preface - icsi.edu

TRANSCRIPT

1

PREFACE Checklists are often used as a tool for performing tasks in a structured and step wise manner for day to day affairs as well as critical professional assignments. Use of checklist not only bring efficiency in work performed by the professionals but also reduces the risk of non-compliances to a great extent. With the evolving legal structure and compliances, the significance of checklist is now more critical for professional assignments and scheduling of tasks in an organised manner. Understanding the need for uniformity in compliance by the professionals while performing their duties and responsibilities under the Companies Act, 2013, the Institute has taken a novel initiative by bringing out a series of checklist compendium under the Companies Act, 2013 and rules made thereunder. The Research wing of ICSI-Centre for Corporate Governance, Research and Training (ICSI-CCGRT) has developed a unique series of e-bulletin titled ‘Ease of Audit – Companies Act 2013 Checklist Compendium’. This issue of e-bulletin specifically covers various aspects enshrined under “Chapter-IX Accounts of Companies and Chapter-XI Appointment and Qualifications of Directors” of the Companies Act 2013 (“the Act”) and relevant rules made thereunder. Based on these provisions, a comprehensive checklist is presented in a lucid manner to facilitate the compliance of law by professionals. The main objective of bringing out this e-bulletin is to serve as a ready reckoner for the professionals. I am sure that this e-bulletin will certainly help the professionals in ensuring compliance as well as identifying section-wise audit questions and supporting documents to be cross-checked for verification of compliance. I would like to acknowledge the efforts and contribution of CS Devendra Deshpande, Vice-President ICSI and the past Chairman, ICSI-CCGRT Management Committee for bringing out the idea and CS Chetan B. Patel, Chairman, ICSI-CCGRT Management Committee for taking the pursuit forward and the team, ICSI-CCGRT for completing the assignment. I convey my special appreciation and acknowledgement to Dr. K S Ravichandran for taking up the task and guiding the team including the reviewer group comprising of eminent experts CS Mahesh Athavale, CS Amit Gupta, CS Bhumitra Vinodchandra Dholakia, CS Kalidas Ramaswami, CS Narayan Shankar, CS (Dr.) S. Chandrasekaran and CS Satish Panditrao Bhattu for devoting their valuable time in reviewing this publication. I also acknowledge the efforts put in by team of professionals empanelled with ICSI

CCGRT for undertaking research work at ground level and preparing the draft

checklists for consideration of reviewer group. I am happy to note that the upcoming

series of this e-bulletin on a chapter-wise basis will be released in the days to come

and a comprehensive publication comprising all such checklists will be released

separately at an appropriate occasion.

To facilitate the stakeholders, the checklist issued under this initiative of ICSI will be made available at the ICSI-CCGRT research initiative portal https://www.icsi.edu/ccgrt/research-initiatives-2/. I request all my professional colleagues to ensure compliance of law in the light of this publication and promote good Corporate Governance. Improvement is a continuous process and therefore, suggestions of the readers to improve this publication are most welcome.

CS Nagendra D. Rao President

The Institute of Company Secretaries of India

FOREWORD

न कर्मणार्नारम्भान्नैष्कम्य ंपुरुषोऽश्नुते। न च संन्यसनादेव ससद्ध ंसर््धगच्छतत॥

[No man can attain freedom from activity by refraining from action;

nor can he reach perfection by merely refusing to act]

- Bhagvad Gita Chapter 3, verse 4

This verse of Bhagvad Gita perfectly fits the moment, the present times, the uncertainty entailing and the measures and counter initiatives undertaken by all of us as individuals, as professionals and even as professional bodies & institutions in this regard. At present, COVID Pandemic has thrown challenges before everyone, individuals as well as institutions in performing the activities. Rather to say, the present situation has changed era of work culture. There is always two sides of coin and the same is applicable to current scenario as well. This pandemic has put the mankind in very challenging situation of survival but simultaneously it has taught us the lessons to live and work in a way which we never done before. The productive use of technology, work from home, adapting to change, etc. are the direct products of the present pandemic. With the Government introducing and launching initiatives like the Aatmanirbhar Bharat, the role of professionals, especially Governance Professionals has heightened, now more than ever before. I am proud that the professional institute like The Institute of Company Secretaries of India continued to play the pivotal role in the development and growth of the professionals even in the challenging pandemic situation. Understanding the need for dedicated support structure in place for the Company Secretaries to perform their duties and responsibilities with diligence and ensure compliance across the length and breadth of India Inc., the ICSI-CCGRT has done commendable efforts to launch “Ease of Audit – Companies Act 2013 Checklist Compendium”. The chapter-wise checklist on Companies Act 2013 with relevant rules made thereunder will be very useful to Practicing Company Secretaries for audit assignments and employee Company Secretaries for creating better compliance structure in the company.

CS Chetan B. Patel Chairman, ICSI-CCGRT Management Committee

5

CHECKLIST FOR CHAPTER ON ACCOUNTS OF COMPANIES

[CHAPTER IX of the COMPANIES ACT, 2013 covering Sections 128 to 138]

Notes:

1. This checklist is purely based on provisions of the Act and rules thereto. It

does not include any reference to SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 or any other law or rules and regulations that may apply to the subject matter of Chapter IX of the Act.

2. This checklist is intended to serve a ready referencer for company

secretaries in employment as well as those in practice. In other words, it is to be applied by persons who are qualified members of the Institute of Company Secretaries of India (ICSI).

3. This checklist takes into account amendments to the provisions and rules

up to 27th September, 2021. 4. While every care has been taken to incorporate all the applicable

provisions and the rules falling with the subjects covered by Chapter IX, it is possible that a particular aspect or point has not been factored. Hence, if any reader notices anything that ought to have been incorporated in this checklist, it may please be brought to the knowledge of CCGRT of ICSI for consideration and necessary action as may be desirable.

5. This checklist does not cover provisions of the Act pertaining exclusively to small companies, one person companies, Nidhis and Section 8 companies.

6. This checklist is not intended to serve as a fool proof document to insulate

members from any professional liability. Members are required to apply the same with due diligence and care as is expected of professionals.

Legends

Companies Act, 2013 – the Act

The Companies (Accounts) Rules. 2014 - The Rules

The Companies (Corporate Social Responsibility Policy) Amendment Rules,

2021 – The CSR Rules

Secretarial Standard 1 - SS1

Board – Board of Directors of the Company as per Section 149 of the Act

Registrar of Companies – ROC

6

Financial Year – FY

Annual General Meeting - AGM

FSs – FS

Consolidated FSs - CFS

Books of Accounts – BOA

Corporate Social Responsibility – CSR

Chief Financial Officer – CFO

National Company Law Tribunal - NCLT Class of Company Code

Private Company –PVC

Unlisted Public Company – UPC

Listed Company – LC

Foreign Company – FC

All Companies –AC

CSR Companies – Companies that meet any of the thresholds specified in Section 135 of the Act

IFSC Public Company – IFSC PC - A public company which is licensed to operate by the RBI or SEBI or IRDAI from the International Financial Services Centre located in an approved multi services Special Economic Zone set-up under the Special Economic Zones Act, 2005 (28 of 2005) r/w the Special Economic Zones Rules, 2006.

IFSC Private Company – IFSC PVC - A private company which is licensed to operate by the RBI or SEBI or IRDAI from the International Financial Services Centre located in an approved multi services Special Economic Zone set-up under the Special Economic Zones Act, 2005 (28 of 2005) r/w the Special Economic Zones Rules, 2006.

Government Company – GC - 45) "Government company" means any company in which not less than fifty-one per cent of the paid-up share capital is held by the Central Government, or by any State Government or Governments, or partly by the Central Government and partly by one or more State Governments, and includes a company which is a subsidiary company of such a Government company. ["paid up share capital" shall be construed as "total voting power", where shares with differential voting rights have been issued.]

“Startup” means startup company, as defined in Notification No. GSR. 127(E), dated the 19th February, 2019 issued by the Department for Promotion of Industry and Internal Trade, Ministry of Commerce and Industry, Government of India, may issue sweat equity shares not exceeding fifty percent of its paid- up capital up to 10 years from the date of its incorporation or registration.

7

Activity Code

Data Collection Question –DCQ

Audit Question -AQ

THE CHECKLIST FOR CHAPTER IX

(SECTIONS 128 to 138 OF THE ACT

&

RULE 1 to 13 OF THE RULES

&

RULE 1 to 10 OF THE CSR RULES)

SL.

NO.

SECTION /

RULE /

NOTIFICATION

APPLICA

BLE

COMPAN

Y

ACTIVITY

CODE

QUESTION SOURCE

DOCUMENT

1. S128(1) and (2) AC AQ Check if the company and

its branch if any,

maintains proper BOA on

accrual basis and

according to the double

entry system and the

branch office periodically

sends the summarized

returns to the company.

Where the company is

not maintaining its BOA at

its Registered Office

check if the company has

notified the same in

advance to the ROC in

the prescribed manner.

Where the BOA is

maintained in electronic

form, check if the

company takes care of

prescribed safeguards

such as having proper

Management

representation, if

any;

Disclosures in the

FS and Auditors

Report;

AOC-5;

Note: PCS is not

expected to ensure

that the company

maintains proper

books of account in

all respects. A

limited

responsibility falls

on the CS in whole-

time employment of

the company as CS

must sign the FS

once approved by

the Board.

Note 2: Note:

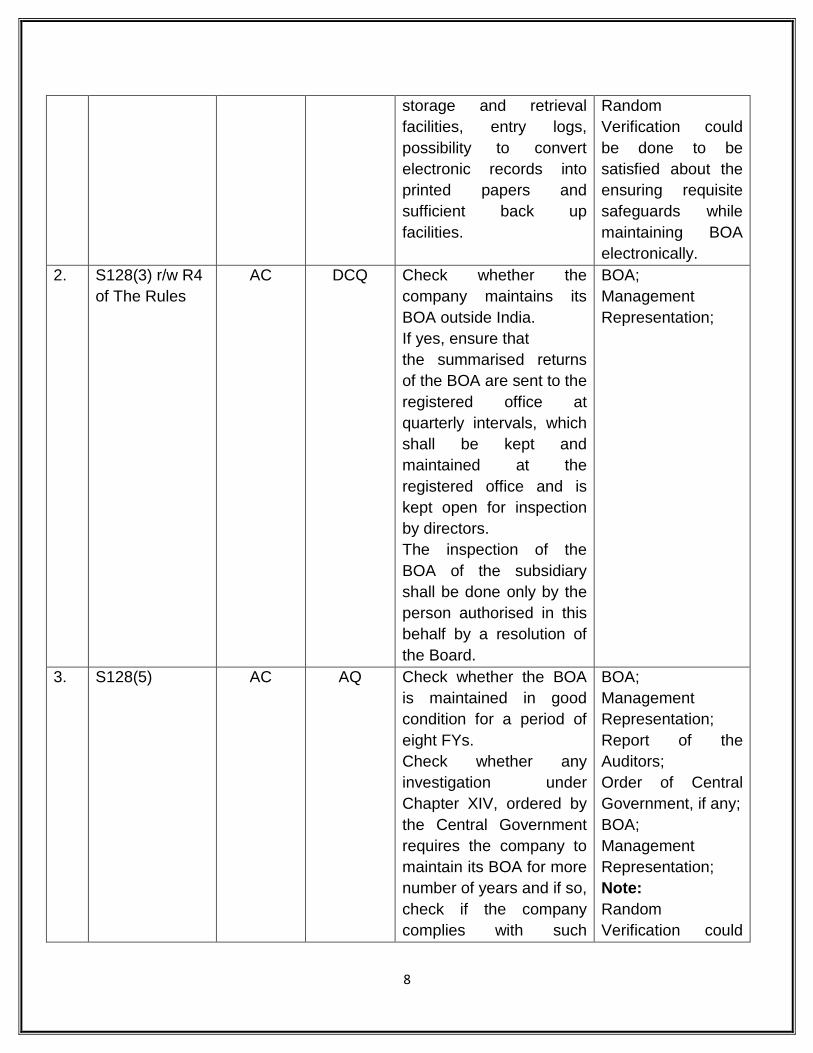

8

storage and retrieval

facilities, entry logs,

possibility to convert

electronic records into

printed papers and

sufficient back up

facilities.

