consumer lending group - wells fargo fargo 2014 investor day consumer lending group 2 consumer...

TRANSCRIPT

Consumer Lending Group

Avid Modjtabai, Senior EVP, Consumer Lending

Mike Heid, EVP, Home Lending

Tom Wolfe, EVP, Consumer Credit Solutions

May 20, 2014

© 2014 Wells Fargo & Company. All rights reserved.

Consumer Lending Group 1 Wells Fargo 2014 Investor Day

Business Overview and

Key Opportunities

Consumer Lending Group 2 Wells Fargo 2014 Investor Day

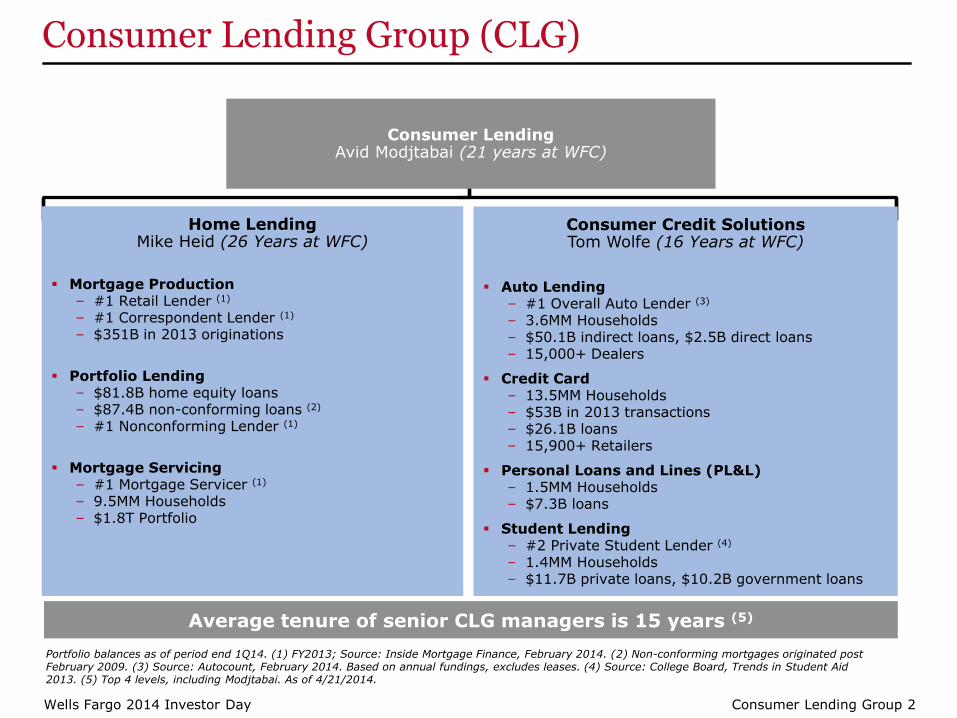

Consumer Lending Group (CLG)

Average tenure of senior CLG managers is 15 years (5)

Home Lending Mike Heid (26 Years at WFC)

Mortgage Production ‒ #1 Retail Lender (1)

‒ #1 Correspondent Lender (1) ‒ $351B in 2013 originations

Portfolio Lending ‒ $81.8B home equity loans ‒ $87.4B non-conforming loans (2)

‒ #1 Nonconforming Lender (1)

Mortgage Servicing ‒ #1 Mortgage Servicer (1) ‒ 9.5MM Households ‒ $1.8T Portfolio

Consumer Credit Solutions Tom Wolfe (16 Years at WFC)

Auto Lending ‒ #1 Overall Auto Lender (3) ‒ 3.6MM Households ‒ $50.1B indirect loans, $2.5B direct loans ‒ 15,000+ Dealers

Credit Card ‒ 13.5MM Households ‒ $53B in 2013 transactions ‒ $26.1B loans ‒ 15,900+ Retailers

Personal Loans and Lines (PL&L) ‒ 1.5MM Households ‒ $7.3B loans

Student Lending ‒ #2 Private Student Lender (4) ‒ 1.4MM Households ‒ $11.7B private loans, $10.2B government loans

Consumer Lending Avid Modjtabai (21 years at WFC)

Portfolio balances as of period end 1Q14. (1) FY2013; Source: Inside Mortgage Finance, February 2014. (2) Non-conforming mortgages originated post February 2009. (3) Source: Autocount, February 2014. Based on annual fundings, excludes leases. (4) Source: College Board, Trends in Student Aid 2013. (5) Top 4 levels, including Modjtabai. As of 4/21/2014.

Consumer Lending Group 3 Wells Fargo 2014 Investor Day

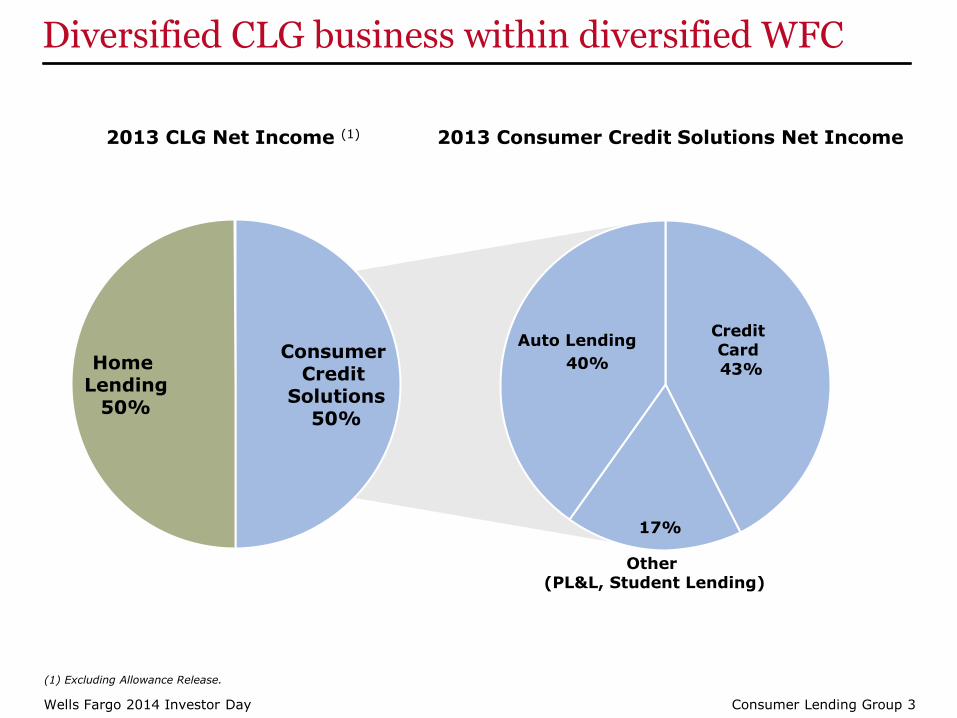

Diversified CLG business within diversified WFC

2013 CLG Net Income (1)

Home Lending

50%

Consumer Credit

Solutions 50%

43%

Credit Card

17%

Other (PL&L, Student Lending)

40%

Auto Lending

2013 Consumer Credit Solutions Net Income

(1) Excluding Allowance Release.

Consumer Lending Group 4 Wells Fargo 2014 Investor Day

Where we were in 2012

New group (August 2011) formed from 8 businesses

Holding leading market positions in most businesses

Accelerating momentum by integrating businesses, building new capabilities, and executing new strategies

Capturing large mortgage refinance opportunity in low rate environment

Managing through elevated credit losses and substantial liquidating portfolios

Understanding and operationalizing regulatory changes

Consumer Lending Group 5 Wells Fargo 2014 Investor Day

What we’ve accomplished since then

Managed successfully through the mortgage cycle

Outpaced competitors to become #1 auto lender

Grew card business and repositioned for additional growth

Executed on cross-sell opportunities

Delivered high quality business and asset growth

Strengthened credit and risk profile of businesses

Consolidated functions and systems to reduce complexity and gain efficiencies

Consumer Lending Group 6 Wells Fargo 2014 Investor Day

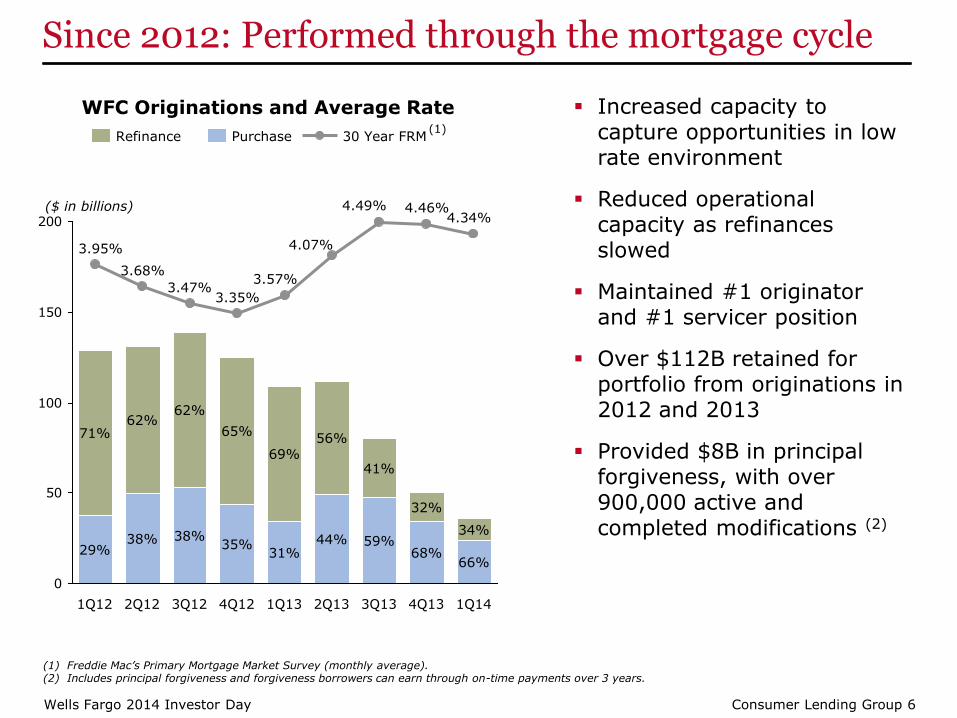

Since 2012: Performed through the mortgage cycle

Increased capacity to capture opportunities in low rate environment

Reduced operational capacity as refinances slowed

Maintained #1 originator and #1 servicer position

Over $112B retained for portfolio from originations in 2012 and 2013

Provided $8B in principal forgiveness, with over 900,000 active and completed modifications (2)

WFC Originations and Average Rate

(1) Freddie Mac’s Primary Mortgage Market Survey (monthly average). (2) Includes principal forgiveness and forgiveness borrowers can earn through on-time payments over 3 years.

(1)

0

50

100

150

200

2Q13 1Q13

3.68%

4.07%

1Q14

3.47%

32%

1Q12 4Q13 3Q12

71%

4.46%

38% 29%

3.57%

41%

2Q12 4Q12

56% 65%

68%

4.34%

31%

62%

44% 59% 38%

62%

69%

4.49%

34%

3.95%

3Q13

3.35%

35%

66%

Purchase Refinance 30 Year FRM

($ in billions)

Consumer Lending Group 7 Wells Fargo 2014 Investor Day

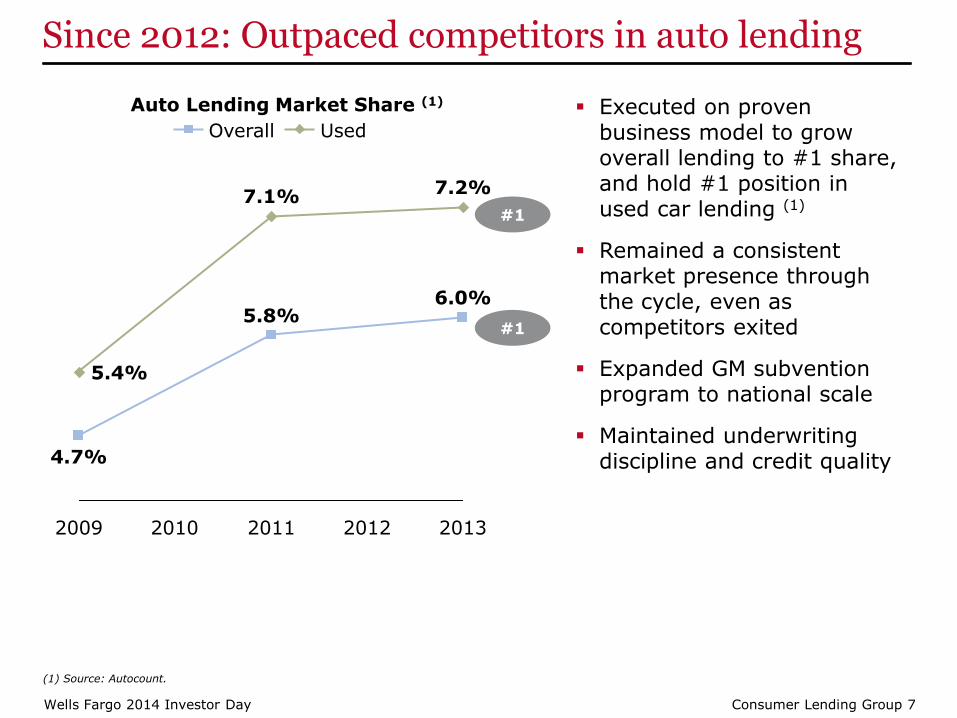

Since 2012: Outpaced competitors in auto lending

Auto Lending Market Share (1) Executed on proven

business model to grow overall lending to #1 share, and hold #1 position in used car lending (1)

Remained a consistent market presence through the cycle, even as competitors exited

Expanded GM subvention program to national scale

Maintained underwriting discipline and credit quality

(1) Source: Autocount.

2009 2010 2011 2012 2013

4.7%

6.0%

7.2% 7.1%

5.4%

5.8%

#1

#1

Overall Used

Consumer Lending Group 8 Wells Fargo 2014 Investor Day

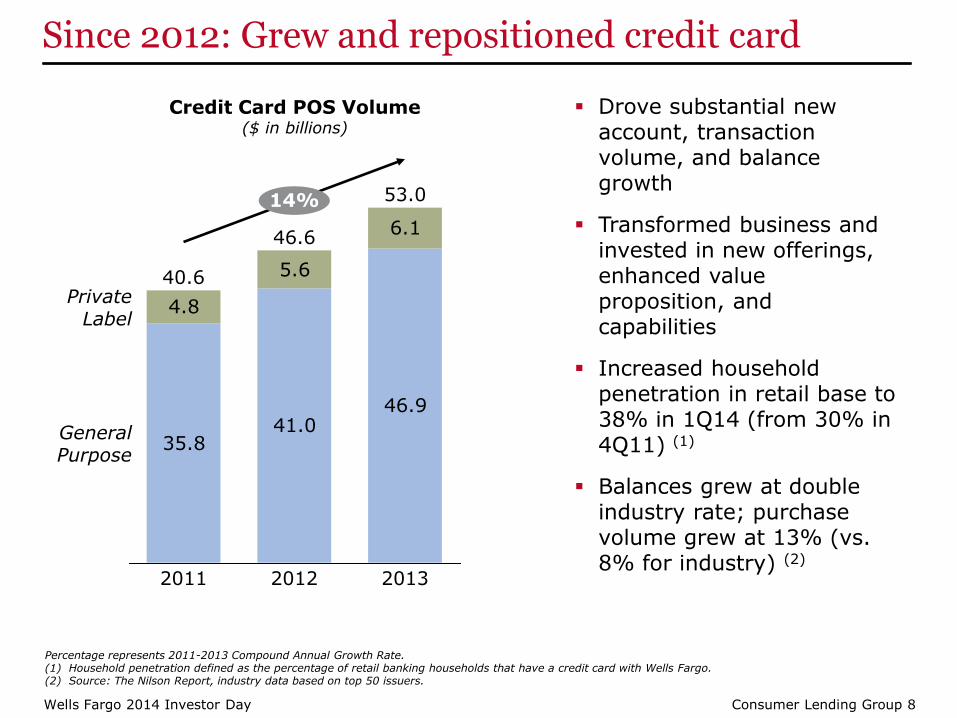

Drove substantial new account, transaction volume, and balance growth

Transformed business and invested in new offerings, enhanced value proposition, and capabilities

Increased household penetration in retail base to 38% in 1Q14 (from 30% in 4Q11) (1)

Balances grew at double industry rate; purchase volume grew at 13% (vs. 8% for industry) (2)

Since 2012: Grew and repositioned credit card

35.841.0

46.9

4.8

5.6

6.1

40.6

General Purpose

46.6

53.0 14%

Private Label

2013 2012 2011

Credit Card POS Volume ($ in billions)

Percentage represents 2011-2013 Compound Annual Growth Rate. (1) Household penetration defined as the percentage of retail banking households that have a credit card with Wells Fargo. (2) Source: The Nilson Report, industry data based on top 50 issuers.

