copyright 2010 kaufman, hall & associates, inc. all rights reserved. florida hfma 1 access to...

Post on 20-Dec-2015

213 views

TRANSCRIPT

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

1

Access to the Capital Markets: Finding Financing in a Down Economy

Hollywood Beach, Florida / September 16, 2010

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

2

• Industry Perspective and Credit Implications

• 2009 Capital Markets Re-Cap

• Capital Markets Update In the New Economy

• Concluding Thoughts: What We’re Telling Our Clients

• Appendix

Agenda

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

3

Industry Perspective and Credit Implications

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

4

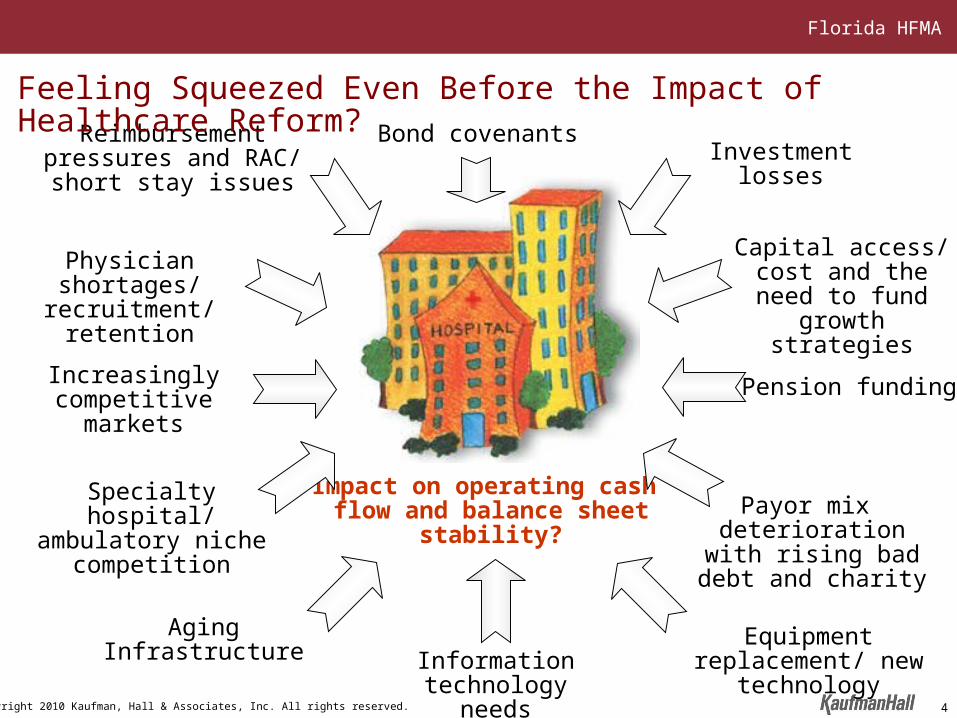

Pension funding

Investment losses

Increasingly competitive markets

Reimbursement pressures and RAC/ short

stay issues

Equipment replacement/ new technology

Aging Infrastructure

Impact on operating cash flow and balance sheet stability?

Feeling Squeezed Even Before the Impact of Healthcare Reform?

Information technology needs

Physician shortages/ recruitment/ retention

Capital access/ cost and the need to fund

growth strategies

Specialty hospital/ ambulatory niche

competition

Payor mix deterioration with rising

bad debt and charity

Bond covenants

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

5

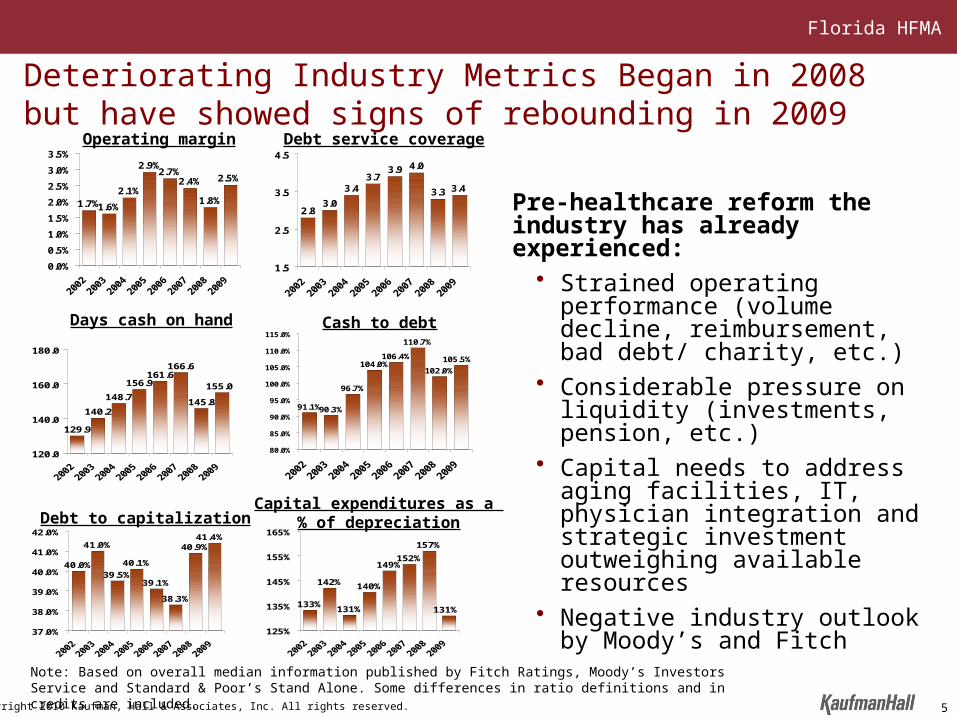

1.7%1.6%

2.1%

2.9%2.7%

2.4%

1.8%

2.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

91.1%90.3%

96.7%

104.0%106.4%

110.7%

102.0%

105.5%

80.0%

85.0%

90.0%

95.0%

100.0%

105.0%

110.0%

115.0%

133%

142%

131%

140%

149%152%

157%

131%

125%

135%

145%

155%

165%

2.83.0

3.43.7

3.9 4.0

3.3 3.4

1.5

2.5

3.5

4.5

129.9

140.2

148.7

156.9161.6

166.6

145.8

155.0

120.0

140.0

160.0

180.0

Deteriorating Industry Metrics Began in 2008 but have showed signs of rebounding in 2009

Operating margin Debt service coverage

Days cash on hand Cash to debt

Debt to capitalizationCapital expenditures as a

% of depreciation

Note: Based on overall median information published by Fitch Ratings, Moody’s Investors Service and Standard & Poor’s Stand Alone. Some differences in ratio definitions and in credits are included.

