country report kazakhstan august 2017 -...

TRANSCRIPT

_________________________________________________________________________________________________________________________________________________________

Country Report

Kazakhstan

Generated on September 7th 2017

Economist Intelligence Unit20 Cabot SquareLondon E14 4QWUnited Kingdom

_________________________________________________________________________________________________________________________________________________________

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For 60 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.The Economist Intelligence Unit delivers its information in four ways: through its digital portfolio, wherethe latest analysis is updated daily; through printed subscription products ranging from newsletters toannual reference works; through research reports; and by organising seminars and presentations. Thefirm is a member of The Economist Group.

London

The Economist Intelligence Unit20 Cabot SquareLondonE14 4QWUnited KingdomTel: +44 (0) 20 7576 8181Fax: +44 (0) 20 7576 8476E-mail: [email protected]

New York

The Economist Intelligence UnitThe Economist Group750 Third Avenue5th FloorNew York, NY 10017, USTel: +1 212 541 0500Fax: +1 212 586 0248E-mail: [email protected]

Hong Kong

The Economist Intelligence Unit1301 Cityplaza Four12 Taikoo Wan RoadTaikoo ShingHong KongTel: +852 2585 3888Fax: +852 2802 7638E-mail: [email protected]

Geneva

The Economist Intelligence UnitRue de l’Athénée 321206 GenevaSwitzerland

Tel: +41 22 566 24 70Fax: +41 22 346 93 47E-mail: [email protected]

This report can be accessed electronically as soon as it is published by visiting store.eiu.com or bycontacting a local sales representative.

The whole report may be viewed in PDF format, or can be navigated section-by-section by using theHTML links. In addition, the full archive of previous reports can be accessed in HTML or PDF format,and our search engine can be used to find content of interest quickly. Our automatic alerting servicewill send a notification via e-mail when new reports become available.

Copyright

© 2017 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor anypart of it may be reproduced, stored in a retrieval system, or transmitted in any form or by any means,electronic, mechanical, photocopying, recording or otherwise, without the prior permission of TheEconomist Intelligence Unit Limited.

All information in this report is verified to the best of the author's and the publisher's ability. However,the Economist Intelligence Unit does not accept responsibility for any loss arising from reliance on it.

ISSN 2047-5101

Symbols for tables

"0 or 0.0" means nil or negligible;"n/a" means not available; "-" means not applicable

Kazakhstan

ForecastHighlights

Outlook for 2017-21 Political stability

Election watch

International relations

Policy trends

Fiscal policy

Monetary policy

International assumptions

Economic growth

Inflation

Exchange rates

External sector

Forecast summary

Data and charts Annual data and forecast

Quarterly data

Monthly data

Annual trends charts

Monthly trends charts

Comparative economic indicators

Summary Basic data

Political structure

Recent analysisPolitics Forecast updates

Analysis

Economy Forecast updates

Analysis

3

4

4

5

6

6

7

8

9

9

9

10

11

12

12

15

16

17

17

19

21

23

27

Kazakhstan 1

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

HighlightsEditor: Maximilien Lambertson

Forecast Closing Date: August 18, 2017

Outlook for 2017-21

There are signs that succession planning is under way. However,uncertainty about how and when a transition of power away from thepresident, Nursultan Nazarbayev, will take place is the main risk to politicalstability.The Economist Intelligence Unit's baseline forecast is that Mr Nazarbayev,who is 77, will serve out his term to 2020, but risks to this forecast haverisen.The relationship with Russia will remain of primary importance in 2017-21.However, the conflict in Ukraine has made Kazakhstan more cautious aboutfurther economic integration, such as via the Eurasian Economic Union.We forecast that real GDP growth will pick up from 0.9% in 2016 to anaverage of 2.7% in 2017-21. Capital spending on infrastructure will besignificant, driven by the government's stimulus programme and investmentfrom China.The projected slowdown in China's economy in 2018, which could furtherdepress commodity prices, represents a significant downside risk to growth.The government will undertake limited reforms to improve the investmentand regulatory environment. The privatisation programme is unlikely to havea significant impact on productivity or competitiveness.Further state support to the banking sector will be required (and is likely tobe forthcoming). Deficiencies in financial oversight are likely to persist. Therisk of further serious problems emerging in the sector cannot bediscounted.

Review

On July 25th Larisa Kharkova, a prominent trade union leader, was convictedof abuse of office, and on August 3rd Olesya Khalabuzar, a civil societyactivist, was convicted of inciting ethnic enmity.According to Berik Sholpankulov, the deputy minister of finance, thegovernment has sold stakes in 447 of the 569 companies that it has put upfor sale since June 2014.On July 17th the National Bank of Kazakhstan (NBK, the central bank) keptits policy rate at 10.5%, with a ±1percentagepoint interest rate corridor.On August 9th the NBK said that it would issue banks with funding ofTenge600bn-Tenge1trn (US$1.8bn-US$3bn) by purchasing bonds to helpthem to write off distressed assets.In the first half real GDP (gross value added) grew by 4.2% year on year,according to a first estimate by the Statistics Agency of the Republic ofKazakhstan.In July retail trade volumes grew by 9.2% year on year, up from 4.6% in June.In July consumer price inflation stood at 7.1% year on year, down from 7.5%in June 2016 and an average of 14.6% in 2016.

Kazakhstan 2

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Outlook for 2017-21

Political stabilityNursultan Nazarbayev, the president, has been in power since before the collapse ofthe Soviet Union. Nur Otan (Radiant-Fatherland), the party headed by the president,dominates parliament. Economic and political power is shared and contested by elitenetworks based on economic and bureaucratic alliances, overlaid in some cases byhistorical or imagined clan allegiances. Parliament at present provides little check onthe presidential administration and the govern ment, but it does offer limited scopefor revision to legislative initiatives in response to lobbying and public opinion.

Mr Nazarbayev enjoys high levels of public support, and his tenure has seen risingliving standards over the past decade. However, high levels of inequality persist,and weaker economic performance in the coming five years could lead to risingpublic dissatisfaction.

Mr Nazarbayev turned 77 in July, and his eventual departure from the political sceneremains the principal risk to political stability. In June parliament approvedconstitutional reforms proposed by Mr Nazarbayev that grant parlia ment greatersay over government appointments and abolish some presidential powers. Inpractice, the presidency will remain the strongest political institution, and the impactof these amendments will be limited as long as Mr Nazarbayev remains in power.The party system is not competitive, and genuine opposition has been marginalised.

The reforms are nevertheless significant, as they suggest that preparations for apolitical transition are under way. After Mr Nazarbayev's departure theredistribution of powers could enable a more collective system of rule, withparliament exercising greater oversight over government and the legislative process.The next president is likely to be weaker than the incumbent and will not enjoy thesame authority over the political and economic elites. Even under such a scenario,however, political decision-making is likely to remain non-transparent, highlyinformal and authoritarian.

How and when a transition of power will be enacted remains uncertain, and there isno clear successor. Kazakhstan’s superpresidential system has prevented thedevelopment of effective institutions that would have ensured political stability andprovided a clear source of legitimacy for Mr Nazarbayev’s successor. Corruption isendemic, civil society is weak and the media are highly controlled. There is a riskthat Mr Nazarbayev’s exit from office will trigger a destabilising power strugglebetween elite factions, but The Economist Intelligence Unit assumes that all partieshave an interest in ensuring an outwardly consensual transition. Our baselineforecast is that Mr Nazarbayev will continue in office until at least 2020, but the risksto this scenario have grown. The impending transition will be perceived as amoment of potential regime vulnerability, which could weigh on businessconfidence.

Sporadic protests and strikes are possible in provincial areas and single-industrytowns, prompted by corruption, inequality and a lack of economic oppor tunities.The risk of mass popular unrest remains low, but the government appears to vieweven smallscale protests as a potential threat to stability. The govern ment alsostruggles to anticipate public opinion or consult effectively with stakeholders, withthe result that legislative initiatives are often poorly conceived.

Kazakhstan 3

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Election watchFormal political opposition has been marginalised. Since Kazakhstan gainedindependence, none of its elections has been judged free or fair by credibleinternational observers. The legal amendments recently passed by parliamentprohibit presidential candidates from nominating themselves to run in elections.This means that candidates will be nominated by parties that are supportive of theadministration. The next presidential election is scheduled for 2020, but there is asignificant possibility that it will be called early to forestall any potential organisedpolitical opposition—particularly in the event of a further economic shock—or aspart of a succession process.

International relationsKazakhstan has been relatively successful in pursuing a multi vector foreign policy,retaining good relations with the West, China, Russia and the Middle East.Avoiding excessive dependence on any single country or bloc by diversi fy ingtrade and investment links will remain a keystone of foreign policy.

