credit process optimization project pdfs/e7 esserman.pdf · • communication and collaboration to...

TRANSCRIPT

1

Credit Process Optimization Project

“If everyone is moving forward together, then success takes care of itself.”

– Henry Ford

2

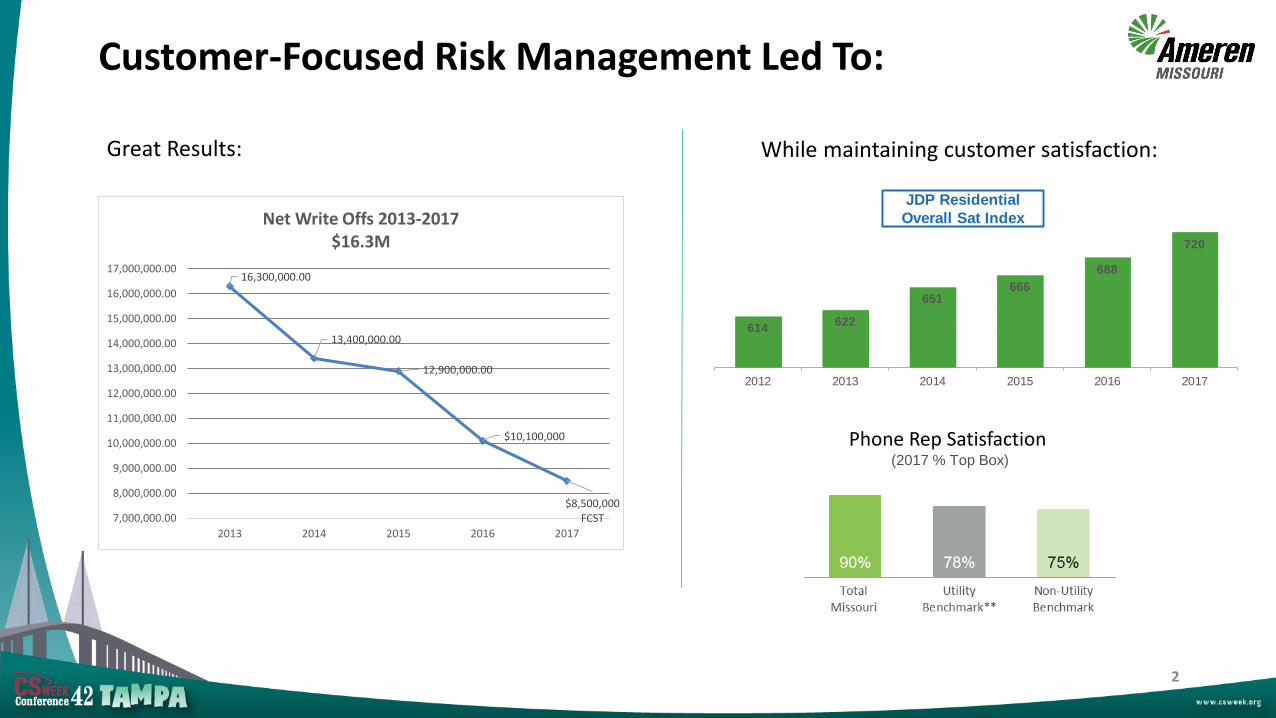

Customer-Focused Risk Management Led To:

16,300,000.00

13,400,000.00

12,900,000.00

$10,100,000

$8,500,000 FCST7,000,000.00

8,000,000.00

9,000,000.00

10,000,000.00

11,000,000.00

12,000,000.00

13,000,000.00

14,000,000.00

15,000,000.00

16,000,000.00

17,000,000.00

2013 2014 2015 2016 2017

Net Write Offs 2013-2017$16.3M

Great Results: While maintaining customer satisfaction:

Phone Rep Satisfaction (2017 % Top Box)

614622

651666

688

720

2012 2013 2014 2015 2016 2017

Ameren MissouriJDP Residential

Overall Sat Index

3

Credit Project Optimization – SWOT Analysis

4

Balancing Credit and Customers in Need“Can’t Pay” versus “Don’t Pay”

• A significant subset of our customer base struggles to afford their energy bills

• The poverty rate in Missouri is 14% - and the poverty rate in St. Louis is 24.3%

• Low-income households spend 3x as much of their income on energy costs as higher-income households

• But, only 4% of our customers received Energy Assistance in 2017

o They received an average of 2.9 service interruption notices that year

o 60% entered into a payment agreement

o They call us more often than other customer groups… average of 6 calls per year

“I don’t qualify for energy assistance. I don’t make enough to

make ends meet, but I make too much to qualify for help!”

