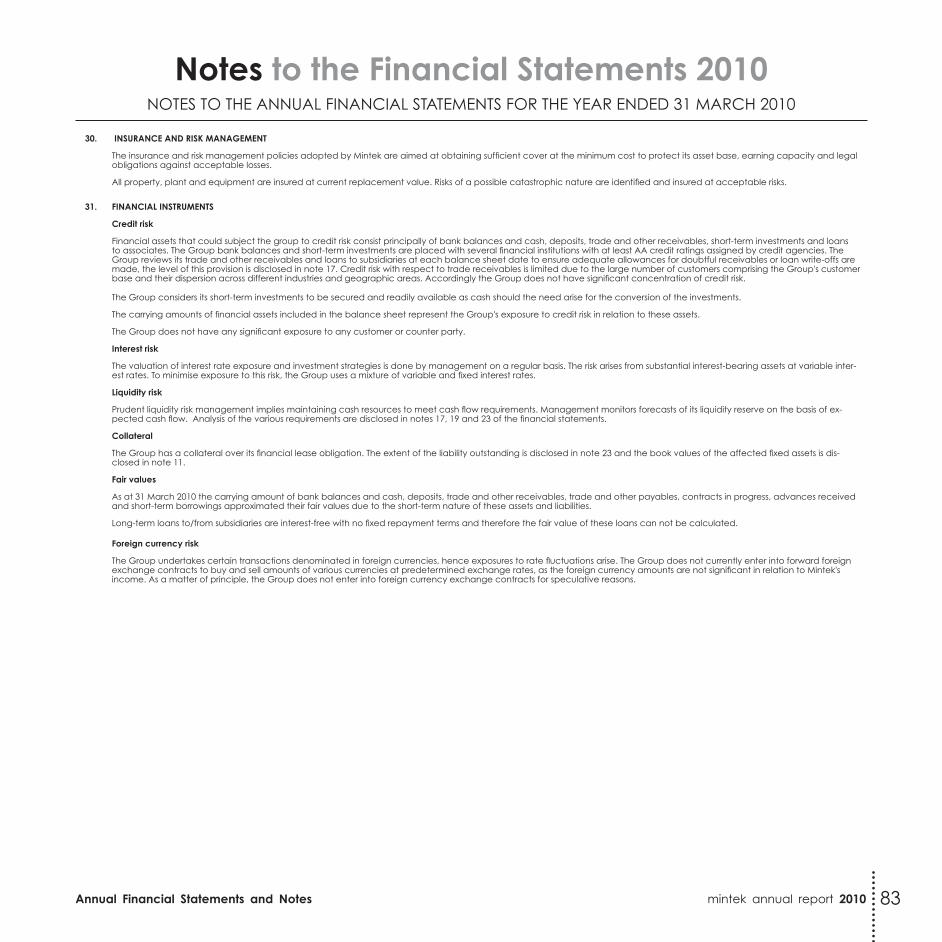

contents of the annual financial statements and notes · contents of the annual financial...

TRANSCRIPT

Annual Financial Statements and Notes mintek annual report 2010

Contents of the Annual Financial Statements and Notes

for the year ended 31 March 2010

56 Audit Committee RepoRt

57 diReCtoRS’ RepoRt

59 RepoRt oF the AuditoR-GeNeRAl

61 StAtemeNtS oF FiNANCiAl poSitioN

62 StAtemeNtS oF CompReheNSive iNCome

63 StAtemeNtS oF CASh FlowS

64 StAtemeNtS oF ChANGeS iN Net ASSetS

65 NoteS to the ANNuAl FiNANCiAl StAtemeNtS

55

mintek annual report 2010 Annual Financial Statements and Notes

Audit Committee Reportthe audit coMMittee has adopted forMal terMs of reference, which have been confirmed by the Mintek Board, and has performed its responsibilities as set out in the terms of reference. In understanding its responsibilities, the Audit Committee has reviewed the following:• The effectiveness of the internal control system;• The effectiveness of the internal audit function;• The risk areas of the entity to be covered in the internal and external audits;• The adequacy, reliability and accuracy of the financial information provided to management and other users of such information;• The accounting or auditing concerns identified as a result of the external and internal audits;• Compliance with legal and regulatory provisions;• The activities of the internal audit function;• The independence and objectivity of the external auditors; and,• The scope and results of the external audit function.

The Audit Committee is also responsible for:• Reporting to the Mintek Board and the Auditor-General where the report implicates any members of the accounting authority in fraud,

corruption or gross negligence;• Communicating any concerns it deems necessary to the Mintek Board;• Confirming the internal auditor’s charter and audit plan;• Encouraging communication between members of the Mintek Board, senior executive management, the internal auditors and

external auditors;• Conducting investigations within the terms of reference;• Concurring with the appointment of the in-house internal audit function;• Approving the internal audit work plan; and,• Setting the principles for recommending the use of the external auditor for non-audit services.

The Audit Committee is satisfied that internal controls and systems have been put in place during the year under review and that controls have functioned effectively during the period. The Audit Committee considers Mintek internal controls and systems to be appropriate in all material respects to:• Reduce the entity’s risk to an acceptable level;• Meet the business objectives of the entity;• Ensure the entity’s assets are adequately safeguarded; and, • Ensure that the transactions undertaken are recorded in the entity’s records.

The Audit Committee has evaluated the group and the company financial statements for the year ended 31 March 2010 and concluded that they fully comply, in all material aspects, with the requirements of the Public Finance Management Act (PFMA) No.1 of 1999, as amended, and South African Statements of Generally Accepted Accounting Practice (SA Statements of GAAP).

The Audit Committee has requested management to review and evaluate Mintek’s internal controls to identify areas that can be improved upon. The Audit Committee agrees that the adoption of the going concern premise is appropriate in preparing the annual financial statements. The Committee acknowledges that Mintek has made significant progress in addressing the control weakness identified previously and looks forward to the future control environment, which will provide a sound basis for Mintek to meet its obligation to its stakeholders.

mohau mphomelaChairperson of the Audit Committee31 March 2010

Audit Committee members:

Mr M MphomelaDr J BredellMs L MhlabeniMs N LilaMr B Mbewu

56

Annual Financial Statements and Notes mintek annual report 2010

directors’ ReportThe directors of Mintek take pleasure in submitting their 2009/2010 report together with the Annual financial statements as at 31 March 2010.

pRoFile

Mintek was established by the Mineral Technology Act 30 of 1989, incorporated as a public company in South Africa in terms of the Companies Act, 1973, as amended, and is listed as a national government business enterprise in schedule 3B of the Public Finance Management Act (PFMA), 1999, as amended.

FiNANCiAl ReSultS

The financial statements represent the financial result of Mintek and the consolidated results of its subsidiary, Mindev (Pty) Ltd, for the year ending 31 March 2010.

RepoRtiNG StANdARdS

The Mintek Group’s Annual Financial Statements comply with South African Statements of Generally Accepted Accounting Practice (GAAP) and the PFMA.

oRGANiSAtioNAl StRuCtuRe

Mintek’s organisational structure is shown on page 9 of the annual report.

pRiNCipAl ACtivitieS

Mintek, South Africa’s national mineral research organisation, is a state-owned enterprise established to ensure the sustainability and growth of the minerals industry through technology development and transfer. In terms of its mandate under the Mineral Technology Act 30 of 1989, Mintek’s main objectives are to promote mineral technology and to foster the establishment and expansion of industries in the field of minerals and products derived therefrom through research.

Specific aims include to:

• Develop efficient mineral processing technologies and sustainable value added products;

• Play a significant role in second economy interventions by developing technologies appropriate to the local jewellery, artisanal and small-scale mining (ASSM) industries;

• Support government regional and continental initiatives;

• Develop human and organisational skills whilst transforming its internal and external business processes and the workforce; and,

• Uphold good governance practices.

FiNANCiAl AFFAiRS

Review of operations

In the 2009/10 financial year Mintek experienced the effect of the economic recession more than anticipated. There was significantly lower demand for research and commercially driven projects forcing Mintek to implement stringent cost control measures to ensure profitability. It was a difficult year exacerbated by the cancellation of large projects and difficulties on other projects such as the smelting of high-chromium platinum concentrates (ConRoast). Mintek has also been affected by the high increase in electricity costs as well as the volatility of our local currency. Mintek has taken the view that these difficulties are short-term and therefore no decision was taken to minimise fixed costs. This view was validated judging by the current strong sales pipeline.

An insurance claim was lodged with the insurers in respect of an accident that occurred at Bay 2 on 27 March 2009. The claim was fully met for damages incurred in this unfortunate event.

Investment property amounting to R12,5m was reclassified in the current financial year as property, plant and equipment after the tenant terminated their lease agreement.

Revenue

Revenue has shown a steady increase in the last three years ending 2008/09. 2009/10 saw a decrease of R42,6m which is largely attributable to difficulties Mintek had with the ConRoast project and fewer pilot plants being executed than anticipated. The government grant, fully ring-fenced on research projects, remained fairly consistent in absolute terms in the last few years not increasing in line with inflation. Interest income almost doubled compared to 2007 (R12m) establishing this as a significant revenue stream for Mintek.