40.0%

41.0%

39.5%

40.1%

39.1%

38.3%

40.9%41.4%

37.0%

38.0%

39.0%

40.0%

41.0%

42.0%

Pre-healthcare reform the industry has already experienced:

• Strained operating performance (volume decline, reimbursement, bad debt/ charity, etc.)

• Considerable pressure on liquidity (investments, pension, etc.)

• Capital needs to address aging facilities, IT, physician integration and strategic investment outweighing available resources

• Negative industry outlook by Moody’s and Fitch

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

6

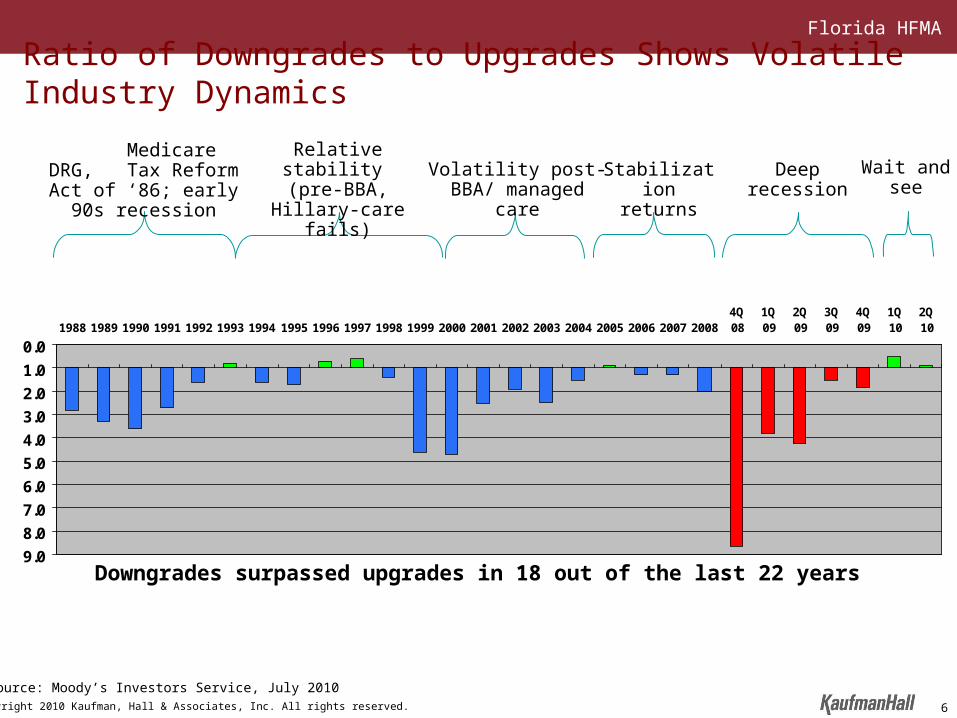

Relative stability (pre-BBA, Hillary-

care fails)Volatility post-BBA/

managed careStabilization

returns

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 20084Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

Medicare DRG, Tax Reform Act of ‘86;

early 90s recessionDeep

recession

Source: Moody’s Investors Service, July 2010

Downgrades surpassed upgrades in 18 out of the last 22 years

Wait andsee

Ratio of Downgrades to Upgrades Shows Volatile Industry Dynamics

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

7

Key Themes from Rating Agencies1. The lingering effects of a weakened economy will continue to

apply pressure on not-for-profit hospitals2. Although equity and credit markets have partially recovered,

many capital structures are exposed to letter of credit renewals, pension fund needs, and liquidity requirements

3. Hospitals must address capital needs that may have previously been delayed during the financial crisis

4. Additional cost cutting may be difficult on top of the significant reductions many hospitals have already made

5. Expiration of federal stimulus subsidies will apply pressure on operating performance

6. Federal healthcare reform places hospitals at risk for significant payment reductions beyond 2010 (reference Moody’s August 9th paper)

7. All of the above will lead to more industry consolidation and possibly hospital closures

8. Strong management and governance will continue to increase the gap between high and low performers

Source: Adapted from Moody’s “Negative Outlook Continues Due to Sluggish Economy and Government Budget Deficits”, January 2010

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

8

• Negative rating agency outlook and downgrade-to-upgrade ratio a continued concern to potential investors and credit enhancers

– Further impact on market access, costs, covenants, and security provisions• New emphasis on liquidity, capital structure and investment portfolio risk

– Cash: Not all investments are liquid– Debt: variable interest rate volatility and put risk– Enhancers: rating, terms, LOC renewability, bank ability to fund a put, etc.– Investment portfolio: risk, returns, hedge fund investment liquidity, etc.– Documents: “springing” and default covenant trigger levels, etc.

• Heightened review of audit footnotes: off balance sheet structures, guarantees, operating leases, derivatives, etc.

– “Off balance sheet” ≠ “off credit”• Consistency, predictability, market position, management team

accountability/ effectiveness, and balance sheet management continue to be key to credit

– “Remember last meeting when you said . . .” – “Show me five years of operating budgets versus audited actual”

• Improved communication and forthright, accurate disclosure are essential

Rating Agency Perspective Implications

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

9

Financial Creditworthiness and Access to Capital Matters Now More than Ever

• Virtually no healthcare system is able to fund its long-term capital requirements from operating cash flow and/or cash reserves

– Access to outside capital, over the long-term, is an imperative• Creditworthy organizations have better/ more flexible capital access

– Less restrictive terms, conditions and provisions– Access to public and private markets (fixed and variable options)– Access to credit enhancement– Taxable or tax-exempt debt

• Creditworthy organizations have a lower cost of capital– Credit spreads are extraordinarily high: “AA” to “BBB” = 125+ basis points– Access to low cost variable-rate debt– Lower issuance costs: insurance premium, letter/ line of credit,

underwriting/ remarketing• Creditworthy organizations are market consolidators

– Organizations with the highest credit rating have been the most attractive partners, have excess capital capacity and the lowest cost of capital to consolidate and remain successful in their respective markets

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

10

Summing Up 2009 in the Capital Markets….

