correlation - cboe | cboe options exchange correlation (definition) 3 pairwise, portfolio-weighted...

TRANSCRIPT

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices. 1

Interpreting Global and U.S. Correlations

CORRELATION

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

AGENDA

2

• Overview of correlation in major markets

• Motivate relationship between correlation and volatility

• Outline derivation of vol / correlation dependence

• Introduce dispersion as the complement to volatility

• Implications, particularly correlation as a measure of fragility

• Consequences of changes in dispersion via equity factors

• Brief remarks on benchmarking dispersion

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

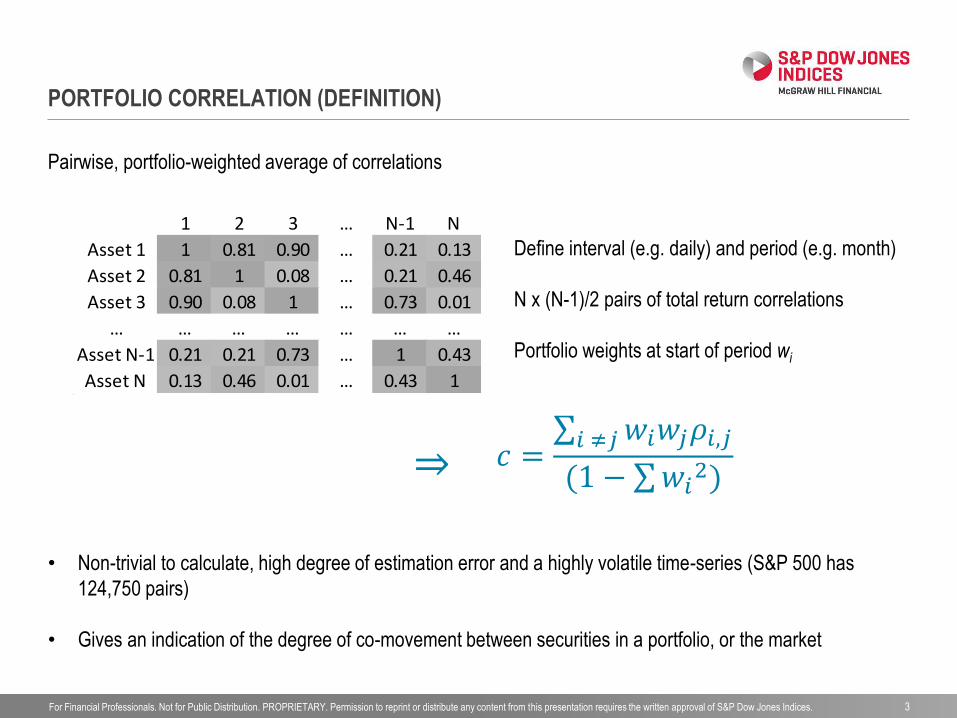

PORTFOLIO CORRELATION (DEFINITION)

3

Pairwise, portfolio-weighted average of correlations

1 2 3 … N-1 N

Asset 1 1 0.81 0.90 … 0.21 0.13

Asset 2 0.81 1 0.08 … 0.21 0.46

Asset 3 0.90 0.08 1 … 0.73 0.01

… … … … … … …

Asset N-1 0.21 0.21 0.73 … 1 0.43

Asset N 0.13 0.46 0.01 … 0.43 1

Define interval (e.g. daily) and period (e.g. month)

N x (N-1)/2 pairs of total return correlations

Portfolio weights at start of period wi

𝑐 = 𝑤𝑖𝑤𝑗𝜌𝑖,𝑗𝑖 ≠𝑗

(1 − 𝑤𝑖2)

• Non-trivial to calculate, high degree of estimation error and a highly volatile time-series (S&P 500 has

124,750 pairs)

• Gives an indication of the degree of co-movement between securities in a portfolio, or the market

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No

v 1

98

9

No

v 1

99

0

No

v 1

99

1

No

v 1

99

2

No

v 1

99

3

No

v 1

99

4

No

v 1

99

5

No

v 1

99

6

No

v 1

99

7

No

v 1

99

8

No

v 1

99

9

No

v 2

00

0

No

v 2

00

1

No

v 2

00

2

No

v 2

00

3

No

v 2

00

4

No

v 2

00

5

No

v 2

00

6

No

v 2

00

7

No

v 2

00

8

No

v 2

00

9

No

v 2

01

0

No

v 2

01

1

No

v 2

01

2

No

v 2

01

3

No

v 2

01

4

S&P 500 Average Pairwise Correlation (Month)

12M Trailing Average

CORRELATION IN U.S. LARGE CAPS

4

S&P 500 monthly correlation and 12m trailing average, Nov 1989– August 2015

0.68 - August 2015

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

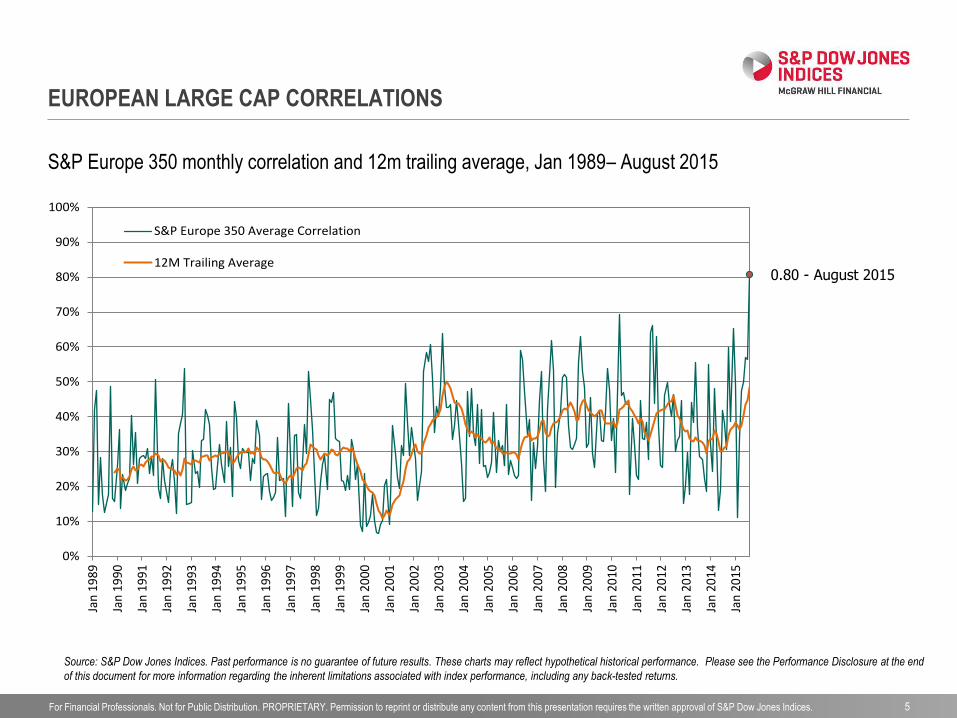

EUROPEAN LARGE CAP CORRELATIONS

5

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Jan

1989

Jan

1990

Jan

1991

Jan

1992

Jan

1993

Jan

1994

Jan

1995

Jan

1996

Jan

1997

Jan

1998

Jan

1999

Jan

2000

Jan

2001

Jan

2002

Jan

2003

Jan

2004

Jan

2005

Jan

2006

Jan

2007

Jan

2008

Jan

2009

Jan

2010

Jan

2011

Jan

2012

Jan

2013

Jan

2014

Jan

2015

S&P Europe 350 Average Correlation

12M Trailing Average0.80 - August 2015

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results. These charts may reflect hypothetical historical performance. Please see the Performance Disclosure at the end

of this document for more information regarding the inherent limitations associated with index performance, including any back-tested returns.

