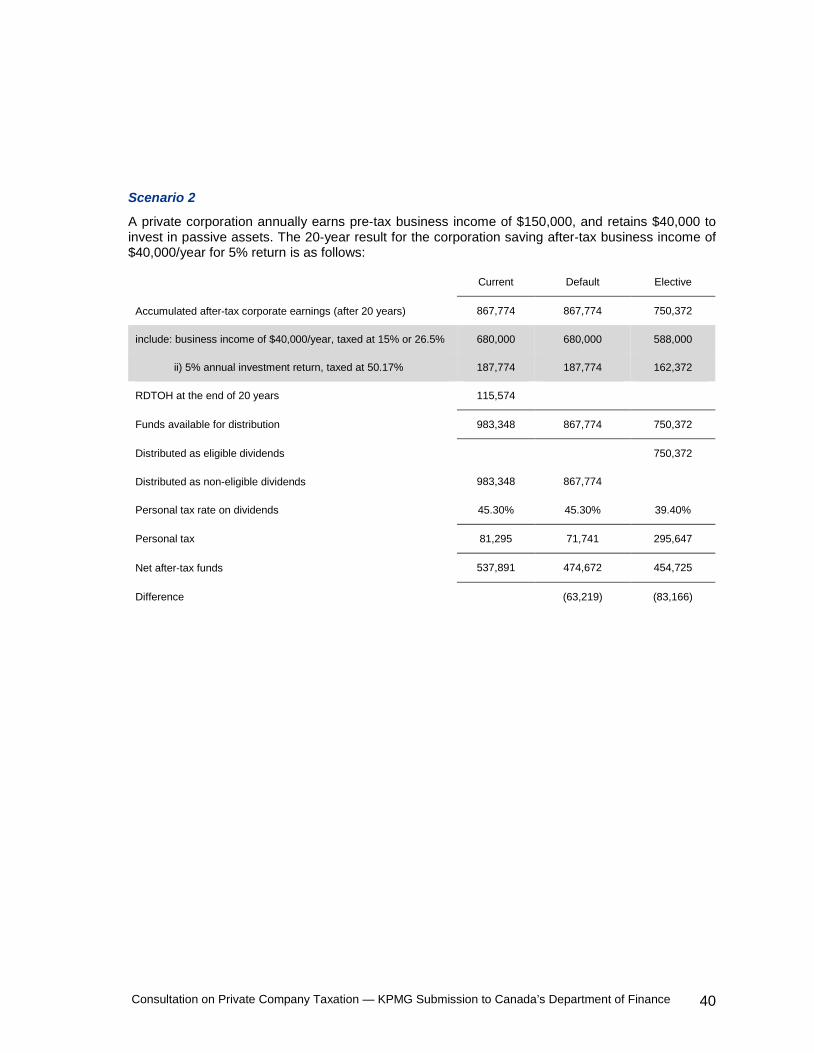

Further, our calculations show that the proposed passive income regime will increase the taxes payable by a private business owner who sets aside part of his or her earnings on an annual basis even at lower income levels compared to the current refundable system. In Appendix B, we illustrate two scenarios. In Scenario 1, a private corporation annually earns pre-tax business income of $73,000 a year and sets aside $7,300 a year, that will accumulate a 5% rate of return, taxed at the investment income tax rate of 50.17%. After 20 years, the amount is distributed. In this scenario, both options under the elective method result in less income available than the current integration method. In Scenario 2, a private corporation making $150,000 and setting aside $40,000 yields a similar result, leaving the taxpayer with less funds on a fully distributed basis.

KPMG recommendations

KPMG’s view is that neither the apportionment method nor the elective method will achieve the government’s stated objectives of neutrality, growth and promotion of innovation, since the flow-through effective tax rates on passive income are too high. If Finance introduces an alternative passive income taxation regime that is not based on integration, KPMG believes Finance should allow companies to opt out of the elective/apportionment method and in to the passive investment company election regime, where a business transitions from earning active income to passive income. For example, once a business is sold, taxpayers should be allowed to make the passive investment company election to opt in to the current refundable tax treatment for subsequent investment income earned on the sale proceeds.

Also, KPMG recommends that Finance clarify that, if the apportionment method is introduced, loans from shareholders and shareholder guarantees will be considered shareholder contributions for purposes of the apportionment method. Finance should also explain how intercompany loans are treated under the apportionment method and whether they would be considered a shareholder contribution.

KPMG recommends that Finance carefully consider the complexity of any proposed system to ensure that private company owners, who often have limited resources, can understand and comply with that system.

