corporate services committee · it is recommended that cabinet approves: ... government departments...

TRANSCRIPT

195

For general release

REPORT TO: CABINET 9 JULY 2012

AGENDA ITEM: 22

SUBJECT: JULY FINANCIAL REVIEW

LEAD OFFICER: NATHAN ELVERY

DEPUTY CHIEF EXECUTIVE & EXECUTIVE DIRECTOR

CORPORATE RESOURCES & CUSTOMER SERVICES

CABINET MEMBER:

COUNCILLOR MIKE FISHER

THE LEADER

COUNCILLOR STEVE O’CONNELL

CABINET MEMBER FOR FINANCE AND PERFORMANCE MANAGEMENT

COUNCILLOR DUDLEY MEADDEPUTY LEADER (STATUTORY) (CAPITAL BUDGET AND ASSET MANAGEMENT) AND

CABINET MEMBER FOR HOUSING WARDS: ALL

CORPORATE PRIORITY/POLICY CONTEXT:

The review of the Financial Strategy as part of the budget setting process enables a balanced budget target to be established with a focus on an affordable level of council tax, delivery of the corporate priorities and policies of the Council and the continued enhancement of value for money and satisfaction with services for the residents of our borough.

FINANCIAL SUMMARY:

This report sets out the Council’s review of its Financial Strategy for the period 2010/14 to establish the context for the Council’s budget and medium term financial planning scenarios and assumptions.

196

1. RECOMMENDATIONS It is recommended that Cabinet approves: 1.1 The strategic financial planning assumptions for the Financial Strategy as

set out in table 2. 1.2 To agree the rolling budget changes to the 2012/13 revenue budget as set

out in paragraph 9.2 1.3 The carry forward of 2011/12 capital schemes as detailed in Appendix 1,

totalling £42.187m for inclusion in the 2012/13 capital programme as previously approved by Cabinet in February 2012.

2. EXECUTIVE SUMMARY 2.1 The Council’s Financial Strategy 2010/14 was reviewed by Cabinet on the

20th February 2012 and approved by Full Council on the 27th February 2012 as part of the annual budget setting cycle of the Council. This report summarises the review of the Council’s Financial Strategy 2010/14 as part of the budget setting process for the medium term and takes into account:

i) The Council’s overall financial position; ii) Key financial changes which impact on Croydon’s local and wider

financial ‘environment’; and iii) The Councils readiness in delivering the 2012/13 budget and any

resultant impact of this on future years. 2.2 This review ensures that the 2013/14 Budget and resultant council tax

level will be set within the context of the financial strategy in order to deliver a balanced budget, updated for the latest information and knowledge available to the Council.

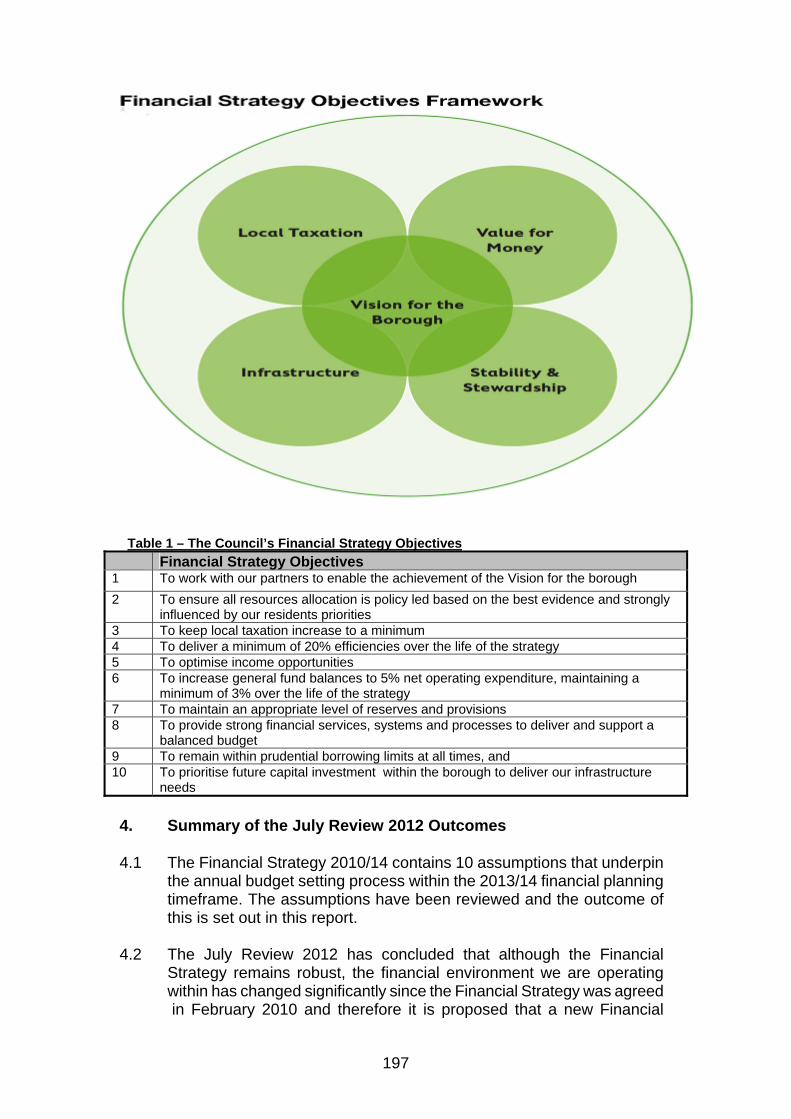

3. Financial Strategy Objectives 3.1 The Financial Strategy’s Objectives Framework is set out in Diagram 1

below with the ten financial strategy objectives outlined in table 1.

FORWARD PLAN KEY DECISION REFERENCE NO.: this is not a key decision

197

Table 1 – The Council’s Financial Strategy Objectives Financial Strategy Objectives

1 To work with our partners to enable the achievement of the Vision for the borough 2 To ensure all resources allocation is policy led based on the best evidence and strongly

influenced by our residents priorities 3 To keep local taxation increase to a minimum 4 To deliver a minimum of 20% efficiencies over the life of the strategy 5 To optimise income opportunities 6 To increase general fund balances to 5% net operating expenditure, maintaining a

minimum of 3% over the life of the strategy 7 To maintain an appropriate level of reserves and provisions 8 To provide strong financial services, systems and processes to deliver and support a

balanced budget 9 To remain within prudential borrowing limits at all times, and 10 To prioritise future capital investment within the borough to deliver our infrastructure

needs 4. Summary of the July Review 2012 Outcomes 4.1 The Financial Strategy 2010/14 contains 10 assumptions that underpin

the annual budget setting process within the 2013/14 financial planning timeframe. The assumptions have been reviewed and the outcome of this is set out in this report.

4.2 The July Review 2012 has concluded that although the Financial

Strategy remains robust, the financial environment we are operating within has changed significantly since the Financial Strategy was agreed in February 2010 and therefore it is proposed that a new Financial

198

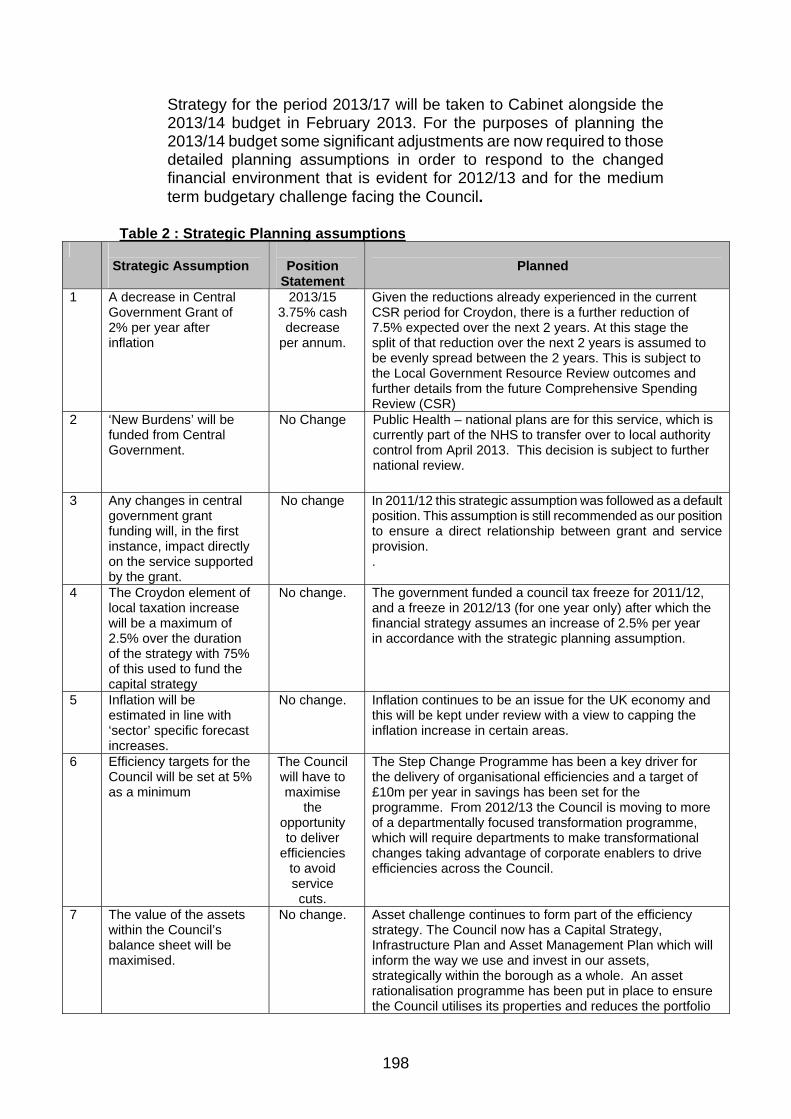

Strategy for the period 2013/17 will be taken to Cabinet alongside the 2013/14 budget in February 2013. For the purposes of planning the 2013/14 budget some significant adjustments are now required to those detailed planning assumptions in order to respond to the changed financial environment that is evident for 2012/13 and for the medium term budgetary challenge facing the Council.

