arvindapp.investmentguruindia.com/mobile/researcharticles/2016...ur coverage has tapered in fy16 on...

TRANSCRIPT

RETAIL SECTOR

July 27, 2016

Sameep Kasbekar, CFA

[email protected]+91 22 66121281

Amit PurohitResearch [email protected]+91 22 66121340

Dhaval Mehta Research [email protected]+91 22 66121284

Research Analyst

Annual Report Analysis

Building blocks for growth in place

Shoppers Stop

Arvind

TitanPage Industries

Arvind

Arvind

Arvind

Arvind

Arvind

Arvind

Titan

Titan

Titan

Page Industries

Page Industries

Page Industries

Shoppers Stop

Shoppers Stop

Shoppers Stop

ShoppersStop

Titan

Titan

TitanArvind

Shoppers Stop

Shoppers Stop

Arvind

Page Industries

Page Industries

Titan

Titan

Page Industries Shoppers StopArvind

Arvind

Titan

TitanShoppers Stop

Titan

Page Industries

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 2

Contents

Growth has tapered, but levers well in place ........................................................................ 3

Industry charts .................................................................................................................... 5

Key excerpts from the Annual report .................................................................................. 6

Valuation charts .................................................................................................................. 7

Companies

Arvind — Growth brands to POWER through ........................................................................... 9

Page Industries — Category and network expansion remain key levers for growth ................ 14

Shoppers Stop — Penetration growth through store expansion and omnichannel ................. 19

Titan Company — Banking on demand revival ....................................................................... 24

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Retail

July 27, 2016

Annual Report Analysis

Retail Sector

Growth has tapered, but levers well in place

Arvind ACCUMULATE

CMP Target Price

305 330

Page Industries BUY

CMP Target Price

13,372 15,050

Shoppers Stop BUY

CMP Target Price

375 476

Titan Company HOLD

CMP Target Price

414 330

Sameep Kasbekar, CFA

+91 22 66121281

Amit Purohit

+91 22 66121340

Dhaval Mehta

+91 22 66121284

Key takeaways from FY16 annual reports

Indian retail remains well placed to benefit from increased discretionary spend and revival

in urban demand. Industry pegs retail sector growth at 14% and modern trade growth at

22% to grow to USD 1.2tn and USD 160bn respectively by 2020

Overall growth across our coverage has tapered in FY16 on account of weak consumer

sentiments, detrimental impact from ecommerce and company specific factors

(restructuring in Arvind’s Megamart, jewellers strike etc.)

Brick and Mortar players are increasingly moving towards an omnichannel strategy to

explore new avenues for growth and compete with ecommerce marketplaces

We believe that a strong brand portfolio, new categories and innovation, focus on improved

mix and increase in penetration are key levers for growth. We have a Buy rating on Page

Industries and Shoppers Stop, Accumulate rating on Arvind and Hold rating on Titan

Indian Retail well placed to benefit from consumption uptick

The annual reports of retail companies indicate an upbeat mood about the growth prospects

of the sector. The size of the Indian Retail sector is estimated at USD 630bn of which organised

retail stands at 9-10% at USD 60bn, accounting for c.25% of India’s GDP. Indian retail is

expected to grow by 14% CAGR to USD 1.2tn by 2020 while organised retail is expected to

outpace the sector growing at 22% to USD 160bn by 2020 driven by i) increasing shift from

unorganised to organised retail, ii) growing urbanisation, iii) rising disposable income, iv)

favourable demographics and growing middle class, v) improving infrastructure (malls,

shopping centres etc) and vi) growing penetration of ecommerce.

Overall growth has slowed down in FY16

Weak consumer sentiments, impact from ecommerce players and company specific factors

has resulted in revenue growth tapering in FY16. In FY16, i) Arvind’s Brand and Retail portfolio

reported a growth of +16.2% (versus +22.7% in FY15) impacted by restructuring in Megamart

(-11% yoy). The power brand portfolio’s growth too tapered to 20.2% (versus 25% in FY15),

ii) Page’s revenues grew at 15.4% (historic CAGR of 35%), on account of slower growth in

menswear and sportswear. Page reported a weaker volume growth at 9.6% in FY16. iii)

Sustained competition from ecommerce players coupled with a slow-down in store expansion

in the last 2 years resulted in Shoppers Stop revenue growth of 11.4% in FY16 (versus 12.2%

in FY15). However the Same-store Sales Growth (SSG) of the departmental store improved

from 5% in FY15 to 8.5% in FY16. iv) Regulatory hurdles (Pan Card rule), fluctuating gold prices,

and jewellers strike impacted Titan’s revenues which declined by 5.4% in FY16. Jewellery

segment reported decline of 8%, watches grew at a muted 2% and eyewear grew at 12%.

Omnichannel strategy – turning their weakness into strength

The Indian retail sector was adversely impacted by the disruptive nature of ecommerce players

through their deep discounting in FY15. However, more rational pricing regime and new DIPP

regulation on cash burn by ecommerce marketplaces has reduced the impact (to a certain

degree) in FY16. Additionally, brick and mortar retailers are increasingly turning towards

ecommerce as a new channel via an omnichannel strategy. During FY16, i) Arvind launched

its omnichannel portal NNNow.com to capture the growing trend in online shopping, ii) Page

continued selling its products via JockeyIndia.com and increased its tie-ups with various

ecommerce market places, iii) Shoppers Stop re-launched its website and introduced mobile

apps in both Android and iOS stores, iv) Titan acquired CaratLane to boost its online presence

and gain technical knowhow of online retailing.

We seek your feedback and support in the ongoing Asia Money survey.

Click here to make your appreciation count

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 4

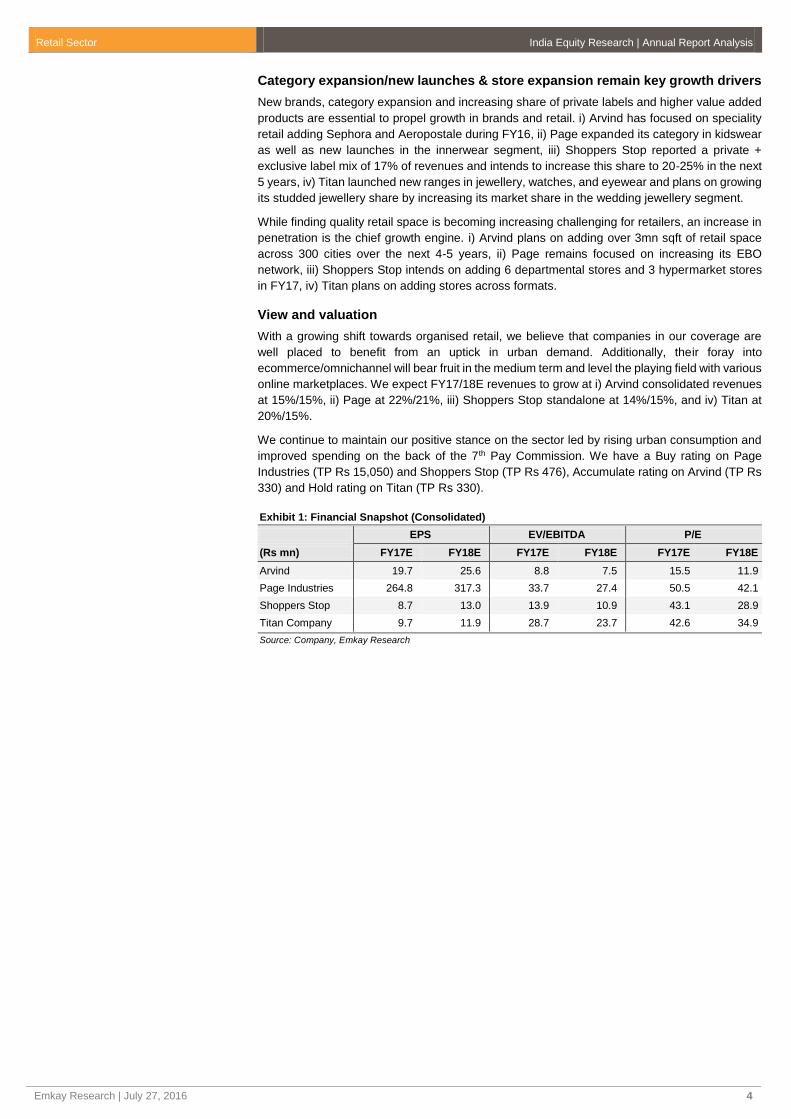

Category expansion/new launches & store expansion remain key growth drivers

New brands, category expansion and increasing share of private labels and higher value added

products are essential to propel growth in brands and retail. i) Arvind has focused on speciality

retail adding Sephora and Aeropostale during FY16, ii) Page expanded its category in kidswear

as well as new launches in the innerwear segment, iii) Shoppers Stop reported a private +

exclusive label mix of 17% of revenues and intends to increase this share to 20-25% in the next

5 years, iv) Titan launched new ranges in jewellery, watches, and eyewear and plans on growing

its studded jewellery share by increasing its market share in the wedding jewellery segment.

While finding quality retail space is becoming increasing challenging for retailers, an increase in

penetration is the chief growth engine. i) Arvind plans on adding over 3mn sqft of retail space

across 300 cities over the next 4-5 years, ii) Page remains focused on increasing its EBO

network, iii) Shoppers Stop intends on adding 6 departmental stores and 3 hypermarket stores

in FY17, iv) Titan plans on adding stores across formats.