S&P Europe 350 monthly correlation and 12m trailing average, Jan 1989– August 2015

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

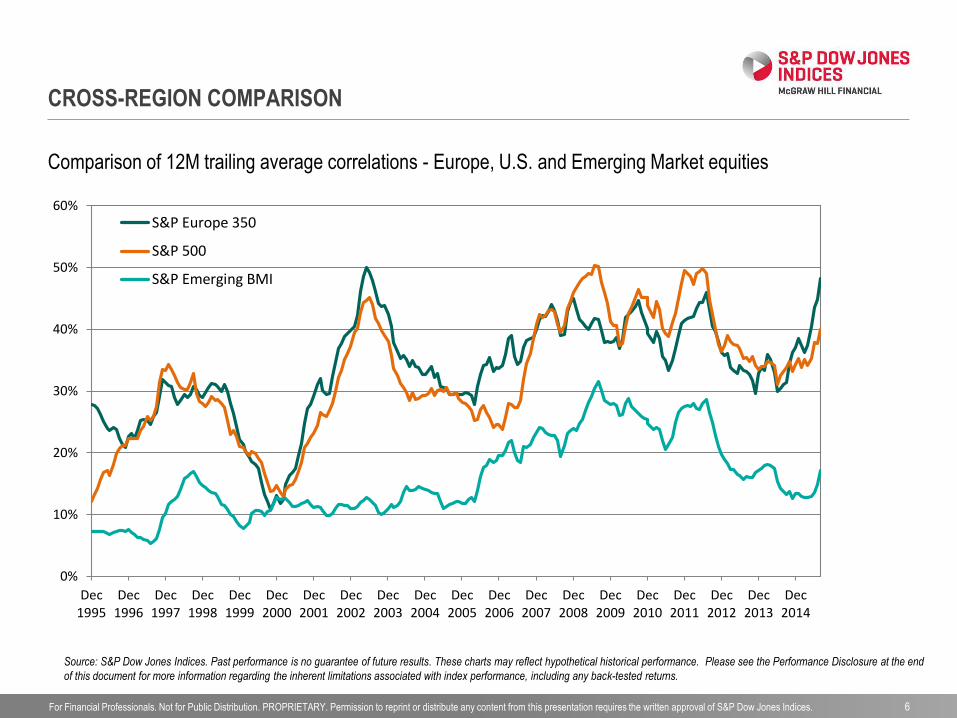

CROSS-REGION COMPARISON

6

Comparison of 12M trailing average correlations - Europe, U.S. and Emerging Market equities

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results. These charts may reflect hypothetical historical performance. Please see the Performance Disclosure at the end

of this document for more information regarding the inherent limitations associated with index performance, including any back-tested returns.

0%

10%

20%

30%

40%

50%

60%

Dec1995

Dec1996

Dec1997

Dec1998

Dec1999

Dec2000

Dec2001

Dec2002

Dec2003

Dec2004

Dec2005

Dec2006

Dec2007

Dec2008

Dec2009

Dec2010

Dec2011

Dec2012

Dec2013

Dec2014

S&P Europe 350

S&P 500

S&P Emerging BMI

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

CORRELATION AND VOLATILITY

7

S&P 500 Monthly correlation and volatility comparison: Oct 1989 – Aug 2015

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Oct

-89

Sep

-90

Aug

-91

Jul-9

2

Jun-

93

May

-94

Apr

-95

Mar

-96

Feb

-97

Jan-

98

Dec

-98

Nov

-99

Oct

-00

Sep

-01

Aug

-02

Jul-0

3

Jun-

04

May

-05

Apr

-06

Mar

-07

Feb

-08

Jan-

09

Dec

-09

Nov

-10

Oct

-11

Sep

-12

Aug

-13

Jul-1

4

Jun-

15

S&P 500 Correlation

S&P 500 R Volatility (Ann.)

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

CORRELATION AND VOLATILITY – HISTORICAL

8

Levels and changes in realized S&P 500 volatility and correlations, Oct 1989 – Aug 2015

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0% 20% 40% 60% 80% 100%

Vo

lati

lity

Lev

el

Correlation Level

Levels

-100%

-50%

0%

50%

100%

150%

200%

250%

300%

-100% 0% 100% 200% 300%

% C

han

ge

In V

ola

tilit

y (M

on

th)

% Change in Correlation (Month)

Changes

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

CORRELATION’S RELATIONSHIP TO VOL (PLAN OF ATTACK)

9

• Interpret / derive correlation in terms of market and individual risk

• Introduce dispersion, as missing piece of the puzzle

• Equations and their real-world accuracy (example)

• Consequences

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

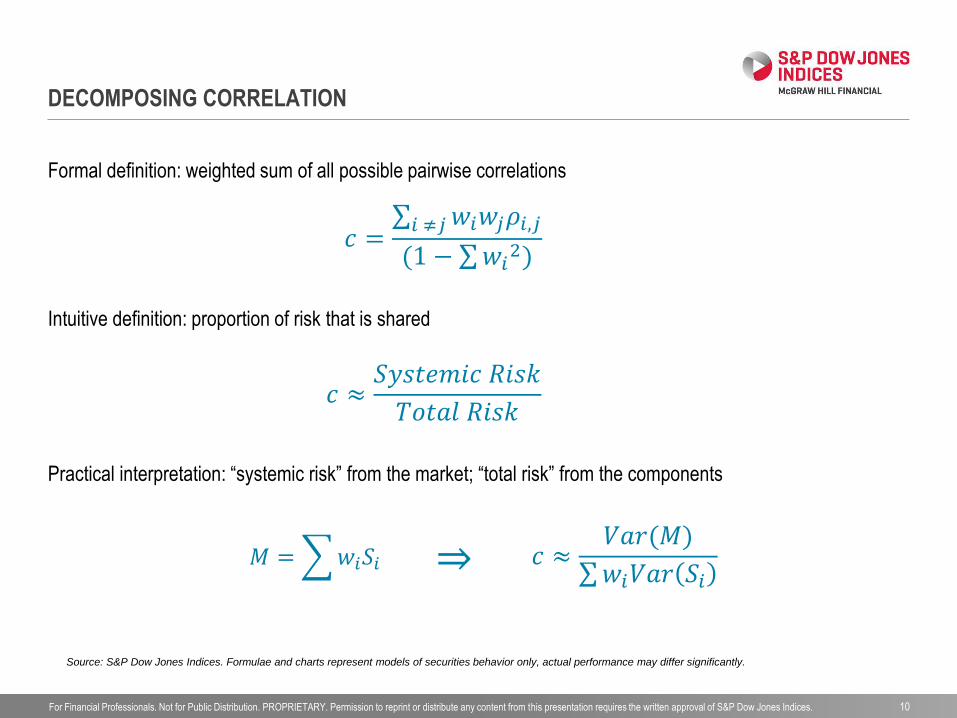

DECOMPOSING CORRELATION

10

Formal definition: weighted sum of all possible pairwise correlations

𝑐 = 𝑤𝑖𝑤𝑗𝜌𝑖,𝑗𝑖 ≠𝑗

(1 − 𝑤𝑖2)

Intuitive definition: proportion of risk that is shared

𝑐 ≈𝑆𝑦𝑠𝑡𝑒𝑚𝑖𝑐 𝑅𝑖𝑠𝑘

𝑇𝑜𝑡𝑎𝑙 𝑅𝑖𝑠𝑘

Practical interpretation: “systemic risk” from the market; “total risk” from the components

𝑐 ≈𝑉𝑎𝑟(𝑀)

𝑤𝑖𝑉𝑎𝑟 𝑆𝑖 𝑀 = 𝑤𝑖𝑆𝑖

Source: S&P Dow Jones Indices. Formulae and charts represent models of securities behavior only, actual performance may differ significantly.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

DECOMPOSING COMPONENT VARIANCE AS MARKET + ?

11

Standard decomposition of stocks as market + error

𝑆𝑖,𝑡 = 𝑀𝑡 + 𝜖𝑖,𝑡

𝑤𝑖𝑉𝑎𝑟 𝑆𝑖 = 𝑉𝑎𝑟 𝑀𝑡 + 𝑤𝑖𝑉𝑎𝑟 𝜖𝑖,𝑡 + (𝐶𝑜𝑣𝑎𝑟𝑖𝑎𝑛𝑐𝑒 𝑡𝑒𝑟𝑚𝑠)

Some basic algebra1 shows that the covariance terms cancel out to leave:

𝑤𝑖𝑉𝑎𝑟 𝑆𝑖 = 𝑉𝑎𝑟 𝑀𝑡 + 𝑤𝑖𝑉𝑎𝑟 𝜖𝑖,𝑡

… but is there an obvious (familiar) way to interpret the final term?