Kazakhstan will be an enthusiastic participant in China's Belt and Road Initiative toboost regional connectivity and infrastructure, but China's growing economicfootprint will remain controversial domestically. Although Russia's cultural,economic and political influence over Kazakshtan is declining gradually, it willcontinue to be Kazakhstan's paramount diplomatic and security partner throughoutthe forecast period (2017-21), and the Kazakh leadership will seek to maintain strongties under almost all circumstances.

The Eurasian Economic Union (EEU), comprising Armenia, Belarus, Kazakh stan,the Kyrgyz Republic and Russia, was officially launched on January 1st 2015, aimedat creating a common market and regulatory regime. In practice, institutionalharmonisation is limited. In the context of weak rule of law, the interaction ofnational and supranational regulatory bodies could further complicate the businessoperating environment and create regulatory uncertainty. Moreover, trade policyhas become less harmonised, owing to Russia’s embargo on Western and Ukrainianproducts. Any successor to Mr Nazarbayev will probably be less instinctivelyintegrationist than the current president. Kazakhstan is highly unlikely to leave theEEU formally, but regulatory harmonisation could, in effect, be allowed to lapse.

There remains a risk that Kazakhstan's succession process will becomeinter nationalised, with Russia seeking to play a prominent role. Kazakhstan has alarge ethnic Russian population, concentrated in areas bordering Russia. Althoughinter-ethnic relations are currently fairly good, Russia could seek to mobilise thisconstituency in the future, particularly if it perceives that the Kazakh leadership isseeking to reorient the country’s foreign policy. However, Kazakhstan has nointerest in deep integration with Western economic or security structures, mitigatingthe risk of geopolitical confrontation.

Kazakhstan 4

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Policy trendsGovernment reshuffles will remain a regular occurrence, but are not generallyshaped by ideological or policy differences. Typically, they are a product of eitherfactional conflicts or attempts to raise institutional effectiveness.

Regular presidential pronouncements and policy papers stress the need to increaseproductivity, diversify the economy away from hydrocarbons, reduce the role of thestate in the economy and increase the effectiveness of the bureaucracy.

We expect incremental improvements in the business environment, although, in theabsence of free media or strong civil society, improvements in the judiciary and inthe effectiveness of the bureaucracy are likely to be limited. The government has seta target of selling stakes in about 800 companies by 2020, totalling more thanUS$7bn. According to Berik Sholpankulov, the deputy minister of finance, thegovernment has sold stakes in 447 of the 569 companies that it has put up for salesince June 2014, raising Tenge125.4bn (US$376m). Although this privatisation pushso far appears to be proceeding faster than previous campaigns, past performancesuggests that there will be delays in the privatisation process, particularly for theeight major companies (mainly energy and transport) in which the governmentintends to offer stakes via initial public offerings in 2019-20. Given the symbioticrelationship between the government and major businesses, the transfer of assetsfrom public to private ownership might not in itself have a significant impact onproductivity or competitiveness.

The banking sector continues to struggle from the fallout of the financial crisis andthe tenge depreciation in 2014-15, and remains a significant systemic risk. The truelevel of non-performing loans could be significantly higher than officially reported(less than 7% at end-2016). Further state support could allow the banking sector togradually consolidate and repair its balance sheet. However, the factors thatexacerbated the banking crisis in 2009, notably corrupt and lax lending practices andpoor corporate governance, have not been resolved. In June Halyk Bank (controlledby a son-in-law of Mr Nazarbayev) acquired a controlling stake in Qazkom, an ailingbank that has been bailed out by the government, creating a large and politicallyexposed institution. This compounds the risks presented by the sector'sconcentrated ownership structure, and the fact that the owners of some ofKazakhstan's largest banks are highly politically exposed individuals.

In 2015 the government launched a stimulus package, running until at least the endof this year, equivalent to 6.6% of 2015 tenge GDP, funded from the National Fundof the Republic of Kazakhstan (NFRK, the sovereign wealth fund). This hassucceeded in partially offsetting the impact of low household demand and weakprivate lending.

Kazakhstan 5

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Fiscal policyOur forecast for general government spending (including that of local authorities) isextrapolated from the central (republican) budget.

In 2016 the budget deficit stood at just 0.3%. In February 2017 the governmentrevised its central 2017 budget expenditure up significantly, to Tenge10.74trn(US$32.1bn), from Tenge8.21trn previously. This will be met in part by an increase ofTenge1.09trn in the "targeted" transfer (earmarked for specific expenditure) from theNFRK. The government expects the central government deficit to widen toTenge1.55trn (3.1% of GDP according to the government's GDP forecast, up from1.2% previously). A large share of the additional spending will be directed tosupporting the banking sector through the purchase of non-performing assets.Based on the revised spending and transfer figures, we forecast a deficit on thegeneral government budget of 2.6% of GDP this year. Ongoing state support for thebanking sector from the NFRK is undermining government efforts to reduce thenonoil deficit. Assuming no further extra ordinary spending, we expect the deficitto narrow to 1.6% of GDP in 2018, and to contract further in subsequent years, toless than 1% of GDP by 2021.

Monetary policyIn mid-2015 the National Bank of Kazakhstan (NBK, the central bank) devalued thetenge against the US dollar and announced a shift to inflation targeting. The currentinflation target is 6-8%, falling to 5-7% in 2018 and 3-4% by 2020. The NBK hadsome success in de-dollarising the economy in 2016. However, the limited level offinancialisation could constrain the central bank's ability to influence interest ratesand the money supply, as well as inflation expectations, through open marketoperations. The oil price will continue to play a dominant role in driving theexchange rate and inflation expectations, making it difficult to achieve price stability.

At its meeting on June 5th 2017 the NBK cut its policy rate by 50 basis points, to10.5%—the second loosening of monetary policy since midNovember 2016. Thepolicy rate corridor was left unchanged at ±1 percentage point. On July 17th theNBK left the policy rate unchanged, but said that inflation was within the 2017target range and that further cuts in the policy rate were likely over the next12 months if the government's inflation forecasts were fulfilled. We expect thegovernment to meet its inflation targets in 2017-18 and anticipate that the policy ratewill be cut to 9.5-10% by the end of this year.

Kazakhstan 6

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

International assumptions 2016 2017 2018 2019 2020 2021

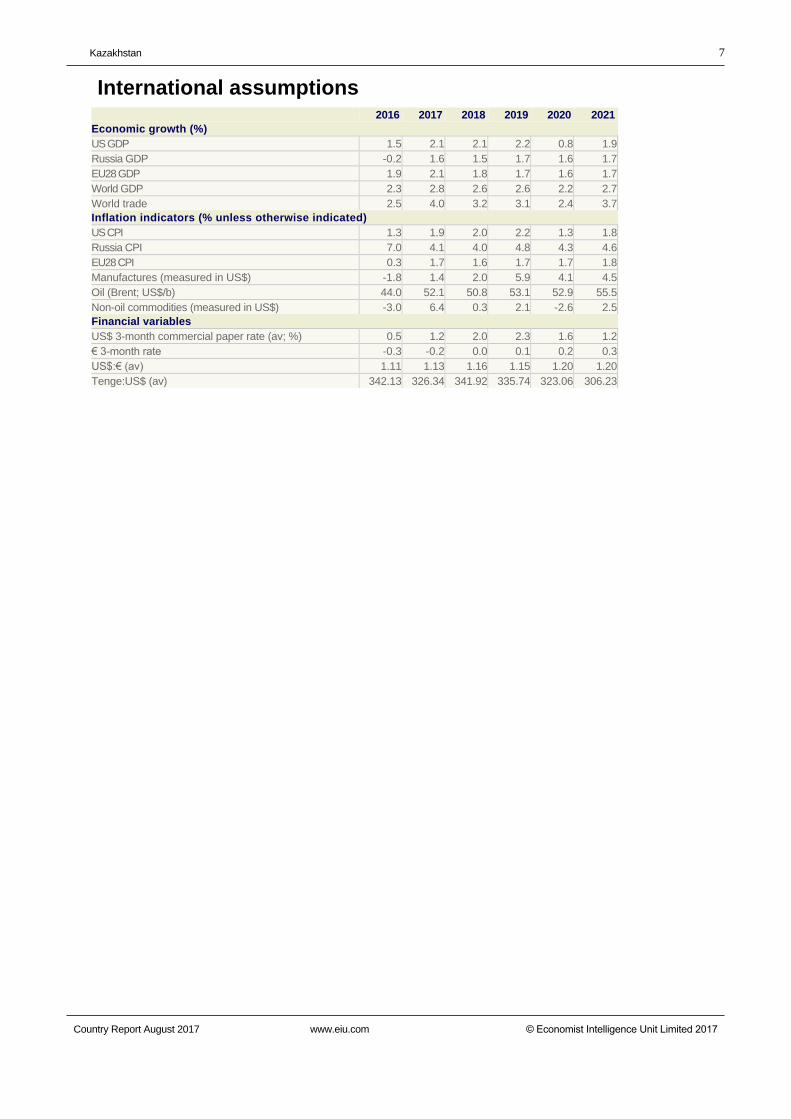

Economic growth (%)

