copyright by timothy gordon jones 2008

TRANSCRIPT

Copyright

by

Timothy Gordon Jones

2008

The Dissertation Committee for Timothy Gordon Jones

certifies that this is the approved version of the following dissertation:

Essays on Money, Inflation and Asset Prices

Committee:

Russell Cooper, Supervisor

Dean Corbae

Kim Ruhl

Jennifer Huang

M. Fatih Guvenen

Essays on Money, Inflation and Asset Prices

by

Timothy Gordon Jones, B.A.; M.S.

Dissertation

Presented to the Faculty of the Graduate School of

The University of Texas at Austin

in Partial Fulfillment

of the Requirements

for the Degree of

Doctor of Philosophy

The University of Texas at Austin

May 2008

Dedicated to Garrett, with love.

Acknowledgments

I would like to thank my advisor, Russell Cooper, whose guidance and support

have been essential both to this dissertation and to my professional development. I

am also grateful to Dean Corbae, Jennifer Huang, Kim Ruhl, and John Willis for

helpful advice and guidance. This work also benefited from useful comments from

the participants of numerous seminars at the department.

Additionally, Chai Chi, Patrick Cosgrove, Shayne McGuire, Kay Cuclis,

Phillip Auth, and KJ van Ackeren are a few of the excellent investment managers

at the Teacher Retirement System of Texas who assisted with their specific ideas

and general contributions to an open and productive exchange of ideas.

I am most grateful to Conan Crum, Jason DeBacker, Pablo D’Erasmo, Rick

Evans, and Anna Yurko for being supportive friends, excellent officemates, and

invaluable colleagues. This dissertation could not have been completed without

their advice and support.

Timothy Gordon Jones

The University of Texas at Austin

May 2008

v

Essays on Money, Inflation and Asset Prices

Publication No.

Timothy Gordon Jones, Ph.D.

The University of Texas at Austin, 2008

Supervisor: Russell Cooper

This dissertation explores different aspects of the interaction between money and

asset prices. The first chapter investigates how a firm’s financing affects its decision

to update prices: does linking interest rates to inflation alter the firm’s optimal price

updating strategy? Building on the state dependent pricing models of Willis (2000)

and the price indexing literature of Azariadis and Cooper (1985) and Freeman and

Tabellini (1998), this model investigates the financing and price updating decisions

of a representative firm facing state-dependent pricing and a cash-in-advance con-

straint. The model shows the circumstances under which a firm’s financing decision

affects its price updating decision, and how the likelihood of changing prices af-

fects the amount borrowed. It also illustrates how the use of nominal (as opposed

to inflation-linked) interest rates leads to a lower frequency of price updating and

vi

higher profits overall for a firm facing menu costs and sticky prices.

The second chapter extends the bank run literature to present a theoretical

mechanism that explains how money supply can affect asset prices and asset price

volatility. In a two period asset allocation model, agents faced with uncertainty

cannot perfectly allocate assets ex-ante. After income shocks are revealed, they will

be willing to pay a premium over the future fundamental value for an asset in order

to consume in the current period. The size of this premium is directly affected by

the supply of money relative to the asset.

This paper explores the relationship between economy-wide monetary liquid-

ity on the mean and variance of equity returns and in relation to market liquidity.

At an index level, I test the impact of money-based liquidity measures against exist-

ing measures of market liquidity. I proceed to do a stock level analysis of liquidity

following Pastor and Stambaugh (2003). The results indicated that measures of

aggregate money supply are able to match several of the observed relationships in

stock return data much better than market liquidity. At an individual stock level,

monetary liquidity is a priced factor for individual stocks. Taken together, these

papers support the idea that changes in the money supply have consequences for

the real economy.

vii

Contents

Acknowledgments v

Abstract vi

Chapter 1 Price and Interest Rate Indexing 1

1.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

1.2.1 Sequence of Decisions . . . . . . . . . . . . . . . . . . . . . . 4

1.2.2 Uncertainty . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1.2.3 Firm’s Problem . . . . . . . . . . . . . . . . . . . . . . . . . . 6

1.3 Solution . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

1.3.1 Solving the Firm’s Problem . . . . . . . . . . . . . . . . . . . 8

1.4 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

1.4.1 Price Updating Decision . . . . . . . . . . . . . . . . . . . . . 12

1.4.2 Financing Decision . . . . . . . . . . . . . . . . . . . . . . . . 23

1.4.3 Indexing Effects . . . . . . . . . . . . . . . . . . . . . . . . . 25

1.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Chapter 2 Asset Prices and Money in a Two-Period Equilibrium 39

2.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

2.2 Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

viii

2.2.1 Timing and Uncertainty . . . . . . . . . . . . . . . . . . . . . 42

2.2.2 Household Problem . . . . . . . . . . . . . . . . . . . . . . . . 44

2.2.3 Market Clearing . . . . . . . . . . . . . . . . . . . . . . . . . 45

2.2.4 Equilibrium . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

2.3 Solving the Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

2.3.1 First period (t = 1) . . . . . . . . . . . . . . . . . . . . . . . . 47

2.3.2 Initial Period . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

2.3.3 Household Problem . . . . . . . . . . . . . . . . . . . . . . . . 50

2.3.4 Initial Price, p0 . . . . . . . . . . . . . . . . . . . . . . . . . . 54

2.4 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

2.4.1 Impact of liquidity shocks on the mean and variance of p0 . . 55

2.4.2 Monetary Services Index . . . . . . . . . . . . . . . . . . . . . 58

2.5 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

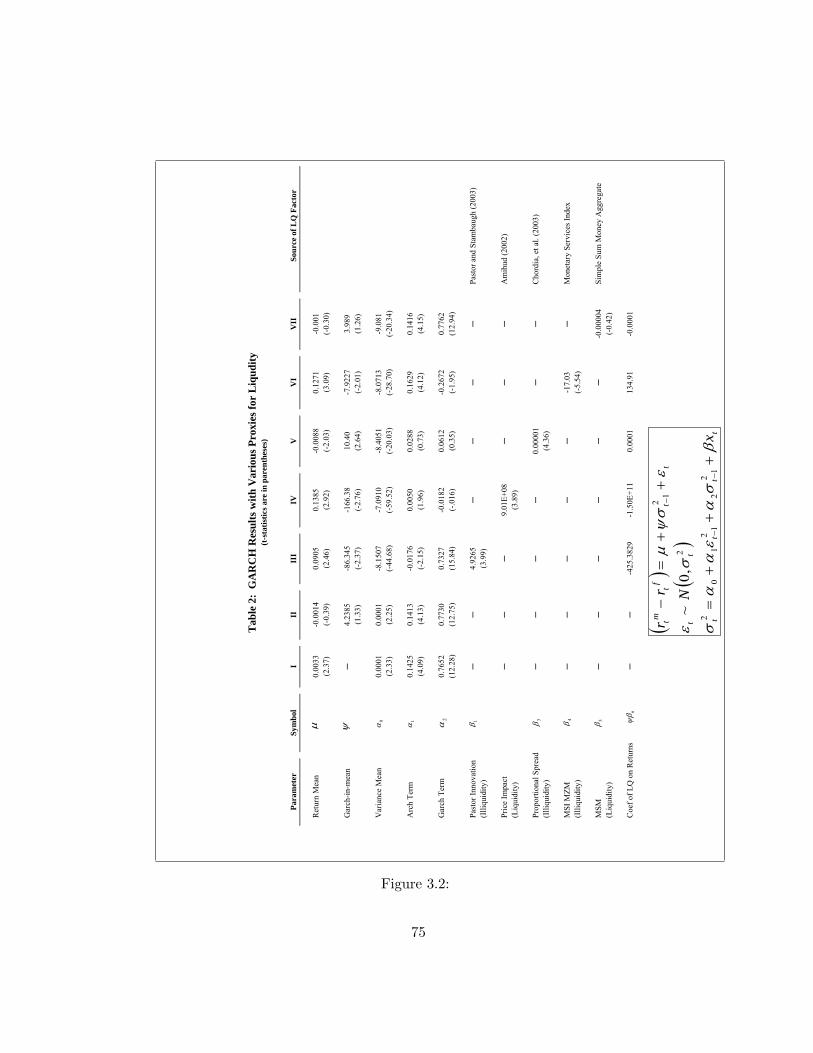

Chapter 3 Monetary Liquidity and Asset Pricing 65

3.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 65

3.2 Data . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

3.3 Testing Liquidity on Index Aggregates . . . . . . . . . . . . . . . . . 73

3.4 Testing Liquidity on a Cross-Section of Stocks . . . . . . . . . . . . . 76

3.5 Causality . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

3.5.1 Impact of Monetary vs. Market Liquidity on Returns and

Volatility . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

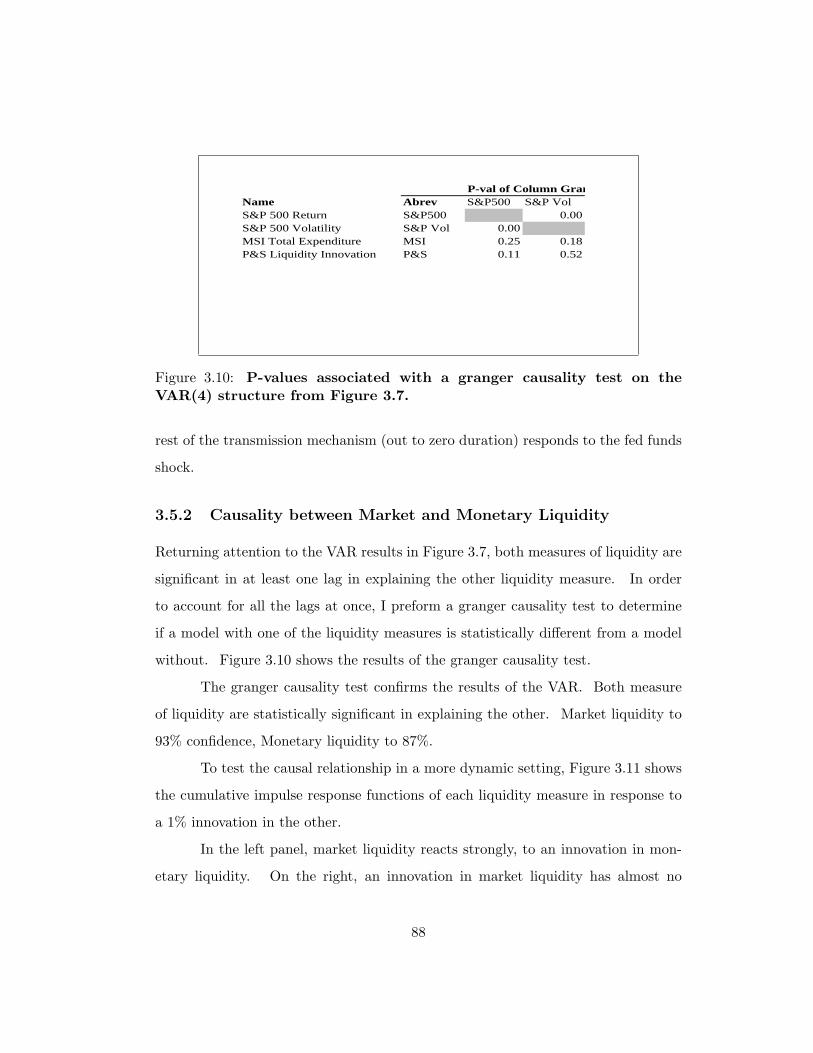

3.5.2 Causality between Market and Monetary Liquidity . . . . . . 88

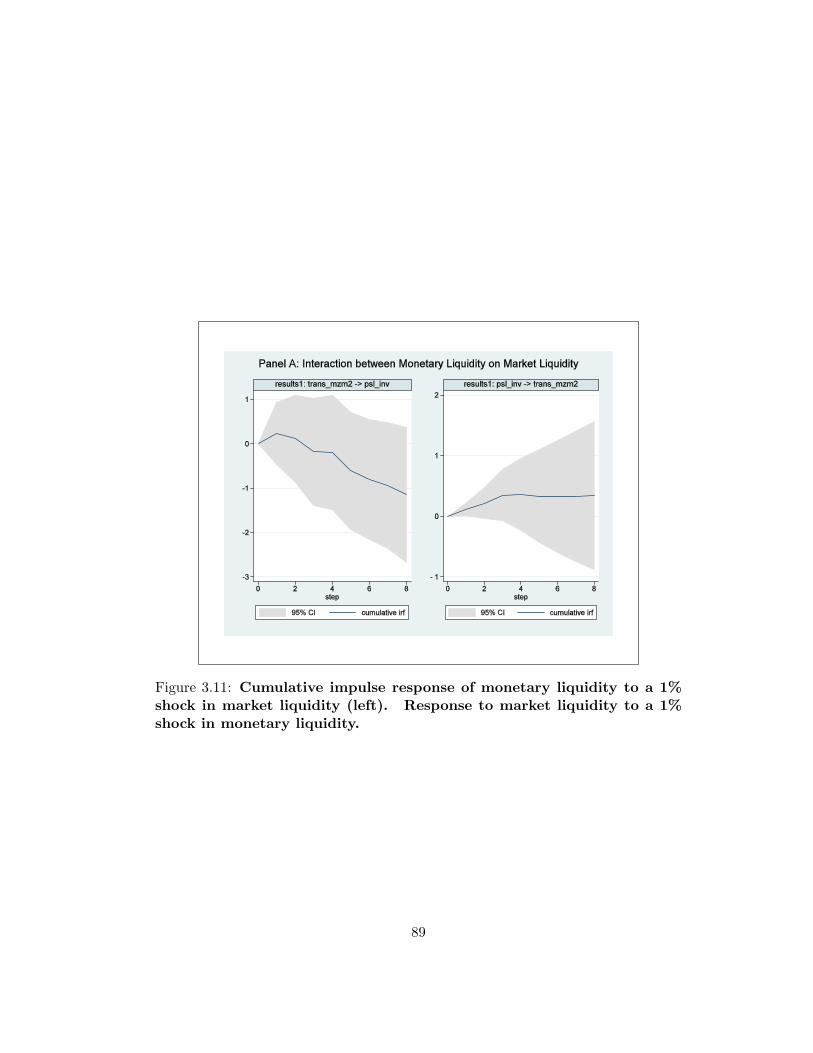

3.6 Conclusion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 90

Bibliography 91

Vita 94

ix

Chapter 1

Price and Interest Rate

Indexing

1.1 Introduction

In an environment where prices are costly to change, firms face a trade-off between

price inefficiency and adjustment costs. In not updating its price, a firm risks a

demand shock from inflation; its real price will be lower than optimal because of an

increase in the aggregate price level. The standard state-dependent pricing solution

is to update prices when the cost of adjusting prices is lower than the profit lost

from having a non-optimal price. Here we consider that a firm’s financing costs can

also be affected by the aggregate price level, and can feed back into the decision to

update prices. The amount borrowed impacts the price updating strategy through

the cash-in-advance constraint. In addition to borrowing, I compare two types of

interest rate regimes, one indexed to inflation (changes in the aggregate price level)

and the other not indexed. The type of interest rate regime alters the optimal

updating strategy of the firm; firms borrowing at non-indexed rates update prices

less frequently and have higher expected profits.