Random

Verification could

be done to be

satisfied about the

ensuring requisite

safeguards while

maintaining BOA

electronically.

2. S128(3) r/w R4

of The Rules

AC DCQ Check whether the

company maintains its

BOA outside India.

If yes, ensure that

the summarised returns

of the BOA are sent to the

registered office at

quarterly intervals, which

shall be kept and

maintained at the

registered office and is

kept open for inspection

by directors.

The inspection of the

BOA of the subsidiary

shall be done only by the

person authorised in this

behalf by a resolution of

the Board.

BOA;

Management

Representation;

3. S128(5) AC AQ Check whether the BOA

is maintained in good

condition for a period of

eight FYs.

Check whether any

investigation under

Chapter XIV, ordered by

the Central Government

requires the company to

maintain its BOA for more

number of years and if so,

check if the company

complies with such

BOA;

Management

Representation;

Report of the

Auditors;

Order of Central

Government, if any;

BOA;

Management

Representation;

Note:

Random

Verification could

9

orders. be done to be

satisfied about this

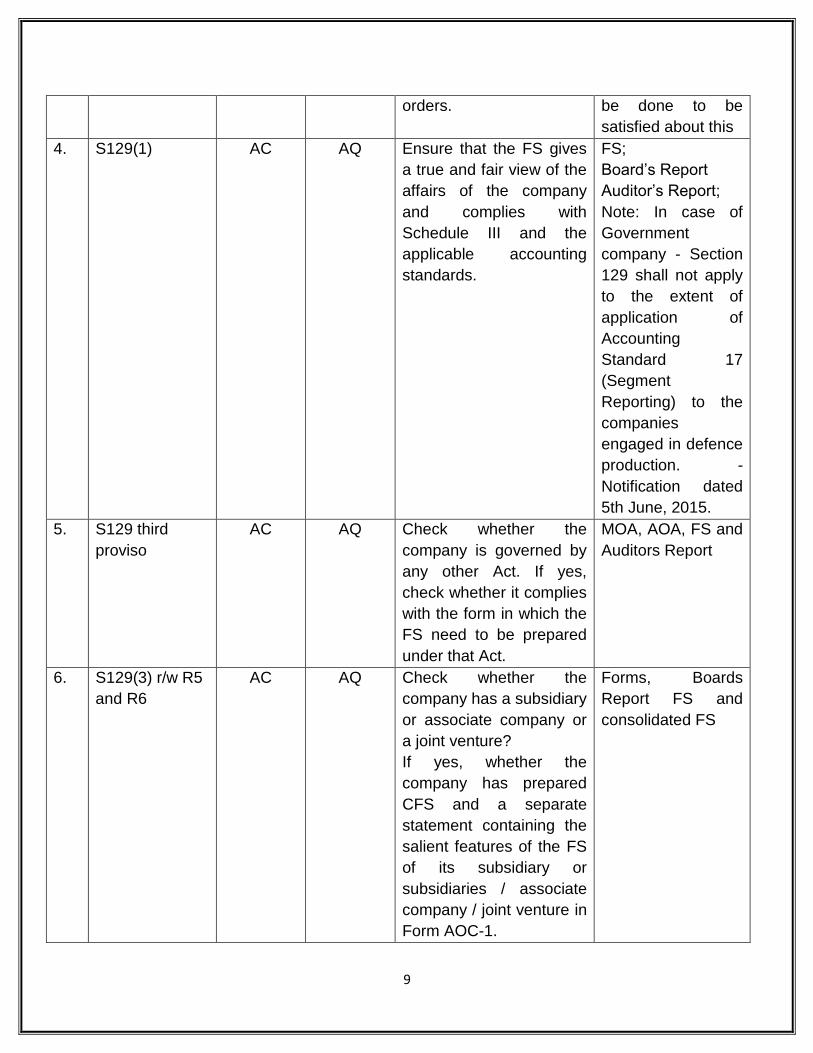

4. S129(1) AC AQ Ensure that the FS gives

a true and fair view of the

affairs of the company

and complies with

Schedule III and the

applicable accounting

standards.

FS;

Board’s Report

Auditor’s Report;

Note: In case of

Government

company - Section

129 shall not apply

to the extent of

application of

Accounting

Standard 17

(Segment

Reporting) to the

companies

engaged in defence

production. -

Notification dated

5th June, 2015.

5. S129 third

proviso

AC AQ Check whether the

company is governed by

any other Act. If yes,

check whether it complies

with the form in which the

FS need to be prepared

under that Act.

MOA, AOA, FS and

Auditors Report

6. S129(3) r/w R5

and R6

AC AQ Check whether the

company has a subsidiary

or associate company or

a joint venture?

If yes, whether the

company has prepared

CFS and a separate

statement containing the

salient features of the FS

of its subsidiary or

subsidiaries / associate

company / joint venture in

Form AOC-1.

Forms, Boards

Report FS and

consolidated FS

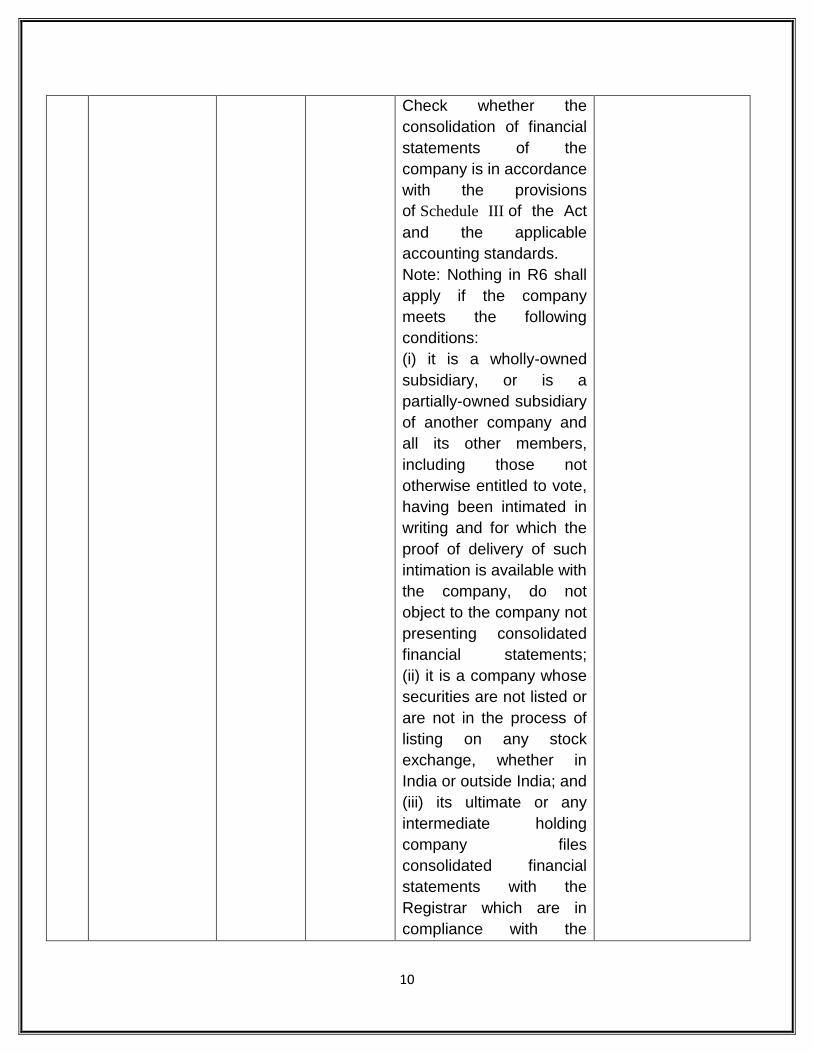

10

Check whether the

consolidation of financial

statements of the

company is in accordance

with the provisions

of Schedule III of the Act

and the applicable

accounting standards.

Note: Nothing in R6 shall

apply if the company

meets the following

conditions:

(i) it is a wholly-owned

subsidiary, or is a

partially-owned subsidiary

of another company and

all its other members,

including those not

otherwise entitled to vote,

having been intimated in

writing and for which the

proof of delivery of such

intimation is available with

the company, do not

object to the company not

presenting consolidated

financial statements;

(ii) it is a company whose

securities are not listed or

are not in the process of

listing on any stock

exchange, whether in

India or outside India; and

(iii) its ultimate or any

intermediate holding

company files

consolidated financial

statements with the

Registrar which are in

compliance with the

11

applicable Accounting

Standards.

(iv) nothing in this rule

shall apply in respect of

consolidation of financial

statement by a company

having subsidiary or

subsidiaries incorporated

outside India only for the

financial year

commencing on or after

1" April, 2014.