US GDP 1.5 2.1 2.1 2.2 0.8 1.9

Russia GDP -0.2 1.6 1.5 1.7 1.6 1.7

EU28 GDP 1.9 2.1 1.8 1.7 1.6 1.7

World GDP 2.3 2.8 2.6 2.6 2.2 2.7

World trade 2.5 4.0 3.2 3.1 2.4 3.7

Inflation indicators (% unless otherwise indicated)

US CPI 1.3 1.9 2.0 2.2 1.3 1.8

Russia CPI 7.0 4.1 4.0 4.8 4.3 4.6

EU28 CPI 0.3 1.7 1.6 1.7 1.7 1.8

Manufactures (measured in US$) -1.8 1.4 2.0 5.9 4.1 4.5

Oil (Brent; US$/b) 44.0 52.1 50.8 53.1 52.9 55.5

Non-oil commodities (measured in US$) -3.0 6.4 0.3 2.1 -2.6 2.5

Financial variables

US$ 3-month commercial paper rate (av; %) 0.5 1.2 2.0 2.3 1.6 1.2

€ 3month rate -0.3 -0.2 0.0 0.1 0.2 0.3

US$:€ (av) 1.11 1.13 1.16 1.15 1.20 1.20

Tenge:US$ (av) 342.13 326.34 341.92 335.74 323.06 306.23

Kazakhstan 7

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Economic growthKazakhstan has a growing labour force and considerable catch-up potential, but thepoor business environment, weak competition in some sectors and large distancesto global markets will remain significant constraints. Growth over the past decadehas largely been driven by expansion of the extractive sector and high commodityprices, which have supported growth in consumption and government spending.Although it is a declared policy priority, the government has struggled to diversifyindustrial production away from mining and expand the tradeables sector. It willcontinue to attract significant investment to its mining and hydrocarbons sector.Chinese investment under the Belt and Road Initiative will contribute to steadyimprovements in infrastructure, but non-tariff barriers will constrain trade gains fromimproved transport connections.

In 2016 the economy expanded by just 0.9% as a result of a decline in commodityexport volumes and high inflation, which depressed household consumption. Weexpect growth to rebound to 3% in 2017. Real GDP (gross value added approach)grew by 4.2% year on year in the first half, against a low base. This is in part owingto rising oil production from the Kashagan oilfield, but the manufacturing sector hasalso performed strongly. Inflation and the exchange rate have stabilised, andalthough wages continue to contract in real terms, household spending will beboosted by a 20% rise in pensions, supporting a recovery in retail spending. Thegovernment's stimulus programme will continue to support investment inconstruction. Strong import growth suggests continued expansion in investment inJanuary-July.

In 2018-21 we forecast growth at an average of 2.7% per year. An expandingworkforce and continuing urbanisation will support output and productivity gains.However, Kazakhstan's trend growth rate is likely to be significantly lower than overthe past decade. Investment from China will remain significant, but uncertaintyabout the domestic political outlook and low commodity prices will depress overalllevels of investment. Ongoing consolidation of the banking sector will constrainbank lending, and there remains the risk of further financial shocks, which could hitbusiness confidence. We project a significant slowdown in China's economy in2018. Lower Chinese demand is reflected in a slowdown in Kazakhstan's growth inthat year, but risks are oriented to the downside.

Economic growth% 2016a 2017b 2018b 2019b 2020b 2021b

GDP 0.9 3.0 2.3 3.0 2.5 2.9

Private consumption 1.1 1.5 2.2 4.0 4.0 4.3

Government consumption 0.0 0.5 1.0 1.0 1.0 1.0

Gross fixed investment 3.0 4.0 4.0 4.1 4.0 4.0

Exports of goods & services -4.4 3.9 4.3 3.0 2.3 1.8

Imports of goods & services -2.2 5.5 5.6 4.7 5.5 5.9

Domestic demand 1.5 1.5 3.2 3.5 3.6 4.1

Agriculture 5.2 3.0 2.8 3.0 2.8 2.8

Industry 1.3 4.9 2.7 3.5 2.4 2.4

Services 0.9 2.0 2.1 2.8 2.5 3.2a Actual. b Economist Intelligence Unit forecasts.

Kazakhstan 8

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

InflationIn 2016 inflation averaged 14.6%, but slowed to 8.5% year on year in December. In2017 inflation has moved to within the NBK's target band, averaging 7.5% year onyear in the second quarter and 7.1% in July. Tenge appreciation in January-Aprilhas helped to reduce import inflation and inflation expectations, and a mildweakening in May-July does not appear to have altered these disinflationary trends.External inflationary pressures are expected to be weak, with global food pricesprojected to fall again slightly in 2017. We expect inflation to average 7.5% this year,and to weaken in 2018, as monetary policy will remain moderately tight and externalinflationary pressures will be low. Should the slowdown in China lead to a largerthan expected fall in oil prices, this would weaken the tenge and boost inflationexpectations. We believe it unlikely that the NBK will bring inflation to within the 3-4% target band by 2020.

Exchange ratesReal interest rates are expected to remain positive in 2017, at about 3%. With oilprices expected to be higher than in 2016 on average, and exports rising as a resultof the expansion of production at Kashagan, we expect the tenge to appreciate onaverage by about 5% this year, although a tightening of US dollar liquidity is adownside risk. We forecast that the tenge will weaken slightly against the dollar in2018, in line with our projection that oil prices will fall slightly. A stable oil price in2019-21 will bring about a modest appreciation against the dollar in those years. Thereal effective exchange rate will remain below the 2013 high throughout the forecastperiod.

External sectorIn 2015 low oil prices pushed the current account into deficit for the first time since2009. The deficit widened to 6.5% of GDP in 2016, covered by record levels offoreign direct investment (FDI). Rising oil exports and a higher average oil price in2017 should narrow the deficit. However, given the moderate oil price outlook, withrisks oriented to the downside, we expect the current account to remain in deficitthroughout the forecast period. Although Kazakhstan runs a significant tradesurplus, large foreign involvement in its oil sector means that net income flows arestrongly negative. Following downward revisions to our global oil price forecast, wenow expect the current-account deficit to average 4% of GDP in the forecast period,from 3% previously.

Despite record FDI inflows in 2016, there is a risk that direct investment, credit andprivate portfolio inflows will be lower than the average of the past decade, owing toperceptions of higher economic and political risk, as well as lower commodity prices.The government will partially offset this through transfers from the NFRK. As aresult, the fund is unlikely to grow further as a share of GDP, and could start todecline.

Kazakhstan 9

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Forecast summaryForecast summary(% unless otherwise indicated)

2016a 2017b 2018b 2019b 2020b 2021b

Real GDP growth 0.9 3.0 2.3 3.0 2.5 2.9

Industrial production growth -2.5 6.4 2.2 3.0 1.9 1.9

Gross agricultural production growth 5.2 3.0 2.8 3.0 2.8 2.8

Crude oil & NGL production ('000 b/d) 1,567.1 1,661.1 1,694.3 1,745.2 1,797.5 1,833.5

Unemployment rate (av) 5.0 4.9 5.0 4.9 4.6 4.8

Consumer price inflation (av) 14.6 7.5 6.2 5.8 5.6 5.5

Consumer price inflation (end-period) 8.3 7.5 6.1 5.4 6.0 5.4

Government balance (% of GDP) -0.3 -2.6 -1.6 -1.4 -1.0 -0.8

Exports of goods fob (US$ bn) 37.3 44.1 44.9 48.7 49.5 52.6

Imports of goods fob (US$ bn) 27.9 31.1 30.9 33.1 35.2 37.8

Current-account balance (US$ bn) -8.5 -7.6 -6.6 -5.4 -7.1 -7.4

Current-account balance (% of GDP) -6.5 -5.2 -4.3 -3.2 -3.8 -3.4

External debt (end-period; US$ bn) 163.8c 159.2 156.8 159.5 164.7 170.8

Exchange rate Tenge:US$ (av) 342.1 326.3 341.9 335.7 323.1 306.2

Exchange rate Tenge:US$ (end-period) 333.3 338.7 335.4 335.5 316.9 299.4

Exchange rate Tenge:Rb (av) 5.10 5.58 5.48 5.47 5.45 5.31

Exchange rate Tenge:Rb (end-period) 5.49 5.48 5.61 5.63 5.40 5.14a Actual. b Economist Intelligence Unit forecasts. c Economist Intelligence Unit estimates.

