corporate financial management june 2004 examiner’s …...corporate financial management june 2004...

TRANSCRIPT

Page 1 of 21

Corporate Financial Management June 2004

Examiner’s Report and Suggested Answers

Important Notice When reading these suggested answers please note that the answers are intended as an indication of what is required rather than a definitive “right” answer. In many cases there are several possible answers/approaches to a question. Please be aware also that the length of the suggested answers given here may be somewhat exaggerated from what might be achieved in the reality of an unseen, time constrained examination.

General Comments As in past diets, some candidates lost marks because they answered the wrong question, sometimes at great length. Many lost marks because they did not read the question properly or spend a few moments to consider what issues were relevant to an answer. Question 6 was a particular example of this. There was, as before, evidence of less complete answers towards the end of the paper. This may have been partly due, as before, to poor examination technique. Students seem to have done better in this paper than in others in the recent past. In some cases answers on similar, but not identical, questions on the same or closely related topics are getting better. Although there is still a lot of room for improvement in exam technique, students seem to be using some shrewd judgment in selecting which questions to answer. If there is any general moral to be drawn from current experience, it is that students need to make sure that they are familiar with the basics of the syllabus and to practise numerical questions using examples (both of which are provided in the study text). Faulty and incomplete calculations are easy to spot (though markers take great pains to identify any marks that have been earned). But candidates should be aware that discursive answers where the candidate does not know the answer are equally obvious. There is no point in waffling if you do not know – you simply waste time. Candidates cannot rely on the same questions being set in successive examinations. But the examiner wishes to find what they know rather than catch them out, and some fundamentals of the subject are likely to be frequently examined. Candidates who wish

Page 2 of 21

to shine will need to display knowledge, accuracy and a degree of judgment that are out of the ordinary, but students who simply learn the theory and practise calculations should be confident of passing.

Section A - Compulsory

10 Questions –Total 40 marks (maximum 4 marks per question)

1. (a) Explain why, despite its drawbacks (which you should identify),

Accounting Rate of Return is still widely used in the evaluation of capital investment projects. (4 marks)

Suggested Answer:

The weaknesses of Accounting Rate of Return are that it does not take account of the time value of money and, being based on accounting profit and asset values consistent with published asset values in the Balance Sheet, it depends on the accounting principles applied and consequently has the same scope for variation in cost and asset values found in the Profit & Loss account and the balance sheet Methods based on discounted cash flows reflect the time value of money by discounting and avoid the scope for variation in calculated values.

However, even decision makers who are not trained in accounting are familiar and comfortable with the profit and asset values used in calculating the ARR, which are prepared on the same basis as figures in the P&L account and balance sheet. Examiner’s comments:

Question 1 was on the whole reasonably well answered. Candidates did best at questions that required a rehearsal of book learning (like 1(a) on Accounting Rate of Return or 1(c) on reasons for going public) rather than requiring them to put together information from more than one place (like 1(b) on the cost of short term finance). The answers to the parts of Question 1 that included numbers were mixed. 1(g) required candidates to identify which of three possible investments could be immediately excluded on the basis of risk and return if considered in isolation from other investments, and when this same investment might be the best choice out of the three for inclusion in a portfolio. Most candidates identified correctly investment C, with the same risk as investment A but a lower return, but many could not explain when C might be the best choice in terms of the correlation of its performance with the rest of the portfolio. 1(h), on weighted average cost of capital, was correctly answered by most candidates. 1(i) on the valuation of a put option for Euro 10 million was not well answered. Some candidates multiplied the Euro amount by the Euro:£ strike price instead of dividing it to find the

Page 3 of 21

sterling value if the option is exercised. Even more used the wrong end of the current Euro:£ spread to find the current sterling value of the Euro sum. It would appear that (a) most candidates have made a good effort to cover the whole syllabus and (b) many candidates may be more comfortable with short questions that test knowledge of the basic aspects of a wide range of subjects and the ability to do simple calculations rather than more extensive and testing questions. There was widespread evidence of poor exam technique: some candidates wrote two pages or more on parts of Question 1 that were worth 4 marks each. It would appear that (a) most candidates have made a good effort to cover the whole syllabus and (b) many candidates may be more comfortable with short questions that test knowledge of the basic aspects of a wide range of subjects and the ability to do simple calculations rather than more extensive and testing questions. There was widespread evidence of poor exam technique: some candidates wrote two pages or more on parts of Question 1 that were worth 4 marks each.

1. (b) Discuss the costs associated with the use of short term finance.

(4 marks)

Suggested Answer:

Short term capital includes trade credit received and bank overdrafts and other short term borrowing. Trade credit usually has no formal cost (though small creditors are allowed to charge interest if payment takes more than 30 days, unless agreed otherwise). There may be a cost in losing discounts for prompt payment or suppliers may be unwilling to supply. Bank overdrafts have an interest cost (which can be kept down by agreeing overdrafts in advance). Factoring and invoice discounting are other forms of short term finance that are now competitive with overdrafts because of their competitive costs, but factors and invoice discounters usually charge fees as well as interest on advances, and their use may adversely affect a company’s relationships with its customers.

Examiner’s comments:

Please see examiners comments on question 1.a

1. (c) Suggest why a private company might go public. (4 marks)

Suggested Answer:

A private company may go public to gain access to a wider range of investors. Private companies cannot offer their shares to the public, and have limited access to capital.

