corporate - icsi.edu

TRANSCRIPT

1

2C O R P O R AT E S O C I A L

R E S P O N S I B I L I T Y

TO

C O M P U L S O R Y S O C I A L

R E S P O N S I B I L I T Y

TODAYS AGENDA

01 04INTRODUCTION

A brief deliberation on the rationale for amendment in Section 135 & the Rules made thereunder

WHATS’ NEXT

Route map on the next course of Action by the Board of Directors & Scope for Professionals

02 05REGULATORY FRAMEWORK

Gist of regulatory framework under Companies Act, 2013 on CSR & Amendments.

RAPID FIRE ROUND- TOP FAQ’S

Intend to capture probable Questionsrunning in the minds of the Participantsand our opinion

03 06AMENDMENTS & ITS IMPACT

A detailed Study of the Amendments , its impact on the Companies to which CSR is applicable.

FLOOR PARTICIPATION

Any further questions and sharing of views, knowledge and experience of the floor

4

Indian Scenario Vs Global Scenario

Rationale for Amendments

Comply or Reply regime to Compulsory Contribution

Responsibility is now being Regulated

01

02

03

04

05

INTRODUCTION

Internal to External

5

CSR – A Business Model or aPhilanthrophy

Now a Punishable Obligation

Spend or Repend

Go with the Intent ..

Scope for Professionals

06

07

08

09

10

INTRODUCTION

SECTION 135 of CA 2013

Sub- Sections 1 to 5

COMPANIES (CSR) RULES, 2014

SCHEDULE VII

Activities which may be included by companies in their CSR Policies

COMPANIES AMENDMENT ACT, 2020

Amendment to Sub- Section 5 & Substitution of Sub-Section 7 & Insertion of Sub- Section 9 to Section 135 of CA 2013

COMPANIES AMENDMENT ACT, 2019

Amendment to Sub- Section 5 & Insertion of Sub- Sections 6,7 & 8 to Section 135 of CA 2013

01

02

03

04

05

Regulatory FrameworkAs amended from time to time

COMPANIES (CSR POLICY) AMENDMENT RULES, 2021

Notified on 22nd January, 2021 vide G.S.R 40 (E)

NOTIFICATION NO. S.O 324 (E) 22/01/2021

NOTIFICATION NO. S.O 325 (E) 22/01/2021

Notifying the Effective date of Cos Amendment 2020 as 22nd

January, 2021

FAQs ON CSR , CIRCULARS, FROM TIME TO TIME

SECTION 450 OF COMPANIES ACT, 2013

06

07

08

09

10

Regulatory Framework

Notifying the Effective date of Cos Amendment 2019 as 22nd January, 2021

8FOOT PRINTS OF CSR AMENDMENTS

Company Law Committee Report.18th November, 2019

Companies Amendment Bill 2020introduced in Lok Sabha.

17th March, 2020

Companies Amendment Bill 2020passed in Lok Sabha

.

19th September, 2020

Companies Amendment Bill 2020passed in Rajya Sabha.

22nd September, 2020

9

Companies Act Bill 2020 received theassent of the President

.

28th September, 2020

Certain Provisions of CompaniesAmendment Act, 2020 notified

21st December, 2020

Further enforcement of CompaniesAmendment Act, 2020..

22nd January,2021

10Analysis of the Amendment of the Act & Rules

IMPACT ASSESSMENT

REGISTRATION OF IMPLEMENTING AGENCIES

DISCLOSURES, REPORTING, BOARD RESPONSIBILITIES

PENAL CONSEQUENCES

MANDATORY SPENDING

CARRY FORWARD OF EXCESS

TRANSFER OF UNSPENT TO FUND

TRANSFER IN CASE OF ONGOING PROJECT

11

Before Amendment After Amendment The Board of every company referred to insub-section (1), shall ensure that thecompany spends, in every financial year, atleast two per cent. of the average net profitsof the company made during the threeimmediately preceding financial years inpursuance of its CSR Policy

The Board of every company referred to insub-section (1), shall ensure that thecompany spends, in every financial year, atleast two per cent. of the average net profitsof the company made during the threeimmediately preceding financial years orwhere the company has not completed theperiod of three financial years since itsincorporation, during such immediatelypreceding financial years, in pursuance of itsCSR Policy

I) Provisions of sub-section (5) of section 135 of the Act.