57

mintek annual report 2010 Annual Financial Statements and Notes

A strong commercial revenue pipeline was the driver to high, but erratic, profits in previous years. Notwithstanding the difficult year, gross margin on commercial projects was maintained at an average of 25%. Mintek still achieved a profit of R1.7m in this financial year, aided by strict expenditure management. Staff costs have increased by only 6% compared to 2009. Measures taken to contain staff costs in this year were the freezing of some vacancies and granting of lower annual increments. Despite a 54% increase in number of staff from 2007, salary costs only increased by 27%.

CASh Flow ANAlYSiS

The cash flow indicates that there have been challenges in making ends meet during the year with the reduced revenue, coupled with slower collections. Normal operations generated an investment of only R2,8m in the current year significantly lower than the R113m invested in the previous financial year. This was mainly as a result of lower working capital being available in the current year.

ASSetS

Capital expenditure

Mintek has seen a major injection into property, plant and equipment (PPE), and specifically equipment funded through state grant and other government agency funding. There has been a reclassification of the investment property as PPE in 2010 due to the termination of the lease from BHP Billiton. Mintek expanded its asset base by R25,1m (2009: R38,6 m) in the 2010 financial year. R14,9m was funded by the State grant received. This grant was specifically allocated to fund capex requirements. Assets with a net book value of R40 000 were written off in the current year.

JudiCiAl pRoCeediNGS

The directors are not aware of any significant judicial proceedings against Mintek, except those as disclosed in note 24 of the Annual Financial Statements.

poSt-BAlANCe Sheet eveNtS

There were no material post-balance sheet events that the directors are aware of.

SuBSidiARieS

The information relating to the entity’s financial interest in its subsidiary is disclosed in note 14 of the Annual Financial Statements.

the diReCtoRS oF miNteK AS At 31 mARCh 2010

executive director Mr MA Mngomezulu

Non-executive directors Mr M Mphomela – Chairperson Mrs N Qunta Mr P Streng Adv D Block Mr p White Ms S Sekgobela Ms S Maja Ms J Ndlovu Mr M Mabuza Mr t nell

The board secretary of Mintek is Ms S Bopape, and the business and postal addresses are as follows:

200 Malibongwe Drive Private Bag X3015Randburg Randburg 2194 2125

mr mA mngomezulu

58

Annual Financial Statements and Notes mintek annual report 2010

Report of the Auditor-GeneralRepoRt oF the AuditoR-GeNeRAl to pARliAmeNt oN the GRoup FiNANCiAl StAtemeNtS ANd peRFoRmANCe iNFoRmAtioN oF the CouNCil FoR miNeRAl teChNoloGY (miNteK) FoR the YeAR eNded 31 mARCh 2010

RepoRt oN the CoNSolidAted FiNANCiAl StAtemeNtS

introduction

I have audited the accompanying consolidated and separate financial statements of Mintek, which comprise the consolidated and separate statement of financial position as at 31 March 2010, and the consolidated and separate statements of comprehensive income, statements of changes in net assets and cash flow statements for the year then ended, and a summary of significant accounting policies and other explanatory information, and the accounting authority’s report as set out on pages 61 to 85.

Accounting Authority’s responsibility for the financial statements

The accounting authority is responsible for the preparation and fair presentation of these financial statements in accordance with South African Statements of Generally Accepted Accounting Practice (SA Statements of GAAP) and in the manner required by the Public Finance Management Act of South Africa, 1999 (Act No.1 of 1999)(PFMA) and the Minerals Technology Act, 1989 (Act 30 of 1989). This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor-General’s responsibility

As required by section 188 of the Constitution of South Africa and section 4 of the Public Audit Act of South Africa, 2004 (Act No. 5 of 2004)(PAA), my responsibility is to express an opinion on these financial statements based on my audit.

I conducted my audit in accordance with International Standards on Auditing and General Notice 1570 of 2009 issued in the Government Gazette 32758 of 27 November 2009. Those standards require that I comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

I believe that the audit evidence I have obtained is sufficient and appropriate to provide a basis for my audit opinion.

opinion

In my opinion, these financial statements present fairly, in all material respects, the consolidated and separate financial position of MINTEK as at 31 March 2010, and its consolidated and separate financial performance and its consolidated and separate cash flows for the year then ended in accordance with the SA Statements of GAAP and in the manner required by the PFMA and the Mineral Technology Act.

RepoRt oN otheR leGAl ANd ReGulAtoRY ReQuiRemeNtS

In terms of the PAA of South Africa and General Notice 1570 of 2009, issued in the Government Gazette No. 32758 of 27 November 2009,

59

mintek annual report 2010 Annual Financial Statements and Notes

I include below my findings on the report on predetermined objectives and compliance with the PFMA, Mineral Technology Act and financial management (internal control).

Findings

Pre-determined objectives.

No matters to report.

Compliance with laws and regulations

income tax Act, 1962 (Act No. 58 of 1962)

Non-adherence to legislation

Contrary to the requirements of the Income Tax Act, 1962 (Act No. 58 of 1962) Fourth Schedule, paragrah 23, the entity has not lodged the Mindev (Pty) Ltd. income tax return with South African Revenue Services for the year under review.

iNteRNAl CoNtRol

I considered internal control relevant to my audit of the financial statements and the report on predetermined objectives and compliance with the PFMA and the Mineral Technology Act, but not for the purposes of expressing an opinion on the effectiveness of internal control. The matters reported are limited to the deficiencies identified during the audit.

No matters to report.

pretoria31 July 2010

60

Annual Financial Statements and Notes mintek annual report 2010

Financial Statements 2010

GRoup miNteK

2010 2009 2010 2009 Notes R r R r

Assets

Non-current assets

Property, plant and equipment 11 191,850,928 187,732,163 191,850,928 187,732,163

Intangible assets 12 3,457,152 4,135,480 3,457,152 4,135,480

Investment property 13 - 12,458,808 - 12,458,808

Investment in subsidiary 14 - - 100 100

Long-term loans and advances 15 4,636 85,690 4,636 85,690

total non-current assets 195,312,716 204,412,141 195,312,816 204,412,241

Current assets

Inventory 16 6,538,871 5,088,576 6,538,871 5,088,576

Trade and other receivables 17 60,242,726 82,422,822 60,242,726 78,977,747

Short-term investments 18 222,888,020 136,206,148 222,888,020 136,206,148

Cash and cash equivalents 3,760,522 79,617,943 3,760,522 79,617,943

total Current assets 293,430,139 303,335,489 293,430,139 299,890,414

Total assets 488,742,855 507,747,630 488,742,955 504,302,655

Equity

Revaluation surplus 109,358,306 110,256,095 109,358,306 110,256,095

Retained earnings 232,698,050 230,107,153 193,386,058 191,055,357

total equity 342,056,356 340,363,248 302,744,364 301,311,452

Liabilities

Non-current liabilities

Long-term retirement benefit obligation 22 30,545,000 32,585,000 30,545,000 32,585,000

Financial lease obligation 23 422,532 667,380 422,532 667,380

30,967,532 33,252,380 30,967,532 33,252,380

Current liabilities

Loans and advances from subsidiary 14 - - 39,472,396 35,665,938

Trade and other payables 19 38,980,835 54,773,871 38,820,531 54,714,754

Deferred income 20 76,373,594 78,510,292 76,373,594 78,510,292

Provisions 21 364,538 847,839 364,538 847,839

Current liabilities 115,718,967 134,132,002 155,031,059 169,738,823

Total equity and liabilities 488,742,855 507,747,630 488,742,955 504,302,655

stateMents of financial position at 31 March 2010

A mngomezulu Sakhi SimelaneCEO, Mintek GM: Finance, MintekRandburg, 30 July 2010

61

mintek annual report 2010 Annual Financial Statements and Notes

GRoup miNteK

2010

R

2009

r

2010

R

2009

r Notes

Continuing operations

revenue 2 346,795,197 389,413,133 346,795,197 389,413,133

Other operating income 3 6,049,878 8,130,036 6,049,878 8,130,036

Foreign currency (loss)/gain (3,718,463) 3,466,892 (3,718,463) 3,466,892

Investment income 4 21,895,534 25,270,245 21,532,951 24,088,317

Staff costs (228,709,077) (216,432,816) (228,709,077) (216,432,816)

Other operating expenses 5 (82,975,150) (118,018,857) (82,973,950) (118,018,857)

Finance expenses 6 (3,328,921) (8,545,590) (3,328,921) (8,545,590)

Audit fees 7 (2,556,579) (1,500,734) (2,556,579) (1,500,734)

Fees for services 8 (37,909,467) (30,157,188) (37,909,467) (30,157,188)

depreciation 9 (14,163,772) (15,500,025) (14,163,772) (15,500,025)

Loss on disposal of property, plant and equipment (81,404) (302,908) (81,404) (302,908)

Post-retirement benefit obligation 10 496,520 4,126,351 496,520 4,126,351

Profit before taxation 1,794,295 39,948,539 1,432,912 38,766,611

Taxation 25 (101,187) (330,940) - -

Profit for the year 1,693,108 39,617,599 1,432,912 38,766,611

Financial Statements 2010stateMents of coMprehensive incoMe for the year ended 31 March 2010

62

Annual Financial Statements and Notes mintek annual report 2010

GRoup miNteK

2010

R

2009

r

2010

R

2009

r Notes

Cash flows from operating activities

Cash receipts from customers 210,448,632 338,533,156 207,003,557 315,218,771

Government grant received 165,840,000 135,834,000 165,840,000 135,834,000

Cash paid to suppliers and employees (373,422,451) (361,127,826) (373,421,251) (361,127,826)

