contents psv touches your life in some way each day

TRANSCRIPT

PSV Holdings Limited Annual Report 2010

Cont

ents

Vision, mission and goals 1

Group overview 3

All about us 4

Local and global footprint 5

Operational review 6

Board of Directors 12

Chairperson’ review 14

Chief executive officer’s review 16

Corporate social investment 20

Corporate governance 21

PSV touches your life in some way each day

Annual financial statements 29

Analysis of ordinary shareholders 76

Shareholders diary 78

Notice of annual general meeting 79

Form of proxy 83

Instructions to the form of proxy 84

Administration IBC

To be a recognised provider of specialised industrial engineering products and

services throughout Africa

To continue developing as a specialised industrial engineering group focused on

pumps, valves, engineering linings, industrial supplies, fuel pumps and dispensers

and cryogenics through the provision of superior customer service throughout Africa

To increase shareholder value

To embrace broad-based black economic empowerment principles

To empower every employee through participation in a share incentive scheme

Visi

onM

issi

onGo

als

1PSV Annual Report 2010

3PSV Annual Report 2010

Pumps, spares and valves Specialised services Engineering linings and industrial supplies

Areas of expertise

• Manufacturer, service and repair of pumps, spares

and valves

• OEM supplier of water and petrochemical pumps

• Supplier of pumps to API 610 specifications for

petrochemical use

• Turnkey mechanical electrical contracts

• Supply of UPVC piping to various industries

• Manufacture of cryogenic storage tanks and road

tankers, road tankers and auxiliary equipment

• Service and maintenance of cryogenic equipment

• Specialised cryogenic solutions

• Manufacture, repair service and support of fuel pump

dispensers

• Bulk meters at forecourt

• Flow meters and consumer fuelling equipment

• Forecourt and retail management software

• Specification, selection and installation of lining

products

• Sole distributor of low tile glass linings

• Specialised geo-synthetic linings contracting for

containment, environment protection and corrosion

protection

• Piping, fittings, flanges and steel to mining and

specialised industry and industrial consumables

Number of staff 84 206 90

Facilities 5 119 m2 5 437 m2 1 340 m2

Applications and

product lines

• vertical turbine pumps

• split-casing

• end-suction

• vertical sump pumps

• API 610 designs for the petrochemical industry

• multi-stage high pressure pumps, all manufactured

to the internationally accredited standard of

ISO 9001:2008

• large bulk storage vessels

• rigid and semi-trailer tankers

• vacuum insulated piping

• a full range of vaporisers

• cryogenic food freezing equipment

• cryogenic dosing systems

• cryogenic ambient vaporizers

• dry phase systems

• transformer drying equipment used to remove moisture

from transformer cores before tanking

• cryogenic pressure vessels and heat exchangers

• waterproofing

• lining of landfills

• evaporation pads

• storage dams, canals and dams in the agricultural

sector

• heap leach pads, slimes disposals, water storage dams

and processing plants for the mining industry

• coal chutes, coal hoppers and storage silos to

overcome blockages and bridging of the various

products within the storage facility

Sectors supplied to

Mining, water reticulation, infrastructure, coal power,

nuclear power and manufacturing

South African industrial gas industry including applications

for hospitals, shipping, manufacturing, carbonated soft

drinks and petrochemical

Mining, infrastructure, coal power, agriculture,

construction, water supply and manufacturing

Group overview

4 PSV Annual Report 2010

’06Listing of PSV as an

industrial engineering group, on the Alternative

Exchange of the JSE

All a

bout

us

PSV Zambia 100%

Pumps, spares and valves

Mather + PlattPumps 100%

PSV Services100%

APE Pumps100%

Specialised services

Rand Air & Gas Industries 100%

Cryoshield100%

Petrologic100%

Engineering linings and industrial supplies

Omnirapid100%

Engineered Linings 100%

Group Line Projects 100%

Milestones

Financial highlights

Group structure

’94Relocation to larger premises to house company expansion

’01Establishment of PSV Zambia

in Kitwe to supply mines in the copper belt

’88Establishment of PSV

Services with three staff members

’90Expansion of manufacturing base to meet order demand

’08PSV successfully

concluded the purchase of Rand Air & Gas Installations

’09PSV adds Mather + Platt as a brand

name to its already sizeable pump capability

’10The acquisition of Cryoshield

becomes unconditional, strengthening PSV’s cryogenics capability

’07PSV successfully concluded the 100% acquisition of APE Pumps, Dasher and

Engineered Linings further strengthening the overall service offering

A Black Economic Empowerment (“BEE”) deal with Vunani Capital is successfully entered into

’03Secure large mining supply

contract in Zambia

Revenue (R’000)500 000

400 000

300 000

200 000

100 000

0’08’07 ’09 ’10

Operating profit (R’000) 50 000

40 000

30 000

20 000

10 000

0

25

20

15

10

5

0’08’07 ’09 ’10

Headline earnings per share (cents) 8.00

6.40

4.80

3.20

1.80

0’08’07 ’09 ’10

6 PSV Annual Report 2010

Pumps, spares and valves

The pumps, spares and valves segment supplies, manufactures, designs, maintains,

refurbishes, imports and services pumps, pumps spares and valves. It is operational primarily

in South Africa and Zambia, while the latter largely focuses on the mining sector. Capabilities

stretch across mechanical, electrical and complete fluid handling contracts. The segment has

OEM (Original Equipment Manufacturer) status as well as the ability to manufacture certain

pumps to ISO 9001 2008 standards. The Mather + Platt acquisition has been absorbed into PSV

with marketing efforts gaining momentum across South Africa.

Our pump manufacturing arm

has been designing,

developing, manufacturing and

refurbishing pumps for more

than half a century and has an

extensive installed product base

in mines, municipalities, paper

mills, minerals beneficiation

companies, ports and harbours,

water authorities, power

generation utilities and

petrochemical refineries

throughout Africa and

worldwide.

Oper

atio

nal r

evie

w

8 PSV Annual Report 2010

Specialised servicesManufacture, support and

supply of services and

product to the petrochemical

and cryogenic markets.

PSV supplies much needed design and manufacturing capability, through the manufacture of

cryogenic storage tankers, road tankers, cryogenic liquid transfer systems including vacuum

insulated lines and vacuum process vessels to the gas industry in South Africa and Africa. It has

the capability to manufacture large capacity, new generation, cryogenic freezing equipment,

which requires specialised fabricating techniques in stainless steel.

The wide range of pumps, valves, regulators and vaporisers supply gases to industries such as

hospitals, welding workshops, food and beverages and ship container purification. Our cryogenic

capability offers a full repair and complete refurbishment service.

The petrochemical sector is supported through the provision of fuel pumps and dispensers,

bulk meters, LPG dispensers and point-of-sale forecourt and retail store software to an array

of petroleum companies in South Africa and neighbouring countries.

Oper

atio

nal r

evie

w

10 PSV Annual Report 2010

Engineering linings and industrial supplies

The segment offers an array of lining solutions including geo-synthetic, glass, ceramic and plastic lining solutions used for the purpose of containment, environmental, wear and corrosion protection. Work is undertaken together with mining operators to assist with functions such as protection of seepage and environmental protection.

The stronger, more durable linings such as glass and ceramics are used to limit the effects of wear and tear and increase product flow properties in storage units such as coal hoppers, coal chutes or bin liners in the movement of bulk product.

All applications are used in power stations and industries such as agriculture, mining, construction and water supply.

The industrial supplies component enables PSV to source piping, fittings, flanges and steel from internal and external suppliers. These consumables are provided to mining and industrial clients locally in South Africa as well as being exported to other African countries.