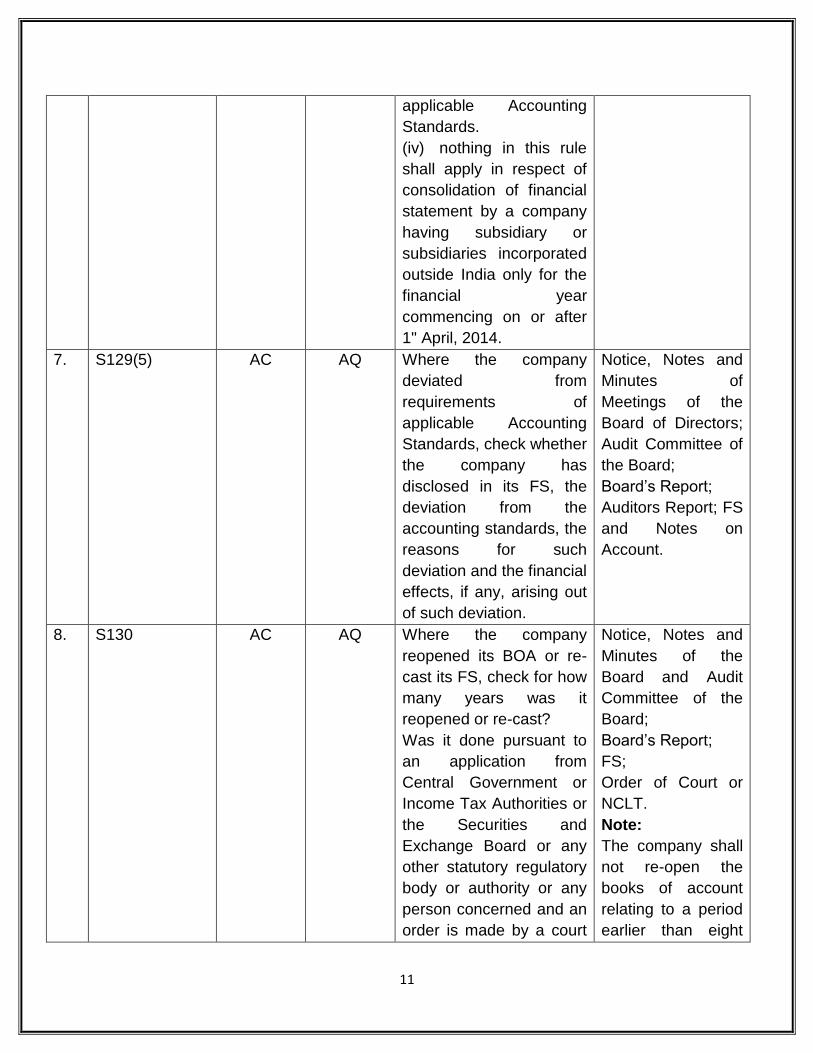

7. S129(5) AC AQ Where the company

deviated from

requirements of

applicable Accounting

Standards, check whether

the company has

disclosed in its FS, the

deviation from the

accounting standards, the

reasons for such

deviation and the financial

effects, if any, arising out

of such deviation.

Notice, Notes and

Minutes of

Meetings of the

Board of Directors;

Audit Committee of

the Board;

Board’s Report;

Auditors Report; FS

and Notes on

Account.

8. S130 AC AQ Where the company

reopened its BOA or re-

cast its FS, check for how

many years was it

reopened or re-cast?

Was it done pursuant to

an application from

Central Government or

Income Tax Authorities or

the Securities and

Exchange Board or any

other statutory regulatory

body or authority or any

person concerned and an

order is made by a court

Notice, Notes and

Minutes of the

Board and Audit

Committee of the

Board;

Board’s Report;

FS;

Order of Court or

NCLT.

Note:

The company shall

not re-open the

books of account

relating to a period

earlier than eight

12

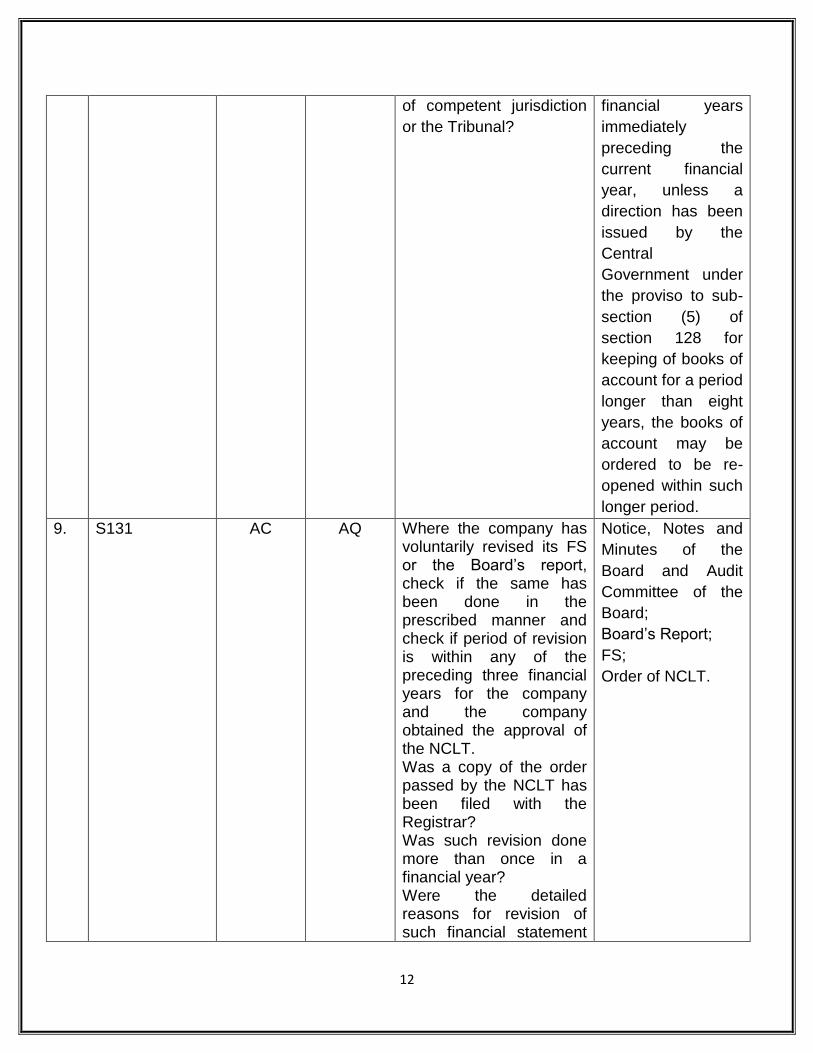

of competent jurisdiction

or the Tribunal?

financial years

immediately

preceding the

current financial

year, unless a

direction has been

issued by the

Central

Government under

the proviso to sub-

section (5) of

section 128 for

keeping of books of

account for a period

longer than eight

years, the books of

account may be

ordered to be re-

opened within such

longer period.

9. S131 AC AQ Where the company has voluntarily revised its FS or the Board’s report, check if the same has been done in the prescribed manner and check if period of revision is within any of the preceding three financial years for the company and the company obtained the approval of the NCLT. Was a copy of the order passed by the NCLT has been filed with the Registrar? Was such revision done more than once in a financial year? Were the detailed reasons for revision of such financial statement

Notice, Notes and

Minutes of the

Board and Audit

Committee of the

Board;

Board’s Report;

FS;

Order of NCLT.

13

or Board’s report disclosed in the Board's report in the relevant financial year in which such revision was made? Were the financial statements or Board’s report already sent to members or to the Registrar or been laid before the general meeting prior to the revision? If yes, were the revisions

confined to: (a) non-

compliances under

sections 129 or 134 and

(b) necessary for

consequential

alternation?

10. S134(1) AC AQ Check whether Board has duly approved the FS, including CFS, and if they have been duly signed by persons authorised in that behalf?

Minutes of meeting

of the Board where

the FS was

approved;

FS;

Note: if any, as approved by the Board are signed on behalf of the Board by (a) the chairperson of the company where he is authorised by the Board or, 2 directors out of which one shall be MD, if any, and (b) the CEO, the CFO and the CS of the company, wherever they are appointed

11. S134(3), (5) r/w

R8 of The

Rules and

AC AQ Ensure that the Boards Report contains the following: (1) Summary of

Board’s Report;

Note: If any

information listed in

14

Standard 9 of

SS1

financial performance based on FS on standalone basis; (2) Highlights of performance and financial position of each Subsidiaries / Associates/ Joint Venture Companies and their contribution to the overall performance of the company during the period under report; (3) State of company’s affairs; (4) Material changes and commitments if any, affecting the financial position of the company during the year; (5) Change in nature of business; (6) Amounts if any, which the which the company proposes to carry any reserves; (7) Amount, if any, which the Board recommends as dividend pay-out; (8) Name of the companies which have become or ceased as Subsidiaries / Associates / Joint Venture Companies during the year; (9) Details of deposits and deposits accepted not in compliance with Chapter V; (10) Particulars of loans / guarantees / investments under Section 186; (11) Details of directors, KMP, appointed / ceased

S134(3) is provided

in the financial

statement, the

company may not

include such

information in the

report of the Board

of Directors.

[S134(3) r/w

Notification dated

4th January, 2017.]

15

during the year; (12) Number of meetings of the Board; (13) Vigil Mechanism / Whistle Blower Policy; (14) CSR policy and details of initiatives by the committee; (15) Risk Management Policy; (16) Particulars of contracts / arrangements with related parties as per AOC-2; (17) Conservation of energy, technology absorption and foreign exchange earnings and outgo; (18) Web address, if any, where annual return (Form MGT-7) referred to in sub-section (3) of section 92 is uploaded; (19) Details of material orders of courts, Tribunals, authorities, Regulators imposing penalties on the company; (20) Directors Responsibility Statement; (21) Statement on compliance with Secretarial Standards; (22) Explanation or comments by the Board on every qualification / reservation / adverse remark / disclaimer by statutory auditor in his report; (23) Explanation or comments by the Board on every qualification / reservation / adverse

16

remark / disclaimer by secretarial auditor in his report;

12. S134(3)(e), (p) AC

(except

GC and

PVC)

AQ Check whether the Boards Report contains (a) Company’s policy on attributes for directors’ appointment and remuneration criteria for directors, key managerial personnel and other employees as provided under 178(3); (b) Formal annual evaluation of Board on its own performance and that of its committees and individual directors

Board’s Report

13. S134(3)(q), (d)

r/w R8,

S177(8), S197

AC

(except

PVC)

AQ Check whether Board’s Report contains (a) Statement regarding opinion of the Board with regard to integrity, expertise and experience (including the proficiency) of the independent directors appointed during the year; (b) Statement on declaration of Independence given by Independent Directors under Section 149(7) of the Act; (c) Composition of Audit Committee; (d) where the Board has not accepted any of the recommendations of the said committee, reasons for Board not accepting any recommendation of Audit Committee; and (e) Details of Managerial Remuneration

Board’s Report

14. S134(5) AC AQ Check whether the Directors Responsibility Statement states

Board’s Report

17

declarations that (a) in the preparation of the annual accounts, the applicable accounting standards had been followed along with proper explanation relating to material departures; (b) the directors had selected such accounting policies and applied them consistently and made judgments and estimates that are reasonable and prudent so as to give a true and fair view of the state of affairs of the company at the end of the financial year and of the profit and loss of the company for that period; (c) the directors had taken proper and sufficient care for the maintenance of adequate accounting records in accordance with the provisions of this Act for safeguarding the assets of the company and for preventing and detecting fraud and other irregularities; (d) the directors had prepared the annual accounts on a going concern basis; and (e) the directors, in the case of a listed company, had laid down internal financial controls to be followed by the company and that such internal financial controls are adequate and were operating effectively.