Kazakhstan 10

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Data and charts

Annual data and forecast 2012a 2013a 2014a 2015a 2016a 2017b 2018b

GDP

Nominal GDP (US$ bn) 200.1 228.3 218.5 179.3 131.3 145.8 152.2

Nominal GDP (Tenge bn) 29,832 34,727 39,150 39,757 44,929 47,593 52,031

Real GDP growth (%) 5.0 5.9 4.3 1.0 0.9 3.0 2.3

Expenditure on GDP (% real change)

Private consumption 10.1 10.7 1.4 1.8 1.1 1.5 2.2

Government consumption 13.5 1.7 9.8 2.4 0.0 0.5 1.0

Gross fixed investment 9.9 5.5 4.4 4.2 3.0 4.0 4.0

Exports of goods & services 4.8 2.7 -2.5 -4.1 -4.4 3.9 4.3

Imports of goods & services 24.8 7.8 -4.0 -0.1 -2.2 5.5 5.6

Origin of GDP (% real change)

Agriculture -17.4 11.2 1.3 3.5 5.2 3.0 2.8

Industry 1.9 3.1 1.8 0.1 1.3 4.9 2.7

Services 10.4 6.9 5.7 3.1 0.9 2.0 2.1

Population and income

Population (m) 16.9 17.2 17.5 17.7 18.0 18.2 18.4

GDP per head (US$ at PPP) 21,372 22,704 24,239 24,072 24,558 25,441 26,318

Recorded unemployment (av; %) 5.3 5.2 5.0 5.0 5.0 4.9 5.0

Fiscal indicators (% of GDP)

General government budget revenue 19.5 18.4 18.7 19.2 20.7 23.4 20.7

General government budget expenditure 21.0 19.7 19.9 20.7 21.0 26.0 22.3

General government budget balance -1.5 -1.4 -1.2 -1.5 -0.3 -2.6 -1.6

Public debt 13.2 13.1 14.8 23.4 26.2 27.5 26.9

Prices and financial indicators

Exchange rate Tenge:US$ (end-period) 150.27 153.61 182.35 339.47 333.28 338.68 335.43

Exchange rate Tenge:€ (endperiod) 199.35 211.17 221.97 371.31 348.94 397.95 387.42

Consumer prices (end-period; %) 6.1 4.5 7.1 13.6 8.3 7.5 6.1

Producer prices (av; %) 3.5 -0.3 9.4 -20.5 16.9 13.4 2.0

Stock of money M2 (% change) 7.3 1.5 -8.2 7.9 46.4 13.3 15.5

Lending interest rate (av; %)c 11.7 11.2 10.9 13.2 15.3 14.1 13.1

Current account (US$ m)

Trade balance 38,145 34,792 36,245 12,672 9,432 13,016 13,996

Goods: exports fob 86,931 85,596 80,309 46,516 37,301 44,108 44,856

Goods: imports fob -48,786 -50,803 -44,064 -33,844 -27,869 -31,092 -30,860

Services balance -7,930 -7,160 -6,298 -5,106 -4,752 -4,309 -4,676

Primary income balance -28,117 -25,148 -22,477 -11,157 -12,805 -15,850 -15,628

Secondary income balance -1,041 -1,297 -1,331 -1,550 -393 -437 -304

Current-account balance 1,058 1,187 6,140 -5,142 -8,518 -7,580 -6,612

External debt (US$ m)

Debt stock 135,498 149,653 157,651 154,288 163,827d 159,249 156,783

Debt service paid 23,205 30,916 31,164 34,951 30,137d 38,332 37,461

Principal repayments 20,862 28,341 27,854 31,266 25,736d 32,643 30,799

Interest 2,343 2,574 3,310 3,685 4,401d 5,689 6,663

International reserves (US$ m)

Total international reserves 28,280 24,678 29,209 27,871 29,532 31,441 33,369a Actual. b Economist Intelligence Unit forecasts. c Interbank loans. d Economist Intelligence Unit estimates.Sources: IMF, International Financial Statistics; Statistics Agency of the Republic of Kazakhstan; World Bank, International

Debt Statistics.

Kazakhstan 11

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Quarterly data 2015 2016 2017

3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr

General government finance (Tenge

bn)

Revenue 1,359.2 2,254.1 1,841.4 2,291.8 2,401.7 2,773.5 2,306.6 2,703.6

Expenditure & net lending 2,015.7 2,431.5 2,144.9 2,177.3 2,218.5 2,893.1 2,126.3 2,540.8

Balance -656.5 -177.4 -303.5 114.6 183.2 -119.5 180.3 162.8

Output

GDP at current prices (US$ bn) 46.7 45.3 25.3 28.3 33.2 45.0 31.4 n/a

GDP at constant 2005 prices (Tenge bn) 3,182.0 3,591.9 2,996.2 3,136.7 3,228.4 3,680.2 3,089.1 n/a

Real GDP (YTD, % change year on year) 1.0 1.0 -0.3 -0.3 0.3 0.9 3.1 n/a

Industrial production (% change, year on

year)-4.3 -3.3 -0.8 -3.1 -4.3 -1.6 5.6 10.2

Employment, wages and prices

Unemployment ('000) 443.8 451.1 447.0 447.4 444.7 441.3 439.2 439.3

Unemployment rate (% of labour force) 4.9 5.0 5.1 5.0 4.9 4.9 4.9 4.9

Monthly earnings (Tenge) 124,506134,738129,307134,239141,759146,208142,380141,277

Monthly earnings (% change, year on

year)1.9 3.0 4.1 9.7 13.9 8.5 10.1 5.2

Consumer prices (% change, year on

year)4.3 12.0 15.1 16.8 17.5 9.5 7.8 7.6

Producer prices (% change, year on year) -25.8 -11.2 7.5 17.0 25.7 17.6 28.5 14.7

Financial indicators

Exchange rate Tenge:US$ (av) 216.2 300.2 356.6 335.5 341.5 334.9 322.5 314.7

Exchange rate Tenge:US$ (end-period) 270.4 339.5 343.1 338.9 334.9 333.3 314.8 321.5

Deposit rate (av; %) 8.9 13.7 15.7 13.5 11.7 10.9 10.1 9.1

Lending rate (av; %)a 12.3 13.8 13.9 16.3 15.5 15.7 15.6 13.8

3-month real money market rate (av; %) 3.8 3.4 0.4 -0.6 -3.1 2.9 3.4 2.8

Long-term government bond yield (av; %) 4.8 4.8 4.9 5.0 5.3 5.4 7.2 7.8

M1 (end-period; Tenge bn) 3,285 3,033 3,587 4,221 4,039 4,603 4,928 n/a

M1 (% change, year on year) -9.7 1.7 17.2 17.2 22.9 51.8 37.4 n/a

M2 (end-period; Tenge bn) 8,431 8,601 9,738 10,670 11,174 12,590 12,727 n/a

M2 (% change, year on year) -11.7 7.9 24.9 25.2 32.5 46.4 30.7 n/a

Sectoral trends

Coal (m tonnes) 26.7 32.7 24.9 20.1 25.4 32.2 29.4 23.2

Natural gas (bn cu metres) 5.1 5.6 5.8 4.3 5.4 5.9 6.0 5.6

Crude oil (m tons) 322.8 334.9 335.8 327.4 301.0 355.9 355.6 364.6

Electricity (m kwh) 20,439 24,571 24,742 21,577 21,478 26,729 27,137 23,860

Foreign trade (US$ m)

Exports fob 11,342 10,034 8,284 8,467 9,471 10,516 10,846 12,321

Imports cif 7,777 7,076 5,228 6,158 6,497 7,494 6,026 7,526

Trade balance 3,565 2,958 3,056 2,309 2,974 3,022 4,820 4,795

Foreign payments (US$ m)

Trade in goods balance 2,645 2,479 2,668 1,886 2,409 2,468 4,290 4,359

Services balance -1,611 -1,455 -991 -901 -1,527 -1,333 -949 -1,083

Primary income balance -2,557 -2,029 -2,780 -3,494 -2,658 -3,872 -4,700 -4,347

Current-account balance -1,915 -1,123 -1,216 -2,595 -1,843 -2,864 -1,441 -1,207

Reserves excl gold (end-period) 20,637 20,295 19,339 20,291 20,634 19,915 19,054 19,149a Interbank loans.Sources: Statistics Agency of the Republic of Kazakhstan; IMF, International Financial Statistics; Ministry of Finance;

National Bank of Kazakhstan.