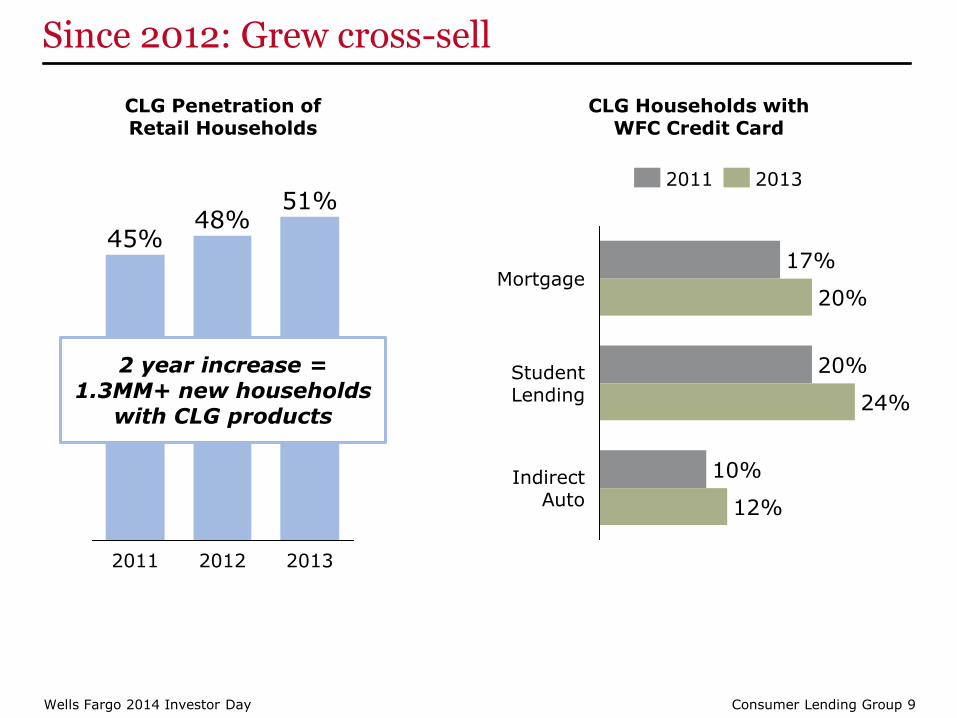

Consumer Lending Group 9 Wells Fargo 2014 Investor Day

Since 2012: Grew cross-sell

CLG Households with WFC Credit Card

45%

2013 2011

48%

2012

51%

CLG Penetration of Retail Households

Indirect Auto

20%

17%

24%

12%

20%

Mortgage

Student Lending

10%

2013 2011

2 year increase = 1.3MM+ new households

with CLG products

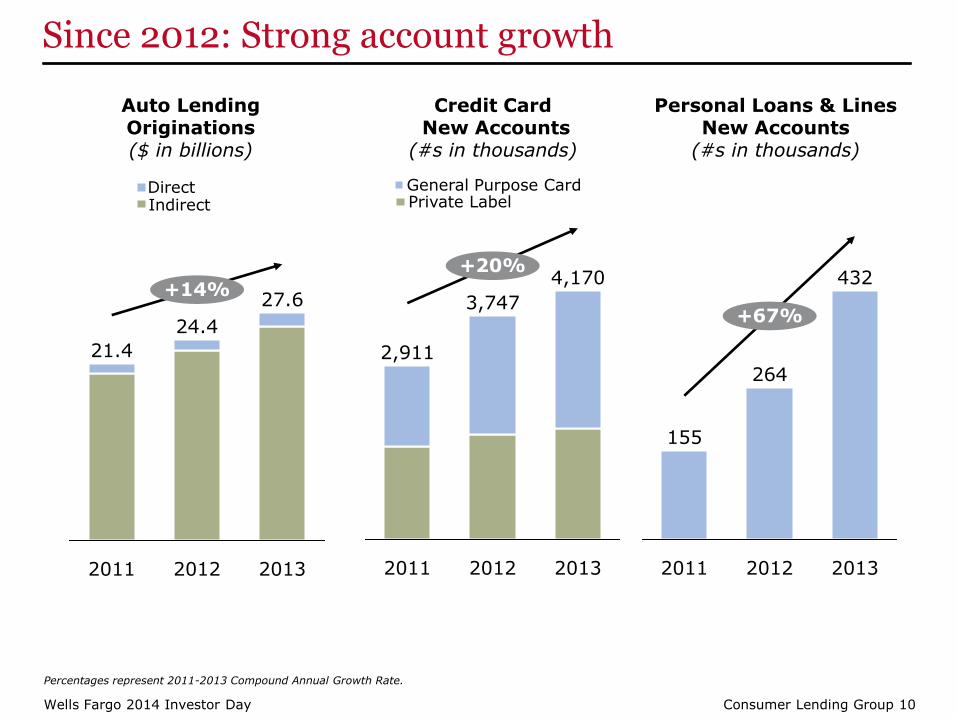

Consumer Lending Group 10 Wells Fargo 2014 Investor Day

Since 2012: Strong account growth

2013

4,170

2012

3,747

2011

2,911

+20%

Credit Card New Accounts

(#s in thousands)

Personal Loans & Lines New Accounts

(#s in thousands)

+67%

2013

432

2012

264

2011

155

Percentages represent 2011-2013 Compound Annual Growth Rate.

Private Label General Purpose Card

Auto Lending Originations ($ in billions)

Indirect Direct

+14%

2013

27.6

2012

24.4

2011

21.4

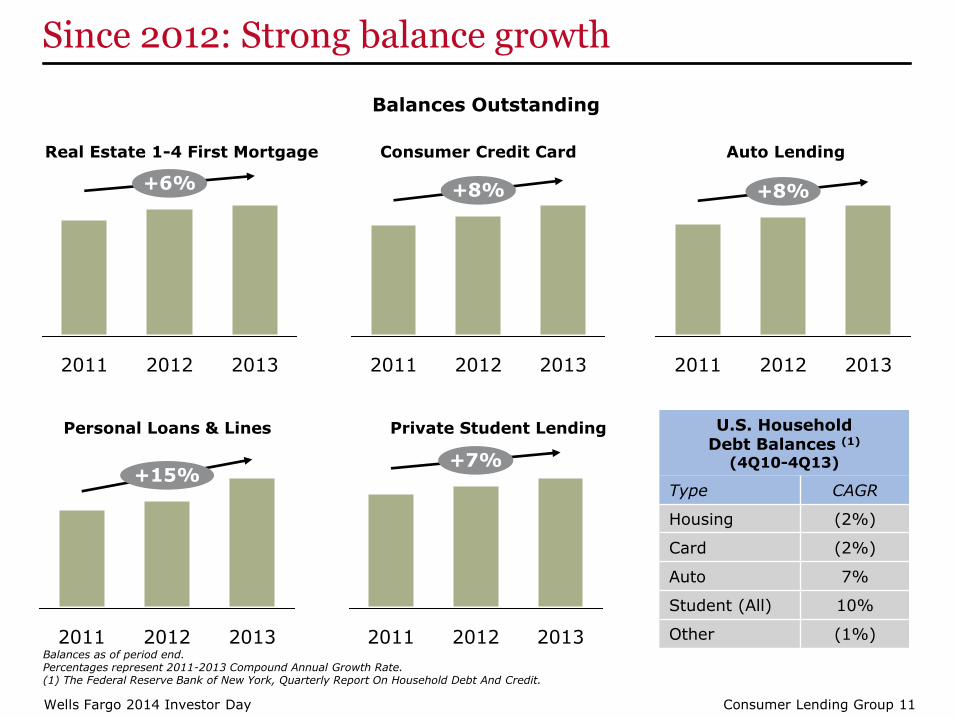

Consumer Lending Group 11 Wells Fargo 2014 Investor Day

Since 2012: Strong balance growth

+6%

2013 2012 2011

+8%

2013 2012 2011

Real Estate 1-4 First Mortgage Consumer Credit Card

Personal Loans & Lines Private Student Lending

Auto Lending

Balances Outstanding

+8%

2013 2012 2011

+15%

2013 2012 2011

+7%

2013 2012 2011

U.S. Household Debt Balances (1)

(4Q10-4Q13)

Type CAGR

Housing (2%)

Card (2%)

Auto 7%

Student (All) 10%

Other (1%) Balances as of period end. Percentages represent 2011-2013 Compound Annual Growth Rate. (1) The Federal Reserve Bank of New York, Quarterly Report On Household Debt And Credit.

Consumer Lending Group 12 Wells Fargo 2014 Investor Day

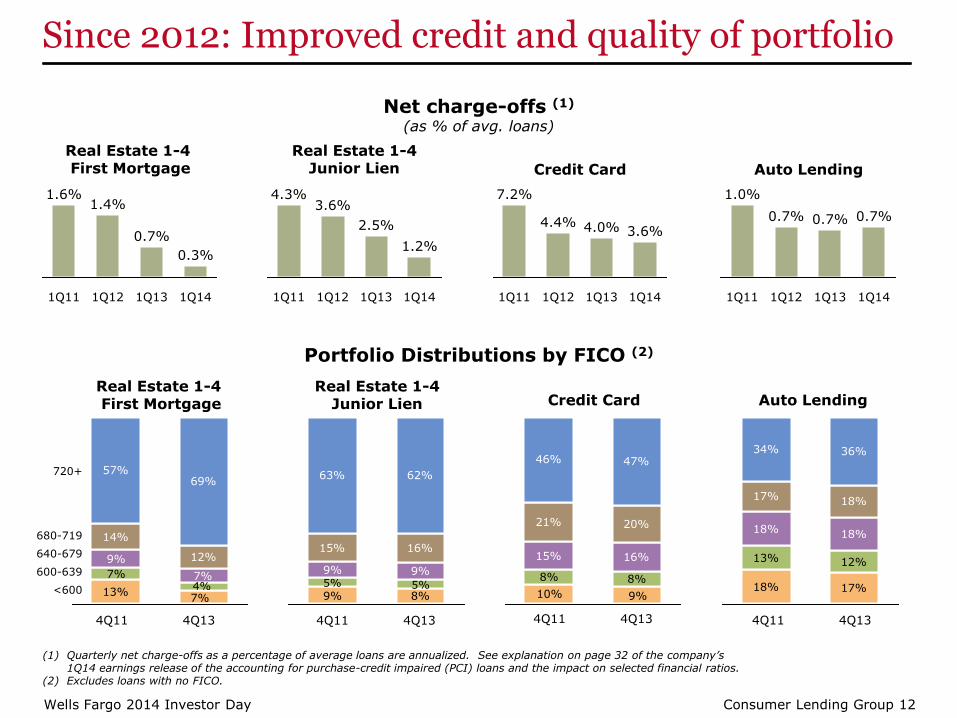

Since 2012: Improved credit and quality of portfolio

Net charge-offs (1) (as % of avg. loans)

1Q14

0.3%

1Q13

0.7%

1Q12

1.4%

1Q11

1.6%

Real Estate 1-4 First Mortgage

2.5%

1Q12

3.6%

1Q11

4.3%

1Q14

1.2%

1Q13

Real Estate 1-4 Junior Lien Credit Card Auto Lending

1Q14

3.6%

1Q13

4.0%

1Q12

4.4%

1Q11

7.2%

1Q14

0.7%

1Q13

0.7%

1Q12

0.7%

1Q11

1.0%

13%

9%

14%

12%

57%69%

7%

7% 7%

720+

680-719

640-679

600-639

<600

4Q13

4%

4Q11

Portfolio Distributions by FICO (2)

Real Estate 1-4 First Mortgage

Real Estate 1-4 Junior Lien Credit Card Auto Lending

(1) Quarterly net charge-offs as a percentage of average loans are annualized. See explanation on page 32 of the company’s 1Q14 earnings release of the accounting for purchase-credit impaired (PCI) loans and the impact on selected financial ratios.

(2) Excludes loans with no FICO.

9% 9%

15% 16%

8%9%

62%63%

5% 5%

15% 16%

9%10%

8%8%

20%21%

47%46%

18% 17%

13% 12%

18% 18%

17% 18%

34% 36%

4Q13 4Q11 4Q13 4Q11 4Q13 4Q11

Consumer Lending Group 13 Wells Fargo 2014 Investor Day

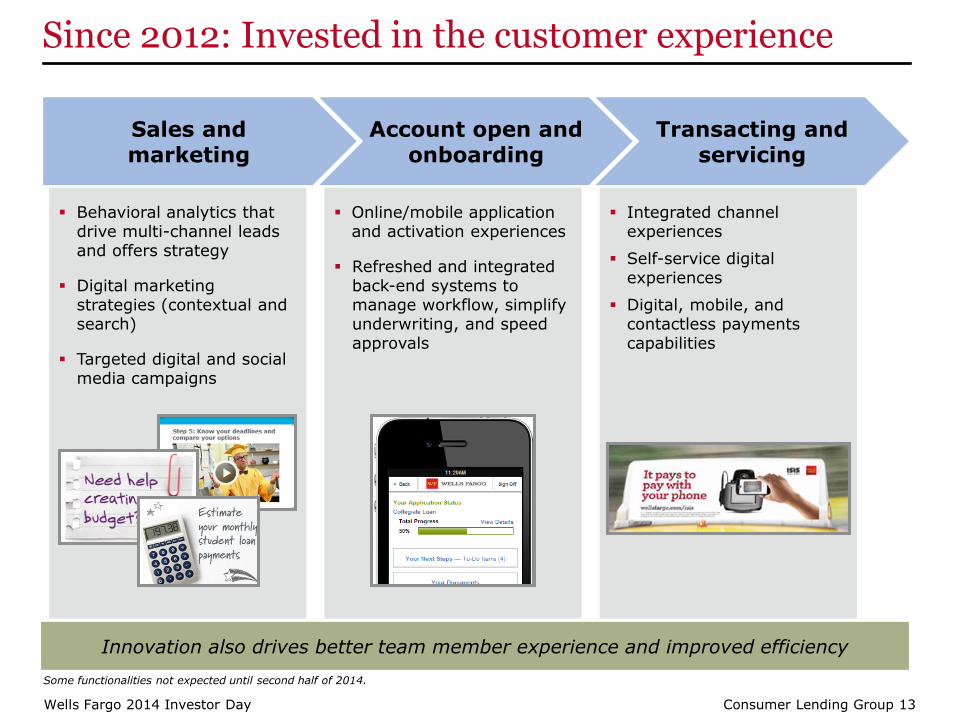

Since 2012: Invested in the customer experience

Sales and marketing

Account open and onboarding

Transacting and servicing

Behavioral analytics that drive multi-channel leads and offers strategy

Digital marketing strategies (contextual and search)

Targeted digital and social media campaigns

Online/mobile application and activation experiences

Refreshed and integrated back-end systems to manage workflow, simplify underwriting, and speed approvals

Integrated channel experiences

Self-service digital experiences

Digital, mobile, and contactless payments capabilities

Innovation also drives better team member experience and improved efficiency

Some functionalities not expected until second half of 2014.