“I’ve called every energy assistance agency in my area. They’re either out

of funds or I have to wait 30 days. My shut off is tomorrow!”

“My job eliminated overtime and I just don’t have it. I need more time!”

5

Inputs

• MO Credit & Collection Journey Mapping Outcomes

• Utilities Industry Credit & Collections Best Practices

• Customer/1 (CSS) Credit & Collections Architecture Knowledge

• Energy Assistance Agencies

Activities

• Workshops to review proposed changes

• Estimated proposed changes and prioritize changes based on goal impact

• Created a high level implementation schedule

• Ensured alignment with Business Team

Outcomes

• Prioritized list of enhancements

• A high level schedule to implement changes

• Refined effort, cost, and timing estimates

• Project Approval Committee Presentation

Project Design: Key Inputs, Activities & Outcomes

6

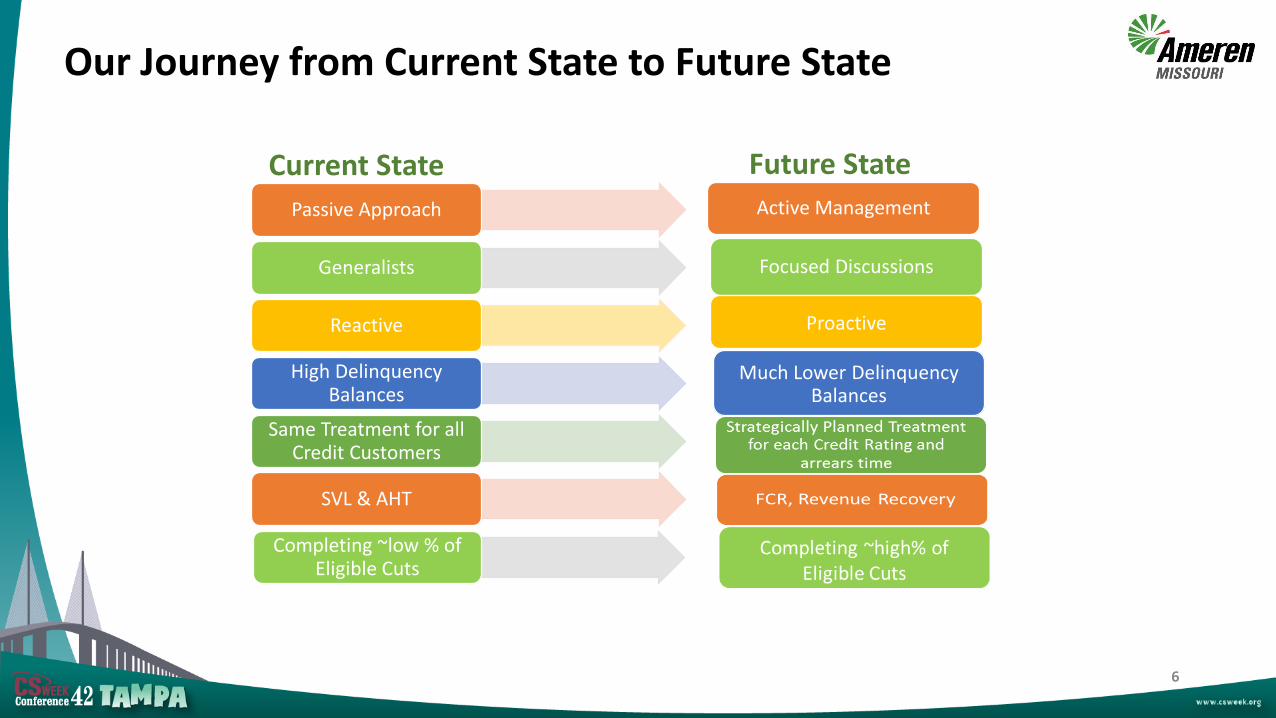

Our Journey from Current State to Future State

Passive Approach

Generalists

Reactive

High Delinquency Balances

Same Treatment for all Credit Customers

SVL & AHT

Completing ~low % of Eligible Cuts

Current State Future State

Active Management

Focused Discussions

Proactive

Much Lower Delinquency Balances

7

Collections Project Optimization – Goal and Objectives

• Goal: Enhance current systems/processes solution in order to reduce write offs

• Objectives:

• Optimize credit scoring methodology

• Reduce the collections timeline and maximize tariff approach

• Increase messages through the collection timeline using various channels

• Include a mandatory reconnection fee to be paid as part of the obligation to fulfill to be reconnected

• Add a new interface with SpeedPay to process payments real-time

• Streamline notification process with an outbound phone call.