Page 4 of 21

Going public is associated with corporate growth. A company may wish to become a public company in order to have its shares quoted on a recognised stock exchange, either the main market or the Alternative Investment Market. This has advantages in terms of the marketability and price of shares, or to determine reliably the value of shares for a sale or taxation purposes.

Examiner’s comments:

Please see examiners comments on question 1.a

1. (d) Identify four possible sources of finance for an organization other than

ordinary share capital, debt and retained funds. (4 marks)

Suggested Answer:

Options include: trade creditors, factors/invoice discounters, regular funding by the Government and other public bodies, grants, charitable donations, sponsorship.

Examiner’s comments:

Please see examiners comments on question 1.a

1. (e) Briefly explain the two principal new risks that a company might face in

starting to do business overseas. (4 Marks)

Suggested Answer:

The two particular risks involved in doing business overseas are political (or country) risk and foreign exchange risk. Political risk includes the problems of running operations that are geographically separated and based in areas with different cultures and traditions, and where political or economic measures taken by the host government may affect the activities of the subsidiary. The host government may restrict the MNC’s activities to prevent exploitation or for other political and financial reasons. Measures could range from imposing import quotas and tariffs to appropriation of the company’s assets with or without compensation. Host governments may place restrictions on the acquisition of companies in sensitive areas such as defence and utilities. Governments may insist on foreign companies operating through joint ventures with local partners or require minimum levels of local shareholding. Host governments may impose exchange controls, limit imports or restrict repatriation of profits in order to protect foreign exchange reserves or exchange rate parities.

Page 5 of 21

Foreign exchange or currency risk can take the form of: Economic risk: the risk that changes in exchange rates can adversely affect the international competitiveness of a firm.

Translation risk: when assets and liabilities of a firm are denominated in different currencies and changes in exchange rates lead to differing effects on assets and liabilities. Transaction risk: when exchange rate movements affect a company’s cash flows through changes in the prices of imports and exports.

Examiner’s comments:

Please see examiners comments on question 1.a

1. (f) What is the agency problem, and how are its effects limited? (4 Marks) Suggested Answer:

The agency problem arises because the duty of the managers of a company is to further the interests of the ordinary shareholders, who are the owners, and on whose behalf they act, but the two groups have agendas that are not identical. This is apparent for example when management rewards are not linked to investment performance in the form of dividends or share price growth. One way of limiting the effect of the agency problem is to provide incentives for managers to act is such a way as to maximise shareholder returns through performance measures and rewards based on shareholder returns. This is an imperfect mechanism since a single measure or a small number of measures can be manipulated by managers to achieve results closer to what is in their interest.

Scrutiny by groups such as institutional shareholders, the press and particularly non-executive directors may limit the effects of the agency problem (though institutional shareholders may not acknowledge a duty to act on behalf of shareholders as a whole).

Another mechanism is the competitive market in management jobs. Managers who act so as to further shareholders’ interests will, other things being equal, tend to be rewarded better, and those who do not will tend to be penalised. The efficiency of this mechanism depends on the efficiency of the job market

Examiner’s comments:

Please see examiners comments on question 1.a

Page 6 of 21

1. (g) A company is planning to invest surplus funds in one of three short

term investments. It will choose the investment on the basis of risk and return. The returns and risks of the three investments are as follows:

Investment Return Risk (% annual (standard deviation

growth rate) of return) A 10 5 B 12 6 C 9 5

(i) If the investment is to be considered in isolation, taking no account of any other investments, state, giving your reasons, which investment can be excluded immediately. (ii) Explain why, if the investment selected from the three above is to be added to a portfolio of investments, it might now be possible for the investment excluded in (i) to be the best choice.

(4 Marks) Suggested Answer:

(i) Rational investors trade off risk against return, but have different preferences concerning where they strike the balance. It would be possible to prefer A to B, since A has a lower risk than B, or B to A, since B has a higher return than A. C has a lower return than A, but the same risk, so a rational investor would prefer A to C, which can be excluded immediately. (ii) Like individual investments, a portfolio can be valued on the basis of its return and risk. The risk of a portfolio can be measured by its beta factor, which is determined by the variability of the portfolio return and the correlation of this return with the variations in the market return. An individual investment whose returns are negatively correlated with the market return will usually reduce the correlation of the portfolio return with the market return, the beta factor and the overall portfolio risk. This reduction in risk can outweigh the lower return on C, making C the best choice to add to the portfolio. Examiner’s comments:

Please see examiners comments on question 1.a

1. (h) A company’s cost of equity capital is 12%, and the cost of its debt

capital, which consists of 10% loan stock currently traded at par, is 10%. The company receives relief against corporation tax at 30% on interest paid. The market value of the ordinary shares is £30 million, and the market value of the loan stock is £20 million. Calculate the

Page 7 of 21

company’s after-tax weighted average cost of capital. (4 marks)

Suggested Answer:

Net cost % Market value Value of return Equity 12% £30m £3.6m Debt (100%-30%) x 10%

= 7% £20m £1.4m Total £50m £5.0m

WACC = %1010.050£

0.5£ ==mm

Examiner’s comments:

Please see examiners comments on question 1.a

1. (i) Three months ago, having secured a contract with a German customer, a

British company bought a three month put option for Euro 10 million at a strike price of Euro 1.42 to the £. The current exchange rate is Euro 1.4523 – 1.4538 to the £. Calculate the value of the option to the company if it exercises it instead of converting Euro 10 million into Sterling at the current rate. (4 marks)