Cash generated from operations 29 2,866,181 113,239,330 (577,694) 89,924,945

Interest received 19,283,636 20,135,737 18,921,053 18,953,809

Finance costs (93,668) (191,324) (93,668) (191,324)

Provisions utilised 21 (1,616,568) (1,759,040) (1,616,568) (1,759,040)

Net cash inflow from operating activities 20,439,581 131,424,703 16,633,123 106,928,390

Cash flows from investing activities

Additions to property, plant and equipment 11.1 (25,120,946) (38,586,851) (25,120,946) (38,586,851)

Additions to intangible assets 12 (533,633) (940,319) (533,633) (940,319)

Funding received towards purchasing of property, plant and equipment 11.1 20,381,777 28,425,147 20,381,777 28,425,147

Funding received towards purchasing of intangible assets 12 46,000 179,515 46,000 179,515

Increase in investment deposits (86,681,872) (39,584,714) (86,681,872) (39,584,714)

Net cash outflow from investing activities (91,908,674) (50,507,222) (91,908,674) (50,507,222)

Cash flows from financing activities

Receipts for subsidiary - - 3,806,458 24,496,313

Long-term creditor payments (244,848) (322,923) (244,848) (322,923)

Post-retirement health care - contributions 22 (72,503) (3,860,467) (72,503) (3,860,467)

Post-retirement health care - settlements 22 (4,070,977) (46,147,137) (4,070,977) (46,147,137)

Net cash outflow from financing activities (4,388,328) (50,330,527) (581,870) (25,834,214)

Net (decrease)/increase in cash and cash equivalents

Cash and cash equivalents at beginning of year

Cash and cash equivalents at end of year

(75,857,421) 30,586,954 (75,857,421) 30,586,954

79,617,943 49,030,989 79,617,943 49,030,989

3,760,522 79,617,943 3,760,522 79,617,943

Financial Statements 2010 stateMents of cash floWs for year ended 31 March 2010

63

mintek annual report 2010 Annual Financial Statements and Notes

Retained earnings Revaluation Surplus total

Note R R R

GRoup

Balance as at 31 march 2008 189,591,765 111,153,884 300,745,649

Depreciation on revaluation of buildings 897,789 (897,789) -

Net profit for the year 39,617,599 - 39,617,599

Balance as at 31 march 2009 230,107,153 110,256,095 340,363,248

Depreciation on revaluation of buildings 897,789 (897,789) -

Net profit for the year 1,693,108 - 1,693,108

Balance as at 31 march 2010 232,698,050 109,358,306 342,056,356

miNteK

Balance as at 31 march 2008 151,390,957 111,153,884 262,544,841

Depreciation on revaluation of buildings 897,789 (897,789) -

Net profit for the year 38,766,611 - 38,766,611

Balance as at 31 march 2009 191,055,357 110,256,095 301,311,452

Depreciation on revaluation of buildings 897,789 (897,789) -

Net profit for the year 1,432,912 - 1,432,912

Balance as at 31 march 2010 193,386,058 109,358,306 302,744,364

Financial Statements 2010STATEMENTS OF CHANGES IN NET ASSETS FOR THE YEAR ENDED 31 MARCH 2010

64

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

General information

The Group consists of Mintek, a schedule 3B public entity and Mindev (Pty) Ltd, a wholly-owned subsidiary incorporated in South Africa.

The principal activities of Mintek and its subsidiary (the “Group”) are to undertake research, development and transfer or commercialisation of mineral technology.

1. Significant accounting policies and basis of preparation

The principal accounting policies applied in the preparation of these consolidated financial statements are materially consistent with those of the previous year, unless otherwise stated.

The consolidated financial statements have been prepared on the historical cost basis except for certain properties and financial instruments, which are measured at revalued amounts and fair values respectively, as explained in the accounting policies set out below.

The financial statements have been prepared in accordance with the South African Statements of Generally Accepted Accounting Practice (SAGAAP), and in the manner required by the Public Finance Management Act (PFMA) and Treasury Guidelines.

The Annual Financial Statements are expressed in its functional currency, South African Rands (R).

The financial statements are prepared in conformity with SAGAAP which requires the use of certain critical accounting estimates. There are no areas that would have involved a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements.

1.1 Basis of consolidation

The consolidated financial statements incorporate the financial statements of Mintek and Mindev.

All intragroup transactions, balances, income and expenses are eliminated on consolidation.

1.2 Foreign currency transactions and balances

At the balance sheet date, monetary assets and liabilities denominated in foreign currencies are translated into South African Rand at exchange rates prevailing at the balance sheet date.

Exchange differences arising on the settlement of monetary items, and on the translation of monetary items, are recognised in profit or loss in the period in which they arise.

1.3 investment in mindev

Subsidiary companies are enterprises in which the company holds a long-term equity interest and over which it has the power to control the financial and operating activities of the entities so as to obtain benefits from its activities. Mindev has over the past year been dormant except for the last payment received on a technology loan.

All investments in Mindev are initially recognised at cost less impairment losses. The carrying amount of such investment is reduced to recognise any decline, other than a temporary decline, in the value of the investment. Any carrying value adjustments are charged to the statement of comprehensive income in the period in which they are incurred.

1.4 investment in associates

The results and assets and liabilities of associates are incorporated in these consolidated financial statements using the equity method of accounting.

An associate is an entity in which the group has significant influence and that is neither a subsidiary nor an interest in a joint venture, through participation in the financial and operating policy decisions of the investee, but not control over those policies.

1.5 intangible assets

Intangible assets acquired separately and with finite useful lives are carried at costs less accumulated amortisation and any accumulated impairment losses. Amortisation for intangible assets with finite useful lives is provided on a straight-line basis over their estimated useful lives.

65

mintek annual report 2010 Annual Financial Statements and Notes

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognised in the statement of comprehensive income when the asset is derecognised.

The estimated useful lives of the major categories of intangible assets are:

Computer Software: 3-5 years

1.6 Research and development costs

Expenditure on research activities is recognised as an expense in the period in which it is incurred.

An internally-generated intangible asset arising from the Group’s research and development is recognised only if all of the following conditions are met:• An asset is created that can be identified (such as software and new processes);• It is probable that the asset created will generate future economic benefits;• The development cost of the asset can be measured reliably;• It is technically feasible to complete the intangible asset so that it will be available for use or sale;• The ability to use or sell the intangible asset; and,• It is the intention to complete the intangible asset so that it will be available for use or sale.

Where no internally-generated intangible asset can be recognised, development expenditure is recognised as an expense in the period in which it is incurred.

Subsequent to initial recognition, internally-generated intangible assets are reported at cost less accumulated amortisation and accumulated impairment losses, on a straight-line basis over their useful lives.

1.7 impairment

At each balance sheet date, the Group assesses the carrying amounts of its tangible and intangible assets to determine whether there is any indication that those assets have suffered an impairment loss. If the recoverable amount of an asset is estimated to be less than its carrying amount, the carrying amount of the asset is reduced to its recoverable amount. An impairment loss is recognised as an expense immediately, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as revaluation decrease.

Where it is not possible to estimate the recoverable amount for an individual asset, the recoverable amount is determined for the cash-generating unit to which the asset belongs.

In addition, intangible assets with indefinite useful lives, intangible assets not yet available for use and goodwill acquired in a business combination are tested for impairment annually, and whenever there is an indication that they may be impaired.

The recoverable amount is determined as the higher of fair value less costs to sell and value in use. Value in use represents the present value of the future cash flows expected to be derived from an asset (cash-generating unit). The expected future cash flows are discounted to their present value using an appropriate discount rate that reflects current market assessments of the time value of money and the risk specific to the asset for which the future cash flow estimates have not been adjusted.

Where an impairment loss subsequently reverses, the carrying amount of the asset (cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (cash-generating unit) in prior years. A reversal of an impairment loss is recognised as income immediately, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

1.8 leases

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards associated with ownership of an asset to the lessee. All other leases are classified as operating leases.

The group as a lessor

Rental income from operating leases is recognised in the statement of comprehensive income on a straight-line basis over the term of the relevant lease.

66

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

The group as a lessee

Assets held under finance leases are recognised as assets of the Group at their fair value at the inception of the lease or, if lower, at the present value of the minimum lease payments. The corresponding liability to the lessor is included in the consolidated balance sheet as a finance lease obligation. Lease payments are apportioned between finance charges and reduction of the lease obligation so as to achieve a constant rate of interest on the remaining balance of the liability.

Finance charges are charged directly to profit or loss, unless they are directly attributable to qualifying assets, in which case they are capitalised.

Rentals payable under operating leases are charged to profit or loss on a straight line basis over the term of the relevant lease. Benefits received and receivable as an incentive to enter into an operating lease are recognised as a reduction of rental expense over the lease term on a straight-line basis.

1.9 property, plant and equipment

Property, plant and equipment, other than land and buildings, are stated at cost less any accumulated depreciation, any earmarked grant funding and any accumulated impairment losses. Costs include all directly attributable expenditure incurred in the acquisition, construction and installation of such assets so as to bring them to the location and condition necessary for them to be capable of operating in the manner intended by management.

Land and buildings held for use in the production or supply of goods and services or for administrative purposes are stated in the balance sheet at their revalued amounts, being the fair value at the date of revaluation, less any subsequent accumulated depreciation and subsequent impairment losses.