15. S134(7) AC AQ Check whether the signed FS

18

copy of every FS, including CFS, if any, is issued, circulated or published along with a copy each of (a) any notes annexed to or forming part of such financial statement; (b) the auditor’s report; and (c) the Board’s Report

16. S135(1) r/w R1,

R5(1)

AC and

FC

DCQ Check whether the provisions of Section 135 of the are applicable to the company?

Note: CSR provisions are applicable to companies having - - net worth of rupees five hundred crore or more, or - turnover of rupees one thousand crore or more or - a net profit of rupees five crore or more during the immediately preceding financial year [Also applies to its holding or subsidiary, having its branch office or project office in India, which fulfils the above-mentioned criteria] Note 2: Section 135 shall not apply for a period of five years from the commencement of business of a Specified IFSC public company

17. S135(2) CSR

Companie

AQ Check if the company has constituted the Corporate

Notice, Notes and

Minutes of

19

s Social Responsibility Committee of the Board consisting of three or more directors, out of which at least one director shall be an independent director.

Meetings of Board;

Boards Report;

Note 1: If the

Company is not

required to have

Independent

Director check

whether the

Company has

constituted CSR

Committee with two

or more directors?

Note 2: In case of

PVC having only

two directors on its

Board shall

constitute its CSR

Committee with two

such directors;

Note 3: In case of a foreign company covered under these rules, the CSR Committee shall comprise of at least two persons of which one person shall be as specified under clause (d) of sub-section (1) of section

380 of the Act and

another person shall be nominated by the foreign company.

Note 4: Where the minimum amount required to be spent on CSR Activities does not exceed Rs.50 Lakhs, there is no need to constitute CSR Committee the functions of the CSR Committee could be carried on by the

20

Board of Directors itself.

18. S135(3), (4) r/w

R9 of The CSR

Rules

CSR

Companie

s

AQ Check whether the CSR committee has formulated the CSR policy, recommended the amount of expenditure to be incurred on CSR activities as per Schedule VII to the Board and monitors the CSR policy from time to time? Check whether the Board has approved the CSR Policy? Check whether the CSR report is Annexed to the Boards Report? Check whether the CSR Policy has been posted on the website of the Company, if any?

CSR committee

minutes and CSR

Policy

19. S135(5), (6) CSR

Companie

s

AQ Check whether the company has spent not less than 2% of the average net profits of the Company made during the three immediately preceding financial years? Where the company has not spent not less than 2% of the average net profits of the Company made during the three immediately preceding financial years, check whether the unspent amount as at the end of the financial year pertains to ongoing project and if so check further whether the same has been transferred to a bank account styled as (Unspent CSR Account)

CSR Report

annexed to the

Boards Report and

FS

21

on or before the 30th April of the next financial year for being spent on such ongoing projects? Where the company has not spent not less than 2% of the average net profits of the Company made during the three immediately preceding financial years, check whether the unspent amount as at the end of the financial year that does not pertain to any “ongoing project” has been transferred on or before the 30th September of the next financial year to any of the funds specified in Schedule VII to the Act? Check whether the company, while spending on CSR Activities, has given preference to local areas where it operates? In case the company has spent more than the requisite amount on CSR Activities in any previous financial year, check if the same has been set off towards the minimum amount required to be spent CSR Activities in the year under audit?

20. R4(1) of The

CSR Rules

CSR

Companie

s

AQ Where the company had carried out CSR Activities through any implementing agency, such as a charitable trust or a society or Section 8 Company, whether established by the company or otherwise,

CSR Policy;

Documents

submitted by the

implementing

agency;

Notices, notes and

Minutes of Board

and CSR

22

check whether the implementing agency is duly registered under the respective laws and having registered under Section 12A and Section 80G of the Income Tax Act, 1961 and further registered with MCA by filing Form CSR-1?

Committee;

Board’s Report on

CSR

21. R4(4) of The

CSR Rules

CSR

Companie

s

AQ Where the company has undertaken CSR projects in collaboration with other companies, check whether the CFO of the company or the person responsible for financial management has certified that the funds so disbursed has been utilised in the manner it was approved by the Board?

CSR Policy;

Contracts, if any

between the

company and other

companies;

Notices, notes and

Minutes of Board

and CSR

Committee;

Board’s Report on

CSR;

22. R4(6) of The

CSR Rules

CSR

Companie

s

AQ In case there is any ongoing project, whether the Board monitors its implementation in a timely manner?

CSR Policy;

Documents, if any

that shows the

manner in which

the Board had been

monitoring the

implementation of

ongoing projects;

23. R5(2) of The

CSR Rules

CSR

Companie

s

AQ Check whether the CSR Committee has recommended to the Board an Annual Action Plan and check if the same covers all requisite aspects?

CSR Policy;

Annual Action Plan;

Notice, Notes and

Minutes of

Meetings of CSR

Committee and

Board of Directors.

24. R7(1) of The

CSR Rules

CSR

Companie

s

AQ Where CSR Expenditure accounted by the company includes any administrative overheads, check that that Administrative Overhead

CSR Policy;

Management

Representation;

Board’s Report;

FS;

23

doesn’t exceed five percent of the total CSR expenditure for that FY. Where any surplus had arisen while carrying out CSR Activities, check if the has been ploughed back in the same project or if it has been added to unspent CSR Amount as per CSR Policy or transferred to any fund specified in Schedule VII

Minutes of CSR

Committee;

25. R7(4) of The

CSR Rules

CSR

Companie

s

AQ Where the company has acquired or created any capital asset, check whether the same has been transferred to (a) Section 8 company/ registered trust / registered society; or (b) beneficiaries of the said CSR projects, in the form of self-help groups, collectives, entities; or (c) a public authority

Books of Account;

FS;

Board’s Report;

Asset Purchase

Details.

Note: If the capital

asset is one which

is already created

prior to 22nd

January 2021, such

assets must be

transferred to (a)

Section 8 company/

registered trust /

registered society;

or (b) beneficiaries

of the said CSR

projects, in the form

of self-help groups,

collectives, entities;

or (c) a public

authority; within

180 days of 22nd

January 2021 or

within another 90

days, subject to a

resolution of the

Board authorising

the extension.

24

26. R8(3)(a) and

(c) of The CSR

Rules

AC AQ Check whether impact assessment is applicable to the comp any? If yes, check that the impact assessment expenditure doesn’t exceed five percent of the total CSR expenditure or Rupees Fifty lakh whichever is less?

27. S135 r/w R9 of

The CSR Rules

AC AQ Check whether the company has a website? If yes, whether the following are displayed on the website –

(1) composition of the CSR committee

(2) CSR policy and (3) Projects approved

by the Board

28. S135 r/w The

CSR Rules

AC AQ Check whether the Boards Report discloses the compositions of the CSR Committee and all other requirements as specified in Section 135 r/w CSR Rules Also, check if the company has given reasons in its Board’s Report for not being able to spend the requisite amount on CSR Activities? Check whether the Impact Assessment report is placed before the Board and annexed to the Boards Report? Check whether the company has made the disclosures as per Annexure II in the CSR Annual Report?

Boards Report

29. S136(1) AC AQ Check if copy of the FS, including CFS, if any,

Proof of Dispatch.

Note: Subject to

25

auditor’s report and every other document required by law to be annexed or attached to the financial statements, requiring approval at general meeting, has been sent at least 21 days before the date of the meeting to: (1) every member of the company; (2) every trustee for the debenture-holder of any debentures issued by the company, and (3) all persons other than such member or trustee, being the person so entitled. Where financial statement and annexures thereto have been sent less than 21 days prior to the annual general meeting, if consent of members to the requisite level has been obtained.

consent of not less

than members

representing 95%

of paid up capital

with voting rights,

financial statement

and other

documents to be

annexed thereto

could be sent with

less than 21 days

too.

30. S136 second

proviso

LC AQ Were the copies of the documents made available for inspection at its registered office during working hours for a period of twenty-one days before the date of the meeting? and also check has a statement containing the salient features of such documents in AOC-3 or copies of the documents, as the company may deem fit, is sent not less than twenty-one days before the date of the meeting unless the shareholders ask for full financial statements to: every member of the

CS to confirm,

despatch proof for

AOC-3

26

company and to every trustee for the holders of any debentures issued by the company?

31. S137(1) r/w

R13 of The

Rules

AC AQ Check whether the company has filed the adopted FS with the ROC within thirty days of the date of AGM or with additional fee in Form AOC-4 and CFS, if any, with Form AOC-4 CFS?

Form AOC-4 along

with attachments

and Form AOC-4

CFS

32. S137(1) r/w

R13 of The

Rules

AC AQ Check whether the company has filed the provisional FS with the ROC within thirty days of the AGM or with additional fee?

Form AOC-4 along

with attachments

and Form AOC-4

CFS

33. S137 second

proviso

OPC AQ Check whether the FS are filed within 180 days from the closure of the financial year?

Form AOC-4 along

with attachments

and Form AOC-4

CFS

34. S137 third

proviso

AC AQ Check whether the company has any foreign subsidiary? If yes, whether the company has attached the accounts of the foreign subsidiary while filing the FS with the ROC?

Form AOC-4 along

with attachments

and Form AOC-4

CFS

35. S137 fourth

proviso

AC AQ Where the company has not held AGM, check whether reasons for the same has been attached to the form?

Form AOC-4 along

with attachments

and Form AOC-4

CFS

36. S138 r/w R13

of The Rules

AC DCQ Check whether the company is one which must have an internal audit done of its functions and activties?

Note:

All listed companies

and unlisted public

companies meeting

any of the following

thresholds must

have internal audit:

27

(a) Paid up share capital of Rs.50 Crores or more; or (b) Turnover of Rs.200 Crores or more; or (c) Outstanding loans or borrowings from banks or PFI exceeding Rs.100 Crores or more at any point of time; or (d) Outstanding deposits of Rs.25 Crores or more. All private companies, meeting any of the following thresholds must have an internal audit: (a) Turnover of Rs.200 Crores or more; or (b) Outstanding loans or borrowings from banks or PFI exceeding Rs.100 Crores or more.

37. S138 r/w R13

of The Rules

AC AQ Check whether the Audit Committee, where applicable, or the Board has in consultation with the Internal Auditor, formulated the scope, functioning, periodicity and methodology of conducting the audit?

Minutes of the Audit committee meeting. Note: Section 177 mandates the requirement to have an audit committee of the Board for the following companies: All listed

28

companies. Companies meeting any of the following thresholds, as on

the date of last audited FS shall be taken into account for the purposes of this rule.: (i) all public companies with a paid up capital of Rs.10 Crores or more; (ii) all public companies having turnover of Rs.100 Crores or more; (iii) all public companies, having in aggregate, outstanding loans or borrowings or debentures or deposits exceeding Rs.50 Crores or more.