1

Before addressing the role of interest rate regimes, its necessary to estab-

lish how a financing decision can be relevant to a firm’s value in the first place.

Modiglianni and Miller (1958) proposition I, also called the irrelevance proposition,

maintains that under a set of basic market efficiency assumptions financing decisions

should not affect the core business of the firm. In order to consider price and inter-

est rate indexing, I am necessarily relaxing those assumptions in two ways. First,

I’m allowing sticky prices by imposing state-dependent costs on price adjustment.

Secondly, in order for firms to need financing in the first place, I introduce a cash-

in-advance constraint. The interaction between these two distortions results in the

relevance of financing structure to the firm’s price updating strategy and overall

value.

A cash-in-advance constraint is sufficient to contradict the irrelevance propo-

sition by itself; it can be considered a special case of incomplete asset markets. A

menu cost hinders price adjustment, which will affect firm value, though not nec-

essarily through the capital structure. The model shows how the amount a firm

borrows affects its price adjustment strategy by limiting the quantity it can pro-

duce. Moreover, the interaction of those frictions produces an environment where

the non-indexed interest rate regime generates higher expected profits for firms than

indexed ones. The model offers a mechanism to explain this outcome: indexing rates

deters borrowings and causes the cash-in-advance constraint to bind more severely.

Firms that do not index their borrowing have less to gain from price changes and

will therefore update prices less frequently, and borrow more.

Previous literature in this area has focused on the optimal risk sharing prop-

erties of nominal contracts (or the equivalent term, non-indexed prices). These

papers address models that share a common approach. Each of at least two agents

is a buyer of one good or service and a seller of another. Therefore, equilibria exist

when either everyone indexes their price or no one does. For an agent to pay an

2

indexed price but offer a non-indexed one would mean taking on a disproportionate

amount of risk. If ex-ante risk preferences were the same, this extra risk would not

be optimal. Blinder (1977) defines this relationship and the equilibrium between

worker’s wages and firm’s returns; Azariadis and Cooper (1985) for worker’s wages

and the price of goods. Freeman and Tabellini (1998) establishes the conditions

necessary for agents to choose a nominal, and therefore monetary, equilibrium.

This paper contributes to the literature by addressing the link between the

price of goods and interest rates. In what follows, I describe how a firm’s financing

mechanism can affect its overall value at all, and if so, under what conditions the firm

would be better off with non-indexed interest rates. I develop a partial equilibrium

model of the firm assuming some positive cost to adjusting its price. The firm

borrows before the menu cost and shocks to taste and inflation are revealed in order

to fund current production. The firm can change its price by paying the cost of

adjustment, or use last period’s price. I show that for positive costs of adjustment,

firms have higher expected profits for all initial price levels when borrowing at non-

indexed interest rates.

Section 2 details the environment of the model, the sequence of decisions, and

the firm’s problem. Section 3 solves the firm’s problem and defines equilibrium.

Section 4 shows how the financing constraint and non-indexed interest rates increase

price stickiness for a given menu cost, and goes on to prove the primary result, that

firms prefer non-indexed rates. A conclusion follows in Section 5.

1.2 Model

The model environment is one of two-period partial equilibrium, designed to high-

light the pricing behavior of a firm. The firm enters the first period with an initial

price and a unique production technology, converting labor into output. The de-

3

mand for its product is know to the firm and can purchase labor competitively. 1

Due to a cash-in-advance constraint, firms must borrow money in the first period

to produce in the second. If a firm opts to change its price, it has to pay a cost

of adjustment drawn in the second period. When the firm makes its financing

decision, it does so under uncertainty about demand, its real price, and the cost of

adjustment. Consider the choices a firm faces in the event of a high realization of

demand (from inflation or a taste shock). If the firm has borrowed more money

than it expected to use, it has additional capacity to hire workers and meet the high

demand rather than paying the menu cost and raising its price. This increased flex-

ibility comes at the price of higher borrowing costs. If the firm borrowed only what

it expected to need, the same high demand scenario makes it more likely that the

firm will pay the menu cost and raise its price rather than sell its limited quantity at

the initial price, which after the demand shock is much lower than the optimal reset

price. This uncertainty about demand connects the financing decision to the price

updating decision. The firm must decide on the amount to borrow, and thereby

commit to both an upper limit on how much it can produce and lower limit on its

costs. Those limits will affect its decision to update its price in the next period.

1.2.1 Sequence of Decisions

The first period is the financing period, when the firm must decide how much money

to borrow for use in the second period. In the second period, capital markets are

closed, and the firm must use what it has borrowed to hire workers and produce

goods. The interest rate, indexation regime, wages, and productivity are exogenous

and held constant. In the first period, before the shocks and menu cost are revealed,

the firm borrows by issuing one period bonds to finance current second period pro-

duction . After the first period’s borrowing is complete, the taste shock, price level,1The particular form of demand can be derived as an outcome of optimized CES preferences,

which is standard in the price adjustment literature.

4

Two-Period Timeline

Initial Price Draw: p-1

Collect Revenue, Repay Debt

Borrow under uncertainty: B*(S)

If changing, set new price: p*(S)

Hire (and pay) labor to fulfill produce: qs

t=0 t=1

Menu cost draw Ψ, taste shock µ, and aggregate price level P revealed

Decide to Update Price or Not: ΨΨ’(S)

Figure 1.1: Sequence of Decisions by the Firm

and menu cost are realized and the firm decides whether to update prices. After

the firm sets its price, it pays wages and produces output. Lastly, the firm collects

revenue and uses it to repay the bonds. [see Figure 1.1].

1.2.2 Uncertainty

The firm faces three types of uncertainty in the first period when making the fi-

nancing decision. The taste shock that will affect demand in the second period is

exogenous and i.i.d. Similarly, the menu cost that the firm will face when making

its price updating decision is unknown in the first period and drawn from a distri-

bution in the second. This is a similar framework for state dependent adjustment

costs as in Dotsey, King and Wolman (1999). The third type of uncertainty the

firm faces is the new price level, or an inflation shock. The inflation shock is drawn

from a mean zero distribution, and the new price level will affect both demand and

5

the firm’s costs (see Equations 1.1 and 1.2).

logP = logP−1 + ε (1.1)

ε ∼ N (0, σ) (1.2)

1.2.3 Firm’s Problem

In the first period, the firm has an initial price (p−1) and knows the initial price

level (P−1). These two values define the ex-ante state, from which the firm takes

expectations about next period’s demand and costs. The firm then borrows in this

period in order to finance production. In the next period, the aggregate shock is

revealed and the firm decides if it should change its price or not.

Firm’s Optimization Problem

In the first period, the firm chooses an amount to borrow. In doing so, it must

take into account the realization of the shocks and its own strategy for updating the

price Equation (1.3) summarizes the first period problem. S−1 is a vector of state

variables known at the time of the financing decision, including the first period price

and aggregate price level. S includes the realizations of the random variables and

the choice of B.

Π (S−1) = maxBE[{

ΠC (p, q, S) ,ΠNC (q, S)}]

(1.3)

S−1 ={P−1, p−1, r

F , φ, λ}

(1.4)

S = {S−1, P,Ψ, µ,B} (1.5)

The two functions that are considered in the first period, ΠC (p, q, S) and

6

ΠNC (q, S), are the profit functions for the firm in the second period, after the

decision to change its price has been made. If the firm decides to change its

price, the second period firm’s problem is equation (1.6). The firm chooses a price

to maximize profits as well as the quantity to produce, subject to the borrowing

constraint and demand equation (1.8). If the firm chooses not to update its price

it simply chooses a quantity. This is meant to allow the firm the option to exit or

partially fulfill demand, not as a tool for optimization.

ΠC(p, q, S) = max{p,q}

pqs (p)− (1 + r (φ))B −

(wn

(P

P−1

)λ

−B

)−Ψ (1.6)

ΠNC(q, S) = max{q}

p−1qs (S)− (1 + r (φ))B −

(wn

(P

P−1

)λ

−B

)(1.7)

s.t. qs (S) ≤ min{qm (S) , qd (S)

}(1.8)

where qm =

[B

w

(P−1

P

)λ]α

; qdi (pi, P ) =

(pi

P

)−γ (D)P

µ; (1.9)

Demand for good i is CES (1.9), where D is a scaling parameter, µ is the

taste shock, γ is the elasticity parameter, P is the aggregate price level, and pi is

the price of a specific good.

The production technology converts labor to output:

qs = f (n) = nα

The structure of the interest rates facing the firm can depend on the price

level, as see above in r.

r =(1 + rF

) [Pt+1

Pt

]φ

(1.10)

The parameters {φ, λ} (1.6,1.7,1.10) define the indexation in the firm’s factor

contracts. φ determines the extent to which the interest rate changes with inflation,

7

while λ controls the extent to which the wage changes with inflation. if λ is zero,

the nominal wage does not change with the price level. If φ and λ are both 1, the

interest rate and the wage are effectively real costs. Ψ is the menu cost (the cost of

updating prices). Equation (1.8) highlights the effect the borrowing constraint has

on the quantity choice. The less a firm has borrowed in the first period, the lower

the maximum quantity it can produce, and the more likely qm will bind.

1.3 Solution

1.3.1 Solving the Firm’s Problem

The firm maximizes (1.3) subject to the cash-in-advance constraint (1.8). The

firm’s problem is solved backwards through the two periods. Solving the second

period first, the firm takes the realized values of µ, Ψ and P as given, and maximizes

profits conditional on changing the price or keeping last period’s price. With the

second period policy function established, the firm solves the first period problem

of how much to borrow, taking expectations over the realizations of the states and

second period policy functions as given.

Second Period

Firms enter the second period with an amount borrowed and a previous price, both

from last period. Current aggregate price level, P , the taste shock, µ, and the menu

cost Ψ, are revealed at that point. Working backwards, the firm’s last decision is to

choose a price to maximize profits, assuming it chooses to pay the adjustment cost.

Choice of Price when Updating When the firm decides to pay the menu cost,

it chooses a price p, (and implicitly, a quantity) to maximize profits subject to the

limits of the cash-in-advance constraint. Substituting demand (1.9) into (1.6) and

adding a Lagrangian multiplier (δ) on the cash in advance constraint reformulates

8

the firm’s problem as an unconstrained maximization:

ΠC (p, q, S) = maxp

( pP

)1−γDµ−Br (φ)− wP z

(p−γDµ

) 1α −Ψ (1.11)

−δ[qd (p)− qm (S)

]where z = λ+

γ − 1α

and Ψ is known

Solving the first order condition yields a policy rule for price setting, condi-

tional on updating the price. The optimal price, p∗, solves:

if δ = 0 : p∗ (S) =γ

α (γ − 1)w

(P

P−1

)(z−γ+1)

(Dµ)1−α

α (1.12)

if δ ≥ 0 : p∗ (S) = (Dµ)1γ

(B [P−1]

λ

w

)−αγ

Pλαγ

+1− 1γ (1.13)

Choice of Quantity when Keeping Initial Price If the firm opts to keep its

price from last period, then demand is determined by the outcome of the shocks

alone. The firm does not have to fulfill demand however; its finance constraint

could bind, or it might not be able to produce at a profit.

ΠNC (q, S) = maxqs

p−1qs (S)− (1 + r (φ))B − wPn+B

s.t.

qs (S) ≤ qm (S) (1.14)

qs (S) ≤ qd (S) (1.15)

First we consider what happens when the firm produces up to the level

demanded, i.e., when constraint (1.15) binds:

9

f (n) = nα ⇒ n = q1α ; z =

α+ γ − 1α

ΠNC (q, S) =(p−1

P

)1−γDµ− (1 + r (φ))B − wP z

(p−γ−1Dµ

) 1α +B

If the demand is higher than anticipated, and the firm attempts to produce

more than it has borrowed for, constraint (1.14) will bind. In that case, profit is

the following:

ΠNC (q, S) = p−1qm(S)− wP [qm(S)]

1α (1 + r (φ)) (1.16)

Alternatively, the firm may have drawn such back shocks that it chooses to

shut down. Thus, the production strategy for the firm after choosing to keep its

initial price can be summarized as the following:

qs∗ (S) =

max[ΠNC (qm, S) ,ΠNC (0, S)

]if qm ≥ qd

max[ΠNC

(qd, S

),ΠNC (0, S)

]if qd ≥ qm

(1.17)

Price Updating Decision Thus, at the beginning of the second period, the firm

faces a decision to change its price or not, taking the policy functions it uses to set

its price and quantity as given. This decision can be written as a policy function,

Ψ∗(S) that determines the highest menu cost that a firm is willing to pay. If the

menu cost is higher than Ψ∗(S) then the firm will leave prices unchanged.

Ψ∗(S) = ΠC (p∗, q, S)−ΠNC (q, S) (1.18)

An important factor in determining Ψ∗ is B, how much the firm borrowed

in the first period (B is part of S). The amount borrowed will affect the profits

that each pricing strategy will return; the less borrowed, the higher the price will

10

need to be take advantage of the reduced capacity. When the initial price is close

to or less than the optimal price (the price that would be chosen if the menu cost

were paid), under-borrowing raises the value of price adjustment, and increases the

threshold menu cost the firm is willing to pay. When the initial price is above the

optimal price, under-borrowing reduces the value of price adjustment. In that case,

constraining capacity offsets the inefficiency created by an initial price that was too

high relative to an unconstrained optimal price.

First Period

In the previous section, the firm solves its pricing problem conditional on an amount

previously borrowed. In the first period, the firm chooses an amount to borrow

based on the following policy rules for updating and setting its price:

B∗ (S−1) = max{B}

∫S

max{ΠC (p, q, S) ,ΠNC (q, S)

}dS (1.19)

This maximization is somewhat tricky, due to the choice of updating or not.