Suggested Answer:

Proceeds of exercising option 254,042,7£42.110 =mEuro

Proceeds from sale at current exchange rate 525,878,6£4538.1

10 =mEuro

Value of option 729,163£

Examiner’s comments:

Please see examiners comments on question 1.a

Page 8 of 21

1. (j) What is the Capital Market Line? (4 marks)

Suggested Answer:

The Capital Market Line is a straight line graph of required return on an investment against its risk. The return on an investment may be in the form of dividend yield or capital growth, or a combination of the two. The risk is represented by the variability of the return, and is measured by the standard deviation of the return over a number of years. The line can be drawn on the basis of two points, which are readily available: the risk-free investment, represented by UK Government stock, and the market investment, represented by the level and standard deviation of the return on a stock market index such as the FTSE 100 share index or the all-share index. The risk on an individual investment is measured by its Beta factor. The Beta factor of the risk free investment is zero, and the Beta factor of the market investment is 1. An investment which, as part of a diversified portfolio, is riskier than the market index has a Beta factor greater than 1 and an investment with a lower risk than the market has a Beta factor between zero and 1. Examiner’s comments:

Please see examiners comments on question 1.a

Page 9 of 21

Section B 3 Questions – 20 Marks each

Total 60 marks

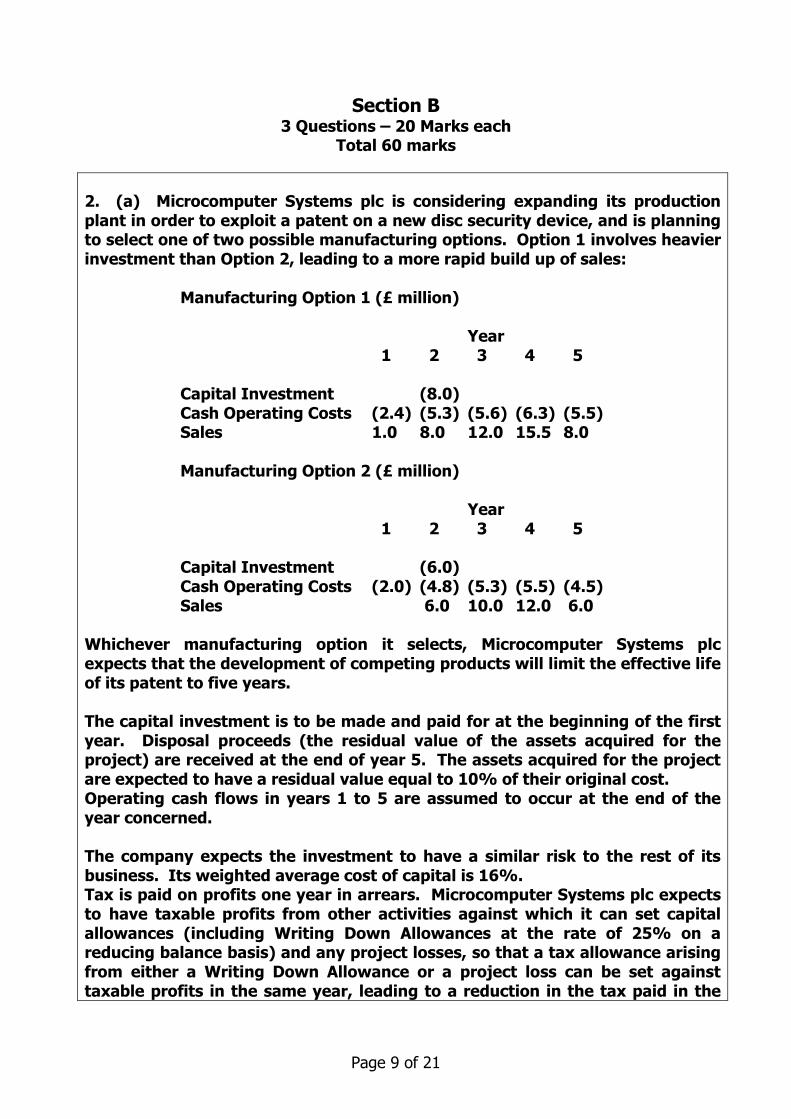

2. (a) Microcomputer Systems plc is considering expanding its production plant in order to exploit a patent on a new disc security device, and is planning to select one of two possible manufacturing options. Option 1 involves heavier investment than Option 2, leading to a more rapid build up of sales: Manufacturing Option 1 (£ million) Year 1 2 3 4 5 Capital Investment (8.0) Cash Operating Costs (2.4) (5.3) (5.6) (6.3) (5.5) Sales 1.0 8.0 12.0 15.5 8.0 Manufacturing Option 2 (£ million) Year 1 2 3 4 5 Capital Investment (6.0) Cash Operating Costs (2.0) (4.8) (5.3) (5.5) (4.5) Sales 6.0 10.0 12.0 6.0 Whichever manufacturing option it selects, Microcomputer Systems plc expects that the development of competing products will limit the effective life of its patent to five years. The capital investment is to be made and paid for at the beginning of the first year. Disposal proceeds (the residual value of the assets acquired for the project) are received at the end of year 5. The assets acquired for the project are expected to have a residual value equal to 10% of their original cost. Operating cash flows in years 1 to 5 are assumed to occur at the end of the year concerned. The company expects the investment to have a similar risk to the rest of its business. Its weighted average cost of capital is 16%. Tax is paid on profits one year in arrears. Microcomputer Systems plc expects to have taxable profits from other activities against which it can set capital allowances (including Writing Down Allowances at the rate of 25% on a reducing balance basis) and any project losses, so that a tax allowance arising from either a Writing Down Allowance or a project loss can be set against taxable profits in the same year, leading to a reduction in the tax paid in the