“If you’re going through hell,keep going”

Winston Churchill

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

11

• Public fixed rate market: early crash, but respectable recovery – Heavy issuer and secondary muni market supply– “Buyer’s market” impact on covenants, security, and credit spreads– Taxable Build America Bond popularity amongst general municipal issuers

removed considerable potential competing tax-exempt paper from the market • Extraordinarily low variable rate market due to fed policy, but LOC

access, pricing and terms oftentimes challenging• Continued destruction of municipal bond insurance providers

– Essentially one non-federal player (Assured/ FSA) – can add value in fixed rate debt situations for lower credits, but not a full credit transfer (buyers will look through to the underlying credit)

• Many providers left in sub-optimal structures– Over-weighted product mix, temporary fixes, “orphan” swaps, etc.

• Investment portfolio partial recovery– 47% increase in S&P 500 from march 2009 low, but 30% off July 2007 high

• Rising long-term LIBOR rates improved mark-to-market valuation of deeply out of the money fixed payor swap positions

– Reduction in very significant collateral postings

2009 Re-Cap

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

12

Capital Markets Update in the New Economy

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

13

Our “Old Economy” Capital Market Assumptions Are No Longer Valid

1. Cheap/ dependable capital access would be facilitated– A fully functioning marketplace– Investment banks as a backstop

2. Credit enhancement to improve market access and lower cost– Expanded buyer universe even for mediocre and unsophisticated

credits– Access to alternative products and structures with ostensibly

lower cost and full commitment3. Cash retention/ creation would generate net investment returns

– Cash as protection during volatile times– Dependence on net positive returns to bolster operating “bumps

in the road” and support higher credit ratings4. Ready availability of funding for large strategic and facility plans

– Assumed access to investor dollars– Only uncertainty related to cost, covenants, and security

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

14

Capital Market Assumptions: The New Economy

• Access to capital is no longer a “given” for every credit and every project – the market is sorting out winners/ losers while the environment is subject to “on and off again” volatility

• Fixed-rate bonds are the sole form of fully committed capital• Fixed rate credit spreads remain wide, and the overall cost of

capital has increased for most organizations • LOC-backed variable-rate debt is largely uncommitted capital

with considerable and unpredictable event risk• Pull back and uncertainty surrounding credit enhancement

(bond insurance and bank letters of credit) requires borrower’s to protect and rely more on their underlying credit rating/ fundamentals

• When push comes to shove, you can’t expect the investment or commercial banks to provide a reliable backstop to an uncommitted capital structure under all circumstances

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

15

Unsettling Potential Capital Market Wild Cards in the New Economy

1. Pronounced inflation expectation2. Saturation of long-term Treasury bond issuance pushing up rates3. Increasing supply of tax-exempt debt, especially when (if) the

taxable Build America Bond program ends, pushing general muni issuers back into tax-exempt market competing with hospitals

4. Healthcare industry sector saturation as more borrowers issue fixed-rate debt and buyers get “full up” on healthcare allocation

5. Further bank industry collapse (e.g., commercial real estate, credit card debt, etc.)

6. Severe capital markets dislocation/ further liquidity crises7. Healthcare industry reform 8. Large-scale hospital bankruptcy announcement (e.g., AHERF in

the 90s)9. Over supply of new fixed-rate issues10. More confidence in equities, real estate, or commodities shifting

money out of tax-exempt bonds

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

16

Capital Sources Today: Good, but Not Great, and No One Size Fits All

1. Variable-rate demand bonds supported by a commercial bank letter of credit or self liquidity

2. Fixed-rate bonds

3. Private placements

4. Direct bank lending (bank or non-bank qualified)

5. Capital/ operating leasing

6. Asset monetization/ developer-funded structures

7. Operations

8. Working capital management (A/R reduction and A/P extension)

9. Outside support: grants, philanthropy, payor rate increases, government tax support, etc.

10. Capital investment deferral, downsizing, and/or elimination

11. Outside capital partner (merger, joint venture, etc.)

12. Other

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

17

• 30-year fixed rate access, costs and terms highly dependent on credit rating, perceived staying power and state tax advantages to investors

– “AA”: 4.62%+– “A”: 5.17%+– “BBB”: 5.87%+

• Underlying credit/ market fundamentals matter most, so expect to speak with buyers more diligently looking for highly rated, well-positioned, long-term market-winning borrowers

– Extended pre-marketing period (full one to two weeks)– Investor calls and possibly in-person investor meetings/ road

shows, depending on credit– Heightened review of Appendix A and credit reports– Buying opportunity for retail investors

Long-Term, Fixed-Rate Investors Remain Cautious, but Are Still Buying

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

18

• Continue to expect a buyer’s market with a lot of supply – now is not the time to cut corners and push the edge on security, structure, covenants, and disclosure– Security structure expectations

Revenue pledge a given for all credits Mortgages for most “A” and lower credits (plan ahead, this takes time) Debt service reserve funding for nearly all “A” category and lower credits

– Covenants and structuring matter more to fixed rate investors Liquidity covenant and periodic use of capitalization covenant Tightening thresholds for additional debt, asset disposition, senior liens,

etc. Parity with existing commercial bank LOC and insurer covenants an

emerging trend (be prepared to address this head-on during investor calls)– Disclosure quality, timeliness and responsiveness

45 to 60 days quarterly (yes, all 4 quarters) and 120 to 150 days audit Direct obligation to investors