Consumer Lending Group 14 Wells Fargo 2014 Investor Day

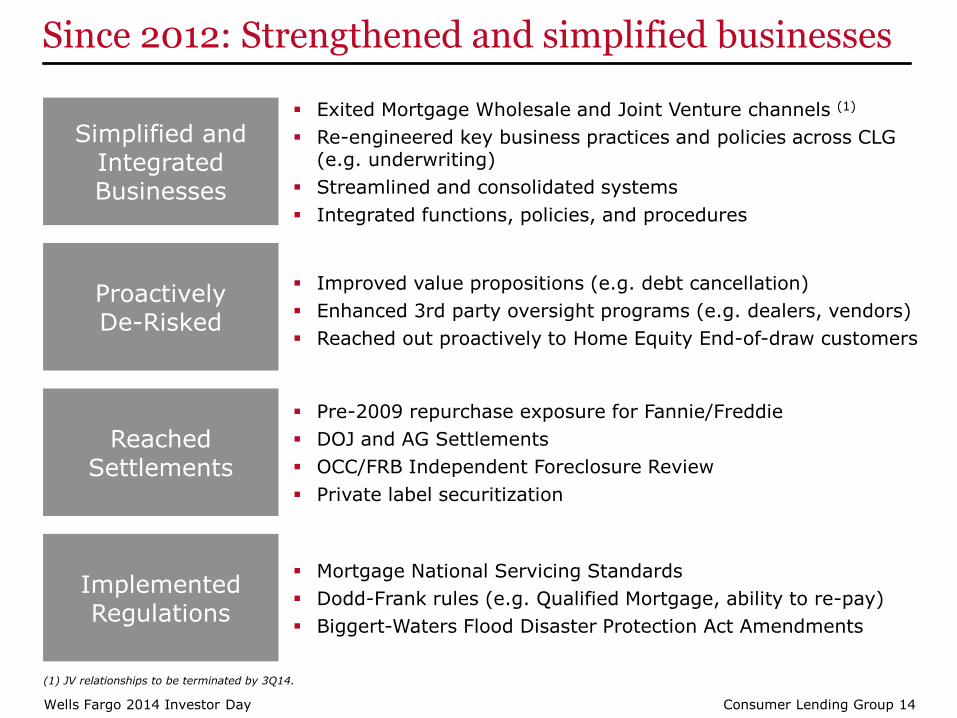

Since 2012: Strengthened and simplified businesses

Simplified and Integrated Businesses

Exited Mortgage Wholesale and Joint Venture channels (1)

Re-engineered key business practices and policies across CLG (e.g. underwriting)

Streamlined and consolidated systems

Integrated functions, policies, and procedures

Reached Settlements

Pre-2009 repurchase exposure for Fannie/Freddie

DOJ and AG Settlements

OCC/FRB Independent Foreclosure Review

Private label securitization

Proactively De-Risked

Improved value propositions (e.g. debt cancellation)

Enhanced 3rd party oversight programs (e.g. dealers, vendors)

Reached out proactively to Home Equity End-of-draw customers

Implemented Regulations

Mortgage National Servicing Standards

Dodd-Frank rules (e.g. Qualified Mortgage, ability to re-pay)

Biggert-Waters Flood Disaster Protection Act Amendments

(1) JV relationships to be terminated by 3Q14.

Consumer Lending Group 15 Wells Fargo 2014 Investor Day

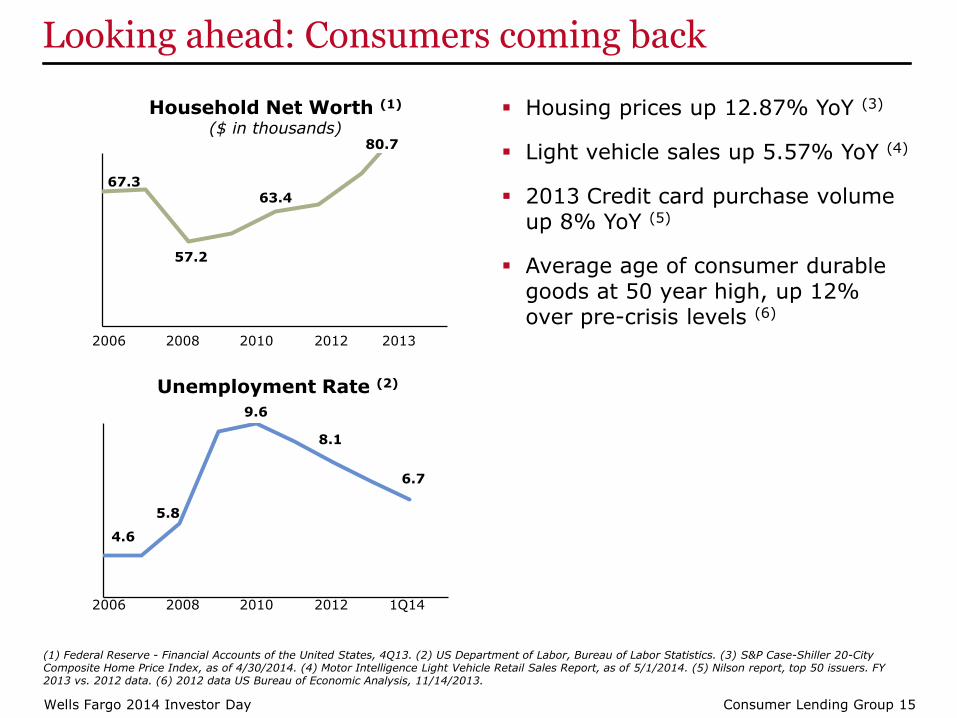

Looking ahead: Consumers coming back

Housing prices up 12.87% YoY (3)

Light vehicle sales up 5.57% YoY (4)

2013 Credit card purchase volume up 8% YoY (5)

Average age of consumer durable goods at 50 year high, up 12% over pre-crisis levels (6)

Household Net Worth (1) ($ in thousands)

57.2

2006 2013

80.7

2008

67.3

Unemployment Rate (2)

2012 2010

9.6

2006

4.6

8.1

6.7

1Q14

2010

63.4

(1) Federal Reserve - Financial Accounts of the United States, 4Q13. (2) US Department of Labor, Bureau of Labor Statistics. (3) S&P Case-Shiller 20-City Composite Home Price Index, as of 4/30/2014. (4) Motor Intelligence Light Vehicle Retail Sales Report, as of 5/1/2014. (5) Nilson report, top 50 issuers. FY 2013 vs. 2012 data. (6) 2012 data US Bureau of Economic Analysis, 11/14/2013.

2008

2012

5.8

Consumer Lending Group 16 Wells Fargo 2014 Investor Day

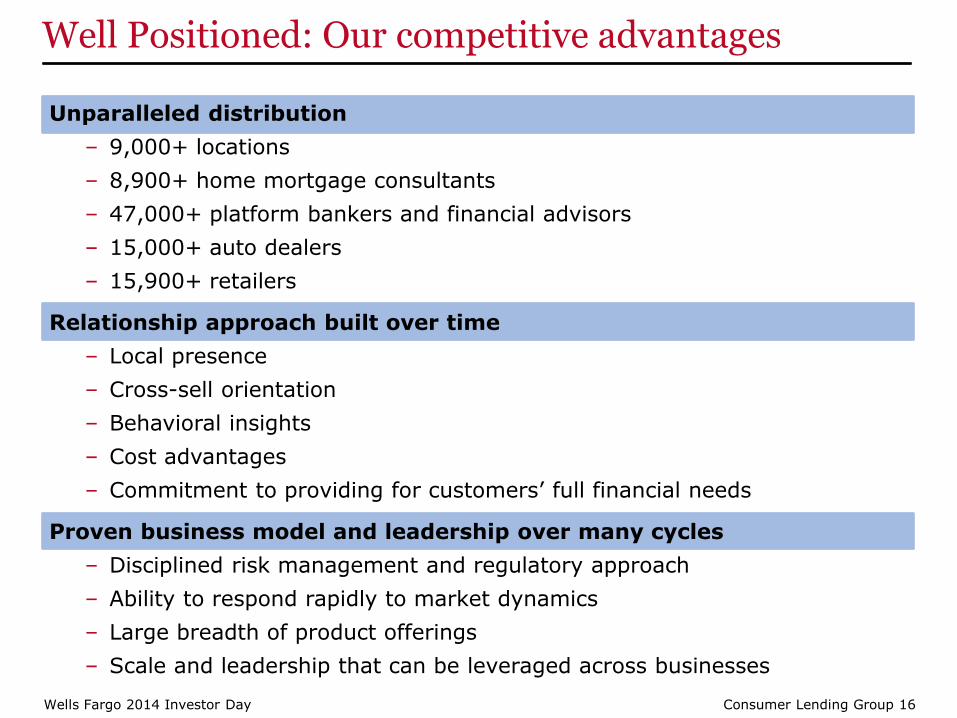

Unparalleled distribution

– 9,000+ locations

– 8,900+ home mortgage consultants

– 47,000+ platform bankers and financial advisors

– 15,000+ auto dealers

– 15,900+ retailers

Relationship approach built over time

– Local presence

– Cross-sell orientation

– Behavioral insights

– Cost advantages

– Commitment to providing for customers’ full financial needs

Proven business model and leadership over many cycles

– Disciplined risk management and regulatory approach

– Ability to respond rapidly to market dynamics

– Large breadth of product offerings

– Scale and leadership that can be leveraged across businesses

Well Positioned: Our competitive advantages

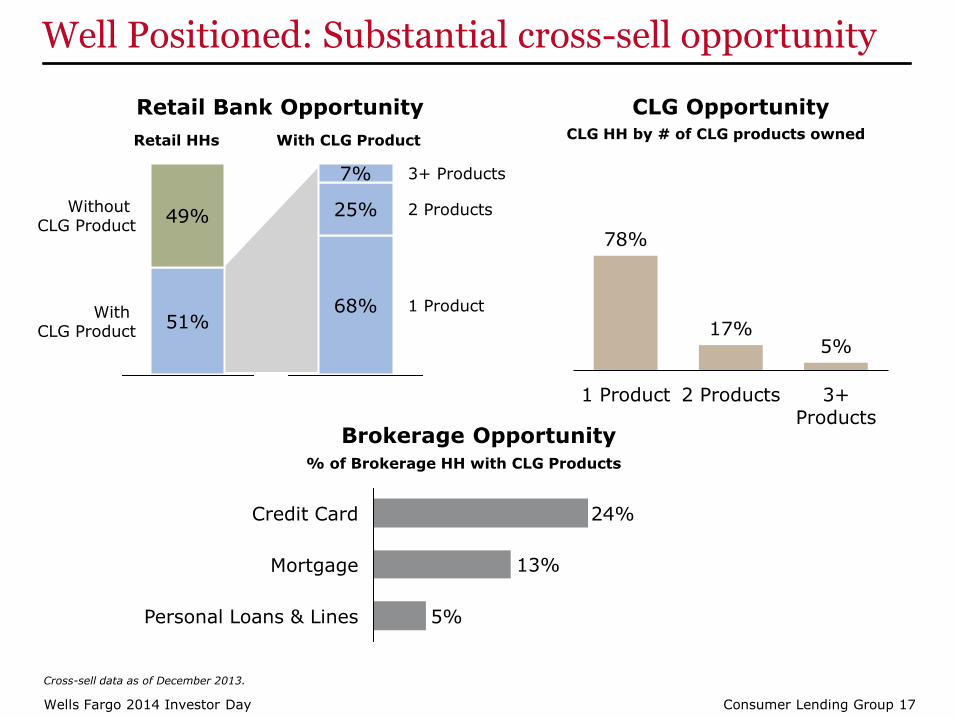

Consumer Lending Group 17 Wells Fargo 2014 Investor Day

Without CLG Product

With CLG Product

49%

51%

3+ Products

2 Products

1 Product

7%

25%

68%

Well Positioned: Substantial cross-sell opportunity

Retail Bank Opportunity

Retail HHs With CLG Product

Brokerage Opportunity

Personal Loans & Lines 5%

Mortgage 13%

Credit Card 24%

% of Brokerage HH with CLG Products

CLG Opportunity CLG HH by # of CLG products owned

Cross-sell data as of December 2013.

78%

17% 5%

1 Product 2 Products 3+Products

Consumer Lending Group 18 Wells Fargo 2014 Investor Day

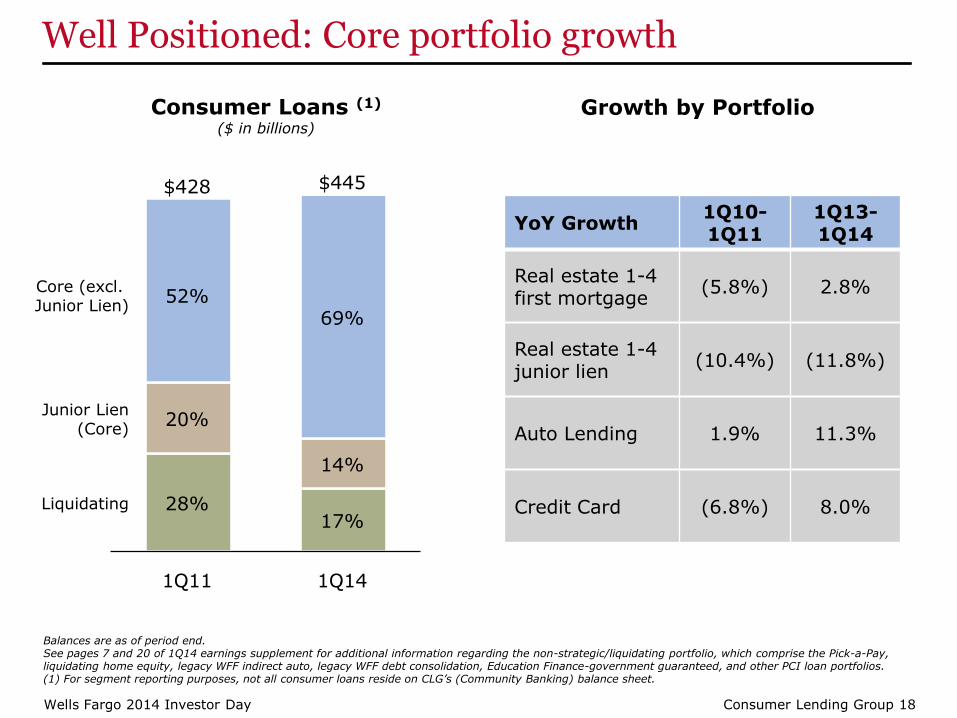

Well Positioned: Core portfolio growth

$445 $428

Liquidating

Junior Lien (Core)

Core (excl. Junior Lien)

1Q14

52%

20%

28%

1Q11

69%

14%

17%

Consumer Loans (1) ($ in billions)

Balances are as of period end. See pages 7 and 20 of 1Q14 earnings supplement for additional information regarding the non-strategic/liquidating portfolio, which comprise the Pick-a-Pay, liquidating home equity, legacy WFF indirect auto, legacy WFF debt consolidation, Education Finance-government guaranteed, and other PCI loan portfolios. (1) For segment reporting purposes, not all consumer loans reside on CLG’s (Community Banking) balance sheet.