AMENDMENTS AND ITS IMPACT

12

Before Amendment After Amendment

Provided further that if the company fails tospend such amount, the Board shall, in itsreport made under clause (o) of sub-section(3) of section 134, specify the reasons for onnot spending the amount

Provided further that if the company fails tospend such amount, the Board shall, in itsreport made under clause (o) of sub-section(3) of section 134, specify the reasons for notspending the amount unless the unspentamount relates to any ongoing projectreferred to in sub-section (6), transfer suchunspent amount to a Fund specified inSchedule VII within a period of six months ofthe expiry of the financial year].

13

Before Amendment After Amendment

-

Provided also that if the company spends anamount in excess of the requirements providedunder this sub-section, such company may set offsuch excess amount against the requirement tospend under this sub-section for such number ofsucceeding financial years and in such manner, asmay be prescribed.]

# succeeding 3 Financial years as mentioned inRule 7 of CSR Amendment Rules , 2021

14II) Sub-section (6) in section 135 has been newly inserted - ONGOING PROJECTS

Amendment

Any amount remaining unspent under sub-section (5), pursuant to any ongoing project, fulfillingsuch conditions as may be prescribed, undertaken by a company in pursuance of its CorporateSocial Responsibility Policy, shall be transferred by the company within a period of thirty days fromthe end of the financial year to a special account to be opened by the company in that behalf forthat financial year in any scheduled bank to be called the “Unspent Corporate SocialResponsibility Account”, and such amount shall be spent by the company in pursuance of itsobligation towards the CSR Policy within a period of three financial years from the date of suchtransfer, failing which, the company shall transfer the same to a Fund specified in Schedule VII,within a period of thirty days from the date of completion of the third financial year.

15III) Sub-section (7) in section 135 has been inserted by the CompaniesAmendment Act 2019 and modified by Cos. Amendment Act, 2021 – PENALTYFOR NON TRANSFER

Penalty to the Company :

Liable to a penalty of twice the amount required to the Fund or the Unspent CSRAccount as the case may be, or one crore rupees, whichever is less.

Penalty to the Officers in default :

Every officer shall be liable to a penalty of one-tenth of the amount required to betransferred, or the Unspent Corporate Social Responsibility Account, as the casemay be, or two lakh rupees, whichever is less.";

Penalty for Non spending and also for non transfer of unspent amount to the special account orto the Fund as the case may be as specified under section 135(5) or Section 135(6)

16

IV) Sub-section (8) in section 135 has been inserted by the CompaniesAmendment Act 2019

The Central Government may give such general or special directions to acompany or class of companies as it considers necessary to ensure compliance ofprovisions of this section and such company or class of companies shall complywith such directions.”

This will entitle the CG to give directions from time to time

17V) Sub-section (9) in section 135 has been inserted by the Companies Amendment Act 2020 – Dispensing of CSR Committee

Where the amount to be spent by a company under sub-section (5) does notexceed fifty lakh rupees, the requirement under sub-section (1) for constitution ofthe CSR Committee shall not be applicable and the functions of such Committeeprovided under this section shall, in such cases, be discharged by the Board ofDirectors of such company.”

Dispensing with the requirement of having CSR committee in respect of certaincompanies

18

AMENDMENTS TO CSR RULES 2014COMPANIES (CORPORATE SOCIAL RESPONSIBILITY POLICY) RULES 2021

EXPENDITURE

REPORTING

DEFINITIONS

IMPLEMENTATION

19

Amendments on Definitions

Rule 2 (d) – What is Corporate Social Responsibility ?

