course on professionalism asop presentation. 2 contents introduction introduction asop highlights...

TRANSCRIPT

Course on Course on ProfessionalismProfessionalism

ASOP PresentationASOP Presentation

2

ContentsContents

IntroductionIntroduction ASOP HighlightsASOP Highlights ASOP in AsiaASOP in Asia

Course on Course on ProfessionalismProfessionalism

ASOP - IntroductionASOP - Introduction

4

OutlineOutline

Perspectives on ProfessionsPerspectives on Professions Standards of Practice Standards of Practice Background for StandardsBackground for Standards

5

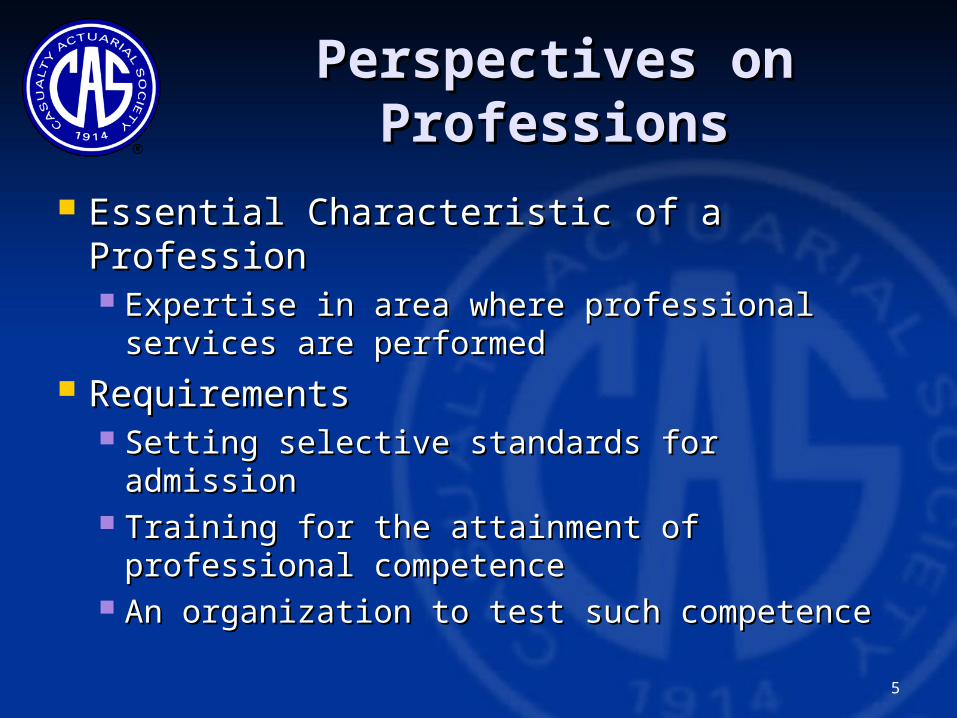

Perspectives on Perspectives on ProfessionsProfessions

Essential Characteristic of a Essential Characteristic of a ProfessionProfession Expertise in area where professional Expertise in area where professional

services are performedservices are performed RequirementsRequirements

Setting selective standards for admissionSetting selective standards for admission Training for the attainment of Training for the attainment of

professional competenceprofessional competence An organization to test such competenceAn organization to test such competence

6

Perspectives on Perspectives on ProfessionsProfessions

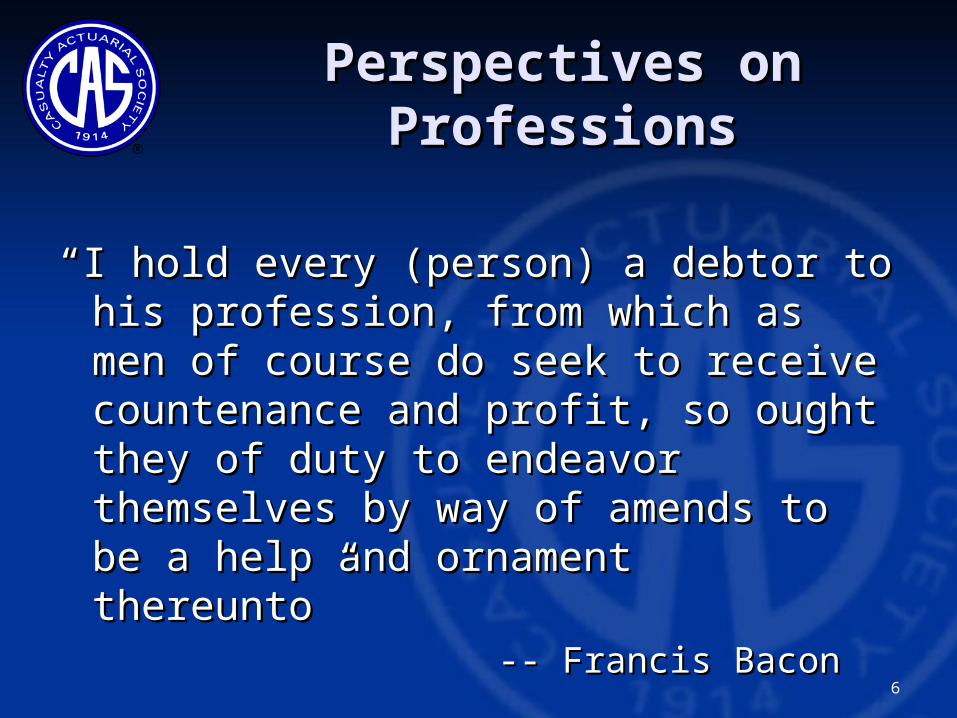

““I hold every (person) a debtor to his I hold every (person) a debtor to his profession, from which as men of profession, from which as men of course do seek to receive course do seek to receive countenance and profit, so ought countenance and profit, so ought they of duty to endeavor themselves they of duty to endeavor themselves by way of amends to be a help and by way of amends to be a help and ornament thereunto”ornament thereunto”