1) See e.g. S&P Dow Jones Indices – “At the Intersection of Diversification, Volatility and Correlation”, April 2014. Formulae and charts represent models of securities behavior only, actual

performance may differ significantly.

Leads to decomposition of variance:

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices. 12

KEY CONCEPT: DISPERSION OR SINGLE-PERIOD CROSS-VARIATION

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

130%

29

-No

v-1

3

03

-De

c-1

3

07

-De

c-1

3

11

-De

c-1

3

15

-De

c-1

3

19

-De

c-1

3

23

-De

c-1

3

27

-De

c-1

3

31

-De

c-1

3

December 2013

80%

85%

90%

95%

100%

105%

110%

115%

120%

125%

130%

28

-Se

p-

01

02

-Oct

-01

06

-Oct

-01

10

-Oct

-01

14

-Oct

-01

18

-Oct

-01

22

-Oct

-01

26

-Oct

-01

30

-Oct

-01

Pri

ce R

etu

rn

October 2001

-21% -15% -9% -3% 3% 9% 15% 21%

V

XOM

AXP

MMM

KO

HD

UNH

TRV

VZ

JNJ

-21% -15% -9% -3% 3% 9% 15% 21%

INTC

C

HPQ

AA

JPM

PG

XOM

CAT

MTLQQ

MRK

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

0% 6% 12% 18% 24% 30% 36% 42%

INTC

MSFT

HD

HPQ

JNJ

EK

JPM

KO

AXP

XOM

IBM

HON

MTLQQ

MCD

T

Difference from Index (%)

-21% -15% -9% -3% 3% 9% 15% 21%

INTC

MSFT

HD

HPQ

JNJ

EK

JPM

KO

AXP

XOM

IBM

HON

MTLQQ

MCD

T

Change (%)

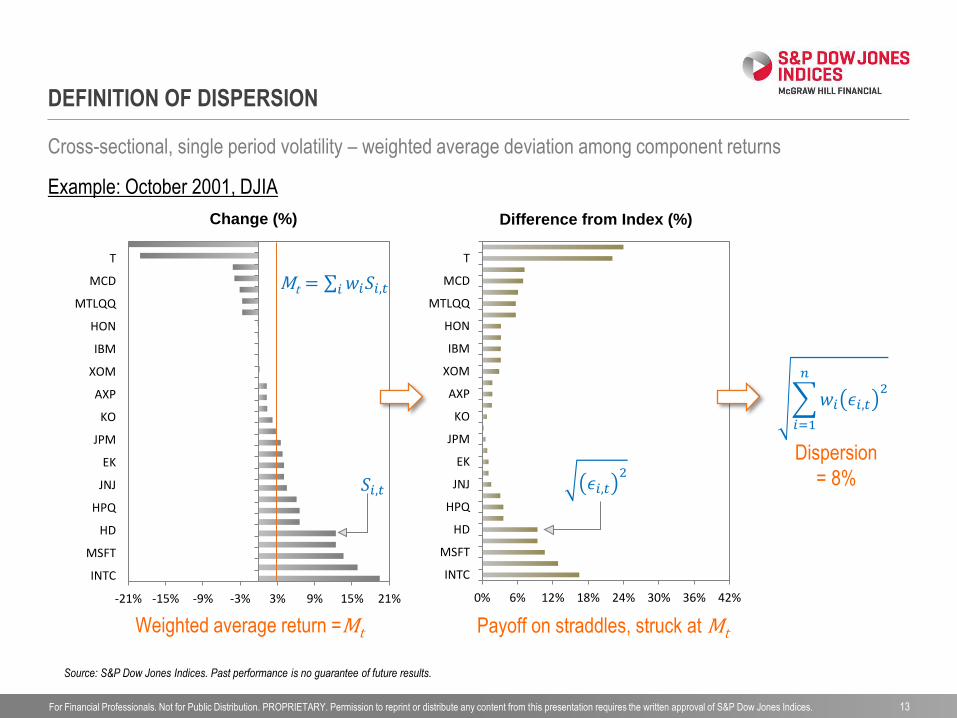

DEFINITION OF DISPERSION

13

Cross-sectional, single period volatility – weighted average deviation among component returns

Mt = 𝑤𝑖𝑆𝑖,𝑡𝑖

Weighted average return =Mt Payoff on straddles, struck at Mt

𝜖𝑖,𝑡2 𝑆𝑖,𝑡

𝑤𝑖 𝜖𝑖,𝑡2

𝑛

𝑖=1

Dispersion

= 8%

Source: S&P Dow Jones Indices. Past performance is no guarantee of future results.

Example: October 2001, DJIA

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

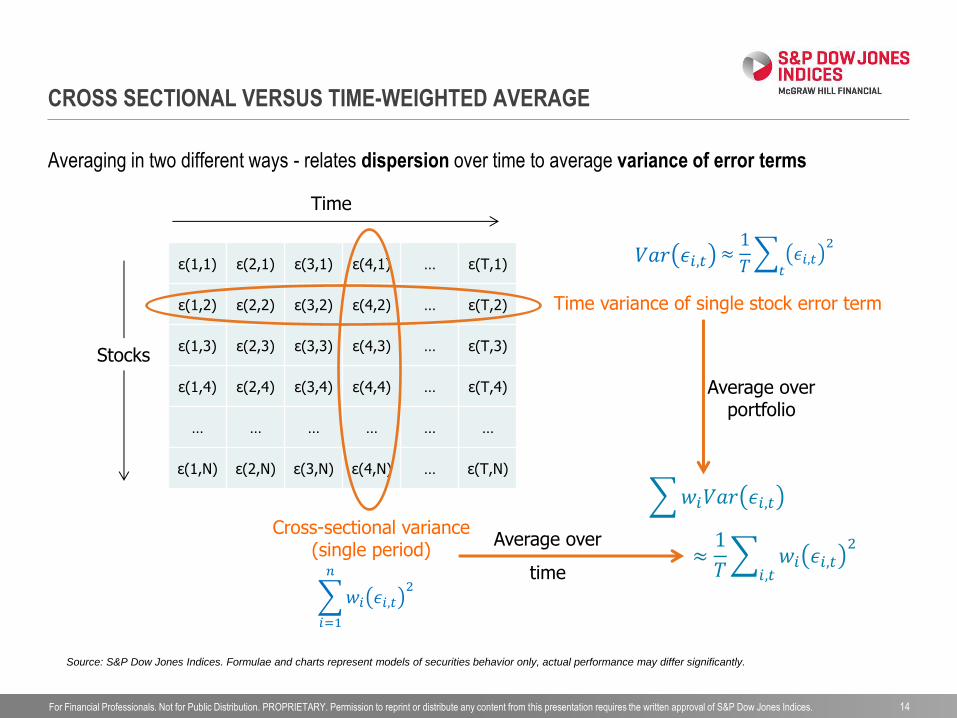

CROSS SECTIONAL VERSUS TIME-WEIGHTED AVERAGE

14

ɛ(1,1) ɛ(2,1) ɛ(3,1) ɛ(4,1) … ɛ(T,1)

ɛ(1,2) ɛ(2,2) ɛ(3,2) ɛ(4,2) … ɛ(T,2)

ɛ(1,3) ɛ(2,3) ɛ(3,3) ɛ(4,3) … ɛ(T,3)

ɛ(1,4) ɛ(2,4) ɛ(3,4) ɛ(4,4) … ɛ(T,4)

… … … … … …

ɛ(1,N) ɛ(2,N) ɛ(3,N) ɛ(4,N) … ɛ(T,N)

Average over

time

Stocks

Cross-sectional variance (single period)

Time variance of single stock error term

Averaging in two different ways - relates dispersion over time to average variance of error terms

𝑤𝑖𝑉𝑎𝑟 𝜖𝑖,𝑡

≈1

𝑇 𝜖𝑖,𝑡

2

𝑡

Average over portfolio

𝑤𝑖 𝜖𝑖,𝑡2

𝑛

𝑖=1

Time

Source: S&P Dow Jones Indices. Formulae and charts represent models of securities behavior only, actual performance may differ significantly.