View and valuation

With a growing shift towards organised retail, we believe that companies in our coverage are

well placed to benefit from an uptick in urban demand. Additionally, their foray into

ecommerce/omnichannel will bear fruit in the medium term and level the playing field with various

online marketplaces. We expect FY17/18E revenues to grow at i) Arvind consolidated revenues

at 15%/15%, ii) Page at 22%/21%, iii) Shoppers Stop standalone at 14%/15%, and iv) Titan at

20%/15%.

We continue to maintain our positive stance on the sector led by rising urban consumption and

improved spending on the back of the 7th Pay Commission. We have a Buy rating on Page

Industries (TP Rs 15,050) and Shoppers Stop (TP Rs 476), Accumulate rating on Arvind (TP Rs

330) and Hold rating on Titan (TP Rs 330).

Exhibit 1: Financial Snapshot (Consolidated)

EPS EV/EBITDA P/E

(Rs mn) FY17E FY18E FY17E FY18E FY17E FY18E

Arvind 19.7 25.6 8.8 7.5 15.5 11.9

Page Industries 264.8 317.3 33.7 27.4 50.5 42.1

Shoppers Stop 8.7 13.0 13.9 10.9 43.1 28.9

Titan Company 9.7 11.9 28.7 23.7 42.6 34.9

Source: Company, Emkay Research

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 5

Industry Charts – SSG/overall revenue growth muted in FY16; increased penetration and healthy balance sheets are positives

Exhibit 2: Only SHOP sees improvement in SSG

Source: Company, Emkay Research

Exhibit 3: Revenue growth was muted in FY16

Source: Company, Emkay Research

Exhibit 4: EBITDA margins a mixed bag

Source: Company, Emkay Research

Exhibit 5: Store count addition has been aggressive

Source: Company, Emkay Research; *Standalone

Exhibit 6: Inventory days have remained fairly stable (Ex.Titan)

Source: Company, Emkay Research

Exhibit 7: Working capital days have marginally increased

Source: Company, Emkay Research

2.3%

-13.0%

8.5%

1%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

Arvind Brands Megamart Shoppers Stop Hypercity

SSG

-10%

0%

10%

20%

30%

Arv

ind B

rands

Pa

ge M

ensw

ear

Pa

ge W

om

ensw

ear

Pa

ge S

port

sw

ear

Titan J

ew

elle

ry

Titan W

atc

hes

Revenue growth (%)

0%

5%

10%

15%

20%

25%

Arvind Page Shoppers Stop Titan

%

EBITDA margins

-30 bps

+35 bps

+20 bps-130 bps

0

500

1000

1500

2000

2500

3000

Arvind Page ShoppersStop*

Titan

Sto

res a

dded

FY15 FY16

+384

+675

+59 +82 +11 +6

+123 +82

0

20

40

60

80

100

120

140

160

Arvind Page Shoppers Stop Titan

Days

FY15 FY16

0

20

40

60

80

100

120

140

Arvind Page Shoppers Stop Titan

Days

FY15 FY16

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 6

Key excerpts from the Annual report

Arvind Ltd. Page Industries

Sector trends and comments

Indian textile sector is expected to grow at 8.7% CAGR over the

next 10 years driven by both domestic consumption (abundant fibre

supply, favourable demographic and work force) and exports

(better cost competitiveness).

Apparel retail sector expected to grow at CAGR of 12% driven by

i) shift from unorganised to organised retail, ii) favourable

demographics, iii) rising income level and consumption, and iv)

increasing investment in organised retail.

Annual report theme

Remains focused on enriching lifestyle using a wide array of brand

offerings and category extensions in Brand & retail portfolio. In

Textiles, company will drive growth through asset-light garmenting

business as part of vertical integration strategy to capture entire

value in textile chain.

Key comments by management ad verbatim

“Your company’s strong portfolio of foreign brands allows it to offer

consumers a whole range of products across all price segments.

“Keeping in view the changing trend in consumer buying behaviour

and to positively gain from the rapid growth of e-commerce as a

sales channel your Company has recently launched India’s first

true omnichannel experience – NNNow.com.”

Sector trends and comments

Innerwear market is Rs 199.6bn and is slated to grow at 13% to

reach Rs 682.7bn by 2024 led by rising income and urbanisation

and shift from un-branded to branded products.

Men’s innerwear is pegged at Rs 74.5bn and growing at 9% CAGR.

Women’s innerwear market at about Rs 125.1bn and growing at

15% CAGR. Higher number of working women, rising share of

western wear and brand consciousness are key growth drivers.

Kidswear market is estimated at $ 8.3bn, with boys wear

contributing to $ 4.3bn. Increased spending on children, growing

brand awareness amongst kids and focus on kids wear by

organised players are levers for growth.

T-shirts is Rs 138.3bn and expected to grow at 13% CAGR to Rs

249.4bn by 2019.

Annual report theme

Jockey highlights its Brand equity and category expansion that

makes it the leading player in the innerwear segment in India.

Further, concerted involvement with consumer via deeper

penetration, adoption of new retail formats and premium product

launches have been key drivers.

Key comments by management ad verbatim

“Your company is highly encouraged by the enduring strong brand

equity, image and leadership of the Jockey brand.”

Shoppers Stop Titan Company

Sector trends and comments

Retail in India is expected to grow at 13% to $1.2tn by 2020 driven

by i) growing urbanisation, ii) rising disposable income, iii) younger

demographics and rising middle class, iv) improving infrastructure

and rising number of malls, v) faster adoption of technology.

Modern retail is expected to grow by 22% CAGR over the next four

years to $160bn.

Annual report theme

Shoppers Stop celebrates 25 years of inception, highlighting their

journey since 1991. In their Annual report of 2016, they exhibit 25

key factors that have contributed to their success as a retailer.

They also mention their strategy moving into the new phase as a

leading omnichannel player.

Key comments by management ad verbatim

“Shoppers Stop embarked on a 3 Year omni-channel journey last

year to tap into the exponential e-commerce growth in India. The

Company has plans for focused investments in technology &

operations set-up over the next few years to provide seamless

shopping experiences online & in-store for our customers and drive

profitable revenue growth through digital.”

“ As part of the Year 1 phase we have re-launched our website and

introduced brand new mobile apps in both Android PlayStore & iOS

AppStore based on the SAP Hybris platform.”

Sector trends and comments

Migration of youngsters to cities, shift from unbranded to branded

jewellery, rising working women population and the unexploited

wedding jewellery market are key drivers for jewellery category.

Technology products like smart watches and emergence of e-

commerce led to competitive intensity and reinvented the category.

In eyewear category, advertising and entry of international players

has led to upgradation to branded lenses. Optometry continues to

remain a key focus area.

Annual report theme

While regulatory hurdles, lukewarm demand in the jewellery and

watches segment and loss of revenues in the jewellers strike has

impacted the overall growth in 2016, Titan remains focused on

introducing new products, innovation and increasing reach through

store expansion.

Key comments by management ad verbatim

“It is increasingly apparent that the watch category has significantly

transformed over the past two decades from being a must have

time keeping device to a nice to have accessory and smart wrist

device. Consequently. With greater opportunity in higher price

points and technology products, our manufacturing base that is

geared for higher volume, needs transformation and this is being

undertaken through cost compression and contract manufacturing”

Source: Company, Emkay Research

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 7

Valuation charts

Exhibit 8: Arvind PE chart – trades between 5x and 20x

Source: Emkay Research

Exhibit 9: Arvind EV/EBITDA chart – trades between 4x and 10x

Source: Emkay Research

Exhibit 10: Page PE chart – trades between 10x and 70x

Source: Emkay Research

Exhibit 11: Page EV/EBITDA chart – trades between 10x and 40x

Source: Emkay Research

Exhibit 12: Shoppers Stop PE chart – trades between 10x and 100x

Source: Emkay Research

Exhibit 13: Shoppers EV/EBITDA chart – trades between 7x and 28x

Source: Emkay Research

Exhibit 14: Titan PE chart – trades between 10x and 40x

Source: Emkay Research

Exhibit 15: Titan EV/EBITDA chart – trades between 8x and 38x

Source: Emkay Research

0

100

200

300

400

500

Ap

r-09

Nov-0

9

Jun

-10

Dec-1

0

Jul-1

1

Fe

b-1

2

Au

g-1

2

Ma

r-13

Oct-

13

Ma

y-1

4

Nov-1

4

Jun

-15

Dec-1

5

Jul-1

6

5x

10x

15x

20x

0

100

200

300

400

500

Ap

r-09

Nov-0

9

Jun

-10

Dec-1

0

Jul-1

1

Fe

b-1

2

Au

g-1

2

Ma

r-13

Oct-

13

Ma

y-1

4

Nov-1

4

Jun

-15

Dec-1

5

Jul-1

6

4x

6x

10x

8x

0

3000

6000

9000

12000

15000

18000

21000

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

Jan

-15

Jul-1

5

Jan

-16

Jul-1

6

10x

30x

50x

70x

0

3000

6000

9000

12000

15000

18000

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

Jan

-15

Jul-1

5

Jan

-16

Jul-1

6

40x

30x

20x

10x

0

200

400

600

800

1000

1200

Ap

r-09

Nov-0

9

Ma

y-1

0

Nov-1

0

Ma

y-1

1

Nov-1

1

Jun

-12

Dec-1

2

Jun

-13

Dec-1

3

Jun

-14

Dec-1

4

Jul-1

5

Jan

-16

Jul-1

6

10x

30x

70x

100x

0

200

400

600

800

1000

Ma

y-0

5

Dec-0

5

Jun

-06

Dec-0

6

Jun

-07

Dec-0

7

Jun

-08

Dec-0

8

Jun

-09

Dec-0

9

Jun

-10

Dec-1

0

Jun

-11

Dec-1

1

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

Jan

-15

Jul-1

5

Jan

-16

Jul-1

67x

14x

28x

21x

0

50

100

150

200

250

300

350

400

450

Ap

r-02

Jun

-03

Jul-0

4

Au

g-0

5

Se

p-0

6

Oct-

07

Nov-0

8

Dec-0

9

Jan

-11

Fe

b-1

2

Ap

r-13

Ma

y-1

4

Jun

-15

Jul-1

6

20x

10x

30x

40x

0

100

200

300

400

500

600

700

Ap

r-02

Jun

-03

Jul-0

4

Au

g-0

5

Se

p-0

6

Oct-

07

Nov-0

8

Dec-0

9

Jan

-11

Fe

b-1

2

Ap

r-13

Ma

y-1

4

Jun

-15

Jul-1

6

8x

18x

28x

38x

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 8

Companies

Arvind

Page Industries

Shoppers Stop

Titan Company

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Retail

July 27, 2016

Annual Report Analysis

Arvind

Growth brands to POWER through

CMP Target Price

Rs305 Rs330 ()