Page 10 of 21

following year. Although the company will treat the initial investment cost as being paid immediately at the start of the project, the first Writing Down Allowance should be calculated on the basis that the initial capital investment is made during the course of the first year. Microcomputer Systems plc’s corporation tax rate is 30%. Assume that the Writing Down Allowance in the final year of operation is equal to the difference between the opening written down value in that year and the residual value. REQUIRED: Evaluate the two options and comment on whether Microcomputer Systems plc should invest to exploit the patent, and if so which manufacturing option it should select. (12 marks) Suggested Answer:

Manufacturing Option 1:WDA (£ million)

Year 1 2 3 4 5

Opening asset value for WDA 8.0 6.0 4.5 3.375 2.531

WDA at 25% 2.0 1.5 1.125 0.844 1.731

Closing asset value for WDA 6.0 4.5 3.375 2.531 0.800 Manufacturing Option 1:Cash flows (£ million) Year 0 1 2 3 4 5 6 Cash flows from

capital investment/ disposal (8.000) 0.800

Operating cash flows (1.400) 2.700 6.400 9.200 2.500

Tax payments/relief on 0.420 (0.810) (1.920) (2.760) (0.750) operating cash flows Tax relief on WDA 0.600 0.450 0.338 0.253 0.519

Net cash flow (8.000) (1.400) 3.720 6.040 7.618 0.793 (0.231)

Present value of cash flow (8.000) (1.207) 2.765 3.870 4.207 0.378 (0.095)

NPV £1.918 million

Page 11 of 21

Manufacturing Option 2:WDA (£ million)

Year 1 2 3 4 5

Opening asset value for WDA 6.0 4.5 3.375 2.531 1.898

WDA at 25% 1.5 1.125 0.844 0.633 1.298

Closing asset value for WDA 4.5 3.375 2.531 1.898 0.600

Manufacturing Option 2:Cash flows (£ million) Year 0 1 2 3 4 5 6 Cash flows from

capital investment/ disposal (6.000) 0.600

Operating cash flows (2.000) 1.200 4.700 6.500 1.500 Tax payments/relief on 0.600 (0.360) (1.410) (1.950) (0.450)

operating cash flows Tax relief on WDA 0.450 0.338 0.253 0.190 0.389

Net cash flow (6.000) (2.000) 2.250 4.678 5.343 0.340 (0.061)

Present value of cash flow (6.000) (1.724) 1.672 2.997 2.951 0.162 (0.025)

NPV £0.033 million

Either manufacturing option gives a positive NPV, so is worth undertaking. Option 1 gives a larger NPV, meaning a larger surplus for shareholders after allowing for the cost of capital, and should be chosen. The reliability of this conclusion depends on the reliability of the assumptions on which it is based, in particular the cash flow projections and the value of the cost of capital.

(b) Beta plc, one of Microcomputer Systems plc’s competitors, evaluates capital investment projects using uninflated projections of sales and costs. Beta plc’s cost of capital and level of risk are the same as those of Microcomputer Systems plc. Beta plc expects inflation over the next few years to be at the rate of 3% per annum. (i) Calculate what discount rate Beta plc should use to evaluate capital

investment projects. (4 marks)

Suggested Answer:

r = %6.12126.003.1

03.016.01

==−=+−iim

Page 12 of 21

(ii) Suggest what advantages there could be for Beta plc in basing its capital

investment appraisal on inflated rather than uninflated projections. (4 marks)Suggested Answer: Using inflated cash flows for discounted cash flow calculations means that the appropriate inflation rate can be applied to each factor. This is an advantage if different factors are expected to inflate at different rates. For example output prices in rapidly growing industries may grow faster than prices in declining industries, and labour costs may inflate at different rates from material. In addition, inflated cash flows can be discounted using discount rates based on figures for the cost of capital related to market rates, whereas uninflated cash flows need to be discounted by a ‘real’ rate (such as that calculated in (i) above, which cannot so easily be tested against the rates of interest or return that companies actually encounter

Examiner’s comments: Question 2 (a) involved the calculation of the Net Present Values of two capital investment projects. It was moderately well answered, though very few candidates dealt accurately with the Writing Down Allowances, even though the question spelt out in some detail what needed to be done. Most candidates who answered this question made some effort to base their recommendations on their calculations. Question 2 (b) required a calculation of a ‘real’ discount rate, with a comment on the use of inflated rather than uninflated cash flows for capital investment appraisal. The calculation of the ‘real’ discount rate needed the use of a standard formula. Most candidates knew the formula, but not all of these used it correctly. Comments on the advantages of using inflated cash flows were not particularly good. Some identified the value of discount rates that could be related to the market, but fewer mentioned the possibility of different factors inflating at different rates. The proportion of candidates answering Question 2 was not particularly high, and varied considerably between examination centres. It seems possible that candidates who chose not to answer it did so either because they avoid computational questions or because they had not studied the topics covered in part (b).