Fixed-Rate Investors Require More Security and Covenants than in Prior Years

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

19

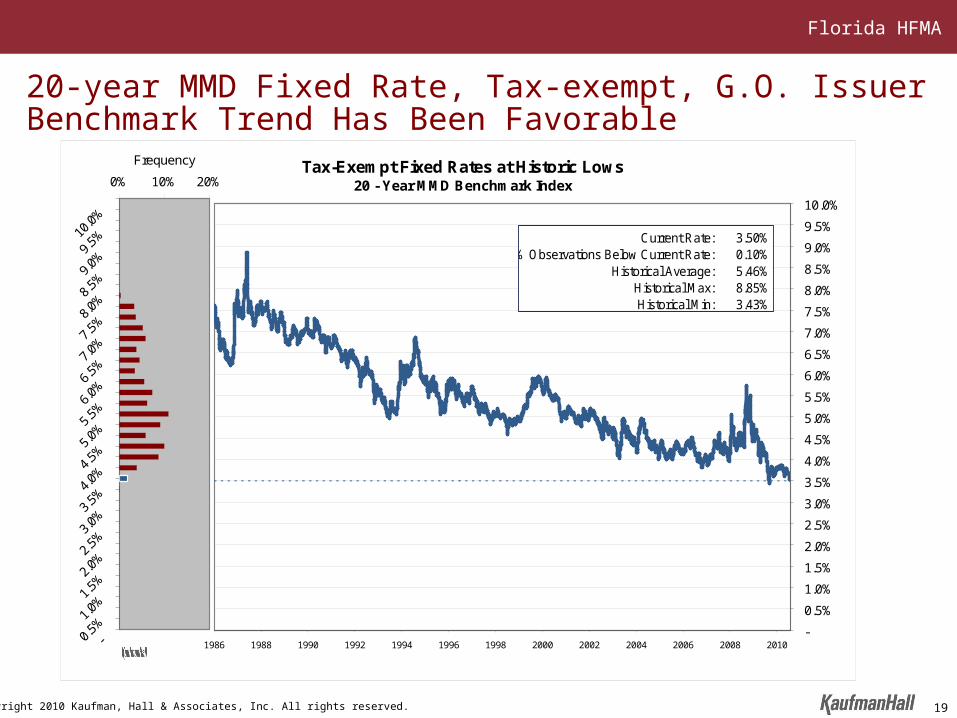

20-year MMD Fixed Rate, Tax-exempt, G.O. Issuer Benchmark Trend Has Been Favorable

Tax-Exempt Fixed Rates at Historic Lows20 - Year MMD Benchmark Index

-

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

0% 10% 20%

- 0

.5%

1.0

% 1

.5%

2.0

% 2

.5%

3.0

% 3

.5%

4.0

% 4

.5%

5.0

% 5

.5%

6.0

% 6

.5%

7.0

% 7

.5%

8.0

% 8

.5%

9.0

% 9

.5%

10.

0%

Frequency

Current Rate: 3.50%% Observations Below Current Rate: 0.10%

Historical Average: 5.46%Historical Max: 8.85%Historical Min: 3.43%

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

20

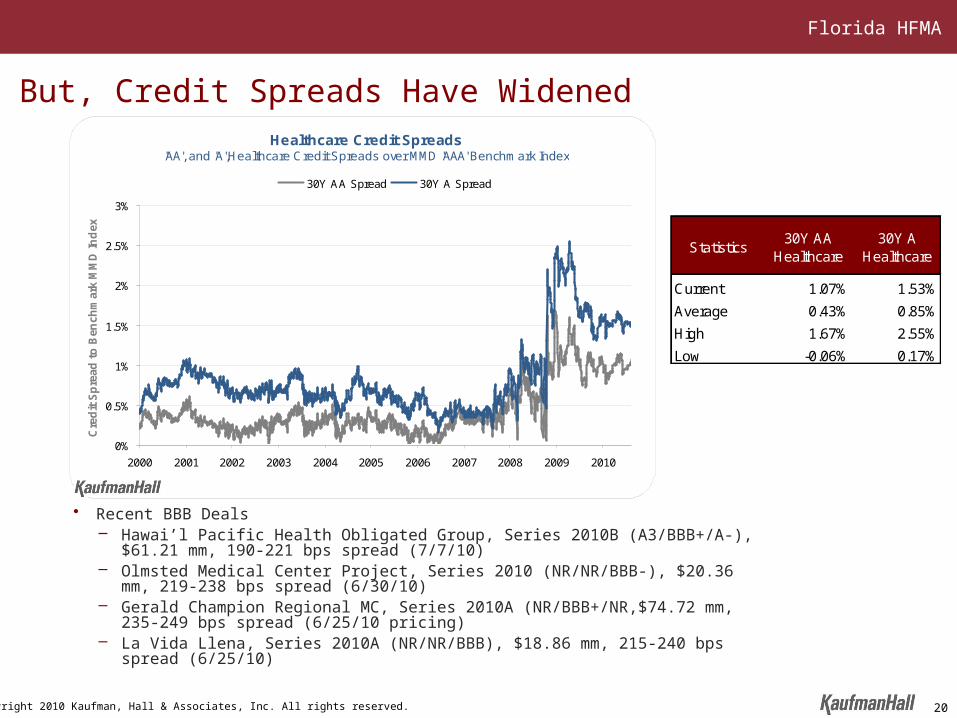

But, Credit Spreads Have WidenedHealthcare Credit Spreads

'AA', and 'A',Healthcare Credit Spreads over MMD 'AAA' Benchmark Index

0%

0.5%

1%

1.5%

2%

2.5%

3%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Cre

dit

Sp

read

to

Ben

chm

ark

MM

D In

dex

30Y AA Spread 30Y A Spread

Statistics30Y AA

Healthcare30Y A

Healthcare

Current 1.07% 1.53%

Average 0.43% 0.85%

High 1.67% 2.55%

Low -0.06% 0.17%

• Recent BBB Deals– Hawai’l Pacific Health Obligated Group, Series 2010B (A3/BBB+/A-), $61.21 mm, 190-

221 bps spread (7/7/10)– Olmsted Medical Center Project, Series 2010 (NR/NR/BBB-), $20.36 mm, 219-238 bps

spread (6/30/10)– Gerald Champion Regional MC, Series 2010A (NR/BBB+/NR,$74.72 mm, 235-249 bps

spread (6/25/10 pricing)– La Vida Llena, Series 2010A (NR/NR/BBB), $18.86 mm, 215-240 bps spread (6/25/10)

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

21

• Large money market funds remain the backbone of this market• VRDBs supported by “good banks” remain attractive

– “Good banks” have the highest ratings (perceived staying power) and are not overexposed in the LOC market

– The best of the “good banks” typically have long-term “AA” category and short-term ratings as follows: Moody’s Investors Service: “VMIG-1”, Standard & Poor’s: “A-1+”, “A-1”, Fitch Ratings: “F-1+”, “F-1”

– Monitor long-term and short-term ratings carefully – many banks have either been downgraded, have negative outlooks, or are on credit watch

• Documentation/ structuring details under heightened review– What exactly happens if the remarketing agent resigns or goes out of

business and a replacement can’t be found?– What exactly happens if the bonds are put and the bank can’t cover?– How close is the borrower to a downgrade-triggering LOC termination?

• How long will investors accept short-term, tax-exempt rates yielding under 0.3% vs. moving into other higher-yielding investment opportunities (equities, real estate, commodities, etc.)?