Land is not depreciated. Properties were initially valued at historical cost. Revaluations are performed every three years by an independent professional valuator, such that the carrying amount does not differ materially from that which would be determined using fair values at the balance sheet date. (Refer Note 11)

Depreciation is provided to write-off the cost or fair value of property, plant and equipment other than land less their estimated residual values on a straight-line basis, over the estimated useful lives. Useful lives and residual values are reviewed and adjusted if appropriate at each balance sheet date.

The carrying values of property, plant and equipment are reviewed for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. If any such indication exists and when the carrying values exceed the estimated recoverable amount, the assets or cash generating units are written down to their recoverable amount.

Assets held under finance leases are depreciated over their expected useful lives on the same basis as owned assets or, where shorter, the term of the relevant lease.

An item of property, plant and equipment is derecognised upon disposal or when no future economic benefits are expected to arise from the continued use of the asset. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the item) is included in the statement of comprehensive income in the year in which the item is derecognised.

Any revaluation increase arising on revaluation of land and buildings is credited to the non-distributable reserves, except to the extent that it reverses a revaluation decrease of the same asset previously recognised as an expense, in which case the increase is credited to the statement of comprehensive income to the extent of the decrease previously charged. A decrease that offsets previous revaluation increases of the same asset is charged against the non-distributable reserve.

A decrease in net carrying amount arising on revaluation of an asset is dealt with as an expense to the extent that it exceeds the balance, if any, on the non-distributable reserve relating to a previous revaluation of that asset.

On the subsequent sale or retirement of a revalued asset, the attributable revaluation surplus balance is transferred to retained profits.

At balance sheet date, the difference between depreciation based on the revalued carrying-amount of the asset (the depreciation charged to the statement of comprehensive income) and the depreciation based on the asset’s original cost is transferred from non-distributable reserves to retained earnings.

67

mintek annual report 2010 Annual Financial Statements and Notes

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

The estimated useful lives of the major categories of property, plant, equipment are:

Buildings 50 yearsPlant 10 yearsEquipment 3 - 10 yearsVehicles 5 yearsFurniture and fittings 5 years

The gains and losses arising on the disposal or retirement of an item of property, plant, equipment and vehicles are determined as the difference between the sales proceeds and the carrying amount of the assets disposed and is recognised in profit and loss.

1.10 investment properties

Investment properties are measured at their fair values using the fair value model. Gains or losses arising from changes in the fair value of investment property are included in profit or loss for the period in which they arise.

An investment property is derecognised upon disposal or when the investment property is permanently withdrawn from use and no future economic benefits are expected from its disposals.

Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of comprehensive income in the year in which the item is derecognised.

The fair value is determined at balance sheet date by an independent professional valuator based on market evidence of the most recent prices achieved in arms length transactions of similar properties in the same area. (Refer Note 13)

1.11 Employee benefits

The Group operates a number of retirement benefit plans for its employees. These plans include a defined contribution plan and other retirement benefits such as medical aid benefit plans.

A defined contribution plan is a scheme under which the Group pays fixed contributions into a separate entity. The Group has no legal or constructive obligations to pay further contributions if the fund does not hold sufficient assets to pay all employees the benefits relating to employee service in the current and prior periods.

A defined benefit plan is a scheme that is not a defined contribution plan. Typically defined benefit plans define an amount of benefits that an employee will receive on retirement, usually dependent on one or more factors such as age, years of service and compensation.

1.11.1 post-retirement pension obligations

The liability recognised in the statement of financial position in respect of defined benefit pension plans is the present value of the defined benefit obligation at the balance sheet date less the fair value of plan assets, together with adjustments for unrecognised past-service costs. The defined benefit obligation is calculated annually by independent actuaries using the projected unit credit method.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions are charged or credited to equity in the statement of comprehensive income in the period in which they arise.

Past-service costs are recognised immediately in income, unless the changes to the pension plan are conditional on the employees remaining in service for a specified period of time (the vesting period). In this case, the past-service costs are amortised on a straight-line basis over the vesting period.

For defined contribution plans, the Group pays contributions to publicly or privately administered pension insurance plans on a mandatory, contractual or voluntary basis. The Group has no further payment obligations once the contributions have been paid. The contributions are recognised as employee benefit expense when they are due. The liability recognised in the balance sheet in respect of defined benefit pension plans is the present value of the defined benefit obligation at the balance sheet date less the fair value of plan assets, together with adjustments for unrecognised past-service costs. The defined benefit obligation is calculated annually by independent actuaries using the projected unit credit method.

Prepaid contributions are recognised as an asset to the extent that a cash refund or a reduction in the future payments is available.

68

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

1.11.2 post-retirement health care costs

This Group has an obligation to fund the medical aid benefits of all its past employees and dependants of past employees who retired or were in the employment of the Group prior to 31 December 1999. The plan liability is unfunded and fully provided for in the financial statements. The Group uses the projected unit credit actuarial method to determine the present value of its past service cost.

Actuarial gains and losses are recognised in full in the reporting period it relates to and is the excess over the greater of the present value of the past service obligation at the end of the reporting period before deducting the present value of assumed assets at the same date.

Valuations of these obligations are carried out annually by independent, qualified actuaries using appropriate mortality tables, long-term estimates of increases in medical costs and appropriate discount rates. General increases to medical aid contributions were estimated taking into account the projected future changes in the cost of medical services resulting from both inflation and specific changes to medical costs. The obligation calculated assumes that the cross-subsidy of pensioner’s benefits by the active members will continue as at present. If this cross–subsidy were to be removed, it would result in an increased estimated liability.

1.12 inventories

Inventories are stated at the lower of cost or net realisable value. Costs comprise direct materials and, where applicable, direct labour costs and those overheads that have been incurred in bringing the inventories to their present location and condition. Cost is calculated using the weighted average method. Net realisable value represents the estimated selling price in the ordinary course of business less any costs of completion and costs to be incurred in marketing, selling and distribution.

1.13 provisions

Provisions are recognised when the Group has a present obligation as a result of a past event and it is probable that this will result in an outflow of economic benefits and the amount can be reasonably determined.

The Group recognises its obligation for guaranteeing its products and services for periods as stipulated in its contracts with the Group’s customers. (Refer Note 21)

1.14 Financial instruments

Financial instruments recognised on the balance sheet include derivative instruments, investments, investments in debt securities, accounts receivable, cash and cash equivalents, accounts payable and interest-bearing debt. Financial instruments are initially measured at cost including transaction costs when the Group becomes a party to their contractual arrangements. The subsequent measurement of financial instruments is dealt with in the subsequent notes. When the Group can legally do so and the Group intends to settle on a net basis, or simultaneously related positive and negative values of financial instruments are offset within the balance sheet amounts.

1.14.1 derivative instruments

The Group does not use derivative financial instruments including forward rate agreements and forward exchange contracts to hedge its exposure to interest rate and foreign fluctuations. It is the Group’s policy not to hedge its exposure from foreign currency fluctuations, as it does not consider the impact to be significant. It is the policy of the Group not to trade in derivative financial instruments for speculative purposes.

1.14.2 investments

Investments consist of short to long-term money market instruments initially recorded at cost, which is the fair value of the cash placed with the institution. These investments are held-to-maturity financial assets. Interest is accrued using the effective interest rate method and included in the statement of comprehensive income on an accrual basis.

1.14.3 trade and other receivables

Trade and other receivables are recognised initially at fair value and subsequently measured at amortised cost using the effective interest method, less provision for impairment.

A provision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the receivables. Significant financial difficulties of the debtor, probability that the debtor will enter bankruptcy or financial reorganisation, and default or delinquency in payments (more than 30 days overdue) are considered indicators that the trade receivable is impaired.

The amount of the provision is the difference between the asset’s carrying amount and the present value of estimated future cash flows, discounted at the original effective interest rate. The carrying amount of the asset is reduced through the use of a provision account, and

69

mintek annual report 2010 Annual Financial Statements and Notes

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

the amount of the loss is recognised in the statement of comprehensive income. When a trade receivable is uncollectible, it is written off in the year in which it is identified.

Subsequent recoveries of amounts previously written off are credited in the statement of comprehensive income.

1.14.4 Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and cash at the bank.

The carrying amount of cash is measured at its fair value.

1.14.5 Financial liabilities

Financial liabilities are amortised at their original debt value less principal payments and amortisation. Derivatives are subsequently measured at fair value and gains and losses are included in the statement of comprehensive income for the period.

1.15 Government grants

Grants from Government are recognised at their fair value where there is a reasonable assurance that the grant will be received and the Group will comply with all attached conditions.

Government grants, which are intended to give immediate financial support to the entity, are recognised as income in the period in which they are received.

Government grants relating to costs are deferred and recognised in the statement of comprehensive income over the period necessary to match them with the costs that they are intended to compensate.

Government grants earmarked for specific fixed asset acquisitions are netted-off against the cost value of the fixed asset to the extent of the funds received.

1.16 Revenue recognition

Revenue is recognised when the sale transactions giving rise to such revenue is concluded and risks and rewards of ownership and title pass to the buyer under the terms of the applicable contract and the pricing is fixed and determinable.

Revenue is measured at the fair value of the consideration received or receivable and represents amounts receivable for goods sold and services provided in the normal course of business, net of discounts and sales related taxes.

Revenue from the sale of goods is recognised when the goods are delivered and title has passed.