-- Francis Bacon-- Francis Bacon

7

Perspectives on Perspectives on ProfessionsProfessions

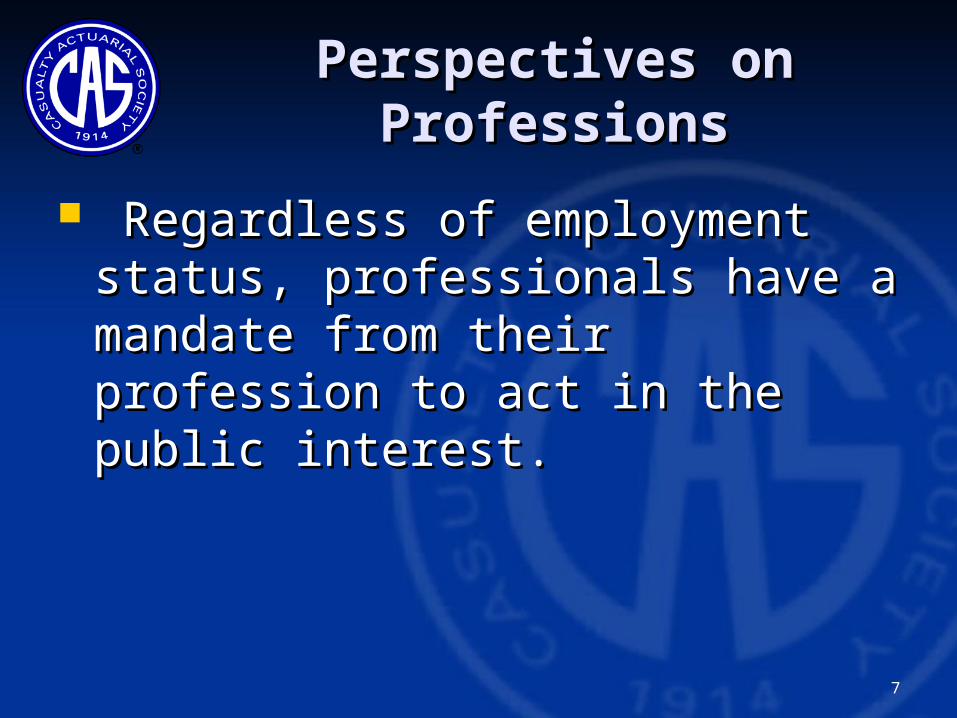

Regardless of employment Regardless of employment status, professionals have a status, professionals have a mandate from their profession to mandate from their profession to act in the public interest.act in the public interest.

8

Standards of Standards of PracticePractice

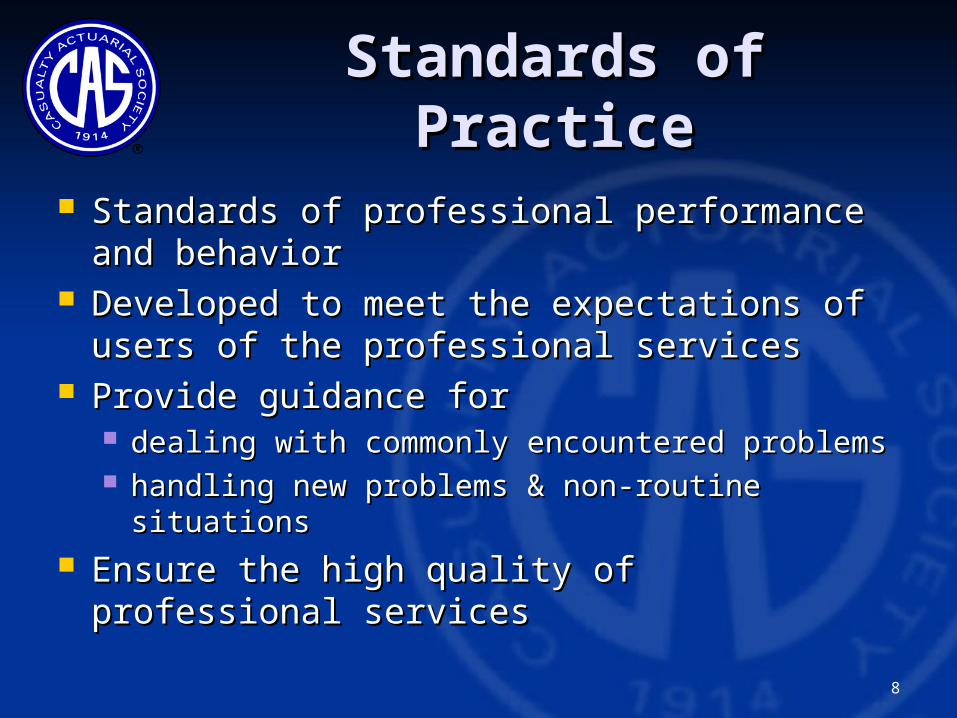

Standards of professional performance and Standards of professional performance and behaviorbehavior

Developed to meet the expectations of Developed to meet the expectations of users of the professional servicesusers of the professional services

Provide guidance forProvide guidance for dealing with commonly encountered problemsdealing with commonly encountered problems handling new problems & non-routine situationshandling new problems & non-routine situations

Ensure the high quality of professional Ensure the high quality of professional servicesservices

9

Background of Background of StandardsStandards

1954: SOA update of 1954: SOA update of Guides to Guides to Professional ConductProfessional Conduct (covered only (covered only general principles & precepts)general principles & precepts)

1956: Conference of Actuaries in 1956: Conference of Actuaries in Public Practice: Public Practice: Code of Professional Code of Professional ConductConduct

10

Background of Background of StandardsStandards

1965: AAA formed; issued its own “Code”:1965: AAA formed; issued its own “Code”: Professional DutyProfessional Duty Member’s responsibility to his/her principalMember’s responsibility to his/her principal Relationship with principalRelationship with principal Impartiality & independenceImpartiality & independence Advertising, publicity, & relations with other Advertising, publicity, & relations with other

membersmembers RemunerationRemuneration Use of titlesUse of titles Little direction in “standards of practice”Little direction in “standards of practice”

11

Background of Background of StandardsStandards

1970’s: “Standards” start to be developed in 1970’s: “Standards” start to be developed in response to guides/laws issued by AICPA, response to guides/laws issued by AICPA, NAIC, Federal Government, et al.NAIC, Federal Government, et al.