YoY Growth 1Q10- 1Q11

1Q13- 1Q14

Real estate 1-4 first mortgage

(5.8%) 2.8%

Real estate 1-4 junior lien

(10.4%) (11.8%)

Auto Lending 1.9% 11.3%

Credit Card (6.8%) 8.0%

Growth by Portfolio

Consumer Lending Group 19 Wells Fargo 2014 Investor Day

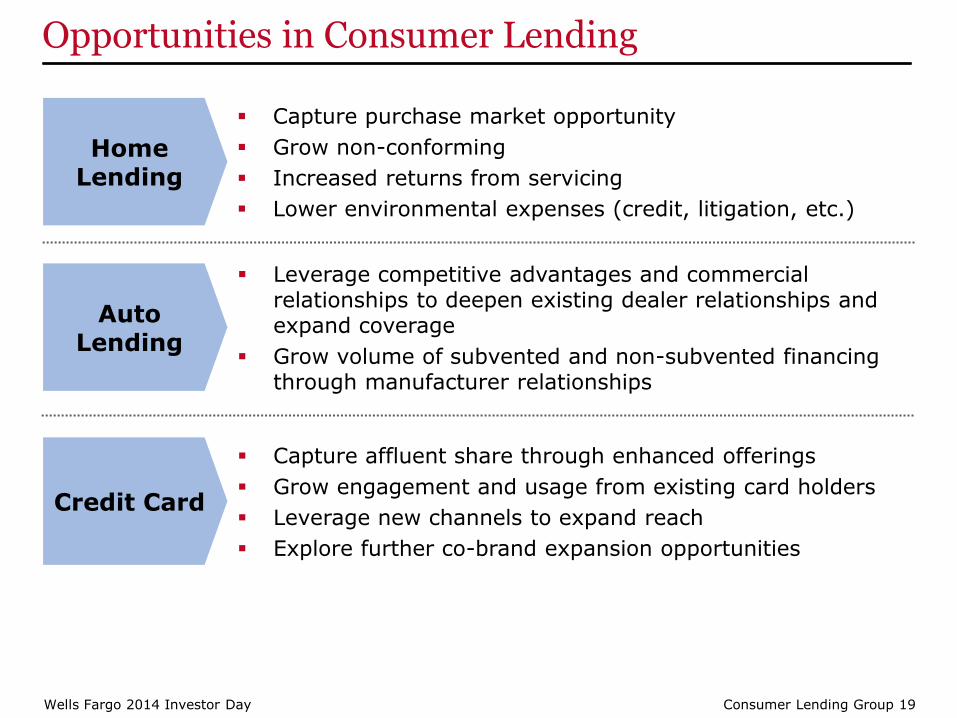

Opportunities in Consumer Lending

Home Lending

Capture purchase market opportunity

Grow non-conforming

Increased returns from servicing

Lower environmental expenses (credit, litigation, etc.)

Leverage competitive advantages and commercial relationships to deepen existing dealer relationships and expand coverage

Grow volume of subvented and non-subvented financing through manufacturer relationships

Auto Lending

Capture affluent share through enhanced offerings

Grow engagement and usage from existing card holders

Leverage new channels to expand reach

Explore further co-brand expansion opportunities

Credit Card

Consumer Lending Group 20 Wells Fargo 2014 Investor Day

Home Lending

Consumer Lending Group 21 Wells Fargo 2014 Investor Day

Mortgages are important to our customers and provide cross-sell opportunities

- Retail bank customers that are non-homeowners have an average of 4.75 products with WFC; customers with a mortgage have 7.61 products (excluding the mortgage)

The mortgage business provides an earning stream for Wells Fargo and has been profitable every year since 1990 (1)

We have a committed, long-term perspective to the mortgage business

- Only firm with a top 5 ranking in both originations and servicing every year since 1994 (2)

Home Lending is a great business

(1) Core mortgage banking business, excluding liquidating portfolios. (2) Inside Mortgage Finance.

Consumer Lending Group 22 Wells Fargo 2014 Investor Day

Keys to success

Ability to lead at scale in origination and servicing

Long-term commitment to the business

Ability to manage origination capacity through rate cycles

Disciplined sales and management culture

Leading Retail origination franchise

Strong operational, credit, and interest rate risk management skills

Experienced leadership team

These capabilities have driven our success in the past and remain the keys to our future success

Consumer Lending Group 23 Wells Fargo 2014 Investor Day

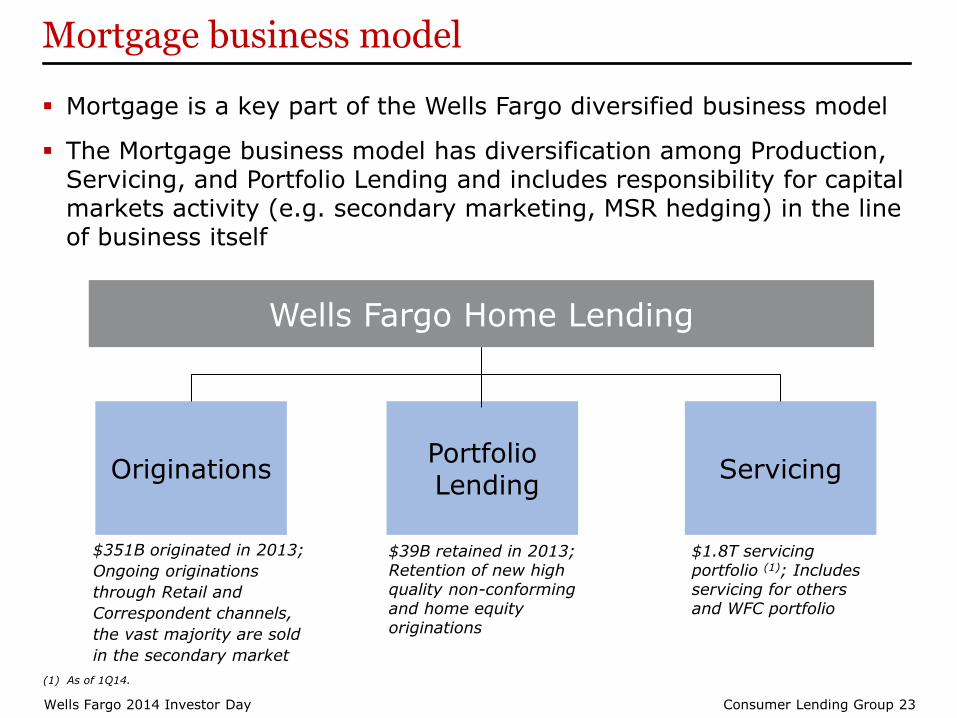

Mortgage is a key part of the Wells Fargo diversified business model

The Mortgage business model has diversification among Production, Servicing, and Portfolio Lending and includes responsibility for capital markets activity (e.g. secondary marketing, MSR hedging) in the line of business itself

Mortgage business model

Portfolio Lending

Originations Servicing

Wells Fargo Home Lending

$351B originated in 2013;

Ongoing originations

through Retail and

Correspondent channels,

the vast majority are sold

in the secondary market

$39B retained in 2013; Retention of new high quality non-conforming and home equity originations

$1.8T servicing portfolio (1); Includes servicing for others and WFC portfolio

(1) As of 1Q14.

Consumer Lending Group 24 Wells Fargo 2014 Investor Day

How we think about the origination business

Origination Returns

- Revenue and expense levels require active and aggressive management

- New product pricing needs to result in adequate return for the risk in the business

Why Scale Matters in Originations

- Wells Fargo’s brand and customer base provides significant opportunities

- Provides ability to attract and retain sales team and leadership team

- Provides ability to invest in the business “through all cycles”

- Regulations have increased costs; larger scale enables leveraging of fixed cost base

- Enables strong vendor relationships

Originations are priced to generate appropriate returns; being the largest mortgage lender in the country provides advantages

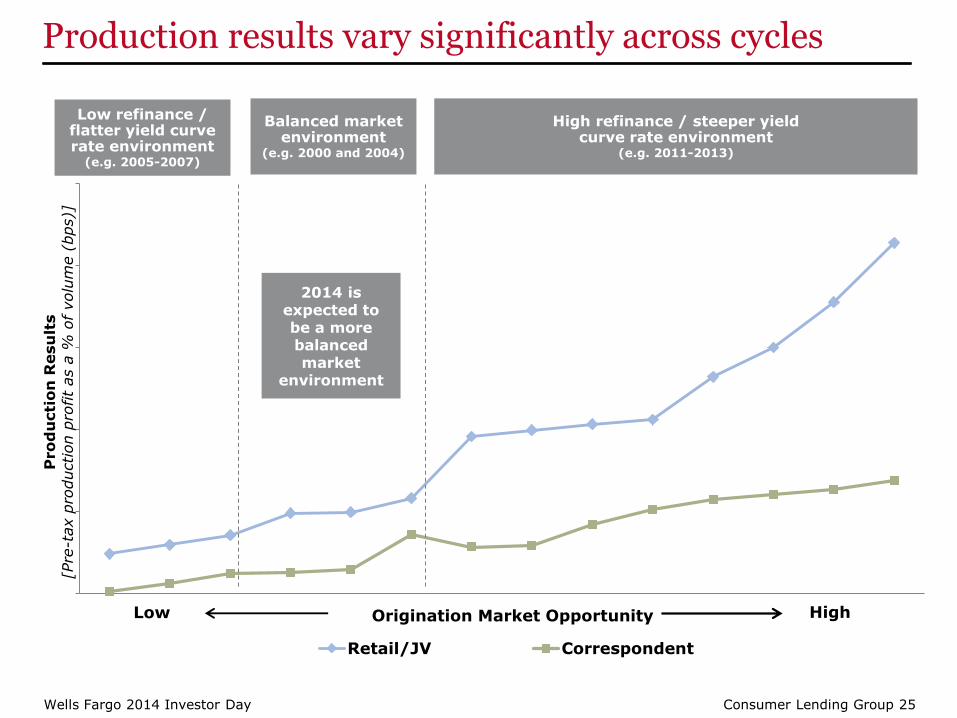

Consumer Lending Group 25 Wells Fargo 2014 Investor Day

Pro

du

cti

on

Resu

lts

[Pre

-tax p

roduction p

rofit

as a

% o

f volu

me (

bps)]

Origination Market Opportunity

Retail/JV Correspondent

Production results vary significantly across cycles

Low High

Low refinance / flatter yield curve rate environment

(e.g. 2005-2007)

Balanced market environment

(e.g. 2000 and 2004)

High refinance / steeper yield curve rate environment

(e.g. 2011-2013)

2014 is expected to be a more balanced market

environment

Consumer Lending Group 26 Wells Fargo 2014 Investor Day

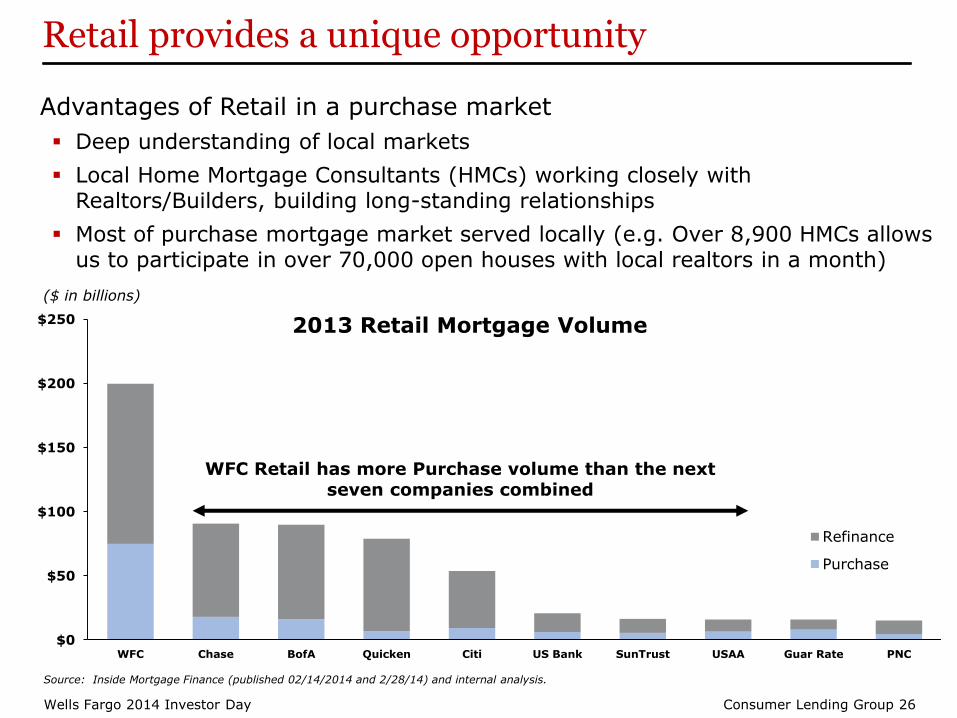

Retail provides a unique opportunity

$0

$50

$100

$150

$200

$250

WFC Chase BofA Quicken Citi US Bank SunTrust USAA Guar Rate PNC

Refinance

Purchase

($ in billions)

Advantages of Retail in a purchase market

Deep understanding of local markets

Local Home Mortgage Consultants (HMCs) working closely with Realtors/Builders, building long-standing relationships

Most of purchase mortgage market served locally (e.g. Over 8,900 HMCs allows us to participate in over 70,000 open houses with local realtors in a month)

2013 Retail Mortgage Volume

WFC Retail has more Purchase volume than the next seven companies combined

Source: Inside Mortgage Finance (published 02/14/2014 and 2/28/14) and internal analysis.

Consumer Lending Group 27 Wells Fargo 2014 Investor Day

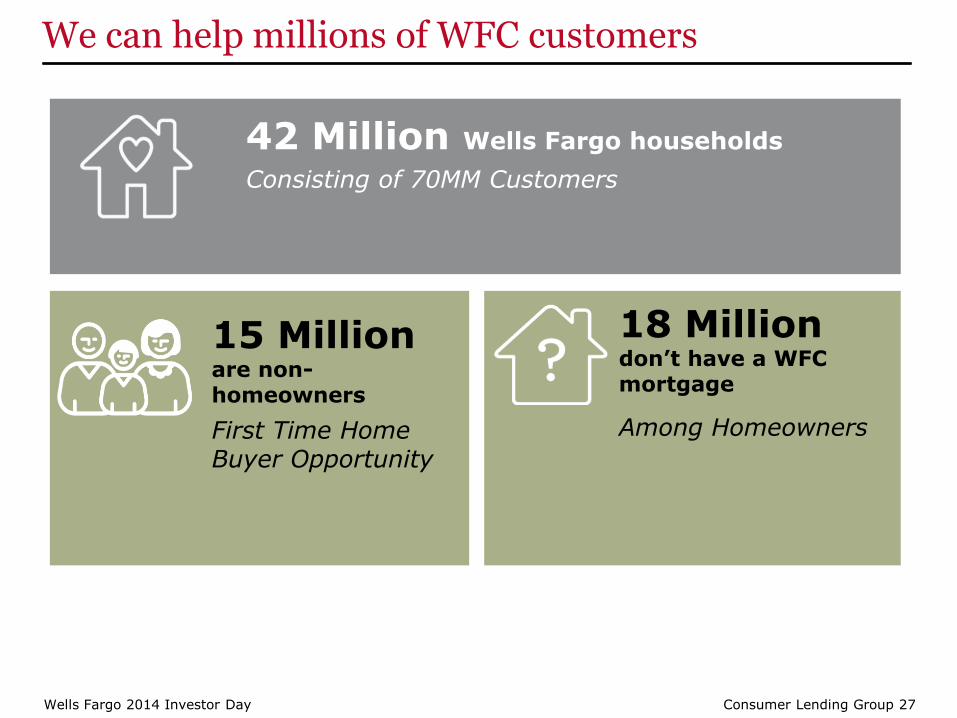

We can help millions of WFC customers

18 Million don’t have a WFC mortgage

Among Homeowners

15 Million are non-homeowners

First Time Home Buyer Opportunity

42 Million Wells Fargo households

Consisting of 70MM Customers

Consumer Lending Group 28 Wells Fargo 2014 Investor Day

How we think about portfolio lending

Portfolio Returns

- Growth of a high-quality non-conforming portfolio priced to provide adequate returns

- Portfolio provides steady stream of earnings; less impacted by cyclicality of originations

- Funding risk is manageable given Wells Fargo’s liquidity and capital position

What does it take to be successful in portfolio lending

- Organization designed and built specifically to support non-conforming lending

- Knowledge of local markets

- Wealth, Brokerage, and Retirement relationship value

- #1 Non-Conforming purchase originator overall and in 17 of the top 20 MSAs (1)

Growth in the non-conforming and home equity portfolios provide a steady stream of earnings

(1) Source: CoreLogic/Marketrac.