Specialising in the supply and

installation of geo-synthetic

linings for all containment

applications including dams,

leach pads and floating covers

and lining solutions to solve a

variety of materials handling

flow and wear problems.

Oper

atio

nal r

evie

w

12 PSV Annual Report 2010

Board of directors

w Abilio (Abie) JD da Silva (48)

Chief executive officer

Abie is the co-founder of the Group and was

appointed as the chief executive officer upon listing.

He has retained the position and steered the Group

towards the growth objectives it has achieved to date.

He obtained a National Technical Certificate 5 from

the Johannesburg Technical College and a Business

Management Diploma from Damelin College.

w Peter Robinson (49)

Executive director and deputy chairman

Peter qualified at Huddersfield Technical College

in the United Kingdom. As a co-founder of PSV,

Peter has been instrumental in securing long-term

contracts for the supply and repair of rotating

machinery (pumps, pump spares, etc) to various

geographical areas throughout Africa. He is the

managing director of PSV Services.

w Evelyn Chimombe-Munyoro (37)

Non-executive chairperson – BA LLB LLM

(Commercial law/Maritime law)

Evelyn is an admitted attorney of the High Court

of South Africa. Having worked at the specialised

corporate finance law firm, Jowell Glyn & Marais,

she joined Fairbridges Attorneys in the commercial

law department in 2002. She was appointed director

and partner at the end of 2004. Evelyn served on the

board of Vunani Capital Holdings (Pty) Limited in her

capacity as a non-executive director during 2005

and joined Vunani Capital Holdings (Pty) Limited as

an executive director in 2006. She serves on the

board of the Southern African German Chamber of

Commerce & Industry as a non-executive director

and chairs its committee representing the interests of

German industry in South Africa in relation to broad-

based black economic empowerment.

w Mitesh M Patel (35)

Independent non-executive director – CA(SA)

Chairman of the Audit Committee

Member of the Remuneration Committee

Chairman of the Nomination Committee

Mitesh, upon completion of his articles, opened his

own audit practice and due to self-motivation and

entrepreneurial skills built up a significant client base

and network over a short period of time. He was

presented with an opportunity to join the fifth

largest audit practice in South Africa and became

the managing director of PKF (Pta) Incorporated.

Currently Mitesh is an audit managing partner at

Nkonki Inc. He currently serves on the boards of

Africa Cellular Towers Limited, African Dawn Capital

Limited, Stratcorp Limited and Wearne Limited

as an independent non-executive director.

w Anthony (Tony) R Dreisenstock (49)

Financial director

Acting company secretary

Tony holds BCom and BAcc degrees obtained

from the University of the Witwatersrand as well

as an H Dip Tax Law obtained at the University

of Johannesburg. Tony is a qualified chartered

accountant. He successfully operated a strategic

management consultancy practice until August 2005

when he was recruited by PSV to assist in listing the

Company and to assume the role of financial director.

w David (Dave) J Kelly (51)

Executive director

Dave was born in Britain and now resides in South

Africa. He obtained an O-level academic qualification

and a City & Guilds diploma at the London Institute in

the United Kingdom. He is the managing director of

Group Line.

w Gordon S Nzalo (44)

Independent non-executive director

BCom BAcc (Wits), CA(SA)

Chairman of the Risk Committee and a member of

the Audit Committee

Gordon has extensive experience in risk management,

corporate governance, external and internal auditing

and was previously a partner with both KPMG and

PWC. He is a director for a number of companies

including Austro Limited, Vunani Limited, Grand

Bridge Trading 65 (Pty) Limited, Mnande Investments

(Pty) Limited, Broad Market Trading 116 (Pty) Limited.

w Ethan Dube (51)

Alternate non-executive director – MSc (Statistics),

executive MBA (Sweden)

Ethan was appointed to the board as an alternate

non-executive director to Evelyn Chimombe-

Munyoro with effect from 2 August 2007. He has

gained significant corporate finance and asset

management experience over the years. He worked

for Southern Asset Managers for three years as

senior analyst and for Standard Chartered and

Merchant Bank for two years in the corporate

finance departments. In 1996 Ethan founded Infinity

Asset Management with three other partners and

in 1998 he started Vunani Capital Holdings (Pty)

Limited, an investment banking company where he

is the current chief executive officer.

Boar

d of

dire

ctor

s

13PSV Annual Report 2010

Front row from left to right: Evelyn Chimombe-Munyoro

Non-executive chairperson, Abie da Silva Chief executive

officer, Gordon Nzalo Independent non-executive director

Back row from left to right: Tony Dreisenstock Financial

director, Acting company secretary, Mitesh Patel Independent

non-executive director, Peter Robinson Executive director

and deputy chairman, Dave Kelly Executive director

Absent: Ethan Dube Alternative non-executive director

14 PSV Annual Report 2010

Fina

ncia

l St

atem

ents

Chairperson’s review

“In spite of difficult market conditions I would like to

commend PSV employees and management for their

commitment to seeing the year through.”

Evelyn Chimombe-Munyoro

Chairperson

14 PSV Annual Report 2010

15PSV Annual Report 2010

Market conditions continued to be challenging for the year

under review, the effects of the global financial crisis which

resulted in the global recession, gave rise to reduced activity in

the mining and industrial sector. This translated into fewer

orders making 2009 an extremely difficult environment to

conduct business. While South Africa initially lagged behind the

recession experienced globally, South Africa was not spared.

The continued recession throughout 2009 resulted in the

closure of many businesses and significant job losses. In short,

2009 proved to be a year most people would like to forget.

In spite of difficult market conditions I would like to commend

PSV employees and management for their commitment to seeing

the year through. PSV employees and management sought to

adapt and adjust to a challenging environment. While turnover for

the year under review decreased by 13,6% to R372,2 million

from R430,9 million, PSV managed to maintain its client base.

The Group’s EBITDA percentage was a satisfactory 9,6% in the

current year compared to 10,1% in the prior year. Normalised

earnings decreased by 6,7% to 8,4 cents per share (“cps”)

compared to 9,0 cps for the previous year underscoring the

difficult economic environment. The Company has improved its

cash flow constraints having implemented strict working capital

procedures at the beginning of the financial year. This has

resulted in efficient repatriation of funds from the Company’s

Zambia operations translating into positive cash flows.

I commend management’s successful turnaround of the

Company’s petrochemical subsidiary Petrologic. Petrologic

secured a number of lucrative new contracts with oil majors

which has improved the Company’s performance. Furthermore,

the Company has received orders in Mozambique and Zimbabwe.

This has extended its footprint beyond South Africa.

The Engineered Linings and Industrial Supplies segment

performed well under the circumstances. While Engineered

Linings adapted to enhance the quantity and sustainability of

earnings, it reduced economic risks by focusing on smaller

projects. Groupline, PSV’s ceramic linings division, posted its

best results in the history of Groupline. The 2011 order book is

equally impressive with orders from Eskom’s power stations and

various orders in Mozambique. Omnirapid continues to produce

exceptional results year on year which is laudable despite tough

economic conditions.

The Pumps, Spares and Valves segment performed well under

the circumstances, and must be commended for reducing its

debtor’s book in respect of its Zambian operations significantly.

The integration of Mather + Platt into the business is well under

way and will enhance earnings in the coming year. The specialised

services division has been certified at 95% nuclear compliant

which is likely to result in additional orders being secured.

Rand Air and Gas, performed well during the year under review

and secured large orders from a blue chip client amongst others

for the manufacture of the largest vertically standing tank in

South Africa for the storage of liquid nitrogen to be deployed in

Richards Bay upon completion.