38. S138 r/w R13

of The Rules

AC AQ Does the internal auditor report to the audit committee or board periodically?

Minutes of the Audit

Committee meeting

or Board minutes

as applicable

39. S138 r/w R13

of the Rules

AC AQ Check if the Internal audit has been done by a chartered accountant or cost accountant or any other professional as the Board may have decided.

Board Minutes;

Appointment of

Internal Auditor;

Scope and terms of

such appointment.

29

Checklist for the Chapter on Appointment and Qualification of Directors (Chapter-XI of the Companies Act, 2013 covering sections 149 to 172)

___________________________________________________________________ Notes :

1. This checklist applicable only to private and public companies with share

capital incorporated for profit making objectives.

2. This checklist is purely based on provisions of the Act and rules thereto. It

does not include any reference to SEBI (Listing Obligations and Disclosure

Requirements) Regulations,2015 or any other law or rules and regulations

that may apply to the subject matter of the Chapter XII of the Act.

3. This checklist is intended to serve a ready reference for company

secretaries in employment as well as those in practice. In other words, it is

to be applied by persons who are qualified members of the Institute of

Company Secretaries of India (ICSI).

4. This checklist takes into account amendments to the provisions and rules

up to 25.09.2021.

5. While every care has been taken to incorporate all the applicable

provisions and the rules falling with the subjects covered by Chapter XI it is

possible that a particular aspect or point has not been factored, Hence, if

any reader brings anything to be incorporated in this checklist or modified

or varied, it may be brought to the knowledge of CCGRT of ICSI for

consideration and necessary action may be desirable.

6. This checklist is not intended to serve as a fool proof document to insulate

members from any professional liability. Members are required to apply the

same with due diligence and care is expected of professionals.

7. This checklist does not cover specific aspects of one person companies,

Section 8 companies, Nidhis.

Legends:

i. The Companies Act, 2013 – the Act.

ii. Ministry of Corporate Affairs – MCA

iii. Registrar of Companies – ROC

iv. The Companies (Appointment and Qualifications of Directors) Rules, 2014) –

the AQD Rules

30

Activity Code:

Data Collection Question – DCQ

Audit Question – AQ

Company Code:

AC- All companies

PC- Public companies

PVC- Private Companies

UPC- Unlisted Public Companies

LC- Listed Public Companies

IFSC PC - A public company which is licensed to operate by the RBI or SEBI or IRDAI from the International Financial Services Centre located in an approved multi services Special Economic Zone set-up under the Special Economic Zones Act, 2005 (28 of 2005) r/w the Special Economic Zones Rules, 2006.

IFSC PVC - A private company which is licensed to operate by the RBI or SEBI or IRDAI from the International Financial Services Centre located in an approved multi services Special Economic Zone set-up under the Special Economic Zones Act, 2005 (28 of 2005) r/w the Special Economic Zones Rules, 2006.

Government Company – GC - 45) "Government company" means any company in which not less than fifty-one per cent of the paid-up share capital is held by the Central Government, or by any State Government or Governments, or partly by the Central Government and partly by one or more State Governments, and includes a company which is a subsidiary company of such a Government company. ["paid up share capital" shall be construed as "total voting power", where shares with differential voting rights have been issued.]

DC- Dormant company as defined under S.455 of the Act.

JV- Joint Venture

WOS- Wholly Owned Subsidiary

HSA- Holding, Subsidiary, Associate Company.

FY-Financial Year

The Concise Checklist for Chapter XI (Section 149-172)

S.No Provision Class of Company

Activity Code

Question Source of Information

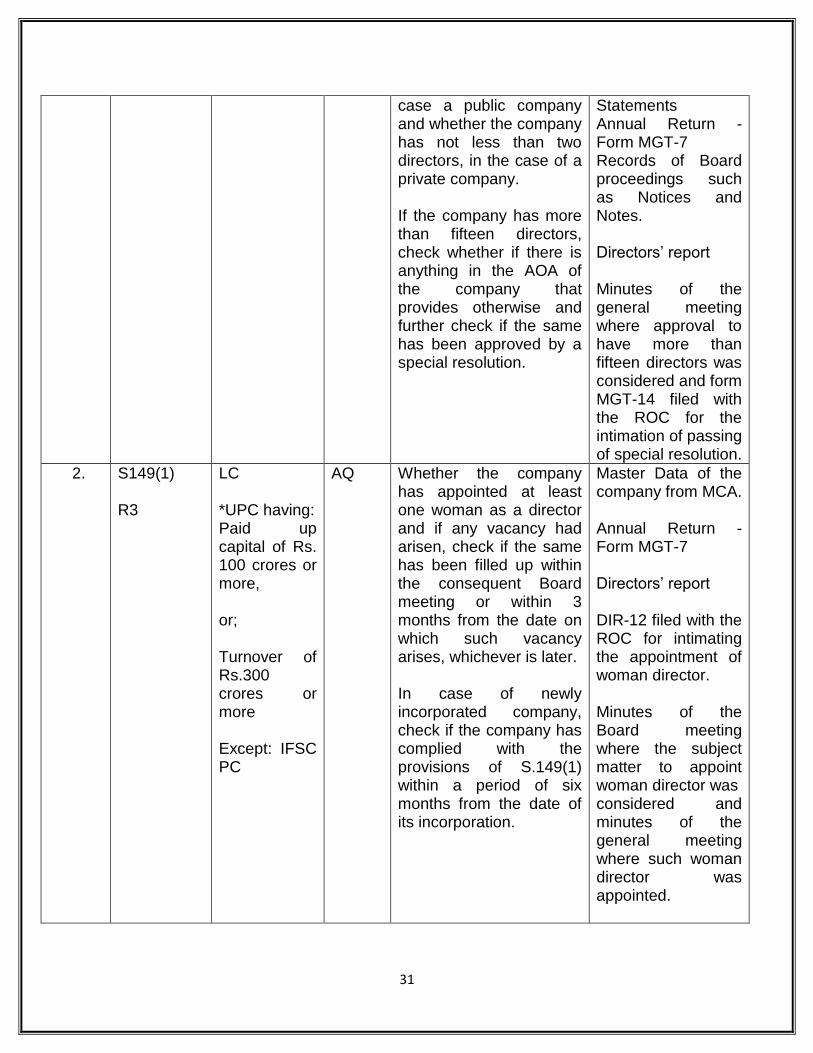

1. S149(1) PC

AQ Check whether the company has a minimum of three directors, in the

Master Data of the company from MCA. Audited Financial

31

case a public company and whether the company has not less than two directors, in the case of a private company. If the company has more than fifteen directors, check whether if there is anything in the AOA of the company that provides otherwise and further check if the same has been approved by a special resolution.

Statements Annual Return -Form MGT-7 Records of Board proceedings such as Notices and Notes. Directors’ report Minutes of the general meeting where approval to have more than fifteen directors was considered and form MGT-14 filed with the ROC for the intimation of passing of special resolution.

2. S149(1) R3

LC *UPC having: Paid up capital of Rs. 100 crores or more, or; Turnover of Rs.300 crores or more Except: IFSC PC

AQ Whether the company has appointed at least one woman as a director and if any vacancy had arisen, check if the same has been filled up within the consequent Board meeting or within 3 months from the date on which such vacancy arises, whichever is later. In case of newly incorporated company, check if the company has complied with the provisions of S.149(1) within a period of six months from the date of its incorporation.

Master Data of the company from MCA. Annual Return -Form MGT-7 Directors’ report DIR-12 filed with the ROC for intimating the appointment of woman director. Minutes of the Board meeting where the subject matter to appoint woman director was considered and minutes of the general meeting where such woman director was appointed.

32

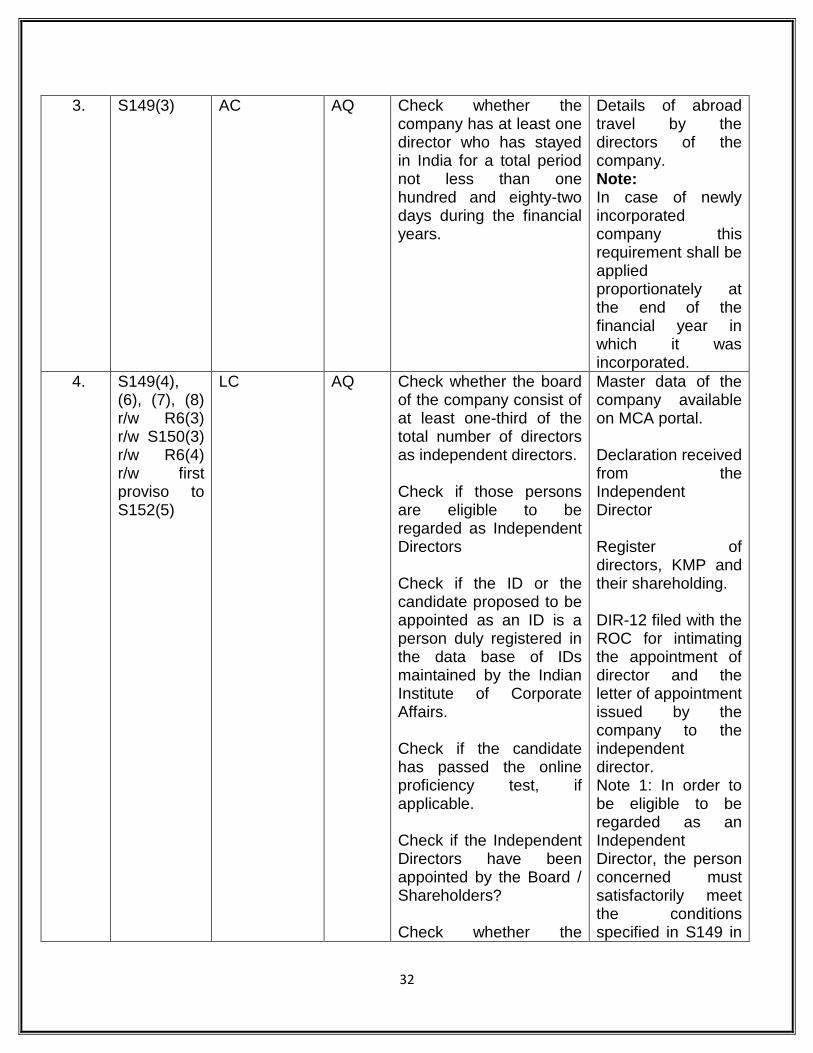

3. S149(3) AC AQ Check whether the company has at least one director who has stayed in India for a total period not less than one hundred and eighty-two days during the financial years.

Details of abroad travel by the directors of the company. Note: In case of newly incorporated company this requirement shall be applied proportionately at the end of the financial year in which it was incorporated.