Late 70’s: Emergence of the “Valuation Late 70’s: Emergence of the “Valuation Actuary”Actuary”

1985: IASB formed1985: IASB formed 1988: ASB formed; given sole discretion to 1988: ASB formed; given sole discretion to

promulgate actuarial standards of practicepromulgate actuarial standards of practice Charge: develop, promulgate standards; Charge: develop, promulgate standards;

continually review them for update needscontinually review them for update needs

12

Focus of StandardsFocus of Standards

Indicate how fundamental concepts & Indicate how fundamental concepts & methodological principles should be methodological principles should be applied in a variety of circumstancesapplied in a variety of circumstances

Five “Areas of Practice” within ASB, each Five “Areas of Practice” within ASB, each with its own operating sub-committee, with its own operating sub-committee, charged with developing & reviewing charged with developing & reviewing appropriate ASOP’s: appropriate ASOP’s: CasualtyCasualty HealthHealth LifeLife PensionPension GeneralGeneral

13

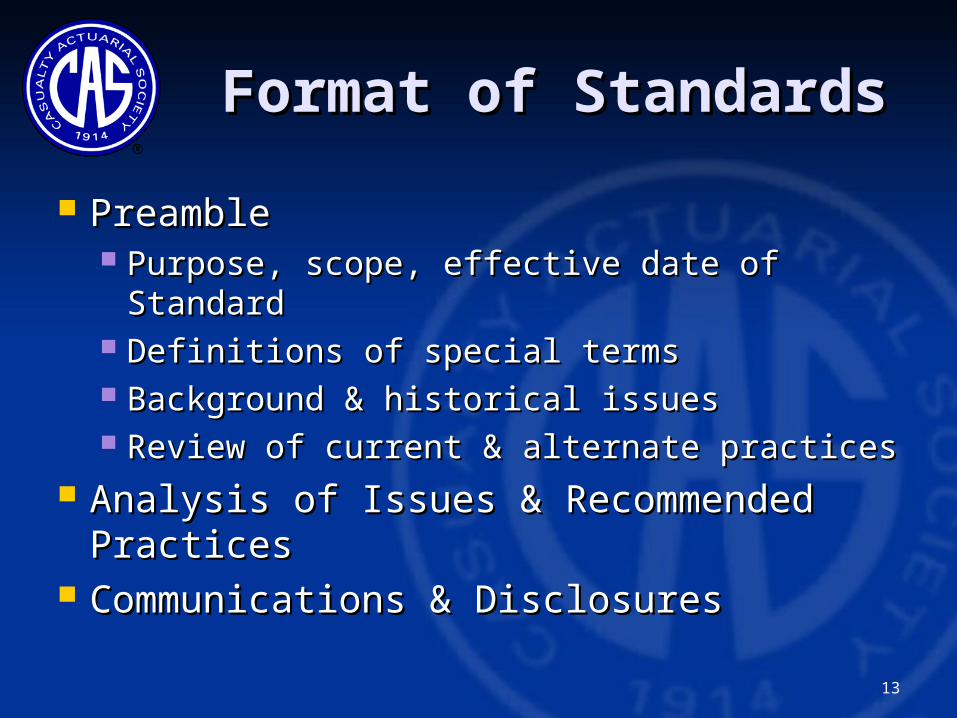

Format of StandardsFormat of Standards

PreamblePreamble Purpose, scope, effective date of Purpose, scope, effective date of

StandardStandard Definitions of special termsDefinitions of special terms Background & historical issuesBackground & historical issues Review of current & alternate practicesReview of current & alternate practices

Analysis of Issues & Recommended Analysis of Issues & Recommended PracticesPractices

Communications & DisclosuresCommunications & Disclosures

Course on Course on ProfessionalismProfessionalism

ASOP HighlightsASOP Highlights

15

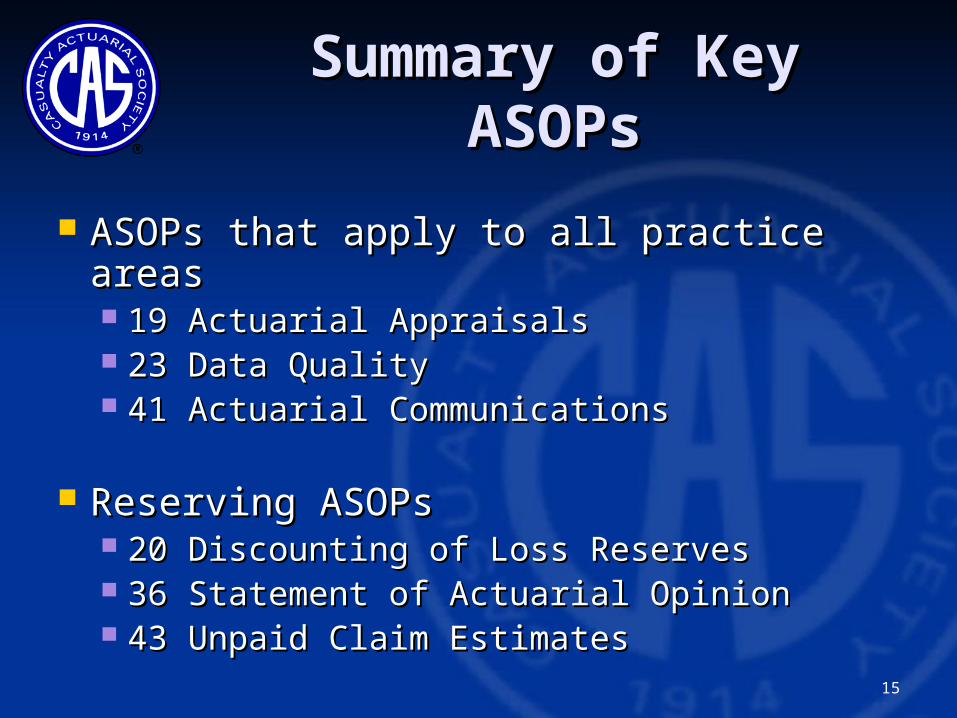

Summary of Key Summary of Key ASOPsASOPs

ASOPs that apply to all practice areasASOPs that apply to all practice areas 19 Actuarial Appraisals19 Actuarial Appraisals 23 Data Quality23 Data Quality 41 Actuarial Communications 41 Actuarial Communications