Table 2 : Strategic Planning assumptions

Strategic Assumption

Position

Statement

Planned

1 A decrease in Central Government Grant of 2% per year after inflation

2013/15 3.75% cash

decrease per annum.

Given the reductions already experienced in the current CSR period for Croydon, there is a further reduction of 7.5% expected over the next 2 years. At this stage the split of that reduction over the next 2 years is assumed to be evenly spread between the 2 years. This is subject to the Local Government Resource Review outcomes and further details from the future Comprehensive Spending Review (CSR)

2 ‘New Burdens’ will be funded from Central Government.

No Change Public Health – national plans are for this service, which is currently part of the NHS to transfer over to local authority control from April 2013. This decision is subject to further national review.

3 Any changes in central government grant funding will, in the first instance, impact directly on the service supported by the grant.

No change In 2011/12 this strategic assumption was followed as a default position. This assumption is still recommended as our position to ensure a direct relationship between grant and service provision. .

4 The Croydon element of local taxation increase will be a maximum of 2.5% over the duration of the strategy with 75% of this used to fund the capital strategy

No change. The government funded a council tax freeze for 2011/12, and a freeze in 2012/13 (for one year only) after which the financial strategy assumes an increase of 2.5% per year in accordance with the strategic planning assumption.

5 Inflation will be estimated in line with ‘sector’ specific forecast increases.

No change. Inflation continues to be an issue for the UK economy and this will be kept under review with a view to capping the inflation increase in certain areas.

6 Efficiency targets for the Council will be set at 5% as a minimum

The Council will have to maximise

the opportunity to deliver

efficiencies to avoid service cuts.

The Step Change Programme has been a key driver for the delivery of organisational efficiencies and a target of £10m per year in savings has been set for the programme. From 2012/13 the Council is moving to more of a departmentally focused transformation programme, which will require departments to make transformational changes taking advantage of corporate enablers to drive efficiencies across the Council.

7 The value of the assets within the Council’s balance sheet will be maximised.

No change. Asset challenge continues to form part of the efficiency strategy. The Council now has a Capital Strategy, Infrastructure Plan and Asset Management Plan which will inform the way we use and invest in our assets, strategically within the borough as a whole. An asset rationalisation programme has been put in place to ensure the Council utilises its properties and reduces the portfolio

199

Strategic Assumption

Position

Statement

Planned

where necessary. 8 The HRA and GF do not

cross subsidise. No change. The appropriate costs are accountable and

proportionately shared to the relevant accounts of the Council in line with SERCOP guidance. Changes to the HRA subsidy regime have changed through HRA self financing rules.

9 Top slicing of 10% of future efficiencies will be used to fund the Step Change Croydon Programme

Change. Resources have been created within earmarked reserves to drive the current efficiency programme. Given the financial challenges ahead the council needs to maximise its opportunities for efficiencies.

5.0 Details of the July Finance Review 2011 outcomes

Government Announcements Budget Assumptions 1, 2, and 3

5.1 In the 2010 Spending Review the Government set out detailed spending

plans for the rest of this Parliament. The outcome was, as expected, a very constrained settlement for local government. Given the stated priorities of education and health there were severe pressures placed on many of the services delivered by local government. Commentators had previously suggested that this would result in a real cut in local government spending in the order of 7.5% per annum. However, although the overall quantum of the reductions was broadly as forecast what was not anticipated was that the reductions would be heavily front-loaded over the 4 year Spending Review period.

5.2 The Spending Review set the next Local Government Finance Settlement

period as the following two years after which the outcomes of the Local Government Resource Review would determine future Settlements.

5.3 The Local Government Finance Settlement for 2012/13 after damping,

resulted in an 8.3% reduction in Croydon’s formula grant. Although the Settlement does not go beyond 2012/13 the Treasury’s Spending review figures indicates that for 2013/14 and 2014/15 Croydon’s Formula Grant (or its successor) will be reduced, in cash terms, by a further 7.5%

5.4 The 2011 Autumn Statement indicated that a continued level of funding

reduction will be targeted at the public sector. Based on the revised economic forecasts of the recent Autumn Statement and reinforced by those in the March 2012 Budget, the Chancellor set the Public Expenditure control totals for the first two years of the 2014 Spending Review period (i.e. for 2015/16 and 2016/17) in line with the spending reductions over the previous 2010 Spending Review, it is estimated that it will fall during those years by 0.9% a year in real terms

200

5.5 However if CSR2014 reflects the differential distributions between government departments as contained within the CSR2010, protecting Education and Health spend, it is likely that Local Government’s funding support will continue to significantly reduce. This is estimated to be a further reduction of 7.5% per year. Therefore the total reduction in funding support from Central Government for Local Government over the period 2011/17 is estimated at 41%.

5.6 The first phase of the Review ended when DCLG launched the business rates retention consultation in July 2011. DCLG subsequently published eight ‘technical papers’, to supplement and provide further detail on the initial consultation paper, in August 2011. The consultation period ended in October 2011, on 19th December 2011, the government produced its response to the business rates retention consultation, setting out how it intended that the business rates retention scheme will operate. The legislative framework required to introduce the business rates retention scheme forms part of the Local Government Finance Bill, introduced on 19th December 2011. The Government’s intention is that the new business rates retention scheme will be implemented from 1st April 2013.

Impacts for Croydon 5.7 In May 2012 the Government has made its intention, over two important

aspects of the scheme, known;-

• The Local/Central share - It has indicated that it intends to set the central share at 50%. This percentage will be fixed until any reset of the system i.e. re-assessing individual authorities’ baseline funding levels, potentially on the basis of a different assessment of need. The creation of a 50% central share will mean that the amount local authorities are able to keep in business rates (i.e. the remaining 50%) will be lower than the SR10 amounts for 2013/14 and 2014/15. The intention is, therefore, for Government to provide the remaining Spending Review allocation for local government through Revenue Support Grant (RSG). In effect, this arrangement extends what was going to be the 2013/14 adjustment grant, with grants for both the remaining SR10 years.

• The safety net and levy – The levy and the safety net are linked, as it is the levy (acting on authorities that have NDR growth) that will fund the safety net (to support authorities in NDR decline). It proposes to set:

a. The safety net threshold in the range 7.5% to 10% below spending baseline; and

b. A proportional levy ratio of 1:1 i.e. for every 1% increase in business rates base, an authority would see no more than a corresponding 1% increase in income, as measured against its spending baseline

201

5.8 Croydon is one of the 16 Community budget pilots and this has been live since April 2011. The work is focusing on building on the original pilot to create a Family Resilience Service. It aims to work with 60-70 families in the first phase building to over 200 families by the end of year 2. It has achieved support and commitment of resources from all partner agencies.

Other policy issues relevant to the July 2012 Review

Ringfencing

5.9 The Government has stated it will phase out the ringfencing of grants to

local government. The coalition government made a significant start to this in 2010/11 and continued it in the 2010 Spending Review. The only significant grant where ringfencing remains is the Dedicated Schools Grant (DSG) although it is proposed that the Public Health Grant will be ringfenced when introduced in 2013/14.

Housing Revenue Account

5.10 The Government reviewed the Housing Revenue Account (HRA) and

proposals to replace the subsidy funding with one of self-financing was contained in the Localism Bill.

5.11 Self Financing for the HRA commenced on 1st April 2012. The Council

borrowed £223.126m of debt financed on a maturity basis from the Public Works Loans Board (PWLB).

5.12 The full cost of introducing self-financing will fall on the HRA and will not

have any impact on the General Fund as the HRA will remain a ringfenced account for the foreseeable future.

New Homes Bonus Scheme 5.13 The scheme’s intention is to incentivise local authorities to increase

housing supply by rewarding them with a New Homes Bonus paid for the following six years as an unringfenced grant (through section 31 of the Local Government Act 2003). There are three elements to the scheme;-

1. Net additional new homes; 2. Empty homes brought back into use; and 3. Affordable Homes

5.14 Initially additional central Government funding arising from the abolition of

the Housing and Planning Delivery Grant will fund the full cost. This equates to £946m in total, initially phased at £196m in 2011/12 and almost £250m in each of the remaining three years. The Government anticipated that this funding will be sufficient until 2014/15. The first two years of the scheme have resulted in actual allocations of £199m in 2011/12 and £233m in 2012/13.

202

5.15 Funding after 2015/16 will come from top-slicing the Formula Grant. This redistributive mechanism of the New Homes Bonus means that the scheme will create financial winners and losers, for any authority to gain financially (relative to their formula grant allocation before the bonus), one or more authorities must lose. The implications for Croydon are currently being modelled for inclusion in the future Financial Strategy.