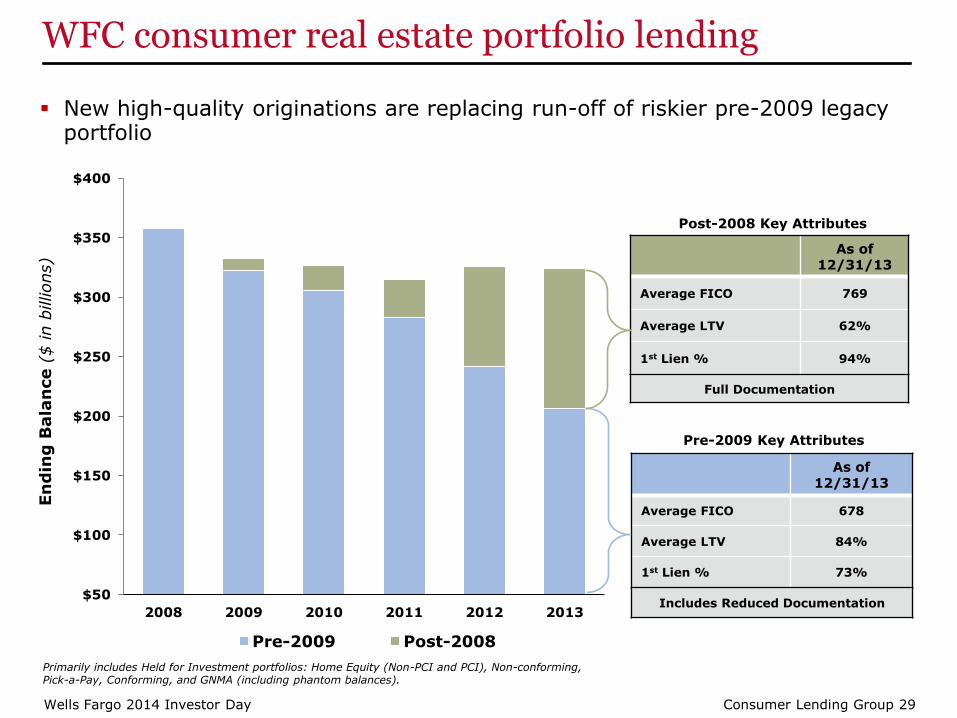

Consumer Lending Group 29 Wells Fargo 2014 Investor Day

WFC consumer real estate portfolio lending

New high-quality originations are replacing run-off of riskier pre-2009 legacy portfolio

$50

$100

$150

$200

$250

$300

$350

$400

2008 2009 2010 2011 2012 2013

En

din

g B

ala

nce (

$ in b

illions)

Pre-2009 Post-2008

Post-2008 Key Attributes

As of 12/31/13

Average FICO 769

Average LTV 62%

1st Lien % 94%

Full Documentation

Pre-2009 Key Attributes

As of 12/31/13

Average FICO 678

Average LTV 84%

1st Lien % 73%

Includes Reduced Documentation

Primarily includes Held for Investment portfolios: Home Equity (Non-PCI and PCI), Non-conforming, Pick-a-Pay, Conforming, and GNMA (including phantom balances).

Consumer Lending Group 30 Wells Fargo 2014 Investor Day

How we think about the servicing business

Servicing Returns

- Servicing provides an ongoing stream of income and increases when prepayments slow and originations decline

- New servicing rights reflect a solid return (servicing values on new originations have been reduced from historic levels)

- Increased cost structure on existing servicing incorporated into MSR value via quarterly valuation process, with over $2.6B absorbed in earnings over the past four years

- Requires aggressive cost management as delinquencies and foreclosures decline

Why Scale Matters in Servicing

- Allows brand recognition through servicing to foster cross-sell opportunity

- Enables substantial investment in the business

- Enables strong vendor relationships

- Regulations have increased costs; larger portfolio enables leveraging of fixed cost base

The servicing business produces appropriate returns; being the largest servicer in the country provides advantages

Consumer Lending Group 31 Wells Fargo 2014 Investor Day

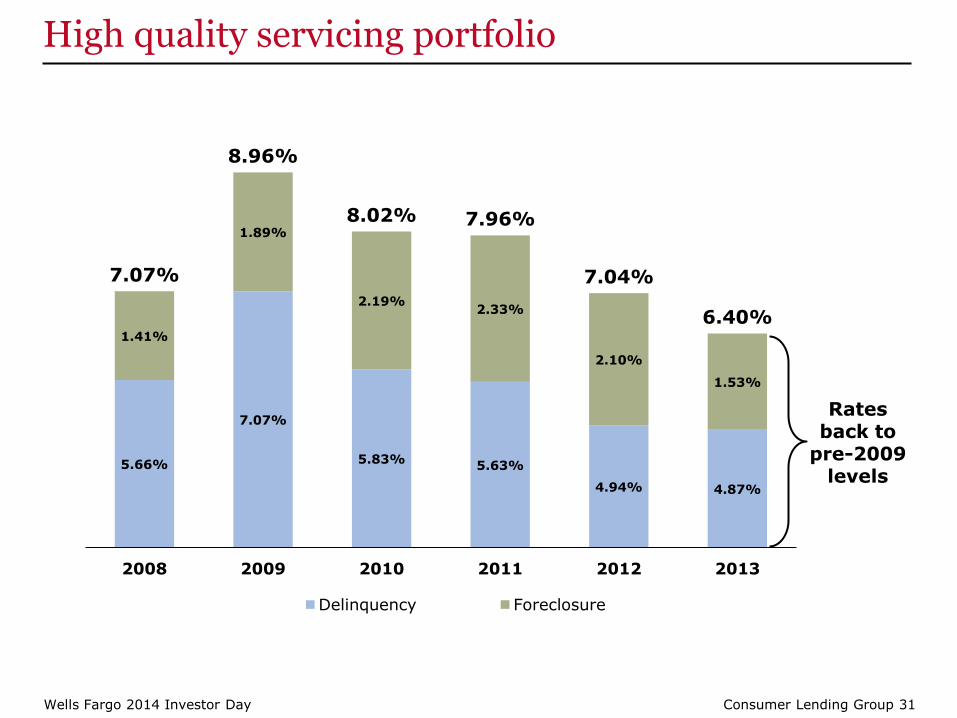

High quality servicing portfolio

5.66%

7.07%

5.83% 5.63%

4.94% 4.87%

1.41%

1.89%

2.19% 2.33%

2.10%

1.53%

7.07%

8.96%

8.02% 7.96%

7.04%

6.40%

2008 2009 2010 2011 2012 2013

Delinquency Foreclosure

Rates back to

pre-2009 levels

Consumer Lending Group 32 Wells Fargo 2014 Investor Day

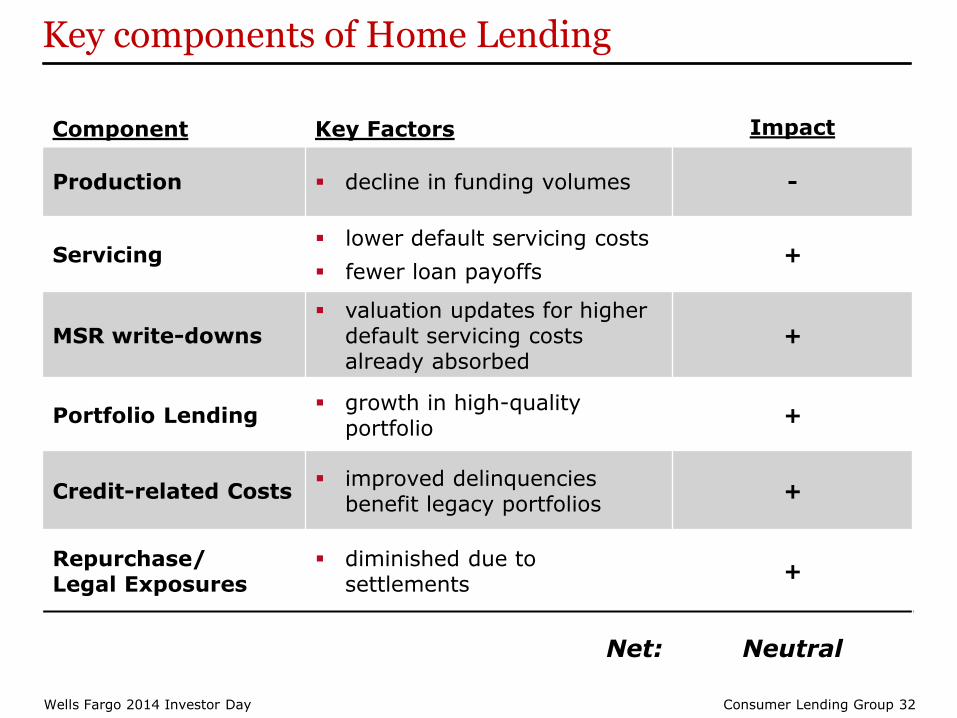

Component Key Factors Impact

Production decline in funding volumes -

Servicing lower default servicing costs

fewer loan payoffs +

MSR write-downs valuation updates for higher

default servicing costs already absorbed

+

Portfolio Lending growth in high-quality

portfolio +

Credit-related Costs improved delinquencies

benefit legacy portfolios +

Repurchase/ Legal Exposures

diminished due to settlements

+

Net: Neutral

Key components of Home Lending

Consumer Lending Group 33 Wells Fargo 2014 Investor Day

Consumer Credit Solutions Auto Lending

Consumer Lending Group 34 Wells Fargo 2014 Investor Day

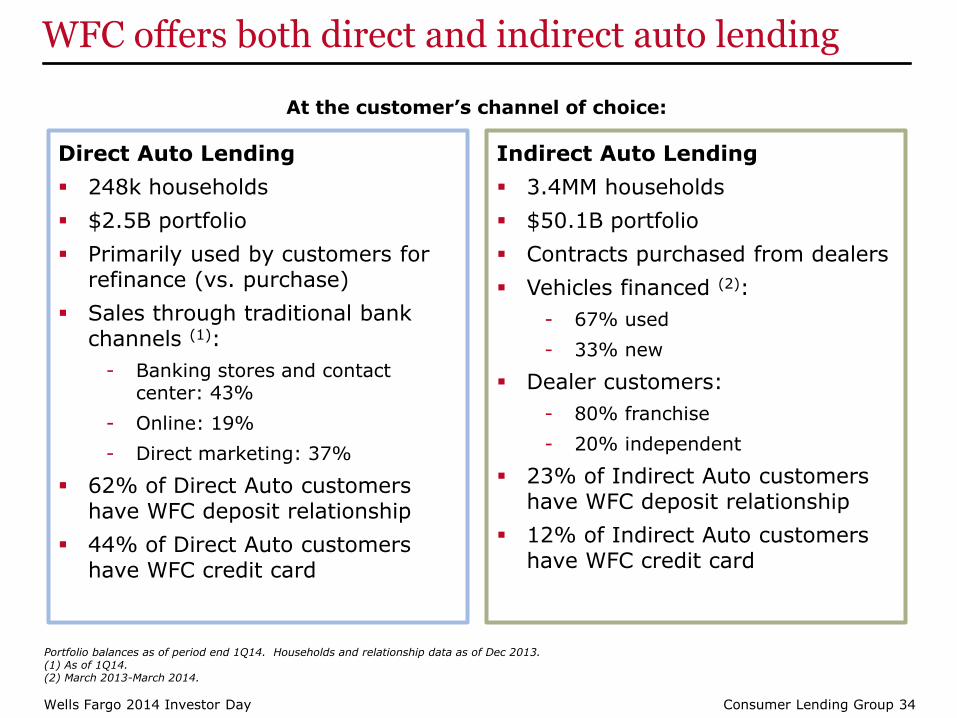

WFC offers both direct and indirect auto lending

Direct Auto Lending

248k households

$2.5B portfolio

Primarily used by customers for refinance (vs. purchase)

Sales through traditional bank channels (1):

- Banking stores and contact center: 43%

- Online: 19%

- Direct marketing: 37%

62% of Direct Auto customers have WFC deposit relationship

44% of Direct Auto customers have WFC credit card

Indirect Auto Lending

3.4MM households

$50.1B portfolio

Contracts purchased from dealers

Vehicles financed (2):

- 67% used

- 33% new

Dealer customers:

- 80% franchise

- 20% independent

23% of Indirect Auto customers have WFC deposit relationship

12% of Indirect Auto customers have WFC credit card

Portfolio balances as of period end 1Q14. Households and relationship data as of Dec 2013. (1) As of 1Q14. (2) March 2013-March 2014.

At the customer’s channel of choice:

Consumer Lending Group 35 Wells Fargo 2014 Investor Day

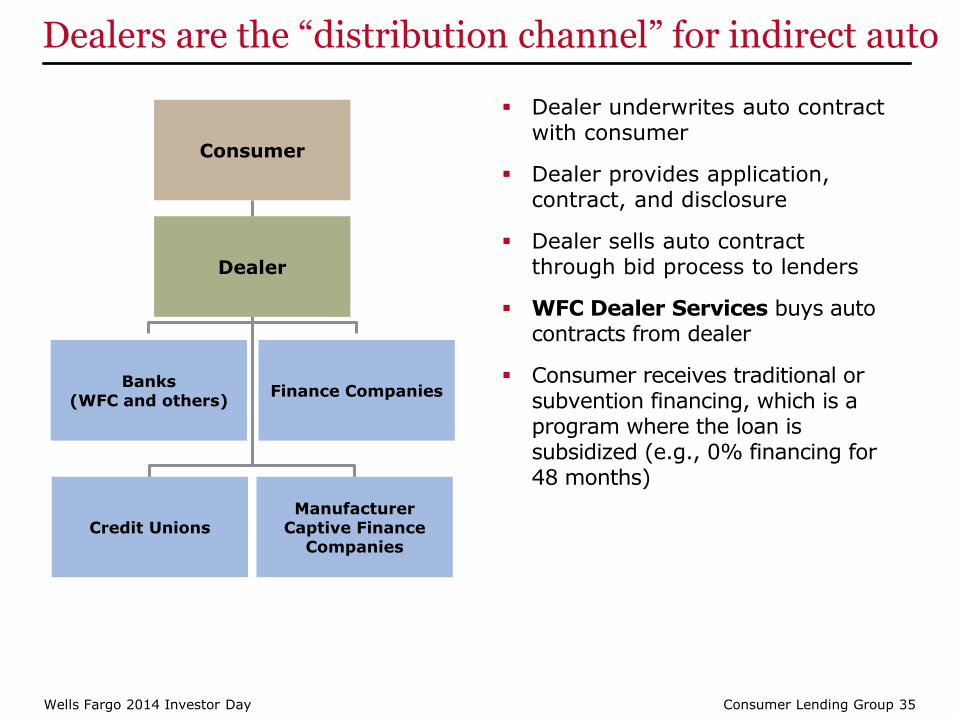

Dealers are the “distribution channel” for indirect auto

Dealer underwrites auto contract with consumer

Dealer provides application, contract, and disclosure

Dealer sells auto contract through bid process to lenders

WFC Dealer Services buys auto contracts from dealer

Consumer receives traditional or subvention financing, which is a program where the loan is subsidized (e.g., 0% financing for 48 months)

Dealer

Consumer

Banks (WFC and others)

Credit Unions

Finance Companies

Manufacturer Captive Finance

Companies

Consumer Lending Group 36 Wells Fargo 2014 Investor Day

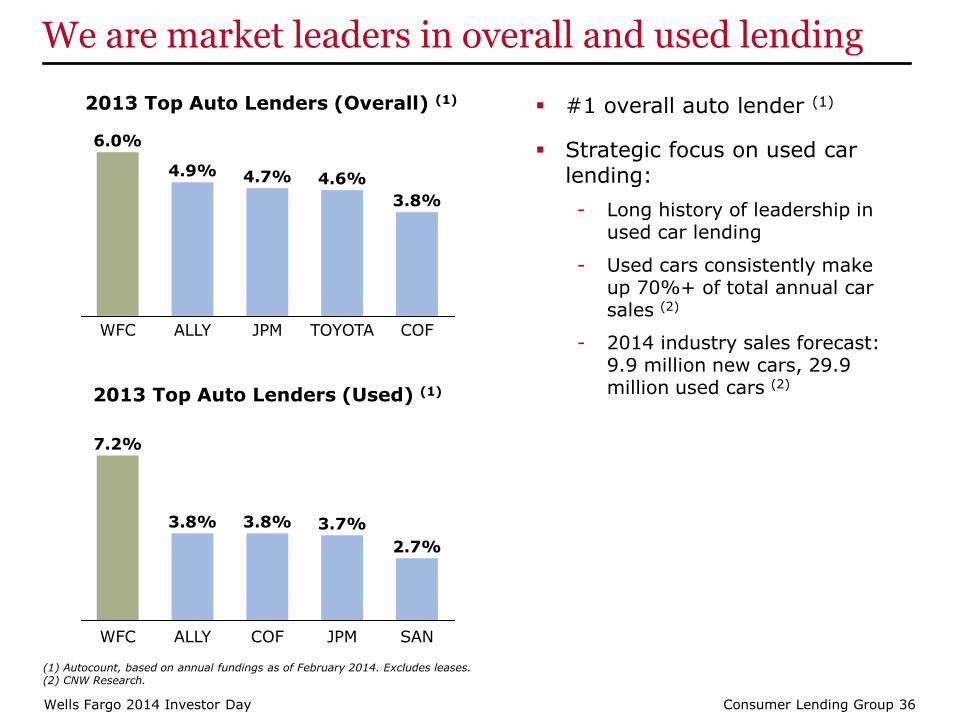

We are market leaders in overall and used lending

#1 overall auto lender (1)

Strategic focus on used car lending:

- Long history of leadership in used car lending

- Used cars consistently make up 70%+ of total annual car sales (2)

- 2014 industry sales forecast: 9.9 million new cars, 29.9 million used cars (2)

2013 Top Auto Lenders (Overall) (1)

3.7% 3.8%

SAN

3.8%

7.2%

COF

2.7%

ALLY WFC JPM

2013 Top Auto Lenders (Used) (1)

TOYOTA

6.0%

4.7%

WFC

4.6%

JPM

4.9%

ALLY COF

3.8%

(1) Autocount, based on annual fundings as of February 2014. Excludes leases. (2) CNW Research.