Reserving ASOPsReserving ASOPs 20 Discounting of Loss Reserves20 Discounting of Loss Reserves 36 Statement of Actuarial Opinion36 Statement of Actuarial Opinion 43 Unpaid Claim Estimates43 Unpaid Claim Estimates

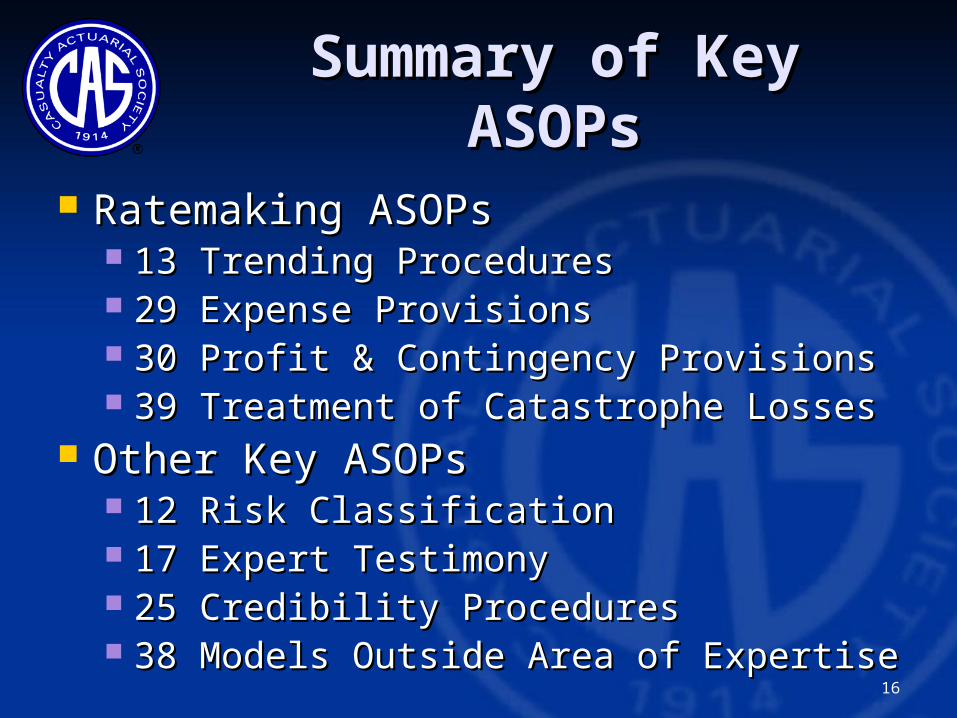

Summary of Key Summary of Key ASOPsASOPs

Ratemaking ASOPsRatemaking ASOPs 13 Trending Procedures13 Trending Procedures 29 Expense Provisions29 Expense Provisions 30 Profit & Contingency Provisions30 Profit & Contingency Provisions 39 Treatment of Catastrophe Losses39 Treatment of Catastrophe Losses

Other Key ASOPsOther Key ASOPs 12 Risk Classification12 Risk Classification 17 Expert Testimony17 Expert Testimony 25 Credibility Procedures25 Credibility Procedures 38 Models Outside Area of Expertise38 Models Outside Area of Expertise

16

17

ASOP 19 – Actuarial ASOP 19 – Actuarial Appraisals Purpose and Appraisals Purpose and

ScopeScope Appraisals of Casualty, Health and Life Insurance Appraisals of Casualty, Health and Life Insurance

BusinessesBusinesses Provides guidance to actuaries performing Provides guidance to actuaries performing

professional services with respect to appraisals professional services with respect to appraisals of casualty, health and life businessesof casualty, health and life businesses

Applies to appraisals performed on an insurance Applies to appraisals performed on an insurance company or HMO, a collection of policies or company or HMO, a collection of policies or contracts in-force, a distribution system that sells contracts in-force, a distribution system that sells such policies or contracts.such policies or contracts.

Effective November 1, 2005 for all appraisals Effective November 1, 2005 for all appraisals initiated on or after that dateinitiated on or after that date

18

ASOP 19 – Actuarial ASOP 19 – Actuarial AppraisalsAppraisals

Issues and Recommended Issues and Recommended PracticesPractices

Setting assumptions (including discount Setting assumptions (including discount rate)rate)

Applicability of AppraisalApplicability of Appraisal Treatment of assetsTreatment of assets Model validationModel validation Sensitivity testingSensitivity testing Reliance on Data and Other InformationReliance on Data and Other Information DocumentationDocumentation

19

ASOP 19 – Actuarial ASOP 19 – Actuarial AppraisalsAppraisals

Communications & Communications & DisclosuresDisclosures

Scope of Assignment, principal, intended Scope of Assignment, principal, intended useuse

Description of entityDescription of entity Appraisal value and dateAppraisal value and date Methodology, model, validation techniquesMethodology, model, validation techniques Level of CapitalLevel of Capital Assumptions Assumptions TaxesTaxes Sensitivity of valueSensitivity of value Reliance on OthersReliance on Others

20

ASOP 19 – Actuarial ASOP 19 – Actuarial AppraisalsAppraisals

Communications & Communications & DisclosuresDisclosures

Variation of ResultsVariation of Results Appropriate use of “Actuarial Appropriate use of “Actuarial