Impact on Croydon

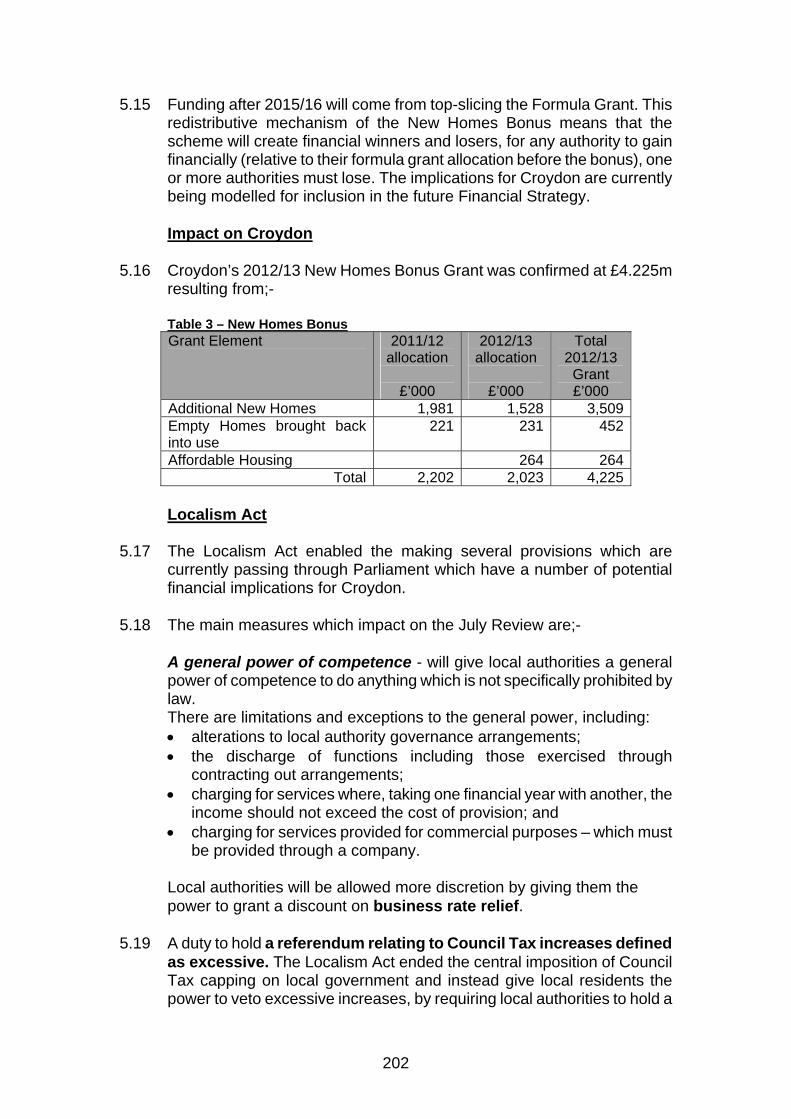

5.16 Croydon’s 2012/13 New Homes Bonus Grant was confirmed at £4.225m

resulting from;- Table 3 – New Homes Bonus

Grant Element 2011/12 allocation

£’000

2012/13 allocation

£’000

Total 2012/13

Grant £’000

Additional New Homes 1,981 1,528 3,509 Empty Homes brought back into use

221 231 452

Affordable Housing 264 264 Total 2,202 2,023 4,225

Localism Act 5.17 The Localism Act enabled the making several provisions which are

currently passing through Parliament which have a number of potential financial implications for Croydon.

5.18 The main measures which impact on the July Review are;-

A general power of competence - will give local authorities a general power of competence to do anything which is not specifically prohibited by law. There are limitations and exceptions to the general power, including: • alterations to local authority governance arrangements; • the discharge of functions including those exercised through

contracting out arrangements; • charging for services where, taking one financial year with another, the

income should not exceed the cost of provision; and • charging for services provided for commercial purposes – which must

be provided through a company.

Local authorities will be allowed more discretion by giving them the power to grant a discount on business rate relief.

5.19 A duty to hold a referendum relating to Council Tax increases defined

as excessive. The Localism Act ended the central imposition of Council Tax capping on local government and instead give local residents the power to veto excessive increases, by requiring local authorities to hold a

203

referendum on any proposed rise above a Government determined threshold.

5.20 The costs to the Council of holding a referendum would be in the region of about £250 – £300k should this need occur.

5.21 Local authorities will now need to allocate a ‘meaningful proportion’ of

Community Infrastructure Levy revenues back to the neighbourhoods where the development has taken place. However the Localism Act provides clarification that funds can be spent on the ongoing costs of infrastructure, as well as the initial costs of new infrastructure. It also gives local authorities greater control over setting their charging levels as although independent examiners will still consider whether the charging schedule is unreasonable, it will be for the authority to decide how to make it reasonable.

6.0 The Dedicated Schools Grant (DSG) 6.1 In the White Paper The Importance of Teaching the Government set out

its view that the current funding system is “opaque, full of anomalies and unfair and therefore in need of reform”.

6.2 The Government launched its consultation on 13 April 2011 and invited

views on the aims and objectives of the school funding system and the high level principles for any potential reforms. The follow up consultation in July 2011 contained details of a national funding formula model which would be introduced in the next spending review period. Its aim is to be clear and transparent, support the needs of pupils and enable schools to be able to make informed decisions. In April 2012 a further consultation was launched, this built on the responses from the earlier consultations and set out the proposed plans to proceed from 2013/14.

6.3 In 2013/14 there will be changes to the DSG funding which will mean the

DfE are well placed to introduce the national funding formula during the next spending review period.

6.4 The proposed changes are the introduction of three notional blocks :- i)

schools, ii) early years and iii) high needs, and the calculation of the DSG earlier.

6.5 Calculating the DSG on October pupil numbers as opposed to the

January numbers that are currently used will result in funding being calculated earlier and aid schools in setting budgets. This could lead to funding lagging behind pupil movements as historic data is being used, and therefore impact on the capacity to meet pupil place needs.

6.6 The Schools Block will result in more funding being delegated to schools 6.7 In the first instance and schools can decide to buy back centrally provided

services on an individual basis or de delegate some of their funding back

204

to the local authority as a collective group via the schools forum. The delegation of a greater proportion of the funding directly to schools may impact on the services provided centrally if schools decide not to buy back these services.

6.8 The Early Years block will continue to be funded on the January pupil

numbers and be updated to reflect actual pupil numbers in the year. This will result in the early years funding from the EFA more accurately reflecting the pupils.

6.9 The High Needs block will cover funding for pupils and students from birth

to 25 years in line with the proposals in the Green Paper on SEN and Disability, this will introduce an integrated and coherent approach to assessment and provision.

6.10 The final funding arrangements for 2013/14 are still being drawn up and

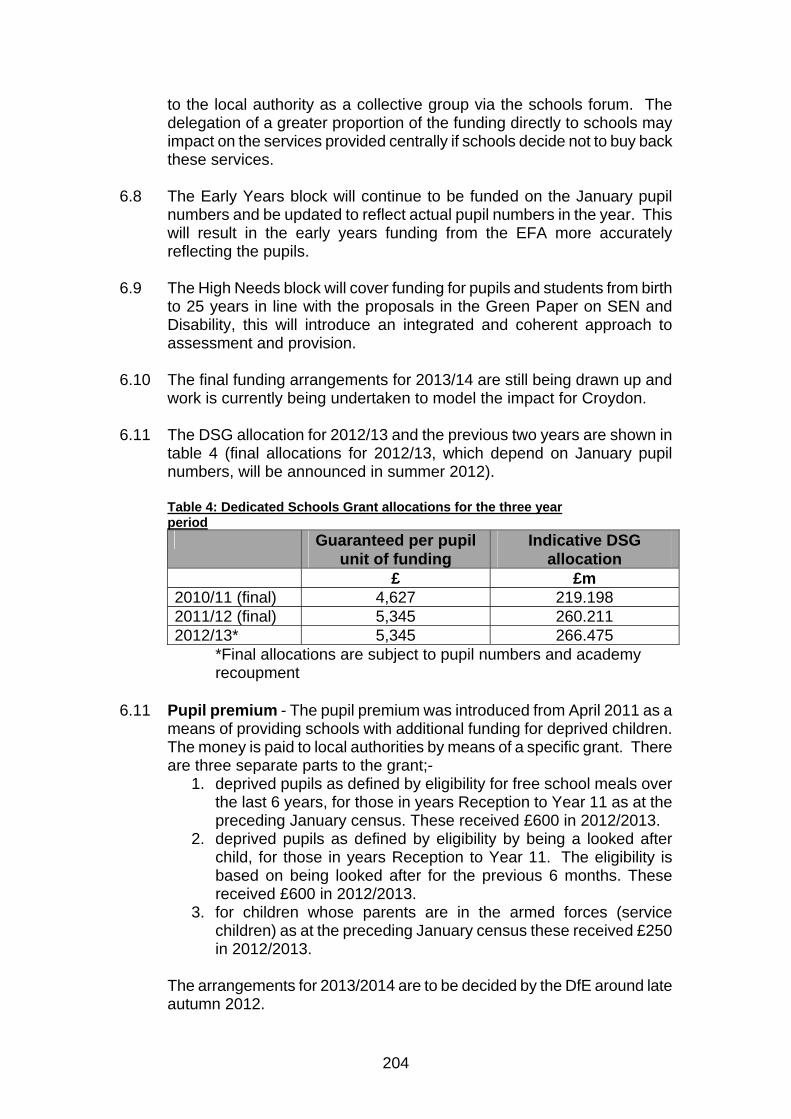

work is currently being undertaken to model the impact for Croydon. 6.11 The DSG allocation for 2012/13 and the previous two years are shown in

table 4 (final allocations for 2012/13, which depend on January pupil numbers, will be announced in summer 2012).

Table 4: Dedicated Schools Grant allocations for the three year period

Guaranteed per pupil unit of funding

Indicative DSG allocation

£ £m 2010/11 (final) 4,627 219.198 2011/12 (final) 5,345 260.211 2012/13* 5,345 266.475

*Final allocations are subject to pupil numbers and academy recoupment

6.11 Pupil premium - The pupil premium was introduced from April 2011 as a

means of providing schools with additional funding for deprived children. The money is paid to local authorities by means of a specific grant. There are three separate parts to the grant;-

1. deprived pupils as defined by eligibility for free school meals over the last 6 years, for those in years Reception to Year 11 as at the preceding January census. These received £600 in 2012/2013.

2. deprived pupils as defined by eligibility by being a looked after child, for those in years Reception to Year 11. The eligibility is based on being looked after for the previous 6 months. These received £600 in 2012/2013.

3. for children whose parents are in the armed forces (service children) as at the preceding January census these received £250 in 2012/2013.

The arrangements for 2013/2014 are to be decided by the DfE around late autumn 2012.

205

6.12 Academy Funding - Academies will continue to be funded by the

Education Funding Agency but on the basis of the formula set by the local authority. This will ensure that both Academies and local maintained schools continue to be funded on a fair and comparable basis. This simplified formula will make it much easier for Academies to understand and manage their budgets. By delegating the maximum amount of the schools block straight to maintained schools and academies from 2013/14 means that there will no longer be the need for LACSEG (Local Authority Central Spend Equivalent Grant). This is because Academies will receive this funding up front as part of their budget share that has been calculated by the EFA in accordance with the Local Authorities formula.

