copyright de beers 2004 de beers seminar to anglo american analysts 23rd september 2004

Post on 21-Dec-2015

217 views

TRANSCRIPT

Copyright De Beers 2004

De Beers Seminar toAnglo American

Analysts

23rd September 2004

Copyright De Beers 2004

Agenda

• Welcome by Nicky Oppenheimer, Chairman

• Introduction by Gary Ralfe, Managing Director

• Paddy Kell, Finance Director

• Gareth Penny, Managing Director, DTC

• Gary Ralfe, Managing Director

• Q&A

• Advertising Commercials

Copyright De Beers 2004

DebswanaGroup

Central HoldingsGroup

Anglo AmericanGroup

CentralInvestments (DBI)

Lux

DB Investments(Lux)

De Beers sa(Lux)

De BeersCentenary

(Swtizerland)

De BeersConsolidated Mines

(South Africa)

Debswana(Botswana)

Namdeb(Namibia)

DTC*(UK)

*DTC (Pty) Ltd(South Africa) wholly owned by DBCM

11% 89%

45%10% 45%

100%

100%

50% 50% 100%

100%

De Beers Group of companies

Copyright De Beers 2004

De Beers & the Diamond Industry

Size of the Diamond Business 2003

World Production of Rough ($bn)De Beers

Group+

OtherProducers

= $9.1

$3.6 $5.5

World Supply of Rough ($bn)De Beers

Group+

OtherProducers

= $10.1

$5.6 $4.5

Polished Equivalent of Supply ($bn) $16.1

Global Sales of Diamond Jewellery ($bn) $57

Copyright De Beers 2004

Change in business modelCustodianship to Leadership

Supply Control Driving Demand Growth

Utilising key assets:– Mystique of the natural diamond– Producer partnerships– Diamond knowledge and expertise– “De Beers” brand potential

With full legal compliance

Driving demandSupplier of

ChoiceDe Beers’

BrandEffective

Organisation

Copyright De Beers 2004

Privatisation - 2001

Dedicated diamond mining and marketing business

Since delisting we have:

– Liberated $2.06 billion from stocks

– Generated operating cash flow of $4.5 billion

– Reduced net gearing level from 57% to 21%

– Repaid $4.5bn acquisition facility ahead of schedule

– Refinanced on favourable terms with $2.5bn revolving facility

– Paid ordinary dividends of $838m (pref dividends $266m)