≈1

𝑇 𝑤𝑖 𝜖𝑖,𝑡

2

𝑖,𝑡

𝑉𝑎𝑟 𝜖𝑖,𝑡

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

… BACK TO CORRELATION

15

Bringing it all together, the portfolio-weighted average pairwise correlation is approximated by

𝑐 ≈ 𝑣2

𝑣2+𝑑2

which also implies:

(1 − 𝑐) ≈ 𝑑2

𝑣2+𝑑2

where

• c is average pairwise correlation

• v is market volatility

• d is (root-mean-square) average dispersion

… this gives a powerful perspective of the interaction of correlation, volatility and dispersion

Source: S&P Dow Jones Indices. Formulae and charts represent models of securities behavior only, actual performance may differ significantly.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

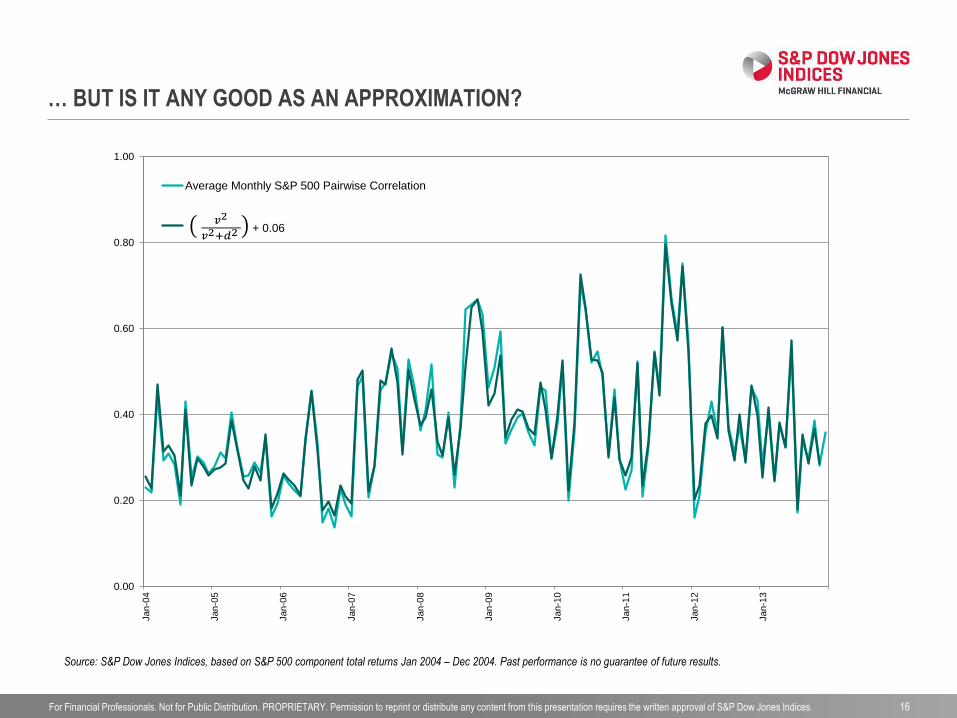

… BUT IS IT ANY GOOD AS AN APPROXIMATION?

16

0.00

0.20

0.40

0.60

0.80

1.00Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Average Monthly S&P 500 Pairwise Correlation

+ 0.06

Source: S&P Dow Jones Indices, based on S&P 500 component total returns Jan 2004 – Dec 2004. Past performance is no guarantee of future results.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Val

ue

of

Co

rrel

atio

n M

ult

iplie

r

Correlation

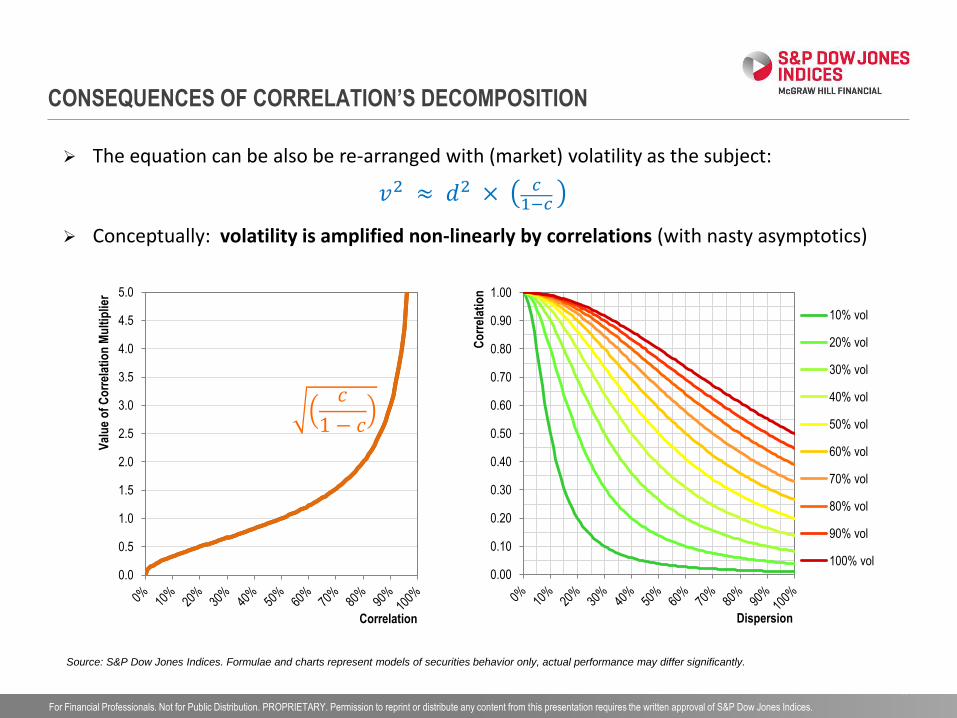

CONSEQUENCES OF CORRELATION’S DECOMPOSITION

17

The equation can be also be re-arranged with (market) volatility as the subject:

𝑣2 ≈ 𝑑2 × 𝑐1−𝑐

Conceptually: volatility is amplified non-linearly by correlations (with nasty asymptotics)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Co

rrel

atio

n

Dispersion

10% vol

20% vol

30% vol

40% vol

50% vol

60% vol

70% vol

80% vol

90% vol

100% vol

𝑐

1 − 𝑐

Source: S&P Dow Jones Indices. Formulae and charts represent models of securities behavior only, actual performance may differ significantly.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

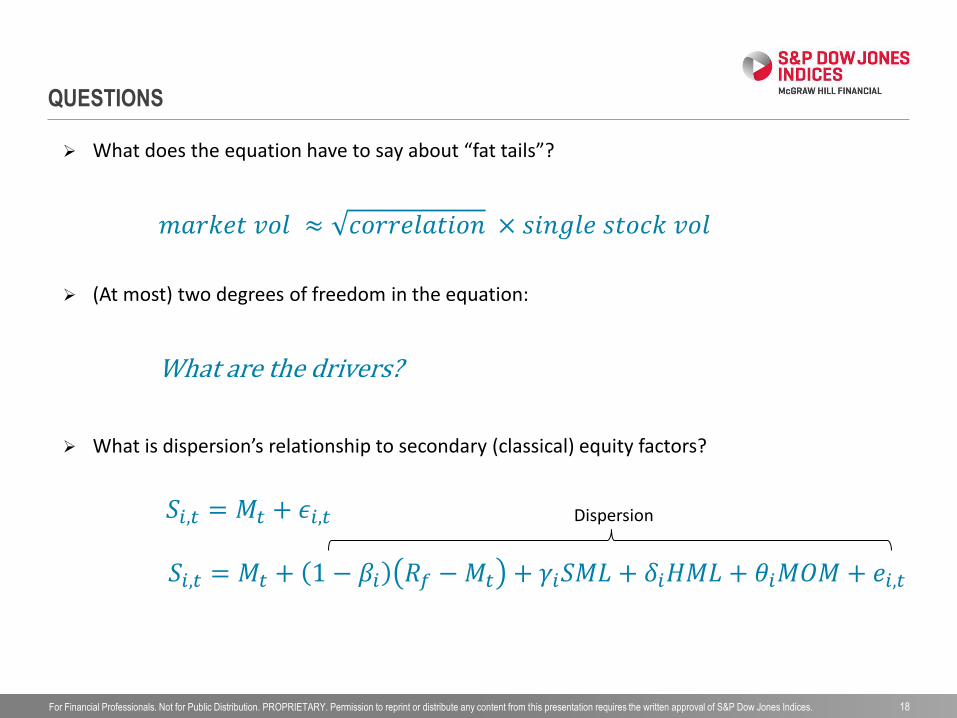

QUESTIONS

18

What does the equation have to say about “fat tails”?