The key issue in the future will rest on positive resolution of

the crisis in certain countries in the European Union, which is

a significant trading partner of South Africa, will need to be

monitored carefully, to gauge the potential impact of this

industrial and mining sector in South Africa and on the PSV

Group in particular.

Mr James Anderson did not make himself available for re-

election at the AGM. I would like to thank Mr Anderson for his

contribution to PSV over the past couple of years. Mr Mitesh

Patel was appointed chairman of the Audit Committee taking

over from Mr Anderson. The board appointed Mr Gordon Nzalo,

effective on 1 November 2009 who was also appointed

chairman of the Risk Committee.

I would like to thank the employees and management of PSV

for their dedication to PSV.

Lastly I would like to thank my fellow directors for the guidance that

they have provided to management and their outstanding fiduciary

responsibility towards the Company and its shareholders.

Evelyn Chimombe-Munyoro

Chairperson

15PSV Annual Report 2010

16 PSV Annual Report 2010

Fina

ncia

l St

atem

ents

Chief executive officer’s review

“The clear strategy to diversify the group has

enabled us to manage the downturn in an

effective manner.”

Abie da Silva

CEO

16 PSV Annual Report 2010

17PSV Annual Report 2010

IntroductionPSV Holdings has survived what I believe to be the country’s

worst recession since PSV’s inception in 1988. The clear

strategy to diversify the group has enabled us to manage this

downturn in an effective manner. The diverse product offering

and customer base has allowed PSV to continue trading and

offering products and services across many sectors of industry

in Southern Africa, where we continue to supply products and

services to the power generation, water, petrochemical and

cryogenic industry as well as a wide range of products to the

mining sector. During the year under review we supplied our

customers located all over Africa as far north as Egypt, but with

a predominant focus on Sub-Saharan Africa.

Financial overviewThe first six months of the year presented tough trading

conditions which deteriorated further in the second half, we

experienced a slowdown in the number of tenders in the

market-place as well as projects awarded. This led to greater

competition in the market and the resultant margin erosion in a

number of our subsidiaries.

Consequently turnover for the year decreased by 13,6% to

R372,2 million (2009: R430,9 million) although the gross

profit margin increased to 24,2% (2009: 22,7%). Not-

withstanding a R2,4 million share based payment expense

being incurred in the current year together with inflationary

adjusted salary increases for staff, the Group’s operational

expenditure, excluding impairment of goodwill and intangible

assets decreased compared to the prior year. The group’s

EBITDA percentage was a satisfactory 9,6% in the current

year compared to 10,1% in the prior year despite the harsh

economic climate.

Meaningful comparison to the prior year’s profit after tax should

be on a normalised earnings basis. Normalised earnings

eliminate the effects of impairment of goodwill and intangible

assets, amortisation of intangible assets, straight-lining of

leases, expensing imputed interest on deferred purchase

considerations and share-based payment expenses. In this

respect, normalised earnings decreased by 6,7% to 8,4 cents

per share (“cps”) (2009: 9,0 cps).

In my report last year I stated that “every endeavour will be

made to strengthen the cash flow” and I am pleased to report

that at the start of this financial year, strict working capital

procedures were implemented and during the first half of the

year the Group’s operating cash flows had turned positive, a

trend we are pleased to report has continued.

Cash flow from operations of R25 million (2009: R2,6 million

outflow) was generated. The Group’s cash flow cycle

reduced from 82 to 76 days primarily attributable to effective

working capital management procedures implemented. The

Group finished the year with a net overdraft of R12,1 million,

mainly as a result of payments made to vendors of

companies acquired and the repayment of external loans.

Based upon a comprehensive evaluation of the Group’s cash

flows, the board is satisfied that there are adequate working

capital facilities available to fund the current level of

business operations. Notwithstanding this, the Group has a

short-term commitment to fund amounts due and payable to

vendors of businesses acquired and other short-term loans.

The vendor payments due will be funded by a combination

of extended vendor financing and medium-term loans. The

short-term loans will be comfortably serviced out of operational

cash flows.

The Group’s debt:equity ratio was 31,6% compared to 26,3%

in the prior year, well within the Group’s debt:equity ratio limit

of 40%. The current ratio increased to 1,55:1 from 1,50:1 in

the prior year, mainly attributable to a reduction in the

inventory and trade payable balance.

The Group’s HEPS reduced by 25% to 5,2 cps (2009: 6,9 cps).

The decline is as a result of the tough trading conditions

experienced during the year. The Group’s balance sheet

continued to strengthen as the net tangible asset value per

share increased by 17,6% to 39,4 cps (2009: 33,5 cps).

A detailed assessment of the carrying value of the Group’s

goodwill was undertaken at year-end. In terms of this

assessment, the goodwill attributable to the Group’s various

cash generating units was not in line with the values

reflected in the balance sheet. In terms of the assessment

and taking into account the world economic crisis, it was

decided to impair goodwill and intangible assets arising on

the acquisition of the Group’s various businesses by an

amount of R98,5 million. It should be noted that the cost of

running the Group’s head office has not been apportioned to

17PSV Annual Report 2010

18 PSV Annual Report 2010

CEO

revi

ew

the cash generating units in assessing the carrying value

of goodwill.

Corporate actionsDuring the year PSV concluded two acquisitions, one to

bolster pumps segment and the other to add strength to our

cryogenics capabilities.

At the start of the financial year, PSV bought Mather + Platt,

established in 1950 and a leading name in the pump

manufacturing industry in South Africa. The product range

enhanced and complemented that of PSV and opened access

to markets such as Angola, Malawi, Mozambique, Namibia

and Zambia. Although PSV is active in the latter, the range of

pumps we were able to supply increased. The total cash

purchase consideration was R10 million.

PSV strengthened its cryogenics capability through the purchase

of Cryoshield with effect from 1 March 2010, a manufacturer of

cryogenic process control equipment. Since its establishment in

1987, Cryoshield has been manufacturing large capacity,

new generation cryogenic freezing equipment, a process that

required specialised fabricating techniques in stainless steel

processes, which are used in the freezing of food products. The

total purchase consideration will be R8 million.

We are delighted with the acquisition, which together with our

subsidiary Rand Air and Gas Installations, added critical mass,

advanced technologies and new clients to the specialised

services segment of the PSV Group.

Operational reviewWe have, in most cases, maintained our existing infrastructure

and have replaced staff who have resigned allowing the PSV

Group to be prepared when economic conditions change.

During the year we completed various large projects and all our

operating units were profitable except for one, Mather + Platt.

Mather + Platt was put under pressure during the year specifically

because of the R9 million two year loan for the acquisition from

Hudaco and an overdraft inherited from Dasher.

Pumps, spares and valves

Our pump subsidiaries performed below expectation due to

low demand from customers largely as a result of reduced

infrastructure spend by government at both local and regional

level. Despite this, the turnover for the three companies

was R112,1 million, 9,66% higher than the previous year

(2009: R102,2 million). The increase in the revenue line was

largely due to the inclusion of a full year of trading from

Mather + Platt. This segment contributes 30% to the overall

revenue of PSV and achieved a profit before tax of R4,7 million

(2009: R5,1 million). Gross margins were squeezed by 20%

resulting in an almost 40% reduction in contributing margins

compared with the previous period. Margin pressure was

primarily due to a reduction in high margin business with

Zambian copper mines and the increase in low margin project

business in Zambia and Malawi.

We experienced a slowdown in overall demand in Zambia

where the mining sector has transcended into a phase of

delayed maintenance on the back of weaker copper prices.