Copyright De Beers 2004

Primary strategic levers

5. Producer proposition

6. Synthetics response

7. Organisation effectiveness

1. Demand growth

2. Profitable production growth

3. Creating value through the DTC

4. Cost and working capital efficiencies

Profitability Sustainability

Copyright De Beers 2004

Paddy Kell

Finance Director

De Beers

Copyright De Beers 2004

Agenda

• Results for 6 months ended 30 Jun 2004

• Trends:• EBITDA• ROCE • ROE• Cash flow / debt• Costs

•

Looking forward

Copyright De Beers 2004

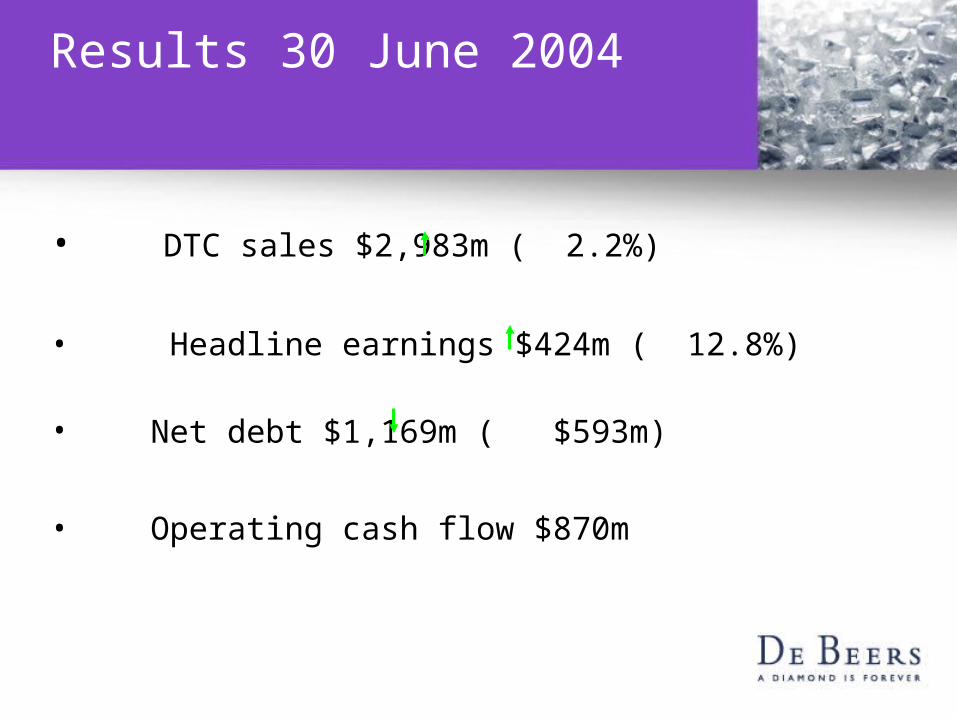

Results 30 June 2004

• DTC sales $2,983m ( 2.2%)

• Headline earnings $424m ( 12.8%)

• Net debt $1,169m ( $593m)

• Operating cash flow $870m

Copyright De Beers 2004

Headline earnings June 2003 - 2004

82

107

112 89

63

24424

376

9

68

200

250

300

350

400

450

500

550

600

650

HeadlineJune 2003

Currency Price &volume

Tradeinvestment

& otherincome

Sorting andmarketing

Financing Tax JV's Other HeadlineJune 2004

US

$ M

Copyright De Beers 2004

EBITDA

0

200

400

600

800

1000

1200

1400

1600

1800

2000

Dec-1994

Dec-1995

Dec-1996

Dec-1997

Dec-1998

Dec-1999

Dec-2000

Dec-2001

Dec-2002

Jun-2003

Dec-2003

Jun-2004

US

$ M

Total Diamond business only June

NFO/GMRappointed

Privatisation

Copyright De Beers 2004

ROCE

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Dec-1994

Dec-1995

Dec-1996

Dec-1997

Dec-1998

Dec-1999

Dec-2000

Dec-2001

Dec-2002

Jun-2003

Dec-2003

Jun-2004

Total Diamond business only Diamond business (June)

Based on headline earnings

Copyright De Beers 2004

ROE

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Dec-1994

Dec-1995

Dec-1996

Dec-1997

Dec-1998

Dec-1999

Dec-2000

Dec-2001

Dec-2002

Jun-2003

Dec-2003

Jun-2004

Total Diamond business only June

Based on headline earnings

Copyright De Beers 2004

Operating cash flowOperating cash flow

-500

0

500

1000

1500

2000

2500

Dec-1994

Dec-1995

Dec-1996

Dec-1997

Dec-1998

Dec-1999

Dec-2000

Dec-2001

Dec-2002

Jun-2003

Dec-2003

Jun-2004

US

$ M

Total Diamond business only Diamond business (June)

Copyright De Beers 2004

4008

3290

2572

1783 1762

1169

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Dec 2001 Jun 2002 Dec 2002 Jun 2003 Dec 2003 Jun 2004 Dec 2004

US

$ M

Net Debt

Copyright De Beers 2004

Net working capital

0

1000

2000

3000

4000

5000

6000

Dec-94

Dec-95

Dec-96

Dec-97

Dec-98

Dec-99

Dec-00

Dec-01

Dec-02

Jun-03

Dec-03

Jun-04

US

$ M

December June

Including diamond stocks

Copyright De Beers 2004

Cash costs

(100)