Consumer Lending Group 37 Wells Fargo 2014 Investor Day

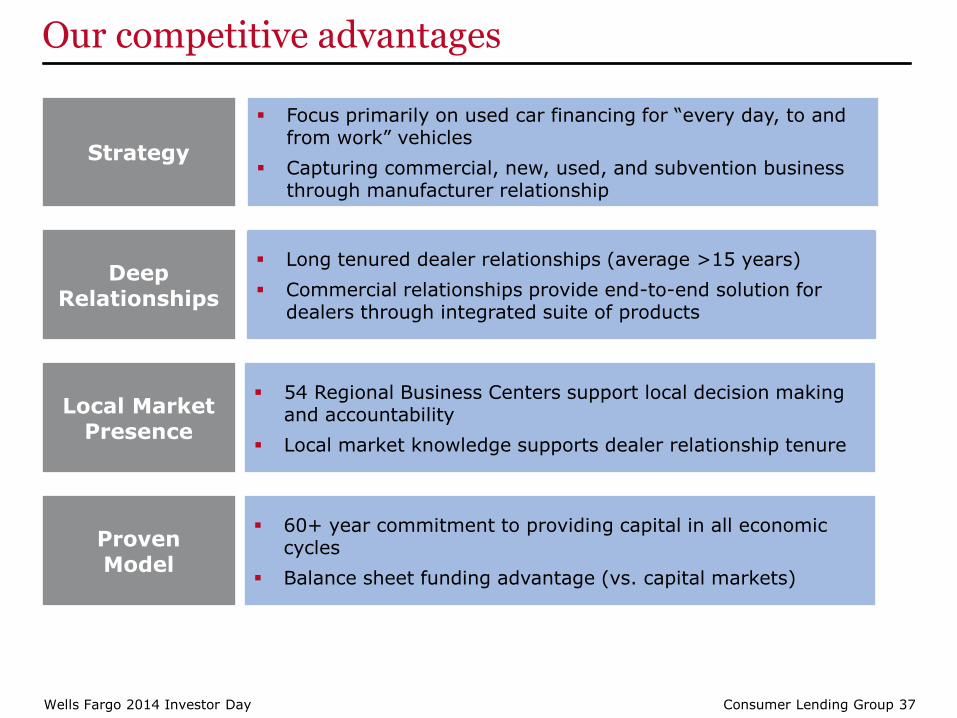

Local Market Presence

54 Regional Business Centers support local decision making and accountability

Local market knowledge supports dealer relationship tenure

Deep Relationships

Long tenured dealer relationships (average >15 years)

Commercial relationships provide end-to-end solution for dealers through integrated suite of products

Strategy

Focus primarily on used car financing for “every day, to and from work” vehicles

Capturing commercial, new, used, and subvention business through manufacturer relationship

Proven Model

60+ year commitment to providing capital in all economic cycles

Balance sheet funding advantage (vs. capital markets)

Our competitive advantages

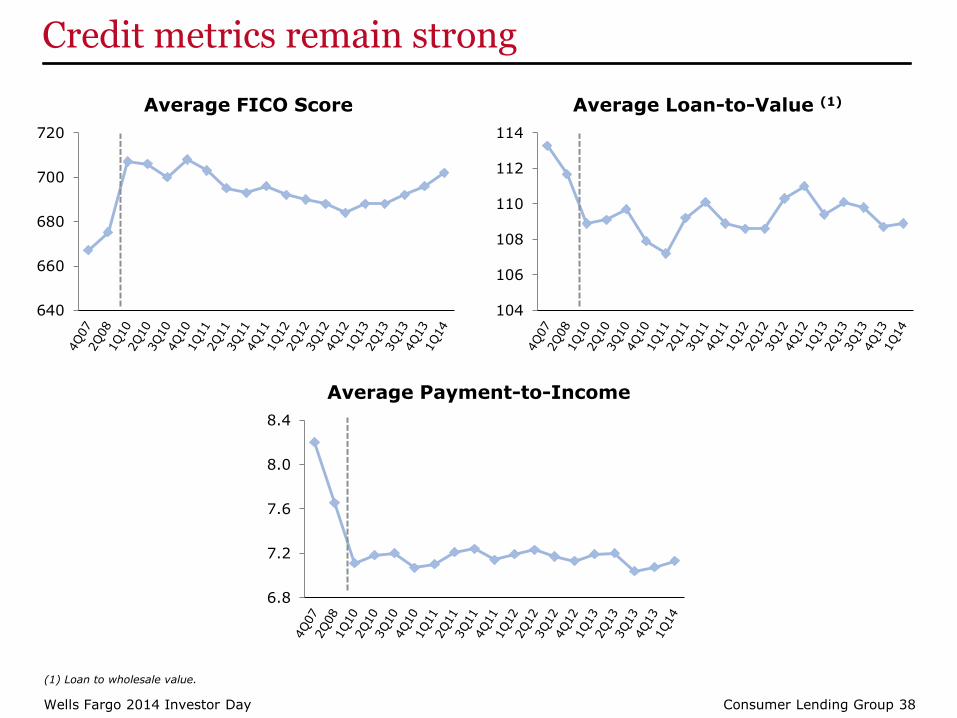

Consumer Lending Group 38 Wells Fargo 2014 Investor Day

Credit metrics remain strong

640

660

680

700

720

Average FICO Score

104

106

108

110

112

114

Average Loan-to-Value (1)

6.8

7.2

7.6

8.0

8.4

Average Payment-to-Income

(1) Loan to wholesale value.

Consumer Lending Group 39 Wells Fargo 2014 Investor Day

We have grown our existing dealer relationships

Volume ($ in millions)

445

504

403

645640

433

20+ Funded

10 - 19 Funded

5 - 9 Funded

71

108110

97

131

116

20+ Funded

10 - 19 Funded

5 - 9 Funded

4Q12

4Q13

Applications (in thousands)

Dealer Segment (Loans/Month) Dealer Segment (Loans/Month)

Consumer Lending Group 40 Wells Fargo 2014 Investor Day

Retail and commercial relationships drive growth

How we think about retail relationships:

Trusted partners – Disciplined underwriting enables us to support dealers through the economic cycles

Full engagement – A strong retail relationship provides contracts in every credit tier we support

Built over time – Deepened relationships grow applications submitted and volume funded

How we think about commercial relationships: Meeting all of our dealers’

financial needs – Offerings include treasury management, floorplan financing, insurance, real estate, etc.

Competitive advantage - captive finance companies do not offer full suite of products

Deep and stable relationships – Average cross-sell of over 11 products

How they work together: Retail and commercial relationship managers can make combined sales

calls to dealers

Every new commercial rooftop deepens or expands retail engagement (more applications and better conversion leads to more fundings)

Consumer Lending Group 41 Wells Fargo 2014 Investor Day

Continued growth opportunities

Use balance sheet funding advantage to reach more customers

- Capital market dependent competitors must raise contract rates in higher-rate environment

Capture additional subvented and non-subvented volume through GM relationship

Leverage flexible capabilities (e.g., support of unique Tesla sales model)

Continue to leverage commercial relationships to expand retail engagement

Deepen cross-sell penetration into indirect auto customers with no other Wells Fargo relationship

Consumer Lending Group 42 Wells Fargo 2014 Investor Day

Consumer Credit Solutions Credit Card

Wells Fargo 2014 Investor Day Consumer Lending Group 43

Our relationship model is a core strength

Large base of 42MM+ households with existing WFC relationships

Distinctive offerings and capabilities enabled by WFC relationships:

- Behavioral insights driven by rich customer data (enhanced underwriting, better needs assessment, presentment/ contact preferences)

- Product linkages (integrated offerings, connectivity, relationship points across full WFC relationship)

- Ability to offer full range of “life stage” offerings – early stage credit through high net worth (HNW)

Wells Fargo 2014 Investor Day Consumer Lending Group 44

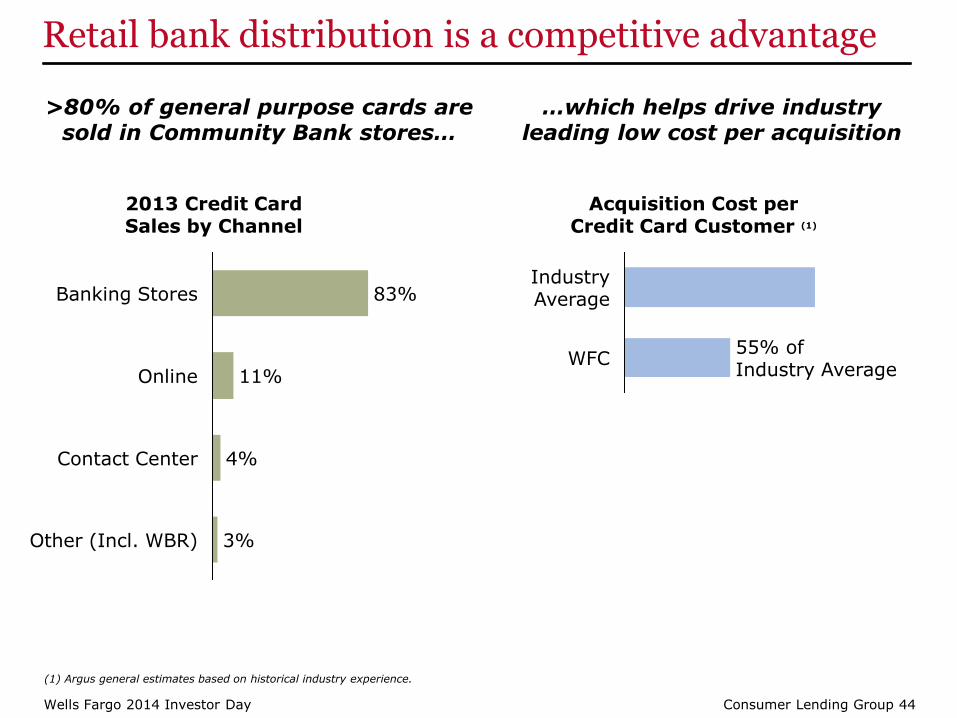

Retail bank distribution is a competitive advantage

WFC 55% of Industry Average

Industry Average

Acquisition Cost per Credit Card Customer (1)

3%

4%

Online 11%

83% Banking Stores

Other (Incl. WBR)

Contact Center

2013 Credit Card Sales by Channel

(1) Argus general estimates based on historical industry experience.

…which helps drive industry leading low cost per acquisition

>80% of general purpose cards are sold in Community Bank stores…

Wells Fargo 2014 Investor Day Consumer Lending Group 45

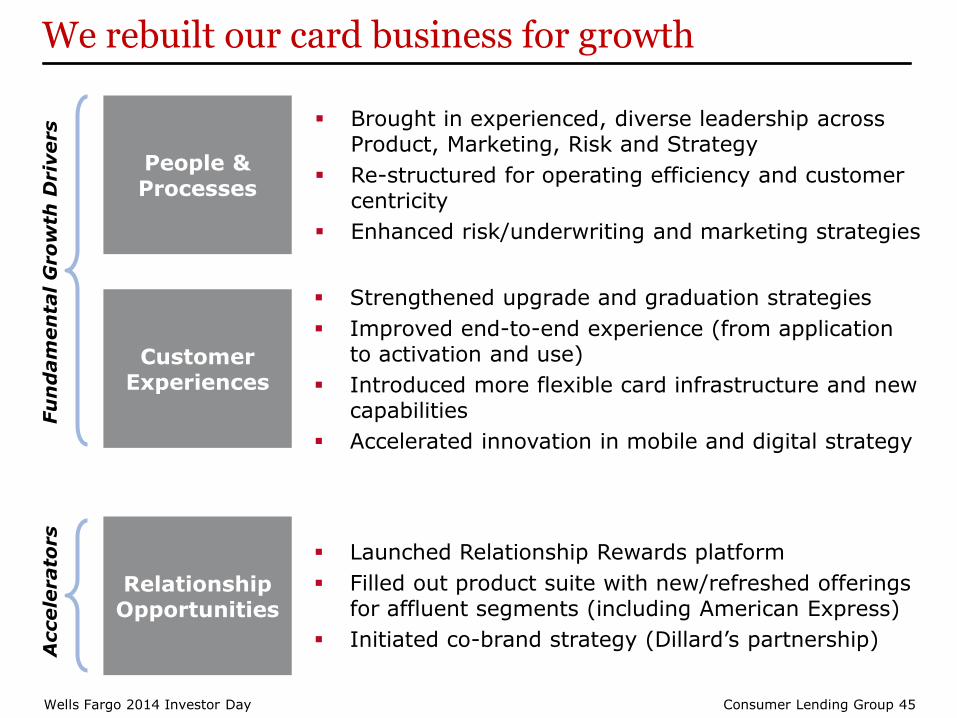

We rebuilt our card business for growth

People & Processes

Brought in experienced, diverse leadership across Product, Marketing, Risk and Strategy

Re-structured for operating efficiency and customer centricity

Enhanced risk/underwriting and marketing strategies

Strengthened upgrade and graduation strategies

Improved end-to-end experience (from application to activation and use)

Introduced more flexible card infrastructure and new capabilities

Accelerated innovation in mobile and digital strategy

Customer Experiences

Fu

nd

am

en

tal G

ro

wth

Driv

ers

Launched Relationship Rewards platform

Filled out product suite with new/refreshed offerings for affluent segments (including American Express)

Initiated co-brand strategy (Dillard’s partnership)

Relationship Opportunities

Accele

rato

rs

Wells Fargo 2014 Investor Day Consumer Lending Group 46

Unique capabilities on new rewards platform

Relationship Benefits

Earn rewards across WFC relationship (e.g. Visa and AmEx cards earn rewards in common account)

AmEx Propel cardholders earn 10% -50% rewards bonus with qualifying Wells Fargo deposit relationships

Gift rewards points to friends, family, or any WFC account holder

Use rewards to make contributions to charities (Coming in 2015)

Community and Connection

Relationship Rewards

Use rewards to lower balances on WFC credit products or to put cash into WFC deposit and savings accounts

Redeem for travel, digital media downloads, gift cards, merchandise, and experiential rewards