Short-Term, Variable Rate Investors Looking for Safety and Liquidity Continue to Step Up…for Now

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

22

• Current relationship bank(s), if highly rated, will likely be your best partner (one-off lenders to non-comprehensive clients are very infrequent)

• Less capacity for any one borrower (generally $50 to $85 million for a stand-alone hospital, perhaps more for systems and highly rated stand-alone hospitals)

– Bank syndication available on a “best efforts” basis, but complicated/ costly– Higher pricing– Shorter renewal cycles (364-day to 3 years)– Annual evergreen renewal provisions very helpful– Insist on “real” term-out provisions in the event of remarketing failure: 3-5 yrs

• Restrictive and highly negotiated covenants, security, and termination provisions

– Be mindful of borrower rating (e.g., “A-”) downgrade termination triggers

• Possible subjective consent provisions (e.g., issuing new debt, asset disposition, mergers, joint ventures, sale/ lease back, etc.)

• Significant tie-in with other commercial banking services a given

Access to Bank Letters of Credit Remains Okay for Now, but Expect…

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

23

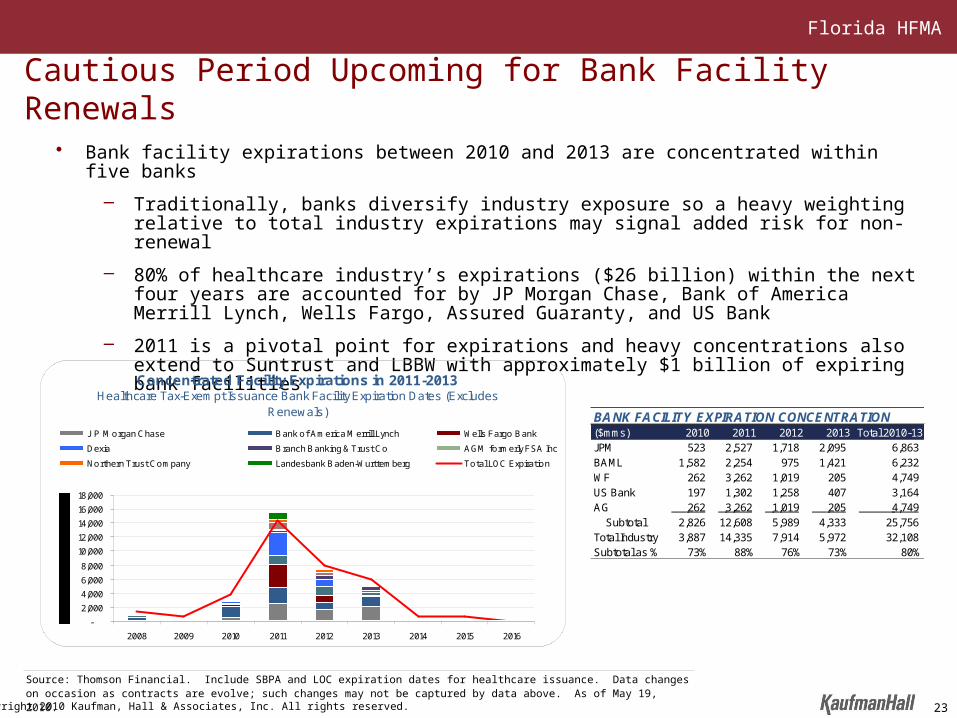

Cautious Period Upcoming for Bank Facility Renewals • Bank facility expirations between 2010 and 2013 are concentrated within five banks

– Traditionally, banks diversify industry exposure so a heavy weighting relative to total industry expirations may signal added risk for non-renewal

– 80% of healthcare industry’s expirations ($26 billion) within the next four years are accounted for by JP Morgan Chase, Bank of America Merrill Lynch, Wells Fargo, Assured Guaranty, and US Bank

– 2011 is a pivotal point for expirations and heavy concentrations also extend to Suntrust and LBBW with approximately $1 billion of expiring bank facilities

Source: Thomson Financial. Include SBPA and LOC expiration dates for healthcare issuance. Data changes on occasion as contracts are evolve; such changes may not be captured by data above. As of May 19, 2010.

BANK FACILITY EXPIRATION CONCENTRATION($mms) 2010 2011 2012 2013 Total 2010-13JPM 523 2,527 1,718 2,095 6,863 BAML 1,582 2,254 975 1,421 6,232 WF 262 3,262 1,019 205 4,749 US Bank 197 1,302 1,258 407 3,164 AG 262 3,262 1,019 205 4,749

Subtotal 2,826 12,608 5,989 4,333 25,756 Total Industry 3,887 14,335 7,914 5,972 32,108 Subtotal as % 73% 88% 76% 73% 80%

Concentrated Facility Expirations in 2011-2013Healthcare Tax-Exempt Issuance Bank Facility Expiration Dates (Excludes

Renewals)

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2008 2009 2010 2011 2012 2013 2014 2015 2016