Revenue arising from the rendering of services is recognised when services are provided. Where the outcome of a commercial work contract can be estimated reliably, revenue and costs are recognised by reference to the stage of completion of the commercial work contract at the balance sheet date, as measured by the proportion that costs incurred for work performed to date bear to the estimated total contract costs, except where this would not be representative of the stage of completion.

Where the outcome of a commercial work contract cannot be estimated reliably, contract revenue is recognised to the extent of contract costs incurred that it is probable will be recoverable. Contract costs are recognised as expenses in the period in which they are incurred.

Advance income arising as result of contracts undertaken in terms of commercial work in respect of invoices raised and paid for in advance but for which no substantial work has been made to justify the recognition of any revenue, is deferred until the income is earned based on the percentage of work completed.

Interest income from a financial asset is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts the estimated future cash receipts through the expected life of the financial asset to that asset’s net carrying amount.

Revenue arising from licence fees is recognised on an accrual basis in accordance with the terms of the applicable contracts.

Rental income is derived from rental of fixed property and is recognised on an accrual basis in accordance with the substance of the relevant agreements.

1.17 Contracts in progress

Where the outcome of a contract can be estimated reliably, revenue and costs are recognised by reference to the stage of completion of the contract activity at the balance sheet date. The stage of completion is determined by the proportion of contract costs incurred to date in relation to the estimated total contract costs except where this would not be representative of the stage of completion.

70

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

Variations in contract work, claims and incentive payments are included to the extent that they have been agreed to by the customer.

Where the outcome of the contract cannot be estimated reliably, contract revenue is recognised to the extent of contract costs incurred that it is probable will be recoverable. Contract costs are recognised as expenses in the period in which they are incurred. When it is probable that total contract costs will exceed total contract revenue, the expected loss is immediately recognised as an expense to the statement of comprehensive income.

Where contract costs incurred to date plus recognised profits less recognised losses exceed progress billings, the surplus is shown as amounts due from customers for contract work. For contracts where progress billings exceed contract costs incurred to date plus recognised profits less recognised losses, the surplus is shown as amounts due to customers for contract work. Amounts received before the related work is performed are included in the consolidated balance sheet, as a liability, as deferred income. Amounts billed for work performed but not yet paid by the customer are included in the consolidated balance sheet under trade and other receivables.

1.18 taxation

Mintek is exempt from paying Income Tax in terms of section 10(1)cA(i) of the Income Tax Act no 58 of 1962 but registered for VAT. Mindev is registered for Income Tax purposes and is a legal tax paying entity.

The tax currently payable is based on taxable profit for the financial year. Taxable profit differs from profit as reported in the statement of comprehensive income because it excludes items of income or Mindev's liability for current tax is calculated using tax rates that have been enacted or substantively enacted by the balance sheet date. (Refer Note 25)

1.19 irregular, fruitless and wasteful expenditure

Irregular expenditure means expenditure incurred in contravention of, or not in accordance with, a requirement of any applicable legislation, including:• The PFMA; or,• Any provincial legislation providing for procurement procedures in that state-owned entity.

Fruitless and wasteful expenditure means expenditure that was made in vain and could have been avoided had reasonable care been exercised. All irregular, fruitless and wasteful expenditure is charged against income in the period in which it is incurred.

1.20 Financing costs

Financing costs are recognised in the statement of comprehensive income in the period in which they are incurred.

1.21 Changes in accounting policies and disclosures

1.21.1 New amendments adopted by the entity

• IAS 1 (AC101): Presentation of financial statements - effective 1 March 2009.

The entity has presented a statement of comprehensive income. Comparative information has been re-presented so that it is also in conformity with this revised standard.

Other new standards, amendments to standards and interpretations that has been issued by the standards board and are effective to the entity for the period beginning 1 March 2009 are currently not relevant to the current operations of the entity.

1.21.2 Standards, amendments and interpretations to existing standards that are not yet effective

The following standards and amendments to existing standards have been published and are mandatory for accounting periods beginning on or after 1 January 2010, or later periods, and have not been early adopted by Mintek:

• IAS 17 (AC105): Leases - effective 1 January 2010

Deletion of specific guidance regarding classification of leases of land, so as to eliminate inconsistency with the general guidance on lease classification. As a result, leases of land should be classified as either finance or operating, using the general principles of IAS 17.

• IAS 24 (AC126): Related party disclosures - effective 1 January 2011

Simplification of the disclosure requirements for government-related entities; clarification of the definition of a related party.

A number of other new standards, amendments to standards and interpretations that are not yet effective for the year ended 31 March 2010 that have not been dealt with in the financial statements as they are not relevant to the entity's current operations.

71

mintek annual report 2010 Annual Financial Statements and Notes

GRoup miNteK

2010 2009 2010 2009

R r R r

2. ReveNue

Government grants 123,561,047 105,777,683 123,561,047 105,777,683

State Grant 136,637,372 119,152,632 136,637,372 119,152,632

Less:

Portion of grant utilised to acquire fixed assets (10,244,537) (13,374,949) (10,244,537) (13,374,949)

Portion of grant carried over for committed capex purchases (2,831,788) - (2,831,788) -

other revenue streams 223,234,150 283,635,450 223,234,150 283,635,450

commercial 169,718,635 243,045,372 169,718,635 243,045,372

Earmarked 53,515,515 40,590,078 53,515,515 40,590,078

346,795,197 389,413,133 346,795,197 389,413,133

3. otheR opeRAtiNG iNCome

operating income 4,314,338 4,950,555 4,314,338 4,950,555

Library services 36,578 17,098 36,578 17,098

Breach of contract (employees) 3,000 158,487 3,000 158,487

Breach of contract (bursary/learnerships) 1,357,361 2,931,592 1,357,361 2,931,592

Bad debts recovered 64,935 5,098 64,935 5,098

Sundry income 2,852,464 1,838,280 2,852,464 1,838,280

Rental income - properties 1,735,540 1,908,743 1,735,540 1,908,743

investment property - Rental income - 1,270,738 - 1,270,738

6,049,878 8,130,036 6,049,878 8,130,036

4. iNveStmeNt iNCome

Interest earned: fixed deposits 18,772,285 18,564,615 18,772,285 18,564,615

Interest earned: loans to associates 362,583 1,181,928 - -

Interest earned: bank balances 84,590 272,161 84,590 272,161

Interest earned: staff debtors 53,086 117,033 53,086 117,033

Interest earned: trade debtors 11,092 - 11,092 -

Fair value Interest on debtors 2,611,898 5,134,508 2,611,898 5,134,508

21,895,534 25,270,245 21,532,951 24,088,317

5. otheR opeRAtiNG eXpeNSeS

Consumables 28,082,652 47,715,971 28,082,652 47,715,971

General running expenses 44,504,865 59,547,988 44,503,665 59,547,988

Repairs and maintenance 8,090,558 9,516,062 8,090,558 9,516,062

Fair value adjustment - investment property - 898,249 - 898,249

Bad debts written off 921,837 505,642 921,837 505,642

Provision for debtors' impairment 1,282,979 (165,055) 1,282,979 (165,055)

Inventory written down 104,197 - 104,197 -

82,987,088 118,018,857 82,985,888 118,018,857

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

72

Annual Financial Statements and Notes mintek annual report 2010

6. FiNANCe eXpeNSeS

Interest other - 9,115 - 9,115

Fair value interest on creditors 635,253 1,556,689 635,253 1,556,689

Interest on post-retirement medical obligation 2,600,000 6,797,577 2,600,000 6,797,577

Interest on finance lease 93,668 182,209 93,668 182,209

3,328,921 8,545,590 3,328,921 8,545,590

7. Audit FeeS

Audit fees 2,556,579 1,500,734 2,556,579 1,500,734

2,556,579 1,500,734 2,556,579 1,500,734

8. FeeS FoR SeRviCeS

Consultants 36,204,808 28,189,203 36,204,808 28,189,203

Legal 1,704,659 1,967,985 1,704,659 1,967,985

37,909,467 30,157,188 37,909,467 30,157,188

9. depReCiAtioN

property, plant and equipment

Buildings 1,462,983 1,308,966 1,462,983 1,308,966

plant 2,558,744 2,292,137 2,558,744 2,292,137

Equipment 8,047,635 9,920,497 8,047,635 9,920,497

Vehicles 107,643 107,643 107,643 107,643

Leased assets 488,481 512,671 488,481 512,671

Furniture and fittings 333,622 300,448 333,622 300,448

12,999,108 14,442,362 12,999,108 14,442,362

intangible assets - amortisation

Computer software 1,164,664 1,057,663 1,164,664 1,057,663

14,163,772 15,500,025 14,163,772 15,500,025

10. poSt-RetiRemeNt BeNeFit oBliGAtioNS

Actuarial gain - post-retirement medical obligation (556,520) (4,189,973) (556,520) (4,189,973)

Actuarial loss - pension fund 60,000 63,622 60,000 63,622

(496,520) (4,126,351) (496,520) (4,126,351)