Appraisal”Appraisal” No obligation to communicate with No obligation to communicate with

other usersother users Deviation from standardDeviation from standard

21

ASOP 23 Data QualityPurpose

Data Quality Give guidance in:

Selecting data Relying on data supplied by others Reviewing data Using Data Making disclosures with regard to

data quality

22

ASOP 23 Data QualityScopeScope

Applies to all areas of practiceApplies to all areas of practice Does NOT require audit of dataDoes NOT require audit of data If standard establishes requirements If standard establishes requirements

in addition to those imposed by law, in addition to those imposed by law, satisfy bothsatisfy both

Originally effective 12/31/1993; Originally effective 12/31/1993; updated effective for work products updated effective for work products started on or after July 1, 2006started on or after July 1, 2006

23

ASOP 23 Data QualitySelection of DataSelection of Data

Understand scope and intended useUnderstand scope and intended use Consider desired and possible alternative Consider desired and possible alternative

data elementsdata elements Data considerations:Data considerations:

Appropriate for intended purpose, including Appropriate for intended purpose, including whether sufficiently currentwhether sufficiently current

Reasonableness and comprehensiveness, with Reasonableness and comprehensiveness, with particular attention to internal and external particular attention to internal and external consistencyconsistency

Known, material limitationsKnown, material limitations Cost and feasibility against benefit of Cost and feasibility against benefit of

alternativesalternatives Sampling methods, if usedSampling methods, if used

24

ASOP 23 Data QualityReliance on Data Supplied eliance on Data Supplied

by Othersby Others Accuracy and comprehensiveness of Accuracy and comprehensiveness of

data is responsibility of the providerdata is responsibility of the provider Actuary may rely on data supplied by Actuary may rely on data supplied by

others but should follow guidance others but should follow guidance under 3.5: review of data under 3.5: review of data firstfirst (new (new clarification) clarification)

Okay, unless material errors or Okay, unless material errors or unreliability becomes apparentunreliability becomes apparent

Disclose relianceDisclose reliance

25

ASOP 23 Data Quality

Review of DataReview of Data Applies whether the actuary prepared the Applies whether the actuary prepared the

data or received data from a third partydata or received data from a third party Review for reasonableness and Review for reasonableness and

consistency, “unless review is not consistency, “unless review is not necessary or is not practical”necessary or is not practical”

Take into account the extent of checking, Take into account the extent of checking, verification, or auditing already verification, or auditing already performed, purpose and nature of performed, purpose and nature of assignment, and constraintsassignment, and constraints

26

ASOP 23 Data Quality

Use of DataUse of DataProfessional judgment prior to Professional judgment prior to use:use:

Will use of imperfect data produce Will use of imperfect data produce material bias or highly uncertain material bias or highly uncertain results?results?

Is the data adequate to satisfy Is the data adequate to satisfy analysis purpose?analysis purpose?

Can data be corrected or additional Can data be corrected or additional data provided?data provided?

27

ASOP 23 Data QualityDocumentation/ Documentation/

DisclosureDisclosure Refer to guidance from ASOP 41: Refer to guidance from ASOP 41: Actuarial Actuarial

CommunicationsCommunications Include in actuary’s report:Include in actuary’s report:

Source(s) of dataSource(s) of data Whether or not data reviewedWhether or not data reviewed Process to evaluate dataProcess to evaluate data Materiality of biases due to imperfect dataMateriality of biases due to imperfect data Adjustments or modifications madeAdjustments or modifications made Extent of reliance on data supplied by othersExtent of reliance on data supplied by others Limitations on use of work productLimitations on use of work product Any unresolved concern about the dataAny unresolved concern about the data Conflicts with law or regulationsConflicts with law or regulations

28

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

Purpose and ScopePurpose and Scope

Actuarial CommunicationsActuarial Communications Guidance for written, electronic or oral Guidance for written, electronic or oral

actuarial communicationsactuarial communications Applies to all actuarial Applies to all actuarial

communications, with some exceptions communications, with some exceptions e.g. testimonye.g. testimony

Effective for any actuarial Effective for any actuarial communications dated or occurring on communications dated or occurring on or after July 15, 2002 or after July 15, 2002

29

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

General RequirementsGeneral Requirements Identify Principal for whom findings are made; clearly Identify Principal for whom findings are made; clearly

state scope and any limitations or constraintsstate scope and any limitations or constraints Form and content clear and appropriate to Form and content clear and appropriate to

circumstances and audiencecircumstances and audience Issued in timely manner, identifying responsible Issued in timely manner, identifying responsible

actuaryactuary Independence and advocacy should be statedIndependence and advocacy should be stated Define extent of reliance on others including PrincipalDefine extent of reliance on others including Principal Applied to cumulative communications so that all of Applied to cumulative communications so that all of

the communications, taken together, satisfy this the communications, taken together, satisfy this standard even though individually may notstandard even though individually may not

30

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

Requirements for Specific Requirements for Specific Communication TypesCommunication Types

Oral communication should not Oral communication should not conflict with written or electronicconflict with written or electronic

Significant findings should be in Significant findings should be in writing or electronic form, actuarial writing or electronic form, actuarial report if appropriatereport if appropriate

Actuarial report should contain data, Actuarial report should contain data, assumptions and methods to enable assumptions and methods to enable another actuary to perform an another actuary to perform an objective appraisalobjective appraisal

31

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

Compliance with Other Compliance with Other StandardsStandards

Other ASOPs may supersede or give Other ASOPs may supersede or give additional clarity to this standardadditional clarity to this standard

Compliance with law, regulation, or Compliance with law, regulation, or another profession's standards may another profession's standards may be sufficient to deem compliance be sufficient to deem compliance with this standardwith this standard