100

300

500

700

900

1,100

1,300

1,500

1,700

2001 2002 2003 2004F

US$

M

Production costs Sorting, selling & marketingExploration & research Corporate

995878

1292

1500est

Copyright De Beers 2004

Increasing carat production…

SOUTH AFRICAN, DEBSWANA & NAMDEB OPERATIONS - DIAMOND RECOVERY

10.7 10.4 11.9 13.4

26.4 28.430.4

29.6

1.41.3

1.5 1.90.3

0.2

0.20.2

-

5

10

15

20

25

30

35

40

45

50

2001 2002 2003 2004 Forecast (Aug)

Mill

ion

sC

ara

ts

DBCM Debswana Namdeb Williamson Diamonds Limited

Copyright De Beers 2004

…together with more waste tons mined...

SOUTH AFRICAN, DEBSWANA & NAMDEB OPERATIONS - WASTE TONS MINED

51.0 52.260.9

83.9

54.260.4

62.1

66.425.5

31.5

33.6

24.4

-

-

-

1.0

-

20

40

60

80

100

120

140

160

180

2001 2002 2003 2004 Forecast (Aug)

Mill

ion

sW

aste

To

ns M

ined

DBCM Debswana Namdeb Williamson Diamonds Limited

Copyright De Beers 2004

…resulting in increased mining costs

SOUTH AFRICAN, DEBSWANA & NAMDEB OPERATIONS - WASTE TONS MINED vs US$ CASH COST PER TON

$7.53

$11.56

$3.25$4.53

-

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

180,000,000

2001 2002 2003 2004 Forecast (Aug)

Was

te T

on

s M

ined

-

2

4

6

8

10

12

14

16

US

$ ca

sh c

ost

per

To

n T

reat

ed

DBCM Debswana Namdeb US$ cash cost per ton treated US$ cash cost per mined

Copyright De Beers 2004

Finance focus

• Risk management, governance

• Cost of capital

• Cash flows and future capital funding

Copyright De Beers 2004

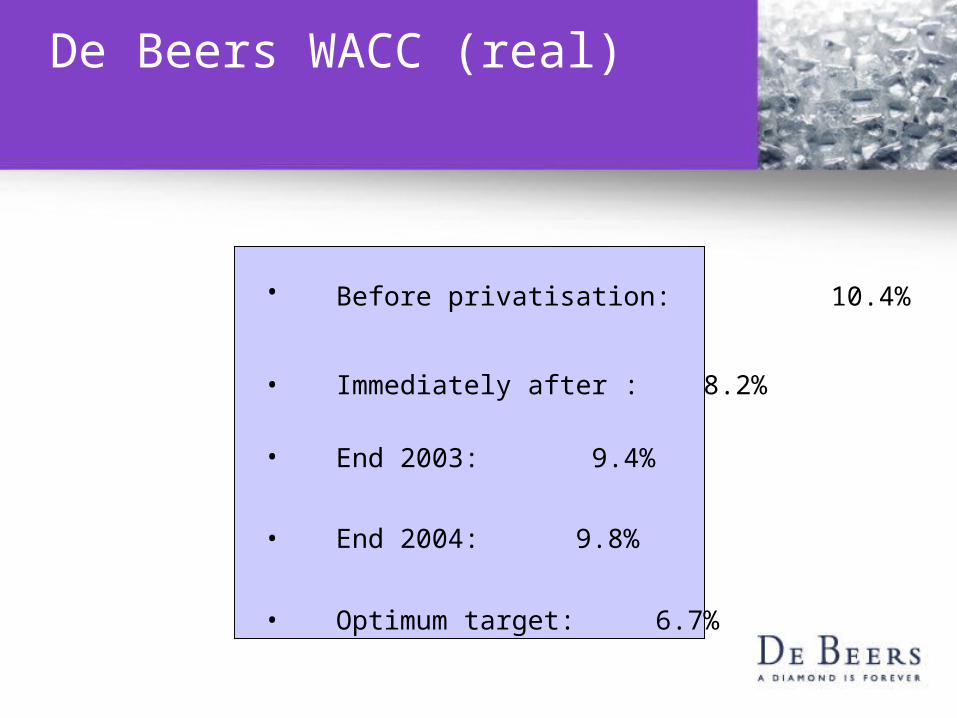

De Beers WACC (real)