Rating Upside

ACCUMULATE () 8.2 %

Change in Estimates

EPS Chg FY17E/FY18E (%) NA

Target Price change (%) NA

Previous Reco ACCUMULATE

Emkay vs Consensus

EPS Estimates

FY17E FY18E

Emkay 19.7 25.6

Consensus 17.3 21.6

Mean Consensus TP Rs 358

Stock Details

Bloomberg Code ARVND IN

Face Value (Rs) 10

Shares outstanding (mn) 258

52 Week H/L 366 / 235

M Cap (Rs bn/USD bn) 79 / 1.17

Daily Avg Volume (nos.) 1,777,009

Daily Avg Turnover (US$ mn) 8.3

Shareholding Pattern Mar '16

Promoters 43.8%

FIIs 22.6%

DIIs 16.4%

Public and Others 17.2%

Price Performance

(%) 1M 3M 6M 12M

Absolute (3) 7 (4) 1

Rel. to Nifty (3) (1) (16) 1

Relative price chart

Source: Bloomberg Sameep Kasbekar, CFA

+91 22 66121281

Amit Purohit

+91 22 66121340

-10

0

10

20

30

40

200

235

270

305

340

375

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16

%Rs

Arvind (LHS) Rel to Nifty (RHS)

Brands segment continues to outpace the textile segment; Category

expansion in brands, space addition, and vertical integration in textiles

through garmenting are key drivers.

Denims and Megamart impact growth - Arvind’s standalone revenue growth was muted

at 3%, adversely impacted by the denims, woven, and voiles businesses. However,

garmenting growth was robust at 24%. Arvind’s consolidated revenues grew by 8% led by

16% growth in the Brand and Retail segment.

Bottlenecks in production and lower realisation impacts textile growth – Constraints

on plant utilization (bottlenecks) due to change in product mix in the denim business led

to 3% decline in revenues. After the expansion in capacities, the woven business reported

a subdued 4% growth led by a 5% growth in volumes (realisations were tad lower yoy).

The voiles business continued to register a decline in revenues of 4%. With the

stabilisation of operations of the garmenting plant in Ethiopia, volumes grew by 28%

resulting in a revenue growth of 24% in garmenting. Knits reported a growth of 10%.

Brand and Retail growth impacted by Megamart – Arvind Lifestyle Brands Ltd‘s growth

trajectory tapered to 16% (versus 20%+ CAGR FY12-15) primarily impacted by

restructuring in Megamart (-11% yoy). However, both Power Brands (+20% yoy) and

Growth Brands (+39%) maintained a healthy revenue traction in FY16. The brand segment

reported LTL growth of 2.3% while Megamart posted a LTL decline of 13%.

Megamart now rebranded as Unlimited – Company has re-branded c.37 Megamart

stores as “Unlimited” with a change in strategy for the retail segment. Unlimited is a small

– medium format store that primarily offers Arvind’s private labels.

Space addition – Arvind remained aggressive with its expansion strategy in the Brands

and Speciality business opening 119 and 20 stores respectively. However, owing to

restructuring in Megamart, company closed down 48 stores in FY16. The Brand and Retail

segment currently has a distribution strength of 953 stores.

EBITDA margins – Consolidated EBITDA margins declined by 30bps to 12.6% in FY16

impacted by lower SSG in the brands portfolio and unfavourable mix (higher contribution

from low margin segments such as Garmenting, and Brands and Retail).

Balance sheet performance - The consolidated debt increased by Rs 1.4bn to Rs 35.4bn

largely to fund capital expenditure (Rs 4.1bn) and higher working capital requirement,

however the debt:equity ratio has remained flat at 1.2x. Working capital days have

marginally increased to 121 days (+3 days yoy) owing to an increase in receivable days.

Despite an increase in capex, company reported free cash flow of Rs 2.8bn led by

improving cash flow from operations. The dividend payout ratio declined from 21% in FY15

to 17% in FY16.

Financial Snapshot (Consolidated)

(Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 66,648 75,392 81,735 94,335 108,892

EBITDA 9,107 10,129 10,651 13,003 15,386

EBITDA Margin (%) 13.3 12.9 12.6 13.4 13.7

APAT 3,703 3,954 3,706 5,074 6,605

EPS (Rs) 14.3 15.3 14.4 19.7 25.6

EPS (% chg) 49.0 6.8 (6.3) 36.9 30.2

ROE (%) 17.3 16.6 14.5 17.7 19.6

P/E (x) 21.3 19.9 21.2 15.5 11.9

EV/EBITDA (x) 11.7 11.0 10.7 8.8 7.5

P/BV (x) 3.4 3.2 3.0 2.6 2.1

Source: Company, Emkay Research

Arvind (ARVND IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 10

Omnichannel initiative – Arvind launched their omnichannel platform NNNow.com to

capture the growing trend of online shopping. This platform intends to shift the online business

model from purely discount driven to one that focusses on quality brands and a variety of

offerings. Company expects the channel to drive volumes and lead to overall margin

expansion in the Brand and Retail business.

Suiting JV going strong - Arvind’s JV, Arvind Goodhill Suit Manufacturing (set up to

manufacture suits) has grown 3x to Rs 490mn in FY16.

Contingent liabilities – Contingent liabilities increased by Rs 600mn to Rs 6.1bn in FY16 on

account of increase in guarantees given by banks and by the company.

Threats – In the near term, the Trans-Pacific Partnership Agreement (TPPA) is an overhang

on the apparel export business of Arvind. In an attempt to buffer any potential loss of business,

the company has set up garmenting factories in Ethiopia to take advantage of lower labour

costs, lower shipment time to US markets and duty savings.

Key drivers going forward – New categories in existing brands and rapid store expansion

are key growth drivers for the Brands & Retail portfolio. In the next 4-5 years, Arvind plans to

have its presence in c.300 cities with a target of 3mn sq ft of retail space. Vertical integration

through asset light garmenting business is expected to drive textile business while capturing

the entire value chain. Company believes that factories in Ethiopia will make their products

more competitive in international markets. Expansion in knits fabrics too is underway.

Outlook and guidance – For FY17, Company expects consolidated revenues to grow by 12-

15% led by 20-22% growth in Brands & Retail business and 8-9% growth in the Textile

business. Change in mix is expected to marginally impact consolidated EBITDA margins while

Brands & Retail EBITDA margins is likely to improve by c.75bps.

Valuation and view – Uptick in urban consumption, improved traction in the Growth Brand

and Speciality Retail portfolios and store expansion are expected to drive revenue growth. We

expect Arvind’s consolidated revenues to grow by 13% CAGR FY16-18E. We have an

Accumulate rating with price target of Rs 330/share.

Arvind (ARVND IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 11

Textile volumes remain weak; Brand impacted by restructuring in Megamart; Brand EBITDA margins see uptick; Working capital steady

Exhibit 16: Textile volumes growth has been muted in FY16

Source: Company, Emkay Research

Exhibit 17: Megamart SSG impacted by restructuring

Source: Company, Emkay Research

Exhibit 18: Brand margins have witnessed an uptick

Source: Company, Emkay Research

Exhibit 19: Aggressive store addition seen in Brands division

Source: Company, Emkay Research

Exhibit 20: Return ratios – a mixed bag

Source: Company, Emkay Research

Exhibit 21: Working capital has remained steady

Source: Company, Emkay Research

-10%

0%

10%

20%

30%

40%

FY13 FY14 FY15 FY16

Volu

me g

row

th

Denim Woven Garments

-15%

-10%

-5%

0%

5%

10%

15%

FY13 FY14 FY15 FY16

Lik

e-t

o-L

ike g

row

th

Brands Megamart

0%

5%

10%

15%

20%

25%

FY13 FY14 FY15 FY16

EB

ITD

A m

arg

in

Textiles Brand & Retail

218

128 113146

-19 -31 -26-48-100

0

100

200

300

FY13 FY14 FY15 FY16

New

sto

res a

dded

Brands Megamart

10%

12%

14%

16%

FY13 FY14 FY15 FY16

ROCE ROE

-1-7 -1 -1

+9 +5

+14 +3

0

20

40

60

80

100

120

140

FY13 FY14 FY15 FY16

Inventory days Working capital days

Arvind (ARVND IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 12

Key Financials (Consolidated)

Income Statement

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 66,648 75,392 81,735 94,335 108,892

Expenditure 59,514 68,386 73,853 84,101 96,690

EBITDA 9,107 10,129 10,651 13,003 15,386

Depreciation 2,252 2,124 2,559 2,784 3,008

EBIT 6,855 8,005 8,092 10,220 12,378

Other Income 694 932 964 1,014 1,148

Interest expenses 3,312 3,946 3,811 3,945 4,039

PBT 4,237 4,991 5,245 7,288 9,487

Tax 548 1,072 1,517 2,184 2,843

Extraordinary Items (164) (543) (80) 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 3,539 3,411 3,627 5,074 6,605