Wells Fargo 2014 Investor Day Consumer Lending Group 47

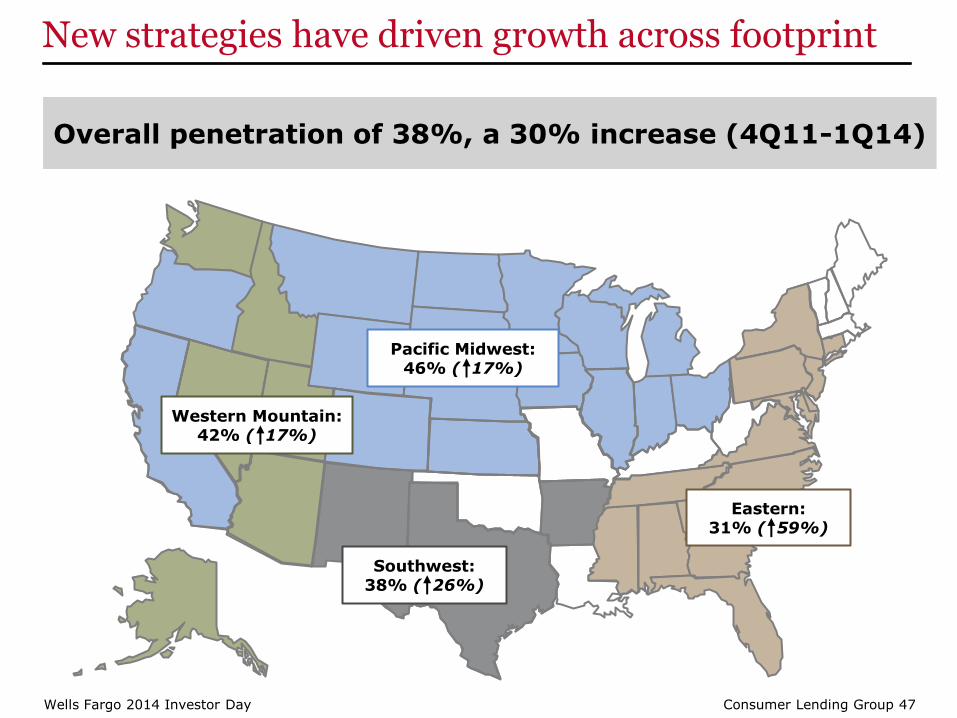

New strategies have driven growth across footprint

Eastern: 31% ( 59%)

Southwest: 38% ( 26%)

Pacific Midwest: 46% ( 17%)

Western Mountain: 42% ( 17%)

Overall penetration of 38%, a 30% increase (4Q11-1Q14)

Wells Fargo 2014 Investor Day Consumer Lending Group 48

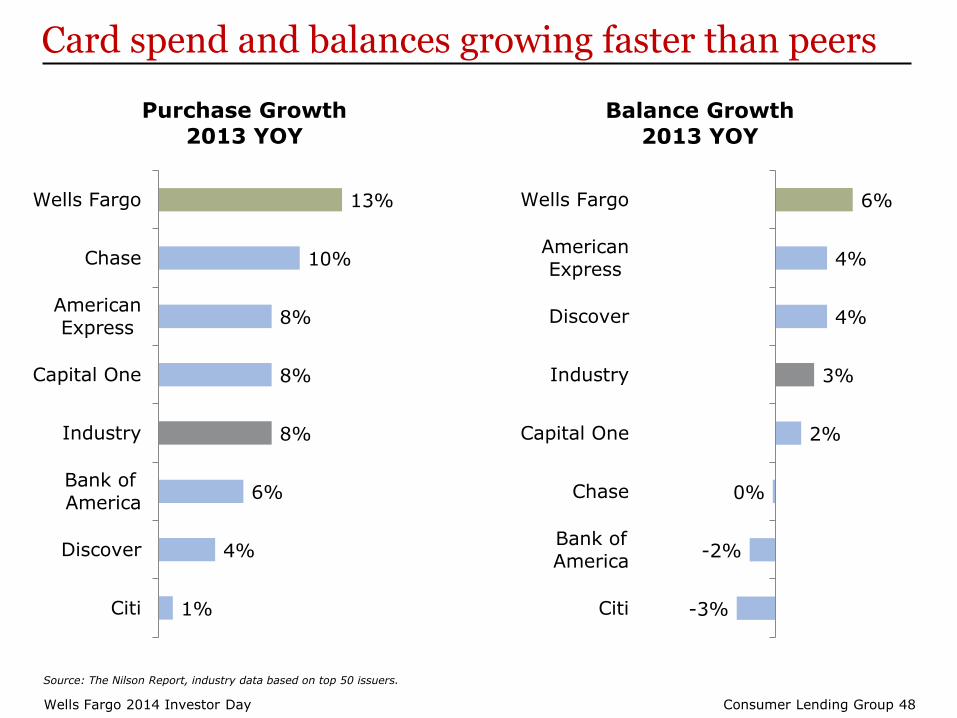

Card spend and balances growing faster than peers

Source: The Nilson Report, industry data based on top 50 issuers.

1%

4%

6%

8%

8%

8%

10%

13%

Citi

Discover

Bank of

America

Industry

Capital One

AmericanExpress

Chase

Wells Fargo

Purchase Growth

2013 YOY

-3%

-2%

0%

2%

3%

4%

4%

6%

Citi

Bank ofAmerica

Chase

Capital One

Industry

Discover

AmericanExpress

Wells Fargo

Balance Growth

2013 YOY

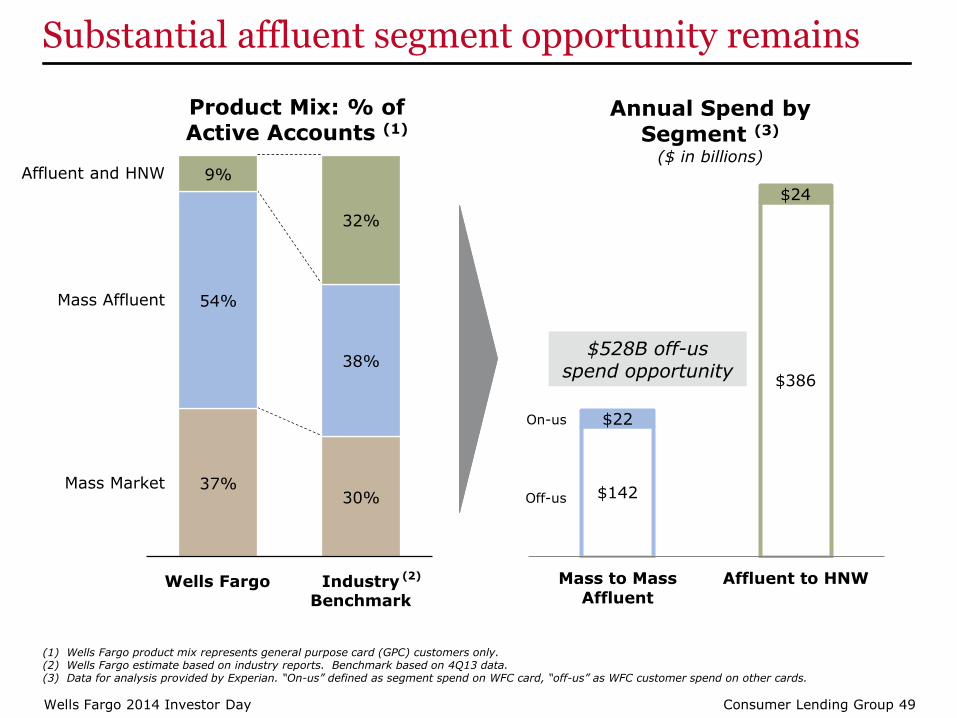

Wells Fargo 2014 Investor Day Consumer Lending Group 49

$142

$386

$22

$24

Mass to Mass

Affluent

Affluent to HNW

Annual Spend by

Segment (3) ($ in billions)

$528B off-us spend opportunity

Substantial affluent segment opportunity remains

Product Mix: % of Active Accounts (1)

37% 30%

54%

38%

9%

32%

Mass Market

Wells Fargo

Affluent and HNW

Industry Benchmark

Mass Affluent

(1) Wells Fargo product mix represents general purpose card (GPC) customers only. (2) Wells Fargo estimate based on industry reports. Benchmark based on 4Q13 data. (3) Data for analysis provided by Experian. “On-us” defined as segment spend on WFC card, “off-us” as WFC customer spend on other cards.

On-us

Off-us

(2)

Wells Fargo 2014 Investor Day Consumer Lending Group 50

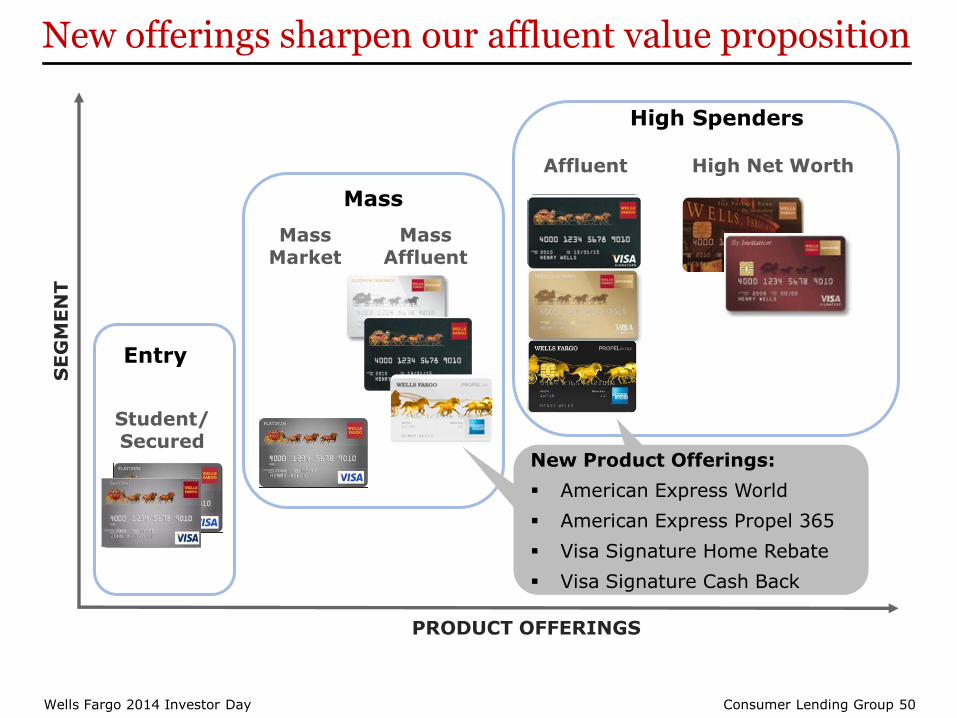

PRODUCT OFFERINGS

SEG

MEN

T

Student/ Secured

Mass Market

Affluent

Mass Affluent

Entry

Mass

High Spenders

High Net Worth

New Product Offerings:

American Express World

American Express Propel 365

Visa Signature Home Rebate

Visa Signature Cash Back

New offerings sharpen our affluent value proposition

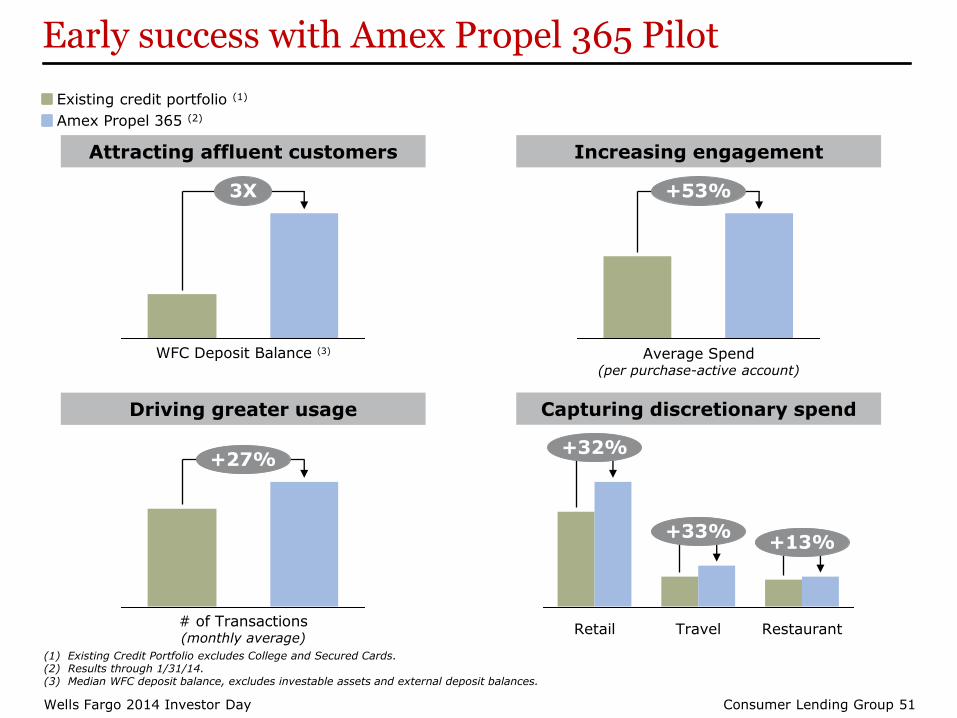

Wells Fargo 2014 Investor Day Consumer Lending Group 51

Attracting affluent customers

Early success with Amex Propel 365 Pilot

Capturing discretionary spend

Increasing engagement

Driving greater usage

(1) Existing Credit Portfolio excludes College and Secured Cards. (2) Results through 1/31/14. (3) Median WFC deposit balance, excludes investable assets and external deposit balances.

3X +53%

Average Spend (per purchase-active account)

# of Transactions (monthly average)

+27%

+33%

Restaurant

+32%

+13%

Travel Retail

Existing credit portfolio (1)

Amex Propel 365 (2)

WFC Deposit Balance (3)