Inclusive definition now made exclusive and activities not considered as CSRspecified clearly. Following activities shall not be considered CSR:

1. Activities undertaken in pursuance of normal course of business of the company(except COVID 19 related R & D up to the financial year 2022-23, subject to certain conditions);

2. Any activity undertaken by the company outside India (except for training ofIndian sports personnel representing any State or Union territory at nationallevel or India at international level);

20

Amendments on Definitions….

3. Contribution of any amount directly or indirectly to any political party undersection 182 of the Act.

4. activities that significantly benefit the employees of the company as defined inclause (k) of section 2 of the Code on Wages, 2019 (29 of 2019);

5. activities supported by the companies on sponsorship basis for derivingmarketing benefits for its products or services;

6. activities carried out for fulfilment of any other statutory obligations under anylaw in force in India;

21

CSR POLICY : Rule 2 (f)

CSR Policy shall contain a statement on the :

• approach and direction given by the board of a company, taking intoaccount the recommendations of its CSR Committee;

• guiding principles for selection, implementation and monitoring ofactivities;

• Formulation of the annual action plan.

22

ONGOING PROJECT : Rule 2 (i)

“Ongoing Project” means a multi-year project having timelines notexceeding 3 years excluding the financial year in which it was commenced.

Project that was initially not approved as a multi-year project can be madeongoing by extending the duration beyond one year by the board based onreasonable justification.

It looks that CSR Project duration cannot be more than 03 years.

23

CSR IMPLEMENTATION : Rule 4 ( Previously CSR Activities)

Rule 4 (1) Who can undertake CSR Activities :