Adjusted PAT 3,703 3,954 3,706 5,074 6,605

Balance Sheet

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Equity share capital 2,582 2,582 2,582 2,582 2,583

Reserves & surplus 23,248 24,656 26,535 30,927 36,782

Net worth 25,830 27,239 29,117 33,510 39,366

Minority Interest 242 348 529 559 597

Loan Funds 29,920 33,967 35,402 35,902 36,502

Net deferred tax liability 435 471 699 699 699

Total Liabilities 56,427 62,024 65,747 70,669 77,164

Net block 28,927 32,082 34,595 36,812 38,803

Investment 1,293 586 726 726 726

Current Assets 42,066 46,089 48,928 53,131 60,847

Cash & bank balance 1,663 833 651 455 510

Other Current Assets 3,403 2,699 3,307 3,459 3,992

Current liabilities & Provision 17,205 17,733 19,972 21,469 24,682

Net current assets 24,860 28,356 28,956 31,662 36,165

Misc. exp 0 0 0 0 0

Total Assets 56,427 62,024 65,747 70,669 77,164

Cash Flow

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 3,543 4,059 4,281 6,274 8,339

Other Non-Cash items 0 0 0 0 0

Chg in working cap (7,061) (4,290) (554) (2,902) (4,447)

Operating Cashflow 3,883 5,584 5,717 5,009 5,085

Capital expenditure (3,537) (4,990) (5,568) (5,000) (5,000)

Free Cash Flow 346 594 149 9 85

Investments (615) 708 (141) 0 0

Other Investing Cash Flow (2,276) (2,523) 0 0 0

Investing Cashflow (5,734) (5,874) (4,745) (3,986) (3,852)

Equity Capital Raised 10 5 (1,000) 0 1

Loans Taken / (Repaid) 5,312 4,047 1,435 500 600

Dividend paid (incl tax) (298) (496) (704) (784) (682)

Other Financing Cash Flow (240) (94) 2,191 2,846 2,942

Financing Cashflow 1,472 (485) (1,889) (1,383) (1,178)

Net chg in cash (380) (775) (917) (360) 56

Opening cash position 1,614 1,234 833 651 455

Closing cash position 1,663 833 186 290 510

Arvind (ARVND IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 13

Key Ratios

Profitability (%) FY14 FY15 FY16 FY17E FY18E

EBITDA Margin 13.3 12.9 12.6 13.4 13.7

EBIT Margin 10.0 10.2 9.6 10.5 11.0

Effective Tax Rate 12.9 21.5 28.9 30.0 30.0

Net Margin 5.4 5.0 4.4 5.3 5.9

ROCE 15.4 15.8 14.8 17.1 19.0

ROE 17.3 16.6 14.5 17.7 19.6

RoIC 15.4 15.1 13.8 16.3 18.0

Per Share Data (Rs) FY14 FY15 FY16 FY17E FY18E

EPS 14.3 15.3 14.4 19.7 25.6

CEPS 23.1 23.5 24.3 30.4 37.2

BVPS 89.4 95.1 102.4 119.5 142.1

DPS 1.9 2.7 2.4 2.6 2.9

Valuations (x) FY14 FY15 FY16 FY17E FY18E

PER 21.3 19.9 21.2 15.5 11.9

P/CEPS 13.2 13.0 12.6 10.0 8.2

P/BV 3.4 3.2 3.0 2.6 2.1

EV / Sales 1.6 1.5 1.4 1.2 1.1

EV / EBITDA 11.7 11.0 10.7 8.8 7.5

Dividend Yield (%) 0.6 0.9 0.8 0.9 1.0

Gearing Ratio (x) FY14 FY15 FY16 FY17E FY18E

Net Debt/ Equity 1.2 1.3 1.3 1.1 1.0

Net Debt/EBIDTA 3.1 3.3 3.3 2.7 2.3

Working Cap Cycle (days) 123.4 127.9 122.3 117.3 116.1

Growth (%) FY14 FY15 FY16 FY17E FY18E

Revenue 29.6 13.1 8.4 15.4 15.4

EBITDA 32.5 11.2 5.2 22.1 18.3

EBIT 41.9 16.8 1.1 26.3 21.1

PAT 42.5 (3.6) 6.3 39.9 30.2

Quarterly (Rs mn) Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Revenue 20,405 18,769 20,964 21,575 23,196

EBITDA 2,550 2,280 2,622 2,815 3,010

EBITDA Margin (%) 12.5 12.1 12.5 13.0 13.0

PAT 482 580 910 1,033 1,103

EPS (Rs) 2.2 2.7 4.2 4.7 5.0

Shareholding Pattern (%) Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Promoters 43.7 43.8 43.8 43.8 43.8

FIIs 16.5 14.7 15.2 23.1 22.6

DIIs 14.6 15.8 16.1 16.6 16.4

Public and Others 25.2 25.7 24.9 16.5 17.2

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Retail

July 27, 2016

Annual Report Analysis

Page Industries

Category and network expansion remain key levers for growth

CMP Target Price

Rs13,372 Rs15,050 ()

Rating Upside

BUY () 12.5 %

Change in Estimates

EPS Chg FY17E/FY18E (%) NA

Target Price change (%) NA

Previous Reco BUY

Emkay vs Consensus

EPS Estimates

FY17E FY18E

Emkay 264.8 317.3

Consensus 260.3 323.6

Mean Consensus TP Rs 12,628

Stock Details

Bloomberg Code PAG IN

Face Value (Rs) 10

Shares outstanding (mn) 11

52 Week H/L 15,075 / 9,752

M Cap (Rs bn/USD bn) 149 / 2.22

Daily Avg Volume (nos.) 7,740

Daily Avg Turnover (US$ mn) 1.6

Shareholding Pattern Mar '16

Promoters 49.0%

FIIs 37.2%

DIIs 4.8%

Public and Others 9.0%

Price Performance

(%) 1M 3M 6M 12M

Absolute (2) 4 7 (9)

Rel. to Nifty (2) (3) (6) (8)

Relative price chart

Source: Bloomberg

Amit Purohit

+91 22 66121340

Sameep Kasbekar, CFA

+91 22 66121281

Dhaval Mehta

[email protected] +91 22 66121284

-20

-12

-4

4

12

20

9850

10820

11790

12760

13730

14700

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16

%Rs

Page Industries (LHS) Rel to Nifty (RHS)

Despite tapered growth in FY16, strong drivers in place; We believe increased

penetration, category expansion into kidswear and innovation in womenswear

and sportswear to drive revenues in the medium term

Tepid demand environment impacts growth - After registering a revenue CAGR of 35%

over FY10-15, revenue growth tapered down to 15% in FY16. Increased penetration,

category expansion, innovation and aggressive branding are key for growth.

Womenswear outpaces other segments – While revenue growth in menswear was

subdued at 10% to Rs 8.5bn led by 6% volume growth, womenswear revenues grew at a

robust 27% at Rs 3.4bn driven by 17% volume growth. Sportswear reported revenue

growth of 15% at Rs 5.6bn led by 10% volume growth. Speedo reported revenues of Rs

295mn, up 26% yoy.

New product launches drives category expansion – During FY16, Jockey launched

POP colour innerwear for women which combined the super combed cotton elastane

stretch fabric with trendy neon trims and fashionable prints targeted towards young

women. Company also launched USA Originals loungewear for Men imbibing the Wild

West American heritage of Texas. Company made inroads into kidswear by launching

USA Original for boys aged 7-12 years and introduced International collection for men’s

innerwear in Tactel and Pima cotton.

Constant focus on increasing penetration – Jockey products are available in over 1,400

cities via Exclusive Brand Outlets (EBOs), Large Format Stores, Multi Brand Outlets and

Traditional hosiery stores and multipurpose stores across the country. Company opened

82 EBOs including 7 EBOs exclusively for women through the franchise route taking its

total tally to 265 stores. Speedo products are available in 1,060 stores including 9 EBOs.

The company also has 4 EBOs in UAE and 1 EBO in Sri Lanka.

Strong brand equity – The Company believes that brand equity, brand image and

leadership of Jockey brand are imperative to sustain a healthy growth rate. Jockey as a

brand enjoys an unmatched position in the innerwear category. As per Brand Equity Index

(BEI) only 23% brands have a BEI of more than 3.0 and Jockey has a BEI of 4.6 in

menswear and 2.9 in womenswear.

Expanded into online platform - Page maintains an online presence through its own

B2C ecommerce channel www.jocketindia.com and has also tied up with various online

marketplaces to increase its distribution reach.

Margins expansion despite higher employee costs – Page reported Gross margin

expansion of 40bps to 53.4% led by lower cotton prices and higher share of premium

products. While provision for bonus payment (Rs 87.4mn) resulted in an increase in

employee costs, the impact was offset by higher gross margin and lower advertising spend

resulting in EBITDA margin improving by 30bps to 19.5% in FY16.

Financial Snapshot (Standalone)

(Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 11,731 15,140 17,495 21,316 25,808

EBITDA 2,367 2,900 3,432 4,459 5,473

EBITDA Margin (%) 20.2 19.2 19.6 20.9 21.2

APAT 1,538 1,960 2,327 2,953 3,540

EPS (Rs) 137.9 175.7 208.6 264.8 317.3

EPS (% chg) 36.7 27.5 18.7 26.9 19.9

ROE (%) 61.2 58.0 52.2 50.8 47.2

P/E (x) 97.0 76.1 64.1 50.5 42.1

EV/EBITDA (x) 63.6 52.0 43.7 33.7 27.4

P/BV (x) 51.6 38.6 29.5 22.7 17.7

Source: Company, Emkay Research

Page Industries (PAG IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 15

Capacity expansion underway – Company started commercial production at Tiptur Unit

during FY16 and currently has installed capacities spread over 1.97mn sqft in 13 locations in

Karnataka. The company is upbeat about the market demand and has planned further

expansion in KIADB Industrial Area, Hassan.