Finally, KPMG recommends that Finance review the taxation of investments held in private corporations as part of a comprehensive review of Canada’s tax system for owner-managers.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 22

4.3 Considerations for Corporations Mostly Engaged in Passive Investments Finance has asked for considerations for the tax treatment of corporations mostly engaged in passive investments (Question 3). Finance is contemplating allowing private corporations to elect to have all of their income taxed as passive investment income (to approximate the personal income tax rate), yet still be subject to a refundable tax regime. Where a taxpayer makes this election, all income earned within the private corporation would therefore be subject to refundable taxes. Similar to the current regime, these taxes would be refunded upon distribution of income as taxable dividends, effectively removing any deferral advantages.

It is not clear from the Consultation Paper which companies are considered eligible to make the passive investment company election. Specifically, it appears that a small business corporation that sells an active business asset (e.g. goodwill, equipment, real property) may not be eligible to make the passive investment company election. As such, the proposed rules would treat that capital gain as passive income, and subject that income to tax at significantly higher effective tax rates. For example, in Ontario, the owner of a small business corporation would effectively be taxed at 59% on capital gains on business assets, while an unincorporated business would be taxed at 27%.

For corporations holding passive investments, the Consultation Paper is also not clear on whether the non-taxable portion of all capital gains would be added to the company’s CDA.

KPMG recommendations

KPMG asks Finance to confirm which companies are allowed to make the passive investment company election, and to ensure that those companies receive the same tax treatment that CCPCs currently have on their passive income (i.e., Finance should maintain the existing RDTOH and CDA system).

KPMG believes that where entrepreneurial corporations take risks that result in capital gains, those capital gains should not be subject to more tax than gains on passive assets sold by a corporation that makes the passive investment company election. Taxing business assets in a private corporation at a higher rate will discourage entrepreneurship in Canada.

KPMG’s view is that a private corporation should be able to receive the equivalent tax treatment on business assets sold (e.g., CDA and RDTOH) as currently allowed, so that a small business owner will continue to be taxed at the same effective tax rates as an unincorporated owner of those assets.

4.4 Scope of the New Tax Regime With Respect to Capital Gains Finance asked for feedback on the appropriate scope of the new tax regime with respect to capital gains, and the criteria that Finance should use in making this determination (Question 4). Currently, gains arising on the sale of business assets such as goodwill and capital assets are treated as capital gains and taxed as passive income. Recaptured depreciation is currently treated as active business income if the deprecation was deducted against active income.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 23

KPMG recommendations

KPMG’s view is that the tax rate on income and capital gains arising from the sale of business assets (e.g., goodwill, equipment, real property) should not be increased under the new passive income rules. KPMG also believes that recaptured depreciation on business assets should continue to be treated as active business income. However, if Finance does apply the new passive income rules to the sale of business assets, Finance should consider introducing grandfathering rules for gains accrued before the proposals are implemented, on both passive and active capital assets.

Small business owners have made tax and investment decisions based on the current rules. If Finance adopts the apportionment method, some consideration should be given to treating existing corporate equity as a shareholder contribution for purposes of determining the effective “capital dividend” portion of future investment income allocations.

4.5 Key Transitional Issues Introducing a new corporate tax regime for passive investments will create certain transitional issues that Finance should account for, as it acknowledges in Question 5. Because all corporate investment decisions to date have been made on the basis of the existing taxation regime, Finance should consider preserving some tax treatments and introducing grandfathering rules to mitigate certain issues that may arise.

4.5.1 Existing corporate balances Corporations have made investments decisions on the premise that certain corporate balances, including RDTOH, CDA and the general rate income pool (GRIP), would continue to exist.

KPMG recommendations

KPMG submits that Finance should maintain existing corporate balances, including RDTOH, CDA and GRIP. These tax attributes are fundamental to the existing integration system.

Also, KPMG’s view is that companies that make the passive investment company election should not lose their GRIP balances.

4.5.2 Additional refundable tax For corporations that make the passive investment company election, the Consultation Paper states that, where the shareholders of the corporation are not individuals, amounts transferred to the corporation (e.g., as dividends) would be subject to an additional refundable tax, the intent of which would be to bridge the gap between the corporate tax rate and the personal income tax rate. It is not clear why the ownership of the company is relevant or whether this distinction was intended. It is also not clear whether Finance would apply the proposed additional refundable tax in the following situations:

— Corporate reorganizations where intercorporate dividends are not subject to subsection 55(2) by virtue of paragraph 55(3)(a) or 55(3)(b)

— Intercorporate dividends received, which are subject to Part IV tax.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 24

KPMG recommendations

KPMG recommends that Finance clarify the situations to which the proposed additional refundable tax may apply, as well as give consideration to exempting corporate reorganizations and intercorporate dividends already subject to Part IV tax.