Monthly data Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Exchange rate Tenge:US$ (av)

2015 183.7 184.9 185.3 185.7 185.8 186.0 186.8 203.6 258.2 275.5 302.3 322.8

2016 365.8 359.2 344.9 337.2 332.7 336.5 341.0 344.9 338.6 332.0 339.1 333.7

2017 331.1 320.2 316.1 312.2 313.5 318.4 325.3 n/a n/a n/a n/a n/a

Exchange rate Tenge:US$ (end-period)

2015 184.5 185.1 185.7 185.8 185.8 186.2 187.5 241.8 270.4 279.2 307.2 339.5

Kazakhstan 12

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

2016 371.6 349.8 343.1 330.4 336.7 338.9 352.8 339.0 334.9 333.5 340.3 333.3

2017 326.3 312.5 314.8 313.9 311.2 321.5 326.7 n/a n/a n/a n/a n/a

Real effective exchange rate (1997=100; CPI-based)

2015 122.9 124.6 124.1 120.0 116.7 118.0 120.1 113.6 90.5 87.9 85.6 81.7

2016 76.6 78.0 79.5 79.5 81.1 80.6 80.8 79.5 80.8 83.0 84.0 86.8

2017 87.3 90.3 91.5 91.9 90.8 89.2 n/a n/a n/a n/a n/a n/a

Budget revenue (Tenge bn)

2015 471.1 674.4 617.9 839.4 748.5 670.2 373.8 559.7 425.8 480.8 624.3 1149.0

2016 446.0 800.6 594.8 762.7 876.9 652.2 802.8 850.3 748.6 1040.2 849.3 884.0

2017 -8753.7 898.9 852.9 904.4 964.5 834.7 n/a n/a n/a n/a n/a n/a

Budget expenditure (Tenge bn)

2015 436.4 626.2 610.1 713.1 682.8 711.2 696.4 652.2 667.1 669.0 633.0 1129.5

2016 735.5 706.6 702.7 702.7 717.4 757.1 729.1 722.9 766.6 845.4 886.8 1160.8

2017 -8792.6 832.8 652.3 791.9 908.6 840.3 n/a n/a n/a n/a n/a n/a

Budget balance (Tenge bn)

2015 34.6 48.2 7.8 126.2 65.7 -41.0 -322.6 -92.5 -241.3 -188.2 -8.8 19.6

2016 -289.6 94.0 -107.9 60.0 159.5 -104.9 73.7 127.4 -18.0 194.8 -37.5 -276.8

2017 38.9 66.1 200.6 112.5 55.9 -5.6 n/a n/a n/a n/a n/a n/a

Deposit rate (av; %)

2015 14.6 13.7 13.5 12.6 11.6 10.2 8.8 8.1 9.8 11.7 14.1 15.4

2016 17.8 17.1 12.2 13.9 13.5 13.2 12.2 11.5 11.5 10.7 10.9 11.1

2017 10.3 10.5 9.5 9.4 9.0 8.8 n/a n/a n/a n/a n/a n/a

Lending rate (av; %)a

2015 11.6 12.8 13.9 14.7 14.2 12.8 12.8 13.4 10.6 13.5 13.9 13.9

2016 14.6 12.8 14.3 16.3 15.8 16.7 16.8 16.9 12.8 16.0 15.9 15.1

2017 16.7 15.3 14.9 15.1 12.0 14.3 n/a n/a n/a n/a n/a n/a

M1 (% change, year on year)

2015 -19.8 -13.1 -11.6 -14.7 -4.2 -9.0 -10.5 -11.5 -9.7 -7.8 -5.7 1.7

2016 6.1 8.0 17.2 27.3 15.2 17.2 22.2 20.5 22.9 36.4 44.5 51.8

2017 45.1 41.8 37.4 30.5 29.7 n/a n/a n/a n/a n/a n/a n/a

M2 (% change, year on year)

2015 -13.8 -13.9 -12.7 -15.2 -15.0 -12.4 -16.1 -13.9 -11.7 -7.7 3.8 7.9

2016 12.3 14.8 24.9 28.8 29.6 25.2 37.4 32.6 32.5 34.2 32.7 46.4

2017 41.2 36.1 30.7 33.0 29.9 n/a n/a n/a n/a n/a n/a n/a

Industrial production (% change, year on year)

2015 -0.8 1.6 0.9 -0.4 1.1 1.3 -2.1 -6.4 -4.2 -3.9 -3.3 -2.5

2016 -0.7 0.1 -1.8 -3.1 -5.3 0.1 0.1 -7.5 0.1 1.2 1.1 1.8

2017 4.9 4.0 8.3 10.9 10.7 7.5 7.4 n/a n/a n/a n/a n/a

Retail sales (% change, year on year)

2015 4.6 3.0 3.0 1.7 2.4 2.9 3.2 2.8 -0.7 -7.0 -9.3 -7.7

2016 -7.4 -1.2 -0.8 -0.2 2.1 0.2 -0.1 4.0 0.1 5.5 0.0 6.4

2017 3.5 5.6 7.3 5.7 9.0 4.6 9.2 n/a n/a n/a n/a n/a

Unemployment rate (%)

2015 5.0 5.0 5.0 5.0 5.0 5.0 4.9 4.9 4.9 5.0 5.0 5.1

2016 5.1 5.1 5.0 5.0 5.0 5.0 4.9 4.9 4.9 4.9 4.9 4.9

2017 4.9 4.9 4.9 4.9 4.9 4.9 4.9 n/a n/a n/a n/a n/a

Kazakhstan stock exchange index KASE (end-period; Dec 7th 2000=100)

2015 827 826 804 862 874 900 861 836 800 891 918 859

2016 859 941 971 940 1,041 985 1,062 1,112 1,191 1,284 1,328 1,358

2017 1,500 1,558 1,554 1,547 1,563 1,660 1,800 n/a n/a n/a n/a n/a

Consumer prices (av; % change, year on year)

2015 7.5 6.1 5.2 4.6 4.3 3.9 3.9 3.8 4.4 9.4 12.8 13.6

2016 14.4 15.2 15.7 16.3 16.7 17.3 17.7 17.6 16.6 11.5 8.7 8.5

2017 7.9 7.8 7.7 7.5 7.5 7.5 7.1 n/a n/a n/a n/a n/a

Producer prices (av; % change, year on year)

2015 -13.0 -21.4 -24.7 -26.3 -25.1 -24.1 -25.9 -26.8 -23.7 -17.0 -9.8 -4.8

2016 4.2 8.8 8.2 15.3 16.4 18.7 24.8 26.3 26.1 19.9 17.8 15.5

2017 25.3 31.2 26.7 18.4 15.3 9.6 4.8 n/a n/a n/a n/a n/a

Average monthly wages (% change, year on year)

2015 14.0 15.3 13.5 2.0 1.8 0.2 0.6 2.6 2.6 3.0 4.2 2.0

2016 6.5 5.0 1.0 14.8 9.2 5.4 13.4 13.9 14.3 15.9 14.5 -1.9

2017 7.7 15.1 7.6 1.8 4.9 9.1 3.7 n/a n/a n/a n/a n/a

Total exports fob (US$ m)

2015 4,803 3,763 3,483 4,004 4,169 4,358 3,938 3,660 3,744 3,302 2,842 3,891

Kazakhstan 13

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

2016 2,757 2,873 2,654 2,737 2,735 2,994 3,162 3,025 3,284 2,827 3,687 4,003

2017 3,257 3,628 3,961 4,042 4,153 4,127 n/a n/a n/a n/a n/a n/a

Total imports cif (US$ m)

2015 2,700 2,221 2,347 2,836 2,752 2,859 2,722 2,690 2,365 2,461 2,296 2,320

2016 1,595 1,668 1,966 2,086 2,076 1,996 1,909 2,329 2,260 2,506 2,404 2,584

2017 1,977 1,883 2,167 2,264 2,672 2,591 n/a n/a n/a n/a n/a n/a

Trade balance fob-cif (US$ m)

2015 2,104 1,542 1,136 1,168 1,417 1,499 1,216 970 1,379 841 546 1,571

2016 1,163 1,205 688 651 659 999 1,253 696 1,024 321 1,283 1,418

2017 1,280 1,745 1,794 1,778 1,481 1,536 n/a n/a n/a n/a n/a n/a

Foreign-exchange reserves excl gold (US$ m)

2015 21,197 21,480 21,597 20,964 20,949 21,123 21,749 21,475 20,637 20,491 20,957 20,295

2016 18,875 18,687 19,339 19,912 19,471 20,291 20,033 20,222 20,634 20,007 19,841 19,915

2017 19,363 19,070 19,054 18,775 18,998 19,149 n/a n/a n/a n/a n/a n/aa Interbank loans.Sources: IMF, International Financial Statistics; Haver Analytics.