J P Morgan Chase Bank of America Merrill Lynch Wells Fargo Bank US Bank

Dexia Branch Banking & Trust Co AGM formerly FSA Inc SunTrust Bank

Northern Trust Company Landesbank Baden-Wurttemberg Total LOC Expiration

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

24

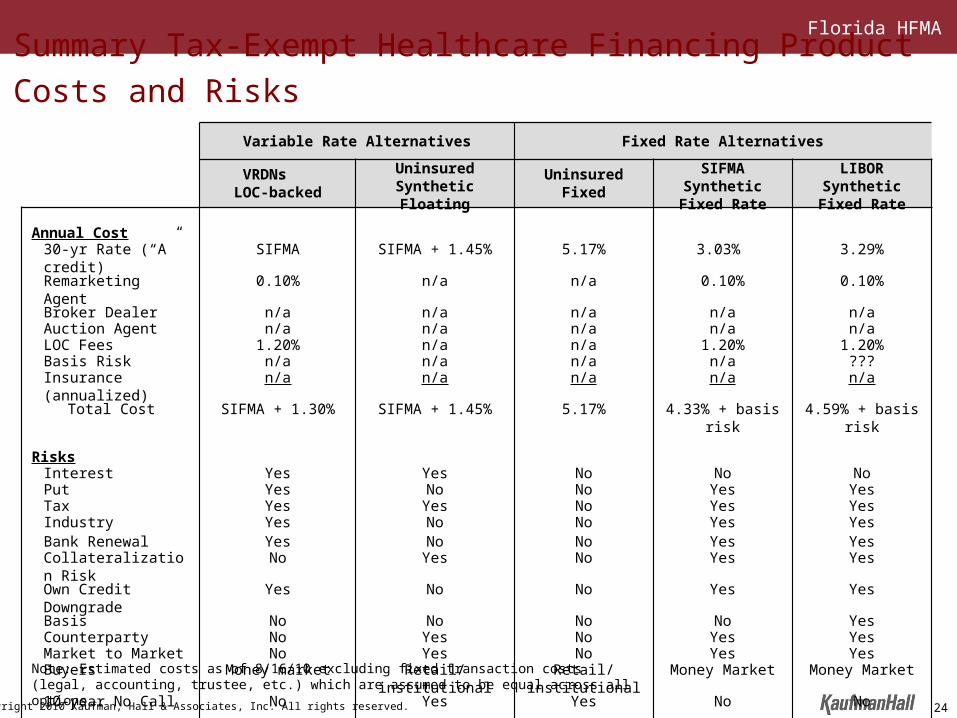

Summary Tax-Exempt Healthcare Financing Product Costs and Risks

Note: Estimated costs as of 8/16/10 excluding fixed transaction costs (legal, accounting, trustee, etc.) which are assumed to be equal across all options.

Variable Rate Alternatives Fixed Rate Alternatives

VRDNs LOC-backed

Uninsured Synthetic Floating Uninsured Fixed SIFMA Synthetic

Fixed RateLIBOR Synthetic

Fixed Rate

Annual Cost30-yr Rate (“A” credit) SIFMA SIFMA + 1.45% 5.17% 3.03% 3.29%Remarketing Agent 0.10% n/a n/a 0.10% 0.10%Broker Dealer n/a n/a n/a n/a n/aAuction Agent n/a n/a n/a n/a n/aLOC Fees 1.20% n/a n/a 1.20% 1.20%Basis Risk n/a n/a n/a n/a ???Insurance (annualized)

n/a n/a n/a n/a n/a

Total Cost SIFMA + 1.30% SIFMA + 1.45% 5.17% 4.33% + basis risk 4.59% + basis risk

RisksInterest Yes Yes No No NoPut Yes No No Yes YesTax Yes Yes No Yes YesIndustry Yes No No Yes YesBank Renewal Yes No No Yes YesCollateralization Risk No Yes No Yes YesOwn Credit Downgrade

Yes No No Yes Yes

Basis No No No No YesCounterparty No Yes No Yes YesMarket to Market No Yes No Yes YesBuyers Money market Retail/ institutional Retail/ institutional Money Market Money Market10-year No Call No Yes Yes No No

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

25

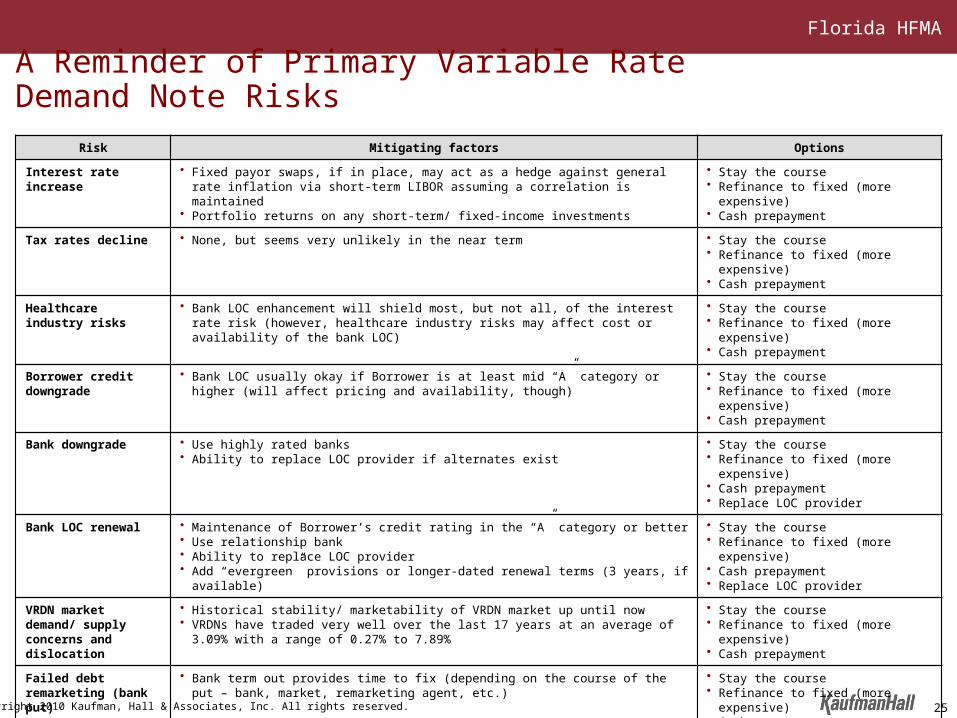

A Reminder of Primary Variable Rate Demand Note RisksRisk Mitigating factors Options

Interest rate increase • Fixed payor swaps, if in place, may act as a hedge against general rate inflation via short-term LIBOR assuming a correlation is maintained

• Portfolio returns on any short-term/ fixed-income investments

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment

Tax rates decline • None, but seems very unlikely in the near term • Stay the course• Refinance to fixed (more expensive)• Cash prepayment

Healthcare industry risks

• Bank LOC enhancement will shield most, but not all, of the interest rate risk (however, healthcare industry risks may affect cost or availability of the bank LOC)

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment

Borrower credit downgrade

• Bank LOC usually okay if Borrower is at least mid “A” category or higher (will affect pricing and availability, though)

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment

Bank downgrade • Use highly rated banks• Ability to replace LOC provider if alternates exist

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment• Replace LOC provider

Bank LOC renewal • Maintenance of Borrower’s credit rating in the “A” category or better• Use relationship bank• Ability to replace LOC provider• Add “evergreen” provisions or longer-dated renewal terms (3 years, if available)

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment• Replace LOC provider

VRDN market demand/ supply concerns and dislocation

• Historical stability/ marketability of VRDN market up until now• VRDNs have traded very well over the last 17 years at an average of 3.09% with a range of

0.27% to 7.89%

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment

Failed debt remarketing (bank put)

• Bank term out provides time to fix (depending on the course of the put – bank, market, remarketing agent, etc.)