𝑚𝑎𝑟𝑘𝑒𝑡 𝑣𝑜𝑙 ≈ 𝑐𝑜𝑟𝑟𝑒𝑙𝑎𝑡𝑖𝑜𝑛 × 𝑠𝑖𝑛𝑔𝑙𝑒 𝑠𝑡𝑜𝑐𝑘 𝑣𝑜𝑙

(At most) two degrees of freedom in the equation:

What are the drivers?

What is dispersion’s relationship to secondary (classical) equity factors?

𝑆𝑖,𝑡 = 𝑀𝑡 + 𝜖𝑖,𝑡

𝑆𝑖,𝑡 = 𝑀𝑡 + 1 − 𝛽𝑖 𝑅𝑓 −𝑀𝑡 + 𝛾𝑖𝑆𝑀𝐿 + 𝛿𝑖𝐻𝑀𝐿 + 𝜃𝑖𝑀𝑂𝑀 + 𝑒𝑖,𝑡

Dispersion

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

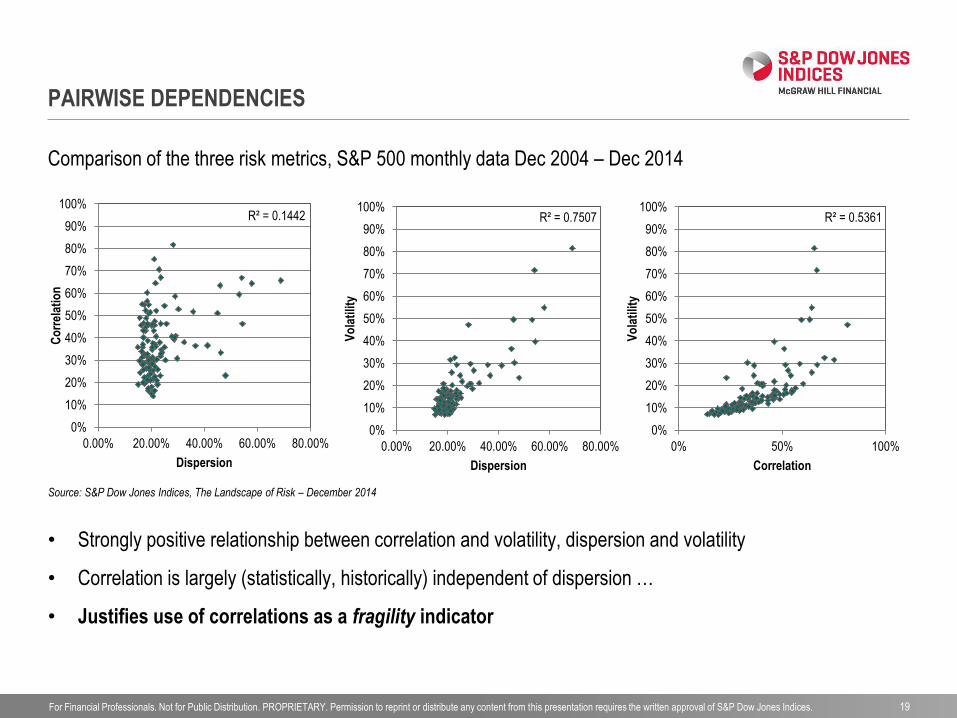

PAIRWISE DEPENDENCIES

19

Source: S&P Dow Jones Indices, The Landscape of Risk – December 2014

R² = 0.1442

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.00% 20.00% 40.00% 60.00% 80.00%

Co

rrel

atio

n

Dispersion

R² = 0.5361

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0% 50% 100%

Vo

lati

lity

Correlation

R² = 0.7507

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0.00% 20.00% 40.00% 60.00% 80.00%

Vo

lati

lity

Dispersion

Comparison of the three risk metrics, S&P 500 monthly data Dec 2004 – Dec 2014

• Strongly positive relationship between correlation and volatility, dispersion and volatility

• Correlation is largely (statistically, historically) independent of dispersion …

• Justifies use of correlations as a fragility indicator

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

DISPERSION AND CLASSICAL FACTORS

20

• Expect dispersion to relate (fairly simply) to rewards from stock-picking skill

• Intuitive relationship with momentum (esp. relative)

• Derived relationship with returns rebalancing (esp. equal weight portfolios)

• Contraction of dispersion in valuations is one cause of value-stock outperformance

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

ASIDE: U.S. EQUITY MANAGERS & DISPERSION

Source: S&P Dow Jones Indices’ SPIVA scorecards (“S&P Index Versus Active”). Data for 2007 are to March end; all other years are full calendar years. Charts are provided for

illustrative purposes. Past performance is no guarantee of future results.

Annual Interquartile Range of U.S. Large-Cap Active Funds vs. S&P 500 Average Monthly Dispersion

“Good” managers performed better in relative terms when dispersion was high

0%

2%

4%

6%

8%

10%

12%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Per

cen

t

Performance Spread: top quartile to bottom quartile funds S&P 500 average monthly dispersion

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

DISPERSION AND REBALANCING/MOMENTUM

22

Illustrative purposes only. Source: S&P Dow Jones Indices.

• “Reversion to the mean” should accompany a tightening of dispersion among stock

performances, while widening performance differentials could accompany momentum effects

• Appropriate time horizons defined by rebalance frequency:

3 months: “short term” dispersion (rebalancing frequency of EQW)

6 - 9 months: Period of rebalancing effect

“Long term” dispersion

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

MOMENTUM & REBALANCING

23

• Equal Weight and Momentum have directly opposing outperformance

12M Outperformance (TR) Outperformance Accumulation

Source: S&P Dow Jones Indices as of March 2015. All index performances are total return in EUR, outperformance shown with respect to the S&P Europe 350 total return index. Past

performance is no guarantee of future results. These charts may reflect hypothetical historical performance. Please see the Performance Disclosure at the end of this document for

more information regarding the inherent limitations associated with index performance, including any back-tested returns.