Kazakhstan 14

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Annual trends charts

Kazakhstan 15

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Monthly trends charts

Kazakhstan 16

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Comparative economic indicators

Basic data

Land area

2,717,300 sq km

Population

17.6m (2016 UN estimate)

Main towns

Kazakhstan 17

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

The capital was moved from Almaty to Astana (formerly Akmola) on December 10th1997

Population in ’000 (2009 census)

Almaty: 1,366

Astana: 613

Shymkent: 603

Karaganda: 460

Aktobe: 346

Taraz: 321

Pavlodar: 318

Ust-Kamenogorsk: 304

Climate

Continental. Average temperature in Astana in winter: 18°C; in summer: 20°C.Average temperature in Almaty in winter: 8°C; in summer: 22°C

Languages

Kazakh is the state language. Russian has the status of an official language and isthe de facto language of administration

Weights and measures

Metric system

Currency

Tenge. Average exchange rate in 2015: Tenge221.7:US$1

Fiscal year

Calendar year

Time

Six hours ahead of GMT; five hours ahead of GMT in western Kazakhstan

Public holidays

January 1st2nd (New Year's Day), March 8th (Women’s Day), March 21st23rd(Novruz), May 1st (Unification holiday), May 9th (Victory Day), July 6th (CapitalCity Day), August 30th (Constitution Day), December 1st (First President’s Day),December 16th (Independence Day)

Kazakhstan 18

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Political structure

Official name

Republic of Kazakhstan

Legal system

On December 16th 1991 the Republic of Kazakhstan became the last of the formerSoviet republics to declare its independence following the collapse of the SovietUnion. Parliament approved amendments to the 1995 constitution in 2007,ostensibly aimed at redistributing the balance of power away from the presidency infavour of the legislature

National legislature

Bicameral: 107-seat Mazhilis (lower house), 47-seat Senate (upper house)

Electoral system

Universal suffrage over the age of 18 for the presidential and Mazhilis elections;senators are partly elected by the regions and partly appointed by the president

National elections

June 2017 (half of the Senate); April 2015 (presidential); March 2016 (Mazhilis). Nextelections: 2020 (half of the Senate); 2020 (presidential); 2021 (Mazhilis)

Head of state

The president, Nursultan Nazarbayev, first elected in December 1991 (term extendedfollowing referendum in 1995). Re-elected in January 1999, December 2005, April

Kazakhstan 19

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

2011 and April 2015

National government

Council of Ministers, headed by a prime minister (appointed by the president). Inpractice, Mr Nazarbayev exercises extensive control over the political and economicspheres

Main political parties

Nur Otan (Radiant-Fatherland); Communist Party of Kazakhstan (KPK); Ak Zhol(Bright Path); Republican People's Party of Kazakhstan (RNPK); Party of Patriots;Communist People's Party of Kazakhstan (KNPK). The alliance of Azat (Freedom)and the National Social Democratic Party (OSDP), which merged in October 2009 toform OSDP Azat, collapsed in February 2013

Council of Ministers

Prime minister: Bakytzhan Sagintayev

First deputy prime minister: Askar Mamin

Deputy prime minister & agriculture minister: Askar Myrzakhmetov

Culture & sport: Arystanbek Mukhamediuly

Defence: Saken Zhasuzakov

Economic integration: Zhanar Aytzhanova

Economy: Timur Suleimenov

Education & science: Yerlan Sagadiev

Energy: Kanat Bozumbayev

Finance: Bakhyt Sultanov

Foreign affairs: Kairat Abdrakhmanov

Health & social development: Elzhan Birtanov

Information & communication: Dauren Abayev

Investment & development: Zhenis Kasymbek

Internal affairs: Kalmukhanbet Kasymov

Justice: Marat Beketayev

Labour & social security: Tamara Duiseynova

Religious affairs: Nurlan Yermekbayev

Head of the presidential administration

Adilbek Dzhaksybekov

Speakers of parliament

Kassym-Jomart Tokayev (Senate)

Nurlan Nigmatulin (Mazhilis)

Central bank chairman

Daniyar Akishev

Kazakhstan 20

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Recent analysisGenerated on September 7th 2017

The following articles have been written in response to events occurring since our most recent forecast was released, andindicate how we expect these events to affect our next forecast.

Politics

Forecast updates

August 18, 2017: Political stability

Trials expose pressure on civil society

Event

The convictions of a prominent civil society campaigner and a trade union leader,combined with ongoing intimidation of journalists, indicate that civil societycontinues to operate under intense pressure.

Analysis

On August 3rd Olesya Khalabuzar, a civil society activist, was convicted of incitingethnic enmity and given a two-year non-custodial sentence of "restricted freedom",which limits her freedom of movement and requires her to report regularly to thepolice. Ms Khalabuzar—who headed a small civil rights movement and hadaspirations of forming a political party—had already recanted her activism followingher detention and interrogation in February over her involvement in a movementagainst land reforms.

On August 4th Ramazan Yesergepov, an outspoken journalist who has previouslyserved a jail sentence on charges of divulging state secrets in a newspaper article,announced that he had fled Kazakhstan for Paris, in fear of arrest on politicallymotivated charges. In May Mr Yesergepov was stabbed as he was travelling bytrain from Almaty to Astana, the capital, to raise awareness about the case ofZhanbolat Mamay, a journalist and youth activist who has been arrested on chargesof laundering money for Mukhtar Ablyazov, a France-based Kazakh oligarch andoutspoken critic of the Kazakh government.

On July 25th Larisa Kharkova, a prominent trade union leader, was convicted ofabuse of office and given a non-custodial sentence that included community serviceand a ban on heading any trade union for five years. Ms Kharkova was the thirdtrade union leader to be convicted in recent months as part of what human rightscampaigners have condemned as a crackdown on trade union activity. She formerlyheaded the Confederation of Independent Trade Unions of Kazakhstan (CITUK),which was closed down in January after a court ruled that it had violated thestringent requirements of the law on trade unions. In May the International TradeUnion Confederation (ITUC) lodged a complaint against Kazakhstan at theInternational Labour Organisation (ILO), following the jailing of two trade unionleaders.

Impact on the forecast

These cases are in line with our forecast that the government will continue to take ahard line against independent civil society. We believe that pressure will remainintense as the authorities seek to maintain tight control over the politicalenvironment in the run-up to an eventual transition of power, when NursultanNazarbayev, the 77 year old president who has been in power since beforeindependence in 1991, eventually leaves office.

Kazakhstan 21

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

August 31, 2017: Political stability

Government plans law banning face-covering veils

Event

On August 28th Nurlan Yermekbayev, the religious affairs minister, said that thegovernment planned to prohibit certain types of religious clothing.

Analysis

Mr Yermekbayev said that a bill prohibiting face-covering veils that prevent aperson from being identified will be put to parliament in November. The law willprohibit the wearing in public of external garments that indicate affiliation to whatthe government identifies as a "destructive" religious creed, a broad definition thatcould be open to abuse. The penalty for infringements will be a fine of up toTenge230,000 (US$680).

The proposed legislation is part of government measures intended to counterIslamic radicalism. This has been a government priority since Kazakhstan sufferedits first suicide attack in 2011. Efforts have acquired fresh impetus since a fatalattack on a military base in the city of Aktobe in June 2016. Nursultan Nazarbayev,the president, has frequently said that he is against the face-covering veil, which heconsiders "non-traditional" for Kazakhstan. The government has denied that thelegislation infringes on human rights, pointing out that some European countrieshave enacted similar laws.

In July Mr Nazarbayev approved a new doctrine governing religious affairs, whichemphasises the promotion of secular values to combat extremism. The governmentis making outreach efforts to discourage extremism, and Mr Yermekbayev said that300 people who had been practising what the government considers to be "radical"forms of Islam had renounced those forms of the religion and returned tomainstream mosques this year.

Some 70% of Kazakhstan's population identifies as Muslim, although not all arepractising. A small but growing number practice what the government deems"destructive" forms of Islam. Since 2011 Kazakhstan has experienced several small-scale attacks that the government has attributed to extremists, and at the trial of thesurviving perpetrators of the 2016 Aktobe attack it was found that the individualswere inspired by Islamic radicalism. Attacks to date have targeted the securityservices, although a small number of civilians have also died. However, the securityservices say that of late they have thwarted attacks intended to target civilians.