Rule 4 (2) Obligation of an Entity which intends to undertake CSR Activity

Rule 4 (3) Engaging International Organization

Rule 4 (4) Collaboration with other companies on CSR Activities

Rule 4 (5) Boards Responsibility

Rule 4 (6) Monitoring on Ongoing Projects by Board

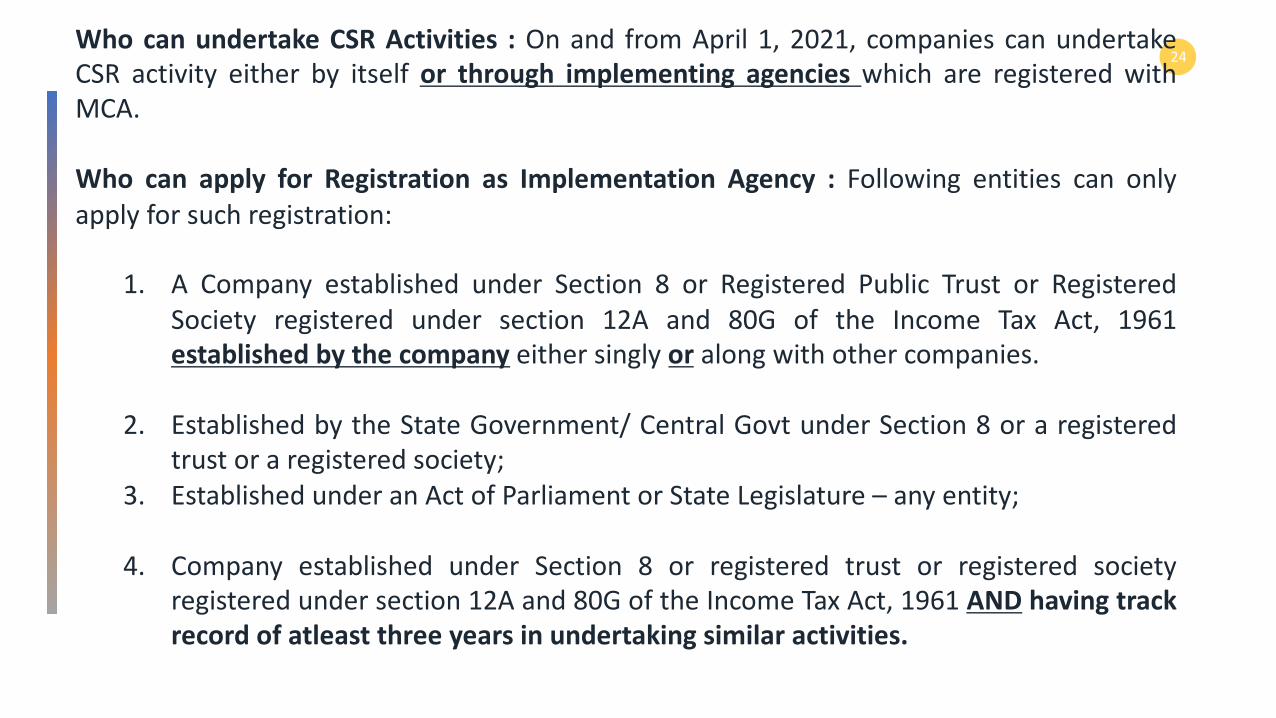

24Who can undertake CSR Activities : On and from April 1, 2021, companies can undertakeCSR activity either by itself or through implementing agencies which are registered withMCA.

Who can apply for Registration as Implementation Agency : Following entities can onlyapply for such registration:

1. A Company established under Section 8 or Registered Public Trust or RegisteredSociety registered under section 12A and 80G of the Income Tax Act, 1961established by the company either singly or along with other companies.

2. Established by the State Government/ Central Govt under Section 8 or a registeredtrust or a registered society;

3. Established under an Act of Parliament or State Legislature – any entity;

4. Company established under Section 8 or registered trust or registered societyregistered under section 12A and 80G of the Income Tax Act, 1961 AND having trackrecord of atleast three years in undertaking similar activities.

25REGISTRATION OF AN IMPLEMENTATION AGENCY :

(a) Every entity, covered under rule 4 (1), who intends to undertake any CSR activity,shall register itself with the Central Government by filing the e-form CSR-1 witheffect from the 01st day of April 2021:

(b) Form CSR-1 shall be verified digitally by a Chartered Accountant in practice or aCompany Secretary in practice or a Cost Accountant in practice.

(c) On the submission of the Form CSR-1, a unique CSR Registration Number shall begenerated by the system automatically.

The provisions of this Rule 4 shall not affect the CSR projects or programmesapproved prior to the 1st day of April 2021.

26ROLE OF INTERNATIONAL ORGANISATIONS :

Rule 2(1)(g) of the Amended Rules defines international organization as anorganization notified by the Central Government as an international organizationunder section 3 of the United Nations (Privileges and Immunities) Act, 1947, towhich the provisions of the Schedule to the said Act apply

The Rules prescribe that companies may engage international organisations fordesigning, monitoring and evaluation of the CSR projects or programmes as per itsCSR policy as well as for capacity building of their own personnel for CSR.

Accordingly, companies can take a call to appoint any other entity to undertake theprescribed overhead jobs in respect of CSR. In any case, the threshold (5% of CSRExpenditure) allowed as administrative overhead will be applicable.

27COLLABORATION WITH OTHER COMPANIES :

A company may also collaborate with other companies for undertaking projects orprogrammes or CSR activities in such a manner that the CSR committees ofrespective companies are in a position to report separately on such projects orprogrammes in accordance with these rules.

The Board of a company shall satisfy itself that the funds so disbursed have beenutilised for the purposes and in the manner as approved by it and the ChiefFinancial Officer or the person responsible for financial management shall certifyto the effect.

In case of ongoing project, the Board of a Company shall monitor theimplementation of the project with reference to the approved timelines and year-wise allocation and shall be competent to make modifications, if any, for smoothimplementation of the project within the overall permissible time period.

28CSR EXPENDITURE. -

(1)administrative overheads shall not exceed five percent of total CSR expenditure

(2) Any surplus arising out of the CSR activities shall not form part of the businessprofit and shall be ploughed back into the same project or transferred to the UnspentCSR Account and spent in pursuance of CSR policy and annual action plan of thecompany or transfer such surplus amount to a Fund specified in Schedule VII, within aperiod of six months of the expiry of the financial year.