4. S149(4), (6), (7), (8) r/w R6(3) r/w S150(3) r/w R6(4) r/w first proviso to S152(5)

LC

AQ Check whether the board of the company consist of at least one-third of the total number of directors as independent directors. Check if those persons are eligible to be regarded as Independent Directors Check if the ID or the candidate proposed to be appointed as an ID is a person duly registered in the data base of IDs maintained by the Indian Institute of Corporate Affairs. Check if the candidate has passed the online proficiency test, if applicable. Check if the Independent Directors have been appointed by the Board / Shareholders? Check whether the

Master data of the company available on MCA portal. Declaration received from the Independent Director Register of directors, KMP and their shareholding. DIR-12 filed with the ROC for intimating the appointment of director and the letter of appointment issued by the company to the independent director. Note 1: In order to be eligible to be regarded as an Independent Director, the person concerned must satisfactorily meet the conditions specified in S149 in

33

company has received a declaration that he meets the criteria of independence as provided in sub-section (6) from the ID at first meeting of the Board in which he participates as a director and thereafter at the first meeting of the Board in every FY or whenever there is any change in the circumstances which may affect his status as an ID. Check if the company has included in the explanatory statement for such appointment, that in the opinion of the Board, he fulfils the conditions specified in this Act for such an appointment.

addition to meeting the conditions specified in LODR.

5. S149(4), (6), (7), (8) r/w R4, R6(3) r/w S150(3) r/w R6(4) r/w first proviso to S152(5)

*UPC having a) Paid up

share capital of 10 crore rupees or,

b) Turnover of 100 crore rupees or more; or

c) Have in aggregate outstanding loan, debentures, deposits, exceeding 50 crore rupees.

Except:

AQ Check if the company has appointed at least two independent directors. Check if those persons are eligible to be regarded as Independent Directors. Check if the ID or the candidate proposed to be appointed as an ID is a person duly registered in the data base of IDs maintained by the Indian Institute of Corporate Affairs. Check if the candidate has passed the online proficiency test, if applicable.

Master data of the company available on MCA portal. Declaration received from the Independent Director Register of directors, KMP and their shareholding Latest audited financial statements. Board and General Meeting Proceedings such as Notices, Notes, and Minutes

34

WOS

JV

DC

Check whether the independent director has been duly appointed by the Board / General meeting. Check if the company has included in the explanatory statement for such appointment, that in the opinion of the Board, he fulfils the conditions specified in this Act for such an appointment. Check whether the company has received a declaration that he meets the criteria of independence as provided in sub-section (6) from the ID at first meeting of the Board in which he participates as a director and thereafter at the first meeting of the Board in every FY or whenever there is any change in the circumstances which may affect his status as an ID. Check if the provision of constitution of Audit Committee, that is, S177 is applicable to the company. If yes, check whether the company is required to appoint a greater number of independent directors due to the composition audit committee. Check if any vacancy that had arisen has been filled

Statement about independence of the director annexed to the Notice of general meeting Any document such as letter or mail showing Resignation or cessation due to any other reason. DIR11, DIR12 Note 1: In order to be eligible to be regarded as an Independent Director, the person concerned must satisfactorily meet the conditions specified in S149. Note 2: As when a company ceases to fulfil any of three thresholds laid down in sub-rule (1) for three consecutive years, it shall not be required to comply with these provisions until such time as it meets any of such conditions.

35

up at the earliest but not later than immediate next Board meeting or three months from the date of such vacancy, whichever is later.

6. S149, Fourth Proviso to R4(1)

UPC covered under R4(1)

AQ Check if the company is regulated by any other authority. If yes, check whether any other law is applicable to such company, as a company belonging to any class of companies for which a higher number of independent directors has been specified in the law for the time being in force shall comply with the requirements specified in such law.

Directors’ Report Master data of the company available on MCA portal.

7. S149(8) Sch IV

LC UPC covered under R4(1)

AQ Check whether the IDs of the company have adhered to the code of conduct as specified in the Schedule IV.

8. S149(8) SchIV(VI)

LC UPC covered under R4(1)

DCQ Where there has been resignation of any Independent Director, check if (a) the person concerned has submitted a resignation letter spelling out the reasons for his resignation; (b) the company has notified the Registrar of Companies / Stock Exchanges of such resignation; and (c) filled up the vacancy, within three months from the date of such resignation or removal, as the case may be. Where there has been a removal of any

Notice of Resignation received from the ID. If any Special Notice received for removal of ID. DIR-12 filed for intimating the ROC about the removal / resignation. Proceedings of Board / General Meeting including Notices, Notes, and Minutes.

36

Independent Director, please check if the removal has been done in accordance with law following proper procedures and after giving reasonable opportunity to the person concerned to explain his stand.

Note: Where the number of Independent Directors on the Board is sufficient even after such resignation or removal, there is no need for filling up the vacancy.

9. S149(8) Sch IV(VII)

LC UPC covered under R.4(1)

AQ Check whether the IDs had at least one separate meeting in the FY and check if they had reviewed the -

performance of non-independent directors and the Board as a whole;

performance of the Chairperson of the company, taking into account the views of executive directors and non-executive directors;

and they had assessed the quality, quantity and timeliness of flow of information between the company management and the Board that is necessary for the Board to effectively and reasonably perform their duties.

Minutes of the meetings of the ID.

10. S149(8) Sch IV (Paras V & VIII)

LC UPC covered under R.4(1)

AQ Ensure that the Board of directors have evaluated the performance of the ID. Check if the output of such performance evaluation has formed the basis for considering the

Minutes of the Board meeting where the subject. Criteria for performance evaluation and performance

37

re-appointment of such ID.

evaluation matrix. Notice, Notes and Minutes of Meeting of the NRC, if any; Explanatory statement annexed to the Notice of General Meeting in which the re-appointment of an ID comes up

11. S149(9) r/w Para IV(4) of Sch IV r/w Sch V

LC UPC covered under R.4(1)

AQ Check if the company has issued a formal letter of appointment to every ID at the time of appointment or re-appointment and verify that the remuneration paid to ID is as per S.149(9) of the Act. Check if the terms of appointment have been kept open for inspection; Check if the terms have been posted in the website, if any, of the company; Check if the company permits remuneration to its IDs when it has no profits or its profits are inadequate, and in such a case, check if the same in accordance with the provisions of Schedule V.

Financial statements of the company. Proof of remuneration paid. Terms of Appointment as shown in the Letter of Appointment Disclosures made in the website of the company

12. S149(10), (11)

LC UPC covered under R.4(1)

AQ Check if any Independent Director has been in office beyond the period of five consecutive years. If yes, check if there has been a reappointed for another term duly approved by a special resolution duly passed at a general meeting of the company. Check if the company has

Minutes of the general meeting where the appointment of ID was approved. Minutes of the meeting where reappointment of ID was approved.

38

appointed as its Independent Director the same person who had already completed two terms of 5 years each as an Independent Director without observing the mandatory gap of 3 years. Check if the company has appointed any person who had already completed two terms of 5 years each as an Independent Director after observing the mandatory gap of 3 years, whether such a person was associated with the company in any other capacity, either directly or indirectly.

Form MGT-14 filed to intimate the ROC about the special Resolution passed for reappointment of ID. DIR-12 filed for intimating the appointment and re-appointment of ID, as the case may be.

13. S151r/w R7 r/w S153 r/w S164 r/w S120

LC AQ Where the listed company has received a valid nomination from any person to be appointed as a small shareholders director, check if the company has initiated a postal ballot process for securing approval of members. Check the candidate has a valid DIN, not disqualified, has consented to act as a small shareholders directors, and is eligible to be appointed as an Independent Director. Check if the appointment has been made for a period of maximum 3 years only and he has not been re-appointed at any time thereafter.

Register of Members of the company Notice, if any received from the small shareholders. List of shareholders as attached to the Annual Return DIN Consent Registration as ID in the database of IICA Online Proficiency Test, wherever applicable.

39

14. S151 r/w R7(7)

LC AQ Check whether the small shareholders director has vacated office for any reason whatsoever such as incurring a disqualification or losing independence or vacating office on any of the grounds specified under Section 167 or not able to continue to meet the criteria to be eligible to represent small shareholders.

“Director Master” service available on MCA portal. List of Disqualified directors as per MCA. Declaration received from the director.

15. S151 R7(8)

LC AQ Check that small shareholder Director does not hold office in more than 2 companies and that the 2nd company is not competing or in conflict with the business of the first company.

“Director Master” service available on MCA portal.

16. S151 R7(9)

LC AQ Check if the Small Shareholders Director had, at any time within 3 years from the date on which he has ceased to be such a director become associated with such company, either directly or indirectly.

Master data of the company as in MCA portal “Director Master” service available on MCA portal.

17. S152(1) AC DCQ Where the AOA of the company does not mention the names of first directors nor is there any provision made in the AOA for appointment of first directors, check whether the subscribers to the MOA have been deemed to be the first directors.

AOA. Master data of the company available on MCA.

18. S152(2), (3), (4)

AC AQ Check, with respect to every director of the company, whether such person has a valid DIN; is

AOA; DIN; “Enquire DIN Status” service of

40

not disqualified on any of the grounds specified in Section 164 of the 2013 Act or on any other additional ground that the AOA of a private company might have specified; has consented to act as a director; and he has been duly appointed at a general meeting of the company, unless such appointed is otherwise validly made by the Board or as per AOA. Verify that the company has filed form DIR-12 for such appointment within thirty days from the date of appointment.

the MCA. Declaration as to disqualification; Consent to act as a Director in DIR-2; Proof of filing of consent with ROCa; Notice, Notes and Minutes of Board and General Meetings and Explanatory statement if any. Master data of the company available on MCA; List of disqualified directors that is available on MCA portal; The “companies / Directors under prosecution” service available on MCA; List of online filed forms of the company available in the view public document section of the MCA portal; DIR-12; Proof of filing of DIR-12

19. 152(6) AC DCQ AQ

Check if the AOA provides for the retirement of all the directors by rotation. Check, in the case of PVC, whether the AOA introduces retirement of directors by rotation. In such a case, check if the retirement of directors as per AOA has happened.

AOA; Notice, Notes and Minutes of Annual General Meeting.

41

20. S152(6) LC and UPC AQ Unless the AOA provides for retirement of all the directors by rotation at every AGM, check if not less than two-thirds of the directors of the company are liable to retire by rotation and at least one-third of directors have retired by rotation at every AGM. Check if the AOA provides for retirement of all the directors by rotation at every AGM, whether all the directors have so retired at every AGM. Where the AOA provides nothing with respect to retirement of directors by rotation and does not also provide that not more than one-third of the directors may be appointed by the Board and they are not liable to retire by rotation, check if the directors other than directors liable to retire by rotation have been appointed at the AGM. Check if the directors who have retired at an AGM are those who have held the office for the longest since their last appointment. Ensure that the company has mentioned the name of directors who are liable to retire by rotation which is one-third of total number of directors liable to retire by rotation in the Notice of general

AOA Notice of the general meeting Minutes of general meeting

Online filed forms maintained by the company. List of online filed forms of the company available in the view public document section of the MCA portal. Consent from the person proposed to be appointed as director in Form DIR-2. The “Director Master” service available on MCA.