32

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

Responsibility to Other Responsibility to Other UsersUsers

Use of Actuarial Communication By Use of Actuarial Communication By Others – recognize risk of Others – recognize risk of misquotation, misinterpretation. To misquotation, misinterpretation. To prevent misuse, ensure communication prevent misuse, ensure communication is clear and presented fairly, may is clear and presented fairly, may include limits on distributioninclude limits on distribution

No obligation to communicate with any No obligation to communicate with any person other than the intended person other than the intended audienceaudience

33

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunicationsDocumentationDocumentation

Maintain appropriate documentation Maintain appropriate documentation of work for a reasonable periods of of work for a reasonable periods of timetime

Identify data, assumptions and Identify data, assumptions and methods such that another actuary methods such that another actuary could evaluate the reasonableness of could evaluate the reasonableness of the workthe work

34

ASOP 41 Actuarial ASOP 41 Actuarial CommunicationsCommunications

Deviation from Standard Deviation from Standard

Must justify any material deviation Must justify any material deviation from standardfrom standard

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

ScopeScope Property/Casualty Unpaid Claim EstimatesProperty/Casualty Unpaid Claim Estimates Applicable when:Applicable when:

Estimating unpaid P&C claim liabilities for all Estimating unpaid P&C claim liabilities for all classes of entitiesclasses of entities

Developing unpaid claim liabilities for events that Developing unpaid claim liabilities for events that have already occurredhave already occurred

Communicating actuarial findings in Communicating actuarial findings in written or written or electronic form electronic form

Applies only to undiscounted value estimates. See Applies only to undiscounted value estimates. See ASOP No. 20ASOP No. 20

Applies to unpaid claim estimate portion for PSAO. Applies to unpaid claim estimate portion for PSAO. See ASOP No. 36See ASOP No. 36

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

Scope Scope (cont’d.)(cont’d.)

Does not apply to:

Oral communicationOral communication

Ratemaking estimates (i.e. future events)Ratemaking estimates (i.e. future events)

Actions taken by the user based on results of analysisActions taken by the user based on results of analysis

Estimation of items that may be a function of unpaid Estimation of items that may be a function of unpaid claim estimates or claim outcomesclaim estimates or claim outcomes

Unpaid claims covered by ASOP No. 5 or ASOP No. 42 Unpaid claims covered by ASOP No. 5 or ASOP No. 42 standard standard doesdoes apply to health benefits associated with apply to health benefits associated with

state or federal WC statutes and liability policies.state or federal WC statutes and liability policies.

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

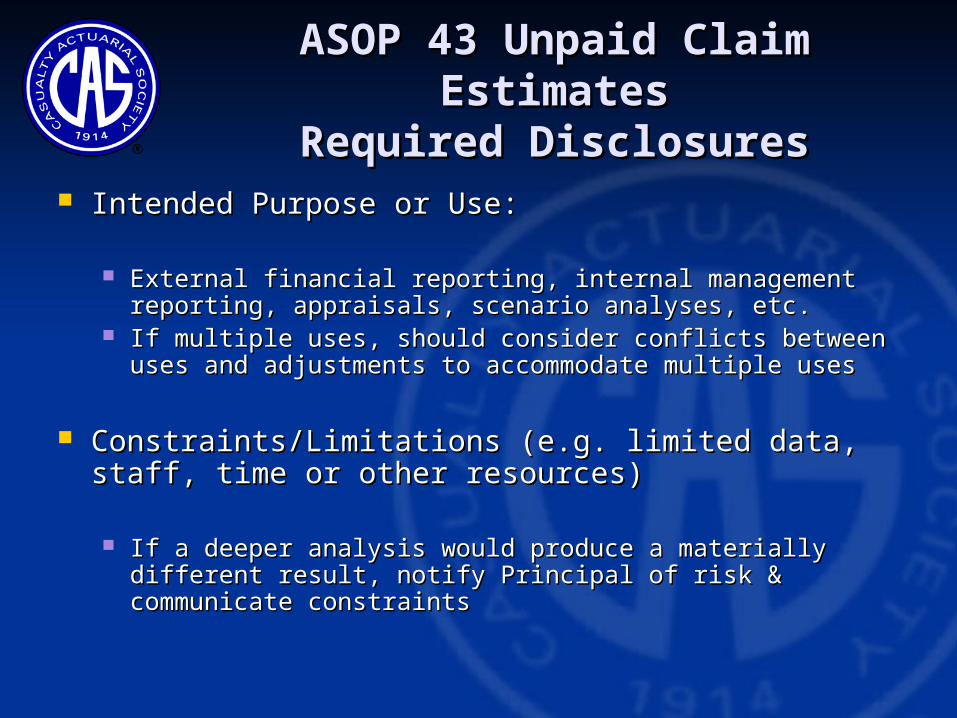

Required DisclosuresRequired Disclosures Intended Purpose or Use:Intended Purpose or Use:

External financial reporting, internal management External financial reporting, internal management reporting, appraisals, scenario analyses, etc.reporting, appraisals, scenario analyses, etc.

If multiple uses, should consider conflicts between uses If multiple uses, should consider conflicts between uses and adjustments to accommodate multiple usesand adjustments to accommodate multiple uses

Constraints/Limitations (e.g. limited data, staff, Constraints/Limitations (e.g. limited data, staff, time or other resources)time or other resources)

If a deeper analysis would produce a materially If a deeper analysis would produce a materially different result, notify Principal of risk & communicate different result, notify Principal of risk & communicate constraintsconstraints