• Before privatisation: 10.4%

• Immediately after : 8.2%

• End 2003: 9.4%

• End 2004: 9.8%

• Optimum target: 6.7%

Copyright De Beers 2004

Finance focus

• Risk management, governance

• Cost of capital

• Cash flows and future capital funding

Copyright De Beers 2004

De Beers Sales and Marketing

Gareth Penny

Managing Director

Diamond Trading Company

Copyright De Beers 2004

De Beers’ 1999 Strategic Plan

Driving demand

Supplier of Choice

De Beers’ Brand

Effective Organisation

Copyright De Beers 2004

Driving Demand

% Growth in World Nominal DJ Sales (CAGR)

94-98 99-03

-0.2

3.6

-1.0

0.0

1.0

2.0

3.0

4.0%

Copyright De Beers 2004

The rate of growth in World diamond jewellery sales is

increasing

(% growth US$ PWP)

% change

3%

6%

8%

0%

10%

2002 2003 H1 2004

Copyright De Beers 2004

USA

Italy

Germany

France

UK

Japan

Taiwan

Thailand

China

Gulf

India

Turkey

WORLD

LC Retail Sales Growth Est. H1 2004

Estimated H1 world retail markets up

+5.5% in LC and +8% in PWP

+8.0% PWP

19

12

7

6

5

17

1

8

6

-4

7

5.5

-3

2.5

Copyright De Beers 2004

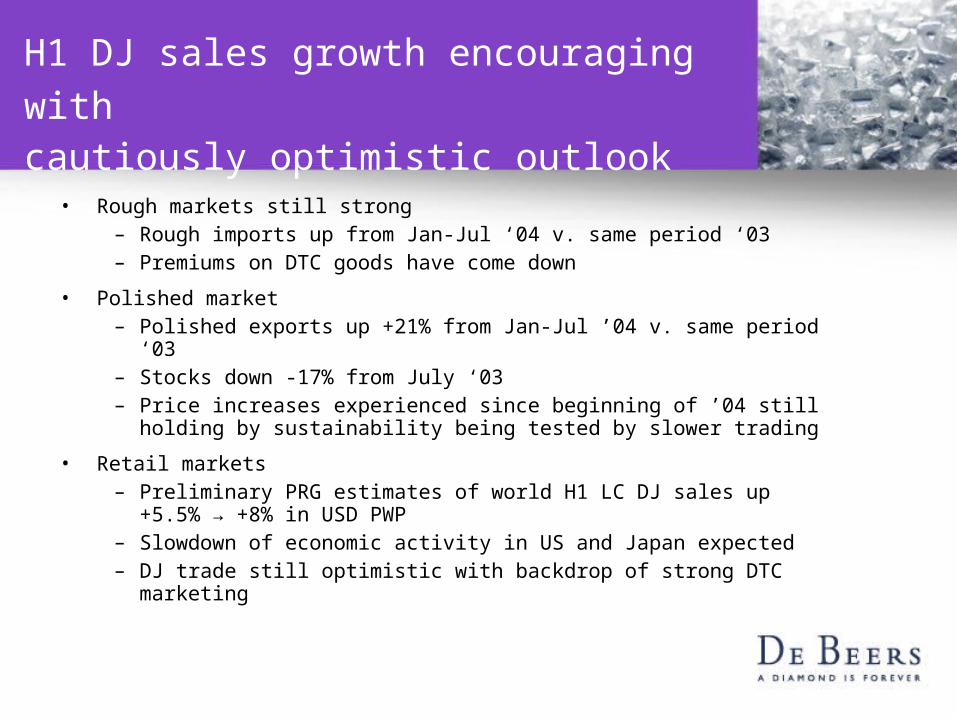

H1 DJ sales growth encouraging with cautiously optimistic outlook

• Rough markets still strong– Rough imports up from Jan-Jul ‘04 v. same period ‘03– Premiums on DTC goods have come down