For each state, the firm must evaluate whether it will change prices or not, i.e., solve

for Ψ∗(S). Equation (1.19) can be rewritten as a strategy if we take Ψ∗(S) as given:

B∗ (S−1) = max{B}

∫S

ΠC (p, q, S) if Ψ ≤ Ψ∗(S)

ΠNC (q, S) if Ψ > Ψ∗(S)

dS (1.20)

Once it knows which profit function will be optimal in each state, it can choose

an amount to borrow that maximizes the expected profit. The problem with this

approach is that Ψ∗(S) itself is dependent upon B. Thus, the problem must be

solved numerically.

11

1.4 Results

The model produces two critical results. First, that the financing amount, B, affects

the price adjustment strategy of the firm. Conversely, the firm takes that strategy

into account when deciding on the amount to borrow. This mechanism is important

to identify as it underpins the second result, that the indexing regime (the value of

φ in the model) also affects the firm’s price adjustment strategy. Related to the

indexing result is the finding that the firm’s expected profits are higher at every

initial price under the non-indexing interest rate regime. In this section, I describe

each result in detail and explain the mechanism driving it.

1.4.1 Price Updating Decision

In order to show how the financing decision affects firm value, I show how the financ-

ing decision B∗ (S−1) affects the price updating decision. Ψ∗ (S) is the reservation

menu cost that determines whether the firm will update prices. If their realized

menu cost is above Ψ∗ (S) , they will not change prices. Ψ∗ (S) depends on the

difference between the profits under a new price and the old price (1.18).

Impact of Amount Borrowed on Price Updating Decision

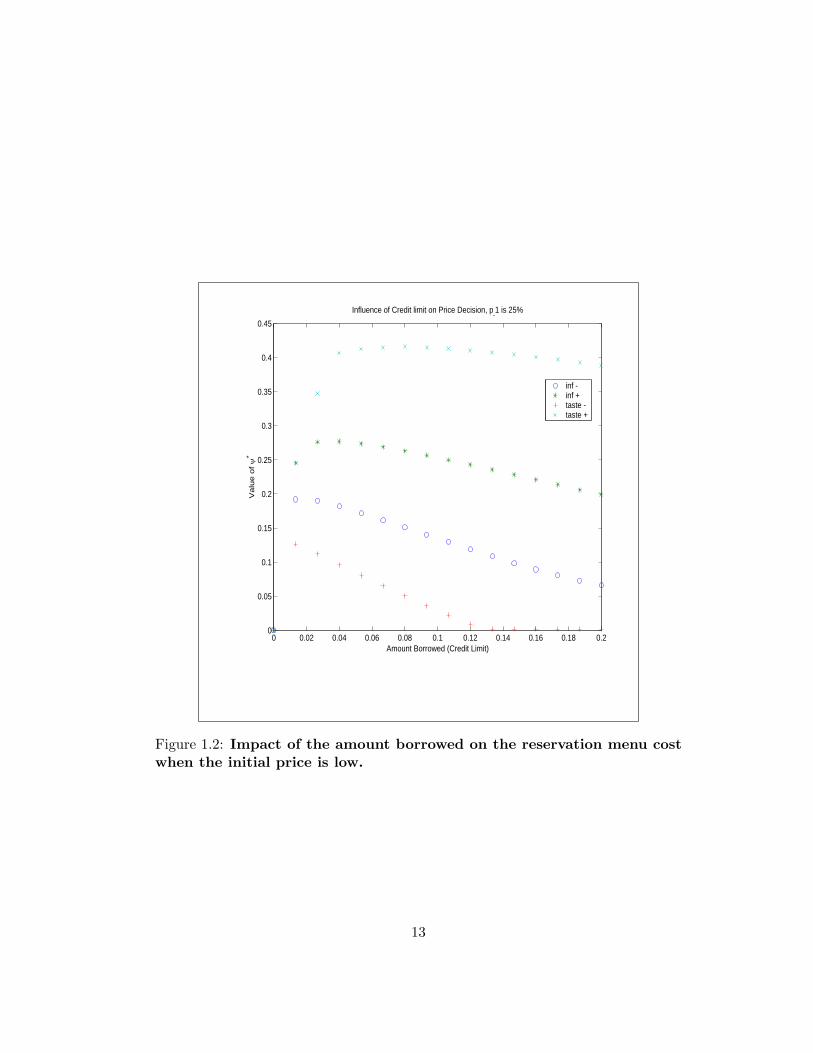

Figures 1.2-1.4 illustrate how the pricing decision (1.18) changes with the amount

borrowed at different initial prices and various shocks.

Figure 1.2 illustrates the price updating function when the initial price is

low. At all levels of borrowing, a positive inflation shock will increase the chances

of a firm changing its price. A positive taste shock, which increases demand for a

particular firm’s good without altering relative prices between it and other goods,

also increases the likelihood of updating the price as it will increase the optimal reset

price and the gap between the reset price and the initial price. A negative taste

shock, by contrast, lowers the optimal reset price and shrinks the gap between that

12

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.20

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Amount Borrowed (Credit Limit)

Val

ue o

f ψ*

Influence of Credit limit on Price Decision, p-1 is 25%

inf -inf +taste -taste +

Figure 1.2: Impact of the amount borrowed on the reservation menu costwhen the initial price is low.

13

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.20

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Amount Borrowed (Credit Limit)

Val

ue o

f ψ*

Influence of Credit limit on Price Decision, p-1 is 50%

inf -inf +taste -taste +

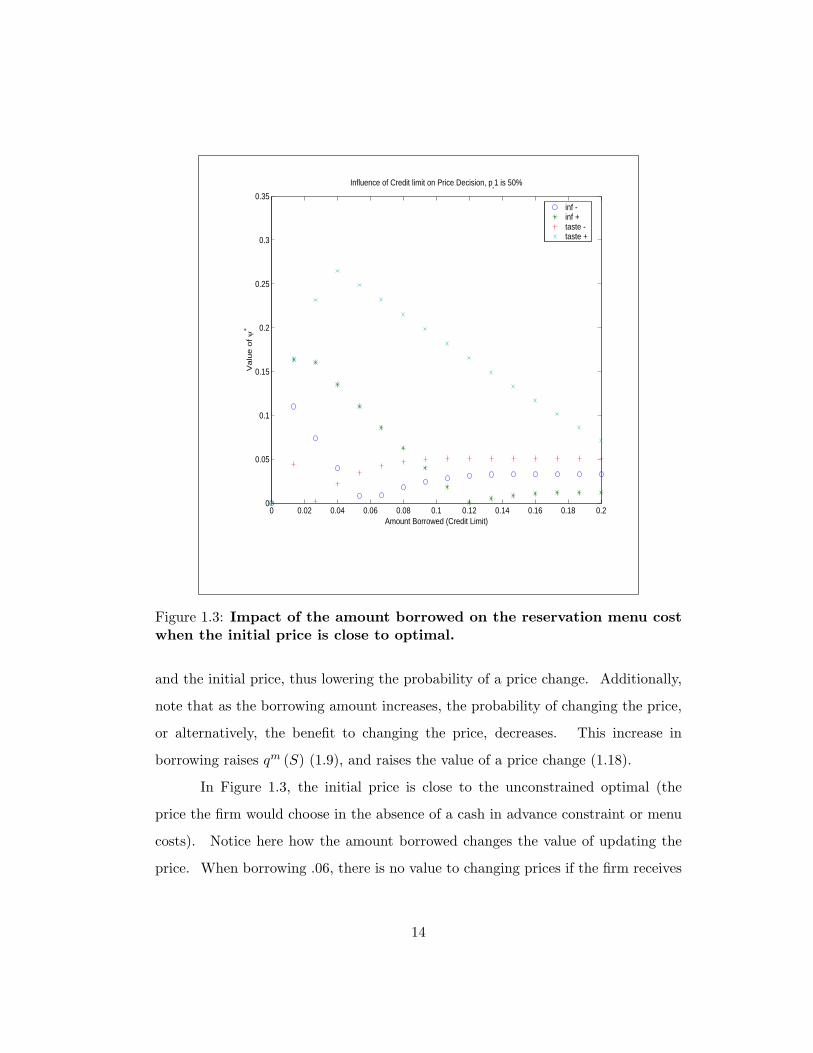

Figure 1.3: Impact of the amount borrowed on the reservation menu costwhen the initial price is close to optimal.

and the initial price, thus lowering the probability of a price change. Additionally,

note that as the borrowing amount increases, the probability of changing the price,

or alternatively, the benefit to changing the price, decreases. This increase in

borrowing raises qm (S) (1.9), and raises the value of a price change (1.18).

In Figure 1.3, the initial price is close to the unconstrained optimal (the

price the firm would choose in the absence of a cash in advance constraint or menu

costs). Notice here how the amount borrowed changes the value of updating the

price. When borrowing .06, there is no value to changing prices if the firm receives

14

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.20

0.02

0.04

0.06

0.08

0.1

0.12

0.14

Amount Borrowed (Credit Limit)

Val

ue o

f ψ*

Influence of Credit limit on Price Decision, p-1 is 75%

inf -inf +taste -taste +

Figure 1.4: Impact of the amount borrowed on the reservation menu costwhen the initial price is high.

a negative inflation shock. This is the ideal amount to borrow with this initial price

for that shock. With a positive inflation shock, the optimal amount to borrow is .12.

The change in the aggregate price level affects the relative price– demand is higher

with an inflation shock because the initial price looks cheaper. More borrowing is

needed to meet this increased demand.

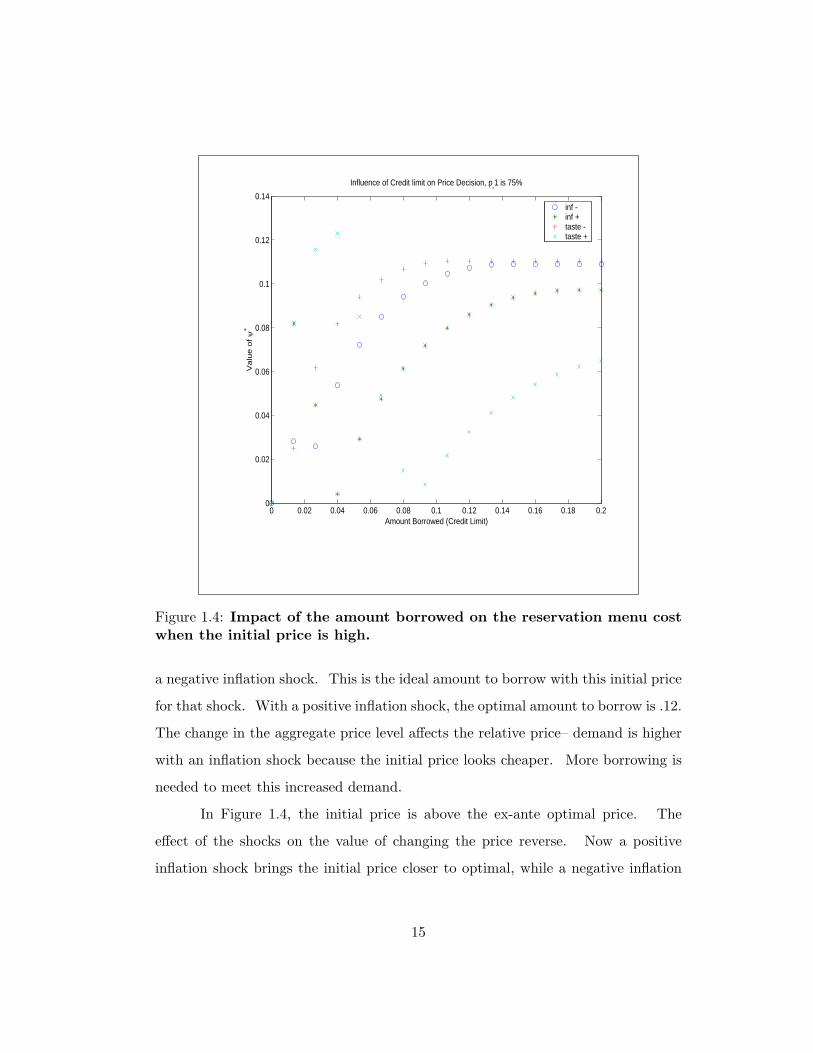

In Figure 1.4, the initial price is above the ex-ante optimal price. The

effect of the shocks on the value of changing the price reverse. Now a positive

inflation shock brings the initial price closer to optimal, while a negative inflation

15

shock moves it further way. A negative taste shock will reduce demand and make

our higher price closer to optimal, while a positive taste shock will do the opposite.

Additionally, borrowing more increases the value of changing price because any

change will be negative. If the firm is lowering its price to increase quantity, it has

to have borrowed enough to produce additional quantity.

Impact of Initial Price on Price Updating Decision

Figures 1.2-1.4 show how the impact that the amount borrowed has on the price

updating decision depends on the initial price. In order to capture the impact

of borrowing in a more systematic way, we can measure the impact of B on Ψ∗

when different constraints are binding. The amount borrowed creates an upper

limit on the quantity of goods that can be produced. This is represented by qm (S)

(1.9). If demand under the optimal unconstrained price is less than qm (S), then the

financing decision will not affect the expected profits in the change case. Similarly,

if demand under the previous price is less than qm (S), then the financing decision

will not affect profits in the no-change case. Thus, the marginal effect of a change

in financing on price adjustment and value needs to be evaluated for four separate

cases.