Impact on the forecast

The number of women who wear face-covering veils in Kazakhstan is low. We donot believe that the law will have a significant effect in reducing extremism. It mayhave the unintended effect of fuelling it, by becoming a source of resentmentagainst the state among those who wear the type of clothing that it prohibits.

Kazakhstan 22

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

Economy

Forecast updates

August 18, 2017: External sector

Government reassures investors about new Russian sanctions

Event

On August 8th Timur Suleimenov, the minister of economy, said that the expandedUS sanctions against Russia would not affect the delivery of Kazakh oil tointernational markets, owing to an exemption for a major transit pipeline providingKazakhstan's oilfields with access to the sea via Russia.

Analysis

US energy companies successfully lobbied US Congress to exempt the CaspianPipeline Consortium (CPC) from the expanded sanctions. They argued that althoughthe CPC passed from western Kazakhstan to the Russian port of Novorossiyskthrough 1,000 km of Russian territory, the pipeline benefited the final recipients ofthe oil that it carried, including Ukraine; and that including it in the sanctionspackage would undermine the US energy industry and its access to lucrative foreignoil contracts. The exemption was secured despite the fact that Russian interestsown 44% of the pipeline, with the Russian state holding 24% and two Russian oilcompanies that are under sanctions, Rosneft and Lukoil, holding minority stakes.

However, Mr Suleimenov and Nursultan Nazarbayev, the president, haveacknowledged that the sanctions could have a negative effect on Russia's economicpartners, including Kazakhstan and other member states of the Eurasian EconomicUnion (EEU), a free trade zone also comprising Armenia, Belarus and the KyrgyzRepublic.

Kazakhstan's trade with Russia fell sharply following the introduction ofinternational sanctions on Russia in 2014 over the annexation of Crimea, owing tothe subsequent economic slowdown in Russia (although the collapse in global oilprices was also a major factor). Mr Suleimenov said that Kazakhstan was used todealing with fluctuations in the economies of major trading partners such as Russiaand China. Mr Nazarbayev urged the government to work hard to sustain anacceleration in growth posted in the first half of this year.

Impact on the forecast

The exemption of the CPC from the new sanctions regime supports our forecast foran economic recovery in Kazakhstan this year. It also allows Kazakhstan tocontinue its pursuit of a multi-vector foreign policy, retaining good relations withthe West and Russia.

Kazakhstan 23

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

August 24, 2017: Policy trends

Government adopts strategy to boost investment

Event

On August 15th the government approved a new five-year investment strategydesigned to increase foreign direct investment (FDI) by 26% over 2018-22.

Analysis

According to Zhenis Kasymbek, the minister for investment and development, thenational investment strategy for 2018-22 aims to boost investment in export-orientedindustries outside the natural resources sector in order to support the government'sgoal of economic diversification. The strategy sets the target of increasing totalinvestment by 2022 by 26% compared with 2016 levels, boosting investment inexport-oriented industries by 50% and increasing capital investment outside thenatural resources sector by 46%.

Mr Kasymbek said that the government had worked with the World Bank to definepriority sectors for investment and had identified two main sector groups. The firstgroup includes advanced refining in the natural resources sector, the food industryand machine-building, which will be targeted for investment in the early part of theforecast period. The second includes the hi-tech industry, tourism and the financialsector, which will be developed and targeted for investment in the latter part of theforecast period.

The government has identified 11 priority countries to target for attractinginvestment: China, France, Germany, Italy, Japan, Russia, South Korea, Turkey, theUAE, the UK and the US. It intends to promote public-private partnerships as astrategy for attracting investment.

The government has made it a priority to increase investment, particularly outsidethe natural resources sector, as Kazakhstan's growth began to slow in 2014 owing tothe collapse in global oil prices and the 2015-16 recession in Russia. In 2014 itadopted a package of investment perks for investors, putting at least US$20m intothe non-extractive sectors and introducing visa-free travel for ten high-investingstates. From January 1st 2017 the government expanded the list of countries eligiblefor visa-free travel to all 34 OECD member states.

Despite record FDI inflows in 2016, we believe that there is a risk that directinvestment, credit and private portfolio inflows will be lower than the average of thepast decade, owing to perceptions of economic and political risk, as well as lowercommodity prices.

Impact on the forecast

The investment strategy is in line with our forecast that the government willincrease incentives for foreign investors in the non-extractive industries in order toboost economic diversification. Nevertheless, we stand by our forecast thatcorruption and red tape will remain deterrents to investment, despite marginalimprovement in those areas.

Kazakhstan 24

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

August 30, 2017: Policy trends

Government pushes ahead with diversification efforts

Event

On August 22nd the Ministry for Investment and Trade said that a number of newfactories and manufacturing plants would be opened by 2020 under thegovernment's industrialisation programme in order to support economicdiversification.

Analysis

The projects, planned under the 2015-20 phase of the government's IndustrialInnovative Development Programme, include metallurgical, pharmaceutical, textileand automobile plants. Many of them will produce output destined for export, inorder to support the government's target of increasing manufacturing exports toreduce reliance on the natural resources sector.

The SAT Nickel plant will open in 2018, with a processing capacity of 9,500 tonnesof nickel and 1.9m tonnes of ore per year. Other projects in the metallurgical sectorinclude plants to produce vanadium concentrate (vanadium is a malleable metalused in manufacturing), alloys, rolled steel and tin. In the automobile industry AziaAvto, Kazakhstan's largest vehicle manufacturer, plans to open a new factory with acomplete production cycle at its base in the north-eastern city of Ust-Kamenogorskin 2019, with an initial annual production capacity of 60,000 vehicles. By 2020 fournew plants producing medicines and pharmaceutical products are also due to open,as well as two textile factories and two glazing-production facilities. A new plantproducing rail wheels and a factory manufacturing power transformers for export toneighbouring markets are also planned. The government did not specify the totalcost of all the projects planned under the strategy, some of which involve foreigninvestors from countries including France, Germany, the UK and the US.

Alik Aydarbayev, the deputy minister for investment and trade, said that since 2010,when the first phase of this industrialisation programme began, a total of1,060 projects had been launched at a total cost of Tenge5.1trn (US$15.1bn),creating 100,000 permanent jobs.

Despite the positive figures and optimistic government projections, we expect thatKazakhstan's weakness in policy towards private enterprise and competition, as wellas in policy towards foreign investment, will restrict the government's ability to shiftindustrial production firmly away from mining and to expand the tradeables sector.

Impact on the forecast

The planned factory openings are in line with our forecast that the government willpush ahead with efforts to diversify the economy, a priority that has acquired freshimpetus since global oil prices dropped in 2014. However, we continue to believethat the economy and state budget will remain reliant on the natural resourcessector in the forecast period.

Kazakhstan 25

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

August 31, 2017: Economic growth

Real GDP growth accelerates to 4.2% in H1

Event

In the first half of 2017 real GDP (gross value added approach) grew by 4.2% year onyear, according to the Statistics Agency of the Republic of Kazakhstan (SARK), upfrom 0.1% in the first half of 2016.

Analysis

The pick-up in growth in the first half was driven by the strong performance of theindustry and services sectors. According to a gross value added breakdown ofGDP, the industrial sector grew by 7.8% year on year in the first half, compared with 1.6% a year earlier, supported by mining and quarrying (+9.4%), and manufacturing(+6.5%). Kazakhstan's long-delayed Kashagan oilfield began production lastSeptember and is expected to reach its capacity of 370,000 barrels/day this year. Thegovernment forecasts that Kashagan will produce 8.9m tonnes of oil in 2017, whichwill sustain industrial growth. Services grew by 2.3% year on year in the first half,up from zero a year earlier, supported by wholesale and retail trade (+2.4%),information and communication (+2.5%), and health and social services (+3.6%).

A breakdown of GDP by expenditure for the first half is not yet available, but theacceleration in industrial production suggests that growth in exports and importspicked up over this period. This will also have been supported by the recovery indemand from Russia, Kazakhstan's major trading partner, and a rebound in global oilprices compared with average 2016 levels. As a result, foreign trade has boomed,with merchandise exports growing by 38% year on year in the first half, and importsby 19%. Private consumption is also recovering, with retail trade growing by anaverage of 5.9% year on year in the first half after a period of weakness owing to thedepreciation of the tenge in the second half of 2015, which held back privateconsumption in 2016.

The latest data indicate that government efforts to diversify the economy continueto show sluggish results. Growth remains much stronger in the extractive sectorthan in other sectors, including manufacturing, and we expect growth to remaindependent on global oil prices.

Impact on the forecast

The latest economic growth data support our forecast for 3% real GDP growth infull-year 2017. Following the economic rebound this year, we continue to forecastslower growth in 2018-21 than in the period that preceded the 2015-16 slowdown,based on weak commodity prices and a managed slowdown of the Chineseeconomy starting in 2018.