• Polished market – Polished exports up +21% from Jan-Jul ’04 v. same period ‘03– Stocks down -17% from July ‘03– Price increases experienced since beginning of ’04 still holding

by sustainability being tested by slower trading

• Retail markets– Preliminary PRG estimates of world H1 LC DJ sales up +5.5%

→ +8% in USD PWP– Slowdown of economic activity in US and Japan expected – DJ trade still optimistic with backdrop of strong DTC marketing

Copyright De Beers 2004

2004 New Initiatives

Japan India ChinaUSA

Copyright De Beers 2004

De Beers built two thirds of the US Market

New Occasions

New Segments New Products

Copyright De Beers 2004

Copyright De Beers 2004

Driving Incremental Sales

USA: Three Stone Jewellery SalesRetail Sales

0

500

1000

1500

2000

2500

3000

3500

1999 2000 2001 2002 2003

$m

Copyright De Beers 2004

Right Hand Ring advertising is a huge hit in 2004

Copyright De Beers 2004

2004 New Initiatives

Japan India ChinaUSA

Copyright De Beers 2004

Highly visible presence in-store

Copyright De Beers 2004

Value Share and Growth Trend (12mmt)

3-stone Diamond Jewellery growing rapidly

Source : DDB

3.4 3.5 3.5 3.5 3.5 3.3 3.4 3.4 3.4 3.5 3.4 3.3 3.4 3.4 3.5 3.5 3.6 3.7 3.8 3.8 3.9 4 4.3 4.7 5 5.2 5.5 5.9

-20

-10

0

10

20

30

40

50

60

70

80

Jan-02

Feb-02

Mar-02

Apr-02

May-02

Jun-02

Jul-02

Aug-02

Sep-02

Oct-02

Nov-02

Dec-02

Jan-03

Feb-03

Mar-03

Apr-03

May-03

Jun-03

Jul-03

Aug-03

Sep-03

Oct-03

Nov-03

Dec-03

Jan-04

Feb-04

Mar-04

Apr-04

(%)

% share (3 stone) Total DJ 3 stone

Copyright De Beers 2004

2004 New Initiatives

Japan India ChinaUSA

Copyright De Beers 2004

• Nakshatra (Constellation) revitalised floral jewellery

• Launched October 2000

• Sales over $100m in 3 years. No. 1 brand in India

• Awarded status

Nakshatra Flagship

Copyright De Beers 2004

Aishwarya Rai – Brand ambassadress

Copyright De Beers 2004

2004 New Initiatives

Japan India ChinaUSA

Copyright De Beers 2004

DLJ acquisition amongst all recently married women

33%

13%

54%

43%

21%

84%

66%73%

Shanghai Beijing Guangzhou

1997

2000

2002

The DWR cultural imperative has

been quickly adopted in

China’s major cities

Source: China DWR 1997; China DCJ 2000, China DCJ 2002

Copyright De Beers 2004

1999 Strategic Plan

Driving demand

Supplier of Choice

De Beers’ Brand

Effective Organisation

Copyright De Beers 2004

StrongConsumerCampaign

Most Major

Retailers

ThreeMajor

Manufacturers

Driving demand through efficient Channels for Trilogy

DTC and Six Clients

Copyright De Beers 2004

Supplier of Choice

Copyright De Beers 2004

What Has Been Achieved….