3. (a) Describe the main features of convertible bonds and loan stocks with warrants attached, and explain what benefits they offer to the issuer and to the investor. (12 Marks) Suggested Answer:

(a) Convertible loan stock pays a fixed rate of interest and may be converted into shares at one or more specified future dates. The share price at which the stock can be converted may increase for later conversion dates, reflecting expected share price growth. At the conversion date or dates, the convertible stock holder can decide whether

Page 13 of 21

to convert the stock into ordinary shares or do nothing and continue to hold the stock. The price of the convertible stock in effect includes an option to buy the ordinary shares. As a result, the interestcost to the company is lower than for conventional, non-convertible stock. The benefits for the investor are the potential value of the conversion rights, combined with interest income which would not be received if the investor simply bought a call option on the shares.

A warrant attached to loan stock gives the purchaser of the loan stock the right to buy shares at a predetermined price at some future date. While it is issued in conjunction with loan stock, it can be traded separately. It is a long-term option on the ordinary shares, and warrants are often issued to makes loan stock issues more attractive. The value of a warrant to loan stock holders is the same as the value of any option. Because the warrant is issued at the same time as the stock, the investor receives interest on the stock, whereas a purchase of options by themselves would not generate income up to the exercise date. Because the exercise date is some years ahead, the value of the warrant at the issue date is probably small, so that it reduces only slightly the return that needs to be offered on the loan stock. It does not involve any immediate dilution in shareholders’ earnings or voting rights. (b) Amalgamated Aggregates plc has issued 8 per cent convertible loan stock which is quoted at £112 per £100 nominal. The first date for conversion is in four years’ time at the rate of 20 ordinary shares per £100 nominal loan stock. The current share price is £5.10. REQUIRED: (i) Calculate the conversion price. (ii) Calculate the conversion premium as a percentage of the current share

price. (4 marks) Suggested Answer: (i) Conversion price 00.5£

20100£ =

(ii) Conversion premium 50.0£10.5£60.5£10.5£

20112£ =−=−

Premium as % of share price %8.9%10010.5£50.0£ =×

(c) Building Materials plc has issued loan stock with 2p warrants (2007) attached. The warrants give the right to purchase 1 ordinary share at a price of 150 pence for every 6 warrants in 2007. The current share price is 120 pence.

Page 14 of 21

REQUIRED: (i) Calculate the conversion premium as a percentage of the current share

price. (ii) Calculate the value of a warrant during the conversion period if the share

price is then 200 pence. (4 marks) Suggested Answer: (i) Cost of 1 share at exercise price £1.50 Cost of 6 warrants £0.12 Cost of acquiring a share using warrants £1.62 Current share price £1.20 Premium £0.42

Premium as % of share price %35%100

20.1£42.0£ =×

(ii) Value of warrant during conversion period = ppp 33.8

6150200 =−

Examiner’s comments:

Question 3 (a) involved a description of convertible bonds and loan stock with warrants, followed by calculations of a conversion price and conversion premium for the convertible stock in part (b) and a conversion premium and valuation for the warrants in part (c). Part (a), which was straightforward, was reasonably well answered. Parts (b) and (c) were poorly answered. This was disappointing, because the calculations were simple.