Wells Fargo 2014 Investor Day Consumer Lending Group 52

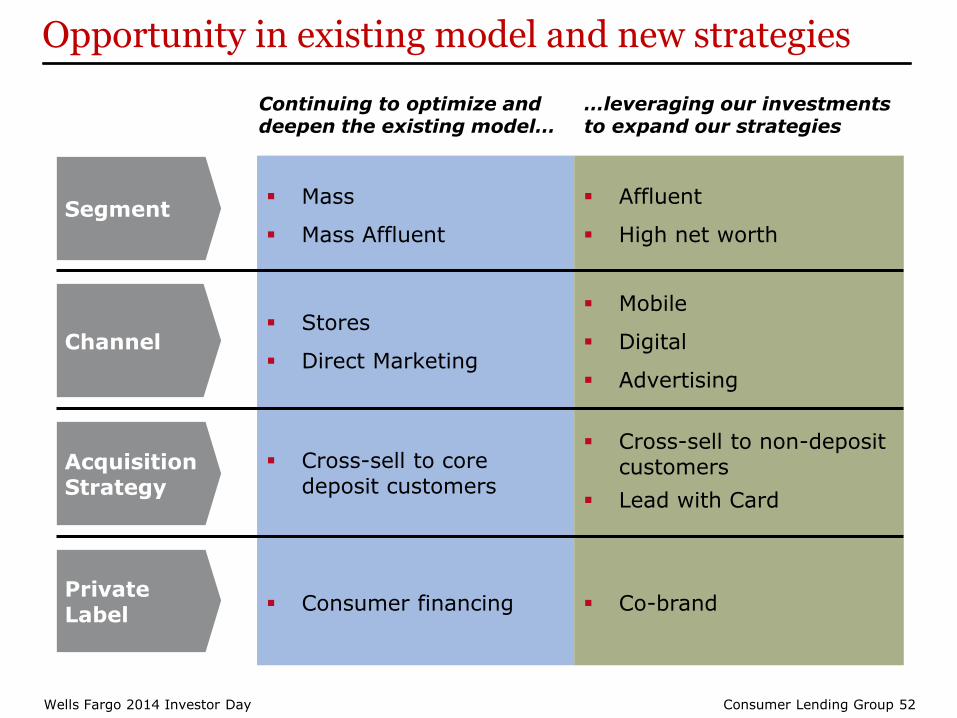

Mass

Mass Affluent

Affluent

High net worth

Stores

Direct Marketing

Mobile

Digital

Advertising

Cross-sell to core deposit customers

Cross-sell to non-deposit customers

Lead with Card

Consumer financing Co-brand

Opportunity in existing model and new strategies

Continuing to optimize and deepen the existing model…

…leveraging our investments to expand our strategies

Segment

Channel

Acquisition Strategy

Private Label

Consumer Lending Group 53 Wells Fargo 2014 Investor Day

Consumer Lending Group

Wells Fargo 2014 Investor Day Consumer Lending Group 54

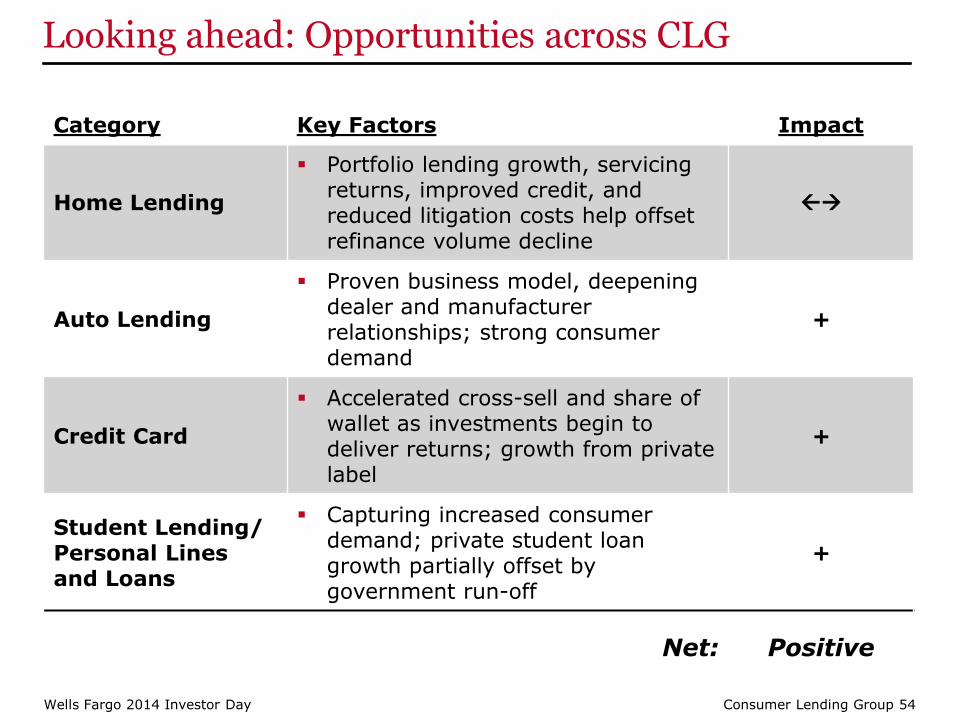

Looking ahead: Opportunities across CLG

Category Key Factors Impact

Home Lending

Portfolio lending growth, servicing returns, improved credit, and reduced litigation costs help offset refinance volume decline

Auto Lending

Proven business model, deepening dealer and manufacturer relationships; strong consumer demand

+

Credit Card

Accelerated cross-sell and share of wallet as investments begin to deliver returns; growth from private label

+

Student Lending/ Personal Lines and Loans

Capturing increased consumer demand; private student loan growth partially offset by government run-off

+

Net: Positive

Consumer Lending Group 55 Wells Fargo 2014 Investor Day

Appendix

Wells Fargo 2014 Investor Day Consumer Lending Group 56

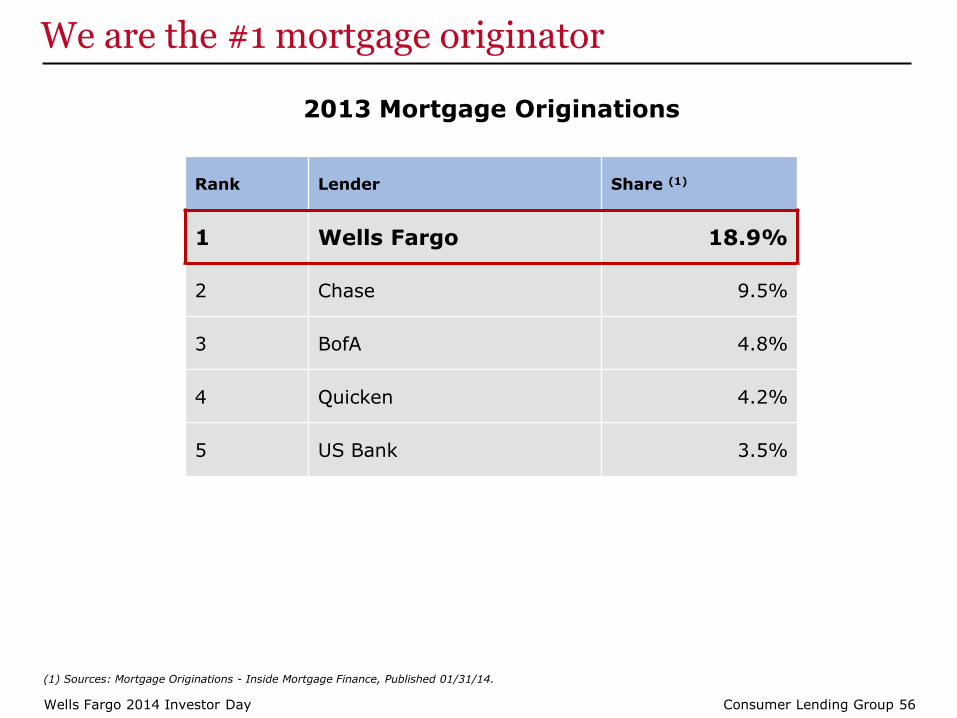

We are the #1 mortgage originator

(1) Sources: Mortgage Originations - Inside Mortgage Finance, Published 01/31/14.

Rank Lender Share (1)

1 Wells Fargo 18.9%

2 Chase 9.5%

3 BofA 4.8%

4 Quicken 4.2%

5 US Bank 3.5%

2013 Mortgage Originations

Wells Fargo 2014 Investor Day Consumer Lending Group 57

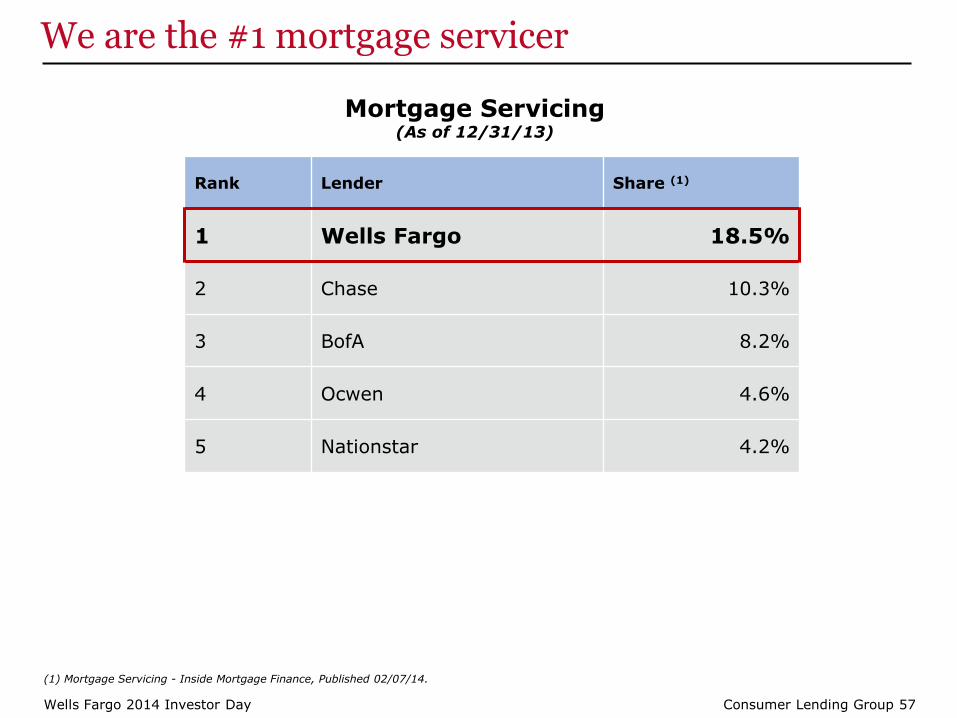

We are the #1 mortgage servicer

Rank Lender Share (1)

1 Wells Fargo 18.5%

2 Chase 10.3%

3 BofA 8.2%

4 Ocwen 4.6%

5 Nationstar 4.2%

Mortgage Servicing (As of 12/31/13)

(1) Mortgage Servicing - Inside Mortgage Finance, Published 02/07/14.

Wells Fargo 2014 Investor Day Consumer Lending Group 58

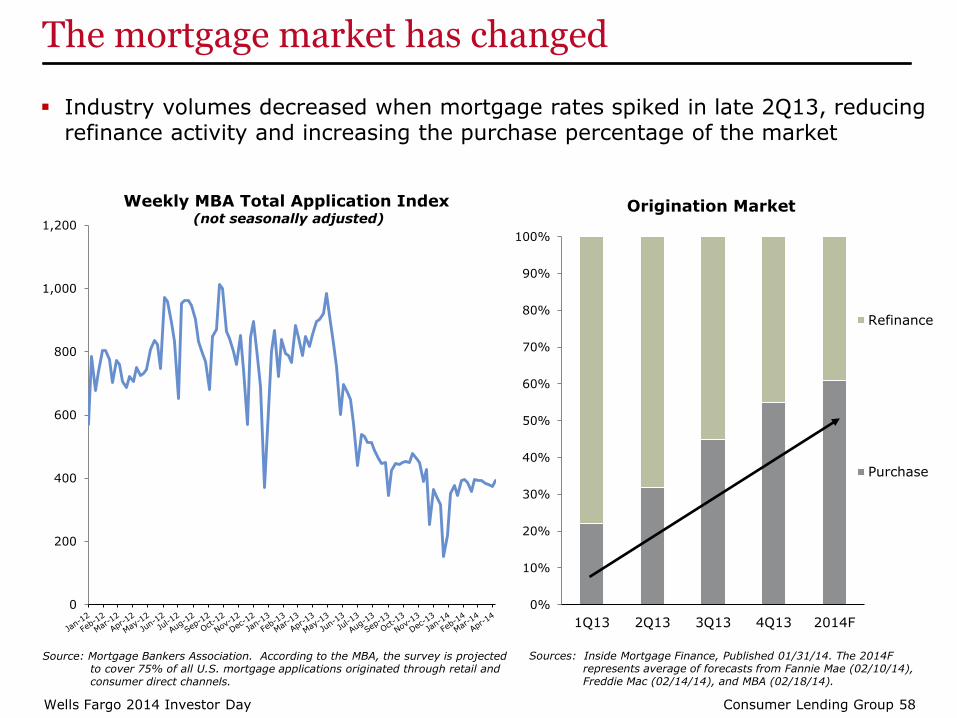

The mortgage market has changed

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1Q13 2Q13 3Q13 4Q13 2014F

Refinance

Purchase

Sources: Inside Mortgage Finance, Published 01/31/14. The 2014F represents average of forecasts from Fannie Mae (02/10/14), Freddie Mac (02/14/14), and MBA (02/18/14).

Industry volumes decreased when mortgage rates spiked in late 2Q13, reducing refinance activity and increasing the purchase percentage of the market

0

200

400

600

800

1,000

1,200

Source: Mortgage Bankers Association. According to the MBA, the survey is projected to cover 75% of all U.S. mortgage applications originated through retail and consumer direct channels.

Weekly MBA Total Application Index (not seasonally adjusted)

Origination Market

Wells Fargo 2014 Investor Day Consumer Lending Group 59

Mortgage is a cornerstone product

4.75

6.43

7.61

0

1

2

3

4

5

6

7

8

9

Non-homeowners Homeowners witha competitor's

mortgage

Homeowners witha Wells Fargo

mortgage

Averag

e W

FC

Pro

du

cts

Mortgage households own more banking products and are more profitable:

Retail Bank (1) Households’ Home Ownership Status and Number of Products (excludes mortgage)

Homeowners with a WFC

mortgage are 12 times

more profitable than non-

homeowners (2)

(1) Retail Bank Products: Checking, Savings, CD, IRA, Installment Loan, Line of Credit. (2) Includes the mortgage profit.

Consumer Lending Group 60 Wells Fargo 2014 Investor Day

Biographies

Wells Fargo 2014 Investor Day Consumer Lending Group 61

Avid Modjtabai Senior Executive Vice President and head of Consumer Lending Group (CLG) for Wells Fargo & Company. CLG includes Auto Lending (Direct and Indirect), Consumer Credit Card (General Purpose and Private Label), Home Lending, Personal Lines and Loans, and Student Lending. Modjtabai serves on the Wells Fargo Operating and Management Committees.

A 21-year veteran of Wells Fargo, Modjtabai has held in a number of leadership roles. Prior to leading CLG she was the head of the Technology and Operations Group and Chief Information Officer. In this role, she led the customer conversion activities, and the systems and infrastructure integration for the Wells Fargo – Wachovia merger. She was also responsible for core technology and operations functions of the company.

Previously, Modjtabai served as Director of Human Resources, with responsibility for compensation and benefits, human resource service centers, systems and payroll, finance, team member relations and assistance, talent management, learning and development and diversity. Prior to that, she was head of the Internet Services Group, where she helped Wells Fargo become the leading provider of online financial services through managing Consumer, Investment and Small Business Internet Services.

Modjtabai earned a bachelor’s degree in industrial engineering from Stanford University and an MBA in finance from Columbia University.

Avid Modjtabai Senior Executive Vice President, Consumer Lending

Wells Fargo 2014 Investor Day Consumer Lending Group 62

Mike Heid is president of Wells Fargo Home Mortgage (WFHM), a division of Wells Fargo Bank, N.A., and an executive vice president and member of the Operating Committee of Wells Fargo & Company. WFHM is the nation’s leading provider of residential mortgages, funding one of every five residential mortgages in the country and servicing one of every six mortgage loans in the U.S. in 2013 including loans Wells Fargo holds, as well as loans held by other mortgage investors.

Heid is responsible for WFHM’s overall business and strategic direction. A 28-year veteran of the mortgage business, he most recently served as co-president of WFHM from June 2004 to July 2011. Previously within the mortgage division, Heid was chief financial officer (2002 to 2004) and head of Loan Servicing (1997 to 2002). Heid joined Wells Fargo in 1988.

Heid is actively involved in legislative and regulatory policy matters affecting the mortgage industry. Currently, he is a member of the Mortgage Bankers Association Board of Directors. From May 2008 through May 2011 – a time of significant industry transformation – Heid served as chairman of the Housing Policy Council of the Financial Services Roundtable. He also has served as chairman of the Fannie Mae National Housing Advisory Council.

Heid earned a bachelor’s degree in accounting from the University of Wisconsin - Whitewater in 1979 where he graduated summa cum laude. He is a Certified Public Accountant.

Mike Heid Executive Vice President, Home Lending

Wells Fargo 2014 Investor Day Consumer Lending Group 63

Tom Wolfe is executive vice president and head of Consumer Credit Solutions for Wells Fargo & Company. The group comprises Wells Fargo’s non real estate consumer credit businesses including Auto Lending (Direct and Indirect), Consumer Credit Card (General Purpose and Private Label), Personal Lines and Loans, and Student Lending. Wells Fargo is the nation’s leading auto lender (excluding leases) and the second-ranked private student lender.

Wolfe is a 31 year veteran of the consumer credit industry. Most recently, he was the head of Dealer Services where he helped Wells Fargo become one of the nation’s leading providers of integrated financial services for the auto industry.

Prior to serving as head of Wells Fargo Dealer Services, he was president of Wachovia Dealer Services, responsible for Indirect Auto Finance, Direct-to-Consumer Auto Finance, Commercial Services, and aftermarket products through Warranty Solutions®.

Wolfe also served as chief executive officer for Westcorp, a holding company for Western Financial Savings Bank. He was also president of its subsidiary company, WFS Financial Inc., a leading auto finance company.

Prior to his career with Westcorp, Wolfe held several management positions in the areas of consumer lending with Ameritrust, Citibank, General Motors Acceptance Corporation (GMAC), and Key Auto Finance.

Tom Wolfe Executive Vice President, Consumer Credit Solutions