Mather + Platt continue to build on their marketing campaign

which has to date successfully reintroduced this prestigious

name into the market place.

Selected projects undertaken during the year include:

• The rehabilitation of pumps, pump stations and valves for

Lusaka Water

• A project for a Zambian mine for axial flow pumps for

concentrators (pumping mine slurry)

• Supplying a number of pumps to a large steel producer in

South Africa for the rehabilitation of a pumping plant for the

descaling of steel.

Engineering linings and industrial supplies

This segment contributed R134,9 million of revenue, 36%

of the total, which was lower than the previous year (2009:

R191 million). Profit before tax was R6,9 million (2009:

R17,5 million), despite this, the gross profit margin increased

by 31%, attributable to Engineered Linings completing many

smaller but more profitable contracts compared to the

prior year.

Groupline had its best year ever with large orders from various

Eskom power stations around the country and large export

orders to Ivory Coast, Zambia, and Mozambique. At the moment

Groupline has a full order book for 2011.

Omnirapid, likewise, had a good year; despite a slight decline in

turnover it still achieved good profits. It has been able to better

Chief executive officer’s review continued

19PSV Annual Report 2010

harness the Group’s buying power to secure better pricing and

discounts from suppliers.

Selected projects undertaken during the year include:

• Landfill lining projects included those at Empangeni and the

Coastal Park Landfill in the Western Cape

• In the mining sector projects included work at Impala

Platinum, Leeuwpan mine and Trekkopje Uranium mine to

name a few

• Linings projects were carried out for Eskom’s Camden and

Hendrina power stations

• Various linings projects have been undertaken for the coal

division of Anglo American as well as for Sasol.

Specialised services

The specialised services segment contributed 34% to the

overall turnover of PSV. Revenue suffered a 9% reduction in

turnover to R125,1 million (2009: R137,1 million), largely as a

result of Rand Air and Gas Installations (“RAGI”) having to cut

margins in order to remain competitive and retain market

share. In the face of these tactics, RAGI received their first

large order from Afrox to supply 10 off-force draft 50 bar, 9

metre high vaporizers for liquid nitrogen and liquid oxygen use.

It has concluded a large contract for Richards Bay, details of

which are contained below.

With the completion of the Cryoshield acquisition, PSV is

now well placed to become the largest supplier of cryogenic

expertise, product knowledge and bespoke manufacturing to

South Africa and Africa. The inclusion of the Cryoshield

business also ensures succession planning for this discipline

going forward.

We are pleased to report that after restructuring Petrologic, the

company has turned the corner and has become profitable. For

the first time in three years Petrologic has diversified its client

base from predominantly Engen to also include Shell, Sasol,

Chevron and Petrotec in Mozambique.

Selected projects undertaken during the year include:

• Continued to supply equipment to the petrochemical sector

throughout South Africa

• Island View Storage (“IVS”), a Bidvest subsidiary, owns and

operates chemical storage facilities in Durban, Richards Bay

and Cape Town Harbours as well as Isando. These facilities

are used for the storage of various liquid chemicals, fuel and

oils either being imported or exported. Certain chemicals

require nitrogen blankets for storage to ensure their integrity

and for safety reasons. Furby Gas manages all nitrogen

supply and distribution for IVS facilities countrywide. In order

to support the continued growth of IVS, RAGI has manufactured

a new 235 ton nitrogen storage tank to support the shipping

activities in Richards Bay. This will assist IVS in meeting the

growing demand of both chemical exports and imports.

OutlookIn conclusion, all our companies are well placed to benefit from

the upturn in the economy. When this occurs we will have

maintained our entire existing infrastructure and be able to

react quickly to the renewed placement of orders and projects.

We intend to secure larger premises for Rand Air and Gas

Installations and Cryoshield and depending on the total size

secured, could also house some of our other companies. This

will ensure sufficient capacity for the cryogenics business to

not have to turn away work and benefits from shared joint

services and facilities can be extracted.

Despite this the management of PSV is expecting the operating

environment to remain difficult for the coming six months, we

have experienced a good start to the year with many prospects

turning in orders and have begun the new financial year with

a positive order book of R110 million and further prospects

of R120 million.

AppreciationThe past year has been tough but our staff has shown

tenacity and for your support and loyalty I wish to thank you.

To the shareholders who have supported and remained

committed to PSV, I sincerely thank you for the interest you

have shown towards PSV. I am grateful to my fellow directors

and board members for your guidance and motivation during

the year. Lastly to senior management and staff, thank

you for your persistence on project tenders and orders,

without these PSV would not be able to strengthen our base

through diversification.

Abie JD da SilvaChief executive officer

20 PSV Annual Report 2010

Corp

orat

e so

cial

in

vest

men

t

PSV continues to support skills shortages across economic

sectors and remains committed to socio-economic development.

PSV has in place a graduate programme aptly named “investing

in tomorrow’s leaders”. During 2009 the budgeted costs for

the programme was R278 199 and in 2010 the total budgeted

cost is R199 372.

The initiative is focusing on the advancement of talented and

dedicated designated groups. The process has been underpinned

by the commitment of the management team, with progress

being measured against stated quantitative targets.

In our 2009 annual report we reported that Victor Makwala,

Thabo Mohlahlo and Derrick Sithole had been adopted

through subsidiary companies of PSV to undertake studies.

We are pleased to announce that each of the candidates have

passed and are now undertaking their second year of study at

the University of Johannesburg, the Vaal University and RAU

Technology Institute respectively.

To the candidates mentioned above, we have added an

additional three people, namely:

• Gerald Mahlangu, studying National Diploma in Information

Technology and has been financed by our subsidiary Petro-

Logic

• Nhlanhla Dhlamini, studying National Diploma in Information

Technology and has been financed by our subsidiary APE

Pumps

• Tulisiwe Madola, studying National Diploma in Human

Resources Management has been financed by our subsidiary

Groupline Projects.

Within the PSV Group of companies, apprenticeships are also a

vital component of our corporate social investment as benefit to

all parts of the business are immediate. We are pleased to

report that our apprentice turner, boilermaker and two fitters

are well established in the group.

The group has embarked on continuous skills improvement, to

enhance employee’s career growth.

• Mothepana Mankga, skills Development and Employment

Equity. Mothepana was employed as an Office Assistant and

appointed as an HR Assistant in 2009.

PSV’s Ubuntu Project

Once gain during the year, we have touched the lives and hearts

of those less fortunate than ourselves, by being involved in the

local community and charity organisations.

The PSV Ubuntu Project consists of three projects namely:

Oliver’s House – This project involved a Christmas party for

180 children and PSV sponsored a Christmas party bucket,

consisting of a soccer ball, soft toy and a T-shirt for each child.

PSV gave 50 children entering Grade I a complete school bag

and stationery kit.

In an initiative to collect clothes, linen and non-perishable

items, we distributed empty boxes to all subsidiaries for

collection. We received an overwhelming response, 64 black

bags were collected, filled with clothes, linen, blankets and

much more. These donations were distributed to the Oliver’s

House Care Centre in Benoni and the Compass Centre for

abused women and children in Edenvale as well as the

Nomthandazo Care Centre in Daveyton.

Compass-PSV sponsored Christmas party buckets for 29

children from the Compass Community Provision and Social

Services in Edenvale, an organisation which cares for abused

and neglected women and children. We also bought and installed

a play gym at the Compass Centre and sponsored six months

worth of Purity foods, nappies and other baby accessories.

In addition, the centre was in desperate need of beds and

linen for the women and children. PSV sponsored 20 bunk

beds, mattresses and complete sets of linen as well as 10

double door wardrobes in which to store clothing for those at

the centre.