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

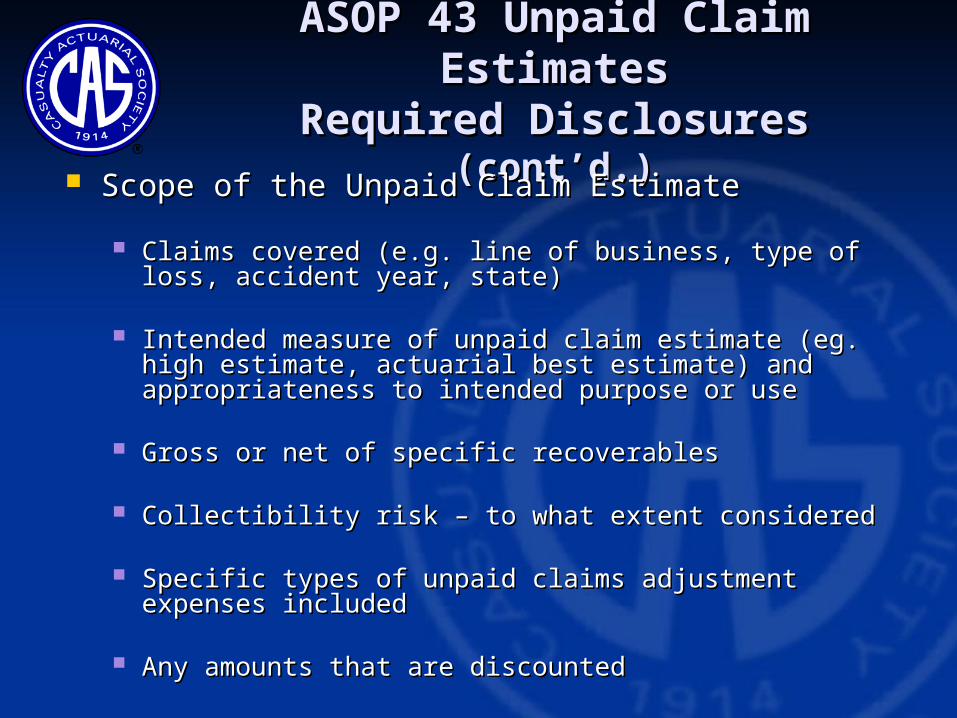

Required Disclosures Required Disclosures (cont’d.)(cont’d.) Scope of the Unpaid Claim EstimateScope of the Unpaid Claim Estimate

Claims covered (e.g. line of business, type of loss, Claims covered (e.g. line of business, type of loss, accident year, state)accident year, state)

Intended measure of unpaid claim estimate (eg. high Intended measure of unpaid claim estimate (eg. high estimate, actuarial best estimate) and appropriateness estimate, actuarial best estimate) and appropriateness to intended purpose or useto intended purpose or use

Gross or net of specific recoverablesGross or net of specific recoverables

Collectibility risk – to what extent consideredCollectibility risk – to what extent considered

Specific types of unpaid claims adjustment expenses Specific types of unpaid claims adjustment expenses included included

Any amounts that are discountedAny amounts that are discounted

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

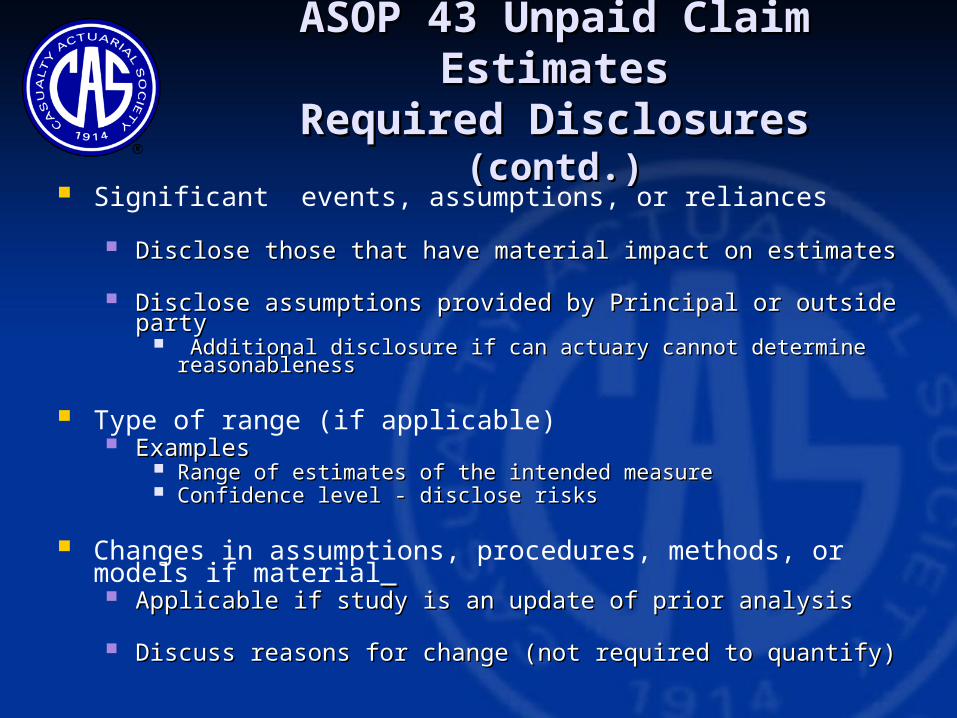

Required Disclosures Required Disclosures (contd.)(contd.) Significant events, assumptions, or reliances

Disclose those that have material impact on estimatesDisclose those that have material impact on estimates

Disclose assumptions provided by Principal or outside partyDisclose assumptions provided by Principal or outside party Additional disclosure if can actuary cannot determine Additional disclosure if can actuary cannot determine

reasonablenessreasonableness

Type of range (if applicable) ExamplesExamples

Range of estimates of the intended measure Range of estimates of the intended measure Confidence level - disclose risksConfidence level - disclose risks

Changes in assumptions, procedures, methods, or models if material Applicable if study is an update of prior analysisApplicable if study is an update of prior analysis

Discuss reasons for change (not required to quantify)Discuss reasons for change (not required to quantify)