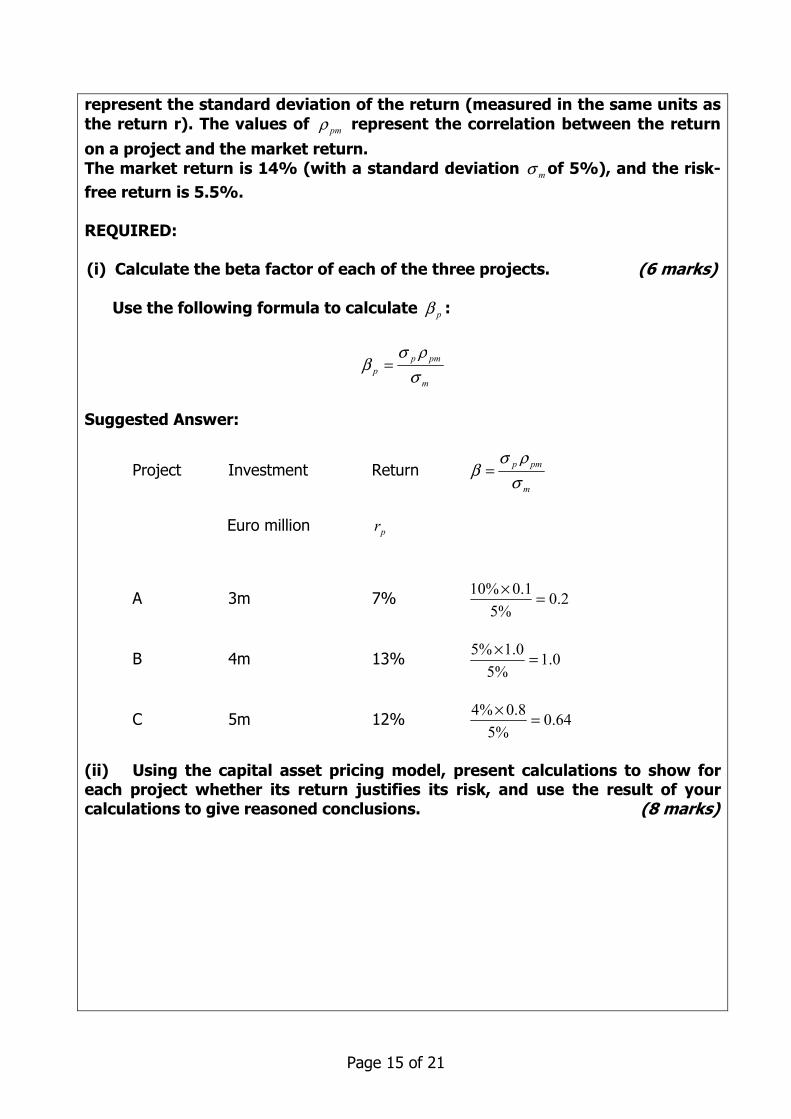

4. (a) The financial management of Produits Domestiques SA (PD) is concerned that the company is not adequately taking account of risk when evaluating investment projects. It has undertaken a study to investigate different ways of reflecting risk. As part of this study, PD has estimated figures having a bearing on the risk of three investment projects that are currently under consideration. These figures, together with the capital investment and estimated returns on the projects, are shown below: Project Investment Return pσ pmρ

Euros million r

A 3m 7% 10% 0.1 B 4m 13% 5% 1.0 C 5m 12% 4% 0.8

The values of pσ have been estimated to provide a measure of risk, and

Page 15 of 21

represent the standard deviation of the return (measured in the same units as the return r). The values of pmρ represent the correlation between the return on a project and the market return. The market return is 14% (with a standard deviation mσ of 5%), and the risk-free return is 5.5%. REQUIRED:

(i) Calculate the beta factor of each of the three projects. (6 marks) Use the following formula to calculate pβ :

m

pmpp σ

ρσβ =

Suggested Answer:

Project Investment Return m

pmp

σρσ

β =

Euro million pr

A 3m 7% 2.0%5

1.0%10 =×

B 4m 13% 0.1%5

0.1%5 =×

C 5m 12% 64.0%5

8.0%4 =×

(ii) Using the capital asset pricing model, present calculations to show for each project whether its return justifies its risk, and use the result of your calculations to give reasoned conclusions. (8 marks)

Page 16 of 21

Suggested Answer: Project Required return )( fmpfp rrrr −+= β Projected return A %2.7%)5.5%0.14(2.0%5.5 =−+=pr 7%

B %0.14%)5.5%0.14(0.1%5.5 =−+=pr 13%

C %94.10%)5.5%0.14(64.0%5.5 =−+=pr 12% Conclusion: For Project A and Project B, projected returns are less than required returns, and do not justify the project risks. For Project C, projected return is greater than required return and justifies the risk. (b) Suggest how a large public limited company may determine its cost of capital. (6 marks) Suggested Answer:

A large public limited company may have capital in the form of equity, long term debt, other prior charge long-term capital such as preference shares and short term borrowing. It can calculate the cost of equity using the Gordon growth model, the cost of long term debt as the internal rate of return on an investment in loan stock at the current market price and the cost of irredeemable preference share capital on the basis of the preference dividend and the market price of the preference shares (if the preference shares are redeemable the return can be calculated as an IRR in the same way as for loan stock). It can find the cost of short term borrowing as the interest rate payable. For a post-tax cost of capital, allowance can be made for tax relief on interest payments, where the company’s prospective profits make this relevant.

The costs of the different kinds of capital can be combined, using weighting factors proportional to the value of each kind of capital, to give the weighted average cost of capital. Since the costs of different kinds of capital have been calculated using market values, it would be appropriate to use the market values of different kinds of capital to find the WACC. This cost of capital would apply to the company as a whole, reflecting the current mix and risks of investments.

If the company is considering raising capital for a particular investment project with a risk that is not typical of the company as a whole, it may wish to adjust the market cost of capital for the whole company to reflect the specific risk.

Examiner’s comments:

Question 4 (a) required calculations of beta factors in part (i), followed by calculations to check whether investments offered good value, allowing for risk, in part (ii). This question was better answered – and by more candidates – than were questions on CAPM in previous examinations. Most candidates calculated the beta factors correctly, though a few failed to use the formula that was given in the question. Many calculated the required returns, but far fewer were able to interpret their calculations to decide whether

Page 17 of 21

investment offered good value. Many failed to register that a projected return higher than the required return is good news. This suggests that, while candidates are getting better at doing CAPM calculations, many still have difficulty in explaining what the results mean. Question 4 (b) asked how a large public limited company may determine its cost of capital. Answers were generally reasonably good, with many explanations of the use of the Gordon dividend growth model for the cost of equity capital, the calculation of the cost of debt (assumed, usually implicitly, to be irredeemable) and the weighted average cost of capital. Some answers mentioned the significance of tax relief on interest. Few answers dealt with the cost of redeemable debt with a market price different from par or preference shares.