-10%

0%

10%

20%

30%

40%

50%

Sep 2

001

Sep 2

002

Sep 2

003

Sep 2

004

Sep 2

005

Sep 2

006

Sep 2

007

Sep 2

008

Sep 2

009

Sep 2

010

Sep 2

011

Sep 2

012

Sep 2

013

Sep 2

014

S&P Europe 350 Equal Weight

S&P Europe 350 Momentum

R² = 0.3634

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

-10% 0% 10% 20%S

&P

Eur

ope

350

Mom

entu

m 1

2M

Out

perf

orm

ance

S&P Europe 350 Equal Weight 12M Outperformance

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

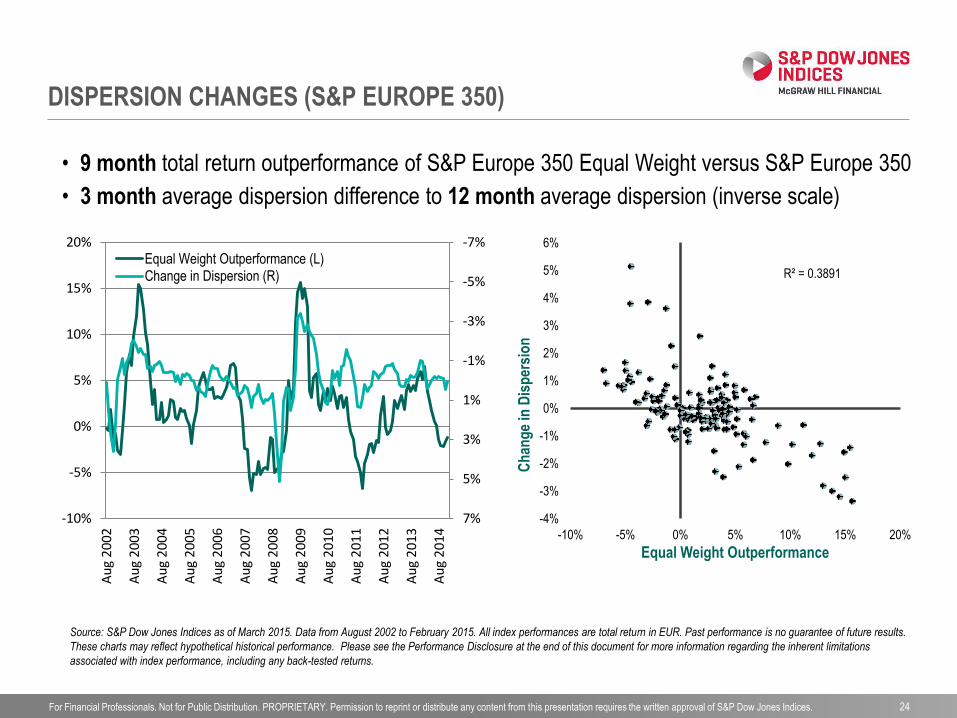

DISPERSION CHANGES (S&P EUROPE 350)

24

• 9 month total return outperformance of S&P Europe 350 Equal Weight versus S&P Europe 350

• 3 month average dispersion difference to 12 month average dispersion (inverse scale)

Source: S&P Dow Jones Indices as of March 2015. Data from August 2002 to February 2015. All index performances are total return in EUR. Past performance is no guarantee of future results.

These charts may reflect hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations

associated with index performance, including any back-tested returns.

-7%

-5%

-3%

-1%

1%

3%

5%

7%-10%

-5%

0%

5%

10%

15%

20%

Au

g 2

002

Au

g 2

003

Au

g 2

004

Au

g 2

005

Au

g 2

006

Au

g 2

007

Au

g 2

008

Au

g 2

009

Au

g 2

010

Au

g 2

011

Au

g 2

012

Au

g 2

013

Au

g 2

014

Equal Weight Outperformance (L)Change in Dispersion (R) R² = 0.3891

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

-10% -5% 0% 5% 10% 15% 20%C

han

ge

in D

isp

ersi

on

Equal Weight Outperformance

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

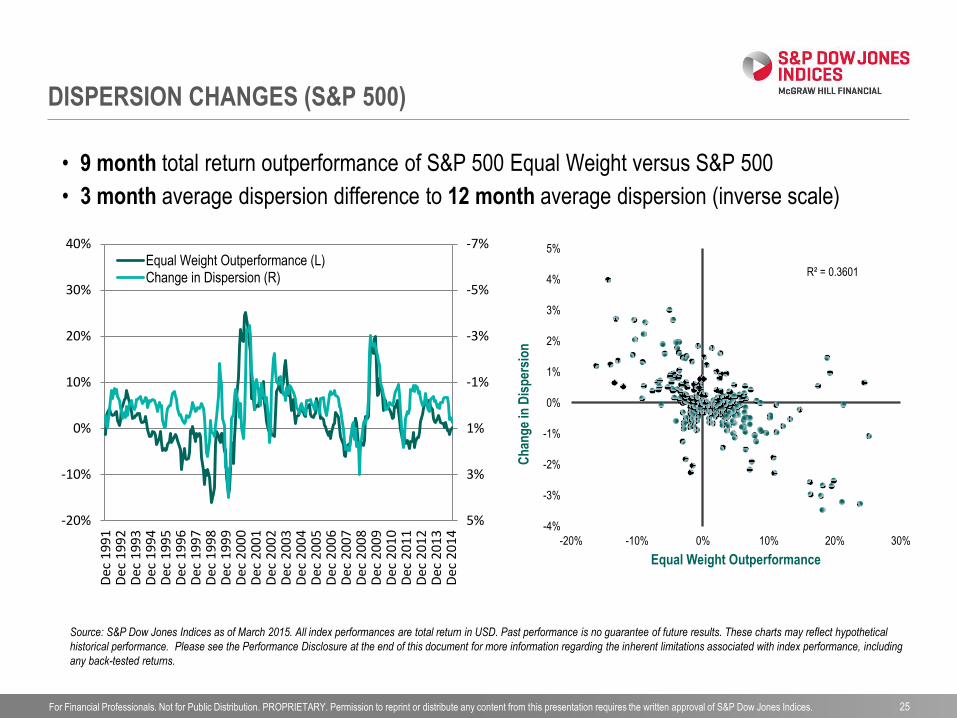

DISPERSION CHANGES (S&P 500)

25

• 9 month total return outperformance of S&P 500 Equal Weight versus S&P 500

• 3 month average dispersion difference to 12 month average dispersion (inverse scale)

-7%

-5%

-3%

-1%

1%

3%

5%-20%

-10%

0%

10%

20%

30%

40%

Dec

199

1D

ec 1

992

Dec

199

3D

ec 1

994

Dec

199

5D

ec 1

996

Dec

199

7D

ec 1

998

Dec

199

9D

ec 2

000

Dec

200

1D

ec 2

002

Dec

200

3D

ec 2

004

Dec

200

5D

ec 2

006

Dec

200

7D

ec 2

008

Dec

200

9D

ec 2

010

Dec

201

1D

ec 2

012

Dec

201

3D

ec 2

014

Equal Weight Outperformance (L)Change in Dispersion (R) R² = 0.3601

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

-20% -10% 0% 10% 20% 30%

Ch

ang

e in

Dis

per

sio

n

Equal Weight Outperformance

Source: S&P Dow Jones Indices as of March 2015. All index performances are total return in USD. Past performance is no guarantee of future results. These charts may reflect hypothetical

historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with index performance, including

any back-tested returns.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

DISPERSION AND VALUE

26

• Intuition: dispersion in valuations (e.g. P/E ratios) is related to dispersion in prices

• Suggests: increasing dispersion favours growth, while decreasing dispersion favours value

• S&P’s original value/growth series weights by market cap: mitigating size and rebalance effects

0%

100%

200%

300%

400%

500%

600%

700%

800%

Mar

1994

Mar

1995

Mar

1996

Mar

1997

Mar

1998

Mar

1999

Mar

2000

Mar

2001

Mar

2002

Mar

2003

Mar

2004

Mar

2005

Mar

2006

Mar

2007

Mar

2008

Mar

2009

Mar

2010

Mar

2011

Mar

2012

Mar

2013

Mar

2014

Mar

2015

S&P 500 Value

S&P 500 Growth

S&P 500

Source: S&P Dow Jones Indices as of March 2015. All index performances are total return in USD. Past performance is no guarantee of future results.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