Text books for high school pupils – PSV donated 120 text

books to high school children in the Daveyton township with

text books for Grade 11 and 12 in the subjects of Math

and Science.

Corporate social investment

21PSV Annual Report 2010

Introduction

PSV is listed on the Altx board of the JSE Limited (“JSE”). The

board of directors (“the board”) is committed to and subscribes

to the values of good corporate governance contained in the King

Code of Governance Principles for South Africa, 2009 (“King III”),

as well as the related Listings Requirements of the JSE.

The board welcomes the introduction of King III and the PSV

Group is measuring itself against these principles. Existing

governance practices are being reviewed to ensure responsible

qualitative or alternative compliance that is in the Group’s

best interests. PSV endorses the principles of integrity and

accountability advocated by King III. The Group’s corporate

governance structures and practices are reviewed on an ongoing

basis in response to changes within and external to the Group.

This corporate governance statement sets out the key

governance principles and practices of PSV to fairly and

honestly inform their internal and external stakeholders through

fair and understandable disclosure.

Endorsement of King III

PSV remains fully committed to the principles of effective

corporate governance and application of the highest ethical

standards in the conduct of its business. We endorse the

principles of integrity and accountability advocated by King III.

In all dealings we strive to ensure that the interests of

stakeholders are foremost in our decisions and that they are

fully informed of the process.

We have long recognised that good corporate governance is

essentially about leadership and there exists the need to conduct the

enterprise with integrity and in compliance with best practices.

Statement of complianceThe Listings Requirements of the JSE require that listed

companies report on the extent to which they comply with

the principles incorporated in the King Report on Corporate

Governance (“King II”).

Based on the information set out in this corporate governance

statement, the board confirms that the company has complied

with the principles of the “King II” on an ongoing basis during

the accounting period under review, unless otherwise indicated

below, and has also complied with the provisions set out in

the Listings Requirements of the JSE.

King III became effective on 1 March 2010 after the year-end of

the company. As indicated above, the company is in the process

of evaluating its current governance performance against the

recommendations contained in King III and will be reporting to

stakeholders on such performance following the current

financial year.

Board of directorsChairperson

The chairperson, Evelyn Chimombe-Munyoro, is a non-executive

director. The board delegates to the chairperson the responsibility

for ensuring the effectiveness of governance practices. The

chairperson leads the board and is responsible for representing

the Company to stakeholders.

As recommended by King III the role of the chairperson is separate from that of the chief executive officer.

Chief executive officer

Chief executive officer (“CEO”), Abie da Silva, is responsible for the day-to-day business of the Group, for the implementation of policies and strategies adopted by the board, and takes full responsibility for all operations. Managing directors of the various businesses assist him in this task. Board authority conferred on management is delegated through the CEO, in accordance with approved authority levels. Abie da Silva is tasked with addressing all communication matters with institutional shareholders, analysts and the media.

Board

PSV is headed by an effective unitary board that can lead and control the group. The board comprises eight directors of whom two are independent non-executive directors, one non-executive director and an alternate non-executive director. The board recognises that this is not in compliance with King III and is seeking to appoint an additional independent non-executive director. The board considers Mr Mitesh Patel and Mr Gordon Nzalo as independent non-executive directors. The independent directors ensure that no one individual has unfettered powers of decision-making and authority, so that all shareholders’ interests are protected. The non-executive directors have no fixed term of office.

The Board has established policy for appointments to the board and normal nominations for the appointment of new directors

are submitted for consideration and the appointment is a matter

dealt with by the board as a whole.

Corporate governance

22 PSV Annual Report 2010

Corp

orat

e go

vern

ance

The guidelines contained in the Listings Requirements of the

JSE were used to test the independence of and category most

applicable to each director. The directors ensure that the

chairperson encourages proper deliberation of all matters

requiring the board’s attention.

The primary responsibilities of the board include the regular

review of the strategic direction of investment decisions and

performance against approved plans, budgets and best practice

standards. The board retains full and effective control of the

Group and decisions on material matters are reserved for the

board. A board charter is in place which, inter alia, addresses

the functions and responsibilities of the board and which

is reviewed on an annual basis. The board charter will be

specifically reviewed during the current financial year to align

the content thereof with the recommendations of King III.

The board meets at least quarterly, and more frequently if

circumstances or decisions require.

Meetings are conducted in accordance with formal agendas,

ensuring that all substantive matters are properly addressed.

Any director may request that additional matters be added

to the agenda. Copies of board papers are circulated to the

directors in advance of the meetings.

There is a clear division between the responsibilities of the

board and management.

All directors have the requisite knowledge and experience

required to properly execute their duties, and all participate

actively in the proceedings at board meetings. Non-executive

directors contribute an unfettered and independent view on

matters considered by the board and enjoy significant influence

in deliberations at meetings.

One-third of the directors are subject, by rotation, to retirement

and re-election at the annual general meeting in terms of the

Company’s articles of association.

The details for each of the directors are set out on page 12 of

the annual report.

Attendance by directors at board meetings is provided below:

6 Mar 18 May 22 Jul 17 Nov

Director 2009 2009 2009 2009

JH Anderson* Yes Yes Yes N/A

CE Chimombe-Munyoro Yes Yes Yes Yes

AJD da Silva Yes Yes Yes Yes

AR Dreisenstock Yes Yes Yes Yes

DJ Kelly Yes Yes Yes Yes

GS Nzalo¤ N/A N/A N/A Yes

P Robinson Yes Yes Yes Yes

GJ Shongwe• Yes N/A N/A N/A • Resigned ¤ Appointed * Removed

A representative from the Company’s Designated Adviser

attended the board meetings as required in terms of the JSE

Listings Requirements.

Changes to the board

Mr James Anderson was not re-elected as an independent non-

executive director at the company’s annual general meeting

and stepped down as chairman of the Audit Committee on

28 August 2009. Mr Mitesh Patel was appointed chairman of

the Audit Committee on 28 August 2009.

Mr Gordon Nzalo was appointed as an independent non-

executive director, chairman of the Risk Committee and member

of the Audit Committee with effect from 1 November 2009.

Mr Vusi Shongwe resigned as an independent non-executive

director of the company on 13 July 2009.

Board committeesWhile the board remains accountable and responsible for

the performance and affairs of the Company, it delegates to

management and board committees certain functions to assist

it to properly discharge its duties. The chairman of each board

committee reports at each scheduled meeting of the board and

minutes of committee meetings are provided to the board.

The members of the Audit Committee are independent, non-

executive directors. The Risk Committee is chaired by an

independent non-executive director, but also comprises senior

management in the group who have the relevant knowledge

and experience.

Both the directors and the members of the board committees

are supplied with full and timely information that enable them

to properly discharge their responsibilities. All directors have

unrestricted access to all group information.