8

#1: ACTIVE MANAGEMENTBeing smarter about how we manage balances with customers

Customer Care Center

• Focus on revenue AND satisfaction

• Handling of payment agreement offer (pay ability vs. extension)

• Interactive Voice Response (IVR) routes delinquent callers to a dedicated, highly trained customer care group

Automated Calls

• Increased frequency

• New criteria

Digital Channels

• Enhance communication via alerts in email, mobile channels

Energy Statement

• Bigger, clearer messaging on bill when in arrears

• Envelope messaging to encourage prompt payment

Key Outcomes

Key Outcomes

9

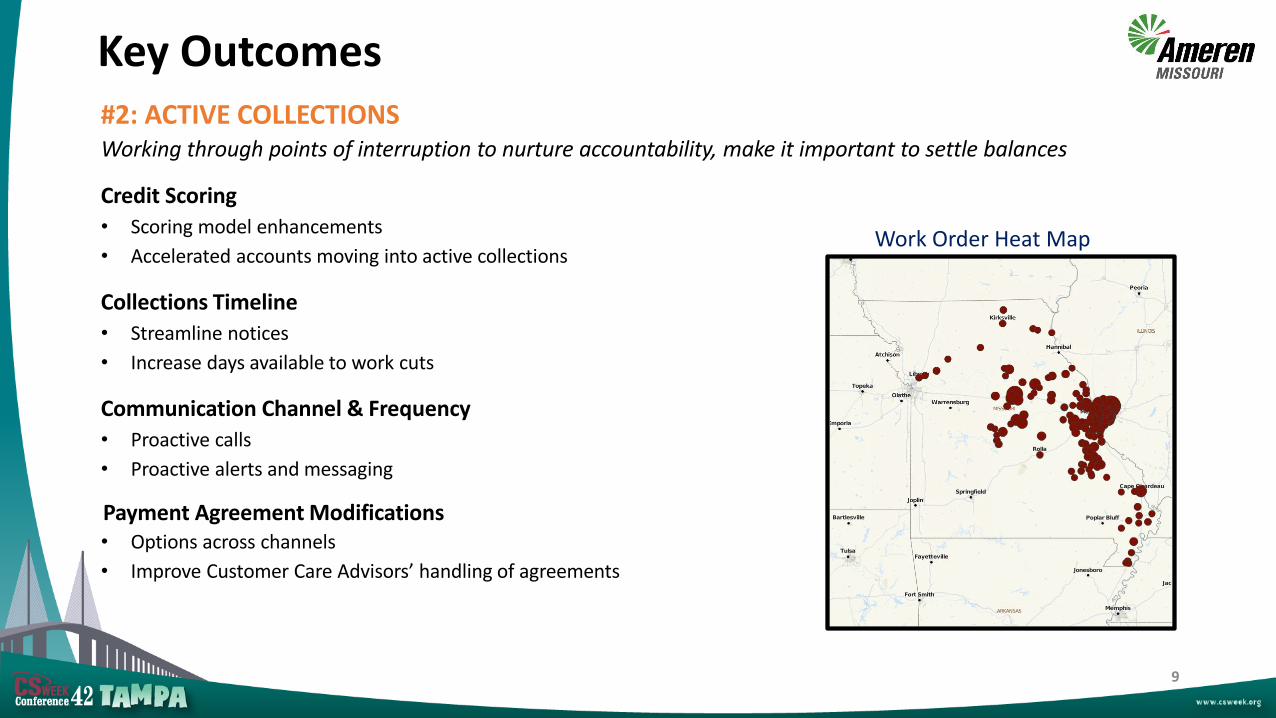

Credit Scoring

• Scoring model enhancements

• Accelerated accounts moving into active collections

Collections Timeline

• Streamline notices

• Increase days available to work cuts

Communication Channel & Frequency

• Proactive calls

• Proactive alerts and messaging

Payment Agreement Modifications • Options across channels

• Improve Customer Care Advisors’ handling of agreements

Work Order Heat Map

#2: ACTIVE COLLECTIONSWorking through points of interruption to nurture accountability, make it important to settle balances

10

#3: CALL CENTER CULTURE & CHANGE MANAGEMENTTalking to customers about opportunities to work through Credit and Collections

Organization Structure

• Dedicated Customer Care Advisor credit roles

Training & Support

• Increased knowledge and skills for Customer Care Advisors to focus on revenue recovery

• Optimized Q&A and coaching

Change Management

• In conjunction with new training

• Communication and collaboration to drive business results

Metrics & Measurement

• Optimized metrics to gauge success of new, dedicated Customer Care Advisor credit roles

Key Outcomes

11

Key Results from our Process Improvements

Arrearages are significantly down over prior years

Uncollectibles expense is approaching Top Quartile performance

12

Uncollectibles – 5 Year Performance

• Key Improvement Factors:

• Improved cut rates and lowered average balances

• Lengthened timeline at the end of 2014 to allow customers more time to pay before charge off

• Improved recoveries and collection agency performance

• Managed Damage Claim loss

Improved by $7.8M over 5 years!