Conclusions on Budget Assumptions 1, 2 and 3

6.13 For this strategy it would be prudent to assume that the provisional CSR

2014 gives a broad indication of the level of Government support that Croydon will actually receive in terms of both Formula and Specific Grants. Therefore our assumption is that this will decline by 7.5% per year in 2015/16 and 2016/17. The distribution of Specific Grants supporting specific services, at the assumed new levels, will be examined through the challenge process with any pressure on or savings from existing services identified through that process.

Budget Assumption 4

6.14 The Council Tax Freeze Grant rewarded Councils who maintained their

2011/12 Council Tax at the previous year’s level with a grant equivalent to a 2.5% increase. The grant has been confirmed for 2011/12 and Treasury figures show Government support for that grant for the duration of the Spending Review period. However CLG have also confirmed that Councils who maintained their 2012/13 Council Tax at the previous year’s level with a grant equivalent to a 2.5% increase will receive the 2012/13 allocation for 2012/13 only and therefore this places additional pressure on balancing the budget for 2013/14.

7.0 Economic Outlook

Budget Assumption 5 7.1 The national and global economic climate has changed dramatically since

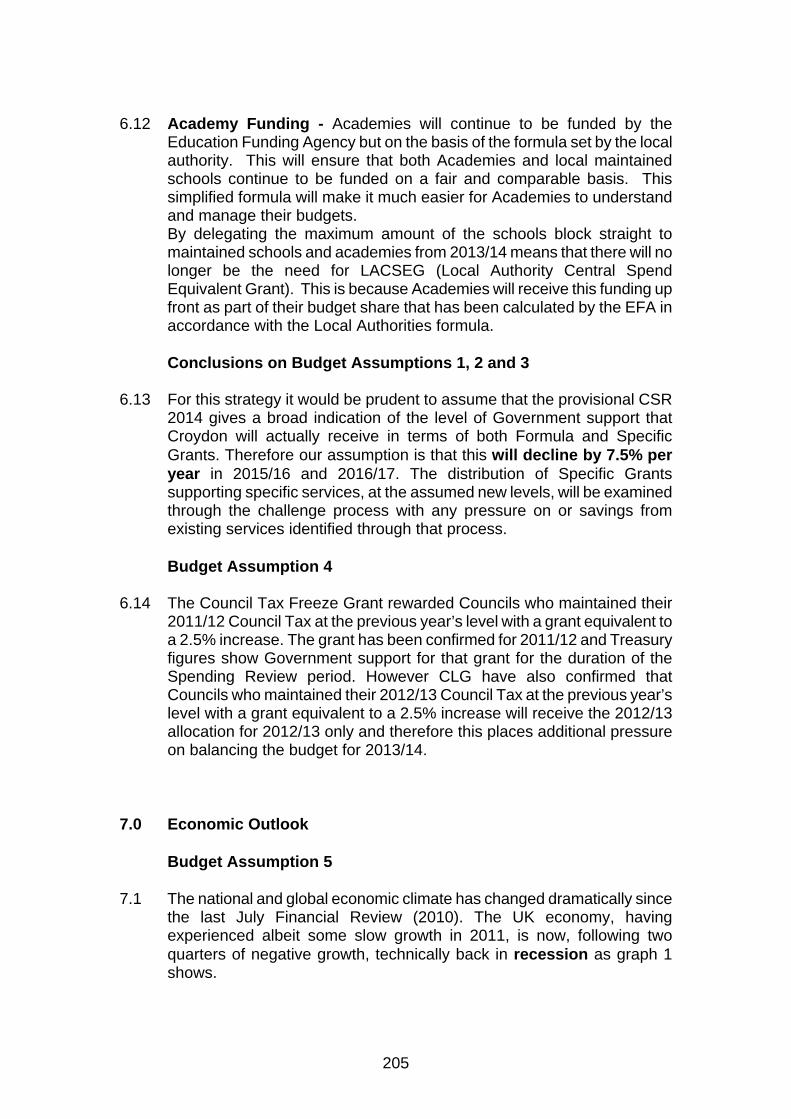

the last July Financial Review (2010). The UK economy, having experienced albeit some slow growth in 2011, is now, following two quarters of negative growth, technically back in recession as graph 1 shows.

206

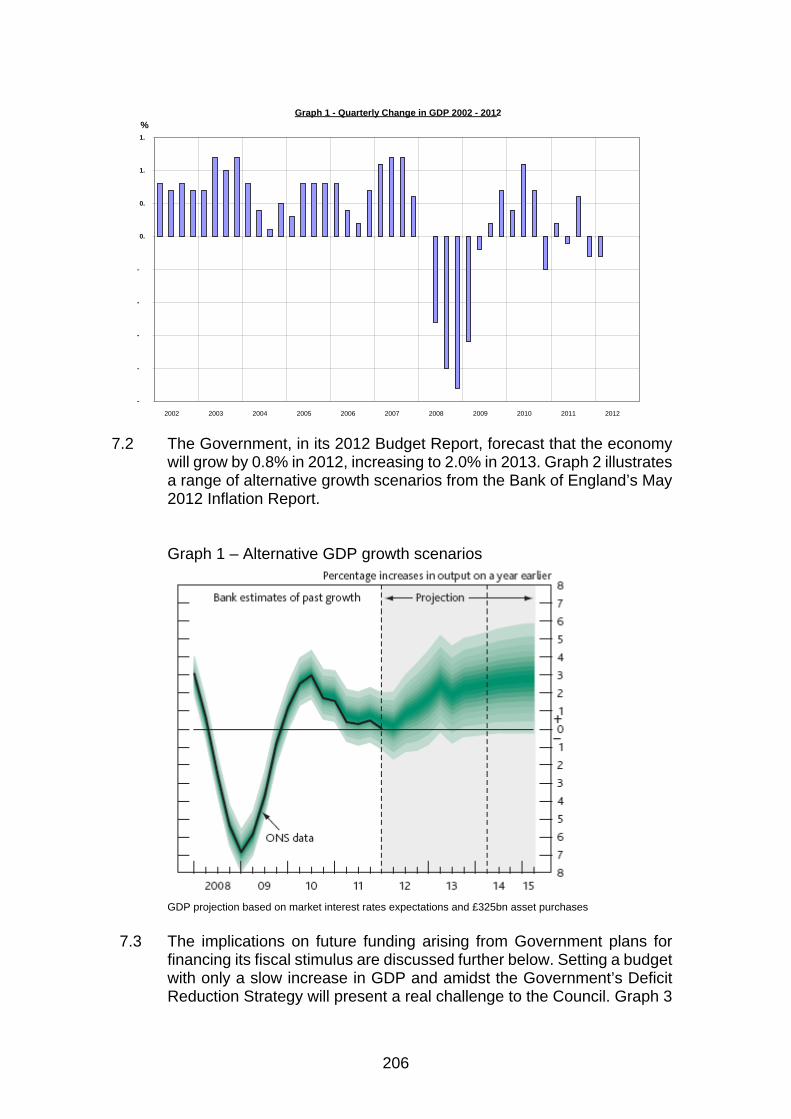

7.2 The Government, in its 2012 Budget Report, forecast that the economy

will grow by 0.8% in 2012, increasing to 2.0% in 2013. Graph 2 illustrates a range of alternative growth scenarios from the Bank of England’s May 2012 Inflation Report. Graph 1 – Alternative GDP growth scenarios

GDP projection based on market interest rates expectations and £325bn asset purchases

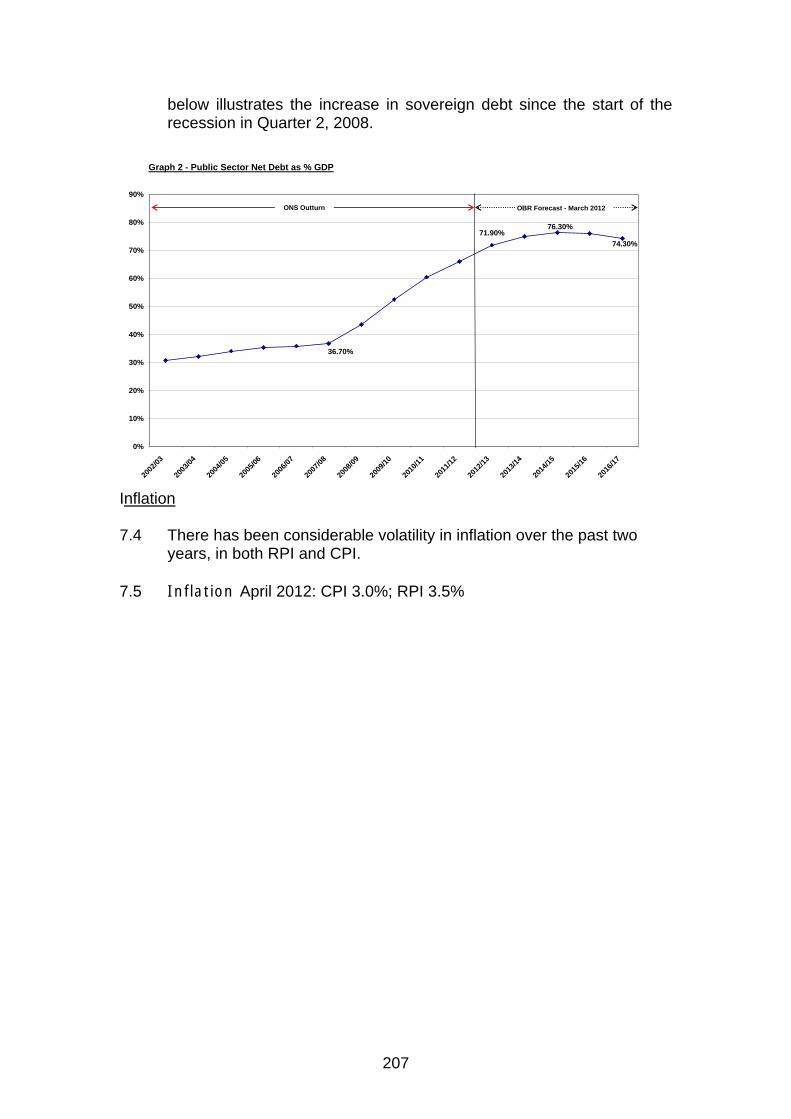

7.3 The implications on future funding arising from Government plans for

financing its fiscal stimulus are discussed further below. Setting a budget with only a slow increase in GDP and amidst the Government’s Deficit Reduction Strategy will present a real challenge to the Council. Graph 3

Graph 1 - Quarterly Change in GDP 2002 - 2012

-

-

-

-

-

0.