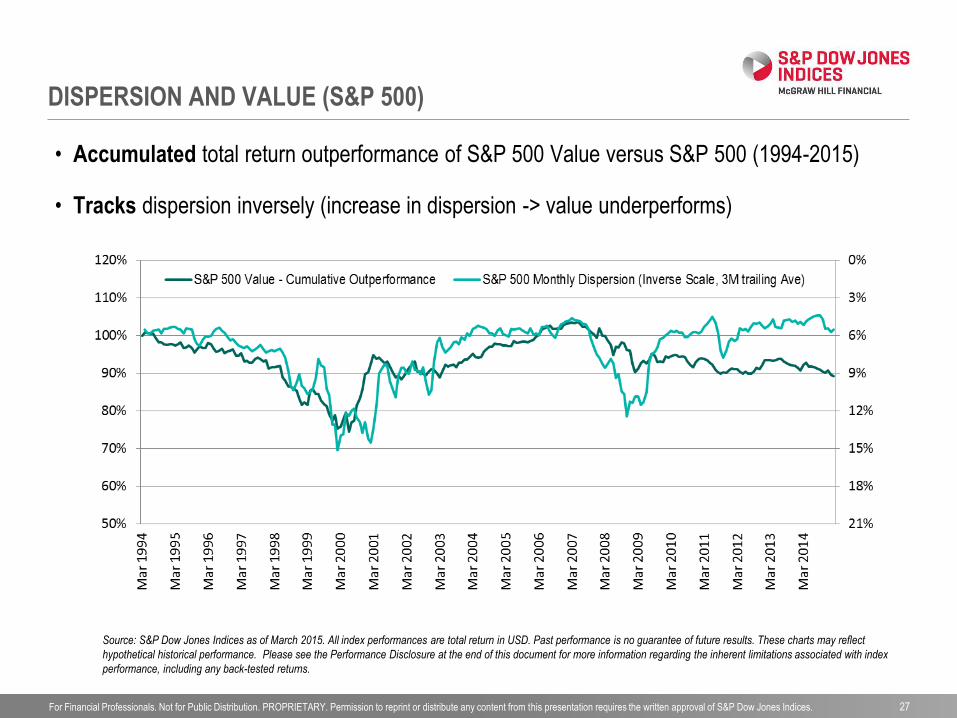

DISPERSION AND VALUE (S&P 500)

27

• Accumulated total return outperformance of S&P 500 Value versus S&P 500 (1994-2015)

• Tracks dispersion inversely (increase in dispersion -> value underperforms)

Source: S&P Dow Jones Indices as of March 2015. All index performances are total return in USD. Past performance is no guarantee of future results. These charts may reflect

hypothetical historical performance. Please see the Performance Disclosure at the end of this document for more information regarding the inherent limitations associated with index

performance, including any back-tested returns.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

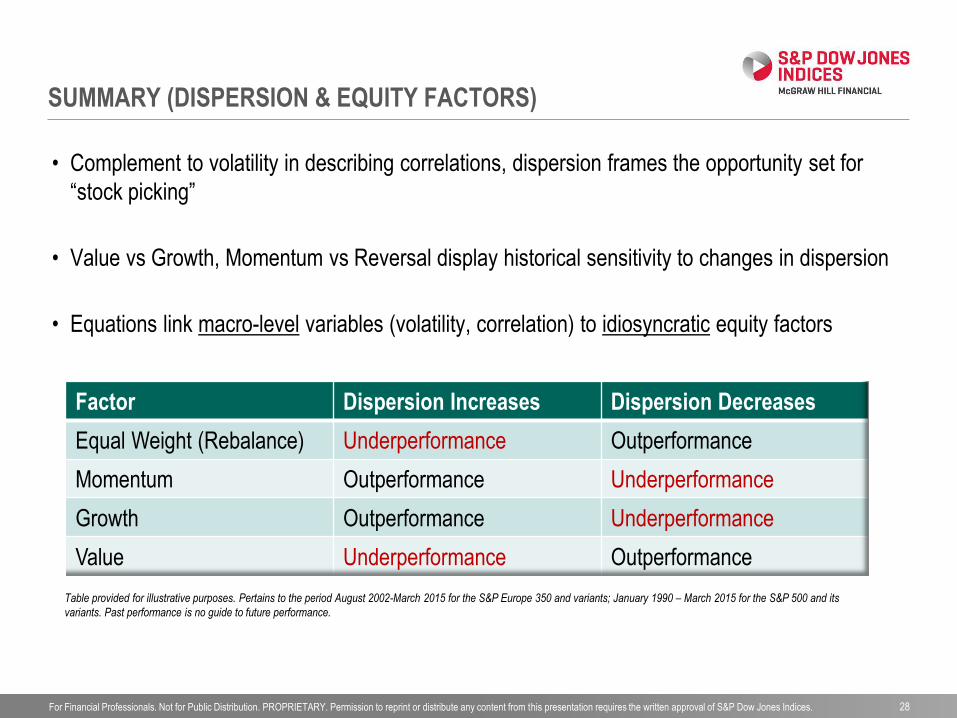

SUMMARY (DISPERSION & EQUITY FACTORS)

28

Factor Dispersion Increases Dispersion Decreases

Equal Weight (Rebalance) Underperformance Outperformance

Momentum Outperformance Underperformance

Growth Outperformance Underperformance

Value Underperformance Outperformance

Table provided for illustrative purposes. Pertains to the period August 2002-March 2015 for the S&P Europe 350 and variants; January 1990 – March 2015 for the S&P 500 and its

variants. Past performance is no guide to future performance.

• Complement to volatility in describing correlations, dispersion frames the opportunity set for

“stock picking”

• Value vs Growth, Momentum vs Reversal display historical sensitivity to changes in dispersion

• Equations link macro-level variables (volatility, correlation) to idiosyncratic equity factors

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

TRADING DISPERSION (BRIEF INTRO)

29

• Via single stock vs index options & variance

d2 ≈ Ave Single Stock var – Index var (mkt-weighted)

• Nothing special about the “market” weighting used to derive the correlation equations,

tradeable as long as options exist on the basket & components:

Stocks vs Index Size vs Broad Global Sectors

Stocks vs Sector U.S. vs Global Other Assets

Sectors vs Index Spread trades Currencies

• Benchmark similar to VIX®, providing market-implied dispersion, is feasible, if not

simple.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

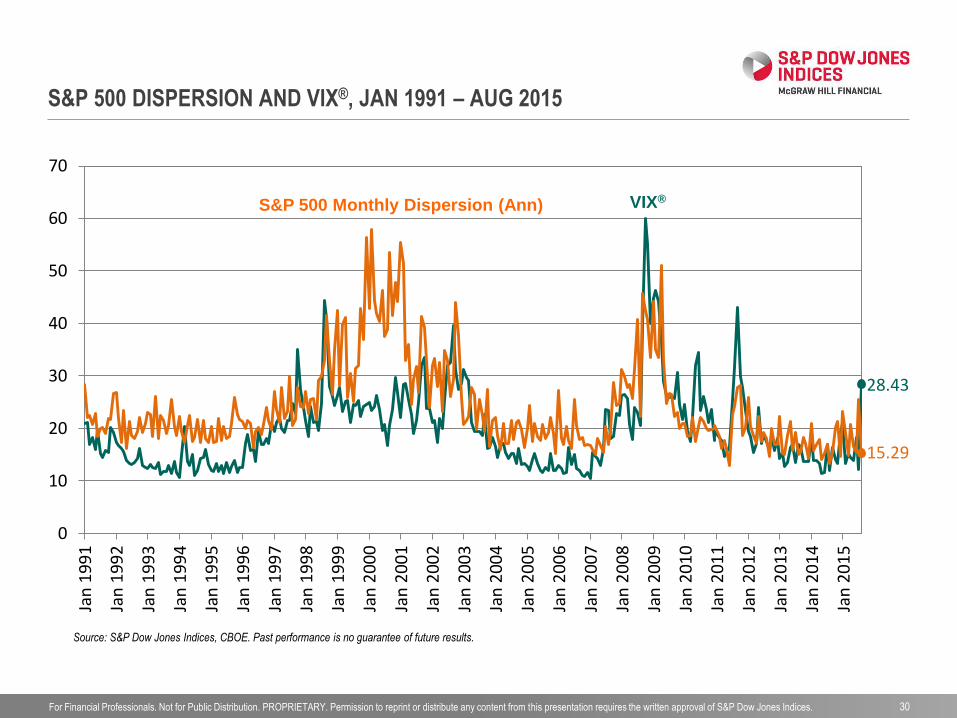

28.43

15.29

0

10

20

30

40

50

60

70

Jan

19

91

Jan

19

92

Jan

19

93

Jan

19

94

Jan

19

95

Jan

19

96

Jan

19

97

Jan

19

98

Jan

19

99

Jan

20

00

Jan

20

01

Jan

20

02

Jan

20

03

Jan

20

04

Jan

20

05

Jan

20

06

Jan

20

07

Jan

20

08

Jan

20

09

Jan

20

10

Jan

20

11

Jan

20

12

Jan

20

13

Jan

20

14

Jan

20

15

30

S&P 500 Monthly Dispersion (Ann) VIX®

S&P 500 DISPERSION AND VIX®, JAN 1991 – AUG 2015

Source: S&P Dow Jones Indices, CBOE. Past performance is no guarantee of future results.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

PERFORMANCE DISCLOSURE

31

The S&P 500 Equal Weight Index was launched on Jan. 9, 2003. S&P Europe 350 Momentum Index was launched on Nov 18, 2014. The S&P Europe 350 Index was launched on

Oct 7, 1998. The S&P Europe 350 Equal Weight Index was launched on Jan. 21, 2014. The S&P Emerging BMI was launched on Dec 31, 1997. All information on each index

presented prior to the launch date is back-tested. Back-tested performance is not actual performance, but is hypothetical. The back-test calculations are based on the same

methodology that was in effect when each index was officially launched. Complete index methodology details are available at www.spdji.com. It is not possible to invest directly in

an index.