4.5.3 Existing passive assets with accrued gains Taxpayers may dispose of passive assets with accrued gains before these rules are implemented to access the current RDTOH and CDA regime. In the Consultation Paper, Finance estimates that private corporations currently hold significant amounts of passive investments, and that these investments generated approximately $27 billion in passive income in 2015. To the extent those passive investments are marketable securities, a sale of these securities to lock into the existing tax rate could have a significant impact on the stock market.

KPMG recommendations

KPMG believes that Finance should grandfather the current capital gains tax treatment for existing passive assets with accrued gains. Doing so may mitigate any impact that the sale of these securities may have on the stock market.

4.5.4 Grandfathering investments In its Consultation Paper, Finance states that any new passive income regime would apply on a “go forward” basis, but does not provide further details. At a Canadian Tax Foundation (CTF) conference on September 25, 2017, Finance said that the intent of the proposals was not to impact the existing stock of savings and investment on those savings, and that Finance was looking at different options for grandfathering investments.

KPMG recommendations

KPMG recommends that Finance consider providing a transitional period for taxpayers to reorganize their corporate structures to maintain the current treatment afforded by the passive investment company election. Finance should allow existing passive investments to be transferred to a sole purpose investment corporation, which would be allowed to make the passive investment company election.

However, because some small business owners may not be able to afford establishing and maintaining a separate sole purpose investment corporation, we also recommend that Finance introduce a method for small business owners to segregate passive assets (creating notional tax balances) within an existing corporation, and having a V-day value so that owners can maintain the status quo treatment on unrealized gains, as of the date any legislation comes into force.

In considering grandfathering options, Finance should be aware that these transitional measures are likely to increase the accounting complexity for small business owners. These measures will also increase compliance costs.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 25

4.6 Applying the New Rules to Private Corporations Other Than CCPCs In Question 6, Finance asks for feedback on why any aspects of the new rules should not apply to private corporations other than CCPCs. In KPMG’s view, the proposed changes to the taxation of passive income may inadvertently discourage non-resident investment in Canada. Increasing the tax rate to more than 60% on passive income (including 25% withholding tax on repatriation) may convince non-resident investors to deploy their investment capital outside Canada to obtain a more optimal after-tax return.

KPMG recommendations

We recommend that the passive income proposals should not apply to non-CCPCs.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 26

5 Converting a Private Corporation's Regular Income into Capital Gains In its Consultation Paper, Finance asks for input on proposals intended to prevent corporate surplus from being extracted at preferential tax rates. To address this concern, Finance has released legislative proposals and Explanatory Notes, including changes to the existing anti-avoidance rule in section 84.1 and the introduction of an additional anti-avoidance rule in proposed section 246.1.

Finance notes that, currently, section 84.1 is intended to ensure that a corporate distribution is taxed as a taxable dividend when an individual sells shares of a corporation to a non-arm’s-length corporation. Otherwise, the corporation could pay out some portion of its surplus to the non-arm’s-length corporation as a tax deductible inter-corporate dividend, and the non-arm’s-length corporation could then use that surplus to pay the individual. In effect, the individual could receive the equivalent of a dividend (i.e., an amount distributed from the corporation and received by the individual) but would have a capital gain on the sale for income tax purposes.

Finance is concerned that taxpayers may convert a private corporation's regular income into capital gains, since capital gains are taxed at a lower rate than regular income, eligible dividends and non-eligible dividends. In the case of regular income, capital gains are taxed at only half the rate of regular income. The anti-surplus stripping rule in section 84.1 is generally intended to prevent corporate surplus from being extracted at the lower capital gains tax. Finance’s proposed changes are intended to prevent individual taxpayers from using non-arm’s-length transactions that “step-up” the cost base of shares of a corporation and avoid the application of section 84.1. Further, Finance has introduced a proposed separate anti-surplus stripping rule in section 246.1 to address tax planning that it believes circumvents the rules on the conversion of a private corporation’s surplus into tax-exempt, or lower-taxed, capital gains.

In considering Finance’s proposals, we have identified the following issues with the anti-surplus stripping rule in section 84.1 and other related matters:

— Transitional issues where it was intended that a pipeline strategy be implemented to avoid double tax

— Punitive consequences where a gain is recharacterized as a dividend under the TOSI rule in subsection 120.4(4)

— Increased tax cost to transferring a corporation between family members

— Increased tax cost arising on death

— Reduced ability to limit double tax as a consequence of death.