Number of employees 150 166 150 166

GRoup miNteK

2010 2009 2010 2009

R r R r

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

73

mintek annual report 2010 Annual Financial Statements and Notes

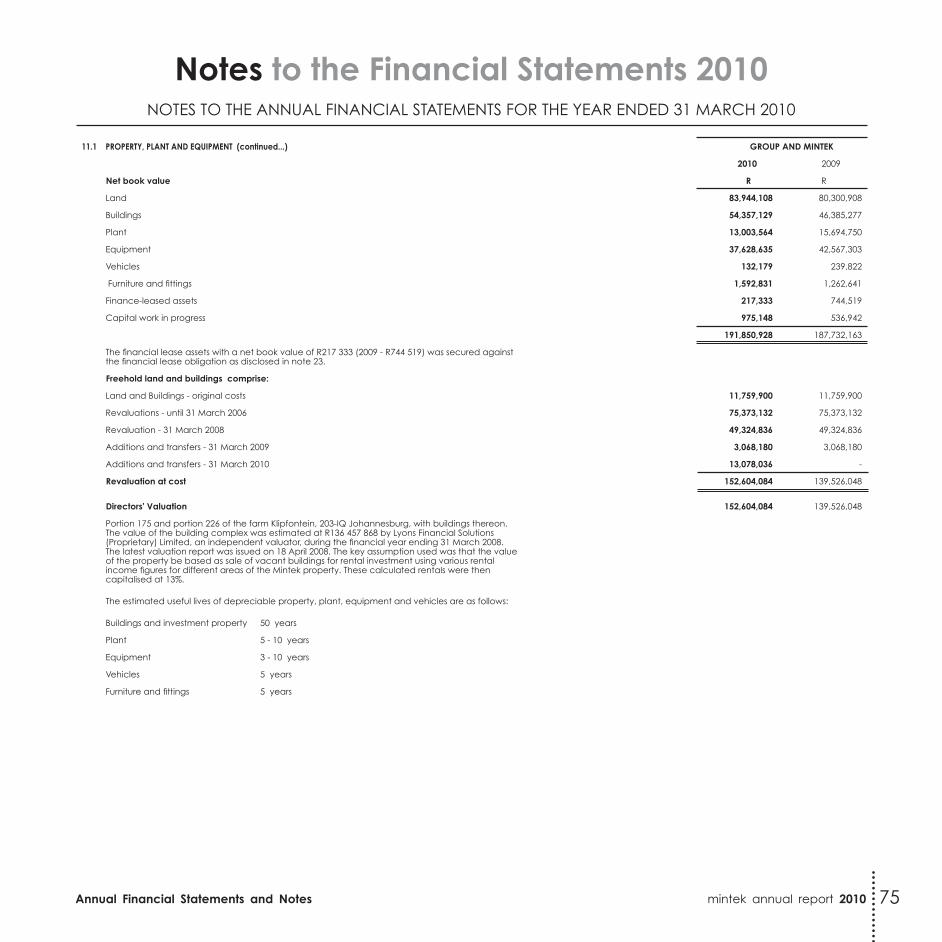

11.1 pRopeRtY, plANt ANd eQuipmeNt

GRoup ANd miNteK 2010 GRoup ANd miNteK 2009

opening Balance

Additions Asset class transfers

Reclass- ification of investment

property

Application of funding to funded

assets

disposals Closing Balance

opening Balance

Additions Asset class transfers

Application of funding to funded

assets

disposals Closing Balance

R R R R R R R R R R R R R

Cost

Land 80,300,908 - - 3,643,200 - - 83,944,108 80,300,908 - - - - 80,300,908

Buildings 59,225,140 79,690 539,540 8,815,608 - (2) 68,659,976 56,156,960 11,641,117 (7,591,267) (981,671) - 59,225,140

plant 40,925,084 7,932 (138,487) - - (18,645) 40,775,884 41,614,440 4,439,084 (138,187) (3,500,716) (1,489,537) 40,925,084

Equipment 102,209,815 23,410,556 119,422 - (20,413,426) (544,659) 104,781,708 91,811,129 22,002,180 13,121,272 (23,936,035) (788,731) 102,209,815

Vehicles 990,580 - - - - - 990,580 990,580 - - - - 990,580

Furniture and fittings 2,763,579 664,234 - - - (11,759) 3,416,054 2,277,909 504,406 - (6,726) (12,010) 2,763,579

finance Leased assets 2,312,644 - - - - (300,396) 2,012,248 2,312,644 - - - - 2,312,644

capital work in progress 536,942 957,382 (519,176) - - - 975,148 5,928,760 - -5,391,818 - - 536,942

289,264,692 25,119,794 1,299 12,458,808 (20,413,426) (875,461) 305,555,707 281,393,330 38,586,787 - (28,425,147) (2,290,278) 289,264,692

opening Current Year

deprec-iation

Asset class transfers

Reclass- ification of investment

property

Application of funding to funded

assets

disposals Closing opening Current Year depreciation

Asset class transfers

Application of funding to funded

assets

disposals Closing

R R R R R R R R R R R R R

Accumulated depreciation

Buildings 12,839,862 1,462,983 2 - - 14,302,847 11,582,593 1,308,966 (51,697) - - 12,839,862

plant 25,230,334 2,558,744 (1,154) - - (15,604) 27,772,320 24,246,180 2,292,137 (21,568) - (1,286,415) 25,230,334

Equipment 59,642,512 8,047,635 - (31,649) (505,425) 67,153,073 50,339,481 9,920,497 72,904 - (690,370) 59,642,512

Vehicles 750,758 107,643 - - - - 858,401 643,115 107,643 - - - 750,758

Furniture and fittings 1,500,938 333,622 - - - (11,337) 1,823,223 1,210,779 300,448 294 - (10,583) 1,500,938

finance Leased assets 1,568,125 488,481 - - - (261,691) 1,794,915 1,055,454 512,671 - - - 1,568,125

101,532,529 12,999,108 (1,152) - (31,649) (794,057) 113,704,779 89,077,602 14,442,362 (67) - (1,987,368) 101,532,529

Fully depreciated assets and funded assets with a total acquisition value of R39 483 261 (2009: R19 948 401) is still in use.

These assets are recorded at R1 in the asset register and are not subject to the annual revaluation.

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

74

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

11.1 pRopeRtY, plANt ANd eQuipmeNt (continued...) GRoup ANd miNteK

2010 2009

Net book value R r

Land 83,944,108 80,300,908

Buildings 54,357,129 46,385,277

plant 13,003,564 15,694,750

Equipment 37,628,635 42,567,303

Vehicles 132,179 239,822

Furniture and fittings 1,592,831 1,262,641

Finance-leased assets 217,333 744,519

Capital work in progress 975,148 536,942

191,850,928 187,732,163

The financial lease assets with a net book value of R217 333 (2009 - R744 519) was secured against the financial lease obligation as disclosed in note 23.

Freehold land and buildings comprise:

Land and Buildings - original costs 11,759,900 11,759,900

Revaluations - until 31 March 2006 75,373,132 75,373,132

Revaluation - 31 March 2008 49,324,836 49,324,836

Additions and transfers - 31 March 2009 3,068,180 3,068,180

Additions and transfers - 31 March 2010 13,078,036 -

Revaluation at cost 152,604,084 139,526,048

directors' valuation 152,604,084 139,526,048

Portion 175 and portion 226 of the farm Klipfontein, 203-IQ Johannesburg, with buildings thereon. The value of the building complex was estimated at R136 457 868 by Lyons Financial Solutions (Proprietary) Limited, an independent valuator, during the financial year ending 31 March 2008. The latest valuation report was issued on 18 April 2008. The key assumption used was that the value of the property be based as sale of vacant buildings for rental investment using various rental income figures for different areas of the Mintek property. These calculated rentals were then capitalised at 13%.

The estimated useful lives of depreciable property, plant, equipment and vehicles are as follows:

Buildings and investment property 50 years

plant 5 - 10 years

Equipment 3 - 10 years

Vehicles 5 years

Furniture and fittings 5 years

75

mintek annual report 2010 Annual Financial Statements and Notes

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

12. iNtANGiBle ASSetS

GRoup ANd miNteK 2010 GRoup ANd miNteK 2009

opening Balance Additions Asset class

transfersApplication of

funding Closing Balance

opening Balance Additions Application

of funding Closing Balance

R R R R R R R R R

Cost

Computer software 6,460,272 533,633 (1,299) (46,000) 6,946,606 5,699,468 940,319 (179,515) 6,460,272

6,460,272 533,633 (1,299) (46,000) 6,946,606 5,699,468 940,319 (179,515) 6,460,272

opening Balance

Current Year Amortisation Adjustment Closing

Balanceopening Balance

Current Year Amortisation Adjustment Closing Balance

R R R R R R R R

Accumulated Amortisation

Computer software 2,324,792 1,164,664 - (2) 3,489,454 1,267,129 1,057,663 - 2,324,792

2,324,792 1,164,664 - (2) 3,489,454 1,267,129 1,057,663 - 2,324,792

value as at 31 march 2010 3,457,152 value as at 31 march 2009 4,135,480

The estimated useful lives of depreciable intangible assets are as follows: 3-5 years

13. iNveStmeNt pRopeRtY

GRoup ANd miNteK 2010 GRoup ANd miNteK 2009

opening Balance

Reversal/ Reclassification

Closing Balance

opening Balance Revaluation Closing

Balance

R R R R R R

Buildings -Billiton 12,458,808 (12,458,808) - 13,357,057 (898,249) 12,458,808

12,458,808 (12,458,808) - 13,357,057 (898,249) 12,458,808

Fair value as at 31 march 2010 - Fair value as at 31 march 2009 12,458,808

Portion of portion 175 of the farm Klipfontein, 203-IQ Johannesburg, with buildings thereon. The value of the building complex was estimated at R12 458 808 by Resurgent Projects (Proprietary) Limited, an independent valuator for the year ended 31 March 2009. The latest valuation report was issued on 30 April 2009. The key assumptions used by the independent valuator were the utilisation of the income capitalisation method based on an average investor's risk rate (13%) and applying additional adjustment due the specialised nature of the property (1%) and the fact that the building is ostensibly vacant (1%). The revised capitalisation rate of 15% was then applied to conservative and competitive rental. This property was reclassified and transferred to property, plant and equipment from 1 April 2009 due to termination of the lease by BHP Billiton.