S&P Dow Jones Indices defines various dates to assist our clients in providing transparency on their products. The First Value Date is the first day for which there is a calculated

value (either live or back-tested) for a given index. The Base Date is the date at which the Index is set at a fixed value for calculation purposes. The Launch Date designates the

date upon which the values of an index are first considered live: index values provided for any date or time period prior to the index’s Launch Date are considered back-tested. S&P

Dow Jones Indices defines the Launch Date as the date by which the values of an index are known to have been released to the public, for example via the company’s public

website or its datafeed to external parties. For Dow Jones-branded indicates introduced prior to May 31, 2013, the Launch Date (which prior to May 31, 2013, was termed “Date of

introduction”) is set at a date upon which no further changes were permitted to be made to the index methodology, but that may have been prior to the Index’s public release date.

Past performance of the Index is not an indication of future results. Prospective application of the methodology used to construct the Index may not result in performance

commensurate with the back-test returns shown. The back-test period does not necessarily correspond to the entire available history of the Index. Please refer to the methodology

paper for the Index, available at www.spdji.com for more details about the index, including the manner in which it is rebalanced, the timing of such rebalancing, criteria for additions

and deletions, as well as all index calculations.

Another limitation of using back-tested information is that the back-tested calculation is generally prepared with the benefit of hindsight. Back-tested information reflects the

application of the index methodology and selection of index constituents in hindsight. No hypothetical record can completely account for the impact of financial risk in actual trading.

For example, there are numerous factors related to the equities, fixed income, or commodities markets in general which cannot be, and have not been accounted for in the

preparation of the index information set forth, all of which can affect actual performance.

The Index returns shown do not represent the results of actual trading of investable assets/securities. S&P Dow Jones Indices LLC maintains the Index and calculates the Index

levels and performance shown or discussed, but does not manage actual assets. Index returns do not reflect payment of any sales charges or fees an investor may pay to

purchase the securities underlying the Index or investment funds that are intended to track the performance of the Index. The imposition of these fees and charges would cause

actual and back-tested performance of the securities/fund to be lower than the Index performance shown. As a simple example, if an index returned 10% on a US $100,000

investment for a 12-month period (or US $10,000) and an actual asset-based fee of 1.5% was imposed at the end of the period on the investment plus accrued interest (or US

$1,650), the net return would be 8.35% (or US $8,350) for the year. Over a three year period, an annual 1.5% fee taken at year end with an assumed 10% return per year would

result in a cumulative gross return of 33.10%, a total fee of US $5,375, and a cumulative net return of 27.2% (or US $27,200).

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices.

GENERAL DISCLAIMER

32

Copyright © 2015 by S&P Dow Jones Indices LLC, a part of McGraw Hill Financial. All rights reserved. S&P, S&P 500, S&P MidCap 400, S&P SmallCap 600, S&P GSCI, S&P Europe 350, S&P

Composite1500 and STANDARD & POOR’S are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a subsidiary of McGraw Hill Financial, Inc. Dow Jones is a registered

trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Trademarks have been licensed to S&P Dow Jones Indices LLC. Redistribution, reproduction and/or photocopying in whole or in

part are prohibited without written permission. This document does not constitute an offer of services in jurisdictions where S&P Dow Jones Indices LLC, Dow Jones, S&P or their respective affiliates

(collectively “S&P Dow Jones Indices”) do not have the necessary licenses. All information provided by S&P Dow Jones Indices is impersonal and not tailored to the needs of any person, entity or

group of persons. S&P Dow Jones Indices receives compensation in connection with licensing its indices to third parties. Past performance of an index is not a guarantee of future results.

It is not possible to invest directly in an index. Exposure to an asset class represented by an index is available through investable instruments based on that index. S&P Dow Jones Indices does not

sponsor, endorse, sell, promote or manage any investment fund or other investment vehicle that is offered by third parties and that seeks to provide an investment return based on the performance of

any index. S&P Dow Jones Indices makes no assurance that investment products based on the index will accurately track index performance or provide positive investment returns. S&P Dow Jones

Indices LLC is not an investment advisor, and S&P Dow Jones Indices makes no representation regarding the advisability of investing in any such investment fund or other investment vehicle. A

decision to invest in any such investment fund or other investment vehicle should not be made in reliance on any of the statements set forth in this document. Prospective investors are advised to

make an investment in any such fund or other vehicle only after carefully considering the risks associated with investing in such funds, as detailed in an offering memorandum or similar document

that is prepared by or on behalf of the issuer of the investment fund or other vehicle. Inclusion of a security within an index is not a recommendation by S&P Dow Jones Indices to buy, sell, or hold

such security, nor is it considered to be investment advice. Closing prices for S&P US benchmark indices and Dow Jones US benchmark indices are calculated by S&P Dow Jones Indices based on

the closing price of the individual constituents of the index as set by their primary exchange. Closing prices are received by S&P Dow Jones Indices from one of its third party vendors and verified by

comparing them with prices from an alternative vendor. The vendors receive the closing price from the primary exchanges.

These materials have been prepared solely for informational purposes based upon information generally available to the public and from sources believed to be reliable. No content contained in

these materials (including index data, ratings, credit-related analyses and data, research, valuations, model, software or other application or output therefrom) or any part thereof (Content) may be

modified, reverse-engineered, reproduced or distributed in any form or by any means, or stored in a database or retrieval system, without the prior written permission of S&P Dow Jones Indices. The

Content shall not be used for any unlawful or unauthorized purposes. S&P Dow Jones Indices and its third-party data providers and licensors (collectively “S&P Dow Jones Indices Parties”) do not

guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Dow Jones Indices Parties are not responsible for any errors or omissions, regardless of the cause, for the

results obtained from the use of the Content. THE CONTENT IS PROVIDED ON AN “AS IS” BASIS. S&P DOW JONES INDICES PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED

WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE

ERRORS OR DEFECTS, THAT THE CONTENT’S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE

CONFIGURATION. In no event shall S&P Dow Jones Indices Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages,

costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the Content even if advised of the possibility of such

damages.

S&P Dow Jones Indices keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain

business units of S&P Dow Jones Indices may have information that is not available to other business units. S&P Dow Jones Indices has established policies and procedures to maintain the

confidentiality of certain non-public information received in connection with each analytical process.

In addition, S&P Dow Jones Indices provides a wide range of services to, or relating to, many organizations, including issuers of securities, investment advisers, broker-dealers, investment banks,

other financial institutions and financial intermediaries, and accordingly may receive fees or other economic benefits from those organizations, including organizations whose securities or services

they may recommend, rate, include in model portfolios, evaluate or otherwise address.

CBOE, CBOE Volatility Index and VIX are registered trademarks of Chicago Board Options Exchange, Incorporated (CBOE). CBOE has granted S&P Dow Jones Indices a license to use the VIX

methodology to create a variety of volatility indices.

For Financial Professionals. Not for Public Distribution. PROPRIETARY. Permission to reprint or distribute any content from this presentation requires the written approval of S&P Dow Jones Indices. 33

THANK YOU

Tim Edwards