(3) Where a company spends an amount in excess of requirement such excess amountmay be set off against the requirement to spend up to immediate succeeding threefinancial years subject to the conditions that –(i) the excess amount available for set off shall not include the surplus arising out of

the CSR activities,(ii) the Board of the company shall pass a resolution to that effect.

29CREATION OR ACQUISITION OF CAPITAL ASSET :

The CSR amount may be spent by a company for creation or acquisition of a capital asset,which shall be held by –

(a) a company established under section 8 or a Registered Public Trust or RegisteredSociety, having charitable objects and CSR Registration Number or

(b) beneficiaries of the said CSR project, in the form of self-help groups, collectives, entities;or(c) a public authority as defined under 2 (h) of RTI Act, 2005:

Provided that any capital asset created by a company prior to the commencement of theCos (CSR Policy) Amendment Rules, 2021, shall within a period of 180 days from suchcommencement comply with the requirement of this rule, which may be extended by afurther period of not more than 90 days with the approval of the Board based onreasonable justification.

30CSR REPORTING :

(1) The Board's Report of a company shall include an Annual report on CSR containing particulars specified inAnnexure I [For the FY upto 31.03. 2020]or Annexure II [For the FY after31.03. 2020], as applicable.

(2) In case of a foreign company, the balance sheet filed under clause (b) of sub-section (1) of section 381 ofthe Act, shall contain an annual report on CSR containing particulars specified in Annexure I or Annexure II, asapplicable.

(3) (a) Every company having average CSR obligation of ten crore rupees or more in the three immediatelypreceding financial years, shall undertake impact assessment, through an independent agency, of their CSRprojects having outlays of one crore rupees or more, and which have been completed not less than one yearbefore undertaking the impact study.

(b) The impact assessment reports shall be placed before the Board and shall be annexed to the annual reporton CSR.(c) A Company undertaking impact assessment may book the expenditure towards Corporate SocialResponsibility for that financial year, which shall not exceed five percent of the total CSR expenditure for thatfinancial year or fifty lakh rupees, whichever is less.

31DISPLAY OF CSR ACTIVITIES ON ITS WEBSITE.

The Board of Directors of the Company shall mandatorily disclose the composition of theCSR Committee, and CSR Policy and Projects approved by the Board on their website, if any,for public access.

Transfer of unspent CSR amount.

Until a fund is specified in Schedule VII for the purposes of subsection (5) and(6) of section 135 of the Act, the unspent CSR amount, if any, shall be transferred by the company to any fund included in schedule VII.

1.Clean Ganga Fund2. Prime minister's national relief fund3. Prime Minister’s Citizen Assistance and Relief in Emergency Situations Fund (PM CARES Fund)

32

WHAT’S NEXT- BOARDS’ PERSPECTIVE

ONGOING PROJECT

ANNUAL ACTION PLAN

TRANSFER OF FUNDS

CAPITAL ASSET

CSR POLICY

33WHAT’S NEXT – NEXT COURSE OF ACTION BY THE BOARD

01

02

03

To amend CSR Policy –Recommendation of CSR Committee(CSRC) and approval of the BoD will be required

To formulate an Annual Action Plan for FY 21-22-Recommendation of CSRC and approval of the BoD will berequired .

To calculate the minimum CSR Spending to be done for FY 21after considering the current CSR activitiesTo see if there will be any deficit in the spending

34WHAT’S NEXT – NEXT COURSE OF ACTION BY THE BOARD

04

05

06

If there is any such ongoing project, then open a bank account(Unspent CSR Account) and transfer the deficit amount towithin 30 days of end of FY 20-21

If there is no such ongoing project, then transfer the deficit amount to the Fund within 6 months from end FY20-21

To Check the type of implementing agency through which CSRactivities are undertaken. Also, to ensure their registrationunder section 12A and 810G Income Tax ACt,1986 as requiredunder Rule 4(1)’’

35WHAT’S NEXT – NEXT COURSE OF ACTION BY THE BOARD

07

08

09

As the implementing agencies shall be required to beregistered with MCA w.e.f 1.4.2021, the Board may initiateaction and intimate the existing implementing agencies andensure its registration

Monitoring of “on-going” projects as per approved timelinesand year wise allocation; Placing of certificate of CFO/authorized person about utilisation of CSR fund.