42

meeting. Also, check if the company has filed form DIR-12 for the purpose of intimating the Registrar about the retirement of the director who has not been reappointed within thirty days from the date of Annual General meeting.

21. S152(7) AC (except PVC)

AQ Check whether the company has not filled up any vacancy caused by retirement of any director by rotation and in case the company has not resolved specifically not to fill up such vacancy, check if the meeting has got adjourned automatically and further check whether at such adjourned meeting also, if the company has not filled up any vacancy caused by retirement of any director by rotation and in case the company has not resolved specifically not to fill up such vacancy, check if the retiring director has been appointed pursuant to automatic appointment provision contained in Section 152(7).

Note: Where the retiring director would not get automatically appointed if any of the several situations specified under clause (b) of Section 152(7) of the 2013 Act. They are as follows: (i) at that meeting or at the previous meeting a resolution for the reappointment of such director has been put to the meeting and lost; (ii) the retiring director has, by a notice in writing addressed to the company or its Board of directors, expressed his unwillingness to be so re-appointed; (iii) he is not qualified or is disqualified for appointment; (iv) a resolution, whether special or ordinary, is required

43

for his appointment or re-appointment by virtue of any provisions of this Act; or (v) Section 162 is applicable to the case.

22. S153 r/w R9 r/w Rule 12A r/w Rule 12B

AC AQ Check if they have submitted their DIR-3-KYC; Check if any director has been marked as Director of ACVTIVE non-compliant company and check if he has taken steps to ensure that the companies of which he / she is a director which have not filed e form ACTIVE.

“Director Master” service available on MCA portal. Check DIN status service of MCA; Check steps taken by every director to get his name tagged as Director of ACTIVE non-compliant company

23. S158 AC AQ Check whether the company while furnishing any return, information or particulars as are required to be furnished under this Act, has mentioned the Director Identification Number in case such return, information or particulars relate to the director or contain any reference of any director.

Online filed forms and their attachments.

24. S161(1) AC

AQ Check whether any director appointed as an Additional Director has been appointed at any AGM that is held subsequent to the date of appointment of the Additional Director. Check whether a person appointed as an Additional Director has continued to act as a

DIR-12 Notice, Notes, and Minutes of Board and General Meetings and Board’s Report

44

director beyond the date of the AGM that has been held subsequent to the date of appointment and if so, check further whether such person has been properly appointed as a director at the AGM. Check whether cessation if any of the directorship of such person at the AGM has been duly reported to ROC.

25. S161(2) AC AQ Check whether the AOA enables appointment of alternate directors and check if anyone has been appointed as an alternate director to any other director (original director) of the company in view of the original director going out of India for more than 3 months. Check if such person has (a) valid DIN; (b) is not disqualified in any respect; (c) has given consent to act as a director; (d) he is not already an alternate director of any other director of the company; (e) he is already not a director of the company; (f) if he is supposed to be alternate for any ID, he must also be eligible to act as an ID in all respects including furnishing statement of independence and opinion of the Board that he meets all eligibility conditions.

AOA; DIR-2; DIR-12 filed for the appointment of alternate director. Declaration of independence received from the person appointed in place of the independent director. Opinion of the Board about independence of the person concerned; Notice, Notes and Minutes of Board Meetings; Register of Directors; Board’s Report Document showing date of returning of the Original Director to India Document showing term of office of Original Director. Note 1: An alternate director cannot remain in

45

Check if the cessation of directorship of the alternate director has been duly taken note of, recorded and notified

office for a period longer than that permissible to the director in whose place he has been appointed. He must vacate the office if and when the director in whose place he has been appointed returns to India. Note 2: Further, if the term of office of the original director is determined before he so returns to India, any provision for the automatic re-appointment of retiring directors in default of another appointment shall apply to the original, and not to the alternate director.

26. S161(2) LC UPC covered under R4

AQ Verify that alternate director is not reappointed as t provision of automatic appointment of retiring Director shall apply only to original Director and not to Alternate Director.

Notice of the General meeting where the original director who is liable to retire by rotation is proposed to be re-appointed.

27. S161(3) AC (Except IFSC-PC or IFSC-PVC)

AQ If the company has director appointed as a nominee director of any institution, check if the same is not contrary to anything contained in the AOA and it is in pursuance of the provisions of any law for the time being in force or of any agreement or by

Nomination document received by the company from the nominating authority. Notice, Notes and Minutes of the Board meeting where the Board has taken note of nomination of the

46

the Central Government or the State Government by virtue of its shareholding in a Government company.

person as director of the company Board’s Report DIR-12 filed for intimating the appointment of nominee director to the ROC.

28. S161(3) IFSC-PC or IFSC-PVC

AQ If the company has director appointed as a nominee director of any institution or any company or body corporate, check if the same is not contrary to anything contained in the AOA and it is in pursuance of the provisions of any law for the time being in force or of any agreement or by the Central Government or the State Government by virtue of its shareholding in a Government company.

Nomination document received by the company from the nominating authority. Notice, Notes and Minutes of the Board meeting where the Board has taken note of nomination of the person as director of the company Board’s Report DIR-12 filed for intimating the appointment of nominee director to the ROC.

29. S161(4) AC AQ Check whether the company has appointed any director in course of any casual vacancy caused. If yes, ensure that the company has appointed a director to fill in the casual vacancy subject to the regulations, if any stated in the Articles of Association. Check if the director appointed to fill a casual vacancy has been approved by the shareholders in the immediate next AGM

Articles of Association Notice, Notes and Minutes of the Board meeting / general meeting where the appointment of director was considered. DIR-2; DIR-12; Proof of arising of casual vacancy; Register of Directors;

47

30. S162 AC Except: 1) PVC 2) Specified

IFSC PC 3) GC

AQ Where the company has appointed several persons as directors under a single resolution, check if the company has, prior to getting such a combined resolution passed, first sought and secured the approval of members to the proposal to move such a single motion for appointing several directors, at the meeting without any vote being cast against it.

Notice of the meeting Notice, Notes and Minutes of the General Meeting Note 1: A motion for approving a person for appointment, or for nominating a person for appointment as a director, shall be treated as a motion for his appointment. Note 2: Where the company did not secure approval of members for moving a single resolution for appointing several persons as directors through a single resolution, such appointment will be VOID even if such a resolution had been passed unanimously.

31. S163 AC (Except GC).

DCQ Check whether company has adopted principle of Proportional Representation for appointment of Directors, whether on account of a provision contained in the AOA or otherwise and if so check if the same specification has been continued.

AOA

32. S164(1) AC AQ Check whether any of the directors are disqualified to continue or get re-appointed as director of the company as per

“Director Master” service of the MCA. List of disqualified directors issued by the MCA in the MCA

48

S.164(1). Check whether the AOA of the company provides for any other disqualifications for appointment of director.

Portal Order of ROC or any Court or any other competent authority showing disqualification. AOA

33. S164(2) AC AQ Check that the director intended to be appointed / re-appointed submits a declaration in form DIR 8 to the Company as per R 14.

DIR-8 received by the company

34. S164(3), r/w R14(2)(3)

AC AQ Where the company has failed to file the financial statements or annual returns, or fails to repay any deposit, interest, dividend, or fails to redeem its debentures, as per S164(2), check if the company has immediately filed with ROC the Form DIR-9 furnishing therein the names and addresses of all directors of the company during the relevant FYs.

Master Data service of the MCA. Board resolution, if any, passed for considering any director or directors as officer in default.

35. S164 r/w R14(5)

AC AQ Check if any disqualified director has applied for removal of disqualification and whether the disqualification has been removed.

Form DIR-10 filed with the ROC. Order if any passed removing or recording the cessation of disqualification

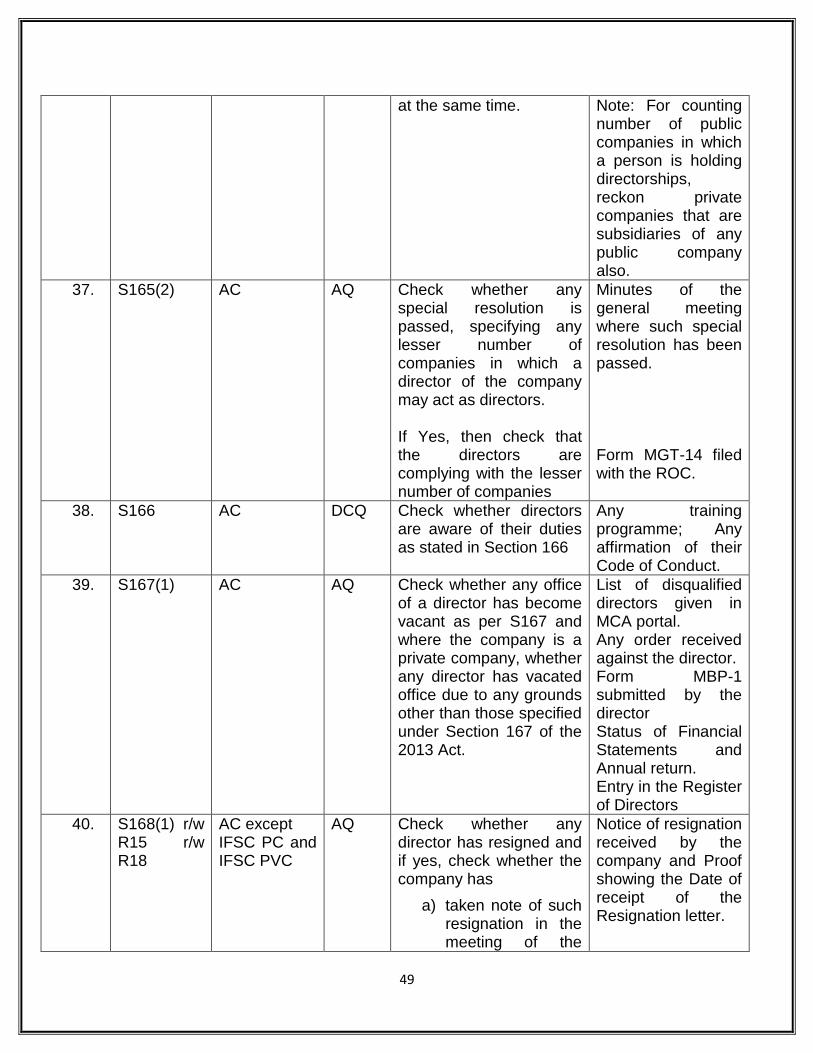

36. S165 AC AQ Check whether any director of the Company holds directorships in more than 20 companies other than directorship in dormant company; and total number of directorships in public companies alone, is not more than 10 companies

The “Director Master” service available on MCA Form DIR-2 submitted by the director to the company Register of directors and KMP and their shareholding.