0.

1.

1.

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

%

207

below illustrates the increase in sovereign debt since the start of the recession in Quarter 2, 2008.

Graph 2 - Public Sector Net Debt as % GDP

36.70%

71.90%74.30%

76.30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

2012

/13

2013

/14

2014

/15

2015

/16

2016

/17

OBR Forecast - March 2012 ONS Outturn

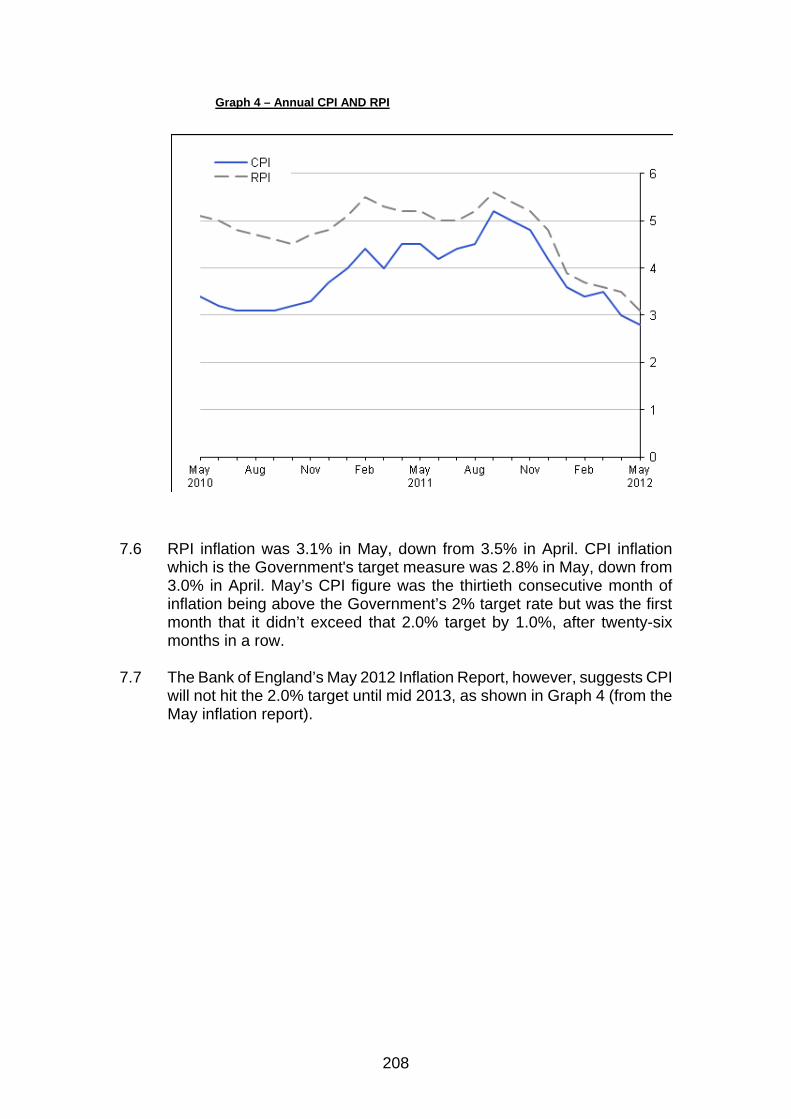

Inflation 7.4 There has been considerable volatility in inflation over the past two

years, in both RPI and CPI. 7.5 Inflation April 2012: CPI 3.0%; RPI 3.5%

208

Graph 4 – Annual CPI AND RPI

7.6 RPI inflation was 3.1% in May, down from 3.5% in April. CPI inflation which is the Government's target measure was 2.8% in May, down from 3.0% in April. May’s CPI figure was the thirtieth consecutive month of inflation being above the Government’s 2% target rate but was the first month that it didn’t exceed that 2.0% target by 1.0%, after twenty-six months in a row.

7.7 The Bank of England’s May 2012 Inflation Report, however, suggests CPI

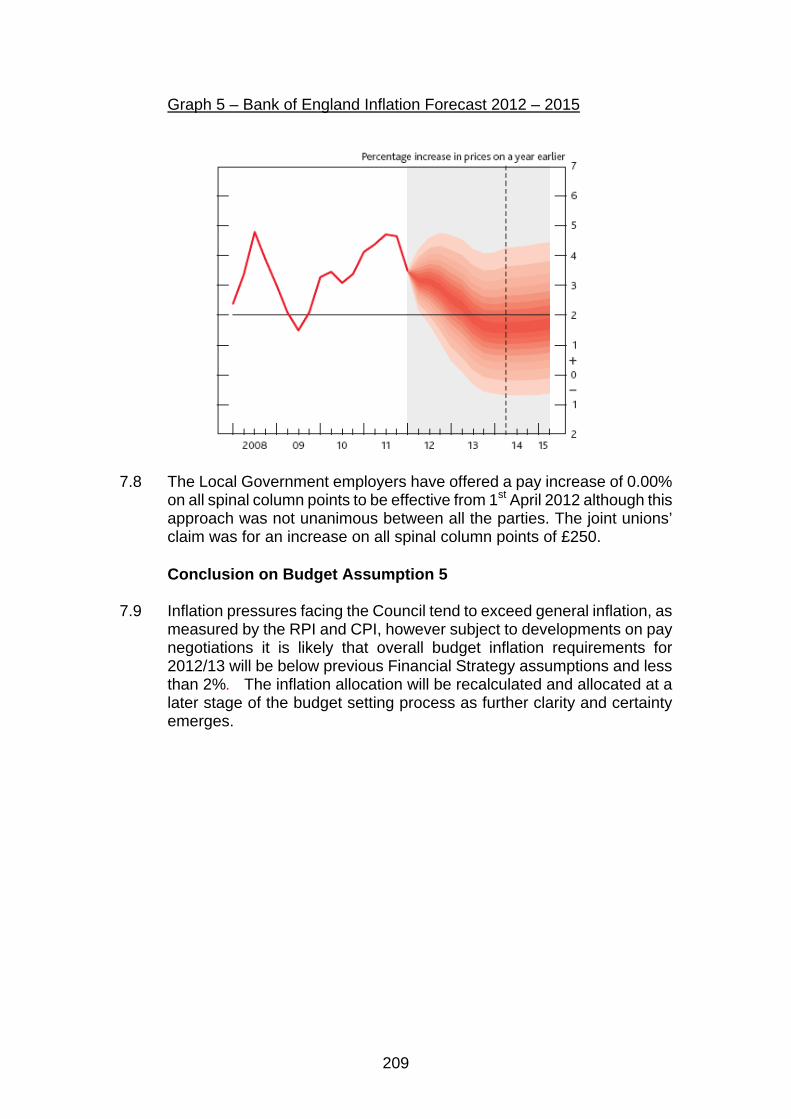

will not hit the 2.0% target until mid 2013, as shown in Graph 4 (from the May inflation report).

209

Graph 5 – Bank of England Inflation Forecast 2012 – 2015

7.8 The Local Government employers have offered a pay increase of 0.00%

on all spinal column points to be effective from 1st April 2012 although this approach was not unanimous between all the parties. The joint unions’ claim was for an increase on all spinal column points of £250.

Conclusion on Budget Assumption 5

7.9 Inflation pressures facing the Council tend to exceed general inflation, as measured by the RPI and CPI, however subject to developments on pay negotiations it is likely that overall budget inflation requirements for 2012/13 will be below previous Financial Strategy assumptions and less than 2%. The inflation allocation will be recalculated and allocated at a later stage of the budget setting process as further clarity and certainty emerges.

210

Budget Assumption 6 7.10 For the period of the next financial strategy the Council will focus on the

delivery of departmental transformation programmes to deliver the efficiencies and improvements required to balance the budgetary gap over this coming period. The transformation plans will form a key part of the budget planning process

Conclusion on Budget Assumption 6

7.11 The Council will be focusing on departmental transformation plans to

delivers efficiencies and it has been assumed that the plans will deliver £10m of savings for the purpose of the financial strategy planning assumptions.

Reserves & Balances

Budget Assumption 8 7.12 The Council has a General Fund balance of £11.597m as at 31 March

2012 (£11.597m as at 31 March 2011) and earmarked reserves of £45.422m (£37.976m as at 31 March 2011).This includes a reserve for CCURV Affordability which has increased by £2.524m to £10.227m. This reserve is where any income is held in order to pay for Bernard Weatherill House.

7.13 Members were aware of the issues relating to having such a limited

General Fund balance before 31st March 2009 and the advice of the Executive Director of Corporate Resources and Customer Services at the time of setting the budget. The General Fund balances act as a fund to meet unanticipated costs arising in the year or overspends against budgets.