The borrowing constraint can affect the price and output decision even when

it doesn’t explicitly bind. I define the impact of the constraint as the difference in

the price and output in the realized second period compared to what the price and

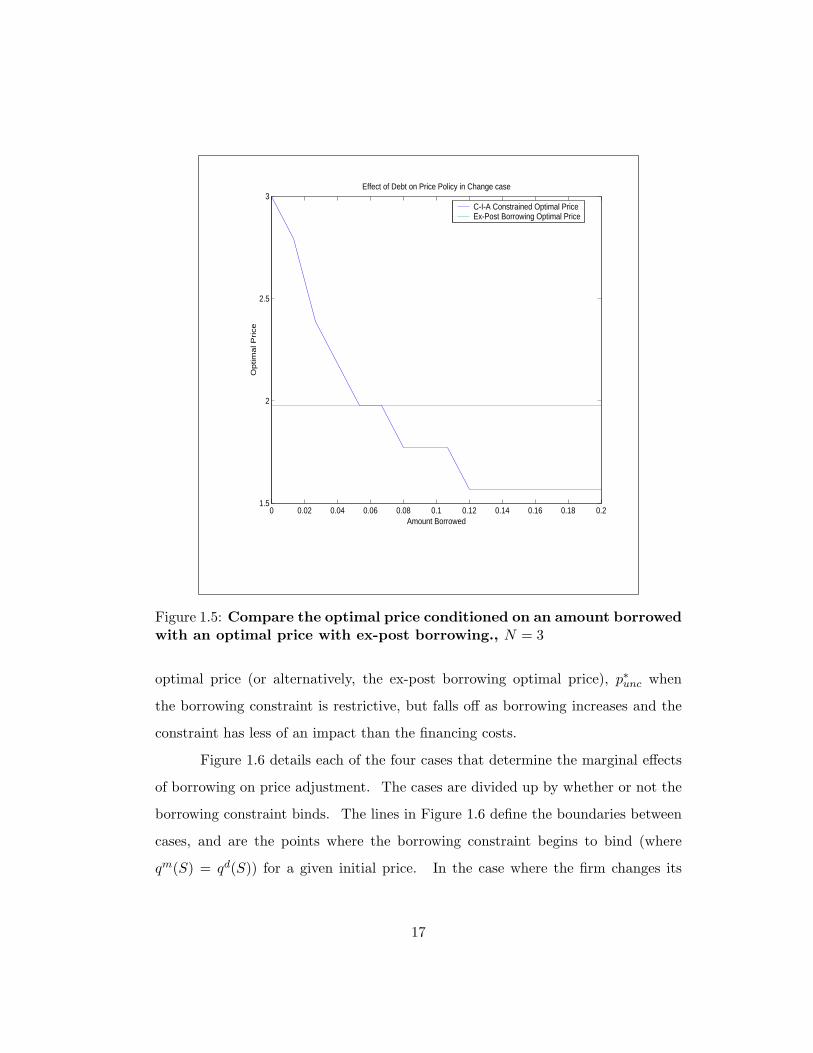

output would have been if the firm had been allowed to borrow ex-post. Figure

1.5 shows how the ex-post and constrained optimal prices differ. Notice how the

constrained price is different from the unconstrained optimal price even when the

borrowing constraint doesn’t explicitly bind. This is due to defining the optimal

price in the second period. At that point, financing costs are fixed, and don’t affect

the marginal cost. Ex-ante, they do matter, so p∗ is higher than the unconstrained

16

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.21.5

2

2.5

3

Amount Borrowed

Opt

imal

Pric

e

Effect of Debt on Price Policy in Change case

C-I-A Constrained Optimal PriceEx-Post Borrowing Optimal Price

Figure 1.5: Compare the optimal price conditioned on an amount borrowedwith an optimal price with ex-post borrowing., N = 3

optimal price (or alternatively, the ex-post borrowing optimal price), p∗unc when

the borrowing constraint is restrictive, but falls off as borrowing increases and the

constraint has less of an impact than the financing costs.

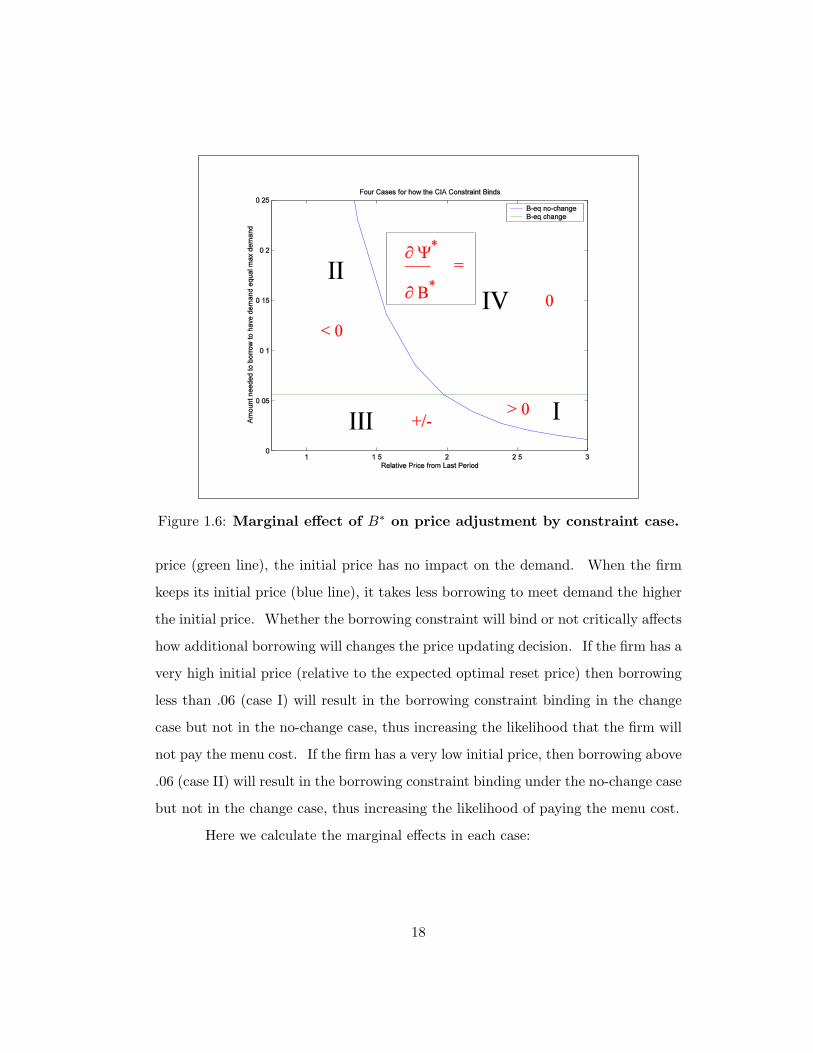

Figure 1.6 details each of the four cases that determine the marginal effects

of borrowing on price adjustment. The cases are divided up by whether or not the

borrowing constraint binds. The lines in Figure 1.6 define the boundaries between

cases, and are the points where the borrowing constraint begins to bind (where

qm(S) = qd(S)) for a given initial price. In the case where the firm changes its

17

Figure 1.6: Marginal effect of B∗ on price adjustment by constraint case.

price (green line), the initial price has no impact on the demand. When the firm

keeps its initial price (blue line), it takes less borrowing to meet demand the higher

the initial price. Whether the borrowing constraint will bind or not critically affects

how additional borrowing will changes the price updating decision. If the firm has a

very high initial price (relative to the expected optimal reset price) then borrowing

less than .06 (case I) will result in the borrowing constraint binding in the change

case but not in the no-change case, thus increasing the likelihood that the firm will

not pay the menu cost. If the firm has a very low initial price, then borrowing above

.06 (case II) will result in the borrowing constraint binding under the no-change case

but not in the change case, thus increasing the likelihood of paying the menu cost.

Here we calculate the marginal effects in each case:

18

Case I: q(p∗unc) > qm (B) , q(p−1) ≤ qm (B)

Ψ∗ (S) = p∗(B

wP

)α

− p−1q(p−1)−B + wPq(p−1)1α

∂

∂BΨ∗ (S) =

∂p∗

∂B

(B

wP

)α

︸ ︷︷ ︸Price Falls

+αp∗

wP

(B

wP

)α−1

︸ ︷︷ ︸Quantity Rises

− 1︸︷︷︸Cost’s Rise

In case I, the borrowing constraint is binding in the change case but not in

no-change case. A firm that has a high initial price and borrows very little will

be in case 1. As the derivative is positive, we see that an increase in the amount

borrowed would increase Ψ∗, increasing the value to a firm of changing its price.

Case II: q(p∗unc) < qm (B) , q(p−1) ≥ qm (B)

Ψ∗ (S) = p∗q(p∗)− p−1

(B

wP

)α

− wPq(p∗)1α +B

∂

∂BΨ∗ (S) = −αp−1

wP

(B

wP

)α−1

+ 1

Case II describes the opposite situation, where the borrowing constraint does

not bind in the change case but does in the no-change case. Here the firm has a

very low initial price and has borrowed a lot. Borrowing more would lower the

value of changing price, as the firm would increase its price if it changes.

Case III: q(p∗unc) > qm (B) , q(p−1) > qm (B)

Ψ∗ (S) = p∗q(p∗)− p−1q(p−1)

∂

∂BΨ∗ (S) =

∂p∗

∂B

(B

wP

)α

+αp∗

wP

(B

wP

)α−1

︸ ︷︷ ︸Change Price

− αp−1

wP

(B

wP

)α−1

︸ ︷︷ ︸No Change

In case III, the constraint binds in both cases. It is unclear what effect an

increase in B would have on Ψ∗.

19

Case IV: q(p∗unc) ≤ qm (B) , q(p−1) ≤ qm (B)

Ψ∗ (S) = p∗q(p∗)− p−1q(p−1)− wP[q(p∗)

1α − q(p−1)

1α

]∂

∂BΨ∗ (S) = 0

Case IV is the unconstrained case. The firm has borrowed enough and has

a high enough initial price that additional borrowing will not affect its decision to

change its price or not.

The table below summarizes the how a change in B∗ (S) affects Ψ∗ through

each price changing scenario:

Table 1.1: Definition of Price Change and Borrowing Cases

Case q(p∗unc) q(p∗−1)

I q(p∗unc) > qm (B) q(p−1) ≤ qm (B)

II q(p∗unc) ≤ qm (B) q(p−1) > qm (B)

III q(p∗unc) > qm (B) q(p−1) > qm (B)

IV q(p∗unc) ≤ qm (B) q(p−1) ≤ qm (B)

Table 1.2: Summary of the Impact of Borrowing on Value

Case ∂∂BC Ψ∗ (θ) ∂

∂BNC Ψ∗ (θ) ∂∂BV (p∗) ∂

∂BV (p−1) ∂∂BV

I ∂p∗

∂B

(B

wP

)α + αp∗

wP

(B

wP

)α−1 − 1 0 + 0 +

II 0 −αp−1

wP

(B

wP

)α−1 + 1 0 + +

III ∂p∗

∂B

(B

wP

)α + αp∗

wP

(B

wP

)α−1 −αp−1

wP

(B

wP

)α−1 + + +/−

IV 0 0 0 0 0

Figure 1.7 shows how the marginal effects of each case change over different

levels of B for a given initial price. We can see that for low levels of borrowing, the

20

0

0.1

0.2

0.3

0.4Overall Effect: ψ* given B

0

5

10

15

ψ*

Marginal Effects: δψ*/δB p* Case

p-1 = 1.36

0 0.02 0.04 0.06 0.08 0.1 0.12 0.14 0.16 0.18 0.2-8

-6

-4

-2

0

Amount Borrowed

Marginal Effects: δψ*/δB p-1 Case

Figure 1.7: Marginal effects of additional borrowing on price adjustmentfor each price case given an initial price level.

change case is made more desirable with additional borrowings, and the no-change

case is made less so. This is consistent with case III, as both derivatives are non-

zero. At a critical amount of borrowing, the change case ceases to be affected by

additional borrowing. At this point, the change case borrowing constraint does

not bind. This is consistent with case II. The first panel of Figure 1.7 shows how

changes in B affect the overall value .

In the top of Figure 1.7 we see how the marginal effect of borrowing on

Ψ∗ changes as borrowings increase. At first it increases, as additional borrowings

21

Figure 1.8: Mapping figure 1.7 back into the constraint space.

make a price change more profitable, but that effect begins to slow, and eventually

stop altogether. The middle and bottom panels decompose the marginal effect into

the change case and the no-change case. The middle panel illustrates the effect

of borrowing on the no-change case. While positive, it quickly falls to zero as

the additional constraint stops binding. In the change case, additional borrowing

actually makes changing the price less desirable, as there are more financing costs to

cover. Figure 1.8 shows the same four-case space again, this time with our chosen

initial price shown explicitly. Figure 1.7 maps into Figure 1.8, as the marginal

effects of each level of borrowing change. Note that as borrowing increases the firm

crosses from case III to case II. The borrowing amount, .06, is the same as where

the no-change effect falls to zero in the middle panel of Figure 1.7.

22

0.5 1 1.5 2 2.5 30.05

0.055

0.06

0.065

0.07

0.075

0.08

Relative Price from Last Period

Bor

row

ing

Dec

isio

n

Optimal Borrowing

Figure 1.9: Optimal borrowing given an inital price level.

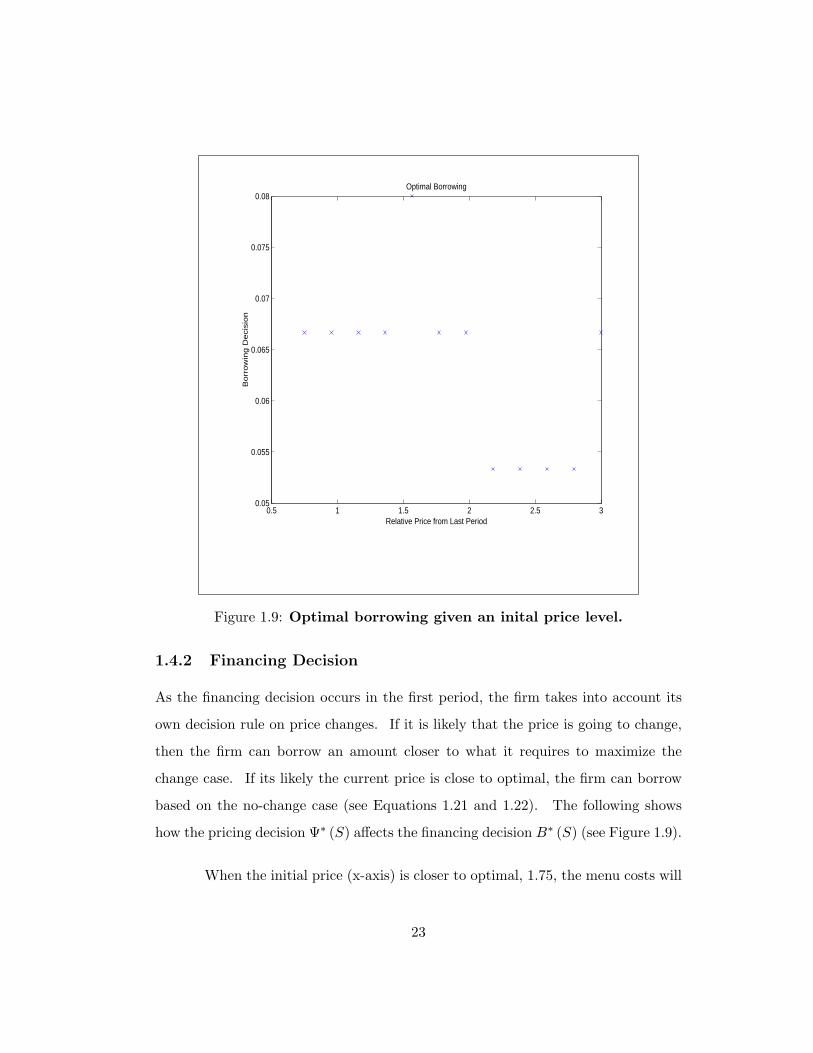

1.4.2 Financing Decision

As the financing decision occurs in the first period, the firm takes into account its

own decision rule on price changes. If it is likely that the price is going to change,

then the firm can borrow an amount closer to what it requires to maximize the

change case. If its likely the current price is close to optimal, the firm can borrow

based on the no-change case (see Equations 1.21 and 1.22). The following shows

how the pricing decision Ψ∗ (S) affects the financing decision B∗ (S) (see Figure 1.9).