CSR Committee to revisit its budget for FY 2020-21 so as toalign with the requirements of the annual action plan

36WHAT’S NEXT – NEXT COURSE OF ACTION BY THE BOARD

10

11

12

To check if there is any excess spent done – then the same is tobe set off within three immediate subsequent FYs – a boardresolution has to be passed. Should be placed before CSRC aswell.

To check if there is any capital asset created by the companyfor undertaking CSR expenditure and take necessary action fortransfer of capital asset if any

To check if there is any profit arising out of CSR expenditureand to either plough back or transfer to the unspent CSR A/cor transfer to the fund within 6 months from the end of FY

37WHAT’S NEXT – NEXT COURSE OF ACTION BY THE BOARD

13

14

15

Annual CSR Report to be prepared as per the revised formatalong with the Impact Assessment Report and to be placedbefore CSRC as well as the BoD

To check impact assessment applicability on the company andto take necessary action .

Website disclosures Composition of the CSR Committee;CSR Policy and Projects approved by the Board

38WHAT’S NEXT – SCOPE FOR PROFESSIONALS

POLICY REDRAFTING

STRATEGY- SPENDING / IDENTIFYING PROJECTS/ INDENTIFYING

IMPLEMENTATION AGENCY

ADJUDICATION & APPEALS – UPON NON COMPLIANCE

ASSIST THE BOARD TO IMPLEMENT CSR IN LINE WITH AMENDMENTS

ASSESSMENT OF CSR EXPENDITURE AND ADVISE ON TRANSFER OF UNSPENT

ASSISTANCE IN REGISTRATION OF IMPLEMENTING AGENCY/ MONITORING OF AGENCY

39FAQ’s – Rapid Fire Round P R O B A B L E Q U E S T I O N S I N O U R M I N D

AREA OF SPENDING ?

CAPITAL ASSET ?

TRANSFER OF FUNDS ?

IMPLEMENTING AGENCY

NON COMPLAINCE PENALTY? IMPACT ASSESSMENT ?

REGISTRATION OF AGENCY POLICY REDRAFTING ?

FAQ’SP R O B A B L E Q U E S T I O N S I N O U R M I N D

Are the Amendments retrospective?

Is the penal proceedings is in addition to the obligation totransfer the unspent amount?

What are the consequenses of non compliances apart from non- spending / non- transfer ?

Apart from transfer of the unspent amount, whether theBoard will still be required to provide a reason for notspending the required CSR amount?