Balance sheet improves – Page’s gross debt reduced by Rs 623mn to Rs 949mn resulting

in a debt:equity of 0.19x. Working capital days remained steady at 64 days despite an increase

in inventory days by 6 days to 113 days offset by an increase in creditor days by 5 days to 70

days. Company spent Rs 264mn on capex during FY16 (lower than 5 year average of Rs

400mn).

Further improvement in Free Cash Flow generation – Free cash flow improved by 67%

yoy to Rs 1.9bn aided by strong operating cash flows and prudent working capital

management. ROCE and ROE marginally declined to 55.4% and 51.6% respectively.

Company declared dividends of Rs 85/share maintaining a dividend payout of 48%.

Contingent liabilities – Contingent liabilities increased by Rs 93mn to Rs 264mn in FY16 on

account of Rs 118mn differential liability on bonus payment for the year FY15.

Outlook – Strong brand equity, increasing demand, expansion of capacities and network

place Jockey in a sweet spot to capture the uptick in discretionary demand.

View & Valuation – New products and innovation, expansion in categories and distribution

expansion is expected to drive revenues by 22% CAGR FY16-18E. We believe that the robust

growth trajectory would ensure premium valuations for the company. We have a BUY rating

with price target of Rs 15,050/share.

Page Industries (PAG IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 16

Volumes muted, but margins improve despite higher employee costs; Working capital steady; Free cash flow generation robust

Exhibit 22: Women’s wear steady; men’s and sports volumes decline

Source: Company, Emkay Research

Exhibit 23: Margins improve despite increase in employee costs

Source: Company, Emkay Research

Exhibit 24: Inventory days increases; Working capital steady

Source: Company, Emkay Research

Exhibit 25: Capex muted, asset turns healthy

Source: Company, Emkay Research

Exhibit 26: Robust FCF generation in FY16

Source: Company, Emkay Research

Exhibit 27: Return ratios have marginally declined in FY16

Source: Company, Emkay Research

0%

10%

20%

30%

40%

FY13 FY14 FY15 FY16

Volu

me g

row

th

Men's wear Women's wear Sports wear

18%

19%

20%

21%

50%

51%

52%

53%

54%

FY13 FY14 FY15 FY16

Gross margin (LHS) EBITDA margin (RHS)

+7

+14-6

+6

+15+7

+7 +1

0

20

40

60

80

100

120

FY13 FY14 FY15 FY16

Inventory days Working capital days

5.0

5.2

5.4

5.6

5.8

0

100

200

300

400

500

600

FY13 FY14 FY15 FY16

Asset tu

rns

Rs m

n

Capex Asset turns

0

500

1000

1500

2000

FY13 FY14 FY15 FY16

Rs m

n

FCF

45%

50%

55%

60%

65%

FY13 FY14 FY15 FY16

ROCE ROE

Page Industries (PAG IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 17

Key Financials (Standalone)

Income Statement

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 11,731 15,140 17,495 21,316 25,808

Expenditure 9,364 12,240 14,063 16,857 20,335

EBITDA 2,367 2,900 3,432 4,459 5,473

Depreciation 139 176 238 310 400

EBIT 2,228 2,723 3,194 4,149 5,073

Other Income 211 377 402 445 448

Interest expenses 104 167 153 209 265

PBT 2,335 2,933 3,443 4,385 5,255

Tax 797 973 1,116 1,431 1,716

Extraordinary Items 0 0 0 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 1,538 1,960 2,327 2,953 3,540

Adjusted PAT 1,538 1,960 2,327 2,953 3,540

Balance Sheet

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Equity share capital 112 112 112 112 112

Reserves & surplus 2,778 3,756 4,941 6,472 8,306

Net worth 2,890 3,868 5,052 6,583 8,418

Minority Interest 0 0 0 0 0

Loan Funds 1,422 1,572 949 1,299 1,650

Net deferred tax liability 95 114 110 110 110

Total Liabilities 4,407 5,554 6,112 7,993 10,178

Net block 1,728 2,173 2,132 2,778 3,573

Investment 0 27 0 0 0

Current Assets 4,932 6,034 7,311 9,135 11,336

Cash & bank balance 35 44 86 294 599

Other Current Assets 0 0 0 0 0

Current liabilities & Provision 2,289 2,680 3,335 3,924 4,734

Net current assets 2,643 3,354 3,976 5,211 6,602

Misc. exp 0 0 0 0 0

Total Assets 4,407 5,554 6,112 7,993 10,178

Cash Flow

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 2,124 2,556 3,041 3,940 4,807

Other Non-Cash items 0 0 0 0 0

Chg in working cap (977) (682) (584) (1,027) (1,085)

Operating Cashflow 740 1,670 2,165 2,445 3,120

Capital expenditure (481) (586) (200) (957) (1,195)

Free Cash Flow 259 1,084 1,965 1,489 1,925

Investments 10 (27) 27 0 0

Other Investing Cash Flow (181) (295) (488) (445) (448)

Investing Cashflow (441) (531) (259) (957) (1,195)

Equity Capital Raised 0 0 0 0 0

Loans Taken / (Repaid) 543 150 (624) 350 350

Dividend paid (incl tax) (783) (940) (1,109) (1,423) (1,705)

Other Financing Cash Flow 34 (173) 22 1 0

Financing Cashflow (310) (1,129) (1,864) (1,280) (1,620)

Net chg in cash (11) 9 42 209 305

Opening cash position 46 35 44 86 294

Closing cash position 35 44 86 295 599

Page Industries (PAG IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 18

Key Ratios

Profitability (%) FY14 FY15 FY16 FY17E FY18E

EBITDA Margin 20.2 19.2 19.6 20.9 21.2

EBIT Margin 19.0 18.0 18.3 19.5 19.7

Effective Tax Rate 34.1 33.2 32.4 32.6 32.6

Net Margin 13.1 12.9 13.3 13.9 13.7

ROCE 65.2 62.2 61.6 65.1 60.8

ROE 61.2 58.0 52.2 50.8 47.2

RoIC 61.4 55.5 55.5 60.5 58.7

Per Share Data (Rs) FY14 FY15 FY16 FY17E FY18E

EPS 137.9 175.7 208.6 264.8 317.3

CEPS 150.4 191.6 229.9 292.6 353.2

BVPS 259.1 346.7 453.0 590.2 754.7

DPS 60.0 72.0 85.0 109.0 130.6

Valuations (x) FY14 FY15 FY16 FY17E FY18E

PER 97.0 76.1 64.1 50.5 42.1

P/CEPS 88.9 69.8 58.2 45.7 37.9

P/BV 51.6 38.6 29.5 22.7 17.7

EV / Sales 12.8 10.0 8.6 7.0 5.8

EV / EBITDA 63.6 52.0 43.7 33.7 27.4

Dividend Yield (%) 0.4 0.5 0.6 0.8 1.0

Gearing Ratio (x) FY14 FY15 FY16 FY17E FY18E

Net Debt/ Equity 0.5 0.4 0.2 0.2 0.1

Net Debt/EBIDTA 0.6 0.5 0.3 0.2 0.2

Working Cap Cycle (days) 81.1 79.8 81.2 84.2 84.9

Growth (%) FY14 FY15 FY16 FY17E FY18E

Revenue 35.9 29.1 15.6 21.8 21.1

EBITDA 44.1 22.5 18.4 29.9 22.7

EBIT 45.7 22.2 17.3 29.9 22.3

PAT 36.7 27.5 18.7 26.9 19.9

Quarterly (Rs mn) Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Revenue 3,720 4,383 4,537 4,331 4,244

EBITDA 690 932 937 763 803

EBITDA Margin (%) 18.5 21.3 20.6 17.6 18.9

PAT 471 632 603 519 573

EPS (Rs) 42.2 56.6 54.1 46.5 51.3

Shareholding Pattern (%) Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Promoters 51.0 51.0 51.0 51.0 49.0

FIIs 32.3 32.9 33.7 34.3 37.2

DIIs 6.5 6.3 5.2 5.4 4.8

Public and Others 10.2 9.8 10.1 9.3 9.0

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Retail

July 27, 2016

Annual Report Analysis

Shoppers Stop

Penetration growth through store expansion and omnichannel

CMP Target Price

Rs375 Rs476 ()

Rating Upside

BUY () 26.9 %

Change in Estimates

EPS Chg FY17E/FY18E (%) NA

Target Price change (%) NA

Previous Reco BUY

Emkay vs Consensus

EPS Estimates

FY17E FY18E

Emkay 8.7 13.0

Consensus 8.9 13.2

Mean Consensus TP Rs 443

Stock Details

Bloomberg Code SHOP IN

Face Value (Rs) 5

Shares outstanding (mn) 83

52 Week H/L 446 / 301

M Cap (Rs bn/USD bn) 31 / 0.47

Daily Avg Volume (nos.) 28,957

Daily Avg Turnover (US$ mn) 0.2

Shareholding Pattern Mar '16

Promoters 67.1%

FIIs 3.7%

DIIs 13.1%

Public and Others 16.1%

Price Performance

(%) 1M 3M 6M 12M

Absolute 4 - (1) (7)

Rel. to Nifty (1) (7) (13) (6)

Relative price chart

Source: Bloomberg

Sameep Kasbekar, CFA

+91 22 66121281

Amit Purohit

+91 22 66121340

-20

-12

-4

4

12

20

300

325

350

375

400

425

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16

%Rs

Shoppers Stop (LHS) Rel to Nifty (RHS)

Revival in Same-store Sales Growth (SSG) and strong loyalty programme

drives sales; Key growth levers include uptick in discretionary spending,

increasing share of private labels and timely launch of omni channel platform

Revival in SSG aids growth - SHOP’s gross retail turnover, standalone sales and SSG

grew by 10.5%, 11.4% and 8.5% respectively driven by well spread out festive season,

company led initiatives such as Choose Your Own Gift and a weak base.