211

Graph 6 - London Borough Reserves & Balances by % for 2010/11

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

BrentH

arrowH

illingdonKingston upon Tham

esBarking & D

agenhamSuttonEnfieldM

ertonH

ounslowW

estminster

IslingtonN

ewham

Croydon

BarnetH

aringeyR

edbridgeBexleyW

altham Forest

Lewisham

Ham

mersm

ith & FulhamR

ichmond upon Tham

esLam

bethEalingH

averingBrom

leySouthw

arkTow

er Ham

letsC

amden

Hackney

City of London

Wandsw

orthKensington & C

helseaG

reenwich

7.14 The 2010/14 Financial Strategy has an objective to increase general fund

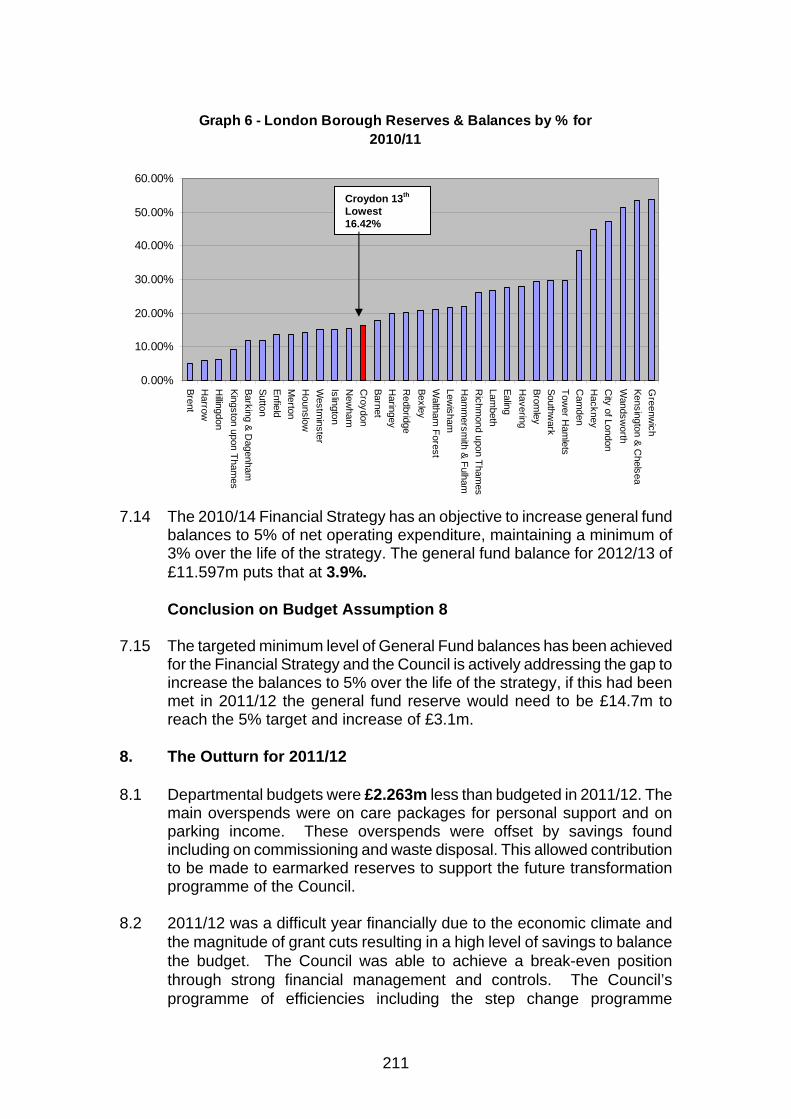

balances to 5% of net operating expenditure, maintaining a minimum of 3% over the life of the strategy. The general fund balance for 2012/13 of £11.597m puts that at 3.9%.

Conclusion on Budget Assumption 8

7.15 The targeted minimum level of General Fund balances has been achieved

for the Financial Strategy and the Council is actively addressing the gap to increase the balances to 5% over the life of the strategy, if this had been met in 2011/12 the general fund reserve would need to be £14.7m to reach the 5% target and increase of £3.1m.

8. The Outturn for 2011/12

8.1 Departmental budgets were £2.263m less than budgeted in 2011/12. The

main overspends were on care packages for personal support and on parking income. These overspends were offset by savings found including on commissioning and waste disposal. This allowed contribution to be made to earmarked reserves to support the future transformation programme of the Council.

8.2 2011/12 was a difficult year financially due to the economic climate and

the magnitude of grant cuts resulting in a high level of savings to balance the budget. The Council was able to achieve a break-even position through strong financial management and controls. The Council’s programme of efficiencies including the step change programme

Croydon 13th Lowest 16.42%

212

successfully delivered the savings required.

8.3 This means that the Council has been able to maintain its General Fund balance of £11.597m against the minimum targeted sum of £8.835m (3% of net service expenditure) for 31st March 2012. This represents general fund balances of 3.9% against the 5% longer-term target established under the new financial strategy. The achievement and maintenance of a prudent level of general balances, provides assurance against the potential risks from the external environment and the significant challenges facing the public sector and has enabled the Council to manage the recent upheaval in the national economy from a position of relative financial strength. This has added importance given the future changes expected in local government funding particularly those in relation to the localisation of business rates and council tax benefit, which add potential risk to local authorities.

8.4 The Council’s General Fund reserves have increased by £4.620m (8.1%) from £57.339m to £60.582m as at 31st March 2012. Within this total, Locally Managed Schools’ reserves have decreased by £4.605m to £15.160m and the remaining reserves have increased by £7.248m (18.8%) to £45.422m.

8.5 The Council’s General Fund Provisions have decreased by £1.744m

(5.3%) from £33.063m to £31.319m as at 31st March 2012. 8.6 The Collection Fund has carried forward a £7.860m surplus at 31st March

2012. This position will be kept under review given the nature and challenges of council tax collection.

8.7 The Council’s Pension Fund increased in value in 2011/12 by £47.093m

(7.5%) to a value of £630.554m.

8.8 The original approved General Fund Services capital programme (excluding the Housing Investment Programme) totalled £158.907m and was increased during the year to £205.774m to reflect programme slippage from 2010/11 and additional government grants. Outturn capital spending was £160.123m. The detail of the programme is set out in Appendix 1. Cabinet are asked to approve the slippage of £42.187m to enable the completion of those schemes.

9. The Budget for 2012/13 9.1 The 2012/13 budget was approved by Council on the 20th February 2012.

Given the loss of government funding the approved budget includes a significant amount of savings which were required to deliver a balanced budget and as such presents the council with a challenge in terms of delivery.

213

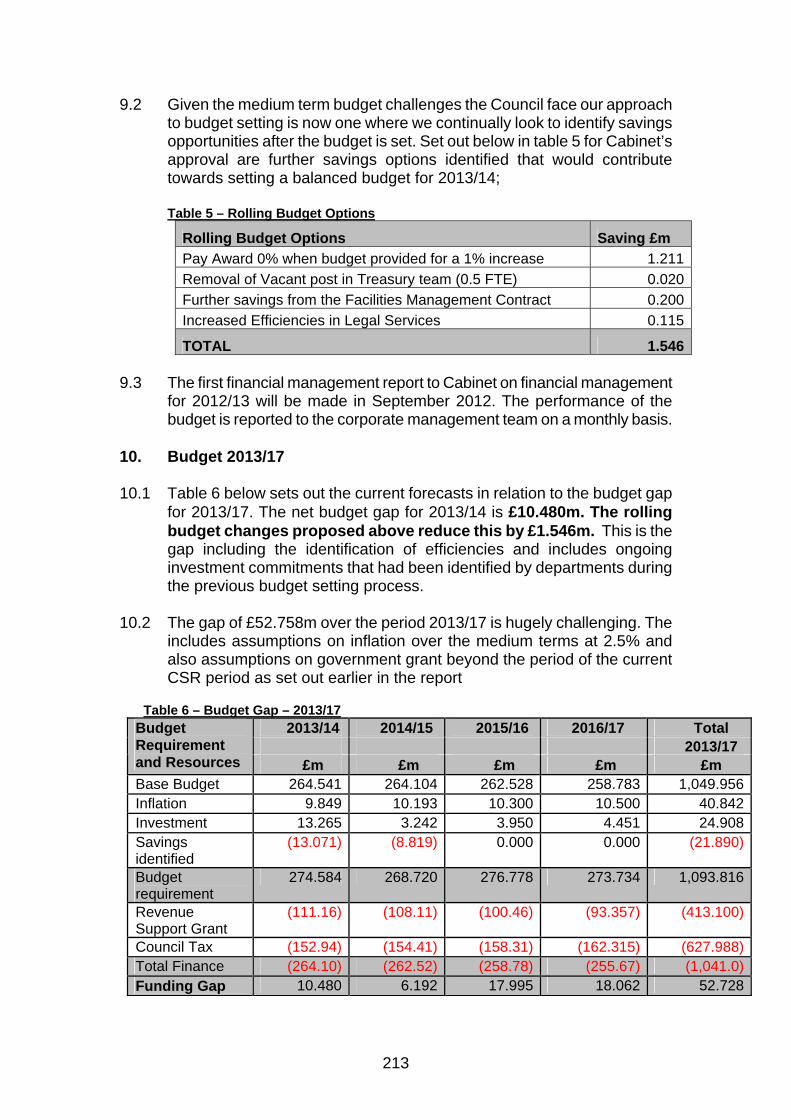

9.2 Given the medium term budget challenges the Council face our approach to budget setting is now one where we continually look to identify savings opportunities after the budget is set. Set out below in table 5 for Cabinet’s approval are further savings options identified that would contribute towards setting a balanced budget for 2013/14;

Table 5 – Rolling Budget Options

Rolling Budget Options Saving £m Pay Award 0% when budget provided for a 1% increase 1.211Removal of Vacant post in Treasury team (0.5 FTE) 0.020Further savings from the Facilities Management Contract 0.200Increased Efficiencies in Legal Services 0.115

TOTAL 1.546 9.3 The first financial management report to Cabinet on financial management

for 2012/13 will be made in September 2012. The performance of the budget is reported to the corporate management team on a monthly basis.

10. Budget 2013/17 10.1 Table 6 below sets out the current forecasts in relation to the budget gap

for 2013/17. The net budget gap for 2013/14 is £10.480m. The rolling budget changes proposed above reduce this by £1.546m. This is the gap including the identification of efficiencies and includes ongoing investment commitments that had been identified by departments during the previous budget setting process.