FAQ’SP R O B A B L E Q U E S T I O N S I N O U R M I N D

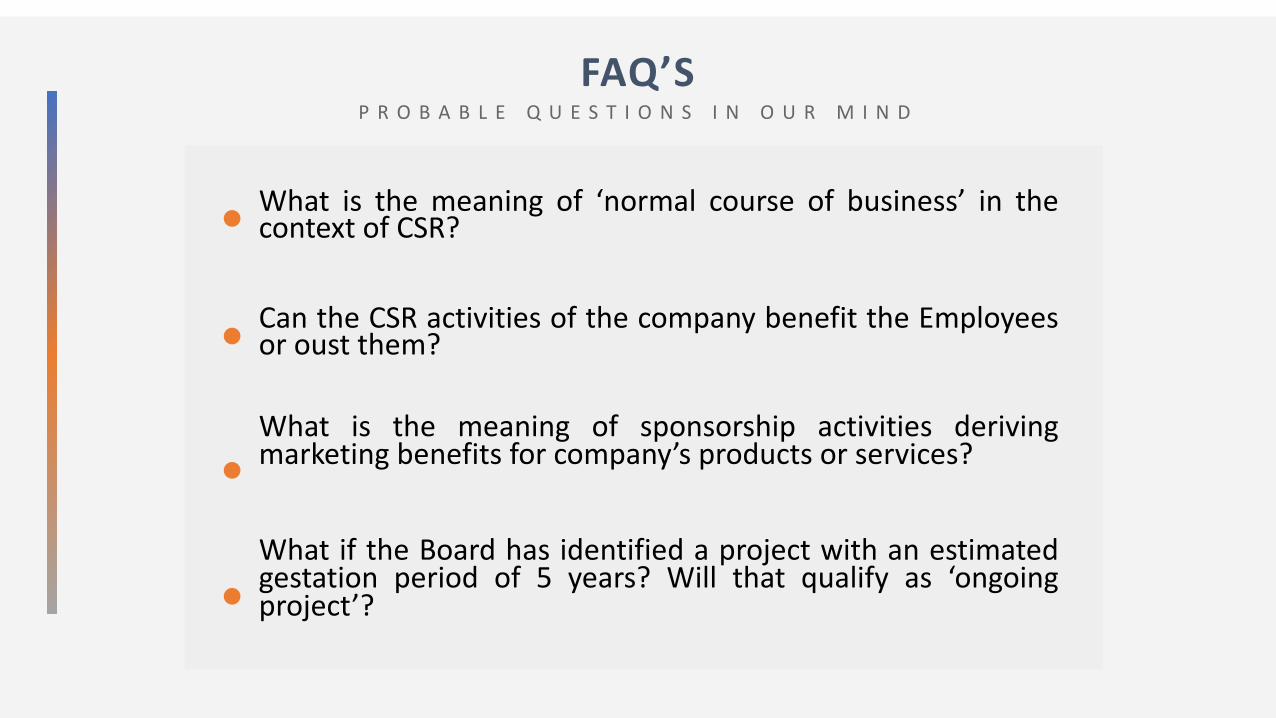

What is the meaning of ‘normal course of business’ in thecontext of CSR?

Can the CSR activities of the company benefit the Employeesor oust them?

What is the meaning of sponsorship activities derivingmarketing benefits for company’s products or services?

What if the Board has identified a project with an estimatedgestation period of 5 years? Will that qualify as ‘ongoingproject’?

FAQ’SP R O B A B L E Q U E S T I O N S I N O U R M I N D

Whether amount transferred to a third party implementingagency (Intermediary) for a project will that be considered asan ongoing project?

Is non-spending considered as non-compliance postamendments coming into force? What will be the role ofauditor on non-compliance? Will he qualify his report?

Whether the benefit of carrying forward will be available to acompany that had zero CSR expense to be incurred onaccount of losses, however, voluntarily incurred certain CSRexpenses?Are all companies who are mandated to undertake CSRexpenditure as per the specified criteria under section 135(5)of the Act, required to have a CSR Committee under section135(1) of the Act ?

FAQ’SP R O B A B L E Q U E S T I O N S I N O U R M I N D

What are the modes of implementing CSR activities availablewith the company post the amendments coming into effect?

Whether all three types of bodies - a section 8 company or aregistered public trust or a registered society, is required tohave income-tax registration u/s 12A as well as 80G of theIncome Tax Act, 1961?

Is it mandatory for the companies to engage suchinternational organizations? Can they undertake CSR onbehalf of Company

What are the other impacts of Non- Compliances apart fromPenalty ?

FAQ’SP R O B A B L E Q U E S T I O N S I N O U R M I N D

Whether the company is required to undertake impactassessment on a regular basis ?

Whether companies are required to undertake impactassessment for FY 2020-21

Who can conduct impact assessment ?

Can the CSR amount be spent within the 6 months periodavailable for transfer of Unspent to Unspent A/c ?

.

-JANIE LEWAS

CS & IP SRIRAM PARTHASARATHY PRACTISING COMPANY SECRETARY