Loyalty programme provides foundation for growth – The First Citizens loyalty

programme has grown by c.11% yoy to 4.12mn members and contributing to over 72% of

sales. Crossword Book Rewards Programme (loyalty scheme for bookstore) currently has

over 0.7mn members contributing to 48% of sales. Hypercity’s loyalty programme,

Discovery Club has grown by 20% yoy to 1.2mn members. SHOP has one of the largest

customer loyalty programme in the country ensuring repeat customers and helping the

retailer to sustain growth.

Focus on increasing the share of private/exclusive labels – While SHOP has

positioned itself in the bridge-to-luxury segment with offerings of over 100 international

brands, the company remains focused on increasing its share of private and exclusive

labels. In FY16, the share of private brands declined 60bps yoy to 13.5% reporting a

growth of 6.3%. Exclusive brand contribution increased by 60bps yoy to 3.5% led by a

31.5% yoy growth. The company is working on initiatives to drive the share of private

brands which would consequently result in a margin expansion.

Store matrix improves – SHOP’s departmental store reported an improvement in nearly

all its performance parameters. The average sales per sq. ft. grew 9% to Rs 8974/sqft

buoyed by increasing average selling price (Rs 1136, +2% yoy), transaction size (Rs 2791,

+7% yoy) and conversion ratio (25.9%, +160bps yoy). Shrinkage too declined by 2bps to

0.36%. However, footfalls continued to decline to 44.6mn (down 2% yoy).

Hypercity on track to profitability – Hypercity reported a muted growth of 3% yoy, with

like-to-like sales growth at a mere 1.3%. In a bid to improve the profitability of the format

the company has right-sized stores to 30,000-50,000 sqft for optimum throughput.

Furthermore, Hypercity is being repositioned as a discovery and fresh store (fresh fruits

and vegetables contribute c.65% of sales). The company believes that Hypercity is on

track to report a positive company level EBITDA by Q4FY16.

Net space addition of 0.12mn sqft in FY16 – SHOP added 0.12mn sqft of retail space

(lowest addition in last 10 years) during FY16, opening 8 Shoppers Stop departmental

stores (77). Company also added one Hypercity store (17), two MAC stores and closed

one Home Stop (18).

Financial Snapshot (Standalone)

(Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 26,807 30,076 33,496 38,135 43,855

EBITDA 1,537 1,889 421 2,643 3,271

EBITDA Margin (%) 5.7 6.2 1.2 6.8 7.3

APAT 377 407 (1,261) 727 1,084

EPS (Rs) 4.5 4.9 (15.1) 8.7 13.0

EPS (% chg) (5.5) 8.1 (409.7) 0.0 49.1

ROE (%) 5.3 5.5 (16.3) 8.9 12.0

P/E (x) 83.0 76.8 (24.8) 43.1 28.9

EV/EBITDA (x) 22.7 19.3 88.2 13.9 10.9

P/BV (x) 4.3 4.1 4.0 3.7 3.3

Source: Company, Emkay Research

Shoppers Stop (SHOP IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 20

Tapping into India’s ecommerce, a growth opportunity – To offset loss of business due to

increasing popularity of online marketplaces, STOP has planned a two pronged strategy which

involves i) tying up leading ecommerce platforms to sell products and brands online and ii)

launching an Omni-channel platform. The company has re-launched their website and

launched mobile apps on the Android and iOS platforms. STOP plans on investing in a

Customer Relation Management (CRM) software and a Warehouse Management System

(WMS) in FY17 to build capabilities to transform into an omnichannel player by FY18.

Improvement in margin profile aided by operating leverage – Higher SSG led operating

leverage and sustained private label/exclusive label mix resulted in EBITDA margins

improving by 20bps to 6.4% in FY16.

Balance sheet healthy, working capital under control – Capex for FY16 stood at Rs 1.4bn,

while working capital cycle remained flat at 33 days. The gross debt increased by Rs 700mn

to Rs 5.9bn, with debt:equity ratio at a comfortable 0.8x. Standalone free cash flow was

marginally negative at Rs 15mn and the company lowered its dividend payout to 15% from

18% in FY15.

Threats – The challenges SHOP faces includes i) weakness in consumer demand, ii)

increasing competition from discounted online sales, iii) lack of quality retail space resulting in

increasing rental costs and iv) possible supply chain constrains with vendors reaching their

supply capacities.

Contingent Liabilities – Contingent liabilities increase by Rs 800mn to Rs 3.9bn in FY16 on

the back of corporate guarantees for loans taken by subsidiary companies.

Outlook – The Company is focused on increasing its penetration especially in tier 1/2 cities

and reinforcing their pan India presence through additional stores. SHOP also plans to capture

wallet share via various lifestyle formats such as M.A.C, Bobby Brown, Estee Lauder and

Clinique. SHOP intends on adding 6 departmental stores and 3 hypermarket stores in FY17.

Valuation and view – Speedy implementation of the omni-channel platform, increased

traction in private and exclusive labels and uptick in urban demand are key growth drivers for

SHOP. We expect revenue growth CAGR of 14.5% FY16-18E and expect Hypercity to turn

profitable in the near term with steady improvement in the margin profile. We have a BUY

rating with a price target of Rs 476/share.

Shoppers Stop (SHOP IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 21

Improving SSG and store matrix drives growth; Margins witness an uptick; Working capital under control; Capex towards store expansion & Omnichannel

Exhibit 28: Shoppers Stop SSG improved in FY16

Source: Company, Emkay Research

Exhibit 29: Conversion ratio too witnessed an uptick

Source: Company, Emkay Research

Exhibit 30: Apparel share continues to expand

Source: Company, Emkay Research

Exhibit 31: ASP and transaction size continues to grow

Source: Company, Emkay Research

Exhibit 32: Lower shrinkage and better EBITDA margins in FY16

Source: Company, Emkay Research

Exhibit 33: GM improvement in space, labour and inventory

Source: Company, Emkay Research

Exhibit 34: Working capital has remained steady

Source: Company, Emkay Research

Exhibit 35: Capex spend of Rs 1.4bn in FY16

Source: Company, Emkay Research

0%

2%

4%

6%

8%

10%

12%

FY13 FY14 FY15 FY16

Shoppers Stop SSG

18%

21%

24%

27%

FY13 FY14 FY15 FY16

Conversion ratio

40.1% 37.8% 36.0% 35.8%

59.9% 62.2% 64.0% 64.2%

0%

20%

40%

60%

80%

100%

FY13 FY14 FY15 FY16

Non-Apparels Apparels

2100

2400

2700

3000

1000

1050

1100

1150

FY13 FY14 FY15 FY16

Average Selling Price (LHS) Transaction Size (RHS)

5.0%

5.5%

6.0%

6.5%

0.30%

0.35%

0.40%

0.45%

FY13 FY14 FY15 FY16

Shrinkage (%) LHS EBITDA margins (%) RHS

0.0

1.0

2.0

3.0

4.0

5.0

FY13 FY14 FY15 FY16

GMROI GMROF ('000) GMROL (mn)

-1 +1 +0 +2

-1

-15

+15 +0

0

10

20

30

40

50

60

FY13 FY14 FY15 FY16

Inventory days Working capital days

-2000

-1000

0

1000

2000

FY13 FY14 FY15 FY16

Capex Increase in Debt

Shoppers Stop (SHOP IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 22

Key Financials (Standalone)

Income Statement

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 26,807 30,076 33,496 38,135 43,855

Expenditure 25,599 28,531 33,711 36,255 41,499

EBITDA 1,537 1,889 421 2,643 3,271

Depreciation 618 858 977 1,067 1,187

EBIT 919 1,031 (555) 1,576 2,084

Other Income 134 177 213 254 280

Interest expenses 419 512 573 590 515

PBT 634 696 (916) 1,240 1,849

Tax 257 288 346 514 766

Extraordinary Items (7) 0 (238) 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 370 407 (1,500) 727 1,084

Adjusted PAT 377 407 (1,261) 727 1,084

Balance Sheet

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Equity share capital 416 417 417 417 417

Reserves & surplus 6,871 7,236 7,437 8,089 9,097

Net worth 7,287 7,653 7,854 8,506 9,514

Minority Interest 0 0 0 0 0

Loan Funds 3,746 5,184 5,902 5,502 4,452

Net deferred tax liability 100 96 17 17 17

Total Liabilities 11,133 12,932 13,773 14,024 13,983

Net block 5,490 5,963 6,315 6,598 6,607

Investment 3,876 4,065 4,047 4,047 4,047

Current Assets 6,903 7,732 8,440 9,435 10,527

Cash & bank balance 87 49 53 26 21

Other Current Assets 149 116 79 79 79

Current liabilities & Provision 5,456 4,971 5,309 6,331 7,472

Net current assets 1,448 2,762 3,131 3,105 3,054

Misc. exp 0 0 0 0 0

Total Assets 11,133 12,932 13,773 14,024 13,983

Cash Flow

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 164 175 (1,764) 223 654

Other Non-Cash items 0 0 0 0 0

Chg in working cap 710 (1,356) (445) 0 45

Operating Cashflow 1,654 (99) (1,005) 1,367 1,635

Capital expenditure (1,593) (1,155) (1,465) (1,345) (1,195)