ASOP 43 Unpaid Claim ASOP 43 Unpaid Claim EstimatesEstimates

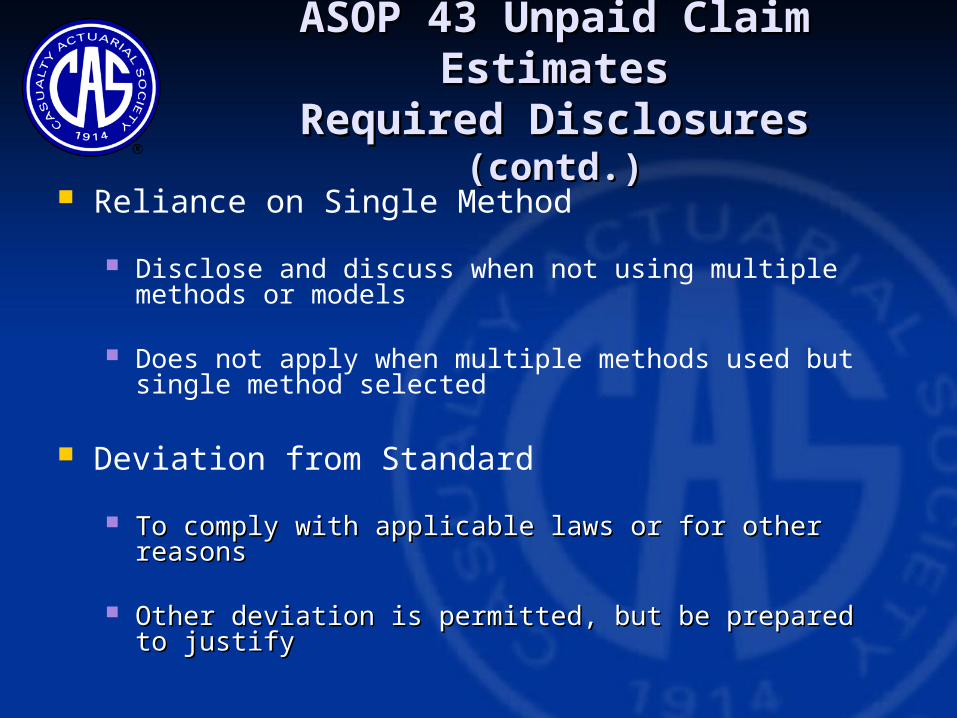

Required Disclosures Required Disclosures (contd.)(contd.) Reliance on Single Method

Disclose and discuss when not using multiple methods or models

Does not apply when multiple methods used but single method selected

Deviation from Standard

To comply with applicable laws or for other reasonsTo comply with applicable laws or for other reasons

Other deviation is permitted, but be prepared to justifyOther deviation is permitted, but be prepared to justify

Course on Course on ProfessionalismProfessionalism

ASOP in AsiaASOP in Asia

42

ASOPs in AsiaASOPs in Asia

ChinaChina Hong KongHong Kong SingaporeSingapore TaiwanTaiwan

43

ASOPs in AsiaASOPs in Asia

China – CIRC Regulation No. 13 on ReservingChina – CIRC Regulation No. 13 on Reserving OverviewOverview Type of Policy ProvisionsType of Policy Provisions MethodologiesMethodologies ReportingReporting

44

ASOPs in AsiaASOPs in Asia

Hong Kong – Hong Kong Insurance Authority Hong Kong – Hong Kong Insurance Authority Guidance Note GN9 on Actuarial Review of Guidance Note GN9 on Actuarial Review of Insurance Liabilities in respect of Employees’ Insurance Liabilities in respect of Employees’ Compensation and Motor Insurance BusinessesCompensation and Motor Insurance Businesses Introduction, Application and ParametersIntroduction, Application and Parameters Actuarial Review ReportActuarial Review Report Certification of the Actuarial OpinionCertification of the Actuarial Opinion The Actuary – QualificationThe Actuary – Qualification Commencement of the Actuarial Review RequirementCommencement of the Actuarial Review Requirement Submission of the Actuarial Review Report and Submission of the Actuarial Review Report and

CertificateCertificate

45

ASOPs in AsiaASOPs in Asia

Hong Kong – Actuarial Guidance Note GN4 on Hong Kong – Actuarial Guidance Note GN4 on Outstanding Claims in General Insurance Note Outstanding Claims in General Insurance Note on Professional Practiceon Professional Practice IntroductionIntroduction The Role of the Actuary – Advisor, must have clear The Role of the Actuary – Advisor, must have clear

agreementagreement Outstanding Claim Liability – Liabilities, Estimates, Outstanding Claim Liability – Liabilities, Estimates,

Discounting, Uncertainty, MethodologyDiscounting, Uncertainty, Methodology Outstanding Claim ProvisionOutstanding Claim Provision Reporting GuidelinesReporting Guidelines

46

ASOPs in AsiaASOPs in Asia

Singapore – Singapore Actuarial Society Guidance Singapore – Singapore Actuarial Society Guidance Note G1 for Actuaries investigating Policy Liabilities Note G1 for Actuaries investigating Policy Liabilities relating to general insurance businessrelating to general insurance business Background and ScopeBackground and Scope Data and informationData and information Assumptions including analysis of experience and Assumptions including analysis of experience and

reconciliation with previous investigationreconciliation with previous investigation Methodology including description of case reserving policy, Methodology including description of case reserving policy,

practical considerations for Provisions for Adverse practical considerations for Provisions for Adverse DevelopmentDevelopment

Uncertainty – Treatment and quantificationUncertainty – Treatment and quantification Business Issues – Importance of face-to-face meetings with key Business Issues – Importance of face-to-face meetings with key

personnelpersonnel Reporting – Format, contents and supporting appendicesReporting – Format, contents and supporting appendices

47

ASOPs in AsiaASOPs in Asia

Taiwan – Standard of Practices and Statement of Taiwan – Standard of Practices and Statement of Principles are combined in Taiwan. They are Principles are combined in Taiwan. They are based on CAS and AAA’s publications with based on CAS and AAA’s publications with adjustments for local issues. adjustments for local issues. Reserving Reserving RatemakingRatemaking Reinsurance – Risk Transfer TestingReinsurance – Risk Transfer Testing Expense ClassificationExpense Classification Profit and Contingency loadProfit and Contingency load