In considering Finance’s proposals, we have identified the following issues with the additional new surplus stripping anti-avoidance rule in proposed section 246.1:

— Uncertain scope of the rule

— Use of vague language

— Retroactive application for existing CDA balances

— CDA reduction

— One-sided adjustment.

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 27

Overall, KPMG submits that Finance should exempt certain intergenerational/sibling transfers from section 84.1 to facilitate the transfer of an operating business between family members. Further, Finance should limit the application of proposed section 84.1 where the non-arm’s-length ACB is created as a consequence of death. If the application of proposed section 84.1 is not limited on death, KPMG recommends that Finance:

— Introduce transitional rules for amended section 84.1 so that ACB resulting from subsection 70(5) is treated as “hard” ACB for purposes of section 84.1, and

— Modify or replace subsection 164(6) to simplify the process to create a dividend as a consequence of death.

KPMG believes that Finance should also simplify the process to increase the cost base of underlying corporate assets to the extent of the gain recognized on death on the deemed disposition of the shares of the corporation.

In addition, overall KPMG recommends that, for proposed section 246.1, Finance should draft a more targeted provision to provide more certainty on the scope of this rule, as well as on certain concepts and terms included within. As well, KPMG believes that certain transactions should be specifically excluded from the application of proposed section 246.1. If Finance is not willing to amend this proposed rule, KPMG recommends specific changes to the Explanatory Notes to provide more clarity for the tax authorities, courts and taxpayers. Further, KPMG recommends that Finance amend proposed section 246.1 so that it can only apply to CDA payments to the extent that a CDA balance (or a portion of it) was created on or after July 18, 2017. Also, transactions that were entered into before July 18, 2017 should not be subject to proposed section 246.1.

5.1 Surplus Stripping Anti-Avoidance Rule in Section 84.1 Finance announced changes to section 84.1 to prevent individuals from using non-arm’s-length transactions that “step-up” the ACB of shares of a corporation in order to avoid the application of section 84.1 on a subsequent disposition of the shares.

Specifically, the proposed rule in subparagraph 84.1(2)(a.1)(ii) excludes a gain created on a prior disposition of a share or a share for which the share was substituted by the individual, or an individual with whom the taxpayer did not deal at arm’s length from “hard” basis for the purpose of section 84.1.

5.1.1 Transitional issues There are many circumstances where an individual passed away before July 18, 2017, the intended pipeline planning has not been implemented and it is no longer possible to rely on subsection 164(6) to avoid double tax on death. These double tax situations may occur, for example, where:

— As at July 18, 2017, more than a year has passed since the time of death

— There was not sufficient time to implement subsection 164(6) planning after July 18, 2017 and within the first taxation year of the estate (for example, if the date of death was on July 20, 2016).

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 28

— Assets were distributed to beneficiaries with the intent that the beneficiaries implement pipeline planning, or

— The estate was not a graduated rate estate and so was not entitled to undertake subsection 164(6) planning.

KPMG recommendations

KPMG believes that Finance should amend subparagraph 84.1(2)(a.1)(ii) so that it does not reduce ACB (for purposes of section 84.1) for capital gains recognized as a consequence of death, where the death occurred prior to July 18, 2017.

5.1.2 Capital gains subject to proposed subsection 120.4(4)

Where proposed subsection 120.4(4) in the TOSI rules applies, an amount equal to twice the taxable capital gain is deemed to be a dividend that is not an eligible dividend. The deeming provision in subsection 120.4(4) does not apply for the purposes of subparagraph 40(1)(a)(i) and therefore “hard basis” would not be created for the purposes of proposed section 84.1. Accordingly, the same inherent gain could give rise to two dividends.

KPMG recommendations

KPMG recommends that Finance either modify subsection 120.4(4) to exclude a capital gain that arises as a consequence of death from the application of subsection 120.4(4). Alternatively, Finance may want to consider modifying subparagraph 84.1(2)(a.1)(ii) to exclude a capital gain that is subject to subsection 120.4(4).