Free Cash Flow 61 (1,254) (2,470) 21 440

Investments (567) (189) 18 0 0

Other Investing Cash Flow 0 0 0 0 0

Investing Cashflow (1,696) (823) (599) (328) 0

Equity Capital Raised 52 34 1,776 0 0

Loans Taken / (Repaid) 453 1,437 718 (400) (1,050)

Dividend paid (incl tax) (73) (75) (75) (75) (75)

Other Financing Cash Flow 0 0 (238) 0 0

Financing Cashflow 13 884 1,608 (1,065) (1,640)

Net chg in cash (30) (38) 4 (27) (5)

Opening cash position 117 87 49 53 26

Closing cash position 88 49 53 26 21

Shoppers Stop (SHOP IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 23

Key Ratios

Profitability (%) FY14 FY15 FY16 FY17E FY18E

EBITDA Margin 5.7 6.2 1.2 6.8 7.3

EBIT Margin 3.4 3.4 (1.6) 4.1 4.7

Effective Tax Rate 40.5 41.4 (37.8) 41.4 41.4

Net Margin 1.4 1.3 (3.7) 1.9 2.4

ROCE 9.8 10.0 (2.6) 13.2 16.9

ROE 5.3 5.5 (16.3) 8.9 12.0

RoIC 13.7 13.3 (6.1) 16.5 21.6

Per Share Data (Rs) FY14 FY15 FY16 FY17E FY18E

EPS 4.5 4.9 (15.1) 8.7 13.0

CEPS 11.9 15.2 (3.4) 21.5 27.2

BVPS 87.3 91.7 94.1 101.9 114.0

DPS 0.7 0.7 0.7 0.7 0.7

Valuations (x) FY14 FY15 FY16 FY17E FY18E

PER 83.0 76.8 (24.8) 43.1 28.9

P/CEPS 31.5 24.7 (109.9) 17.4 13.8

P/BV 4.3 4.1 4.0 3.7 3.3

EV / Sales 1.3 1.2 1.1 1.0 0.8

EV / EBITDA 22.7 19.3 88.2 13.9 10.9

Dividend Yield (%) 0.2 0.2 0.2 0.2 0.2

Gearing Ratio (x) FY14 FY15 FY16 FY17E FY18E

Net Debt/ Equity 0.5 0.7 0.7 0.6 0.5

Net Debt/EBIDTA 2.4 2.7 13.9 2.1 1.4

Working Cap Cycle (days) 18.3 32.5 32.9 28.9 24.7

Growth (%) FY14 FY15 FY16 FY17E FY18E

Revenue 20.3 12.2 11.4 13.8 15.0

EBITDA 21.6 23.0 (77.7) 527.4 23.8

EBIT 21.4 12.2 (153.9) 0.0 32.3

PAT (7.2) 10.0 (468.1) 0.0 49.1

Quarterly (Rs mn) Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Revenue 8,157 7,112 8,943 9,118 8,959

EBITDA 491 327 610 712 523

EBITDA Margin (%) 6.0 4.6 6.8 7.8 5.8

PAT 103 24 128 236 102

EPS (Rs) 1.2 0.3 1.5 2.8 1.2

Shareholding Pattern (%) Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Promoters 67.2 67.2 67.2 67.1 67.1

FIIs 3.8 4.1 4.5 4.4 3.7

DIIs 13.9 13.4 12.2 13.0 13.1

Public and Others 15.1 15.3 16.2 15.5 16.1

Emkay Research is also available on www.emkayglobal.com, Bloomberg EMKAY<GO>, Reuters and DOWJONES. Emkay Global Financial Services Ltd.

©

Your success is our success

Emkay

India Equity Research | Retail

July 27, 2016

Annual Report Analysis

Titan Company

Banking on demand revival

CMP Target Price

Rs414 Rs330 ()

Rating Upside

HOLD () (20.3) %

Change in Estimates

EPS Chg FY17E/FY18E (%) NA

Target Price change (%) NA

Previous Reco HOLD

Emkay vs Consensus

EPS Estimates

FY17E FY18E

Emkay 9.7 11.9

Consensus 9.6 11.6

Mean Consensus TP Rs 359

Stock Details

Bloomberg Code TTAN IN

Face Value (Rs) 1

Shares outstanding (mn) 888

52 Week H/L 435 / 302

M Cap (Rs bn/USD bn) 368 / 5.46

Daily Avg Volume (nos.) 604,407

Daily Avg Turnover (US$ mn) 3.7

Shareholding Pattern Mar '16

Promoters 53.1%

FIIs 19.7%

DIIs 5.4%

Public and Others 21.9%

Price Performance

(%) 1M 3M 6M 12M

Absolute 6 11 17 22

Rel. to Nifty 1 3 2 22

Relative price chart

Source: Bloomberg

Amit Purohit

+91 22 66121340

Sameep Kasbekar, CFA

+91 22 66121281

Dhaval Mehta

+91 22 66121284

-10

-2

6

14

22

30

300

325

350

375

400

425

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16

%Rs

Titan Industries (LHS) Rel to Nifty (RHS)

Weak consumer sentiments, regulatory hurdles and jewellers strike in March

2016 impacted growth. Expect store expansion, revival in discretionary

demand and reinstatement of Golden Harvest Scheme (GHS) to drive growth.

Weak demand and macro factors impacts jewellery sales - Titan’s standalone

revenues declined by 5.4% to Rs 112.6bn impacted by weak performance in the jewellery

segment (-7.6% yoy) due to new PAN card rule, weak demand environment and jewellers

strike despite reintroduction of the GHS in H2FY16. Watches reported a muted growth of

1.7% yoy in FY16 while the Eyewear division registered a healthy 11.8% growth aided by

aggressive store expansion.

Regulatory hurdles persist – The government introduced regulations making PAN card

compulsory for purchases over Rs 0.2mn from January 2016. While sales over Rs 0.2mn

contributes c.10% of sales, the company witnessed overall dampening of sentiments

amongst customers. The company has seen some visible impact in some products and

price bands, but expect sales to stabilise in the medium term as customers adjust to the

new norm (previous limit set at Rs 0.5mn).

Space addition – Titan remained aggressive in their store addition. In the watches

segment, the number of stores of World of Titan increased to 452, Fastrack to 159 and

Helios to 41. In jewellery, Tanishq increased its store count to 195 and Gold Plus stores

stood at 32. In Eyewear, Titan retained its vigour for growth adding 70 stores during FY16

taking the store count to 402.

5 pillars for Tanishq – Acting on the overall slowdown in jewellery consumption, Titan

has set 5 long term initiatives for its flagship brand Tanishq. These initiatives include i)

Reduction in making charges of gold jewellery while increasing the value-for-money

proposition of Tanishq. This move is expected to drive brand metrics and increase

customer share. ii) To increase share of wedding jewellery and to correct trousseau pricing

while communicating these initiatives with customers. This initiative is expected to begin

in H2FY17. iii) Increased innovation, development and inventory of high valued diamond

jewellery (> Rs 0.2mn) to attract affluent customers and thereby increase market share.

iv) To introduce new jewellery collections including market following and customer leading

segments to increase footfalls in stores. v) Store expansion especially in middle India to

drive network expansion led growth.

Online presence beefed up – Disruptive discounting by ecommerce players has

adversely impacted all the established retailers over the past 24 months. Titan is looking

to address this issue and has consequently acquired CaratLane for its online retailing

capabilities. Titan has acquired c.62% of CaratLane for Rs 3.57bn in July ‘16, valuing the

entity at 4x FY16 sales.

Financial Snapshot (Standalone)

(Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 109,158 119,032 112,645 134,700 154,201

EBITDA 10,484 11,534 9,455 12,737 15,323

EBITDA Margin (%) 9.6 9.7 8.4 9.5 9.9

APAT 7,411 8,231 7,058 8,637 10,538

EPS (Rs) 8.3 9.3 8.0 9.7 11.9

EPS (% chg) 2.2 11.1 (14.2) 22.4 22.0

ROE (%) 33.0 29.3 21.4 22.8 24.0

P/E (x) 49.6 44.7 52.1 42.6 34.9

EV/EBITDA (x) 35.0 31.8 38.9 28.7 23.7

P/BV (x) 14.6 11.9 10.5 9.1 7.8

Source: Company, Emkay Research

Titan Company (TTAN IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 25

Innovation and new launches to drive growth in watches – Consolidation and facelift for

World of Titan stores resulted in a disproportionate retail growth. Growth across retail

channels was flat in FY16, with Helios outperforming with a double digit growth. During the

year Titan launched new and differentiated products such as Raga Moonlight Collection, Titan

Regal Crest, Sonata Shagun watch, Sonata Rahu Kaal watch, Fastract Tribe and Animal

Instinct collections. Titan also entered the smart watch category with the launch of Juxt and

expects to introduce Favre Leuba (heritage Swiss brand that Titan acquired) by the end of

FY17. Company is focused on innovation and reducing imports both by enhancing in-house

capabilities and developing Indian vendors. Titan has commenced commercial production in

Stainless Steel Case Plant in Coimbatore in this regard. The international business reported

a double digit growth driven by improved brand scores in Vietnam, UAE and Malaysia.

Massive potential in Eyewear – Rapid store expansion (+70 stores) and new products (+300

new products in FY16) has resulted in a 12% growth in FY16. The market size of Eyewear is

estimated at Rs 50bn and is expected to grow at 12-15% CAGR implying a great potential for

this business to grow.