• Commodity focus • Consumer dreams and needs focused

Pre SOC

PostSOC

• Little product differentiation • Product differentiation

• Low investment in marketing • Higher investment in marketing

• Few brands • Some recognised brands

• Luxury goods beating us • Diamonds closing the gap

• Few proprietary channels • Many proprietary channels

• Price driven • Added value driven

• Unhealthy declining industry • Healthy growth driven industry

• High stocks poor business • Low stocks good business

Copyright De Beers 2004

Major Competitors

• Luxury travel

• Luxury watches

• Hi-Tech equipment

• Luxury leather goods

• Luxury fashion

Copyright De Beers 2004

Areas of focus: Conflict Diamonds

Copyright De Beers 2004

Area of focus : Synthetics!

Firms currently producing synthetics:

•Apollo

•Gemesis

Copyright De Beers 2004

Current workstreams

• Enhance Consumer Confidence• Trade education• Diamond promotion• Detection technology• Promoting Disclosure best

practice• Vigilance• Maintaining perspective

Copyright De Beers 2004

Our Strategic Objectives

We will be focussed on:

1. Driving consumer demand2. Maintaining consumer confidence3. “Supplier of Choice” 4. “Purchaser of Choice” 5. The skills and talents of our employees6. Providing exceptional value to our

shareholders

Copyright De Beers 2004

Gary Ralfe

Managing Director

De Beers

Copyright De Beers 2004

Mining and ExplorationHistoric Performance

DE BEERS GROUPTotal Diamond production (1995 - 2003)

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1995 1996 1997 1998 1999 2000 2001 2002 2003

Dia

mo

nd

s R

ec

ov

ere

d (

Ca

rats

00

0's

)