Corporate governance continued

23PSV Annual Report 2010

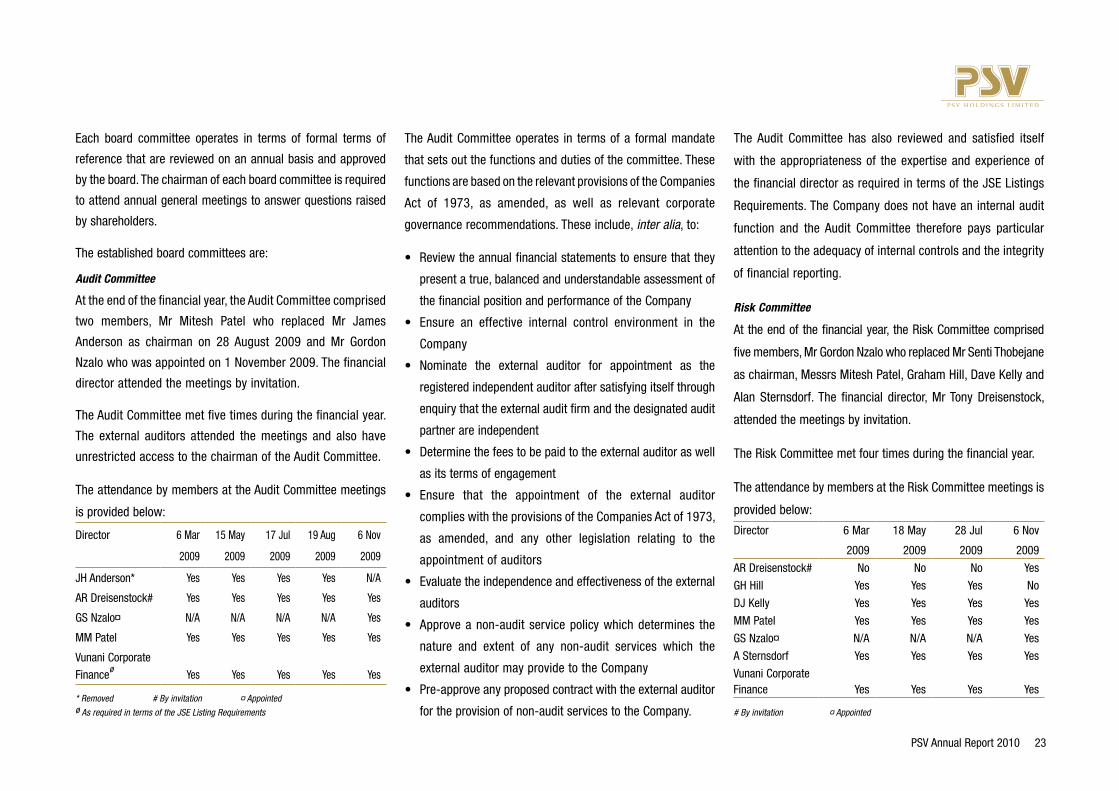

Each board committee operates in terms of formal terms of

reference that are reviewed on an annual basis and approved

by the board. The chairman of each board committee is required

to attend annual general meetings to answer questions raised

by shareholders.

The established board committees are:

Audit Committee

At the end of the financial year, the Audit Committee comprised

two members, Mr Mitesh Patel who replaced Mr James

Anderson as chairman on 28 August 2009 and Mr Gordon

Nzalo who was appointed on 1 November 2009. The financial

director attended the meetings by invitation.

The Audit Committee met five times during the financial year.

The external auditors attended the meetings and also have

unrestricted access to the chairman of the Audit Committee.

The attendance by members at the Audit Committee meetings

is provided below:

Director 6 Mar

2009

15 May

2009

17 Jul

2009

19 Aug

2009

6 Nov

2009

JH Anderson* Yes Yes Yes Yes N/A

AR Dreisenstock# Yes Yes Yes Yes Yes

GS Nzalo¤ N/A N/A N/A N/A Yes

MM Patel Yes Yes Yes Yes Yes

Vunani Corporate

Financeø Yes Yes Yes Yes Yes

* Removed # By invitation ¤ Appointed ø As required in terms of the JSE Listing Requirements

The Audit Committee operates in terms of a formal mandate

that sets out the functions and duties of the committee. These

functions are based on the relevant provisions of the Companies

Act of 1973, as amended, as well as relevant corporate

governance recommendations. These include, inter alia, to:

• Review the annual financial statements to ensure that they

present a true, balanced and understandable assessment of

the financial position and performance of the Company

• Ensure an effective internal control environment in the

Company

• Nominate the external auditor for appointment as the

registered independent auditor after satisfying itself through

enquiry that the external audit firm and the designated audit

partner are independent

• Determine the fees to be paid to the external auditor as well

as its terms of engagement

• Ensure that the appointment of the external auditor

complies with the provisions of the Companies Act of 1973,

as amended, and any other legislation relating to the

appointment of auditors

• Evaluate the independence and effectiveness of the external

auditors

• Approve a non-audit service policy which determines the

nature and extent of any non-audit services which the

external auditor may provide to the Company

• Pre-approve any proposed contract with the external auditor

for the provision of non-audit services to the Company.

The Audit Committee has also reviewed and satisfied itself

with the appropriateness of the expertise and experience of

the financial director as required in terms of the JSE Listings

Requirements. The Company does not have an internal audit

function and the Audit Committee therefore pays particular

attention to the adequacy of internal controls and the integrity

of financial reporting.

Risk Committee

At the end of the financial year, the Risk Committee comprised

five members, Mr Gordon Nzalo who replaced Mr Senti Thobejane

as chairman, Messrs Mitesh Patel, Graham Hill, Dave Kelly and

Alan Sternsdorf. The financial director, Mr Tony Dreisenstock,

attended the meetings by invitation.

The Risk Committee met four times during the financial year.

The attendance by members at the Risk Committee meetings is

provided below:

Director 6 Mar

2009

18 May

2009

28 Jul

2009

6 Nov

2009

AR Dreisenstock# No No No Yes

GH Hill Yes Yes Yes No

DJ Kelly Yes Yes Yes Yes

MM Patel Yes Yes Yes Yes

GS Nzalo¤ N/A N/A N/A Yes

A Sternsdorf Yes Yes Yes Yes

Vunani Corporate Finance Yes Yes Yes Yes

# By invitation ¤ Appointed

24 PSV Annual Report 2010

The Group acknowledges the importance of risk management

and corporate governance principles. Risk is an intrinsic part of

all activities undertaken by PSV. The organisation is exposed to

certain peculiar risks, which are influenced by its specific

choices and actions. The board of PSV along with its executive

and management recognises that risk management is a critical

management tool to ensure that the Group achieves its

objectives. The Risk Committee has been formulated with the

specific objective of identifying those risks and implementing

policies to combat and mitigate those risks.

Risk management matrix

Description of risk Mitigation strategies

Strategic

Succession

planning

• Focus on the recruitment of young talent and

nurturing them for the future

• Apprenticeship programme in place

• Extensive training programmes

B-BBEE • Identification of new viable strategic partners

• Re-aligning procurement policies to acquire from

level 4 and higher rated companies

• Identification of previously disadvantaged

individuals working within the company and

promoting them accordingly

Financial

Debtors

collections

• Strict credit vetting and granting of credit limits to

customers

• Accountability KPAs implemented with senior

management of subsidiaries

• Advanced payments wherever possible

Description of risk Mitigation strategies

Foreign currency

exposure

• Covering exposure with a combination of forward

exchange contracts or currency futures

Loan covenants • Monitoring and policing cash flows through

group treasury

• Implementation of working capital management

targets with senior management of subsidiaries

Operational

Over trading • Tight controls for declining prospective contracts

if requisite funding is not available

Quality assurance • Appointment of group health and safety officer

and subordinate health and safety officers at

subsidiary level

• Regular meetings and follow up to ensure

compliance with all regulatory covenants

Human resources

Change

management

• The Risk Committee will develop a formal policy

in this regard

Standardisation

of employment

contracts

• Dedicated HR function to, in the long term,

standardise all employment contracts

Legal

Proper

authorisation

of material

contracts

• Implemented limits of authority in place at

subsidiary level

• Will be enforcing the approval of material

contracts through soon to be appointed legal

officer for the group

Remuneration Committee

In terms of the JSE Listings Requirements it is not a

requirement for Altx companies to constitute a Remuneration

Committee. Although a recommendation of King II, the board

is comfortable that remuneration matters are appropriately

dealt with at board level.