49

at the same time. Note: For counting number of public companies in which a person is holding directorships, reckon private companies that are subsidiaries of any public company also.

37. S165(2) AC AQ Check whether any special resolution is passed, specifying any lesser number of companies in which a director of the company may act as directors. If Yes, then check that the directors are complying with the lesser number of companies

Minutes of the general meeting where such special resolution has been passed. Form MGT-14 filed with the ROC.

38. S166 AC DCQ Check whether directors are aware of their duties as stated in Section 166

Any training programme; Any affirmation of their Code of Conduct.

39. S167(1) AC AQ Check whether any office of a director has become vacant as per S167 and where the company is a private company, whether any director has vacated office due to any grounds other than those specified under Section 167 of the 2013 Act.

List of disqualified directors given in MCA portal. Any order received against the director. Form MBP-1 submitted by the director Status of Financial Statements and Annual return. Entry in the Register of Directors

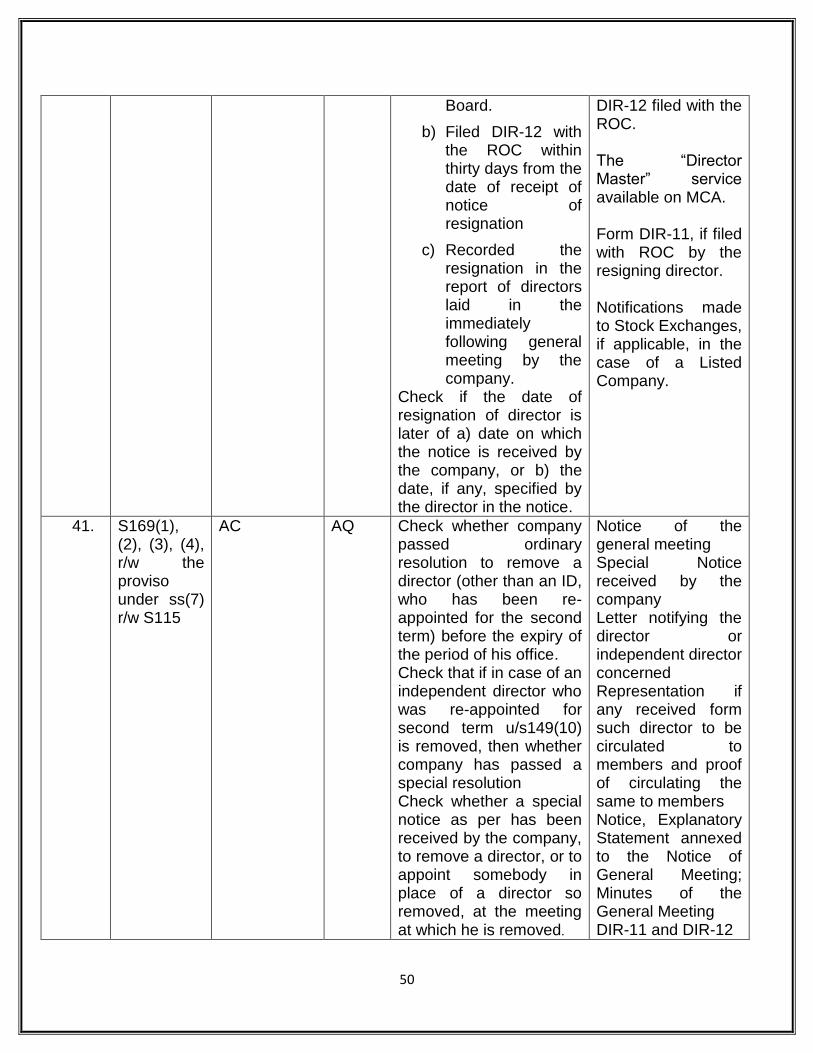

40. S168(1) r/w R15 r/w R18

AC except IFSC PC and IFSC PVC

AQ Check whether any director has resigned and if yes, check whether the company has

a) taken note of such resignation in the meeting of the

Notice of resignation received by the company and Proof showing the Date of receipt of the Resignation letter.

50

Board.

b) Filed DIR-12 with the ROC within thirty days from the date of receipt of notice of resignation

c) Recorded the resignation in the report of directors laid in the immediately following general meeting by the company.

Check if the date of resignation of director is later of a) date on which the notice is received by the company, or b) the date, if any, specified by the director in the notice.

DIR-12 filed with the ROC. The “Director Master” service available on MCA. Form DIR-11, if filed with ROC by the resigning director. Notifications made to Stock Exchanges, if applicable, in the case of a Listed Company.

41. S169(1), (2), (3), (4), r/w the proviso under ss(7) r/w S115

AC AQ Check whether company passed ordinary resolution to remove a director (other than an ID, who has been re-appointed for the second term) before the expiry of the period of his office. Check that if in case of an independent director who was re-appointed for second term u/s149(10) is removed, then whether company has passed a special resolution Check whether a special notice as per has been received by the company, to remove a director, or to appoint somebody in place of a director so removed, at the meeting at which he is removed.

Notice of the general meeting Special Notice received by the company Letter notifying the director or independent director concerned Representation if any received form such director to be circulated to members and proof of circulating the same to members Notice, Explanatory Statement annexed to the Notice of General Meeting; Minutes of the General Meeting DIR-11 and DIR-12

51

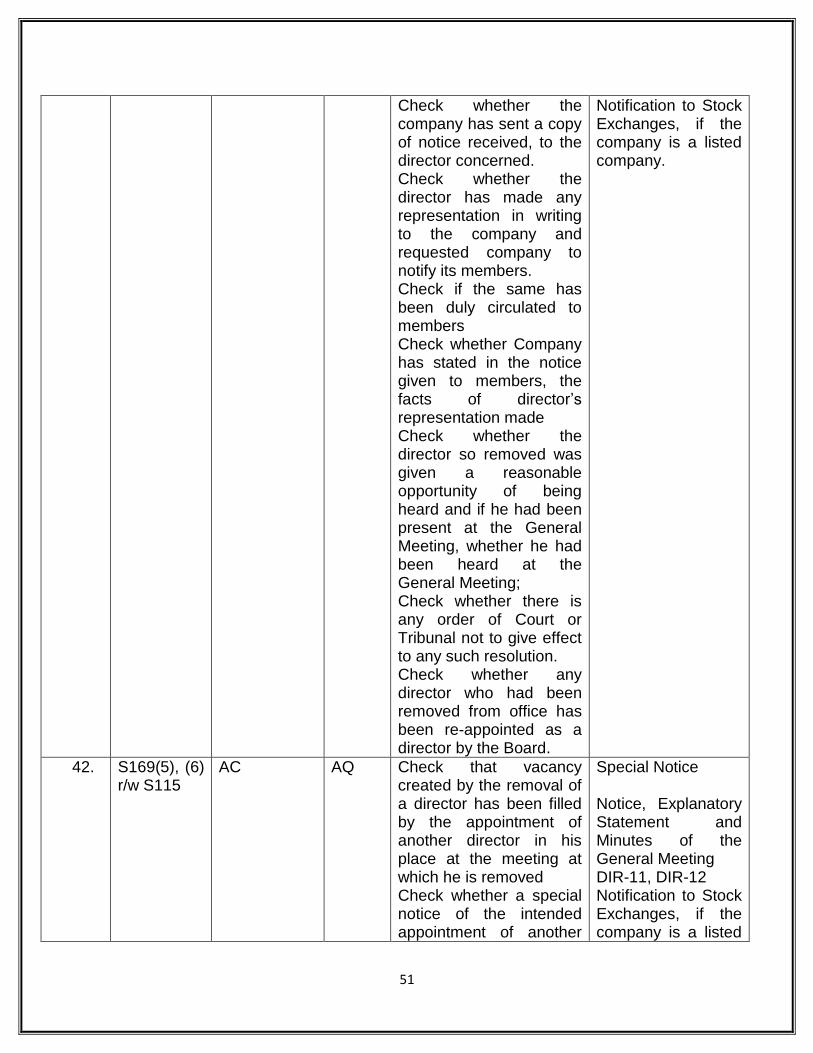

Check whether the company has sent a copy of notice received, to the director concerned. Check whether the director has made any representation in writing to the company and requested company to notify its members. Check if the same has been duly circulated to members Check whether Company has stated in the notice given to members, the facts of director’s representation made Check whether the director so removed was given a reasonable opportunity of being heard and if he had been present at the General Meeting, whether he had been heard at the General Meeting; Check whether there is any order of Court or Tribunal not to give effect to any such resolution. Check whether any director who had been removed from office has been re-appointed as a director by the Board.

Notification to Stock Exchanges, if the company is a listed company.

42. S169(5), (6) r/w S115

AC AQ Check that vacancy created by the removal of a director has been filled by the appointment of another director in his place at the meeting at which he is removed Check whether a special notice of the intended appointment of another

Special Notice Notice, Explanatory Statement and Minutes of the General Meeting DIR-11, DIR-12 Notification to Stock Exchanges, if the company is a listed

52

director has been given to members Where such vacancy had been so been filled up, check if the director appointed in that vacancy has been appointed to be in that office for the period upto which the removed director would have held that office.

company.

43. S169(7) AC DCQ Check if the Board has filled up the vacancy caused by the removal of a director as a casual vacancy.

Notice, Notes and Minutes of the Board meeting; Consent of the Director concerned. Resolution passed for the appointment. DIR-11, DIR-12 Notification to Stock Exchanges, in the case of a Listed Company.

44. S170(1) r/w R17

AC AQ Check whether the company is maintaining a Register of Directors and Key Managerial Personnel and their shareholding either in physical or in electronic form and check if it contains all requisite particulars.

The Register; The Minutes of Board and General Meetings; Audited Financial Statements Disclosures made to Stock Exchanges and Registrar of Companies; Disclosures made by directors and KMPs

45. S170(2) R18

AC AQ Check if there has been any appointment, Cessation or change in designation of directors in the company. If yes, check if the company has filed DIR-12 within 30 days from the date of such event.

Filed forms as maintained by the company. View public documents service of the MCA.

53

46. S171(1) AC Except: GC where the entire paid-up capital is held by CG or SG, by CG and SG or by CG and one or more SG.

AQ Check whether there have been any requests for inspection or extracts of the Register kept u/s 170 and whether the company has permitted the inspection of / taking extracts of the same; Check whether Registers kept u/s 170 are kept open for inspection at every AGM and is made accessible to any person attending the meeting. Where the company has refused to permit inspection or give extracts, check whether ROC has issued any order for immediate inspection and supply of copies.

Register maintained pursuant to Section 170. Requests, if any, received from the members for obtaining certified copies. Refusal to permit inspection of Register and reasons thereof; Proceedings if any against such refusals.