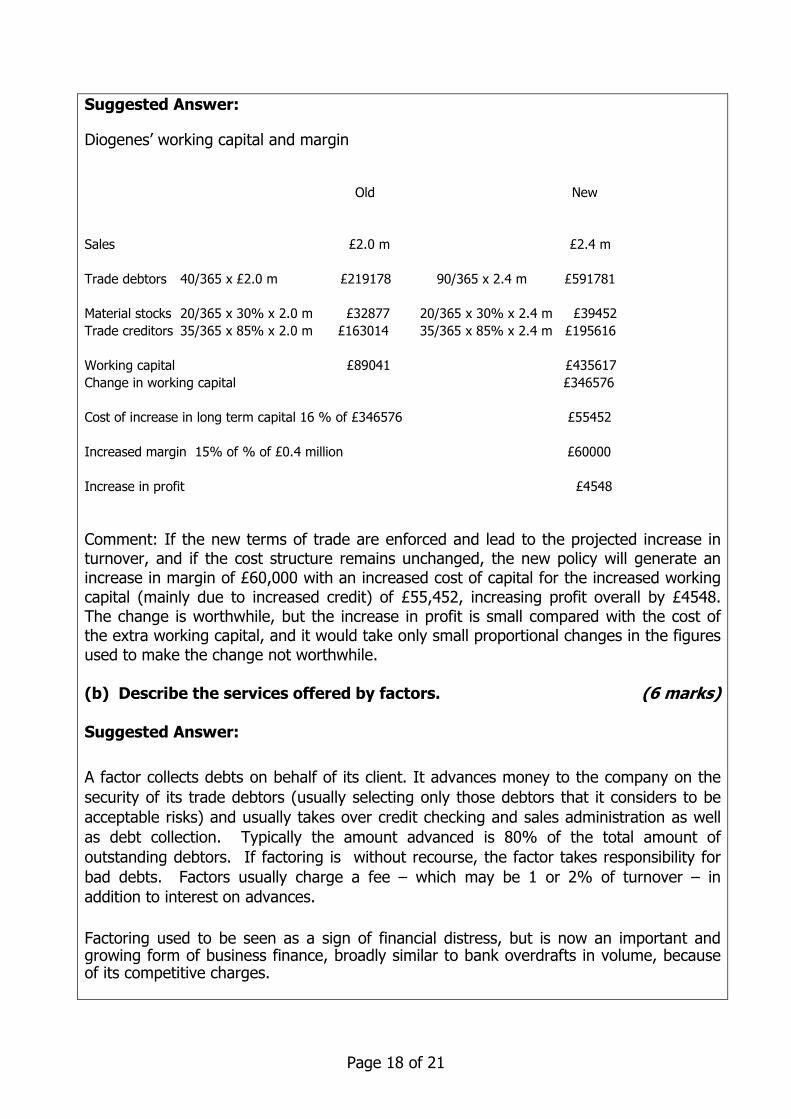

5. (a) Diogenes plc is a small but rapidly growing company providing management services and supplies to IT companies. Since many of its customers are also growing rapidly, and are net consumers of cash, Diogenes is hoping to increase its business by allowing its customers extended credit terms, and is considering giving them 90 days to pay. Its terms of trade are currently net payment in 30 days, but its debtor day figure at present is 40 days. Diogenes believes that it can enforce the new payment terms, and estimates that the new policy will increase its annual turnover by 20% from its present level of £2 million. Diogenes is aware of the risks of overtrading, and plans to finance the increased debtors by raising new long-term capital at a cost of 16%. Diogenes’ material costs are 30% of sales, and the company keeps 20 days’ stock of raw materials. Its stocks of work-in-progress and finished goods are negligible. Other variable costs, related to purchases of services, are 55% of sales. Diogenes receives on average 35 days’ credit from its suppliers. REQUIRED: Calculate the resulting changes in working capital and margin, and comment on whether the proposed change is worthwhile. Evaluate the proposed change. (14 marks)

Page 18 of 21

Suggested Answer:

Diogenes’ working capital and margin Old New Sales £2.0 m £2.4 m Trade debtors 40/365 x £2.0 m £219178 90/365 x 2.4 m £591781 Material stocks 20/365 x 30% x 2.0 m £32877 20/365 x 30% x 2.4 m £39452 Trade creditors 35/365 x 85% x 2.0 m £163014 35/365 x 85% x 2.4 m £195616

Working capital £89041 £435617 Change in working capital £346576 Cost of increase in long term capital 16 % of £346576 £55452 Increased margin 15% of % of £0.4 million £60000 Increase in profit £4548 Comment: If the new terms of trade are enforced and lead to the projected increase in turnover, and if the cost structure remains unchanged, the new policy will generate an increase in margin of £60,000 with an increased cost of capital for the increased working capital (mainly due to increased credit) of £55,452, increasing profit overall by £4548. The change is worthwhile, but the increase in profit is small compared with the cost of the extra working capital, and it would take only small proportional changes in the figures used to make the change not worthwhile. (b) Describe the services offered by factors. (6 marks)

Suggested Answer:

A factor collects debts on behalf of its client. It advances money to the company on the security of its trade debtors (usually selecting only those debtors that it considers to be acceptable risks) and usually takes over credit checking and sales administration as well as debt collection. Typically the amount advanced is 80% of the total amount of outstanding debtors. If factoring is without recourse, the factor takes responsibility for bad debts. Factors usually charge a fee – which may be 1 or 2% of turnover – in addition to interest on advances. Factoring used to be seen as a sign of financial distress, but is now an important and growing form of business finance, broadly similar to bank overdrafts in volume, because of its competitive charges.

Page 19 of 21

A risk of factoring is that a company may lose touch with its customers. In addition, depending on the factor’s approach in collecting debts, there may also be a risk of upsetting customers. Factoring is particularly useful to firms trading in markets that require a considerable period of trade credit and to companies that are expanding rapidly, as it will leave other lines of credit open for use elsewhere in the business. Examiner’s comments:

Relatively few candidates answered this question, and few of those who did produced good answers. Question 5(a) required an evaluation of a proposed change in the terms of trade, with associated changes in working capital. Frequently encountered errors were: not including all the elements of working capital (many answers included only debtors); confusion between changes in the value of material stocks (needed as part of the extra working capital) and the annual cost of materials (as a component of the contribution from extra sales); incorrect calculation of the sales contribution; and failure to use the cost of capital – which was given – to calculate the cost of extra working capital. Most candidates who answered this question made some attempt to comment on what they had calculated.