Health and safety policyPSV has begun implementing OHSAS 18001 to ensure a high

standard of health and safety within the Group and its

subsidiaries. The implementation of the policy demonstrates

the continuous commitment to providing all our employees with

a safe and satisfying working environment, and to assist in the

drive towards zero work-related injuries and accidents.

Within each subsidiary, there are appointed health and safety

representatives who assist with the implementation of the

health and safety systems. Bi-monthly meetings are held in

order to ensure the effectiveness of the system.

Social responsibility PSV is a committed, socially responsible organisation with a

dedicated corporate social investment programme in place,

supported by various initiatives. The Group continues to support

skills shortages across economic sectors and in an endeavour

to fill shortages the Group itself experiences, it has put in place

an apprenticeship programme.

A graduate programme, “investing in tomorrow’s leaders”, is

also in place, which focuses on the advancement of talent. The

programme is underpinned by PSV assisting identified students

with the advancement of their university degrees.

Corporate governance continued

Corp

orat

e go

vern

ance

25PSV Annual Report 2010

The Group embarks on continuous skills improvement, to

enhance an employee’s career growth.

On a social level PSV participates in various projects for

Oliver’s House, Compass and an initiative to distribute school

text books.

For further information on our corporate social investment

and social responsibility projects refer to page 20 in this

annual report.

Company secretary

The appointment and removal of the company secretary is

approved by the board. The company secretary advises

the board on the appropriate procedures for the management

of meetings and the implementation of governance

procedures, and is further responsible for providing the board

collectively, and each director individually, with guidance

on the discharge of their responsibilities in terms of

the legislation and regulatory requirements applicable to

South Africa.

The board has unlimited access to the company secretary, who

advises the board and its committees on issues including

compliance with group policies and procedures, statutory

regulations and relevant governance principles and

recommendations.

Megan Saayman was appointed as company secretary with

effect from 13 July 2009. On 29 June 2010 it was announced

that Mrs Saayman had resigned as the company secretary and

PSV will, in due course, make a further announcement on

SENS detailing a new appointment. As an interim measure

Tony Dreisenstock, financial director will fulfill the role of

acting company secretary.

Interest in contracts

During the year ended 28 February 2010 none of the directors

had a significant interest in any contract or arrangement

entered into by the company or its subsidiaries, other than as

disclosed in note 24 to the annual financial statements.

Directors are required to inform the board timeously of conflicts

or potential conflicts of interest they may have in relation to

particular items of business. Directors are obliged to recuse

themselves from discussions or decisions on matters in which

they have a conflicting interest.

Relations with shareholders

The Group maintains dialogue with its key financial audiences,

especially institutional shareholders and analysts. The investor

relations team manages the dialogue with these audiences and

presentations take place at the time of publishing interim and

final results.

The Group adopts a proactive stance in timely dissemination

of appropriate information to stakeholders through print and

electronic news releases and the statutory publication of the

Group’s financial performance.

The Group’s website provides the latest and historical financial

and other information, including the financial reports.

The board encourages shareholders to attend its annual general

meeting, notice of which is contained in this annual report,

where shareholders will have the opportunity to put questions

to the board, including the chairmen of the board committees.

Directors’ share dealings

The board has an approved trading policy in terms of which

dealing in the Group’s shares by directors and employees is

prohibited during closed periods.

Directors may not deal in the Company’s shares without first

advising and obtaining clearance from the CEO and the

financial director. The CEO and financial director may not deal

in the Company’s shares without first advising and obtaining

clearance from the chairman of the board. No director or

executive may trade in PSV shares during closed periods as

defined in the JSE Listings Requirements. The directors of the

Company keep the company secretary advised of all their

dealings in securities.

26 PSV Annual Report 2010

Corporate governance continued

Fraud and illegal acts

The Group does not engage in or accept any illegal acts in the

conduct of its business. The directors’ policy is to actively

pursue and prosecute the perpetrators of fraudulent or other

illegal activities, should they become aware of any such acts.

Insider trading

No employee may deal, directly or indirectly, in PSV shares on

the basis of unpublished price-sensitive information regarding

the business or affairs of the Group.

Code of conduct

The Group is committed to the highest ethical standards of

business conduct and to complying fully with all applicable

laws and regulations.

The directors, employees, employees of outsourced functions

as well as suppliers to PSV, are all expected to comply with the

principles and act in terms of the code of conduct. The directors

believe that the ethical standards of the Group, as stipulated in

the code of conduct, are monitored and are being met. Where

there is non-compliance with the code of conduct, the

appropriate discipline is enforced with consistency as the Group

responds to offences and prevents recurrences.

Going concern

The annual financial statements contained in this annual report

have been prepared on the going concern basis. The directors

report that, after making enquiries, they have a reasonable

expectation that the Group has adequate resources to continue

in operational existence for the foreseeable future. For this

reason, the Group continues to adopt the going concern basis

in preparing the annual financial statements.

Corp

orat

e go

vern

ance

28 PSV Annual Report 2010

Fina

ncia

l St

atem

ents

Annual financial statements

ContentsReport of the independent auditors ....................................................................................... 29

Audit Committee report ......................................................................................................... 30

Directors’ responsibility and approval ................................................................................... 31

Certification by company secretary ....................................................................................... 31

Directors’ report ................................................................................................................... 32

Consolidated statement of comprehensive income ............................................................... 34

Consolidated statement of financial position ......................................................................... 35

Statements of changes in equity ........................................................................................... 36

Consolidated statement of cash flows .................................................................................. 38

Accounting policies ............................................................................................................... 39

Notes to the annual financial statements .............................................................................. 44

29PSV Annual Report 2010

Report of the independent auditors

To the members of PSV Holdings Limited

Independent auditor’s reportWe have audited the Group’s annual financial statements and the annual financial statements of PSV Holdings Limited, which comprise the statements of financial position at 28 February 2010, and the statements of comprehensive income, the statements of changes in equity and statements of cash flows for the year then ended, and the notes to the financial statements, which include a summary of significant accounting policies and other explanatory notes, and the directors’ report as set out on pages 32 to 75.

Directors’ responsibility for the financial statementsThe Company’s directors are responsible for the preparation and fair presentation of these financial statements in accordance with International Financial Reporting Standards and in the manner required by the Companies Act of South Africa. This responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibilityOur responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, these financial statements present fairly, in all material respects, the consolidated and separate financial position of PSV Holdings Limited at 28 February 2010, and its consolidated and separate financial performance and consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards, and in the manner required by the Companies Act of South Africa.

KPMG Inc.

Per TG CheadleChartered Accountant (SA) 85 Empire RoadRegistered Auditor Parktown, South AfricaDirector 20 July 2010

30 PSV Annual Report 2010

Fina

ncia

l St

atem

ents

Audit Committee report

BACKGROunDThe committee is pleased to present our report for the financial year ended 28 February 2010 as recommended by the King II report on Corporate Governance and in line with the South African Companies Act, 61 of 1973 (as amended) (the Act).

OBjeCtIve AnD sCOPeThe overall objectives of the committee are as follows:• To review the principles, policies and practices adopted in

the preparation of the accounts of Companies in the Group and to ensure that the annual financial statements of the Group and any other formal announcements relating to the financial performance comply with all statutory, regulatory and PSV requirements as may be required.