When the initial price (x-axis) is closer to optimal, 1.75, the menu costs will

23

outweigh the benefit of changing the price and the firm will adjust its borrowing

to maximize under the initial price. Thus, the firm borrows more when the initial

price is below optimal, 1.5, in order to meet the higher demand. Conversely, they

can borrow less when the initial price is slightly too high, 2.1, to meet lower demand.

This process is limited by the magnitude of the menu cost however, and we can see

it break down at extreme initial price levels, 1 and 3. When the initial price is so

far away from the optimal that updating is a virtual certainty, the initial price has

little effect on borrowing and the firm borrows to maximize under its newly updated

price.

When faced with the borrowing decision, the firm knows the current price

level and its own price. This is enough for the firm to determine how far its current

price will deviate from the optimal price in the next period for each realization

of the shocks. The likelihood of updating the firm’s price is summarized in the

price change policy function. It is an important factor in the borrowing decision

because the optimal amount of borrowing depends on the demand. To see the

mechanism more clearly, separate the borrowing decision into two policy functions,

each conditional on a particular price updating strategy:

B∗C (S−1) = max{B}

∫S

ΠC (p, q, S) dS (1.21)

B∗NC (S−1) = max{B}

∫S

ΠNC (q, S) dS (1.22)

B∗C (S−1) is the optimal amount to borrow if the firm was changing its price

for sure, B∗NC (S−1) the amount if the firm was definitely not going to change its

price.

Now divide the second period into two states defined by the relative size of

the optimal amount to borrow for each price change scenario. If the initial price is

very low, a decision to raise it will reduce demand and require less borrowing. If

24

the initial price is very high, updating it will increase demand, and necessitate more

borrowing. Define these two situations as cases 1 and 2:

Case 1: B∗C (S−1) < B∗NC (S−1) (1.23)

Case 2: B∗C (S−1) ≥ B∗NC (S−1) (1.24)

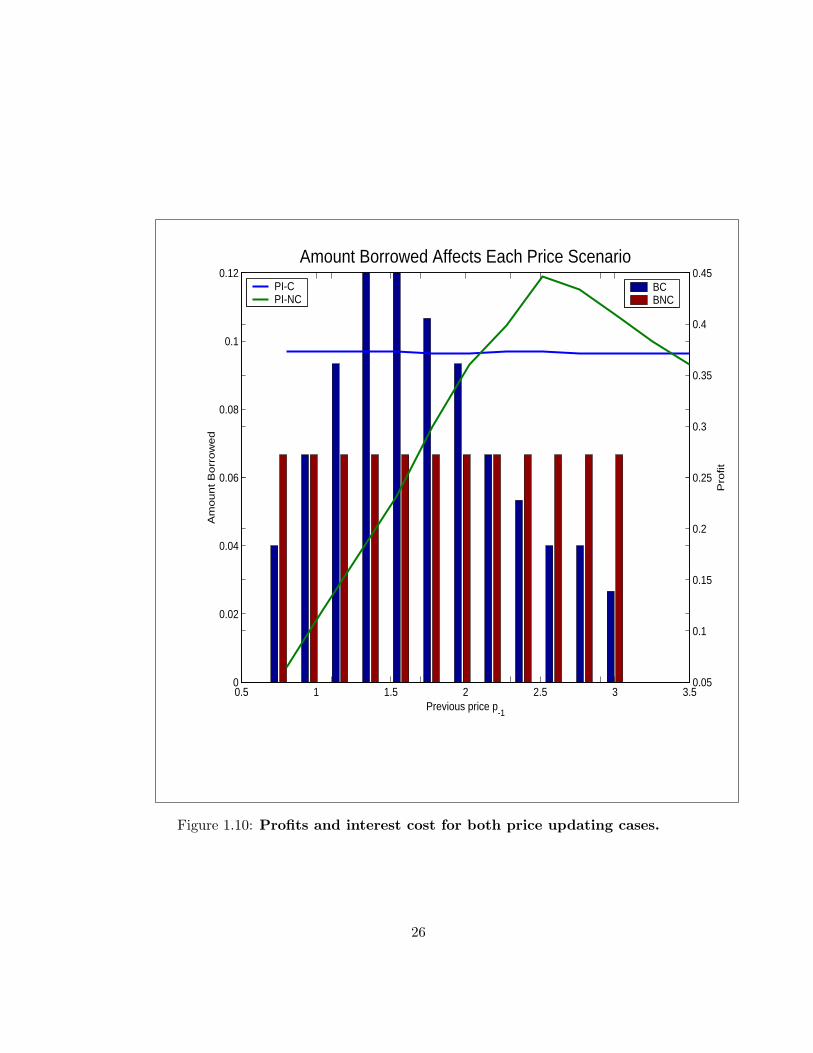

There are two channels through which the price change affects the borrow-

ing decision: the benefit of relaxing a binding cash-in-advance constraint, thereby

allowing supply to be optimal, and the cost of paying interest on the borrowing. In

case 1, these two channels reinforce each other; changing the price will move the firm

closer to first-best profits and also mean less borrowing and interest costs. In case

2, the two channels are at odds, as changing the price will yield greater efficiency

but also increased borrowing costs. Figure 1.10 illustrates these two mechanisms

across different values of the initial price.

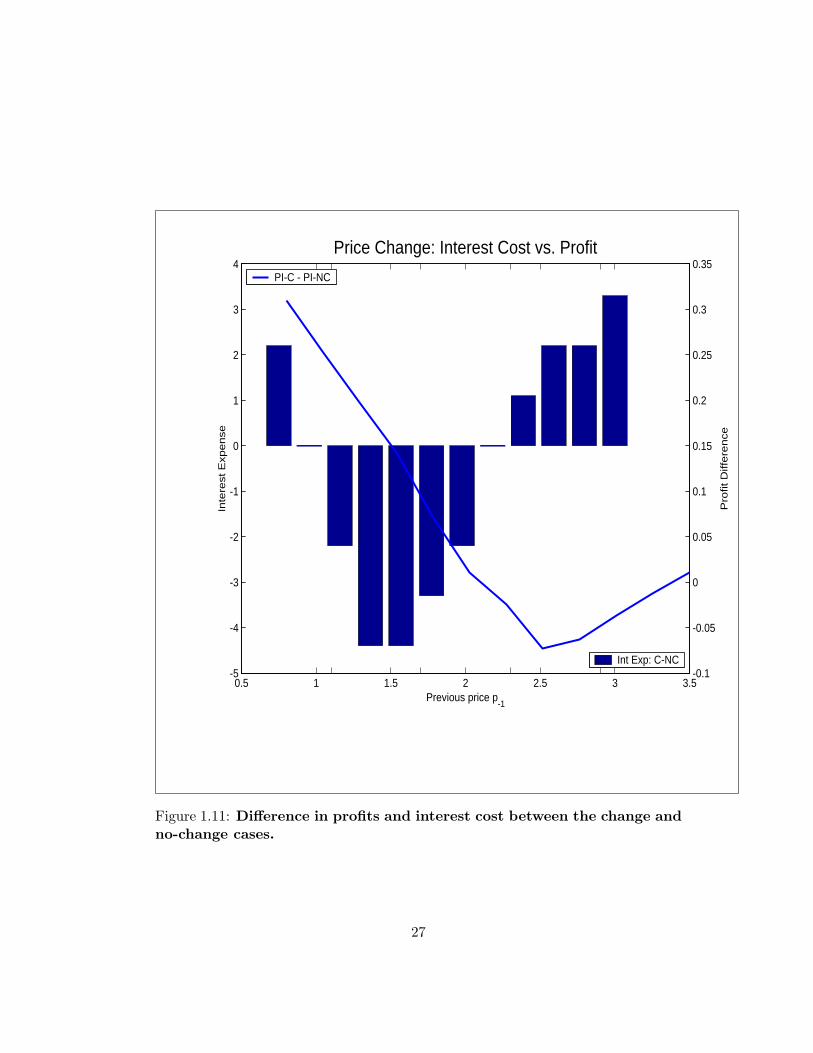

If we think of the reservation menu cost as the amount of inefficiency the

firm will accept before changing its price, then an increase in Ψ∗ tilts the borrowing

more towards the no-change optimum.

∂

∂Ψ∗B∗ (S−1) =

Case Interest Optimal Net Effect

1 − + +

2 − − −

Figures 1.11 illustrates the net effect.

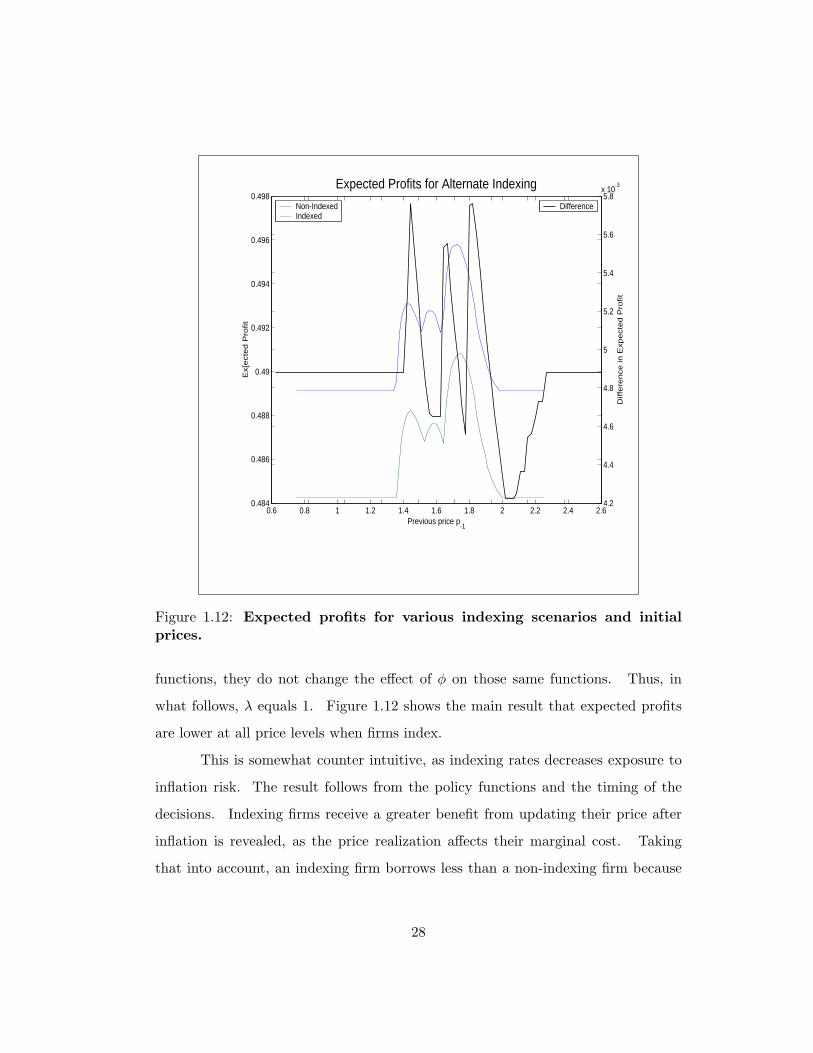

1.4.3 Indexing Effects

We are now ready to consider the effects of indexing costs to inflation. If firms

choose to set φ greater than zero, then the interest rate will rise and fall with

inflation. Changes in λ, the wage indexation, were also considered but did not

affect the results presented here. While changes in λ impact profits and the policy

25

0.5 1 1.5 2 2.5 3 3.50

0.02

0.04

0.06

0.08

0.1

0.12

Previous price p-1

Am

ount

Bor

row

ed

BCBNC

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

Pro

fit

Amount Borrowed Affects Each Price ScenarioPI-CPI-NC

Figure 1.10: Profits and interest cost for both price updating cases.

26

0.5 1 1.5 2 2.5 3 3.5-5

-4

-3

-2

-1

0

1

2

3

4

Previous price p-1

Inte

rest

Exp

ense

Int Exp: C-NC-0.1

-0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

Pro

fit D

iffer

ence

Price Change: Interest Cost vs. ProfitPI-C - PI-NC

Figure 1.11: Difference in profits and interest cost between the change andno-change cases.

27

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60.484

0.486

0.488

0.49

0.492

0.494

0.496

0.498

Previous price p-1

Ex[

ecte

d P

rofit

Non-IndexedIndexed

4.2

4.4

4.6

4.8

5

5.2

5.4

5.6

5.8x 10-3

Diff

eren

ce in

Exp

ecte

d P

rofit

Expected Profits for Alternate IndexingDifference

Figure 1.12: Expected profits for various indexing scenarios and initialprices.

functions, they do not change the effect of φ on those same functions. Thus, in

what follows, λ equals 1. Figure 1.12 shows the main result that expected profits

are lower at all price levels when firms index.

This is somewhat counter intuitive, as indexing rates decreases exposure to

inflation risk. The result follows from the policy functions and the timing of the

decisions. Indexing firms receive a greater benefit from updating their price after

inflation is revealed, as the price realization affects their marginal cost. Taking

that into account, an indexing firm borrows less than a non-indexing firm because

28

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60.46

0.48

0.5

0.52

0.54

0.56

0.58

Previous price p-1

Rea

lized

Pro

fit

Non-IndexedIndexed

0.055

0.06

0.065

0.07

0.075

0.08

Diff

eren

ce in

Pro

fit

Realized Profits for Alternate Indexing (Inflation Shock)Difference

Figure 1.13: Realized profits for each indexation scenario when the tasteshock is zero and the inflation shock is positive.

it is less concerned about a low nominal price (1.24). This becomes a self fulfilling

result after price levels are realized. If inflation is positive, the indexed firm will

either have to change prices or produce less, because it did not borrow as much as

the non-indexing firm. Indexing firms manage their exposure to shocks by changing

price, whereas non-indexed firms manage these shocks by borrowing more.

To understand this result more clearly, consider the how each indexation

scenario preforms under the case of a positive inflation shock.