• Stay the course• Refinance to fixed (more expensive)• Cash prepayment• Replace LOC provider

Inability of bank to fund a bond put

• Check documents for provisions and procedures as to whether this is an event of default • Refinance to fixed (more expensive)• Cash prepayment• Replace LOC provider

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

26

Where Do We Go from Here?

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

27

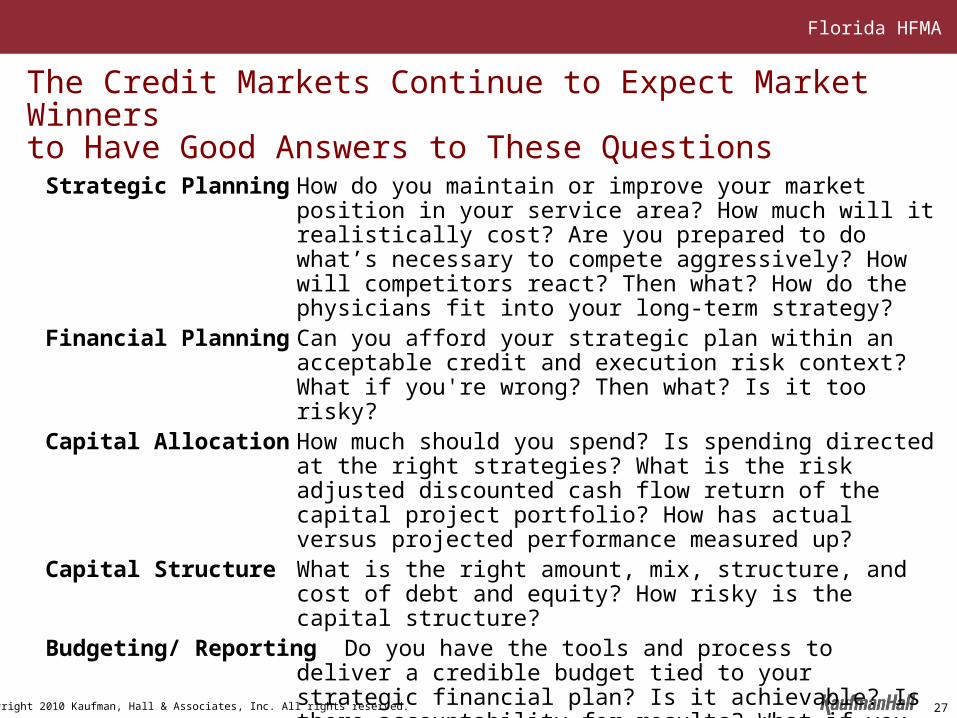

Strategic Planning How do you maintain or improve your market position in your service area? How much will it realistically cost? Are you prepared to do what’s necessary to compete aggressively? How will competitors react? Then what? How do the physicians fit into your long-term strategy?

Financial Planning Can you afford your strategic plan within an acceptable credit and execution risk context? What if you're wrong? Then what? Is it too risky?

Capital Allocation How much should you spend? Is spending directed at the right strategies? What is the risk adjusted discounted cash flow return of the capital project portfolio? How has actual versus projected performance measured up?

Capital Structure What is the right amount, mix, structure, and cost of debt and equity? How risky is the capital structure?

Budgeting/ Reporting Do you have the tools and process to deliver a credible budget tied to your strategic financial plan? Is it achievable? Is there accountability for results? What if you fall short? Then what?

Exit Rules/ Options Which services or facilities? Under what conditions? How?

The Credit Markets Continue to Expect Market Winners to Have Good Answers to These Questions

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

28

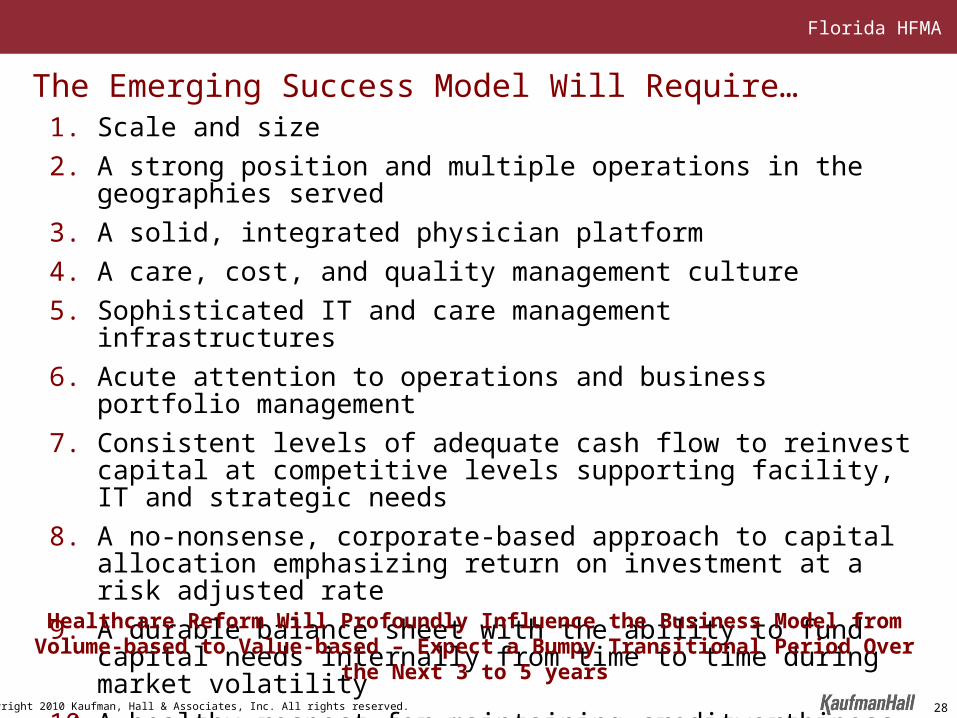

The Emerging Success Model Will Require… 1. Scale and size

2. A strong position and multiple operations in the geographies served

3. A solid, integrated physician platform

4. A care, cost, and quality management culture

5. Sophisticated IT and care management infrastructures

6. Acute attention to operations and business portfolio management

7. Consistent levels of adequate cash flow to reinvest capital at competitive levels supporting facility, IT and strategic needs

8. A no-nonsense, corporate-based approach to capital allocation emphasizing return on investment at a risk adjusted rate