• To ensure that the consolidated financial statements of the group comply with all statutory, regulatory and PSV requirements and similarly, that the financial information contained in any consolidated submissions to PSV is suitable for inclusion in its consolidated financial statements.

• To annually assess the appointment of the auditors and their independence, recommend their appointment and approve their fees.

• To review the work of the group’s external and internal auditors to ensure the adequacy and effectiveness of the Group’s financial, operating compliance and risk management controls.

• To review the management of risk and the monitoring of compliance effectiveness within the Group.

• To perform duties that are attributed to it by the Act, the JSE and King II.

The committee performed the following activities:• Received and reviewed reports from external auditors

concerning the effectiveness of the internal control environment, systems and processes.

• Reviewed the reports of external auditors detailing their concerns arising out of their audits and requested appropriate responses from management resulting in their concerns being addressed.

• Made appropriate recommendations to the board of directors regarding the corrective actions to be taken as a consequence of audit findings.

• Considered the independence and objectivity of the external auditors and ensured that the scope of their additional services provided was not such that they could be seen to have impaired their independence.

• Reviewed and recommended for adoption by the board such financial information that is publicly disclosed which for the year included:

– the audited results for the year ended 28 February 2010 – the interim results for the six months ended 31 August 2009.

The Audit Committee is of the opinion that the objectives of the committee were met during the year under review.

Where weaknesses in specific controls had been identified, management undertook to implement appropriate corrective actions to mitigate the weakness identified.

MeMBeRshIPDuring the course of the year, the membership of the committee comprised solely independent non-executive directors. They are Mitesh Patel (Chairman) and Gordon Nzalo

exteRnAl AuDItThe committee has satisfied itself through enquiry that the auditor of PSV is independent as defined by the Act.

The committee, in consultation with executive management,

agreed to an audit fee for the 2010 financial year. The fee is

considered appropriate for the work that could reasonably have

been foreseen at that time.

There is a formal procedure that governs the process whereby

the external auditor is considered for the provision of non-audit

services, and each engagement letter for such work is reviewed

in accordance with set policy and procedure.

Meetings were held with the auditor where management was

not present, and no matters of concern were raised.

The committee has reviewed the performance of the external

auditors and nominated, for approval at the annual general

meeting, KPMG as the external auditor for the 2011 financial year.

AnnuAl fInAnCIAl stAteMentsThe Audit Committee has evaluated the consolidated annual

financial statements for the year ended 28 February 2010 and

considers that it complies, in all material aspects, with the

requirements of the Act and International Financial Reporting

Standards. The committee has therefore recommended the

annual financial statements for approval to the board. The

board has subsequently approved the financial statements

which will be open for discussion at the forthcoming annual

general meeting.

Mitesh PatelAudit Committee chairman20 July 2010

31PSV Annual Report 2010

Directors’ responsibility and approval

The directors are responsible for the preparation and fair presentation of the Group annual financial statements and the annual financial statements, comprising the statement of financial position as at 28 February 2010 and the statement of comprehensive income, the statement of changes in equity and the statement of cash flows for the year then ended, and the notes to the financial statements, which include a summary of significant accounting policies and other explanatory notes in accordance with International Financial Reporting Standards and in the manner required by the Companies Act of South Africa.

The directors’ responsibility includes: designing, implementing and maintaining internal control relevant to the preparation and the fair presentation of these financial statements that are free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

The directors’ responsibility also includes maintaining adequate accounting records and an effective system of risk management.

The directors have made an assessment of the Group and Company’s ability to continue as a going concern and have no reason to believe the businesses will not be going concerns in the year ahead.

The auditor is responsible for reporting on whether the Group annual financial statements and the annual financial statements are fairly presented in accordance with the applicable financial reporting framework.

AjD da silva AR DreisenstockChief Executive Officer Chief Financial Officer

Certification by company secretary

In terms of section 268(G) of the Companies Act, 61 of 1973, as amended (“the Act”), I certify that, to the best of my knowledge and belief, the Group has, in respect of the financial year reported upon, lodged with CIPRO all returns required of a public company in terms of the Act and that all such returns are true, correct and up to date.

AR DreisenstockActing company secretary

32 PSV Annual Report 2010

Fina

ncia

l St

atem

ents

Directors’ report

The directors have pleasure in submitting their report together with the Company and Group annual financial statements for the financial year ended 28 February 2010.

nAtuRe Of BusInessPSV is a specialised industrial engineering group focused on the provision of pumps, valves, engineering linings, industrial supplies and fuel pumps and dispensers and cryogenics to the mining, petrochemical, water and waste water management sectors in South Africa and Africa.

fInAnCIAl stAteMentsThe Company and Group’s results and financial position are contained in the annual financial statements on pages 34 to 75 of the report.

The audited annual financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and their interpretation adopted by the International Accounting Standards Board (“IASB”), the Listings Requirements of the JSE Limited (“JSE”) and the Companies Act, 61 of 1973, as amended (“the Act”) and remain consistent with those applied to the abridged results announced on 24 May 2010.

Results Of OPeRAtIOnsThe Company and Group’s statement of comprehensive income and segmental analysis for the period set out the results of the operations.

DIvIDenDsNo dividends were paid nor recommended to shareholders during the financial year ended 28 February 2010 (2009: nil).

PROPeRtY, PlAnt AnD eQuIPMentDuring the year the Group invested R10 944 756 in new property, plant and equipment in order to expand its operations. Details of property, plant and equipment are contained in note 7 of the annual financial statements.

BORROWInG POWeRsIn terms of the Company’s articles of association, its borrowing powers are unlimited. The borrowing powers of the Group’s wholly owned operating subsidiaries may in terms of its articles of association be limited by the Company.

lItIGAtIOnThere are no legal or arbitration proceedings, including any such proceedings that are pending or threatened, of which PSV is aware that may have, or have had during the 12 months preceding the date of the annual report, a material effect on the financial position of the Group.

InDePenDent AuDItORsThe reappointment of the auditors KPMG Inc., for the ensuing year, will be confirmed at the Company’s annual general meeting in accordance with Section 270(1) of the Companies Act.

stAteD CAPItAlDetails of the authorised and issued stated capital of the Company and the movements during the period are contained in note 15 of the annual financial statements.

DIReCtORs AnD seCRetARYThe names of the directors in office are set out on page 12 of the annual report.

33PSV Annual Report 2010

The following changes to the Board occurred during the period under review:Mr JA Anderson was not re-elected as an independent non-executive director of the company and stepped down as Chairman of the Audit Committee on 28 August 2009.Mr MM Patel stepped down as chairman of the risk committee and was appointed Chairman of the Audit Committee with effect from 28 August 2009.Mr GS Nzalo was appointed as an independent non-executive director, Chairman of the Risk Committee and member of the Audit Committee with effect from 1 November 2009.The interests of directors in the issued share capital of the Company are provided below.In accordance with the requirements of the JSE Limited, a detailed report on directors’ remuneration appears in note 25.

hOlDInGs Of Psv shARes BY DIReCtORs2010 2009

Name Direct holding Indirect holding Direct holding Indirect holding

Mr P Robinson 51 350 000 974 217 47 600 000 –

Mr AJD da Silva 51 150 000 974 218 47 200 000 –

Mr AR Dreisenstock 4 400 000 974 218 4 600 000 –

Mr DJ Kelly 2 000 000 – 2 000 000 –

Total 108 900 000 2 922 653 101 400 000 –

MAjOR shARehOlDeRsDetails of major shareholders are included on page 76 of this annual report.

suBsIDIARY COMPAnIesDetails of the Company’s subsidiary companies appear in note 11 to the annual financial statements.