16,300,000.00

13,400,000.00

12,900,000.00

$10,100,000

$8,500,000

7,000,000.00

8,000,000.00

9,000,000.00

10,000,000.00

11,000,000.00

12,000,000.00

13,000,000.00

14,000,000.00

15,000,000.00

16,000,000.00

17,000,000.00

2013 2014 2015 2016 2017

Net Write Offs 2013-2017$16.3M

13

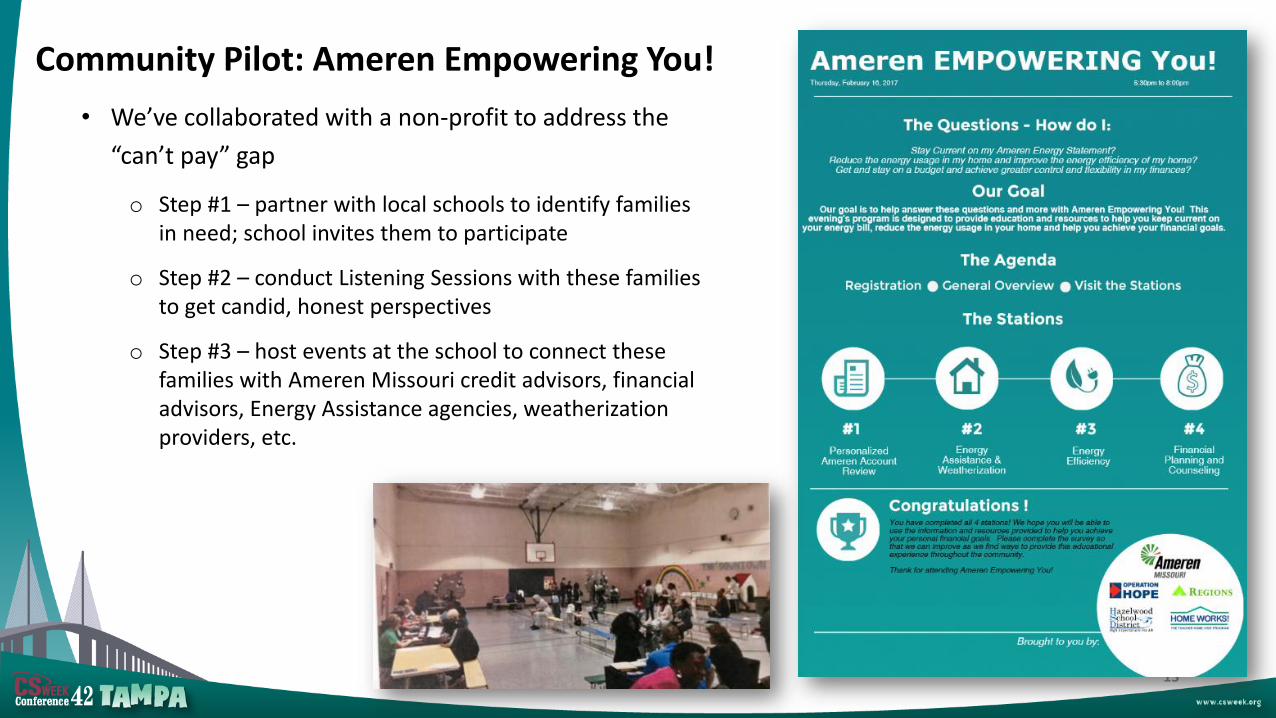

Community Pilot: Ameren Empowering You!

• We’ve collaborated with a non-profit to address the

“can’t pay” gap

o Step #1 – partner with local schools to identify families in need; school invites them to participate

o Step #2 – conduct Listening Sessions with these families to get candid, honest perspectives

o Step #3 – host events at the school to connect these families with Ameren Missouri credit advisors, financial advisors, Energy Assistance agencies, weatherization providers, etc.

14

Low-Income Customer Advocacy

• We are dedicating additional resources to programming and outreach for low-income and vulnerable customers

• We’re defining a three-year roadmap to develop a service model for low-income customers that is…

• 2018 plans include expansion of Ameren Empowering You, Empathy (Poverty Simulation) Training for all Customer Experience co-workers, and input on new 2019 Energy Efficiency programs for low-income customers

Affordable

More certain

Focused on customer

control and empowerment

Flexible and situational

Segmented

Easier and less confusing

Collaborative and Innovative

15