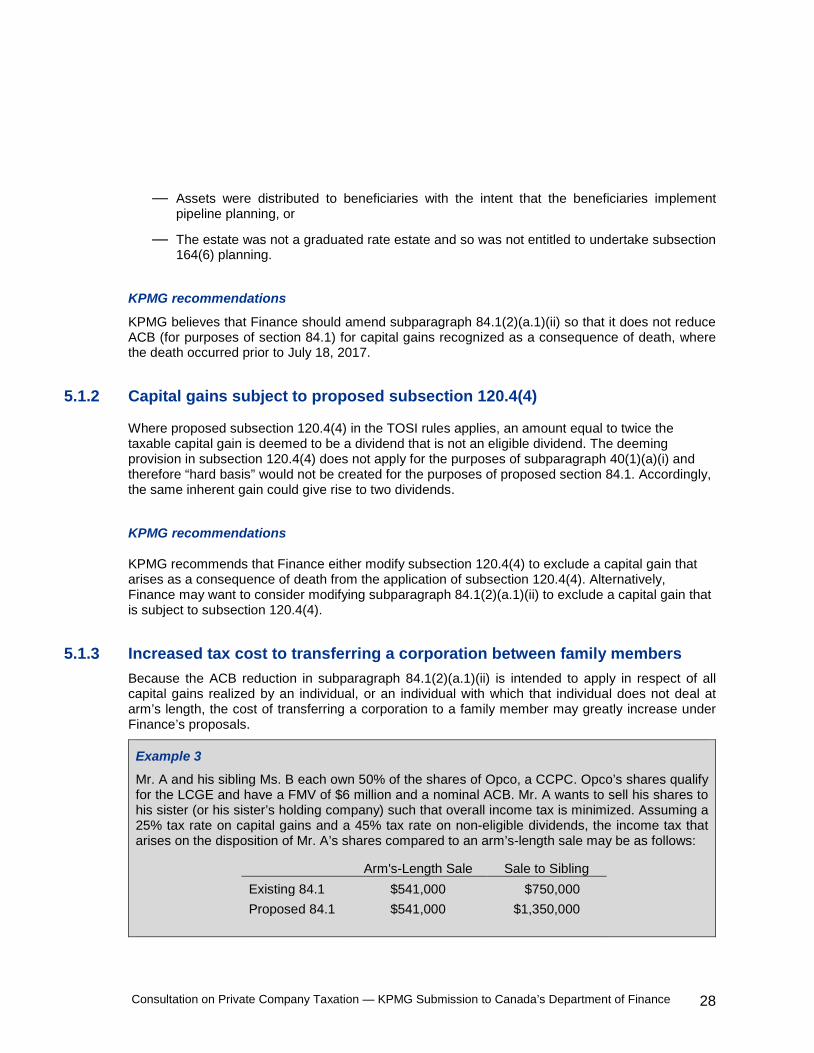

5.1.3 Increased tax cost to transferring a corporation between family members Because the ACB reduction in subparagraph 84.1(2)(a.1)(ii) is intended to apply in respect of all capital gains realized by an individual, or an individual with which that individual does not deal at arm’s length, the cost of transferring a corporation to a family member may greatly increase under Finance’s proposals.

Example 3

Mr. A and his sibling Ms. B each own 50% of the shares of Opco, a CCPC. Opco’s shares qualify for the LCGE and have a FMV of $6 million and a nominal ACB. Mr. A wants to sell his shares to his sister (or his sister’s holding company) such that overall income tax is minimized. Assuming a 25% tax rate on capital gains and a 45% tax rate on non-eligible dividends, the income tax that arises on the disposition of Mr. A’s shares compared to an arm’s-length sale may be as follows:

Arm's-Length Sale Sale to Sibling Existing 84.1 $541,000 $750,000 Proposed 84.1 $541,000 $1,350,000

Consultation on Private Company Taxation — KPMG Submission to Canada’s Department of Finance 29

In this example, there is an incremental cost of transferring a corporation’s shares to a non-arm’s-length individual (in this case, Ms. B). This is because it is not possible to use Opco’s funds to finance the acquisition by selling Opco’s shares to Ms. B’s acquisition company (or for her to transfer the shares to her acquisition company) without section 84.1 applying.

Finance’s Consultation Paper describes hallmarks of a genuine business transfer including that:

— The vendor ceases to have factual and legal control of the transferred business on the transfer

— The new owner intends to continue the business as a going concern long after its purchase — The vendor does not have any financial interest in the transferred business, and — The vendor does not participate in the management and operations of the business.

KPMG recommendations

KPMG recommends that Finance introduce an exception to proposed section 84.1 to facilitate “true” dispositions of shares of corporations between family members (both inter-vivos and testamentary). The provision could include the following or similar conditions:

— All or substantially all the value of the corporation is attributable to an active business

— The shareholder would have to sell a significant portion of their interest in the corporation

— The rate of return on any share/debt consideration would be limited.

Further, the provision should include an anti-avoidance rule to ensure that the exception to section 84.1 would not apply to a disguised surplus strip.