9. A durable balance sheet with the ability to fund capital needs internally from time to time during market volatility

10. A healthy respect for maintaining creditworthiness, appropriately managing capital structure and preserving access to capital

Healthcare Reform Will Profoundly Influence the Business Model from Volume-based to Value-based – Expect a Bumpy Transitional Period Over the Next 3 to 5 years

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

29

Final Thoughts: What We’re Telling Our Clients

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

30

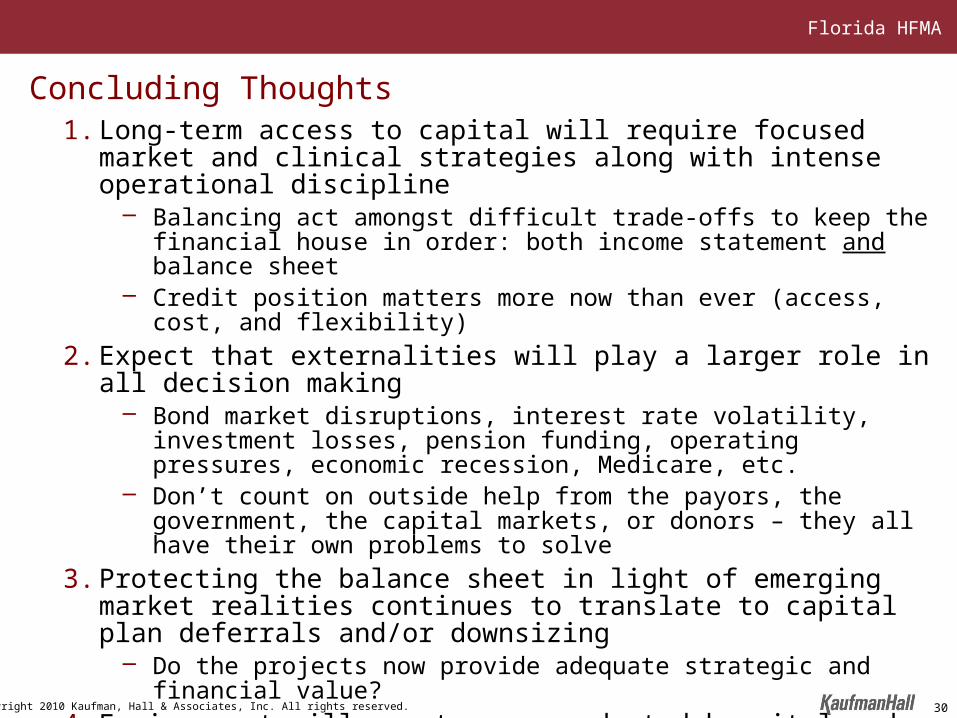

Concluding Thoughts1. Long-term access to capital will require focused market and clinical

strategies along with intense operational discipline– Balancing act amongst difficult trade-offs to keep the financial house in

order: both income statement and balance sheet– Credit position matters more now than ever (access, cost, and flexibility)

2. Expect that externalities will play a larger role in all decision making– Bond market disruptions, interest rate volatility, investment losses,

pension funding, operating pressures, economic recession, Medicare, etc. – Don’t count on outside help from the payors, the government, the capital

markets, or donors – they all have their own problems to solve

3. Protecting the balance sheet in light of emerging market realities continues to translate to capital plan deferrals and/or downsizing

– Do the projects now provide adequate strategic and financial value?

4. Environment will create unprecedented hospital and physician consolidation opportunities

– Driven by the search for long-term growth and scale and the need to cut costs and access capital in support of long-term survivability

– Materially financially impaired organizations may not be able to find a partner

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

31

5. Know your bond, bank and swap documents well – unpleasant issues are continuing to surface

– Covenant breaches requiring waivers, consents, swap collateralization, downgrade triggers, springing DSRFs, etc.

6. Capital structure risk continues to be front and center– Fixed-rate bonds are the only form of long-term, committed capital– Untangling existing capital structures contingent upon insurance ratings,

bank LOC availability, swaps, etc., has been more difficult and expensive– Read the fine print – deal details important to fully understand– Diversification is ideal, but may not be possible in many circumstances:

credit providers, remarketing agents, swap providers, etc.

7. If you have to borrow, there’s nothing wrong with fixed-rate bonds if that market is available to you

– The low-rate, freewheeling credit environment prior to July 2007 no longer exists – expect interest rates in the 5% to 7% range, credit depending

– Pay attention to the timing of selling your bonds and what other deals will be in the market at that time – over supply continues to be an issue

Concluding Thoughts (continued)

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

32

8. Variable-rate debt is currently very attractively priced and needs to be considered, but generally requires a stable relationship with a “good bank” and creates exposure to many risks

– Risks are considerable: interest rate, market dislocation, bond put, bank downgrade, LOC renewal, bank covenants, etc.

– A new ratio to consider: unrestricted cash to variable-rate debt

9. Nontraditional sources of capital are an option– HUD/ FHA 242– Bank loans (bank qualified and non-bank qualified)– Other direct loans/ private placements – Real estate monetization– Leasing

Concluding Thoughts (continued)

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

33

Appendix

Copyright 2010 Kaufman, Hall & Associates, Inc. All rights reserved.

Florida HFMA

34

Mark McIntire is a Vice President of Kaufman Hall and a member of the firm’s financial advisory practice. Mr. McIntire works with a wide range of healthcare organizations, providing financial advisory services for clients engaged in bond issues, derivative transactions, and/or merger and acquisition activity. Mr. McIntire also supports Kaufman Hall’s financial management software, the ENUFF Software Suite®.

Prior to joining Kaufman Hall, Mr. McIntire served as a senior analyst in JPMorgan’s Midwest healthcare investment banking practice, where he focused on structuring bond transactions and advising on derivative products.

Mr. McIntire is a frequent speaker at professional conferences, including chapters and regional meetings of the Healthcare Financial Management Association, the Child Health Corporation of America, and other organizations. He has written extensively on the topics of leasing and best-practice financing, with articles having appeared in hfm magazine and Strategic Financial Planning, among others.

Mr. McIntire has an M.B.A. from the University of Michigan Business School and a B.S. from Indiana University.

Kaufman, Hall & Associates, Inc.5202 Old Orchard Road, Suite N700Skokie, Illinois 60077847.441.8780, ext. 114847.965.3511 [email protected]

Mark E. McIntire, Vice President