CAGR 7%

+ 9%+9%

Copyright De Beers 2004

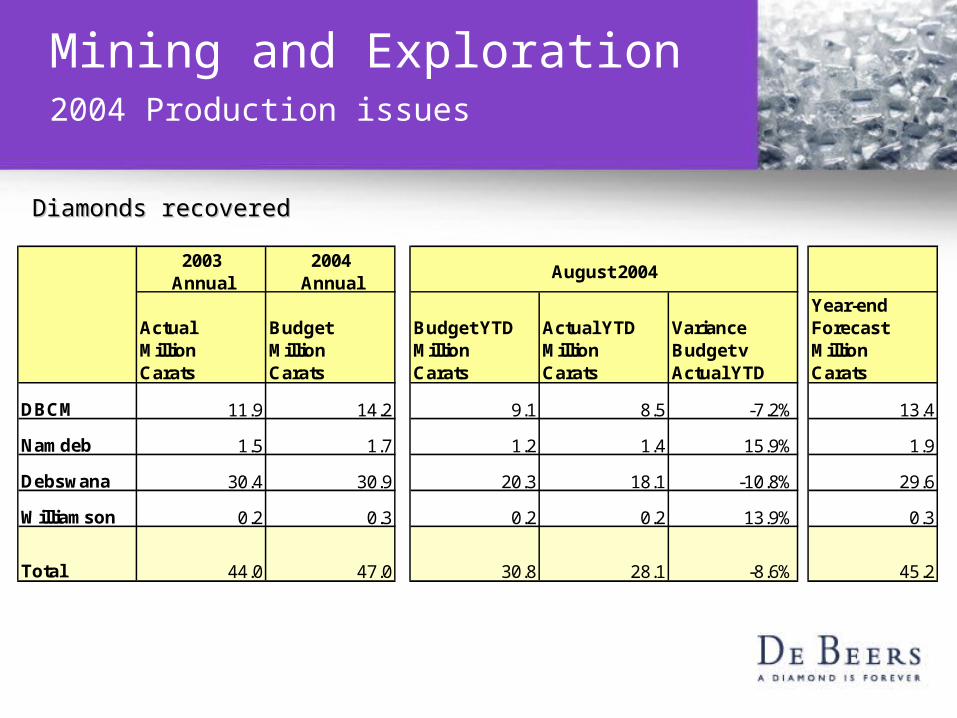

Mining and Exploration2004 Production issues

Diamonds recoveredDiamonds recovered

2003Annual

2004Annual

August 2004

ActualMillionCarats

BudgetMillionCarats

Budget YTDMillionCarats

Actual YTDMillionCarats

VarianceBudget vActual YTD

Year-endForecastMillion Carats

DBCM 11.9 14.2 9.1 8.5 -7.2% 13.4

Namdeb 1.5 1.7 1.2 1.4 15.9% 1.9

Debswana 30.4 30.9 20.3 18.1 -10.8% 29.6

Williamson 0.2 0.3 0.2 0.2 13.9% 0.3

Total 44.0 47.0 30.8 28.1 -8.6% 45.2

Copyright De Beers 2004

Continuing to Drive Supply Beyond 2004 - Production Forecast

Supply Growth 2004 - 2009

42

44

46

48

50

52

54

Car

ats

reco

vere

d -

Mil

lio

n

In the project pipeline

Projects under review

Base Case

2004 2005 2006 2007 2008 2009

Copyright De Beers 2004

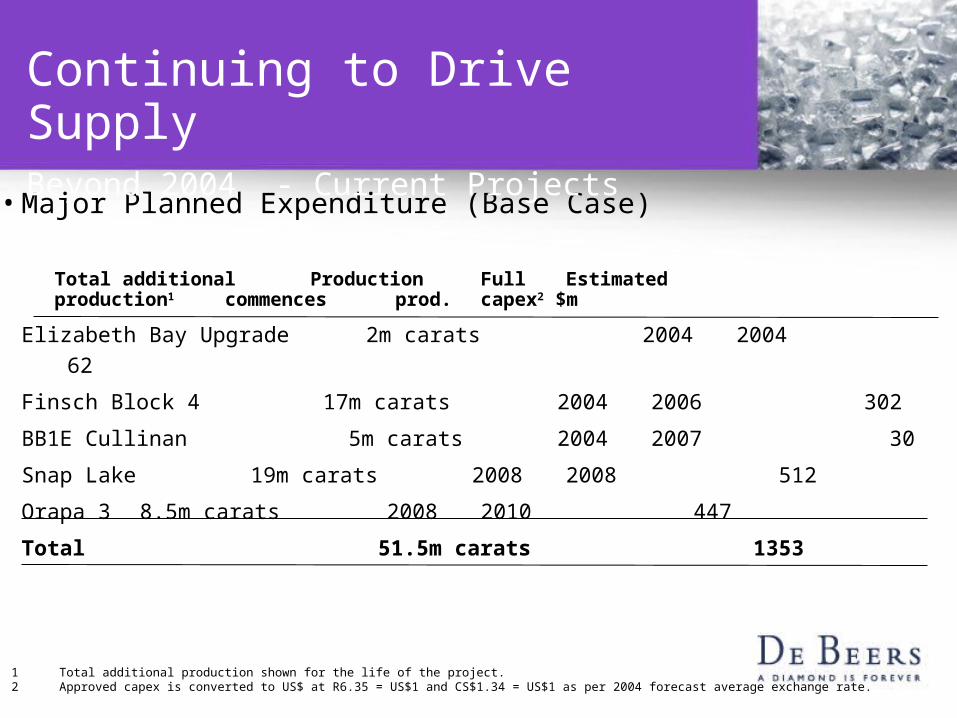

• Major Planned Expenditure (Base Case)

Total additional Production Full Estimatedproduction1 commences prod. capex2 $m

Elizabeth Bay Upgrade 2m carats 2004 2004 62

Finsch Block 4 17m carats 2004 2006 302

BB1E Cullinan 5m carats 2004 2007 30

Snap Lake 19m carats 2008 2008 512

Orapa 3 8.5m carats 2008 2010 447

Total 51.5m carats 1353

1 Total additional production shown for the life of the project. 2 Approved capex is converted to US$ at R6.35 = US$1 and CS$1.34 = US$1 as per 2004 forecast average exchange rate.