10.2 The gap of £52.758m over the period 2013/17 is hugely challenging. The

includes assumptions on inflation over the medium terms at 2.5% and also assumptions on government grant beyond the period of the current CSR period as set out earlier in the report

Table 6 – Budget Gap – 2013/17

2013/14 2014/15 2015/16 2016/17 Total 2013/17

Budget Requirement and Resources £m £m £m £m £m Base Budget 264.541 264.104 262.528 258.783 1,049.956Inflation 9.849 10.193 10.300 10.500 40.842Investment 13.265 3.242 3.950 4.451 24.908Savings identified

(13.071) (8.819) 0.000 0.000 (21.890)

Budget requirement

274.584 268.720 276.778 273.734 1,093.816

Revenue Support Grant

(111.16) (108.11) (100.46) (93.357) (413.100)

Council Tax (152.94) (154.41) (158.31) (162.315) (627.988)Total Finance (264.10) (262.52) (258.78) (255.67) (1,041.0)Funding Gap 10.480 6.192 17.995 18.062 52.728

214

Major Financial Impacts over the period 2013/17

10.3 Council Tax Benefit Localisation

10.4 As part of the Spending Review 2010, the Government announced that it intended to localise council tax benefit (CTB) from 2013/14 (1st April) with a 10% reduction in funding support for local authorities to meet the cost of council tax benefit. These plans were included as part of the terms of reference for the Local Government Resource Review.

10.5 These proposed changes represent a significant potential cost to the

Council of £4.84m per annum with an additional increased cost each financial year as a consequence of the continuing increase in demand for council tax benefit. This is factored into the budget gap set out in Table 6.

10.6 The Council is therefore proposing a consultation process in relation to

potential options to include within a local council tax benefit scheme with a clear intention to reduce the financial impact resulting directly from a reduction in central Government funding towards the cost of council tax benefit. A report is set out elsewhere on the agenda which recommends launching consultation of a series of principles in relation to a local scheme

10.7 Demographic changes

10.8 Croydon’s population is estimated at 345,600 (2010 mid-year estimates) which is up by 2,700 people from 2009. This is one of the highest increases across the London boroughs. Croydon’s population is weighted towards those in their late 20s – 50, with fewer people in their teens/early twenties. There is also a high population aged around 65 - the immediate post-war generation. Croydon’s population is estimated to grow to 377,100 by 2031 (London Plan estimates). In particular, increases are expected in the under 15 and the 25 to 40 age groups. Croydon’s population is also less transient (mobile) than the average for London. Over the next twenty years there is expected to be an increase nationally of 1.7m people with a care need and of the present cohort of over 65 year olds one in five will individually require care costing over £50k. For Croydon since 2006/07 there has been on average a 5% increase in service demand. To date these costs have been met through transformational savings but this is not sustainable indefinitely.

215

10.9 Increases in the cost of Homelessness

10.10 With the impact of the recession, reduced government funding for public

services and the changes to housing benefit Croydon has already started to see an increase in homelessness. A report commissioned (Jenkins Duval) indicates that there are forecast to be an extra 435 statutory homelessness cases in 2012/13 and a further 500 in 2013/14. The likely increase in costs for Croydon to deal with these cases is £0.990m in 2012/13 and £1.140m in 2013/14.

10.11 Various initiatives are being progressed to provide additional

accommodation within the private rented sector as well as increasing capacity within Council stock. Whilst these will help alleviate the pressure, there is a risk that continuing numbers will present themselves as homeless as a result of the implementation of Universal Credit which will cap total benefits to £500 per week.

10.12 Dilnot review

10.13 The Dilnot review was launched on 20th July 2010; the Commission on Funding of Care and Support was an independent body tasked by Government with reviewing the funding system for care and support in England. The report built on the extensive body of work already done in this area and carried out new analysis before providing advice and recommendations on how to reform the system to Government on 4th July 2011.

10.14 Previous commitments to publish a White Paper on Social Care reform have been delayed, with the latest estimate for publication being June 2012. Reports in some quarters that the costs of implementing the recommendations made by the Dilnot Commission are a key obstacle to any reform of adult social care, though cross party talks on reform are said to be progressing well.

10.15 However without Government support to the recommendations this will

leave all local authorities with a major ongoing financial problem as the numbers of people requiring social care services will grow significantly over the next 10 to 15 years.

10.16 Social care services are also currently covered by ‘at least’ twelve pieces

of legislation, and the Government has previously suggested that any new Bill would bring all those statutes together. This bill along with additional funding would be welcomed.

10.17 HRA Self Financing 10.18 Self Financing for the HRA commenced on 1st April 2012. Croydon took

on £223.126m of debt financed on a maturity basis from the Public Works Loans Board. The HRA has a 30 year business plan in place which is fully

216

self funded and its financial strategy will now run in tandem with the General Fund. The end of the former subsidy system has already enabled Croydon to invest and additional £9m in its Repair and Improvement Programme in 2012/13 as well as ongoing investment in its new build programme which will deliver 32 new homes a year from 2013/14. Given the change to funding, as a council we can now approach the long term with more certainty and ensure that our Housing Financial Strategy is a key strand of our Financial Strategy

10.19 Public Health 10.20 From 1 April 2013 the responsibility for providing this service will transfer

to local authorities. There are still many details to be finalised nationally including whether the staff will transfer over or remain part of the NHS (where it would appear they will retain their pensions) and the exact level of funding. Council staff are working with PCT colleagues to validate information using a 2010/11 baseline and imminently there will be a submission of 2011/12 data, the whole envelope of funding (which includes services in relation to children that are likely to transfer over circa 2015) is approximately £17m (to be confirmed), but figures are still some way off being finalised. This transfer will also mean that the Director of Public Health will be a full member of the Council’s Management Team. Croydon have already embraced this change and much joint working is already underway.

11.0 Capital Programme Financing and Investment Income 11.1 Slippage on capital spending from the 2011/12 financial outturn has been

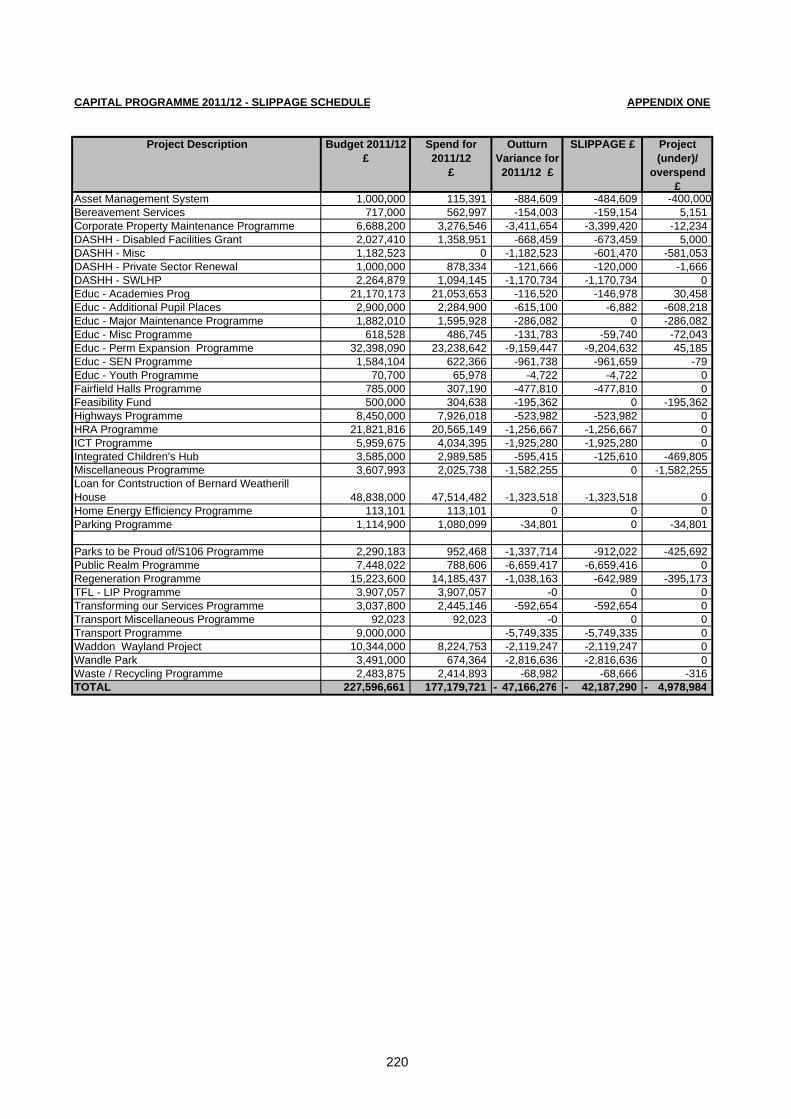

reviewed and it is recommended that the slippage on the schemes set out in Appendix 1, totalling £42.187m, is approved to be carried forward to 2012/13.

11.2 General Fund (GF) Debt 11.3 The long term strategic planning assumption underpinning the current policy

is that for the GF, Croydon needs to take up £54.1m of prudential borrowing in 2012/13, and thereafter £50.0m in 2013/14 and £50.0m in 2014/15. This is as set out in the Treasury Management Strategy approved by Full Council on 27th February 2012. The Council’s overall debt as at 31 March 2012 was £619.264m. This debt included loans taken to fund past GF and Housing Revenue Account (HRA) capital schemes, the £223.126m borrowed on 28/03/12 for the HRA Self Financing settlement sum (see 12.4 below) and borrowing undertaken to finance Bernard Weatherill House. The level of future planned borrowing will leave the Authority with an estimated debt outstanding of £821.181m as at 31st March 2015.