Kazakhstan 26

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

August 31, 2017: Policy trends

Central bank provides bail-out to write off bad loans

Event

On August 9th the National Bank of Kazakhstan (NBK, the central bank) announcedthat it would provide up to US$3bn to help commercial banks write off distressedassets.

Analysis

The NBK said that it would issue banks with funding of Tenge600bn 1trn(US$1.8bn 3bn) by purchasing bonds to help them fund writeoffs of nonperforming loans (NPLs). It will contribute double the amount that shareholdersprovide to recapitalise banks and improve the quality of their assets.

The funding injection is part of a new programme to boost the stability of thebanking sector. The NBK said that this would be done through recapitalisation anddebt write-offs. The bank hopes to boost lending to the non-financial private sector.Lending to this sector is currently weak, contracting by 0.4% year on year at end-July.

Banks must have a minimum capital of Tenge45bn to qualify for the programme,which will begin in September and run for 15 years. Sixteen of Kazakhstan's 33 bankswill be eligible to apply for funding.

The latest bail-out reveals how the banking industry continues to struggle withdistressed assets dating back to the financial crisis of 2009. This legacy—whenmost NPLs were not written off owing to fiscal disincentives—has beencompounded by the fall in oil prices in 2014, the economic slowdown in 2015 16 andthe depreciation of the tenge, which raised the cost of foreign-currency liabilitiesand weakened asset quality. In February the government announced a banking bail-out of Tenge2trn, to be allocated to the government's Problem Loans Fund to speedup its purchases of NPLs from commercial banks.

Official figures suggest that the level of NPLs has been brought down significantlysince 2015—they stood at 24% at the start of that year—but the ratio has risen thisyear. According to NBK data, the ratio of NPLs to the credit stock in the bankingsector stood at 10.7% on July 1st, up from 6.7% on January 1st. These figures mayoverstate the quality of banks' balance sheets, as some NPLs have been moved intospecial-purpose vehicles. Olzhas Kizatov, head of NBK banking sector supervision,said that the central bank believes the real ratio of NPLs to be higher than officialfigures suggest.

Impact on the forecast

This bail-out is in line with our forecast that Kazakhstan's banking system willremain fragile in the early part of the 2017 21 forecast period and that further statesupport is likely to be forthcoming.

Analysis

August 31, 2017: External sector

Kazakh PM calls for removal of EEU trade barriers

At an August 14th meeting of the heads of government of Eurasian EconomicUnion (EEU) member states in Astana, the Kazakh capital, Bakytzhan Sagintayev,Kazakhstan's prime minister, called for the removal of barriers to trade not onlyon paper but in practice. His remarks underscored Kazakhstan's concerns thatthe union was failing to fulfil its economic potential, and that Kazakhstan was not

Kazakhstan 27

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

reaping the economic benefits that it had anticipated.

Mr Sagintayev urged the EEU—consisting of Armenia, Belarus, Kazakhstan, theKyrgyz Republic and Russia—to remove 60 barriers to trade that remain within thefree-trade zone. He said that a list of these barriers had already been agreed bymember states and that work was under way to draft a road map to eradicate them.However, he urged member states to remove these barriers not just on paper but inpractice. Mr Sagintayev's remarks hint at Kazakhstan's behind-the-scenes concernsthat the union risks becoming a lame-duck organisation along the lines of theCommonwealth of Independent States (CIS), a grouping of post-Soviet statescreated after the fall of the Soviet Union that today is little more than a talking shop.

The meeting discussed issues including the ratification of a new customs code andthe adoption of an agreement on pensions allowing citizens from one state tocontinue accumulating their pensions while working in another. Stalling on theseissues underlines the slow and bureaucratic nature of EEU decision-making.Protracted discussions on the customs code ended in it being signed by fourmembers in December 2016, but Belarus refused to sign. Belarus eventually signedin April, but the code has yet to be ratified by member states. As a result, thedeadline for it to come into force has been postponed from July 1st 2017 toJanuary 1st 2018. Likewise, the pensions agreement has proceeded more slowly thanintended, as Andrei Kobyakov, the Belarusian prime minister, acknowledged inAstana. That members have proved unable so far to resolve a relatively simpleprocedure reveals the cumbersome nature of EEU red tape, and highlights that it hasbrought fewer tangible results than originally anticipated.

Teething troubles

The EEU was set up in 2014 by Russia, Kazakhstan and Belarus out of an existingcustoms union to create a free-trade zone with a population of 180m. Armeniaacceded on the day that the union was founded (despite Kazakhstan's publiclyexpressed reservations over accepting a country embroiled in a territorial disputewith an ally, Azerbaijan) and the Kyrgyz Republic joined in 2015. Despite pressurefrom Vladimir Putin, the Russian president, no other post-Soviet states have joined,nor have any expressed any intention of doing so in the early part of our forecastperiod (2017 21).

The Kazakh president, Nursultan Nazarbayev, was a staunch supporter of the EEUin the run-up to its foundation, frequently pointing out that he had first proposedthe idea after the collapse of the Soviet Union. However, the EEU was created amidchallenging geopolitical conditions and suffered teething troubles that haveseriously hampered its development.

The EEU was set up as a vehicle for economic integration in 2014, at a time ofheightened suspicions among member states—including Kazakhstan—overRussia's regional geopolitical intentions following its annexation of Crimea and theoutbreak of an unresolved conflict involving Russian-backed rebels in easternUkraine. The economic prospects of the union, which started to function in January2015, were damaged in the early stages by Western sanctions imposed on Russiaover its actions in Ukraine and by a regional economic downturn stemming from afall in global oil prices that negatively affected the economies of regional energyproducers.

The union was created to boost trade between member states, but trade betweenthem fell in 2015 and 2016 as a result of the economic downturn in Russia and othermember states resulting from sanctions and the fall in oil prices. Trade betweenmembers fell by 25% in 2015 and by 6% in 2016, according to data from the EurasianEconomic Commission, the supranational body that administers the union. Tradebetween Kazakhstan and the EEU (mainly consisting of trade with Russia, as itstrade with other members is negligible) fell by 29% in 2015 and by 23% in 2016.

In 2017, as member states' economies have begun to recover, trade has grown forthe first time since the union was formed. EEU trade rose by 32% in the first quarter

Kazakhstan 28

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017

of 2017, and Kazakhstan's trade with other members grew by 39%. Kazakhstanmakes up 10% of the union's trade balance, Russia 63%, Belarus 25%, and Armeniaand the Kyrgyz Republic 1% each.

However, prospects for a boost in trade from this year have now been marred by theintroduction of new US sanctions against Russia in August. The Kazakhgovernment has acknowledged that the sanctions will have negative repercussionsfor Kazakhstan's economy, and it is clearly concerned that the sanctions will hitdemand in Russia, its largest trading partner, undermining the pick-up inKazakhstan's economy this year.

Kazakh concerns

Mr Nazarbayev's enthusiasm for the union was curbed in its early days owing to hisconcerns over Russia's geopolitical ambitions for the union as a vehicle for anexpansionist Russia to reassert its authority over former Soviet republics.Mr Nazarbayev has continually stressed that Kazakhstan views the EEU as a purelyeconomic organisation designed to boost trade and improve the economicprospects of member states, and as an important vehicle for landlocked Kazakhstanto gain access to export routes and help it achieve its goal of becoming a Eurasiantransit, transport and logistics hub. In 2014, shortly after the union was created, hestated that Kazakhstan reserved the right to withdraw if the organisation posed athreat to the country's sovereignty. Although Mr Nazarbayev continues publicly tosupport the union, and called at the Astana meeting for it to be strengthened, healso continues to pursue diversification of Kazakhstan's trading partnerships byforging links with Europe, the Middle East and Asia, in particular China.

EEU prospects

We believe that in the forecast period EEU integration will proceed far more slowlythan originally anticipated. Its prospects will be hampered by the impact of Westernsanctions on the Russian economy and by concerns among other members—particularly Belarus, but also Kazakhstan—about Russia using the union as avehicle to pursue hegemonic regional ambitions.

Mr Nazarbayev regularly states that Russia is Kazakhstan's closest ally, and that theEEU is a vital economic alliance for his country. However, as a pragmatist heundoubtedly recognises the EEU's limitations, given the economic implications ofnew sanctions against Russia and the lack of prospects in the immediate future for asignificant improvement in the Russia's relations with the West. As a result,Kazakhstan will continue to pursue closer EEU integration while seeking to diversifyits trading partnerships, as the union has failed to deliver the promised boost intrade.

Kazakhstan 29

Country Report August 2017 www.eiu.com © Economist Intelligence Unit Limited 2017