Continuing to Drive SupplyBeyond 2004 - Current Projects

Copyright De Beers 2004

Continuing to Drive SupplyBeyond 2004 - Current Projects

• Projects under review:

Total additional Production Full Estimated production1 commences prod. capex2 $m

Finsch Plant Upgrade 2m carats 2006 2007 90Victor 6m carats 2008 2008 625C-Cut Cullinan 115m carats 2009 2012-14 1291Finsch Block 5 16m carats 2009 2010 425Total 139m carats 2431

1 Total additional production shown for the life of the project. 2 Approved capex is converted to US$ at R6.35 = US$1 and CS$1.34 = US$1 as per 2004 forecast average exchange rate.

Copyright De Beers 2004

Continuing to Drive SupplyIn the project pipeline

– South Africa

• Voorspoed (production from 2007)

• Venetia– Underground (2015)

– Satellite pipes

– Botswana: multiple projects at existing mines

– Canada

• Gahcho Kué (production from 2012)

Copyright De Beers 2004

Continuing to Drive SupplyAdvanced Exploration Projects

Canadao Attawapiskat Satellites

o Forte a la Corne JV

o Knife Lake JV

o Hardy Lake JV

o Rockinghorse JV

Russia o Grib

Botswanao Jwaneng DK7

o Orapa Satellites

Guinea, Gabon, Zimbabwe, South Africa, Brazil

Copyright De Beers 2004

Mining and ExplorationSupply side challenges

• Jwaneng Lease Renewal

• Rand strength - impact on marginal mines

• Working stock levels

• De Beers market share

• Alrosa contract

Copyright De Beers 2004

DBsa

Gary Ralfe

DBsa

Nicky Oppenheimer

DTC

Gareth Penny(MD Designate)

Debswana

Blackie Marole(MD Designate)

Namdeb

IngeZaamwani

DBCM

Jonathan Oppenheimer

(MD Designate)

Louis Nchindo

DBsa

Gary Ralfe

DBsa

Nicky Oppenheimer

DTC

Gareth Penny

Debswana

Marole(MD Designate)

Namdeb

IngeZaamwani

DBCM

Jonathan OppenheimerNchindo

De Beers Group Services

Gary Ralfe

Group CFO

Paddy Kell

Group HR Director

Craig Mudge

Group IT Director

Debbie Farnaby

Group General

Counsel

Glenn Turner

Group Mining/Tech.

Services Director

Gavin Beevers

Group CFD

Ollie Oliveira

Group CFOPaddy Kell

Group HR Director

Craig Mudge

Group IT Director

Debbie Farnaby

Group General Counsel

Glenn Turner

Group Mining & Exploration Director Gavin Beevers

Strategy & Business Development Director

Ollie Oliveira

External Affairs Director

Being recruited

New Organisation

Copyright De Beers 2004

External Relations

• USA– DoJ settlement

– Civil litigation

• Angola– Arbitration settlement

• Russia– Alrosa trade agreement

Copyright De Beers 2004

External Relations

• RSA

– Transformation and Black Economic Empowerment transaction

– Diamond Amendment Bill

• Botswana

– Jwaneng Lease Renewal

• Namibia

– Renewal of sales agreement

Copyright De Beers 2004

Adjacent Businesses

• Element 6

Sales H1 2004 up 20% compared to H1 2003 to $121m

Net earnings H1 2004 more than tripled compared to H1 2003 from $4.5m to $14.6m due to

efficiency improvements

• De Beers LV

Total sales 2004 YTD $10.5m (+4% > budget)

New Chief Executive and strengthened management team

US rollout planned for 2005

Both shareholders committed to long term investment of $400m ($80.5m invested to date by De

Beers)

Copyright De Beers 2004

Primary strategic levers

5. Producer proposition

6. Synthetics response

7. Organisation effectiveness

1. Demand growth

2. Profitable production growth

3. Creating value through the DTC

4. Cost and working capital efficiencies

Profitability Sustainability

Copyright De Beers 2004

Strategic Goal

Maintain the leadership position of the De Beers Group of Companies and deliver sustainable

returns on capital in line with this position.

Copyright De Beers 2004

Q & A SESSION