Question 5 (b) required a straightforward description of what factors do, and was reasonably well answered.

6. (a) Describe the circumstances in which a company may be threatened with liquidation, the actions that it can take to avoid it and the consequences for the present stakeholders. (12 marks) Suggested Answer:

A company that runs short of cash so that it is unable to pay what it owes is at risk of liquidation. (A company may also go into voluntarily liquidation, for example if the objects for which it was set up have been achieved.) A shortage of cash that threatens liquidation may be due to poor profitability or poor cash management, or both. If cash shortages are caused by poor profitability, changes will be needed in the management of the business. This may mean making cost reductions or focusing on the most profitable businesses (in the short term those that generate most cash). It may mean appointing new managers, either by passing a resolution at a general meeting of the company to appoint a new board or by appointing new managers. If the risk of liquidation arises from poor cash management, a rescue package may involve improving the cash situation by reducing working capital. This can be done by reducing stocks, reducing the credit granted to customers and taking increased credit from suppliers (usually by negotiation). Increased working capital can be raised by raising cash against invoices through factors or invoice discounters or, preferably in the short term, by a bank overdraft. Other actions may include deferring capital investment expenditure, using leasing or borrowing rather than cash for capital expenditure and financing working capital increases through debt or equity issues.

Page 20 of 21

A rescue package to avoid liquidation often involves a capital reconstruction scheme. This means raising new capital or converting liabilities into different forms which defer or reduce cash payments (such as payments to suppliers, payments of interest and repayment of loans). Since different kinds of creditors have different requirements, it may be possible to make changes acceptable to all types of creditors by offering each group something that it wants. Trade creditors may be willing to wait for payment if interest is paid on what they are owed, or if the alternative to waiting for payment is a liquidation. in which they may receive nothing. Loan stock holders may be willing to have interest payments increased but deferred, or to exchange some of their loan stock for equity. Equity shareholders who believe that the company has a future may be willing to accept a reduction in the nominal value of their equity and subscribe for more shares. The principle underlying a capital reconstruction is that the company gains the agreement of shareholders and of all classes of creditors to varying their rights by altering the capital structure in a way that allows the company to continue in business and leaves them better off than if the company had been liquidated Secured creditors, who may expect to get their money in the event of a liquidation, may have to be paid in full. A capital reconstruction scheme must treat all groups of shareholders and creditors fairly, and not favour one group over others. This will involve protecting the voting rights of all groups, and as far as possible maintaining their income. Calculations need to be presented to show how the reconstruction protects the interests of each group as compared with their situation in a liquidation. The different classes of creditors and shareholders are placed in order of priority in the event of a liquidation, with secured creditors first and ordinary shareholders last. The order of priority affects how much creditors in each different class stand to receive, and will be a factor in their judgment of whether the capital reconstruction is acceptable

(b) Explain why a company may choose to dispose of one of its businesses by arranging a management buy-out (MBO). (8 marks) Suggested Answer: A company may dispose of a business that it cannot make profitable or which does not fit its corporate strategy because, though profitable, it does not contribute to the achievement of corporate objectives. An MBO is one means of disposing of a business. In an MBO the existing managers buy the business from the parent company, usually raising funds in the form of loans from banks or venture capital companies (who may also take an equity stake so as to share control over management decisions). An MBO provides an alternative to the closure of the business, and the disposal of a going concern is likely to fetch a higher price. An MBO prevents acquisition by a third party who could be a competitor. The staff of the business that is to be disposed of may be more cooperative with management in an MBO than in a sale to a third party. The management team involved in the buy-out are purchasing a business with which they

Page 21 of 21

are familiar. They are likely to know better than any third party buyer what needs to be and can be done to maximise returns. In particular they should be well informed about changes of policy that can be introduced with benefit once constraints imposed by corporate policies are removed. They may therefore be in a position to pay a good price for the business. An MBO allows the management team to be owners rather than employees and, if the business is threatened with closure, an MBO will allow some, at least, of the staff to keep their jobs. If jobs are to be lost, this will happen under the new owners after the MBO rather than under the current management by the parent company before. This may provide the parent company with an exit route that is relatively acceptable in terms of its social impact, or the light in which the parent company is seen. Examiner’s comments: Part (a) was a brief question, which required several aspects to be considered. Few answers covered all the aspects, so there were few very high marks, though most answers were reasonably good. Perhaps most importantly, the question needed comments on possible causes of liquidation (which are not limited to potential insolvency) and to actions that can be taken both to prevent these causes arising and to deal with their consequences if they do. Few answers did all of these things. Perhaps the most frequent omissions were causes of liquidation other than lack of liquidity; and capital reconstruction. Part (b) was similar to (a) in that many candidates did not deal with both the main issues implied by the question. Most answers dealt with the reasons for choosing a Management Buy Out, but fewer explained why a company might choose to dispose of a business. Question 6 was almost universally popular, and moderately well answered. The students who knew the relevant topics, planned their answers and expressed themselves clearly and concisely did best. Many candidates clearly prefer writing essays to doing calculations. It is difficult to pass this examination without doing both.