14.1 iNveStmeNt iN SuBSidiARY

Details of subsidiary are as follows:

Name of subsidiary place of incorporation

portion of ownership

Financial year end

Shares at cost 31 march 2010

Shares at cost 31 march 2009

indebtness 31 march 2010

indebtness 31 march 2009

Mindev (Proprietary) Limited South Africa 100% 31 March 2010 100 100 39,472,396 35,665,938

100 100 39,472,396 35,665,938

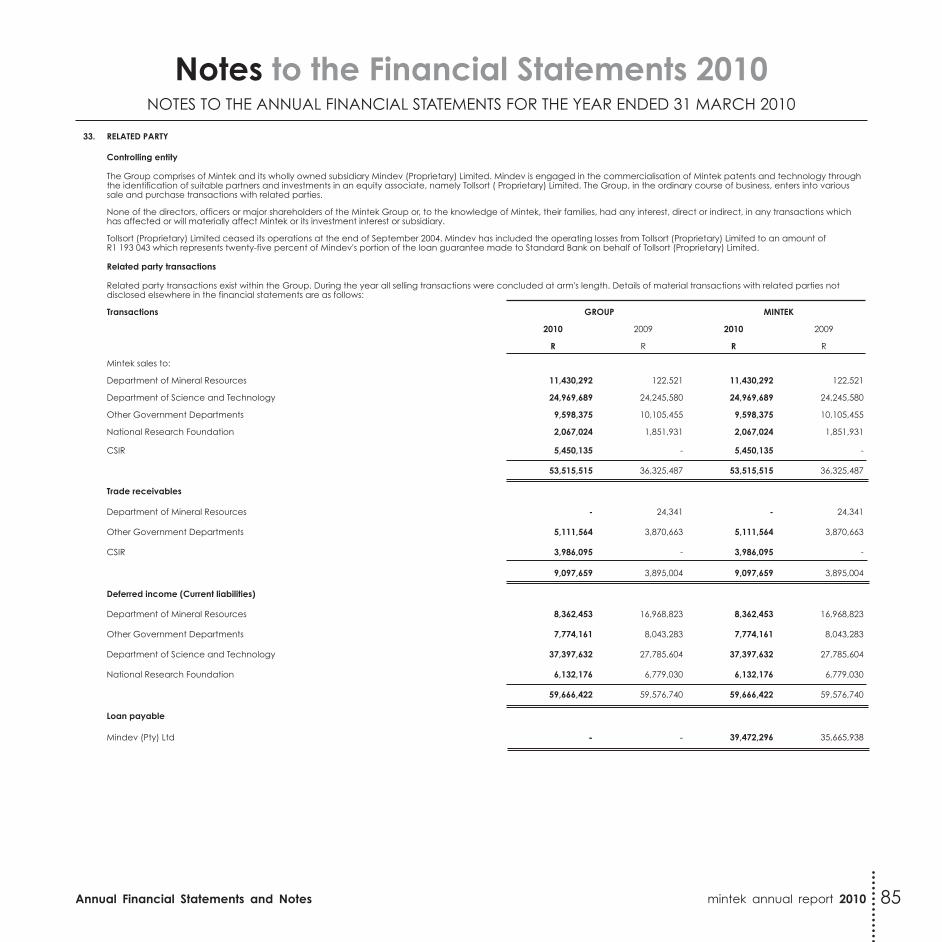

Mindev is engaged in the commercialisation of Mintek's patents and technology through the identification of suitable partners to advance such interests by way of direct investments in equity and through joint ventures.

Mintek holds 100% of the issued share capital of Mindev (Proprietary) Limited. The loans granted are unsecured and do not have fixed repayments terms.

14.2 iNveStmeNt iN ASSoCiAteS

SuBSidiARY ASSoCiAte: tollSoRt (pRopRietARY) limited

Tollsort (Proprietary) Limited ceased its operations at the end of September 2004 and as such there are no current financial statements available for Tollsort to provide adequate disclosure. Mindev has included the operating losses from Tollsort (Proprietary) Limited to an amount of R1 193 043 which represents twenty-five percent of Mindev's portion of the loan guarantee made to Standard Bank on behalf of Tollsort (Proprietary) Limited.

The investment was written off in 2010 after African Mineral Exploration Company did not accept the donation of the shares.

76

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

GRoup miNteK

2010 2009 2010 2009

Notes R r R r

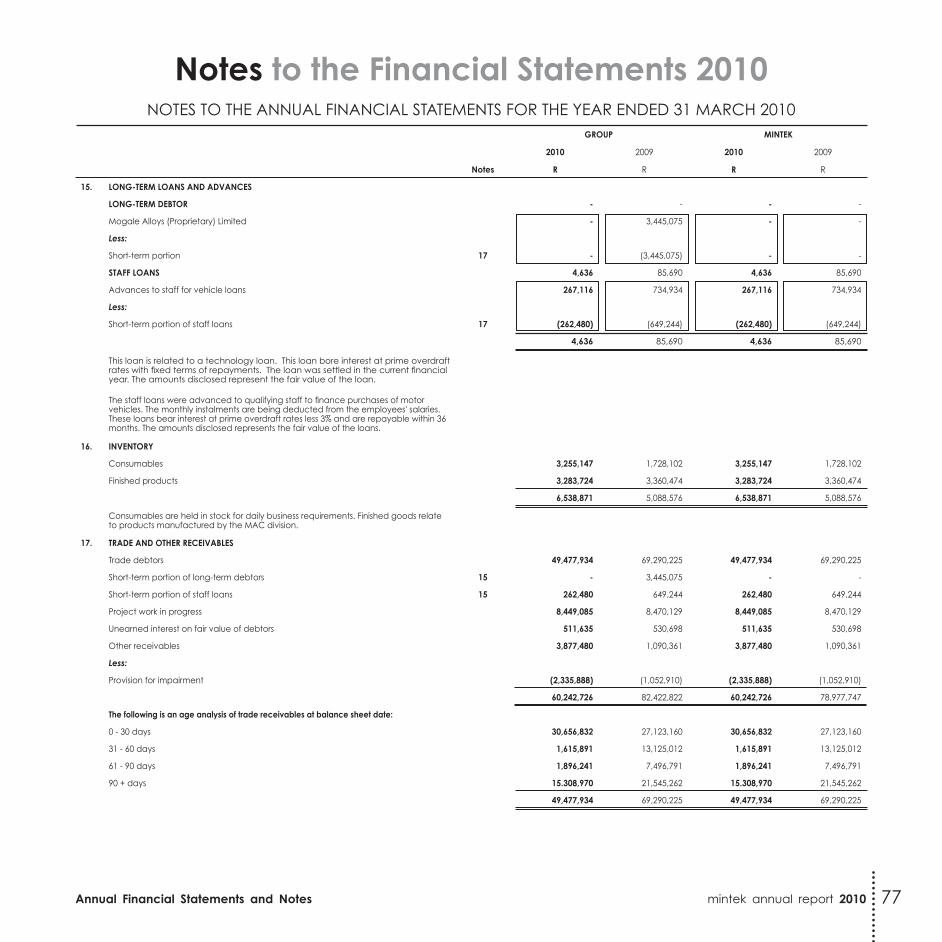

15. loNG-teRm loANS ANd AdvANCeS

loNG-teRm deBtoR - - - -

Mogale Alloys (Proprietary) Limited - 3,445,075 - -

Less:

Short-term portion 17 - (3,445,075) - -

StAFF loANS 4,636 85,690 4,636 85,690

Advances to staff for vehicle loans 267,116 734,934 267,116 734,934

Less:

Short-term portion of staff loans 17 (262,480) (649,244) (262,480) (649,244)

4,636 85,690 4,636 85,690

This loan is related to a technology loan. This loan bore interest at prime overdraft rates with fixed terms of repayments. The loan was settled in the current financial year. The amounts disclosed represent the fair value of the loan.

The staff loans were advanced to qualifying staff to finance purchases of motor vehicles. The monthly instalments are being deducted from the employees' salaries. These loans bear interest at prime overdraft rates less 3% and are repayable within 36 months. The amounts disclosed represents the fair value of the loans.

16. iNveNtoRY

Consumables 3,255,147 1,728,102 3,255,147 1,728,102

Finished products 3,283,724 3,360,474 3,283,724 3,360,474

6,538,871 5,088,576 6,538,871 5,088,576

Consumables are held in stock for daily business requirements. Finished goods relate to products manufactured by the MAC division.