Figure 1.13 shows how the non-indexing firm does much better than the

29

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60.42

0.43

0.44

0.45

0.46

0.47

0.48

0.49

0.5

0.51

Previous price p-1

Rea

lized

Pro

fit

Non-IndexedIndexed

-0.07

-0.065

-0.06

-0.055

-0.05

-0.045

Diff

eren

ce in

Pro

fit

Realized Profits for Alternate Indexing (Deflation Shock)Difference

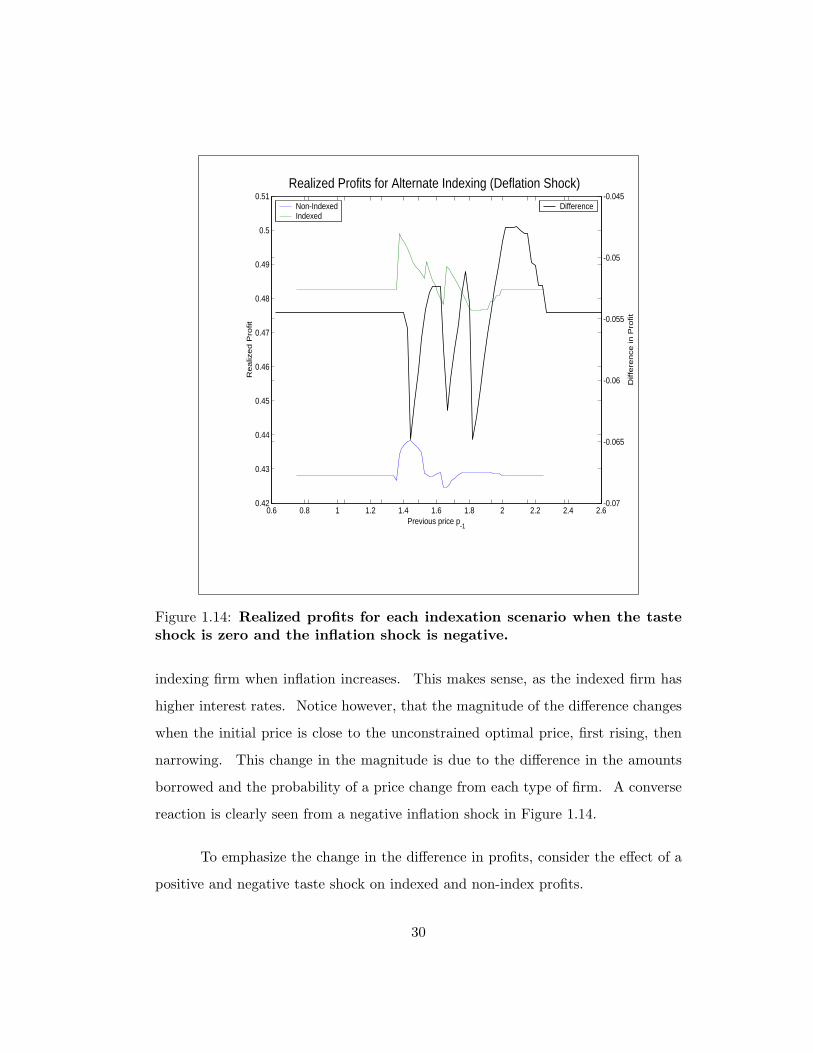

Figure 1.14: Realized profits for each indexation scenario when the tasteshock is zero and the inflation shock is negative.

indexing firm when inflation increases. This makes sense, as the indexed firm has

higher interest rates. Notice however, that the magnitude of the difference changes

when the initial price is close to the unconstrained optimal price, first rising, then

narrowing. This change in the magnitude is due to the difference in the amounts

borrowed and the probability of a price change from each type of firm. A converse

reaction is clearly seen from a negative inflation shock in Figure 1.14.

To emphasize the change in the difference in profits, consider the effect of a

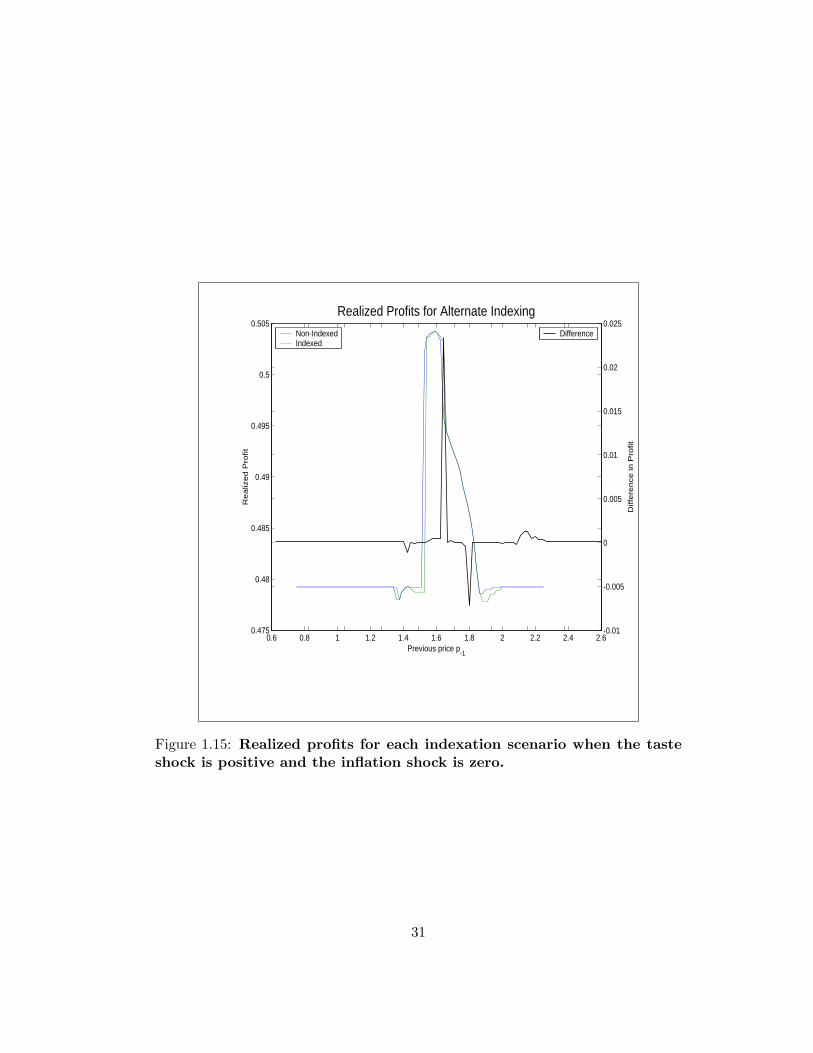

positive and negative taste shock on indexed and non-index profits.

30

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60.475

0.48

0.485

0.49

0.495

0.5

0.505

Previous price p-1

Rea

lized

Pro

fit

Non-IndexedIndexed

-0.01

-0.005

0

0.005

0.01

0.015

0.02

0.025

Diff

eren

ce in

Pro

fit

Realized Profits for Alternate IndexingDifference

Figure 1.15: Realized profits for each indexation scenario when the tasteshock is positive and the inflation shock is zero.

31

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.6

0.503

0.5035

0.504

0.5045

Previous price p-1

Rea

lized

Pro

fit

Non-IndexedIndexed

-1.5

-1

-0.5

0

0.5

1

1.5x 10-3

Diff

eren

ce in

Pro

fit

Realized Profits for Alternate IndexingDifference

Figure 1.16: Realized profits for each indexation scenario when the tasteshock is negative and the inflation shock is zero.

Figure 1.15 shows the impact of a demand shock without a corresponding

change in indexed interest rates. This eliminates the large but fixed cost associated

with a higher interest rate bill. There is still a difference in profits right around the

critical optimal reset price, though it slightly favors the non-indexing firm. When

the price is close to the optimal reset price, the non-indexing firm borrows more,

which is an advantage under a positive demand shock. When the taste shock in

negative, as in Figure 1.16, the reverse is true, and the indexing firm does better.

The following example illustrates the asymmetry that leads the non-indexing

32

firm to higher profits. Firm I indexes its financing, while Firm N does not. Firms I

and N have the same initial price in period 1, which is lower than their ex-ante opti-

mal price. When considering how much to borrow, each firm assesses the likelihood

of changing its price. Figure 1.17 illustrates the differences in their assessment.

In the case of positive inflation, the firms have almost identical reservation menu

costs. The positive inflation shock exacerbates the gap between their initial price

and optimal price, and both firms will likely update their price. The case of a

negative inflation shock leads to a much different result. Firm I is willing to pay

a much higher menu cost to update its price. Because its financing is indexed, the

deflation changes the firm’s optimal reset price, moving it further from the initial

price. The deflation has no effect on Firm N’s as its optimal reset price as it is

independent of the price level. The deflation shock merely shrinks the gap between

its initial price and the optimal reset price.

After assessing the likelihood of updating their prices, the firms choose an

amount to borrow. This amount can be thought of as the weighted average of the

amount the firm would borrow if it were certain it was going to change its price and

the amount it would borrow if it were certain it would leave the price unchanged

(see Equations 1.21 and 1.22). Firm I is more certain that it will update its price,

so the amount it borrows will be more heavily weighted to B∗C . Since the initial

price is lower than the ex-ante optimal price, borrowing case 2 applies. In case 2,

B∗C is less than B∗NC , and any change in price will be an increase and will lower

the quantity demanded. Thus, Firm I borrows less than Firm N in this case.

Having made their borrowing decisions, the firms move into the second pe-

riod. In the case of positive inflation, both firms change their price and meet

demand. In that scenario, it is unclear who profits more. Firm I borrowed less

overall, but pays a higher interest cost due to the inflation. If there is negative

inflation, Firm I pays the menu cost and changes its price before Firm N. Firm I is

33

0.6 0.8 1 1.2 1.4 1.6 1.8 2 2.2 2.4 2.60.4

0.5

0.6

0.7

0.8

0.9

1

Relative Price from Last Period

Pro

babi

lity

of C

hang

ing

Pric

e

Probability of Changing Price for Various Indexing Scenarios

Non-Indexed BorrowingsIndexed Borrowings

Figure 1.17: Expected reservation menu cost for various indexing scenariosand initial prices.

more borrowing constrained than Firm N, and its optimal reset price is increasing.

In this case, Firm N comes out ahead, as it pays the menu cost less frequently.

Summing over all the states, it’s clear that the non-indexed firm is more profitable

than the indexed firm. The non-indexed interest rate helps affects the borrowing

decision by reducing the benefit to changing price and keeps the optimal reset price

fixed over both periods. The same asymmetries that drive the above example are

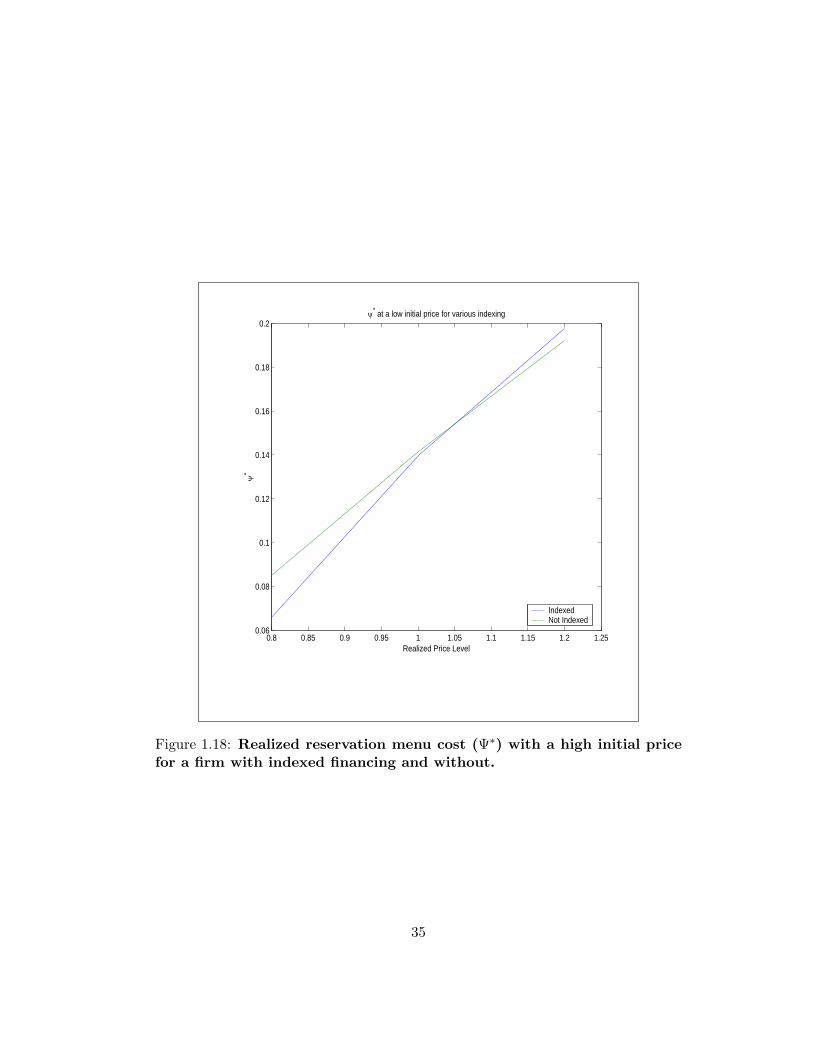

present in a situation where the initial price is higher than the optimal rest price

(see Figure 1.18).

34

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15 1.2 1.250.06

0.08

0.1

0.12

0.14

0.16

0.18

0.2

Realized Price Level

ψ*

ψ* at a low initial price for various indexing

IndexedNot Indexed

Figure 1.18: Realized reservation menu cost (Ψ∗) with a high initial pricefor a firm with indexed financing and without.

35

0.8 0.85 0.9 0.95 1 1.05 1.1 1.15 1.2 1.250.04

0.05

0.06

0.07

0.08

0.09

0.1

0.11

0.12

Realized Price Level

ψ*

ψ* at a high initial price for various indexing

IndexedNot Indexed

Figure 1.19: Realized reservation menu cost (Ψ∗) with a low initial pricefor a firm with indexed financing and without.

36

1.5 Conclusion

This paper presents a model of the firm that incorporates state dependent pricing

and a cash-in-advance constraint. This simple framework illustrates how these two

inefficiencies work together to violate the irrelevance proposition and make a firm’s

financing an important factor in determining value.

I show that the cash-in-advance constraint affects both the price updating

decision and the optimal price if the optimal price in either the no-change or the

change case would require additional borrowing. In some cases this influenced the

new optimal price even when the cash-in-advance constraint didn’t appear to be

binding.

Additionally, I show that the type of interest rates alone affect price updating

behavior as well as expected profits. Firm’s paying interest rates indexed to infla-

tion borrowed less and updated their price more frequently, earning lower expected

profits. Financing costs under non-indexed rates move with inflation based demand

shocks. This allows firms to change prices more efficiently and earn higher expected

profits. These results depend critically on the assumption of positive menu costs.