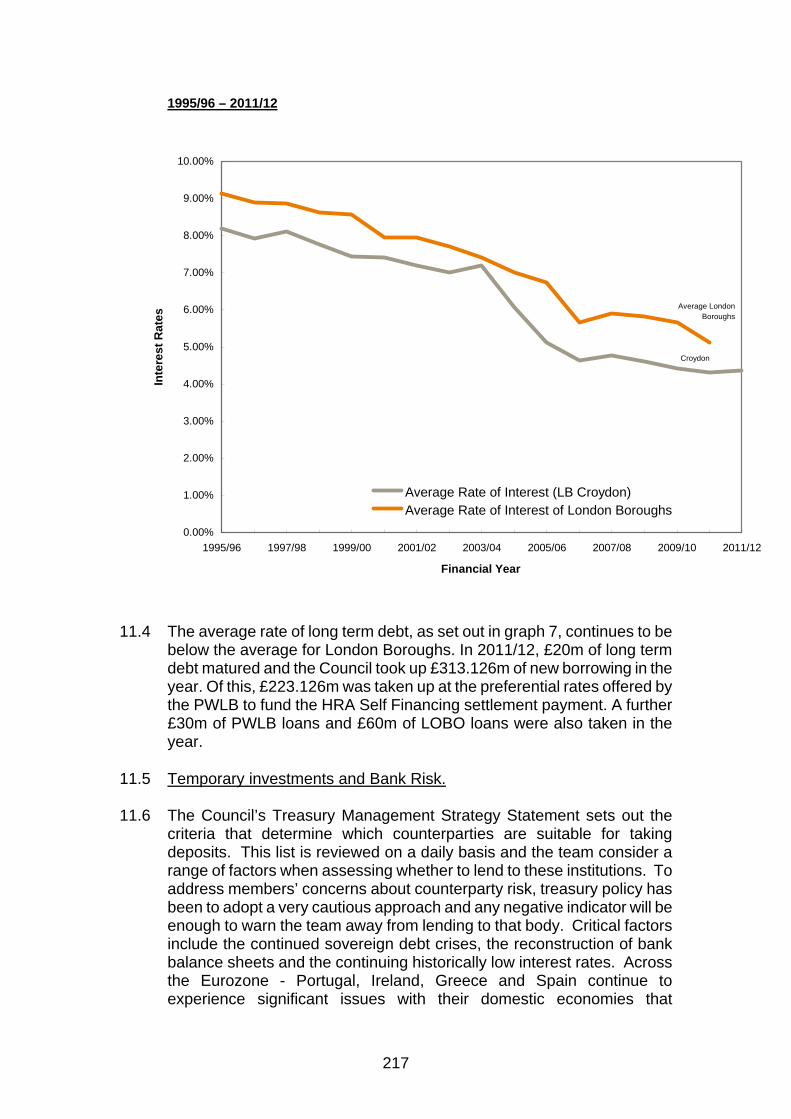

Graph 7 - London Borough of Croydon - Average Rate of Long Term Debt

217

1995/96 – 2011/12

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

1995/96 1997/98 1999/00 2001/02 2003/04 2005/06 2007/08 2009/10 2011/12

Financial Year

Inte

rest

Rat

es

Average Rate of Interest (LB Croydon)Average Rate of Interest of London Boroughs

Average London Boroughs

Croydon

11.4 The average rate of long term debt, as set out in graph 7, continues to be below the average for London Boroughs. In 2011/12, £20m of long term debt matured and the Council took up £313.126m of new borrowing in the year. Of this, £223.126m was taken up at the preferential rates offered by the PWLB to fund the HRA Self Financing settlement payment. A further £30m of PWLB loans and £60m of LOBO loans were also taken in the year.

11.5 Temporary investments and Bank Risk. 11.6 The Council’s Treasury Management Strategy Statement sets out the

criteria that determine which counterparties are suitable for taking deposits. This list is reviewed on a daily basis and the team consider a range of factors when assessing whether to lend to these institutions. To address members’ concerns about counterparty risk, treasury policy has been to adopt a very cautious approach and any negative indicator will be enough to warn the team away from lending to that body. Critical factors include the continued sovereign debt crises, the reconstruction of bank balance sheets and the continuing historically low interest rates. Across the Eurozone - Portugal, Ireland, Greece and Spain continue to experience significant issues with their domestic economies that

218

effectively excludes their banking sectors from the Authority’s authorised lending list. Within the global banking sector, Australian and Canadian banks have maintained their robust ratings and for some of the UK’s part nationalised banks longer term deposits are attracting slightly higher rates. However for the remainder of 2012 the outlook looks like continuing low rates being offered by a select group of quality banks, augmented by lending to other local authorities and short-term deposits in AAA-rated vehicles. The focus will continue to be on diligent scrutiny to prioritise security of deposits over riskier rates of return.

Graph 8 - Temporary Investments Outstanding at Year End 1998/99 to 2011/12

0

20

40

60

80

100

120

140

160

180

200

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

2004

/05

2005

/06

2006

/07

2007

/08

2008

/09

2009

/10

2010

/11

2011

/12

Financial Years

£m

12. Timetable 12.1 The Financial Planning Timetable for 2012/13 can be seen in Table 9.

Table 8 – The Council’s Service and Financial Planning Timetable Date Activity April 12 Commence work on strategic budget setting, in

conjunction with service planning. 9th July 12 Report to Cabinet setting out the financial environment

and the annual review of the Financial Strategy. Dec 12 Local Government Provisional Settlement announced. 10th Dec 12 Cabinet approves the options package and recommends

to Council. Jan 13 Local Government Final Settlement announced. 15 Jan 13 Scrutiny & Strategic Overview Committee. 11th Feb 13 Cabinet approves the Council Tax and recommends it to

the Council. 25th Feb 13 Council approves the Council Tax.

219

13. SUMMARY AND CONCLUSIONS 13.1 As all Members are aware, setting a budget for 2013/15 that is robust,

balanced and deliverable is challenging and will involved a number of difficult decisions in these challenging of times.

14. FINANCIAL CONSIDERATIONS 14.1 This report deals with the Financial Strategy assumptions in planning a

balanced budget over the medium term. (Approved by Richard Simpson, Director of Finance). 15. COMMENTS OF THE SOLICITOR TO THE COUNCIL 15.1 The Solicitor to the Council comments that the information in this report

supports the Council’s statutory duty to set a balanced budget. (Approved by Gabriel MacGregor, Head of Corporate Law on behalf of the

Council Solicitor and Monitoring Officer.) 16. HUMAN RESOURCES IMPACT 16.1 There are no direct Human Resources implications arising from this

report. Approved by: Chris Baldwin, on behalf of the Director, Workforce &

Community Relations 17. EQUALITIES IMPACT 17.1 There are no specific issues arising from this report. 18. ENVIRONMENTAL IMPACT 18.1 There are no specific issues arising from this report. 19. CRIME AND DISORDER REDUCTION IMPACT 19.1 There are no specific issues arising from this report.

Report Author: Nathan Elvery, Executive Director of Resources & Customer Services

Contact Person: Nathan Elvery, Executive Director of Resources & Customer Services

Background docs: Financial Strategy

CAPITAL PROGRAMME 2011/12 - SLIPPAGE SCHEDULE APPENDIX ONE

Project Description Budget 2011/12 £

Spend for 2011/12

£

Outturn Variance for 2011/12 £

SLIPPAGE £ Project (under)/

overspend £

Asset Management System 1,000,000 115,391 -884,609 -484,609 -400,000 Bereavement Services 717,000 562,997 -154,003 -159,154 5,151Corporate Property Maintenance Programme 6,688,200 3,276,546 -3,411,654 -3,399,420 -12,234 DASHH - Disabled Facilities Grant 2,027,410 1,358,951 -668,459 -673,459 5,000DASHH - Misc 1,182,523 0 -1,182,523 -601,470 -581,053 DASHH - Private Sector Renewal 1,000,000 878,334 -121,666 -120,000 -1,666 DASHH - SWLHP 2,264,879 1,094,145 -1,170,734 -1,170,734 0Educ - Academies Prog 21,170,173 21,053,653 -116,520 -146,978 30,458Educ - Additional Pupil Places 2,900,000 2,284,900 -615,100 -6,882 -608,218 Educ - Major Maintenance Programme 1,882,010 1,595,928 -286,082 0 -286,082 Educ - Misc Programme 618,528 486,745 -131,783 -59,740 -72,043 Educ - Perm Expansion Programme 32,398,090 23,238,642 -9,159,447 -9,204,632 45,185Educ - SEN Programme 1,584,104 622,366 -961,738 -961,659 -79 Educ - Youth Programme 70,700 65,978 -4,722 -4,722 0Fairfield Halls Programme 785,000 307,190 -477,810 -477,810 0Feasibility Fund 500,000 304,638 -195,362 0 -195,362 Highways Programme 8,450,000 7,926,018 -523,982 -523,982 0HRA Programme 21,821,816 20,565,149 -1,256,667 -1,256,667 0ICT Programme 5,959,675 4,034,395 -1,925,280 -1,925,280 0Integrated Children's Hub 3,585,000 2,989,585 -595,415 -125,610 -469,805 Miscellaneous Programme 3,607,993 2,025,738 -1,582,255 0 -1,582,255 Loan for Contstruction of Bernard Weatherill House 48,838,000 47,514,482 -1,323,518 -1,323,518 0Home Energy Efficiency Programme 113,101 113,101 0 0 0Parking Programme 1,114,900 1,080,099 -34,801 0 -34,801

Parks to be Proud of/S106 Programme 2,290,183 952,468 -1,337,714 -912,022 -425,692 Public Realm Programme 7,448,022 788,606 -6,659,417 -6,659,416 0Regeneration Programme 15,223,600 14,185,437 -1,038,163 -642,989 -395,173 TFL - LIP Programme 3,907,057 3,907,057 -0 0 0Transforming our Services Programme 3,037,800 2,445,146 -592,654 -592,654 0Transport Miscellaneous Programme 92,023 92,023 -0 0 0Transport Programme 9,000,000 -5,749,335 -5,749,335 0Waddon Wayland Project 10,344,000 8,224,753 -2,119,247 -2,119,247 0Wandle Park 3,491,000 674,364 -2,816,636 -2,816,636 0Waste / Recycling Programme 2,483,875 2,414,893 -68,982 -68,666 -316 TOTAL 227,596,661 177,179,721 47,166,276- 42,187,290- 4,978,984-

220