17. tRAde ANd otheR ReCeivABleS

Trade debtors 49,477,934 69,290,225 49,477,934 69,290,225

Short-term portion of long-term debtors 15 - 3,445,075 - -

Short-term portion of staff loans 15 262,480 649,244 262,480 649,244

Project work in progress 8,449,085 8,470,129 8,449,085 8,470,129

Unearned interest on fair value of debtors 511,635 530,698 511,635 530,698

Other receivables 3,877,480 1,090,361 3,877,480 1,090,361

Less:

Provision for impairment (2,335,888) (1,052,910) (2,335,888) (1,052,910)

60,242,726 82,422,822 60,242,726 78,977,747

the following is an age analysis of trade receivables at balance sheet date:

0 - 30 days 30,656,832 27,123,160 30,656,832 27,123,160

31 - 60 days 1,615,891 13,125,012 1,615,891 13,125,012

61 - 90 days 1,896,241 7,496,791 1,896,241 7,496,791

90 + days 15.308,970 21,545,262 15.308,970 21,545,262

49,477,934 69,290,225 49,477,934 69,290,225

77

mintek annual report 2010 Annual Financial Statements and Notes

17. tRAde ANd otheR ReCeivABleS (continued...)

provision for impairment

included in the trade receivable balance are debtors which are past the original expected collection date (past due) at the reporting date, with a carrying amount of R14,721,789 (2009: R8,952,518) for which the company has not provided as there has not been a significant change in credit quality and the amounts are still considered recoverable. The company does not hold any collateral over these balances. The average age of these receivables is 76 days (2009: 100 days). A summarised age analysis of past debtors is set out below.

Ageing of past due but not impaired

60 - 90 days 1,896,241 7,434,945 1,896,241 7,434,945

90 - 120 days 12,825,548 1,517,573 12,825,548 1,517,573

14,721,789 8,952,518 14,721,789 8,952,518

movement in the allowance for doubtful debts

Balance at beginning of the year 1,052,910 1,217,964 1,052,910 1,217,964

Increase / (decrease) in provision 1,282,978 (165,054) 1,282,978 (165,054)

Balance at end of the year 2,335,888 1,052,910 2,335,888 1,052,910

Ageing of impaired trade receivables

60 - 90 days - - - -

90 - 120 days 2,335,888 1,052,910 2,335,888 1,052,910

Balance at end of the year 2,335,888 1,052,910 2,335,888 1,052,910

In determining the recoverability of a trade receivable, the company considers any change in the credit quality of the trade receivable from the date credit was initially granted up to the reporting date. Accordingly, the directors believe that there is no further credit provision required in excess of the allowance for doubtful debts. The company does not hold any collateral over these balances.

18. ShoRt-teRm iNveStmeNtS

Short-term investments 222,888,020 136,206,148 222,888,020 136,206,148

Investments in short-term fixed deposits are held with various reputable financial institutions at market value and interest has been earned at prime overdraft rates less a varied percentage over the year.Fixed investments held with various public financial institutions is partly earmarked as financing for the post-retirement medical aid liability.

19. tRAde ANd otheR pAYABleS

Trade payables 15,717,455 23,457,019 15,717,455 23,457,019

Unpaid interest - creditors (48,143) 290,946 (48,143) 290,946

Salary related payables 3,661,940 1,087,594 3,661,940 1,087,594

Current portion of lease creditor 23 227,929 359,586 227,929 359,586

SA Revenue Services - Other 3,335,608 10,582,837 3,335,608 10,582,837

SA Revenue Services - Income Tax 160,304 59,119 - -

Provision for leave pay 10,380,283 11,157,215 10,380,283 11,157,215

Accruals 5,545,459 7,779,557 5,545,459 7,779,557

38,980,835 54,773,873 38,820,531 54,714,754

The following is an age analysis of the trade and salary payables and accruals at balance sheet date:

0 - 60 days 27,405,512 32,324,170 27,405,512 32,324,170

61 - 90 days 559,441 - 559,441 -

90 + days 247,365 - 247,365 -

28,212,318 32,324,170 28,212,318 32,324,170

The average credit period for purchases is 45 days. Mintek has financial risk management policies to ensure that payables are paid within the credit timelines.

GROUP MINTEK

2010 2009 2010 2009

Notes R R R R

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

78

Annual Financial Statements and Notes mintek annual report 2010

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

20. deFeRRed iNCome

Deferred income 59,666,422 59,576,740 59,666,422 59,576,740

Advance client billing (Unearned income) 16,707,172 18,933,552 16,707,172 18,933,552

76,373,594 78,510,292 76,373,594 78,510,292

Deferred income arises as a result of contracts undertaken for several government departments and institutions in respects of amounts received in cash not yet accounted for as revenue.

Advance client billing income arise as a result of contracts undertaken in terms of commercial work where invoices are raised based on work that has not been done. The quantum of cost incurred provides the basis for the level of revenue recognised in the period.

21. pRoviSioNS opening Balance

RAdditional provisions

Rutilised and reversed

RClosing Balance

R

GRoup ANd miNteK

31 march 2010

Product warranties 847,839 1,133,267 (1,616,568) 364,538

847,839 1,133,267 (1,616,568) 364,538

GRoup ANd miNteK

31 march 2009

Product warranties 409,606 2,197,273 (1,759,040) 847,839

409,606 2,197,273 (1,759,040) 847,839

The provision for product warranties is Mintek recognising its probable liability for meeting its obligations in terms of products and services as stipulated in its contracts with its customers.

GROUP MINTEK

2010 2009 2010 2009

R R R R

22. loNG-teRm RetiRemeNt BeNeFit oBliGAtioN

Post-retirement medical aid 29,300,000 31,400,000 29,300,000 31,400,000

Pension benefit liability 1,245,000 1,185,000 1,245,000 1,185,000

long-term retirement benefit obligation 30,545,000 32,585,000 30,545,000 32,585,000

Number of employees members 150 166 150 166

post-retirement medical benefits

The amounts included in the balance sheet arising from Mintek's obligation in respect of post-retirement medical benefits is as follows:

Present value of obligations as at 31 March 2010 29,300,000 31,400,000 29,300,000 31,400,000

Post-retirement benefit obligation

Fixed investments held with various public financial institutions is partly earmarked as financing for the post-retirement medical aid liability. Mintek has not assigned a specific fund to hedge against the post-retirement medical aid liability.

movement in the net liability recognised in the balance sheet

Net-past service benefit liability: Beginning of the year 31,400,000 78,800,000 31,400,000 78,800,000

Interest cost 2,600,000 6,797,577 2,600,000 6,797,577

Contributions paid to service providers (72,503) (3,860,467) (72,503) (3,860,467)

Net actuarial gain (556,520) (4,189,973) (556,520) (4,189,973)

Settlements (4,070,977) (46,147,137) (4,070,977) (46,147,137)

Net-past service benefit liability: End of the year 29,300,000 31,400,000 29,300,000 31,400,000

GROUP MINTEK

2010 2009 2010 2009

R R R R

79

mintek annual report 2010 Annual Financial Statements and Notes

Pension benefit liability

Pension benefits are provided by membership of the Mintek Retirement Fund (MRF) and the Mintek Employees Retirement Fund (MERF).

movement in the net-liability recognised in the balance sheet

Employer liability at beginning of year 1,185,000 1,121,378 1,185,000 1,121,378

Prior year adjustments - 622,622 - 622,622

Payments - (972,000) - (972,000)

Interest costs - 133,000 - 133,000

Actuarial loss 60,000 280,000 60,000 280,000

Net employer liability at end of year 1,245,000 1,185,000 1,245,000 1,185,000

Current cost 60,000 63,622 60,000 63,622

At inception of the Fund a Retirement Reserve was allocated to certain members which will become payable at the time of the members' death or withdrawal. The employer also funds a minimum guaranteed pension for a member who entered the fund as at 1 January 1995. For purpose of calculating the valuation investment returns are expected to exceed salary increases by 3%.

* These payments are made from within the MRF and Mintek has no direct control over it.

Contributions are charged against income in the period in which they are incurred. Contributions so charged were as follows:

MRF and MERF 23,098,815 16,263,908 23,098,815 16,263,908

22. loNG-teRm RetiRemeNt BeNeFit oBliGAtioN (continued...)

Key assumptions

Expected long-term rate of return on plan assets 9.3% 8.5% 9.3% 8.5%

Expected increase in health care costs 7.0% 9.5% 7.0% 9.5%

Amounts recognised in income in respect of the scheme are as follows:

Current cost 2,600,000 - 2,600,000 -

Benefits paid

Contributions paid 72,503 3,860,467 72,503 3,860,467

Expected average remaining life of employees (years) 25 16 25 16

Sensitivity Analysis on past Service Cost

Discount rate increased by 1% p.a. 25,390,000 27,200,000 25,390,000 27,200,000

Discount rate decreased by 1% p.a. 34,180,000 36,700,000 34,180,000 36,700,000

Subsidy inflation increase by 1% p.a. 34,320,000 36,700,000 34,320,000 36,700,000

Subsidy inflation decrease by 1% p.a. 25,220,000 27,100,000 25,220,000 27,100,000

Retirement age 58 32,470,000 34,400,000 32,470,000 34,400,000

Medical cover is provided through a number of different schemes. Post-retirement medical cover in respect of qualifying employees is recognised as an expense over the expected remaining service lives of the relevant employees. The group has an obligation to provide medical benefits to certain pensioners and dependants. These liabilities have been provided in full, calculated on an actuarial basis. The liabilities are unfunded. Periodic valuation of these obligation is carried out by independent actuaries every year, the latest one being 31 March 2010.

GRoup miNteK

2010 2009 2010 2009

R r R r

Notes to the Financial Statements 2010notes to the annual financial stateMents for the year ended 31 March 2010

80