Precision engineering – A leading player in aerospace, the company has over 750 customer

qualified parts that helps boost the outlook. Company expects strengthening relationship with

UTC group internationally, and HAL domestically should propel growth. The Machine Building

and Automation (MBA) segment acquired 85 customers in FY16 and improved their overall

order position (+50% yoy). Depreciating rupee, reduction in operating costs and focus on

niche areas and innovative products are likely to provide key levers to this segment.

Contingent liabilities – The contingent liabilities have marginally declined to Rs 2.9bn from

Rs 3bn in FY15 due to lower sales tax, customs and excise duties.

Outlook – Strategic initiatives set for Tanishq coupled with revival in discretionary spending

are expected to be key metrics that the company would be closely tracking. In addition,

acquisition of CaratLane and reinstatement of GHS would provide further fillip for growth in

FY17.

View and valuation – While growth drivers in jewellery business are in place, demand uptick

remains essential. Regulatory overhang (Pan Card rule) is expected to lead to near term

headwinds. We maintain Hold rating with price target of Rs 330/share.

Titan Company (TTAN IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 26

Jewellery revenue declines; EBITDA margins impacted by higher employee and advertisement costs; Free cash flows and working capital stable

Exhibit 36: Tepid demand and jewellers strike hits jewellery growth

Source: Company, Emkay Research

Exhibit 37: EBITDA margins impacted by higher employee & ad costs

Source: Company, Emkay Research

Exhibit 38: Debt has marginally increased in FY16

Source: Company, Emkay Research

Exhibit 39: However free cash flows remain robust

Source: Company, Emkay Research

Exhibit 40: Poor profitability impacts return ratios

Source: Company, Emkay Research

Exhibit 41: Working capital has remained stable

Source: Company, Emkay Research

-10%

-5%

0%

5%

10%

15%

20%

FY13 FY14 FY15 FY16

Jewellery Sales growth Watches Sales growth

7.5%

8.0%

8.5%

9.0%

9.5%

10.0%

10.5%

25.8%

26.2%

26.6%

27.0%

27.4%

FY13 FY14 FY15 FY16

Gross Margin EBITDA Margin

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0

2000

4000

6000

8000

10000

FY13 FY14 FY15 FY16

Total Borrowings (Rs mn) LHS D/E (x) RHS

-8000

-6000

-4000

-2000

0

2000

4000

FY13 FY14 FY15 FY16

FCF (Rs mn)

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

FY13 FY14 FY15 FY16

ROCE ROE

0.0

50.0

100.0

150.0

200.0

FY13 FY14 FY15 FY16

Inventory Days Debtor Days

Creditor Days Working Capital Days

Titan Company (TTAN IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 27

Key Financials (Standalone)

Income Statement

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Net Sales 109,158 119,032 112,645 134,700 154,201

Expenditure 98,673 107,499 103,190 121,963 138,878

EBITDA 10,484 11,534 9,455 12,737 15,323

Depreciation 656 874 969 1,073 1,176

EBIT 9,829 10,660 8,486 11,664 14,147

Other Income 1,202 706 644 772 927

Interest expenses 871 807 423 452 452

PBT 10,159 10,559 8,707 11,984 14,622

Tax 2,748 2,328 1,648 3,347 4,084

Extraordinary Items 0 0 0 0 0

Minority Int./Income from Assoc. 0 0 0 0 0

Reported Net Income 7,411 8,231 7,058 8,637 10,538

Adjusted PAT 7,411 8,231 7,058 8,637 10,538

Balance Sheet

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

Equity share capital 888 888 888 888 888

Reserves & surplus 24,352 30,032 34,258 39,676 46,371

Net worth 25,240 30,920 35,146 40,563 47,258

Minority Interest 0 0 0 0 0

Loan Funds 8,063 998 1,131 1,131 1,131

Net deferred tax liability (93) (197) (239) (239) (239)

Total Liabilities 33,209 31,721 36,037 41,455 48,150

Net block 5,962 6,832 7,686 8,113 8,437

Investment 266 326 740 740 740

Current Assets 54,420 50,818 54,040 63,626 74,447

Cash & bank balance 8,889 2,102 1,117 3,446 5,859

Other Current Assets 167 44 37 48 55

Current liabilities & Provision 27,768 26,804 27,489 32,085 36,535

Net current assets 26,652 24,013 26,551 31,541 37,912

Misc. exp 0 0 0 0 0

Total Assets 33,209 31,721 36,037 41,455 48,150

Cash Flow

Y/E Mar (Rs mn) FY14 FY15 FY16 FY17E FY18E

PBT (Ex-Other income) (NI+Dep) 8,957 9,853 8,063 11,212 13,695

Other Non-Cash items 0 0 0 0 0

Chg in working cap (14,661) (4,252) (3,566) (2,661) (3,957)

Operating Cashflow (5,513) 5,078 5,979 7,501 8,209

Capital expenditure (2,044) (1,964) (2,334) (1,500) (1,500)

Free Cash Flow (7,557) 3,114 3,645 6,001 6,709

Investments (81) (61) (413) 0 0

Other Investing Cash Flow (1,007) (498) 286 (772) (927)

Investing Cashflow (1,930) (1,818) (1,818) (1,500) (1,500)

Equity Capital Raised 0 0 0 0 0

Loans Taken / (Repaid) 8,063 (7,065) 133 0 0

Dividend paid (incl tax) (1,852) (1,852) (4,757) (3,220) (3,843)

Other Financing Cash Flow (371) (317) 0 0 0

Financing Cashflow 4,968 (10,041) (5,048) (3,672) (4,295)

Net chg in cash (2,474) (6,780) (887) 2,329 2,414

Opening cash position 11,365 8,889 2,102 1,117 3,446

Closing cash position 8,889 2,102 668 3,446 5,859

Titan Company (TTAN IN) India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 28

Key Ratios

Profitability (%) FY14 FY15 FY16 FY17E FY18E

EBITDA Margin 9.6 9.7 8.4 9.5 9.9

EBIT Margin 9.0 9.0 7.5 8.7 9.2

Effective Tax Rate 27.0 22.0 18.9 27.9 27.9

Net Margin 6.8 6.9 6.3 6.4 6.8

ROCE 41.8 35.0 26.9 32.1 33.6

ROE 33.0 29.3 21.4 22.8 24.0

RoIC 62.7 40.6 27.4 33.6 36.9

Per Share Data (Rs) FY14 FY15 FY16 FY17E FY18E

EPS 8.3 9.3 8.0 9.7 11.9

CEPS 9.1 10.3 9.0 10.9 13.2

BVPS 28.4 34.8 39.6 45.7 53.2

DPS 2.1 2.1 5.4 3.6 4.3

Valuations (x) FY14 FY15 FY16 FY17E FY18E

PER 49.6 44.7 52.1 42.6 34.9

P/CEPS 44.1 39.0 44.3 36.6 30.3

P/BV 14.6 11.9 10.5 9.1 7.8

EV / Sales 3.4 3.1 3.3 2.7 2.4

EV / EBITDA 35.0 31.8 38.9 28.7 23.7

Dividend Yield (%) 0.5 0.5 1.3 0.9 1.0

Gearing Ratio (x) FY14 FY15 FY16 FY17E FY18E

Net Debt/ Equity 0.0 0.0 0.0 (0.1) (0.1)

Net Debt/EBIDTA (0.1) (0.1) 0.0 (0.2) (0.3)

Working Cap Cycle (days) 59.4 67.2 82.4 76.1 75.9

Growth (%) FY14 FY15 FY16 FY17E FY18E

Revenue 7.9 9.0 (5.4) 19.6 14.5

EBITDA 3.7 10.0 (18.0) 34.7 20.3

EBIT 2.8 8.5 (20.4) 37.5 21.3

PAT 2.2 11.1 (14.2) 22.4 22.0

Quarterly (Rs mn) Q4FY15 Q1FY16 Q2FY16 Q3FY16 Q4FY16

Revenue 24,962 27,086 26,735 34,262 24,563

EBITDA 2,701 2,227 2,028 3,099 2,101

EBITDA Margin (%) 10.8 8.2 7.6 9.0 8.6

PAT 2,151 1,511 1,454 2,253 1,841

EPS (Rs) 2.4 1.7 1.6 2.5 2.1

Shareholding Pattern (%) Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Promoters 53.1 53.1 53.1 53.1 53.1

FIIs 21.6 21.5 21.1 20.5 19.7

DIIs 3.2 3.2 4.1 4.7 5.4

Public and Others 22.2 22.2 21.8 21.8 21.9

Retail Sector India Equity Research | Annual Report Analysis

Emkay Research | July 27, 2016 29 www.emkayglobal.com

Emkay Rating Distribution

BUY Expected total return (%) (Stock price appreciation and dividend yield) of over 25% within the next 12-18 months.

ACCUMULATE Expected total return (%) (Stock price appreciation and dividend yield) of over 10% within the next 12-18 months.

HOLD Expected total return (%) (Stock price appreciation and dividend yield) of upto 10% within the next 12-18 months.

REDUCE Expected total return (%) (Stock price depreciation) of upto (-) 10% within the next 12-18 months.

SELL The stock is believed to underperform the broad market indices or its related universe within the next 12-18 months.

DISCLAIMERS AND DISCLOSURES: Emkay Global Financial Services Limited (CIN-L67120MH1995PLC084899) and its affiliates are a full-service, brokerage, investment banking, investment

management and financing group. Emkay Global Financial Services Limited (EGFSL) along with its affiliates are participants in virtually all securities trading markets in India. EGFSL was established in