If a firm could change its price costlessly, then there wouldn’t be an advantage to

borrowing at nominal rates.

As a next step in this investigation, I would like to estimate the nature of

the relationship between price stickiness and the degree of indexation in a firm’s

capital structure. I would expect to find the firms that change their price relatively

infrequently would have a high degree of indexation in their capital structure.

37

Appendix A. Parameter ValuesFor the policy functions shown in the paper the following parameter values

were used:

α

γ

β

Ψ

D

w

µ

P−1

rF

λ

φ

=

0.5

1.9

.99

[0, 0.025]

1

.75

(.5, 1.5)

1

0.2

{0, 1}

{0, 2}

description:

Returns to scale

Price elasticity

Discount rate

Menu cost

Money Balance (hh)

Real Wage

Taste shock

Initial price level

Risk Free Rate

Amount Indexing

Interest Rate Indexing

38

Chapter 2

Asset Prices and Money in a

Two-Period Equilibrium

2.1 Introduction

Observers of public securities markets have often documented a level of price volatil-

ity that is much higher than justified by our current understanding of fundamental

value. In attempting to explain this anomaly, liquidity demands have frequently

been proposed as an explanation. If every trade were motivated by new information

about the fundamental value of an asset, we would expect much smaller moves in the

price. However, if some of the trades were motivated simply by a desire to convert

the asset into consumption, price fluctuations could be explained by differences in

agents’ desire to consume or save at a specific point in time.

This paper uses a Diamond and Dybvig (1983) style liquidity model to show

how the money supply relative to the supply of productive assets can affect asset

prices and asset price volatility. The model shows that higher levels of money

relative to assets will result in lower volatility for the price of the asset.

The link between asset price volatility and liquidity has been approached

39

using several modeling techniques. One method of obtaining excess volatility and

increased risk premium is to assume a fixed cost of participation. Models utilizing

this have linked market liquidity to both high and low levels of volatility. Pagano

(1989) uses participation costs to create endogenously thin markets. The thinness

of the market contributes to volatility though the number of agents. The fewer

the number of agents, the greater the impact of idiosyncratic liquidity shocks. The

expected increase in volatility due to idiosyncratic shocks feeds back into the par-

ticipation decision, multiplying the impact of an initial shock on volatility. Orsel

(1995) uses a similar model to Pagano but generates an increase in volatility due to

participation. In his model, the marginal participant only enters after observing a

positive signal about returns. This agent will have the highest cost to participate,

so will accept the largest liquidity cost. Thus, increased participation is correlated

with high level of volatility. Dubra and Herrera (2001) generates a similar result,

using the marginal risk aversion of the agent instead of a signal.

Allen and Gale (1994) model asset price volatility using a Diamond and

Dyvbig style asset market. They introduce a fixed cost of participation to buy the

illiquid asset and uncertainty about the payoff of the asset. The Allen and Gale

model is remarkable in its ability to generate liquidity-based asset price volatility

without the use of thin markets, as in Pagano. At all times, assets and money are

costlessly exchanged. The changes in the level and volatility of the price are driven

solely by agents’ evolving demand for liquidity.

This paper follows the Allen Gale approach of assuming thick markets with

two innovations. First, while I include a liquidity demand shock as in Diamond

and Dyvbig, I also add a supply shock that alters the total supply of money in the

second period. This shock is known to agents in the initial period. I conclude

that shocks to the money supply increase the mean price level of the asset, and

decrease the price volatility. Secondly, I simplify the model by removing the fixed

40

cost of participation. While this innovation has been used to generate excessive risk

premia, I show that it is not necessary to establish the interaction between liquidity

and price volatility in this framework.

In the model, the volatility of the asset price is determined by the relative

value of the liquidity price of the asset, which is determined by the relative supply

of money and the asset at a point in time, and the fundamental value price of

the asset, which is determined by its return if held to maturity. If the liquidity

price is uncertain, the distribution of expected realizations of the price will have

an upper bound at the fundamental value; no one holding money would take a loss

for the privilege of holding the asset. The more of the liquidity price distribution

is truncated by the fundamental value price, the lower the overall volatility of the

price.

Section two presents the household problem in general terms and defines an

equilibrium. Section three derives explicitly policy functions to solve the household

problem and satisfy the equilibrium conditions. Section four utilizes comparative

statics to address the impact of liquidity on asset prices, demand and volatility.

Section five concludes.

2.2 Model

The model follows a simplified version of the Allen Gale portfolio problem. House-

holds face a choice in the initial period of allocating wealth between two assets,

while under uncertainty about which of the remaining two periods they will need to

consume. The model solution is partial equilibrium in the sense that its scope is

limited to the choice of asset allocation; I abstract from specific consumption and

production processes. The liquid asset (money, m) yields no return but can be used

for consumption in either the first or second period. The illiquid asset (“the asset”,

a) yields a positive real return (r), but is only realized in the second period. Money

41

is assumed to be the numeraire good, with consumption denominated in terms of

money. This allows us to avoid a separate aggregate price level between goods and

money. The only price in the model relates to the exchange between money and

assets. Agents face both idiosyncratic and aggregate uncertainty about whether

they are will be early or late consumers. Their liquidity needs will be determined

by an individual draw of a random variable λ. The distribution of λ is partially

revealed; the standard deviation is known, but the mean of the distribution is itself

a random variable (ν). This compound uncertainty creates both idiosyncratic risk

for a consumer about his or her demand timing, and also creates aggregate uncer-

tainty about fraction of total consumers who will consumer early or late. In the

first period, after the liquidity preference shock is revealed, there is a market for

early consumers to sell illiquid assets to late consumers. The aggregate uncertainty

about the distribution of λ creates uncertainty about the market clearing price of

the asset in the first period.

2.2.1 Timing and Uncertainty

t = 0 1 2

a −1 → 1 + r

m1 −1 ε

m2 −1 1

(2.1)

The diagram in (2.1) outlines the performance of each asset by period. Both

money and the asset require an initial outlay of wealth to produce each type of asset.

In the case of money, the initial investment is returned in the first period, where

it can be either reinvested until the second period (in the case of a late consumer)

or consumed (in the case of the early consumer). The proportional money supply

shock, ε, adds money to the initial balance of each consumer at the beginning of the

first period. The asset is more illiquid; after being purchased in the initial period, it

42

cannot be consumed in the first period. However, the asset returns all of the initial

investment in the second period plus the return r.

In the initial period, households make their allocation decision without know-

ing their liquidity preference. This allocation is accomplished through a constant

returns to scale process for both the money and the asset. Thus, the total supply

of money and the asset is determined by the agents’ initial period assessment of

their individual liquidity needs. The liquidity shock is revealed in the first period,

after which the agents attempt to reallocate between money and the asset. Con-

sumption occurs after that reallocation in the first period for early consumers. Late

consumers wait until the second period when the asset and its return converts to

consumption.

The liquidity shock creates both idiosyncratic and aggregate uncertainly. For

household i, the liquidity preference is determine by its draw of λi :

if λi ≥ 0, z = 1

if λi < 0, z = 0

λi is drawn from a normal distribution, where the standard deviation is known to

the households but the mean is not:

λ ∼ N (υ, σ) (2.2)

v ∼ N (ν, 1) (2.3)

The expected mean of the liquidity preference distribution, ν, is know to the con-

sumers in the initial period. Similarly to ε, it will act as a policy parameter and

define the space over which we investigate the changes to the price of the asset and

the volatility of that price.

43

2.2.2 Household Problem

The household essentially faces an optimal insurance problem. If a late consumer

knew his type in the initial period, he would allocate all his wealth to the asset and

earn the superior return. An early consumer would allocate all his wealth to money,

as the asset would be worthless to him. Thus, an allocation to money is insurance

against early consumption. This feature matches a critical aspect of liquidity in

general; the value of liquidity is the ability to access wealth at any time, without

necessarily knowing ahead of time if it will be needed. The premium agents pay

for this insurance is the opportunity cost of a higher return on the less liquid asset.

Stated formally, the household solves the following problem:

V (wi, ε, v, r) = maxci1,ci2

Ez,λ [u (ci1, ci2)] s.t. (2.4)

ci1 ≤ mi0ε+mi1 (2.5)

ci2 ≤ mi0ε+mi1 + (1 + r) (ai0 + ai1) (2.6)

wi ≥ mi0ε+ p0ai0 (2.7)

p1ai1 −mi1 = 0 (2.8)

ai0,mi0ε ≥ 0; ai1 ≥ −ai0, mi1 ≥ −mi0ε, (2.9)

The household attempts maximizes its total utility in each allocation period.

In the first period, it chooses ci1 and ci2 knowing there is a chance it could consume

either early or late.

u (ci1, ci2) =

u (ci1) if z = 1

u (ci2) if z = 0

(2.10)

This choice is subject to a cash-in-advance constraint for each consumption

period (2.5, 2.6) and a budget constraint for each period (2.7, 2.8). Additionally, I

impose a restriction on short selling and net borrowing (2.9).

44

In order to get some meaningful intuition on the comparative statics, and to

attempt a more rigorous answer to the questions posed by the paper, I assume the

following quadratic form to the utility function:

u (c) = c− b

2c2 (2.11)

Any well behaved utility function (continuous, differentiable, u′ (·) > 0,

u′′ (·) < 0) will yield similar results.

2.2.3 Market Clearing

As in the Allen Gale model, the allocation decision in the initial period is actually

a production decision, as agents transform wealth into money and the asset. This

process endogenizes the entire of supply of assets and money in the initial period.

The money supply shock, ε, is applied to balances in the first period, but known to

the agents in the initial period.

∑i

ai = A; ε ·∑

i

mi = M (2.12)

First period market clearing involves only a subset of the total supply of

money and assets. Late consumers who hold assets and early consumers who hold

money will not offer them for exchange as the assets will be held and consumed,

respectively. Thus, the first period market is made up of assets held by early

consumers and money held by late consumers. The proportion of each type can be

determined from the realization of the mean of the λ distribution (ν)

z∗ = Pr(λi ≥ 0|ν = ν) (2.13)

z∗ informs the fraction of total assets and money that are being traded in

45

period 1.

∑i

p1aEi =

∑i

mLi

z∗p1A = (1− z∗)M (2.14)

Its not strictly correct to say that p1 will clear the market for assets in period

1. There are several corner solutions where the market does not clear. In period

1, the asset has a guaranteed return of 1 + r in the next period. Those selling the

asset will be unable to charge more than 1 + r for it no matter how strong the

demand is for late consumption. That is, p1 will be the lesser of either the market

clearing price. or 1 + r. This difference between the market clearing price, which

I referred to in the introduction as the liquidity price, and the true value of the

asset, the fundamental value price, drives the volatility result. If those prices are

close together in expectation, the distribution of the liquidity price will be truncated

more severely than if they’re further apart. The more the distribution is limited,

the lower the volatility.

2.2.4 Equilibrium

Define a set of parameters S = {w, ε, v, r} . An equilibrium for this model is defined

as a series of policy functions a0 (S) , m0(S), aE1 (p1) , mE

1 (p1) , aL1 (p1) , mL

1 (p1)

that solve the household problem (2.4) subject to the constraints (2.5-2.9) and a

price, p1, that clears the market in period 1 (2.14). The next section will use the

assumed functional form of demand to develop a solution for the equilibrium, and

derive expressions for the expected price and volatility of the first period asset.

46

2.3 Solving the Model

The household faces two sequential decisions, with the second depending critically

on the first. The solution to the household’s problem begins in the first period

and works back to the initial allocation. In what follows, I have dropped the ”i”

subscripts on the policy functions, as the only difference between consumers is their

ex-post type, which is labelled where appropriate.

2.3.1 First period (t = 1)

At the beginning of the first period, the household has already allocated its wealth

between money and assets. At the time of the allocation, the household did not

know if it would be an early or late consumer; liquidity preference is revealed at

the start of the first period. Thus, while in the initial period our agents were

homogenous, the first period sorts them into two groups, early and late consumers,

who each solve a separate problem.

Early Consumer

Early consumers experience utility from consuming in the first period, but none

from consuming in the second, when the asset pays off.

u(c1, c2; z = 1) = maxa1,m1

1 · u(c1) + 0 · u(c2)

c1 ≤ m0ε+m1

c2 ≤ m1 + (1 + r) (a1 + a2)

Thus, the early consumer will want to exchange his asset holdings for money in

order to maximize his current period consumption and overall utility. Substituting

the first period budget constraint (2.7), which we can assume will bind, into the

household problem (2.4), the early consumer will have the following demand for

47

money and assets:

mE∗1 = p1a0 (2.15)

aE∗1 = −a0 (2.16)

The market will always clear for the early consumer, as they will accept any

price for their initial asset allocation.

Late Consumer

Late consumers experience utility from consuming in the second period, when the

asset pays off and returns the initial investment plus the return in terms of con-

sumption. In the first period, upon learning that they are late consumers, these

households no longer have a need to insure against early consumption, and would

like to put the wealth that they allocated towards money in the initial period (m0)

to a more productive use, i.e., buy the asset. Rewriting the early consumer problem

to account for z = 0 :

u(c1, c2; z = 0) = maxa1,m1

0 · u(c1) + 1 · u(c2) (2.17)

c1 = m0ε+m1 (2.18)

c2 = m0ε+m1 + (1 + r) (a0 + a1) (2.19)

The late consumers problem is slightly more complex than the early consumer’s.

By substituting the second period budget constraint (2.8) into (2.19), we can write

48

the late consumers problem as a Lagrange maximization:

L(a,m, µ) = maxa1

m0 − p1a1 + (1 + r) (a0 + a1)− µ [m0ε− p1a1]

FOC :∂L

∂a1: −p1 + (1 + r) + µp1 = 0

µ : m0ε− p1a1

µ [m0ε− p1a1] ≤ 0

Unlike the early consumers, for whom the allocation to assets in the initial period

is now worthless if the hold onto it, late consumers value their money holdings to

the extent they can hold them until the second period. Where the early consumers

would accept any p1 ≥ 0, late consumers are only willing to pay p1 ≤ 1+r, the price

where they are indifferent between holding money and the asset. That is, when the

liquidity price is less than or equal to the fundamental value price.

Case 1: p1 ≤ 1 + r , µ > 0 (2.20)

Case 2: p1 > 1 + r , µ = 0 (2.21)

Therefore, the demand for the asset depends on the price:

aL∗1 =

m0εp1

if µ > 0

0 if µ = 0

(2.22)

Thus, by the first period budget constraint (2.7):

mL∗1 =

−p1a1 if µ > 0

0 if µ = 0

(2.23)

49

Market Clearing

Early consumers are natural buyers of money, late consumers will demand assets

as long as the price is not above the fundamental value of the asset, 1 + r. From

the market clearing condition (2.14) we can derive an expression for the first period

price:

p1 = min{

1− z∗

z∗M

A, 1 + r

}(2.24)

The late consumers each demand aL∗1 . They are willing to exchange all of the

money holdings, and there are a total of 1−z∗ of them. Conversely, early consumers

each demand mE∗1 , and there are z∗ of them (2.15 and 2.13). The distribution of

the expected realization of p1 in period 0 will be negatively skewed, as any value of

z∗ that yields a price above 1 + r will be truncated to 1 + r. For every realization

of the shock where the true value dominates, the price equals the true value. This

discrete choice drives the key result that volatility decreases as liquidity increases.

The more states yield market clearing prices above 1 + r, the more the distribution

is truncated, and the lower the volatility.

2.3.2 Initial Period

In contrast to the first and second periods, agents in the initial period do not know

whether they will be consuming earlier or later, and thus all face the same prob-

lem. Agents solve the household allocation problem by taking expectations over the

probability of drawing an early or late liquidity preference and the expected mean

of that distribution.

2.3.3 Household Problem

Rewrite the household problem (2.4) after substituting in the demand functions

from the first period (2.15, 2.22). As each consumption period is exclusive to the

50

other, c1 is optimized assuming an early liquidity preference, c2 assuming a late

liquidity preference.

V (wi, ε, v, r) = maxc1,c2

∫ν

∫λ[λu (c1) + (1− λ)u (c2)] dλdν (2.25)

c1 = m0ε+mE∗1 (p1) (2.26)

c2 = (1 + r)(a0 + aL∗

1 (p1))

if µ > 0 (2.27)

c2 = (1 + r) a0 +m0ε if µ = 0 (2.28)

Substituting in the budget constraint (2.7), the expectation of p1 (2.24) and

the specific demand functions in for c1 and c2 yields the following first order condition

for each λi and υ realization:

∂V

∂a0: −λ (1− p1)u′ (c1) + (1− λ)u′ (c2) (1 + r)

(1− 1

p1

)= 0 (2.29)

If we assume quadratic utility (2.11), demand in the initial period is a function of

the parameters and the shocks:

a∗0 = g (wi, ε, v, r) (2.30)

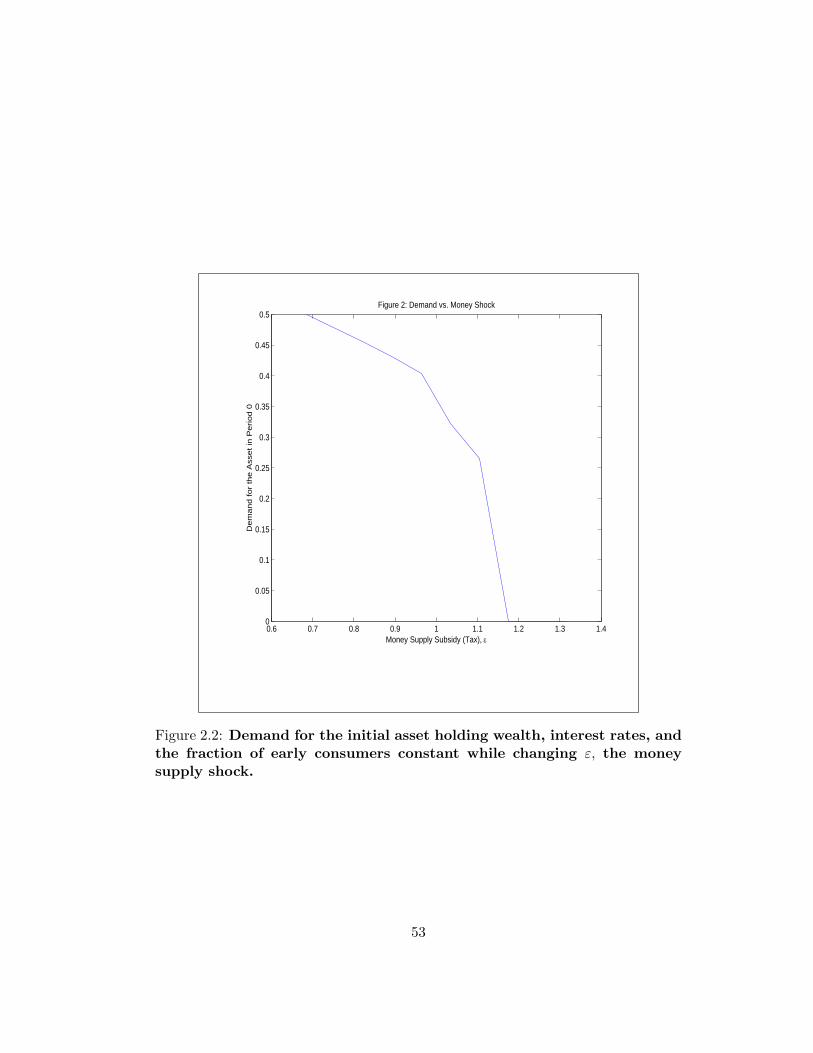

Figure’s 2.1 and 2.2 show how demand for the asset changes with the expected

fraction of early consumers and with the money shock.

Demand for the asset falls off as liquidity demand increases, as agents find

money to be more valuable relative to the asset as the chance of consuming early

increases. As the money shock increases, the return for owning money increases

and eventually overtakes the return on the asset. Hence zero demand for the asset

when ε is above 1.17.

51

0.44 0.46 0.48 0.5 0.52 0.54 0.56 0.58 0.60.41

0.42

0.43

0.44

0.45

0.46

0.47

0.48

0.49

0.5

Expected Mean of z*

Dem

and

for

the

Ass

et in

Per

iod

0

Figure 1: Demand vs. z*

Figure 2.1: Demand for the initial asset holding wealth, interest rates, andthe money supply shock constant and changing z∗, the fraction of peopleconsuming early.

52

0.6 0.7 0.8 0.9 1 1.1 1.2 1.3 1.40

0.05

0.1

0.15

0.2

0.25

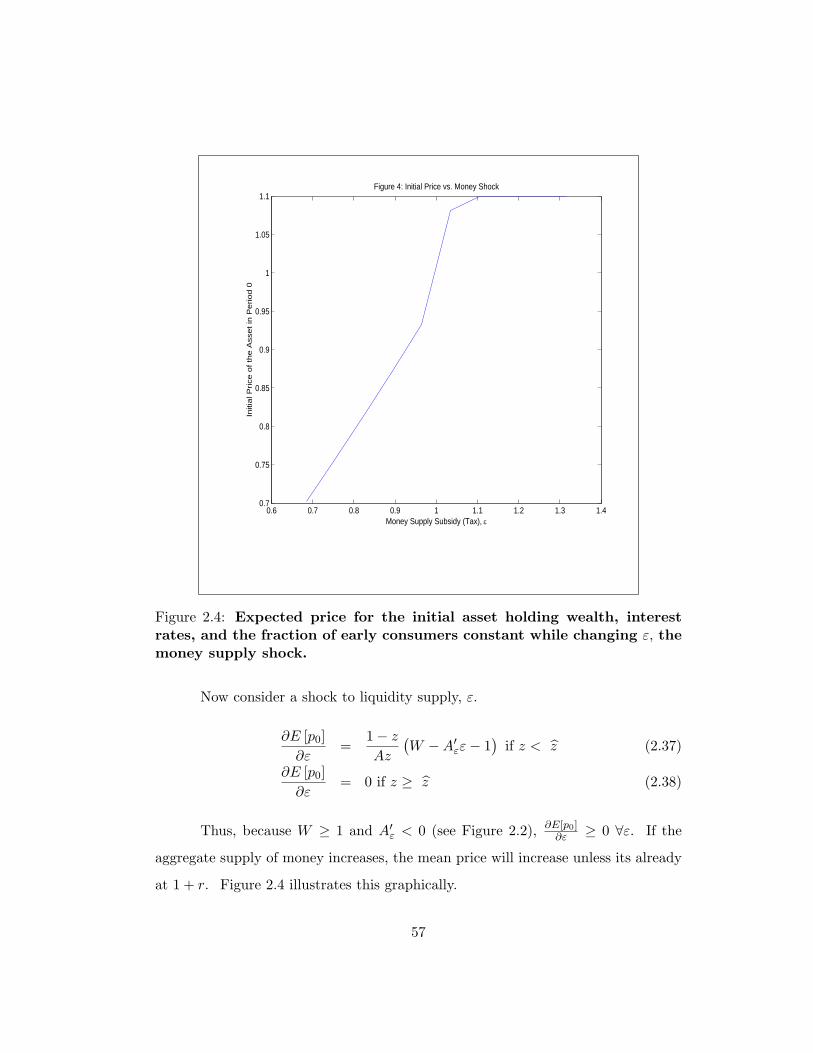

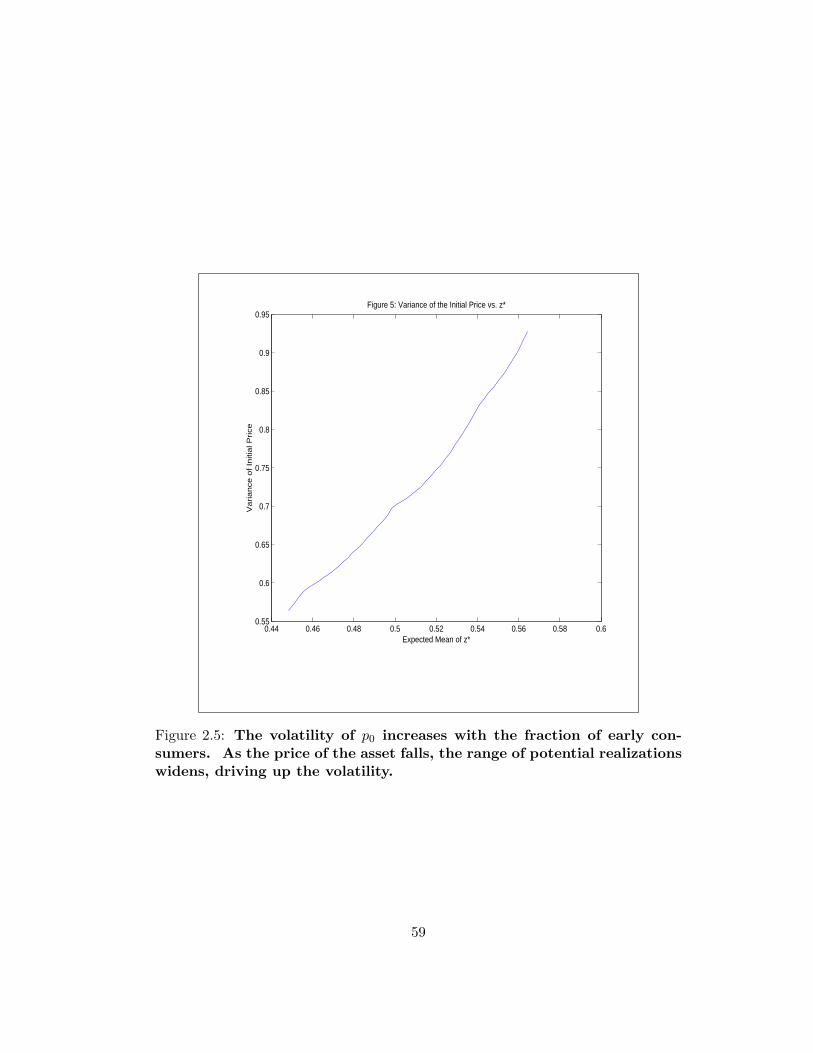

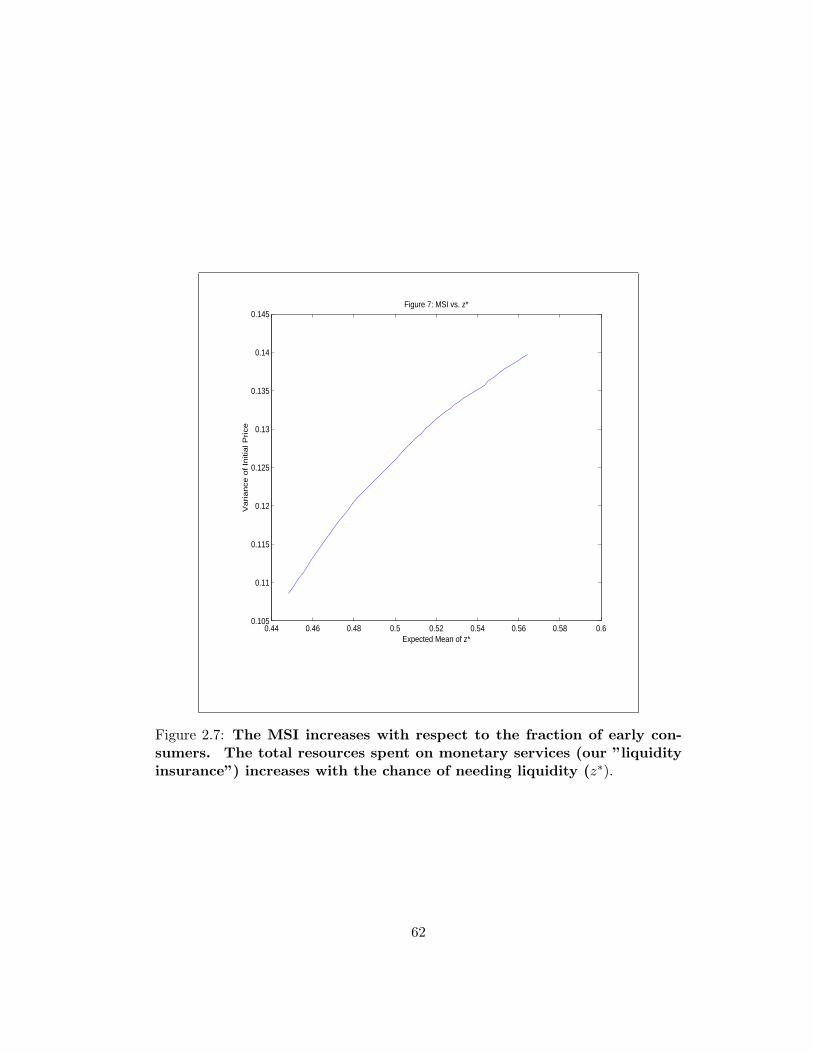

0.3